Alpha edge - January 2016

26

www.citadelle.in Questions Insight Analysis Action “Why the delay?” India Strategy | January 2016

-

Upload

socialcitadelle -

Category

Economy & Finance

-

view

58 -

download

1

Transcript of Alpha edge - January 2016

www.citadelle.in

Questions

Insight

Analysis

Action

“Why the delay?”

India Strategy | January 2016

January 2016 3

End of fear? India Strategy | January, 2016

Foreword

Dear Investor,

The year ended more or less on a flattish note with Nifty shedding 4.1%. When compared to the year

earlier (CY2014 - ~30%) 2015 is a pretty forgettable one. Our fear that Equity Markets will both price

and time correct, and that Liquid Funds may do better than Equities turned out to be true {as shared in

the March 2015 note}. Infact 2015 could be termed as the year when “High hopes turned in to realism”

and new investors bore the brunt of it. 2015 started with hopes of big ticket reforms like the Land bill & GST, earnings recovery,

improvement in macroeconomic condition on lower commodity prices etc., eventually realism set in, in that they may been expecting

too much, too soon. This realism may spread wider, causing further negative sentiments in the near term, gravitating the Nifty to

around 7000 +/- 200 points. That’s when value may emerge and the next leg of the bull market is likely to resume. You may well be

reminded of the frustrating time of 2012 & 2013, when markets went sideways till it became cheap enough to re-rate.

Going by the four thumb rules that form the basis for our expectation of higher equity returns, the picture is far from encouraging…

a) Attractive valuations aren’t cheap to begin with b) earnings growth & momentum isn’t strong even if valuations are expensive c)

interest rate cuts aren’t translating into softening secondary market yields d) and confidence inspiring progress in policy making is

lacking. On each of the counts we may not exactly be in a sweet spot. Moreover, there are upside risks to inflation and fund flows

from FIIs. Especially the latter. Anecdotally we hear that one another fall out of collapsing oil & commodity prices is a steady increase

in redemptions by Sovereign Wealth Funds, which for years have funded the actual liquidity that circulates globally. A few of them

have started to develop deficits that need to be funded back home. We wonder if this is why Saudi’s are considering an IPO of Aramco.

Are we then looking at a repetition of 2008 that we should be afraid of? We don’t think so, unless US markets extends its price

correction well after a year of time correction in 2015. Speaking of which, there are worrying and increasing divergences in the

internals of US markets. For example, Down Jones Transportation Index is already in a bear market that is not evident in S&P 500

which is skating on thin ice with the support of its FANG {Facebook, Amazon, Netflix and Google}. Widely evident is a general technical

weakening of long term picture that needs reverse quickly, along with a revival in its broader markets. We will change our mind if it

doesn’t improve.

Back home, where our bread and butter lies, we think that there has been a delay in the recovery and that all is not yet lost. We are

in an environment where the ground is changing structurally thanks to the executive reforms {different from legislative reforms, GST

etc.,} and other various initiatives undertaken by the government along with the certain technological changes impacting existing

businesses. Generally the process of change is painful and we are witnessing the same in our earnings, however the long term outcome

of it would be more than fruitful. In all, 2016 may not the year of great returns without deft exploitation of market rallies through

tactical asset allocation calls just like 2015. For those who have been ahead of the curve in 2015, excellent re-entry points will emerge

that need to be bought into rather than feared. Remember 2013… Ah! How time flies.

For those interested in bottoms up stock picking strategy, we have overhauled our process and made it completely quantitative. This

approach, a first in India, will make it easier for investors to believe in what they are investing in, due to its simplicity and transparency.

As 2016 is likely to be the year where one would be better off sticking with the best, a portfolio of our 4* and above rated stocks,

some 30 of the best in the country can work well, just as it could have been in 2015. Read on to find out how a quantitative method

that cuts all noise in the process of investing, may well have beaten most fund managers. This portfolio strategy of 4* and above

rated stocks, would have delivered 26% CAGR vs Nifty return of 14.5%. At sectoral level we are bullish on consumer discretionary as a

theme and we believe Pharma & Media will do well.

Warm Regards,

A V Srikanth

January 2016 4

Alpha Edge | “Why the delay?”

Asset Class performance

Asset Class returns for Calendar Year 2015

Source: Bloomberg

2015 has been turbulent post a reset seen expectations of and Equity markets were down by 4.06%. Gold has been the worst performer with returns of 7.19%.

FII Flows for CY 2015

Source: ACEMF

Equity as well as Debt markets have seen outflows in December. Equities saw a net outflow of Rs 2,817 Crs whereas Debt market has seen net inflow of Rs 5,488 Crs. The outflows have been due to rate hike by US Federal Reserve.

Sector Returns for CY 2015

Source: Bloomberg

Consumer Durables, Healthcare and IT have been

outperformers for CY 2015. Metal, PSU and Realty have

been the laggards during the same period.

-4.06%

7.48% 8.01%

-7.19%-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Equity 10 yrTreasuries

Cash Gold

Asset Class Returns For CY 2015

Equity 10 yr Treasuries Cash Gold

47 3771

-53

83133

-3

128 113 97

18

-6

4

9

12

5

46

42

35

-51

160

46

-100

-50

0

50

100

150

200

250

300

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

19

05

FII F

low

s (i

n `

00

0 C

rs)

Equity Debt

-31.2

-17.2

-13.6

-9.9

-8.5

-6.4

-5.0

-3.4

-0.6

1.4

3.6

4.5

6.8

7.4

15.1

24.0

-35.0 -21.0 -7.0 7.0 21.0 35.0

S&P BSE METAL Index

S&P BSE PSU

S&P BSE Realty Index

S&P BSE BANKEX

S&P BSE Capital Goods

S&P BSE Power Index

S&P BSE SENSEX

S&P BSE OIL & GAS Index

S&P BSE AUTO Index

S&P BSE FMCG

S&P BSE TECk Index

S&P BSE IT

S&P BSE Small-Cap

S&P BSE Mid-Cap

S&P BSE Health Care

S&P BSE Consumer Durables

Sector Returns for CY 2015 (%)

January 2016 5

Alpha Edge | “Why the delay?”

Global markets 2015 - A recap

In 2015 there were few events that defined global markets in 2015. We have tried to list down the same and give a quick

review through a timeline

Falling oil prices

Grexit fear looms

Russian ruble crisis

China financial crisis

Our Clients

After equity markets stellar

performance around the world

in 2014, 2015 started with the

world adjusting to falling oil

prices which favoured all the

oil importing countries. Oil

plunged to $44 per barrel on

record high US oil inventories

The European Central Bank

(ECB) started its massive 60

billion euro-a-month bond-

buying program. Total bond

buying programme of $1.2

trillion. Added liquidity meant

suppression of yields which in

turn meant lower financing of

debt and faster recovery

process for Eurozone

Loose monetary policy

Greece defaults on $1.7 billion

payment to IMF. Greece becomes

the first developed nation to default

on payment. It was almost

confirmed that Greece will exit,

however Greece cut a deal with its

lenders but emerging markets came

under pressure again as currency

weakness dented investor

confidence in the regions. Eurozone

leaders reach an agreement over

third Greek bailout

Ruble hits a new low with falling oil

prices and economic sanctions. Oil

constitutes about 70% of total

exports for Russia. On top of the oil

slump, Russia is also facing pain

from Western sanctions imposed

over its role in the crisis in Ukraine. This double hit has pushed Russia

into deep recession. Russia's

economy shrank 4.6% in the second

quarter, the biggest drop since the

global financial crisis in 2009 Stock market in China collapsed 40%

from peak since June 2015. Chinese

economy has been on a borrowing

binge creating huge capacity. Due to

over capacity and high debt levels the

Chinese economy has slowed to a

multi year low. China devalued yuan

to spur exports which rattled the

markets. The world took notice of the

problems of the economy trying to

avoid hard landing as it transitions

from an investment led to

consumption led economy.

The lift off and the normalisation

Finally as anticipated Fed raised interest rates

for the first time in nearly a decade to start

the process of normalization of rates. The

year ended as it had started with the central

bank hogging the headlines. Equities fell in

the build up to the announcement pricing the

risk off and FII’s withdrew significant amount

of money from the emerging markets.

Jan 2015

Mar 2015

July 2015

Aug 2015

Aug 2015

Dec 2015

January 2016 6

Alpha Edge | “Why the delay?”

US Interest rates – Finally the lift off

It was probably the most awaited event of the year,

and Fed finally pulled the trigger by increasing the

Fed funds rate by 25 bps to 25-50 bps. The first in

nearly a decade and signaled the end of a zero rate

era. Markets braced for it, but when it happened it

turned out to be just another day signaling that first

hike was priced in, as we anticipated.

The central bank noted that the economy has come

a long way in recovery, although not completely. This

shows that the central bank has good confidence of

a recovery in the US economy. It also mentioned the

further course of interest rate hikes would be data

dependent and the economic conditions will only

warrant gradual increases in the Fed funds rate with

expectation of economy growing at 2.4% next year

and unemployment falling further to 4.7%.

The first hike was anticipated but the risk now lies in

the market’s expectations of a “slow and low” rate

hiking cycle. Right now the path of interest hike is of

utmost importance. Since the expectation is of a

slow rate hike, if conditions later warrant for a faster

rate hike (Inflation recovering faster than

anticipated) than what is expected right now, then it

could result into volatility.

Crude oil below $40

Brent crude started the year at around US$58 a

barrel having halved in the previous six months and

hitting a new 6 year low of around $36 per barrel.

Robust production from U.S. shale-oil fields pushed

the global crude market into oversupply in late 2014,

and production rose again this year as producers,

including Saudi Arabia and Russia opted to keep

output levels high. Inventories of crude oil in the U.S.

stand near eight-decade highs as producers continue

to produce at high rates to maximize profits in a low-

price environment. Although lower crude has

benefitted by increasing the consumption

expenditure due to increase in savings, it has rattled

the energy producers with cutbacks in earnings and

oil producing nations suffering from lower revenues

and weaker currencies.

The outlook for Oil prices for 2016 still looks under

pressure as Saudi Arabia, the world’s largest oil

exporter is preparing for a long period of low returns.

Saudi Arabia announced that they will reduce the

budget deficit of $98bn for 2016 through spending

cuts and reducing subsidies whilst it intends to stick

to its policy of no cut in oil production. It shows that

they are prepared to accept cheap prices for its crude

as it seeks to put pressure on higher cost rivals such

as US shale producers and waits for the market to

rebalance. Also, once the sanctions on Iran is lifted it

will result in even higher production of oil.

Global outlook 2016

0

2

4

6

8

Jan

-91

Jan

-93

Jan

-95

Jan

-97

Jan

-99

Jan

-01

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

Jan

-13

Jan

-15

Fed Rate

Fed Rate

020406080

100120140160

Crude oil

January 2016 7

Alpha Edge | “Why the delay?”

Modest growth in the US and a meagre recovery in the

Eurozone along with slowing down of emerging markets

meant 2015 was to be a year of downward revision of

growth estimates. IMF has recently cut its projections for

2015 to 3.1% down from 3.3% confirming the conditions

that prevailed through the year. The prediction for 2016

too was reduced from 3.8% to 3.6%.

