Americas financial reviewAmericas financial review

32

1 Americas financial review Americas financial review Darryl Button CFO Americas Analyst and Investor Day, New York City, December 2, 2009

Transcript of Americas financial reviewAmericas financial review

1

Americas financial reviewAmericas financial review

Darryl Button CFO Americas

Analyst and Investor Day, New York City, December 2, 2009

o Adjusted operating expenses down 10%

Key messages

o Reporting structure aligned with management changes

o Earnings impacted by financial crisis – franchises intact and producing

strong underlying earnings growth going forward

o Institutional spread lending in run off – reduced exposure to credit risk over

time

o Adjusted operating expenses down 10%

o US impairment trend improving

o Significant improvement in unrealized bond losses

o Additional capital markets de-risking resulting in higher quality, consistent

earnings going forward

Local knowledge. Global power. 2

o Financial review

Agenda

o Business review

Local knowledge. Global power. 3

Ope

ratin

ea

rnin

g

rotect on ro ucts e nsuranceSavin s and and Asset

P i

P d

R i

Reporting structure - today

Over /

(under)

performance

of fair value

items

Life and Protection

Individual Savings and Retirement

Pension and Asset

Management

Institutional Products

Life Reinsurance

Life Institutional guaranteed

products

Accident and

health

Fixed annuities

Variable annuities

Retail mutual funds

BOLI / COLI U

nd

erlyin

gea

rnin

gs

g s Life and

Individual Savings and

Pension and Asset

Institutional Life

Ope

ratin

gea

rnin

gs Protection

g Retirement Management

Products Reinsurance

Life Institutional guaranteed

products

Accident and

health

Fixed annuities

Variable annuities

Retail mutual funds

BOLI / COLI

o Gains / losses

o Impairment charges

o Other income

o Income tax

o Americas net income

Local knowledge. Global power. 4

U ede

rlyin

g

rnin

gs

Reporting structure – aligned with management changes

Unnde

rlyin

g

ea

a

rnin

gs

US Work Mon AFP SVS Canada EU Life site Japan

LTC TCM DIA Argos Mexico ADMS TAM TRS BOLI

Korea /COLI

Mong WFG TRM Clark Brazil eral

Individual Employer Life and Alternative Life

Savings and Solutions and Protection Markets Reinsurance

Retirement Retirement Pensions Pensions

o Over / (under) performance of fair value items

o Run-off business

o Gains / losses

o Impairment charges

o Other income

o Income tax

o Americas net income

Local knowledge. Global power. 5

Development of underlying earnings before tax per quarter

Pre-crisis Current Post-crisis

<2008 Q3 2009 >2010

USD

700

million

Earnings impacted by

o Run-off institutional

spread-based business

o Equity markets

o De-risking

USD

430*

million

Earnings drivers

o Growth of business

o Cost savings

o Redeployment of cash

o Financial markets

* Excluding exceptional items (USD 30 million)

Local knowledge. Global power. 6

Quarterly run-rate underlying earnings before tax

Pre-Crisis Current

(<2008) Change (Q3 09) (USD million) (USD million) (USD million)

Americas 630 (160) 470

(excluding IGP spread)

IGP spread 70 (110) (40)

Total Americas 700 (270) 430

Excluding IGP spread (160) o (70) lower equity based fees and higher DPAC amortization on variable annuity, mutual fund and pension businesses

o (50) investment de-risking (reduced hedge funds, high yield, BBB and credit derivatives)

o (40) employee pension plan expenses

IGP spread (110) o Spread compression driven by shortening of institutional liabilities during financial crisis

o IGP run-off loss follows maturity pattern of internally transferred assets and amortizes off over next four years

Local knowledge. Global power. 7

Impact of run-off institutional spread-based business

Spread balances (USD billion)

33

24

13 8

3 2

2008 Q3 2009 2010E 2012E 2014E 2016E

o Institutional cash shortfall due to shortening of liabilities

– 12 month notice putable funding agreements (USD 6 billion)

– Municipal GICs (USD 5 billion)

