AFPM QA _2012 - Day One

20

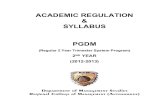

American Fuel & Petrochemical Manufacturers 2012 Q&A and Technology Forum Conference Daily Published by HYDROCARBON PROCESSING ® See us in our suite at the AFPM, Tuesday, October 2, Riviera Room, Third Floor Advanced Refining Technologies ● 7500 Grace Drive ● Columbia, MD 21044 USA V +1.410.531.4000 F +1.410.531.4540 W artcatalysts.com Let ART be a part of your solution. For more information on our products, please contact us. The World’s Leading Supplier of Hydroprocessing Catalysts Distillate Hydrotreating ● Fixed Bed Resid Hydrotreating ● Ebullating Bed Resid Hydrocracking DAY ONE Sunday/Monday | September 30/October 1, 2012 Welcome to Salt Lake City and the 2012 AFPM Q&A and Technology Forum. We’re happy to be here with you this year as the American Fuel & Petrochemical Manufac- turers. Since this group last met, our name has changed to one that better describes who we are and what we do. As Ameri- can manufacturers of fuel and petrochemicals, we’re fully invested in doing everything we can to help our country continue down the road to economic recov- ery through increased employment, and by helping to strengthen our national security by ensuring that the fuels and petrochemical feedstocks Americans rely on continue to be manufactured in the US. The Q&A and Technology Forum meets each year to address the problems and challenges that refiners and petrochemical manufacturers tackle each day. By coming together and discussing the issues we face, sharing best practices, and hearing from other experts in the field, we work together to solve our problems and grow our businesses. Un- fortunately, a large looming problem exists that this group cannot immediately solve, but AFPM contin- ues to work diligently to overcome. It is the current administration’s regulatory onslaught, which seems intent on putting our industry out of business. The policies of the Obama administration are inundating domestic refiners with costly and of- ten conflicting regulations that threaten our com- petitiveness and offer little to no environmental benefits. The president’s automobile mandate, dis- ingenuously advanced under the guise of “CAFE standards,” and the federal biofuels mandate will together lead to a significant decline in demand for gasoline, equivalent to 18 refinery closures. The impact of the regulations will not only be felt by our industry. Consumers also stand to pay dearly. New gasoline regulations will raise costs and could threaten additional refinery closures. Studies show the new “Tier 3” regulations could lead to a six- to 25-cent-per-gallon increase in consumer fuel costs and up to seven refinery closures, depending on how stringent the Environmental Protection Agen- cy (EPA) decides to make the standards. Additionally, EPA is moving forward with regulat- ing greenhouse gases (GHG) under the Clean Air Act, despite the fact that EPA Administrator Lisa Jackson has indicated that they will do nothing to reduce global GHG emissions. These requirements conflict with many other existing regulations, which would Overcoming a regulatory onslaught CHARLES T. DREVNA, President, American Fuel & Petrochemical Manufacturers See WELCOME, page 8 The outlook for US refining mar - gins is particularly bearish beyond 2013. Strong demand from export mar- kets and discounted crude prices in the Midwest will keep US refining mar- gins supported initially. Beyond mid- 2013 though, a substantial expansion in clean fuel production will add to the US exportable surplus and thus put some downward pressure on margins. So far in 2012, despite relatively weak US product market fundamen- tals, US refining margins have been strong, buoyed by refinery outages and growing export markets. With US product markets expected to weaken further as production capacity rises, the health of US refining margins will be similarly dependent on the growth (or lack thereof) in export markets during the next five years. US petroleum demand growth. Global petroleum product demand is expect- ed to average roughly 1.1 million bpd annually through 2016. Most of that growth will continue to come from developing regions such as Asia, the Middle East, Latin America and Af- rica. OECD product demand growth will recover a bit, but slow finished product demand growth will hide even weaker petroleum-based gasoline and diesel growth, undermined by alter- native fuels. In the US, gasoline de- mand will rise by less than 100,000 bpd through 2016. With ethanol use expected to rise as well, demand for petroleum based gasoline will grow even more slowly. Diesel growth will be much more robust growing at more than 300,000 bpd during the same five years. However, declining demand for other products will keep total US petroleum product demand growth to just 250,000 bpd by 2016. Meanwhile, US refining invest- ment in clean fuels production will rise significantly, particularly in 2013. Overall, US refinery upgrades will add substantial volumes to diesel, jet and gasoline output in the next five years. Table 1 lists the largest refinery proj- ects that will boost clean fuels produc- tion and all of them are expected to be online by end 2013. With the US al- ready running larger surpluses in gaso- line, jet and diesel in 2011 and 2012 Product export markets will weigh on Gulf Coast refining after 2013 CHRIS BARBER, ESAI Energy LLC See REFINING, page 9 FIG 1. Global refining capacity vs. demand, 1996–2016. 85 88 90 93 95 98 100 50 60 70 80 90 100 110 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 Percent million b/d Refining capacity Demand Demand as % of capacity (with alt fuels) Demand as % of capacity (w/o alt fuels) Refining capacity utilization taking into account alternative fuel penetration into petroleum markets Refining capacity utilization ignoring alternative fuel penetration into petroleum markets Forecast Source: ESAI

description

Oil & Gas

Transcript of AFPM QA _2012 - Day One

American Fuel & Petrochemical Manufacturers

2012 Q&A and Technology Forum

Conference Daily Published by HYDROCARBON PROCESSING®

See us in our suite at the AFPM, Tuesday, October 2, Riviera Room, Third Floor

Advanced Refining Technologies ● 7500 Grace Drive ● Columbia, MD 21044 USAV +1.410.531.4000 F +1.410.531.4540 W artcatalysts.com

Let ART be a part of your solution. For more

information on our products,please contact us.

The World’s Leading Supplier of Hydroprocessing CatalystsDistillate Hydrotreating ● Fixed Bed Resid Hydrotreating ● Ebullating Bed Resid Hydrocracking

Day One Sunday/Monday | September 30/October 1, 2012

Welcome to Salt Lake City and the 2012 AFPM Q&A and Technology Forum. We’re happy to be here with you this year as the American Fuel & Petrochemical Manufac-turers. Since this group last met, our name has changed to one that better describes who we are and what we do. As Ameri-can manufacturers of fuel and petrochemicals, we’re fully invested in doing everything we can to help our country continue down the road to economic recov-ery through increased employment, and by helping to strengthen our national security by ensuring that the fuels and petrochemical feedstocks Americans rely on continue to be manufactured in the US.

The Q&A and Technology Forum meets each year to address the problems and challenges that refiners and petrochemical manufacturers tackle each day. By coming together and discussing the issues we face, sharing best practices, and hearing from other experts in the field, we work together to solve our problems and grow our businesses. Un-fortunately, a large looming problem exists that this group cannot immediately solve, but AFPM contin-ues to work diligently to overcome. It is the current administration’s regulatory onslaught, which seems intent on putting our industry out of business.

The policies of the Obama administration are inundating domestic refiners with costly and of-ten conflicting regulations that threaten our com-petitiveness and offer little to no environmental benefits. The president’s automobile mandate, dis-ingenuously advanced under the guise of “CAFE standards,” and the federal biofuels mandate will

together lead to a significant decline in demand for gasoline, equivalent to 18 refinery closures.

The impact of the regulations will not only be felt by our industry. Consumers also stand to pay dearly. New gasoline regulations will raise costs and could threaten additional refinery closures. Studies show the new “Tier 3” regulations could lead to a six- to 25-cent-per-gallon increase in consumer fuel costs and up to seven refinery closures, depending on how stringent the Environmental Protection Agen-cy (EPA) decides to make the standards.

Additionally, EPA is moving forward with regulat-ing greenhouse gases (GHG) under the Clean Air Act, despite the fact that EPA Administrator Lisa Jackson has indicated that they will do nothing to reduce global GHG emissions. These requirements conflict with many other existing regulations, which would

Overcoming a regulatory onslaughtCharles T. Drevna, President, American Fuel & Petrochemical Manufacturers

See WelCOme, page 8

The outlook for US refining mar-gins is particularly bearish beyond 2013. Strong demand from export mar-kets and discounted crude prices in the Midwest will keep US refining mar-gins supported initially. Beyond mid-2013 though, a substantial expansion in clean fuel production will add to the US exportable surplus and thus put some downward pressure on margins.

So far in 2012, despite relatively weak US product market fundamen-tals, US refining margins have been strong, buoyed by refinery outages and growing export markets. With US product markets expected to weaken further as production capacity rises, the health of US refining margins will be similarly dependent on the growth (or lack thereof) in export markets during the next five years.

