Alternative Sources of Finance - ICAEW.com

35

BUSINESS WITH CONFIDENCE icaew.com Alternative Sources of Finance Making it big in business Clive Lewis, Head of Enterprise [email protected]

Transcript of Alternative Sources of Finance - ICAEW.com

BUSINESS WITH CONFIDENCE icaew.com

Alternative Sources of Finance

Making it big in business

Clive Lewis, Head of Enterprise

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

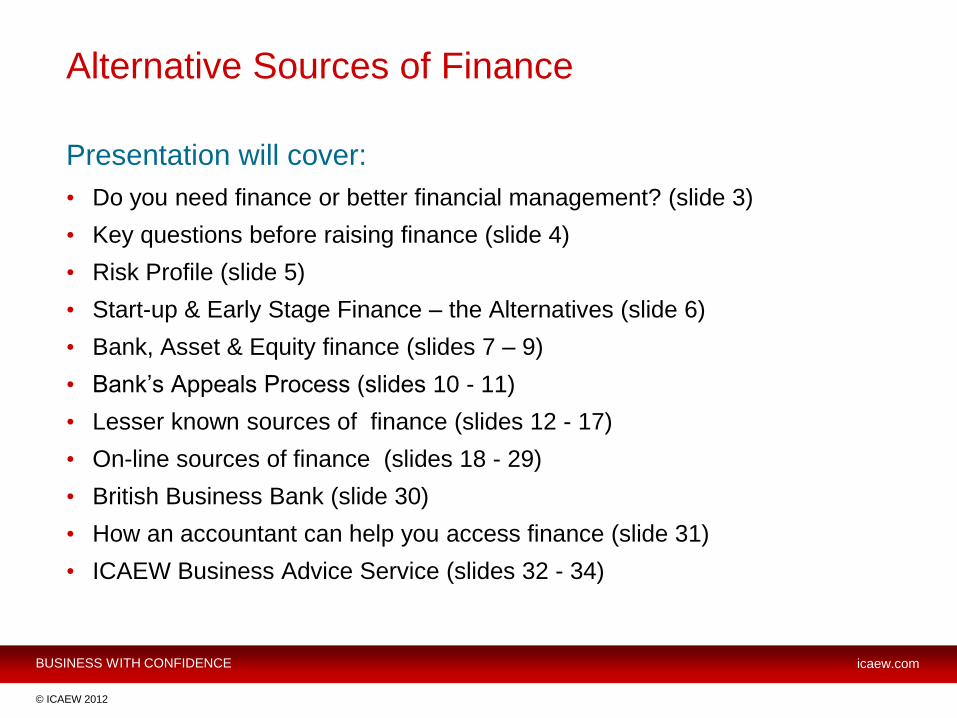

Alternative Sources of Finance

Presentation will cover:

• Do you need finance or better financial management? (slide 3)

• Key questions before raising finance (slide 4)

• Risk Profile (slide 5)

• Start-up & Early Stage Finance – the Alternatives (slide 6)

• Bank, Asset & Equity finance (slides 7 – 9)

• Bank’s Appeals Process (slides 10 - 11)

• Lesser known sources of finance (slides 12 - 17)

• On-line sources of finance (slides 18 - 29)

• British Business Bank (slide 30)

• How an accountant can help you access finance (slide 31)

• ICAEW Business Advice Service (slides 32 - 34)

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Do you need finance or better financial management?

• A business should have a continuous focus on cash flow

• Good practices and clear lines of responsibility are important.

• Have clear credit agreements with customers and suppliers

• Have a system for following up late receipts from customers

• Knowing your current bank balance and how you expect it to

change over next 3 months is vital

• Good financial management not only helps manage cash it will

reassure finance providers

• A growing business can mean increased working capital.

Arrange your finances to meet any increased need.

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting the appropriate finance for your

business

Key questions to consider before seeking finance:

• How much are you looking to raise?

• Are monies needed for short or long term needs?

• Are monies needed for growth or just to sustain your

business?

• Are you prepared to offer security over an asset being

personal or business?

• Are you prepared to bring in an outside investor and give up

either a minority or majority stake?

