Alang - Ship Recycling Industries Association India A Green Re-Incarnation - March 2013.pdfAlang A...

36

Alang A Green Re-Incarnation Volume 1 Issue No 1 March 2013 Ship Recycling Industries Association (India) 206, Turning Point, 2 Floor, Waghawadi Road, Bhavnagar, Gujarat-364001 Tel: (0278) 2428696, 2439334, 3001853 www.sriaindia.com • E-mail: [email protected] To Make we may have to BREAK but in the END we CREATE

Transcript of Alang - Ship Recycling Industries Association India A Green Re-Incarnation - March 2013.pdfAlang A...

AlangA Green Re-Incarnation

Volume 1

Issue No 1

March 2013

Ship Recycling Industries Association (India)206, Turning Point, 2 Floor, Waghawadi Road, Bhavnagar, Gujarat-364001

Tel: (0278) 2428696, 2439334, 3001853

www.sriaindia.com •

��

E-mail: [email protected]

To Make

we may have to

BREAK

but in the

END

we

CREATE

Content

Editorial & Luminaries 1

Ship Recycling Industries Association (India) 2

Alang Ship Recycling Yard 6

Ship Breaking Industry 8

Trend Report 13

News and Updates 20

Annual Tradewind Conference 23

Beaching Report 25

Tide Time Table ( April / May / June - 2013 ) 29

Miscellaneous 27

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 131

Dear Readers,

It is a matter of pride and pleasure for me to introduce this business

magazine to the world. Many pundits/experts including media players have

frequently viewed Alang as the last destination of ageing ships, but much

against their views, the ship recycling yard Alang-Sosiya is not the graveyard

of ageing ships, but it is worthwhile naming this yard as the Re-incarnation

of these vessels. The end of life of these ships after recycling is converted

into buildings, bridges and other umpteen structures. Hence, this Magazine

is titled as “Alang- A Green Re-incarnation”

The Ship Recycling Industry is the only industry which contributes

production of steel to the extent of 4 Million Tones approximately without

replenishing the natural resources. However, this industry always remains at

the receiving end of the NGO's Environmentalists.

It is our humble effort, by launching this Magazine, to depict the true picture

of the industry.

The Industry largely contributes to the Indian Growth engine. The Magazine

showcases the contribution of the industry towards society and Nation by

way of employment generation, steel production and creating business

opportunities for SME sector.

The Ship Recycling Industry is a cyclic industry in nature and the economics

of the industry work totally in inverse proportion to the world economy viz,

any recession in the world economy is a blessing in disguise to this industry.

This Magazine provides an insight view on current and future trends of ship

recycling markets and its relations with world economy, freight indexes and

steel markets.

The ship recycling industry is very unique in its own way. It is a business for

some, bread earners to many and a punching bag for the NGO.

The association, on the completion of 30 Birth Anniversary of the industry,

grabs an opportunity to launch this Magazine to the world to unleash the

mysteries of ship recycling at Alang in India, which was once termed as the

“World's biggest Ship Recycling Yard”.

Welcome to the world of Ship Recycling

With thanks and warm regards,

��

Sukesh Aggarwal

Hon. Jt. Secretary

Ship Recycling Industries Association (India)

Editorial

Luminaries

of SRIA

Jivrajbhai Patel

President

Ramesh Mendpara

Vice President

V. B. Tayal

Vice President

Kapur Bansal

Hon. Treasurer

Nitin Kanakiya

Secretary

Haresh Parmar

Hon. Jt. Secretary

Nikhil Gupta

Hon. Jt. Secretary

Sukesh Aggarwal

Hon. Jt. Secretary

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

When ship breaking activity started in Alang at Bhavnagar, in India in 1983, ship breakers had their own way of

carrying the activities of ship breaking, with no organized framework of industry. But later with the growth of

industry it became essential to set up an organized structure with which ship recycling industry can perform in

more smooth and organized form.

Hence, Ship Recycling Industries Association was formed on 28th August 1983 and obtained its registration

under Non Trading Corporation. The Association safeguards the rights of its member ship recyclers and ensures

safe and eco-friendly recycling activity

Ship Recycling Industries Association (India) is an organization established for the welfare of ship recyclers'

activity in India. All the Plot Holders at Alang-Sosiya are members of the Ship Recycling Industries Association

(India). The Association represents the Industry at all levels of State, National and International Forums.

The Association is also a part of every district, state and national committee formed for better functioning of the

ship recycling yard.

• Industry extends financial assistance for the facilities and equipments of Red Cross hospital at Alang

• Fully equipped mobile hospital to handle emergencies, and free medical check-up for workers and their family

is provided by the industry.

• Medical camps for diagnosis and treatment of workers at the yard being organized by the association.

• Visiting team of IMO/ILO/Basel expressed their satisfaction over the improvements of safety and environment

that have taken place at Alang. They were not only impressed but astonished to see the actual picture of Alang.

• Regular safety training programs are conducted and audio-visual training is given to the workers.

• Health awareness camps are organized on regular basis.

• Safety Audit is conducted jointly by GMB and SRIA.

Labour welfare activities:

Ship Recycling Industries Association (India)

2

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Recently a capsule training program on “ was organized by SRIA

under the guidance of GMB and it was for short duration On the Job Training. The response from the

members as well as from the workers was overwhelming. This capsule training program has encouraged

SRIA to go for more such training programs in the days to come.

The participants in the training and the plot holders have been awarded certificates in token of active

participation by workers and appreciation to the members respectively.

Safe handling of Crane Operations”

Ship Recycling Industries Association (India)

3

Social welfare activities:

• Generous contributions to the hospitals and charitable

trusts in Bhavnagar.

• Contribution towards CM Relief Funds in the eventuality

of natural calamities.

• Provides funds to educational institutions and health

centre in Bhavnagar

• Handsome contributions towards PM'S RELIEF FUND

during Kargil war and Tsunami

• Rescue operations debris clearance during the Gujarat

Earthquake

• The construction of 4 primary schools in Kutch region is

fully sponsored by industry.

• Association also organizes and participates in the trade

fares.

• Set up Disaster Management Centre at Bhavnagar for

government

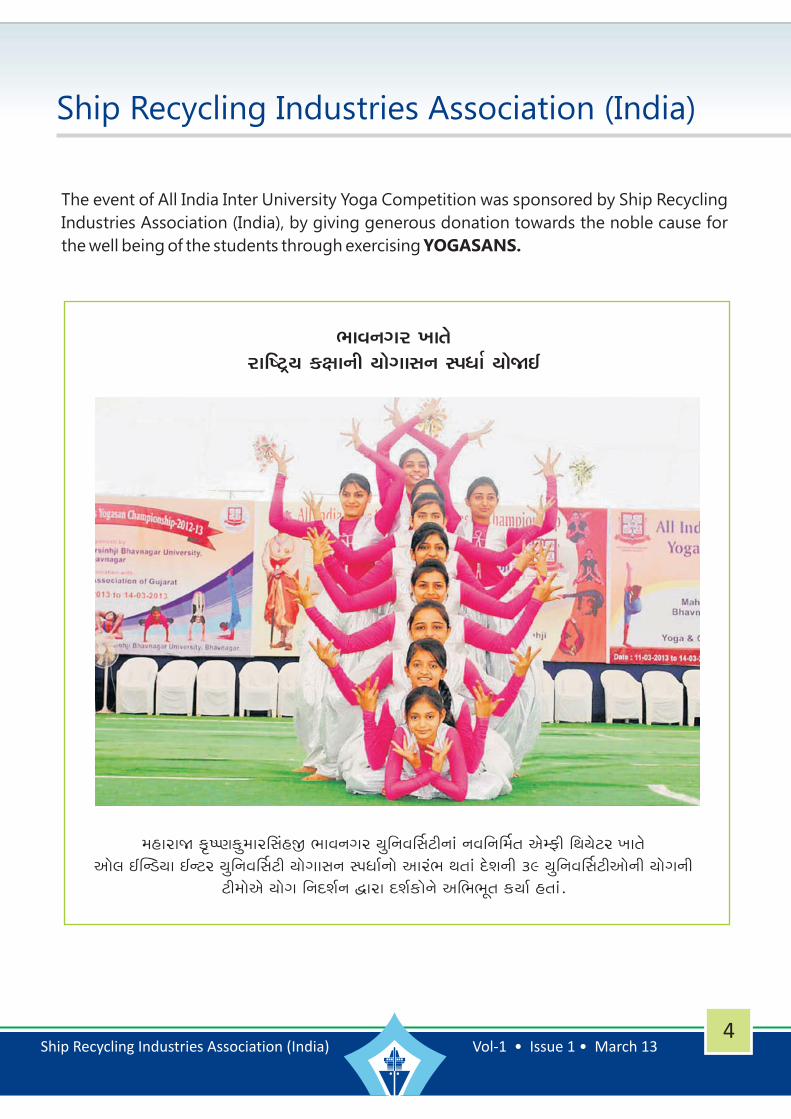

¼kðLkøkh ¾kíkuhkr»xÙÞ fûkkLke ÞkuøkkMkLk MÃkÄko ÞkuòE

{nkhkò f]»Ãýfw{kh®MknS ¼kðLkøkh ÞwrLkðŠMkxeLkkt LkðrLkŠ{ík yuBVe rÚkÞuxh ¾kíkuyku÷ EÂLzÞk ELxh ÞwrLkðŠMkxe ÞkuøkkMkLk MÃkÄkoLkku ykht¼ Úkíkkt ËuþLke 39 ÞwrLkðŠMkxeykuLke ÞkuøkLke

xe{kuyu Þkuøk rLkËþoLk îkhk ËþofkuLku yr¼¼qík fÞko níkkt.