US petroleum demand growth. Global petroleum product demand is expect-

ed to average roughly 1.1 million bpd annually through 2016. Most of that growth will continue to come from developing regions such as Asia, the Middle East, Latin America and Af-rica. OECD product demand growth will recover a bit, but slow finished product demand growth will hide even weaker petroleum-based gasoline and diesel growth, undermined by alter-native fuels. In the US, gasoline de-mand will rise by less than 100,000 bpd through 2016. With ethanol use expected to rise as well, demand for petroleum based gasoline will grow even more slowly. Diesel growth will be much more robust growing at more than 300,000 bpd during the same five years. However, declining demand for other products will keep total US petroleum product demand growth to just 250,000 bpd by 2016.

Meanwhile, US refining invest-ment in clean fuels production will

rise significantly, particularly in 2013. Overall, US refinery upgrades will add substantial volumes to diesel, jet and gasoline output in the next five years. Table 1 lists the largest refinery proj-ects that will boost clean fuels produc-

tion and all of them are expected to be online by end 2013. With the US al-ready running larger surpluses in gaso-line, jet and diesel in 2011 and 2012

Product export markets will weigh on Gulf Coast refining after 2013 Chris BarBer, ESAI Energy LLC

See refininG, page 9

FIG 1. Global refining capacity vs. demand, 1996–2016.

85

88

90

93

95

98

100

50

60

70

80

90

100

110

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Perce

nt

milli

on b/

d

Refining capacity

Demand Demand as % of capacity (with alt fuels)

Demand as % of capacity (w/o alt fuels)

Refining capacity utilizationtaking into account alternativefuel penetration into petroleummarkets

Refining capacity utilizationignoring alternative fuelpenetration into petroleummarkets

Forecast

Source: ESAI

2012 Q&A and Technology Forum | American Fuel & Petrochemical Manufacturers Sunday/Monday, September 30/October 1, 2012 3

SUnDay

4–7 p.m. Registration/Badge Pick up

MOnDay

7 a.m.–6:30 p.m. Registration

8–8:55 a.m. General Session Presentation of the Lifetime Service Awards Keynote Address

9–10 a.m. Plant automation: Keynote address

9 a.m.–12 p.m. Principles & Practices: Plant Services Q&a: Hydroprocessing Panelists: Christopher Bodolus, Coffeyville Resources LLC, Sugar Land, TX; Kevin Carlson, Criterion Catalysts & Technologies, Houston, TX; James Esteban, Suncor Energy, Inc., Commerce City, CO; Bob Henderson, Hunt Refining Company, Tuscaloosa, AL; Steve Leichty, Chevron USA, Inc., Boulder, CO; Robert Ohmes, KBC Advanced Technologies, Inc., Houston, TX

10–10:15 a.m. Coffee Break

10:15 a.m.–12 p.m. Plant automation: The Transformation of Today’s Plant automation • Boundary Control of Operating Envelopes Increases Process Profitability, Robin Brooks • Recent Advances in Use of Emerging Technologies for Plant Automation and Optimization in Chevron: Implementation Experience, Success Stories, Lessons Learned, and Future Plans, Paul Singh, Chevron • Strategic Oil Movement Control & Infrastructure Upgrades, David Seiver, Valero

12–2 p.m. Lunch in Exhibit Hall

2–3:30 p.m. Plant automation: The Transformation of Today’s Plant automation • Remote Asset Monitoring & Diagnostics: An Expert Always On-Line, Nikki Bishop, Emerson • Successfully Utilizing Procedural Automation—Lessons Learned from Other Industries & The Business Case for Procedural Automation and Work Process Automation, Marty Moran, AspenTech • Using Detailed Whole Refinery Models for Setting Operational Strategies, Robert Powell, KBC & Alex Velikoff, Marathon Petroleum Company

2–5:15 p.m. Principles & Practices: Hydroprocessing Q&a: Gasoline Processes Panelists: Geoff Dubin, Axens North America, Princeton, NJ; Ross McDaniel, MPEC, Inc., Houston, TX; Paul Pizzini, Phillips 66, Roxana, IL; Chris Steves, Norton Engineering Consultants, Inc., Boonton, NJ

3:30–3:45 p.m. Refreshment break

3:45–5:15 p.m. Plant automation: IT and Industrial Control Systems (ICS) Security • Eric Cornelius, DHS/Idaho National Labs • DuQu, Stuxnet, APT and Other Failures of ICS Security, Andrew Gintner, Waterfall Security

5:15–6:30 p.m. Reception in Exhibit Hall

sCheDule Of sessiOns anD sPeCial evenTs

PublisherBret Ronk

AFPM ContactsDiana Cronan Sandra Garcia

EditorBilly Thinnes [email protected]

Production ManagerAngela Bathe

Contributing EditorsAdrienne Blume Ben DuBoseStephany Romanow

Hydrocarbon Processing2 Greenway Plaza, Suite 1020Houston, TX 77252-77046713-529-4301

Advertisers:AFPM .................................................. 19Alfa Laval .............................................. 8ART ...................................................... 1BASF .................................................. 20Cameron ............................................. 13Champion Technologies ...................... 11Criterion Catalysts and Technologies ... 10Foster Wheeler ...................................... 5Grace Catalysts Technologies ................ 1Haldør Topsoe ....................................... 9Johnson Matthey .................................. 2Nalco .................................................. 17Saudi Aramco ..................................... 16Selas Fluid .......................................... 15UOP ...................................................... 7URS .................................................... 12

www.HydrocarbonProcessing.com

Published by Hydrocarbon Processing as three daily editions, September 30/ October 1, October 2 and as an electronic edition on October 3. If you wish to advertise in this newspaper, or to submit a press release, please contact the editor via email at [email protected].

2012 Q&A And TEChnology ForuM

GunvOr has siGneD a PurChase aGreemenT TO aCquire PeTrOPlus’ refinery in Ingolstadt, Germany, and related marketing activities. Gunvor said it intends to restart operations as soon as possible. That follows the refinery’s closure in early February as a result of Petroplus’ ongoing financial woes. The company said the Ingolstadt refinery has a “strong regional footprint” in Ger-many’s prosperous Bavaria region. It has a processing capacity of approximate-ly 100,000 bpd. Gunvor said it is committed to operating the refinery on a long-term basis, and the more than 400 existing employees will be retained. Earlier this year, Gunvor also acquired the Petroplus refinery in Antwerp, Belgium.

hOneyWell’s uOP has Been seleCTeD By halDOr TOPsøe TO PrOviDe technology to purify hydrogen from a steam reforming unit to be installed at the Antipinsky refinery in Tyumen, Russia. The UOP pressure swing adsorp-tion system will recover and purify hydrogen to help the refinery meet increas-ing demand for clean transportation fuels, such as diesel and gasoline, the companies said. The new hydrogen unit, which is scheduled to startup in 2013, is part of the refinery’s plan to increase its capacity for crude oil processing by as much as 7 MM tpy. It will also enable the production of fuel products that meet the European Union’s Euro-5 emissions standards aimed at reducing emissions from light-duty vehicles.

exxOnmOBil saiD ThaT iT Will exPanD The size Of iTs CamPus un-Der construction in Houston to accommodate additional employees from the immediate area and from company locations in Fairfax, Virginia, and Akron, Ohio. The affected units include ExxonMobil Refining and Supply in Fairfax, which had played host to the business unit for some time. Mobil was based in Fairfax prior to its 1999 merger with Exxon. Other companies involved are ExxonMobil Research and Engineering; ExxonMobil Fuels, Lubricants and Specialties Marketing; the Akron-based employees of ExxonMobil Chemical; and select positions from ExxonMobil Research and Engineering and Exxon-Mobil Chemical now located at the Baytown, Texas, refinery complex. The new campus is located on a 385-acre wooded site on company-owned land north of Houston. It will accommodate approximately 10,000 employees. Con-struction began in 2011, and full occupancy for employees is expected by 2015.

shell has COnfirmeD ThaT refininG OPeraTiOns aT iTs 79,000-BPD Clyde refinery in Australia ceased on September 30. This follows an an-nouncement in July 2011 that the refinery would be converted into a dedi-cated fuel terminal. According to Shell Australia Downstream Vice President Andrew Smith, “The initial decision to close and convert Clyde, taken in July last year, was consistent with Shell’s strategy to focus its refining portfolio on larger assets and to build a profitable downstream business here in Aus-tralia. Since the decision was taken, the refinery has continued to struggle against sustained poor industry margins and intense competition from mega-refineries in Asia.”

a CeremOny Was reCenTly helD aT The mOTiva refinery in POrT Arthur, Texas, to celebrate the completion of a five-year expansion project that more than doubled crude processing capacity to 600,000 bpd, making the Mo-tiva refinery the largest in the US. With more than 14,000 employees working on the project at peak construction and more than 300 new permanent jobs, the expansion bolstered Motiva’s position as an employer and as a leading revenue source for the city, county and local public schools, the company said. The regional economic impact of the project has been estimated in excess of $17 billion. The expanded refinery can process a wide variety of crude oils, rang-ing from relatively light to heavy. It also has the flexibility to switch between producing primarily gasoline and diesel to adapt to varying market conditions.

