Accountable Care Act Employer Compliance.sharedoc.

15

ACCOUNTABLE CARE ACT EMPLOYER SHARED RESPONSIBILITY COMPLIANCE ROADMAP FOR HEALTH PLANS ACA Insurance Mandate Employer Compliance Guide Roberta E. Winter, MHA, MPA, healthpolicymaven.com [email protected] Abstract Much of the focus on the Accountable Care Act and the Public Health Services Act mandates for employer medical plans address compliance but do not discuss opting out. This guide provides analysis of both outcomes so employers and their representatives can make informed decisions.

-

Upload

roberta-winter -

Category

Documents

-

view

31 -

download

0

Transcript of Accountable Care Act Employer Compliance.sharedoc.

ACCOUNTABLE CARE ACT EMPLOYER SHARED

RESPONSIBILITY COMPLIANCE ROADMAP FOR HEALTH

PLANS ACA Insurance Mandate Employer Compliance Guide

Roberta E. Winter, MHA, MPA, healthpolicymaven.com [email protected]

Abstract Much of the focus on the Accountable Care Act and the Public Health Services Act mandates for

employer medical plans address compliance but do not discuss opting out. This guide provides analysis of both outcomes so employers and their representatives can make informed decisions.

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 1

ACA Employer Responsibility Compliance Roadmap for Health Plans

Table of Contents P.2 Author Credentials P. 3-5 Explanation of the Accountable Care Act 2015 Medical Insurance

Mandate for Employers P. 6-7 Instructions for Determining Includable Employees, Measuring Plan

Participation, and Contribution Testing P. 8-10 Calculation of Penalties P. 11 Conclusion P. 12 Bibliography P. 13-17 Opt Out Kit for Employers-This is provided under separate cover for

purchase and is not part of the whitepaper, which is offered for free. The compliance kit includes election forms, an interactive presentation, and an employee notification poster.

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 2

Author Credentials Roberta E. Winter is a veteran of the health insurance industry, having spent over fifteen years negotiating health & welfare contracts for private employer benefit plans. Winter owned her own insurance brokerage firm for eight years, before returning to school in 2002. She completed work on her Master of Health Administration degree from the University of Washington, School of Public Health and Community Medicine in 2004. Her studies focused on health policy and her graduation capstone project was developing a radio broadcast called, “Increasing the Engagement of the Public in Understanding Health Systems.” In 2007, she completed work for her Master of Public Administration from the University of Washington, Evans School of Public Affairs. In addition to these formal education programs, she also completed a Master of Science in Management, for financial institutions, from the American College in Bryn Mawr, Pennsylvania in 2000. Winter maintains her life and health insurance license in Washington State, but does not sell or provide insurance plan advice. She has published more than fifty articles on healthcare policy and regulatory issues since 2007. She has also served as a peer reviewer for academic articles and a technical writer for health care and other scientific publications. In 2013, her first book Unraveling U.S. Healthcare-A Personal Guide, was published by Rowman and Littlefield, a respected institutional book publisher. For more information on her work, you may read her monthly column, Straight Talk on Healthcare or follow the healthpolicymaven through social media. Winter still performs healthcare consulting for policy analysis and process improvement through her corporation, Praevalere Inc.

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 3

Accountable Care Act Employer Responsibility Compliance Roadmap for Health Plans Beginning in 2015, businesses will have to meet certain standards for health care plans in the United States and this is your roadmap for compliance to the employer insurance mandate. Health Plan Provisions for All Employers with Fifty or More Workers Public Health Services Act, Section 2708 stipulates that health plans offered by employers with fifty or more employees are subject to these standards: Waiting period maximum is ninety days before an employee is enrolled in the medical plan Children who are still dependents of their parents are able to remain on parent’s coverage to age 26 Pre-existing conditions clauses are not allowed

