A WORLD OF OPPORTUNITY - pra-global.com oil prices and accommodative monetary policies are driving...

62

1 A WORLD OF OPPORTUNITY

Transcript of A WORLD OF OPPORTUNITY - pra-global.com oil prices and accommodative monetary policies are driving...

1

A WORLD OF OPPORTUNITY

Our Rapidly Changing World Last Year

2

Recession

Recovery

Expansion

At Risk

Our Rapidly Changing World Today

3

Recession

Recovery

Expansion

At Risk

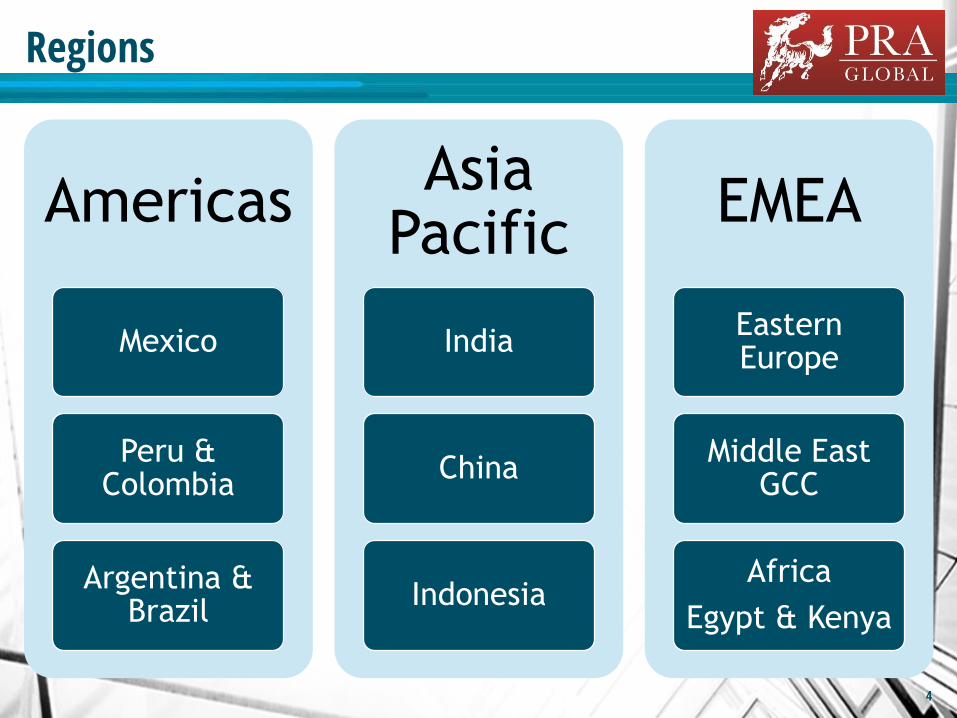

Regions

Americas

Mexico

Peru & Colombia

Argentina & Brazil

Asia Pacific

India

China

Indonesia

EMEA

Eastern Europe

Middle East GCC

Africa

Egypt & Kenya

4

Americas

Mexico; Peru & Colombia; Argentina & Brazil

5

Americas

• Mexico

• Peru

• Columbia

• Argentina

• Brazil

6

Mexico

7

Mexico

8

GDP

• $1.064 Trillion USD

Population

• 123.1 Million

GDP Growth

• 5 Year Projected Growth Average 2.7%

Growth Drivers

• Automotive, High-end Manufacturing, Telecommunications & E-Retail

• Skilled, competitive workforce.

• Free Trade Agreements with over

50 countries, including NAFTA.

• Average manufacturing labor

costs already 20% lower than

China; but varies by geographic

region and industry sector.

• Easy to setup and run a business

compared to many other Latin

American countries.

• Security an issue near border and

in other select areas.

• Difficult to find and keep mid-

level managers.

• Government reforms slow.

• Infrastructure improvements

critical to development.

• VAT Tax regime needs to be

managed properly.

• Heightened uncertainty in the

wake of the US election.

9

Business & Social Challenges

Mexico - Business Environment

Business Climate

Mexico - Business Opportunities

High-end Manufacturing

•High-end Manufacturing in the central region and near border.

•Aerospace, Plastics, Appliances, and Electronics.

•Textiles and more labor intensive products in the South.

Automotive

•18 OEM Automotive Facilities and 5 more under development.

•By 2020, 1 in 4 vehicles produced in North America will be assembled in Mexico.

•71% of total Mexican demand for manufacturing processes is met through imports

Telecommunications

•18% fixed line density with Telmex and Telcel with > 66% of market share.

•Telecom industry has grown by more than 400% between 2010 and 2016, AT&T to invest 3 Billion USD by 2018 on mobile internet service infrastructure.

E-Retail

•Amazon, Best Buy, Wal-Mart and Palacio de Hierro all investing in E-commerce.

•21.6% growth in 2016 on $14B USD, with an additional 14% to 18% year-on-year growth through 2020.