– Extendable MTNs (USD 1 billion)

o Remainder of US businesses cash flow positive through the crisis

Local knowledge. Global power. 8

exchan e for cash

Impact of run-off institutional spread-based business

Pre-Crisis Current (<2008) Change (Q3 09)

(USD million) (USD million) (USD million)

IGP spread per quarter 70 (110) (40)

o USD 10 billion internal asset transfer from institutional to other US portfolios in

exchange for cash g

– Transfer pricing basis – what other portfolios priced for

– Actual book value of USD 11.4 billion

– Unrealized loss before tax of USD (1.4) billion amortized through run-off

institutional earnings:

• 2009 (0.3) billion • 2012 (0.2) billion

• 2010 (0.3) billion • 2013 (0.2) billion

• 2011 (0.3) billion • 2014 (0.1) billion

o Run-off will reduce sensitivity to credit markets going forward and free up USD 0.8

billion of capital by the end of 2010

Local knowledge. Global power. 9

.

0

.

.

Mean reversion – equity return assumptions

7.50%

8.25%

7.50%

8.25%

6 25%

7.25% 7.25%

6.25% 6.00% 5.00% 6.25%

5.75%

4.75% 4.75% 4.75% 4.75%

6.00%

9.00%

10.0 %

15 00% 15.00% 15.00%

11 00%

8.00%

Corridor cap

Corridor floor

Negative DAC unlocking above cap �

Corridor floor

Positive DAC unlocking below floor �

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 '03 '04 '04 '04 '04 '05 '05 '05 '05 '06 '06 '06 '06 '07 '07 '07 '07 '08 '08 '08 '08 '09 '09 '09

o Equity return assumptions adjusted quarterly within the corridor

o Corridor based on current information and management best estimate

o Over last six years, corridor breached once in Q207 (floor) and then in Q308-Q109

(cap)

o Underlying earnings impact is approximately USD 60 million per point change

in equity growth rate assumption

Local knowledge. Global power. 10

Proven ability to execute on cost reduction initiatives

Adjusted operating expenses down 10% year to date

Category 9M 2009 9M 2008 Change

Total operating expenses 1,678 1,640 38

Less: employee pension plan costs (90) 76 (166)

Less: restructuring charges (40) n/a (40)

Adjusted operating expenses 1,548 1,716 (168)

o Restructuring the organization resulted in charges during 2009; however,

the efficiencies gained will result in reduced costs going forward

o We are not done – we will continue to aggressively pursue expense savings

initiatives throughout the organization

Local knowledge. Global power. 11

–

Fair value items

Liabilities

Assets

Macro

Hedge

Local knowledge. Global power.

o GMWB (USD 14 billion) - delta / rho hedged

o Segregated funds (USD 3.4 billion) – 92% delta hedged

o Total return annuities (USD 1.4 billion) – closed blocks

o Hedge funds (USD 0.7 billion) – reduced by 1.7 billion reduced by 1.7 billion o Hedge funds (USD 0.7 billion)

o Private equity (USD 0.7 billion) and REAP (USD 0.7 billion)

o Credit derivatives – super senior program unwound

o Capital protection – 50% of unhedged retail VA

o Total return swap (USD 1.3 billion)

o Put options (USD 0.8 billion)

Balances reflect ending balances as of September 30, 2009 12

Q3 '07 Q4 '07 Q1 '08 Q2 '08 Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09

Improved US impairment losses

Gross impairments (USD million)

US housing (ABS and RMBS)

Corporate Bonds

US commercial mortgages (CMBS and CML) 550 516 491

Other 430 370

131 61

40 36

Q3 '07 Q4 '07 Q1 '08 Q2 '08 Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09

Recoveries (USD million)

49

5

20 18

3 4

38

3

24

Q3 '07 Q4 '07 Q1 '08 Q2 '08 Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09

Local knowledge. Global power. 13

Reduced unrealized bond losses

Revaluation account (USD billion)

Q3 '07 Q4 '07 Q1 '08 Q2 '08 Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09

(5)

(10)

(15)

(20) (20)

