Analysts: 45 650 - stjohns.edu · It had no case, monitor or keyboard ... Apple Inc. sells its...

37

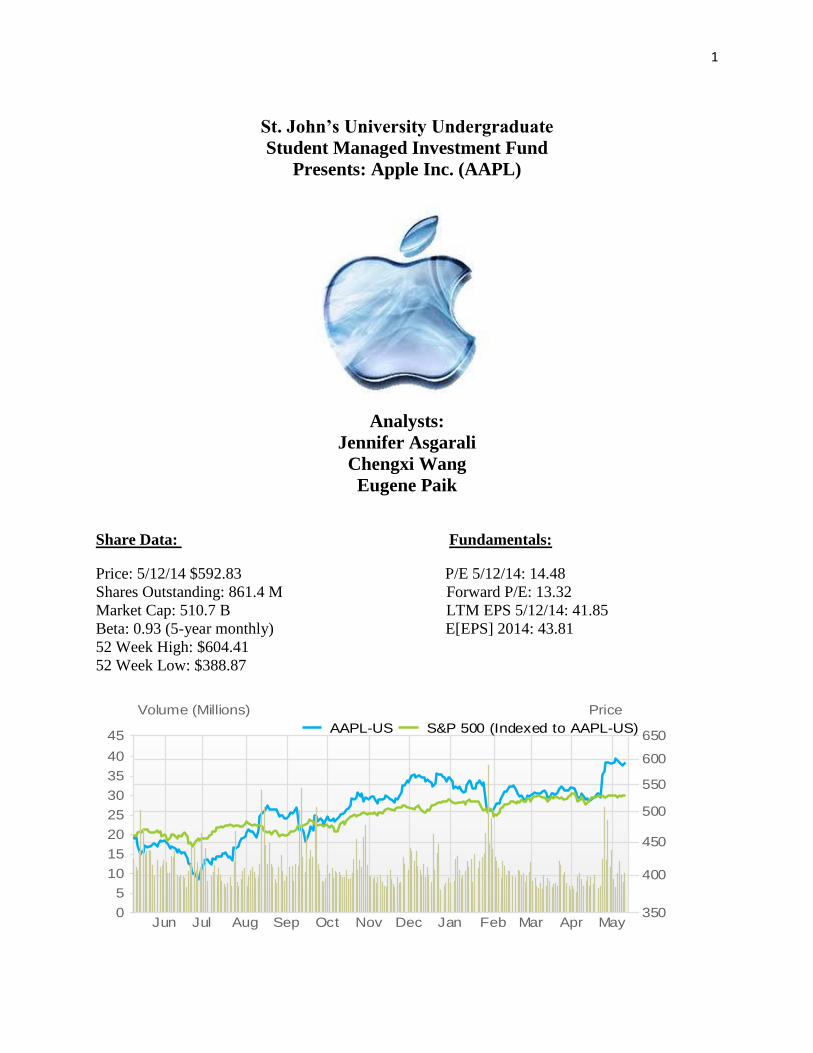

1 St. John’s University Undergraduate Student Managed Investment Fund Presents: Apple Inc. (AAPL) Analysts: Jennifer Asgarali Chengxi Wang Eugene Paik Share Data: Fundamentals: Price: 5/12/14 $592.83 P/E 5/12/14: 14.48 Shares Outstanding: 861.4 M Forward P/E: 13.32 Market Cap: 510.7 B LTM EPS 5/12/14: 41.85 Beta: 0.93 (5-year monthly) E[EPS] 2014: 43.81 52 Week High: $604.41 52 Week Low: $388.87 Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May 350 400 450 500 550 600 650 0 5 10 15 20 25 30 35 40 45 Volume (Millions) Price AAPL-US S&P 500 (Indexed to AAPL-US)

Transcript of Analysts: 45 650 - stjohns.edu · It had no case, monitor or keyboard ... Apple Inc. sells its...

1

St. John’s University Undergraduate

Student Managed Investment Fund

Presents: Apple Inc. (AAPL)

Analysts:

Jennifer Asgarali

Chengxi Wang

Eugene Paik

Share Data: Fundamentals:

Price: 5/12/14 $592.83 P/E 5/12/14: 14.48

Shares Outstanding: 861.4 M Forward P/E: 13.32

Market Cap: 510.7 B LTM EPS 5/12/14: 41.85

Beta: 0.93 (5-year monthly) E[EPS] 2014: 43.81

52 Week High: $604.41

52 Week Low: $388.87

Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

350

400

450

500

550

600

650

0

5

10

15

20

25

30

35

40

45

Volume (Millions) Price

AAPL-US S&P 500 (Indexed to AAPL-US)

2

Table of Contents

Executive Summary 3

Company Overview 4

Industry Overview 11

Fundamental Analysis 12

Income Statement 24

Relative Valuation 27

Absolute Valuation 30

Conclusion/ Recommendation 35

3

Executive Summary

As a result of analyzing Apple Inc. as firm and its position within the personal computer and consumer

electronics industry, we are recommending to sell 35 shares of Apple Inc.’s stock. This decision is based on the

following:

1. According to the Relative Valuation as of 5/5/14, Apple Inc.’s stock should be selling at $538.79.

However, on that date, Apple’s stock was actually priced at $600.96 so Apple’s stock is overpriced.

2. According to our forecasted income statements for 2014 and 2015, Apple’s net income is projected to be

$35.13 B and $35.82 B respectively. Both of these numbers are lower than the net income of $37.04 B

in 2013. Hence, we are expecting Apple’s incomes to fall in the next two years and by extension,

Apple’s profitability.

3. According to the Absolute Valuation Apple must maintain a growth rate of 10.25% post 2020 for Apple

to be fairly valued today. However, we do not expect that Apple’s growth rate will be this high in the

future. Consequently, Apple’s stock is overvalued.

4. Apple has been facing more competition in recent years, from Samsung especially and it is expected that

Apple will experience even more competition in the future from other companies in the information

technology industry. Hence, Apple’s market share will decline and by extension their revenues.

5. Apple has not introduced any real new products since it launched the iPad in 2010. Apple has just been

innovating existing products. This is rather disappointing and based on this trend we are not expecting

much from the company for 2014 and 2015 in terms of new products (except for the iWatch).

4

I. Company Overview

History

Apple Computer was founded on April 1st 1976 by Steven Wozniak, Steven Jobs and Ronald Wayne in

Cupertino, California. Both Wozniak and Jobs attended high school together and also dropped out of college.

Jobs and Wayne had worked together at Atari (a company that created entertainment software), while Wozniak

had worked at Hewlett-Packard. Both Wozniak and Jobs had a dream to make computers user friendly but

Wayne had different intentions since he sold his share of the company for a mere $800 just three months after it

was founded.

“Apple I”, the first computer created by the company was designed by Wozniak in Jobs’ parents’ garage in

1976. It had no case, monitor or keyboard and did not make much of an impact in the computer industry.

However, the company’s fortunes changed in 1977 with the introduction of the “Apple II”. The Apple II was

the first personal computer to have color graphics and enclosed in a plastic case. Sales increased significantly

and the company grew in size. That same year (1977), the company was incorporated as Apple Computer Inc.

In 1980, the company went public and Apple Computer launched “Apple III”. The Macintosh (also known as

the “Mac”) was introduced by Jobs in 1984 and has evolved significantly over the years. On January 9, 2007,

the company became “Apple Inc.” as it dropped the word “computer” since it aimed to expand its presence in

the consumer electronics market.

Today Apple Inc. is an American multinational corporation that is headquartered in Cupertino California.

The company “designs, manufactures, and markets mobile communication and media devices, personal

computers, portable digital music players, and sells a variety of related software, services, peripherals,

networking solutions, and third-party digital content and applications.” 1

Apple Inc.’s hardware products include Macintosh computers, the ipod, the iphone, the ipad and the Apple

TV. Software products include Mac OS X operating system, itunes, ilife (a suite of software applications for

photos, movies and music), iwork (an office suite of applications), Aperture (professional photography software

package), Final Cut Studio (a suite of professional video and audio production software) and Logic Studio (a

suite of audio software).

Apple Inc. sells its products and services worldwide through retail stores, online stores, third party cellular

network carriers and wholesalers. In the U.S. Apple, has approximately 26,000 store employees serving at 250

stores in 44 states. For 2003, Apple Inc. ranked at number 6 on the Fortune 500 list of companies in terms of

revenues.

1 Factset

5

Geographical Locations

Apple Inc. operates literal retail stores in the following 14 countries:

Austrialia

Canada

China

France

Germany

Hong Kong

Italy

Japan

Netherlands

Spain

Sweden

Switzerland

United Kingdom

United States

Outside of those countries listed above, Apple Inc. also operates internet shopping websites in 24 other countries

as of July 2013. These countries are Austria, Belgium, Brazil, Czech Republic, Denmark, Finland, Hungary,

Indonesia, Ireland, Luxembourg, Malaysia, Mexico, New Zealand, Mexico, Philippines, Poland, Portugal,

Russia, Singapore, South Korea, Taiwan, Thailand, United Arab Emirates and Vietnam.

Most of Apple Inc.’s sales for their fiscal year September 2013 came from the Americas. The pie chart below

shows the geographical revenue distribution for Apple Inc. as of September 2013. Please note that the numbers

are all in billions of dollars.

62,739

37,883

25,417

20,228

13,462

11,181

Americas

Europe

Greater China

Retail

Japan

Rest of Asia Pacific

6

Products The chart below shows Apple Inc.’s major revenue earning products/services for the fiscal year September

2013. The numbers shown are in billions of dollars.

91,279

31,980

21,483

16,051

5,706 4,411

iPhone

iPad

Mac

iTunes, Software & Services

Accessories

iPod

7

Corporate Structure

Below is a list of the members on Apple Inc.’s management board.

