Airport Monitoring Report 2011-12

556

Airport Monitoring Report 2011–12 Adelaide Brisbane Melbourne Perth Sydney Report

description

A report on Australian's airports from consumer watchdog Australian Competition and Consumer Commission.

Transcript of Airport Monitoring Report 2011-12

AirportMonitoringReport 2011–12Adelaide Brisbane Melbourne Perth Sydney

Report

Airport Monitoring Report 2011-12

Price, financial performance and quality of service monitoring

April 2013

ISBN 978 1 921973 61 1

Australian Competition and Consumer Commission 23 Marcus Clarke Street, Canberra, Australian Capital Territory, 2601

© Commonwealth of Australia 2013

This work is copyright. In addition to any use permitted under the Copyright Act 1968, all material contained within this work is provided under a Creative Commons Attribution 3.0 Australia licence, with the exception of:

• the Commonwealth Coat of Arms • the ACCC and AER logos • any illustration, diagram, photograph or graphic over which the Australian Competition and Consumer Commission does not hold copyright, but which

may be part of or contained within this publication.

The details of the relevant licence conditions are available on the Creative Commons website, as is the full legal code for the CC BY 3.0 AU licence.

Requests and inquiries concerning reproduction and rights should be addressed to the Director, Internal Communication and Publishing Services, ACCC, GPO Box 3131, Canberra ACT 2601, or [email protected].

Important notice

The information in this publication is for general guidance only. It does not constitute legal or other professional advice, and should not be relied on as a statement of the law in any jurisdiction. Because it is intended only as a general guide, it may contain generalisations. You should obtain professional advice if you have any specific concern.

The ACCC has made every reasonable effort to provide current and accurate information, but it does not make any guarantees regarding the accuracy,

currency or completeness of that information.

Parties who wish to re-publish or otherwise use the information in this publication must check this information for currency and accuracy prior to publication. This should be done prior to each publication edition, as ACCC guidance and relevant transitional legislation frequently change. Any queries parties have should be addressed to the Director, Internal Communications and Publishing Services, ACCC, GPO Box 3131, Canberra ACT 2601, or

ACCC 04/13_700

www.accc.gov.au

Airport Monitoring Report 2011-12 Contents

iii

Contents

Glossary v

Key Findings vii

Summary xiii

1 Overview of the monitoring results for aeronautical services 1

1.1 Introduction 2

1.2 Airport terminal configurations 2

1.3 Key observations from the monitoring results for aeronautical services 4

1.4 Price monitoring results 15

1.5 Quality of service monitoring results 46

1.6 Price and quality outcomes for the airports 52

2 Potential aeronautical capacity issues at airports 53

2.1 Introduction 53

2.2 Recent growth in passenger throughput and aeronautical investment 54

2.3 Congestion is emerging at a number of monitored airports 57

2.4 Passenger throughput is forecast to continue to grow over the next 59

two decades

2.5 Inadequate investment and effects on ongoing congestion 60

2.6 Approaches for dealing with congestion in the short-term and long-term 60

2.7 Airports’ incentives for aeronautical investment 64

2.8 Airports’ current investment plans in response to emerging congestion 65

2.9 Different approaches to funding aeronautical investment 68

2.10 The impact of regulatory access arrangements 71

3 Overview of airport car parking and landside services 73

3.1 Introduction 74

3.2 Airport car parking configurations 74

3.3 Airport car parking prices 77

3.4 Airport car parking revenues, costs and profits 80

3.5 Airport car parking availability and quality 86

3.6 Landside access charges and revenues 90

3.7 Observations from the monitoring results for airport car parking and 93

landside access

3.8 Passenger growth, capacity constraints and investment in airport 97

car parking and landside services

4 Adelaide Airport 103

4.1 Overview of aeronautical and car parking monitoring results 104

4.2 Airport overview and major airport investments 105

Contents Airport Monitoring Report 2011-12

iv

4.3 Aeronautical prices monitoring and financial performance results 108

4.4 Aeronautical services quality of service monitoring results 132

4.5 Car parking services monitoring results 154

4.6 Adelaide Airport price and quality of service monitoring beyond 2011-12 164

5 Brisbane Airport 167

5.1 Overview of aeronautical and car parking monitoring results 168

5.2 Airport overview and major airport investments 170

5.3 Aeronautical prices monitoring and financial performance results 173

5.4 Aeronautical services quality of service monitoring results 193

5.5 Car parking services monitoring results 218

6 Melbourne Airport 231

6.1 Overview of aeronautical and car parking monitoring results 232

6.2 Airport overview and major airport investments 234

6.3 Aeronautical prices monitoring and financial performance results 236

6.4 Aeronautical services quality of service monitoring results 253

6.5 Car parking services monitoring results 282

7 Perth Airport 295

7.1 Overview of aeronautical and car parking monitoring results 296

7.2 Airport overview and major airport investments 298

7.3 Aeronautical prices monitoring and financial performance results 301

7.4 Aeronautical services quality of service monitoring results 322

7.5 Car parking services monitoring results 351

8 Sydney Airport 363

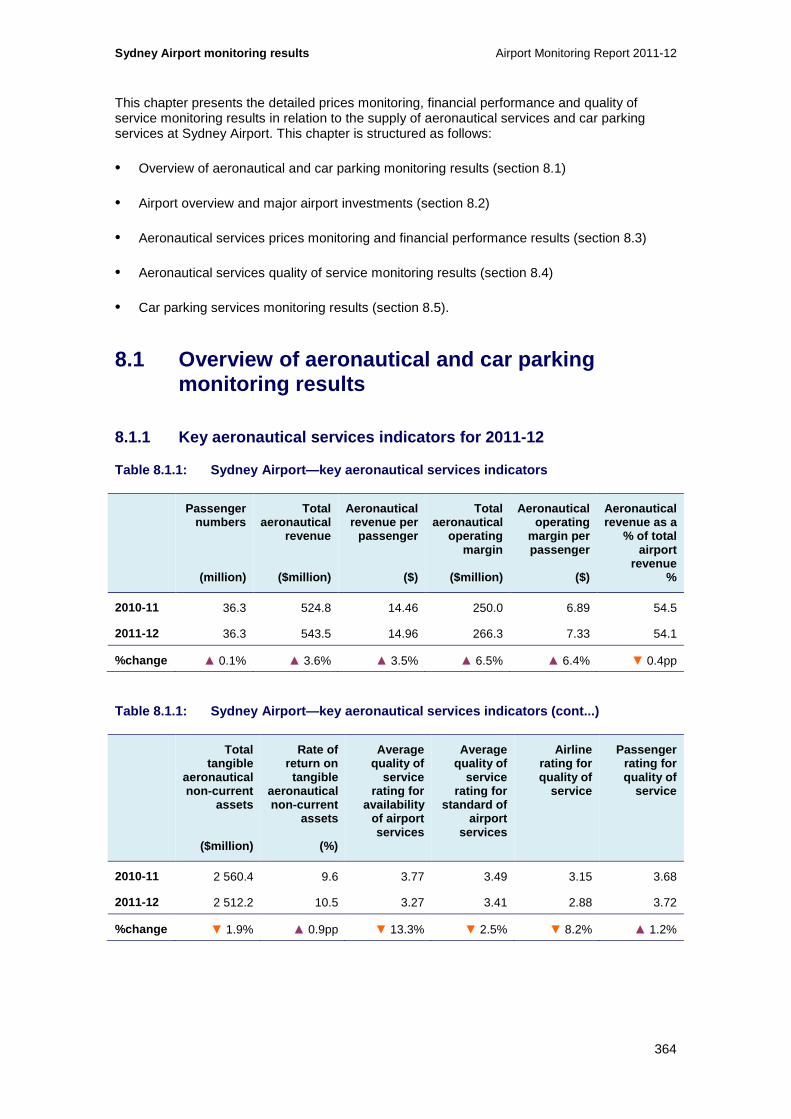

8.1 Overview of aeronautical and car parking monitoring results 364

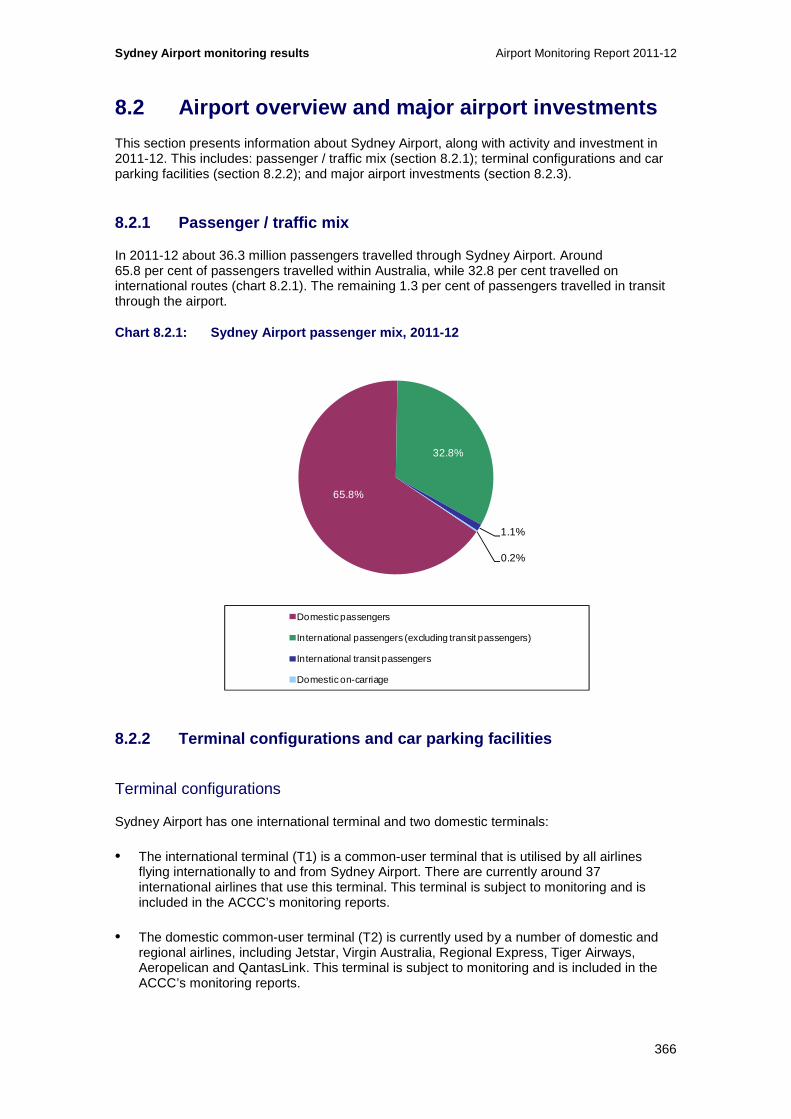

8.2 Airport overview and major airport investments 366

8.3 Aeronautical prices monitoring and financial performance results 370

8.4 Aeronautical services quality of service monitoring results 394

8.5 Car parking services monitoring results 422

Appendices

A1 Regulatory accounts for the monitored airports 437

A2 Indicators and statistics used in the report 458

A3 Airport car parking statistics 489

A4 History of airport regulation in Australia 504

A5 Regulatory framework 509

A6 Services provided by airports 514

A7 Methodology for this report 517

Airport Monitoring Report 2011-12 Glossary

v

Glossary

AASB Australian Accounting Standards Board

ACCC Australian Competition and Consumer Commission

AC&BPS Australian Customs and Border Protection Service

AGAAP Australian Generally Accepted Accounting Principles

AIFRS Australian equivalents to International Financial Reporting Standards

APS Australian Protective Service

Availability Describes the amount of the facility/service made available relative to demands for the facility or service. May include whether facilities or services are available or restricted due to congestion, positioning, maintenance, or repairs, the accessibility or usefulness of the facility/service provided, and the efficiency of the system to allocate usage.

