ANNUAL REPORT - Royal London Asset Management · Royal London UK Real Estate Fund 3 We are pleased...

29

ASSET MANAGEMENT ANNUAL REPORT Royal London UK Real Estate Fund For the period 1 October 2017 to 31 December 2017

Transcript of ANNUAL REPORT - Royal London Asset Management · Royal London UK Real Estate Fund 3 We are pleased...

ASSET MANAGEMENT

ANNUALREPORT

Royal London UK Real Estate FundFor the period 1 October 2017 to 31 December 2017

Royal London UK Real Estate Fund2

FundRoyal London UK Real Estate Fund

Registered office:55 Gracechurch Street, London, EC3V 0RL

Authorised Contractual Scheme Manager (the “ACS Manager”)The ACS Manager is Royal London Unit Trust Managers Limited.

Place of business and Registered office:55 Gracechurch Street, London, EC3V 0RL

Authorised and regulated by the Financial Conduct Authority; a member of The Investment Association (IA).

T: 020 3272 5000F: 020 7506 6501

Directors’ of the ACS ManagerDirectors: A.S. Carter, R.A.D. Williams, A. Hunt, R. Kumar, S. Spiller,

C.R. Read (appointed 11 January 2018)

Investment AdviserRoyal London Asset Management Limited

Place of business and Registered office:55 Gracechurch Street, London, EC3V 0RL

Authorised and Regulated by the Financial Conduct Authority.

Depositary of the ACSHSBC Bank plc8 Canada Square, Canary Wharf, London, E14 5HQ

Authorised and Regulated by the Financial Conduct Authority.

Registrar and Transfer AgentsHSBC Securities Services (Ireland) DAC

The Register may be inspected at:1 Grand Canal Square, Grand Canal Harbour, Dublin 2, Ireland

Authorised and Regulated by the Financial Conduct Authority.

The Administrator of the ACSHSBC Bank plc8 Canada Square, Canary Wharf, London, E14 5HQ

Authorised and Regulated by the Financial Conduct Authority.

Standing Independent ValuersCushman & Wakefield LLP125 Old Broad Street, London, EC2N 1AR

CBRE LimitedSt Martin’s Court, 10 Paternoster Row, London, EC4M 7HP

Property ManagerJones Lang LaSalle Limited30 Warwick Street, London, W1B 5NH

Legal Advisers to the ACS ManagerEversheds Sutherland (International) LLPOne Wood Street, London, EC2V 7WS

Independent AuditorsPricewaterhouseCoopers LLPChartered Accountants and Statutory Auditors1 Embankment Place, London, WC2N 6RH

FUND INFORMATION

Contents Page

Fund Information 2

Directors’ Report* 3

ACS Manager’s Investment Report* 4

Portfolio Statement* 5

Summary of Material Portfolio Changes 7

Comparative Table 8

Statement of ACS Managers’ Responsibilities* 9

Statement of the Depositary’s Responsibilities 10

Report of the Depositary 10

Independent Auditors’ Report 11

Statement of Total Return 13

Statement of Change in Net Assets Attributable to Unitholders 13

Balance Sheet 14

Statement of Cash Flows 15

Notes to the Financial Statements 16

Distribution Table 25

Fact File 26

Remuneration Policy (unaudited) 27

General Information* 28

*The ACS Manager’s report comprises these items.

Royal London UK Real Estate Fund 3

We are pleased to present the Annual Report for the Royal London UK Real Estate Fund (‘the Fund’), covering the period from 1 October 2017 to 31 December 2017.

About the ACSRoyal London UK Real Estate Fund (the “ACS”) is an authorised contractual scheme in co-ownership form under section 235A of the Financial Services and Markets Act 2000 and was authorised by the FCA with effect from 3 February 2017. The FCA’s product reference number (PRN) for the ACS is 769047.

As a consequence of being constituted as an authorised co-ownership scheme, the ACS is treated as tax-transparent in the UK.

The structure was designed with the intention of its being regarded as tax-transparent elsewhere. Unitholders which are resident for tax purposes in the UK or in any other jurisdiction which recognises the tax-transparency of the ACS will be treated as receiving their appropriate proportion of the net income arising from the Scheme Property as it arises.

The ACS, which is structured as a stand-alone ACS, is a Qualified Investor Scheme (QIS) and an alternative investment fund for the purposes of the AIFM Directive and the AIFM Regulation.

Risk and Reward Profile

1 2 3 4 5 6 7Lower risk Typically lower rewards

Higher risk Typically higher rewards

About this indicator• This Synthetic Risk and Reward Indicator (SRRI) is calculated according to

European Securities and Markets Authority (ESMA) regulations, to allow investors to compare funds on the same basis. According to this methodology the ACS has been classed as category 4.

• The scale shows that the higher the risk, the higher the potential for greater returns. The numerical indicator which is referenced on the scale, is a measure of how much the unit price of this ACS has risen and fallen (over the last five years) and therefore how much the ACS’s returns have varied.

• The ACS is shown in risk category 4 because its unit price has shown a medium level of volatility historically. As an investment, bonds are typically more volatile than money market instruments but less volatile than shares. This ACS is primarily invested in real estate.

Investors should note• The indicator is based on historical data and may not be a reliable indication of

the future risk profile of this ACS.

• The lowest rating does not mean ‘risk free’ and it does not measure the risk that you may suffer a capital loss.

• The risk and reward profile shown is not guaranteed to remain the same and may change over time.

This report has been prepared in accordance with the requirements of the Collective Investment Schemes Sourcebook as issued and amended by the Financial Conduct Authority.

For and behalf of Royal London Unit Trust Managers Limited

ACS Manager

(Director)

(Director)

23 April 2018

DIRECTORS’ REPORT

Royal London UK Real Estate Fund4

ACS performance for 3 months to 31 December 20173 month

total return %

Royal London UK Real Estate Fund 3.33

AREF/IPD UK Quarterly Property Fund Index – All Balanced Funds index 3.10

Source: RLAM and MSCI, as at 31 December 2017. Returns are net of management fees. It should be remembered that past performance is not a reliable indicator of future performance and that the value of units, and the income derived from them, can vary.

Portfolio commentaryRLUKREF was launched on 1 October 2017. Over the 3 months to December, the ACS outperformed its benchmark by 23 basis points. Performance was driven by capital appreciation of the underlying property assets within the ACS.

Over the quarter, the ACS made two acquisitions. The ACS purchased the freehold interest of Century Retail Park, Watford. It also acquired an adjoining ownership at International Trading Estate, Southall in West London.

Market commentaryLooking back at 2017, in spite of a number of headwinds, the UK economy was surprisingly resilient. Despite ongoing uncertainty surrounding Brexit, a snap general election and heightened geo-political tensions in parts of the world, the UK economy delivered steady, if unspectacular growth.

Twelve months ago we had anticipated that 2017 could be a difficult year for the UK real estate market. At the time, we believed the increasingly uncertain macroeconomic environment could dampen investor sentiment.

Despite these concerns, commercial property in the UK delivered a relatively strong year, with total returns of 11.2%, as reported by the IPD Monthly Index. On average, capital values have increased by 5.4% when compared to twelve months ago.

One of the main drivers of this capital appreciation, and a key component has been the continued wave of overseas investment into UK real estate. While total investment turnover at £56bn for the year did not match the level seen in 2015, it was up slightly on 2016. The proportion of investment involving overseas capital continues to grow and is a particularly dominant trend in the UK market. As an asset class, real estate remains very popular. As the hunt for yield persists and investors seek income, many global institutions have increased their allocation to the sector. We expect these trends to continue in the near term. The major cities of the UK remain attractively priced in a global context, and also when compared to domestic bond yields.

