Air Transport Aircraft Production Outlook

19

Air Transport Aircraft Production Outlook Presented by Kevin Michaels, Partner Ann Arbor, Michigan • Amersham, United Kingdom • Singapore www.AeroStrategy.com October 6, 2010 Orlando, FL TITANIUM 2010 Conference - Economics Panel

Transcript of Air Transport Aircraft Production Outlook

Air Transport Aircraft

Production Outlook

Presented by

Kevin Michaels, Partner

Ann Arbor, Michigan • Amersham, United Kingdom • Singaporewww.AeroStrategy.com

October 6, 2010

Orlando, FL

TITANIUM 2010 Conference - Economics Panel

© 2010 AeroStrategy Titanium 2010 1

© 2010 AeroStrategy Titanium 2010 1

© 2010 AeroStrategy Titanium 2010 1

© 2010 AeroStrategy Titanium 2010 1

© 2010 AeroStrategy Titanium 2010

How Can Air Transport OEMs

Increase Production Rates On The

Heels Of A Global Recession?

6

© 2010 AeroStrategy Titanium 2010

Fuel Costs Have Increased 500% Since 2000…

7

Fuel Costs 1978 to present

(cents per gallon)

0

50

100

150

200

250

300

350

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Source: Airline Monitor; Air Transport Association

500%2002: 11% of

airline expenses

2008: 30% of

airline expenses

Production

Outlook

© 2010 AeroStrategy Titanium 2010

…And Over The Same Timeframe Airline Yields Were Flat, Creating A Major Imperative For Fuel Savings…

8

• Yields fell during

the 2002 and 2009

downturns and are

unchanged from

the beginning of

the decade

• Fuel is now 30% of

an airline’s cost

structure compared

to 10-12% earlier in

the decade

Fuel Costs vs. US Major Yields

1999 to presentFuel Cost

(cents/gallon)Yield

(in cents/RPM),

0

2

4

6

8

10

12

14

16

0

50

100

150

200

250

300

350

Yield

Fuel

Source: Airline Monitor; Air Transport Association

Production

Outlook

© 2010 AeroStrategy Titanium 2010

…As Evidenced By A Comparison Of MD-80 And B737NG Operating Economics…

9

Fuel Cost Per Passenger (USD)

DFW – New York LGA (1,447 miles)

MD-80

B737-800

$18/passenger cost difference with fuel at $2.60/gallon

Source: Dallas Morning News

Production

Outlook

© 2010 AeroStrategy Titanium 2010

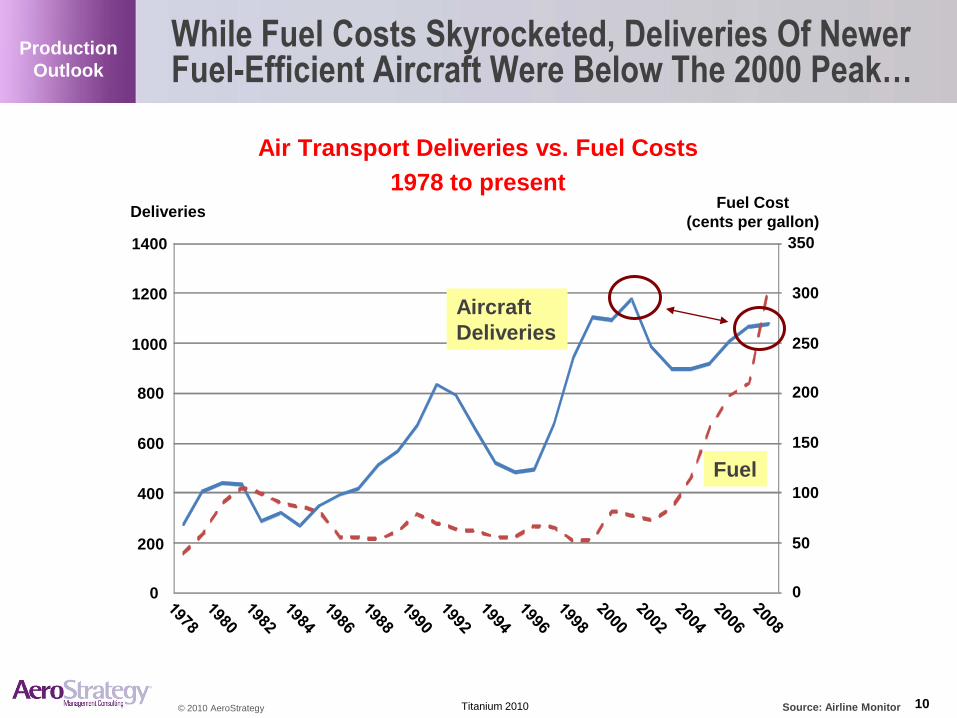

While Fuel Costs Skyrocketed, Deliveries Of Newer Fuel-Efficient Aircraft Were Below The 2000 Peak…

10

DeliveriesFuel Cost

(cents per gallon)