Chief Executive Officer and Director: Timothy Donald Cook

Senior Vice President Operations: Jeffrey Williams

Chief Financial Officer & Senior Vice President: Peter Oppenheimer

Secretary, Senior Vice President & General Counsel: D. Bruce Sewell

Vice President: Paul Deneve

Treasurer & Vice President: Gary Wipfler

Senior Vice President-Software Engineering: Craig Federighi

Senior Vice President-Hardware Engineering: Daniel J. Riccio

Senior Vice President-Design: Jonathan P. Ive

Senior Vice President-Internet Software & Services: Eduardo H. Cue

Senior Director-Product Marketing, EMEA: Erik Stannow

Senior Vice President-Software Engineering: Guy Tribble

Vice President-Sales: Zane C. Rowe

Manager-Public Relations & Buzz Marketing: Christina Caballero

Senior Vice President-Worldwide Marketing: Philip W. Schiller

Vice President-Finance & Corporate Controller: Luca Maestri

Director-Investor Relations: Joan Hoover

Director-Mac Public Relations: Bill Evans

Director-Public Relations: Colin Smith

Director-Public Relations: Natalie N. Kerris

Director-Public Relations: Trudy Muller

Head-iPod, iBookstore & Apple TV Public Relations: Jennifer Ramsay Newhart

Head-Public Relations: Monica Sarkar

Head-Public Relations: Lizzie Garlinghouse

Manager-Public Relations: Tom Neumayr

Manager-Public Relations: Kristin Huguet

Senior Director-Corporate Public Relations: Steve R. Dowling

Senior Director-Investor Relations: Nancy Paxton

Vice President-Communications: Katie Cotton

Head-Human Resources: Denise Young Smith

8

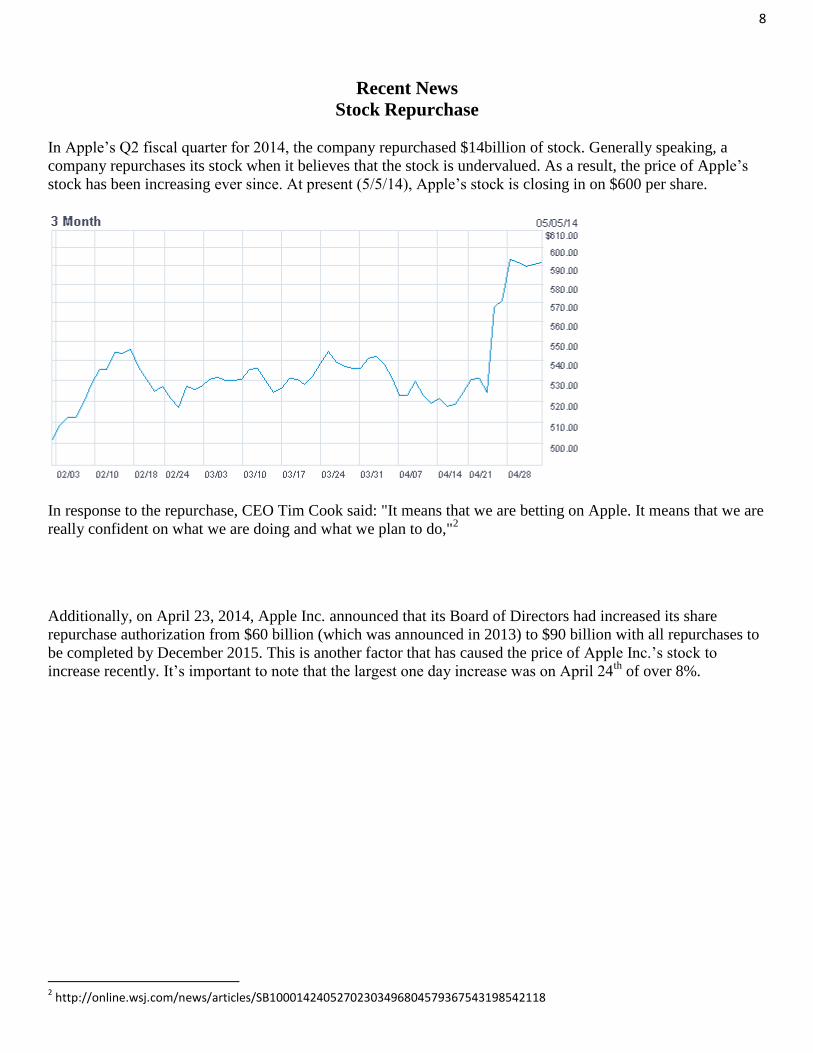

Recent News

Stock Repurchase

In Apple’s Q2 fiscal quarter for 2014, the company repurchased $14billion of stock. Generally speaking, a

company repurchases its stock when it believes that the stock is undervalued. As a result, the price of Apple’s

stock has been increasing ever since. At present (5/5/14), Apple’s stock is closing in on $600 per share.

In response to the repurchase, CEO Tim Cook said: "It means that we are betting on Apple. It means that we are

really confident on what we are doing and what we plan to do,"2

Additionally, on April 23, 2014, Apple Inc. announced that its Board of Directors had increased its share

repurchase authorization from $60 billion (which was announced in 2013) to $90 billion with all repurchases to

be completed by December 2015. This is another factor that has caused the price of Apple Inc.’s stock to

increase recently. It’s important to note that the largest one day increase was on April 24th

of over 8%.

2 http://online.wsj.com/news/articles/SB10001424052702303496804579367543198542118

9

Dividends

On April 23, 2014 Apple Inc. declared that it will increase its quarterly dividend by 7.79% from $3.05 to $3.29.

The first payment date of this higher dividend will be May 15, 2014. The increased dividend has also

contributed to the increasing price of Apple Inc.’s stock. Since Apple, began paying dividends in 2012, it has

consistently been growing its dividend payments to shareholders.

According to an analyst from S&P Indices: “the 8% dividend increase pushes Apple to the top of the list of

dividend stock payers in the world”3

The diagram below shows Apple Inc. leading the list with the highest announced dividend payout for 2014 as of

April 24, 2014.

The bar chart clearly shows that as of this moment Apple Inc. is ranked as the company to pay out the most cash

dividends to its stock holders this year (2014).

3 http://qz.com/202630/apple-just-became-the-worlds-biggest-dividend-stock/#/h/63658,2/

10

Stock Split

Apple Inc. announced a 7-for-1 stock split which will come into effect on June 6, 2014 after the close of

business. As a result, the price of Apple Inc.’s stock is going to be 1/7th

the pre-split price, while maintaining

the market value of the company. Consequently, Apple Inc.’s stock will become more affordable so it will be

financially easier for Apple investors to buy more shares in the company and for potential investors (those who

may have lacked the financial wherewithal to purchase Apple’s stock) to acquire holdings. In fact Apple Inc.

stated that its reason for the split is: “We want Apple stock to be more accessible to a larger number of

investors.”4

As we know the stock split should not have any effect on the total market value of Apple Inc.’s stock (unless the

split is conveying some information about the company to the market). However, the post-split price can cause

the demand for Apple’s stock to increase since more investors can afford to purchase the company’s stock and

as a result, the increased demand can cause the price per share to rise.

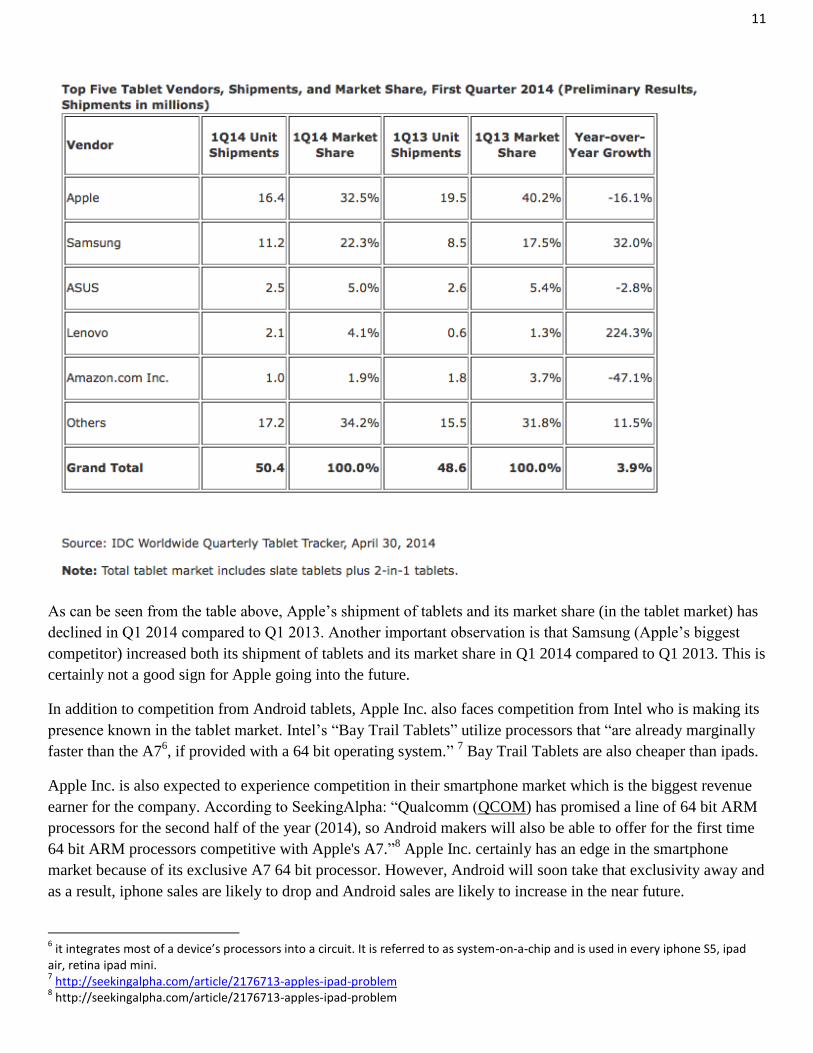

Competition

In an article dated 5/1/14, AppleInsider stated: “Apple is close to losing its dominance in tablet sales, as the ipad

slipped to less than a third of all tablet devices sold in Q1 2014, according to the research firm IDC. A year

earlier, Apple’s ipad was more than 40% of all tablets sold.”5 The 7.7% decline in market share, from 40.2 to

32.5 resulted in a16% decline in units shipped.

The table below shows Apple’s tablet shipments and share compared to its competitors for Q1 in 2013 and

2014.

4 http://investor.apple.com/faq.cfm?FaqSetID=2

5 http://appleinsider.com/articles/14/05/04/apples-ipad-business-isnt-collapsing-but-the-rest-of-the-tablet-industry-sure-is

11

As can be seen from the table above, Apple’s shipment of tablets and its market share (in the tablet market) has

declined in Q1 2014 compared to Q1 2013. Another important observation is that Samsung (Apple’s biggest

competitor) increased both its shipment of tablets and its market share in Q1 2014 compared to Q1 2013. This is

certainly not a good sign for Apple going into the future.

In addition to competition from Android tablets, Apple Inc. also faces competition from Intel who is making its

presence known in the tablet market. Intel’s “Bay Trail Tablets” utilize processors that “are already marginally

faster than the A76, if provided with a 64 bit operating system.”

7 Bay Trail Tablets are also cheaper than ipads.

Apple Inc. is also expected to experience competition in their smartphone market which is the biggest revenue

earner for the company. According to SeekingAlpha: “Qualcomm (QCOM) has promised a line of 64 bit ARM

processors for the second half of the year (2014), so Android makers will also be able to offer for the first time

64 bit ARM processors competitive with Apple's A7.”8 Apple Inc. certainly has an edge in the smartphone

market because of its exclusive A7 64 bit processor. However, Android will soon take that exclusivity away and

as a result, iphone sales are likely to drop and Android sales are likely to increase in the near future.