10

Mexico – Opportunities

11

Manufacturing

Automotive/Transportation

Telecommunications

E-Retail

12

South America

South America

• Peru

• Colombia

• Argentina

• Brazil

13

Peru, Colombia, Argentina & Brazil

Metric

GDP $

Population

GDP Growth (Next 5 Years)

Growth Drivers

Peru

$195.1 Billion

30.74 Million

3.7%

Telecom, Financial Services,

Ores/Minerals and Food Products

Colombia

$282.4 Billion

47.2 Million

3.6%

Telecom, Infrastructure,

Specialty Consumer Products, E-Retail

Argentina

$545.1 Billion

43.8 Million

3%

Infrastructure, Agriculture

Equipment, Lithium Mining

Brazil

$1.79 Trillion

205.8 Million

2%

Food & Specialty Consumer Products,

Aerospace, Automotive

14

15

Business Environment

Peru• 7th largest economy in LATAM with Solid growth

over the past 5+ years, slowed by devastating

floods and landslides in coastal areas.

• Government reconstruction program, strength in

mining and strong internal demand will drive

continued growth.

• Inflation low and steady, interest rates being

held in check and favorable trade policies.

Argentina• Inflation declining, but remains very high at 24%

in May against targets of 12 to 17%.

• Pro-market reforms and liberalization of capital

controls are driving slow improvement.

• Third largest economy in Latin America with

pent up consumer demand.

Colombia• Recent comprehensive tax reform with 3% hike

in VAT has slowed internal consumption in the

short term.

• Controversial FARC agreement implementation

has been slowly progressing.

• Strong government infrastructure spending,

higher oil prices and accommodative monetary

policies are driving growth.

Brazil• Weak R$ creates opportunity for acquisition

/capital investment.

• New and prior government weakened by

corruption scandals.

• Still the largest economy in Latin America with

disposable income.

• Challenging tax structure requires localization.

South America - Business Opportunities

Specialty Consumer Products - All

• Small ticket consumer goods.

• Small ticket personal care products.

Fresh and Packaged Food Products

• Specialty packaged foods – Brazil.

• Fish related products - Peru.

• Agriculture equipment – Argentina.

Mining

• Lithium mining triangle – Argentina, Chile, Bolivia.

• Minerals, metals and ores – Peru and Colombia.

• Heavy equipment for the mining industries.

Aerospace & Defense

• This is the bright spot for Brazil. The country is the third largest domestic aviation market in the world with Embraer’s presence.

• Aircraft parts and aerospace products. $3B imported into Brazil in 2016.

Telecommunication Infrastructure and Services

• Broadband subscriber penetration 7% in Peru and 4% in Colombia.

• New regional fiber based networks and telecom infrastructure projects

Infrastructure

•Road and building construction – Peru rebuild; Argentina new and refurb.

•Government driven infrastructure projects – Colombia.

16

17

South America - Opportunities

Specialty Consumer Products

Fresh & Packaged Food Products

Mining

Aerospace

Telecommunications

Infrastructure

Asia Pacific

India, China and Indonesia

18

Asia

19

• India

• China

• Indonesia

India

20

India

21

GDP

• $2.26 Trillion USD

Population

• 1.26 Billion

GDP Growth

• 5 Year Projected Growth Average 7.9%

Growth Drivers

• Manufacturing, Consumer-Ready Food Products, Infrastructure, Tourism

• Modi’s ‘Make It In India’ vision.

• Large, educated, young, English

speaking population.

• World’s largest democracy;

federal system with 29 states.

• Becoming more business friendly

with recent reforms; encouraging

foreign investment.

• Manufacturing labor costs are 4 to

5 times less than China.

• New GST tax reform is much

needed change; luxury goods

being hit with 28%+ GST.

• Companies are often inefficient

and would benefit from rigid

processes, training and

leadership.

• Class based society that must be

understood to succeed.

• Infrastructure improvements on

the rise.

• Government reforms slow.

• State owned institutions

dominate financial sector and

capital markets.

22

Business & Social Challenges

India - Business Environment

Business Climate

India - Business Opportunities

Manufacturing & Automotive

•Commercial, Passenger, two and three wheeled segments all growing 9% overall driven by two-wheelers (9.6%) and Cars (7%).

•Largest exporter of machinery and engineering products to Africa.

Engineering, IT & Financial Services

•Engineering Services Global Spend $750 Billion today; $1 Trillion by 2020.

• India IoT market value expected to be $9B with an installed base of 1.9B by 2020.

•Expected to be the fifth largest banking sector in the world by 2020.

Healthcare & Medical Products

•Leading exporter of medicines.

•Second largest number of diabetes sufferers (69 million) globally.

Retail

• Indian Retail market is expected to by $1 Trillion in 2020.

•Demand for high-end, branded luxury goods is growing rapidly.

•Pop-Up Shops a new trend to reach second and third tier cities.

Transportation/Infrastructure (Roadways, Ports, Airports, Rail)

•Goal of $376B USD in investment over the next 3 years with 70% of these funds for power, roads and urban infrastructure.

•Public / Private partnerships now open to foreign investment with FDI reforms.

