ACE accounts-miniguide v1

21

ACE Accounts & Tax mini guide The really easy mini guide to running a limited company. This is your handy intro to ACE accounts & Tax andthe things you need to know about limited company tax, admin and law. We’ve kept it short and sweet. Anything else? Just ask.

-

Upload

akshay-shah -

Category

Documents

-

view

23 -

download

1

Transcript of ACE accounts-miniguide v1

ACE

Accounts & Tax

mini guide

The really easy mini guide

to running a limited company. This is your handy intro to ACE accounts & Tax and the things you need to

know about limited company tax, admin and law. We’ve kept it short and

sweet.

Anything else? Just ask.

Contents

1 Introduction: working

with ACE accounts

2 Company formation

Company name

Registered office address

Company directors

Accounting year end

Company shares

3 Share capital structure

Share capital

Shareholder/s

Settlements Legislation

4 Business bank account

5 Business insurances for VAT? Factors HMRC consider

Professional indemnity How do I register the company for VAT?

Public liability VAT schemes 13 Remuneration – ways to

Employers liability

11 Business expenses

withdraw funds

Expenses

Salary

6 Responsibilities & duties of

a limited company director What expenses can be claimed?

Legitimate business expenses

Salary to a partner or spouse

Dividend

7 Money laundering regulations Making an expense claim

24-month rule

40% rule

Business travel

Subsistence

Accommodation

Overnight incidentals allowance

14 Financial planning

Pensions

Income protection

Critical illness cover

Personal accident cover

Mortgages

Use of home as office

Company cars

15 Closing your company

8 Statutory filing

requirements & deadlines

PAYE and NICs

VAT

Corporation tax

Statutory accounts

Companies House annual return

Directors personal tax return

P11D & dispensation

9

Statutory record-keeping

10

Value Added Tax (VAT)

12 IR35

How does VAT work? What is IR35?

Do I need to register the company Inside or outside IR35?

Dorma

ncy

Windi

ng up

1 Introduction:

working with

ACE accounts &

Tax

Now that you’re choosing to step into

the world of independence with your

own limited company, you’ll want

support that makes it all easy – that’s

what we’re here to do.

The whole point of contracting is

freedom. So you don’t want to be tied

up with admin. Yes, you’re the boss, but

we’re here to look after you.

Just some of the many services you get:

• super-fast set-up – less than 24 hours

• expert advice on tap – Personal

Qualified Accountant and support team

• top tech – accountancy software,

secure bank data-feed, 24:7 personal

portal

• core admin – VAT, tax and year-end

returns done for you

• real-time updates – for financial

insight and control

• director’s payroll and self-assessment

2

Company

formation When you decide to form your own

limited company, there are some

key areas you’ll need to consider

with your business objectives

in mind...

What happens once the company is formed?

Your contact at ACE accounts can form

the company for you within a matter of

hours. The following documents will then

be made available to you on your client

portal, which you may need to provide to

any party that wishes to do business with

your company – e.g. a recruitment

agency, a client, a bank for your business

banking, insurance companies and so

on...

Company name

It’s best to have a few names to choose

from, as your first choice may already

be in use or it may be very similar to an

existing company – in which case you’ll

need to seek their permission first. Your

contact at ACE accounts will be able to

check which names are available.

Registered office address

You will decide where you want your

company to be legally registered. You can

choose ACE accounts to act as your

registered office, or your home address, or

any other address you wish as long as you

can run a business from it.

Company directors

You must legally appoint at least one

director, which is usually yourself. There

is no longer a requirement for small

Companies to appoint a company secretary.

Accounting year end

We’ll help you choose the appropriate

accounting year end. This is the date which

your annual accounts are made up to and

is normally one year after the date of

incorporation.

Company shares

When you form your company, you will

be able to issue shares. This entitles the

shareholder/s to receive dividends in

proportion to their shareholdings.

3

Share capital

structure

The share capital in a private limited company is the amount of

money invested by its owners in exchange for shares of ownership.

How many shares a company can issue and when they can be issued

is set down in the company’s Articles of Association – essentially,

the company’s rule book.

Share capital

When forming a company, the director

(you) can allot shares to shareholder/s

– up to any number of shares as set out

in the Articles of Association.

Each share will have a fixed nominal value.