China’s slowdown has dramatically reshaped the demand

environment in the global commodity market, which

many emerging economies rely on, to drive growth. With

a benign outlook on the commodity prices for 2016 it

seems that growth will be weak (though not worse) for

some more time with continued worries on China’s

economy nosediving due to unsustainability of the credit

fueled bubble. Adding to this, emerging markets have

their debt in dollars and a further rate hike would only

mean pressure on public and private balance sheets.

The developed economies would continue with the

moderate pace of recovery under the current deflationary

environment with US leading the pack. India would

continue to outperform its peers with better domestic

macroeconomic environment and reliance on domestic

consumption.

It would be another year of challenging environment for

global economy with disintegrated growth along with geo

political issues continuing

January 2016 8

Alpha Edge | “Why the delay?”

Indian Economy

The good

1) Pradhan Mantri Jan Dhan Yojana exceeds Rs.

25,000 crore – Results in financial inclusion

2) Direct benefits transfer in LPG saved Rs.

14,672 crore of subsidy last fiscal

3) Gold monetization scheme to help curb the

import of gold as the gold lying physically in

households is put to use in the economy

4) Government sets up Rs 40,000 crore National

Investment and Infrastructure fund

5) Pick up in public expenditure

6) IIP making a strong come back with capital

goods and consumption clocking double digit

growth. Industrial production in India rose

9.8 percent year-on-year in October of 2015,

the fastest pace since October of 2010 when

it went up 10 percent. Manufacturing output

jumped 10.6 percent, also the strongest in

five years

7) The 7th Pay commission would result in to

increase in savings and consumption

expenditure.

8) Even as growth has slowed in virtually every

other emerging market (EM), India’s growth

has accelerated over the last year

9) Low crude and other commodity prices for

the year have resulted in lowering of CAD to

1.4% of GDP from 1.8% last year H1.

10) Lower CPI & WPI numbers have resulted in

positive real interest rates.

11) A falling interest rate regime would result in

further increase in demand in the economy.

12) ‘Make in India’ campaign resulting in 35% FDI

growth wherein it has fallen by 17% in rest of

the world.

The not so good

1) Even though public expenditure is on the rise,

private expenditure is lacking

2) Urban consumption is on the rise however

rural consumption remains weak. Lower

hikes in MSP and weak monsoons

3) Missing big ticket reforms like GST & land bill

4) Weak global demand resulted in negative

topline growth for Indian companies, a bleak

outlook towards the global economy for the

next year persists

5) Second consecutive drought season resulting

in weak rural demand

6) Lack FII inflows in anticipation of the Fed rate

hike

7) Even though the Nominal GDP is growing at

10% in the last few years the earnings of Nifty

companies has been subdued.

-1.2-1.3

0.11.1

-2.0-0.5

3.75.6

4.3

0.90.5

2.6

-2.7

5.23.6

2.8

4.8

2.53.02.54.24.1

6.3

3.8

9.8

-4

-2

0

2

4

6

8

10

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

Dec

-14

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

IIP 3 months mov. Avg.

-2.6

-4.2 -4.7

-1.7 -1.3 -1.1

-7.6

-10.3 -10.5

-7.9-7.0

-6.4

FY11 FY12 FY13 FY14 FY15 FY16E

Current A/c deficit Trade deficit

4.9

5.9

4.94.4 4.1 3.9

FY11 FY12 FY13 FY14 FY15 FY16E

Fiscal Deficit

January 2016 9

Alpha Edge | “Why the delay?”

Why the delay… in recovery??

For most of 2015, we have been hearing about all the

good that has happened in the economy with its

growth as one of the fastest in the world, Crude

falling to lower levels helping inflation come down,

Government expenditure on the rise etc. Despite all

of the above investors aren’t really seeing ‘things

moving on the ground’ in a way that all of it

percolates to improved corporate earnings,

represented by in the Nifty/Sensex companies. Why

then is there a disparity in the growth of the

economy and the corporate profitability and why has

there been a delay in the economic recovery.

Almost 55% of the BSE100 revenues are export oriented

and are hurt by the weak global growth. Around 45% of it

is domestic oriented which too have been hurt by weak

rural economy, that’s no longer being supported by NDA

through artificial hikes in MSP that led to sustained

inflation under UPA. Further, using the decisive mandate

the NDA government is attempting to clean the fallout of

the UPA regime which pushed India towards crony

capitalism, suppression of competition, wasteful

subsidies and populist measures. The latter, especially the

uneconomical hikes in Minimum Support Prices (MSP) for

rural producers not only led to artificial inflation but also

led to transfer of money from urban to rural economy, all

of which doesn’t came back into the banking systems,

keeping the cost of capital high and liquidity poor. We

believe that the Jodi of Modi and Rajan through their

initiatives (mentioned below) are trying to address these

issues, by trying to overhaul the malaise that’s plaguing

India. It’s unfortunate that the much needed cleanup is

happening when the global growth is weak. Their policies

while good for all of us are changing things for established

business whose profits are under pressure for now as they

adapt to a new regime of transparency and competition.

What exactly are they doing and how some of it is it

hurting listed companies temporarily?

1) Moving from Physical assets to Financial

assets- India has one of the highest savings

rate in the world, despite that we have high

interest rates. The prime reason for the same

is most of the savings go into physical assets

like gold, real asset etc. which is ideally not

put to use in the economy. Modi introduced

several measures that bring the parallel

economy to main stream by building bridges

between the two. Initiatives like Jan Dhan

accounts, promoting use of Aadhar card, Gold

monetization scheme etc. move the physical

savings into financial savings steadily, which

would eventually lead to even higher

financial savings and higher availability of

capital to all at sustainably lower costs. The

lower cost of debt would help businesses

grow and increase overall demand which

creates more jobs in the economy.

2) Transition from protective to Competitive

business environment. While we moved

away from the license raj of yore, India’s

growth is still concentrated in the hands of a

few. The Modi government wants to change

that through many interconnected steps. Like

relaxing the regulatory environment for

businesses, expediting FDI proposals and

increasing the limit that needs government

approval, transparent auctions of natural

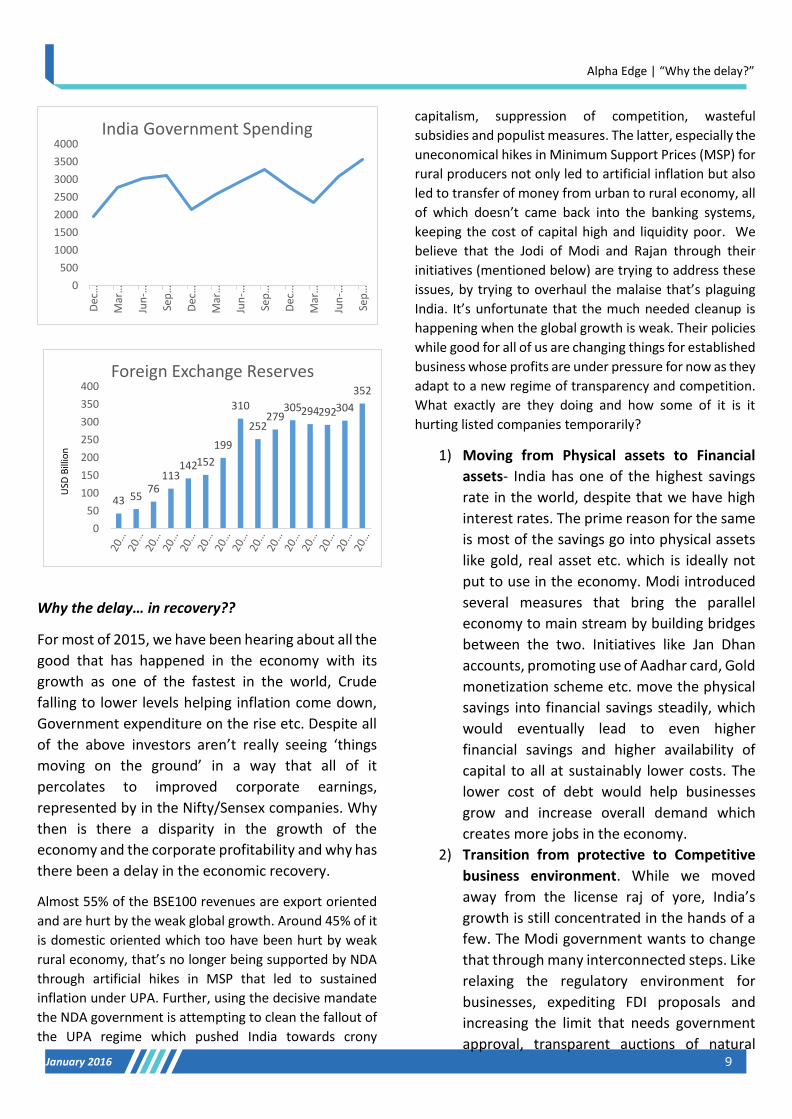

43 5576

113142152

199

310

252279

305294292304

352

0

50

100

150

200

250

300

350

400Foreign Exchange Reserves

USD

Bill

ion

0

500

1000

1500

2000

2500

3000

3500

4000

Dec

…

Mar

…

Jun

-…

Sep

…

Dec

…

Mar

…

Jun

-…

Sep

…

Dec

…

Mar

…

Jun

-…

Sep

…

India Government Spending

January 2016 10

Alpha Edge | “Why the delay?”

resources, faster environmental clearances,

digital India initiative, and simplification of

procedures through online mechanism and

passing of crucial Bills through the ordinance

route. All these steps make the business

environment more conducive but much more

competitive. The aim is to reduce corruption

and make a level playing field for all the

existing corporates and new ones who want

to enter. What this is doing is, it is disrupting

the traditional way the bigger businesses

have operated under the earlier regime

where they could protect their interests

through maneuvering (Crony Capitalism).

What the measures taken by government do,

is that it will reduce the entry barriers to new

and efficient. As established ones compete to

survive and grow, their profits will be under

pressure from new players who are funded

by FDI or PE players. This is why the domestic

facing large cap companies are struggling to

take off even though GDP is growing. As luck

would have it, this coincides with an

environment that has seen temporary

deflation – a direct hit to pricing power of

corporates and their margins

3) Direct benefit transfer plan (DBT) - DBT plan

is a mechanism for transferring government

benefits and subsidies directly into the hands

of residents through a biometric based

identification system (Aadhaar ), that aims to

speed up payments, removing leakages, and

enhancing financial inclusion. Citizens can

thus bypass an often circuitous and tedious

government mechanism and can obtain

funds directly. This also enables transparency

and prevents funds from being pilfered or

misused and more importantly increasing the

likelihood that it will come back to the

banking system. Already almost Rs. 40,000

crore has been transferred to the accounts of

the beneficiaries which directly results in to

higher savings and expenditure of the same

amount, Since the scheme is targeted more

towards the rural areas it also results in a

more sustainable inclusive growth. The plan

also would result in more savings to the

government as well. The increased incomes

of the households will also have a multiplier

effect on the GDP over the long run.