23

India - Opportunities

24

Engineering, IT and Financial Services

Healthcare & Medical

Retail

Transportation/ Infrastructure

Automotive / Transportation

China

25

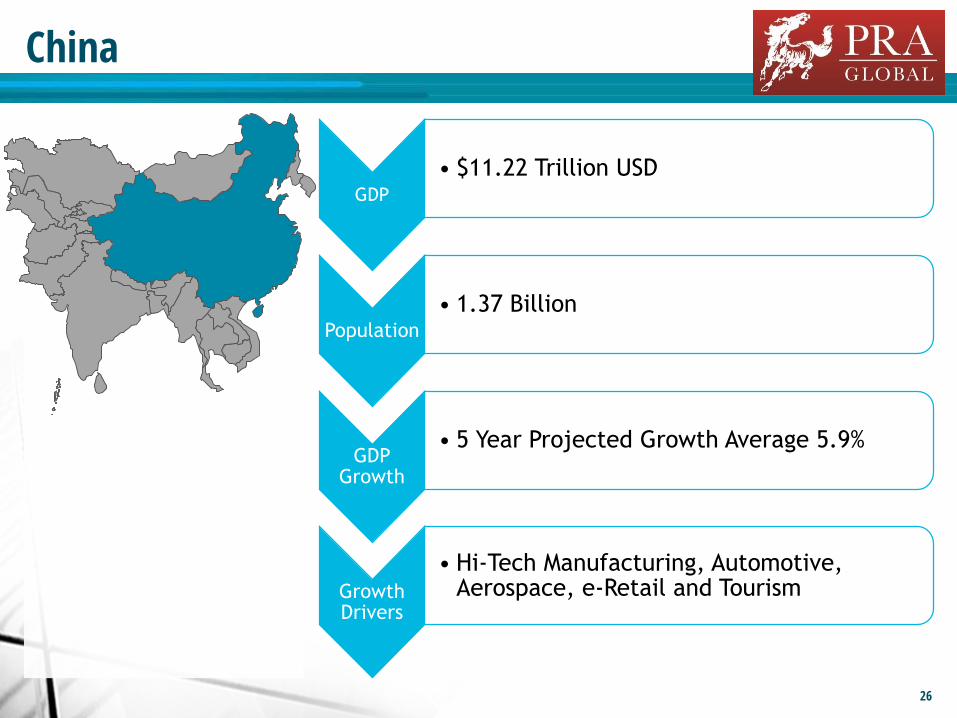

China

26

GDP

• $11.22 Trillion USD

Population

• 1.37 Billion

GDP Growth

• 5 Year Projected Growth Average 5.9%

Growth Drivers

• Hi-Tech Manufacturing, Automotive, Aerospace, e-Retail and Tourism

• Skilled, highly productive

workforce, increasing labor rates.

• Quality and competitive pressures

driving automation.

• Shifting from export driven to

consumption based economy.

• Consumers prefer high-quality

foreign brands.

• Foreign companies investing to

serve the Asia market not for

export.

• Difficult to find and keep

qualified employees.

• RMB is a managed currency.

• Intellectual property remains

hard to protect.

• Despite China’s economic shift

from socialism to managed

capitalism, there has been little

political reform.

• Labor Costs are now

comparatively higher than other

regions.

27

Business & Social Challenges

China - Business Environment

Business Climate

China - Business Opportunities

Hi-Tech Manufacturing & Aerospace

•Advanced manufacturing equipment including robotics and automation.

•Aerospace OEM Comac competing globally driving supply chain opportunities and Chinese companies buying US small aerospace such as Mooney and Cirrus.

•Food Processing of ready-to-eat foods, organic foods, and specialty beverages.

Automotive

•By 2020, forecasted sales of 30 million vehicles.

•Need for advanced automotive technologies: electric steering, electric braking, driverless car technologies.

E-Retail

•Number one e-commerce market in the world, with China expected to be 50% of global online sales by 2019, equaling $1.7 trillion.

•Second and third tier cities represent largest opportunities.

•Branded consumer goods & specialty foods and beverages are leading segments.

Tourism

•Chinese investing heavily with $180B in new projects and 11% or GDP growth and national employment.

•68 Million tourists visited China last year, a 3.8% increase over 2015.

•Total Inbound tourism income was $57 billion last year.

28

29

Hi-Tech Manufacturing

Automotive

e-Retail

Tourism

China - Business Opportunities

Indonesia

30

Indonesia

31

GDP

• $932.45 Billion USD

Population

• 258.3 Million across 17,000 islands

GDP Growth

• 5 Year Projected Growth Average 5.5%

Growth Drivers

• Manufacturing, Consumer-Ready Food Products, Infrastructure, Tourism

• Southeast Asia’s largest economy.

• Largest Muslim Democracy.

• Has potential to become a major

Asian manufacturing hub.

• Large, young workforce and rich

natural resources attract

investment.

• Government trying to increase

exports and drive growth.

• Industrial sector contributes 13%

to GDP.

• President Widodo struggling to

implement reforms to combat

corruption and improve

infrastructure.

• Barriers to market entry and

bureaucracy slowly being

reduced.

