23.04.15 WINE 1/23 ¡ tHe WiNe ! How to make wine at home. HOME MADE WINE. By:N¡L.

Winning strategies in wine

Annual review 2012/2013Baarsma Wine Group Holding B.V.

3

Table of contents

5Management of the Group

6Key figures of the Group

7Mission, vision and strategic goals

15Report of the Board of Directors

19Financial overview

Consolidated balance sheet as of 31 March 2013 22

Consolidated profit and loss statement 2012/2013 24

Consolidated cash flow statement 2012/2013 25

26Contact information

BWGH

Baarsma Wine Group Holding (BWGH) is a worldwide wine distributor of quality wines with a fast growing distribution network in all sectors of the wine market in North-West Europe. Established some 30 years ago in the Netherlands, BWGH has evolved into one of the main players in the European wine market.

5

Management of the Group

Board of Directors

Cees de Rade CEO

Tjeerd van der Hoek RA CFO

Supervisory Board Members (through Veenwijk Holding B.V.)

Frans Barel Chairman

Paul Hugenholtz

Frank Trijbels

Corporate Management Team

Ronald van den Berg RA Group Finance Director

Nancy de Vries Corporate HR Manager

Martijn Brander Country Manager Netherlands

Rene Tulner Manager Business to Consumer

Management of the most important group companies

Netherlands Martijn Brander Country Manager

Age ten Brink Finance Manager

Roelof Speckmann Baarsma Wines B.V.

Marcel Campen Operations Manager

Chris Rabie Baarsma South Africa (Pty) Ltd

Christiaan Hintzen Oud Reuchlin & Boelen B.V.

Roelof Speckmann Wine Excel B.V.

Eric Welles Winetracks International B.V.

Ilja Gort La Tulipe Holding B.V.

Bence Nieland La Tulipe Holding B.V.

Business to Consumer Rene Tulner General manager

Matthieu Bletgen RA Finance manager

Annemijn Hofdijk Grand Cru Expertise ‘De Nederlandse Wijnbeurs’ B.V.

Ruud Heuvelmans Leon Colaris B.V.

Jacco Oosterhof Wijnvoordeel International B.V.

Belgium Michel Fryns Hasselt Millesime B.V.B.A.

Ann Marx Finance Manager

United Kingdom Mike Laing John Armit Wines Ltd

Graham Jeffs Finance Manager

Switzerland Christian Häberli Rutishauser Weinkellerei A.G.

