AIF Club Luxembourg - Presentation Real Estate Niche Workshop 16 October 2014

41

Real estate niche workshop Building momentum 16 October 2014

-

Upload

thorsten-lederer- -

Category

Presentations & Public Speaking

-

view

236 -

download

1

Transcript of AIF Club Luxembourg - Presentation Real Estate Niche Workshop 16 October 2014

Real estate niche workshop

Building momentum

16 October 2014

Page 2 Real estate niche workshop

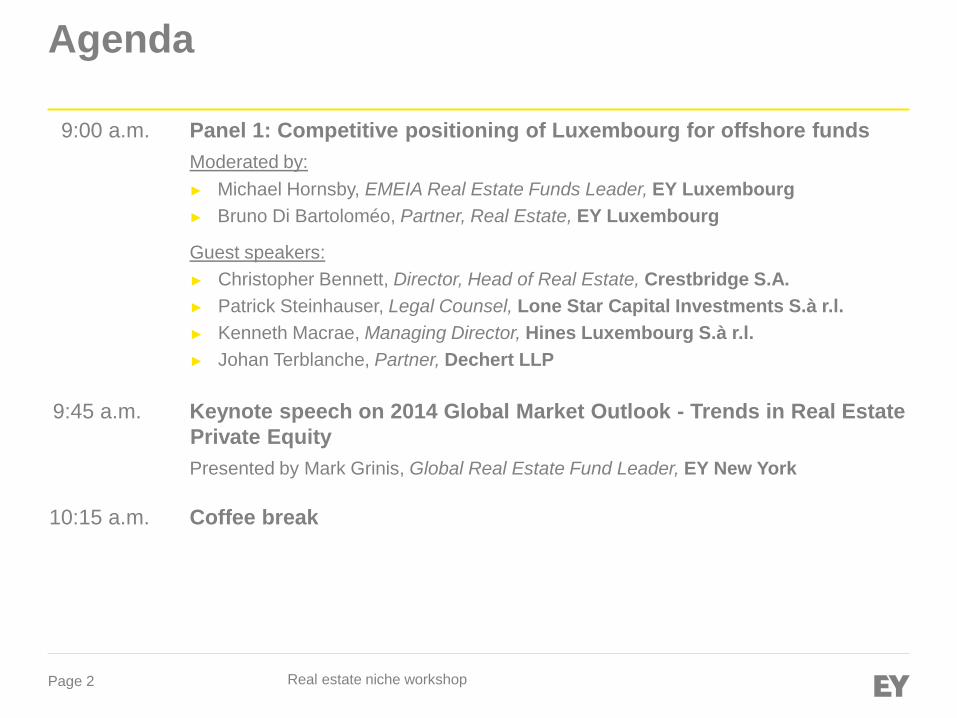

Agenda

9:00 a.m. Panel 1: Competitive positioning of Luxembourg for offshore funds

Moderated by:

► Michael Hornsby, EMEIA Real Estate Funds Leader, EY Luxembourg

► Bruno Di Bartoloméo, Partner, Real Estate, EY Luxembourg

Guest speakers:

► Christopher Bennett, Director, Head of Real Estate, Crestbridge S.A.

► Patrick Steinhauser, Legal Counsel, Lone Star Capital Investments S.à r.l.

► Kenneth Macrae, Managing Director, Hines Luxembourg S.à r.l.

► Johan Terblanche, Partner, Dechert LLP

9:45 a.m. Keynote speech on 2014 Global Market Outlook - Trends in Real Estate

Private Equity

Presented by Mark Grinis, Global Real Estate Fund Leader, EY New York

10:15 a.m. Coffee break

Page 3 Real estate niche workshop

Agenda (cont’d)

10:30 a.m. Panel 2: Does Luxembourg need a REIT regime?

Moderated by:

► Dietmar Klos, Partner, Head of Financial Services Tax, EY Luxembourg

► Mathieu Volckrick, Executive Director, Regulatory Services Leader, EY

Luxembourg

Guest speakers:

► Keith Burman, Partner, ManagementPlus (Luxembourg) S.A.

► Patrick Reuter, Partner, Elvinger, Hoss & Prussen

11:15 a.m Panel 3: Fund distribution and capital raising

Moderated by:

► Kai Braun, Executive Director, Alternatives Advisory Leader, EY Luxembourg

► Rafael Aguilera, Executive Director, Advisory Services, EY Luxembourg

Guest speakers:

► Marnix Arickx, CEO, BNP Paribas Investment Partners Belgium

► Rudolf Kömen, Head of Luxembourg based global fund product platform, Credit

Suisse

12:00 p.m. Wrap-up by Michael Hornsby

12:15 p.m. Networking lunch

Page 4 Real estate niche workshop

Panel 1 - Competitive positioning of Luxembourg for offshore funds

Page 5 Real estate niche workshop

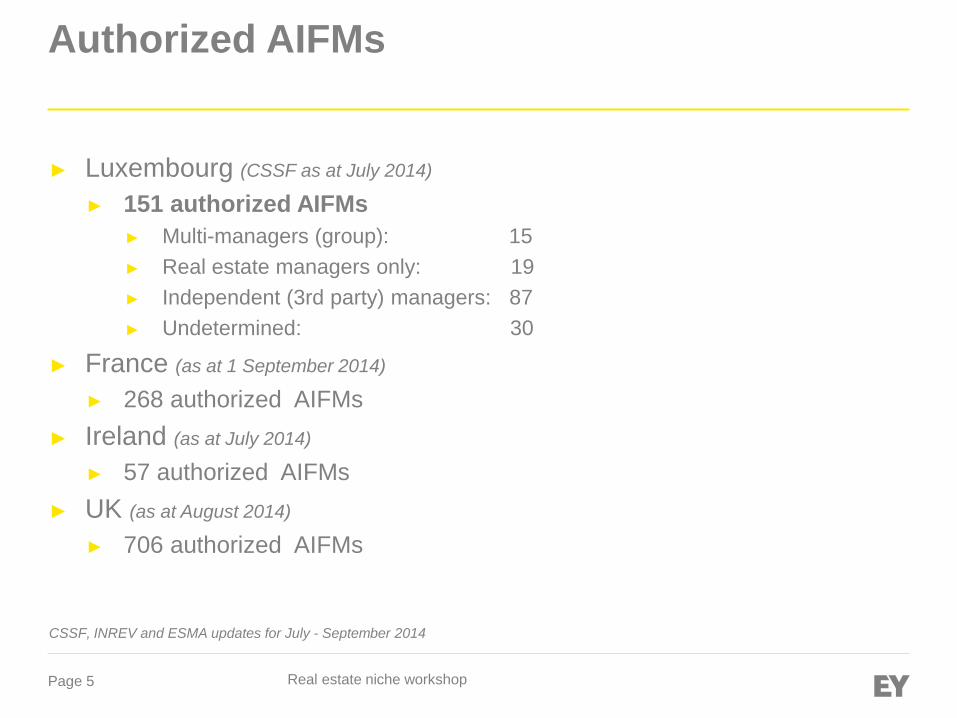

Authorized AIFMs

► Luxembourg (CSSF as at July 2014)

► 151 authorized AIFMs

► Multi-managers (group): 15

► Real estate managers only: 19

► Independent (3rd party) managers: 87

► Undetermined: 30

► France (as at 1 September 2014)

► 268 authorized AIFMs

► Ireland (as at July 2014)

► 57 authorized AIFMs

► UK (as at August 2014)

► 706 authorized AIFMs

CSSF, INREV and ESMA updates for July - September 2014

Page 6 Real estate niche workshop

Options for non-European managers wishing to access capital from European investors going forward