• Road and airport infrastructure is

severely lacking.

• Serious shortage of engineers.

• Aggressive stance against

terrorism has kept security issues

in check.

32

Business & Social Challenges

Indonesia - Business Environment

Business Climate

Indonesia - Business Opportunities

Manufacturing / Industrial

•Automotive vehicles and parts.

•Electronics, Footwear, Textiles, Paper Products and Furniture.

•Mining which is part of the Industrial sector includes Coal, Ore and Gold.

Consumer Ready Food Products

• Imported read-to-eat food products are in high demand with young consumers.

•Trend is for healthier foods; dairy and fresh fruit products leading categories.

•Eating snacks is part of the daily culture.

Infrastructure

•By 2034 Indonesia is expected to be the 6th largest market for air travel with 270 million domestic and international travelers.

•ASEAN Open Skies Agreement will further increase demand.

• Increased expenditure in investment as country develops further.

Tourism

•Over 10 million international tourists in 2016, with forecasted annual growth rate of 5.3% per year through 2025.

•Key government objective is to grow this sector, resulting in new attractions and resort locations beyond Bali.

33

34

Manufacturing

Mining

Consumer Ready Food Products

Infrastructure

Tourism

Indonesia - Business Opportunities

EMEA

Europe, Middle East, Africa

35

EMEA

• Poland

• Czech Republic

• Slovakia

• UAE

• KSA

• Egypt

• Kenya

• South Africa

36

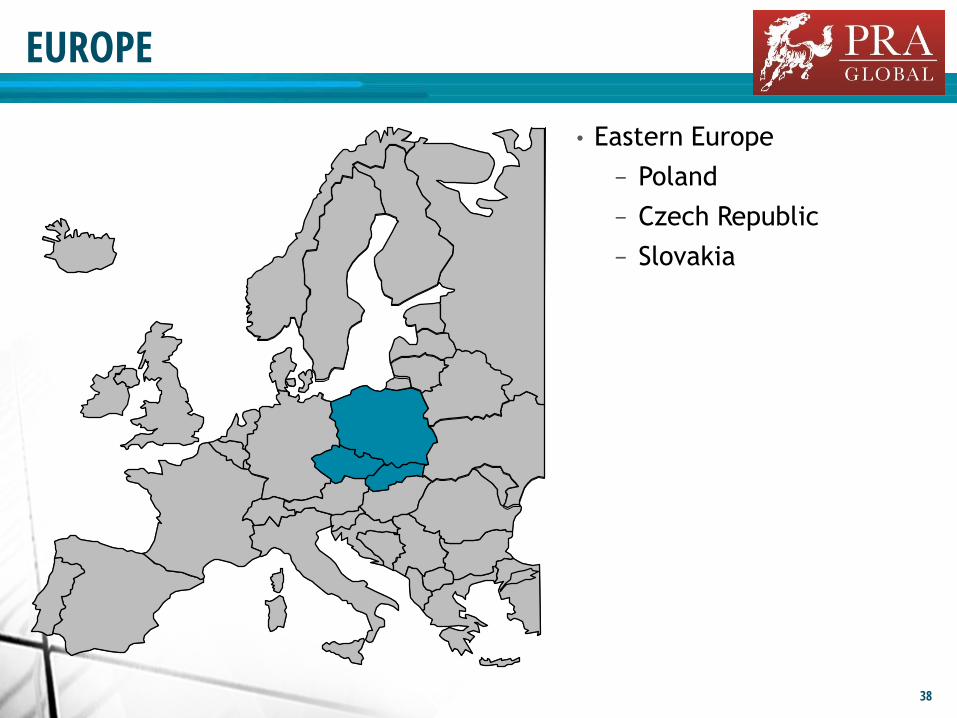

Europe

37

• Eastern Europe

− Poland

− Czech Republic

− Slovakia

EUROPE

38

Eastern Europe

Metric

GDP $

Population

GDP Growth (Next 5 Years)

Growth Drivers

Poland

$467.6 Billion

38.5 Million

2.9%

Manufacturing, Automotive,

Construction, IT & Infrastructure

Czech Republic

$192.9 Billion

10.6 Million

2.3%

Machine-building, Steel Metalworking,

Automotive

Slovakia

$89.5 Billion

5.4 Million

3.5%

Automotive, Engineering,

Electronics, Chemical Engineering, IT.

39

• Manufacturing is moving steadily

into the Eastern European

countries.

• Rising wages, steady

employment, reduced energy

costs driving consumption.

• Silk Road linking Europe to China.

• Poland taking a lead position as it

becomes Europe’s low-cost

manufacturing hub.

• Czech and Slovakia also have low

labor rates, strategic locations,

strong internal demand and

abundance of land.

• UK’s vote to leave the EU creates

uncertainty that will further drive

manufacturing and processing

into Eastern Europe.

• Skilled, educated, aging work

force, but populations growing in

the region, particularly Poland.

• Productivity improvements

needed in the region to remain

competitive against Germany.

• Engineering and Automotive are

strong drivers, but other

manufacturing operations like

Electronics, entering the market.