Most freelancers choose to own 100% of

the company by issuing themselves all

of the share capital, e.g. 10 ordinary

£1 shares, totaling a value of £10.

More shares can be issued later. Your

personal qualified accountant will be

able to help you with this.

Shareholder/s

Shareholder/s is the term used to

describe the owner/s of the shares in a

company.

Each share a person buys will give them

some rights in deciding how the company

is run, the greater the percentage of

the shares they own, the more control

they have. It also gives them a right to a

proportionate percentage of any dividends

issued by the company.

Settlements Legislation

The purpose of the Settlements

Legislation, commonly known as

Section 660, is to control who pays tax

on the dividend income derived from

shares allocated to a family member.

There is a common misconception that

when you set up your limited company

you can give shares to family members

in order to pay less tax by making use

of their tax-free allowances. But the

legislation, which targets arrangements

put in place to avoid tax, means that you

may remain assessable for tax on the

dividends you pay to them.

4

Business bank account

Once your company has been incorporated, one of the

most important first steps to take is to set up your

company’s business bank account. Your limited company

is its own legal entity separate from yourself and so you cannot use your own personal bank account.

With strict money laundering regulations,

opening a bank account can be a lengthy

process. So we strongly recommend that

you make a bank application as soon as

possible to avoid any delays in receiving

monies or being able to make payments.

Your clients should pay all monies owed

to the company into this account. All

funds in this account do not belong to you

personally until the company formally

pays you.

It’s totally up to you which bank you

choose for your business banking. You may

wish to liaise with the bank you already

bank with personally, or you can look

for other banks offering useful services

such as internet banking facilities,

downloadable statements, free banking

period offers, good interest rates…

It’s good practice if you choose to run two

accounts: a current account for everyday

banking transactions and a deposit

account to set aside funds for future tax

and VAT liabilities.

If you’re unsure, ACE accounts can

arrange for the Barclays Business Banking

Team to contact you within 24 hours of

your company being incorporated. They’ll

provide a fast-track service and book you

an appointment with a Business Manager

who can establish projected turnover,

international requirements and growth

aspirations to tailor your business banking

requirements.

5

Business insurances

When you run your own business, certain insurances may be needed.

Each one is designed to protect your business against claims from

different parties. Also, check your contracts to see if they stipulate

insurance requirements, and the levels of cover required.

We can put you in touch with specialist

business insurance providers Kingsbridge

Contractor Insurance. They can talk you

through your options, so you choose the

insurance package that’s right for you. They

offer very competitive prices. And we’ve

negotiated the market’s highest discount for

our clients.

Insurance certificates will be held

securely on your online portal, available

whenever you need them.

Professional Indemnity

PI provides you with protection against

claims made against your company as

a result of allegations of professional

negligence.

Most hirers require this insurance as part

of your contract with them.

Public Liability

PL provides protection against

claims for legal liability in respect of

accidental bodily injury to third parties,

or damage to third party property

arising in the course of your business

activities.

Although the hirer may not require you to

hold this insurance, it’s usually advisable

to have it.

Employers Liability

EL provides protection against claims

from employees of your company for

legal liability in respect of injury or

disease which arise in the course

of their work and for which you are

responsible.

Although the hirer may not require you to

hold this insurance, it is usually advisable

to have it and it’s compulsory if you

employ any additional staff.

6

Responsibilities & duties of

a limited company director

As a company director, you are ultimately

responsible for the running of your

company on a day-to-day basis and have

legal responsibilities and duties to uphold

under company law. You’re responsible

for ensuring that the company maintains

accurate accounting records to enable

the preparation of the statutory accounts

and returns.

Whilst ACE accounts will assist you

with the preparation of these returns,

we will be acting upon your instructions,

so our work does not relieve you of your

responsibilities as director.

7

Money laundering

regulations

To comply with the Money Laundering

Regulations, ACE accounts will request

identity and proof of address documents

from you once you agree to appoint us as

your accountant. The process is quick and

easy and you can securely upload your

documents onto your client portal.

8

Statutory filing requirements & deadlines

Every limited company must file certain

statutory documents by their deadlines.

Pay As You Earn (PAYE) & National Insurance Contributions (NICs)

PAYE is the scheme used to collect income

tax and NICs from the gross pay of any

employee. If your company is paying

you or another employee a salary, you

will need a PAYE scheme with HMRC and

submit returns under their Real Time

Information (RTI) system.

