ABFA 3114 Principle of Audit

151

School of Business Studies ABFA 3114 PRINCIPLES OF AUDITING

description

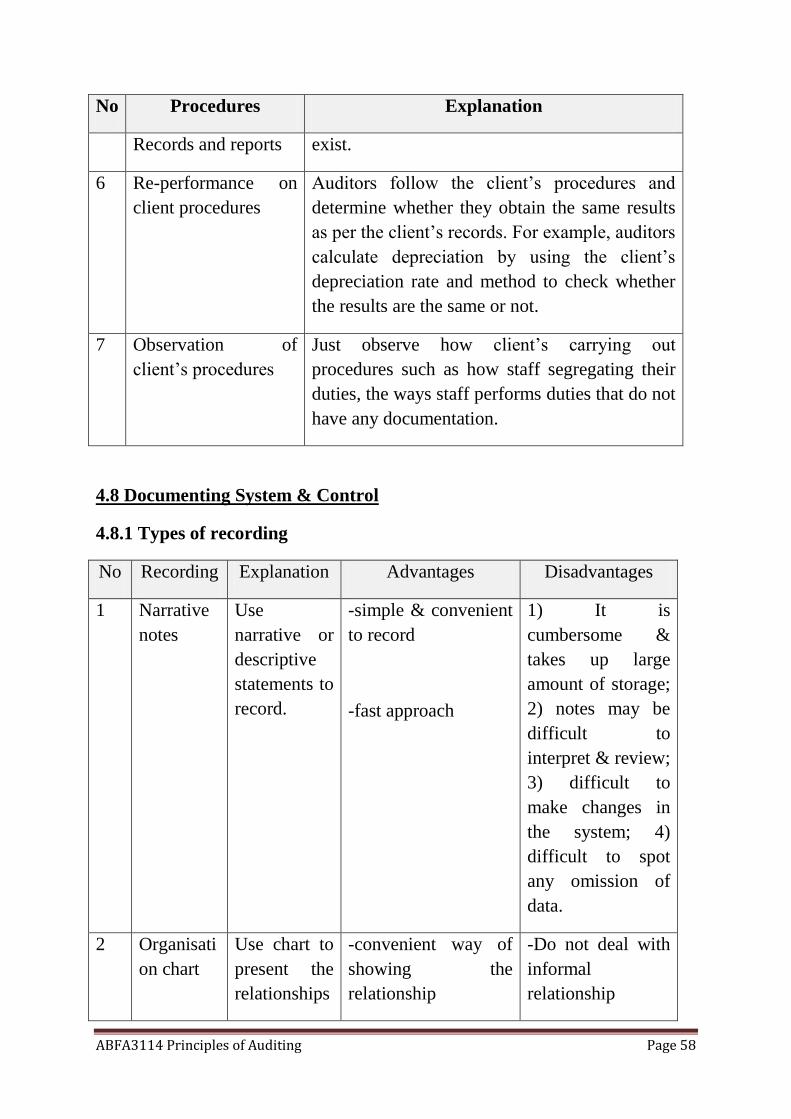

Additional Notes

Transcript of ABFA 3114 Principle of Audit

School of Business Studies

ABFA 3114 PRINCIPLES OF AUDITING

ABFA3114 Principles of Auditing Page 2

TABLE OF CONTENT

A Syllabus and Course Strategy

Unit Plan

Assessment Format

B Chapter

1: Introduction to Auditing

2: Regulatory Framework and Professional Ethics

3: Auditor‟s Report

4: Accounting and Internal Control Systems

5: Audit Evidence

6: Audit Procedures

7: Audit Risk and Materiality

8: Audit Planning and Control

9: Auditing Cash & Bank System

10: Auditing Property, Plant & Equipment

11: Computer in Auditing

ABFA3114 Principles of Auditing Page 3

Course Strategy and Syllabus

Unit title : Principles of Auditing

Unit code : ABFA 3114

Level of study : 3

Credit point : 4

School offering this unit : School of Business Studies

Class contact Hours

Average Weekly : 4

-Lecture : 3

-Tutorial : 1.5

-Practical : none

Semester : 7

Assessment mode : Examination (60%) Coursework (40%)

Pre-requisite unit : none

Co-requisite unit : none

Rationale

The unit introduces students to the role of external audit, a core activity in the

accountancy profession. Accounting students at this level must have an

understanding of the role and responsibility of the external auditor in relation to

an independence audit and the principles that bind the auditor.

Aims

1. To provide students with a basic understanding of the nature, purpose and

scope of a statutory audit

ABFA3114 Principles of Auditing Page 4

2. To equip students with basic knowledge of an audit process and the

general auditing procedures an external auditor undertakes to achieve the

audit objectives

3. To enable students to apply their knowledge in the audit of Property,

Plant and Equipment (PPE) and Cash and Bank systems.

Anticipated Learning Outcomes

On completion of this unit, students should be able to :

1. Explain the development, nature, purpose and scope of an audit in

relation to the regulatory framework that affects or binds the auditor

2. Demonstrate an understanding of audit risk assessment.

3. Apply the internal control systems in PPE and cash and Bank system

4. Explain the key audit procedures to be performed in relation to a given

audit objective

5. Demonstrate an understanding of the elements and types of audit report.

Syllabus Content

1. Nature, purpose, scope and regulatory framework of auditing (20%)

2. An understanding of audit planning and audit strategy and audit evidence

(25%)

3. Accounting system and internal control (20%)

4. Audit procedures (20%)

5. Audit report (15%)

Skills Integration

Skills developed in the unit include identifying auditing issues in a given

scenario and applying the appropriate auditing procedures

ABFA3114 Principles of Auditing Page 5

Teaching and Learning Strategy

Topics will be introduced by ways of lectures and developed through tutorials.

During tutorials, Q&A sessions are held to assess students‟ understanding of the

concepts, principles and procedures of auditing. In addition, students are also

grouped into smaller groups of 5-6 students per group where they work together

on a given scenario to identify key auditing issues and apply the appropriate

procedures.

Core text

1. Auditing and Assurance Service in Malaysia, Messier/Glover/Prawitt

Margaret Boh, 3rd

Edition, Mc Graw Hill (ISBN978-983-3850-075) 2007.

Other references

2. Auditing In Malaysia- An Integrated Approach, Alvin A. Arens, 11th Edition.

ABFA3114 Principles of Auditing Page 6

SCHOOL OF BUSINESS STUDIES

Week Topic Reference

Week 1

Introduction to Auditing AAS-Chapter 1 & 2

Week 2

Regulatory Framework and Professional

Ethics

AAS- Chapter 1,2 & 19

Week 3

Auditor‟s Report AAS- Chapter 18

Week 4

Accounting and Internal Control System AAS- Chapter 6

Week 5

Audit Evidence AAS- Chapter 4

Week 6

Audit Procedures (I) AAS- Chapter 4

Week 7

Audit Procedures (II) AAS- Chapter 4

Week 8

Audit Risk and Materiality AAS-Chapter 3

Week 9

Audit Planning and Control (I) AAS- Chapter 5

Week 10

Audit Planning and Control (II) AAS- Chapter 5

Week 11

Auditing Cash and Bank System AAS-Chapter 16

Week 12

Auditing Property, Plant & Equipment AAS- Chapter 14

Week 13

Computer in Auditing AAS- Chapter 7

Week 14

Computer in Auditing AAS- Chapter 7

Reference

Core text

1. Auditing and Assurance Service (AAS) in Malaysia, Messier/Glover/Prawitt

Margaret Boh, 3rd

Edition, Mc Graw Hill (ISBN978-983-3850-075) 2007.

Other references

2. Auditing In Malaysia- An Integrated Approach, Alvin A. Arens, 11th Edition.

ABFA3114 Principles of Auditing Page 7

Assessment Format

There are 2 parts of your assessment of the course: group assignment and final

examination.

Component Threshold

Course

work

40% Group Assignment 40 marks

Mid-term Test 60 marks

100 marks x

0.4

50%

Final Exam 60% Written Exam 100 marks x

0.6

40%

Total 100%

Group Assignment

You will be required to form a group and carry out a specific research on the

subject topics.

Format of Final Examination

The final examination will be of THREE (3) hours long and comprise two

parts:

Part A: One Compulsory question (25%). You are given a case study and you

are required to analyse the case and apply the theories to the scenario.