1. No longer market funds to European investors

2. Stay offshore with no active marketing in Europe (reverse solicitation)

3. Establish a European Feeder fund

4. Raise money from European investors through segregated accounts

5. Stay offshore in the mid-term, comply with transparency provisions

and access selected investors through remaining private placement

regimes

6. Stay offshore and seek AIFM equivalence for the non-EU manager

7. Set up on-shore entry point for EU investors for a global co-

investment platform

Page 7 Real estate niche workshop

Integrating AIFM into a global platform Global Model

Manager

Level US GP

Fund level

Asset level

Investment Advisor

EU AIFM US/Cayman GP

Investor

Level

SPV SPV SPV

SPV

SPV SPV

SPV

SPV

SPV

SPV SPV

Board

members A B C A D E A F G

GP/Decision

taker/Substance

Local series of

funds for 3

different investor

groups (ring-

fencing)

Asset

management

Investor Level

…

Local Governance

Administration

Transfer Agency

Depository control

Valuation

Marketing /

Placement agent

Global continuity

with local expertise

SPV

Delaware

Fund 3 Lux SIF 4

Cayman

Fund 3

EU investors US investors Asian / other

investors

Page 8 Real estate niche workshop

1. Create an attractive REIT regime

2. Promoter use of non-regulated AIF regime solely regulated through AIFMD

compliant Manager

3. Punctual improvements in SIF and SICAR regulatory practice

4. Create industry leading technical dialogue platform

5. Achieve positive reputation/market perception in terms of offering the most

efficient and quickest process for authorizing/ registering AIF/ AIFM

6. Enhance the attractiveness towards non-EU AIFMs choosing Luxembourg as

Member State of Reference

7. Resolve remaining taxation issues related to SCS/SCSp

8. Expand / update tax treaty network

9. Address BEPS concerns

Ideas for enhancing Luxembourg’s attractiveness

Page 9 Real estate niche workshop

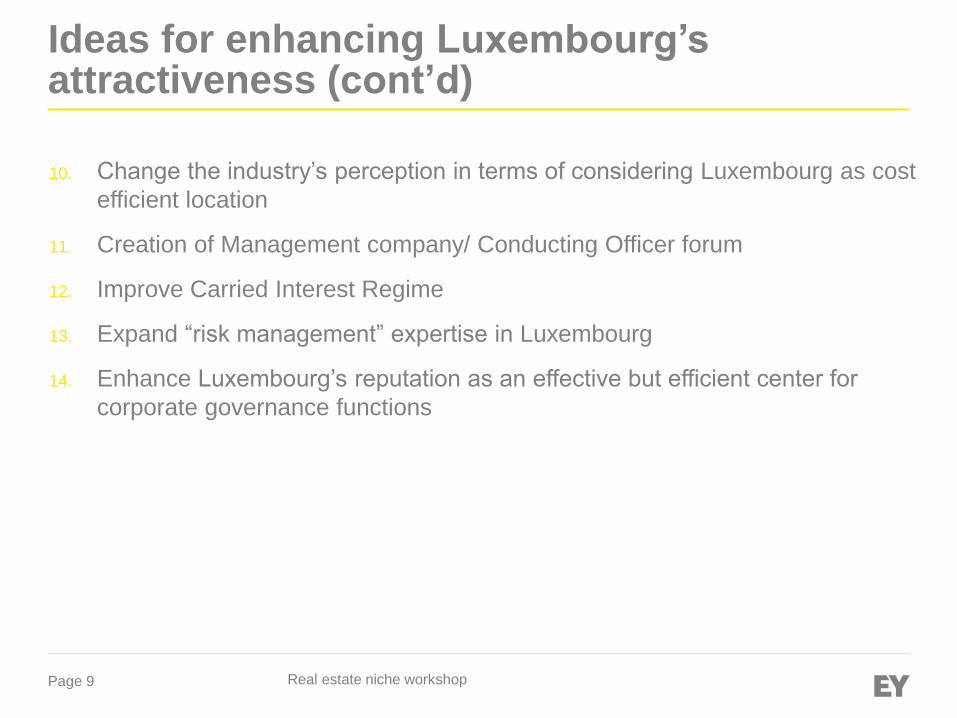

10. Change the industry’s perception in terms of considering Luxembourg as cost

efficient location

11. Creation of Management company/ Conducting Officer forum

12. Improve Carried Interest Regime

13. Expand “risk management” expertise in Luxembourg

14. Enhance Luxembourg’s reputation as an effective but efficient center for

corporate governance functions

Ideas for enhancing Luxembourg’s attractiveness (cont’d)

Page 10 Real estate niche workshop

Panel 1 - guest speakers

Guest speakers:

► Christopher Bennett, Director, Head of Real Estate, Crestbridge S.A.

► Patrick Steinhauser, Legal Counsel, Lone Star Capital Investments

S.à r.l.

► Kenneth Macrae, Managing Director, Hines Luxembourg S.à r.l.

► Johan Terblanche, Partner, Dechert LLP

Moderators:

► Michael Hornsby, EMEIA Real Estate Funds Leader, EY Luxembourg

► Bruno Di Bartoloméo, Partner, Real Estate, EY Luxembourg

Real Estate Renaissance

Real Estate Private Equity Funds

Global Market Outlook

Luxembourg 16 October 2014

Page 12

Location, Location, Location London Underground ca. 1860

Real Estate Renaissance 16 October 2014

Page 13

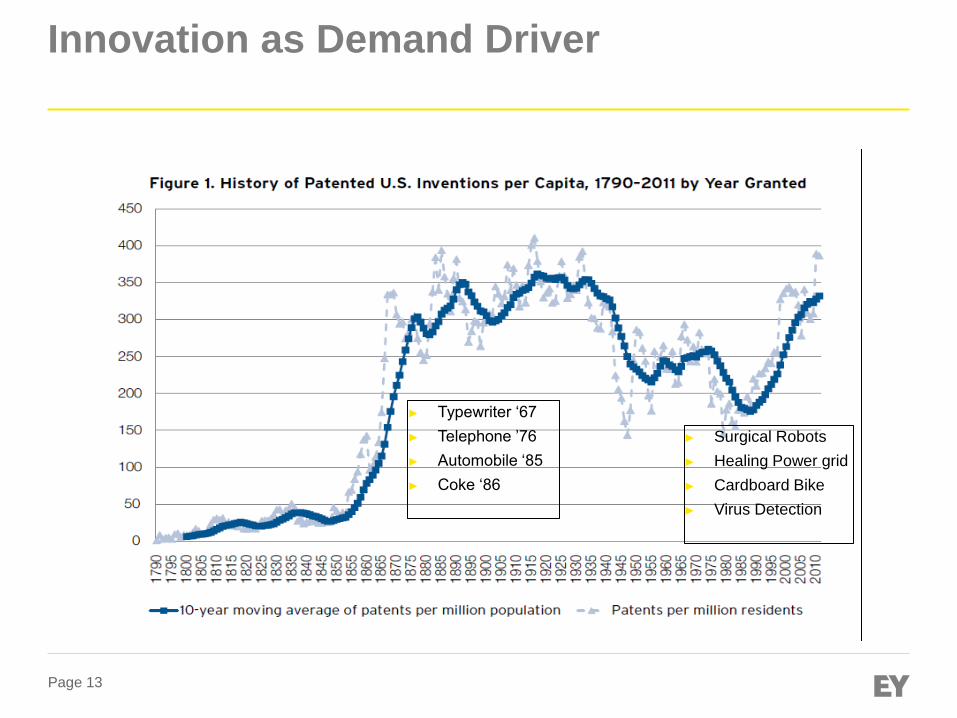

Innovation as Demand Driver

► Typewriter ‘67

► Telephone ’76

► Automobile ‘85

► Coke ‘86

► Surgical Robots

► Healing Power grid

► Cardboard Bike

► Virus Detection

Page 14

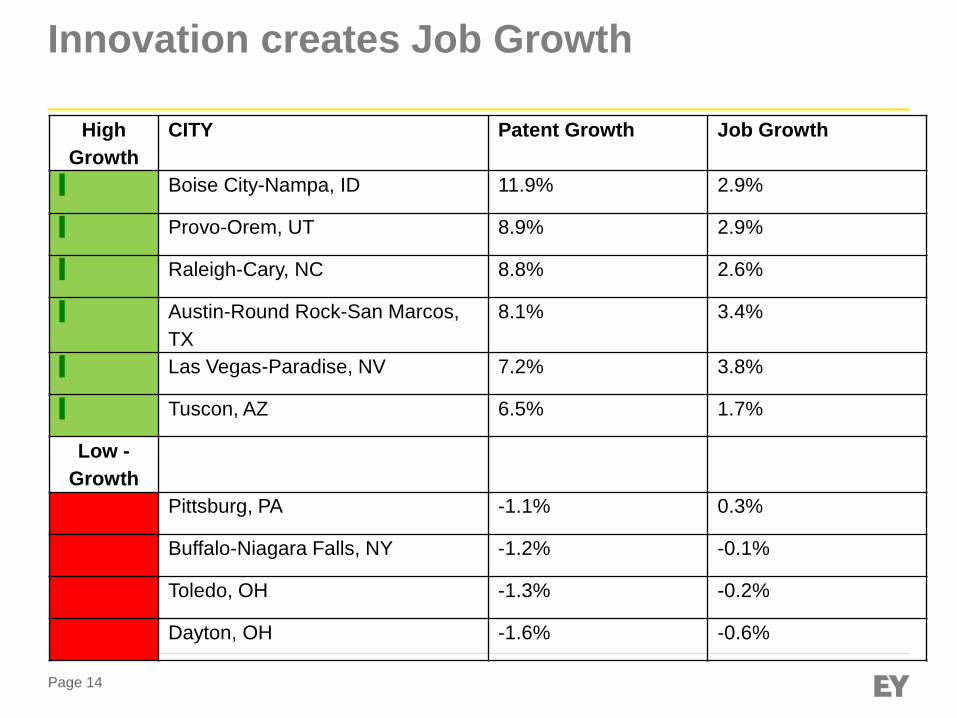

Innovation creates Job Growth

High

Growth

CITY Patent Growth Job Growth

Boise City-Nampa, ID 11.9% 2.9%

Provo-Orem, UT 8.9% 2.9%

Raleigh-Cary, NC 8.8% 2.6%

Austin-Round Rock-San Marcos,

TX

8.1% 3.4%

Las Vegas-Paradise, NV 7.2% 3.8%

Tuscon, AZ 6.5% 1.7%

Low -

Growth

Pittsburg, PA -1.1% 0.3%

Buffalo-Niagara Falls, NY -1.2% -0.1%

Toledo, OH -1.3% -0.2%

Dayton, OH -1.6% -0.6%

Page 15

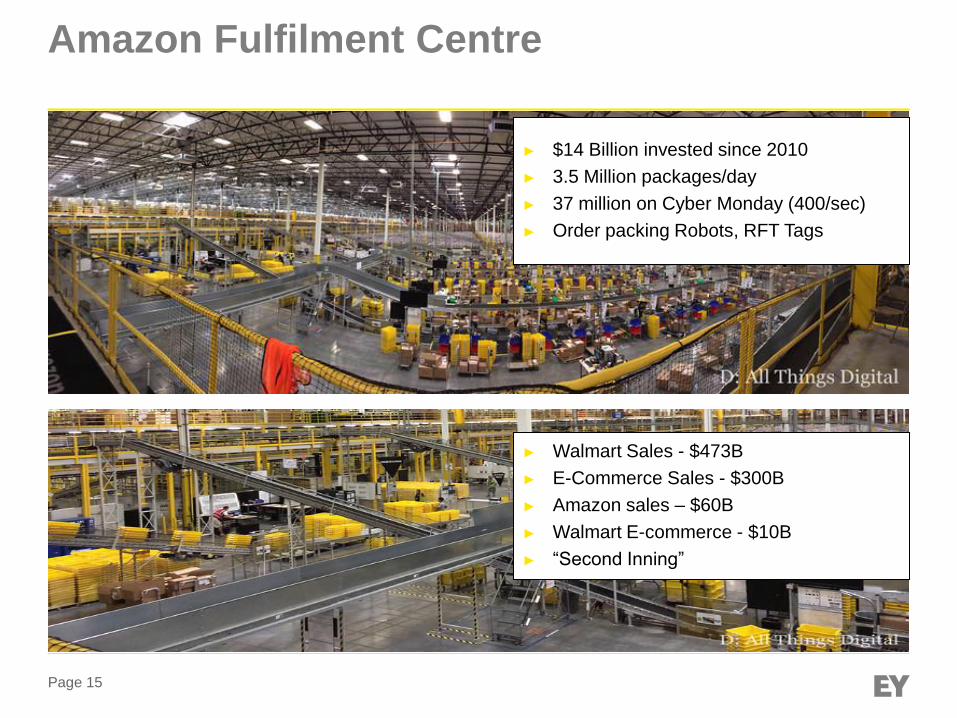

Amazon Fulfilment Centre

► Walmart Sales - $473B

► E-Commerce Sales - $300B

► Amazon sales – $60B

► Walmart E-commerce - $10B

► “Second Inning”

► $14 Billion invested since 2010

► 3.5 Million packages/day

► 37 million on Cyber Monday (400/sec)