Deductions your company makes for

PAYE and NICs are paid to HMRC by the

19th of each month. The exception to this

monthly rule would be if your ongoing

average monthly payments were to be

less than £1,500 – then you could submit

your payments on a quarterly basis. With

your instruction, ACE accounts will

establish and administer either a monthly

or quarterly scheme for you.

Value Added Tax (VAT)

If your company is VAT registered (through

choice or obligation), quarterly returns are

submitted to HMRC at the end of the month

following the quarter end. So, for example,

if your VAT quarter is 1st January to 31st

March, the formal deadline will be 7th May,

but it’s good practice to ensure that they’re

submitted by the end of April.

We can prepare your VAT returns for you.

Corporation Tax

UK limited companies pay corporation

tax (CT) on their profits. The rate of tax

depends upon the level of profits earned.

Profits are calculated on the income (net

of any VAT) less the business costs of the

company such as salaries and day to day

running costs.

The deadline for receiving the Corporation

Tax Return (CT600), detailing the

company’s annual tax liability, is 12

months after the year end but the tax is

usually paid 9 months after the company

year end. Interest is applicable on late

payments. Earlier dates may apply within

the first year of trading. Your ACE

accounts online portal will remind you

of these important dates.

At ACE accounts we will prepare and

file your Corporation Tax Return for you.

Statutory accounts

The Companies House deadline for

receiving abbreviated annual accounts is 9

months after the company’s year-end.

We can help you prepare the annual

statutory accounts.

Companies House Annual Return (AR01)

Within 28 days of each annual anniversary

of your company’s incorporation date,

Companies House requires the submission

of an annual return. This details the

directors, registered office, share capital

and the shareholders. There are no financial

penalties for late filing, but Companies

House may strike off your company from

their register if the return is late.

We can assist you with filing this annual

return along with a set of abbreviated

accounts.

Personal tax return of directors

As a director of the company, you’ll

complete an annual self-assessment tax

return detailing your income from all

sources. The self-assessment process will

calculate any additional tax due which

might include tax on benefits you have

received, if they have not been taxed under

PAYE, or higher rate tax on dividends.

If you’re a director shareholder, you may

receive part of your remuneration package

as a dividend. Dividends are treated as

paid by the company after deduction of tax

at 10%. This 10% ‘tax credit’ covers the

basic rate income tax liability when paid

to you. Further tax will be due at 25%, if

you’re a higher rate tax payer, or 36.1% if

you’re an additional rate tax payer, of the

net dividend you received. This additional

tax will be collected through your self-

assessment.

We can assist you with completing and

filing your self-assessment tax return.

P11D and dispensation

A P11D is an annual form that reports

the cash value of any benefits-in-kind or

expense payments received by directors

and employees during the course of

the tax year. This form allows HMRC to

calculate what additional personal tax may

be due. If you have applied for and been

given a dispensation from HMRC then this

form is not required for those expenses

listed in the dispensation.

At ACE accounts, we can help you

complete and file the P11D. Should you

wish to apply for a dispensation, we can

apply and obtain this from HMRC for

your company.

9

Statutory

Record-keeping

The company is responsible for

maintaining and keeping accounting

and business records for up to 6 years.

With the software that we provide,

together with our help, we make this

very simple for you.

10

Value Added Tax

VAT is a tax that is levied on most goods

and services sold in the UK and unlike

other taxes, VAT is one that is collected by

businesses on behalf of HMRC. The current

standard VAT rate for 2015/16 is 20%.

What VAT schemes are available?

How does VAT work?

Once your company registers for VAT, you

will charge VAT on all your sales invoices.

The good news is that you can reclaim VAT

on your business purchases made from

other VAT-registered businesses.

At the end of every three months your

company will submit a VAT return to HMRC

(ACE accounts can prepare this for you)

which details how much VAT you have

charged and how much you are reclaiming

for that period. You then pay or reclaim the

difference with HMRC.

Do I need to register the company for VAT?

You’ll need to register for VAT if your

company turnover exceeds the current

2015/16 VAT threshold of £82,000 at any

given point in a rolling 12 months, or

expects to do so in the next 30 days. This

isn’t a fixed period like the tax year or the

calendar year – it could be any period, eg

the start of June to the end of May.