Part B: You are required to answer THREE (3) questions out of FOUR (4)

questions. You are given some short questions to work on. Each question

constitutes 25%.

ABFA3114 Principles of Auditing Page 8

CHAPTER 1

INTRODUCTION TO AUDITING

________________________________________________________________

Learning Outcomes

When you have completed this lesson you will be able to:

Understand the nature, purpose and scope of audit

Distinguish between accounting and auditing

Understand different types of audits and auditors

Understand the concept of true and fair view

Reference text: Auditing and Assurance Services in Malaysia- Chapter 1 & 2

ABFA3114 Principles of Auditing Page 9

1,1 Nature, Purpose and Scope of Audit

1.1.1 A statutory audit simply means “a legally required examination of an

organisation‟s annual accounts and financial records”.

1.1.2 The objective/purpose of an audit is to enable the auditor to express an

opinion on whether the financial statements are prepared, in all material

respects, in accordance with an applicable financial reporting framework.

1.1.3 Auditors do not certify or guarantee the correctness of financial

statements; they report whether in their opinion they give a “True and

Fair View” of the financial position. True and Fair View (UK) = Present

Fairly (US). Express opinion is different from guarantee or certification

of 100% correctness. Auditor just obtains reasonable assurance that the

financial statements do not contain material misstatement (serious

mistakes).

1.1.4 Reasonable assurance means the auditor obtains certain degree of

comfort that the financial statements do not contain material

misstatement.

1.1.5 Why reasonable (less than 100%) assurance? Or why not absolute (100%)

assurance? This is because auditing has some inherent limitations.

These inherent limitations are:

Use of sampling testing. Auditors use samples to test the

transactions because it is impossible for auditor to check every

transaction. When applying sampling, there is always a risk of

taking the wrong samples.

Inherent limitations of internal control. There is always

possibility of employee collusion, management override or human

errors.

Audit evidence is persuasive, not conclusive. Persuasive means

giving evidence to believe; whereas, conclusive means 100%

correct or wrong.

Use of auditor’s judgement. Auditors often use professional

judgement to make decision where there is always a risk that the

judgement may be inappropriate.

ABFA3114 Principles of Auditing Page 10

1.1.6 In Malaysia, external audit of financial statements is mandatory (i.e.

mandatory audit is also known as Statutory Audit) for every company,

regardless of size, that is registered under Malaysia‟s Companies Act

1965.

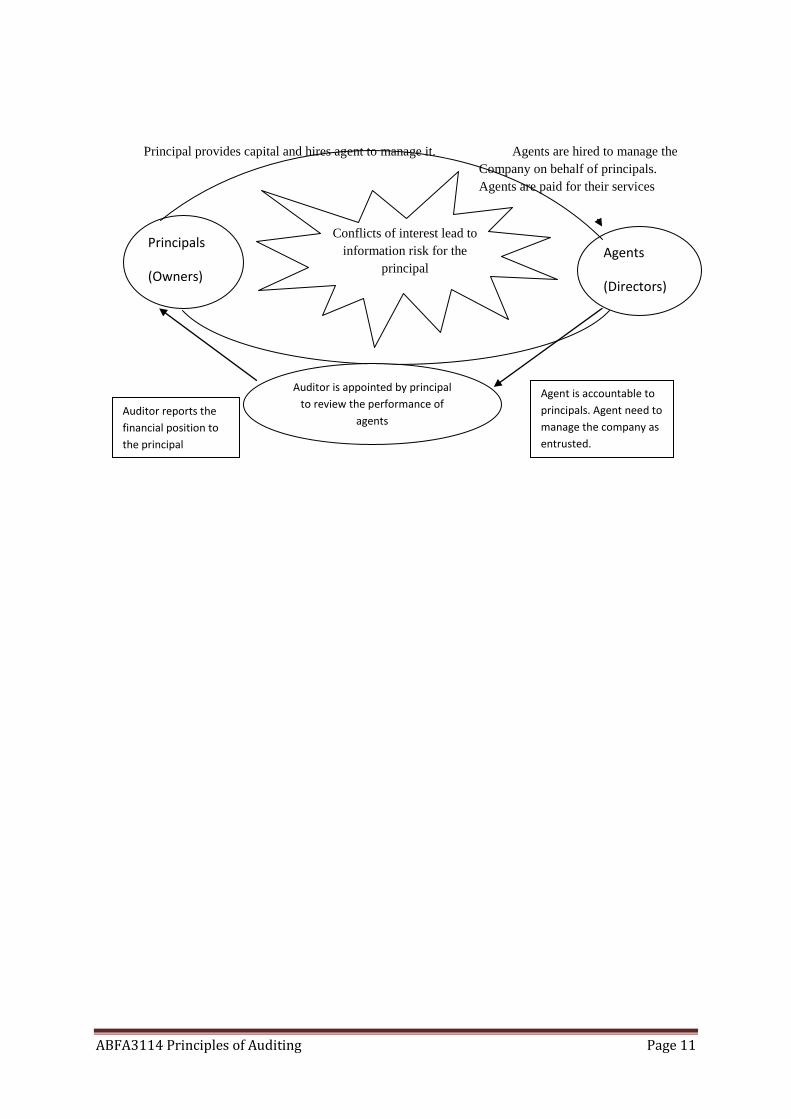

1.1.7 The concept of agency (Principals and Agents)

Modern auditing has developed since the concept of a company as a

separate legal entity came into existence. It means the separation of

ownership and the management of the company.

For listed companies the owners of company are its shareholders and they

may not be involved in the daily operation of company. The company

will be run by directors, who are elected by shareholders. The

shareholders expect a return on investment, while the directors expect to

be paid for salary.

Thus shareholders need to have confidence that accounts prepared by

directors are accurate and comply with the required standards and

regulations. To ensure that the financial statements are drawn accurately,

they employ auditors to check its financial statements.

The job of external auditors is to report whether the financial statements

show True & Fair view. By having this independence check the

shareholders gain confidence in terms of money is being handled

properly.

ABFA3114 Principles of Auditing Page 11

Principal provides capital and hires agent to manage it. Agents are hired to manage the

Company on behalf of principals.

Agents are paid for their services

Conflicts of interest lead to

information risk for the

principal

Principals

(Owners)

Agents

(Directors)

Auditor is appointed by principal

to review the performance of

agents Auditor reports the

financial position to

the principal

Agent is accountable to

principals. Agent need to

manage the company as

entrusted.

ABFA3114 Principles of Auditing Page 12

An overview of the Principal-Agent relationship leading to the demand for

auditing

1.1.8 The concepts of accountability, stewardship and agency.

Accountability means that people in positions of power can be held to

account for their action. For example, they are compelled to explain their

decision/action or be punished if they have misuse their power.

Stewardship is the responsibility to take good care of resources. A

steward is someone employed to manage another person's property.

A fiduciary relationship is a relationship of good faith such as between

directors and shareholders. The directors must take their decisions in the

interests of the shareholders rather than in their own personal interest.

Agents are people employed or used to provide a particular service. In

the case of a company, the people being used to provide the service

managing the business also have the second role of being people in their

own right trying to maximise their personal wealth

Directors’ Accountability and Responsibilities

Directors are accountable to the shareholders for the assets that they

control on their behalf. It means that the directors are responsible for the

preparation of the accounts of the company. If the directors ask

accounting firm to perform its accounting functions, they could not

escape their responsibilities to the shareholders. The directors are

responsible for the proper set up of accounts.

1.1.9 Advantages of a statutory audit

a. Dispute between management may be more easily settled

b. Major changes in ownership may be facilitated if the past accounts

contain an unqualified audit report

c. To enhance the loan application

d. To improve efficiency of the business operation by improving internal

control system or control procedures

e. To serve as a basis for preparation of tax returns

ABFA3114 Principles of Auditing Page 13

1.1.10 Disadvantages of an Audit

a. Audit fee is incurred

b. Disruption of work to the client‟s staff

1.2 Distinction between Auditing and Accounting

1.2.1 These activities are closely related but separated activities. It is very

common that some companies engage the same accountant from the same

accounting and audit firm to prepare the accounts. It should make clear

that the directors are still responsible for the preparation of accounts.

1.2.2 A………………… is the recording, classifying and summarising of

transactions in a systematic manner for the purpose of providing financial

information for decision making.