► Order packing Robots, RFT Tags

Page 16

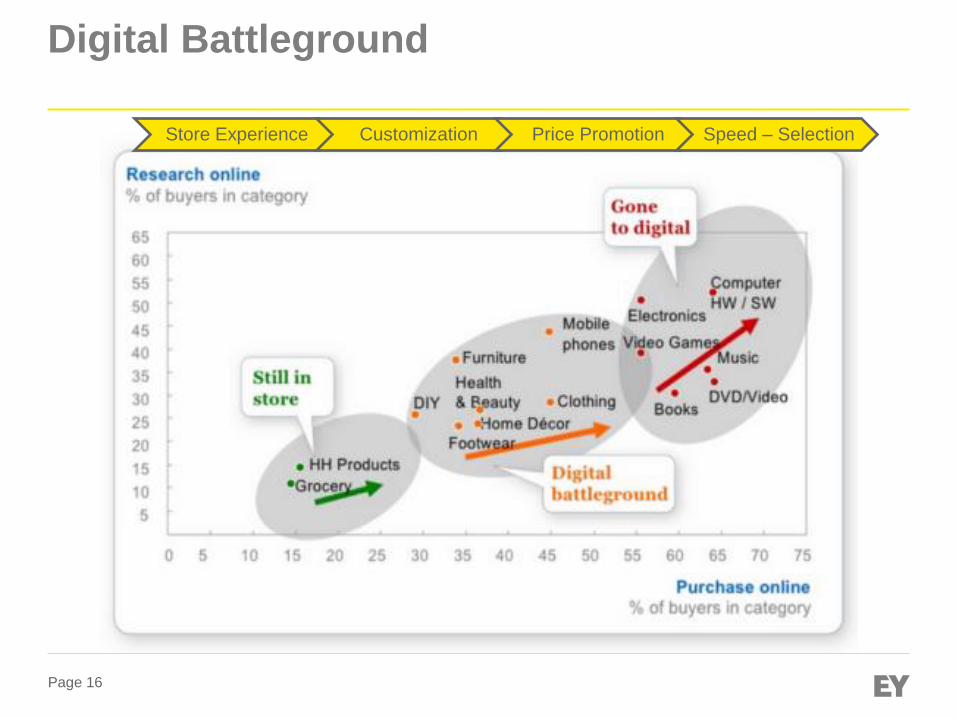

Digital Battleground

Store Experience Customization Price Promotion Speed – Selection

Page 17

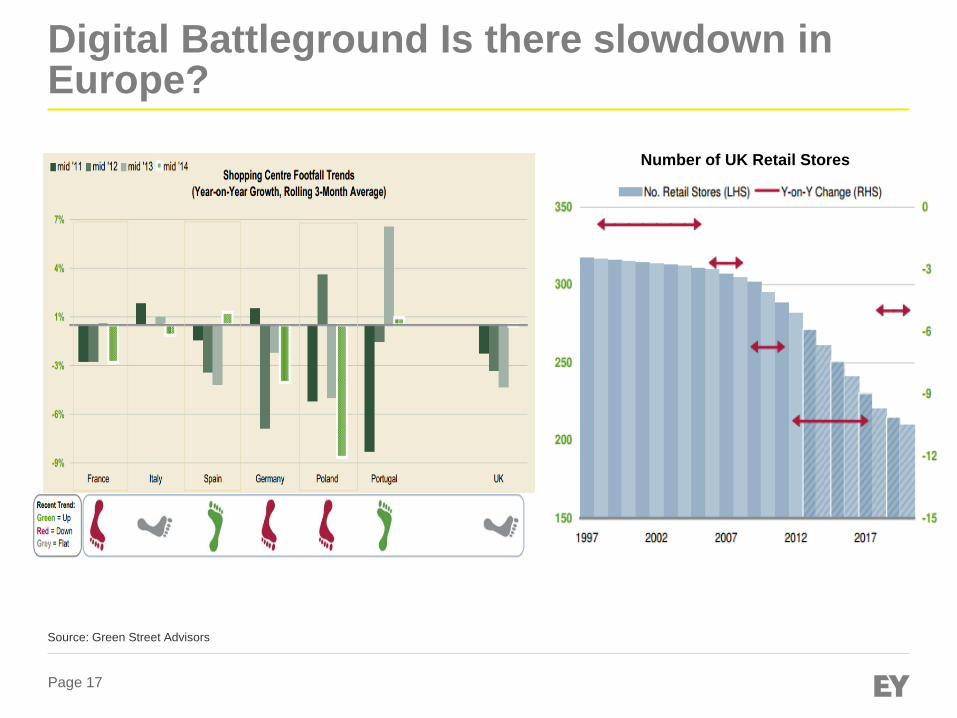

Digital Battleground Is there slowdown in Europe?

Number of UK Retail Stores

Source: Green Street Advisors

Page 18

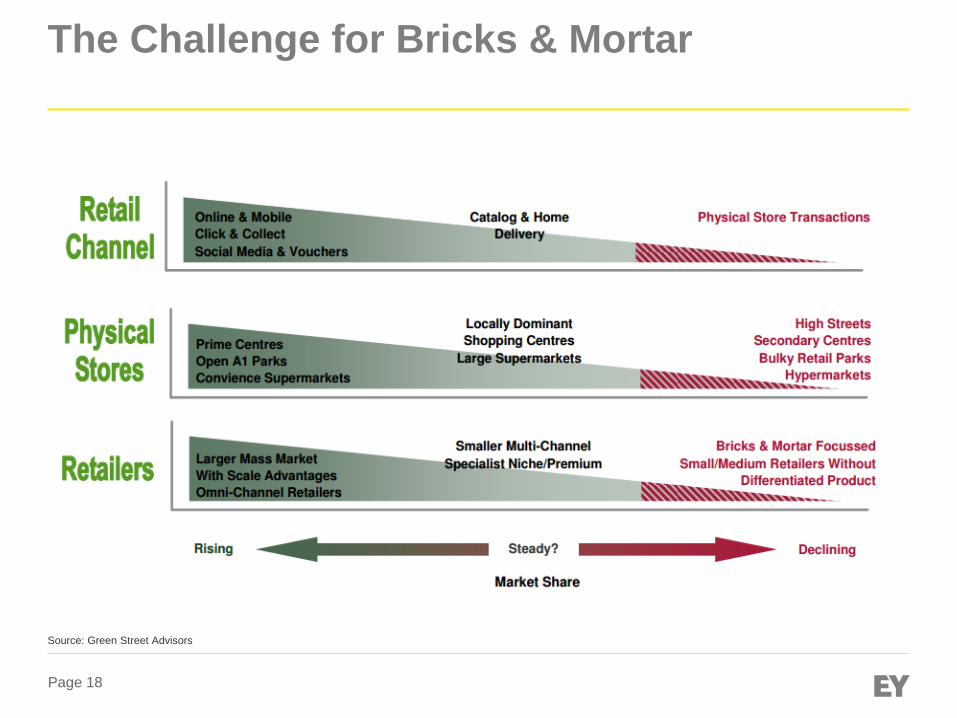

The Challenge for Bricks & Mortar

Source: Green Street Advisors

Page 19

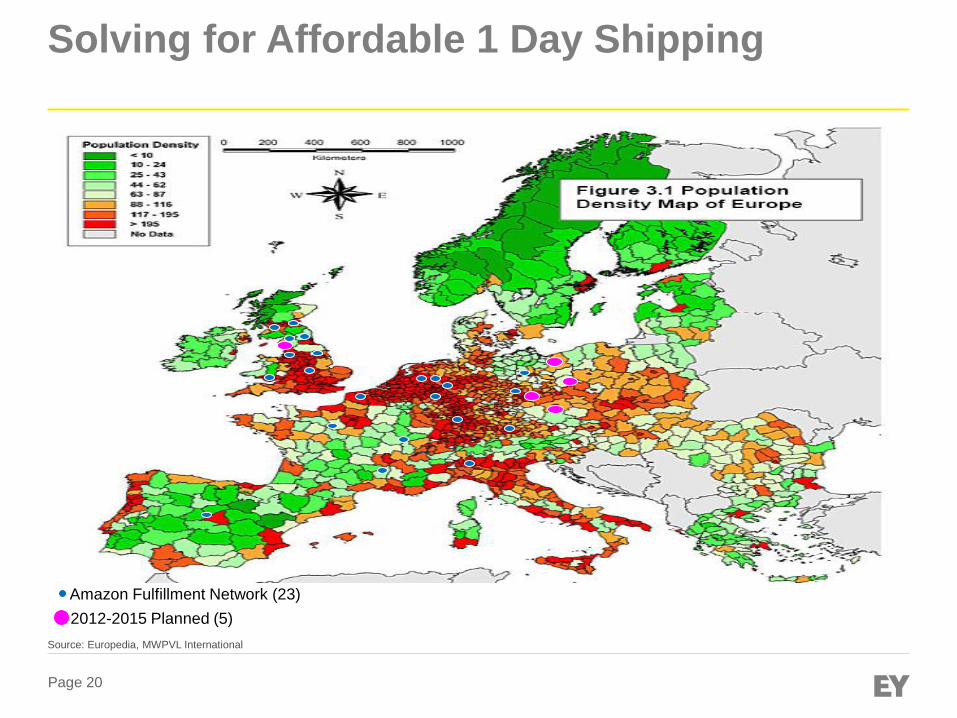

E-commerce

The Online Challenge

Consumers will not select an online retailer when:

► Delivery costs are High

► Cannot offer Next Day Delivery

90% of companies offer Next Day shipping at generally 4x of

ground

NOT SUSTAINABLE

Page 20

Solving for Affordable 1 Day Shipping

Amazon Fulfillment Network (23)

2012-2015 Planned (5)