40

Business & Social Challenges

Eastern Europe - Business Environment

Business Climate

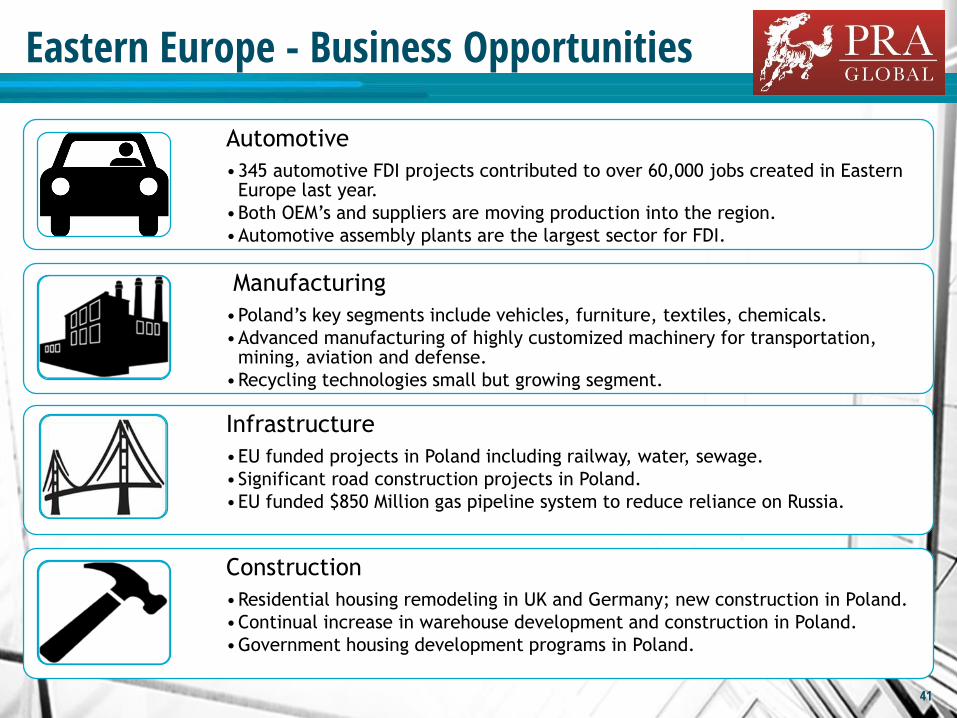

Eastern Europe - Business Opportunities

Automotive

•345 automotive FDI projects contributed to over 60,000 jobs created in Eastern Europe last year.

•Both OEM’s and suppliers are moving production into the region.

•Automotive assembly plants are the largest sector for FDI.

Manufacturing

•Poland’s key segments include vehicles, furniture, textiles, chemicals.

•Advanced manufacturing of highly customized machinery for transportation, mining, aviation and defense.

•Recycling technologies small but growing segment.

Infrastructure

•EU funded projects in Poland including railway, water, sewage.

•Significant road construction projects in Poland.

•EU funded $850 Million gas pipeline system to reduce reliance on Russia.

Construction

•Residential housing remodeling in UK and Germany; new construction in Poland.

•Continual increase in warehouse development and construction in Poland.

•Government housing development programs in Poland.

41

42

Eastern Europe - Opportunities

Automotive

Manufacturing

Infrastructure

Construction

Middle East

43

Gulf Cooperation Council (GCC)

• United Arab Emirates (UAE)

• Kingdom of Saudi Arabia

44

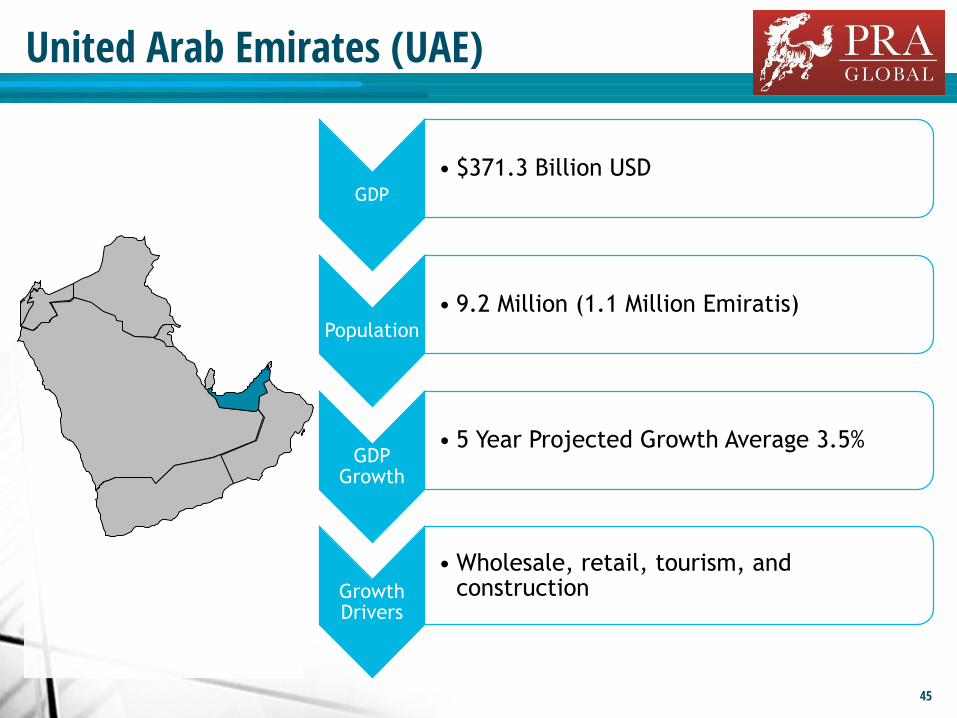

United Arab Emirates (UAE)