Gross Bond Unrealized Gain (Loss) Net Revaluation Reserve

o Significant improvement in recent quarters

o Not a proxy for actual impairments

Local knowledge. Global power. 14

o Business review

Agenda

o Financial review

Local knowledge. Global power. 15

Variable annuities

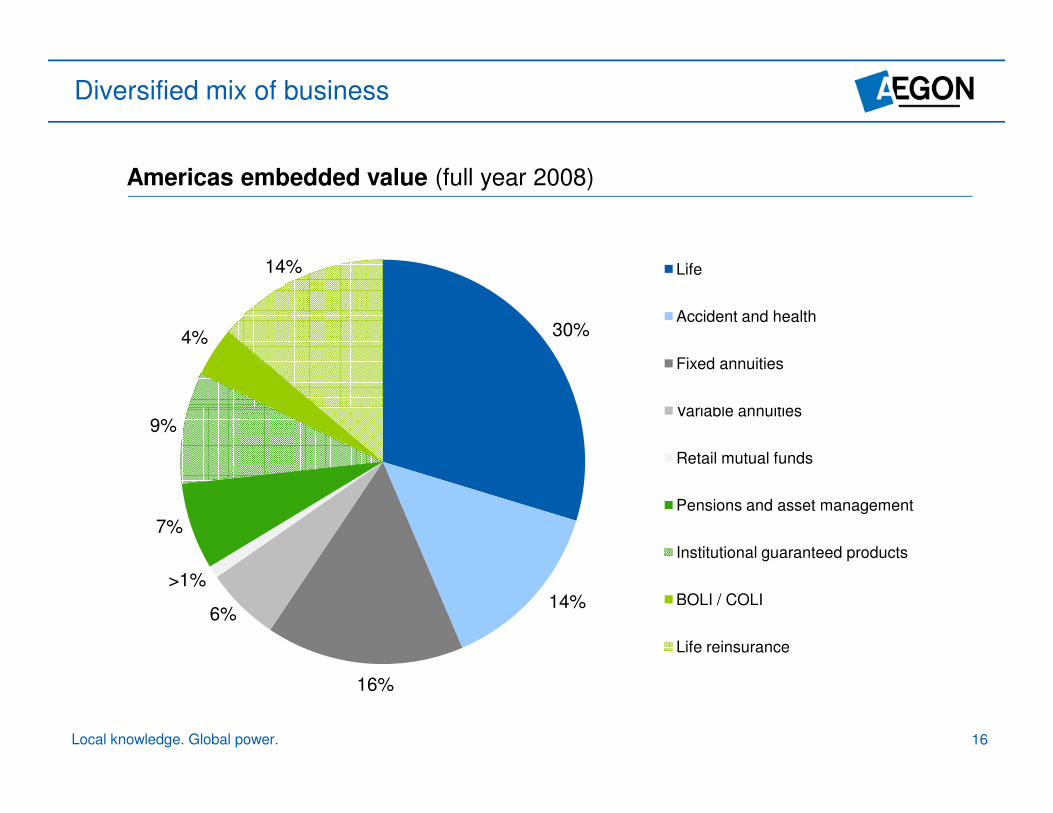

Diversified mix of business

Americas embedded value (full year 2008)