Another feature of 2017 was the outperformance of the industrial sector, which surged ahead in both capital and rental terms. Supply and demand dynamics still look favourable and should support further growth. While momentum could cool and returns could therefore decline, we expect the sector to outperform the market average again this year.

There is a market consensus view that Central London offices may see further rental falls and on average underperform against other UK property sectors. Importantly however, this is a view of the sub-sector as a whole, and is not indicative of individual assets. The Central London office portfolio held by RLUKREF is well positioned, with a focus on the prime end of the market and benefits from a number of medium term development opportunities. The portfolio includes mini-estates located in destinations set to benefit from the opening of Crossrail and offers a diverse occupier mix with limited exposure to financial services and no exposure to Canary Wharf.

Rents in Central London remain high compared to historical averages and Brexit uncertainty has weighed on occupier demand and in some cases has delayed corporate decision making. Take up of offices in most Central London submarkets during 2017 was close to the long term average, with flexible or shared workspace providers growing rapidly and increasing their footprint on the landscape. Despite concerns over Brexit, London’s occupier base has continued to evolve with a number of global tech occupiers taking space recently and many fintech operators starting up in the city.

To summarise, last year exceeded expectations. With a shortage of good product and other asset classes remaining expensive, we could see a repeat in 2018, but a number of the risks from twelve months ago have not disappeared and stock selection will remain paramount.

Drew WatkinsFund Manager 26 January 2018Royal London Asset Management

The views expressed are the author’s own and do not constitute investment advice and are not an indicator of future Fund performance.

Source: RLAM, unless otherwise stated.

ACS MANAGER’S INVESTMENT REPORT

Royal London UK Real Estate Fund 5

PORTFOLIO STATEMENTAS AT 31 DECEMBER 2017

31 December 2017

Investments Sector Market value

(£’000)Total net assets

(%)

Direct PropertiesDirect Properties Market Values up to £25mBedfont – Cargo 30 Industrial Brighton – 1-8 Regent Hill and 188/191 Western Road Retail Bristol – 1-3 & 5-9 Broad Plain Offices Cambridge – 30/31 Petty Cury Retail Chelmsford – 5 Springfield Business Park Industrial Chelmsford – 5 Springfield Business Park Phase 1 Industrial Chelmsford – 5 Springfield Business Park Phase 3 Industrial Chelmsford – Land at Springfield Business Park Industrial Chester – 22/24 Eastgate Street and 30 Eastgate Row Retail Chichester – 9, 10, 11 East Street Retail Daventry – Distribution Centre Industrial Egham – Runnymede Centre Industrial Erdington – B&Q Retail Gatwick – 2 City Place Offices Guildford – 145-147 High Street Retail Guildford – Woodbridge Road Retail Warehouse Hayes – Chailey Industrial Estate Industrial Hayes – Pasadena Close Industrial Hedge End – Royal London Park Industrial Hemel – Robert Dyas Industrial Kingston-upon-Thames – 6/8a Church Street Retail Kingston-upon-Thames – 83/83A Clarence Street Retail Leeds – Phase 1 and 2 Manston Industrial Estate Industrial Leeds – Queens Arcade Retail Leeds – Stourton Link Haigh Park Road Industrial Leicester – GP2002 Unit Grove Park Industrial London EC4 – 32/33a Farringdon Street Offices London EC4 – 68-71 Fleet Street Offices London EC4 – Meridian House Offices London NW10 – 1-11 Cumberland Avenue Industrial London NW10 – Cumberland and Whitby Avenue Industrial London SW3 – 124 Kings Road Retail London W1 – 103/103A Oxford Street Retail London W1 – 22 Old Bond Street Retail London WC1 – Medius House Offices London WC2 – 2-4 Bucknall Street and 12 Dyott Street Offices Maidenhead – 68 Lower Cookham Road, Whitebrook Park Offices Maidenhead – Beach House Offices Maidenhead – King’s Gate Offices Manchester – Davenport Green Offices Manchester – H&M – Kings Court Retail Newcastle – Central Exchange Buildings Retail Newcastle – 102 Grey Street Retail Northampton – Units 1-5 Brackmills Industrial Estate Industrial Nottingham – Unit 1, PC World Retail Oxford – 43/44 Queen Street Retail Oxford – Centremead / Ferry Mills Industrial Redhill – Gatton Park Business Centre Industrial Richmond Upon Thames – 9-10 George Street Retail Southall – 169 Brent Road Industrial Southall – Brent Park Industrial Estate Industrial Southall – Bulls Bridge Trading Estate Industrial Southall – Units 3-6 Boeing Way Industrial Southampton – Southampton Mail Centre Industrial Staffordshire – Tamworth Audi Garage Leisure Tamworth – Plot 1 – Mini Car Showroom Leisure Tamworth – Plot 4 – BMW Car Showroom Leisure Tamworth – Unit 1, Cardinal Point Industrial Tamworth – Ventura Park Trading Estate Industrial

Royal London UK Real Estate Fund6

31 December 2017

Investments Sector Market value

(£’000)Total net assets

(%)Direct Properties Market Values up to £25m – continuedWindsor – Minton Place and Consort House Offices York – 21/23 Coney Street Retail York – 29/31 Coney Street Retail Total Direct Properties Market Values up to £25m 712,745 25.27

Direct Properties Market Values between £25m and £50m Brixton – Ellerslie Square Industrial Estate Industrial Chatham – Horsted Retail Park Retail Hayes – 1/3 Uxbridge Road Industrial Leeds – Colton Retail Park Retail Warehouse London EC1 – 14-21 Holborn Viaduct Offices London SE1 – Land at Six Bridges Trading Estate Industrial London SE18 – Westminster Industrial Estate Industrial London SW6 – Hurlingham Retail Park Retail Warehouse London WC2 – 20 and 1-3 Long Acre and 20 Garrick Street Offices Norwich – Sprowston Retail Park Retail Preston – Capitol Leisure Park Leisure Reading – 410 Thames Valley Park Offices Salford – Metroplex Business Park Industrial Southall – International Trading Estate Industrial Tamworth – Cardinal Point Retail Park Retail Warehouse Tunbridge Wells – Longfield Road Retail Park Retail Warehouse Total Direct Properties Market Values between £25m and £50m 588,255 20.86

Direct Properties Market Values between £50m and £100m Greenford – Westway Shopping Park Retail London E1 – Eden House Offices London EC3 – 62-63 Fenchurch Street Offices London EC4 – 1-3 St Pauls Churchyard Offices London SW1 – 85/87 Jermyn Street Offices London SW1 – Parnell House Offices London W1 – Frith & Dean Street and Soho Square Offices London W1 – Ham Yard Hotel Leisure London W1 – 149 & 151/151A Oxford Street Retail London WC1 – Castlewood House Offices London WC2 – Trafalgar Buildings Offices Preston – Capitol Retail Park Retail Warehouse Watford – Century Retail Park Retail Warehouse Total Direct Properties Market Values between £50m and £100m 860,685 30.52

Direct Properties Market Values greater than £100m London W1 – 120-122 New Bond Street Retail London W1 – Kingsley House Offices London W1 – 470/482 Oxford Street and Granville Place Retail London WC2 – 9-12 Bow Street and Hanover Place Retail Total Direct Properties Market Values greater than £100m 572,066 20.28

Collective Investment Schemes Industrial Property Investment Fund Collectives 46,928 1.66Royal London Cash Fund Z Acc Collectives 27,029 0.96Royal London Enhanced Cash Plus Fund Z Acc Collectives 27,045 0.96Total Collective Investment Schemes 101,002 3.58

Portfolio of investments 2,834,753 100.51

Fair value adjustments 9,235 0.33

Net other liabilities (23,625) (0.84)

Total net assets 2,820,363 100.00

PORTFOLIO STATEMENT (CONTINUED)AS AT 31 DECEMBER 2017

Royal London UK Real Estate Fund 7

The purchases, sales and capital expenditure detail the material changes in the portfolio during the period.