Source: Europedia, MWPVL International

Page 21

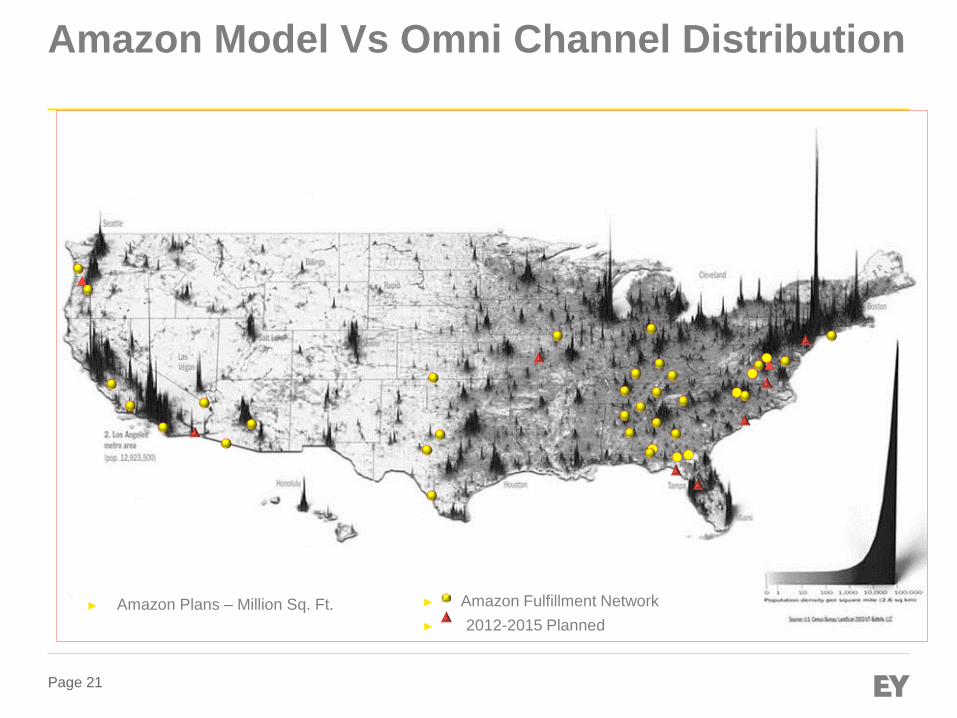

Amazon Model Vs Omni Channel Distribution

► Amazon Fulfillment Network

► 2012-2015 Planned

► Amazon Plans – Million Sq. Ft.

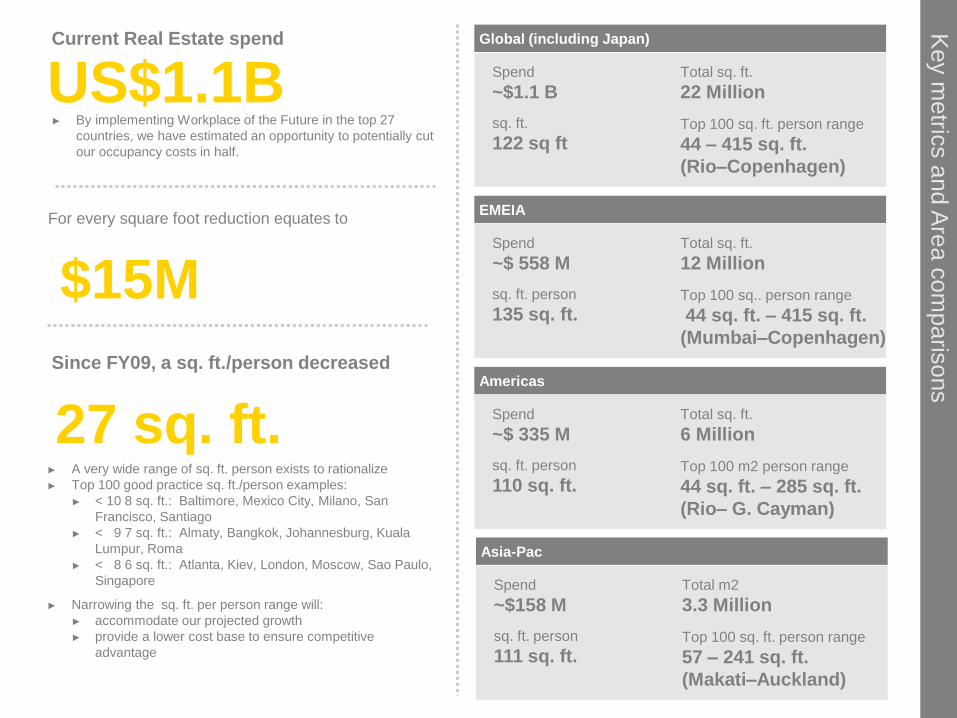

Key m

etric

s a

nd A

rea c

om

paris

ons

27 sq. ft.

Since FY09, a sq. ft./person decreased

$15M

► A very wide range of sq. ft. person exists to rationalize

► Top 100 good practice sq. ft./person examples:

► < 10 8 sq. ft.: Baltimore, Mexico City, Milano, San

Francisco, Santiago

► < 9 7 sq. ft.: Almaty, Bangkok, Johannesburg, Kuala

Lumpur, Roma

► < 8 6 sq. ft.: Atlanta, Kiev, London, Moscow, Sao Paulo,

Singapore

► Narrowing the sq. ft. per person range will:

► accommodate our projected growth

► provide a lower cost base to ensure competitive

advantage

Global (including Japan)

Top 100 sq. ft. person range

44 – 415 sq. ft.

(Rio–Copenhagen)

Spend

~$1.1 B Total sq. ft.

22 Million

sq. ft.

122 sq ft

EMEIA

Top 100 sq.. person range

44 sq. ft. – 415 sq. ft.

(Mumbai–Copenhagen)

Spend

~$ 558 M Total sq. ft.

12 Million

sq. ft. person

135 sq. ft.

Americas

Top 100 m2 person range

44 sq. ft. – 285 sq. ft.

(Rio– G. Cayman)

Spend

~$ 335 M Total sq. ft.

6 Million

sq. ft. person

110 sq. ft.

Asia-Pac

Top 100 sq. ft. person range

57 – 241 sq. ft.

(Makati–Auckland)

Spend

~$158 M Total m2

3.3 Million

sq. ft. person

111 sq. ft.

US$1.1B Current Real Estate spend

► By implementing Workplace of the Future in the top 27

countries, we have estimated an opportunity to potentially cut

our occupancy costs in half.

For every square foot reduction equates to

Work

pla

ce o

f the F

utu

re 1

2 K

ey In

dic

ato

rs

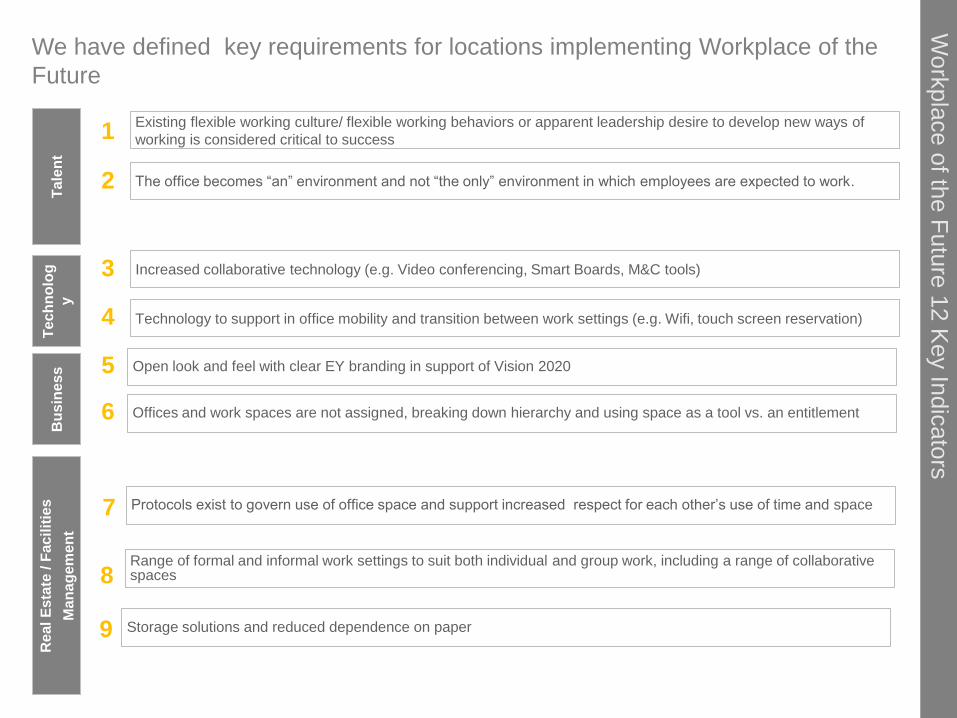

We have defined key requirements for locations implementing Workplace of the

Future

Te

ch

no

log

y

Increased collaborative technology (e.g. Video conferencing, Smart Boards, M&C tools)

1

Technology to support in office mobility and transition between work settings (e.g. Wifi, touch screen reservation)

2

Ta

len

t

3

Existing flexible working culture/ flexible working behaviors or apparent leadership desire to develop new ways of

working is considered critical to success

4

The office becomes “an” environment and not “the only” environment in which employees are expected to work.