45

GDP

• $371.3 Billion USD

Population

• 9.2 Million (1.1 Million Emiratis)

GDP Growth

• 5 Year Projected Growth Average 3.5%

Growth Drivers

• Wholesale, retail, tourism, and construction

• Open economy with significant

disposable income.

• Oil dependence reduced to 21% of

GDP.

• Free trade zones offering 100%

foreign ownership and zero taxes.

• Largely expatriate workforce,

with high standard of living.

• Government five year plan to

continue diversification into

manufacturing and improve

education and opportunity for

nationals.

• Abu Dhabi Bank bailout of Dubai

in 2009.

• Highly susceptible to oil and real

estate prices.

• Low skilled workers often from

Philippines, India and Pakistan.

• Product certifications required

for importing into the Middle East

are challenging; often best

accomplished in UAE.

• Airport development underway to

support growth in aviation,

servicing and tourism sectors.

46

Business & Social Challenges

UAE - Business Environment

Business Climate

Kingdom of Saudi Arabia (KSA)

47

GDP

• $639.6 Billion USD

Population

• 28.1 Million

GDP Growth

• 5 Year Projected Growth Average 1.4%

Growth Drivers

• Oil and manufacturing

• Closed economy, managed by

Royal Family, supported by

significant Oil income.

• Major change in leadership when

King Salman unexpectedly

succeeded his half-brother in

2015.

• Oil is 87% of Government income.

• Government focus on Economic

Development diluted by war

being waged in Yemen.

• Nevertheless, Government

instituted an Economic Reform

Plan, Saudi Vision 2030, in 2016.

• Economic Freedom and

transparency still lags behind

other Emerging Economies.

• Saudi Vision 2030 aims to

significantly reduce dependence

on Oil and grow manufacturing.

• Foreign Companies can now own

Stock in Saudi Companies.

• Saudi ARAMCO (State Oil) is

selling off 5% of company to

generate funds to pay local

benefits programs.

• Foreigners have few rights and

Judiciary is not transparent.48

Business & Social Challenges

KSA - Business Environment

Business Climate

GCC - Business Opportunities

Tourism

•Fastest Growing sector in UAE with 40 million tourists expected annually by 2024.

•Expo 2020 in Dubai driving public/private investment in infrastructure and hotels.

•Dubai International preparing for 20 million visitors to Expo 2020.

Infrastructure

•Massive expansion in UAE Al Maktoum airport to become the world’s largest.

•Estimated $37 Billion in new infrastructure contracts made in 2016-2017.

• Increased spending on metro transportation including first ever Hyper-Loop.

Construction

•Top growth sector in value for UAE with 1.7 million workers.

•Hotels, Tourist Attractions, Shopping Malls and Airports and $3B on Expo 2020.

•High-end furniture, fitments and specialty materials needed for this expansion.

Financial, Trade & Real Estate Services

•Business sector follows the Construction sector in GDP contribution.

•Banking, Finance and Trade are top 3, followed by Real Estate and Leasing.

•KSA building major manufacturing facilities in effort to catch up with world.

49

GCC - Opportunities

50

Tourism

Aviation

Construction

Manufacturing

Financial & Trade Services

Africa

51

Africa – Egypt and Kenya

52

• Egypt

• Kenya

• South Africa (monitor)