1.2.3 A……………… is a process of reviewing the transactions and balances

of accounting records to project a true and fair view of the financial

position of the company.

1.3 Different types of audits and auditors

1.3.1 Types of audit

a. F…………………………… Audit. It is conducted to determine

whether the overall financial statements are prepared according to the

acceptable accounting principles. The financial statement audit covers

the audit on Statement of Financial Position, Statement of

Comprehensive Income, statement of changes in shareholders‟ equity

and cash flow statement together with the accounting policies and

explanatory notes to the financial statements.

b. O………………….. Audit. It is conducted on the operating

procedures and process of the organisation to determine whether it is

operating in effective and efficient manner. At the end of the

operational audit, auditor will recommend how to improve

effectiveness and efficiency of the whole organisation‟s operation

system.

ABFA3114 Principles of Auditing Page 14

c. C……………… Audit. It involves checking whether the organisation

follows the specific laws, regulations, specific procedures set by the

authority. For example, a compliance audit for a listed company may

focus on whether the company follows the stock market ruling and

pays the appropriate taxes.

d. F………………. Audit. It is a special investigation audit that mainly

focuses on fraud, criminal cases, shareholders dispute or negligence. It

requires high investigation skills, knowledge and experience to obtain

and develop information as legal evidence or for use by expert

witnesses in the court of law.

1.3.2 Types of auditors

a. I………………… Auditors. They are employees of organisation

whose activity set by management to examine and evaluate the

organisation‟s risk management processes and systems of control, and

to make recommendations for the achievement of company objectives.

The focus of internal audit now is on adding value to an organisation

through improvements in controlling risk and looking at all types of

risk and control. It functions by, amongst other things, examining,

evaluating and reporting to management and the directors on the

adequacy and effectiveness of components of the accounting and

internal control systems.

The Roles of Internal Audit (IA)

IA is part of the organisational control of a business; it is one of the

methods used to ensure the orderly and efficient running of the

business.

A properly function of IA is part of a good corporate governance,

as recognised by national and international codes on corporate

governance

IA procedures meet the needs of good corporate governance of

meeting the needs of all stakeholders.

IA enable management exercises proper risk management

ABFA3114 Principles of Auditing Page 15

b. E……………….. Auditors (or Public Accounting Firm). They are

external parties who conduct auditing services for both public and

private companies. For example, Ernst & Young, KPMG,

PriceWaterhouseCoopers, Delloite, Crowe Horwarth and so on. It is

an exercise whose objective is to express an opinion whether the

financial statements give a true and fair view of the organisation 's

activities have been properly prepared in accordance with the

applicable reporting framework.

c. G……………….. Auditors (also known as Auditor General) are

responsible for auditing all the Federal government, State government,

public authorities and the statutory bodies‟ accounts. At the Federal

level, the Auditor General reports to the King (Yang Di-Pertuan

Agong) and presents his audit reports to the House of Parliament.

d. F………………….. Auditors. They are specially trained to detect,

investigate and deter fraud and crime.

e. Inland Revenue Assessment Auditor. These auditors are responsible

for enforcing the Income Tax Act. They audit tax payers‟ returns to

determine whether the computation of taxes is complied with the laws.

1.3.3 Difference between internal audit and external audit (SAROL)

Internal Audit External Audit

Scope (S) Cover all areas

including operation and

finance

Financial focus

Approach (A) Risk based, assess risk,

evaluation on control

system, test on

operations of system,

and make

recommendations for

improvement.

Risk based, test on

transactions that form

the basis of the final

financial statement

ABFA3114 Principles of Auditing Page 16

Responsibility ( R) Advise and make

recommendations on

internal control and

corporate governance.

Form opinion on

financial statements.

Objectives (O) Advise to protect

organisation against

loss due to weak

internal control

Provide opinion on

financial statement

whether provide True &

Fair view

Legal (L) Not legal requirement.

But recommended to

have internal audit dept

for good corporate

governance practice

Legal requirement to

have an audit on their

financial statement

1.4 The concept of true and fair view

1.4.1 External auditors give an opinion on the truth and fairness of financial

statements. It does not mean that the financial statements are free from

error.

1.4.2 It is generally understood that the presentation of accounts are drawn up

according to accepted accounting principles using accurate figures as far

as possible and reasonable estimates and arranging them so as to show a

true picture of accounts that free from material bias, distortion,

manipulation or concealment of material facts.

1.4.3 True - Information is factual and conforms to the reality, not false. In

addition the information must conform to the required standards and

laws. And, the accounts have also been correctly extracted from the

books and records.

ABFA3114 Principles of Auditing Page 17

1.4.4 Fair - Information is free from discrimination and bias and in

compliance with expected standards and rules. The accounts should

reflect the commercial substance of the company's underlying

transactions. Fairness depends on the following factors:

Relevance of the information to the user‟s needs

Free from bias

Facts can be verified by evidence

Materiality of item. A transaction is material if its disclosure would

change the user‟s view on the accounts.

1.4.5 Why the concept of true and fair is important to auditor? This is

because:

Auditor certainly cannot certify/guarantee the accounts are 100%

accurate and free from mistakes. This is because auditor uses

sampling method to draw audit evidence to support the opinion.

Moreover, there many different accounting interpretations and

presentation such as depreciation, goodwill, inventory etc.

The concept of truth and fairness is more important than 100%

accurate.

In reaching his opinion whether accounts show true and fair view,

the auditor is required to exercise his skills and judgment.

1.5 The Chronology of an audit

Determine audit approach

Stage 1. Determine the ..................... of the audit and the auditors' approach.

For statutory audits the scope is laid down by legislation and

expanded by Auditing Standards. The auditors should prepare an

audit plan, which should be placed on file.

Ascertain the system and controls

Stage 2. Determine the flow of ....................... and extent of .................... in

existence in the client's system.

ABFA3114 Principles of Auditing Page 18

This is a fact finding exercise which is achieved by discussing the

accounting system and document flow with all the relevant

departments (for example, sales, purchases, cash, inventory and

accounts personnel).

It is good practice to make a rough record of the system during this

fact finding stage which will be converted to a formal record at

Stage 3.

Stage 3. Prepare a comprehensive record of the system to facilitate

evaluation of the systems. The records may be in various formats

(for example, charts, narrative notes, internal control

questionnaires and flowcharts).

Stage 4. Confirm that the system recorded is the same as that in operation.

This is achieved by performing walk-through tests. These involve

tracing a handful of transactions through the system and observing

the operation of controls over them.

This check is useful because sometimes client staff will tell the

auditors what they should be doing rather than what is actually

done.

Assess the system and internal controls

Stage 5. Evaluate the .................. to determine their reliability and

formulate a basis for testing their effectiveness in practice.

Test the system and internal controls

Stage 6. (This should only be carried out if the controls are evaluated as

effective at Stage 5. If not, Steps 6 and 7 should be omitted.)

If controls are effective, tests should are designed to establish

compliance with the system should be selected and performed.

Tests of controls, which cover a larger number of items than

walkthrough tests and cover a more representative sample of

transactions through the period, should be carried out.

If controls are strong, the records should be reliable and the

amount of detailed testing can be reduced. If controls are

ineffective in practice, more extensive substantive procedures will

be required.

ABFA3114 Principles of Auditing Page 19

Stage 7. After evaluating the systems and testing controls, auditors normally

send an interim report to management identifying weaknesses

and recommending improvements.

Test the financial statements

Stages These tests are concerned with substantiating the figures given in the

final financial statements

8 and 9. Substantive tests also serve to assess the effect of errors, should

errors exist.

Before designing a substantive procedure it is essential to consider

whether any errors produced could be significant. If the answer is

no, there is no point in performing a test.

Review the financial statements

Stage 10. The financial statements should be reviewed to determine the

overall reliability of the account by making a critical analysis of

content and presentation.

Express an opinion

Stage 11. The auditors evaluate the evidence that they have obtained and

they express their .............................. to members in the form of

an audit report.

Stage 12. The final report to .................................... is an important end

product of the audit. The purpose of it is to make further

suggestions for improvements in the systems and to place on

record specific points in connection with the audit and the

accounts.

ABFA3114 Principles of Auditing Page 20

CHAPTER 2

REGULATORY FRAMEWORK AND PROFESSIONAL ETHICS

________________________________________________________________

Learning Outcomes

When you have completed this lesson you will be able to:

Understand the provision of Companies Act in audit

Explain the duties, power and responsibility of auditor

Explain the responsibility of auditor in detecting fraud and errors and

illegal activities

Understand the professional ethics.