4) RBI increasing competition in the banking

sector - While the government is focused on

growth our central bank is focused on taming

inflation and improving competition in the

banking sector. Raghuram Rajan’s monetary

policy in the last 2 years has helped break the

back of inflation from chronically high levels.

RBI in the last 2 years have given banking

licenses to 23 banks whereas only 12 bank

licenses were given in the last 20 years. This

increase in competition would put lot of

pressure on the earnings of current banks.

Another reason that the headline corporate

growth numbers may be subdued

Hence one can draw a conclusion that the result of

the actions taken by the current government & RBI

coupled with improvements in technology are more

focused towards changing the structural economic

landscape of India. And whenever there is a

structural change, it results in changes to the way

businesses function, which is painful in the short

term and this is what we are currently witnessing in

the corporate sector. The reforms undertaken by the

government are in the right direction and address

long term structural problems and transform the

economy in to a modern place to do business

however it will take time for this process to bear the

fruits. We strongly believe that while these

measures may test your patience as an investor

temporarily, they may in fact lay the foundation for

a structural bull run that puts all our current worries

to rest. And for a long time.

January 2016 11

Alpha Edge | “Why the delay?”

Key risks to watch out for in 2016 -

1) One more drought season is of a key risk this

year, if it happens it will result in further

impact on the rural consumption and could

hurt the earnings of FY17

2) If the inflation hardens (Either because of

weak monsoons or rise in global commodity

prices from its current low levels) we could

see no significant rate cuts in FY17

3) Government going slow on the big ticket

reforms (GST, Land bill) would dent the

confidence of the private sector leading to

another year of muted corporate capital

expenditure.

4) Risk to global economy arising, specially out

of China, could result in to further weakening

of global demand

5) Fed hiking the interest rates aggressively

would impact the flows to India

6) US markets correcting can have a global

domino effect

Fixed income

Inflation hits 14-month high of 5.41% in November

In Nov we saw CPI & WPI spiking to 5.41% and -1.99%

respectively. One important observation is food

inflation seems to be contributing to the rise in CPI

for the last couple of months. The food inflation rose

to 6.07 percent from 5.25 percent, vegetables rose

by 4 percent compared with 2 percent and that of the

pulses zoomed by 46 percent compared with 42.8

percent. The food inflation is likely to stay high

through the March-quarter on account of two

reasons. One, the benefit of base effect clearly

vanishing. Two, the fear of unseasonal rains

impacting crops.

The year that was & outlook 2016

As compared to 2014, 2015 was a subdued year for

fixed income with 10 year benchmark yields falling 10

bps from 7.85 to 7.75 in CY2015. During the year the

yields fell to 7.5% only to recover quickly back to 7.75

levels. RBI governor cut the repo by 125 bps,

suggesting most of the yield fall was front ended.

With CPI & WPI outlook benign for the year the

governor had head room for rate cuts. Currently the

repo rate stands at 6.75%. With a real rate of return

target of RBI at 1.5% to 2% and CPI projection of 5%

by Mar 2017 we expect not more than 25-50 bps rate

cut till FY17, 50 bps possible if RBI undershoots its

inflation target. Also the rate cut would depend on

how well the government manages its fiscal situation

as that would affect the inflation. We see few upside

risks to inflation viz. unfavourable base effect for

inflation which is already evident for the last few

months, fiscal slippage on account of pay

commission, OROP etc., another year of weak

rainfall, rebound in commodity prices or aggressive

rate hikes by Fed.

With a gradual economic recovery under play with

improving macros, stable outlook on inflation and an

accommodative RBI governor we do expect yields to

fall though, marginally.

-10

-5

0

5

10

CPI and WPI

CPI WPI

6

7

8

9

10

2-J

an-1

4

2-M

ar-1

4

2-M

ay-1

4

2-J

ul-

14

2-S

ep

-14

2-N

ov-

14

2-J

an-1

5

2-M

ar-1

5

2-M

ay-1

5

2-J

ul-

15

2-S

ep

-15

2-N

ov-

15

Repo vs Gsec

Repo Rate Gsec yield

January 2016 12

Alpha Edge | “Why the delay?”

Equity

After a big rally in 2014, 2015 was a subdued year for

equities with Nifty falling 4.1% attributable to the

weak earnings numbers. 2015 was a year of

considerable volatility thanks to the i)anticipation of

the Fed rate hike which consumed all the 12 months

of 2015, ii) oil making a new low and iii) China growth

concerns. For the second consecutive year the mid

and small caps have outperformed their larger peers.

Mid cap index was up 7.4% and small cap index was

up 6.8%. From a sectoral point of view the sectors

that did well for the year were Consumer durables

(24%), Healthcare (15%) & IT (4.5%) and the worst

performing sectors for the year were Metals (-31.2%)

PSU (-17.2%) & Realty (-13.6%).

Few reasons attributed towards the dismal equity

performance for the year could be FII outflows in

the current year on global woes, slow pace of

economic reforms than what was expected, and

delay in the earnings recovery.

2015 was the year where we saw global commodity

prices falling which helped an importing country like

India however the benefits of the same was more

than offset by lower prices of the finished goods

and low global demand environment which

eventually resulted de growth in the sales number

and flat PAT growth. There was a surge seen in

public expenditure, however private expenditure

was muted as the cyclical businesses are facing

excess capacity and high debt levels. Even though

we saw recovery in IIP numbers for the year along

with decent GDP growth numbers the same was not

visible in the earnings.

So what has kept the earnings growth at bay? We

have tried to answer this question in the earlier

section by outlining how the current government is

changing the structural landscape which in turn

changes the way businesses function. This change

will bring out new businesses and put pressure on

the earnings of the old ones. We could see

disproportionate earnings growth as few companies

will do well and others would languish, which also

means we could see turnover in the index with new

companies coming in. Such inflection points are

sometimes marred by pain in the shorter term

(which we are currently witnessing). However, these

reforms along with the technological changes would

help us move in the right direction however, the

pace may be slow initially.

We think that currently the markets are little over

valued and one should expect single digit returns

over the next one year on the index, however we do

feel there is merit in bottoms up approach as good

quality companies and few sectors would continue

to do well in the next year. We would continue to

see volatility due to political and global economic

factors over the next one year and believe that

these are the best times to accumulate and invest in

equity as the medium to long term growth outlook

for markets and economy remains intact.

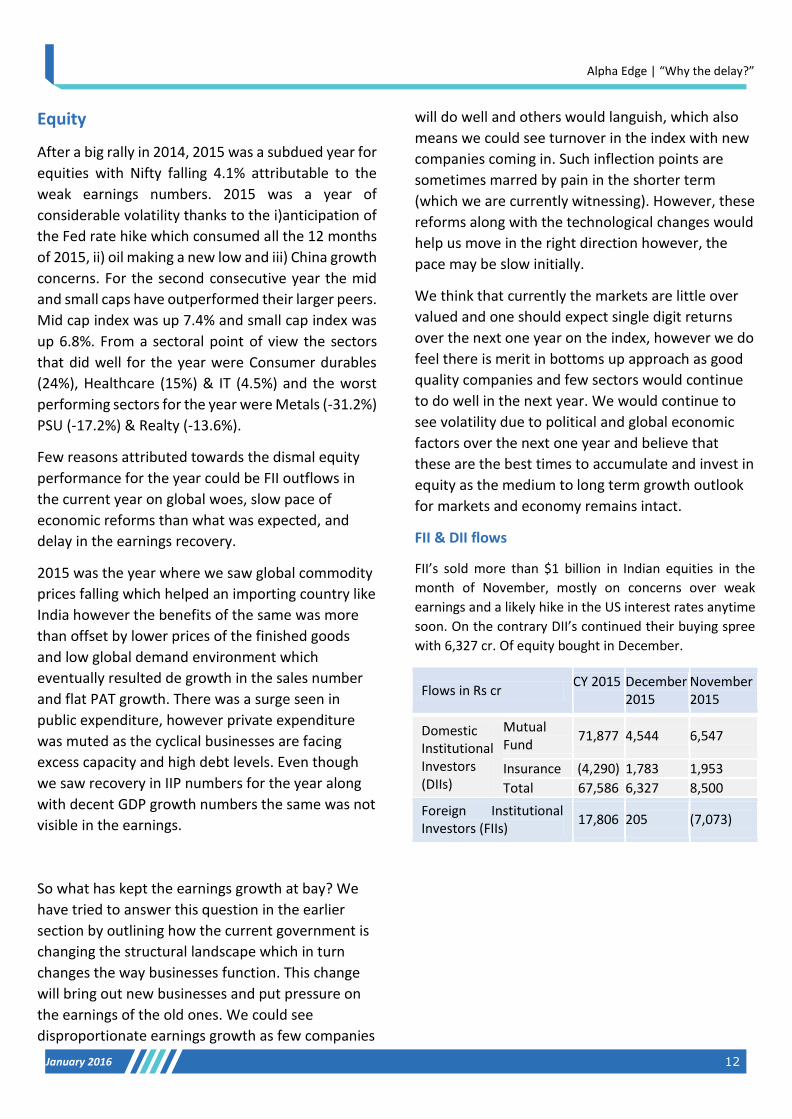

FII & DII flows

FII’s sold more than $1 billion in Indian equities in the

month of November, mostly on concerns over weak

earnings and a likely hike in the US interest rates anytime

soon. On the contrary DII’s continued their buying spree

with 6,327 cr. Of equity bought in December.

Flows in Rs cr CY 2015 December

2015 November 2015

Domestic Institutional Investors (DIIs)

Mutual Fund

71,877 4,544 6,547

Insurance (4,290) 1,783 1,953

Total 67,586 6,327 8,500

Foreign Institutional Investors (FIIs)

17,806 205 (7,073)

January 2016 13

Alpha Edge | “Why the delay?”