BARA Board of Airline Representatives of Australia

BITRE Bureau of Infrastructure, Transport and Regional Economics

CBD central business district

CCA Competition and Consumer Act 2010

CTFR Counter Terrorism First Response

CPI consumer price index

DAFF Department of Agriculture, Fisheries and Forestry, Biosecurity Biosecurity

DIAC Department of Immigration and Citizenship

DIT Department of Infrastructure and Transport

DTL domestic terminal lease

EBITA earnings before interest, tax and amortisation

EBITDA earnings before interest, tax, depreciation and amortisation

FAC Federal Airports Corporation

FSC full service carrier

GA general aviation

GST goods and services tax

IASB International Accounting Standards Board

LCC low cost carrier

Glossary Airport Monitoring Report 2011-12

vi

LHS left-hand side

LIS Line in the sand

Minister Minister with portfolio responsibility for Transport and Infrastructure

MTOW maximum take-off weight

Peak hour The hour that, on average for each day in the financial year, has the highest number of (arriving/departing/total of both) passengers.

PC Productivity Commission

PFC passenger facilitation charges

PSC passenger services charge

RHS right-hand side

RPT regular public transport

SLA Service level agreements

Standard Describes the physical condition of the facility/service supplied and condition in which it is generally maintained.

SAR state of the art renewal

TPA Trade Practices Act 1974 (renamed the Competition and Consumer Act 2010 on 1 January 2011)

White paper Aviation White Paper: Flight path to the future, Australian Government, 2009

Airport Monitoring Report 2011-12 Key Findings

vii

Key Findings – Airport Monitoring 2011-12

The ACCC’s monitoring role for the major airports

This report presents the results of the ACCC’s monitoring of the quality, prices, costs and profits related to aeronautical and car parking services supplied by Adelaide, Brisbane, Melbourne, Perth and Sydney airports for the 2011-12 financial year.

As confirmed in the recent inquiry into the economic regulation of airport services by the Productivity Commission (PC), the monitored airports have market power. These airports are monitored to provide information to the public and the government about the airport operators' performance. However, monitoring does not restrict the airports from increasing prices or degrading service standards to earn monopoly profits.

In 2011-12, airports continued to be profitable but quality of service was down

Monitored airports earned profits in 2011-12 but despite continued investment in aeronautical assets, overall ratings for quality of service were lower at each of the monitored airports compared with 2010-11.

Sydney, Brisbane and Perth airports reported higher margins in 2011-12 relative to the previous year. Melbourne Airport’s margins were adversely affected by a jump in costs while Adelaide Airport experienced a large drop in passenger numbers and revenue.

The lower overall ratings for quality of service at monitored airports reinforces the need for more investment as demand for airport services grows more quickly than airports’ capacity to accommodate the increase in demand.

In 2011-12, demand for airport services was underpinned by solid growth in passenger numbers

Growth in combined passenger numbers at the monitored airports continued to drive demand for airport services during 2011-12. Passenger numbers at the monitored airports increased 2.5 per cent in 2011-12, the tenth consecutive year of growth in airport patronage.

Total passenger numbers fell at Adelaide Airport, but falls in domestic travel Sydney and Melbourne airports were offset by solid growth in international travel at these airports.

Perth Airport registered the strongest growth among monitored airports driven by substantial growth in domestic travel and strong growth in international travel. Growth in both domestic and international travel contributed to a solid increase in passenger numbers at Brisbane Airport.

Average prices charged by airports and aeronautical revenue higher in 2011-12

Combined revenues from aeronautical services at the monitored airports increased 4.5 per cent in 2011-12. All airports other than Adelaide Airport earned higher aeronautical revenues.

Key Findings Airport Monitoring Report 2011-12

viii

Average aeronautical revenue per passenger (a proxy for average prices) across monitored airports increased around 1.9 per cent.

Aeronautical revenue per passenger increased at Sydney, Melbourne and Brisbane airports but fell at Adelaide and Perth airports.

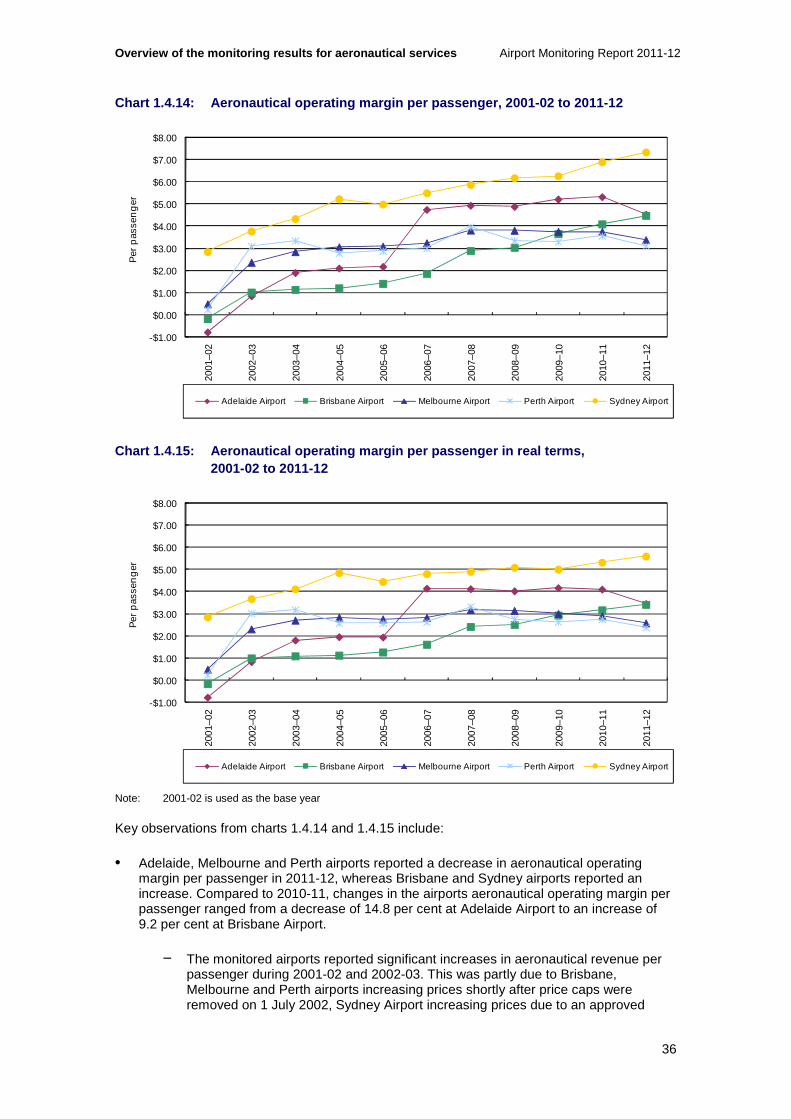

Sydney Airport remained the airport with the highest aeronautical revenue per passenger at $14.96.

Aeronautical margins also higher in 2011-12

Combined margins on aeronautical services at the five monitored airports increased 2.2 per cent during 2011-12. Margins increased at all airports other than Adelaide and Melbourne airports.

On a per passenger basis, average aeronautical margins across the monitored airports were largely unchanged in 2011-12.

Brisbane and Sydney airports earned higher margins per passenger but Adelaide, Melbourne and Perth airports experiencing lower margins.

Sydney Airport continued to be the airport with the highest aeronautical margin per passenger at $7.33 per passenger.

Overall quality of aeronautical services fell at all airports during 2011-12

The overall ratings for quality of service (that is, quality of service ratings from surveys of airlines, passengers, border agencies as well as objective indicators) fell at each of the monitored airports during 2011-12.

For the first time since 2007-08, none of the airports achieved an overall rating of at least good, that is, all airports were rated satisfactory.

Key quality of service results for Australia’s monitored airports during 2011-12 were:

Sydney Airport continues to be rated lowest overall. Passengers increased their ratings within the satisfactory category, while airlines’ ratings dropped from satisfactory to poor.

Brisbane Airport was rated highest for overall quality of service. Passengers continued to rate Brisbane Airport good while airlines dropped their ratings within the satisfactory category. Airlines’ ratings for runway availability decreased significantly from good in 2010-11 to poor in 2011-12.

Perth Airport continued to be rated second lowest overall. Airlines’ ratings remained unchanged at poor while passengers’ ratings decreased from good to satisfactory.

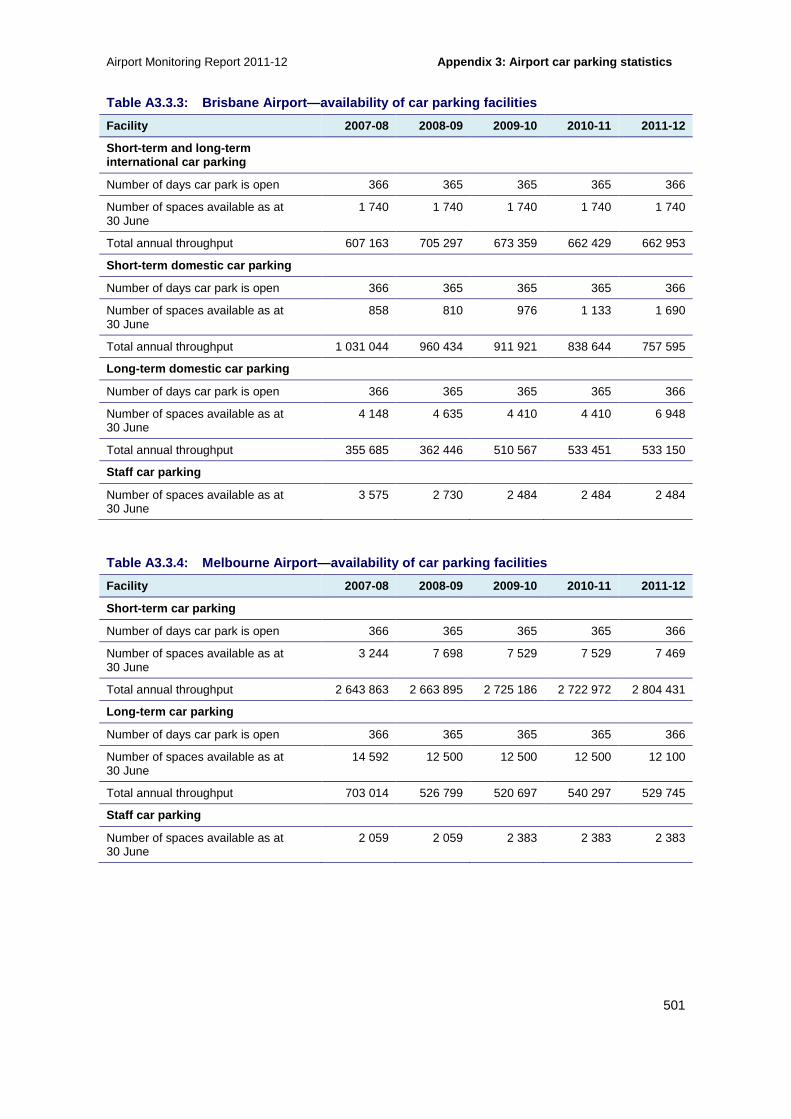

Car parking revenues higher during 2011-12

The number of car park spaces increased at all airports other than Melbourne Airport in 2011-12. Overall, Melbourne Airport had the largest number of car park spaces (21 924) followed by Perth Airport (15 626) and Sydney Airport (13 116).