The event of All India Inter University Yoga Competition was sponsored by Ship Recycling

Industries Association (India), by giving generous donation towards the noble cause for

the well being of the students through exercising YOGASANS.

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Ship Recycling Industries Association (India)

4

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 136

Alang has become a major worldwide centre for

ship breaking and considered as the largest ship

recycling yard in the world. To know more about the

history of ship recycling, we have to travel back to

the inception point.

The ships have always been valuable and even after

they being recycled, when they are not seaworthy.

World War II left huge amount of steel locked up

warships and cargo ships. These ships were when

scrapped, yielded in million tones of high quality of

steel. After the war was over the ship scrapping

continued and the Ship Building Industry shifted

eastwards in the 1970s, so did the scrapping

industry. Taiwan was the principal destination, until,

an explosion and fire on board near residentail area

killed and injured many lives. Due to a huge public

outcry the ship scrapping industry moved,

overnight.

Exactly in the same period, Alang, which is located

on Coast of Gulf of Cambay, on the West Coast of

India, experienced its first major growth spurt in

scrapping.

The first vessel – MV KOTA TENJONG was beached

at Alang on 13th Feb, 1983. Since then, the yard has

witnessed spectacular growth and has emerged as

a leading Ship Breaking Yard in the world.

Ever since its inception, Alang dominates the ship

breaking industry in India.

The ship recycling industry has during the year

2011-12 processed 415 ships amounting to 3.86

Million tones, the similar trend is likely to be

maintained this year also. This industry provides

direct employment to the tune of 50,000 workers

Alang Ship Recycling Yard

and indirect employment to lakhs of workers, by

way of rolling mills, scrap traders, oxygen gas plants,

transporters, real estate market and money market.

This industry produces 4 million tones of steel

without replenishing natural resources like, iron ore,

coal etc., in comparison to steel produced by

integrated steel plants. The ship recycling industry

is known as a green and eco-friendly industry.

The major producing centers for steel are situated

in eastern part of the country. Hence, the total

production of steel in the eastern part is not fully

demanded there at. Resultantly, the eastern part

has to stretch to the demand of western part of the

country. In order to resolve this situation the steel

generated from ship recycling activities is of

superior quality and is capable enough to meet the

demand of western part. Thus, the regional balance

of demand and supply of steel and transportation

cost will be resolved.

In the view of the above when the ship recycling

activity offers employment to lakhs of people

directly and indirectly and crores of rupees by way

of revenue to the ex-chequers of state and nation

as well, it is humble suggestion that the full

infrastructure and amenities should be accorded to,

by State Government and Central Government.

• High inter-tidal gradient and flat surface

enables the ship to beach right at the shore

during high tide and when the tide recedes

the ship stands almost at a dry-dock.

Since the beach consist of stones and hard clay,

the heavy items do not sink in the mud.

As Alang is sheltered from high velocity winds or

excessive humid conditions, ship recycling is a

perennial activity.

Larger ships can come straight in to the shore.

This reduces the total working time on each ship.

There is a layer of hard rock just beneath the

sand, thus danger of subsoil decontamination is

ruled out.

Geographical Features:

•

•

•

•

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 137

Alang Ship Recycling Yard

• One of the largest tidal ranges of over 11mtrs can take vessels of any draft.

Capacity of the plot at the yard :

Employment:

Ship breaking industry is Labour intensive, the survival of the ship breaking depends on the availability of

Labour and there is little scope of machinery.

Thus, Ship breakers need very little sunk capital or physical assets. The highest costs are the interest on

working capital and rent towards the beach area.

The industry generates 300 employment (Direct Labour) opportunities per plot in the ship breaking yard.

In terms of GMB policy of 2006, the efficiency of each plot is required to break at least 10000 LDT as per

revival package within the period of 5 years. However, a plot having 30 meters waterfront can recycle

approximately 25000-30000 tones in a year, whereas larger plots have comparatively higher tonnage

capacity.

J. R. GROUP OF INDUSTRIES

Bhavnagar Office : No. 201/202, B-Wing, Leela Efcee,Beside Aksharwadi Temple, Waghawadi Road,Bhavnagar - 364 002

Off. Phone No. :Off. Fax No. :

+ 91-278-2570210, 3005630+ 91-278-3005630

Works :

Phone : E-Mail :

Plot No. 38, Ship Recycling Yard, Alang,P. O. Manar - 364 150 (Gujarat)

+91-2842 -235254 gsbpl38@g,ail.com

GHAZIABAD SHIP BREAKERS PVT. LTD.(Ship Breaking) An ISO : 30000-2009 & Certified Company

J. R. CASTING(Casting Plant) An ISO 9001-2008 Certified Company

IS : 1786

CM/L-3830966

IS : 2830

CM/L-3787485

IS : 2062

CM/L-3809267

IS : 2830

CM/L-3787485

J. R. STEEL INDUSTRIES(Rolling Mil) ISO 9001-2008

J. R. ISPAT PVT. LTD.(Steel Plant) An ISO 9001-2008 Certified Company

Managing DirectorDirector

Shri T. L. GuptaShri Raman Gupta

+91 - 9825205580+91 - 9825205630

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

The ship breaking Industry is dominated by South Asia particularly India, Bangladesh and Pakistan. In the

year 2011, according to the latest available statistic, India, Bangladesh and Pakistan together accounts to

67% of the global ship recycling market in terms of LDT broken. Apart from this, significant recycling activity

also takes place in China which is 21%, while Turkey and other countries account for the balance 12% of the

market. In comparison with Western countries, Asian countries dominate the ship breaking activity mainly

because of factors like low manpower cost and relatively less stringent environment and health regulation.

Further, India, Bangladesh and Pakistan have become the preferred ship dismantling destinations by virtue

of their naturally favorable tidal conditions that enabled to use the beaching techniques for ship breaking

which is less capital intensive and hence more cost effective compared to the advanced dry dock method.

Ship Breaking Industry

9

In India, ship breaking yards are present in Gujarat, Maharashtra and West Bengal. However, majority of the

ship breaking activity is concentrated in the Alang and Sosiya yards in Gujarat with Alang alone accounting

for more than 90% of the ships dismantled in India. The ship breaking industry in India was present only in a

very limited form till the early 1990s with about 72 plots existing at Alang. However, post liberalization in

1991, the ship breaking industry started growing rapidly following the increased domestic steel

requirements particularly from the large number of rolling mills that were set up at the same time. The

Gujarat Maritime Board (GMB) issued a large number of licenses for plots and as per estimates there are

currently close to 140 plots for use as ship recycling facilities having a maximum capacity of about 4.58

million tones per year of steel scrap production (Source: GMB). The volume and number of ships dismantled

has been on an increasing trend and in FY 2011-12, 415 ships were dismantled in India.

The supply of old ships for

recycling is inversely correlated to the freight rate of shipping vessels which in turn is a function of the global

demand for seaborne transport and supply of new vessels. This is in contrast to the performance of the ship

building industry which is directly correlated with the freight rates. Driven by increased demand for maritime