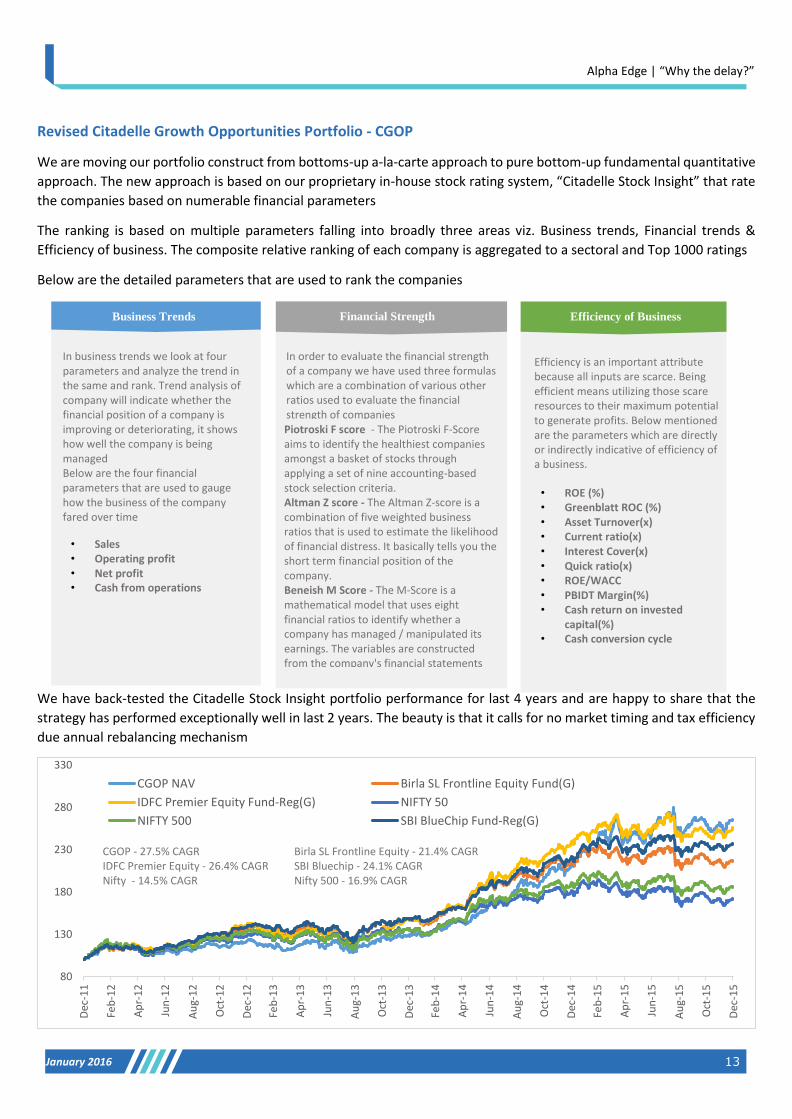

Revised Citadelle Growth Opportunities Portfolio - CGOP

We are moving our portfolio construct from bottoms-up a-la-carte approach to pure bottom-up fundamental quantitative

approach. The new approach is based on our proprietary in-house stock rating system, “Citadelle Stock Insight” that rate

the companies based on numerable financial parameters

The ranking is based on multiple parameters falling into broadly three areas viz. Business trends, Financial trends &

Efficiency of business. The composite relative ranking of each company is aggregated to a sectoral and Top 1000 ratings

Below are the detailed parameters that are used to rank the companies

We have back-tested the Citadelle Stock Insight portfolio performance for last 4 years and are happy to share that the

strategy has performed exceptionally well in last 2 years. The beauty is that it calls for no market timing and tax efficiency

due annual rebalancing mechanism

80

130

180

230

280

330

Dec

-11

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

Dec

-14

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

Dec

-15

CGOP NAV Birla SL Frontline Equity Fund(G)

IDFC Premier Equity Fund-Reg(G) NIFTY 50

NIFTY 500 SBI BlueChip Fund-Reg(G)

Business Trends

In business trends we look at four parameters and analyze the trend in the same and rank. Trend analysis of company will indicate whether the financial position of a company is improving or deteriorating, it shows how well the company is being managed

Below are the four financial parameters that are used to gauge how the business of the company fared over time

• Sales • Operating profit • Net profit • Cash from operations

Efficiency of Business

• ROE (%) • Greenblatt ROC (%) • Asset Turnover(x) • Current ratio(x) • Interest Cover(x) • Quick ratio(x) • ROE/WACC • PBIDT Margin(%) • Cash return on invested

capital(%) • Cash conversion cycle

Efficiency is an important attribute because all inputs are scarce. Being efficient means utilizing those scare resources to their maximum potential to generate profits. Below mentioned are the parameters which are directly or indirectly indicative of efficiency of a business.

Financial Strength

In order to evaluate the financial strength of a company we have used three formulas which are a combination of various other ratios used to evaluate the financial strength of companies Piotroski F score - The Piotroski F-Score aims to identify the healthiest companies amongst a basket of stocks through applying a set of nine accounting-based stock selection criteria. Altman Z score - The Altman Z-score is a combination of five weighted business ratios that is used to estimate the likelihood of financial distress. It basically tells you the short term financial position of the company. Beneish M Score - The M-Score is a mathematical model that uses eight financial ratios to identify whether a company has managed / manipulated its earnings. The variables are constructed from the company's financial statements and create a score to describe the degree to

CGOP - 27.5% CAGR Birla SL Frontline Equity - 21.4% CAGR IDFC Premier Equity - 26.4% CAGR SBI Bluechip - 24.1% CAGR

Nifty - 14.5% CAGR Nifty 500 - 16.9% CAGR

January 2016 14

Alpha Edge | “Why the delay?”

Citadelle Growth Opportunities Portfolio

Company Name 3 yr Avg ROE PAT 3yr CAGR Dividend Yield(%)

Ahluwalia Contracts (India) Ltd. 1.04 133.11 0.00

AIA Engineering Ltd. 19.71 33.44 0.64

Ajanta Pharma Ltd. 41.05 58.81 0.49

Aurobindo Pharma Ltd. 27.95 236.96 0.37

Avanti Feeds Ltd. 41.93 60.69 1.79

Bajaj Corp Ltd. 33.50 12.86 2.50

Bajaj Finance Ltd. 20.11 30.20 0.44

Bajaj Finserv Ltd. 27.26 8.42 0.13

Bosch Ltd. 17.71 6.01 0.33

Cadila Healthcare Ltd. 27.33 20.28 0.69

Caplin Point Laboratories Ltd. 49.84 72.28 0.54

CCL Products (India) Ltd. 21.00 37.34 0.84

Cholamandalam Investment & Finance Company Ltd. 17.88 37.96 0.60

DB Corp Ltd. 25.60 16.06 2.09

Gillette India Ltd. 14.84 27.78 0.33

Gujarat Pipavav Port Ltd. 15.43 89.17 0.00

Gulf Oil Lubricants India Ltd. 24.48 3560.17 1.08

Himachal Futuristic Communications Ltd. 88.88 179.95 0.00

Honeywell Automation India Ltd. 12.70 2.15 0.15

JM Financial Ltd. 11.29 43.00 2.81

Kitex Garments Ltd. 36.80 53.67 0.23

KRBL Ltd. 23.73 63.85 1.02

Lupin Ltd. 30.37 40.13 0.37

Marksans Pharma Ltd. 39.39 117.64 0.19

Navneet Education Ltd. 26.35 18.83 2.22

Procter & Gamble Hygiene & Health Care Ltd. 30.49 24.03 0.45

Skipper Ltd. 19.20 107.95 0.85

Sonata Software Ltd. 15.69 204.12 3.93

Tata Elxsi Ltd. 28.13 38.09 0.95

Vinati Organics Ltd. 31.48 28.29 0.67

108.66

95.94

90

95

100

105

110

115120

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Citadelle Growth Opportunities Portfolio Performance

Citadelle Growth Opportunities Portfolio NAV Nifty Index

90%

10%

Citadelle Growth Opportunities Portfolio Current Asset Allocation

Equity CashPerformance of CGOP as per previous methodology

January 2016 15

Alpha Edge | “Why the delay?”

Sample analysis of few stocks that make the cut

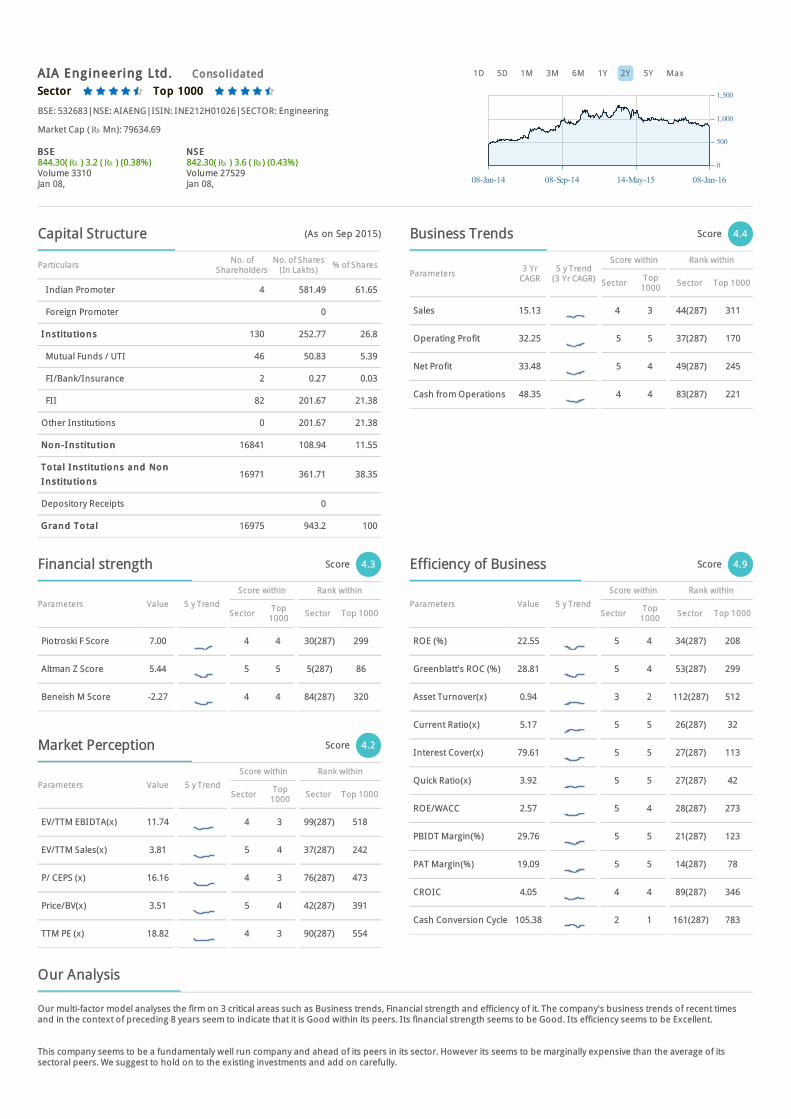

Sector Sector Top 1000 Top 1000

BSE: 532683|NSE: AIAENG|ISIN: INE212H01026|SECTOR: Engineering

Market Cap (Rs Mn): 79634.69

Jan 08,

BSE BSE 844.30(Rs ) 3.2 (Rs ) (0.38%)Volume 3310

Jan 08,

NSE NSE 842.30(Rs ) 3.6 (Rs) (0.43%)Volume 27529

AIA Engineering Ltd.AIA Engineering Ltd. ConsolidatedConsolidated 1D 5D 1M 3M 6M 1Y 2Y 5Y Max

Particulars No. ofShareholders

No. of Shares(In Lakhs)

% of Shares

Indian Promoter 4 581.49 61.65

Foreign Promoter 0

I n stitu tio n sI n stitu tio n s 130 252.77 26.8

Mutual Funds / UTI 46 50.83 5.39

FI/Bank/Insurance 2 0.27 0.03

FII 82 201.67 21.38

Other Institutions 0 201.67 21.38

No n -I n stitu tio nNo n -I n stitu tio n 16841 108.94 11.55

To tal I n stitu tio n s an d No nTo tal I n stitu tio n s an d No n

I n stitu tio n sI n stitu tio n s16971 361.71 38.35

Depository Receipts 0

Gran d To ta lGran d To ta l 16975 943.2 100

Parameters3 Yr

CAGR5 y Trend

(3 Yr CAGR)