Airport Monitoring Report 2011-12 Key Findings

ix

Total revenue earned from the monitored airports’ landside access operations increased by almost 20 per cent to around $28.7 million.

Sydney Airport continues to earn the highest revenue and margin per car park space ($7654 and $5290 respectively) while Perth Airport reported the lowest ($3239 and $2187 respectively).

Sydney Airport reported the largest increase in landside revenues (36.9 per cent) and continued to be the airport with the highest revenues from landside charges ($13.3 million).

Airport investments increased during 2011-12

In 2011-12, monitored airports collectively invested $547.4 million in aeronautical assets - this was 61.7 per cent more than $339.5 million invested in 2010-11.

Congestion emerging at some airports

Strong growth in passenger numbers in recent years has placed increasing pressure on existing aeronautical infrastructure and landside arrangements.

Despite continued investment in aeronautical assets, there are signs of congestion emerging at Australia’s monitored airports. Data published by the Bureau of Infrastructure, Transport and Regional Economics (BITRE) indicates increasing incidence of delays to scheduled domestic flight arrivals and departures at monitored airports. While these data are not direct evidence of capacity constraints at airports, they are indicative of emerging system-wide congestion.

Aeronautical services:

Brisbane Airport: According to Brisbane Airport the current runway system is likely to reach capacity in the next two years. While Brisbane Airport is in the early stages of constructing a new runway, there is conjecture as to how the project will proceed given the differences between the airport and airlines on how its cost should be recovered.

Melbourne Airport: investment is planned for expansion of runway capacity in the next seven years in order to meet the growing demand.

Perth Airport: demand concentration, particularly during ‘fly-in/fly-out’ peak periods, is placing pressure on its infrastructure. A new domestic terminal was completed in March 2013.

Sydney Airport: concerns over capacity issues are reflected in the reduction to poor in this year’s ratings by airlines of availability of airside services, including runways, taxiways and aprons. The current legislated runway management system sets a cap of 80 hourly aircraft movements which places limits on options.

Car parking and landside arrangements:

Evidence of congestion in terminal forecourts and landside services has prompted airports to improve arrangements for dealing with traffic flows, such as establishing new public passenger pick up areas and additional car parking spaces.

Key Findings Airport Monitoring Report 2011-12

x

Investment will be required for additional capacity

Aeronautical services

Forecasts of continued growth in passenger throughput and aircraft movements at monitored airports suggests that existing aeronautical infrastructure will be under increasing pressure in the years ahead.

In 2011-12, the decline in overall ratings for quality of service suggests that demand for aeronautical services, may be growing more quickly than the apparent ability to accommodate the increased demands placed on infrastructure, particularly at Brisbane, Sydney and Perth airports.

Australian airports have typically not used peak-period pricing to efficiently ration excess demand, preferring to ration quantity through slot management schemes. In the short term, dealing with congestion through slot management schemes based on grandfathered landing rights may discourage entry of new airlines.

In the long term, it is apparent that without additional investment in aeronautical capacity Australia’s largest airports will face challenges in the next few years continuing to provide aeronautical services that meet the reasonable expectations of users.

Landside services

In order to facilitate access to landside services and maximise the efficiency of landside infrastructure networks, Australia’s major airports will need to ensure that they engage all relevant stakeholders. While an airport is responsible for planning and developing terminal access roads and car parking facilities within the airport boundaries, local and state governments must work in conjunction with the airports.

The ACCC will continue to report on progress with airport investments and how airports are responding to airside and landside congestion.

Airport Monitoring Report 2011-12 Key Findings

xi

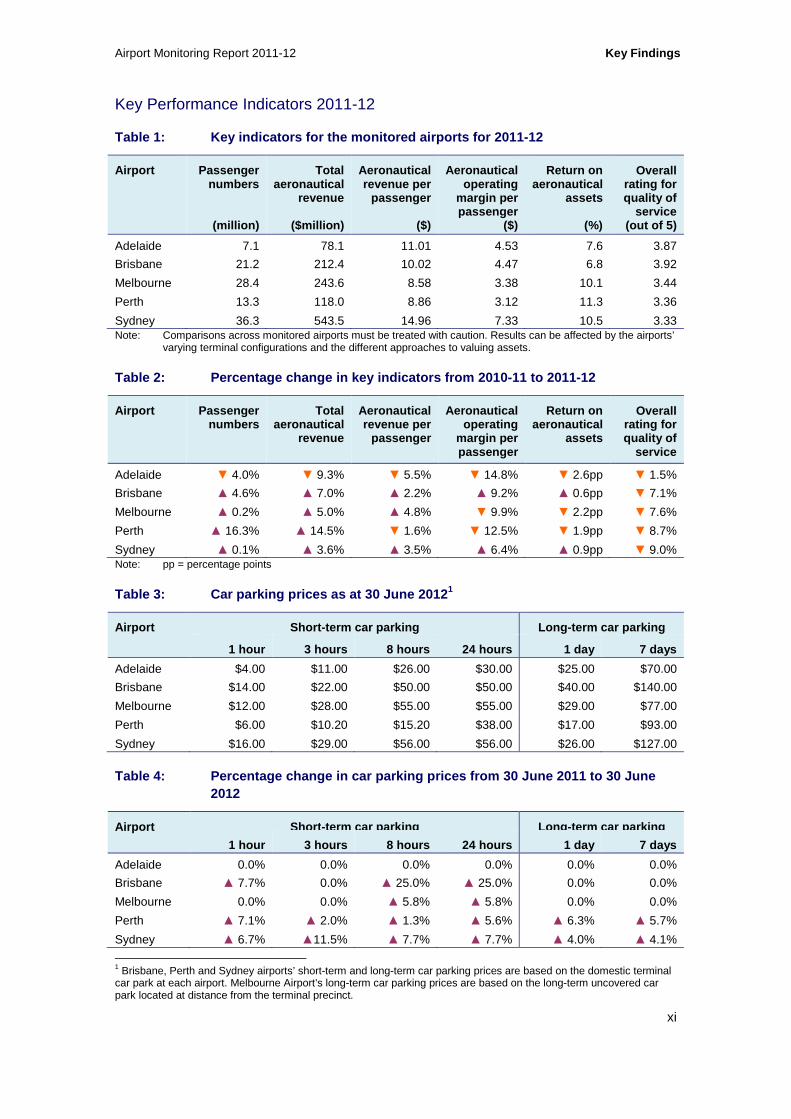

Key Performance Indicators 2011-12

Table 1: Key indicators for the monitored airports for 2011-12

Airport Passenger numbers

(million)

Total aeronautical

revenue

($million)

Aeronautical revenue per

passenger

($)

Aeronautical operating

margin per passenger

($)

Return on aeronautical

assets

(%)

Overall rating for quality of

service (out of 5)

Adelaide 7.1 78.1 11.01 4.53 7.6 3.87

Brisbane 21.2 212.4 10.02 4.47 6.8 3.92

Melbourne 28.4 243.6 8.58 3.38 10.1 3.44

Perth 13.3 118.0 8.86 3.12 11.3 3.36

Sydney 36.3 543.5 14.96 7.33 10.5 3.33 Note: Comparisons across monitored airports must be treated with caution. Results can be affected by the airports’

varying terminal configurations and the different approaches to valuing assets.