Benefit Specifications Though the Patient Protection and Affordable Care Act mandates that employers provide medical coverage to employees, the specific benefit design specifications mostly apply to traditionally insured health plans. However, neither self-insured nor fully insured medical plans may exceed the ninety day waiting period limit, they must cover adult children to age 26, and finally, pre-existing conditions clauses which restrict insurance coverage are not allowed. Minimum health benefits, which are part of the insurance mandates for essential coverage, also apply to self-insured medical plans. Penalties for noncompliance If a self-insured plan fails to comply with the provisions of the Public Health Services Act, employees designated as highly compensated individuals could lose the tax favored status of their benefits, which means they would have to pay tax on their health plan benefits. If an insured group health plan fails to comply with the provisions of section 105-H of the Public Health Services Act, an excise tax may be exacted. 1 If a self-funded plan does not offer a medical plan that meets the minimum for essential health benefits, an excise tax may be demanded, starting in 2015. Safe Harbor Provisions Safe harbor provisions include foreign employees, or those working in other countries. The PHSA and the ACA applies to employees working within the confines of the United States and its territories. Compliance Testing To comply with the federal regulations regarding the provision of employer provided health insurance plans, continue to the next section and work through the exercises to determine your eligibility and if you have to pay a penalty for a noncompliant plan.

1 Internal Revenue Service Notice 2011-1 and found online at: http://www.irs.gov/pub/irs-drop/n-11-01.pdf (Service November)

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 4

Mandates Effective in 2015 I. Determining the Number of Eligible Employees for the Participation Test The first thing any employer needs to assess is whether or not the 50 employee standard applies. Note that the penalty for noncompliant or nonexistent medical plans is waived for employers with less than 100 employees for 2015. First you must determine which employees are included in the criteria for insurance eligibility. Figure 1

Determining full-time employee equivalents requires an algorithm and here are the steps in more detail: Have you had fifty or more fulltime or fulltime equivalent employees in the prior year? If you have a lot of part-time employees or if you own multiple corporations which are part of a controlled group, you still need to do this analysis. Determine your fulltime employees, which for purposes of the ACA are those working at least 30 hours a week. The language “on average” is used, but that can be a bit dicey, I suggest using a quarterly look-back. Next, determine your fulltime equivalent employees, which is defined as anyone who has worked at least twenty hours in a month. The ACA also allows employers to use the 130 hours-per-month of work definition to determine fulltime status. Take the number of hours the employees worked in this category and divide it by the number of employees to arrive at your sum. Determine all other employees, regardless of the hours worked and divide that sum by 120 To assess whether or not your firm is subject to the fifty employees or more ACA compliance mandates, add the sums of the fulltime employees, the fulltime equivalents, and the sum for the “other employees” criteria. If this total equals or exceeds fifty, you must comply with the federal mandates of the Affordable Care Act. This total also determines which provisions of the Public Health Services Act apply and the various sections of the Internal Revenue Service Code.

Determine if You Have 50 Employees

1st-How Many Employees Work an Average of 30 hours a Week

2nd-Determine Fulltime Equivalent Employees-Anyone Working at Least 20 Hours a Month

3rd-Divide the Number of Hours Worked by the Number of Fulltime Equivalent Employees

4th-Determine the Number of Other Employees By Dividing the Total of Employees Left by 120

5th-Add the sums of the Fulltime, the Fulltime Equivalent, and the Other Employees Criteria.

If 50 or more-Your Firm Must Comply with the Insurance Mandates or Pay a Fine per Eligible Employee