The in-specie value of investments to launch the ACS was £2,702,222,000.

SUMMARY OF MATERIAL PORTFOLIO CHANGESFOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

Significant Purchases

Cost £’000

Royal London Cash Fund Z Acc 27,000

Royal London Enhanced Cash Plus Fund Z Acc 27,000

Watford – Century Retail Park 5,750

Southall – International Trading Estate 5,087

Subtotal 64,837

Total cost of purchases, including the above, for the period 64,837

Portfolio Capital Expenditure

Cost £’000

Southall – International Trading Estate 436

Watford – Century Retail Park 349

London SW6 – Hurlingham Retail Park 244

Bristol – 1-3 & 5-9 Broad Plain 218

London W1- 149 &151/151A Oxford Street 164

Chatham – Horsted Retail Park 77

Brixton – Ellerslie Square Industrial Estate 49

London SE18 – Westminster Industrial Estate 41

London WC1 – Castlewood House 39

London WC2 – Trafalgar Buildings 21

London W1 – 22 Old Bond Street 16

London SE1 – Land at Six Bridges Trading Estate 15

Southall – Units 3-6 Boeing Way 9

London SW1 – Parnell House 7

London EC1 – 14-21 Holborn Viaduct 6

Windsor – Minton Place and Consort House 4

Manchester – Davenport Green 1

Reading – 410 Thames Valley Park 1

London W1 – 103/103A Oxford Street 1

Subtotal 1,698

Total capital expenditure for the period 1,698

Significant Sales

Proceeds £’000

No sales in the period

Royal London UK Real Estate Fund8

COMPARATIVE TABLE

Class Z Gross Income

Change in net assets per unit31/12/17

(£)

Opening net asset value per unit 100.00

Return before operating charges* 3.59

Operating charges (0.26)

Return after operating charges* 3.33

Distribution on income units (0.99)

Closing net asset value per unit 102.34

* after direct transaction costs of: 0.00

Performance

Return after charges 0.00%

Other information

Closing net asset value (£'000) 2,820,363

Closing number of units 27,558,517

Operating charges excluding property expenses 0.70%

Property expenses 0.29%

Operating charges 0.99%

Direct transaction costs 0.00%

Prices

Highest unit price 102.34Lowest unit price 102.34

It should be remembered that past performance is not a reliable indicator of future performance and that the value of units, and the income derived from them, can vary.

Royal London UK Real Estate Fund 9

The Collective Investment Schemes Sourcebook (COLL) requires the ACS Manager to prepare financial statements for each accounting period which give a true and fair view of the financial position of the ACS for the period.

The financial statements are prepared on the basis that the ACS will continue in operation unless it is inappropriate to assume this. In preparing the financial statements the ACS Manager is required to:

• select suitable accounting policies and apply them consistently;

• make adjustments and estimates that are reasonable and prudent;

• comply with the disclosure requirements of the Statement of Recommended Practice for Authorised Funds issued by the Investment Association in May 2014 (the 2014 SORP);

• comply with the disclosure requirements of the prospectus;

• follow generally accepted accounting principles and applicable accounting standards;

• keep proper accounting records which enable it to demonstrate that the financial statements as prepared comply with the above requirements; and

• take reasonable steps for the prevention and detection of fraud and other irregularities.

The ACS Manager is responsible for the management of the ACS in accordance with its Prospectus.

STATEMENT OF ACS MANAGERS’ RESPONSIBILITIES IN RELATION TO THE FINANCIAL STATEMENTS OF THE FUND

Royal London UK Real Estate Fund10

STATEMENT OF DEPOSITARY’S RESPONSIBILITIES

The Depositary must ensure that the Scheme is managed in accordance with the Financial Conduct Authority’s Collective Investment Schemes Sourcebook, the Investment Funds Sourcebook, the Financial Services and Markets Act 2000, as amended, the Collective Investment in Transferable Securities (Contractual Scheme) Regulations 2013 (together “the Regulations”) and the Contractual Scheme Deed and Prospectus (together the “Scheme documents”) as detailed below.

The Depositary must in the context of its role act honestly, fairly, professionally, independently and in the interests of the Scheme and its investors.

The Depositary is responsible for the safekeeping of all custodial assets and maintaining a record of all other assets of the Scheme in accordance with the Regulations.

The Depositary must ensure that:

• the Scheme’s cash flows are properly monitored and that cash of the Scheme is booked in cash accounts in accordance with the Regulations;

• the sale, issue, repurchase, redemption and cancellation of units are carried out in accordance with the Regulations;

• the value of units of the Scheme are calculated in accordance with the Regulations;

• any consideration relating to transactions in the Scheme’s assets is remitted to the Scheme within the usual time limits;

• the Scheme’s income is applied in accordance with the Regulations; and

• the instructions of the Alternative Investment Fund Manager (“the AIFM”) are carried out (unless they conflict with the Regulations).

REPORT OF THE DEPOSITARY TO THE UNITHOLDERS OF THE ROYAL LONDON UK REAL ESTATE FUND

Having carried out such procedures as we consider necessary to discharge our responsibilities as Depositary of the Scheme, it is our opinion, based on the information available to us and the explanations provided, that in all material respects the Scheme, acting through the AIFM:

(i) has carried out the issue, sale, redemption and cancellation, and calculation of the price of the Scheme’s units and the application of the Scheme’s income in accordance with the Regulations and the Scheme documents, and

(ii) has observed the investment and borrowing powers and restrictions applicable to the Scheme in accordance with the Regulations and Scheme documents of the Scheme.

The Depositary also has a duty to take reasonable care to ensure that Scheme is managed in accordance with the Scheme documents and the Regulations in relation to the investment and borrowing powers applicable to the Scheme.

HSBC Bank plc

23 April 2018

Royal London UK Real Estate Fund 11

Report on the financial statementsOpinion In our opinion, Royal London UK Real Estate Fund’s financial statements:

• give a true and fair view of the financial position of the Scheme as at 31 December 2017 and of the net revenue and the net capital gains on the scheme property of the Scheme for the period then ended; and

• have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice (United Kingdom Accounting Standards, comprising FRS 102 “The Financial Reporting Standard applicable in the UK and Republic of Ireland”, and applicable law), the Statement of Recommended Practice for UK Authorised Funds, the Collective Investment Schemes sourcebook and the Contractual Scheme Deed.

The Royal London UK Real Estate Fund is an Authorised Contractual Scheme. The financial statements of the Scheme comprise the financial statements. We have audited the financial statements, included within the Annual Report (the “Annual Report”), which comprise: the balance sheet as at 31 December 2017; the statement of total return and the statement of change in net assets attributable to unitholders shareholders and the statement of cash flows for the year then ended; the distribution tables; and the notes to the financial statements, which include a description of the significant accounting policies.