BrennTaG has aCquireD PeTrOluBe, The exClusive DisTriBuTOr Of Infineum specialty fuel and oil additives based in Milan, Italy. For financial year 2012, the Italian company expects an EBITDA of about €800,000. The acquisition follows Brenntag’s November 2011 purchase of Multisol Group, a specialist in the distribution of lubricant additives and base oils in Europe and Africa. •

neWs in Brief

4 Sunday/Monday, September 30/October 1, 2012 American Fuel & Petrochemical Manufacturers | 2012 Q&A and Technology Forum

Clifford avery, albemarle

Kevin Basham, Marathon Petroleum Corp. is the tech-nical services department manager for Marathon Petro-leum at the Catlettsburg, Kentucky, refinery where is he responsible for the refinery optimization, process design engineering, and process control groups. He has 20 years of experience which includes process design engineer-ing, lubes production, and crude unit revamps at the Catlettsburg refinery as well as operations supervision of

delayed coking and fuels hydrotreating units at the Garyville, Louisiana, refinery. Kevin holds a BSChE degree from Virginia Tech and is a registered professional engineer in Kentucky.

Christopher Bodolus, Coffeyville Resources LLC is the hydroprocessing manager for CVR Energy in Sugar Land, Texas. He is responsible for technical performance of hydrogen production and consumption processes at CVR’s Coffeyville, Kansas, and Wynnewood, Oklahoma, refiner-ies. He has process engineering experience in refining and chemical manufacturing at many locations in the US, Canada and the UK. Christopher holds a BSChE degree

from the University of Delaware and has over 30 years experience and eight patents in the hydrocarbon processing industry.

Halle Brooks, BP is a process engineer and the FCC continuous improvement forum performance leader in the engineering department of BP Refining and Logistics Technology. Her current responsibilities include providing direct support to all of BP’s FCC assets with respect to catalyst and additive evaluation as well as technical and operational support to our FCC units. She is also respon-sible for the day to day operation of the continuous

improvement forum including our internal question and response system. She has experience as a refinery asset engineer at BP’s Toledo refinery where she covered a number of units including FCC, alkylation, reformer, and the hydrocracker. Halle has both a BSChE degree and an MSChE degree from Purdue University and the University of Michigan, respectively. She is a licensed professional engineer in Illinois.

Kevin Carlson, Criterion Catalysts & Technologies is business development manager with over 23 years of experience in the downstream refining industry. He has been with Criterion for the past 11 years in a number of roles, including global business manager for FCCPT appli-cation, technical lead for the clean fuels projects and a technical specialist for hydroprocessing, and residue upgrading. Kevin began his career as a process engineer

with Husky Oil where he was involved with the design and operations of a heavy oil upgrading complex. Kevin has a BSChE degree from the Univer-sity of Saskatchewan.

Steve Clifford, Motiva enterprises LLC is an operations support engineer for the Motiva Enterprises Convent refin-ery. His responsibilities include support for two crude distillation units and a light naphtha isomerization unit as well as supporting the refinery crude selection team and margin improvement efforts. He has spent eight years at Convent. His other roles have included the logistics and utilities areas and process engineering support for proj-

ects. Steve holds a BSChe degree from Carnegie Mellon University

Mike Dion, Ge Water & Process Technologies is a phase separation senior product applications specialist for GE Water & Process Technologies. His responsibilities include technical support and marketing of the refining sepa-ration product line. Mike has seven years of oilfield experience and 21 years of refining experience. He is co-author of two patents and numerous articles.

Geoff Dubin, axens north america is a senior technology engineer for Axens North America in Princeton, New Jersey. In his current position, he is responsible for licensing and technical assistance covering a number of technologies feeding the refinery gasoline pool including FCC gasoline desulfurization, catalytic reforming, isomerization, selective hydrogenation, and benzene saturation. Mr. Dubin has over of 10 years of experience in the refining and petrochemical

industry including process design, R&D, licensing and technical assistance. Geoff holds a BSChE degree from the University of Delaware.

James esteban, Suncor energy. is a capital projects process engineer at the Suncor Energy Commerce City refinery in Commerce City, Colorado. His role includes capital project development and oversight as well as tech-nical support to the refinery’s operating and turnaround groups. He is a member of the Suncor Technical Excel-lence Network for hydroprocezssing as well as a volunteer officer for the refinery’s Emergency Response Team.

James holds a BS degree in chemical and petroleum refining engineering from the Colorado School of Mines and has served in the industry at the Suncor refinery for nine years.

Mark Koontz, HollyFrontier is a lead process design engineer for HollyFrontier at its El Dorado, Kansas, refin-ery. He is responsible for front end development and pro-cess design for large capital projects in El Dorado. He has over 12 years of experience at refineries and chemical plants in Texas, Louisiana and Kansas. Mark holds a BSChE degree from Kansas State University and is a licensed professional engineer in the state of Kansas.

Jag Lall, UOP LLC is a member of UOP’s FCC/alkylation/treating technology services group based in a regional office in the UK. He joined UOP in 2004. Jag has over 15 years of international experience with design, operational and troubleshooting of FCC units including positions held at KBR and ESSO Petroleum. In his current position, Jag has responsibility for providing trou-bleshooting and unit optimization, start-up support for new and revamped FCC units, and turnaround support for the EMEA region. He started his career as a process engineer at M.W. Kellogg Ltd (KBR) in 1989. He later joined ESSO Fawley where he was the senior staff engineer on the FCCU.

Howard Lee, BP is the discipline leader for separations and works for BP Products North America in Naperville, Illinois. He supervises a group of personnel responsible for the operational, optimization and engineering support of BP Refining’s worldwide CDU-VDU and separations unit assets. He has experience in refineries for both BP and some third parties on a worldwide basis. Howard holds a BSChE degree from Illinois Institute of Technology, and

has 35 years of experience in the petroleum refining industry.

Steve Leichty, Chevron USa, Inc. is a senior staff engi-neer for Chevron in strategy, technology and commercial integration. He is responsible for global technical support in hydroprocessing process monitoring and also works in the field of gross margin improvement, early concept project development and project technical reviews. He has experience at wholly owned and joint venture refineries in North America, Africa and Asia Pacific. Steve holds a

BSChE degree from the California State Polytechnic University, Pomona and has 22 years of refining experience at Chevron in process engineering, plan-ning, operations and management.

2012 afPm q&a anD TeChnOlOGy fOrum PanelisT BiOs

2012 Q&A and Technology Forum | American Fuel & Petrochemical Manufacturers Sunday/Monday, September 30/October 1, 2012 5

Joe Muehlbauer, Valero Refining is an operations complex manager at Valero’s Benicia, California, refinery. He is currently responsible for FCC, fluid coker, and waste water treatment operations, and in his previous role as process engineering manager was responsible for technical support throughout the refinery. He has experience in multiple refineries within California and off-shore natural gas platforms in Mobile Bay, Alabama. Joe holds a BSChE degree from the University of Arizona and an MBA degree from the University of California, Berkeley. He has 10 years of experience in the hydrocarbon processing industry.

Robert Ohmes, KBC advanced Technologies is a prin-cipal consultant for the company in Houston, Texas. His primary responsibilities are centered on profit improve-ment initiatives, hydroprocessing unit consulting and organizational consulting for domestic and international clients. Prior to joining KBC, he worked as a refinery engineer for Koch Refining in Corpus Christi, Texas. Robert holds degrees from Kansas State University

(BSChE) and Tulane University (MBA) and is a licensed professional engi-neer in Louisiana.