6 it integrates most of a device’s processors into a circuit. It is referred to as system-on-a-chip and is used in every iphone S5, ipad

air, retina ipad mini. 7 http://seekingalpha.com/article/2176713-apples-ipad-problem

8 http://seekingalpha.com/article/2176713-apples-ipad-problem

12

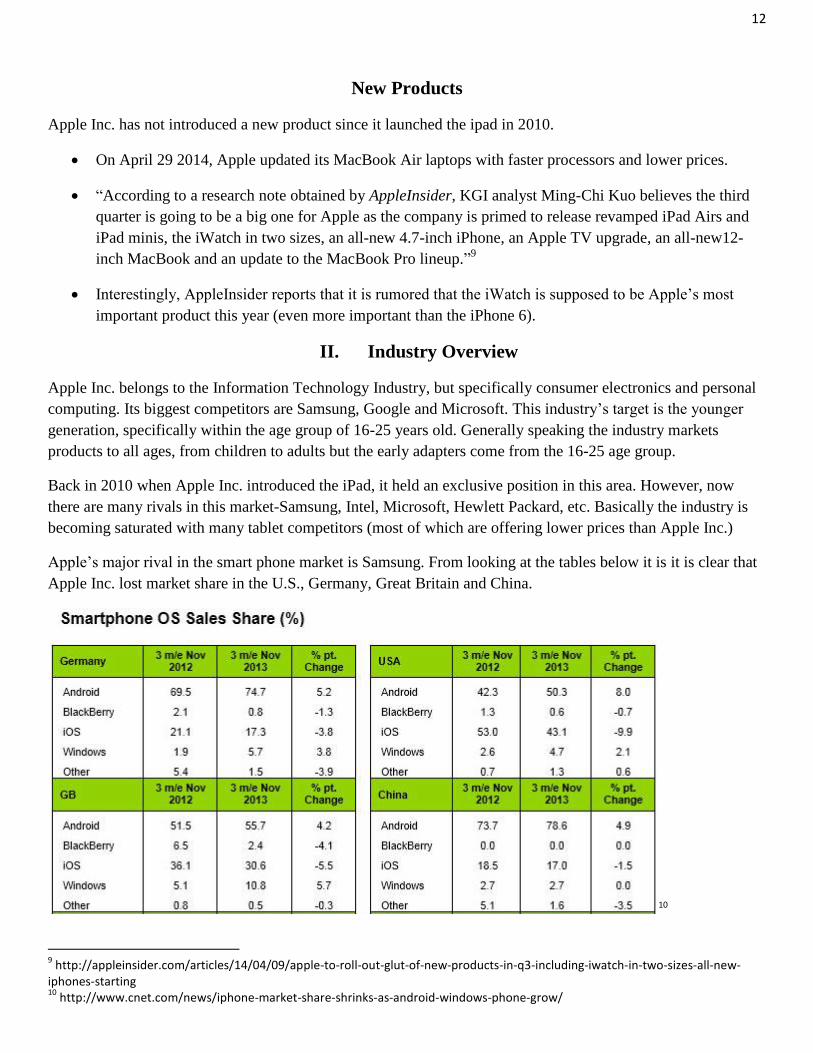

New Products

Apple Inc. has not introduced a new product since it launched the ipad in 2010.

On April 29 2014, Apple updated its MacBook Air laptops with faster processors and lower prices.

“According to a research note obtained by AppleInsider, KGI analyst Ming-Chi Kuo believes the third

quarter is going to be a big one for Apple as the company is primed to release revamped iPad Airs and

iPad minis, the iWatch in two sizes, an all-new 4.7-inch iPhone, an Apple TV upgrade, an all-new12-

inch MacBook and an update to the MacBook Pro lineup.”9

Interestingly, AppleInsider reports that it is rumored that the iWatch is supposed to be Apple’s most

important product this year (even more important than the iPhone 6).

II. Industry Overview

Apple Inc. belongs to the Information Technology Industry, but specifically consumer electronics and personal

computing. Its biggest competitors are Samsung, Google and Microsoft. This industry’s target is the younger

generation, specifically within the age group of 16-25 years old. Generally speaking the industry markets

products to all ages, from children to adults but the early adapters come from the 16-25 age group.

Back in 2010 when Apple Inc. introduced the iPad, it held an exclusive position in this area. However, now

there are many rivals in this market-Samsung, Intel, Microsoft, Hewlett Packard, etc. Basically the industry is

becoming saturated with many tablet competitors (most of which are offering lower prices than Apple Inc.)

Apple’s major rival in the smart phone market is Samsung. From looking at the tables below it is it is clear that

Apple Inc. lost market share in the U.S., Germany, Great Britain and China.

10

9 http://appleinsider.com/articles/14/04/09/apple-to-roll-out-glut-of-new-products-in-q3-including-iwatch-in-two-sizes-all-new-

iphones-starting 10

http://www.cnet.com/news/iphone-market-share-shrinks-as-android-windows-phone-grow/

13

Unfortunately, it appears that Apple Inc. could possibly lose even more market share in this industry in the near

future as Android is expected to offer smart phones with 64 bit processors that is competitive with Apple’s A7.

Generally speaking Apple Inc. is expected to face more competition in its industry in the near future. Most of

Apple’s competitors have a price advantage over Apple Inc. since Apple’s products are highly priced compared

to that of other companies in the industry. In fact Apple Inc. seems to cater to the middle and upper classes

since low income earners often cannot afford, for example a MacBook Air which costs $900+.

III. Fundamental Analysis

A) Ratio Analysis

In the ratio analysis, we include Google, Intel, Microsoft, Samsung, HP, IBM, Research in Motion and Dell as

Apple’s major comparables. The industry average refers to the average performance of the above comparables.

However, in order to give a clear visual chart presentation, we select a few Apple’s major competitors, Google,

Intel, Microsoft and Samsung, to do the chart analysis.

Income & Cash Flow: with regard to Revenue, EBIT, CFO, Industry leadership is threatened by its competitors,

especially Samsung.

Sales Growth

Apple’s sales growth slowed significantly from 2010 to 2013. And in 2013, it was below Google, Intel and

Samsung. One explanation for the trend is since 2010 Apple has not introduced any new products. Its major

product strategy is innovation of existing products. In comparison, its competitors such as Samsung and Google

are introducing new products to create new market.

44.830%

65.830%

27.739% 28.132% 24.676% 26.521%

82.737%

67.242%

28.651%

5.725%

-20.000%

0.000%

20.000%

40.000%

60.000%

80.000%

100.000%

120.000%

140.000%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

to to to to to to to to to to

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Apple

Intel

Microsoft

14

EBIT Growth

From 2012-2013, Apple experienced a decrease in EBIT, when its EBIT yearly growth rate was -11.945%,

which was below industry average. In contrast, Google, Samsung were positive. The fierce competition was

from Samsung, which from 2012-2013 had high growth rate around 30%. And in view of recent 5 years’

average, while Apple’s recent 5 years’ average is lower than its 10 years’ average, Samsung had a significant

increase of 20% in its 5 years’ average compared to its 10 years’ performance.

EBIT Growth: 2003-2013 average vs. 2008-2013 average

2003-2013 2008-2013

Apple 83.28% 50.43%

Google 44.92% 16.11%

Intel 4.39% 5.38%

Microsoft 9.33% 3.48%

Samsung 20.32% 43.73%

HPQ 7.27% -4.81%

IBM 6.43% 3.29%

Research in

Motion

54.43% -7.95%

Dell -3.76% -7.02%

500.000%

194.543%

51.477% 72.331% 20.372%

58.629%

119.017% 98.706%

26.734% -11.945%

-100.000%

0.000%

100.000%

200.000%

300.000%

400.000%

500.000%

600.000%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

to to to to to to to to to to

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Apple

Intel

Microsoft

Samsung

15

Industry

Average

14.11% 13.89%

Cash Flow from Operations

Cash Flow from Operations indicates whether a company is able to generate sufficient positive cash flow to

maintain and grow its operations, or whether it may require external financing. Apple experienced a decrease in

CFO from 2012-2013 (CFO yearly growth rate was -7.374% from 2012 to 2013, below industry).

274.372%

37.114%

83.554% 71.840% 66.775%

11.678%

88.194% 100.602%

25.200%

-7.374%

-50.000%

0.000%

50.000%

100.000%

150.000%

200.000%

250.000%

300.000%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

to to to to to to to to to to

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Apple

Intel

Microsoft

Samsung

16

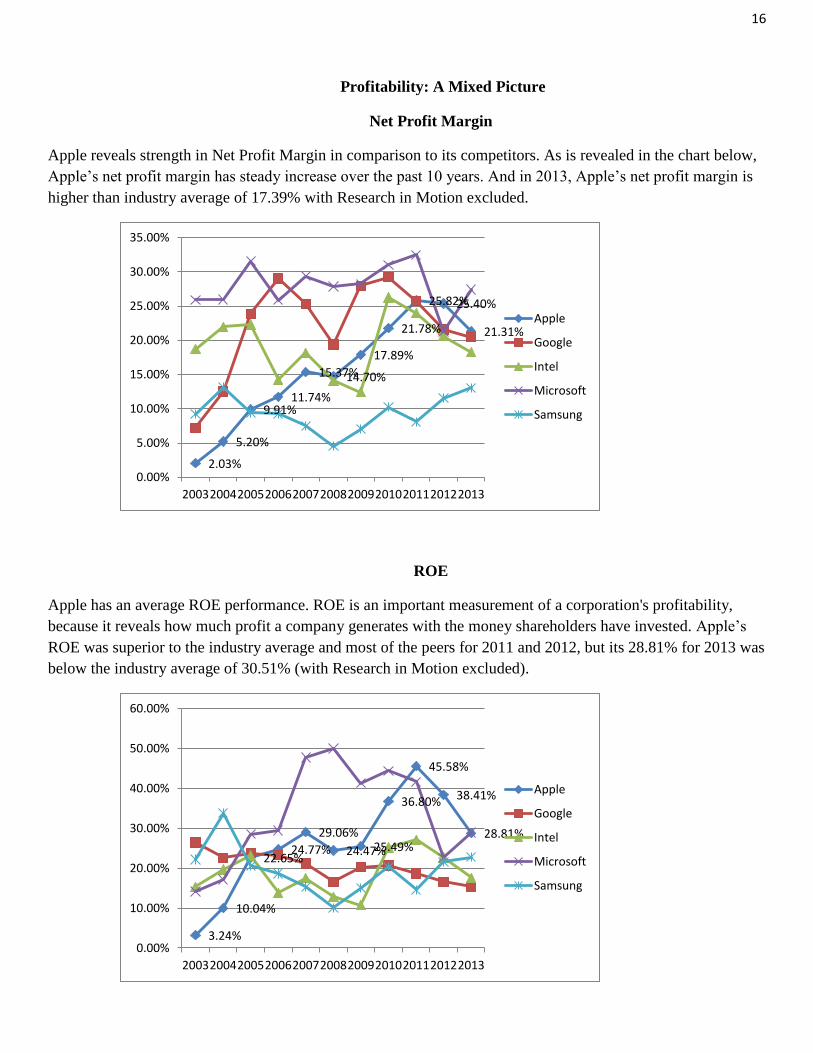

Profitability: A Mixed Picture

Net Profit Margin

Apple reveals strength in Net Profit Margin in comparison to its competitors. As is revealed in the chart below,

Apple’s net profit margin has steady increase over the past 10 years. And in 2013, Apple’s net profit margin is

higher than industry average of 17.39% with Research in Motion excluded.