14% Life

Accident and health

4% 30%

Fixed annuities

Variable annuities 9%

Retail mutual funds

Pensions and asset management

7%

Institutional guaranteed products

>1% 14% BOLI / COLI

6%

Life reinsurance

16%

Local knowledge. Global power. 16

o yn e c so Variable life insurance

Diversified product offering

Life and Protection

Individual Savings

and Retirement

Employer Solutions

and Pensions

Alternative Markets

Life Reinsurance

o Traditional life

o Term life

o Universal life

o Equity indexed universal life

o Variable life

o Fixed annuities

o Variable annuities

o Mutual funds

o 401(k) plans

o 403(b) plans

o Defined benefit

o Variable annuities

o Mutual funds

S th ti GIC

o Canadian life and segregated funds

o Latin America life insurance products

o Bank and corporate owned life insurance

o Term coinsurance

o Annuities

o Product consulting and development

o Automated underwriting

Local knowledge. Global power. 17

o Health and supplemental health

o Long term care

o Synthetic GICs

o ome serv ceartners o Worksite ecialists

Diversified distribution

Life and Protection

Individual Savings

and Retirement

Employer Solutions

and Pensions

Alternative Markets

Life Reinsurance

o General agents

o Registered representatives

o Independent marketing organizations

H i

o Banks

o Wirehouses

o Broker/dealers

o Financial planners

o Institutional partners

o Consulting firms

o Broker/dealers

o Banks

o Independent producers

o Worksite specialists

o General agents

o Company representatives

o Consultants

o Company representatives (business to business)

Local knowledge. Global power. 18

o Home service agents

o Direct marketing

p

o Agents

sp

o Employee benefit brokers and benefit consultants

o Third-party administrators

Life and Protection Canada

WFG

ADMS AFP

Mon Life LTC

Work site

Sources of

earnings

Financial

model*

Risk

management

o Investment spreads (30%) o Insurance fee margins (70%)

400

300

200

100

0

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09

Underlying Earnings 2007 Sample Model 10% of Premium 1% of Reserves

o Actuarial experience studies o External reinsurance o Effective ALM strategies o Extensive operational controls and processes

Local knowledge. Global power. *Model based on old reporting structure 19

Individual Savings and Retirement

TRM

TAM TCM

Canada

Sources of

earnings

o Fixed annuities - investment spreads (100%) o Variable annuities

- fees net of hedging (70%) - investment spreads (30%)

o Mutual funds - fees (100%)

Financial

model*

Variable Annuities 150 100 Fixed Annuities

100 50

050

-50 0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 07 07 07 07 08 08 08 08 09 09 09 07 07 07 07 08 08 08 08 09 09 09

Underlying Earnings 2007 Sample Model Underlying Earnings 2007 Sample Model

Risk

management

o ALM matching for fixed annuities o Delta / rho hedging on GMWB o Macro hedge for 50% of previously unhedged business o New product launched Q3 ‘09 � reduced hedge costs, tiered pricing

Local knowledge. Global power. *Model based on old reporting structure 20

TRS

DIA

Employer Solutions and Pensions SVS

Work

site

Clark TIM

Sources of

earnings

Financial

model*

Risk

management

o Separate account and off balance sheet � fees o Purchased annuities and general account � spread o Worksite voluntary � insurance margins

60

50

40

30

20

10

0

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09

Underlying earnings 2007 Sample Model

o ALM matching for general account o Extensive operational controls and processes o Actuarial experience studies for voluntary benefits o Strict investment mandates for synthetic GICs