Sergio Pimentel, CITGO Petroleum has over 21 years of experience in refining and petrochemical plants in technical service, operations and projects both in Ven-ezuela and the US. He presently works in process engi-neering as an area supervisor for process engineers providing technical support to several FCC units and hydrotreating units. He has over 13 years of technical service experience and project experience in revamps

of FCC units of different technology vendors including catalyst evaluations. He has worked as a strategic planning engineer for developing ULSD and other projects. He has several years of experience as an environmental engineer in refineries meeting air regulations and overseeing routine reporting to environmental agencies.

Paul Pizzini, Phillips 66 is a lead process engineer at the company’s Wood River refinery in Illinois. His areas of responsibility includes straight run naphtha hydrotreating, catalytic reforming, distillate hydrotreating, coker naphtha hydroteating, and cracked naphtha treating including Szorb and ISAL units. His reforming experience includes both cyclic and semi-regen units. Paul has also been involved with the design and startup of two new hydrogen plants, the addition of a reformate splitter and the expansion of an aromatics extraction unit. Paul has a BSChE degree from the University of Notre Dame and 29 years of experience in refining.

Christian Schoepe, Phillips 66 is a senior process engineer for the com-pany with 22 years of refining experience, primarily in FCC technology. Before joining Phillips 66, Christian worked 17 years at UOP as a FCC consultant, FCC design engineer and FCC technical service engineer. He is currently working as a process engineer on a Kellogg Orthoflow FCC unit at the Phillips 66 refinery in Ferndale, Washington. Christian holds a BSChE degree from the University of Wisconsin.

al Shelton, KBC advanced Technologies

Chris Steves, norton engineering Consultants is a principal engineer with the company in Swedesboro, New Jersey. He is responsible for providing process engineering support for Norton’s clients throughout the world, including conceptual process design, process and technology development, operations and equipment assessment, troubleshooting and optimization. He has experience in process engineering, economics and plan-

ning and operations at refineries throughout North America and the Carib-bean. Chris holds a BSChE degree from the University of Delaware and has over 24 years of experience in the refining industry.

What you can do

with atouch of blue.

Improve your refinery profitability by maximizing the production of clean transportation fuels with our leading residue upgrading technologies.

You can…

And there is so much more you can do with a touch of blue. Visit www.fwc.com/touchofblue

Don Tran, Houston Refining LP is a principal engineer for the LyondellBasell, Process Design and Technology Group at Houston Refining. He is responsible for the delayed cok-ing technology including lead process engineer capital project support, technical mentorship of unit process engi-neers and operators, process hazards risk assessments and general refinery technical support. He has held engineering positions as a unit process engineer at the Houston Refin-

ery’s reforming, hydrotreating, and delayed coking units and for the ExxonMo-bil Research and Engineering, Process Division, as a delayed coking technology specialist. He has also worked in operations management as the second line operations supervisor at the Houston Refinery’s sulfur recovery complex. Don holds a BSChE degree from Texas A&M University and has over 12 years of refinery experiences including five years in the delayed coking technology.

Jesse Williams, KBR is a senior technical advisor for Kel-logg, Brown and Root specializeing in fluid catalytic crack-ing technology in Houston, Texas. He is responsible for FCC technical service and FCC process design for both grass-roots and revamped processing facilities for the company’s global refinery clients. He has experience with global refin-eries in North America, Central America, Europe and Africa. Jesse holds a global energy executive MBA degree and a

BSChE degree from the University of South Alabama. He has over 16 years of experience in the petroleum industry.

each year, the q&a and Technology forum features four q&a sessions that allow engineers to discuss issues related to the production of fuel products. This year, the hydroprocessing and Gasoline Processes q&as will take place on monday, while the Crude/vacuum Distillation and Coking and fCC panels are slated for Tuesday.

6 Sunday/Monday, September 30/October 1, 2012 American Fuel & Petrochemical Manufacturers | 2012 Q&A and Technology Forum

545Dx: higher performance with a new nimo catalyst for ulsDBrian WaTkins, Advanced Refining Technologies

Advanced Refining Technologies (ART) continues to expand its line of ultra high activity DX Catalyst Se-ries in response to refiner’s demands for superior technology that delivers premium performance. This family of catalysts has exceeded expectations with its performance in demanding ULSD applications and the expan-sion of this line with 545DX will provide additional opportunities for refiners wanting additional capacity and increased yields without sacrific-ing cycle life. The ability to process difficult feed blends is one of the key advantages observed with this cata-lyst family. 420DX and NDXi have both demonstrated the benefits of this technology in ULSD units around the world both as stand-alone catalysts and as part of a SmART staged cata-lyst system.

545DX builds on this great success as shown in Fig. 1, which compares the activity of several generations of ART NiMo catalysts. The figure shows that 545DX offers significant improvement in both HDS and HDN activity over NDXi. The feedstock used in this work contained 1.26 wt% sulfur and 130 wppm nitrogen. 545DX has provided over a 25°F (14°C) advantage for HDS compared to NDXi as well as a 20°F (11°C) improvement in HDN activity.

Researchers at ART have been able to create a novel alumina support that was identified as a key property for improved catalytic performance. It is understood that there is a strong rela-tionship between the role of increased surface acidity coupled with a tailored pore size distribution for improv-ing the kinetic ability of the catalyst for reactions controlled through ring

saturation, such as nitrogen and hard sulfur removal. This catalyst utilizes similar impregnation technology as NDXi using a chelate to bind to the nickel ions in the impregnation solu-tion and reduce interactions with the alumina support. With some modifi-cations to the manufacturing process, ART has been able to enhance this interaction allowing the chelate/ion complex to stay intact on the catalyst surface and promote the formation of significantly more Type II active sites.

In a concentrated effort to under-stand the improved activity of 545DX, ART has completed pilot plant test-ing over a wide variety of conditions and feedstocks, which clearly dem-onstrates the performance advantage available to refiners. Fig. 2 shows the results of side-by-side testing of NDXi and 545DX at 775 psi hydro-gen partial pressure and 2,200 SCFB H2 /Oil ratio. At these conditions, 545DX clearly outperforms NDXi by over 20°F (11°C) at 10 ppm sulfur on a difficult feed containing 30% light cycle oil (LCO).

Additional benefits of 545DX are the improved HDN activity and increased aromatic saturation capabilities. This offers the flexibility for refiners to meet their HDS activity requirement while gaining additional volume swell. Fig. 3 compares the additional API upgrade with 545DX relative to NDXi over a range of operating temperatures. As the chart shows, 545DX can provide upwards of one full number higher API upgrade when producing ULSD as compared to NDXi.

The need for refiners with lower pressure applications to be able to gain additional activity can present a ki-

netic challenge and is often addressed by utilizing predominantly CoMo type catalysts. The ability of NiMo catalyst to handle lower hydrogen pressure sit-uations can be beneficial and can allow these refiners to increase throughput as well as see gains in cycle life. Fig. 4 compares NDXi with 545DX at 580 psi hydrogen partial pressure over a range of LHSV, and it can be seen that even as the process conditions become more severe, 545DX maintains its ac-tivity advantage over NDXi for ULSD.

The additional HDS activity com-bined with improved nitrogen re-moval and aromatic saturation allows refiners to utilize 545DX as a stand-alone catalyst for maximum upgrade in refinery markets demanding in-creased yields. 545DX can also be coupled with ART’s premium CoMo catalyst 420DX, in a SmART Cata-lyst System, which is ideal for hy-drotreaters that need to operate with controlled or minimized hydrogen consumption. These units are able to benefit from a lower start of run temperature as well as being able to gain some additional yield improve-ments that are not often gained in a hydrotreater system of 100% CoMo.

Extensive pilot testing and expertise enable ART to provide the right catalyst system tailored for maximum refinery profit. 545DX will enable refiners to enhance their ULSD operation with either increased cycle length or addi-tional use of opportunity feedstocks in order to maximize margin. The ability of 545DX to perform in different con-figurations provides a high level of ver-satility and makes it a top tier catalyst capable of exceeding refiners needs in demanding ULSD applications. •

FIG 1. Advanced Refining Technologies Line of high performance NiMo catalysts.

545DX

NDXi

AT580

560580600620640660

680

HDSHDN

Tem

pera

ture

, °F

FIG 2. Comparison of NDXi and 545DX at high pressure.

650660670680690700710

HDS HDN

WAB

T, °F

(10 w

pppm

sulfu

ran

d 1 w

ppm

nitro

gen) NDXi

545DX

FIG 3. Comparison of NDXi and 545DX diesel upgrade.