Score within Rank within

Sector Top1000

Sector Top 1000

Sales 15.13 4 3 44(287) 311

Operating Profit 32.25 5 5 37(287) 170

Net Profit 33.48 5 4 49(287) 245

Cash from Operations 48.35 4 4 83(287) 221

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

Piotroski F Score 7.00 4 4 30(287) 299

Altman Z Score 5.44 5 5 5(287) 86

Beneish M Score -2.27 4 4 84(287) 320

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

EV/TTM EBIDTA(x) 11.74 4 3 99(287) 518

EV/TTM Sales(x) 3.81 5 4 37(287) 242

P/ CEPS (x) 16.16 4 3 76(287) 473

Price/BV(x) 3.51 5 4 42(287) 391

TTM PE (x) 18.82 4 3 90(287) 554

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

ROE (%) 22.55 5 4 34(287) 208

Greenblatt's ROC (%) 28.81 5 4 53(287) 299

Asset Turnover(x) 0.94 3 2 112(287) 512

Current Ratio(x) 5.17 5 5 26(287) 32

Interest Cover(x) 79.61 5 5 27(287) 113

Quick Ratio(x) 3.92 5 5 27(287) 42

ROE/WACC 2.57 5 4 28(287) 273

PBIDT Margin(%) 29.76 5 5 21(287) 123

PAT Margin(%) 19.09 5 5 14(287) 78

CROIC 4.05 4 4 89(287) 346

Cash Conversion Cycle 105.38 2 1 161(287) 783

Our multi-factor model analyses the firm on 3 critical areas such as Business trends, Financial strength and efficiency of it. The company's business trends of recent timesand in the context of preceding 8 years seem to indicate that it is Good within its peers. Its financial strength seems to be Good. Its efficiency seems to be Excellent.

This company seems to be a fundamentaly well run company and ahead of its peers in its sector. However its seems to be marginally expensive than the average of itssectoral peers. We suggest to hold on to the existing investments and add on carefully.

08-Jan-14 08-Sep-14 14-May-15 08-Jan-16

0

500

1,000

1,500

Capital Structure (As on Sep 2015) Business Trends Score 4.4

Financial strength Score 4.3

Market Perception Score 4.2

Efficiency of Business Score 4.9

Our Analysis

Sector Sector Within BFS Within BFS

BSE: 500034|NSE: BAJFINANCE|ISIN: INE296A01016|SECTOR: Finance - NBFC

Market Cap (Rs Mn): 338666.84

Jan 08,

BSE BSE 6314.55(Rs ) 201.6 (Rs ) (3.3%)Volume 4677

Jan 08,

NSE NSE 6314.50(Rs ) 208.2 (Rs) (3.41%)Volume 103507

Bajaj Finance Ltd.Bajaj Finance Ltd. StandaloneStandalone 1D 5D 1M 3M 6M 1Y 2Y 5Y Max

Particulars No. ofShareholders

No. of Shares(In Lakhs)

% of Shares

Indian Promoter 4 308.94 57.6

Foreign Promoter 0

I n stitu tio n sI n stitu tio n s 293 127.98 23.86

Mutual Funds / UTI 106 33.4 6.23

FI/Bank/Insurance 5 0.25 0.05

FII 182 94.33 17.59

Other Institutions 0 94.33 17.58

No n -I n stitu tio nNo n -I n stitu tio n 33982 99.4 18.53

To tal I n stitu tio n s an d No nTo tal I n stitu tio n s an d No n

I n stitu tio n sI n stitu tio n s34275 227.39 42.4

Depository Receipts 0

Gran d To ta lGran d To ta l 34279 536.33 100

Parameters3Yr

CAGR5 y Trend

(3 Yr CAGR)

Score within Rank within

Sector BFS Sector BFS

Advances 36.82 4 5 224(1192) 24.00

Core Operating

Income38.72 3 5 361(1192) 23

Net Interest Income 31.67 3 5 280(1192) 25

Net Profit 30.24 3 4 450(1192) 36

Adjusted Book Value

per share26.60 5 5 61(1192) 12

Adjusted Earnings

per share23.40 2 4 482(1192) 40

CASA % NA - -

Parameters Value 5 y TrendScore within Rank within

Sector BFS Sector BFS

CAR % (Basel III) 17.97 4 4 37(1192) 27

Credit/Deposits NA - -

Citadelle BFS Score 21.00 5 5 7(1192) 15

Parameters Value 5 y TrendScore within Rank within

Sector BFS Sector BFS

Price / Adj Book Value 4.27 5 5 72(1192) 25

Adj Price / Earnings 22.81 5 4 184(1192) 40

Parameters Value 5 y TrendScore within Rank within

Sector BFS Sector BFS

ROE (%) 20.43 4 5 69(1192) 12

ROA % 2.99 3 4 320(1192) 34

Interest Spread(%) 6.61 3 4 284(1192) 48

NIM % 54.99 3 4 442(1192) 31

Core Cost to Income

Ratio42.91 3 3 303(1192) 71

Net NPAs to net

Advances0.45 1 2 1186(1192) 96

Provision Coverage

ratio70.57 5 5 8(1192) 10

Our multi-factor model analyses the firm on 3 critical areas such as Business trends, Financial strength and efficiency of it. The company's business trends of recent timesand in the context of preceding 8 years seem to indicate that it is Good within its peers. Its financial strength seems to be Good. Its efficiency seems to be Average.

This company seems to be a fundamentaly well run company and ahead of its peers in its sector. However its seems to be very expensive than the average of its sectoralpeers. We suggest to hold on any existing investments and add on on it very carefully. Such companies have very little room for error

08-Jan-14 08-Sep-14 14-May-15 08-Jan-16

0

2,000

4,000

6,000

8,000

Capital Structure (As on Sep 2015) Business Trends Score 3.5

Financial strength Score 3.8

Market Perception Score 5

Efficiency of Business Score 3.3

Our Analysis

Sector Sector Top 1000 Top 1000

BSE: 532321|NSE: CADILAHC|ISIN: INE010B01027|SECTOR: Pharmaceuticals & Drugs

Market Cap (Rs Mn): 317462.58

Jan 08,

BSE BSE 310.10(Rs ) 3.3 (Rs ) (1.08%)Volume 217758

Jan 08,

NSE NSE 310.30(Rs ) 3.45 (Rs) (1.12%)Volume 1615678

Cadila Healthcare Ltd.Cadila Healthcare Ltd. ConsolidatedConsolidated 1D 5D 1M 3M 6M 1Y 2Y 5Y Max

Particulars No. ofShareholders

No. of Shares(In Lakhs)

% of Shares

Indian Promoter 11 1531.38 74.79

Foreign Promoter 0

I n stitu tio n sI n stitu tio n s 265 308.69 15.08

Mutual Funds / UTI 104 93.42 4.56

FI/Bank/Insurance 28 75.59 3.69

FII 130 137.9 6.73

Other Institutions 3 139.68 6.83

No n -I n stitu tio nNo n -I n stitu tio n 52165 207.42 10.13

To tal I n stitu tio n s an d No nTo tal I n stitu tio n s an d No n

I n stitu tio n sI n stitu tio n s52430 516.1 25.21

Depository Receipts 0

Gran d To ta lGran d To ta l 52441 2047.49 100

Parameters3 Yr

CAGR5 y Trend

(3 Yr CAGR)

Score within Rank within

Sector Top1000

Sector Top 1000

Sales 18.07 4 3 48(243) 244

Operating Profit 16.86 4 4 88(243) 357

Net Profit 20.30 4 4 92(243) 349

Cash from Operations 24.81 4 4 81(243) 364

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

Piotroski F Score 8.00 5 5 7(243) 201

Altman Z Score 4.29 5 5 28(243) 163

Beneish M Score -2.02 4 5 60(243) 191

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

EV/TTM EBIDTA(x) 15.05 4 4 93(243) 385

EV/TTM Sales(x) 3.68 4 4 87(243) 257

P/ CEPS (x) 18.61 4 4 88(243) 398

Price/BV(x) 6.39 5 5 38(243) 186

TTM PE (x) 23.05 3 3 98(243) 455

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

ROE (%) 31.12 5 5 26(243) 94

Greenblatt's ROC (%) 35.08 5 4 38(243) 201

Asset Turnover(x) 1.03 4 3 72(243) 460

Current Ratio(x) 1.29 3 3 129(243) 531

Interest Cover(x) 22.29 4 4 49(243) 212

Quick Ratio(x) 0.83 3 3 139(243) 556

ROE/WACC 3.58 5 5 23(243) 142

PBIDT Margin(%) 20.55 4 4 54(243) 253

PAT Margin(%) 13.46 5 5 34(243) 149

CROIC 6.24 5 4 46(243) 259

Cash Conversion Cycle 60.73 2 2 139(243) 558

Our multi-factor model analyses the firm on 3 critical areas such as Business trends, Financial strength and efficiency of it. The company's business trends of recent timesand in the context of preceding 8 years seem to indicate that it is Good within its peers. Its financial strength seems to be Excellent. Its efficiency seems to be Excellent.

This company seems to be a fundamentaly well run company and ahead of its peers in its sector. However its seems to be marginally expensive than the average of itssectoral peers. We suggest to hold on to the existing investments and add on carefully.