5

Re

al E

sta

te / F

ac

ilit

ies

Man

ag

em

en

t

Offices and work spaces are not assigned, breaking down hierarchy and using space as a tool vs. an entitlement 6

7

Open look and feel with clear EY branding in support of Vision 2020

8

Protocols exist to govern use of office space and support increased respect for each other’s use of time and space

9

Range of formal and informal work settings to suit both individual and group work, including a range of collaborative spaces

Storage solutions and reduced dependence on paper

Bu

sin

es

s

2014 Global market outlook

Trends in real estate private equity Executive summary

Page 25

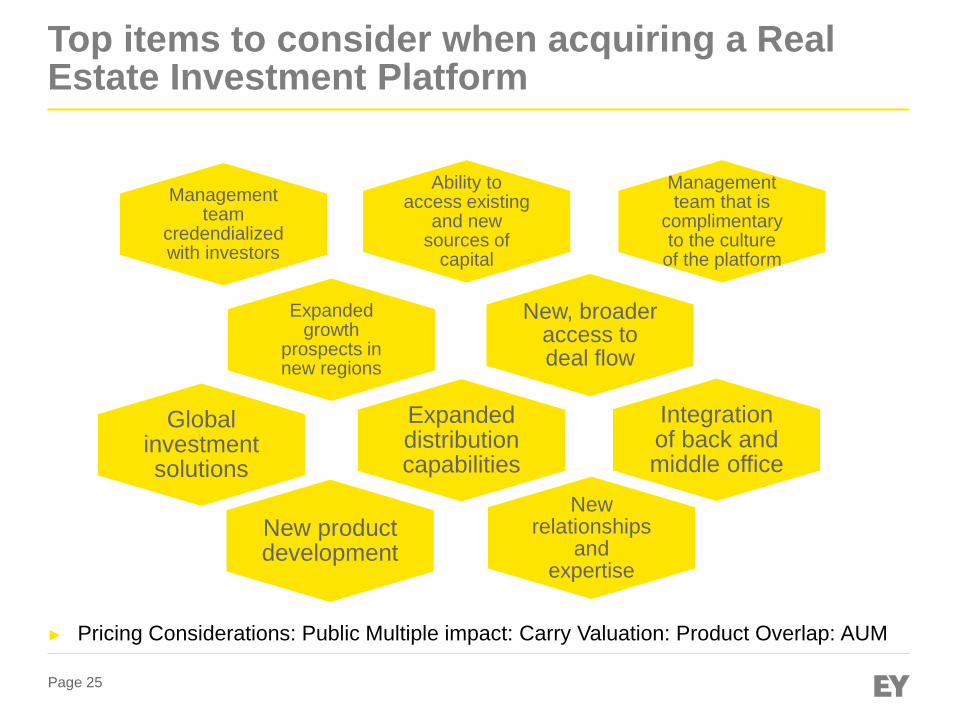

Top items to consider when acquiring a Real Estate Investment Platform

Ability to access existing

and new sources of

capital

Management team

credendialized with investors

Management team that is

complimentary to the culture

of the platform

Expanded growth

prospects in new regions

Global investment solutions

New, broader access to deal flow

Expanded distribution capabilities

New product development

New relationships

and expertise

Integration of back and middle office

► Pricing Considerations: Public Multiple impact: Carry Valuation: Product Overlap: AUM

Page 26

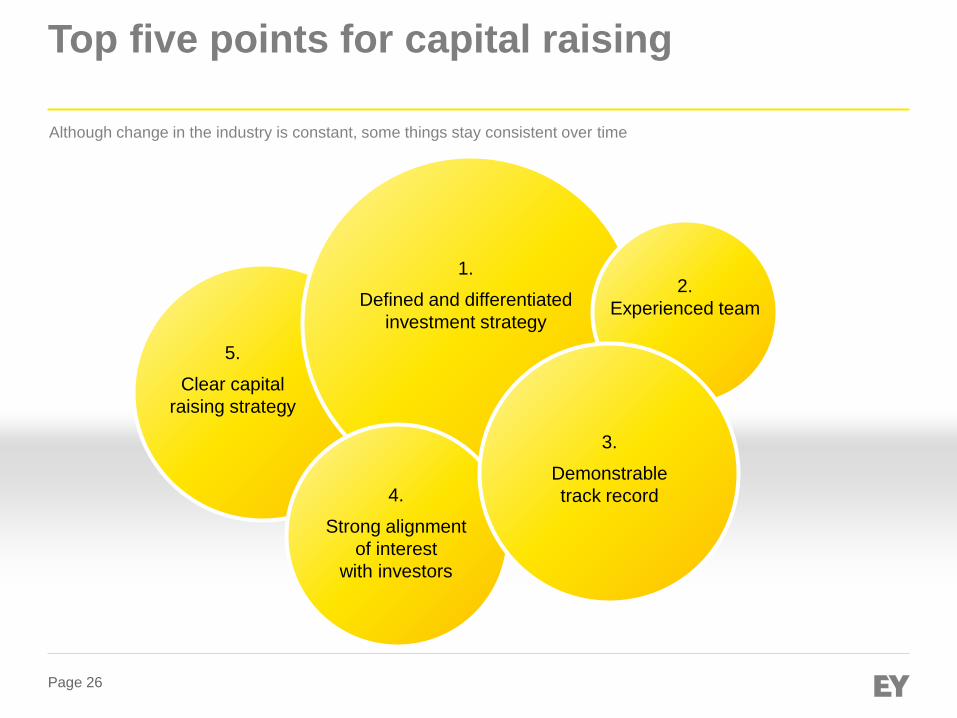

Top five points for capital raising

1.

Defined and differentiated

investment strategy

3.

Demonstrable

track record

2.

Experienced team

4.

Strong alignment

of interest

with investors

5.

Clear capital

raising strategy

Although change in the industry is constant, some things stay consistent over time