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 5

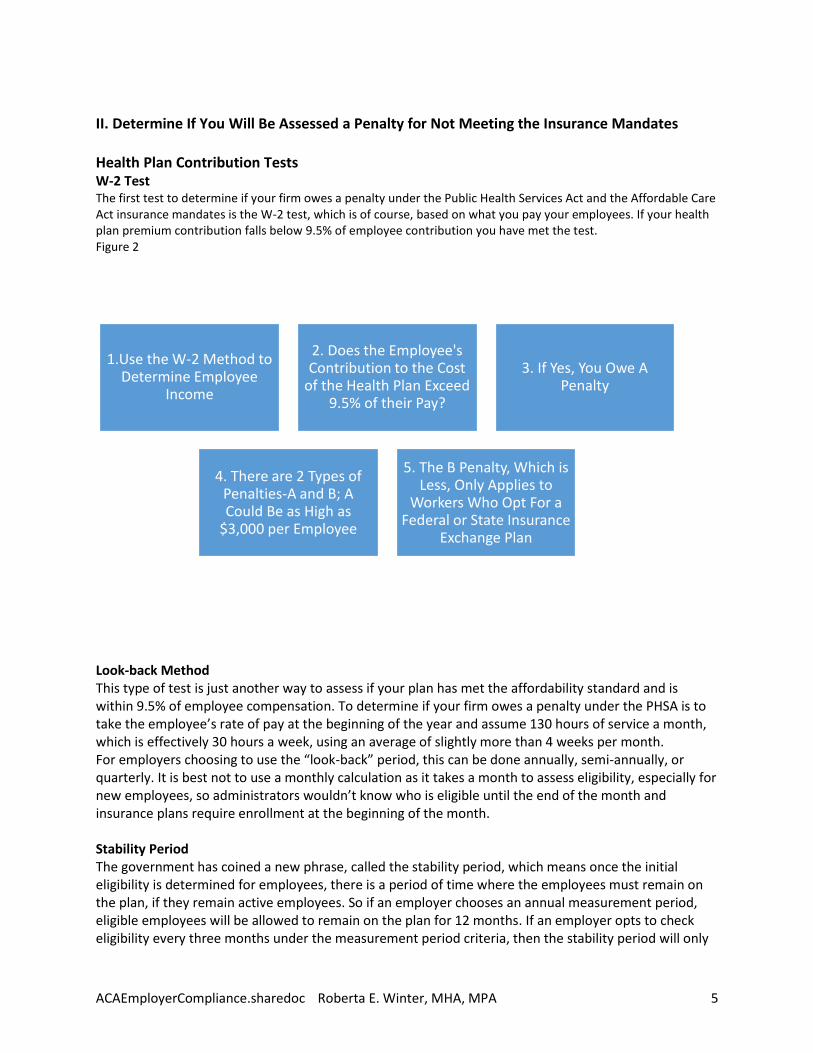

II. Determine If You Will Be Assessed a Penalty for Not Meeting the Insurance Mandates Health Plan Contribution Tests W-2 Test The first test to determine if your firm owes a penalty under the Public Health Services Act and the Affordable Care Act insurance mandates is the W-2 test, which is of course, based on what you pay your employees. If your health plan premium contribution falls below 9.5% of employee contribution you have met the test. Figure 2

Look-back Method This type of test is just another way to assess if your plan has met the affordability standard and is within 9.5% of employee compensation. To determine if your firm owes a penalty under the PHSA is to take the employee’s rate of pay at the beginning of the year and assume 130 hours of service a month, which is effectively 30 hours a week, using an average of slightly more than 4 weeks per month. For employers choosing to use the “look-back” period, this can be done annually, semi-annually, or quarterly. It is best not to use a monthly calculation as it takes a month to assess eligibility, especially for new employees, so administrators wouldn’t know who is eligible until the end of the month and insurance plans require enrollment at the beginning of the month. Stability Period The government has coined a new phrase, called the stability period, which means once the initial eligibility is determined for employees, there is a period of time where the employees must remain on the plan, if they remain active employees. So if an employer chooses an annual measurement period, eligible employees will be allowed to remain on the plan for 12 months. If an employer opts to check eligibility every three months under the measurement period criteria, then the stability period will only

1.Use the W-2 Method to Determine Employee

Income

2. Does the Employee's Contribution to the Cost

of the Health Plan Exceed 9.5% of their Pay?