293304

315

326

337

349

360

371

560580

600

620

640

660

680

700

0.00 0.20 0.40 0.60 0.80 1.00

WAB

T, °C

WAB

T, °F

Degrees API upgrade

FIG 4. Benefits of 545DX at lower hydrogen pressure.

338344349355360366371377

640650660670680690700710

0.5 0.8 1.0 1.3 1.5 1.8

WAB

T, °F

WAB

T, °C

LHSV, hr-1

NDXi545DX

Auto repair costs for consumers could rise due to adverse effects of fuel containing 15% ethanol blends (E15), according to new results from a two-year study on engine durability.

The study was conducted by FEV, a longtime consultant to the US Environmental Protection Agency, on behalf of the Coordinating Research Council (CRC).

The CRC study showed adverse results from E15 use in certain popular, high-volume models of cars (Table 1), its authors said.

Problems included damaged valves and valve seats, which can lead to loss of compression and pow-er; diminished vehicle performance; misfires; engine damage; poor fuel economy and increased emissions.

“Clearly, many vehicles on the road today are at risk of harm from E15. The unknowns concern us greatly, since only a fraction of vehicles have been tested to determine their tolerance to E15,” said Mitch Bainwol, CEO of the Auto Alliance trade group.

“Automakers did not build these vehicles to handle the more corrosive E15 fuel. That’s why we urged EPA to wait for the results of further testing.”

The potential costs to consumers are significant, the study says. The most likely repair would be cyl-inder head replacement, which costs from $2,000-

$4,000 for single cylinder head engines and twice as much for V-type engines.

“Our goal is to ensure that new alternative fuels are not placed into retail until it has been proven they are safe and do not cause harm to vehicles, consum-ers or the environment,” said Mike Stanton, CEO of the Global Automakers trade group. “The EPA should have waited until all the studies on the potential im-pacts of E15 on the current fleet were completed.”

“Automakers believe that renewable fuels are an important component of our national energy secu-rity, but it is not in the longer term interest of the government, vehicle manufacturers, fuel distributors or the ethanol industry itself to find out after the fact that equipment or performance problems are occur-ring from rushing a new fuel into the national mar-ketplace,” added Bainwol.

Growth Energy, an ethanol industry trade group, petitioned the EPA in March 2009 to raise the limit on ethanol in gasoline from 10% to 15%.

In June 2008, EPA outlined testing needed for the agency to approve a waiver, and EPA requirements were consistent with test plans developed by the auto and oil industries.

The CRC, composed of engineers from the auto and oil industries, was working with EPA and US

Department of Energy (DOE) on a multi-year suite of tests on the effects of higher blends of ethanol, according to the trade groups.

This testing included more than $14.5 million of research sponsored by the auto and oil industries, and $40 million of testing sponsored by the federal government.

Before those tests were completed—in October 2010 and January 2011—the EPA granted “partial” waivers to allow the introduction of E15 into the marketplace for use in model year 2001 and later vehicles.

EPA’s decision was based largely on a DOE study of the effects of E15 on durability of catalytic con-verters, the primary pollution control system in a vehicle

EPA did not undertake or wait to consider the re-sults of this engine durability test, or for other E15 related research still underway, the groups allege.

The CRC study took duplicates of eight differ-ent vehicle model engines spanning the 2001–2009 model years. All 16 vehicles were tested over a 500-hour durability cycle corresponding to about 100,000 miles of vehicle usage, the authors said.

A range of engine operating parameters was monitored during the test. •

e15 ethanol fuel can damage auto engines

For more information, visit www.uop.com/uniflex.© 2012 Honeywell International, Inc. All rights reserved.

refinement redefined

UOP Uniflex™ residue-upgrading technology yields 25% more clean fuel, turning “bottom of the barrel” into “top of the line.”

Get the most from every barrel. The UOP Uniflex Process can double the diesel yield

of other residue-upgrading technologies, turning the “bottom of the barrel” into more

black on your bottom line. The Uniflex Process is a high-conversion, commercially

proven technology that processes low-quality residue streams like vacuum residue into

high-quality distillate products — leading to refinery margin increases of up to 100%.

Simply put, with the Uniflex Process from UOP, you’ll maximize production and profits

from every barrel.

SPM-UOP-30 Uniflex Ad 9_21_12.indd 1 9/21/12 2:12 PM

8 Sunday/Monday, September 30/October 1, 2012 American Fuel & Petrochemical Manufacturers | 2012 Q&A and Technology Forum

Heatric recently supplied Echogen Power Systems Inc. with Printed Cir-cuit Heat Exchangers (PCHEs) for Echogen’s Supercritical CO2 (ScCO2) power generation cycle. The power

generation system converts industrial waste heat into electricity, using su-percritical CO2 as the working fluid and without creating new emissions. Heatric’s PCHEs help transfer more

of the waste heat into electricity than would be possible with non-super-critical fluids.

In the Echogen system, liquid CO2 is pumped to supercritical pressure, where it accepts internally recycled heat at the recuperator, followed by waste heat from the hot flue gas supply (Fig. 1). High-energy ScCO2 is then expanded through a turbine, which drives a generator to produce electri-cal power to customer specifications. The expanded ScCO2 is cooled at the recuperator and condensed to a liquid at the condenser. Then the cycle be-gins again.

Heatric PCHEs are used for recu-perating and condensing heat transfer services at pressures over 200 times at-mospheric pressure. They allow great-er heat recovery and process efficiency than other heat exchangers, with the resulting electricity produced at a low-er cost per unit. If widely utilized, such

systems could significantly reduce the demand that heavy power consumers place on the grid. Also, the compact size of Heatric’s PCHEs allows sys-tems to be retrofitted more easily to existing industrial facilities. •

actually force refiners to increase GHG emissions and threaten to send more of our refining jobs overseas.

Add to the regulations President Obama’s unrelenting efforts to prop-up fuels that can’t stand on their own and give an unfair advantage to some, while harming others. One example is the Navy’s Green Fleet program. The program is a deplorable example of government spending that demon-strates complete disregard for Ameri-can taxpayers’ money. This program allows the Navy to knowingly pur-chase $27 per gallon biofuel, over tra-ditional petroleum fuel, which remains under $4 per gallon.

Further, this administration has re-peatedly discouraged energy explora-tion and energy production, contribut-ing to higher refinery crude-oil costs. The most glaring example of such a policy is the president’s decision to disapprove the Keystone XL pipeline, a project that would have created tens of thousands of jobs and provided our nation with a more secure oil source, greatly benefiting American refineries and consumers.

Our companies manufacture fuels and petrochemicals—combined with activities to produce oil and natural gas—that support more than nine mil-lion American jobs. We could create more if President Obama would stop throwing regulatory roadblocks and proposed tax increases in our path.

Sensible regulations are fine, but excessive regulations that bring little or no real benefit have been placed on refiners in a number of areas, includ-ing fuel and emission standards. The number of regulations our companies need to follow are staggering, and they seem to multiply by the day.

As we meet on the eve of a very important election for our industry and the nation’s economy, we need Washington to get focused on the im-portant role that AFPM members and other energy companies play in the American economy and in job cre-ation. It’s time that our leaders con-sider an energy policy based on reality rather than ideology.

No one knows today what the out-come of the election will be, but I hope that whoever is in office in Janu-ary (regardless of their political party) will consider working cooperatively with Congress and our nation’s ener-gy workers and companies to do what is right for America. •

Let’s talk numbers

Prize performance, capacity gains

Packinox heat exchangers pack up to 16 000 m2 of heat transfer surface area into one single unit. That makes them the largest plate heat exchangers in the world. The performance benefits of the Packinox design include closer temperature approach, which gives rise to lower fuel consumption, and reduced emissions, plus a lower pressure drop. It all adds up to gigantic savings on your infrastructure and installation costs as well as your operating costs. Those kinds of numbers really make you a winner. P

PI0

0181

EN

WelCOme, continued from page 1

PChes boost power from waste heat

FIG 1. Echogen’s power generation system converts industrial waste into electricity using Heatric’s heat exchange technology.

Heat engine skid

Cooledflue gas

Flue gassupply

Waste heatexchanger

Recuperator

CondenserPower electronics

Coolingwaterreturn

Generator Gear Turbine

Cooling watersupply

Pump

Net power

FOR MORe InFORMaTIOn, VISIT WWW.aFPM.ORG

2012 Q&A and Technology Forum | American Fuel & Petrochemical Manufacturers Sunday/Monday, September 30/October 1, 2012 9

Choose your footprintWWW.TOPSOE.COM

Design your plant layout to determine your energy efficiency and carbon emissions

this additional capacity will be bearish for overall US product markets and will pressure US refining margins.