Reference text: Auditing & Assurance Services in Malaysia- Chapter 1,2 & 19

ABFA3114 Principles of Auditing Page 21

2.1 Understand the provision of Companies Act in audit

2.1.1 Section 169 of the Companies Act 1965 requires the directors of every

company to present the audited financial statements that give true and fair

view of the activities of the company in its annual general meeting.

2.1.2 Under Section 174 of the Companies Act, 1965, there are two main

requirements relating to the auditor‟s reporting duties:

The auditor must state, whether in his opinion, the financial statements

have been properly drawn up in accordance with the provisions of the Act

and applicable approved accounting standards, so as to give a true and

fair view of the company‟s state of affairs and result of operations; and

matters required by section 169 to be dealt with in the financial

statements; and

The auditor must state, whether in his opinion, the accounting and other

records and the registers required by the Act to be kept by the

company, have been properly kept in accordance with the Act.

2.1.3 Under the Companies Act, 1965, the statutory duties of company directors

in relation to accounting functions are:

Ensuring proper accounting records are kept. Directors are

required to design the accounting system and keep all the accounting

records of the companies in a proper manner.

Taking reasonable steps to safeguard the assets of the company

and prevent and detect fraud and errors. Directors are responsible

for designing an effective internal control system to protect the

companies‟ assets from any possibility of fraud and error.

Preparing financial statements that give true and fair view.

Though, directors may delegate the preparation of financial

statements to accountant, they are still responsible for ensuring the

financial statements are drawn up in accordance with the standards

and regulation.

Adopting good accounting policies and establish adequate

internal control. Directors are responsible for compliance to the

best practice of accounting standards and effective internal control

system.

ABFA3114 Principles of Auditing Page 22

File in annual return of the company to Companies Commission

of Malaysia (CCM). Directors are responsible for preparing an

annual return to the regulators.

2.1.4 Appointment of Auditors.

Appointed by When

Members

(Shareholders)

Shareholders can appoint the first auditors of the

company or to fill a casual vacancy and the auditor will

hold office until the end of first annual general meeting.

In an Annual General Meeting (AGM), shareholders can

reappoint retiring auditor, appoint a new auditor or

appoint an auditor who has been appointed by directors

previously.

Directors Directors can appoint the company‟s first auditor between

the date of incorporation (establishment) and the first

AGM. Directors can also appoint an auditor to fill in a

causal vacancy.

Companies

Commission of

Malaysia (CCM)

If a company does not appoint an auditor as requested by

Companies Act-section 172, the CCM can appoint an

auditor.

2.1.5 Disqualification of Auditors. Under section 9(1) of the Companies Act, a

person is prohibited from acting or accepting an appointment as the auditor

of company if he is:

Indebted to the company or its related company in an amount

exceeding RM2,500.

An officer of the company.

A partner, employer or employee of an officer of the company.

A partner, employee of an employee of an officer of the company.

A shareholder of the company whose employee is an officer of the

company or

Responsible for or if he is the partner, employer or employee of a

person responsible for keeping company‟s assets or the register of

debenture holders of the company

ABFA3114 Principles of Auditing Page 23

2.1.5 Departure from auditor’s office. Auditors can leave office by one of the

following reasons:-

Resignation

Not seeking reappointment

Being removed at a general meeting before their term of office is

expired.

Being removed at a general meeting at which their term of office is

expired.

2.1.6 Resignation usually requires written notice by the auditor to the company

and to the CCM. It also requires a statement of circumstances. The auditor

concerned is permitted to speak and communicate in writing with shareholders

and other stakeholders.

RESIGNATION OF AUDITORS

1 Resignation procedures Auditors deposit written notice together with

statement of circumstances or statement

that no circumstances exist relevant to

members/creditors

2 Notice of resignation Sent by company to regulatory authority

3 Statement of

circumstances

Sent by:

(a) Auditors to regulatory authority

(b) Company to everyone entitled to receive a

copy of accounts

4 Convening of general

meeting

Auditors can require directors to call

extraordinary general meeting to discuss

circumstances of resignation

Directors must send out notice for meeting

within 21 days of having received requisition

by auditors

5 Statement prior to

general meeting

Auditors may require company to circulate

(different) statement of circumstances to

everyone entitled to notice of meeting

6 Other rights of auditors Auditors can receive all notices that relate to:

(a) A general meeting at which their term of

office would have expired

ABFA3114 Principles of Auditing Page 24

RESIGNATION OF AUDITORS

(b) A general meeting where casual vacancy

caused by their resignation to be filled

(c) Auditors can speak at these meetings on

any matter which concerns them as auditors

2.1.7 Removal of auditor

Any removal or resignation of auditor before end of the audit contract

implies serious disagreement b/w auditor and client. If auditors disagree

with the fee or accounting practices, they simply do not offer themselves

to be reappointment. Removal must usually be notified to regulatory

authority. 2/3 majority resolution is required to remove an auditor. The

concerned auditor is given the right to make written representations

and speak at the meeting or AGM.

Removal procedures. The reasons to have removal procedures are to

ensure that the auditors are not removed for improper reasons without the

knowledge of the shareholders and auditors do not seek to avoid their

responsibility by going quietly.

Removal

Procedure

Description

1 Notice of removal Either special notice (28 days) with copy sent to

auditor

Or if elective resolution in place, written

resolution to terminate auditors' appointment

Directors must convene meeting to take place

within reasonable time.

2 Representations Auditors can make representations on why they

ought to stay in office, and may require company to

state in notice representations have been made and

send copy to members.

3 If resolution is

passed (a) Company must notify regulatory authority

(b) Auditors must deposit statement of

circumstances at company's registered office

ABFA3114 Principles of Auditing Page 25

Removal

Procedure

Description

within 14 days of ceasing to hold office. Statement

must be sent to regulatory authority.

4 Auditor rights Auditor can receive notice of and speak at:

(a) General meeting at which their term of office

would have expired

(b) General meeting where casual vacancy caused

by their removal to be filled

The auditor will have to issue a written statement either:

(i) Statement of ............................ (Some disagreement issues need to be

highlighted to the attention of the shareholders. E.g. Fraud, severe disagreement

over accounting practice)

OR

(ii) Statement of ............................. (No issues need to be brought to the

attention of the shareholders. E.g. Disagreement over auditor fee)

2.2 Explain the duties, power and responsibility of auditor

2.2.1 Auditor’s rights and duties

The audit is primarily a statutory concept, and eligibility to conduct an audit is

often set down in statute. Similarly, the rights and duties of auditors can be set

down in law, to ensure that the auditors have sufficient power to carry out an

effective audit.

Auditor’s Duties

The duties of the auditors are:-

(a) To report the shareholders/directors on whether the financial statements

show true and fair view and have been properly prepared, in all material

respect, in accordance with legislation and applicable accounting standards.

(b) To consider whether the information in the management report is

consistent with the audited financial statement

ABFA3114 Principles of Auditing Page 26

(c) To give various details required by legislation in their report. Common

details are directors‟ transactions & emoluments.

(d) To form opinion on the financial statements whether they are presented in

true and fair view.

(e) To report on any violation of law or the company‟s constitution.

(f) To make a “statement of circumstance” when they cease to hold office for

any reason.

Auditor’s Rights

The principal rights auditors should have, excepting those dealing with

resignation or removal, are set out in the table below, and the following are

notes on more detailed points.

Access to records A right of access at all times to the books,

accounts and vouchers of the company

Information and

explanations

A right to require from the company's

officers such information and explanations

as they think necessary for the performance

of their duties as auditors

Attendance at/notices of

general meetings

A right to attend any general meetings of

the company and to receive all notices of

and communications relating to such

meetings which any member of the

company is entitled to receive

Right to speak at general

meetings

A right to be heard at general meetings

which they attend on any part of the

business that concerns them as auditors

Rights in relation to

written resolutions

A right to receive a copy of any written

resolution proposed

Right to require laying of

accounts

A right to give notice in writing requiring

that a general meeting be held for the

purpose of laying the accounts and reports

before the company (if elective resolution

dispensing with laying of accounts in force)

ABFA3114 Principles of Auditing Page 27

2.3 Explain the responsibility of auditor in detecting fraud and errors and

illegal activities

2.3.1 Auditors’ Responsibility for the Prevention & Detection of Fraud &

Error

ISA 240 The Auditor’s Responsibility to Consider Fraud in an Audit of

Financial Statements states that:-

Fraud is to intentional acts which may involve the falsification of documents

or misappropriation of assets.