0

50

100

150

200

250

300

350

0

200

400

600

800

1000

1200

1400

Air Transport Deliveries vs. Fuel Costs

1978 to present

Aircraft

Deliveries

Fuel

Source: Airline Monitor

Production

Outlook

© 2010 AeroStrategy Titanium 2010

…Which Contributed To Record Backlogs For Air Transport Aircraft

11

• Airbus and Boeing

achieved record

backlogs in 2007/08

by maintaining

relatively steady

production during

record orders

• The backlog peaked

at 90 months – far in

excess of the

previous record of

55 months in the

late 1980s

Air Transport Backlog

1970 to presentBacklog

(as a % of Fleet)Production Backlog

(in months)

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

45

Source: Airline Monitor Feb 2010

% of Fleet

Months

Production

Outlook

© 2010 AeroStrategy Titanium 2010

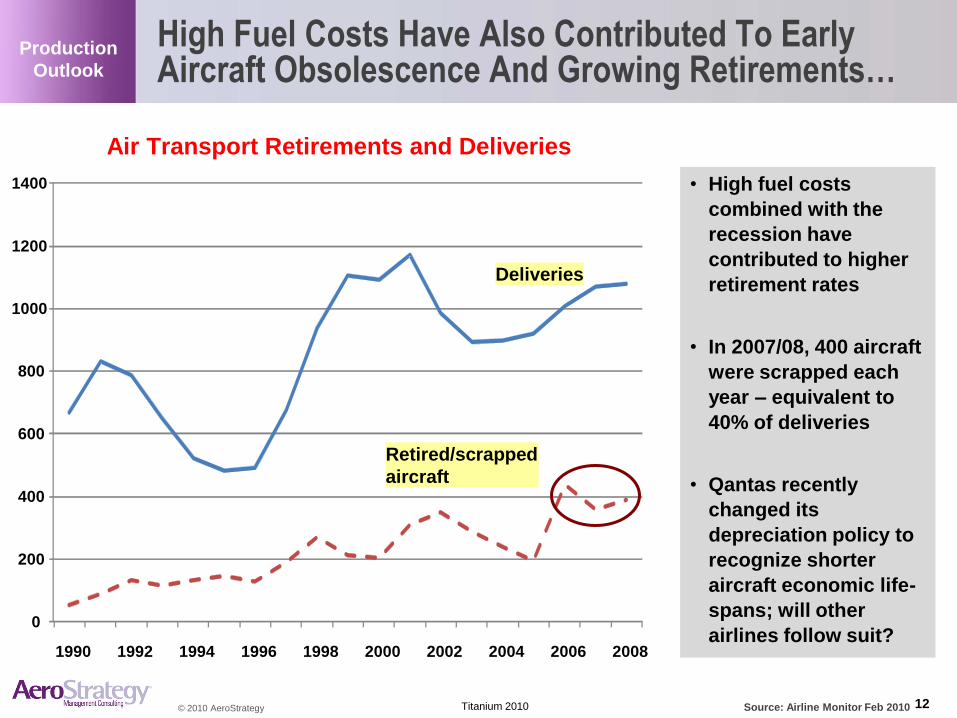

High Fuel Costs Have Also Contributed To Early Aircraft Obsolescence And Growing Retirements…

12

• High fuel costs

combined with the

recession have

contributed to higher

retirement rates

• In 2007/08, 400 aircraft

were scrapped each

year – equivalent to

40% of deliveries

• Qantas recently

changed its

depreciation policy to

recognize shorter

aircraft economic life-

spans; will other

airlines follow suit?

Source: Airline Monitor Feb 2010

0

200

400

600

800

1000

1200

1400

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Air Transport Retirements and Deliveries

Retired/scrapped

aircraft

Deliveries

Production

Outlook

© 2010 AeroStrategy Aviation Week MRO Europe 2010

12%

88%

…And A Small Portion Of The 1,500+ Parked Fleet Is Economically Viable At Current Fuel Prices…

13

Air Transport Fleet: Temporarily Inactive/ In Storage (Sept 2010)

1,553

High

potential to

return to

service at

current fuel

prices

Low-

moderate

potential /

obsolete

• Despite the large size (1,553) of the parked fleet, only a

small portion – 200 – is likely to return to service at

current fuel prices

• This equates to 1% of global capacity….or

approximately two months of production rates

Source: OAG Aviation

Aircraft Family Sep-10

737-3/4/500 201

MD80 181

DC9 136

737-1/200 106

146 74

727 73

EMB-135/140/145 78

757 54

747-1/2/300 47

747-400 47

CRJ-100/200 56

F100 48

A300-600 43

DC8-6/70 32

DC10 38

F28 31

328JET 29

A310 12

A300 19

MD11 9

717 9

L1011 12

707 10

F70 4

BAC 1-11 2

MD10 5

MD90 6

Total 1,362

Aircraft Family Sep-10

767 67

737-6/7/8/900 15

777 3

A320 Series 64

A330 11

A340 20

CRJ-700/900/1000 4

EMB-170/190 7

Total 191

Production

Outlook

© 2010 AeroStrategy Titanium 2010 14

High Potential – Return To Service

Air Transport Fleet: Temporarily Inactive/ In Storage (Sept 2010 vs. April 2010)