Page 27

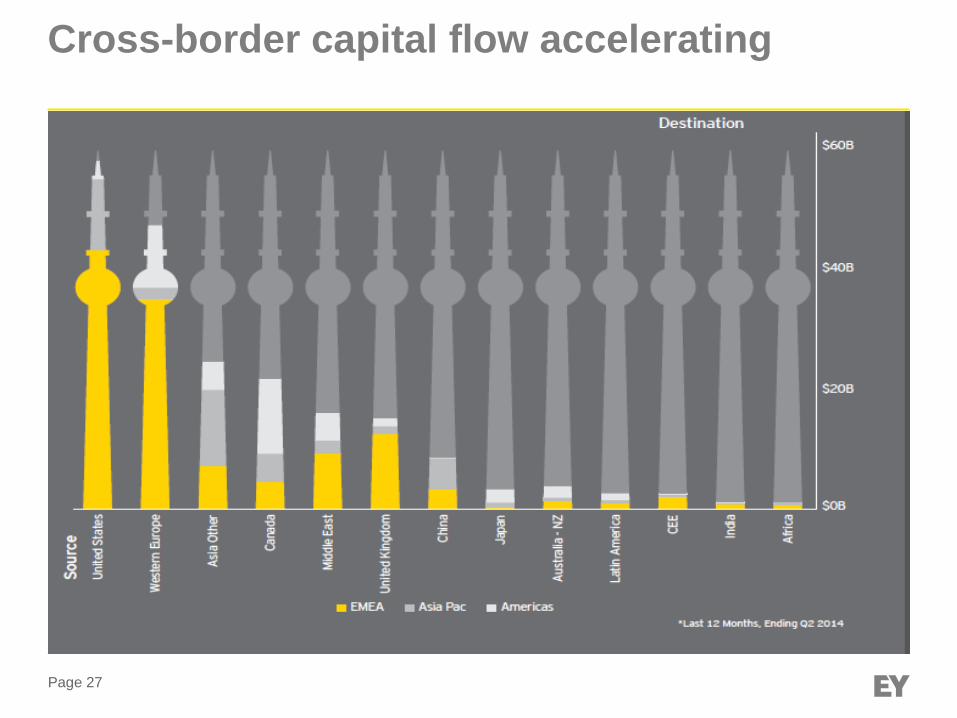

Cross-border capital flow accelerating

Page 28

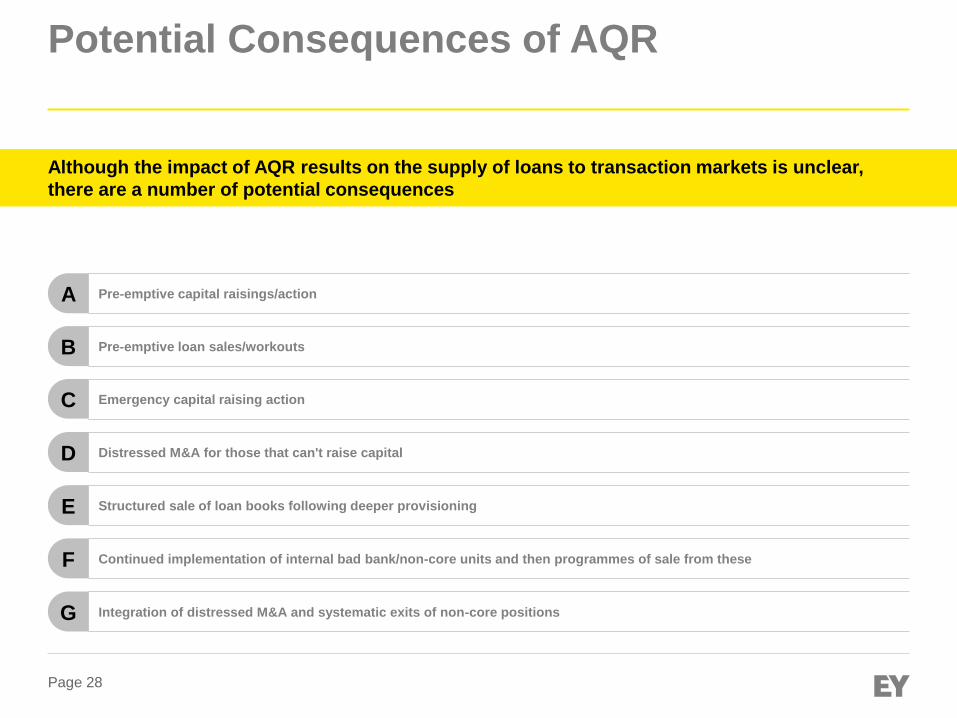

Potential Consequences of AQR

A Pre-emptive capital raisings/action

B Pre-emptive loan sales/workouts

C Emergency capital raising action

D Distressed M&A for those that can't raise capital

E Structured sale of loan books following deeper provisioning

F Continued implementation of internal bad bank/non-core units and then programmes of sale from these

Integration of distressed M&A and systematic exits of non-core positions G

Although the impact of AQR results on the supply of loans to transaction markets is unclear,

there are a number of potential consequences

Page 29

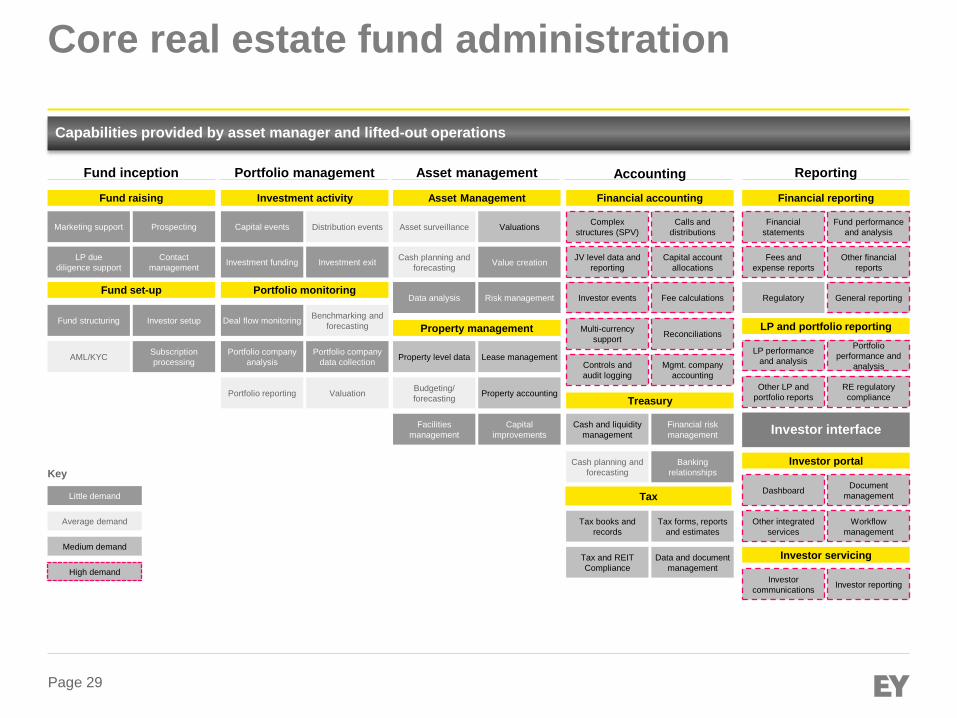

Investor

communications Investor reporting

Dashboard

Other integrated

services

Document

management

Workflow

management

LP performance

and analysis

Other LP and

portfolio reports

Portfolio

performance and

analysis

RE regulatory

compliance

Financial

statements

Fees and

expense reports

Fund performance

and analysis

Other financial

reports

General reporting

Multi-currency

support Reconciliations

Controls and

audit logging

Mgmt. company

accounting

Complex

structures (SPV)

Calls and

distributions

JV level data and

reporting

Capital account

allocations

Investor events Fee calculations

Fund inception Portfolio management Asset management Reporting Accounting

Fund set-up Portfolio monitoring

Fund raising Investment activity Asset Management Financial reporting Financial accounting