Error is the unintentional misappropriation of accounting policies,

oversights or misinterpretations of facts.

In the new audit engagement, auditors should be very careful to avoid accepting

responsibility for detection of fraud that they cannot discharge.

2.3.1 Management responsibility in preventing fraud & error

Management is responsible for the prevention and detection of fraud. They

should implement and operate adequate internal control system to safeguard the

assets.

2.3.2 Internal Auditor’s responsibility in preventing fraud and error.

Internal auditor is to REVIEW the measures that designed by management to

ensure adequate control is in place.

Internal auditor can help management manage risks in relation to fraud and

error by

1. commenting on the process used by management to identify fraud and error

risks.

2. commenting on the appropriateness and effectiveness of actions taken by

management to manage the risks identified

3. periodically auditing or reviewing systems or operations to determine

whether the risks of fraud and error are being effectively managed;

ABFA3114 Principles of Auditing Page 28

4. monitoring the incidence of fraud and error, investigating serious cases and

making recommendations for appropriate management responses

2.3.3 External Auditor’s responsibility in preventing and detecting fraud

and error.

1. External Auditor‟s responsibility is to ASSESS the risk that fraud or error

may cause the financial statements to contain material misstatement.

2. The objective of an audit is to report on the truth and fairness of the

financial information but not purposely to detect fraud and errors. However,

in the course of conducting audit if the auditor discovers the fraud and

material misstatements affecting the financial statements, auditor should

investigate further.

3. Auditor must perform the auditing with an attitude

of......................................... i.e. it requires that the auditor objectively

evaluate audit evidence. This means the auditor should constantly maintain a

critical and questioning mind in assessing the validity of audit evidence he

accumulates during the audit process.

4. An attitude of professional scepticism is necessary for the auditor to identify

circumstances that increase the risk of a material misstatement resulting from

fraud or error, and suspicious circumstances that indicate that the financial

statements are materially misstated. If the auditor suspected that there might

be a material misstatement due to fraud or error, the auditor would be more

sensitive to the selection and type of evidence examined.

2.3.4 Limitation of statutory audits

As per ISA 200, the inherent limitations of statutory audits are:

1. The use of sampling testing. Auditors could not able to conduct 100%

checking on all the transactions. Due to sampling selection, some items may

not be checked if not being selected in a sample. Due to this sampling test

basis, it may happen that misstatement may remain undetected.

ABFA3114 Principles of Auditing Page 29

2. The inherent limitations of internal control system. Auditor relies on the

internal controls if they are effective. But by nature, internal control of the

company has its inherent limitations such as human error. Therefore, the

auditor cannot give absolute assurance but only reasonable assurance.

3. The fact that most audit evidence is persuasive rather than conclusive.

The auditor‟s opinion is based on the evidence gathered which is not

conclusive to draw a conclusion.

4. Limitations of the reporting framework. The auditor report given is fixed

format which may not be understandable and readable by all the users.

5. Audit does not provide up-to-date position. The financial statements

provide past information. The auditor‟s opinion given on the past

information sometime is not relevant.

2.4 Understand the professional ethics.

2.4.1 Definition of ethics.

Ethics refers to code of conduct based on moral duties and obligations that

indicate how an individual should behave in society. For example, businessman

should be ethical not to produce harmful products for consumers.

2.4.2 Fundamental Principles of Ethics “C.O.B.I.C.”

The Fundamental PrinciplesError! Bookmark not defined.

Integrity (I) Members should behave with integrity in all

professional, business and personal financial

relationships. Integrity implies not merely honesty

but fair dealing and truthfulness.

Objectivity

(0)

Members should strive for objectivity in all

professional and business judgements, (objectivity is

the state of mind which has regard to all

considerations relevant to the task in hand but no

other, it presupposes intellectual honesty).

ABFA3114 Principles of Auditing Page 30

The Fundamental PrinciplesError! Bookmark not defined.

Professional

Competence

(C)

Members should not accept or perform work which

they are not competent to undertake unless they

obtain such advice and assistance as will enable them

competently to carry out the work.

Confidentiali

ty (C)

Members should carry out their professional work with

confidentiality. Information obtained in a business

relationship should not disclose outside the firm unless

there is a proper and specific authority or duty to

disclose.

Professional

Behaviour

(B)

Members should behave with courtesy and

consideration towards all with whom they come into

contact during the course of performing their work.

2.4.3 Ethical Threats

Threats

The potential threats that may lead to conflict of interest are:

Self- interest threat. It occurs when auditor could benefit from a

financial interest in an audit client. Examples of self interest threats are

- if the auditor has a ownership of shares in client company or any

joint venture with the audit client.

- having personal relationship with senior members of client

company.

- providing loan or guarantee to or from an audit client.

- highly depending on total fees from one audit client

Self- review threat. It occurs when the audit firm or member of audit

team put itself in a position of reviewing the subject that previously the

member is responsible. Examples are:

- Auditor offers accounting services and other non audit services and

auditor audit his own work.

- Custodian for and ownership of assets of audit client.

- Assist /supervise employees of audit client

ABFA3114 Principles of Auditing Page 31

- Performing valuation / internal audit service for financial

statement

- Recruiting senior management for audit client

- Advise / assist in securing source of finance.

Advocacy threat. It occurs when the audit firm or a member of the audit

team promotes or may be perceived to promote, an audit client‟s position

or opinion. Examples are:

- promoting client‟s shares or IPO

- acting on behalf of client in litigation case or in resolving disputes

with other 3rd

party.

Familiarity threat. It occurs when by virtual of a close relationship with

an audit client. Examples are

- having a close family member who as a director, officer or

employee of the audit client.

- Long outstanding business relationship with the client.

- Become close friend of the audit client

- Acceptance of an expensive gifts

- Auditor is ex-employee of audit client.

Intimidation threat. It occurs when a member of the audit team may be

deterred from acting objectivity and exercising professional judgement

due to pressure given by the audit client to terminate the service,

dominant personality in a senior position at the audit client. Examples

are:

- Disagreement with client, auditor is being threatened to be

removed from service.

- Threat to reduce fees due to pressure applied in order to reduce the

scope of an audit.

- Litigation situation in between auditor and client

2.4.4 Safeguards to Address Threats

Safeguards can be grouped under 3 categories.

Category 1- Safeguarded by …………………

Prohibition of providing non-auditing services by auditors. Auditor

should be prohibited to carry out services such as internal audit,

ABFA3114 Principles of Auditing Page 32

bookkeeping, management functions, designing control services or

legal advices.

Category 2- Safeguarded by …………………

This safeguard is by preparing its own code of ethics for the entire

audit firm or a specific client/assignment.

Category 3- Safeguarded by ………..

This safeguard is by the client itself. Safeguard could be:

appointment of auditor is by the audit committee; verifying the

qualification of auditor by the client, monitoring auditor‟s work by

audit committee.

2.4.5 Confidentiality of Information.

Information confidential to a client should not be disclosed, except where

consent has been obtained, or where there is a public duty or a legal or

professional right or duty to disclose. Accountant should only act for a client on

the understanding that the client will make full disclosure to them.

There are circumstances in which auditor is free to disclose information

regardless of the client‟s wishes and circumstances in which the auditor has an

obligation to do so.

Auditors have an obligation to disclose:

(1) where the courts order them to do so;

(2) where they suspect their client of offences of terrorism;

(3) they suspect the client to be a drug trafficker;

(4) where under banking, insurance and financial services, they consider the

client is either acting recklessly or is not fit or proper to manage such

business.

2.4.6 Basic principles of independence

a) It states that a member’s objectivity must be beyond question if they are

to report as auditor. The followings are the enforcement mechanisms to

maintain its integrity, objectivity and independence.

(Note: Independence means an attribute of the relationship between 2 parties. It

is said that 2 parties are independent if neither has any obligation to the other)

ABFA3114 Principles of Auditing Page 33

Guideline 1: Undue dependence on an audit client for dependence on

Income. Recurring fees paid by one client or group of connected clients should

............................... of the gross practice income- (10% for public companies).