08-Jan-14 08-Sep-14 14-May-15 08-Jan-16

0

200

400

600

Capital Structure (As on Sep 2015) Business Trends Score 4

Financial strength Score 4.8

Market Perception Score 4

Efficiency of Business Score 4.7

Our Analysis

Sector Sector Top 1000 Top 1000

BSE: 521248|NSE: KITEX|ISIN: INE602G01020|SECTOR: Textile

Market Cap (Rs Mn): 32152.75

Jan 08,

BSE BSE 676.90(Rs ) 3.65 (Rs ) (0.54%)Volume 4972

Jan 08,

NSE NSE 675.35(Rs ) 1.55 (Rs) (0.23%)Volume 41052

Kitex Garments Ltd.Kitex Garments Ltd. StandaloneStandalone 1D 5D 1M 3M 6M 1Y 2Y 5Y Max

Particulars No. ofShareholders

No. of Shares(In Lakhs)

% of Shares

Indian Promoter 10 257.66 54.24

Foreign Promoter 0

I n stitu tio n sI n stitu tio n s 54 14.18 2.98

Mutual Funds / UTI 5 0.27 0.06

FI/Bank/Insurance 0

FII 37 10.74 2.26

Other Institutions 12 13.9 2.92

No n -I n stitu tio nNo n -I n stitu tio n 24926 203.17 42.77

To tal I n stitu tio n s an d No nTo tal I n stitu tio n s an d No n

I n stitu tio n sI n stitu tio n s24980 217.34 45.76

Depository Receipts 0

Gran d To ta lGran d To ta l 24990 475 100

Parameters3 Yr

CAGR5 y Trend

(3 Yr CAGR)

Score within Rank within

Sector Top1000

Sector Top 1000

Sales 17.92 5 4 89(501) 248

Operating Profit 40.97 4 5 104(501) 115

Net Profit 53.73 4 5 127(501) 165

Cash from Operations 27.06 3 3 153(501) 339

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

Piotroski F Score 8.00 5 5 9(501) 80

Altman Z Score 5.52 5 5 8(501) 83

Beneish M Score -2.49 4 3 155(501) 471

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

EV/TTM EBIDTA(x) 15.79 5 4 91(501) 364

EV/TTM Sales(x) 6.65 5 5 62(501) 107

P/ CEPS (x) 24.82 5 4 58(501) 285

Price/BV(x) 10.66 5 5 12(501) 77

TTM PE (x) 29.90 5 4 63(501) 341

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

ROE (%) 44.98 5 5 22(501) 40

Greenblatt's ROC (%) 52.39 5 5 31(501) 80

Asset Turnover(x) 1.09 2 2 208(501) 426

Current Ratio(x) 1.56 4 4 170(501) 378

Interest Cover(x) 7.71 5 4 70(501) 334

Quick Ratio(x) 1.51 4 4 119(501) 244

ROE/WACC 4.52 5 5 50(501) 83

PBIDT Margin(%) 35.99 5 5 23(501) 86

PAT Margin(%) 19.26 5 5 20(501) 76

CROIC 15.38 5 5 44(501) 63

Cash Conversion Cycle 26.43 3 3 141(501) 292

Our multi-factor model analyses the firm on 3 critical areas such as Business trends, Financial strength and efficiency of it. The company's business trends of recent timesand in the context of preceding 8 years seem to indicate that it is Good within its peers. Its financial strength seems to be Excellent. Its efficiency seems to be Excellent.

This company seems to be a fundamentaly well run company and ahead of its peers in its sector. However its seems to be very expensive than the average of its sectoralpeers. We suggest to hold on any existing investments and add on on it very carefully. Such companies have very little room for error

08-Jan-14 08-Sep-14 14-May-15 08-Jan-16

0

500

1,000

1,500

Capital Structure (As on Sep 2015) Business Trends Score 3.9

Financial strength Score 4.8

Market Perception Score 5

Efficiency of Business Score 4.9

Our Analysis

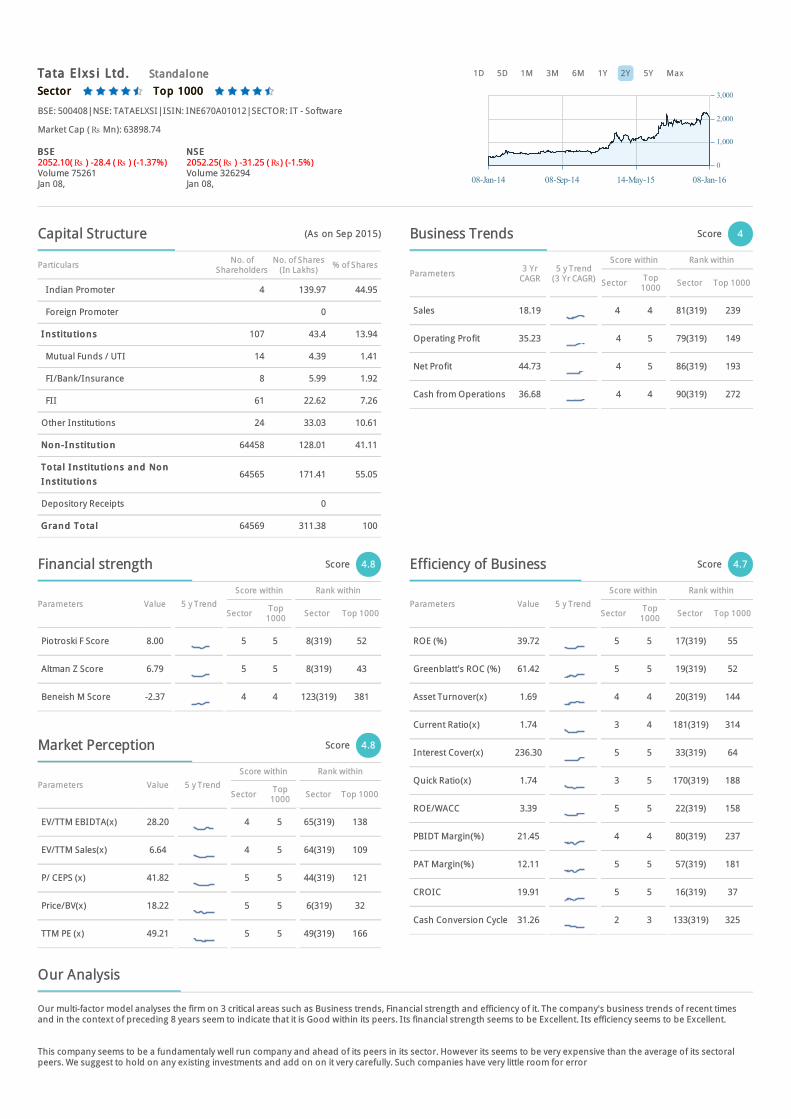

Sector Sector Top 1000 Top 1000

BSE: 500408|NSE: TATAELXSI|ISIN: INE670A01012|SECTOR: IT - Software

Market Cap (Rs Mn): 63898.74

Jan 08,

BSE BSE 2052.10(Rs ) -28.4 (Rs ) (-1.37%)Volume 75261

Jan 08,

NSE NSE 2052.25(Rs ) -31.25 (Rs) (-1.5%)Volume 326294

Tata Elxs i Ltd.Tata Elxs i Ltd. StandaloneStandalone 1D 5D 1M 3M 6M 1Y 2Y 5Y Max

Particulars No. ofShareholders

No. of Shares(In Lakhs)

% of Shares

Indian Promoter 4 139.97 44.95

Foreign Promoter 0

I n stitu tio n sI n stitu tio n s 107 43.4 13.94

Mutual Funds / UTI 14 4.39 1.41

FI/Bank/Insurance 8 5.99 1.92

FII 61 22.62 7.26

Other Institutions 24 33.03 10.61

No n -I n stitu tio nNo n -I n stitu tio n 64458 128.01 41.11

To tal I n stitu tio n s an d No nTo tal I n stitu tio n s an d No n

I n stitu tio n sI n stitu tio n s64565 171.41 55.05

Depository Receipts 0

Gran d To ta lGran d To ta l 64569 311.38 100

Parameters3 Yr

CAGR5 y Trend

(3 Yr CAGR)

Score within Rank within

Sector Top1000

Sector Top 1000

Sales 18.19 4 4 81(319) 239

Operating Profit 35.23 4 5 79(319) 149

Net Profit 44.73 4 5 86(319) 193

Cash from Operations 36.68 4 4 90(319) 272

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

Piotroski F Score 8.00 5 5 8(319) 52

Altman Z Score 6.79 5 5 8(319) 43

Beneish M Score -2.37 4 4 123(319) 381

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

EV/TTM EBIDTA(x) 28.20 4 5 65(319) 138

EV/TTM Sales(x) 6.64 4 5 64(319) 109

P/ CEPS (x) 41.82 5 5 44(319) 121

Price/BV(x) 18.22 5 5 6(319) 32

TTM PE (x) 49.21 5 5 49(319) 166

Parameters Value 5 y Trend

Score within Rank within

Sector Top1000 Sector Top 1000

ROE (%) 39.72 5 5 17(319) 55

Greenblatt's ROC (%) 61.42 5 5 19(319) 52

Asset Turnover(x) 1.69 4 4 20(319) 144

Current Ratio(x) 1.74 3 4 181(319) 314

Interest Cover(x) 236.30 5 5 33(319) 64

Quick Ratio(x) 1.74 3 5 170(319) 188

ROE/WACC 3.39 5 5 22(319) 158

PBIDT Margin(%) 21.45 4 4 80(319) 237

PAT Margin(%) 12.11 5 5 57(319) 181

CROIC 19.91 5 5 16(319) 37

Cash Conversion Cycle 31.26 2 3 133(319) 325

Our multi-factor model analyses the firm on 3 critical areas such as Business trends, Financial strength and efficiency of it. The company's business trends of recent timesand in the context of preceding 8 years seem to indicate that it is Good within its peers. Its financial strength seems to be Excellent. Its efficiency seems to be Excellent.

This company seems to be a fundamentaly well run company and ahead of its peers in its sector. However its seems to be very expensive than the average of its sectoralpeers. We suggest to hold on any existing investments and add on on it very carefully. Such companies have very little room for error

08-Jan-14 08-Sep-14 14-May-15 08-Jan-16

0

1,000

2,000

3,000

Capital Structure (As on Sep 2015) Business Trends Score 4

Financial strength Score 4.8

Market Perception Score 4.8

Efficiency of Business Score 4.7

Our Analysis

January 2016 16

Alpha Edge | “Why the delay?”

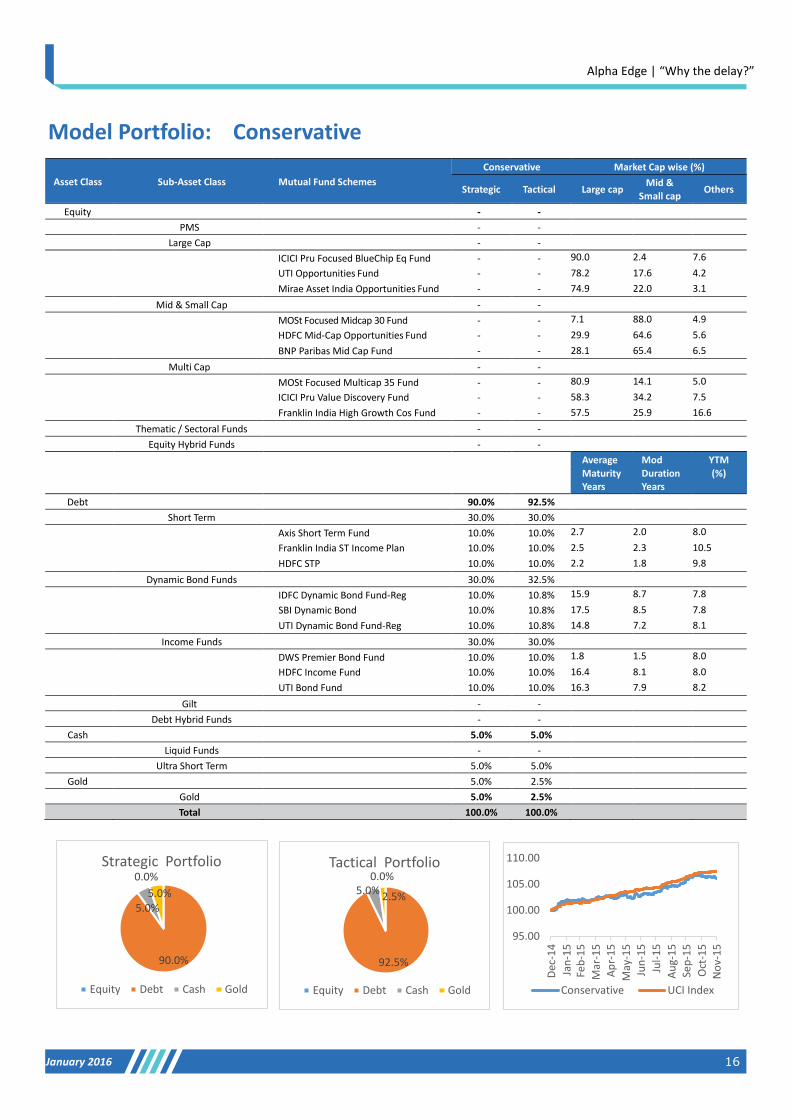

Model Portfolio: Conservative

Conservative Market Cap wise (%)