Karin Koller Finance Manager

6Annual review 2012/2013baarsma wine group holding

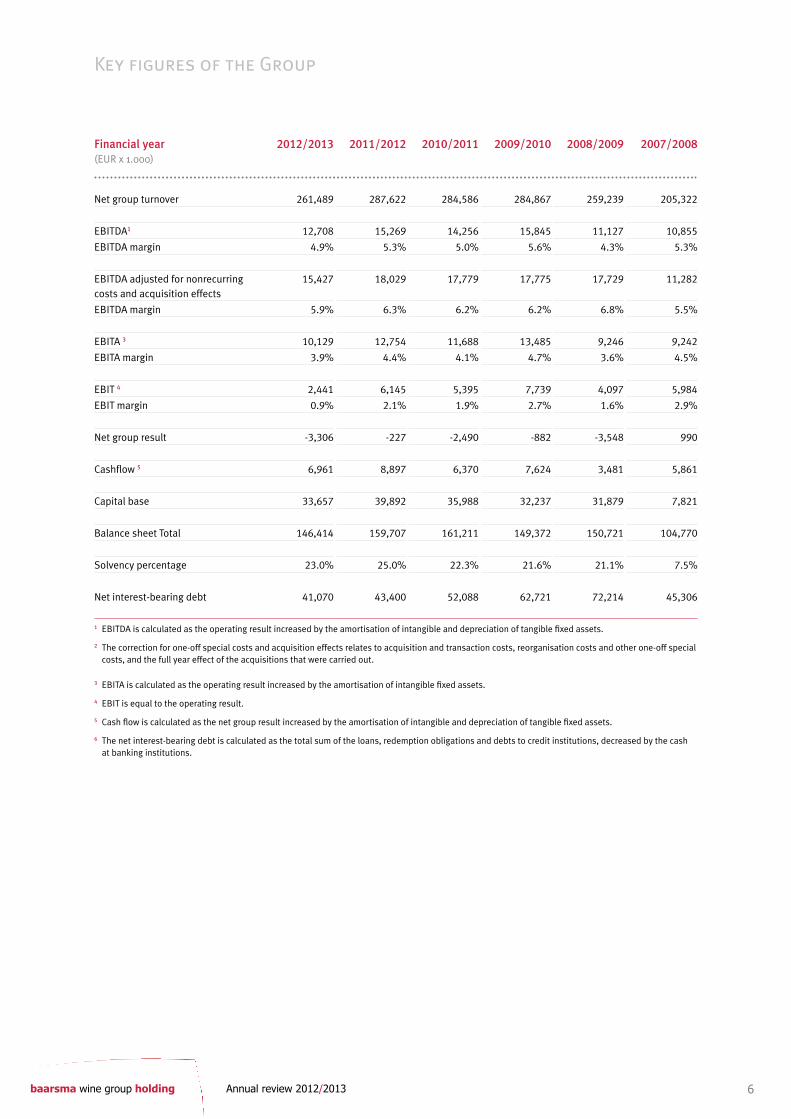

Key figures of the Group

Financial year (EUR x 1.000)

2012/2013 2011/2012 2010/2011 2009/2010 2008/2009 2007/2008

Net group turnover 261,489 287,622 284,586 284,867 259,239 205,322

EBITDA1 12,708 15,269 14,256 15,845 11,127 10,855

EBITDA margin 4.9% 5.3% 5.0% 5.6% 4.3% 5.3%

EBITDA adjusted for nonrecurring costs and acquisition effects

15,427 18,029 17,779 17,775 17,729 11,282

EBITDA margin 5.9% 6.3% 6.2% 6.2% 6.8% 5.5%

EBITA 3 10,129 12,754 11,688 13,485 9,246 9,242

EBITA margin 3.9% 4.4% 4.1% 4.7% 3.6% 4.5%

EBIT 4 2,441 6,145 5,395 7,739 4,097 5,984

EBIT margin 0.9% 2.1% 1.9% 2.7% 1.6% 2.9%

Net group result -3,306 -227 -2,490 -882 -3,548 990

Cashflow 5 6,961 8,897 6,370 7,624 3,481 5,861

Capital base 33,657 39,892 35,988 32,237 31,879 7,821

Balance sheet Total 146,414 159,707 161,211 149,372 150,721 104,770

Solvency percentage 23.0% 25.0% 22.3% 21.6% 21.1% 7.5%

Net interest-bearing debt 41,070 43,400 52,088 62,721 72,214 45,306

1 EBITDA is calculated as the operating result increased by the amortisation of intangible and depreciation of tangible fixed assets.

2 The correction for one-off special costs and acquisition effects relates to acquisition and transaction costs, reorganisation costs and other one-off special costs, and the full year effect of the acquisitions that were carried out.

3 EBITA is calculated as the operating result increased by the amortisation of intangible fixed assets.

4 EBIT is equal to the operating result.

5 Cash flow is calculated as the net group result increased by the amortisation of intangible and depreciation of tangible fixed assets.

6 The net interest-bearing debt is calculated as the total sum of the loans, redemption obligations and debts to credit institutions, decreased by the cash at banking institutions.

7 Annual review 2012/2013 baarsma wine group holding

Structure of the Group

31 March 2013

Profile

Baarsma Wine Group Holding (BWGH) is a worldwide wine distributor of quality wines with a fast growing

distribution network in all sectors of the wine market in North-West Europe. With its refreshing philosophy and

innovative approach, BWGH seeks to make a difference in the competitive world of wines, combining a focus on

results with an informal company culture.

The Group is the leading distributor of wines in the Netherlands, realised by several specialised business units

operating in each channel of the Dutch wine market. Typical of the organisation is the independent status of

every business unit. By combining the forces of the total Group a unique wine strategy and market approach is

realised.

By means of autonomous growth and acquisition, the Group will expand its position even further over the

coming years. The basis for growth is a ratio of profitability that is sufficient to guarantee the continuity of the

Group.