Guideline 2: Family and other personal relationship. A family or other close

relationship may pose a threat to independence and safeguards should be in

place to preserve independence. Auditor should ensure personal relationship do

not affect their objectivity

Guideline 3: Beneficial interests in shares and other investment .An auditor

should ensure that it does not have as an audit client a company in which any

partner or anyone closely connected with a partner holds shares or has a

beneficial interest in shares.

Guideline 4: Loans. An auditor or anyone closely connected with it should not

make or accept loans to or guarantee from an audit client. This also applies to

a partner in a practice or spouse or minor child.

Guideline 5: Goods & services- hospitality. Goods and services should not be

accepted by an auditor or by anyone closely connected with it unless the value

of any benefit is modest.

Guideline 6: Provision of other services. There is no objection in practice to

the provision of other services to audit clients, but care must be taken not to

perform management functions or to make management decision.

Guideline 7: Overdue fees. The existence of significant overdue fees can be a

threat to objectivity.

Guideline 8: Litigation. Objectivity may be threatened (or appear to be) where

there is actual or threatened litigation between auditor and clients.

Guideline 9: Associated firm’s influence outside the practice. Pressure may

arise from outside the practice form associated practices or organisation.

ABFA3114 Principles of Auditing Page 34

Guideline 10: Auditor should not perform management functions or take

executive decision. Auditor‟s involvement is only advisory.

ABFA3114 Principles of Auditing Page 35

CHAPTER 3

AUDITOR’S REPORT

________________________________________________________________

Learning Outcomes

When you have completed this lesson you will be able to:

Understand the standard unqualified audit report

Understand the implication of unqualified audit report

Explain the departure from standard report and deciding appropriate

auditor‟s report.

Reference text: Auditing & Assurance Services in Malaysia- Chapter 18

ABFA3114 Principles of Auditing Page 36

3.1 The Auditor’s Report

3.1.1 What is an audit report?

Audit report is the principal channel of communication between the

auditor and the user of the financial statements.

Audit report is the review and evaluation report resulted from the test of

control and substantive procedures that auditor has performed. Before

issuing an audit report, auditor should assess the types of audit reports to

be issued.

The two main reporting requirements under the Companies Act are:

The auditor should state in his opinion whether the financial statements

give a true and fair view, and are in compliance with the Act and

applicable approved accounting standards.

Auditor's opinion on whether the accounting and other records and the

registers required by the Act have been properly kept in accordance with

Act.

3.1.2 Users of audit report. The followings are the users of an audit report:-

Potential investors- To evaluate the performance of company before

investing.

Shareholders of a company- To know the profitability of the company

they owned.

Employees of a company- To know the performance of company.

Bankers- To evaluate the credit worthiness of the borrower before

lending.

Suppliers- To evaluate the liquidity of the company before supplying

goods.

3.1.3 ISA 700 Forming an Opinion and Reporting on Financial Statements

indicates the basic elements that will ordinarily be included in the

audit report. The basic elements of an auditor‟s report include the

followings:-

ABFA3114 Principles of Auditing Page 37

No Audit report

element/feature

Reason for that element/feature

1 Title of „independent

auditor”

To identify this as an audit report and

distinguish it from other reports on financial

statements that might be issued by others,

directors, etc

2 Addressee To identify the person(s) who may use or rely

on the report.

3 Introductory paragraph It states that when an audit was conducted and

identifies which financial statements are

covered by the auditor‟s report.

Management‟s

responsibility for the

financial statements

To explain the responsibility of management

for the preparation of financial statements in

accordance with the applicable financial

reporting framework

Auditor‟s

responsibility

To state that the auditor‟s responsibility is to

express an opinion on the financial statements

based on the audit

To explain the scope of the audit so that the

standards of the auditor‟s work is clear and

other factors such as limitation of audit testing

is known

5 Auditor‟s Opinion

paragraph referring to

the financial reporting

framework followed

and expressing the

auditor‟s opinion.

To provide the auditor‟s opinion on the

financial statements in terms of true and fair

view, to assure the reader that the audit has

been carried out in accordance with

established principles and practices

Other reporting

responsibility

Auditor‟s signature This is normally the signature of the audit firm

as the firm assumes responsibility for the

audit, not the individual engagement partner.

Date of the report To inform the reader that the auditor has

considered effects of transactions that the

ABFA3114 Principles of Auditing Page 38

No Audit report

element/feature

Reason for that element/feature

auditor became aware of on the financial

statements up to that date.

Auditor‟s address This is normally the city where the auditor

responsible for the audit is located so he/she

can be contacted, if necessary.

3.1.4 Types of audit reports. (Exam focus)

Unmodified report. This report is a standard good report that does not

require any change/modification on certain issues. A standard unqualified

auditor's report contains the standard wording in terms of format and

contents in compliance with the requirements under the auditing standard

and the provisions of the Companies Act, 1965 and/or other statutory

requirements

Modified unqualified report. This report has an emphasis of matter

paragraph. A modified unqualified report contains an unqualified opinion

but the wording of the report is modified normally by the inclusion of an

additional explanatory paragraph that highlights or makes reference to a

matter such as going concern uncertainty.

“Except for” report. This report is a qualified audit report with

limitation of scope or disagreement but the effect of misstatement on

financial statement only material but not pervasive.

Adverse report. This report is a qualified audit report with disagreement

and the effect of misstatement on financial statement is material and

pervasive.

Disclaimer of opinion report. This report is a qualified report with

limitation of scope and the effect of misstatement on financial statement

is material and pervasive.

ABFA3114 Principles of Auditing Page 39

3.1.5 Meaning of terms

a. Unqualified report = ..........................

b. Qualified report = ........................

c. Emphasis of matter means auditor wishes to highlight certain issues to

the user‟s attention provided that the directors have disclosed all the

information.

d. Limitation of scope means auditor does not have full information when

conducting an audit. In other words, auditor faces some limitations to

access all the necessary information (evidence) to support his audit

opinion. For example, lack of accounting records that have been

destroyed or lack of explanation from directors.

e. Except for means “......................” a certain item. Except that particular

item, the rest of the items are true and fair.

f. Disagreement means auditor does not agree with the management about

matters such as accounting treatment or disclosure in the financial

statements such as provision of bad debt, depreciation etc.

g. Adverse opinion means that auditor .................... in the accounting /

disclosure matters because they affect all the areas of financial

statements. The financials as a whole do not give true and fair view.

h. Disclaimer of opinion means the auditor does not provide any opinion

on the financial statements because the financial statements are material

and pervasive misstatement.

i. Material. An item is said material means that omission of it will change

the audit opinion. It can say that the transaction has a significant impact

to the financial statements.

j. Pervasive. An item is said pervasive means that the item seriously affects

ALL the areas of the whole financial statements. The users view on the

financial statements will be affected.

3.1.6 Date of audit report

The date of auditor‟s report should be appropriate because it indicates to

the users the last day of auditor‟s responsibility in reviewing significant

post Statement of Financial Position events.

The date should not be dated before the date of director‟s reports.

ABFA3114 Principles of Auditing Page 40

3.1.7 Matters that an auditor should report in the auditor’s report on the

accounts presented at the annual general meeting of a company.

i. Whether or not the financial statements are true and fair.

ii. Whether or not the financial statements have been properly

prepared in accordance with the Companies Act 1965.

iii. Whether the financial statements are in accordance with the

applicable accounting standards.

iv. Whether the accounting and other records are properly kept in

accordance with the Companies Act, 1965.

v. Whether the auditor has not received sufficient information or

explanations necessary for his auditing.

3.1.8 Conditions that have to be met before a standard unqualified

auditor’s report can be issued.

i. Auditors has obtained without restriction all information and

explanation he required.

ii. Financial statements have been prepared in accordance with the

approved accounting standard and present a true and fair view.

iii. Adequate disclosure of all matters to present a true and fair view of

the financial statements.

iv. All reporting duties under Companies Act have been satisfied.

v. There are no circumstances requiring additional explanatory or

modification of wording of the annual report.

vi. the importance of auditors adopting a conventional and uniform

wording in auditor‟s report.

3.1.9 Use of standardised wording in audit report

The reason for using standardised wording in audit report is to avoid confusion

to the readers and prevent misunderstanding in the message being

communicated to the users of FS.