What if I want to register for VAT even though I am under the VAT threshold?

If you haven’t exceeded the VAT threshold,

you can still register for VAT voluntarily if

it makes sense to do so. There are several

reasons why you might choose to take this

course of action:

• the clients who use your services

require you to be VAT-registered

• to make your business look more

professional

• the service you supply incurs lots

of expenses where input VAT can be

claimed from HMRC.

How do I register the company for VAT?

We can register your company for VAT.

Just speak to the ACE accounts team.

HMRC try to complete 70% of applications

within 10 working days, but sometimes it

may take longer. Once registered, you will

receive a VAT certificate from HMRC which

we can hold securely on your client portal.

While you’re waiting for your VAT number,

you can enter “VAT number pending” in the

VAT number section of your invoices.

There are two main schemes available:

Standard accounting v. cash accounting:

Under the standard accounting scheme,

VAT is paid based on the date invoices are

raised or received, regardless of whether

they have been paid. Small businesses

can alternatively use the cash accounting

scheme where VAT is paid at the end

of the quarter in which the invoice was

paid. Cash accounting is preferred for its

positive effect on cash flow.

Flat Rate Scheme (FRS):

This scheme is for small businesses with

an estimated annual turnover of less

than £150,000 excluding VAT. Under this

scheme, you do not have to calculate VAT

on each and every transaction. Instead, it’s

simply calculated as a flat-rate percentage

of the gross sales. The flat-rate percentage

is less than the standard VAT rate because

it accounts for the fact that you won’t be

reclaiming VAT on your purchases. The

percentage depends on which industry you

operate in. As an incentive, HMRC offer a

1% discount on the rate in the first year

of registration. For freelancers operating

a small business, the FRS is generally the

most advantageous VAT scheme.

11

Business expenses

What expenses can be claimed?

When it comes to claiming business

expenses as a director of a limited

company, it can be challenging to figure

out what you can and cannot claim. Whilst

in theory you can put almost anything

through your business, in reality the

company will not get tax relief on anything

which is not a legitimate business

expense. What’s more, you are likely to

end up paying more personal tax on the

‘benefit’ you receive from the company.

To know which costs are allowable for tax

relief, HMRC use the expression “wholly,

exclusively and necessarily incurred

in the performance of your duties” and

they will disallow any expenses that do

not fulfil this criteria.

It’s essential to obtain and retain receipts

for all expenses incurred in order to be

able to justify the expense if questioned by

HMRC. This should be a proper till receipt

or invoice, not just a credit card slip. Receipts should be kept for 6 years.

Legitimate business expenses

Legitimate business expenses are unique to

every business and they should contribute

towards the company’s future revenue

generation. They’re likely to include:

• accountancy fees

• business travel and accommodation

• subsistence

• postage, stationery and printing costs

• business telephone calls (if claiming

the cost of the line rental, then the

contract should be taken out in your

limited company’s name and payment

for the line should be made from the

business bank account)

• contributions to executive pension plan

• computer equipment and software

• technical books and business

journals

• training course fees (as long as the

skills are relevant to your business)

• business insurances

• certain professional subscriptions –

must be a professional body on HMRC’s

approved list: https://www.gov.uk/

government/publications/professional-

bodies-approved-for-tax-relief-list-3/

approved-professional-organizations-

and-learned-societies

• use of home as office (a flat £4 per week

without receipts is allowed by HMRC)

• cost of advertising and marketing

your business

• company bank charges and interest

• eye tests if you regularly use a

computer in course of your work

• business entertainment

• annual Christmas party event

allowance of £150 per employee.

HMRC do not allow...

...any expenses deemed to be personal/

non-business related. These can include:

• ordinary commuting

• items for personal use such as

cameras and televisions

• rent, mortgage or council tax of your

main residence

• private club subscriptions such as

gym or golf club membership

• clothing (except safety clothing) such

as business suits

• training courses not related to your

business

• glasses – unless used solely for

VDU use.

How is an expense claim made?

You claim via the accountancy software

provided by ACE accounts on your

online portal and then reimburse the total

expenses value to yourself monthly from

the funds held in your business bank

account.