3. If Yes, You Owe A Penalty

4. There are 2 Types of Penalties-A and B; A Could Be as High as

$3,000 per Employee

5. The B Penalty, Which is Less, Only Applies to

Workers Who Opt For a Federal or State Insurance

Exchange Plan

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 6

be for three months. This effectively means that an employee’s health plan inclusion status could change every quarter. Federal Poverty Level Method The federal poverty level method of assessing health plan compliance stipulates that as long as the employee is not expected to pay more than 9.5% of his or her income for health insurance, the plan is acceptable. This is different than the qualified federal and state insurance exchange standards which state that 8% of adjusted gross income is the maximum an employee is expected to pay for health insurance. This table shows the 2014 federal poverty level standards in the 48 contiguous states. Income levels qualifying for poverty status are higher in Alaska and Hawaii.2 (U.S. Department of Health & Human Services, n.d.)

2 (Health & Human Services Agency 2015)

Federal Assistance for Medical Insurance Purchasing

Federal Subsidies to buy medical in the insurance exchanges impact people earning between 133%-400% of the federal poverty level

FPL

Income

Under

133%

Equal to

133%

Equal to

133%

Equal to

133%

Equal to

133%

Equal to

133%

Equal to

133%

Equal to

133%

Equal to

133%

Up to

400%

Up to

400%

Up to

400%

Up to

400%

Up to

400%

Up to

400%

Up to

400%

Up to

400%

Base

income

level $15,654 $15,654 $21,187 $26,720 $32,253 $37,785 $43,318 $48,851 $54,384 $47,080 $63,720 $80,360 $97,000 $113,640 $130,280 $146,920 $163,560

Family size All 1 2 3 4 5 6 7 8 1 2 3 4 5 6 7 8

Governme

nt subsidy 98.00% 97.00% 97.00% 97.00% 97.00% 97.00% 97.00% 97.00% 97.00% 90.50% 90.50% 90.50% 90.50% 90.50% 90.50% 90.50% 90.50%

Av/yr/

insurance

premium/fa

mily $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102 $7,102

Indiv/net

cost/yr $72 $108 $343 $675 $675 $675 $675 $675 $675 $675

Family net

cost/yr $142 $213 $213 $213 $213 $213 $213 $213 $213 $675 $675 $675 $675 $675 $675 $675 $675Monthly

Cost 11.84$ 17.76$ 17.76$ 17.76$ 17.76$ 17.76$ 17.76$ 17.76$ 17.76$ 56.22$ 56.22$ 56.22$ 56.22$ 56.22$ 56.22$ 56.22$ 56.22$

Notes:

Poverty levels are based on 2015 federal guidelines and are for the 48 contiguous states.

Insurance estimates are from Kaiser Foundation's 2010 survey of people who bought individual insurance contracts. The average price paid for a single individual was $3,600, family insurance price is in the chart.

Regional Insurance Exchange Premiums will probably be higher than these costs because of mandated coverage levels.

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 7

How to Avoid an Employer PHSA Shared Responsibility Penalty The good news is that a modest health plan can still avoid the tax penalties and here are the criteria to meet this hurdle, according to Alan Tawshunsky, Tax Counsel for the Department of the Treasury.3 Coverage Test-The health plan must be offered to the fulltime employees, as defined in the previous eligible employee section or the employer will have to pay a tax penalty. The level “B” penalty would only apply to employees who opted to purchase insurance through a federal or state insurance exchange (only for those firms with fifty or more eligible employees). Benefit Level Test- To avoid the “A” penalty of $2,000 per employee, the health plan must meet the minimum benefit threshold of 60% based on an actuarial formula. The acceptable health plan benefit threshold can be determined two ways, by going to the government Health & Human Services web site and use their calculator4 or by using one of the percentage of income methods previously described. Health plan coverage must be offered to at least 33% of the workforce and at least 25% must enroll to avoid a 2015 penalty. Note that the employer penalty for a noncompliant or nonexistent medical plan is waived for employers with less than 100 includable employees for 2015. Here is the link to the Centers for Medicare and Medicaid Minimum Health Plan Value Calculator, which provides a downloadable EXCEL file for which you can enter your firm’s data:

http://www.cms.gov/site-search/search-results.html?q=health%20plan%20minimum%20value%20calcuator