ABFA3114 Principles of Auditing Page 41

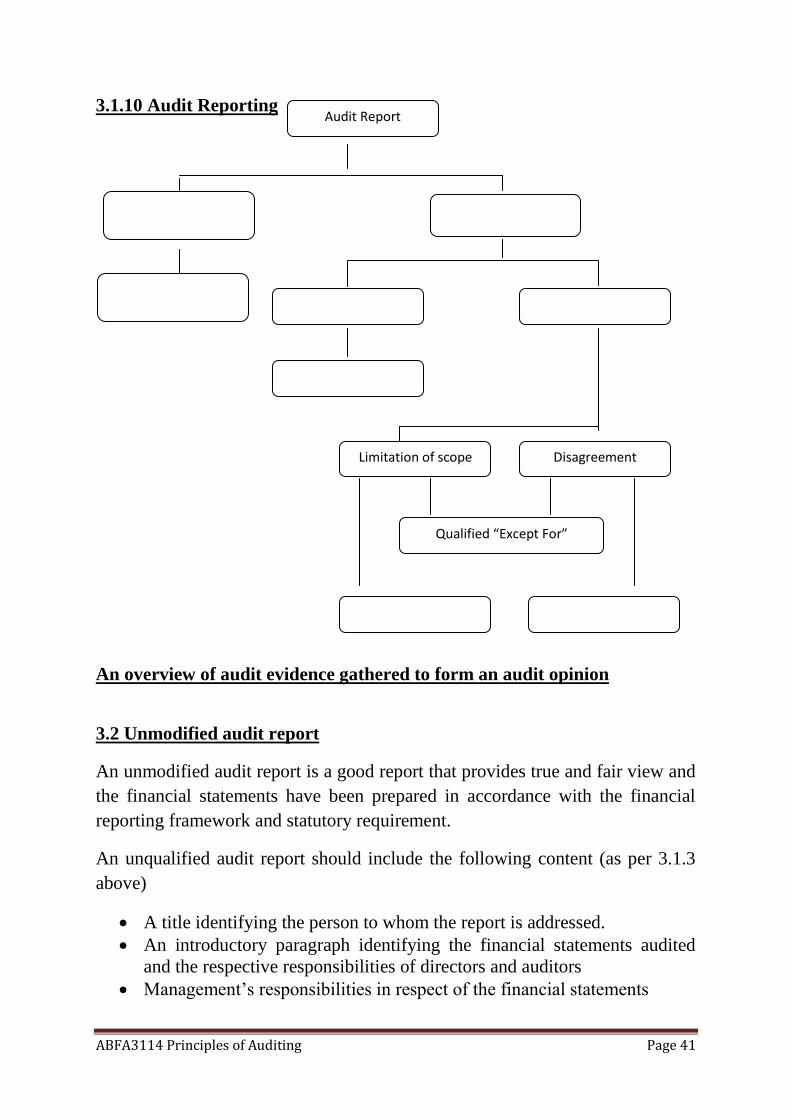

3.1.10 Audit Reporting

An overview of audit evidence gathered to form an audit opinion

3.2 Unmodified audit report

An unmodified audit report is a good report that provides true and fair view and

the financial statements have been prepared in accordance with the financial

reporting framework and statutory requirement.

An unqualified audit report should include the following content (as per 3.1.3

above)

A title identifying the person to whom the report is addressed.

An introductory paragraph identifying the financial statements audited

and the respective responsibilities of directors and auditors

Management‟s responsibilities in respect of the financial statements

Audit Report

Disagreement Limitation of scope

Qualified “Except For”

ABFA3114 Principles of Auditing Page 42

The auditors‟ responsibilities in forming their audit opinion

The scope paragraph detailing the nature of the audit

The auditors‟ opinion on the financial statements

The manuscript or printed signature of the auditors.

The date of the auditors‟ report

The auditors‟ address.

3.3 Modification To The Standard Auditor’s Report

3.3.1 Modified audit reports

Modified audit reports arise when auditors do not believe that they can state

without reservation that the accounts give a true and fair view. ISA 701

Modifications to the independent auditor’s report states that there are 2 types of

modified report

i. Matters that do not affect the auditor’s opinion: “Emphasis

of matter paragraph (just wish to highlight to the attention of

users)

ii. Matters that do affect the auditor’s opinion

Qualified

Disclaimer

Adverse opinion.

3.4 Modified Unqualified Auditors’ Report- Emphasis of Matter

3.4.1 Emphasis of matter paragraph

Emphasis of matter paragraph is used where the auditor wishes to draw

attention to an important item in the financial statements. The

conditions to use this report are the directors must fully disclose all the

information and the item is significant.

An emphasis of matter does not constitute a qualified opinion. It is

usually situated after the opinion paragraph and states that the opinion is

not qualified with regard to that matter.

It is used when there is a significant uncertainty or going concern issue

that has been fully disclosed in the notes to the financial statements and

the outcome of the issue is dependent on events yet to happen.

ABFA3114 Principles of Auditing Page 43

3.5 Departures From An Unqualified Auditors’ Report

3.5.1 Qualified audit opinion

Qualifications may be material and pervasive. The difference between them is

a matter of degree of effect and materiality. A pervasive qualification (very

serious) is one that affects the view given by the financial statements “AS A

WHOLE”. For example, if the auditors are not able to collect evidence from

whatever sources to form audit opinion, it is said to be pervasive.

Qualified audit opinions arise where there are either

i. disagreement on accounting matters such as accounting treatment

and disclosure. It is used where the auditor disagrees concerning the

accounting treatment, amount or disclosure of an item in the financial

statements.

OR

ii. limitations in the scope of the audit that unable the auditors to carry

out their duties. It is used where the audit cannot obtain sufficient

evidence regarding an item in the financial statements.

Common circumstances that may give rise to a disagreement with the

management of the company are:

Non compliance with Companies Act or other legislations.

No compliance with approved accounting standards.

Disagreement with the facts or amounts included in the Financial

Statements

Inadequate disclosure.

ABFA3114 Principles of Auditing Page 44

Qualification Matrix (Students should have a clear understanding on this

matrix).

Two levels of

qualified

opinion

Limitation of scope

(auditors could not access

full information in the

respect of the audit)

Disagreement

(auditors disagree with

management on accounting

policies selected, method of

application or disclosure

requirements)

Level 1

MATERIAL

ONLY NOT

pervasive

(less serious &

affect only a

particular

area)

QUALIFIED “EXCEPT

FOR”

(e.g. No inventory count

carried out)

QUALIFIED “EXCEPT FOR”

(e.g. Difference of opinion

between directors and auditor

as to whether to provide for a

doubtful debt.

Level 2

BOTH

MATERIAL

&

PERVASIVE

(Very serious

& affect the

whole

financial

statements)

DISCLAIMER OF

OPINION (e.g.

Destruction of accounting

records)

ADVERSE OPINION

(e.g. Auditors state that the

accounts do not give true and

fair view)

Summary

i. Limitation of scope (material) = Except For

ii. Limitation of scope (material & pervasive) = Disclaimer of opinion

iii. Disagreement (material) = Except For

iv. Disagreement (material & pervasive) = Adverse opinion

ABFA3114 Principles of Auditing Page 45

3.5.2 A disclaimer of opinion should be expressed when the possible effect of

a limitation of scope is so material and pervasive that the auditor could not able

to obtain appropriate and sufficient evidence to express opinion on the financial

statements. Example of disclaimer of opinion,

Example: “Due to the significant of the matters above, we (auditor) do not

express an opinion on the financial statements.”

3.5.3 An adverse opinion should be expressed when the effect of a

disagreement is so material and pervasive that the auditor concludes a

qualification of the report. Adverse and Disclaimer opinions do not support

credibility of the financial statements. Example,

“In our opinion, because of the effects of the matters above, the financial

statements do not give a true and fair view of the financial position”

3.5.4 Except for opinion is used when the disagreement or limitation of scope

is not so serious or not due to fundamental errors. “Except for” opinions are

generally less extreme because they are positively supporting other matters

other than those matters being highlighted. Example,

“In our opinion, except for the effect of adjustments, we had been able to

satisfy ourselves as to the physical inventory quantities….”