Mission, vision and strategic goals

Holding

Armit Wines Hasselt MillesimeBaarsma Wines

Oud Reuchlin & Boelen

Wine Excel

Wijnvoordeel

Leon Colaris

Wijnbeurs

94 Wines

Baarsma South Africa

Winetracks

Rutishauser

B2CNetherlands

United Kingdom Belgium Switzerland

8Annual review 2012/2013baarsma wine group holding

Mission of the Group

The corporate objective is to become the first choice provider of basic and premium wines in North-West

Europe, to strengthen our market position in this region by selling qualitative wines via dedicated people

and by expanding our distribution network.

In doing so, our ambition is to achieve a sustainable growth in both turnover and in profit to maximise

shareholders’ value.

Core ideologies

• Focus on consumers and brands

• To turn every customer into a friend

• Excellence in reputation, work with passion

• Focus on execution, walk while you talk

• Be in partnership with employees

• Honesty, integrity and ethics in all aspects of business

Group Strategy

• Expanding our distribution network in North-West Europe, especially in Business to consumer

• Maintaining and reinforcing the Group’s competitive position

• Strengthening our position as a partner and preferred supplier for important clients

• Positioning the Group as an ideal partner for brand owners

• Responding quickly to developments in the international market

• Reducing our dependence on certain markets and product groups

Mission, vision and strategic goals

Our Approach

11 Annual review 2012/2013 baarsma wine group holding

Business to Consumer Wijnvoordeel

Our approach is characterised by considerable investments in the Business to Consumer market in North-West

Europe. We have several labels and different propositions on the market. Wijnvoordeel is one of the most

successful labels within the Business to Consumer segment.

Within Baarsma, Wijnvoordeel specialises in the sale of wine through the internet. In 1999, Wijnvoordeel was

the first Dutch wine web shop. Recent years have seen a sensational expansion of Wijnvoordeel as a joint

effort with Baarsma, allowing it to take the leading position in the online sale of wine. Currently Wijnvoordeel

is among the 50 largest internet companies in The Netherlands. A unique achievement for a company that

specialises in wine, especially given the fact that we have to compete with players such as Wehkamp, Bol and

Zalando.

Our strength is to combine a passion for wine with a highly efficient e-commerce approach. Year on year,

innovations quickly follow each other. We maintain a continuous search for the most commercially viable wines,

which we then offer through, for example, the internet, e-mail and social media by means of high-profile

campaigns. Each customer is specifically targeted and his or her every wish catered to. This means that we do

not follow the latest trends but, rather, set them.

Thanks to its spectacular growth, Wijnvoordeel now represents a number of leading brands. Casa Safra is an

excellent example of this, but Queensland Cellars, Skoonuitsig and Pierre Baptist are also extremely popular

with the wine-buying consumer. This year, Wijnvoordeel has once again set the trend with the launch of

Goldish Noir, a red bubbly! The first wine reviewers are calling it the wine sensation of 2013.

The success of Wijnvoordeel has not been limited to the Netherlands. Both Germany and Belgium are already

showing spectacular growth results. Additionally, the innovative know-how of Wijnvoordeel is also used for

other Business Units within Baarsma. The online sale of wine opens up possibilities for the future and we are

particularly proud of the pioneering role of Baarsma in realising these possibilities.

03/04

30,000,000Turnover in Euros

Euro

25,000,000

20,000,000

15,000,000

10,000,000

5,000,000

004/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13

Date

12Annual review 2012/2013baarsma wine group holding

UNITED KINGDOM

REST OF EUROPE

REST OF THE WORLD

SWITZERLAND

FRANCE

GERMANY

NETHERLANDS

BELGIUM AND LUXEMBOURG

167,8

23,2

6,7

33,2

6,0

30,6

1,2

18,9

Division of Turnover per country

Below, the division of turnover has been represented according to country, channel and brand. It shows the

long-term group strategy of growth in B2C and the growth in the sale of brands. In 2012/13, the upward trend

of increased turnover in B2C and brands was interrupted, in particular due to a drop in sales of Bordeaux wines.

It is expected for 2013/14 that the increase in these segments will return. It is also the Group’s ambition to

spread turnover over several countries. This strategy allows us to reduce the Group’s vulnerability. Additionally,

the growth in B2C and brands will result in increased and permanent profitability.