Table 2: Percentage change in key indicators from 2 010-11 to 2011-12

Airport Passenger numbers

Total aeronautical

revenue

Aeronautical revenue per

passenger

Aeronautical operating

margin per passenger

Return on aeronautical

assets

Overall rating for quality of

service

Adelaide ▼ 4.0% ▼ 9.3% ▼ 5.5% ▼ 14.8% ▼ 2.6pp ▼ 1.5%

Brisbane ▲ 4.6% ▲ 7.0% ▲ 2.2% ▲ 9.2% ▲ 0.6pp ▼ 7.1%

Melbourne ▲ 0.2% ▲ 5.0% ▲ 4.8% ▼ 9.9% ▼ 2.2pp ▼ 7.6%

Perth ▲ 16.3% ▲ 14.5% ▼ 1.6% ▼ 12.5% ▼ 1.9pp ▼ 8.7%

Sydney ▲ 0.1% ▲ 3.6% ▲ 3.5% ▲ 6.4% ▲ 0.9pp ▼ 9.0% Note: pp = percentage points

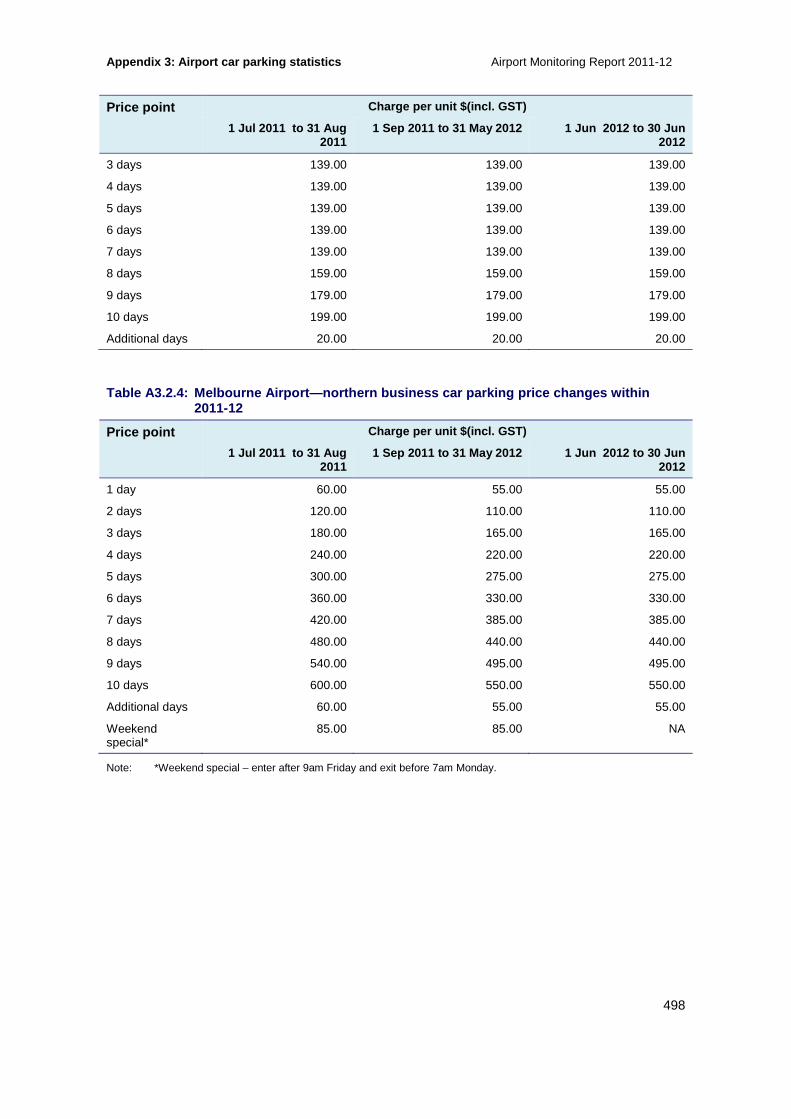

Table 3: Car parking prices as at 30 June 2012 1

Airport Short-term car parking Long-term car parking

1 hour 3 hours 8 hours 24 hours 1 day 7 days

Adelaide $4.00 $11.00 $26.00 $30.00 $25.00 $70.00

Brisbane $14.00 $22.00 $50.00 $50.00 $40.00 $140.00

Melbourne $12.00 $28.00 $55.00 $55.00 $29.00 $77.00

Perth $6.00 $10.20 $15.20 $38.00 $17.00 $93.00

Sydney $16.00 $29.00 $56.00 $56.00 $26.00 $127.00

Table 4: Percentage change in car parking prices fr om 30 June 2011 to 30 June 2012

Airport Short -term car parking Long -term car parking

1 hour 3 hours 8 hours 24 hours 1 day 7 days

Adelaide 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Brisbane ▲ 7.7% 0.0% ▲ 25.0% ▲ 25.0% 0.0% 0.0%

Melbourne 0.0% 0.0% ▲ 5.8% ▲ 5.8% 0.0% 0.0%

Perth ▲ 7.1% ▲ 2.0% ▲ 1.3% ▲ 5.6% ▲ 6.3% ▲ 5.7%

Sydney ▲ 6.7% ▲11.5% ▲ 7.7% ▲ 7.7% ▲ 4.0% ▲ 4.1%

1 Brisbane, Perth and Sydney airports’ short-term and long-term car parking prices are based on the domestic terminal car park at each airport. Melbourne Airport’s long-term car parking prices are based on the long-term uncovered car park located at distance from the terminal precinct.

Key Findings Airport Monitoring Report 2011-12

xii

Table 5: Key car park indicators for the monitored airports for 2011-12

Airport Total airport car

parking revenue

($million)

Total airport car

parking operating

margin

($million)

Total airport car

parking spaces

Airport car parking

revenue per car park

space

($)

Airport car parking

margin per car park

space

Airport car parking

revenue as % of total

airport revenue

(%)

Adelaide 14.0 9.5 3 002 4 673 3 179 9.7

Brisbane 60.9 37.9 12 862 4 738 2 944 12.5

Melbourne 114.7 86.4 21 924 5 231 3 942 20.0

Perth 50.6 34.2 15 626 3 239 2 187 7.0

Sydney 100.4 69.4 13 116 7 654 5 290 10.0

Table 6: Percentage change in key indicators from 2 010-11 to 2011-12

Airport Total airport car

parking revenue

($million)

Total airport car

parking operating

margin

($million)

Total airport car

parking spaces

Airport car parking

revenue per car park

space

($)

Airport car parking

margin per car park

space

Airport car parking

revenue as % of total

airport revenue

(%)

Adelaide ▼ 4.9% ▼ 10.0% ▲ 0.1% ▼ 5.0% ▼ 10.1% ▲ 0.5pp

Brisbane ▲ 1.4% ▼ 11.8% ▲ 31.7% ▼ 23.0% ▼ 33.0% ▼ 0.6pp

Melbourne ▲ 0.05% ▼ 0.6% ▼ 2.2% ▲ 2.3% ▲ 1.6% ▼ 1.0pp

Perth ▲ 23.2% ▲ 24.3% ▲ 7.4% ▲ 14.7% ▲ 15.8% ▼ 6.9pp

Sydney ▲ 2.5% ▲0.4% ▲ 6.9% ▼ 4.1% ▼ 6.1% ▼ 0.2pp Note: pp = percentage points

Table 7: Investments in tangible aeronautical non-c urrent assets – 2002-03 to 2011-12 ($M)

$M 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Adelaide 4.4 49.8 135.1 25.3 1.8 3.8 3.1 4.4 38.1 59.9

Brisbane 16.0 8.7 19.9 32.5 92.5 247.6 199.1 150.9 63.2 155.9

Melbourne 22.5 19.7 70.6 42.2 60.6 83.7 161.0 136.7 103.4 155.8

Perth 6.7 7.1 27.6 10.7 15.8 28.4 47.4 45.3 69.7 75.6

Sydney 151.1 49.2 46.3 124.4 161.6 83.9 345.3 227.1 65.0 100.2

Table 8: Investments as proportions of tangible aer onautical non-current assets – 2002-03 to 2011-12 (%)

2002-03

%

2003-04

%

2004-05

%

2005-06

%

2006-07

%

2007-08

%

2008-09

%

2009-10

%

2010-11

%

2011-12

%

Adelaide 3.4 28.3 32.8 6.3 0.5 1.0 0.8 1.2 9.5 13.4

Brisbane 2.8 1.5 2.2 3.5 9.1 19.5 14.2 11.4 4.7 10.8

Melbourne 5.3 4.7 14.9 8.5 11.3 14.1 22.1 16.4 11.5 15.5

Perth 7.7 4.0 14.1 5.9 8.4 13.8 19.4 16.2 20.6 19.0

Sydney 9.2 3.0 2.9 5.6 7.0 3.6 13.5 8.6 2.5 4.0

Airport Monitoring Report 2011-12 Summary

xiii

Summary - Airport Monitoring 2011-12

Prices, revenue, margins and quality of service for aeronautical services

Demand for aeronautical services

In 2011-12 demand for aeronautical services increased at all airports except Adelaide Airport.

Growth in total passenger numbers was relatively flat at Melbourne and Sydney airports increasing by 0.2 per cent and 0.1 per cent respectively. Growth was stronger at Brisbane Airport (4.6 per cent) and Perth Airport (16.3 per cent).

Passenger numbers at Adelaide Airport fell by 4.0 per cent compared with 2010-11. It is likely that a number of factors may have contributed to the drop in passenger numbers at Adelaide Airport, including subdued economic conditions, Tiger Airways ceasing operations at the airport from July 2011 and the Qantas grounding and associated industrial action. 2

Perth and Brisbane airport have experienced strong growth in domestic passenger numbers. Falls in domestic passenger numbers at Sydney and Melbourne airports were off-set by higher numbers of international passengers.

Section 1.4.1 discusses airport throughput levels at monitored airports.

Total and average revenues and prices

All airports other than Adelaide Airport earned higher aeronautical revenues during 2011-12.

In 2011-12, higher average prices at Sydney and Melbourne airports contributed to solid growth in aeronautical revenues of 3.6 per cent and 5.0 per cent respectively despite relatively low growth in passenger numbers.

Higher average prices and an increase in passenger numbers at Brisbane Airport during 2011-12 contributed to a strong increase in aeronautical revenues of 7.0 per cent.

Perth Airport reported a slight fall in aeronautical revenue per passenger (average prices) (-1.6 per cent) but significantly higher total aeronautical revenues (14.5 per cent) due mainly to strong growth in total passenger numbers.

At Adelaide Airport, lower average prices and a fall in passenger numbers resulted in lower aeronautical revenues (-9.3 per cent).

Sections 1.4.2 and 1.4.3 describe total aeronautical revenues and average prices at monitored airports.

2 Tiger Airways re-commenced operations at Adelaide Airport after the end of the 2011-12 financial year.

Summary Airport Monitoring Report 2011-12

xiv

Aeronautical margins

Sydney and Brisbane airports were the only two airports to report higher aeronautical operating margins per passenger during 2011-12.

At Sydney Airport, aeronautical operating margins per passenger increased 6.4 per cent due to higher increases in revenue than costs and comparatively low growth in overall passenger numbers.

At Brisbane Airport, higher aeronautical revenue per passenger coupled with lower aeronautical operating expenses per passenger resulted in an increase in operating aeronautical margins per passenger of 9.2 per cent.

Adelaide, Melbourne and Perth airports experienced falls in aeronautical operating margins per passenger of 14.8 per cent, 9.9 per cent and 12.5 per cent respectively.

At Melbourne Airport, an increase in average aeronautical revenues per passenger of 4.8 per cent was not enough to offset the effects of an increase in aeronautical operating expenses of 17.3 per cent. Higher depreciation and salaries contributed to higher costs at Melbourne Airport.

At Adelaide Airport, aeronautical margins per passenger fell as aeronautical revenues per passenger decreased while operating expenses per passenger increased by 2.4 per cent.

At Perth Airport, aeronautical margins per passenger fell as aeronautical revenues per passenger fell 1.6 per cent while operating expenses associated with the airport’s expansion increased.

Section 1.4.5 presents an analysis of aeronautical margins at monitored airports.

Returns on assets

Sydney and Brisbane airports recorded slightly higher returns on aeronautical assets in 2011-12 relative to 2010-11, consistent with the changes in aeronautical operating margins. Returns fell at the other three monitored airports.

In the 2009-10 and 2010-11 AMRs, the ACCC noted that airports are partially insulated from the effects of economic shocks (such as the global financial crisis and natural disasters) that can reduce demand for air travel.

Section 1.4.6 describes returns on assets at monitored airports.

Quality of services

The overall ratings for quality of service (that is, quality of service ratings based on objective indicators and responses from surveys of airlines, passengers and border agencies) fell at all monitored airports during 2011-12, with each airport receiving an overall rating of satisfactory.

For the first time since 2007-08, none of the airports achieved an overall rating of good (that is, a rating equal to 4.0 or higher).