Once you have determined if your plan meets an acceptable level of employer responsibility you only need to pay a tax penalty for the employees who opt out of the employer plan for the insurance exchange model. Typically these employees will make this selection because they are eligible for the federal tax credits, which apply to all (green card or citizen requirements apply) individuals within 400% of the federal poverty rate. The penalty due would be based on the B penalty schedule as opposed to the A penalty. Determining Your Tax Penalty Now that you understand the requirements for medical insurance or health plans, it is possible that your firm may not meet the standards and have to pay a tax penalty. In fact, some of you may wish to avoid a group insurance plan altogether and simply pay the penalty. Of course there are many considerations in this complex decision making process including; the availability of health care plans through state and federal insurance exchanges, the ability of people, regardless of their health to obtain medical insurance under the Affordable Care Act, and the high cost of health insurance plans. There are also many methods to reward and recognize employees such as a fixed benefit allowance per year, which could be used to purchase individual insurance, a pay raise in lieu of insurance, and voluntary programs. To assist you in this process, here is a quick summary: If you plan does not meet the participation or benefit specifications of the ACA you will have to pay a $2,000 penalty per includable employee.

3 Alan Tawshunsky, Tax Counsel, U.S. Department of the Treasury; Affordable Care Act: Employer Shared Responsibility, Compliance Assistance Seminar, U.S. Department of Labor Health Benefits Education Campaign in coordination with the Washington Office of the Insurance Commissioner, Bothell Washington, August 20, 2014 4 Centers for Medicare and Medicaid, Fact Sheet, May 16, 2014, and found online at: http://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/Downloads/Final-Master-FAQs-5-16-14.pdf

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 8

If your plan meets the benefit specifications and the participation requirements, you may only have to pay a penalty for those employees who opt out of the employer plan and chose an insurance exchange plan. This penalty is $3,000 for every employee who opts to obtain coverage through a state or federal insurance exchange and is called the B penalty. If your firm decides not to offer a medical plan you will have to pay a tax of $2,000 per includable employee. This is called the A penalty.