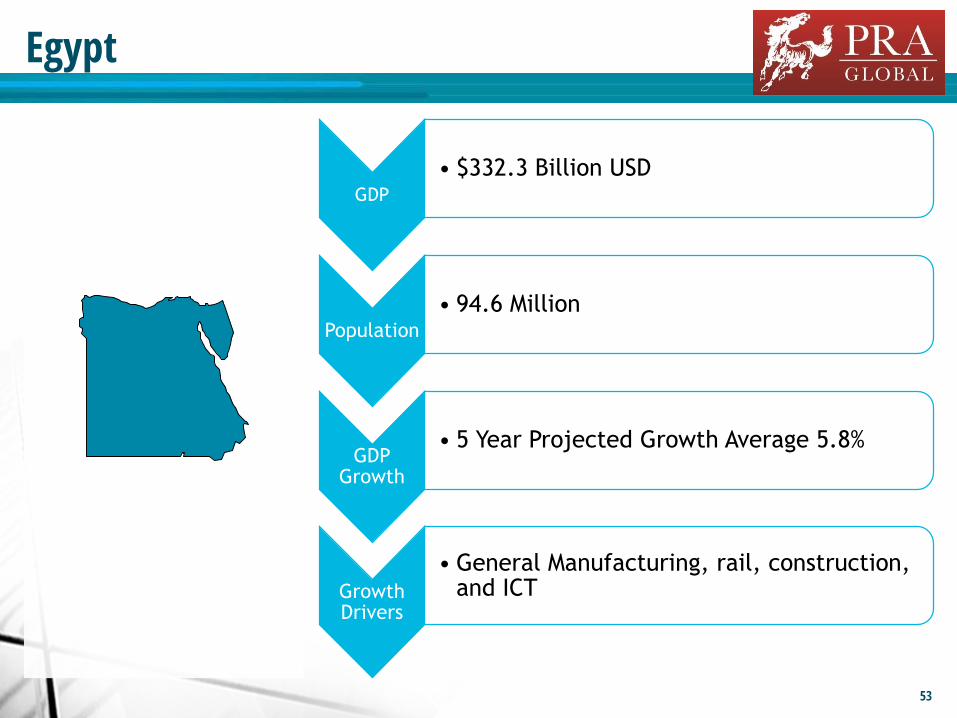

Egypt

53

GDP

• $332.3 Billion USD

Population

• 94.6 Million

GDP Growth

• 5 Year Projected Growth Average 5.8%

Growth Drivers

• General Manufacturing, rail, construction, and ICT

• Slow economic progress since the

Army took control following the

revolution in 2011.

• In 2014 President el-Sisi directed

changes to the economy to

include the removal of fuel

subsidies, the revaluation of the

Egyptian Pound, and start of VAT.

• To offset the creation of problems

for the poor, Social Safety Nets

were put in place.

• These actions, aided by

Government borrowing, has

stimulated business activity which

is now taking hold.

• The Government has established

the Suez Canal Economic Zone

project to stimulate new

manufacturing.

• Training Programs have been put

in place to further develop a

trained workforce.

• GE have embarked on a $575M

Rail Infrastructure program to

develop a rail network.

• President el-Sisi due to sign new

laws making business easier and

more secure.

• Industrial Manufacturing, is on

the increase.54

Business & Social Challenges

Egypt - Business Environment

Business Climate

Egypt - Business Opportunities

Infrastructure

• 5,000 kilometers of new roads, to support Manufacturing and Logistics

• Continued expansion of airport facilities and infrastructure.

• 1200 kilometers of New Railway structure with supporting stations and trains.

• IT/Telecom infrastructure that is supporting the ICT sector growth.

Manufacturing

•Government establishment of Suez Canal Industrial Zone with 4 new Ports.

•Focus on Building materials, Plastics and Automotive Components.

•Government have targeted Year on Year growth of 9% for manufacturing.

•Expectation is for an additional 3 Million jobs by 2020.

Technology

•Recognition by the Egyptian Government of the importance of ICT.

•The establishment of an Technology Valley near Cairo

•The access to 8 Submarine Cables that can deliver up to 60 TB ps

• Industry Sector delivered $10.2B in economic activity in 2016.