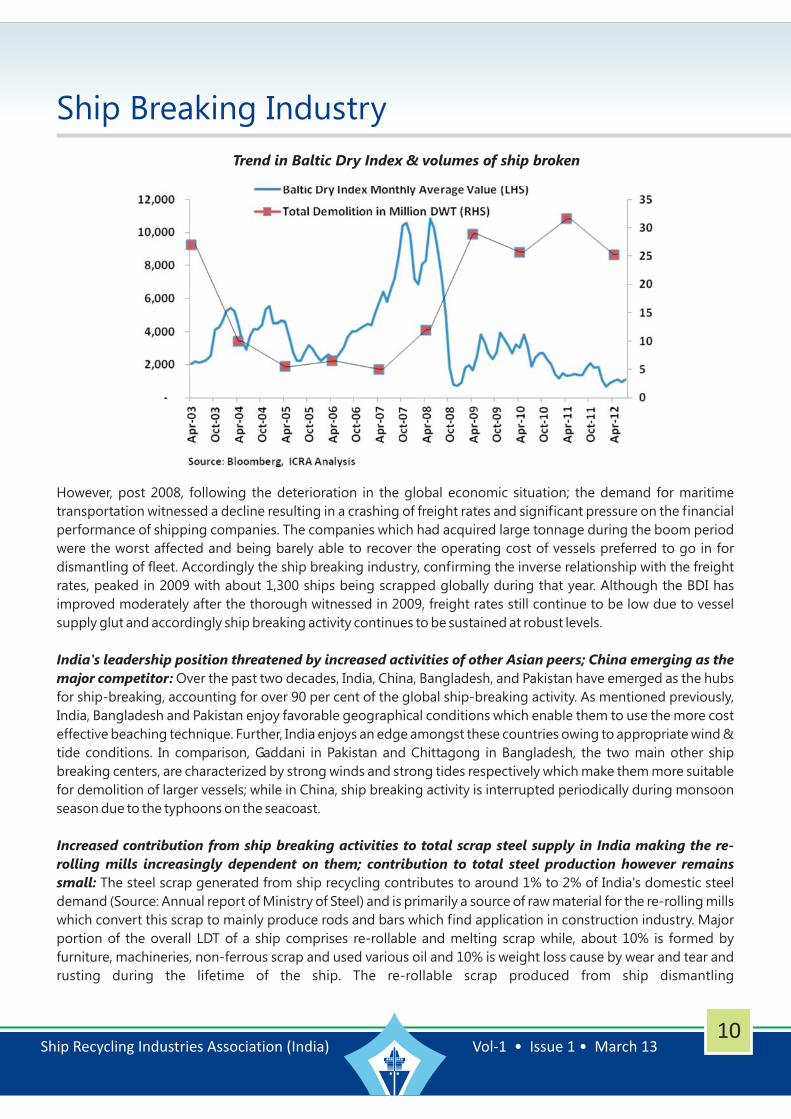

transportation, the freight rates, as reflected by the Baltic Dry Index (BDI), reached a peak value of 11,793 in

May 2008. In order to cater to this strong demand, even older ships were kept into operations resulting in

higher average operating life and the orders for new ships also witnessed an increment. The result was a drop

in the number of vessels scrapped globally to around 500 to 800 ships per annum from a historical average of

1000 to 1100 ships per annum.

Demand for ship dismantling inversely correlated to freight rates; Challenging market conditions for

the ship-owners has resulted in significant increase in tonnage dismantled :

Ship Recycling Market share in LDT

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1310

Ship Breaking Industry

However, post 2008, following the deterioration in the global economic situation; the demand for maritime

transportation witnessed a decline resulting in a crashing of freight rates and significant pressure on the financial

performance of shipping companies. The companies which had acquired large tonnage during the boom period

were the worst affected and being barely able to recover the operating cost of vessels preferred to go in for

dismantling of fleet. Accordingly the ship breaking industry, confirming the inverse relationship with the freight

rates, peaked in 2009 with about 1,300 ships being scrapped globally during that year. Although the BDI has

improved moderately after the thorough witnessed in 2009, freight rates still continue to be low due to vessel

supply glut and accordingly ship breaking activity continues to be sustained at robust levels.

Over the past two decades, India, China, Bangladesh, and Pakistan have emerged as the hubs

for ship-breaking, accounting for over 90 per cent of the global ship-breaking activity. As mentioned previously,

India, Bangladesh and Pakistan enjoy favorable geographical conditions which enable them to use the more cost

effective beaching technique. Further, India enjoys an edge amongst these countries owing to appropriate wind &

tide conditions. In comparison, Gaddani in Pakistan and Chittagong in Bangladesh, the two main other ship

breaking centers, are characterized by strong winds and strong tides respectively which make them more suitable

for demolition of larger vessels; while in China, ship breaking activity is interrupted periodically during monsoon

season due to the typhoons on the seacoast.

The steel scrap generated from ship recycling contributes to around 1% to 2% of India's domestic steel

demand (Source: Annual report of Ministry of Steel) and is primarily a source of raw material for the re-rolling mills

which convert this scrap to mainly produce rods and bars which find application in construction industry. Major

portion of the overall LDT of a ship comprises re-rollable and melting scrap while, about 10% is formed by

furniture, machineries, non-ferrous scrap and used various oil and 10% is weight loss cause by wear and tear and

rusting during the lifetime of the ship. The re-rollable scrap produced from ship dismantling

India's leadership position threatened by increased activities of other Asian peers; China emerging as the

major competitor:

Increased contribution from ship breaking activities to total scrap steel supply in India making the re-

rolling mills increasingly dependent on them; contribution to total steel production however remains

small:

Trend in Baltic Dry Index & volumes of ship broken

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1311

Ship Breaking Industry

is of a superior quality in comparison to other sources as ships are manufactured under strict specifications

and continuous monitoring and with material having better yield strength, ductility and impact strength in

order to withstand continuous strain, pressure and impact, and to that extent is preferred as a raw material by

the rolling mills.

Increase in purchase prices as a result of decline in INR expected to impact both profitability as well as

volumes; gain in INR necessary for sustainability of the ship breaking business: As steel content forms the

majority of the value of the ship, the international steel prices play an important role in determining the

prices of the ships to be scrapped. The vessel purchase transaction is typically denominated in USD and is

generally backed by 90-180 days of letter of credit. On the other hand, the sale of scrap is typically in the

domestic market with realizations being denominated in INR. Consequently, Indian ship breaking players

remain exposed to any adverse forex movements more so as only a limited number out of these engage in

foreign exchange hedging.

The significant depreciation in INR (vis-a-vis USD) in the second half of the year 2011-12 has adversely

affected the ship breakers having purchase payments due during this period. The problem has been further

compounded by the fact that the prices of steel in the Indian market have not moved in synchronization with

INR depreciation resulting in an inability of the ship breakers to pass on their increased procurement costs to

their customers thereby resulting in a squeeze on profitability. The high volatility in USD-INR has also

resulted in a cautious approach by the ship breakers with many of them deferring new purchases. The

sustenance of INR at present weak levels or further deterioration and volatility, will create significant stress

on the credit profiles of ship breaking players due to its adverse impact on both volume of business as well as

profitability. Indian ship breaking companies have lost almost Rs 800-1000 crore during financial year 2011-

12 due to rupee depreciation against US dollar. According to the industry, weak rupee converted profits into

losses, mainly after October 2011 period (Source: Business Standard, Apr 04, 2012 at 00:16).

(Source: ICRA Rating Feature, Ship Breaking Industry: Key Trends and Credit Implications)

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1312

Ship Breaking Industry

Speed breakers in the growth of ship breaking industry at Alang :

Norms of Bureau of Indian Standard (BIS):

GMB Policy:

In terms of the provision of WTO the BIS is applicable to finished

goods only. As against this, the steel generated from ship recycling industry is termed as raw material for

rolling mills and therefore this raw material should be out of the purview of BIS standard as this steel is of

superior quality.

With the re-introduction of long term policy by GMB for renewal of permission to ship breaking

plots will relieve the ship breakers from the tension of getting the plots renewed frequently. This will facilitate

the consistency and will increase the efficiency of the plots.

B M Eco Waste Management Pvt. Ltd.Friends Corporation

With Best Compliments

Office :

302, 3rd Floor, 'Sarthik'

1874-C, Atabhai Avenue, Atabhai Chowk

Bhavnagar - 364 002

Units :

Survey No. 85 Paiky 1, Block No. 20

Opp. Plot No. 88, Behind Alang,

Dist. Bhavnagar

Suppliers of All Types of Scrap Processors

and Bundlers

M/s. Baijnath Melaram Concern

Website : www.baijnathmelaram.com

mail ID : [email protected]

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1313

Consequent upon the downturn of the global shipping and weak macro-economic headwinds since

2009,the growth of the ship breaking industry has been boosted and India, having its natural geographical

advantage of a higher inter-tidal gradient, favorable weather conditions and low manpower costs has come

out as a leader in terms of both volume and number of ships broken. With the view on international shipping

freight rates being controlled over the near to medium term and large tonnage is expected to be booked in

post 2012, the ship breaking industry is expected to continue witnessing a steady supply of vessels for

demolition over the medium term. Significant improvement in the global economic scenario resulting in a

pick-up in freight rates could present a downside for the ship breaking industry. However, the pace of any

such positive development is likely to be moderate and to that extent the supply risk appears to be limited

over the near to medium term. At the same time, any further deterioration in the macroeconomic scenario

and shipping freight rates could provide additional boost to the volume of ships available for dismantling.

The ship breaking industry is dominated by a few Asian countries namely India, Bangladesh, Pakistan and

China owing to certain natural, regulatory and cost advantages. The competitive intensity in the business is

high owing to low entry barriers with respect to capital and technical intensity. Some of the key factors which

determine the relative competitiveness of ship breaking activity in various countries include the government

policies/regulations with respect to environment and human health hazards of ship breaking, import duty

structure, currency movements and local steel demand.

The Indian ship breakers have witnessed a healthy growth in operating income in recent years due to

increased availability of ships for dismantling. Profitability margins in the business are inherently thin due to

the low value additive and highly competitive nature of business and have come under further pressure in

the recent past owing to steep rupee depreciation which has increased the cost of purchase of ships coupled

with decline in realizations of the end product, i.e. steel melting scrap, due to slowdown in steel consuming

sectors.