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 9

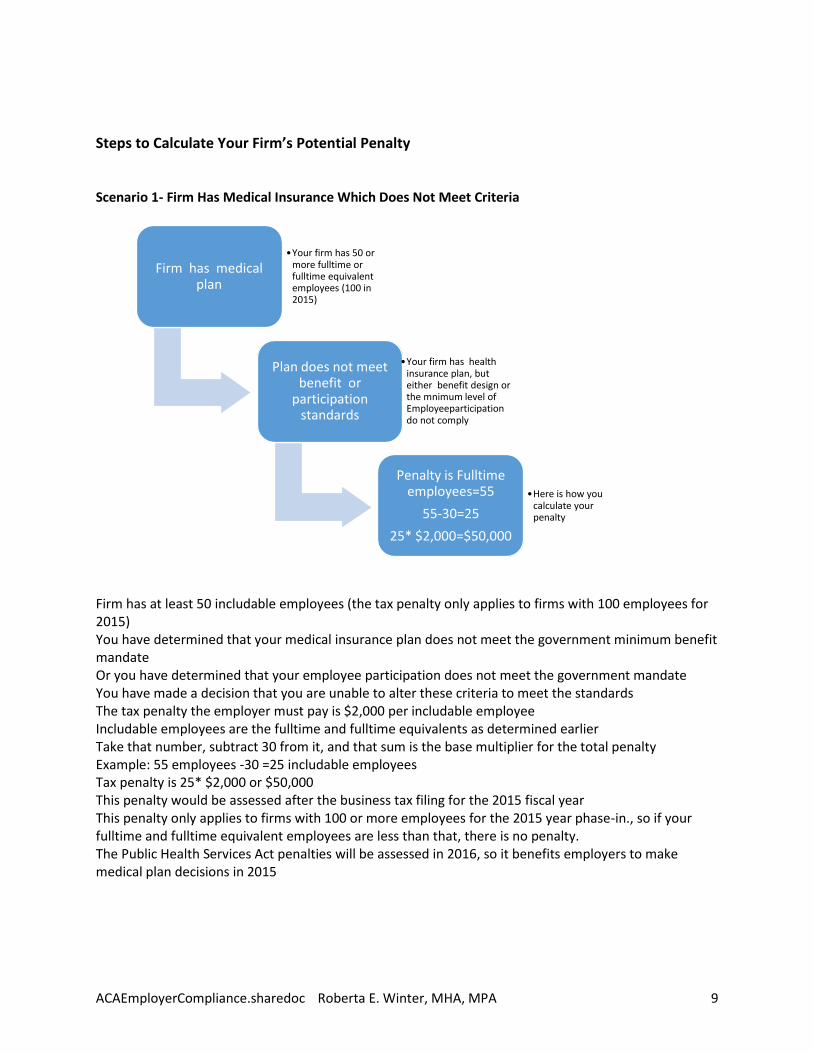

Steps to Calculate Your Firm’s Potential Penalty Scenario 1- Firm Has Medical Insurance Which Does Not Meet Criteria

Firm has at least 50 includable employees (the tax penalty only applies to firms with 100 employees for 2015) You have determined that your medical insurance plan does not meet the government minimum benefit mandate Or you have determined that your employee participation does not meet the government mandate You have made a decision that you are unable to alter these criteria to meet the standards The tax penalty the employer must pay is $2,000 per includable employee Includable employees are the fulltime and fulltime equivalents as determined earlier Take that number, subtract 30 from it, and that sum is the base multiplier for the total penalty Example: 55 employees -30 =25 includable employees Tax penalty is 25* $2,000 or $50,000 This penalty would be assessed after the business tax filing for the 2015 fiscal year This penalty only applies to firms with 100 or more employees for the 2015 year phase-in., so if your fulltime and fulltime equivalent employees are less than that, there is no penalty. The Public Health Services Act penalties will be assessed in 2016, so it benefits employers to make medical plan decisions in 2015

Firm has medical plan

•Your firm has 50 or more fulltime or fulltime equivalent employees (100 in 2015)

Plan does not meet benefit or

participation standards

•Your firm has health insurance plan, but either benefit design or the mnimum level of Employeeparticipation do not comply

Penalty is Fulltime employees=55

55-30=25

25* $2,000=$50,000

•Here is how you calculate your penalty

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 10

Scenario 2-Firm Does Not Offer Medical Insurance

Firm has at least 50 fulltime or fulltime equivalent employees (penalty only applies to those with 100 or more in 2015) Firm has decided not to offer a medical insurance plan or a self-funded plan Determine the fulltime and fulltime equivalent employees Subtract 30 from that total and this is the multiplier for the penalty tax Multiply $2,000 by that number Example-100 FT EE-30 = 70 70 * $2,000 = $140,000 Compare that to the cost of purchasing medical insurance for at least 100 employees That cost averages $4,885 per year according to the Kaiser Family Foundation Net cost to the firm is still less than providing medical insurance for workers >$400,000 Employees can go to federal or state insurance exchanges and obtain medical insurance, with government subsidies to help pay the premiums, regardless of their health Employer does not have to be in the insurance business Penalty is assessed after the filing of the 2016 tax year for firms with 50-99, but does apply to firms with 100 employees in 2015