ROE

Apple has an average ROE performance. ROE is an important measurement of a corporation's profitability,

because it reveals how much profit a company generates with the money shareholders have invested. Apple’s

ROE was superior to the industry average and most of the peers for 2011 and 2012, but its 28.81% for 2013 was

below the industry average of 30.51% (with Research in Motion excluded).

2.03%

5.20%

9.91% 11.74%

15.37% 14.70%

17.89%

21.78%

25.82% 25.40%

21.31%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

3.24%

10.04%

22.65% 24.77%

29.06%

24.47% 25.49%

36.80%

45.58%

38.41%

28.81%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

17

Gross Margin

Gross Margin represents the proportion of each dollar of revenue that the company retains as gross profit, and

its mark-up per dollar of sales. Apple’s gross margin reveals disadvantage. Although Apple showed trend of

slight increase, it’s still lower than industry average.

ROA

ROA is an indicator of how profitable a company is relative to its total assets. ROA gives an idea as

to how efficient management is at using its assets to generate earnings. As is indicated in the chart

below, since 2010, there has been an industry trend of ROA decrease, but Apple’s ROA still

managed to remain high above industry average.

27.27% 27.85% 28.48% 30.24% 34.97% 34.34%

37.60% 39.12% 42.46% 41.87%

36.94%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Apple

Intel

Microsoft

Samsung

Industry Average

2.07%

6.22%

13.63% 14.43% 16.46%

13.34% 15.46%

23.66%

29.26%

24.94%

17.58%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Apple

Intel

Microsoft

Samsung

Industry Average

18

Operating Efficiency: Slightly Positive

Average Performance: Asset Turnover and Receivables Turnover.

The Asset Turnover: an indicator of the efficiency with which a company is deploying its assets, since it

measure sales per dollar of assets. Apple’s Asset Turnover is around the industry average over the past

10 years.

Receivables Turnover: how quickly the firm collects on its credit sales, turning sales into cash.

Apple’s Receivables Turnover is around industry average over the past 10 years.

1.018 1.195

1.375 1.229

1.071 0.907 0.864

1.086 1.133 0.982

0.825

0.000

0.500

1.000

1.500

2.000

2.500

3.000

Apple

Intel

Microsoft

Samsung

Industry Average

10.500 9.842

8.970

7.485 7.034 8.433

10.080 9.700 9.340 8.646

7.44

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

20.000

Apple

Intel

Microsoft

Samsung

Industry Average

19

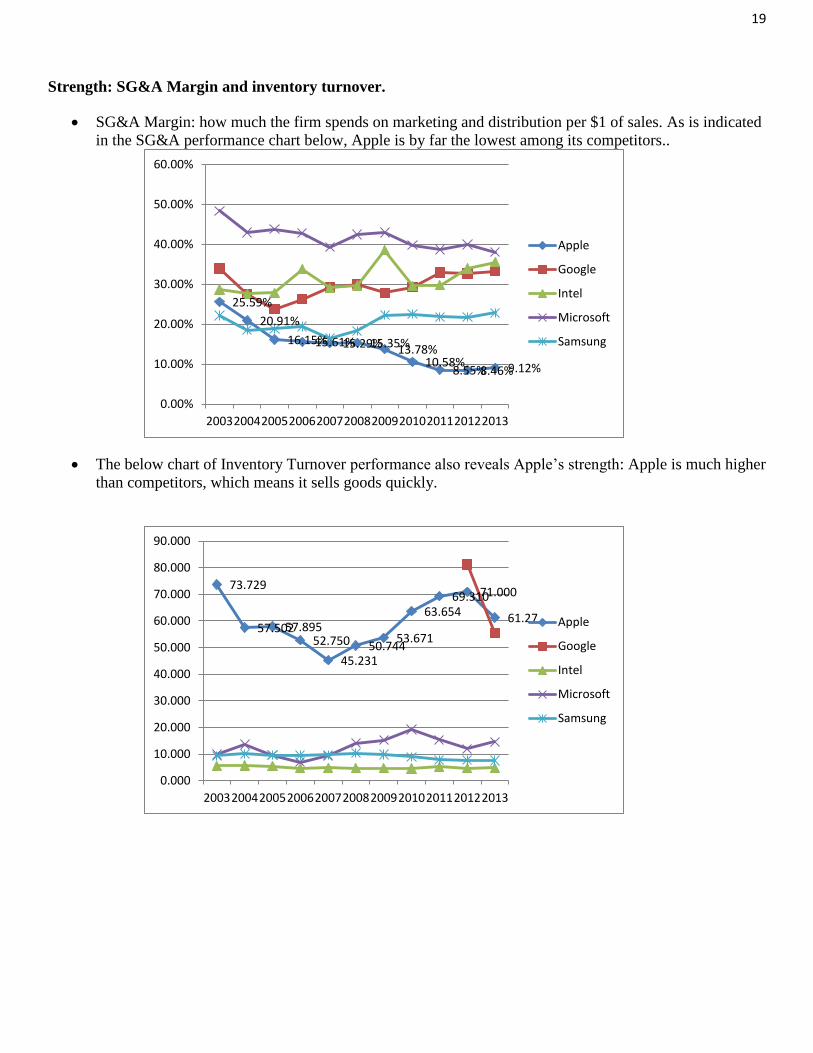

Strength: SG&A Margin and inventory turnover.

SG&A Margin: how much the firm spends on marketing and distribution per $1 of sales. As is indicated

in the SG&A performance chart below, Apple is by far the lowest among its competitors..

The below chart of Inventory Turnover performance also reveals Apple’s strength: Apple is much higher

than competitors, which means it sells goods quickly.

25.59%

20.91%

16.15% 15.61% 15.29% 15.35% 13.78% 10.58%

8.55% 8.46% 9.12%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

73.729

57.502 57.895 52.750

45.231 50.744

53.671

63.654 69.310 71.000

61.27

0.000

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

20

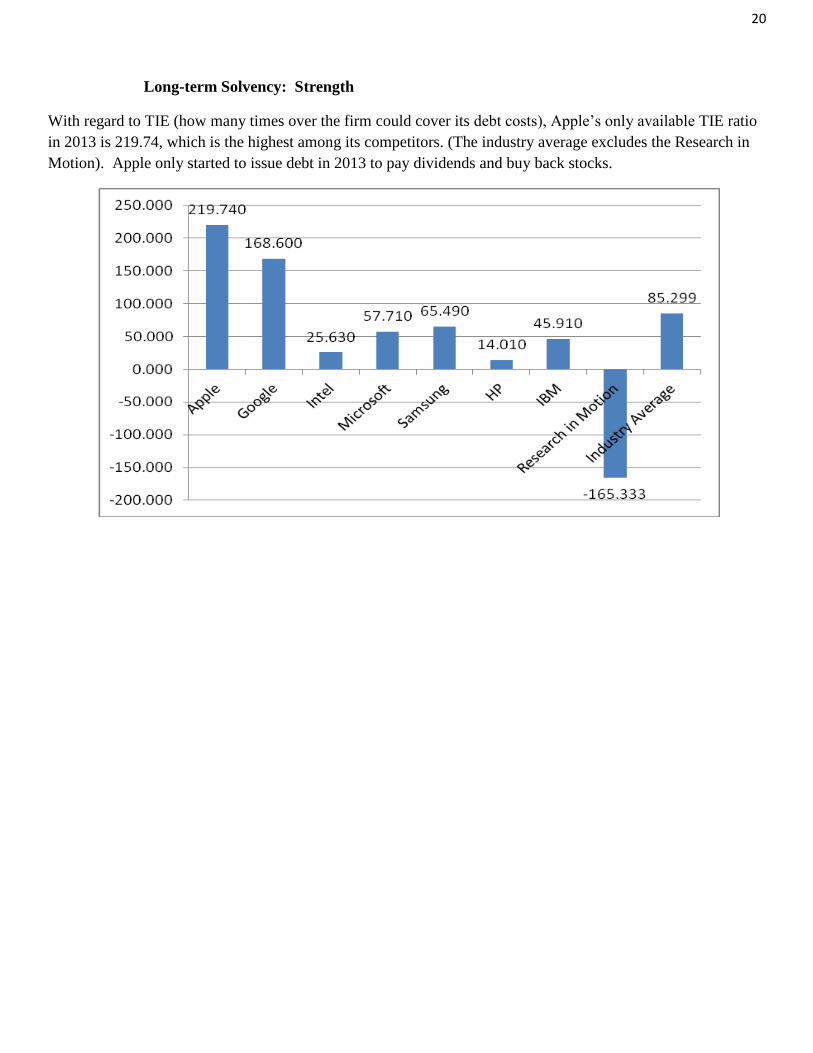

Long-term Solvency: Strength

With regard to TIE (how many times over the firm could cover its debt costs), Apple’s only available TIE ratio

in 2013 is 219.74, which is the highest among its competitors. (The industry average excludes the Research in

Motion). Apple only started to issue debt in 2013 to pay dividends and buy back stocks.

21

Short-term Liquidity

The Current ratio and Quick ratio 2 reveal that in comparison to the majority of its competitors, Apple’s ability

to pay its short-term obligations with its short-term assets is lower. As is indicated in the two charts below,

Apple’s current ratio and quick ratio 2 are below the industry average, and the firm shows decrease trend over

the past 10 years.

Current Ratio

Quick Ratio 2

2.531 2.581 2.404 2.271 2.486 2.219 2.545 1.846 1.583 1.543 1.49

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

2.342 2.371 2.198 2.042 2.171 1.969 2.266 1.591 1.348 1.309 1.226

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

22

DuPont Analysis

The DuPont identity breaks down Return on Equity (that is, the returns that investors receive from the firm) into

three distinct elements: ROE= (Profit Margin)*(Assets turnover)*(Financial Leverage-Averages). In Apple’s

case:

• Threat: Assets Turnover is around industry average.

• Uncertainty: Although Net Profit Margin is high, there’s uncertainty about its future profitability

considering its major product strategy of Innovating old products.

• Strength: Financial Leverage is low in comparison to Apple’s competitors. Apple only started to take on

debt in 2013.