Basis for opinionWe conducted our audit in accordance with International Standards on Auditing (UK) (“ISAs (UK)”) and applicable law. Our responsibilities under ISAs (UK) are further described in the Auditors’ responsibilities for the audit of the financial statements section of our report. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

IndependenceWe remained independent of the Scheme in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, which includes the FRC’s Ethical Standard, and we have fulfilled our other ethical responsibilities in accordance with these requirements.

Conclusions relating to going concernIn relation to the funds not mentioned in the emphasis of matter above, we have nothing to report in respect of the following matters in relation to which ISAs (UK) require us to report to you when:

• the Authorised Contractual Scheme Manager’s use of the going concern basis of accounting in the preparation of the financial statements is not appropriate; or

• the Authorised Contractual Scheme Manager has not disclosed in the financial statements any identified material uncertainties that may cast significant doubt about the Scheme’s ability to continue to adopt the going concern basis of accounting for a period of at least twelve months from the date when the financial statements are authorised for issue.

However, because not all future events or conditions can be predicted, this statement is not a guarantee as to the Scheme’s ability to continue as a going concern.

Reporting on other information The other information comprises all of the information in the Annual Report other than the financial statements and our auditors’ report thereon. The Authorised Corporate Scheme Manager is responsible for the other information. Our opinion on the financial statements does not cover the other information and, accordingly, we do not express an audit opinion or, except to the extent otherwise explicitly stated in this report, any form of assurance thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If we identify an apparent material inconsistency or material misstatement, we are required to perform procedures to conclude whether there is a material misstatement of the financial statements or a material misstatement of the other information. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report based on these responsibilities.

Authorised Contractual Scheme Manager’s Investment ReportIn our opinion, the information given in the Authorised Contractual Scheme Manager’s Investment Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

INDEPENDENT AUDITORS’ REPORT TO THE UNITHOLDERS OF THE ROYAL LONDON UK REAL ESTATE FUND

Royal London UK Real Estate Fund12

INDEPENDENT AUDITORS’ REPORT TO THE UNITHOLDERS OF THE ROYAL LONDON UK REAL ESTATE FUND (CONTINUED)

Responsibilities for the financial statements and the auditResponsibilities of the Authorised Contractual Scheme Manager for the financial statementsAs explained more fully in the Authorised Contractual Scheme Manager’s Responsibilities set out on page 9, the Authorised Contractual Scheme Manager is responsible for the preparation of the financial statements in accordance with the applicable framework and for being satisfied that they give a true and fair view. The Authorised Contractual Scheme Manager is also responsible for such internal control as they determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the Authorised Contractual Scheme Manager is responsible for assessing the Scheme’s ability to continue as a going concern, disclosing as applicable, matters related to going concern and using the going concern basis of accounting unless the Authorised Contractual Scheme Manager either intends to wind up or terminate the Scheme, or has no realistic alternative but to do so.

Auditors’ responsibilities for the audit of the financial statementsOur objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

A further description of our responsibilities for the audit of the financial statements is located on the Financial Reporting Council’s website at: www.frc.org.uk/auditorsresponsibilities. This description forms part of our auditors’ report.

Use of this reportThis report, including the opinions, has been prepared for and only for the Scheme’s unitholders as a body in accordance with paragraph 4.5.12 of the Collective Investment Schemes sourcebook as required by paragraph 67(2) of the Open-Ended Investment Companies Regulations 2001 and for no other purpose. We do not, in giving these opinions, accept or assume responsibility for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

Other required reportingOpinion on matter required by the Collective Investment Schemes sourcebookIn our opinion, we have obtained all the information and explanations we consider necessary for the purposes of the audit.

Collective Investment Schemes sourcebook exception reportingUnder the Collective Investment Schemes sourcebook we are also required to report to you if, in our opinion:

• proper accounting records have not been kept; or

• the financial statements are not in agreement with the accounting records.

We have no exceptions to report arising from this responsibility.

PricewaterhouseCoopers LLPChartered Accountants and Statutory AuditorsLondon

23 April 2018

Royal London UK Real Estate Fund 13

FINANCIAL STATEMENTS

Statement of Total Returnfor the period from 1 October 2017 to 31 December 2017

Note £’00031 December 2017

£’000

Income Net capital gains 7 75,231 Revenue 8 34,249

Expenses 9 (7,067)

Net revenue before taxation 27,182 Taxation 10 –

Net revenue after taxation 27,182 Finance lease amortisation 15 (10,710)

Total return before distributions 91,703 Distributions 11 (27,192)

Change in net assets attributable to unitholders from investment activities 64,511

Statement of Change In Net Assets Attributable To Unitholdersfor the period from 1 October 2017 to 31 December 2017

£’00031 December 2017

£’000

Opening net assets attributable to unitholders

Amounts receivable on in-specie transfer of units 2,755,852 Amounts receivable on issue of units –Amounts payable on cancellation of units –

2,755,852

Change in net assets attributable to unitholders from investment activities 64,511

Closing net assets attributable to unitholders 2,820,363

Royal London UK Real Estate Fund14

FINANCIAL STATEMENTS (CONTINUED)

Balance Sheetas at 31 December 2017

Note31 December 2017

£’000

ASSETS

Fixed assets:Investments 2,843,988

Current assets:Debtors 12 15,207 Cash and cash equivalents 13 41,556

Total current assets 56,763

Total assets 2,900,751

LIABILITIES

Creditors: Other creditors 14 42,486 Finance lease payable 15 10,710 Distribution payable 27,192

Total liabilities 80,388

Net assets attributable to unitholders 2,820,363

The notes on pages 16 to 23 are an integral part of these financial statements.

Royal London UK Real Estate Fund 15

FINANCIAL STATEMENTS (CONTINUED)