Geographically

(numbers in EUR x mln)

2012/2013 2011/2012 2010/2011 2009/2010

Netherlands 161,0 167,8 177,5 184,6

United Kingdom 21,8 33,2 36,1 29,5

Belgium & Luxembourg 27,3 23,2 19,4 17,5

Switzerland 28,5 30,6 29,1 26,7

France 0,9 1,2 1,1 3,8

Germany 4,9 6,0 3,5 3,4

Rest of Europe 5,1 6,7 4,9 6,4

Rest of the world 11,9 18,9 12,4 13,0

Total 261,4 287,6 284,0 284,9

13 Annual review 2012/2013 baarsma wine group holding

Turnover per channel

Channels 2012/2013 2011/2012 2010/2011 2009/2010

Retail

Specialist

Catering

Other B2B

B2C

38%

7%

16%

12%

27%

37%

6%

16%

13%

29%

39%

5%

14%

14%

27%

43%

5%

14%

18%

20%

Total 100% 100% 100% 100%

%

Channels 2012/2013 2011/2012 2010/2011 2009/2010

Brands 35% 42% 37% 39%

Other 65% 58% 63% 61%

Total 100% 100% 100% 100%

50

40

30

20

10

0

B2C

B2B

2010/20112011/20122012/2013 2009/2010

90

100

80

70

60

50

40

30

20

10

0

Brands

Other

35

42

37

39

65

58

63

61

11/1212/13 09/1010/11

Channels

Retail

Turnover ratio

Catering

Specialist

15 Annual review 2012/2013 baarsma wine group holding

General

For Baarsma Wine Group, the year under review 2012/13 was strongly influenced by the wine harvests in

Europe. Italy saw the worst harvest in over 60 years, which meant that the quantity of available wine was

drastically reduced and consequently wine prises rose by more than 20%. This had a significant impact on the

cost price of the Group’s largest brand: Canei. In an effort to limit the price increase for the consumer, it was

decided that we would pay a large part of the increased cost price ourselves. This naturally did put pressure on

the Group’s results. Furthermore, the quality of the Bordeaux harvest 2011 paled in comparison to the excellent

years of 2009 and 2010. This meant that Armit’s En-Primeur Campagne 2011 was considerably smaller in

comparison to previous years and the trade in older Bordeaux years declined drastically. The subsequent

decline, therefore, was considerable compared to last year.

On the positive side, Baarsma Wine Group was highly successful in the expansion of its B2C-activities in the

Netherlands, Belgium, Germany & Switzerland. In the B2C segment, both turnover and profitability increased

significantly. Wijnvoordeel managed to strengthen its leading position on the Dutch market and now ranks 45 in

the Twinkle top 100, the list of the largest internet companies in the Netherlands. The turnover of Wijnvoordeel

in Belgium and Germany increased significantly (by 19 %). In addition, the reorganisation of De Wijnbeurs was

completed in 2012 and De Wijnbeurs made a strong contribution to the growth of the results in B2C, in both

the Netherlands and Belgium.

The influence of the European financial crisis and the corresponding low consumer confidence was especially

felt in the Netherlands. The consumer kept a tight rein on the purse strings, which had a negative effect on

the margin mix. Consumers are price conscious. They buy cheaper wines at the supermarket or discount

wine store. In the catering industry, wine is increasingly sold per glass rather than per bottle. B2C, too, saw a

decrease in the average order size. In Switzerland, too, the market was under pressure, in particular due to the

decline in tourism resulting from the strong Swiss Franc, which has made Switzerland A relatively expensive

country to spend your holiday.

The group has implemented reorganisations at various locations within the Group in an effort to make the

company more efficient. This mainly involved combining back-offices and reducing overhead costs. The

corresponding reorganisation costs amounted to € 2.1 mln and the expected annual savings also amounted to

€ 2.1 mln.

The sale of the wines of La Tulipe, the most recent acquisition, increased by more than 10% in the year under

review. In light of the circumstances mentioned above, this is a truly remarkable performance. Consequently,

the acquisition did not fall short of expectations. The introduction of the new Slurp! wines also proved to be

highly succesful. A further strong increase in turnover of La Tulipe & Slurp! is expected for the coming years.

Against the background of the challenging market circumstances described above, the results of the Group are

satisfactory. In the year under review, the position in B2C was further expanded and the market share in the

on-trade industry increased. Despite the poor harvests and the general low consumer confidence, the Group’s

profitability remained largely the same, thus providing a solid foundation for profit recovery in 2013/2014.