55

Egypt - Opportunities

56

Infrastructure

Agriculture

Manufacturing

Technology

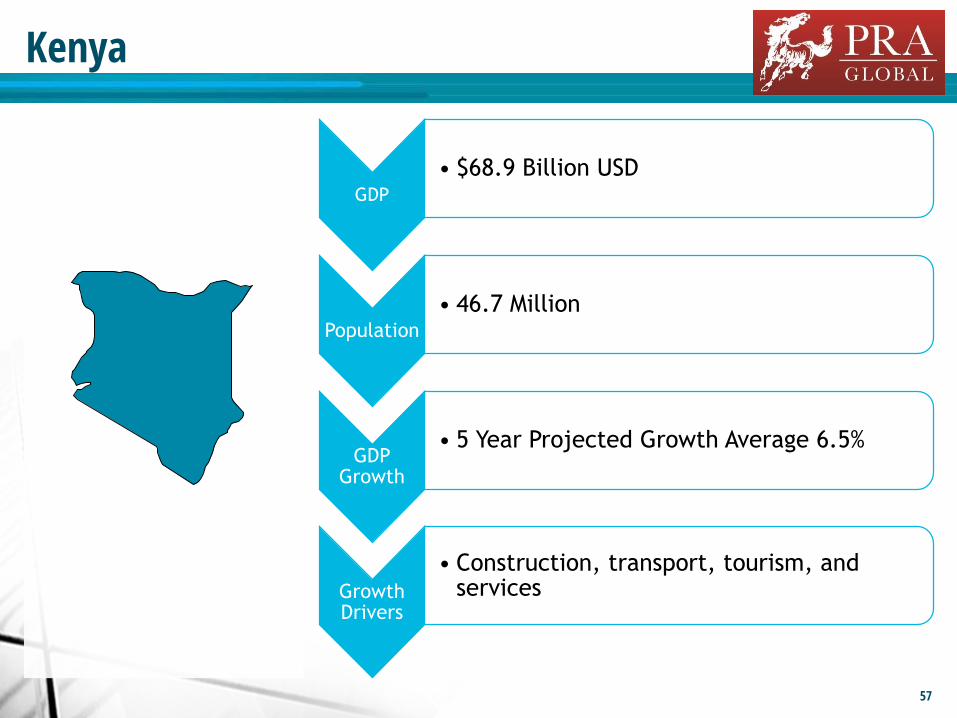

Kenya

57

GDP

• $68.9 Billion USD

Population

• 46.7 Million

GDP Growth

• 5 Year Projected Growth Average 6.5%

Growth Drivers

• Construction, transport, tourism, and services

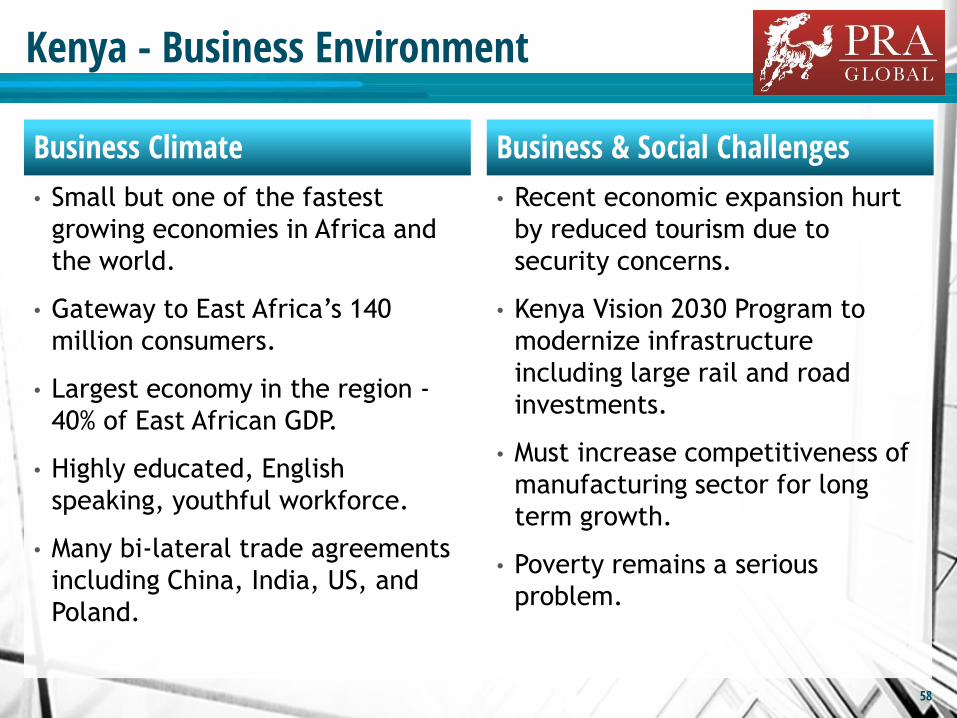

• Small but one of the fastest

growing economies in Africa and

the world.

• Gateway to East Africa’s 140

million consumers.

• Largest economy in the region -

40% of East African GDP.

• Highly educated, English

speaking, youthful workforce.

• Many bi-lateral trade agreements

including China, India, US, and

Poland.

• Recent economic expansion hurt

by reduced tourism due to

security concerns.

• Kenya Vision 2030 Program to

modernize infrastructure

including large rail and road

investments.

• Must increase competitiveness of

manufacturing sector for long

term growth.

• Poverty remains a serious

problem.

58

Business & Social Challenges

Kenya - Business Environment

Business Climate

Kenya - Business Opportunities

Infrastructure

•10,000 kilometers of new roads, an airport expansion and 700 km of new rail.

•Power grid modernization.

• IT/Telecom infrastructure that is supporting the Tech sector growth.

Agriculture

•Tea, horticulture and coffee are the largest crops & most valuable exports.

• In need of agro-processing technology & infrastructure development.

•AG Accounts for 30% of GDP, employs 80% of the workforce.

•Only 17% total land area had adequate rainfall and fertility to be farmed.

Manufacturing

•13% of workers tied to Manufacturing & Distribution Supply Chain.

• Iron, Steel and cement production are core growth sectors.

•Petroleum processing hurt by drop in oil prices.

Technology

•Google, IBM, Facebook, Oracle, Microsoft, SAP, and IBM all have regional headquarters in Nairobi.

•Tech start-up boom producing impressive results with seed capital funds and the construction of Konza Techno City – 5000 acres with more innovation hubs.

59

Kenya - Opportunities

60

Infrastructure

Agriculture

Manufacturing

Technology

In Summary: A World of Opportunity

61

Recession

Recovery

Expansion

At Risk

THANK YOU

62Grand Rapids, Michigan, USA | 1.616.942.5666 | www.PRA-Global.com |

Valerie Kozikowski

Managing Director

PRA GlobalGrand Rapids, Michigan World Headquarters

+1 616-942-5666 (office)

+1 248-705-0014 (mobile)