LP and portfolio reporting

Tax

Treasury

Property management

Investor portal

Investor servicing

Investor interface

Marketing support Prospecting

LP due

diligence support

Contact

management

Fund structuring Investor setup Benchmarking and

forecasting Deal flow monitoring

Tax and REIT

Compliance

Data and document

management

Cash planning and

forecasting

Banking

relationships

AML/KYC Subscription

processing

Portfolio company

data collection

Portfolio company

analysis Property level data Lease management

Valuation Portfolio reporting Budgeting/

forecasting Property accounting

Cash and liquidity

management

Financial risk

management

Facilities

management

Capital

improvements

Distribution events Capital events Asset surveillance Valuations

Investment exit Investment funding Cash planning and

forecasting Value creation

Data analysis Risk management Regulatory

Tax books and

records

Tax forms, reports

and estimates

Key

High demand

Little demand

Medium demand

Average demand

Core real estate fund administration

Capabilities provided by asset manager and lifted-out operations

Page 30

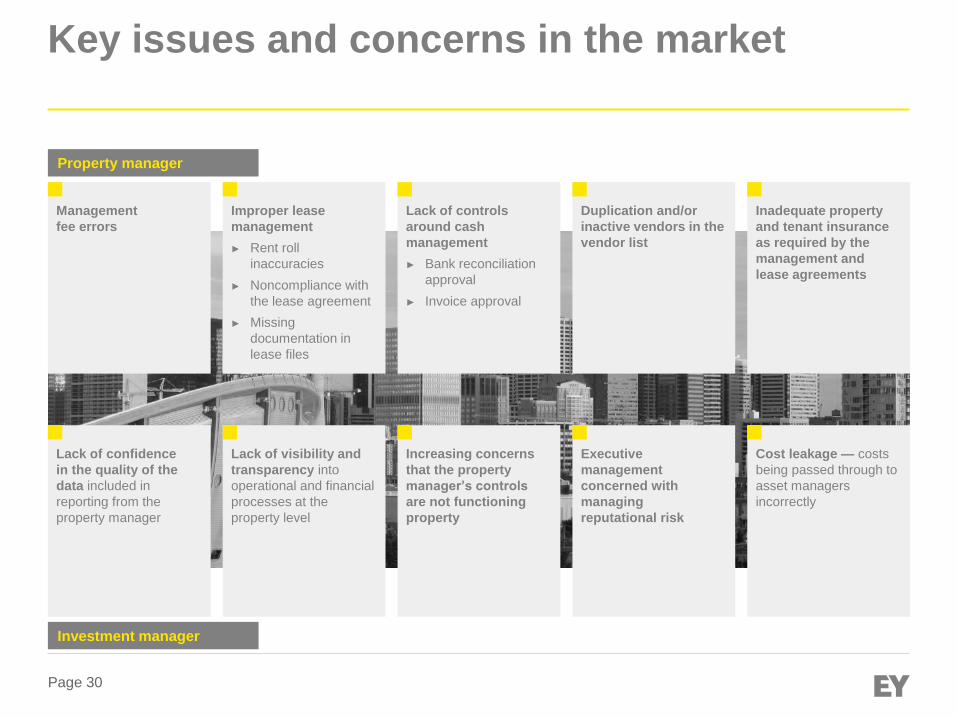

Key issues and concerns in the market

Management

fee errors

Improper lease

management

► Rent roll

inaccuracies

► Noncompliance with

the lease agreement

► Missing

documentation in

lease files

Lack of controls

around cash

management

► Bank reconciliation

approval

► Invoice approval

Duplication and/or

inactive vendors in the

vendor list

Inadequate property

and tenant insurance

as required by the

management and

lease agreements

Property manager

Lack of confidence

in the quality of the

data included in

reporting from the

property manager

Lack of visibility and

transparency into

operational and financial

processes at the

property level

Increasing concerns

that the property

manager’s controls

are not functioning

property

Executive

management

concerned with

managing

reputational risk

Cost leakage — costs

being passed through to

asset managers

incorrectly

Investment manager

Thank you.

Page 32 Real estate niche workshop

Panel 2 - Does Luxembourg need a REIT regime?

Page 33 Real estate niche workshop

Panel 2 - guest speakers

Guest speakers:

► Keith Burman, Partner, ManagementPlus (Luxembourg) S.A.

► Patrick Reuter, Partner, Elvinger, Hoss & Prussen

Moderators:

► Dietmar Klos, Partner, Head of Financial Services Tax,

EY Luxembourg

► Mathieu Volckrick, Executive Director, Regulatory Services Leader,

EY Luxembourg

Page 34 Real estate niche workshop

What is a REIT?

REIT is

► a generic concept commonly used in order to refer to an investment

vehicle (usually widely held)

► that derives its income primarily from long-term investment in

immovable property

► and that benefits from a flow-through tax regime on its (direct and

indirect) real estate income and gains

► These vehicles usually provide for a single-level of taxation in the hands

of the investors in the REIT

Page 35 Real estate niche workshop

What is a REIT?

Tax considerations

► General: Taxation of REITs should ideally enable the investor to obtain a

similar after tax result to what would occur had they invested directly in

property (single-level taxation)

► Flow-through entity (partnership or contractual)

► No taxation at REIT level

► Taxation at property level as well as investor level to be considered

► Corporate REIT

► Tax exemption recommendable (exemption as such, exemption of RE

income, or eligible to claim a deduction for distributions to investors)

► WHT considerations

► Access to double tax treaties and EU Directives

► Taxation at property level as well as investor level to be considered

Page 36 Real estate niche workshop

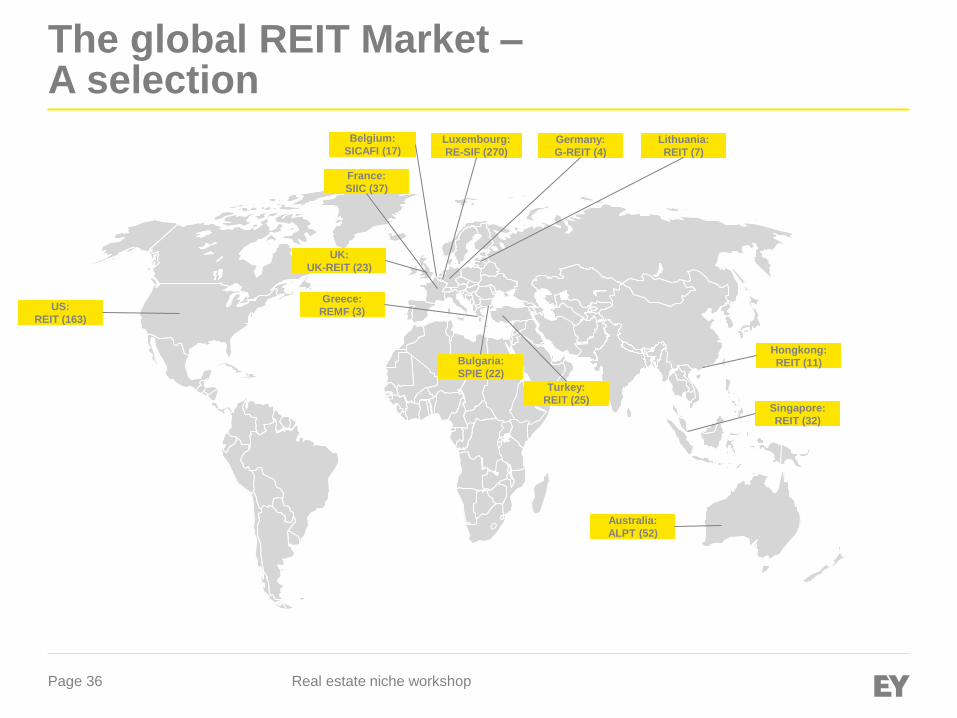

The global REIT Market – A selection

Belgium:

SICAFI (17) Luxembourg:

RE-SIF (270)

Germany:

G-REIT (4)

Lithuania:

REIT (7)

France:

SIIC (37)

US:

REIT (163)

Bulgaria:

SPIE (22)

Singapore:

REIT (32)

UK:

UK-REIT (23)

Hongkong:

REIT (11)

Greece:

REMF (3)

Australia:

ALPT (52)

Turkey:

REIT (25)

Page 37 Real estate niche workshop

Panel 3 - Fund distribution and capital raising

Page 38 Real estate niche workshop

Panel 3 - guest speakers

Guest speakers:

► Marnix Arickx, CEO, BNP Paribas Investment Partners Belgium

► Rudolf Kömen, Head of Luxembourg based global fund product

platform, Credit Suisse

Moderators:

► Kai Braun, Executive Director, Alternatives Advisory Leader,

EY Luxembourg

► Rafael Aguilera, Executive Director, Advisory Services,

EY Luxembourg

Page 39 Real estate niche workshop

Wrap-up

Thank you.

Page 41 Real estate niche workshop

Contacts

Michael Hornsby

Partner

EMEIA Real Estate Funds Leader

+352 42 124 8310

Bruno Di Bartoloméo

Partner

Real Estate

+352 42 124 8493

Dietmar Klos

Partner

Head of Financial Services Tax

+352 42 124 7282

Rafael Aguilera

Executive Director

Advisory Services

+352 42 124 8365

Kai Braun

Executive Director

Alternatives Advisory Leader

+352 42 124 8800

Mark Grinis

Partner

Global Real Estate Fund Leader

+1 212 7735 148

Mathieu Volckrick

Executive Director

Regulatory Services Leader

+352 42 124 7014