Report of the Board of Directors

17 Annual review 2012/2013 baarsma wine group holding

Results

The results of the Group have decreased in comparison to last year. A turnover of € 261 mln was realised in

the year under review. A decrease of over € 26 mln, caused mainly (€ 20 mln) by the lower sales of Bordeaux

wines at Armit and the cancellation of two large wine contracts with retailers with a very low gross margin.

Additionally, the growth in turnover at B2C, La Tulipe and Hasselt Millesime and the lower turnover in the

on-trade Industry balanced each other out.

The EBITDA in particular was negatively influenced by the lower Bordeaux sales at Armit and increased pressure

on the margins within retail, especially because of the higher cost prices that could not be completely passed on

to the retailers. The margin pressure on Canei was the largest negative contributor here. The contribution from

the on-trade Industry (Oud Reuchlin & Boelen and Rutishauser) declined in comparison to last year.

The strong performance of Wijnvoordeel and Wijnbeurs had a positive influence on the EBITDA and Hasselt

Millesime (strong growth of Cava MVSA) and La Tulipe also contributed to the growth of the EBITDA.

An EBITDA of € 12.7 mln has been reported in the Financial Overview. This is after the deduction of € 2.7 mln

non-recurring costs. In particular, these costs include integration and reorganisation costs. Major items include

the combining of the customer contact centres of Wijnvoordeel and Wijnbeurs in Gorredijk, along with the

provision for the lease obligations of the former head office in Oudeschoot. The consolidated profit and loss

account closes with a net loss of € 3.3 mln. In the previous year under review, the net loss amounted to

€ 0.2 mln.

On pages 12 and 13, the division of turnover has been represented according to country, channel and brand.

It shows the long-term group strategy of growth in B2C and the growth in the sale of brands. In 2012/13, the

upward trend of increased turnover in B2C and brands was interrupted, in particular due to the aforementioned

drop in sales of Bordeaux wines. For 2012/2013, turnover in Switzerland has been reported as other turnover.

This means that a decrease has been reported in the ‘brands’ share. When corrected for this adjustment, the

division brand/other would have been 40%/60%.

Financial year(numbers in EUR x mln)

2012/13 2011/12

Reported net result -3,3 -0,2

Add: result of the participations (no tax effect) 0,7 -0,2

Add: non-recurring costs (after 25% taxes) 2,0 1,7

Add: goodwill amortisation (no tax deduction) 3,3 3,5

Add: interest charges shareholders’ loan (after 25% taxes) 0,4 0,4

Add: impairment IT systems (after 25% taxes) 0,6 -

Net Operational Result 1 3,7 5,2

This overview shows that the company shows good profitability, although the chosen financing structure

(shareholders’ loans instead of equity), the acquisition strategy and the resulting amortisation of goodwill

(the goodwill is basically maintained given the results of the company) and the non-recurring costs have put

the net result under pressure.

1) Net Operational Result is a concept that is not recognised under generally accepted Dutch accounting principles. It involves the reported net result, adjusted for normalisation items, amortised goodwill and interest charges for the subordinated shareholder’s loan. Normalisation items are income or expenditure that results from certain events or transactions that are part of normal business operations, but which must be adjusted in the reported net result because of their nature, volume or incidental occurrence. This is done in order to offer insight into the EBITDA and, more specifically, the EBITDA development.

Report of the Board of Directors

18Annual review 2012/2013baarsma wine group holding

Investments

Intangible fixed assets

This item consists of goodwill, intellectual property rights, operational software and customer bases.

Because of a release of part of the goodwill reported in the previous year and amortisation amounting to

€ 3.2 mln, the item goodwill was reduced by a total of € 3.5 mln in the year under review. € 2.2 mln was

invested in intellectual property rights in the financial year. This mainly involved investments in the acquisition

of customer bases for the B2C branch and the purchase of new software. The amortisation of intellectual

property rights amounted to € 4.6 mln, so that this item was reduced by € 2.3 mln on balance.

Tangible fixed assets

In the financial year, approximately € 1 mln (2011: € 1.4 mln) was invested in tangible fixed assets. This

involved approximately € 0.4 mln of investments at Rutishauser in new machines as well as shop fixtures and

fittings. The amortisation amounted to approximately € 2.6 mln, so that the item tangible fixed assets was

reduced by approximately € 1.7 mln on balance.

Financial fixed assets

This item was reduced by approximately € 0.9 mln, which was mainly caused by lower deferred tax assets.

