Agriculture Sector Analysis 300113

24

India Agricultural Sector review

-

Upload

arnav-sarkar -

Category

Documents

-

view

225 -

download

1

description

agricultural sector review INDIA

Transcript of Agriculture Sector Analysis 300113

India Agricultural Sector review

Overview

• Post independence till 1964. Reliance on imported food and Food AID from Developed countries and UN.

• 1960s –Green Revolution (wheat)• 1970s – extension to Rice – poorly irrigated areas.

Tube well system of irrigation increased.• 1980s - White revolution (milk)• 1990s - Yellow revolution (vegetable oils)• 2000s - Blue revolution (fisheries)• 2010s - Pink revolution (horticulture)

Overview

• Punjab, UP, MP, Haryana, Bihar top 5• Agriculture is a state list item and central govt can not

form uniform national policies• MSP generally is below market prices due to

inefficiency

Quick overview

• 20.43% of electricity consumption• Rs 8349 Cr import of fertilizer (8% of import bill)• 46 mn farmers covered under NAIS• Average size of holdings: 1.23 ha• Nearly 50% unirrigated• MSP and PDS systems• Various environmental concerns

• Fertilizers and pesticides• Animal husbandry

Farm SubsidiesCountry Subsidy / ha ($) % Pop dependent on

agriculture

USA 32 5

Japan 35 4

China 30 24

S Africa 24 18

India 14 60

Farm Subsidies

• Accounts for 40% of subsidy bill (Rs 190 K Cr); around 0.8% of GDP

• 87% through fertilizer subsidies (Rs 67K Cr)• 13% through electricity subsidies (Rs 10 K Cr)

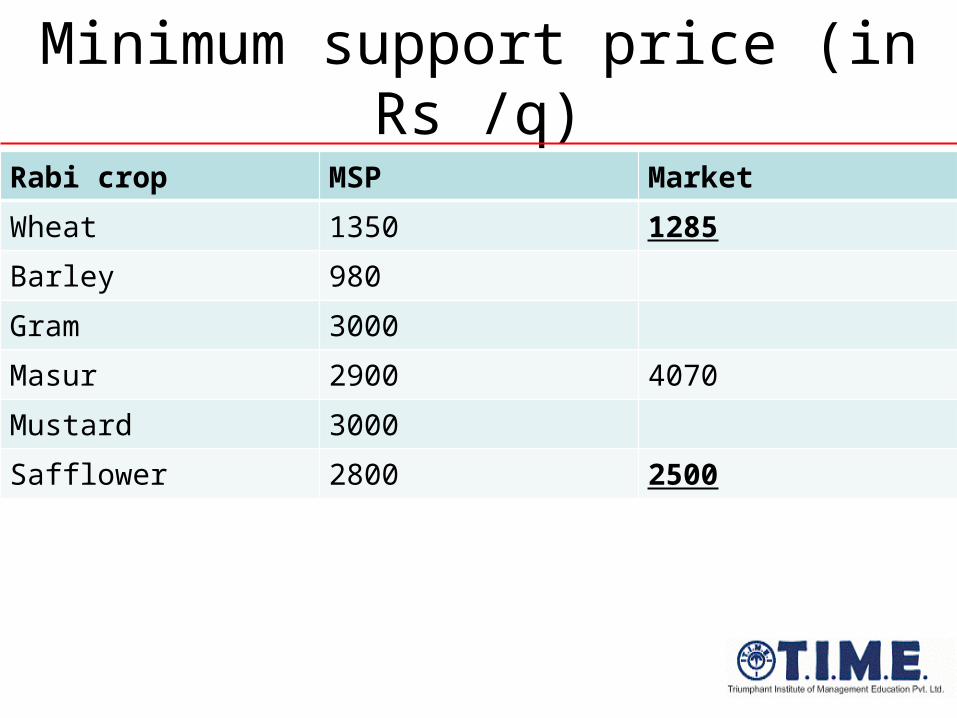

Minimum support price (in Rs /q)

Kharif crop MSP Market

Paddy 1250 1300

Jowar / Ragi 1500 1500

Bajra / Maize 1175 1175

Arhar 3200 3850

Moong 3500 4400

Urad 4300 4300

Cotton 3600 3600

Groundnut/Sunflower 3700 3700

Soybean 2200 2200

Sesame 4200 4200

Minimum support price (in Rs /q)

Rabi crop MSP Market

Wheat 1350 1285

Barley 980

Gram 3000

Masur 2900 4070

Mustard 3000

Safflower 2800 2500

Land distribution: 305.7 mn ha

Forest69.6316% Non-agri

6%

Barren4%

Pasture2%

Trees/Groves1%

Wasteland3%Fallow land

33%

Net area sown33%

Fertilizer consumption: kg/ha

USA (40.1)China (92.7)

India (138.6)World (31.9)

N; 26.5N; 63.6 N; 84

N; 20.2

P; 7.5

P; 20.1

P; 36.2

P; 7

K; 6.2

K; 9

K; 18.4

K; 4.7

Land usage pattern

% land area % irrigated % fertilizers0

10

20

30

40

50

60

70

80

21

53

77

21

43

75

24

42

72

23

42

67

10

37

51MarginalSmallS MediumMediumLarge

Share in production (figures in percentage)

Food/cash crops; 52

Fruits/Veg; 16

Livestock; 26

Fisheries; 4 Horticulture etc; 2

Exports: 10.47% (figures in percentage)