1.018 1.195

1.375 1.229

1.071 0.907 0.864

1.086 1.133 0.982

0.825

0.000

0.500

1.000

1.500

2.000

2.500

3.000

Apple

Intel

Microsoft

Samsung

Industry Average

2.03%

5.20%

9.91% 11.74%

15.37% 14.70%

17.89%

21.78%

25.82% 25.40%

21.31%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple

Intel

Microsoft

Samsung

23

1.568 1.614 1.661 1.716 1.766 1.834 1.648

1.555 1.558 1.540 1.639

0.000

0.500

1.000

1.500

2.000

2.500

3.000

Apple

Intel

Microsoft

Samsung

Industry Average

24

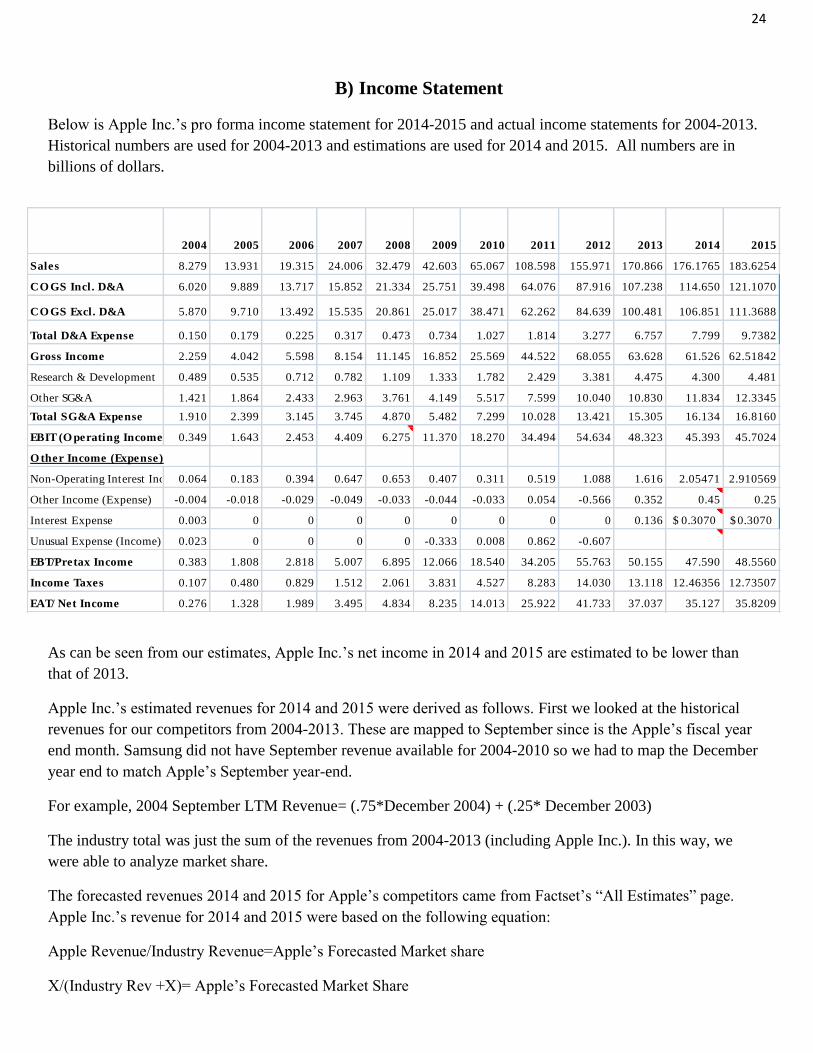

B) Income Statement

Below is Apple Inc.’s pro forma income statement for 2014-2015 and actual income statements for 2004-2013.

Historical numbers are used for 2004-2013 and estimations are used for 2014 and 2015. All numbers are in

billions of dollars.

As can be seen from our estimates, Apple Inc.’s net income in 2014 and 2015 are estimated to be lower than

that of 2013.

Apple Inc.’s estimated revenues for 2014 and 2015 were derived as follows. First we looked at the historical

revenues for our competitors from 2004-2013. These are mapped to September since is the Apple’s fiscal year

end month. Samsung did not have September revenue available for 2004-2010 so we had to map the December

year end to match Apple’s September year-end.

For example, 2004 September LTM Revenue= (.75*December 2004) + (.25* December 2003)

The industry total was just the sum of the revenues from 2004-2013 (including Apple Inc.). In this way, we

were able to analyze market share.

The forecasted revenues 2014 and 2015 for Apple’s competitors came from Factset’s “All Estimates” page.

Apple Inc.’s revenue for 2014 and 2015 were based on the following equation:

Apple Revenue/Industry Revenue=Apple’s Forecasted Market share

X/(Industry Rev +X)= Apple’s Forecasted Market Share

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Sales 8.279 13.931 19.315 24.006 32.479 42.603 65.067 108.598 155.971 170.866 176.1765 183.6254

CO GS Incl. D&A 6.020 9.889 13.717 15.852 21.334 25.751 39.498 64.076 87.916 107.238 114.650 121.1070

CO GS Excl. D&A 5.870 9.710 13.492 15.535 20.861 25.017 38.471 62.262 84.639 100.481 106.851 111.3688

Total D&A Expense 0.150 0.179 0.225 0.317 0.473 0.734 1.027 1.814 3.277 6.757 7.799 9.7382

Gross Income 2.259 4.042 5.598 8.154 11.145 16.852 25.569 44.522 68.055 63.628 61.526 62.51842

Research & Development 0.489 0.535 0.712 0.782 1.109 1.333 1.782 2.429 3.381 4.475 4.300 4.481

Other SG&A 1.421 1.864 2.433 2.963 3.761 4.149 5.517 7.599 10.040 10.830 11.834 12.3345

Total SG&A Expense 1.910 2.399 3.145 3.745 4.870 5.482 7.299 10.028 13.421 15.305 16.134 16.8160

EBIT (O perating Income) 0.349 1.643 2.453 4.409 6.275 11.370 18.270 34.494 54.634 48.323 45.393 45.7024

O ther Income (Expense)

Non-Operating Interest Inc. 0.064 0.183 0.394 0.647 0.653 0.407 0.311 0.519 1.088 1.616 2.05471 2.910569

Other Income (Expense) -0.004 -0.018 -0.029 -0.049 -0.033 -0.044 -0.033 0.054 -0.566 0.352 0.45 0.25

Interest Expense 0.003 0 0 0 0 0 0 0 0 0.136 0.3070$ 0.3070$

Unusual Expense (Income) 0.023 0 0 0 0 -0.333 0.008 0.862 -0.607

EBT/Pretax Income 0.383 1.808 2.818 5.007 6.895 12.066 18.540 34.205 55.763 50.155 47.590 48.5560

Income Taxes 0.107 0.480 0.829 1.512 2.061 3.831 4.527 8.283 14.030 13.118 12.46356 12.73507

EAT/ Net Income 0.276 1.328 1.989 3.495 4.834 8.235 14.013 25.922 41.733 37.037 35.127 35.8209

25

The market share average in the table above is from 2004-2013 but it was much lower than the last three years

so we used the 2013 market share of 21.685% for 2014 and 2015.

Forecasted Depreciation and Amortization- Apple’s 2013 10K contained amortization estimates for 2014 and

2015. We used lagged depreciation on our income statement. For 2004-2013 we calculated depreciation

divided by prior year PPE. Then we found an average from 2010-2013 (23.66%) This average was used to

estimate depreciation for 2014 and 2015.

For example, 2014 depreciation= PPE in 2013 * 23.66%

The estimates for PPE in 2014 and 2015 came from Factset. Basically we just added the consensus estimates for

capital expenditures from the “All Estimates” page to the actual PPE from previous years.

For example, PPE 2014= Capital Expenditures 2014 + 2013 PPE

Research and Development for 2014 and 2015 were calculated as a percentage of sales.

For example, Research and Development 2014= (Average R&D % of Sales 2010-2013) * Forecasted Sales

2014.

Other SG&A Expense for 2014 and 2015 were also calculated as a percentage of sales.

R e v e nue

( in m illio ns ) 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13 2 0 14 2 0 15

Go o gle as o f 09/xxxx 2670 5251 9319 14973 20921 22361 27369 35718 47339 56053 64419 74605

Inte l as o f 09/xxxx 33352 38223 35889 37316 40072 32784 42735 51569 53751 52351 53120 53909

Micro s o ft as o f 09/xxxx 37809 40340 45352 53905 61615 55243 65349 71260 72302 80191 85861 91825

Sams ung as o f 12/xxxx 71576.2 78722.6 89479.8 106019.3 110167.8 106,818.4 133724.1 148937.7 178499.3 208897 223413 232245

HP as o f 10/xxxx 79905 86696 91658 104286 118364 114077 125682 127854 119934 112250 111239.8 110583.3

IBM as o f 09/xxxx 94745 94168 89593 96178 105489 95535 98082 106448 104689 101356 97690 98352

Blackberry as o f 08/xxxx 944 1715 2393 4220 8375 13194 16801 20289 14954 10048 4143 3847

Apple as o f 09/xxxx 8279 13931 19315 24006 32479 42603 65067 108598 155971 170866 176176.52 183625.42

Indus try To ta l

Inc l. Apple (until 2013) 324986.93 357260 380309.5 436768.43 496445.68 483452.75 568082.68 665538 738246 787944 636257 663158

Indus try to ta l Inc l. Apple 812433 846784

Sams ung Sept. LTM 67282.925 76936 86790.5 101884.43 109130.68 107655.75 126997.68 143802 169306 204829 219784 230037

2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13 2 0 14 2 0 15

Indus try R e v e nue (billio ns ) 324986.925 357260 380309.5 436768.43 496445.7 483452.75 568082.675 665538 738246 787944 636256.8 663158.3

A pple 's M a rke t S ha re 0.025474871 0.038994 0.050788 0.0549628 0.065423 0.08812237 0.11453791 0.1631733 0.211272 0.21685 0.21685 0.21685044

M a rke t S ha re A v e ra g e 10.296%

26

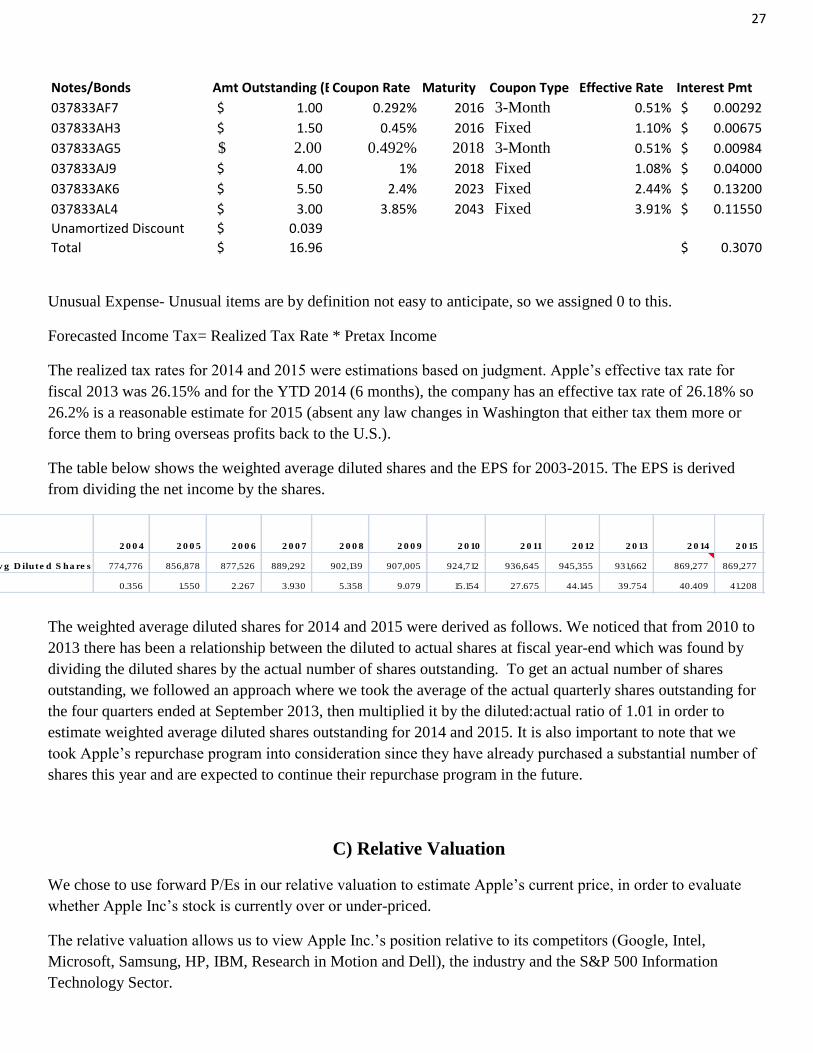

Non-Operating Interest Income- Interest Rate Yield * (ST Investment + LT Marketable Securities)

Forecasted Interest Rate Yield- this was based on judgment. For example, for 2014 we used a yield of 1.4%

because interest rates are at an all time low and they can only go up so since the yield in 2012 = 1.334% and

2013= 1.333%, I predicted 1.4%.