Adelaide Airport’s rating by passengers and airlines decreased within the satisfactory category. Passengers rated Adelaide Airport lowest along with Sydney Airport while airlines rated it highest for quality of service provided to airlines.

Airport Monitoring Report 2011-12 Summary

xv

Brisbane Airport achieved highest overall rating among monitored airports. Passengers’ rating dropped slightly within the good range while airlines’ ratings decreased but remained satisfactory. Airlines’ rating for runway availability fell significantly in 2011-12 to poor after it was rated good in 2010-11. Brisbane Airport was ranked highest by passengers and second highest by airlines.

Melbourne Airport’s rating by passengers decreased slightly in 2011-12, though remained good. Airlines’ ratings increased within the satisfactory range. Passengers rated Melbourne Airport second among the five monitored airports while airlines ranked it third.

Perth Airports’ average passenger rating decreased from good in 2010-11 to satisfactory in 2011-12. Airlines’ rating for Perth Airport remained poor. Passengers rated Perth Airport third while airlines rated it last for quality of service provided to airlines.

Sydney Airport had the lowest overall rating among monitored airports for 2011-12. Passengers’ rating increased within the satisfactory range in 2011-12. Sydney Airport was the only airport that received an increased passenger rating in 2011-12. Airlines’ rating decreased from satisfactory in 2010-11 to poor in 2011-12. Passengers rated Sydney Airport, along with Adelaide Airport, lowest among monitored airports while airlines rated it second lowest.

Section 1.5 presents an analysis of quality of service outcomes for all monitored airports.

Emerging capacity constraints in aeronautical infrastructure

While in 2011-12 passenger numbers fell at Adelaide Airport and were essentially flat at Melbourne and Sydney airports, the monitored airports as a whole have experienced significant growth in passenger numbers in recent years.

Total passenger throughput at the five monitored airports has increased by 71.1 per cent since 2001-02, with passenger numbers increasing from 62.1 million in 2001-02 to 106.3 million in 2011-12. Aircraft movements have increased by 30.7 per cent over the same time period, increasing from 733 694 in 2001-02 to 958 863 in 2011-12.

It is likely that further investment will be required by the monitored airports over the next few years to ensure that aeronautical capacity is sufficient to accommodate the future needs of users.

Forecasts of continued growth in passenger throughput and aircraft movements at the monitored airports suggests that existing aeronautical infrastructure is likely to be under increasing pressure in the medium to long term. The Bureau of Infrastructure, Transport and Regional Economics (BITRE) has projected that by 2031 total passenger throughput at the five monitored airports will increase by 103.8 per cent, from 106.3 million passengers in 2011-12 to 216.7 million passengers in 2030-31.3 BITRE also projected that by 2030, total aircraft movements at the five monitored airports will increase by 55.5 per cent, from 958 863 movements in 2011-12 to just under 1.5 million movements in 2029-30.4

If unaddressed, congestion issues will have direct impacts on users of the airports, as well as indirect impacts on the economy more broadly. Australia’s major airports are a significant component of the national transport infrastructure, facilitating the movement of people and the supply of goods and services. As a result, the major airports make a considerable contribution to Australia’s overall economic prosperity. Notably, the direct contribution of the air and space

3 Bureau of Infrastructure, Transport and Regional Economics, Research Report 133: Air passenger movements through capital and non-capital city airports to 2030-31, November 2012. 4 Bureau of Infrastructure, Transport and Regional Economics, Research Report 117: Aircraft movements through capital city airports to 2029-30, April 2010.

Summary Airport Monitoring Report 2011-12

xvi

industry to the Australian economy in the year ending 30 June 2012 was approximately $7.1 billion, or approximately 0.5 per cent of Australia’s Gross Domestic Product.5

Despite investment in aeronautical assets over the last 11 years, there is evidence of emerging system-wide congestion at Australia’s monitored airports. According to the BITRE, between November 2003 and January 2013, the proportion of domestic flights that arrived on-time fell, on average, 11.4 per cent while the proportion of domestic flights that departed on-time fell 8.9 per cent across monitored airports. At the same time the number of flights into and out of the monitored airports has increased markedly.6

The government’s pricing principles for Australian monitored airports provide for the use of peak-period pricing to deal with the effects of congestion. It is noted, however, that monitored airports have preferred to ration excess demand through slot management schemes based on grandfathered landing rights. The use of grandfathered quantity rationing systems may have the effect of discouraging efficient new entry.

In the long run, the most efficient way for airports to respond to congestion is to invest in new infrastructure to accommodate the increase in demand. A number of airports have noted the emergence of capacity constraints and the need for additional capacity.

Melbourne Airport has noted that investment to expand runway capacity will be required before the end of the decade in order to meet growing demand. Brisbane Airport has stated that it expects the growth in air travel to start exceeding the capacity of its current runway system between 2013 and 2015. Perth Airport has noted that demand concentration during peak periods is placing pressure on its infrastructure.7

In respect of Sydney Airport, the report to the Australian and NSW governments by the Steering Committee of the Joint Study on aviation capacity in the Sydney region concluded that immediate action is needed to increase Sydney Airport’s capacity to meet growing demand. The Steering Committee concluded that from around 2030, an additional airport will be needed to supplement the capacity of Sydney Airport.8

Section 2.3 discusses evidence of congestion at monitored airports.

Master planning process at Australian airports

To ensure that airports continue to invest in airport infrastructure, the government requires airports to prepare master plans and major development plans, so that airports can indicate the areas where investments will be undertaken. These plans also require public consultation, so that users can express views to the airports and the Government about where investment should be targeted to meet their needs.

Under the Airports Act 1996 (Airports Act), Australian airports are required to establish a 20 year forward-looking master plan, which identifies, for example, development objectives and future aviation requirements. Master plans are updated by the airports every five years and have to be approved by the Minister for Infrastructure and Transport (the Minister). The five monitored airports have master plans in place which are due to be updated over the next two years.

5 ABS, Australian National Accounts, National Income, Expenditure and Product (ABS cat. no. 5206.0, June 2012, Table 45).

6 Bureau of Infrastructure, Transport and Regional Economics, Domestic airline on time performance, December 2003

and December 2012. 7 Perth Airport, Submission to ACCC Airport Monitoring Report, 28 September 2012. See also Brad Geatches, Perth Airport challenges, West Australian Perth, 15 October 2012. 8 Steering Committee, Joint Study on aviation capacity in the Sydney region, March 2012.

Airport Monitoring Report 2011-12 Summary

xvii

The Government stated in its 2009 National Aviation Policy White Paper (the White Paper) that improved planning is one of its policy goals for Australian airports, in order to facilitate better integration and coordination with off-airport planning and to facilitate continued investment in Australia’s airport infrastructure and land transport links.9 Following the release of the White Paper, the Government has increased the requirements for airports to consult and engage with the broader community throughput the planning process.

Airports must also prepare major development plans for major projects

Under the Airports Act, Australian airports are also required to prepare a major development plan for each major individual development at an airport, including aeronautical and non-aeronautical projects. Airports must undertake public consultation on draft major development plans before submitting the plan to the Minister for approval.

Planning for future investment in aeronautical serv ices

The monitored airports have plans to invest in aeronautical assets over the next few years, in order to expand aeronautical capacity.

Brisbane Airport has recently completed the detailed design for the first construction phase of its new parallel runway and has commenced civil works. Brisbane Airport has proposed that construction will be completed by 2020.

In November 2012, Melbourne Airport announced its preferred orientation for a third runway, with its proposal to be outlined in its 2013 master plan.10 Melbourne Airport noted that a third runway will be required from around 2018-22 to meet the growing demand for access to the airport.

Perth Airport has planned a number of projects within the international terminal following opening of a new domestic terminal in March 2013, including an expansion and redesign of the international arrivals area and the departures customs, security screening and lounge areas. It has been reported in the media that Perth Airport has commenced planning for a third runway.11

Sydney Airport, while constrained by legislative requirements from increasing runway capacity, is planning to undertake a number of initiatives, including a proposed reconfiguration of the current domestic and international precincts.12

ACCC to monitor and report on airports’ investment projects

The ACCC intends to track progress by airports in implementing investment plans. Future AMRs will assess and report on the extent to which planned investments are taking place.

Chapter 2 presents an in-depth analysis of emerging capacity constraints on the supply of aeronautical services and future investment needs at monitored airports.

9 Australian Government, National Aviation Policy White Paper, December 2009. 10 Melbourne Airport, Melbourne Airport announces third runway preference, Media Release, 20 November 2012. 11 Examples include; Geoffrey Thomas, Airport had warning of chaos, West Australian, 12 October 2012 and; Brad Geatches, Perth Airport challenges, 15 October 2012 and; Natalie Gerritsen, Perth unlocks keys to terminal, Australian Financial Review, 8 January 2013. 12 Sydney Airport, New Vision To Integrate International , Domestic and Regional Services, 5 December 2011, viewed on 9 January 2013 at; http://www.sydneyairport.com.au/corporate/media-centre/media-releases/media-release-detail.aspx?item=%7B19FE83DF-66A6-49CA-A219-72C3A4A4C7E0%7D&lst=%7BC313C142-0E4E-4269-A2FB-BDEB95B3BC9E%7D.

Summary Airport Monitoring Report 2011-12

xviii

Prices, revenue, margins and capacity for airport c ar parking

The ACCC monitors on-airport car parking prices and revenues, costs and profits associated with on-airport car parking for all monitored airports.

The ACCC also collects information on charges imposed by airports on operators of alternative services to on-airport car parking as well as the amount of revenue received from those operators. Alternatives to on-airport car parking include taxi services, limousine and hire car services, and private and public bus services.

By imposing excessive charges or restrictive terms and conditions for landside access, airports could potentially obstruct competition from alternatives to on-airport car parking. This could have the effect of shifting demand from those alternatives to an airport’s own car parking services, and allow the airport to charge higher prices.

However, it is important to note that, for the reasons outlined at the end of this chapter, care needs to be taken when interpreting the levels of on-airport car parking and landside access prices, revenues, costs and profits, and when making comparisons of performance across the monitored airports and over time.

Because of the many different types of price points available on car parking (that is, different prices per different lengths of car park stays), it is not possible to make reference to an average price for car parking. Instead, car parking revenue, costs and margins per car park space are used as indicators of unit revenue, unit costs and unit margins.

Prices and Revenues

At Brisbane, Melbourne Perth and Sydney airports car park revenues increased in 2011-12 due to a combination of higher car parking charges and increased demand. See Table 3 in the Key Findings for data on car parking prices and revenues.

Perth Airport reported a 23.2 per cent increase in revenues as a result of increases in car park prices in three of the four price points shown in Table 3 in the Key Findings and an increase of 7.4 per cent in the number of car park spaces.

Brisbane and Sydney airports recorded slight increases in revenue (up 1.4 per cent and 2.5 per cent respectively) and large increases in the number of car park spaces (up 31.7 per cent and 6.9 per cent respectively).