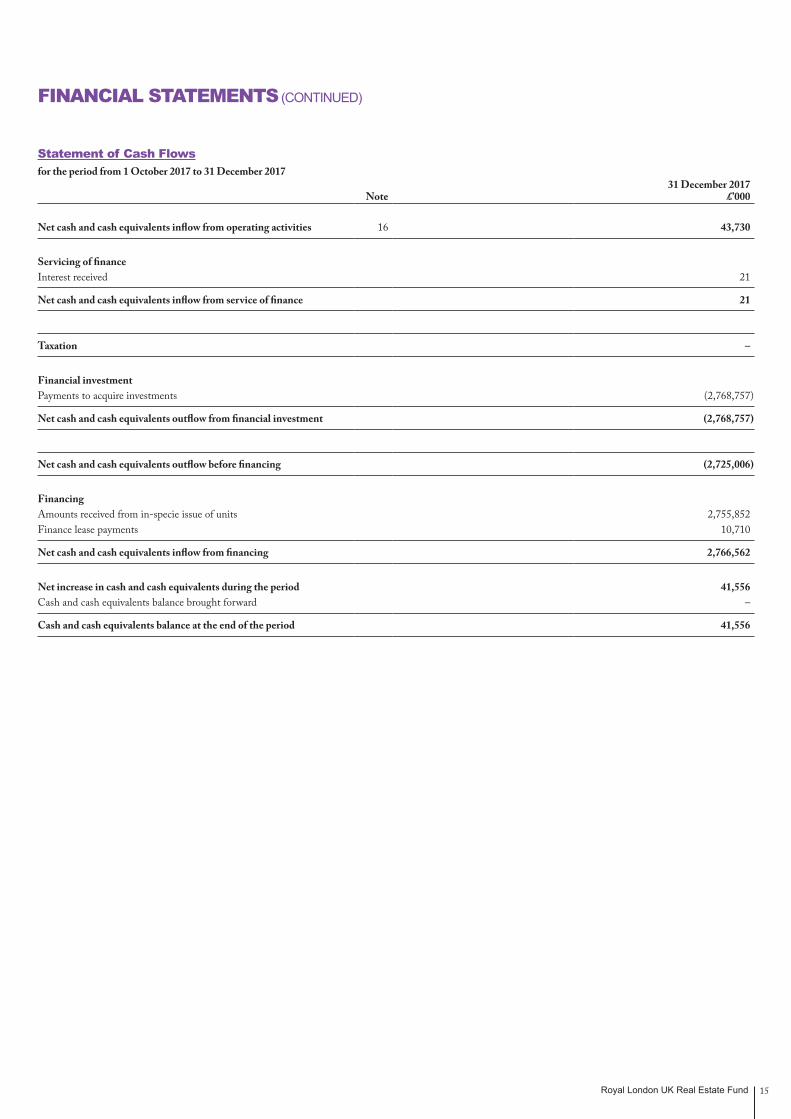

Statement of Cash Flowsfor the period from 1 October 2017 to 31 December 2017

Note31 December 2017

£’000

Net cash and cash equivalents inflow from operating activities 16 43,730

Servicing of financeInterest received 21

Net cash and cash equivalents inflow from service of finance 21

Taxation –

Financial investmentPayments to acquire investments (2,768,757)

Net cash and cash equivalents outflow from financial investment (2,768,757)

Net cash and cash equivalents outflow before financing (2,725,006)

FinancingAmounts received from in-specie issue of units 2,755,852Finance lease payments 10,710

Net cash and cash equivalents inflow from financing 2,766,562

Net increase in cash and cash equivalents during the period 41,556Cash and cash equivalents balance brought forward –

Cash and cash equivalents balance at the end of the period 41,556

Royal London UK Real Estate Fund16

NOTES TO THE FINANCIAL STATEMENTSFOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

1. General InformationRoyal London UK Real Estate Fund (the “ACS”) is an authorised contractual scheme in co-ownership form under section 235A of the Financial Services and Markets Act 2000 and was authorised by the FCA with effect from 3 February 2017. The FCA’s product reference number (PRN) for the ACS is 769047.

As a consequence of being constituted as an authorised co-ownership scheme, the ACS is treated as tax-transparent in the UK.

The structure was designed with the intention of its being regarded as tax-transparent elsewhere. Unitholders which are resident for tax purposes in the UK or in any other jurisdiction which recognises the tax-transparency of the ACS will be treated as receiving their appropriate proportion of the net income arising from the Scheme Property as it arises.

2. Statement of ComplianceThe individual financial statements of the ACS have been prepared in compliance with the Financial Conduct Authority’s Collective Investment Schemes Sourcebook and in accordance with the United Kingdom Accounting Standards, including Financial Reporting Standard 102, ‘‘The Financial Reporting Standard applicable in the United Kingdom and the Republic of Ireland’’ (‘‘FRS 102’’), the Statement of Recommended Practice (SORP) for Financial Statements of Authorised ACSs issued by the Investment Association in May 2014 (the “2014 SORP”) and the Trust Deed.

3. Summary of Significant Accounting PoliciesThe principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied unless otherwise stated. The ACS has adopted FRS 102 in these financial statements.

Basis of preparationThese financial statements are prepared on a going concern basis, under the historical cost convention, as modified by the revaluation of land and buildings and certain financial assets and liabilities measured at fair value through profit or loss.

The preparation of financial statements in conformity with FRS 102 requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the ACS’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in note 4.

FRS 102 requires financial statements to be prepared annually. However, since the ACS was launched on 1 October 2017, the ACS Manager has elected to prepare the first financial statements for the part period from 1 October 2017 to 31 December 2017. As such, there are no prior period comparisons in the financial statements.

Going concernThe ACS meets its working capital requirements through its positive cash inflows including rental income and new subscriptions. There is well placed optimism about the level of demand from investors for ACS as a tax transparent fund with a strong as well as the availability of bank finance for the foreseeable future. The ACS’s forecasts and projections, taking account of reasonably possible changes in investment performance, show that the ACS should be able to operate within the level of its current working capital and credit facilities. After making enquiries, the directors of the ACS Manager have a reasonable expectation that the ACS has adequate resources to continue in operational existence for the foreseeable future. The ACS therefore continues to adopt the going concern basis in preparing its financial statements.

Exemptions for qualifying entities under FRS 102FRS 102 allows a qualifying entity certain disclosure exemptions. The ACS has not taken advantage of any available exemption for qualifying entities.

Consolidated financial statementsThe Royal London Mutual Insurance Society Limited (“RLMIS”) consolidates the ACS on the basis that RLMIS has full control of the ACS through the investment management activities of the ACS Manager, Royal London Unit Trust Manager, which is a wholly owned subsidiary of RLMIS and of its ultimate parent, Royal London Group plc. The ACS is included in the consolidated financial statements of the Royal London Group plc which are publicly available.

Revenue recognitionRevenue is measured at the fair value of the consideration received or receivable and represents the amount receivable for goods supplied or services rendered, net of returns, discounts and rebates allowed by the ACS and value added taxes.

The ACS recognises revenue when (a) the significant risks and rewards of ownership have been transferred to the buyer; (b) the ACS retains no continuing involvement or control over the goods; (c) the amount of revenue can be measured reliably; (d) it is probable that future economic benefits will flow to the entity and (e) when the specific criteria relating to the each of ACS’s sales channels have been met, as described below.

Rental incomeRental income is recognised in the statement of total return on an accrual basis. Revenue from unsettled rent reviews is not accrued until the negotiations are finalised due to the unpredictable nature of the outcome of negotiations.

Interest incomeInterest income is recognised as they are received.

Dividend incomeDividend income is recognised when the right to receive payment is established.

Expenses recognitionExpenses are recognised on an accrual basis

All expenses other than those relating to purchase, sale and capital expense and SDRT from purchase or sale of units are included in expenses on the statement of total return.

TaxationAs the ACS is an umbrealla co-ownership ACS the ACS isn’t subject to UK tax on income or capital gains.

On a daily basis unitholders will be advised of their share of the aggregated accrued income and expenses. It is the responsibility of the unitholder to maintain a record of the relevant amount(s) of income equalisation and to make the appropriate adjustment when completing the tax calculations.

Investment propertiesInvestment properties are those properties, owned by the ACS, that are held either to earn rental income or for capital appreciation or both.

Acquisitions and disposals of investment properties are recognised where, by the end of the accounting period, there is a legally binding, unconditional and irrevocable contract. Additions to investment properties consist of costs of a capital nature. After initial recognition, investment property is carried at open market value, after deduction of lease incentive, rent free debtor and finance lease adjustments.

The difference between the fair value of an investment property at the reporting date and its carrying amount prior to re-measurement is included in the statement of total return as a valuation gain or loss within the ‘net capital gains’ figure.

Royal London UK Real Estate Fund 17

3. Summary of Significant Accounting Policies – continued

Leased assetsAt inception the ACS assesses agreements that transfer the right to use assets. The assessment considers whether the arrangement is, or contains, a lease based on the substance of the arrangement.