Local knowledge. Global power. *Model based on old reporting structure 21

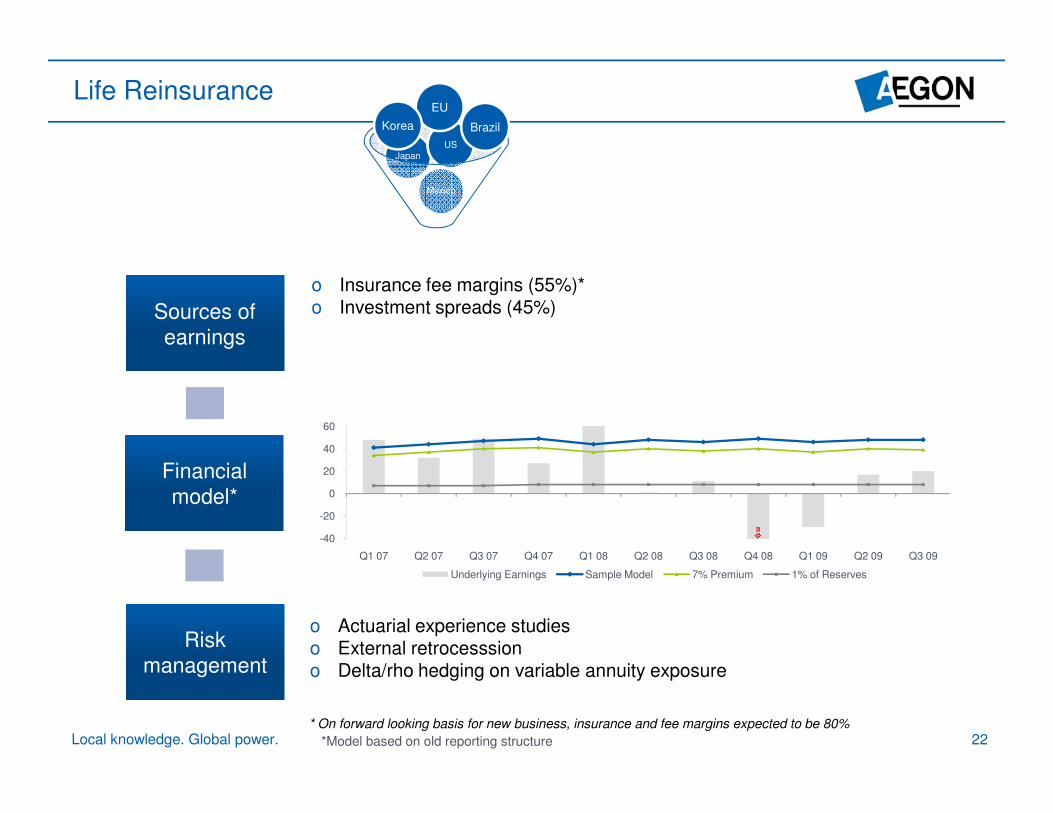

Life Reinsurance

Mexico

Japan

US

Brazil

EU

Korea

Sources of

earnings

o Insurance fee margins (55%)* o Investment spreads (45%)

60

40

20

0

Financial

model* -20

-40

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09

Underlying Earnings Sample Model 7% Premium 1% of Reserves

Risk

management

o Actuarial experience studies o External retrocesssion o Delta/rho hedging on variable annuity exposure

* On forward looking basis for new business, insurance and fee margins expected to be 80%

Local knowledge. Global power. *Model based on old reporting structure 22

• Reduced hedge fund • Floating rate assets

Reduced capital markets risk

Equity Risk

• VA hedging

• Common equity divestment

• Reduced hedge fund investment exposure

Interest Rate Risk

• Effective ALM

• Cash and forward starting swaps

• Floating rate assets added to fixed annuity portfolio

Improved risk / return profile

Credit Risk

• Run-off institutional spread lending

• Asset de-risking to mitigate migration

• Upgraded credit quality in mortgage tranches over last 5 years

Local knowledge. Global power. 23

Conclusion

o Organizational changes to simplify the business and extract synergies

o Strong franchises positioned to win

o Focused on costs to drive competitive advantage

o Reduced exposure to capital markets risk will result in higher quality,

consistent earnings going forward

Local knowledge. Global power. 24

Q&A

Local knowledge. Global power. 25

Appendix

Local knowledge. Global power. 26

Divisional restructuring

Previous Reporting Structure New Reporting Structure

Life and Protection

AEGON Direct Marketing Services No change Life and Protection

Long Term Care No change Life and Protection

Monumental Life No change Life and Protection

World Financial Group No change Life and Protection

AEGON Financial Partners (including TIIG) No change Life and Protection

Transamerica Worksite Marketing Moved to Employer Solutions and Pensions

Transamerica Canada Moved to Alternative Markets

Individual Savings and Retirement

Transamerica Capital Management No change Individual Savings and Retirement

Transamerica Asset Management Transamerica Asset Management No change No change Individual Savings and Retirement Individual Savings and Retirement

Transamerica Retirement Management No change Individual Savings and Retirement

Transamerica Canada Moved to Alternative Markets

Pensions and Asset Management

Transamerica Investment Management Moved to Global Asset Management

Diversified Investment Advisors Moved to Employer Solutions and Pensions

Transamerica Retirement Services Moved to Employer Solutions and Pensions

Transamerica Canada Moved to Alternative Markets

Institutional Markets

Extraordinary Markets Moved to Alternative Markets

Institutional Markets Division spread Moved to Below the line in run-off

Institutional Markets Division Stable Value Solutions (synthetic GICs) Moved to Employer Solutions and Pensions