Operating Capital

Managing working capital control continues to be a focus point within the group. Because of the extensive

product range and the long supply lines from the wine-producing countries, it is of importance that the right

balance has to be found in terms of stock. On the one hand, timely delivery is essential for the company

but, on the other hand, too much stock means higher storage costs, less credit facilities and an increased

risk of obsolete stock. Compared to last year, stock was reduced by EUR 1.6 mln. Stock management, and

consequently the reduction of working capital, have top priority within the group. The business units are

strongly focused on improving the cash-conversion cycle. This cycle is measured continually and targets have

been agreed upon with the management of the business units to improve it even further. The following three

elements are relevant here:

1 Improving the rate of stock turnover

2 Constant credit management to keep the debtor position as low as possible

3 Optimising the terms of payment to our suppliers

The ratios of these three working capital aspects are as follows:

Financial Year 2012/13 2011/12

Stock Days 74 69

Debtor Days 47 47

Creditor Days 113 112

Report by the Board of Directors

19 Annual review 2012/2013 baarsma wine group holding

Debts to participants

Baarsma Wine Group Holding B.V. is a fully-owned subsidiary of Veenwijk Holding B.V. The equity that is

required to finance the Group’s acquisitions has been raised by Baarsma Wine Group’s parent company,

Veenwijk Holding B.V. The debt to the shareholders decreased due to the repayments that were made.

The total debt to the shareholder amounted to € 5.8 mln at the end of the financial year, which has been

fully subordinated and included in the bank guarantee capital of Baarsma Wine Group Holding B.V.

Net interest-bearing debt

The Group aims to structurally reduce the net interest-bearing debt, in order to be less vulnerable to

fluctuations in the interest and credit markets. In the financial year, the net debt position improved from

€ 43.4 mln to € 41.1 mln. Additionally, the purchase price for the acquisition of La Tulipe was paid in the

financial year.

Financial Instruments

Because of our foreign group companies, the Swiss Franc, the British Pound and South-African Rand are

important to the Group. Fluctuations in these currencies have caused changes in the foreign currency value

of the assets and liabilities of the Group compared to the Euro. Additionally, the American Dollar and the

Australian Dollar are currencies that are relevant to us because of our business activities. When buying and

selling, it is our policy to cover exchange rate risks as soon as they occur. To this end, our policy is to use

forward exchange contracts and option structures.

Given the Group’s financing structure, the interest charges are a significant cost item. Debts to credit

institutions are based on variable interest rates. In order to protect itself against large fluctuations in the

financial markets for the medium term, the Group has covered a large part of its interest-bearing debts with

interest swaps and option structures/interest caps.

In order to protect itself against credit risks, the Group has covered a large part of our debtor positions.

Given the nature of the debtors, it is not possible to insure the amounts owed by consumers. Our other debtor

positions are usually covered by our credit insurance.

The Groups uses a cash pool as protection against the liquidity risk. Given the diversity of our clients and the

agreements we have made with them, it will be fairly easy to predict the incoming cash flow. The liquidity

prognoses are consequently reliable, allowing the Group to manage the liquidity risk.

Market Developments

Wine consumption also showed a very small increase this past year. The decrease of the volumes in the

on-trade industry was counterbalanced by increased volumes in retail and B2C. Prices were put under pressure

by a shift in demand for cheaper wines. On the other hand, excise duty increases in the Netherlands, Belgium

and the United Kingdom and the cost price increases in the wine-producing countries pushed the prices up.

On balance, the average price per bottle in retail in the Netherlands stabilised around € 3.

For the next year, the Group expects a moderate development in volume and turnover. The turnover in the

on-trade industry will continue to be under pressure and will slightly increase in retail and B2C. Restoring

consumer confidence is of paramount importance when it comes to boosting the long-term positive trend

towards increased wine volumes and wine prices.

Report of the Board of Directors

20Annual review 2012/2013baarsma wine group holding

Quality

Within the Group, the concept of ‘quality’ is of paramount importance. All the wines marketed by the group

are subject to permanent quality control, using highly reputable external laboratories. Next to quality control,

great value is attached to the quality of the organisation. Various group companies have the appropriate ISO

certificates. Wine Excel and Baarsma Wines have the prominent ‘higher-level’ BRC certificate, which indicates

that our quality has also been independently reviewed.