Firm has no medical plan

•No medical insurance

Determine includable EE's

•Fulltime and FT equivalent Employees

Total FT EE's is 30

30* $2,000= $60,000•Calculate Penalty

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 11

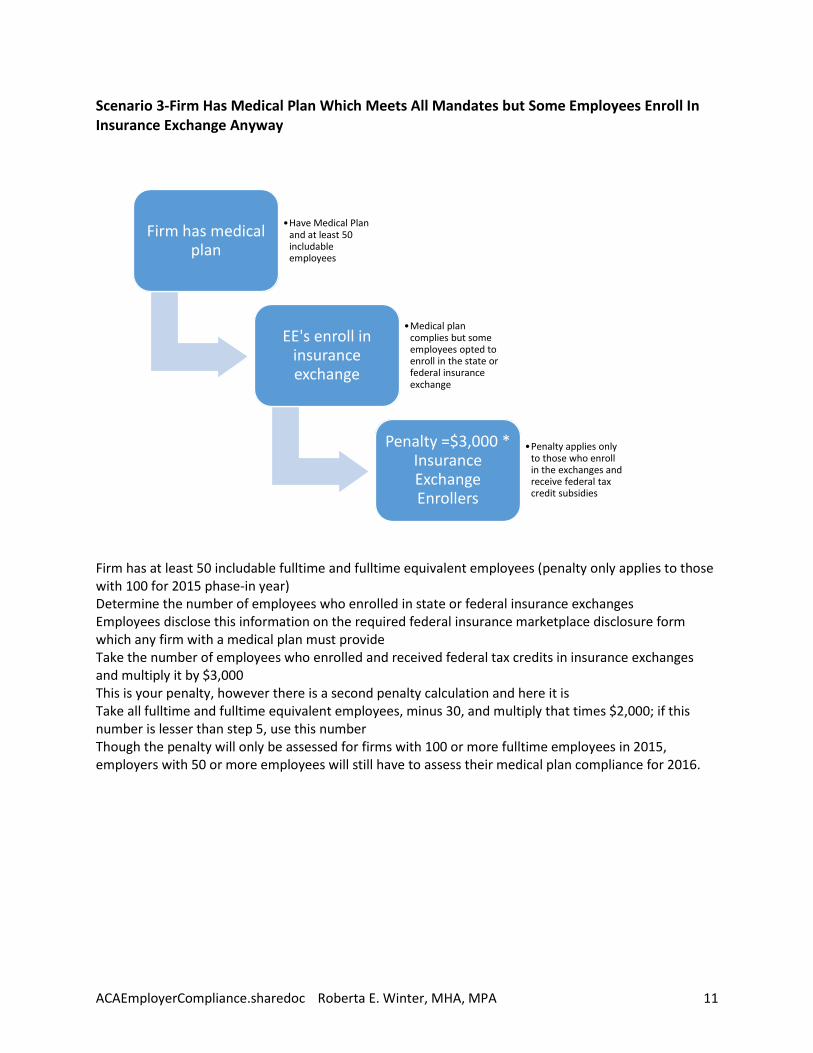

Scenario 3-Firm Has Medical Plan Which Meets All Mandates but Some Employees Enroll In Insurance Exchange Anyway

Firm has at least 50 includable fulltime and fulltime equivalent employees (penalty only applies to those with 100 for 2015 phase-in year) Determine the number of employees who enrolled in state or federal insurance exchanges Employees disclose this information on the required federal insurance marketplace disclosure form which any firm with a medical plan must provide Take the number of employees who enrolled and received federal tax credits in insurance exchanges and multiply it by $3,000 This is your penalty, however there is a second penalty calculation and here it is Take all fulltime and fulltime equivalent employees, minus 30, and multiply that times $2,000; if this number is lesser than step 5, use this number Though the penalty will only be assessed for firms with 100 or more fulltime employees in 2015, employers with 50 or more employees will still have to assess their medical plan compliance for 2016.

Firm has medical plan

•Have Medical Plan and at least 50 includable employees

EE's enroll in insurance exchange

•Medical plan complies but some employees opted to enroll in the state or federal insurance exchange

Penalty =$3,000 * Insurance Exchange Enrollers

•Penalty applies only to those who enroll in the exchanges and receive federal tax credit subsidies