Clark Consulting Moved to Employer Solutions and Pensions

Life Reinsurance

Transamerica Reinsurance No change Life Reinsurance

Local knowledge. Global power. 27

variable life

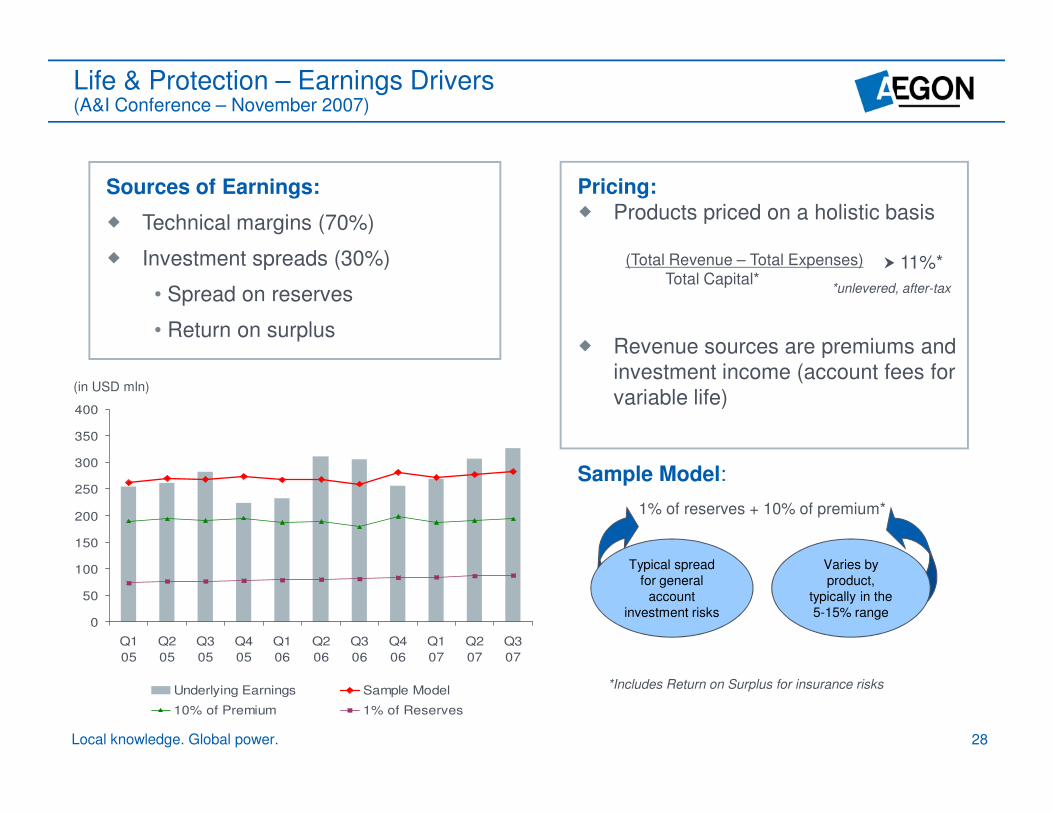

Life & Protection – Earnings Drivers (A&I Conference – November 2007)

Sources of Earnings: Pricing:

� Products priced on a holistic basis � Technical margins (70%)

� Investment spreads (30%) (Total Revenue – Total Expenses) � 11%* Total Capital*

*unlevered, after-tax • Spread on reserves

• Return on surplus � Revenue sources are premiums and

investment income (account fees for

variable life) (in USD mln)

400

Local knowledge. Global power. 28

0

50

100

150

200

250

300

350

400

Q1

05

Q2

05

Q3

05

Q4

05

Q1

06

Q2

06

Q3

06

Q4

06

Q1

07

Q2

07

Q3

07

Underlying Earnings Sample Model

10% of Premium 1% of Reserves

)

Sample Model:

1% of reserves + 10% of premium*

*Includes Return on Surplus for insurance risks

Typical spread

for general

account

investment risks

Varies by

product,

typically in the

5-15% range

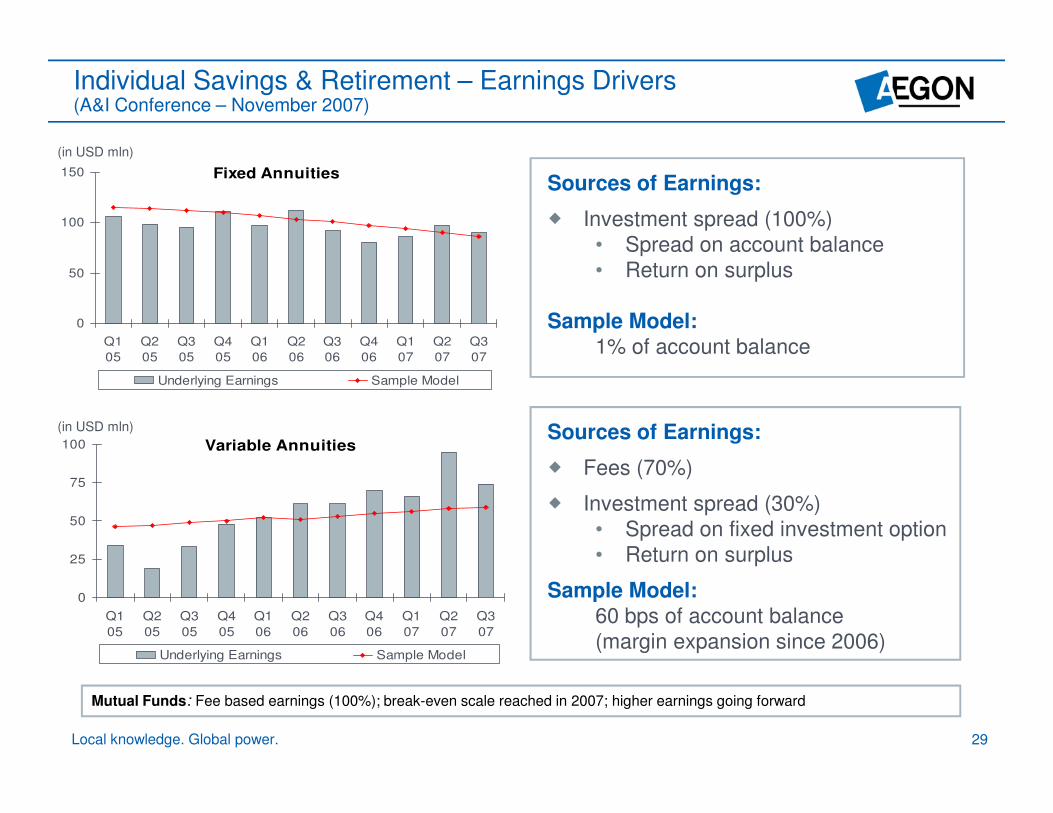

Individual Savings & Retirement – Earnings Drivers (A&I Conference – November 2007)

(in USD mln)

150

100

50

0

100

75

50

25

0

Fixed Annuities Sources of Earnings:

� Investment spread (100%)

• Spread on account balance

• Return on surplus

Sample Model:

1% of account balance Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

05 05 05 05 06 06 06 06 07 07 07

Underlying Earnings Sample Model

(in USD mln)

Variable Annuities

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

05 05 05 05 06 06 06 06 07 07 07

Underlying Earnings Sample Model

Sources of Earnings:

� Fees (70%)

� Investment spread (30%)

• Spread on fixed investment option

• Return on surplus

Sample Model:

60 bps of account balance

(margin expansion since 2006)

Mutual Funds: Fee based earnings (100%); break-even scale reached in 2007; higher earnings going forward

Local knowledge. Global power. 29

Pension & Asset Management – Earnings Drivers (A&I Conference – November 2007)

60

50

40

30

20

10

0

Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

Underlying earnings Sample Model Local knowledge. Global power.