Melbourne Airport’s car parking revenues were largely unchanged in 2011-12. Two of the price points were increased and the number of car spaces decreased by 2.2 per cent. In 2011-12, Melbourne Airport earned the highest revenues from car parking ($114.7 million) and the highest proportion of total airport revenue from car parking (20 per cent).

Car parking prices did not change at Adelaide Airport which recorded a fall in car parking revenues of 4.9 per cent.

Section 3.3 describes prices charged for car parking at monitored airports, while section 3.4 discusses revenues earned by airport operators from their car parking businesses.

Margins

Two airports, Adelaide and Brisbane, experienced a fall in margins earned on their car parking operations. Adelaide and Brisbane airports recorded falls in margins, of 10.0 per cent and

Airport Monitoring Report 2011-12 Summary

xix

11.8 per cent respectively, and in margins per car park space of 10.1 per cent and 33.0 per cent respectively.

Sydney Airport reported a rise in total margins of 0.4 per cent but, because of a rise of 6.9 per cent in the number of car park spaces, margins per car park space fell 6.1 per cent. Despite this, Sydney Airport continued to earn the highest margin per car park space with $5 290.

Perth Airport car parking margins increased 24.3 per cent while margin per car park space increased 15.8 per cent.

Melbourne Airport car parking margins were largely unchanged from 2010-11 levels but remained the highest among monitored airports ($86.4 million).

Section 3.4 assesses margins earned on car parking facilities at monitored airports.

Landside services

Recent trends in landside access prices and revenue s

The ability of operators of landside alternatives to on-airport car parking, such as taxis, trains, off-airport car parking, buses and hire cars, to supply these services depends on whether they can have access to airport land, and on the terms and conditions of access.

Airports control access to airport land, and the associated terms and conditions of access, and so have the ability to influence the level of competition between on-airport car parking and other off-airport landside alternatives.

Results of monitoring charges and revenues associated with landside access include:

Three airports, Brisbane, Perth and Sydney, increased some charges while Melbourne and Adelaide airports left all landside access charges unchanged in 2011-12.

Total landside revenue increased at all airports other than Adelaide Airport. Total revenue earned from landside access operations at all airports increased by almost 20 per cent to around $28.7 million in 2011-12.

Revenue at Brisbane, Melbourne and Perth airports increased 9.2 per cent, 6.4 per cent and 10.1 per cent respectively. Sydney Airport’s revenue from landside access was the highest of all five airports at about $13.3 million, increasing by around 36.9 per cent in 2011-12. Sydney Airport accounted for around 46 per cent of the combined land-side revenue earned by monitored airports.

Section 3.6 presents additional information on landside charges and revenues.

Investing in landside services

Projected growth in passenger numbers will also increase demand for landside access at monitored airports. This will create the need for investment in car parking facilities, terminal roads, kerbside management, and other facilities used by landside operators supplying alternatives to on-airport car parking.

An airport’s landside infrastructure can be broadly categorised as that existing within an airport and immediately adjacent to the airport precinct. Landside infrastructure within an airport broadly consists of car parks, taxi holding areas, train platforms and other facilities, pick-up and drop-off areas and roads surrounding the terminals and connecting the airport to the major roads outside of the airport precinct. Beyond the airport boundaries, landside infrastructure consists of road and rail networks used by consumers to access the airport.

Summary Airport Monitoring Report 2011-12

xx

As noted, several major investment projects are underway or have recently been completed by the monitored airports. Looking forward, it will be imperative that the airports liaise with users and governments to develop appropriate landside solutions to address growth. Such engagement with stakeholders will ensure landside developments are fit for purpose, deliver sufficient spare capacity and integrate with wider infrastructure networks.

Section 3.8 analyses possible capacity issues at landside facilities including future investment requirements in section 3.8.1.

Cooperation is necessary

Planning, collaboration and investment in landside facilities, particularly those transportation networks outside of airport borders, will be required to complement significant airside capacity expansion and aeronautical growth at airports.

Establishing efficient landside networks for getting to and from an airport requires input from a number of parties such as airports, landside operators, state governments and the Commonwealth. As airports continue to grow, and the surrounding landside infrastructure becomes increasingly congested, effective cooperation between responsible parties will be important to implement effective landside solutions.

It will be important that the airports liaise with users and governments to develop appropriate landside solutions to address forecast growth, to ensure that they are fit for purpose and deliver sufficient spare capacity.

Section 3.8.2 discusses investment planning processes for landside facilities.

Monitoring investment outcomes

To improve the scope and ability for the ACCC to assess the airport operator’s performance and progress against investment plans, this year’s airport monitoring program was extended to collect details of completed, ongoing and planned investment in landside infrastructure.

By reporting on progress with airport investment, the AMR can provide further observations of how airports are responding to any congestion issues at the landside and whether there are issues outside the airport boundaries that are influencing the efficiency of landside infrastructure networks.

This information, in conjunction with the airports’ own master plans, will assist in assessing the extent to which the airports are meeting the needs of their users.

The ACCC’s role in monitoring aeronautical and car parking services

The ACCC’s monitoring role for the major airports

In a number of inquiries into the economic regulation of airport services, the most recent of which was in 2011, the PC has reiterated that airports monitored by the ACCC have market power. According to the PC “...the market power of Sydney, Melbourne, Brisbane and Perth Airports is sufficient to warrant policy attention”. 13 Airports control access to the key infrastructure necessary for air transportation and for users of airports to access terminals. In many cases, there is a lack of practical alternatives for travelling overseas and the large distances between capital cities. Consequently, the air transportation industry plays a pivotal

13 Productivity Commission, Economic Regulation of Airport Services, Inquiry report No. 57, Canberra, December 2011.

Airport Monitoring Report 2011-12 Summary

xxi

role in the Australian economy in facilitating travel as well as movement of time sensitive goods and services.

Due to concerns that airports could use their position to earn monopoly profits to the detriment of Australians, the Australian Government has directed the ACCC to monitor the quality, prices, costs and profits relating to the supply of aeronautical and car parking services by Australia’s five major airports—Adelaide, Brisbane, Melbourne (Tullamarine), Perth and Sydney (Kingsford Smith) airports.

The government established a price monitoring approach to regulating airports in 2002 following consideration of the recommendations of a PC inquiry. The move from a price regulation regime to a monitoring regime was intended to facilitate investment and innovation, while retaining a constraint on the exercise of market power by the airports in their dealings with airlines and other customers. In responses to subsequent PC inquiries in 2006 and 2011, the government has reiterated its commitment to the continuation of the airports monitoring program.

The ACCC is also required to monitor the quality of service in relation to the provision of prescribed aspects of airport services and facilities by those airports.

Productivity Commission 2011 inquiry into the economic regulation of airport services and the Government’s response

During 2010, the government responded to concerns raised by the ACCC in relation to its 2008-09 AMR. These concerns included that Sydney Airport had potentially increased profits by permitting service-quality standards to fall below that which could be expected in a competitive environment over a sustained period.

The 2011 PC report into the economic regulation of airport services concluded that Brisbane, Melbourne, Perth and Sydney airports retain sufficient market power to be of policy concern.14 The PC recommended that the current monitoring program should continue to operate until at least 2020.

The government agreed in principle with the PC’s recommendations to continue monitoring of airports by the ACCC and that the next review of the monitoring program should be done in 2018.

Limitations of monitoring

Monitoring of itself does not restrict airports from using their monopoly position to increase prices and/or lower service standards.

Monitoring is limited in its scope to undertake a detailed assessment of the performance of airport operators. The results from monitoring do not provide conclusive evidence as to whether airport operators are exercising market power. For example, it is not possible to determine whether airports are earning monopoly rents from information obtained through the monitoring program. A more detailed evaluation of the airports’ performance would be required to make more definitive findings, including a comparison with economically efficient benchmarks. However, such an evaluation is beyond the scope of monitoring. Among other things, within accepted accounting conventions airports have discretion on asset values. This limits the usefulness of data on returns on assets as an indicator of economic performance.

14Productivity Commission, Economic Regulation of Airport Services, Inquiry Report No. 57, Canberra, December 2011.

Summary Airport Monitoring Report 2011-12

xxii

Importantly, monitoring does not directly restrict the airports from increasing prices and/or lowering service standards and does not provide the ACCC with a general power to intervene in the airports’ conduct in setting of terms and conditions of access.

For these reasons, monitoring is not effective in addressing the policy concern that an unconstrained airport presents and is not a substitute for effective regulation.

That said, monitoring allows the performance of airports to be considered based on observations from the monitoring results over time. It is possible for the ACCC to make general observations about whether certain outcomes might be consistent with firms with market power. For example, the ACCC may express concerns about an airport’s performance where prices increase while quality of service is observed to have remained constant or even fallen below satisfactory, over a sustained period of time.

By providing a greater level of transparency to the airports’ performance, monitoring also seeks to address information asymmetries that may exist between airports and its customers.

Analysis and interpretation of monitoring results

Presentation of data and charts in the 2011-12 report

The 2010-11 AMR presented most charts and tables with airport data commencing from 2006-07.

In the current AMR, the time series presented and discussed in the accompanying notes extends from 2001-02 to 2011-12, representing 11 years of data.

The ACCC believes that an appropriate period to assess trends over time is for data to be presented from 2001-02 to 2011-12. The change to presenting data with a longer time series enables analysis of pricing and long term asset values and changes over time. Airport assets are usually long-term investments. Where practicable, long-term time series, such as data covering the period from 2001-02 is presented in both nominal and real terms.

Monitoring prices, profits and quality of aeronautical services

A number of indicators have been developed to monitor prices, profits and quality of aeronautical services.

The ACCC publishes a schedule of prices charged by each airport for the supply of aeronautical services (see chapters 4-8). Airports provide many different types of services with charges levied on different bases - such as on a per passenger basis or by aircraft weight. Further, airports might offer discounts for certain periods or to certain users, or there might be minimum and maximum charges in place which affect some users but not others.

In addition, the price changes for particular airport users might vary depending on the composition of the airport services they utilise, the times at which they use them and so on. For example, the costs to an airline of a domestic flight are likely to be different to those associated with an international one due to differing security and processing requirements. Similarly, changes in price structure by an airport might affect users in different ways—even to the point of effectively lowering the costs for one user while raising them for another.

For these reasons, it is difficult to aggregate all services and prices into a single average price of aeronautical services for monitoring purposes. The lack of a single aggregate price complicates the task of establishing trends over time given and comparing prices across airports.

Airport Monitoring Report 2011-12 Summary

xxiii

Given these complications, the ACCC’s primary measure of average airport prices is aeronautical revenue per passenger. This relies on a consistently defined service definition and provides a measure of the cost to airlines expressed in terms of the most significant charging unit.

Similarly, when measuring net earnings, the ACCC has relied on aeronautical operating margins per passenger as an indicator of unit profits and return on aeronautical assets as an indicator of profitability.