Shrinking target markets for US export. In recent years, US refiners have ben-efited from the absence of refining in-vestment in developing regions, espe-cially in Latin America where product import requirements of have grown. Latin America, the main export mar-ket for growing US product surpluses, has had a particularly bullish impact on US refinery operations and profits. In addition, in 2012, throughput lev-els were lower in Europe due to high-er crude costs, lackluster petroleum gasoline demand growth and surprise outages. The expansion of import re-quirements in both Europe and Latin America pushed US exports of diesel to more than one million bpd in the second quarter, nearly five times what they were five years ago.

Beyond 2013, global distillation capacity is expected to rise signifi-cantly faster than demand, expanding by nearly eight million bpd between 2012 and 2016, compared to just 1.1 million bpd of average annual product demand growth during the same five years. In Fig. 1, refining capacity, the darker blue area, expands much faster than the demand forecast. As a result, the bullish trend that saw demand expand faster than capacity in recent years will also reverse. The bearish decline in the ratio of demand to refin-ing capacity expected beyond 2013, depicted by the dark blue line in Fig. 1, will pressure margins. This ratio is even more bearish when demand for oil products is adjusted for alternative fuel substitution, as the red line shows in Fig. 1.

Lowered requirements. In addition, many product importing regions will lower their import requirements, and regions like the Middle East are likely to begin exporting additional product. Asia, the largest developing region will continue adding capacity in order to keep pace with regional demand

growth. However, the Middle East and Latin America, the two largest demand growth regions outside of Asia will ac-celerate capacity additions, breaking with recent trends.

US export markets contract slowly. Despite recent refinery delays in Bra-zil that will significantly temper ca-pacity additions, Latin American re-fining capacity expansion in the next five years remains impressive. The region collectively will add roughly 730,000 bpd of capacity through 2016, adjusted for the closure of the HOVENSA refinery in 2012, which mainly served the US market. Bra-zil still accounts for the majority of the growth, adding roughly 400,000 bpd, but most of that capacity is not expected until end-2014. Notably, the delays include the first phase of PRE-MIUM I, which would have added 300,000 bpd in 2016.

The remainder of the growth in Latin America (Fig. 2) will be made up of smaller projects that will add less than 100,000 bpd and mainly through capacity expansions at ex-isting refineries. The goal of most of these projects will be to increase diesel production, lowering import requirements, while processing ad-ditional heavy crude from the region. However, further delays with some of these projects are likely.

More competition for export markets. Europe’s import requirement is ex-pected to rise slightly beyond 2013, but only because Europe’s refiners will come under increased competi-tion from growth in the exportable surplus of gasoline and diesel outside the region. In addition to the rise in US capacity, as is well-known, the Middle East will see a sharp rise in distillation capacity by 2016. Saudi Arabia, Iran and the UAE all have large projects planned that will contribute to roughly two million bpd of new distillation ca-pacity. Saudi Aramco is expected to finish both 400,000 bpd joint venture refinery projects with Total and Sino-

pec. They will contribute to a regional surplus and both are expected to ex-port product as well. The UAE and Iran are both expected to add some capacity, further contributing to the re-gion’s ability to export product. Iran’s capacity expansion is likely to be lim-ited or delayed severely, however, by continued sanctions.

US crude advantage will decline. The price discounts for the growing pro-duction of crude oil from Canadian oil sands and Bakken shale in 2011 and 2012 have set off a race to move North American crude oil to the coast, where most US refining capacity is located. Outlets for this crude, both pipeline and rail, will continue to expand rap-idly in the coming years. Although this rising domestic production and re-sulting price weakness has helped US refiners initially, the benefit will dis-sipate significantly as more and more crude oil reaches the coast, backing out imports and forcing price equili-bration with the global oil market.

Lower US refining margins ahead. In sum, after rising to more than $15 ear-lier this year, ESAI expects notional USGC Cracking margins to LLS will to find some support next year before falling below $10 beyond 2013. The impact of these lower margins will be increased pressure for marginal refin-ing capacity particularly in the US and Europe, with spare capacity in the two regions rising and export markets shrinking. The lower margin environ-ment and resulting spare capacity in the USGC will also likely delay or discourage additional capacity expan-sion projects outside the US, particu-larly in Latin America, where financ-ing continues to be an issue. •

Chris Barber is a refining ana-lyst at the global energy forecasting and analysis firm, ESAI Energy LLC (www.esaI.com). For more detail on this analysis, please contact Mr. Bar-ber at [email protected]. For more information on ESAI Energy, please contact Tom Lovett at [email protected] +1-781-245-2036.

refininG, continued from page 1

FIG 2. Latin America product balances.

-800

-600

-400

-200

0

200

400

600

800

2011 2012 2013 2014 2015 2016

Gasoil and diesel Gasoline Fuel oil

Source: ESAI

TaBLe 1. US refinery projects that will increase clean fuel production

Company location PaDD main unit Capacity (‘000 bpd)Motiva Port Arthur, TX 3 CDU 325Valero Port Arthur, TX 3 Hydrocracker 57Valero St. Charles, LA 3 Hydrocracker 60BP Whiting, IN 2 Coker 102Marathon Detroit, MI 2 Coker 27Marathon Garyville, LA 3 Hydrocracker 20Wood River Wood River, IL 2 Coker 65Source: ESAI

WaSHInGTOn— Statement by aFPM President Charles T. Drevna on the ePa decision to increase bio-based diesel volumes to 1.28 billion gallons in 2012:

“EPA’s decision to increase the biomass diesel volumes is whol-ly discretionary and irrespon-sible. It only serves to increase our nation’s fuel bill. Given the exorbitant cost of biodiesel, its poor performance qualities, sig-nificant fraud in the biodiesel industry, and the drought facing our nation’s farmers and ranch-ers, this is a bad decision at the wrong time. Today’s decision will force consumers to pay al-most $500 million more next year for diesel fuel.” •

DiD yOu knOW?

10 Sunday/Monday, September 30/October 1, 2012 American Fuel & Petrochemical Manufacturers | 2012 Q&A and Technology Forum

EVER WONDER WHAT MAKES OUR CATALYSTS SO ADVANCED?

INDUSTRY-LEADING MINDS, OF COURSE.Even with the wide range of proven Criterion catalysts, like CENTERA® in our portfolio and successfully upgrading challenging feeds to hydrocracker, distillate and FCC pretreat operations around the world; we still think the ultimate key to performance is our people. Come connect with Criterion Catalysts & Technologies and Shell Global Solutions in our suite:

Monday, October, 1 20126:30 pm - MidnightVienna Room, 3rd Floor, The Grand America Hotel

www.CRITERIONCatalysts.com

Trial shows aeGis to be an innovative and flexible resid cracking catalystCarl keeley, Jeremy mayOl, yves-alain JOllien, sTefanO riva and vasileiOs kOmvOkis, BASF

Tamoil is a major operator in the oil and energy industry with operat-ing refineries in in Germany (Ham-burg) and Switzerland (Collombey) in addition to distribution networks in Italy, Germany, Switzerland, The Netherlands and Spain.

Tamoil’s FCC asset at its Col-lombey refinery is an R2R unit op-erating with a heavy residue feed-

stock (3-7% Conradson carbon) and high contaminant metal level (Ni+V up to 12,000 ppm). R2R technology was originally developed by Total as a cost-effective, flexible and reliable means to profit from residue feed-stock. The R2R residue FCC technol-ogy is offered through the FCC Al-liance between Axens, IFP Energies Nouvelles, Total and Shaw.

Beginning in 2011, the Collombey refinery evaluated FCC unit catalyst options to optimize performance and cost in face of adverse RE market conditions. The base case catalyst in use was the market leading resid catalyst in EMEA supplied by the market share leader in the region. A trial was conducted using one of the market leader’s low rare earth al-ternative products touted to deliver equivalent performance at lower RE levels. However, the proposed lower rare earth alternative product trial was abandoned due to the sub-par performance of the product; unit performance showed an increase in LPG yield (which is the main unit constraint), bottoms yield and cata-lyst addition rate. As the drivers for a change in catalyst were still valid, BASF was invited to offer a solution.