Finance leased assetsLeases of assets that transfer substantially all the risks and rewards incidental to ownership are classified as finance leases.

Finance leases are capitalised at commencement of the lease as assets at the fair value of the leased asset or, if lower, the present value of the minimum lease payments calculated using the interest rate implicit in the lease. Where the implicit rate cannot be determined the ACS’s incremental borrowing rate is used. Incremental direct costs incurred in negotiating and arranging the lease, are included in the cost of the asset.

Assets are depreciated over the shorter of the lease term and the estimated useful life of the asset. Assets are assessed for impairment at each reporting date.

The capital element of lease obligations is recorded as a liability on inception of the arrangement. Lease payments are apportioned between capital repayment and finance charge, using the effective interest rate method, to produce a constant rate of charge on the balance of the capital repayments outstanding.

Operating leased assetsLeases that do not transfer all the risks and rewards of ownership are classified as operating leases. Payments under operating leases are charged to the profit and loss account on a straight-line basis over the period of the lease.

Lease incentivesIncentives received to enter into a finance lease reduce the fair value of the asset and are included in the calculation of present value of minimum lease payments.

Incentives received to enter into an operating lease are credited to the profit and loss account, to reduce the lease expense, on a straight-line basis over the period of the lease.

InvestmentsInvestment in collective investment schemes (CIS) is held at fair value with changes recognised in statement.

Cash and cash equivalentsCash and cash equivalents includes cash in hand, deposits held at call with banks, other short-term highly liquid investments with original maturities of three months or less and bank overdrafts. Bank overdrafts are shown within borrowings in current liabilities.

Financial instrumentsThe ACS has chosen to adopt the Sections 11 and 12 of FRS 102 in respect of financial instruments.

Financial assetsBasic financial assets, including trade and other receivables, cash and bank balances and investments in commercial paper, are initially recognised at transaction price, unless the arrangement constitutes a financing transaction, where the transaction is measured at the present value of the future receipts discounted at a market rate of interest.

Such assets are subsequently carried at amortised cost using the effective interest method.

At the end of each reporting period financial assets measured at amortised cost are assessed for objective evidence of impairment. If an asset is impaired the impairment loss is the difference between the carrying amount and the present value of the estimated cash flows discounted at the asset’s original effective interest rate. The impairment loss is recognised in profit or loss.

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

If there is decrease in the impairment loss arising from an event occurring after the impairment was recognised the impairment is reversed. The reversal is such that the current carrying amount does not exceed what the carrying amount would have been had the impairment not previously been recognised. The impairment reversal is recognised in profit or loss.

Other financial assets, including investments in equity instruments which are not subsidiaries, associates or joint ventures, are initially measured at fair value, which is normally the transaction price.

Such assets are subsequently carried at fair value and the changes in fair value are recognised in profit or loss, except that investments in equity instruments that are not publically traded and whose fair values cannot be measured reliably are measured at cost less impairment

Financial assets are derecognised when (a) the contractual rights to the cash flows from the asset expire or are settled, or (b) substantially all the risks and rewards of the ownership of the asset are transferred to another party or (c) control of the asset has been transferred to another party who has the practical ability to unilaterally sell the asset to an unrelated third party without imposing additional restrictions.

Financial liabilitiesBasic financial liabilities, including trade and other payables are initially recognised at transaction price, unless the arrangement constitutes a financing transaction, where the credit instrument is measured at the present value of the future receipts discounted at a market rate of interest.

Trade payables are obligations to pay for goods or services that have been acquired in the ordinary course of operations from suppliers. Accounts payable are classified as current liabilities if payment is due within one year or less. If not, they are presented as non-current liabilities. Trade payables are recognised initially at transaction price and subsequently measured at amortised cost using the effective interest method.

Financial liabilities are derecognised when the liability is extinguished, that is when the contractual obligation is discharged, cancelled or expires.

UnitsUnits are classified as equity. Incremental costs directly attributable to the issue of new units are shown in equity as a deduction, net of tax, from the proceeds.

Units have no par value and, within each Class subject to their denomination, are entitled to participate equally in the profits arising in respect of, and in the proceeds of, the winding up of the ACS. Units do not carry preferential or pre-emptive rights to acquire further units.

Distribution to unitholders Dividends and other distributions to ACS’s unitholders are recognised as a liability in the financial statements in the period in which the dividends and other distributions are approved by the ACS’s Depositary. These amounts are recognised in the statement of changes in net assets attributable to unitholders.

Related party transactions The ACS discloses transactions with related parties which are not wholly owned with the same group. It does not disclose transactions with its parent or with members of the same group that are wholly owned.

Royal London UK Real Estate Fund18

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

4. Critical accounting estimation uncertaintyCritical accounting estimates and assumptionsThe ACS makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are addressed below.

Impairment of debtorsThe ACS makes an estimate of the recoverable value of trade and other debtors. When assessing impairment of trade and other debtors, management considers factors including the current credit rating of the debtor, the ageing profile of debtors and historical experience to make provisions for bad and doubtful debts. See note 12 for the net carrying amount of the debtors and associated impairment provision.

5. Distribution policiesBasis of distributionRevenue is generated by the ACS’s investments during each accounting period. Where revenue exceeds expenses, the net income of the ACS is available to be distributed to unitholders. In order to conduct a controlled distribution flow to unitholders, interim distributions will be made at the ACS Manager’s discretion, up to a maximum of the distributable income available for the period. All remaining income is distributed, at share class level, to the unitholders in accordance with the ACS’s prospectus.

ExpensesIn determining the net revenue available for distribution, expenses related to the purchase and sale of investments are ultimately charged to the capital of the ACS.

6. Risk Management policiesIn accordance with its investment objective, the ACS holds financial instruments such as UK properties. The risks are summarised below.

Market price risk and valuation of propertyThe exposure to market risk arising from the prevailing general economic conditions and market sentiment, may affect the balance sheet and total return of the ACS. Immovable property and immovable property-related assets are inherently difficult to value due to the individual nature of each property. As a result, valuations are subject to uncertainty and are a matter of an independent valuers’ opinion. There is no assurance that the estimates resulting from the valuation process will reflect the actual sales price even where a sale occurs shortly after the valuation date.

Market risk is minimised through holding a geographically diversified portfolio that invests across various property sectors. The Manager adheres to the investment guidelines and investment and borrowing powers established in the Prospectus, instrument of incorporation and in the rules governing the operation of open ended investment companies.

Credit risk and liquidity riskThe ACS can be exposed to credit risk arising from the possibility that another party fails to fulfil its obligations and liquidity risk surrounding its capacity to meet its liabilities.

Investments in immovable property are relatively illiquid and more difficult to realise than most equities or bonds. If an asset cannot be liquidated in a timely manner then it may be harder to attain a reasonable price. The liquidity risk, derived from the liability to unitholders, is minimised through holding cash which can meet the usual requirements of unit redemptions.

However, in times of poor liquidity, the ACS Manager may permit deferral of redemptions for up to one month where a validly submitted redemption notice is received and accepted for a redemption exceeding 5% of the Net Asset Value.

Currency riskAll financial assets and financial liabilities of the ACS are in sterling, thus the ACS has no exposure to currency risk at the balance sheet date.

Interest rate riskThe ACS has the ability to borrow up to 10% of the value of the ACS, but it did not take advantage of this. However, the ACS held £41.6m cash at the end of the period and this is exposed to interest rate risk.