Asset Class Sub-Asset Class Mutual Fund Schemes

Strategic

Tactical

Large cap Mid &

Small cap

Others

Equity - - PMS - - Large Cap - - ICICI Pru Focused BlueChip Eq Fund - - 90.0 2.4 7.6

UTI Opportunities Fund - - 78.2 17.6 4.2

Mirae Asset India Opportunities Fund - - 74.9 22.0 3.1

Mid & Small Cap - - MOSt Focused Midcap 30 Fund - - 7.1 88.0 4.9

HDFC Mid-Cap Opportunities Fund - - 29.9 64.6 5.6

BNP Paribas Mid Cap Fund - - 28.1 65.4 6.5

Multi Cap - - MOSt Focused Multicap 35 Fund - - 80.9 14.1 5.0

ICICI Pru Value Discovery Fund - - 58.3 34.2 7.5

Franklin India High Growth Cos Fund - - 57.5 25.9 16.6

Thematic / Sectoral Funds - - Equity Hybrid Funds - - Average

Maturity Years

Mod

Duration Years

YTM

(%)

Debt 90.0% 92.5% Short Term 30.0% 30.0% Axis Short Term Fund 10.0% 10.0% 2.7 2.0 8.0

Franklin India ST Income Plan 10.0% 10.0% 2.5 2.3 10.5

HDFC STP 10.0% 10.0% 2.2 1.8 9.8

Dynamic Bond Funds 30.0% 32.5% IDFC Dynamic Bond Fund-Reg 10.0% 10.8% 15.9 8.7 7.8

SBI Dynamic Bond 10.0% 10.8% 17.5 8.5 7.8

UTI Dynamic Bond Fund-Reg 10.0% 10.8% 14.8 7.2 8.1

Income Funds 30.0% 30.0% DWS Premier Bond Fund 10.0% 10.0% 1.8 1.5 8.0

HDFC Income Fund 10.0% 10.0% 16.4 8.1 8.0

UTI Bond Fund 10.0% 10.0% 16.3 7.9 8.2

Gilt - - Debt Hybrid Funds - -

Cash 5.0% 5.0% Liquid Funds - - Ultra Short Term 5.0% 5.0%

Gold 5.0% 2.5% Gold 5.0% 2.5% Total 100.0% 100.0%

0.0%

90.0%

5.0%5.0%

Strategic Portfolio

Equity Debt Cash Gold

0.0%

92.5%

5.0%2.5%

Tactical Portfolio

Equity Debt Cash Gold

95.00

100.00

105.00

110.00

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5Se

p-1

5

Oct

-15

No

v-1

5

Conservative UCI Index

January 2016 17

Alpha Edge | “Why the delay?”

Model Portfolio: Moderately Conservative

Mod Conservative Market Cap wise (%)

Asset Class Sub-Asset Class Mutual Fund Schemes

Strategic

Tactical

Large cap Mid &

Small cap

Others

Equity 25.0% 25.0% PMS - - Large Cap 25.0% 25.0% ICICI Pru Focused BlueChip Eq Fund 10.0% 10.0% 90.0 2.4 7.6

UTI Opportunities Fund 10.0% 10.0% 78.2 17.6 4.2

Mirae Asset India Opportunities Fund 5.0% 5.0% 74.9 22.0 3.1

Mid & Small Cap - - MOSt Focused Midcap 30 Fund - - 7.1 88.0 4.9

HDFC Mid-Cap Opportunities Fund - - 29.9 64.6 5.6

BNP Paribas Mid Cap Fund - - 28.1 65.4 6.5

Multi Cap - - MOSt Focused Multicap 35 Fund - - 80.9 14.1 5.0

ICICI Pru Value Discovery Fund - - 58.3 34.2 7.5

Franklin India High Growth Cos Fund - - 57.5 25.9 16.6

Thematic / Sectoral Funds - - Equity Hybrid Funds - - Average

Maturity Years

Mod

Duration Years

YTM

(%)

Debt 65.0% 67.5% Short Term 30.0% 30.0% Axis Short Term Fund 10.0% 10.0% 2.7 2.0 8.0

Franklin India ST Income Plan 10.0% 10.0% 2.5 2.3 10.5

HDFC STP 10.0% 10.0% 2.2 1.8 9.8

Dynamic Bond Funds 30.0% 32.5% IDFC Dynamic Bond Fund-Reg 10.0% 10.8% 15.9 8.7 7.8

SBI Dynamic Bond 10.0% 10.8% 17.5 8.5 7.8

UTI Dynamic Bond Fund-Reg 10.0% 10.8% 14.8 7.2 8.1

Income Funds 5.0% 5.0% DWS Premier Bond Fund - - 1.8 1.5 8.0

HDFC Income Fund - - 16.4 8.1 8.0

UTI Bond Fund 5.0% 5.0% 16.3 7.9 8.2

Gilt - - Debt Hybrid Funds - -

Cash 5.0% 5.0% Liquid Funds - - Ultra Short Term 5.0% 5.0%

Gold 5.0% 2.5% Gold 5.0% 2.5% Total 100.0% 100.0%

25.0%

65.0%

5.0%5.0%

Strategic Portfolio

Equity Debt Cash Gold

25.0%

67.5%

5.0% 2.5%

Tactical Portfolio

Equity Debt Cash Gold

96.0098.00

100.00102.00104.00106.00108.00

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5M

ay-1

5Ju

n-1

5Ju

l-1

5A

ug-

15

Sep

-15

Oct

-15

No

v-1

5D

ec-1

5

Mod Conservative UCI Index

January 2016 18

Alpha Edge | “Why the delay?”

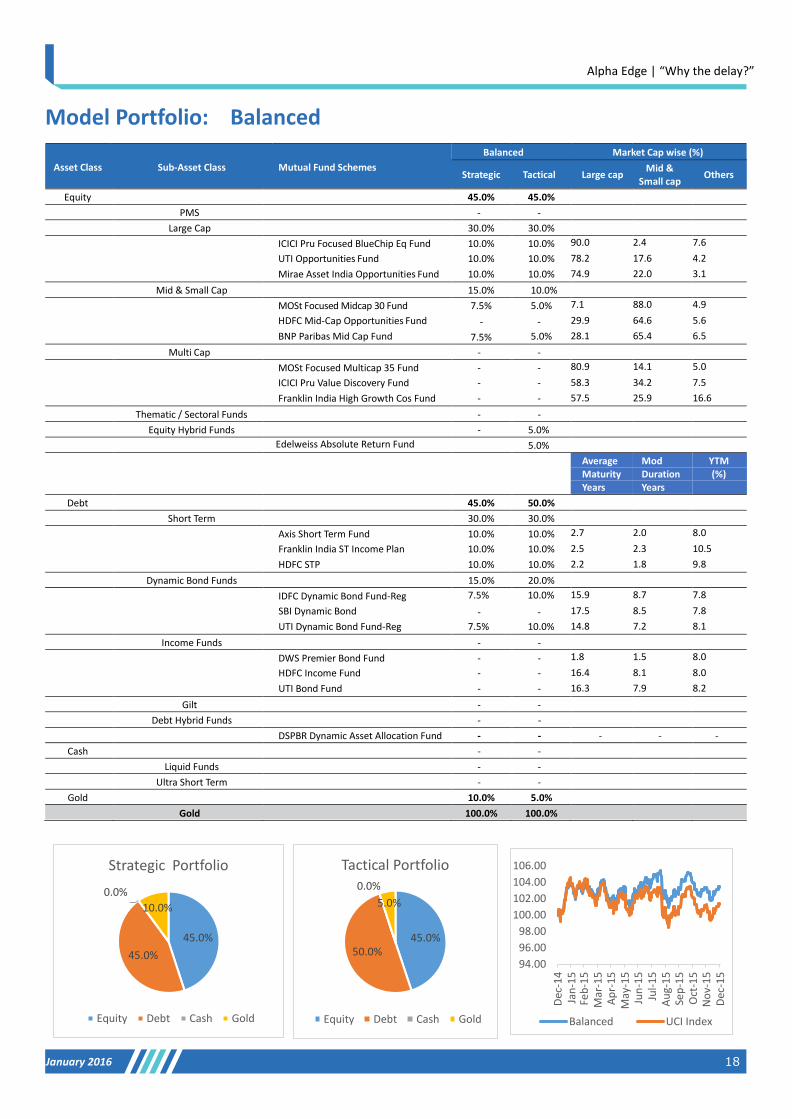

Model Portfolio: Balanced

Balanced Market Cap wise (%)

Asset Class Sub-Asset Class Mutual Fund Schemes

Strategic

Tactical

Large cap Mid & Small cap

Others

Equity 45.0% 45.0% PMS - - Large Cap 30.0% 30.0% ICICI Pru Focused BlueChip Eq Fund 10.0% 10.0% 90.0 2.4 7.6

UTI Opportunities Fund 10.0% 10.0% 78.2 17.6 4.2

Mirae Asset India Opportunities Fund 10.0% 10.0% 74.9 22.0 3.1

Mid & Small Cap 15.0% 10.0% MOSt Focused Midcap 30 Fund 7.5% 5.0% 7.1 88.0 4.9

HDFC Mid-Cap Opportunities Fund - - 29.9 64.6 5.6

BNP Paribas Mid Cap Fund 7.5% 5.0% 28.1 65.4 6.5

Multi Cap - - MOSt Focused Multicap 35 Fund - - 80.9 14.1 5.0

ICICI Pru Value Discovery Fund - - 58.3 34.2 7.5

Franklin India High Growth Cos Fund - - 57.5 25.9 16.6

Thematic / Sectoral Funds - - Equity Hybrid Funds - 5.0% Edelweiss Absolute Return Fund 5.0%

%

Average Maturity Years

Mod Duration Years

YTM (%)

Debt 45.0% 50.0% Short Term 30.0% 30.0% Axis Short Term Fund 10.0% 10.0% 2.7 2.0 8.0

Franklin India ST Income Plan 10.0% 10.0% 2.5 2.3 10.5

HDFC STP 10.0% 10.0% 2.2 1.8 9.8

Dynamic Bond Funds 15.0% 20.0% IDFC Dynamic Bond Fund-Reg 7.5% 10.0% 15.9 8.7 7.8

SBI Dynamic Bond - - 17.5 8.5 7.8

UTI Dynamic Bond Fund-Reg 7.5% 10.0% 14.8 7.2 8.1

Income Funds - - DWS Premier Bond Fund - - 1.8 1.5 8.0

HDFC Income Fund - - 16.4 8.1 8.0

UTI Bond Fund - - 16.3 7.9 8.2

Gilt - - Debt Hybrid Funds - - DSPBR Dynamic Asset Allocation Fund - - - - -

Cash - - Liquid Funds - - Ultra Short Term - -

Gold 10.0% 5.0% Gold 100.0% 100.0%

45.0%

45.0%

0.0%

10.0%

Strategic Portfolio

Equity Debt Cash Gold

45.0%50.0%

0.0%

5.0%

Tactical Portfolio

Equity Debt Cash Gold

94.00

96.00

98.00

100.00

102.00

104.00

106.00

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5M

ay-1

5Ju

n-1

5Ju

l-1

5A

ug-

15

Sep

-15

Oct

-15

No

v-1

5D

ec-1

5

Balanced UCI Index

January 2016 19

Alpha Edge | “Why the delay?”