Sources of Earnings:

� Fees (40%)

� Investment spread (60%)

• Spread on account balance

• Return on surplus

Margins vary

significantly by

product based on

capital allocation –

range from 10 to 100

bps

10 bps => large case off balance sheet 401(k)

service contract

100 bps => purchased annuities and general

account fixed option of retirement plans

Sample earnings model:

25 bps of account balance

30

n m ninvestment income and account

Life Reinsurance – Earnings Drivers (A&I Conference – November 2007)

� Products priced on a holistic basis Sources of Earnings: Pricing:

� Technical Margins (45%) to return minimum return on capital

� Investment Spreads (45%) (Total Revenue – Total Expenses)

• Spread on reserves � 11%* Total Capital*

*unlevered, after-tax • Return on surplus

� Fees (10%) � Revenue sources are premiums,

investment income, and account (i USD l )

Local knowledge. Global power. 31

0

20

40

60

Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

Underlying Earnings Sample Model

7% Premium 1% of Reserves

,

fees

Sample earnings model:

1% of reserves + 7% of premium*

Typical spread

for general

account

investment risks

Varies by

product,

typically in the

5-15% range

*Includes Return on Surplus for insurance risks

(in USD mln)

Disclaimer

Forward-looking statements

The statements contained in this presentation that are not historical facts are forward-looking statements as defined in the US Private Securities Litigation Reform

Act of 1995. The following are words that identify such forward-looking statements: aim, believe, estimate, target, intend, may, expect, anticipate, predict, project,

counting on, plan, continue, want, forecast, goal, should, would, is confident, will, and similar expressions as they relate to our company. These statements are

not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. We undertake no obligation to publicly update

or revise any forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which merely reflect company

expectations at the time of writing. Actual results may differ materially from expectations conveyed in forward-looking statements due to changes caused by

various risks and uncertainties. Such risks and uncertainties include but are not limited to the following:

o Changes in general economic conditions, particularly in the United States, the Netherlands and the United Kingdom;

o Changes in the performance of financial markets, including emerging markets, such as with regard to:

- The frequency and severity of defaults by issuers in our fixed income investment portfolios; and

- The effects of corporate bankruptcies and/or accounting restatements on the financial markets and the resulting decline in the value of equity and

debt securities we hold;

o The frequency and severity of insured loss events;

o Changes affecting mortality, morbidity and other factors that may impact the profitability of our insurance products;

o Changes affecting interest rate levels and continuing low or rapidly changing interest rate levels; interest rate levels and continuing low or rapidly changing interest rate levels; o Changes affecting

o Changes affecting currency exchange rates, in particular the EUR/USD and EUR/GBP exchange rates;

o Increasing levels of competition in the United States, the Netherlands, the United Kingdom and emerging markets;

o Changes in laws and regulations, particularly those affecting our operations, the products we sell, and the attractiveness of certain products to our consumers;

o Regulatory changes relating to the insurance industry in the jurisdictions in which we operate;

o Acts of God, acts of terrorism, acts of war and pandemics;

o Effects of deliberations of the European Commission regarding the aid we received from the Dutch State in December 2008;

o Changes in the policies of central banks and/or governments;

o Litigation or regulatory action that could require us to pay significant damages or change the way we do business;

o Customer responsiveness to both new products and distribution channels;

o Competitive, legal, regulatory, or tax changes that affect the distribution cost of or demand for our products;

o Our failure to achieve anticipated levels of earnings or operational efficiencies as well as other cost saving initiatives; and

o The impact our adoption of the International Financial Reporting Standards may have on our reported financial results and financial condition.

Further details of potential risks and uncertainties affecting the company are described in the company’s filings with Euronext Amsterdam and the US Securities

and Exchange Commission, including the Annual Report on Form 20-F. These forward-looking statements speak only as of the date of this document. Except as

required by any applicable law or regulation, the company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any

forward-looking statements contained herein to reflect any change in the company’s expectations with regard thereto or any change in events, conditions or

circumstances on which any such statement is based.

Local knowledge. Global power. 32