24-month rule

Some expenses, such as travel to and from

home, subsistence and accommodation

can only be claimed where your workplace

is ‘temporary’. A workplace is a ‘temporary’

workplace if the assignment will last, or

you expect it to last, less than 24 months.

40% rule

One exception to the 24-month rule is

where you spend 40% or less of your time

at a site. Then all expenses travelling to

and from that site are allowed.

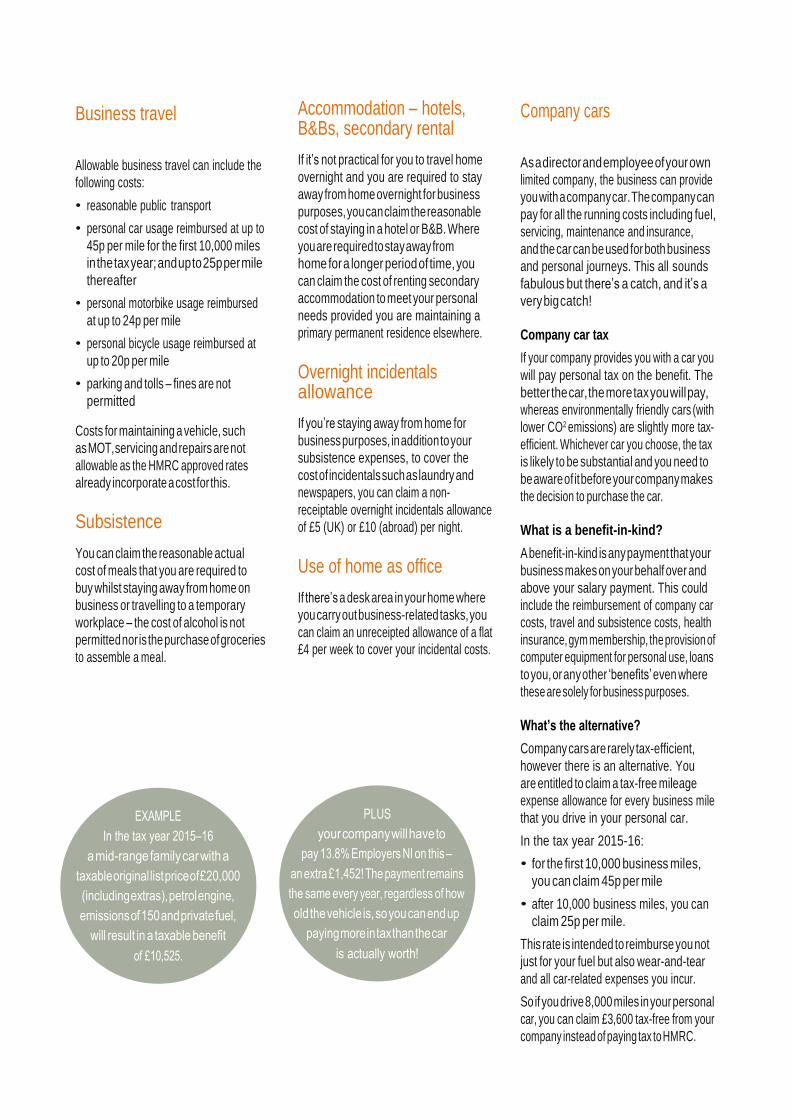

Business travel

Allowable business travel can include the

following costs:

• reasonable public transport

• personal car usage reimbursed at up to

45p per mile for the first 10,000 miles

in the tax year; and up to 25p per mile

thereafter

• personal motorbike usage reimbursed

at up to 24p per mile

• personal bicycle usage reimbursed at

up to 20p per mile

• parking and tolls – fines are not

permitted

Costs for maintaining a vehicle, such

as MOT, servicing and repairs are not

allowable as the HMRC approved rates

already incorporate a cost for this.

Subsistence

You can claim the reasonable actual

cost of meals that you are required to

buy whilst staying away from home on

business or travelling to a temporary

workplace – the cost of alcohol is not

permitted nor is the purchase of groceries

to assemble a meal.

Accommodation – hotels, B&Bs, secondary rental

If it’s not practical for you to travel home

overnight and you are required to stay

away from home overnight for business

purposes, you can claim the reasonable

cost of staying in a hotel or B&B. Where

you are required to stay away from

home for a longer period of time, you

can claim the cost of renting secondary

accommodation to meet your personal

needs provided you are maintaining a

primary permanent residence elsewhere.