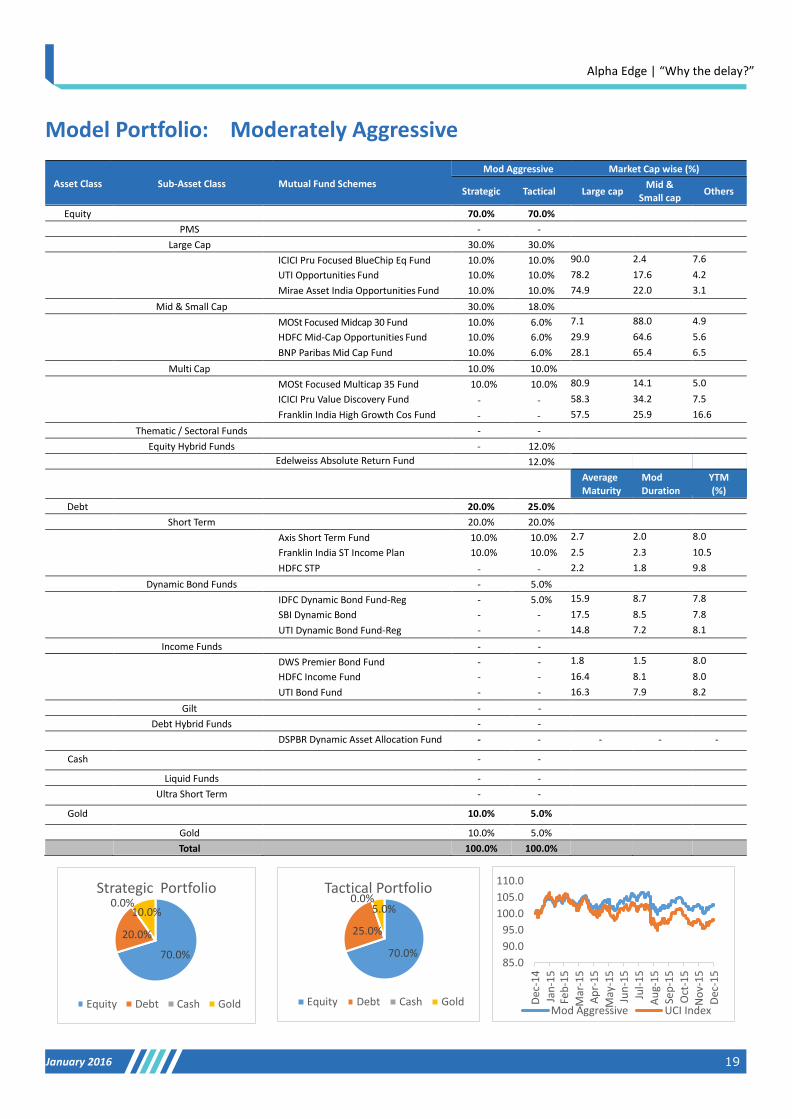

Model Portfolio: Moderately Aggressive

Mod Aggressive Market Cap wise (%)

Asset Class Sub-Asset Class Mutual Fund Schemes

Strategic

Tactical

Large cap Mid & Small cap

Others

Equity 70.0% 70.0% PMS - - Large Cap 30.0% 30.0% ICICI Pru Focused BlueChip Eq Fund 10.0% 10.0% 90.0 2.4 7.6

UTI Opportunities Fund 10.0% 10.0% 78.2 17.6 4.2

Mirae Asset India Opportunities Fund 10.0% 10.0% 74.9 22.0 3.1

Mid & Small Cap 30.0% 18.0% MOSt Focused Midcap 30 Fund 10.0% 6.0% 7.1 88.0 4.9

HDFC Mid-Cap Opportunities Fund 10.0% 6.0% 29.9 64.6 5.6

BNP Paribas Mid Cap Fund 10.0% 6.0% 28.1 65.4 6.5

Multi Cap 10.0% 10.0% MOSt Focused Multicap 35 Fund 10.0% 10.0% 80.9 14.1 5.0

ICICI Pru Value Discovery Fund - - 58.3 34.2 7.5

Franklin India High Growth Cos Fund - - 57.5 25.9 16.6

Thematic / Sectoral Funds - - Equity Hybrid Funds - 12.0% Edelweiss Absolute Return Fund 12.0% Average

Maturity Years

Mod

Duration Years

YTM

(%) Debt 20.0% 25.0%

Short Term 20.0% 20.0% Axis Short Term Fund 10.0% 10.0% 2.7 2.0 8.0

Franklin India ST Income Plan 10.0% 10.0% 2.5 2.3 10.5

HDFC STP - - 2.2 1.8 9.8

Dynamic Bond Funds - 5.0% IDFC Dynamic Bond Fund-Reg - 5.0% 15.9 8.7 7.8

SBI Dynamic Bond - - 17.5 8.5 7.8

UTI Dynamic Bond Fund-Reg - - 14.8 7.2 8.1

Income Funds - - DWS Premier Bond Fund - - 1.8 1.5 8.0

HDFC Income Fund - - 16.4 8.1 8.0

UTI Bond Fund - - 16.3 7.9 8.2

Gilt - - Debt Hybrid Funds - - DSPBR Dynamic Asset Allocation Fund - - - - -

Cash - -

Liquid Funds - - Ultra Short Term - -

Gold 10.0% 5.0%

Gold 10.0% 5.0% Total 100.0% 100.0%

70.0%

20.0%

0.0%10.0%

Strategic Portfolio

Equity Debt Cash Gold

70.0%

25.0%

0.0%5.0%

Tactical Portfolio

Equity Debt Cash Gold

85.0

90.0

95.0

100.0

105.0

110.0

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5Se

p-1

5

Oct

-15

No

v-1

5

Dec

-15

Mod Aggressive UCI Index

January 2016 20

Alpha Edge | “Why the delay?”

Model Portfolio: Aggressive

Aggressive Market Cap wise (%)

Asset Class Sub-Asset Class Mutual Fund Schemes

Strategic

Tactical

Large cap Mid & Small cap

Others

Equity 90.0% 90.0% PMS - - Large Cap 30.0% 30.0% ICICI Pru Focused BlueChip Eq Fund 10.0% 10.0% 90.0 2.4 7.6

UTI Opportunities Fund 10.0% 10.0% 78.2 17.6 4.2

Mirae Asset India Opportunities Fund 10.0% 10.0% 74.9 22.0 3.1

Mid & Small Cap 30.0% 20.0% MOSt Focused Midcap 30 Fund 10.0% 6.6% 7.1 88.0 4.9

HDFC Mid-Cap Opportunities Fund 10.0% 6.6% 29.9 64.6 5.6

BNP Paribas Mid Cap Fund 10.0% 6.6% 28.1 65.4 6.5

Multi Cap 30.0% 30.0% MOSt Focused Multicap 35 Fund 10.0% 10.0% 80.9 14.1 5.0

ICICI Pru Value Discovery Fund 10.0% 10.0% 58.3 34.2 7.5

Franklin India High Growth Cos Fund 10.0% 10.0% 57.5 25.9 16.6

Thematic / Sectoral Funds - - Equity Hybrid Funds - 10.0% Edelweiss Absolute Return Fund 10.0% Average

Maturity Years

Mod

Duration Years

YTM

(%)

Debt - 5.0% Short Term - - Axis Short Term Fund - - 2.7 2.0 8.0

Franklin India ST Income Plan - - 2.5 2.3 10.5

HDFC STP - - 2.2 1.8 9.8

Dynamic Bond Funds - 5.0% IDFC Dynamic Bond Fund-Reg - 5.0% 15.9 8.7 7.8

SBI Dynamic Bond - - 17.5 8.5 7.8

UTI Dynamic Bond Fund-Reg - - 14.8 7.2 8.1

Income Funds - - DWS Premier Bond Fund - - 1.8 1.5 8.0

HDFC Income Fund - - 16.4 8.1 8.0

UTI Bond Fund - - 16.3 7.9 8.2

Gilt - - Debt Hybrid Funds - - DSPBR Dynamic Asset Allocation Fund - - - - -

Cash - - Liquid Funds - - Ultra Short Term - -

Gold 10.0% 5.0% Gold 10.0% 5.0% Total 100.0% 100.0%

90.0%

0.0%0.0%10.0%

Strategic Portfolio

Equity Debt Cash Gold

90.0%

5.0%

0.0% 5.0%Tactical Portfolio

Equity Debt Cash Gold

90.00

95.00

100.00

105.00

110.00

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5M

ay-1

5Ju

n-1

5Ju

l-1

5A

ug-

15

Sep

-15

Oct

-15

No

v-1

5D

ec-1

5

Aggressive Nifty

January 2016 21

Alpha Edge | “Why the delay?”

Thank you for your time!

Safe harbor statement!

This document has been prepared by Citadelle Asset Advisors Private Limited (CAAPL). CAAPL, its holding company and associate companies offer full range of, integrated investment banking, portfolio management and brokerage services, through own and or partnerships.

Our research analysts and sales persons provide important input into our investment advisory activities. This document does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data or other sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. CAAPL or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision.

The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors. We and our affiliates, group companies, officers, directors, and employees may: (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company (is) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as advisor or lender/borrower to such company (ies) or have other potential conflict of interest with respect to any recommendation and related information and opinions. This information is strictly confidential and is being furnished to you solely for your information.

This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject CAAPL and affiliates/ group companies to any registration or licensing requirements within such jurisdiction.

The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe, any such restrictions. The information given in this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. CAAPL reserves the right to make modifications and alterations to this statement as may be required from time to time. However, CAAPL is under no obligation to update or keep the information current. Nevertheless, CAAPL is committed to providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither CAAPL nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Past performance is not necessarily a guide to future performance.

The disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. CAAPL generally prohibits its analysts, persons reporting to analysts and their family members from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Any dispute arising out of the document shall be subject to the exclusive jurisdiction of the Courts in Mumbai, India