Measures of service quality include survey ratings by airlines, passengers and border agencies as well as objective indicators.

Caveats - monitoring costs and profits

As noted, care should be taken when making comparisons of performance across airports and over time. There are many factors that may influence the price and quality of service monitoring results.

The price, cost and profit data presented in this report is based on accounting data provided by the monitored airports. The main caveats for price monitoring results include:

• difficulties in consistently reporting financial information because of changes in legislation and regulations that can affect how items are reported (including in accounting practices such as the transition to Australian equivalents to International Financial Reporting Standards in 2005–06)

• indicators of profitability based on accounting data in particular are not effective measures of economic performance and only provide guidance on trends in operating performance over time

• airports’ return on assets can be significantly affected by the discretion they have on asset revaluations. This affects the usefulness of analyses of rates of return on assets for assessing economic performance and also complicates comparisons of changes in rates of return over time and across airports.

A change in the definition of aeronautical services and non-aeronautical services in 2007–08 by the Australian Government significantly affected how revenues are reported and reduced the comparability of airports’ revenues with prior years.

As with other multi-product firms, airports incur a range of costs that are common across aeronautical and non-aeronautical services. As there is no economically meaningful way of allocating common costs to individual products and services, allocation of expenses to different types of services requires some discretion by the airport operators, which in turn can influence measures of profitability of services.

Financial indicators can provide useful insights into the operational performance of airports over time. However, they should not be interpreted in isolation as they only provide a partial indication of performance and are not definitive. Trends of operational performance across airports are more reliable if comparable results are present for a range of relevant indicators.

For example, the ACCC employs a number of indicators to measure profitability to account for their respective limitations. Aeronautical operating margin per passenger is used by the ACCC as a measure of unit profits. However, this measure does not make an allowance for risk-adjusted returns on capital associated with the provision of services.

The ACCC also uses return on average assets as an additional measure of profitability, although this measure is likely to vary according to the stage of a given airport’s investment

Summary Airport Monitoring Report 2011-12

xxiv

cycle. In addition, rates of return can also be affected by different asset valuation methodologies employed by airports. Among other things, airports’ upward revaluation of assets might lower measures of return on average assets. This can possibly distort comparisons across airports and over time.

In order to establish asset values to facilitate the monitoring of rates of return a ‘line in the sand’ measure was reported for the first time in the 2007–08 ACCC AMR. The line in the sand approach removes for monitoring purposes the effects of revaluations of aeronautical assets by airports after 30 June 2005. This approach, however, may also be affected to the extent that airport operators had chosen to revalue assets prior to this cut-off date.

Another reason that may make comparisons across airports difficult is the fact that the ACCC’s monitoring role for aeronautical services relates only to those terminals that are owned and operated by the monitored airports. However, some of the airports’ domestic terminals, such as the Qantas and Virgin Australia domestic terminals at Brisbane Airport are leased and operated by those airlines and are not subject to the ACCC’s monitoring. Therefore the revenues, costs, profits and quality of service associated with those terminals are not included in the monitoring results presented in this report.15

Caveats - monitoring quality of service

The provision of airport services can be influenced by different parties and, therefore, interpretation of the quality of service results need to take these different factors into account. Indeed, airport services are commonly the combined responsibility of a number of entities—including airlines, government agencies, the airport operator and sub-lessees of the airport operator.

The quality of service results should not be considered in isolation of other indicators as doing so can result in misinterpretation of the outcomes. The objective measures of quality of service may provide useful context to the understanding of survey results and should therefore be interpreted in conjunction with each other.

15 Note that the rent charged by the Airport operators to Airlines such as Qantas and Virgin for the use of the terminal is included in non-aeronautical revenue.

Airport Monitoring Report 2011-12 Overview of the monitoring results for aeronautica l services

1

1 Overview of the monitoring results for aeronautical services

Key points

Trends in prices, costs and margins for aeronautical services

• With the exception of Adelaide Airport, passenger numbers increased at the monitored airports in 2011-12. Sydney Airport has had the highest passenger throughput in every year since 2001-02, while Perth Airport has had the highest growth in passenger throughput since 2001-02.

• Domestic passenger numbers fell but international passenger numbers increased in 2011-12 at Australia’s two largest airports at Sydney and Melbourne. On the other hand, domestic passenger travel made significant contributions to the strong growth in passenger numbers at Perth and Brisbane airports.

• Aeronautical revenue per passenger (an indicator of average prices) fell at Adelaide and Perth airports but rose at the other monitored airports.

• Sydney Airport remained the airport with the highest aeronautical revenue per passenger at $14.95 per passenger compared with the second highest at Adelaide Airport with $11.01 per passenger.

• Adelaide, Melbourne and Perth airports reported a decrease in aeronautical operating margin per passenger (an indicator of profitability), while Brisbane and Sydney airports reported an increase in aeronautical operating margin per passenger.

• Sydney Airport continued to be the airport with the highest aeronautical margin per passenger at $7.33 per passenger compared with the second highest at Adelaide Airport with $4.53 per passenger.

Trends in quality of service for aeronautical services

• Overall quality of service ratings, based on objective indicators and encompassing the views of airlines, passengers and border agencies, decreased for all monitored airports in 2011-12, though all airports remained rated as satisfactory.

• Sydney Airport recorded the lowest ratings in terms of overall quality of service for the seventh consecutive year.

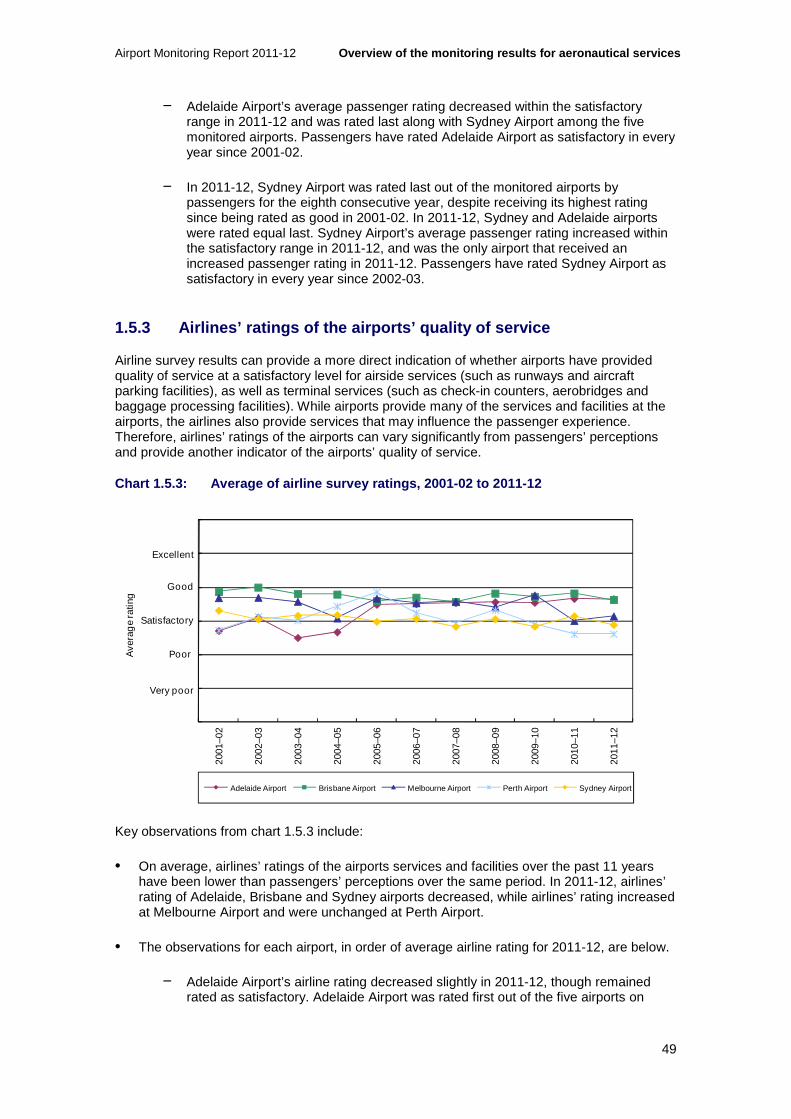

• Airlines’ ratings, which can provide a more direct indication of the quality that the airport operators provide, decreased at Adelaide, Brisbane and Sydney airports in 2011-12. Airlines’ rating of Melbourne Airport’s quality of service increased, and remained unchanged at Perth Airport.

Price and quality ratings for the airports

• Sydney Airport had the highest aeronautical revenue per passenger and the lowest overall rating for quality of service in 2011-12.

• In contrast, Melbourne Airport had the lowest aeronautical revenue per passenger and was third behind Brisbane and Adelaide airports for overall quality of service.

Overview of the monitoring results for aeronautical services Airport Monitoring Report 2011-12

2

1.1 Introduction

This chapter presents observations on the performance of Adelaide, Brisbane, Melbourne (Tullamarine), Perth and Sydney (Kingsford Smith) airports in relation to the supply of aeronautical services.

For the purposes of the ACCC AMRs, aeronautical services are defined as services provided by airport infrastructure to facilitate air transportation of passengers and freight. Under regulation 7.02 of the Airports Regulations 1997, aeronautical services and facilities are defined as “services and facilities at an airport that are necessary for the operation and maintenance of civil aviation at the airport”. These include services and facilities listed in the tables accompanying the regulations: aircraft-related services and facilities such as runways, taxiways, and passenger-related services and facilities such as public areas in terminals, departure and holding lounges.

Section 2 describes terminal configurations at different airports. Section 1.3 provides some key observations about the performance of each of the monitored airports during 2011-12. Key indicators relating to activity, prices, revenues, costs, margins and investments for aeronautical services are discussed in section 1.4, showing changes in indicators over time in nominal values, as well as inflation-adjusted values. Section 1.5 presents the quality of service results, while section 1.6 compares the airports’ price and quality of service outcomes for the most recent year (2011-12).

More detailed information about the monitoring results for aeronautical services since 2001-02 is provided on an airport-by-airport basis in chapters 4 to 8. Monitoring data going back to 2001-02 is presented in order to provide an analysis of long-term trends. Aeronautical assets, such as terminals and runways, are generally long-lived assets, and long-term analysis can provide an indication of the adequacy of these investments over time.

Appendices A.1 and A.2 of this report provide the individual airports’ regulatory accounts and detailed information on the airports’ indicators and statistics used in this report. For details regarding the approach taken by the ACCC in preparing the measures used in this report, as well as a full list of aeronautical services covered by the monitoring program, see appendices A.4 to A.7.