Overnight incidentals allowance

If you’re staying away from home for

business purposes, in addition to your

subsistence expenses, to cover the

cost of incidentals such as laundry and

newspapers, you can claim a non-

receiptable overnight incidentals allowance

of £5 (UK) or £10 (abroad) per night.

Use of home as office

If there’s a desk area in your home where

you carry out business-related tasks, you

can claim an unreceipted allowance of a flat £4 per week to cover your incidental costs.

Company cars

As a director and employee of your own

limited company, the business can provide

you with a company car. The company can

pay for all the running costs including fuel,

servicing, maintenance and insurance,

and the car can be used for both business

and personal journeys. This all sounds

fabulous but there’s a catch, and it’s a

very big catch!

Company car tax

If your company provides you with a car you

will pay personal tax on the benefit. The

better the car, the more tax you will pay,

whereas environmentally friendly cars (with

lower CO2 emissions) are slightly more tax-

efficient. Whichever car you choose, the tax

is likely to be substantial and you need to

be aware of it before your company makes

the decision to purchase the car.

What is a benefit-in-kind?

A benefit-in-kind is any payment that your

business makes on your behalf over and

above your salary payment. This could

include the reimbursement of company car

costs, travel and subsistence costs, health

insurance, gym membership, the provision of

computer equipment for personal use, loans

to you, or any other ‘benefits’ even where

these are solely for business purposes.

What’s the alternative?

Company cars are rarely tax-efficient,

however there is an alternative. You

are entitled to claim a tax-free mileage

expense allowance for every business mile

that you drive in your personal car.

In the tax year 2015-16:

• for the first 10,000 business miles,

you can claim 45p per mile

• after 10,000 business miles, you can

claim 25p per mile.

This rate is intended to reimburse you not

just for your fuel but also wear-and-tear

and all car-related expenses you incur.

So if you drive 8,000 miles in your personal

car, you can claim £3,600 tax-free from your

company instead of paying tax to HMRC.

12

IR35

What is IR35?

IR35 is a piece of legislation which

HMRC introduced in April 2000. It

deals specifically with individuals who

‘freelance’ through a limited company

but work as if they are an employee of

the hirer. The initial intention of IR35 was

to stop a traditional employee leaving

his/her job one day, only to return to

work in the same or similar role shortly

afterwards, but working via a limited

company structure to reduce the amount of

income tax (PAYE) and national insurance

contributions (NIC) that they pay.

IR35 attempts to determine the true

employment status of the freelancer by

examining the relationship between them

and the hirer to establish whether it is one

of ‘disguised’ employment or a genuine

business-to-business relationship.

Inside or outside IR35?

Under the legislation, the onus is on the

director of the limited company to decide

whether a specific contract or assignment

passes or fails IR35.

If the relationship is assessed to be one

of employment, you are said to be ‘inside’

IR35 and as such need to pay PAYE and NIC

on 95% of the assignment income after

the deduction of any direct assignment

costs (which will include gross salaries

and pension contributions paid by the

company during the year).

If your contract falls ‘outside’ IR35, you can

take the more tax-advantageous route of

having a lower salary and higher dividends

which is the preferred option of most

limited company directors.

The IR35 status of an individual is

determined on an assignment-by-

assignment basis by a combination of

both the contractual terms and the actual

working practices.

Factors HMRC consider

HMRC have a set of guidelines to help

them form their opinion of employment

status.

The main three are:

• the right to send a substitute when

the principal worker (you) is not

available

• whether the worker can be told what

to do and how to do it (the level of

control)

• whether there is any obligation

for the worker to offer or provide

ongoing services to the hirer.

We strongly recommend that you get each

assignment you undertake professionally

reviewed so as to determine its IR35

contract status.

The ACE accounts team can put you in

contact with specialist IR35 advisors QDOS

who can talk you through your options

and help you determine whether you are

inside or outside of the IR35 tests. We’ve

negotiated a market-leading discount for

their services and you can interact directly

with them via your giant portal.

13

Remuneration – ways

to withdraw funds

Expenses

Expenses are the costs which you incur

personally on behalf of your business.