Any further depreciation in INR, decline in steel prices or increase in interest costs would be some of the key

downside sensitivities affecting the business and financial risk profile of the Indian ship breakers. Indian ship

breakers have a high reliance on non-fund based facilities like import letter of credit (LC) which are used for

funding the purchase of ships. In comparison, their fund based facilities are rather limited which exposes

them to a risk of liquidity crisis in case of significant delays in the ship breaking process which may take place

at the approval level, before beaching or during demolition. (Source: www.ICRA.in, Ship Breaking Industry:

Key Trends and Credit Implications)

In a report published in late 2012: 'India makes history in terms of maximum number of ships beached this

year, with 527 vessels making an average of 1.4 ships beached per day. With 5.2 million tonnes being recycled

from ships, ship recycling in India contributed to 9% of total steel manufactured in India.'

Though optimism characterized the sector in Bangladesh towards the end of last year, more movements and

bigger vessels are expected to be continue, remarks Star Matrix. And it adds that China's demolition market

'has again geared up with a little influx in price' - a development which subsequently 'opened doors' for ship

owners to benefit from competitive offers from markets in India, Pakistan and Bangladesh, as well as China.

The demolition experts have also shared a theory as to why ships in the 1000 to 6500 ldt range generally

command lower rates, arguing that they typically make their end-of-life voyage to Mumbai ship recycling

yards, resulting in a complete change in ship breaking estimations and costing.

Trend Report

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1314

Trend Report

As opposed to the Alang yards, Mumbai boasts some 12-15 breaking plots which are all operated on a rental

basis, thus putting breakers 'at the mercy of Mumbai Port Trust for the permissions and the approvals of

breaking a particular ship'. Mumbai has been breaking some 60 small ships a year, according to Star Matrix.

(Source: Hellenic Shipping News Worldwide.)

With the announcement of budget, implementation of new taxes and instability undermining fundamentals

across the Indian sub-continent has created an attention grabbing situation for all the business fronts.

Consequent to fluctuation, in local market together with the chronic oversupply, created challenging

situation of instability for the previously bullish end buyers of China. In this context, the industry players

decided to convene the annual Tradewinds recycling conference in Dubai, to cover the turbulent events of

the year to be a hot topic of debate.

India being the largest recycling destination, where the much anticipated budget was announced, has

remained central to sentiments across the sub-continent. Resultantly, there were few overall material

changes to affect the recycling industry. As it remains, if it's not local steel plate prices causing suffering on

the Indian shorefront, the currency is sure to play its role to the despair of local buyers!

News of 5% tax hike on new vessels to be imported for recycling came as a biggest shock for the Pakistan.

With this sudden shocking news buyers across the board at Gadani have decided to put a halt on buying

activities for the time being until the fine print has been read and all is fully understood regarding the

potential new payments/taxes. Bangladesh, facing the traumatic situation of riots, strikes and unfortunate

deaths after the announcement, that an Islamist party leader was sentenced to death. The whole country has

ground to a virtual standstill with police and rioters reportedly clashing.

China experienced some worrying signs of decline as many end buyers chose simply not to offer following

the recent binge on units there and sentiment stuttered for the first time this year. Finally, as Turkey continues

its encouraging start to the year, a few more sales come to light.

Global Scenario

DemoRanking

Country MarketSentiment

GEN CargoPrices

TankerPrices

1

2

3

4

Bangladesh

Pakistan

India

China

Cautious

Cautious

Weak

Cautious

USD 400/lt ldt.

USD 390/lt ldt.

USD 385/lt ldt.

USD 375/lt ldt.

USD 425/lt ldt.

USD 420/lt ldt.

USD 420/lt ldt.

USD 400/lt ldt.

GMS demo rankings for the week are as below:

(Source: GSM Weekly March 01, 2013, Volume 128, Issue 557, Week 09)

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1315

Trend Report

Domestic Market

Indian steel demand to grow by 6.7pct till FY17 - CARE Research (Source Steelrates.com)

• According to a report on steel industry by Credit Analysis & Research Limited, domestic steel demand is

likely to grow by 6.7% annually till 2016-17, faster than the expected growth in Chinese demand during

the same period.

• Domestic steel capacity increased at a compound annual growth rate (CAGR) of 8% in 2004-05 to 2011-

12. In line with the domestic steel capacity, steel production in the domestic market also recorded a

similar increase during the same period.

• However, in near terms, the domestic steel industry would remain in a deficit state for the next 2 years.

· Increase in the demand is likely to be offset by the rise in supply of the metal, thereby, keeping the

domestic demand stable in the near term.

• CARE said that the demand for flat products in the domestic market is likely to be supported by the

automobiles and the pipe manufacturing sector, although at a timid pace, demand for long products will

continue to increase on the back of modest growth in demand from the construction sector.

• The global supply of steel is expected to continue to adjust itself with the change in demand.

• The global steel industry witnessed a rather structural shift in its consumption pattern as the demand for

steel in the European Union and the US failed to reach the consumption levels it achieved in calendar year

2001.

However, steel appetite from the emerging economies like China and India increased significantly.

Globally, steel production is likely to increase at a CAGR of around 2 per cent during CY11 to CY14.

Domestic Scrap prices as on date: 13-03-2013

MANDI GOBINDGARH

RAIPUR

DURGAPUR

HYDERABAD

MUMBAI

CHENNAI

KOLKATA

LUDHIANA

ALANG

KANDLA

JAMSHEDPUR

JALNA

BHIWADI

COIMBATORE

VIZAG

29700-800#

24400-500++

27400#

23800++

22500++

23300-500++

26900#

-

23500++

22900++

28700-800#

26800#

26500#

21500-22++

22500-23++

31700-800#

25400-500++

27900#

25000++

23000++

24300-500++

27400#

30500#

-

-

29700-800#

27400#

-

-

23500-24++

-

-

-

-

-

-

-

-

+ 200

+ 200

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

PlacePrize / Size

HMS 80:20 Change End Cutting Change

++Basic Price,ED & Taxes extra *Payment Next Day # Including all

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1316

Trend ReportBhavnagar prices as on date: 13-03-2013

Size Prize

2-5 KG

1-2 KG

12 ANE(19-22MM)

1 INCH

10 ANE(15-18MM)

8 ANE(12-14MM)

4 ANE(6-8MM)

6 ANE(9-11MM)

5-10 KG

ALANG SCRAP

24000

23700

25500-600

25800

25200-300

24800

23400

24200

24700

23400

(Source: SteelMint 13/03/2013)

Steel outlook:

Stable Outlook for 2013:

Moderate Demand Growth:

Modest Margins:

High Interest Cost:

India Ratings, which is a group firm of global rating agency Fitch, expects credit

profiles of its rated steel producers to remain stable in 2013, driven by continued albeit slow growth in

domestic steel demand. The majorities (92%) of ratings are on Stable Outlooks and most of them are below

'IND BBB-', which reflects the inherent risks in the steel sector.

(National Long-Term Issuer rating of 'BBB-(ind)' (BBB minus (ind)) to the company. The Outlook is Stable.)

World Steel Association has forecasted steel consumption in India to grow at

5% in 2013. Steel producers may see a spurt in demand in the medium-term if the Indian government

implements its USD 1 trillion infrastructure investment plan in a timely manner. The demand for flat steel

from automobile, white goods and capital goods sectors is likely to remain modest in 2013, given the

continued slow economic growth.

Though Indian steel producers

increased prices by INR500-INR1,000 per tonne in

December 2012, India Ratings expects profit margins in

2013 to remain broadly similar to 2012 levels. This is due

to the persistent high cost of steel production and steel

producers' limited ability to pass on higher costs due to

subdued demand from end-user industries. The margin

pressure will be higher on the producers with no captive

raw material linkages.

The cost of funding working-capital

requirements has remained high despite the marginal reduction in repo rate by the Reserve Bank of India

(RBI) in early 2012. India Ratings expects a gradual reduction in the interest rate in 2013 which should provide

some relief in interest cost. While higher-rated issuers invariably have access to bank funding and capital

markets in certain cases, most issuers in the 'IND A' (a strong credit risk relative to other issuers or issues in

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1317

Trend Report

the country)and below categories rely largely on bank financing and are severely affected by high interest

costs.

Considering the modest demand scenario, a further rupee

depreciation could pressurize the margins of companies producing flat steel through blast furnace route as

bulk of coking coal is imported. This is despite import price parity of flat steel products. Moreover, a weaker

rupee raises the financial leverage of steel producers with significant un-hedged foreign-currency liabilities

resulting in a decrease in financial flexibility. However, the agency expects financial leverage of rated entities

to remain within the guidelines stipulated for the respective rating category.

A negative outlook may arise from continued weak macroeconomic environment in India

which could adversely affect financial and liquidity profiles of issuers beyond that expected by the agency.

Positive rating changes are unlikely in 2013, with India Ratings being more likely to take rating actions on a

company-basis rather than on the sector as a whole.

The demand for steel from automobile, white goods and capital goods will remain

muted throughout 2013, given the continued slowdown of Indian economy. Any prolonged deferral of

corporate capex due to prevailing high interest rate could further impede growth in steel demand. India

Ratings expects RBI to reduce interest rates gradually in 2013 and the magnitude of reduction will determine

the extent of demand revival from end user industries. Also, Indian government's plan to invest USD 1 trillion

in the infrastructure sector could boost demand for steel, provided it is implemented on time. Domestic steel

consumption grew by a modest 5.3% yoy over January-November 2012 due to headwinds from the

unfavorable macroeconomic environment. During the same period, imports grew by 24.8% yoy to 7mt, while

exports increased 15.4% yoy to 4.3mt.