To calculate forecasted ST investment we used a 2010-2013 growth rate to forecast 2014 and 2015.

To calculate forecasted LT marketable securities we used a 2011-2013 growth rate to forecast 2014 and 2015.

Other income expense - 2014 was difficult to estimate because the actual numbers in the previous years

fluctuated a lot. An average was not helpful (it actually resulted in negative numbers. The LTM March

preliminary number is .67 so I believe that the September 2014 number will also be positive. As a result, we

estimated 0.45. For 2015, we just used judgment to estimate 0.25.

Interest Expense- This was based on notes and bonds that Apple Inc. issued. We found interest payment on each

individual note/bond as:

Interest Payment= Coupon Rate * Amount Outstanding.

All of the interest payments were summed to get a total of $0.3070 billion which is forecasted interest expense

for 2014 and 2015.

2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13

A v e ra g e

/

Gro wth

R a te

2 0 14 2 0 15

R &D a s a % o f S a le s 5.907% 3.840% 3.686% 3.258% 3.415% 3.129% 2.739% 2.237% 2.168% 2.619% 2.441% 4.300 4.4814

Othe r S G&A a s a % o f S a le s 17.164% 13.380% 12.596% 12.343% 11.580% 9.739% 8.479% 6.997% 6.437% 6.338% 6.72% 11.834 12.3345

D e pre c ia t io n a s a % o f P P E 0.00% 9.46% 8.65% 9.86% 11.47% 13.06% 13.28% 13.76% 11.88% 20.34% 15.33% 5.669 7.1905

P P E (Gro s s ) 1.300 1.480 2.080 2.840 3.750 4.670 7.230 11.770 21.890 28.520 36.989 46.9170

D e pre c ia t io n 0.140 0.180 0.280 0.430 0.610 0.960 1.620 2.600 5.800 6.749 8.7532

A m o rt iza t io n 0.192 0.605 0.96 1.05 0.985

To ta l C OGS Exc l. D &A a s

a % o f S a le s 70.90% 69.70% 69.85% 64.71% 64.23% 58.72% 59.13% 57.33% 54.27% 58.81% 60.65% 106.8511 111.3688

To ta l S G&A Expe ns e a s

a % o f R e v e nue 23.07% 17.22% 16.28% 15.60% 14.99% 12.87% 11.22% 9.23% 8.60% 8.96% 13.80%

R e a lize d Ta x R a te s 27.94% 26.55% 29.42% 30.20% 29.89% 31.75% 24.42% 24.22% 25.16% 26.15% 26.189% 26.228%

D e pre c ia t io n/ P rio r Ye a r P P E 10.77% 12.16% 13.46% 15.14% 16.27% 20.56% 22.41% 22.09% 26.50% 23.66% 6.74905 8.753177

2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13

Gro wth

R a te 2 0 14 2 0 15

Cas h & ST Inves tments 4.57 5.46 8.26 10.11 15.39 24.49 23.46 25.62 25.95 29.13 40.55 0.1654 47.2565 55.072148

Lo ng Term Marketable Securities 0 0 0 0 0 0 10.528 25.391 55.618 92.122 106.215 0.38193 146.781 202.84128

Interes t Inco me 0.064 0.183 0.394 0.647 0.653 0.407 0.311 0.519 1.088 1.616 2.05471 2.9105687

Interes t Yie ld 1.400% 3.352% 4.770% 6.400% 4.243% 1.662% 0.915% 1.017% 1.334% 1.333%

27

Notes/Bonds Amt Outstanding (BillionsCoupon Rate Maturity Coupon Type Effective Rate Interest Pmt

037833AF7 1.00$ 0.292% 2016 3-Month 0.51% 0.00292$

037833AH3 1.50$ 0.45% 2016 Fixed 1.10% 0.00675$

037833AG5 2.00$ 0.492% 2018 3-Month 0.51% 0.00984$

037833AJ9 4.00$ 1% 2018 Fixed 1.08% 0.04000$

037833AK6 5.50$ 2.4% 2023 Fixed 2.44% 0.13200$

037833AL4 3.00$ 3.85% 2043 Fixed 3.91% 0.11550$

Unamortized Discount 0.039$

Total 16.96$ 0.3070$

Unusual Expense- Unusual items are by definition not easy to anticipate, so we assigned 0 to this.

Forecasted Income Tax= Realized Tax Rate * Pretax Income

The realized tax rates for 2014 and 2015 were estimations based on judgment. Apple’s effective tax rate for

fiscal 2013 was 26.15% and for the YTD 2014 (6 months), the company has an effective tax rate of 26.18% so

26.2% is a reasonable estimate for 2015 (absent any law changes in Washington that either tax them more or

force them to bring overseas profits back to the U.S.).

The table below shows the weighted average diluted shares and the EPS for 2003-2015. The EPS is derived

from dividing the net income by the shares.

The weighted average diluted shares for 2014 and 2015 were derived as follows. We noticed that from 2010 to

2013 there has been a relationship between the diluted to actual shares at fiscal year-end which was found by

dividing the diluted shares by the actual number of shares outstanding. To get an actual number of shares

outstanding, we followed an approach where we took the average of the actual quarterly shares outstanding for

the four quarters ended at September 2013, then multiplied it by the diluted:actual ratio of 1.01 in order to

estimate weighted average diluted shares outstanding for 2014 and 2015. It is also important to note that we

took Apple’s repurchase program into consideration since they have already purchased a substantial number of

shares this year and are expected to continue their repurchase program in the future.

C) Relative Valuation

We chose to use forward P/Es in our relative valuation to estimate Apple’s current price, in order to evaluate

whether Apple Inc’s stock is currently over or under-priced.

The relative valuation allows us to view Apple Inc.’s position relative to its competitors (Google, Intel,

Microsoft, Samsung, HP, IBM, Research in Motion and Dell), the industry and the S&P 500 Information

Technology Sector.

2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13 2 0 14 2 0 15

Wg t A v g D ilute d S ha re s 774,776 856,878 877,526 889,292 902,139 907,005 924,712 936,645 945,355 931,662 869,277 869,277

EP S 0.356 1.550 2.267 3.930 5.358 9.079 15.154 27.675 44.145 39.754 40.409 41.208

28

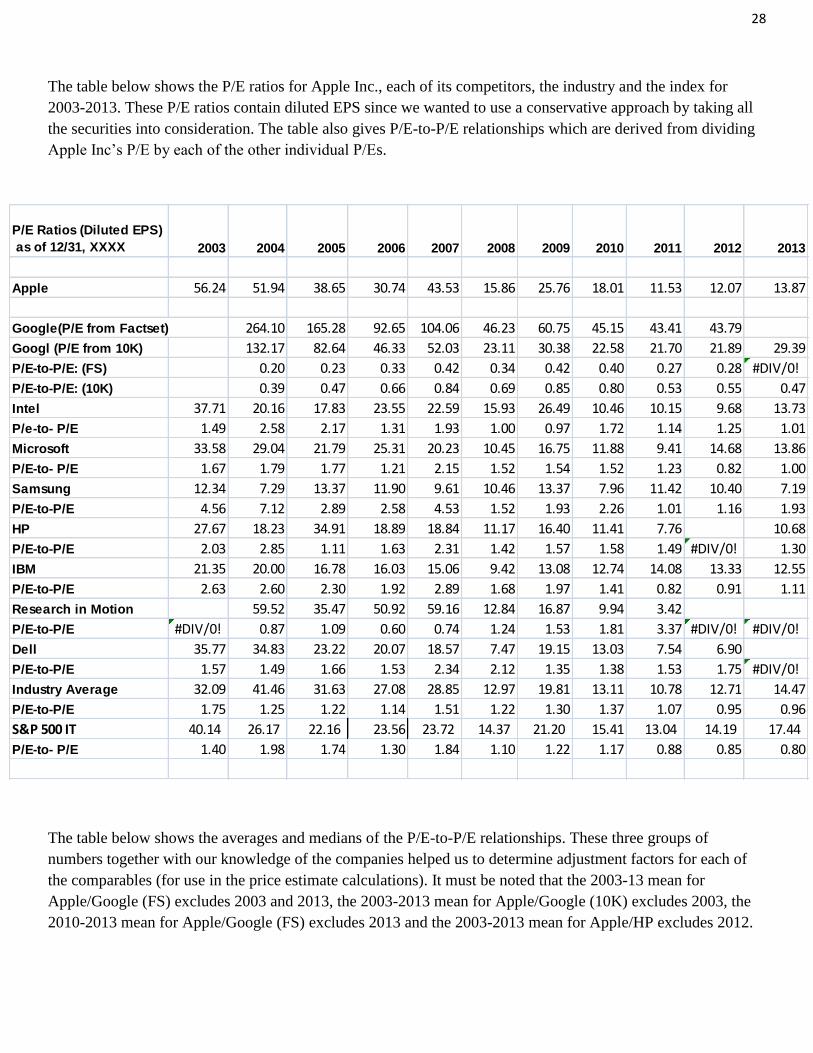

The table below shows the P/E ratios for Apple Inc., each of its competitors, the industry and the index for

2003-2013. These P/E ratios contain diluted EPS since we wanted to use a conservative approach by taking all

the securities into consideration. The table also gives P/E-to-P/E relationships which are derived from dividing

Apple Inc’s P/E by each of the other individual P/Es.

The table below shows the averages and medians of the P/E-to-P/E relationships. These three groups of

numbers together with our knowledge of the companies helped us to determine adjustment factors for each of

the comparables (for use in the price estimate calculations). It must be noted that the 2003-13 mean for

Apple/Google (FS) excludes 2003 and 2013, the 2003-2013 mean for Apple/Google (10K) excludes 2003, the

2010-2013 mean for Apple/Google (FS) excludes 2013 and the 2003-2013 mean for Apple/HP excludes 2012.