Future Developments

Personnel and Organisation

The average number of employees decreased from 378 to 372 in the financial year. This means a decrease of

5 employees compared to last year.

Employees are key to the success of the Baarsma Wine Group. They work on the company’s continued growth

every day with passion and customer-focus. Using management development programmes, wine courses and

practical training courses, the Group continues to invest in the personal development of all its employees and,

consequently, in the growth of its organisation.

It is expected that the workforce will also decrease slightly in 2013/2014. In the next financial year, the focus

will be on a further roll-out of talent management.

Investments

Baarsma Wine Group is always looking for suitable acquisition candidates who will blend in with the Group’s

strategy. Using an accurate analysis of the markets in our target area, North-West Europe, the Group

has gained a precise insight into which acquisitions it should make and is now actively approaching these

companies.

Any acquisitions which might result from this could considerably influence the development of the balance sheet

and the profit & loss account.

When financing acquisitions, the Group’s aim is not to raise the leverage-ratio and to apply a financing structure

in which equity and external debts are combined. Additionally, the Group will continue to invest in the further

expansion of the B2C activities in order to boost the autonomous growth of these activities even further.

Report by the Board of Directors

21 Annual review 2012/2013 baarsma wine group holding

Liquidity and Solvency

During the financial year, our solvency decreased slightly from 25% to 23%. The subordinated bank loans from

participants have been included in the solvency calculation. The Group expects a slight increase in solvency

during the next year.

Apart from new acquisitions, the net interest-bearing debt will decrease, which is in line with the agreements

made with the banks.

Expected Turnover and Result

Based on the current market circumstances, the objective for 2013/2014 is to achieve an improvement of the

turnover and the EBITDA of the Group.

Huizen, 20 June 2013

The Board of Directors

On behalf of Alta Beheer B.V. On behalf of Hoeksterpoort Holding B.V.

Cees de Rade Tjeerd van der Hoek RA

Managing Director Managing Director

Ronald van den Berg RA

Managing Director

Report of the Board of Directors

22Annual review 2012/2013baarsma wine group holding

Consolidated balance sheetas of 31 March 2013

(before appropriation of result)

A s s e t s 2013 / EUR x 1.000 2012 / EUR x 1.000

Fixed assets

Intangible fixed assets

Goodwill 37,412 40,865

Intellectual property rights 14,947 17,233

52,359 58,098

Tangible fixed assets

Land and buildings 178 211

Equipment, fixtures and fittings 3,995 4,929

Other fixed assets 1,981 2,693

6,154 7,833

Financial fixed assets

Non-consolidated participations 1,025 1,088

Loans to non-consolidated participations 7 0

Deferred tax assets 3,016 3,828

Other receivables 350 409

4,398 5,325

CURRENT ASSETS

Inventories

Finished goods and goods for resale 39,649 41,144

Prepayments on inventories 2,246 2,324

41,895 43,468

Receivables

Trade receivables 29,077 29,863

Receivables on non-consolidated participations 519 938

Corporate income tax 644 358

Other receivables 1,435 3,149

Prepayments and accrued income 2,311 1,936

33,986 36,244

Cash 7,622 8,739

146,414 159,707

* The above figures were derived from the Financial Statement 2012/2013 of Baarsma Wine Group Holding B.V., on which Deloitte Accountants B.V. issued an unqualified auditor’s report dated 20 June 2013.

23 Annual review 2012/2013 baarsma wine group holding

Consolidated balance sheetas of 31 March 2013

(before appropriation of result)

E q u i t y & L i a b i l i t i e s 2013 / EUR x 1.000 2012 / EUR x 1.000

Group equity

Legal entity share in group equity 19,968 23,756

Third-party share in group equity 7,889 7,698

27,857 * 31,454 *

Provisions

VUT, pension and anniversary provisions 73 123

Deferred tax liabilities 4,210 4,744

Provision for warranties 27 27

Reorganisation 37 80

Other 950 471

5,297 5,445

Long-term liabilities

Loans from shareholders 5,800 * 8,438 *

Amounts owed to banks 34,374 24,993

40,174* 33,431

Current liabilities

Amounts owed to banks 2,551 14,468

Current portion of long-term liabilities 5,967 4,240

Trade creditors 43,720 40,930

Taxes and social security charges 10,349 12,531

Debts to non-consolidated participations 53 552

Debts to participants 2,724 7,539

Other liabilities and accruals 7,722 9,117

73,086 89,377

146,414 159,707

* Capital base to the banks 33,657 39,892

* The above figures were derived from the Financial Statement 2012/2013 of Baarsma Wine Group Holding B.V., on which Deloitte Accountants B.V. issued an unqualified auditor’s report dated 20 June 2013.