Rupee Depreciation, Mixed Impact:

Factors leading change in the outlook:

Global Recession:

Moderate Demand:

Demand-Supply Trend of Steel

Modest Increase in Steel Prices: India Ratings expects steel prices to show modest recovery in 2013 due to

the cost-push effect. The ability to raise steel prices in the Indian market is also limited by the global nature of

the market, coupled with oversupply and weak demand in the international market. Imports, though

contained to an extent by rupee depreciation, have already touched an all-time high of 10% of the total

production in 2012. Moreover, Indian government's free trade agreements with Japan and South Korea,

under which these countries are eligible for lower custom duties, are resulting in an increase in imports of

steel from these countries, thus further pressurizing the domestic steel prices.

Source: India Ratings, Joint Plant Committee (JPC)

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1318

Trend Report

Overcapacity Risk:

Steel Industry in India:

The domestic steel industry could face the risk of overcapacity in the Medium-to-long-

term as Indian steelmaking capacity is slated to cross 100mt in 2013, which could pressure steel prices.

However, given the expected shortage of iron ore in 2013 due to iron ore mining mess, most steelmakers who

depend on external mines for their iron-ore requirement may not run on full capacity thus limiting the

overcapacity concern. Also, the delay in greenfield capacity additions, due to regulatory hurdles such as land

acquisitions and the rehabilitation of settlements, will continue to mitigate some of the overcapacity

concerns.

(Sources: India Ratings & Research, 2013 Outlook: Indian Steel Producers)

India improved its ranking to become the 4th largest producer of crude steel in the

world during 2011 after China, Japan and the USA. The country's production grew by around 6% in 2011 over

2010. India's rank in the world order of steel production remained unchanged at fourth slot with an output of

76.7 million tonnes, despite logging the highest growth of 4.3 per cent among major producing nations in

2012.The trend of crude steel production in India is shown in the following table:

India's position in Global Steel Market

(http://www.worldsteel.org/media-centre/press-releases/2012/12-2012-crude-steel.html)

Rank Country 2012

1

2

3

4

5

6

7

8

9

10

China

Japan

United States

India

Russia

South Korea

Germany

Turkey

Brazil

Ukraine

2011

716.5

107.2

88.6

76.7

70.6

69.3

42.7

35.9

34.7

32.9

694.8

107.6

86.4

73.6

68.9

68.5

44.3

34.1

35.2

35.3

2012 /2011(%)

3.1

-0.3

2.5

4.3

2.5

1.2

-3.7

5.2

-1.5

-6.9

Top 10 steel exporting countries in ASIA: Top 10 steel importing countries in ASIA:

Rank Exporters milliontonnes

2010 2011

%Change

1

2

3

4

5

6

7

8

9

10

China

Japam

Soth Korea

Taiwan

Malaysia

Singapore

Thailand

Hond Kong

Indonesia

Other

India*

38.8

42.4

23.9

9.8

6.2

2.0

1.7

1.6

1.4

1.2

1.0

44.4

40.3

28.0

10.3

2.5

2.1

1.4

1.2

1.2

1.4

9.3

15

17

5

50

23

22

0

40

-5

-13

-13

Total 129.8 142.0 9

Rank Exporters milliontonnes

2010 2011

%Change

1

2

3

4

5

6

7

8

9

10

South Korea

China

Thailand

Indonesai

Taiwan

Singapore

Japan

Malaysia

Other

India*

Vietnam**

24.3

16.8

12.1

7.3

9.3

9.0

8.3

4.0

4.1

5.0

12.7

22.3

15.9

12.3

8.3

7.7

7.3

5.2

5.1

4.8

12.9

8.2

-8

-5

-12

-15

-12

-3

2

14

29

26

2

Total 112.8 110.1 -2

* estimated data * estimate** Exports from

Sources:http://www.issb.co.uk/index.html

RAJENDRA

Office : DM-79, Kalvibid, Behind Ram Mantra Mandir,

Near O.B.C. Bank, Bhavnagar - 364 002

Ph. : 0278-2566033, 2566041 • Fax : 0278-2567861

E-mail : [email protected]

SHIP BREAKERS PVT. LTD.

Contact Person

Mr. Rajendra Gupta : +919825205356

Mr. Devesh Gupta : +919825708196

Works : Plot No. 114 & V-9, Sosiya Ship Recycling Yard,

Sosiya, Alang, Dist. Bhavnagar - 364 120

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

India's 5-yr steel output 2nd highest in the world :

China's production grew by 39% during 2008-2012, the latest World Steel

Association (WSA) data has revealed.

GMB approves extra land for private hospital in Alang

(Press Trust of India / New Delhi Jan 25, 2013, 16:54 IST, Source: Business

Standard)

India's 33% growth in steel production in the last five years was second only to

China among the top-five producing nations. China's production grew by 39%

during 2008-2012, the latest World Steel Association (WSA) data has revealed.

• India's production grew constantly in the last five years from 57.8 MT in 2008 to 63.5 MT in 2009, 69 MT in

2010, 73.6 MT in 2011 and 76.7 MT in 2012,

• China, which produces nearly half of world's steel, had output of 512.3 MT in 2008, 577.1 MT in 2009,

638.7 MT in 2010, 694.8 MT in 2011 and 716.5 MT in 2012.

• World's steel production grew to 1,548 MT in 2012, up from 1,341 MT in 2008, recording a growth of

15%.

• Russia, which holds the fifth rank in the world order of steel production in 2012, had clocked a mere

three% growth in output during the last five years.

• In 2008, it had produced 68.5 MT and in 2012, it stood at 70.6 MT.

• Japan and the US, which occupy the second and third ranks respectively since 2010, have, in fact,

produced less steel in 2012 than what they had produced in 2008.

• Japan's production fell to 107.2 MT in 2012 from 118.7 MT in 2008. Similarly, production in the US

slipped to 88.6 MT in 2012 from 91.4 MT, the WSA data revealed.

• India is projected to grab the second slot in the world of steel production within a year or two on new

capacity expansions, mainly through the brown field route.

• The government expects the country's installed steel production capacity to go up to 200 MT by 2020

from around 90 MT now.

(BS Reporter / Mumbai/ Ahmedabad Jan 30, 2013, 00:11 IST, Source: Business Standard)

The Gujarat Maritime Board (GMB) has approved extra land for private hospital in world's largest ship

breaking yard Alang, with an aim to provide better health care facilities to the workers and their families.

The board is also mulling to build a trust-run hospital and housing facility for workers employed in the yard,

said Pankaj Kumar, VC & CEO, GMB on Tuesday, while dedicating 108 ambulance service at the Alang-Sosiya

Shipbreaking Yard in Bhavnagar district. "Approval has been given for provision of extra space for a private

hospital at Alang. A trust hospital at Alang and housing facility for the workers is also being looked into,"

Kumar said. He further added that Alang aims to retaining its top position of the largest ship recycling yard in

the world and it could also become a tourism centre of Gujarat.

News and Updates

20

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

News and Updates

21

GMB has taken adequate steps to provide safety for all workers. Healthcare facilities are being provided by

Indian Red Cross Society for which financial assistance is provided by GMB to the tune of Rs 12 lacs every year.

Alang-Sosiya ship breaking yard is one of the largest ship recycling yards in the world with 130 operational

plots employing over 40,000 workers. Till date, nearly 6000 vessels have been beached at Alang and over 43

million LDT (light displacement tonnage) has been recycled there.

The yard provides employment to various categories of labourers in specialized and specific jobs such as

crane operators, gas cutters, welders, oil removers, hauling and breaking and metal movers.

108 ambulance service dedicated at Alang yard. GMB, with support of Health Department of Government of

Gujarat has dedicated the 108 ambulance service as a special care facility for the workers and their families at

Alang Ship breaking Yard in association with GVK EMRI on Tuesday. Entire capital and operating expenditure

would be borne by GMB. An ambulance station and parking area, along with residential accommodation for

staff of the ambulance is also being provided by GMB.

(BS Reporter / Mumbai/ Ahmedabad Jan 17, 2013, 00:13 IST, Source: Business Standard)

Gujarat Finance Minister Nitinbhai Patel on 16/01/2013 strongly demanded that Government of India

should consider waiver of custom duty on import of ships being brought for breaking and bring it at par with

import of melting scrap.

(BS Reporter / Mumbai/ Ahmedabad Apr 09, 2012, 00:06, Source: Business Standard)

Ship breaking yard at Alang, Asia's largest, has recorded highest number of 415 ships coming for breaking

during fiscal ended March 31, 2012 with the 38.60 million tonnes of light ton displacement or LDT against

28.20 million tonnes LDT recorded in 2010-11, GMB informed in an official statement.