Your company can reimburse you for these

costs, however rules apply. Take a look at

our expenses information in chapter 11 or

contact the ACE accounts team.

Salary

You can pay yourself a salary at

whatever level you choose.

Although directors are not bound by the

National Minimum Wage (NMW), the

majority of freelancers choose to pay the

equivalent of at least the NMW at a higher

level, as:

• it utilizes your personal tax-free

allowance

• it preserves your National Insurance

contributions record

• it may be required for references or

mortgage applications

• it shows HMRC that you are covering

your normal outgoings with salary.

If your assignment falls ‘inside’ of IR35,

you will need to pay yourself the majority

of your income as salary.

Salary to a partner or spouse

Some freelancers may choose to pay a

salary to a partner or spouse in order

to benefit from their partner’s tax

allowance. To benefit from this, the

partner or spouse must be involved in

the running of the business and you

can clearly demonstrate this.

Dividend

A dividend is a profit-share payment

made from the post-tax profits of a

company, to the shareholders (owners)

of the company.

Dividends are generally a more tax

efficient method of withdrawing money

from your company, as they are taxed

differently to salary and are not subject

to National Insurance contributions.

14

Financial planning

Pensions

Company pension contributions represent

one of the most tax-efficient ways of

using business profits as it can save

National Insurance Contributions (NICs),

income tax and corporation tax.

You can choose to make pension

contributions personally, or your limited

company can make them for you (paid

from the company bank account).

Company Pension Contributions

The company can contribute up to

£40,000 each year into your pension

pot. This contribution will reduce your

corporation tax liabilities as it will be

treated as a business expense.

Personal Pension Contributions

You may choose to contribute into a

pension personally if you’re a higher-

rate tax-payer and would like to extend

your basic tax-rate band. This would be

beneficial if you only wanted to make

small pension contributions and you

would receive income tax and NICs relief

on this.

Income protection

As a freelancer operating your own

business, you do not have the protection

of sick pay, so it’s worth considering

income protection cover. When you’re

reviewing policies, you’ll want to ensure

that both salary and dividends are

covered.

Critical illness cover

On top of income protection, critical

illness cover can pay out a lump sum or

monthly allowance in the event of being

diagnosed with a critical illness.

Personal accident cover

You may wish to protect yourself as a

result of an accident that leaves you

unable to work. Plans typically pay out

a weekly amount whilst recovering from

an injury, or a lump-sum payment for

death or permanent disablement. We’ve

negotiated the best market discounts

with specialist business insurance

providers Kingsbridge who can offer

advice and very competitive prices.

Mortgages

The challenge freelancers often face is

that mainstream lenders don’t always

understand how freelancers work and

may see this as a barrier to keeping up

with mortgage repayments.

It’s well worth speaking with mortgage

brokers who specialize in the freelance

industry. They should be able to secure

you a competitive mortgage with many of

the mainstream lenders. We can introduce

you to specialists.

15

Closing your company

Dormancy

If you plan to take a long break from

freelancing, you may want to consider

making your company ‘dormant’. This

is a temporary suspension of some

services, but the company remains on the

Companies House Register as a trading

company and all returns still have to be

filed.

The advantage of putting your company

into dormancy is that the company

remains there and ready to use when you

need it – no need to re-register for VAT –

and the company bank account is already

up and running. You may need to re-

register for the PAYE scheme. The ACE

accounts team can help you with this.

Winding up

If you don’t think you’ll need your

company again in the foreseeable

future (eg if you take on a permanent

role) you can opt to wind it up. This is

permanent closure. The company will

be de-registered for VAT and PAYE, so

there’s usually just one final submission

to make.

Final accounts are submitted to HMRC

and then you can apply to have the

company struck off the Companies House

register.

If there’s money left in your company, you

have options to distribute the funds:

• make a company pension contribution,

which reduces your corporation tax bill

• pay the remaining funds out as a

dividend, which may be subject to

income tax

• distribute funds as capital, which has

a potentially lower overall tax charge,

as the distribution is subject to capital

gains tax not income tax, and it can

also attract Entrepreneurs Relief.

? Just ask.

Questions then why not call in or call us

Technology House 151 Silbury Boulevard

Milton Keynes MK9 1LH

Tel No: 01908 424365 Fax: 01908 424347 Web: www.aceaccountax.co.uk

Email: [email protected]