BASF recognises that refiners may have concerns about potential risks associated with changing to a new catalyst and supplier. This may be the case, even if the catalyst tech-nology is commercially proven, as was the case here, and the supplier has a proven track record; BASF is the market leader in North America, where there are around 42 resid FCCs

and 134 GO FCCs in operation. Be-cause BASF recognizes this concern refiners may have, the first step was to provide value-added technical ser-vice to further understand the opera-tion and constraints of the unit; activ-ities included: site based audits and reviews, pilot plant testing and prepa-ration of a very successful catalyst change-over risk minimisation plan.

Based on the technical evalua-tions, a catalyst system was selected that would fit the unit operation and deliver the highest value. AEGIS, an innovative catalyst from BASF was selected to provide the greatest flexibility. The final catalyst formu-lation was customized for the trial objectives as described by Tamoil; BASF’s portfolio of FCC catalysts and additives are used to produce customized products with specifica-tions prepared for a target to meet the customers’ needs.

The trial was conducted from March 30 to June 19 in 2012. Initial-ly, the unit was set-up to mimic the performance of the market leading resid catalyst in EMEA, then the unit was optimized, so that all the benefits

FIG 1. Significantly improved LPG selectivity while comparing similar operating conditions (summer months only).

Comp. 3.5%REhigh CCR feed

LPG/

gaso

line r

atio,

wt/w

t

0.26

0.27

0.28

0.29

0.30

0.31

0.32

Comp. 3.5%RElow CCR feed

Comp. 3.5%REavg. feed 2006-11

Comp. 2.6%RElow RE catalyst

CustomisedAegis 2.8%RE

See Basf, page 11

2012 Q&A and Technology Forum | American Fuel & Petrochemical Manufacturers Sunday/Monday, September 30/October 1, 2012 11

Champion Technologies’ Water and Process Solutions teams are working to ensure that the priorities and strategic business drivers of your operations are met.

Customers tell us that they value Champion’s response to three significant priorities that affect all aspects of their operation. Water and Process chemical treatment programs are designed to fully meet expectations in terms of:

• Training and systems to reinforce safe conduct and operation

• Engineering support and predictive tools to monitor and improve equipment reliability

• Process and Utility system analytics for best outcome to support profitability

Customers’ priorities are Champion’s priorities.

Learn more at champ-tech.com

Refiners spoke…

We responded!

SAFETY, RELIABILITY, PROFITABILITY!

Champion_AFPM_Q&A_AD 1 9/21/12 8:18 AM

of the new catalyst could be mea-sured. Tamoil remarked that, “it was a very smooth change-over, with no problems and the new catalyst perfor-mance was very good indeed.”

Meeting Tamoil’s expectations the dry gas yield, gasoline yield, coke yield and delta Coke are all similar to past performance at a satisfactory catalyst addition rate.

What exceeded Tamoil’s expecta-tions was the significant improvement in LPG selectivity and an outstanding benefit on bottoms cracking.

The LPG selectivity of the custom-ised AEGIS catalyst, that has a low 2.8% RE content, was significantly better than the competitor’s low RE al-ternative, which had 2.6% RE content; and it was also better than the market

leading resid catalyst in EMEA, which had around 3.5% RE content. This im-proved performance of the customized AEGIS catalyst has eliminated the historic main unit constraint.

There is quite a benefit on the bot-toms cracking, that being increased LCO yield and reduced slurry yield. This was an important achievement that allowed Tamoil to increase die-sel production.

Summation. The customized AEGIS catalyst solution outshined the com-petitor’s low rare earth catalyst and was also better than the market lead-ing resid catalyst in EMEA. Due to the significantly improved LPG selec-tivity, outstanding benefit on bottoms cracking and improved conversion,

there is substantial economic benefit.Using an indicative set of feed,

product and utility prices, Tamoil’s improved profitability is estimated to be around:

• +1.2 $/bbl, compared to the com-petitor low rare earth catalyst; and

• +0.4 $/bbl, compared to the mar-ket leading resid catalyst in EMEA.

The factors that made this success possible were: close cooperation be-tween Tamoil and BASF; BASF’s innovative, flexible AEGIS catalyst; BASF’s customized technical ser-vice; BASF’s catalyst changeover risk minimization plan; and BASF’s European catalyst facility and cus-tomer service team. •

FIG 2. Improvement on bottoms cracking.

FIG 3. AEGIS catalyst economic benefit.

Comp 3.5%REaverage 2006-11to high CCR feed

Unit

profi

tabil

ity, U

S $/b

bl of

feed

Comp 2.6%RE

Profitability

+ 0.4 $/bbl

+ 2.6 Mio $/year at18,900 bbl/day full capacity

+ 7.8 Mio $/year at18,900 bbl/day full capacity

+ 1.2 $/bbl

Aegis 2.8%RE

Basf, continued from page 10

SWITCH LIne ReCeIVeS SIL CeRTIFICaTIOnSOR Inc.’s line of pressure, differential pressure,

temperature, vacuum and level switches has been certified fit for use in Safety Integrity Level (SIL) environments. SOR is one of only a few manu-facturers in the industry to offer its entire range of switches certified to the IEC 61508 safety standard.

To obtain SIL certification, the products were assessed by FM Approvals per the requirements of IEC 61508 parts 1, 2 and 3. When implement-ing Safety Instrumented Systems (SIS) in process plant environments such as power plants, offshore oil platforms, refineries and chemical plants, the SIL certification helps mitigate risk at the process instrument level.

The SOR line of pressure switches and level switches are rugged, field-mounted instruments. Nearly every SOR product can be designed to meet the demands of specific processes and custom-built to suit exact specifications.

COOLeR DeSIGn RaISeS eFFICIenCy By 25%GEA Heat Exchangers’ Groovy Fin Cooling in-

dustrial cooler design improves efficiency by 25%. The process technology supplier featured its air

coolers at the ACHEMA 2012 conference in Frank-furt, Germany from June 18–22.

The Groovy Fin Cooling design features a pat-ented fin shaping that reduces the “slipstream,” or dead space, behind the finned tubes. This allows for smaller coolers with reduced space requirements and less power consumption by fans—i.e., reduced investment and operating costs.

The central idea of using air instead of water as the coolant saves water resources and prevents the warming of bodies of water—and it is the technolo-gy preferably used in regions where water is scarce. Air coolers comprise finned-tube bundles and fans that generate airflow to cool the gas or liquid in-side the tubes. When the air flows across the finned tubes, it cannot reach the area located immediately behind the tubes because a dead space is formed on the side not facing the airflow. Until now, a part of the fins was not used as a cooling surface.

“Groovy Fin Cooling” means that the fins are grooved to guide the airflow behind the tube. The efficiency of the air cooler is increased by up to 25%, and the environmental footprint (in this case, the space requirement and the energy consumption) is also significantly reduced.

If the customer uses the improved efficiency for higher cooling performance while retaining the same heat exchanger size, then performance can be improved by up to 20%. Cleaning of the grooved finned tubes is the same as in conventional finned tubes, and the mechanical stability of the patented design is even higher. GEA offers a variant with special protection for applications in aggressive ambient air conditions, e.g. in LNG terminals.

THIRD-GeneRaTIOn VaLVe DIaGnOSTICS enHanCe FLexIBILITy

The new Metso Valve Manager represents state-of-the-art, third-generation valve diagnostics that are capable of processing collected diagnostics in-formation to visualize the condition of a valve with five different indices: control performance, valve condition, actuator condition, positioner condition and environmental conditions.

With diagnostics information, engineers and operators can make decisions concerning control valve maintenance, without deep valve know-how. Unexpected shutdowns can be avoided, and the control valve performance can be maintained at an optimum level. •

innOvaTiOns

12 Sunday/Monday, September 30/October 1, 2012 American Fuel & Petrochemical Manufacturers | 2012 Q&A and Technology Forum

Energy price fluctuations present both near-term challenges and interesting opportunities for the oil and gas mergers and acquisitions (M&A) market. As Deloitte Consulting points out in a recently re-leased report, current depressed North American natural gas prices (prices far below the market rates in other continents) will likely continue to at-tract both domestic and international supermajors that have money to spend on natural gas assets at low prices. Deloitte believes the long-term outlook for US natural gas holds promise, as gas gradually gains domestic market share, and as prospects for LNG exports from the US improve.

The consulting company sees buying interest and E&P activity in liquids-rich shale plays con-

tinuing, as well as midstream consolidation and infrastructure investment, as that segment restruc-tures and invests to serve the rapidly changing North American energy landscape. According to Deloitte, a resurgent North American energy mar-ket and the investment needs that accompany that resurgence should set the stage for sustained M&A activity over the longer term.