• How do you plan to repay the finance?

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

The business’ risk profile matters.

• Banks use a variety of information to assess risk

• Behavioural scoring data (how accounts are run, facilities

repaid and evidence of a drop in turnover)

• Credit reference data also referred to (paying suppliers later,

court judgements, late filings at Cos House)

• If the business is a limited company, finance providers will look

behind the company at the directors credit history

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Possible types of Start-up & Early Stage Finance

• Your own personal savings

• Friends and Family

• Credit cards

• Credit Unions

• Grants (usually for specific groups of people or sectors)

• StartUp Loans

• Bank finance – overdraft or loans

• Invoice Factoring and Discounting

• Hire purchase , leasing or hiring

• Small scale equity finance such as Business Angels

• Crowd Funding or Peer-to-Peer Lending

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting the appropriate finance for your business

Bank and Invoice Finance

Loans - Normally secured by a charge over asset(s). Often has

conditions attaching to the loan (“covenants”) which can trigger a

demand for immediate repayment if they are not met.

Overdraft -The lender offers a facility with a limit with an agreed

interest rate and probably secured. The business can dip in and out of

the facility up to the limit.

Debt Factoring – To consider factoring the business needs debtors

with a good credit record. The factoring company pays a percentage of

the debtor book immediately to your business. Factor chases debt

Invoice Discounting allows the business to administer the sales

ledger and the customer is unaware that the debt has been discounted.

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting the appropriate finance for your business

Other Asset Finance

Outright Purchase or Deferred Payment -asset(s) can either be

purchased outright or paid for by instalments. There are various

types of deferred payment - hire, hire purchase or leasing.

Mortgage – normally be used to finance a property acquisition or to

expand an existing business premises. Similar to a bank loan with the

mortgage usually being secured over the premises. Loan to value

ratios vary but unlikely to exceed 70%

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting the appropriate finance for your business

Equity Finance

Self funding, friends and family -Business owner with their own funds or those

of friends and family, inject monies into your business. This can be by way of a

loan or equity finance. Must put agreement in writing

Small Scale Equity Finance - businesses sell a share in the business to friends,

family, business angels or other private investors. They must be prepared to

allow others a say in how the business is run. Business angels bring (up to £2

million) finance to a business and they normally have experience in what makes

a successful business

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting the best from your bank

If refused credit by a bank

• Get a written explanation for the decision

• Consider requesting an appeal – 40% of appeals result in the

decision being overturned frequently because business

provides additional information.

• Bank should offer suggested alternative sources/types of

finance

• Review banks feedback and consider applying to another

bank or source of finance

• Ask is equity finance the way forward?

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting the best from your bank

• All major UK banks have agreed a set of principles if your formal

application for finance has been refused and you appeal the decision

• An independent and external team of reviewers monitor the

principles and the banks application of them

• The appeal is reviewed by a second person from the bank not

involved in the original decision

• The reviewers have 30 days to communicate the result of your

appeal to you.

• 40% of appeals reviewed in the first year resulted in the original

refusal being overturned. In a majority of these cases this followed

additional information being submitted.

• For more information ask your bank or look on the Better Business

Finance Website – www.betterbusinessfinance.co.uk

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Own Personal Savings & Friends & Family

• Business owner with their own funds or those of friends and

family, inject monies into your business. People who have

previously run a business are often more prepared to lend /

invest

• This can be by way of a loan or equity finance

• It is important to understand the expectations of the family and

friend on what they will receive back and when. To avoid

arguments put the key features of the arrangement into a

written agreement

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Start-up- Loans

• Start-Up loans are loans aimed at start-up businesses. This

scheme started as only for 18-30 year olds, but has now been

extended to all ages. Applicants must be living in England and

looking for finance to start a business.