Royal London UK Real Estate Fund 19

7. Net capital gains31 December 2017

£’000 The net capital gains during the period comprise:

Non derivative securities unrealised gains 2,026

Investment property unrealised gains 73,205

Net capital gains 75,231

8. Revenue31 December 2017

£’000 Overseas income 344

Property rental income 33,884

Bank interest 21

Total revenue 34,249

9. Expenses31 December 2017

£’000 Payable to the ACS Manager or associates of the ACS Manager and their agents:

Manager’s fee 4,862

Payable to the Depositary, associates of the Depositary and their agents:

Depositary's fee 60

Safe custody fee 1

61

Other expenses

Administration fee 40

Audit fee 24

Insurance expense 70

Legal and lettings fees 20

Registration fee 1

Surveyor's fee 318

Valuation fee 67

Other 1,604

2,144

Total expenses 7,067

10. Taxation31 December 2017

£’000 Overseas tax –

Total taxation –

As the ACS is an umbrella co-ownership ACS, the ACS isn’t subject to UK tax on income or capital profits.

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

Royal London UK Real Estate Fund20

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

11. Distributions31 December 2017

£’000Final distribution 27,192

Total distributions for the period 27,192

The difference between the net revenue after taxation and the distribution paid is as follows:

Net revenue after taxation 27,182

Expenses charged to capital 10

Total distributions for the period 27,192

Details of the distribution per unit are set out on page 25.

12. Debtors31 December 2017

£’000 Accrued income 344

Accrued interest 1

Rental income receivable 13,365

Other debtors 1,497

Total debtors 15,207

13. Cash and cash equivalents31 December 2017

£’000Cash and cash equivalents 41,556

Total cash and cash equivalents 41,556

14. Other creditors31 December 2017

£’000 Deferred rent 27,722

Accrued expenses 4,988

Managing agent 1,312

VAT payable 6,115

Other creditors 2,349

Total other creditors 42,486

Royal London UK Real Estate Fund 21

15. Finance lease payable31 December 2017

£’000 Commitments in relation to finance leases are payable as follows:

Within one year 517

Later than one year but not later than five years 2,067

Later than five years 97,414

Minimum lease payments 99,998

Future finance charges (89,288)

Total lease liabilities 10,710

The present value of finance lease liabilities is as follows:

Within one year 500

Later than one year but not later than five years 1,767

Later than five years 8,443

Minimum lease payments 10,710

16. Reconciliation of total return before distributions to net cash flow from operating activities31 December 2017

£’000 Total return before distributions 91,703

Less: Net capital gains (75,231)

Less: Interest received (21)

Net income from operating activities 16,451

Increase in debtors (15,207)

Increase in creditors 42,486

Net cash inflow from operating activities 43,730

17. Reconciliation of number of unitsClass Z

Gross IncomeOpening units –

Unit movements 01/10/17 to 31/12/17

Units issued 27,558,517

Units cancelled –

Closing units at 31/12/17 27,558,517

18. Contingent liabilities and outstanding commitmentsThere were no contingent liabilities or outstanding commitments at the current balance sheet date.

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

Royal London UK Real Estate Fund22

19. Related party transactionsThe Fund’s Authorised Contractual Scheme Manager, Royal London Unit Trust Managers Limited and the Depositary, HSBC Bank plc, are related parties to the Fund as defined by Financial Reporting Standard 8 ‘Related Party Disclosures’.

The ACS holds units in the following funds managed by the Authorised Contractual Scheme Manager in proportion to the ACS’s assets as shown:

31 December 2017Fund Managed by £’000 %Royal London Cash Fund Royal London Unit Trust Managers Limited 27,029 0.01

Royal London Enhanced Cash Plus Fund Royal London Unit Trust Managers Limited 27,045 0.01

54,074

The investments income generated is disclosed in Note 7.

Manager fees charged by Royal London Unit Trust Managers Limited are shown in note 9 and details of units issues and cancelled by Royal London Unit Trust Managers Limited are shown in the statement of change in unitholders’ net assets. At the period end the balance due to Royal London Unit Trust Managers Limited in respect of these transactions was £4,862,000.

Depositary fees, safe custody fees and activity fees charged by HSBC Bank plc and their associates are shown in note 9. At the period end the balance due to HSBC Bank plc and their associates in respect of these transactions was £61,000.

The Royal London Mutual Insurance Society, as a material unitholder, is a related party holding units comprising 100% of the total net assets of the ACS as at 31 December 2017.

20. Financial instrumentsThe policies applied to the management of the financial instruments are set out in note 6. The fair values of the ACS’s assets and liabilities are represented by the values shown in the balance sheet on page 14. There is no material difference between the value of the financial assets and liabilities, as shown in the balance sheet, and their fair value.

The ACS’s financial assets comprise cash, on which interest is receivable. However, no interest is receivable or payable on the ACS’s other assets (debtors) or liabilities (creditors).

21. Portfolio transaction costsFor the period ended 31 December 2017

31 December 2017£’000

No transaction costs for the period ended 31 December 2017

Total purchases 64,837

Total sales –

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

Royal London UK Real Estate Fund 23

22. Fair value of investmentsThe primary financial instruments held by the ACS at 31 December 2017 were property related investments, cash, short term assets and liabilities to be settled in cash. The ACS did not hold, and was not a counterparty to, any derivative instruments either during the period or at the period end.

The policies applied to the management of the financial instruments are set out in note 3. The fair values of the ACS’s assets and liabilities are represented by the values shown in the balance sheet on page 14. There is no material difference between the value of the financial assets and liabilities, as shown in the balance sheet, and their fair value.

The fair value of investments has been determined using the following hierarchy:

Category 1 The unadjusted quoted price in an active market for identical assets or liabilities that the entity can access at the measurement date.

Category 2 Inputs other than quoted prices included within Level 1 that are observable (i.e. developed using market data) for the asset or liability, either directly or indirectly.

Category 3 Inputs are unobservable (i.e for which market data is unavailable) for the asset or liability.

For the period ended 31 December 2017Category 1 2 3 TotalInvestments £’000 £’000 £’000 £’000

Collective Investment Schemes – 101,002 – 101,002

Investment properties – – 2,742,986 2,742,986

– 101,002 2,742,986 2,843,988

Reconciliation to Fair Value 31 December 2017

£’000 Cost

At 1 October

Additions on in-specie transfer 2,702,222

Additions – acquisitions 64,837

Additions – subsequent expenditure 1,698

Disposals –

At 31 December 2,768,757

Revaluation Surplus

At 1 October

Revaluations in the period 75,231

Transferred to realised –

At 31 December 75,231

At 31 December 2,843,988

Reconciliation to Market Valuation

Fair value at 31 December 2,843,988

Rent free debtor fair value adjustment 1,475

Finance lease fair value adjustment (10,710)

Market value reported by valuers 2,834,753

The ACS’s interests in investment properties were valued as at 31 December 2017 by Cushman & Wakefield LLP and CBRE Limited in accordance with the Royal Institution of Chartered Surveyors (‘RICS’) Valuation Standards, on the basis of Market Value. Market Value represents the figure that would appear in a hypothetical contract of sale between a willing buyer and a willing seller.

The investment value is a product of rent and yield derived using comparison techniques. In undertaking the valuation of properties under this method, an assessment has been made on the basis of a collation and analysis of appropriate comparable investment, rental and sale transactions, together with evidence of demand within the vicinity of the subject property. With the benefit of such transactions, capitalisation rates have then been applied to the properties, taking into account size, location, terms, covenant and other material factors.