P/E Ratios (Diluted EPS)

as of 12/31, XXXX 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Apple 56.24 51.94 38.65 30.74 43.53 15.86 25.76 18.01 11.53 12.07 13.87

Google(P/E from Factset) 264.10 165.28 92.65 104.06 46.23 60.75 45.15 43.41 43.79

Googl (P/E from 10K) 132.17 82.64 46.33 52.03 23.11 30.38 22.58 21.70 21.89 29.39

P/E-to-P/E: (FS) 0.20 0.23 0.33 0.42 0.34 0.42 0.40 0.27 0.28 #DIV/0!

P/E-to-P/E: (10K) 0.39 0.47 0.66 0.84 0.69 0.85 0.80 0.53 0.55 0.47

Intel 37.71 20.16 17.83 23.55 22.59 15.93 26.49 10.46 10.15 9.68 13.73

P/e-to- P/E 1.49 2.58 2.17 1.31 1.93 1.00 0.97 1.72 1.14 1.25 1.01

Microsoft 33.58 29.04 21.79 25.31 20.23 10.45 16.75 11.88 9.41 14.68 13.86

P/E-to- P/E 1.67 1.79 1.77 1.21 2.15 1.52 1.54 1.52 1.23 0.82 1.00

Samsung 12.34 7.29 13.37 11.90 9.61 10.46 13.37 7.96 11.42 10.40 7.19

P/E-to-P/E 4.56 7.12 2.89 2.58 4.53 1.52 1.93 2.26 1.01 1.16 1.93

HP 27.67 18.23 34.91 18.89 18.84 11.17 16.40 11.41 7.76 10.68

P/E-to-P/E 2.03 2.85 1.11 1.63 2.31 1.42 1.57 1.58 1.49 #DIV/0! 1.30

IBM 21.35 20.00 16.78 16.03 15.06 9.42 13.08 12.74 14.08 13.33 12.55

P/E-to-P/E 2.63 2.60 2.30 1.92 2.89 1.68 1.97 1.41 0.82 0.91 1.11

Research in Motion 59.52 35.47 50.92 59.16 12.84 16.87 9.94 3.42

P/E-to-P/E #DIV/0! 0.87 1.09 0.60 0.74 1.24 1.53 1.81 3.37 #DIV/0! #DIV/0!

Dell 35.77 34.83 23.22 20.07 18.57 7.47 19.15 13.03 7.54 6.90

P/E-to-P/E 1.57 1.49 1.66 1.53 2.34 2.12 1.35 1.38 1.53 1.75 #DIV/0!

Industry Average 32.09 41.46 31.63 27.08 28.85 12.97 19.81 13.11 10.78 12.71 14.47

P/E-to-P/E 1.75 1.25 1.22 1.14 1.51 1.22 1.30 1.37 1.07 0.95 0.96

S&P 500 IT 40.14 26.17 22.16 23.56 23.72 14.37 21.20 15.41 13.04 14.19 17.44

P/E-to- P/E 1.40 1.98 1.74 1.30 1.84 1.10 1.22 1.17 0.88 0.85 0.80

29

The table below shows the adjustment factors for Apple Inc. relative to each competitor, the industry and the

index. Dell and Research in Motion are excluded.

Adjustment Factor

Apple relative to Google 0.600

Apple relative to Intel 1.61

Apple relative to Microsoft 0.90

Apple relative to Samsung 1.59

Apple relative to HP 1.454

Apple relative to IBM 1.200

Apple relative to RIMM 3.5

Apple relative to S&P 500 IT 0.925

Next we collected the 2015 forward P/Es for each competitor as of 5/5/14, mapped to September 2015 since this

is Apple Inc’s fiscal year end.

Forward P/E to

map Apple's Sept

2015 Fiscal year

5/5/14

Google 17.71$

Intel 13.21$

Microsoft 13.35$

Samsung 6.76$

HP 8.51

IBM 9.88$

Research in Motion

Dell

S&P 500 Information Technology (Sector) 13.67$

P/E Ratios (Diluted EPS) as of 12/31, XXXX

Arithmetic Average

2003-2013

Arithmetic Average

2010-13 Median

P/E: Apple/Google (FS) 0.321 0.313 0.332

P/E: Apple/Google (10K) 0.625 0.588 0.664

P/E: Apple/Intel 1.505 1.279 1.305

P/E: Apple/Microsoft 1.475 1.141 1.518

P/E: Apple/Samsung 2.863 1.590 2.263

P/E: Apple/HP 1.728 1.454 1.575

P/E: Apple/IBM 1.840 1.061 1.918

P/E: Apple/RIM 1.406 1.296 1.162

P/E: Apple/Dell 1.673 1.165 1.552

P/E: Apple/Industry Avg 1.250 1.088 1.223

P/E: Apple/Index 1.299 0.925 1.215

30

The Estimated EPS that was used in the price calculation was derived from the Income Statement. The E[EPS]

for Apple Inc. for 2015 is 41.21

The price estimates for Apple Inc. relative to each competitor was derived as follows.

Apple’s Price Estimate= Apple’s E[EPS] 2015 * Competitor Forward P/E Sept 2015 * Adjustment Factor

The table below shows Apple Inc’s price estimates relative to each competitor. The prices are then averaged to

give an estimate of Apple Inc.’s current price.

Price Estimate

Apple relative to Google 437.84$

Apple relative to Intel 876.13$

Apple relative to Microsoft 495.14$

Apple relative to Samsung 442.74$

Apple relative to HP 510.03$

Apple relative to IBM 488.71$

Apple relative to RIMM

Apple relative to S&P 500 IT 520.92$

Apple's Current Price 5/5/14 538.79$

However, Apple’s actual current price on 5/5/14 was $600.96. Therefore, Apple Inc.’s stock is overpriced.

D) Absolute Valuation

Absolute valuation is used to determine a company’s financial worth by finding the intrinsic value of the

company. Because Apple issues dividends, the Dividend Discount Model (DDM) will be calculated to find

future dividend payouts and be brought back to present value, to find the intrinsic value. Once we find the

intrinsic value, we will be able to analyze Apple by comparing it to today’s stock price.

Cost of Capital (k)

10-year 30-year

STRIP rates 2.859 3.681

Figure 1

To find the cost of capital, we first extracted data from Bloomberg, as you can see in figure 1. For the risk-free

rate, we used the 10-year and 30-year STRIP rates of 2.859% and 3.681%, respectively. We set the as of date to

be April 30, 2014.

31

5-year 10-year

Adjusted

BETA

0.952 1.179

Figure 2

If you look at figure 2, for the Beta, we decided to use 1.1 because we are taking a conservative approach. This

number is clearly closer to the 10-year adjusted beta than the 5- year. The reason why we decided in being

conservative is because it is expected that in the near future Apple will have much more competition in the

tablet and smartphone markets, which are their highest revenue earners.

Market Risk Premium 8.400%

Using Bloomberg market

return of 9.896% and

10-Year STRIP rate

7.037%

Using Bloomberg market

return of 9.896% and

30-year STRIP rate

6.215%

Market Return (Bloomberg) 9.896%

Figure 3

We used two different approaches to find the market risk premium for four different k calculations. The first

method, we used the arithmetic average of historical average we got in class of 8.4%,, to calculate the first two

set of k’s. For the second method, we used the formula, (E[rmkt] - rf), where E[rmkt] is the expected market return

and rf is the risk-free rate. Finally, the market return was pulled from Bloomberg and set the end date as April

30, 2014.

k1 12.099%

k2 12.921%

k3 10.600%

k4 10.518%

Figure 4

In finding the four k calculations, we used the Capital Asset Price Model (CAPM). For k1 and k2, we used the

10-year and 30-year STRIP rates, respectively, and first method for the market risk premium in solving the cost

of capital. For k3 and k4, we used the 10-year and 30-year STRIP rates, respectively, and the second method for

the market risk premium in solving the cost of capital. We decided to proceed with k1, 12.099%, and k2,

12.921%, to use for our dividend discount model and intrinsic value.

32

Dividend Discount Model (DDM)

From FactSet we were able to extract the diluted earnings per share (EPS) and dividends per share (DPS). The

reason why we only pulled data starting from 2012 was because Apple had recently issued dividends from the

fourth quarter of 2012. This is why the dividends per share for 2012, 2.65, is a lot lower than 2013, 11.40. The

dividend payout ratio was calculated by dividing the earnings per share by the dividends per share. This ratio

shows us how much of the earnings were paid to the shareholders in dividends.

For 2014, only two quarters have passed. The earnings per share were taken as an estimate from FactSet. For

the dividends per share, we multiplied the quarter dividend payouts, 3.05, by two. Apple stated that dividends

would increase to 3.29 starting from the third quarter onward. So we multiplied the new dividend, 3,29, by two,

again. We added both totals to get the dividends per share total for 2014.

2012 2013 2014 2015

EPS (diluted) 44.15 39.75 43.81 41.21

DPS 2.65 11.40 12.68 12.78

Dividend Payout Ratio 24.01% 28.68% 28.94% 31.00%

Figure 5

For 2015, we found the earnings per share from the income statement we had formulated, previously. We

estimated the dividend payout ratio, 31%, from looking at the previous dividend payout ratios and realized that

Apple has a history of increasing its annual dividends per share. The dividends per share was calculated by

multiplying earnings per share by our expected dividend payout ratio, 41.21 * 31% = 12.78.

The short history of paying dividends made it problematic for us to analyze the dividend growth rate for Apple.

Because of this we decided to assume that dividends were issued for the full year 2012. The adjusted dividends

per share total came out to 10.60 and the dividend payout ratio went up to 24.01%.

Growth

Rate

Average

DPS 6.42%

Dividend Payout

Ratio

9.80% 27.21%

Figure 6

The average annual growth rates for dividends per share came out to a total of 6.42% from year 2012 to 2015.

And the growth rate for dividend payout ratio was 9.80%, while the average was 27.21% from year 2012 to

2014.

33

2015 2016 2017 2018 2019 2020

E[DPS] $12.78 $13.60 $14.47 $15.40 $16.38 $17.44

Annual Growth

Rate

0.75% 6.42% 6.42% 6.42% 6.42% 6.42%

Figure 7

We took the recent historical growth rate of 6.42% and extended dividends per share from $12.78 in 2015,

estimate with a payout ratio and our EPS forecast, up to 2020. The growth rate was assumed that it would stay

constant yearly because we did not want to over or under evaluate the future growth rates. Dividends per share

will slowly rise yearly, just in case earnings per share drops. If dividends per share dropped, too, shareholders

will be suspicious about the firm. For obvious reasons, we are not able to measure year-to-year growth rates, so

we decided to be on the conservative side and keep the growth rate constant.

We then brought the expected dividends per share for each year back to present value, 2014. To get the present

value for the expected dividends we used k1, 12.099%. After each year was brought to present value, we

summed up the present values to get a total of $72.96. This total will be then calculated into the intrinsic value.