• After applying on-line a Delivery Partner is selected to identify

what stage the start-up is at in the ideas process, and help

them present their business proposal to a panel where they

will pitch for a personal loan

• Originally the maximum amount was £2,500 but this has been

increased to a maximum of £25,000. The loans are typically

less than £10,000 and average around £5,000 at present

Start-up Loans - http://www.startuploans.co.uk/

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Credit Cards

• A regular source of finance for start-up businesses

• Often used for items such as travel, stationery, petrol, car

repairs

• A good way of smoothing out unexpected big bills

• Allowing debt to get out of control will damage a business

owner’s credit rating

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Credit Unions

• Association of British Credit Unions (ABCUL) website provides

information regarding location of member credit unions and

their services

• Some larger CUs offer current account facilities

• Savers in a CU (usually for a period of at least 3 months) will

allow you to access lending facilities.

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Community Finance

Community Development Finance Institutions (CDFIs) provide

community finance tailored to the needs of businesses in

deprived areas, owned by entrepreneurs from disadvantaged

communities or unable to access mainstream finance

• Most CDFI business loans unsecured

• Banks now routinely refer businesses refused credit to CDFIs

• CDFIs can help business owners become “finance ready”

More information including finding the right CDFI and an on-line

application for finance go to:

Community Development Finance Association

• http://www.cdfa.org.uk/

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Grants

• Grants and support tend to be sector specific, so your trade

body or association are a good place to make enquiries

• The Local Enterprise Partnership should also be a first port of

call for grants and training courses

• Technology and green projects can be incentivised

• The government offers help with moving from benefits to work/

self-employment and the Job Centre Plus will have details.

• The GOV.uk website has a “Business finance and support

finder”

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Newer online sources of finance:

• Debt funding

• Equity finance

• Working capital funding – factoring & invoice discounting

Seeking to match businesses looking for finance with individuals

and businesses looking for diversification of risk and yield.

Business models vary. Vital to understand how risk of

proposition has been assessed.

Cost proportionately higher than bank finance but risk often

greater.

Internet Finance not within the Financial Services Compensation

Scheme

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Debt Funding (or Peer to Peer Lending) through the

Internet

• Applicants fill in on-line application form

• Acceptance criteria vary but for Funding Circle will include the

following:

– Must be UK based limited company

– At least two years financial reports

– Making a profit and a good credit rating

– May require up-to-date management accounts

– Details of other loans and commitments

– Responses are usually quick. Funding Circle says it’s credit

assessment team will give an answer on the application in 2 days.

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Peer to Peer Lending – On acceptance

• Once accepted for entry loan applicants enter auction in a marketplace. A

risk rating is applied to guide lenders

• Registered lenders start bidding the amount they are prepared to lend and

the interest rate they expect to be paid

• As bidding intensifies the interest rate tends to drop

• Applicants can accept the loan as soon as it is fully funded . Alternatively the

loan can be kept live for 14 days to see if the rate drops further

• Once loan accepted applicants can expect the money to be in their bank

accounts. This varies from same working day to two weeks

• An arrangement fee – either a percentage of the loan or a fixed amount – is

charged on the loan.

• The applicant repays the loan to the peer-to-peer lender who is responsible

for distributing the repayments to all lenders involved in the loan

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Peer to Peer Lending

Some providers :

• Funding Circle – loans £5,000 to £500,000

www’fundingcircle.com

• Thincats – loans £50,000 to £1M – www.ThinCats.com

• Rebuildingsociety - £2,000 to £50,000 to cos with turnover

over £200,000. www.rebuildingsociety.com

• FundingKnight – loans £25,000 to £100,000 to well

established SMEs. www.Fundingknight.com

• Wonga for business – short-term loans to £30,000

www.wongaforbusiness.com

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Peer to Peer Lending Vs Bank Finance

Advantages over bank finance:

• Application process is generally quicker

• Generally less onerous security requirements

Disadvantages over bank finance:

• Interest rates generally higher particularly where security and

guarantees not available

• Arrangement fees higher

For lenders:

• P2P in early stages so bad debt levels low.

• Bad debts not tax deductible for lenders

• But some P2P lenders have central fund to help mitigate bad debts

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Equity finance (Or Crowd Funding) through the Internet

Businesses seeking equity must:

• Complete a questionnaire specifying how much finance

required and the equity on offer

• The disclosures are reviewed to ensure they are fair, clear and

not misleading. Listing is then approved

• Investors can invest from up to the full amount required

• If full amount offered within a specified period go to closing, if

not investors get money back

• In closing legal due diligence is conducted and business signs

documentation and on-line platform subscribes for shares on

behalf of investors

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Crowd Funding Continued

• Fee for obtaining finance paid at this point

• Post-investment online platform holds shares as nominees for

investors.