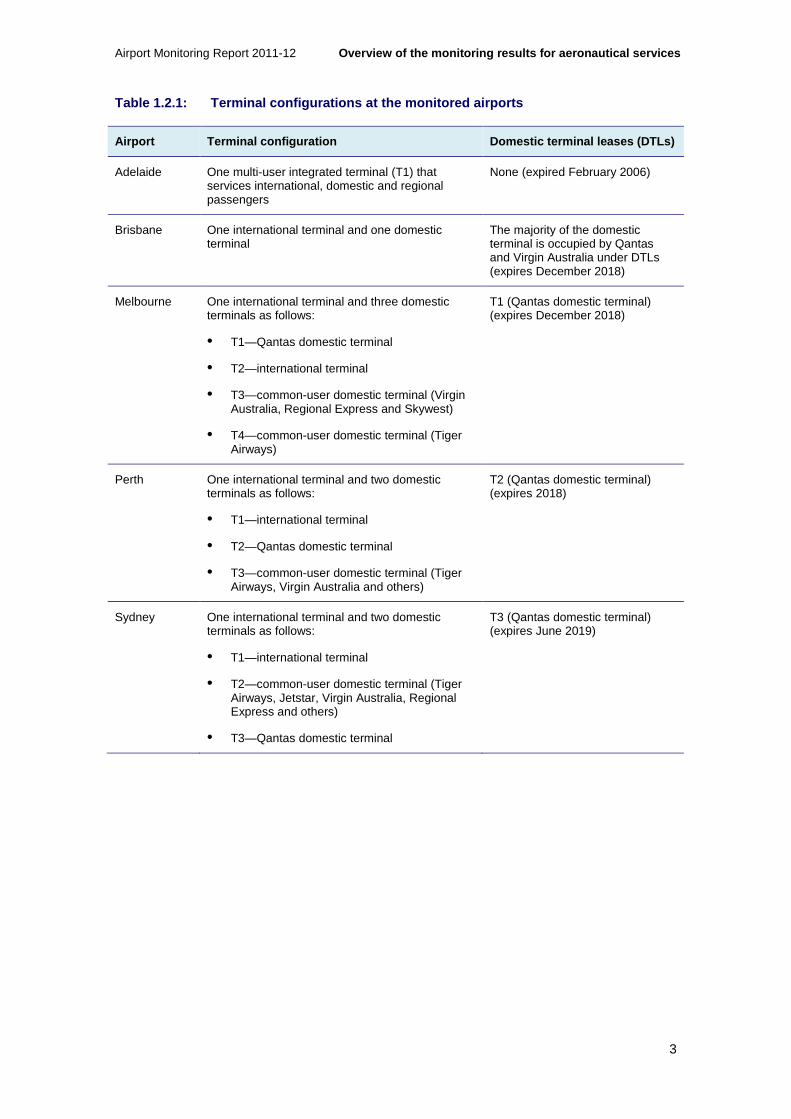

1.2 Airport terminal configurations

The monitored airports have considerably different terminal configurations. Some airports offer a combined terminal for international and domestic passengers, while others have separate terminals.

Importantly, some of the domestic terminals at the monitored airports are leased and operated by airlines under domestic terminal leases (DTLs). Under DTLs, airlines operate their terminals independently of the airports and have greater discretion over the quality of services and facilities offered.16 The existence of DTLs at some of the monitored airports complicates comparisons of monitoring results across airports (see box 1.2.1)

The various terminal configurations offered by the monitored airports and the DTLs that apply are outlined in table 1.2.1.

16 For more detailed information on the implications of domestic terminal leases, see chapter 3 of the ACCC’s Airport Monitoring Report 2008-09.

Airport Monitoring Report 2011-12 Overview of the monitoring results for aeronautica l services

3

Table 1.2.1: Terminal configurations at the monitor ed airports

Airport Terminal configuration Domestic terminal leases (DTLs)

Adelaide One multi-user integrated terminal (T1) that services international, domestic and regional passengers

None (expired February 2006)

Brisbane One international terminal and one domestic terminal

The majority of the domestic terminal is occupied by Qantas and Virgin Australia under DTLs (expires December 2018)

Melbourne One international terminal and three domestic terminals as follows:

• T1—Qantas domestic terminal

• T2—international terminal

• T3—common-user domestic terminal (Virgin Australia, Regional Express and Skywest)

• T4—common-user domestic terminal (Tiger Airways)

T1 (Qantas domestic terminal) (expires December 2018)

Perth One international terminal and two domestic terminals as follows:

• T1—international terminal

• T2—Qantas domestic terminal

• T3—common-user domestic terminal (Tiger Airways, Virgin Australia and others)

T2 (Qantas domestic terminal) (expires 2018)

Sydney One international terminal and two domestic terminals as follows:

• T1—international terminal

• T2—common-user domestic terminal (Tiger Airways, Jetstar, Virgin Australia, Regional Express and others)

• T3—Qantas domestic terminal

T3 (Qantas domestic terminal) (expires June 2019)

Overview of the monitoring results for aeronautical services Airport Monitoring Report 2011-12

4

Box 1.2.1: Domestic Terminal Leases

Comparisons of airports’ revenues, prices, costs, margins and quality of service are complicated by domestic terminal leases (DTLs) at some of the monitored airports.

The direction issued to the ACCC under s.95ZF of the CCA to undertake airport monitoring up to 2011-12 (Direction No 29) relates to aeronautical and car parking services and facilities provided by Sydney Airport Corporation Limited (Sydney Airport), Australia Pacific Airports Corporation Limited (Melbourne Airport), Brisbane Airport Corporation Pty Limited (Brisbane Airport), Perth Airport Pty Ltd (Perth Airport) and Adelaide Airport Limited (Adelaide Airport).

The Airports Regulations 1997 define aeronautical services and facilities to include both aircraft-related and passenger-related services and facilities provided at an airport.17 However, the ACCC’s monitoring program does not include passenger-related services and facilities that are provided within a terminal that is occupied and operated by an airline under a DTL. Therefore, the revenues, prices, costs, margins and quality of service associated with the passenger-related services and facilities provided within these terminals are excluded from the results presented in this report.18

Adelaide Airport is the only monitored airport that does not have any DTLs. Adelaide Airport opened its multi-user terminal in October 2005, with Qantas transferring its domestic operations from the terminal that it occupied and operated under a DTL to the new terminal in February 2006. Therefore, monitoring data collected from Adelaide Airport prior to February 2006 does not include data on passenger-related services and facilities provided within the domestic terminal operations of Qantas. This contributed to Adelaide Airport reporting significant increases in aeronautical revenue, expenses and margins in 2005-06 and 2006-07, as data on passenger-related services and facilities previously provided within the domestic terminal operations of Qantas were included in the monitoring programme for the first time.

1.3 Key observations from the monitoring results fo r aeronautical services

In performing its monitoring role, the ACCC looks at levels and trends across a range of indicators—including prices, costs, margins, returns on assets, investment and quality of service—at the individual airports. However, although observations from monitoring may raise some concerns about an individual airport’s performance, monitoring does not allow a detailed assessment of the airport’s performance to be undertaken and cannot be used to conclusively establish whether an airport has exercised market power to earn monopoly rents. The limitations of monitoring are set out in further detail in the executive summary, while appendix A.7 discusses the ACCC’s monitoring methodology.

For the purposes of the discussion in this section, analysis of quality of service is focused on the quality of service provided to airlines and on the results of the airline survey results, as airline ratings can provide a more direct indicator of the quality of service that the airport operator provides. This is because airports provide services directly to airlines under commercial arrangements and are in a position to make an informed assessment of quality against price.

17 Aeronautical services and facilities have the meaning given by regulation 7.02A of the Airports Regulations 1997. 18 For more detailed information on the implications of domestic terminal leases, see chapter 3 of the ACCC’s Airport Monitoring Report 2008-09.

Airport Monitoring Report 2011-12 Overview of the monitoring results for aeronautica l services

5

Given the complex nature of airports’ bundling of charges, and changes on the basis of how these charges are applied, the ACCC adopts aeronautical revenue per passenger as an indicator of average prices that the airlines pay to airports. Aeronautical operating expenses per passenger are used as an indication of unit costs.

It should be noted that aeronautical revenue and aeronautical operating expenses on a per passenger basis include revenues and costs associated with the provision of government mandated security services. The revenues and costs associated with these services do not reflect decisions made by airport operators. Therefore, where appropriate, the discussion in this chapter and the individual airport chapters (chapters 4-8) also consider aeronautical revenue per passenger and aeronautical operating expenses per passenger excluding security.

Unlike average prices and unit costs, aeronautical operating margin per passenger is discussed including security. This is because government mandated security revenue is set to recover the costs associated with security services and does not affect the overall profitability of the airports.

The following sections outline some observations from the monitoring results for each of the airports.

1.3.1 Observations about Adelaide Airport

In 2011-12, Adelaide Airport was the only monitored airport to report a decrease in passenger numbers, with passenger numbers decreasing by 4.0 per cent to 7.1 million passengers. A number of factors may have contributed to the drop in passenger numbers at Adelaide Airport, including subdued economic conditions, Tiger Airways ceasing operations at the airport from July 201119 and the Qantas grounding and associated industrial action.

Declining passenger numbers impacted on Adelaide Airport’s aeronautical revenue during 2011-12, with total aeronautical revenue decreasing by 9.3 per cent. The impact on aeronautical operating expenses was less pronounced, with total aeronautical operating expenses decreasing by 1.7 per cent.

In 2011-12, Adelaide Airport’s aeronautical operating margin decreased by 18.3 per cent and decreased by 14.8 per cent on a per passenger basis.

As a measure of investment in aeronautical services, Adelaide Airport’s additions as a percentage of tangible non-current assets for aeronautical services have been relatively low since the completion of the new multi-user terminal in 2006. However, Adelaide Airport has begun to increase its additions over the last two years, with additions increasing to 13.4 per cent of tangible non-current aeronautical assets in 2011-12. Adelaide Airport’s additions during 2011-12 have mostly related to the landside infrastructure project, which involved construction of a new car park and landside facilities.

Chart 1.3.1 shows that since the opening of its new multi-user terminal in 2006, quality of service results improved significantly at Adelaide Airport and have on average been rated as satisfactory or above. This is in contrast with the period prior to the opening of the new terminal, when Adelaide Airport recorded poor quality of service results.

19 Tiger Airways re-commenced operations at Adelaide Airport after the end of the 2011-12 financial year.

Overview of the monitoring results for aeronautical services Airport Monitoring Report 2011-12

6

Chart 1.3.1: Airlines’ average ratings for quality of service at Adelaide Airport, 2001-02 to 2011-12

It should be noted that following the release of the 2011-12 AMR, Adelaide Airport will be required to join the second-tier price and quality of service reporting process established by the National Aviation Policy White Paper in December 2009. This is a self-administered scheme, where the airport will be expected to disclose on its website:

• prices of aeronautical services

• prices of car parking services

• various quality of service outcomes

• airport complaint-handling processes and outcomes.

The reasons for this change to the monitoring regime are discussed in more detail in Adelaide Airport’s individual airport chapter (chapter 4).

1.3.2 Observations about Brisbane Airport