Low Potential – Return To Service

• The “high potential” parked fleet has

declined 48 (~20%) since April 2010;

most were likely returned to service

• The “low potential” fleet is also 110

smaller; most of this difference is due to

scrapping and “parting out” aircraft

…And The Parked Fleet Continues To Shrink –Primarily Due To Scrapping And Parting Out Aircraft

Source: OAG Aviation

© 2010 AeroStrategy Titanium 2010

Numerous Platforms – Including Two Chinese Programs -- Will Soon Enter The Narrowbody Market

15

2010 2011 2012 2014 2017 2018 2019 2020

737

Update

Next generation

single aisles

from Boeing

and Airbus

A320

Sharklet

CSeries

Re-Engined B737 or A320?

2015 20162013

Comac C919 Irkut MS-21

2020-2025

Production

Outlook

ARJ21

© 2010 AeroStrategy Titanium 2010

One Other Factor – EADS’s Need For Cash – Will Underpin Air Transport Production Rates

16Source: AeroStrategy analysis

Economic fallout of

skyrocketing fuel prices

Record production

backlogs

EADS need for cash- Mounting losses on A400M and A380

- Need to fund A350 XWB development

- A320 is a positive cash generator

Factors Sustaining Air Transport Production Rates

Production

Outlook

Emerging Single Aisle

Competition

© 2010 AeroStrategy Titanium 2010

Combined, These Factor Will Underpin Steady Production Rates Despite The Global Recession

17Source: AeroStrategy analysis

0

200

400

600

800

1000

1200

1400

2009 2010 2011 2012 2013 2014

Other

787 Family

A380767

EMB-170/175CRJ-700/900/1000

EMB-190/195

A330/A340 Family777 Family

A320 Family

737 Family

AeroStrategy Air Transport Delivery Forecast(March 2010)

Production

Outlook

Production rates will

be even higher after

the recently

announced B737 /

A320 production rate

increases materialize

© 2010 AeroStrategy Titanium 2010

There Will Be Interesting Dynamics For Individual Aircraft Models As Production Rates Increase

18

Aircraft Family 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Grand

Total

A320 Family 385 369 376 396 396 363 370 370 396 396 396 4,213

737 Family 284 372 360 360 360 336 336 336 360 360 360 3,824

787 Family 0 0 0 15 80 120 144 144 144 144 156 947

A330 72 76 80 80 71 74 51 41 38 36 36 655

777 Family 62 88 60 72 84 84 60 48 25 35 23 641

EMB-190/195 92 84 72 39 36 41 43 41 54 51 55 608

A350 0 0 0 0 0 0 26 66 96 120 120 428

CRJ-700/900/1000 50 60 45 24 21 20 20 26 28 30 32 356

EMB-170/175 64 33 23 20 20 22 20 23 29 22 26 302

A380 12 10 20 24 26 32 32 21 18 18 15 228

747 Family 14 8 8 18 21 24 24 20 20 20 16 193

ARJ 0 0 1 9 16 16 13 15 15 20 20 125

SUPERJET 0 0 6 8 12 15 15 15 15 15 15 116

C110/C130 0 0 0 0 0 0 2 10 20 30 30 92

MRJ 0 0 0 0 0 0 10 18 18 20 20 86

767 10 13 12 6 7 6 5 5 0 0 0 64

EMB-135/140/145 6 8 8 1 5 7 7 8 0 0 0 50

NEW 50SEAT RJ 0 0 0 0 0 0 0 0 0 0 33 33

A340 Family 12 10 8 0 0 0 0 0 0 0 0 30

Grand Total 1,063 1,131 1,079 1,072 1,155 1,160 1,178 1,207 1,276 1,317 1,353 12,991

Air Transport Delivery Forecast(March 2010)

A320 or B737 re-

engining in could

reduce single aisle

deliveries

considerably in mid-

2010s

A significant B777

refresh could increase

deliveries in late

2010s beyond the

current baseline

Higher fuel prices

could push C-Series

production rates well

beyond the current

forecast of 30/year

USAF tanker decision

could change

increase and extend

B767 production

considerably

Production

Outlook

Projected C919 introduction

In September 2010, Airbus announced a further

increase to 440/year; Boeing responded with

B737 rate of 38/mo (not integrated into forecast)

Source: AeroStrategy analysis

© 2010 AeroStrategy Titanium 2010

1

EMEALondon, England

43 Hill Avenue, Amersham

Buckinghamshire HP6 5BX

United Kingdom

Phone: +44 1494 431-600

Fax: +44 1494 434-500

Email: [email protected]

AmericasAnn Arbor, Michigan

101 North Main Street, Suite 400

Ann Arbor, Michigan 48104

United States of America

Phone: +1 734 821-0220

Fax: +1 734 821-0221

Email: [email protected]

Asia PacificSingapore

314 Tanglin Road, #01-05

Phoenix Park Office Campus

Singapore 247977

Phone: +65 9111-8435

Fax: +65 6884-4951

Email: [email protected]

www.aerostrategy.com

19