• Dividends or when business floats or sells out the on-line

platform passes the proceeds back to investors

Some on-line equity funding: (eight in UK, these two are FCA

regulated)

• Crowdcube – www. Crowdcube.com Raised £11m for 60+cos

with 42,000 registered investors

• Seedrs – invests in seed-stage start-ups seeking up to

£100,000 of equity- www.seedrs.com

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Other Points on Crowd Funding

• Tax breaks such as Seed Enterprise Investment Scheme

(SEIS) can make Crowd funding more attractive

• Issues with second round funding with so many first time

shareholders.

• Research indicates that around 50% to 70% of business start-

ups fail completely. Likelihood is that investors will lose all their

money.

• FCA intention is to restrict financial promotions for unlisted

shares or debt securities to sophisticated investors, high net

worth individuals, investors taking authorised advice and to

limit investment in this class to 10% of net investible portfolio

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Working capital through the Internet

Lending usually based on factoring and invoice discounting or

selling future credit card income

Factors & invoice discounters include

• Marketinvoice – www.marketinvoice.com

• Platform Black – www.platformblack.com

• Receivables Exchange – www.receivablesxchange.com

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Working capital through the Internet

Credit card companies include Boost

- Business supplies evidence of recent card turnover

- Boost makes an offer of a cash advance based on turnover

- Boost agree to by future credit/ debit card receivables at a discount

- Daily repayment made via small fixed percentage of future credit/

debit card sales

- Business advises card processor to send settlement funds to escrow

account

- Funds collected and remitted through a proprietary escrow service

using Barclays AMS client account

www.boostcapital.co.uk

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

E-Invoicing, debtor management & arranging

finance

Various packages available. Following is Bilbus

• Create a sales invoice or upload from a template

• Invoices can be electronically submitted to customers in a

number of ways including by email direct from your accounting

platform or integrating with accounting platform and sending

direct to customer portal

• Platform sends automated reminders to customers

• Customer updates to status of invoice in their system can

result in automatic update of your collections forecast

• Platform provides feedback on customers’ payment

performance and cost of outstanding debt

• Platform can be linked to an application to a finance provider

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Recent Developments in Internet Finance

• The Financial Conduct Authority (FCA) has issued a

consultation paper on regulation of the sector scheduled for

early 2014.

• Discussions likely to focus on areas such as establishing

standards for credit checking procedures and minimum capital

requirements

• Concern that too strict standards will push up costs making

alternatives forms of finance more attractive.

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

British Business Bank

• The British Business Bank has been formed by the UK

government and will control £2,8 billion existing government

finance schemes and will get £1 billion in new funding.

• Working with 70 partners, it uses its funds to unlock finance for

thousands of smaller UK businesses

• http://british-business-bank.co.uk/applying-for-finance/

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

Getting finance – how might an accountant help?

Many accountants offer advice on business finance. An adviser

can help with:

• Reviewing the business to identify its financing status and

needs

• Identifying the most appropriate sources of money

• Guidance on investor expectations and attitudes

• Preparation of the business plan and of the live presentation

• Mentoring through the funding and due diligence process

They will make a charge for the work – ask for a quote before

you ask them to help.

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

ICAEW Business Advice Service (BAS)

ICAEW firms displaying this logo:

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

ICAEW Business Advice Service

• BAS offers an initial consultation for businesses and start-ups with

an ICAEW Chartered Accountant free of charge.

• An opportunity to discuss your business issues with a finance

professional

• Discussion can cover business issues from record-keeping to

managing cashflow

BUSINESS WITH CONFIDENCE icaew.com

© ICAEW 2012

ICAEW Business Advice Service

Go to:

businessadviceservice.com

Or email:

To find BAS firms in your area.

A world leader

of the accountancy

and finance profession

BUSINESS WITH CONFIDENCE icaew.com