Cotton11%

Marine10%

Oil9%

B.Rice9%

Sugar9%

Meats7%

Spices7%

Paper/Wood6%

Cereals3%

Tea3%

Others27%

Imports: 3.5% (figures in percentage)

Vegetable Oils52%

Wood13%

Pulses12%

Fruits & Nuts7%

Sugar 5%

Cashew Nuts4%

Spices2%

Cotton1%

Milk1%

Jute0%

Others2%

Sources of irrigation (51 mn ha)

Canals28%

Tanks4%

Wells18%

Tubewells 40%

Others9%

Crop-wise irrigation

Paddy Wheat Pulses Sugarcane Oilseeds Fibres

58.9

90.0

17.6

94.3

33.9

44.7

41.1

10.0

82.4

5.7

66.155.3

Monsoons in India (in mm)

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

800

900

1000

1100

1200

1300

ActualNormal

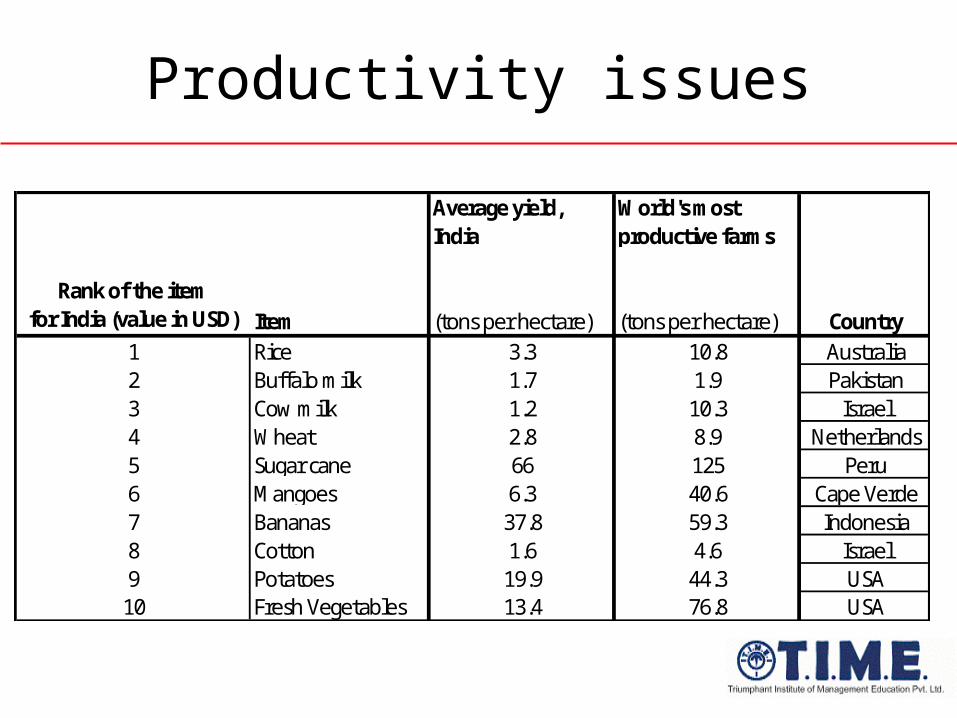

Average yield, India

World's most productive farms

Rank of the item for India (value in USD) Item (tons per hectare) (tons per hectare) Country

1 Rice 3.3 10.8 Australia2 Buffalo milk 1.7 1.9 Pakistan3 Cow milk 1.2 10.3 Israel4 Wheat 2.8 8.9 Netherlands5 Sugar cane 66 125 Peru6 Mangoes 6.3 40.6 Cape Verde7 Bananas 37.8 59.3 Indonesia8 Cotton 1.6 4.6 Israel9 Potatoes 19.9 44.3 USA

10 Fresh Vegetables 13.4 76.8 USA

Productivity issues

Crop Average farm yield in Bihar Average farm yield in Punjabkilogram per hectare kilogram per hectare

Wheat 2020 3880Rice 1370 3130Pulses 610 820Oil seeds 620 1200Sugarcane 45510 65300

Productivity issues

Supply chain issues

Supply Chain Farmer

Village Comm. Agent

District Comm. Agent

Wholesaler

Sub-Wholesaler

Retailer Consumer

Margin-% share of final price

35% 15% 10% 10% 10% 20%

Issues

Non transparent pricingLimited financial capabilityPrimitive cleaning, sorting & grading facility

Wastage rampantLack of quality and hygiene consciousnessLop sided pricingOpportunistic profiteering

High pricesLimited choices

Supply chain issues

Description Cumulative Wastage

Potato 24%

Cauliflower 24%

Banana 30%

Cabbage 36%

Tomato 40%

Road ahead

• ITC e-choupal: from 2000-2007,– 6,400 internet kiosks , 4 million farmers, 38,000 villages, 9 states– It also serves as a purchase centre for 13 agricultural commodities– In 2006-07, ITC purchased about 2 million tons of wheat, soybeans,

coffee, shrimps & pulses, worth $ 400 million through these e-choupal networks.

• ITC Choupal Fresh Model:– Providing Extension services (technical know-how, market

information) – Freedom to sell anywhere at prevailing market price, ITC offering a

buying platform production and market risks are borne by the farmer.– On retail front, instead of super markets, chain of “push carts”

More opportunities

• Drip irrigation• Rainwater harvesting• Organic farming• Packaged farming products• Microfinance• Crop insurance• CSR initiatives

WTO

• Agreement on Agriculture– domestic support – MSP, subsidies – Market access

– reduction of import duties by 24%– export subsidies

– Reduce by 14% by volume, 24% by valye