How to decide which modified opinion is appropriate in the exam? Follow these

rules

i. If accounting records have been destroyed or gone missing and affect

the WHOLE financial statements, then “Disclaimer of Opinion” is

appropriate.

ii. If only part of the accounting records have been destroyed or gone

missing such as only receivable records; the rest of the accounting

records are still complete, then “Except for” is appropriate.

iii. If the disagreement is fundamental and affects the WHOLE financial

statement, then “Adverse opinion” is appropriate.

iv. If only a small portion such as depreciation treatment, then use

“Except for”.

ABFA3114 Principles of Auditing Page 46

Auditors normally would not issue a qualified report unless it is absolutely

necessary to do so. In practice, issuing qualifying report is avoided by

discussion and negotiation with the directors. Management will usually make

whatever changes necessary in order to avoid a qualified report.

3.5.5 Other information disclosed in the annual report

a) Other information disclosed in the annual report includes:

i. Opening balance

ii. Prior year figures

iii. Other information issued with audited financial statements.

b) ISA510 Initial Audit Engagements- Opening Balances requires that an

auditor obtains sufficient appropriate evidence about whether the opening

balances contain misstatements that materially affect the current period‟s

financial statements by:

i. determining whether the prior period‟s opening balances have been

correctly brought forward to the current period, (or restated)

ii. determining whether the opening balances reflect the application of

appropriate accounting policies.

c) ISA710 Comparative Information requires that comparatives comply in all

material respects with the identified financial reporting framework. Two

categories of comparatives exist are:-

i. Corresponding figures.

ii. Comparative financial statements.

d) ISA720 The Auditor’s Responsibility in Relation to Other Information

Documents Containing Audited Financial Statements requires that “the auditor

should read the other information to identify material inconsistencies with the

audited financial statements”. This may include items such as employee reports,

five-year summaries and management commentaries on operations. Thus,

auditors should have full access to other information.

ABFA3114 Principles of Auditing Page 47

CHAPTER 4

ACCOUNTING AND INTERNAL CONTROL SYSTEM

________________________________________________________________

Learning Outcomes

When you have completed this lesson you will be able to:

Define the objective and types of internal control

Understand the limitations of internal control

Ascertain the internal control

Evaluating the internal controls

Understand the audit strategy and internal controls.

Reference Text: Audit & Assurance Services in Malaysia- Chapter 6

ABFA3114 Principles of Auditing Page 48

“Within an organisation, internal control provides a way to meet

management’s stewardship or agency responsibilities. Management also

needs a sound internal control system that generates reliable information

for decision-making purposes.”

4.1 Accounting Systems

4.1.1 Definition of Accounting System:

It is a series of tasks and records of an entity by which transactions are

processed as a mean of maintaining financial records. Such system identify,

assemble, analyse, calculate, classify, records, summarise and report

transactions and other events.

4.1.2 Management’s/Directors’ responsibility on accounting system

Management/directors of the organisation is/are supposed to:

Set up and maintain an adequate accounting and internal control system

in the company.

Deliver a copy of company audited annual report to Companies

Commission of Malaysia (CCM).

Prepare annual financial statements to show true and fair view of the

company.

Ensure company keeps proper accounting records as required by

Companies Act.

Safeguard the company‟s assets and to prevent fraud and errors in the

company.

4.1.3 Auditor’s responsibility on accounting system

Auditor‟s responsibility is to assess and review the effectiveness of accounting

system to ascertain its adequacy as a basis of preparation of financial

statements.

4.2 Internal Control

4.2.1 Definition of Internal control

It is a process designed and implemented by the management to provide

reasonable assurance about the achievement of the entity's objectives with

regard to reliability of financial reporting, effectiveness and efficiency of

operations and compliance with applicable laws and regulations.

It is also designed and implemented to address identified business risks that

threaten achievement of any of these objectives

ABFA3114 Principles of Auditing Page 49

4.2.2 Objectives of Internal Control System

Validity. To ensure business is carried out in an orderly, effective and

efficient manner.

Timeliness. To ensure all the transactions are recorded on a timely basis.

Compliance. To ensure compliance with laws and regulations.

Valuation. To ensure assets are properly safeguarded and valued.

Authorisation. To prevent and detect fraud and errors.

Completeness. To secure the completeness an accuracy of the records

and the timely preparation of reliable financial information.

Classification. To ensure all the transactions are classified into the proper

account.

Posting and summarisation. To ensure all transactions are properly

recorded in journals and posted to the General Ledger.

[Note to students: Not all the objectives of internal control mentioned above are

relevant to external audit on financial statements; for example, control over the

product design. Only those items that related to financial statements are likely to

be relevant to external audit such as internal control over compliance with the

laws and regulations because any violating the laws is subject to financial

losses.]

4.2.3 Reasons for understanding the accounting & internal control systems

In a financial statement audit, the auditor should understand the client‟s

accounting and internal control systems in order to:

i. assess their reliability for the presentation of financial statement and

design suitable audit procedures.

ii. identify the types of potential misstatements.

iii. determine the control risk level.

iv. determine the audit strategy and plan audit tests

4.2.4 To gain understanding on the internal control system, auditor will

perform the following:

i. Review the previous audit files for recurring engagement. Auditor can

obtain great deal of information about the client‟s internal controls

ABFA3114 Principles of Auditing Page 50

developed prior years. Because systems and controls usually don‟t change

frequently; this information can be updated and carried forward to current

year.

ii. Inquiry of the client’s personnel. Interview the key staff to obtain some

information.

iii. Read the relevant documentation of client such as policy, system

manuals, documents, reports and records. By examine the actual,

completed documents and records, auditor can obtain evidence that the

control policies and procedures have been run effectively.

iv. Visit the client’s office to have physical inspection on the existence of

assets. Auditor will gain the information on condition of the physical

assets and control system in safeguarding the physical assets.

v. Observe the client’s activities. Auditor can observe staff to carry out the

process of preparing the documents, records and accounting system. This

observation will enhance the understanding of auditor towards the control

that has been in place.

-The knowledge gained from the above procedures on internal control

system, auditor will use this knowledge to :

Identify the types of potential misstatements.

Determine control risk which in turn affects the detection risk.

Assist in the designing further audit procedures such as substantive

procedures.

- In deciding the nature (types) and extent (depth) of the understanding

of the internal control required to carry out audit engagement, auditor

should consider the following factors:

The materiality level.

Knowledge gained from the previous audit.

Auditor‟s knowledge on the client‟s industry.

The size of entity and the ownership.

The complexity of the client‟s operations and system.

ABFA3114 Principles of Auditing Page 51

4.2.5.1The relationship between control risk and the client’s internal

control system is that if the internal control system is weak, the control risk is

high. The effectiveness of internal control system will directly influence the

control risk.

4.2.6 The difference between management’s and auditor’s concern on

internal control system.

Management’s concern on internal control system is to ensure the

effectiveness of internal control system so that organisation is able to achieve

the corporate objectives. Management is concerned whether the internal

controls established and implemented are effective enough to provide them with

reasonable assurance that the company would able to achieve its objectives.

Auditor’s concern on internal control is towards the impact of internal control

to the financial reporting and safeguarding of assets. The main reason auditor is

interested in internal control is that reliance on internal control will reduce the

amount of substantive testing of transactions. If auditor is satisfied that the

internal control system is functioning effectively, there is a reduced risk of error

in the accounting records.

4.3 5 Components of an internal control system.

Components

of Internal

Control

1.Control

Environment

2.Control

Procedures

3.Risk

Assessment

5.Monitoring

4.Information &

Communication

ABFA3114 Principles of Auditing Page 52

4.3.1 Component 1- Control environment. It is concerned an overall attitude

of directors and management towards internal control system. . It is the

framework (background) within which controls operate.

Factors that affect the control environment are:-

Integrity and ethical values. An entity needs to establish ethical and

behavioural standards that are communicated to employees and are

reinforced by daily practice.

Commitment to Competences. Management must specify the

competence level for a particular job and translate it into the required

level of knowledge and skills.

Participation of the Board of Directors or Audit Committee. The

board of directors and its audit committee significantly influence the

control consciousness of the entity. They must take their fiduciary

responsibilities seriously and actively oversee the entity‟s accounting and

reporting policies and procedures.

Management’s Philosophy and Operating Style. Establishing,

maintaining and monitoring the entity‟s internal controls are

management‟s responsibility. Management‟s philosophy and operating

style may significantly affect the quality of internal control.

Organizational Structure. The organizational structure defines how