Gujarat demands waiver of custom duty on ship breaking :

Alang yard dismantles record ships in 2011-12 :

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

A Safety Week

22

A safety week commencing from 04/03/2013 to 09/03/2013, was celebrated by Gujarat Maritime Board

Alang under the guidance of Shri Sudhir Chaddha, Port Officer- Alang. The programme was well received

by the workers of all the plots. The various activities viz, essay competition, poem competition relating to

safety were undertaken during this week.

In one of these competitions, the first price for poem was awarded to the worker of Plot no. 128.

And the Poem goes like:

����� ������ ���� �

H¢ïx¢ Ü ã¼ï ãï çÜ ¶¼ÚÝ¢Ü ²ï Îéçݲ¢ ãñ Ï¢Çè JçÜ ¼ïH ТÝè ± Á¢ã¢Á¢¢ï S¢ï´ çÍ¢Úè ²ï Îéçݲ¢ ãï Á¢¢ïç¶}¢ |¢Úè JJ

ÐÚ }¢éÁ¢ï çÜ S¢è ÐíÜ ¢Ú Ü ¢ ÇÚ Ýãè J}¢ïÚè S¢ÚÜ ¢Ú Ü ¢ ¼ÚèÜ ¢ ãñ ϢǢ S¢ãè JJ

H¢¶¢ï´ S¢éç±{¢»´ Îï Ü Ú ©‹ã¢ïÝï Ϣݢ Ç¢Hè J§S¢ ¥Ý¢ï¶è Îéçݲ¢ Ü ¢ï´ S¢éÚÿ¢¢ ±¢Hè JJ

ã}¢¢Úè ¥Hæx¢ Á¢è.¥ï}¢.Ï¢è. Ü è ±¢¼ ãè Üé À çÝÚ¢Hè ãñ JãïË}¢ïÅ, Ó¢à}¢ï´ Üï Ï¢x¢ñÚ Ü ¢}¢ Ü ÚÝï ÐÚ Ð¢Ï¢‹{è ãñ JJ

²ã¢ Ü ¢}¢ Ü ÚÝï Ü è ã}¢ï Îè Á¢¢¼è ãñ ÅîïôÝx¢ ÐêÚè JãÚ ±¢ï Ü Î}¢ ©Æ¢²¢ Á¢¢¼¢ ãñ, Á¢¢ï ãñ ã}¢¢Úè Úÿ¢¢ Üï çH» Á¢LÚè JJ

S¢È ¢§ü Ü ¢ Ú¶¢ Á¢¢¼¢ ãñ ²ã¢ ¶¢S¢ Š²¢Ý JÓ¢¢ãï´ ã¢ï ±¢ï ã±¢, S¢}¢éÎí ²¢ ã}¢¢Úï }¢Ü ¢Ý JJ

Á¢x¢ã Á¢x¢ã ²ã¢ ¶Çï´ ãñ Ç¢vÅÚ ¥¢ñÚ Ü }¢üÓ¢¢Úè J¶Çï ãñ HïÜ Ú ãæ}¢ïࢢ S±¢S‰² Ü è çÁ¢}}¢ï΢Úè JJ

}¢ñ §S¢ Îéçݲ¢ }¢ï´ S¢éÚçÿ¢¼ ãêæ J²ï }¢ïÚï Á¢ã¢Á¢¢ï´ Ü è Îéçݲ¢, ²ï }¢ïÚè ¥Ý¢ï¶è Îéçݲ¢

�� ����� ������ �� �� ��

News and Updates

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Annual Tradewind Conference

23

Annual Tradewinds recycling conference was held in Dubai on 05/03/2013, to cover the turbulent

events of the year in regard to Ship Recycling activities. SRIA had actively participated

in the said conference. The due coverage of the conference was published in local dailies.

Plot No. 2299, 'Prithvi Vallabh', Hill Drive, Bhavnagar

Plot No. 30, Ship Recycling Yard, Alang,

www.jrdindustries.co.in

With Best ComplimentsISO 30000-2009

BUREAU VERITAS

Certification

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 1325

Beaching Report

Plot Vessel Name Type Arrival Beaching

121

018

025

V-1

Csl Marie

Alma Ata

Henry

Marlin

Container

Bulk Carrier

Container

Oil Tanker

17,654.02

15,583.00

14,158.00

14,910.00

08/02/13

25/02/13

26/02/13

28/02/13

01/03/13

01/03/13

01/03/13

04/03/13

LDT

TOTAL : LDT – 62,305.02 MT / VESSELS – 04 (Four)

VESSELS AT ANCHORAGE ON: 09-03-2013

Sr. Vessel Name Arrived on Type Status

1

2

3

4

MED GREEN

SILVER STAR

HAYDER

POLONIO

18-Feb-13

06-Mar-13

08-Mar-13

08-Mar-13

7835.00

5486.00

11796.90

13282.00

Bulk Carrier

Bulk Carrier

Bulk Carrier

Container

Boarded

Boarded

Boarded

Waiting

LDT Boarded on

19-Feb-13

07-Mar-13

08-Mar-13

VESSELS BEACHED DURING THE HIGH TIDE

Sr.

1

2

3

4

5

6

Beached on

MSC NORMANDIE

MSC SENA

CSL MARIE

ALMA ATA

HENRY

MARLIN

21-Feb-13

23-Feb-13

07-Feb-13

25-Feb-13

26-Feb-13

28-Feb-13

9127.00

15137.00

17654.00

15583.00

14158.00

14910.00

Container

Container

Container

Bulk Carrier

Container

Tanker

22-Feb-13

24-Feb-13

09-Feb-13

25-Feb-13

27-Feb-13

28-Feb-13

1-Mar-13

1-Mar-13

1-Mar-13

1-Mar-13

1-Mar-13

4-Mar-13

��������� ����� ��� ������� ��� ��� ���� ����� �� � ���� ����� ����� �� ��� �� ���� ���

�� ���������� � ��������� �� ��� ������� �� ��� ����� �����������

Consolidated Beaching Report for the period from – 01 MARCH, 2013 to 08 MARCH, 2013:

(A ) VESSELS BEACHED FROM – 01 MARCH, 2013 to 08 MARCH, 2013:

�� ��

�� ��

Vessel Name Arrived on TypeLDT Boarded on

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Miscellaneous

27

Quotes:

• “If your ship doesn't come in,

swim out to meet it!”

• “A goal is a dream with a deadline.”

• “If you don't have a competitive advantage,

don't compete.”

• Change your thoughts and you change your

world. ~

Jonathan Winters

Napoleon Hill

Jack Welch

Norman Vincent Peale.

Knowledge Point

• Construction of Titanic began on 31 March 1909,

when her keel was laid. She was launched on 31

May 1911

• All the steel used in Titanic's hull had to be

imported.

• Titanic was 882ft 9in in length, 92 ft in width, 175

ft in height and it weighed 46,328 tonnes.

• There were only 3 funnels operational on the

Titanic. The fourth funnel was a dummy.

• The cost to build Titanic in 1912 was $7.5million.

The cost today is $400million.

• In 1912, skilled shipyard workers who built

Titanic earned £2 per week. Unskilled workers

earned £1 or less per week.

• An iceberg was reported 'dead ahead' at

11.40pm on the 14 April 1912.

• The Titanic sank at 2.20am on Monday 15 April –

2 hours and 40mins after hitting the iceberg.

• Many of the lifeboats were launched less than

half-full.

• Today, the Titanic lies approximately 12,460ft at

the bot tom of the At l an t i c Ocean

(approximately 2.5 miles)

Test your G. K. - Quiz Section

1. ICICI is the name of a

(A) Chemical industry (B) Bureau

(C) Corporation (D) Financial Institution

2. Gilt-edged market means

(A) Bullion Market

(B) Market of Government securities

(C) Market of guns (D) Market of pure metal

3. In the second nationalization of commercial banks, ___

banks were nationalized.

(A) 4 (B) 5

(C) 6 (D) 8

4. If the cash reserve ratio is lowered by the RBI, its impact

on credit creation will be to

(A) Increase it (B) Decrease it

(C) no impact (D) None of the above

5. As per the latest ICC Test Championship rankings issued

in Dubai on 17 December 2012, what is the position of

India?

(A) 2nd, (B) 5 ,

(C) 3 (D) 6th

6. Which Bollywood star was selected as jury member for

the Cannes Film Festival in 2003?

(A) Aishwarya Rai (B) Lara Dutta

(C) Priyanka Chopra (D) Rekha

7. Sachin Tendulkar has endorsed three brands of shoes.

The well-known ones are Adidas and Action. Which is the

third?

(A) Power (B) Puma

(C) Fila (D) Nike

8. Ghoomar is a dance form from—

(A) Jammu and Kashmir (B) Punjab

(C) Himachal Pradesh (D) Rajasthan

9. Ravan was also a skilled:

(A) Dancer (B) Musician

(C) Sculptor (D) Painter

10. Where was the first Indian Institute of Management (IIM)

established in 1961?