2014 2015 2016 2017 2018 2019 2020 Total

E[DPS] $12.68 $12.78 $13.60 $14.47 $15.40 $16.38 $17.44

PV ($12.68) ($11.40) ($10.82) ($10.27) ($9.75) ($9.26) ($8.79) ($72.96)

Figure 8

Terminal Value

To get the terminal value for Apple, we made two sensitivity analysis charts using different growth rates

between 1 to 9 percent and k1 and k2. For the first chart we used k1 and the second chart we used k2.

g

E(DPS2021)/

(k1-g) PV k1 IV k1

1.00% 158.6716127 ($79.96) ($152.92)

2.00% 176.1097956 ($88.75) ($161.71)

3.00% 197.3809674 ($99.47) ($172.43)

4.00% 223.9049288 ($112.84) ($185.80)

34

5.00% 257.9014812 ($129.97) ($202.93)

6.00% 303.0462717 ($152.72) ($225.68)

7.00% 365.8983737 ($184.40) ($257.35)

8.00% 459.4175174 ($231.52) ($304.48)

10.25% 1039.688884 ($523.95) ($596.91)

Figure 9

To get the intrinsic value, we first had to find the expected dividends per share for 2021 and divide that by (k1-

g). We then brought it back to present value at year 2014 and then added it to the total sum of the present value

of the dividends per share from years 2014 to 2020. If you see on the bottom line, the highlighted row, we

pumped in different growth rates so that the intrinsic value was matched to Apple’s stock price on May 05,

2014, which was $600.96. This shows that for Apple to be undervalued or fair valued the actual long-term

growth must exceed the expected long-term growth rate of 10.25%.

Before we start on the second sensitivity analysis chart, we had to bring back the expected dividends per share

from 2014 to 2020 using the k2, 12.921%. The sum of the present values came out to a total of $71.51.

2014 2015 2016 2017 2018 2019 2020 Total

E[DPS] $12.68 $12.78 $13.60 $14.47 $15.40 $16.38 $17.44

PV ($12.68) ($11.31) ($10.66) ($10.05) ($9.47) ($8.92) ($8.41) ($71.51)

Figure 10

g

E(DPS2021)/

(k2-g) PV k2 IV k2

1.00% 147.7305788 ($71.26) ($142.76)

2.00% 162.854393 ($78.55) ($150.06)

3.00% 181.027056 ($87.32) ($158.82)

4.00% 203.2738503 ($98.05) ($169.55)

5.00% 231.1378128 ($111.49) ($182.99)

6.00% 267.05378 ($128.81) ($200.32)

35

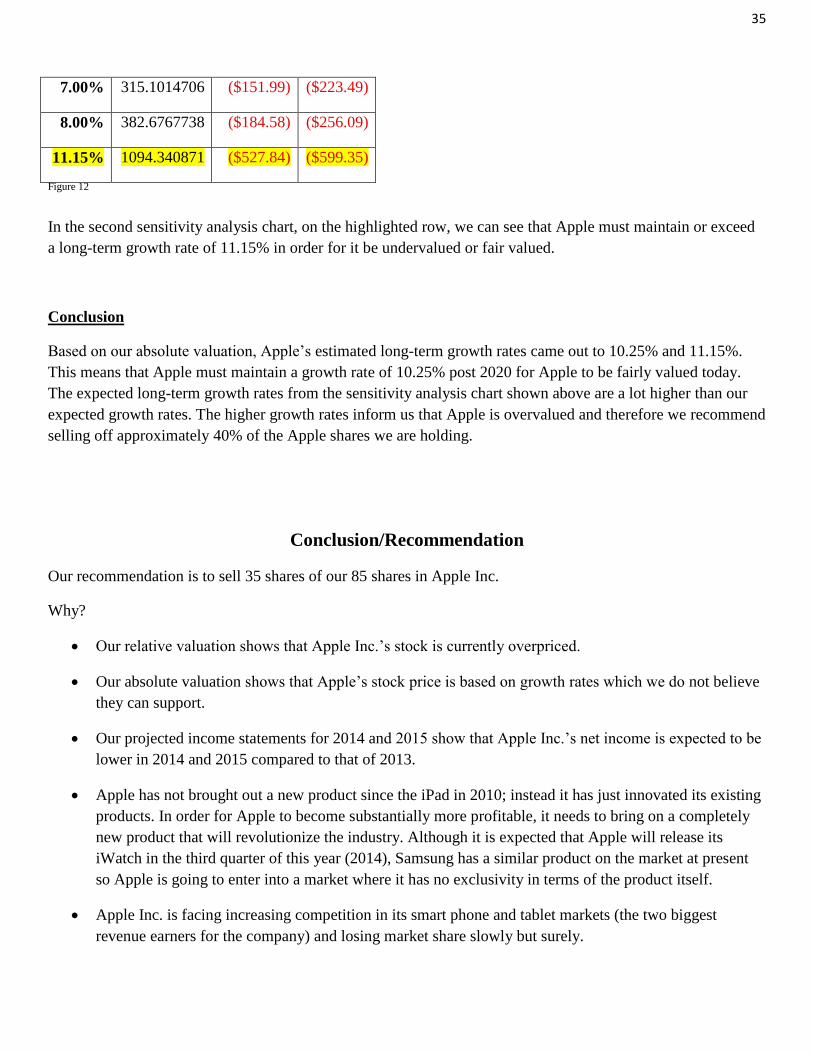

7.00% 315.1014706 ($151.99) ($223.49)

8.00% 382.6767738 ($184.58) ($256.09)

11.15% 1094.340871 ($527.84) ($599.35)

Figure 12

In the second sensitivity analysis chart, on the highlighted row, we can see that Apple must maintain or exceed

a long-term growth rate of 11.15% in order for it be undervalued or fair valued.

Conclusion

Based on our absolute valuation, Apple’s estimated long-term growth rates came out to 10.25% and 11.15%.

This means that Apple must maintain a growth rate of 10.25% post 2020 for Apple to be fairly valued today.

The expected long-term growth rates from the sensitivity analysis chart shown above are a lot higher than our

expected growth rates. The higher growth rates inform us that Apple is overvalued and therefore we recommend

selling off approximately 40% of the Apple shares we are holding.

Conclusion/Recommendation

Our recommendation is to sell 35 shares of our 85 shares in Apple Inc.

Why?

Our relative valuation shows that Apple Inc.’s stock is currently overpriced.

Our absolute valuation shows that Apple’s stock price is based on growth rates which we do not believe

they can support.

Our projected income statements for 2014 and 2015 show that Apple Inc.’s net income is expected to be

lower in 2014 and 2015 compared to that of 2013.

Apple has not brought out a new product since the iPad in 2010; instead it has just innovated its existing

products. In order for Apple to become substantially more profitable, it needs to bring on a completely

new product that will revolutionize the industry. Although it is expected that Apple will release its

iWatch in the third quarter of this year (2014), Samsung has a similar product on the market at present

so Apple is going to enter into a market where it has no exclusivity in terms of the product itself.

Apple Inc. is facing increasing competition in its smart phone and tablet markets (the two biggest

revenue earners for the company) and losing market share slowly but surely.

36

Bibliography

Alpha, Seeking. Every Dividend Income Investor Should Own Apple Now. 27 April 2014. 5 May 2014

<http://seekingalpha.com/article/2167923-every-dividend-income-investor-should-own-apple-now>.

Apple, About. Apple. 4 May 2014 <http://www.about-apple.com/>.

Ciaccia, Chris. Why Did Apple Buy Back $14B of Its Own Stock? 7 February 2014. 4 May 2014

<http://www.thestreet.com/story/12317347/1/why-did-apple-buy-back-14-billion-of-its-own-stock.html>.

Industry, About.Com Retail. Where are the locations of Apple Computer retail stores outside of the U.S.? 4 May 2014

<http://retailindustry.about.com/od/worldslargestretailers/f/Where-Are-The-Locations-Of-Apple-Computer-Retail-

Stores-Outside-Of-The-U-S.htm>.

Info, Apple Press. Apple Expands Capital Return Program to Over $130 Billion. 23 April 2014. 5 May 2014

<https://www.apple.com/pr/library/2014/04/23Apple-Expands-Capital-Return-Program-to-Over-130-Billion.html>.

Insider, Apple. Why Apple, Inc decided to split its stock 7-1. 29 April 2014. 5 May 2014

<http://appleinsider.com/articles/14/04/29/why-apple-inc-decided-to-split-its-stock-7-1->.

Money, CNN. Apple Inc.- Company Description. 4 May 2014

<http://money.cnn.com/quote/profile/profile.html?symb=AAPL>.

—. Fortune 500. 4 May 2014 <http://money.cnn.com/magazines/fortune/fortune500/>.

Nasdaq. Apple Inc. Dividend Date & History. 5 May 2014. 5 May 2014 <http://www.nasdaq.com/symbol/aapl/dividend-

history>.

—. Apple Inc. Stock Chart. 2 May 2014. 5 May 2014 <http://www.nasdaq.com/symbol/aapl/stock-

chart?intraday=off&timeframe=3m&charttype=line&splits=off&earnings=off&movingaverage=None&lowerstudy=volum

e&comparison=off&index=&drilldown=off&sDefault=true>.

Phillips, Matthew. Apple just became the world’s biggest-dividend stock. 24 April 2014. 5 May 2014

<http://qz.com/202630/apple-just-became-the-worlds-biggest-dividend-stock/>.

Ritchie, Rene. Apple A7. April 2014. 5 May 2014 <http://www.imore.com/apple-a7>.

Su, Reissa. Apple Inc Stock Split Decision May Cause Dramatic Fall in Stock Price to Below $100 Theoretically. 29 April

2014. 5 May 2014 <http://au.ibtimes.com/articles/549961/20140429/apple-inc-aapl-stock-buybacks-split.htm#.U2d-

HPldWSo>.

Terrell, Angelique Richardson & Ellen. Apple Computer Inc. April 2008. 4 May 2014

<http://www.loc.gov/rr/business/businesshistory/April/apple.html>.

Time. The Apple Revolution: 10 Key Moments. 4 May 2014

<http://content.time.com/time/specials/packages/article/0,28804,1873486_1873491_1873530,00.html>.

Whitney, Lance. iPhone market share shrinks as Android, Windows Phone grow. 6 January 2014. 7 May 2014

<http://www.cnet.com/news/iphone-market-share-shrinks-as-android-windows-phone-grow/>.

Factset

37

Bloomberg

![arXiv:1908.08984v1 [cs.CV] 12 Aug 2019 · provide correct details. Each E-commerce store has its own product taxonomy and a seller typically sells in multiple stores. This implies](https://static.fdocuments.in/doc/165x107/5eb38f1d32f7d33aa86e9c3d/arxiv190808984v1-cscv-12-aug-2019-provide-correct-details-each-e-commerce.jpg)

![Sh - [∫] [∫] She sells sea shells at the sea shore. The shells she sells are surely sea shells. So if she sells shells on the seashore, I'm sure she sells.](https://static.fdocuments.in/doc/165x107/56649f165503460f94c2b775/sh-she-sells-sea-shells-at-the-sea-shore-the-shells-she-sells.jpg)