Downstream M&a. Only nine refining and market-ing (R&M) deals took place during the first half of 2012, compared to 12 transactions in the first half of 2011 and 13 during the second half of 2011 (Fig. 1). However, the total value of transactions picked up during this year’s first half to $10.6 billion, up 36%, when compared to $7.8 billion in the first half of 2011, and several orders of magnitude larger than the $2.6 billion during the second half of 2011.

“We actually saw a good increase in deal value year over year in this segment,” said Roger Ihne, a principal at Deloitte Consulting. “This was primar-ily driven by two large deals that took place outside the US: one in Asia and one in Europe.”

One refinery acquisition during this period was notable not for its size but for the industry affilia-tion of the buyer. A major international airline an-nounced in the second quarter of 2012 that it would buy a Trainer, Pennsylvania, refinery for $180 mil-lion. The company intends to upgrade the refinery’s capabilities so that it can produce a much higher proportion of jet fuel, giving the airline a source of fuel in a region of the US that has very little jet fuel production, as well as exchanges to allow jet fuel to be supplied throughout other geographic areas.

“This is certainly a unique situation that has ev-eryone intrigued both within and outside the indus-try,” said Mr. Ihne.

From integrated to independent. Ownership within the R&M segment of the energy industry has been transformed over the past decade as large integrated companies have “high-graded” their portfolios, sell-ing or spinning off their downstream assets to focus on higher-performing upstream operations. Now, over two-thirds of US R&M operations are in the hands of independent rather than integrated compa-nies. Many of these independent operators have ben-efited over the past two years from rising profits in the US due to advantage-priced crude supplies from Canada and the developing tight oil plays in Ameri-ca, but long-term prospects are more uncertain.

“Gasoline demand in the US is down 5% com-pared to last year,” said Mr. Ihne. “Long-term de-mand for refined products in the US is still uncertain due to stricter corporate average fuel economy and renewable fuel standards, as well as future compe-tition from natural gas-based transportation fuels.”

However, reduced domestic consumption of gaso-line and distillate fuels has largely been offset by ex-ports of refined products from US Gulf Coast refin-ers to Mexico, South America and Northern Europe. Fig. 2 provides an overview of the net exports of US petroleum products from January 2010 to May 2012.

“Without export demand, US refiners would likely be challenged to operate near the 85%-plus capacity they reached this year,” said Mr. Ihne.

“Refining assets in the Gulf are some of the most sophisticated in the world,” said Mr. Ihne. “They can process heavy crude from Canada and the new tight oil supplied from various US plays, but un-less refiners gain access to that oil, we will have assets in the US that have a comparative economic advantage to the rest of the world—but, nonetheless will have to rely on higher cost imported crude from elsewhere.” •

FIG 1. Refining and marketing M&A deals by value and count.

FIG 2. Net exports of US petroleum products.

Taking a glance at mergers and acquisitions

AD00387P

CAMER-1058_PRS_refine_AFPM_rev.indd 1 9/24/12 9:08 AM

14 Sunday/Monday, September 30/October 1, 2012 American Fuel & Petrochemical Manufacturers | 2012 Q&A and Technology Forum

The value of employing an experienced strategic licensorDave Clark, Shell Global Solutions International BV

Refinery projects can encounter problems if they become unexpect-edly complex or fail owing to insuf-ficient integration between the dis-tillation, conversion, treating and emissions control processes. The im-pact on a business can be devastating but, by following a different approach, such issues can usually be avoided.

Astounding levels of complexity can be encountered during the instal-lation of new process units owing to the overwhelming number of inter-faces with other parts of the plant. For instance, the Pearl GTL devel-opment in Qatar involved 800 pipe-lines crossing between contracts, and there were over 2,600 cases where it was necessary to pass process data among contractors. There were more than 3,600 construction inter-face points, including those for the exchange of schedule information and overlapping responsibilities for cross-contract system hydrotesting. This is clearly not an assignment for the faint-hearted. As a general rule of thumb, every interface increases project complexity by a square fac-tor; it is not unusual for a project’s complexity to mushroom.

There are various forms of inter-face, including technical interfaces that occur between structures and process units, and organisational in-

terfaces. Investigation revealed fail-ures in the latter category to be the cause of the Three Mile Island nucle-ar incident in 1979.

At Qatar, the project schedule was maintained because the complexity was mitigated with tried-and-tested techniques. Seamless integration among contractors was achieved through sophisticated work pro-cesses that facilitated communica-tion and data exchange, and by an interface database that consolidated all the interface points and issued weekly status reports. On highly complex capital projects, the value of experience and best practices can-not be overstated.

Decisions made during the front-end development phase can have a major influence on complexity. For instance, I have heard of refiners that have licensed multiple technologies from different suppliers only to find out—sometimes when it was too late—that they do not match at the interfaces. Often, the cause is that they were designed to different stan-dards or philosophies.

Sourcing from multiple suppliers is the traditional approach, as it en-ables solutions to be cherry-picked and the various suppliers to be beaten down on price. Increasingly, howev-er, the progressive refiners are realis-

ing the substantial value that is at risk with this approach: delays, rework costs and plant underperformance.

Sourcing from a limited number of licensors can help to avoid this. For instance, an owner can license a package of residue upgrading tech-nologies that combines the high vacuum unit, the hydrocracker and the solvent dewaxing unit from one supplier. Many customers find this to be a much better way of executing a project because their dealings are only with one party—the strategic li-censor. It then becomes the strategic licensor’s responsibility to ensure, for instance, that the numerous inter-faces match and that the schedule is optimised. It also promotes safety.

As a strategic licensor that has operational experience, Shell Global Solutions strives to take a holistic approach during projects because it sees opportunities to be the architect of value creation across the business, not just within an individual project or activity. Our value creation archi-tecture provides the platform for this.

A wide-ranging portfolio of refin-ery processes is also a prerequisite for this approach, which is why, at Shell Global Solutions, we actively seek strategic technical alliances with specialist companies that offer leading-edge technologies in areas where we do not have a proprietary technology.

A good example of this is the Shell Sulphur Technology Platform through which we license a suite of technologies that can handle sulphur in any form: in crude, products and emissions, and also as a solid. Many of these are proprietary technologies, but we also have agreements with, for example, Cansolv Technologies Inc. (now owned by Shell), Merichem, Praxair, Sandvik and Sulzer to com-plete our portfolio.

The Grupa LOTOS DAO hydro-cracker demonstrates the customer value of such an alliance. As dis-cussed in the article on page 7, the quality of the DAO feed from KBR’s

SDA unit to Shell Global Solutions’ DAO hydrocracker was pivotal. In theory, Grupa LOTOS could have licensed a standalone SDA unit, but that option would have missed the opportunity to optimise the interface between those two crucial processes. Because of our alliance, we were able to work with KBR to optimise the feed. You cannot optimise units individually and expect to maximise the refinery’s overall performance.

Customers also receive consistent guarantees that are aligned with their overall objectives, which can be ex-tremely reassuring, especially to fi-nanciers. This can also minimise the potential for liability disputes.

I heard of a refinery that installed a Claus unit that was too big: they could not turn it down sufficiently for it to operate. It seems that the licensor, which was not an operator, designed in contingency capacity in all the up-stream units that resulted in a deliv-ered unit so large that there was not enough hydrogen sulphide in the re-finery to fill it, even at maximum turn-down. Integrating new process units is rarely straightforward, but experience can often prove invaluable.

Employing a strategic licensor that has itself operated large, complex in-dustrial facilities might also help you to address investor concerns and, as a result, secure preferable terms for finance and insurance. In financiers’ eyes, it helps to mitigate the comple-tion risks associated with complexity and integration; it is much less risky than having multiple partners.

Shell Global Solutions has mul-tiple strategic technical alliances with specialist technology provid-ers, some of which date back de-cades. In addition, we leverage rela-tionships with our affiliates such as Criterion and our in-house trading teams (for crude supply optimisa-tion and product offtake deals). All of these share a common fundamen-tal objective: to help us work with customers to enhance the value that we deliver to them. •

1. OVeRWHeLMInG COMPLexITy“We identified processes that would achieve our objectives. But when it

came to licensing the technologies from different suppliers…the complexity was just overwhelming.”

Best practices are key. A strategic licensor should be experienced at co-ordinating the interfaces and will supply units that leverage the same de-sign standards.

2. POOR SOLUTIOn InTeGRaTIOn“To get the best performance out of our new unit, we have to compromise