24Annual review 2012/2013baarsma wine group holding

Consolidated profit and loss accountover 2012/2013

2012-2013 / EUR x 1.000 2011-2012 / EUR x 1.000

Net turnover 261,489 287,622

Change in inventories of finished goods -1,573 2,343

Total operating income 259,916 289,965

Costs of raw materials and consumables 186,018 214,917

Costs of subcontracted work and other external costs 20,276 18,816

Wages and salaries 21,914 23,112

Social security costs 4,016 4,096

Depreciation and amortisation of intangible and tangible fixed assets 10,161 9,124

Special value adjustments in respect of intangible and tangible fixed asset 106 0

Other operating expenses 14,984 13,755

Total operating expenses 257,475 283,820

Operating result 2,441 6,145

Financial income and expenses -4,881 -5,205

Result before taxation -2,440 940

Taxation on result of ordinary activities -300 -841

Result from participations -681 164

Consolidated result after taxation -3,421 263

Third-party share 115 -490

Result of the legal entity -3,306 -227

* The above figures were derived from the Financial Statement 2012/2013 of Baarsma Wine Group Holding B.V., on which Deloitte Accountants B.V. issued an unqualified auditor’s report dated 20 June 2013.

25 Annual review 2012/2013 baarsma wine group holding

Consolidated cash flow statement2012/2013

(indirect method) 2012-2013 / EUR x 1.000 2011-2012 / EUR x 1.000

Cash flow from operating activities

Operating result 2,441 6,145

Depreciation and other changes in value 10,267 9,124

Acquisition of non-consolidated participations -148 1,537

10,119 10,661

Changes in working capital

Movement in provisions 1,573 -2,341

Accounts receivable 2,544 4,728

Current liabilities -6,119 -5,086

-2,002 -2,699

Cash flow from business activities 10,558 14,107

Interest received 317 691

Dividend received 0 5,646

Corporate income tax -586 -841

-269 5,496

Cash flow from operating activities 10,289 19,603

Cash flow from investment activities

Investments in intangible fixed assets -2,278 -2,836

Disposals of intangible fixed assets 167 260

Investments in tangible fixed assets -952 -1,367

Disposals of tangible fixed assets 0 14

Acquisition of group companies 0 96

Acquisition of non-consolidated participations 357 -5

Investments in other financial fixed assets -990 -4,610

Disposals of financial fixed assets 871 493

Cash flow from investment activities -2,825 -7,955

Cash flow from financing activities

Movements in third-party share capital 306 68

Capital contribution shareholders 0 3,198

Redemption of short-term amounts owed to banks -11,917 -4,773

Withdrawal / redemption long-term debts 8,719 -4,337

Interest expenses -5,200 -5,880

Cash flow from financial activities -8,092 -11,724

Exchange rate results -489 510

Net cash flow(= change in net cash position)

-1,117 434

Net cash position at the start of the financial year 8,739 8,305

Net cash position at the end of the financial year 7,622 8,739

Net cash movement -1,117 434

* The above figures were derived from the Financial Statement 2012/2013 of Baarsma Wine Group Holding B.V., on which Deloitte Accountants B.V. issued an unqualified auditor’s report dated 20 June 2013.

26Annual review 2012/2013baarsma wine group holding

Contact Information

Baarsma Wine Group Holding

Zwaardklamp 14

1271GK Huizen

T +31 (0) 35 626 1270

F +31 (0) 35 626 1271

www.baarsmawinegroup.com

Colofon

Design Miazo

www.miazo.com

Baarsma Wine Group Holding © 2013. All rights reserved.

www.baarsmawinegroup.com

Baarsma Wine Group Holding (BWGH)

is a worldwide wine distributor of

quality wines with a fast growing

distribution network in all sectors

of the wine market in North-West

Europe.

With its refreshing philosophy

and innovative approach, BWGH

seeks to make a difference

in the competitive world of

wines, combining a focus

on results with an informal

company culture.