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

Royal London UK Real Estate Fund24

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)FOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

23. Events after the end of the reporting periodRoyal London UK Real Estate Property Feeder Fund launched on 1 January 2018. Distribution was paid on 15 January 2018.

Royal London UK Real Estate Fund 25

Distribution in pence per unit

Class Z Gross Income

Distribution paidDistribution period 15/01/2018October to December 98.6706

DISTRIBUTION TABLEFOR THE PERIOD 1 OCTOBER 2017 TO 31 DECEMBER 2017

Royal London UK Real Estate Fund26

Royal London UK Real Estate Fund

Launch date Class Z – Gross Income Units 1 October 2017

Accounting end dates 31 December (Final)

30 June (Interim)

Distribution dates 15 January (Final)

15 April

15 July

15 October

Minimum investment £50m

Management charges Preliminary charge 0.00%

Annual management charge 0.70%

FACT FILE

Royal London UK Real Estate Fund 27

REMUNERATION POLICY (UNAUDITED)

The ACS Manager of the Royal London UK Real Estate Fund, Royal London Unit Managers Trust Limited (“RLUTM”), is subject to remuneration policies, procedures and practices (together, the “Remuneration Policy”), as required under the UCITS Directive (“UCITS V”). RLTUM has appointed Royal London Asset Management Limited (“RLAM”) as the Investment Adviser to the ACS.

The Remuneration Policy is in line with the business strategy, objectives and values of the ACS Manager and the interests of the Royal London UK Real Estate Fund and the investors in the ACS and includes measures to avoid conflicts of interest. The Remuneration Policy applies to staff of the ACS Manager whose professional activities have a material impact on the risk profile of the ACS Manager or the ACS, and ensures that an individual cannot be involved in determining or approving their own remuneration. The Remuneration Policy will be reviewed and updated annually by the board of directors of the ACS Manager (the “Board of Directors”). Details of the up-to-date Remuneration Policy (provided in the form of the “UCITS Summary Remuneration Policy”), include a description of how remuneration and benefits are calculated, the identity of persons responsible for awarding the remuneration and benefits and the composition of the remuneration committee (if any). The UCITS Summary Remuneration Policy is available on the ACS Manager’s website and a paper copy may be obtained, free of charge, at the registered office of the ACS Manager, upon request.

RLUTM must identify its code staff, whose professional activities have a material impact on the risk profiles of RLUTM and the ACS. Code staff includes senior management, risk takers, control functions, and any employees receiving total remuneration that takes them into the same remuneration bracket as senior management and risk takers. The Remuneration Policy outlines how fixed and variable remuneration is calculated, which includes, but not limited to:

• an assessment of the individual member of staff ’s performance, the relevant ACS, the business unit and its risks;

• restrictions on the awarding of guaranteed variable remuneration;

• the balance between fixed and variable remuneration;

• payment of non-financial remuneration in the form of units or shares in the UCITS funds the Authorised Unit Trust Manger manages;

• a mandatory deferral period of at least 3 years for the payment of a substantial portion of the variable remuneration component; and

• the reduction or cancellation of remuneration in the case of under-performance.

RLUTM has a board of directors (the “Directors”). The Directors have waived their entitlement to receive a director’s fee from RLUTM. RLUTM has no employees and therefore there are no other controlled functions, or senior management employed and paid by RLUTM. However, for the financial period ending 31 December 2016, total remuneration of £7,205,000 was paid to 10 individuals whose actions may have a material impact on the risk profile of RLUTM, of which £4,530,000 related to senior management. The fixed element of the total remuneration mentioned above is £2,502,000 and the variable element is £4,703,000.

In accordance with the Remuneration Policy and the requirements of UCITS V, staff working for RLAM are not remunerated by the ACS Manager but they are subject to remuneration requirements which are equally as effective as those in place under the UCITS Directive. RLAM is also subject to the Financial Conduct Authority’s Remuneration Code.

Royal London UK Real Estate Fund28

GENERAL INFORMATION

Pricing and DealingFor the purposes of determining the prices at which units may be purchased from or redeemed by the ACS Manager, the ACS Manager will carry out a valuation of the ACS’s Property at 5:00 p.m. (the “valuation point”) on the last business day (a day on which the London Stock Exchange Limited is open for business) of each calendar quarter, unless otherwise agreed by the Depositary. However, the ACS Manager may, at its discretion, value the ACS at any other time.

Dealing in units conducted on a monthly basis; on the seventh business day following the end of the previous month, between 9:00 a.m. and 5:00 p.m.

Buying UnitsInvestors should complete an application form available from the ACS Manager and send it to the ACS Manager on or before the 15th of the month prior to the Dealing Day, at its administration centre with a cheque payable to Royal London Unit Trust Managers Limited. On acceptance of the application, units will be sold at the relevant sale price, and a contract note confirming the sale price and the number of units sold together with, in appropriate cases, a notice of the applicant’s right to cancel, will be issued. An order for the purchase of units will only be deemed to have been accepted by the ACS Manager once it is in receipt of cleared funds for the application.

Selling UnitsTo redeem units, investors should provide a written instruction, three months in advance of a monthly Dealing Day, to the ACS Manager at its administration centre with instructions to redeem the relevant number (if known) or value of units. The units will be repurchased at the price calculated at the valuation point on the appropriate Dealing Day. Proceeds of redemption (less, if the proceeds are to be remitted abroad, the cost of such remittance) will be paid no later than the close of business on the fourth business day following receipt of a signed form of renunciation.

Cancellation RightsWhere a person purchases units the Conduct Of Business Sourcebook (as amended from time to time) may give the investor the right to cancel the relevant purchase within 14 days of receipt of the requisite notice of a right to cancel. The right to cancel does not arise if (a) the investor is not a private customer, (b) the investor is not an execution-only customer, (c) the agreement to purchase is entered into through a direct offer financial promotion, or (d) the agreement is entered into under a customer agreement or during negotiations (which are not ISA related) intended to lead to a client agreement.

UK TaxationCapital gains: The sale of the units by a unitholder will constitute a disposal for the purposes of tax on capital gains. The extent of any liability to tax will depend upon the particular circumstances of unitholders. For unitholders within the charge to corporation tax, net capital gains on units should be added to their profits chargeable to corporation tax.

Any individual unitholders resident or ordinarily resident in the United Kingdom will generally be liable to tax on their capital gains. A unitholder who is an individual, and is not resident or ordinarily resident in the United Kingdom, would not normally be liable to United Kingdom tax on capital gains.

SDLT: Stamp Duty Land Tax (SDLT) is payable by the ACS on the purchase of property investments.

AuthorisationThe ACS was authorised by the Financial Conduct Authority on 3 February 2017.

ACS Reports and ProspectusCopies of the latest yearly and half yearly financial statements and copies of the Prospectus may be obtained from Royal London Unit Trust Managers Limited upon request.

SR

EP

RLA

M P

D 0

048

Royal London Asset Management Limited is a marketing group which includes Royal London Unit Trust Managers Limited, authorised and regulated by the Financial Conduct Authority and which manages collective investment schemes, registered in England and Wales number 2372439. This company is a subsidiary of The Royal London Mutual Insurance Society Limited, registered in England and Wales number 99064. Registered office: 55 Gracechurch Street, London EC3V 0RL.