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 12

Transition Relief for Employers in 2015 During 2015, the employer group can use any six months in a plan year to determine eligibility and it does not have to be six consecutive months. This means the employer could “game the system” if it wanted to put in the effort. Also, medical coverage must be offered to 33% of the workforce and 25% must actually be covered on the plan. In other words, an employer can’t have a sham group health plan. This harkens back to the pre ERISA days when employers set up fabulous pensions for themselves, to the exclusion of their employees, resulting in the “top heavy” rules to prevent discrimination and tax ruses. ERISA is the Employee Retirement Income Security Act of 1976, which was landmark legislation for employee benefit plans and included the provision for self-insured medical plan exemptions, as well as the pension rules. Final Remarks In conclusion, the government has determined and the courts have upheld the provision of medical insurance as a Patient Protection and Affordable Care Act requirement. Additionally, the Supreme Court upheld the right of the government to assess fines through the Public Health Services Act, for employers who do not comply with the law. If you are an employer with fifty or more fulltime or fulltime-equivalent employees, you must provide medical insurance or a medical plan and contribute an acceptable amount toward the cost of the program, or pay a tax penalty. However, since the cost of a group medical plan is now $4,885 per year just for the employee, many employers may elect to pay the $2,000 or $3,000 per employee penalty and avoid the employer health plan morass. According to the Kaiser Family Foundation’s 2013 Survey of Employer-Sponsored Health Benefits, family health plan premiums now run $11,786.5 This means the employer may also opt to pay a penalty on some classes of employees who fall under the annual shared responsibility rules, but continue to operate a health benefit plan. It is doubtful that many employers with fifty or more employees would cancel a medical benefits program, as this would have a negative impact on recruitment and retention of employees. However, smaller employers may choose to reduce the size of their firm in order to avoid the penalties. For brevity purposes this article has not listed any of the exemption criteria for the Accountable Care Act or Public Health Services Act provisions, though employers may elect not to provide birth control coverage for employees, they are not exempt from the insurance mandate. For more information on the exemption criteria go to this previously published article, Religiously Exempt Health Care Reimbursement Plans-A Closer Look, which was published in Straight Talk on Healthcare, on August 13, 2014 and is found online at: http://healthpolicymaven.blogspot.com/2014/08/v-behaviorurldefaultvmlo.html This document was written by Roberta E. Winter, who is a health policy analyst, consultant, and author of Unraveling U.S. Healthcare-A Personal Guide, published by Rowman and Littlefield in 2013 and found online at: http://www.amazon.com/Unraveling-U-S-Health-Care-Personal/dp/1442222972#. This document does not offer tax, legal, or insurance advice. It is meant as a simplified guide to important provisions of the Affordable Care Act and the Public Health Services Act. This document is protected by copyright laws of the United States and any reprints are subject to the author’s permission. For questions on the document please contact Ms. Winter at [email protected].

5 Kaiser Family Foundation 2013 Survey of Employer Sponsored Health Benefits and found online at: http://kff.org/report-section/2013-summary-of-findings/

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 13

Bibliography Alan Tawshunsky, J.D. 2014. "Tax Counsel, U.S. Department of the Treasury." Affordable Care Act:

Emoloyer Shared Responsibility, Compliance Assistance Seminar, U.S. Department of Labor, Health Benefits Education Campaign. Bothell, Washington.

Health & Human Services Agency, U.S. A. 2015. U.S. Federal Poverty Guidelines Health & Human Services. January 1. Accessed March 2015, 30. http://aspe.hhs.gov/poverty/15poverty.cfm#thresholds.

Henry J. Kaiser Family Foundation. 2014. 2013 Survey of Employer Sponsored Health Benefits. Menlo Park, CA: Kaiser Family Foundation. Accessed November 2014. http://kff.org/report-section/2013-summary-of-findings/.

Internal Revenue Service Notice 2011-1. n.d. http://www.irs.gov/pub/irs-drop/n-11-01.pdf. Service, Internal Revenue. November. Internal Revenue Service Public Notice. 1. Accessed October 2014,

2014. http://www.irs.gov/pub/irs-drop/n-11-0.pdf. U.S. Centers for Medicare and Medicaid. 2014. Centers for Medicare and Medicaid Fact Sheet, CCHIIO.

May 16. http://www.cms.gov/CCIIO?Resources/Fact-Sheets-and-FAQs/Downloads/Final-Master-FAQs-5-16-14.pdf.

ACAEmployerCompliance.sharedoc Roberta E. Winter, MHA, MPA 14