(A) Kolkata (B) Bengaluru

(C) Ahmedabad (D) Lucknow

th

rd

Answer:1) D 2)B 3)C 4)A 5)B 6)A 7)A 8)D 9)B 10)A

Your suggestions and ideas are invaluable as we seek to

produce subsequent issues of this magazine that

continues to inform and benefit our readers. Please

send your comments and/or questions about this

magazine to [email protected]

Disclaimer: All material that appears in this edition is printed at the discretion of the publishers, but does not necessarily reflect the opinions

of the publishers. We endeavor to maintain a high standard of credibility in the quality of articles published and our articles are intended as

informed contributions to people seeking to pursue a rich and rewarding experience in business. Readers are advised to always use their

discretion in using any product, service or approach either advertised or written about in this magazine. SRIA doesn't own any responsibility

in any capacity.

With Best Compliments

Works :

Plot No. 83, SBY, Alang

Tel. : 02842 - 235143

������� �����

��� ����

�� � � ��

�������

�� ��

������� ��

Works :

Plot No. 84-F, SBY, Alang

Tel. : 02842 - 235584

Office :

S/1, Jalaram Flat, Dery Road, Diamond Chowk, Bhavnagar.

Tel. : (O) 0278 - 2207577, 2567831 (R) 2202363

Mobile : 9825207733, 9426918323, 9825206323

Works : Plot No. 114 & V-9, Sosiya Ship Recycling Yard,

Sosiya, Alang, Dist. Bhavnagar - 364 120

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

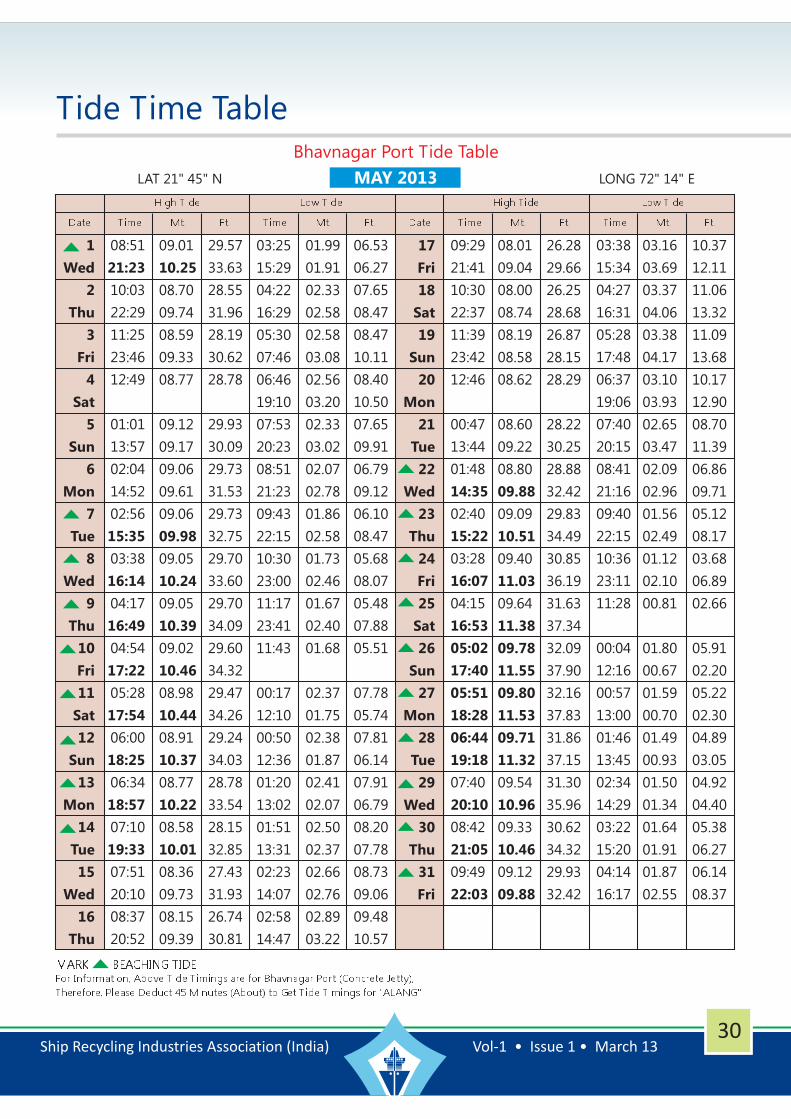

Tide Time Table

29

Bhavnagar Port Tide Table

���� ���� � ���� ���� ���� � ����

�� � ���� � � � � ���� � � � � �� � ���� � � � � ���� � � � �

1

Mon

2

Tue

3

Wed

4

Thu

5

Fri

6

Sat

7

Sun

8

Mon

9

Tue

10

Wed

11

Thu

12

Fri

13

Sat

14

Sun

15

Mon

16

Tue

07:54

08:53

10:03

22:45

11:30

00:09

13:02

01:29

14:15

02:32

15:11

03:22

05:16

05:49

06:22

06:56

07:33

08:14

20:39

20:36

21:33

15:57

04:05

16:36

04:42

17:13

17:46

18:20

18:52

19:25

20:00

09.37

08.89

08.41

09.56

08.15

09.32

08.32

09.36

08.80

09.53

09.35

09.68

09.66

09.49

09.27

08.98

08.64

08.40

09.42

10.44

10.01

09.85

09.76

10.21

09.75

10.43

10.50

10.45

10.31

10.09

09.79

30.75

34.26

29.17

32.85

27.60

31.37

26.74

30.58

27.30

30.71

28.88

31.27

30.68

31.76

32.32

32.03

33.50

31.99

34.23

31.70

34.45

31.14

34.29

30.42

33.83

29.47

33.11

28.35

32.12

27.56

30.91

02:38

14:51

03:26

15:35

04:24

16:34

05:42

17:54

07:10

19:25

08:23

20:40

09:23

21:44

10:15

22:36

11:02

23:23

11:43

00:04

12:18

00:41

12:48

01:13

13:11

01:43

13:35

02:12

14:01

02:42

14:32

01.91

01.21

02.30

01.78

02.76

02.48

03.07

02.97

02.95

03.00

02.51

02.67

02.04

02.27

01.65

01.97

01.40

01.84

01.30

01.85

01.31

01.96

01.41

02.12

01.60

02.32

01.87

02.56

02.26

02.88

02.77

06.27

03.97

07.55

05.84

09.06

08.14

10.07

09.75

09.68

09.84

08.24

08.76

06.69

07.45

05.41

06.46

04.59

06.04

04.27

06.07

04.30

06.43

04.63

06.96

05.25

07.61

06.14

08.40

07.42

09.45

09.09

17

Wed

18

Thu

19

Fri

20

Sat

21

Sun

22

Mon

23

Tue

24

Wed

25

Thu

26

Fri

27

Sat

28

Sun

29

Mon

30

Tue

09:03

21:27

10:04

22:26

11:19

23:37

12:35

00:49

13:38

01:49

14:29

02:39

15:12

03:20

04:01

06:54

07:49

15:51

16:31

04:39

17:13

05:19

17:56

06:05

18:42

19:31

20:24

07.89

09.02

07.59

08.66

07.52

08.48

07.76

08.53

08.26

08.75

08.90

09.07

09.56

09.40

09.68

09.65

09.35

10.19

10.71

09.86

11.08

09.92

11.28

09.84

11.28

11.09

10.74

25.89

29.60

24.91

28.42

24.68

27.83

25.46

27.99

27.10

28.71

29.20

29.76

31.37

30.85

33.44

31.76

35.14

32.35

36.36

32.55

37.01

32.29

37.01

31.67

36.39

30.68

35.24

03:18

15:11

04:05

16:01

05:11

17:10

06:34

18:39

07:41

19:55

08:36

20:56

09:29

21:50

10:20

22:43

11:10

23:34

11:55

00:20

12:36

01:07

13:17

01:51

13:57

02:36

14:40

03.28

03.37

03.69

03.94

03.95

04.31

03.84

04.24

03.38

03.77

02.79

03.17

02.18

02.62

01.63

02.18

01.18

01.87

00.86

01.67

00.69

01.56

00.69

01.58

00.89

01.72

01.31

10.76

11.06

12.11

12.93

12.96

14.14

12.60

13.91

11.09

12.37

09.16

10.40

07.15

08.60

05.35

07.15

03.87

06.14

02.82

05.48

02.26

05.12

02.26

05.18

02.92

05.64

04.30

��� �������� ������ ������ ��� ���� ���� ������� ��� �� ��������� �� ������ � � !"�

��������� �#���� ���$� %& ���$ �� ���$ " '� ���� ������� �� (���)'(

LAT 21" 45" N LONG 72" 14" EAPRIL 2013

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Tide Time Table

30

Bhavnagar Port Tide Table

���� ���� � ���� ���� ���� � ����

�� � ���� � � � � ���� � � � � �� � ���� � � � � ���� � � � �

1

Wed

2

Thu

3

Fri

4

Sat

5

Sun

6

Mon

7

Tue

8

Wed

9

Thu

10

Fri

11

Sat

12

Sun

13

Mon

14

Tue

15

Wed

16

Thu

08:51

10:03

22:29

11:25

23:46

12:49

01:01

13:57

02:04

14:52

02:56

03:38

04:17

04:54

05:28

06:00

06:34

07:10

07:51

20:10

08:37

20:52

21:23

15:35

16:14

16:49

17:22

17:54

18:25

18:57

19:33

09.01

08.70

09.74

08.59

09.33

08.77

09.12

09.17

09.06

09.61

09.06

09.05

09.05

09.02

08.98

08.91

08.77

08.58

08.36

09.73

08.15

09.39

10.25

09.98

10.24

10.39

10.46

10.44

10.37

10.22

10.01

29.57

33.63

28.55

31.96

28.19

30.62

28.78

29.93

30.09

29.73

31.53

29.73

32.75

29.70

33.60

29.70

34.09

29.60

34.32

29.47

34.26

29.24

34.03

28.78

33.54

28.15

32.85

27.43

31.93

26.74

30.81

03:25

15:29

04:22

16:29

05:30

07:46

06:46

19:10

07:53

20:23

08:51

21:23

09:43

22:15

10:30

23:00

11:17

23:41

11:43

00:17

12:10

00:50

12:36

01:20

13:02

01:51

13:31

02:23

14:07

02:58

14:47

01.99

01.91

02.33

02.58

02.58

03.08

02.56

03.20

02.33

03.02

02.07

02.78

01.86

02.58

01.73

02.46

01.67

02.40

01.68

02.37

01.75

02.38

01.87

02.41

02.07

02.50

02.37

02.66

02.76

02.89

03.22

06.53

06.27

07.65

08.47

08.47

10.11

08.40

10.50

07.65

09.91

06.79

09.12

06.10

08.47

05.68

08.07

05.48

07.88

05.51

07.78

05.74

07.81

06.14

07.91

06.79

08.20

07.78

08.73

09.06

09.48

10.57

17

Fri

18

Sat

19

Sun

20

Mon

21

Tue

22

Wed

23

Thu

24

Fri

25

Sat

26

Sun

27

Mon

28

Tue

29

Wed

30

Thu

31

Fri

09:29

21:41

10:30

22:37

11:39

23:42

12:46

00:47

13:44

01:48

02:40

03:28

04:15

07:40

08:42

09:49

14:35

15:22

16:07

16:53

05:02

17:40

05:51

18:28

06:44

19:18

20:10

21:05

22:03

08.01

09.04

08.00

08.74

08.19

08.58

08.62

08.60

09.22

08.80

09.09

09.40

09.64

09.54

09.33

09.12

09.88

10.51

11.03

11.38

09.78

11.55

09.80

11.53

09.71

11.32

10.96

10.46

09.88

26.28

29.66

26.25

28.68

26.87

28.15

28.29

28.22

30.25

28.88

32.42

29.83

34.49

30.85

36.19

31.63

37.34

32.09

37.90

32.16

37.83

31.86

37.15

31.30

35.96

30.62

34.32

29.93

32.42

��� �������� ������ ������ ��� ���� ���� ������� ��� �� ��������� �� ������ � � !"�

��������� �#���� ���$� %& ���$ �� ���$ " '� ���� ������� �� (���)'(

LAT 21" 45" N LONG 72" 14" E

03:38

15:34

04:27

16:31

05:28

17:48

06:37

19:06

07:40

20:15

08:41

21:16

09:40

22:15

10:36

23:11

11:28

00:04

12:16

00:57

13:00

01:46

13:45

02:34

14:29

03:22

15:20

04:14

16:17

03.16

03.69

03.37

04.06

03.38

04.17

03.10

03.93

02.65

03.47

02.09

02.96

01.56

02.49

01.12

02.10

00.81

01.80

00.67

01.59

00.70

01.49

00.93

01.50

01.34

01.64

01.91

01.87

02.55

10.37

12.11

11.06

13.32

11.09

13.68

10.17

12.90

08.70

11.39

06.86

09.71

05.12

08.17

03.68

06.89

02.66

05.91

02.20

05.22

02.30

04.89

03.05

04.92

04.40

05.38

06.27

06.14

08.37

MAY 2013

Ship Recycling Industries Association (India) Vol-1 • Issue 1 • March 13

Tide Time Table

31

Bhavnagar Port Tide Table

���� ���� � ���� ���� ���� � ����

�� � ���� � � � � ���� � � � � �� � ���� � � � � ���� � � � �

��� �������� ������ ������ ��� ���� ���� ������� ��� �� ��������� �� ������ � � !"�

��������� �#���� ���$� %& ���$ �� ���$ " '� ���� ������� �� (���)'(

LAT 21" 45" N LONG 72" 14" E

1

Sat

2

Sun

3

Mon

4

Tue

5

Wed

6

Thu

7

Fri

8

Sat

9

Sun

10

Mon

11

Tue

12

Wed

13

Thu

14

Fri

15

Sat

16

Sun

11:04

23:10

12:20

00:22

13:28

01:29

14:24

02:24

03:13

03:54

04:33

05:07

05:41

06:15

06:49

07:27

08:09

20:20

08:55

21:01

09:46

21:49

15:10

15:48

16:24

16:58

17:31

18:02

18:35

19:08

19:43

09.02

09.30

09.09

08.84

09.33

08.57

09.63

08.45

08.44

08.49

08.58

08.68

08.74

08.74

08.69

08.61

08.55

09.72

08.52

09.41

08.55

09.06

09.91

10.11

10.25

10.34

10.38

10.38

10.31

10.18

09.99

29.60

30.52

29.83

29.01

30.62

28.12

31.60

27.73

32.52

27.70

33.17

27.86

33.63

28.15

33.93

28.48

34.06

28.68

34.06

28.68

33.83

28.52

33.40

28.25

32.78

28.06

31.90

27.96

30.88

28.06

29.73

05:10

17:27

06:12

18:44

07:15

19:56

08:11

20:58

09:04

21:53

09:51

22:38

10:35

23:18

11:11

23:55

11:42

00:28

12:11

01:00

12:39

01:33

13:13

02:08

13:47

02:42

14:27

03:18

15:11

03:55

16:01

02.12

03.12

02.29

03.42

02.34

03.44

02.32

03.32

02.27

03.15

02.21

02.96

02.12

02.77

02.04

02.61

01.99

02.50

02.01

02.42

02.12

02.40

02.33

02.43

02.61

02.49

02.94

02.60

03.32

02.71

03.67

06.96

10.24

07.51

11.22

07.68

11.29

07.61

10.89

07.45

10.34

07.25

09.71

06.96

09.09

06.69

08.56

06.53

08.20

06.60

07.94

06.96

07.88

07.65

07.97

08.56

08.17

09.65

08.53

10.89

08.89

12.04

17

Mon

18

Tue

19

Wed

20

Thu

21

Fri

22

Sat

23

Sun

24

Mon

25

Tue

26

Wed

27

Thu

28

Fri

29

Sat

30

Sun

10:45

22:44

11:52

23:50

13:00

01:02

02:08

03:05

03:59

08:24

09:23

10:28

22:28

14:01

14:55

15:47

16:36

04:50

17:25

05:42

18:13

06:33

19:01

07:28

19:48

20:38

21:31

08.69

08.74

08.98

08.55

09.45

08.57

08.81

09.15

09.50

09.73

09.52

09.31

09.17

10.04

10.62

11.12

11.47

09.76

11.64

09.92

11.61

09.96

11.41

09.89

11.04

10.52

09.87

28.52

28.68

29.47

28.06

31.01

28.12

32.95

28.91

34.85

30.02

36.49

31.17

37.64

32.03

38.20

32.55

38.10

32.68

37.44

32.45

36.23

31.93

34.52

31.24

32.39

30.55

30.09

04:41

17:03

05:38

18:21

06:45

19:36

07:54

20:47

09:02

21:52

10:07

22:52

11:07

23:50

12:01

00:46

12:50

01:37

13:35

02:26

14:19

03:12

15:05

03:56

15:55

04:41

16:55

02.78

03.93

02.72

03.94

02.47

03.65

02.08

03.19

01.62

02.69

01.19

02.22

00.85

01.82

00.67

01.51

00.67

01.31

00.87

01.23

01.25

01.28

01.80

01.49

02.46

01.82

03.13

09.12

12.90

08.93

12.93

08.11

11.98

06.83

10.47

05.32

08.83

03.90

07.28

02.79

05.97

02.20

04.95

02.20

04.30

02.85

04.04

04.10

04.20

05.91

04.89

08.07

05.97

10.27

JUNE 2013

Engaged in Ship Recycling business

An ISO 14000:2004 and

BS OHSAS 18001:2007 certified recycling yard,

certified by Bureau Veritas.

Specialist in recycling of Chemical Tankers

Exporters of scrap Propellers and

Marine Machinery.

Safe and Environmentally sound

Green Recycling of ships.

Contact Person

Udai Agarwal (Director)

Alang Auto andGen. Engg. Co. Pvt. Ltd.Office : CM-458, Rukmani Kunj, Kaliabid,

Bhavnagar - 364 002 (Guj.)

Tel : +91-278-2560473, Fax : +91-278-2563837

E-mail : [email protected]

www.alangauto.com

Works : Plot No. 24, Ship Recycling Yard,

Alang-364 081, Bhavnagar (Guj)

Conserving

the Future

by Recycling

the Past