A new dimension in ETF investing - cdn.ymaws.com... As of 6/30/16. FOR INSTITUTIONAL ... Dimensional...

23

A new dimension in ETF investing Robin Thompson Regional Director Dimensional Fund Advisors Justin Clarke Business Consultant John Hancock Investments THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Transcript of A new dimension in ETF investing - cdn.ymaws.com... As of 6/30/16. FOR INSTITUTIONAL ... Dimensional...

A new dimension in ETF investing

Robin Thompson Regional Director Dimensional Fund Advisors

Justin ClarkeBusiness ConsultantJohn Hancock Investments

THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Agenda

Why strategic beta?

Why Dimensional Fund Advisors?

Why John Hancock Multifactor ETFs?

2 FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Why strategic beta?

3

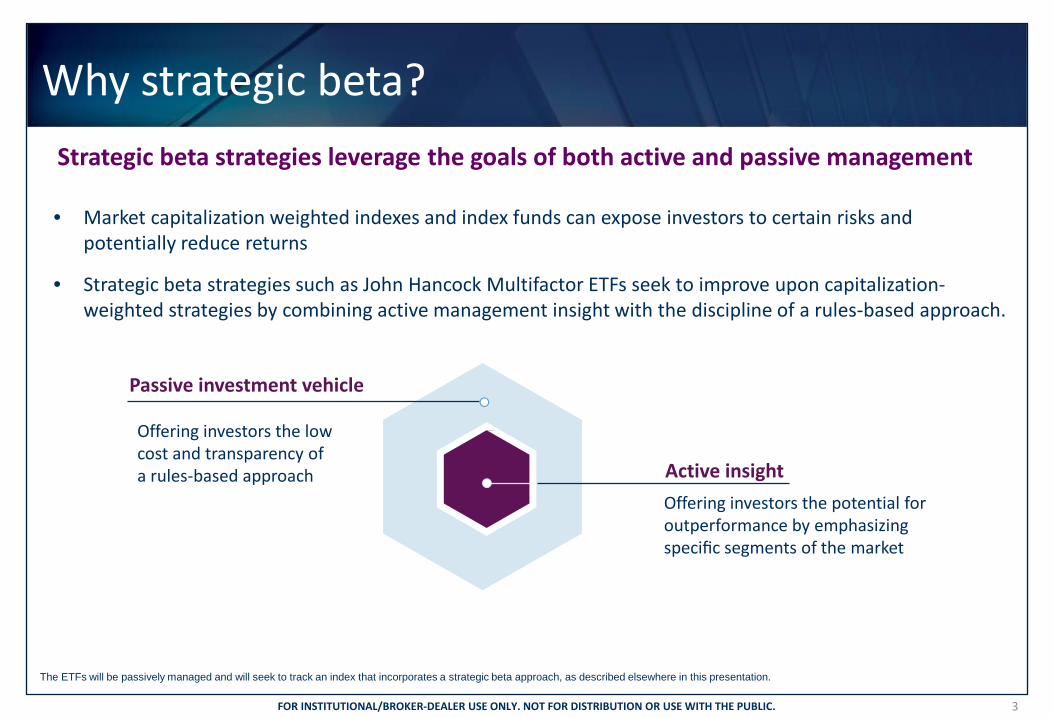

• Market capitalization weighted indexes and index funds can expose investors to certain risks andpotentially reduce returns

• Strategic beta strategies such as John Hancock Multifactor ETFs seek to improve upon capitalization-weighted strategies by combining active management insight with the discipline of a rules-based approach.

Offering investors the low cost and transparency of a rules-based approach

Passive investment vehicle

Active insightOffering investors the potential for outperformance by emphasizing specific segments of the market

Strategic beta strategies leverage the goals of both active and passive management

The ETFs will be passively managed and will seek to track an index that incorporates a strategic beta approach, as described elsewhere in this presentation.

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Why Dimensional Fund Advisors?

4

An idea rooted in academia

• Dimensional Fund Advisors is a pioneer of multifactor investing• It has applied ideas rooted in academia for more than three decades and today it is one of the most well-respected

managers in the field• Strategic beta concepts combine multiple factors that may better equip a portfolio to improve the likelihood of

outperformance versus broad market indexes across different types of markets

A proven approach

• Dimensional’s systematic approach is backed by insight gained from decades of academic research and experienceimplementing rules-based strategies in competitive markets

• Founded in 1981, Dimensional Fund Advisors has built a $415 billion global asset management business based onthe implementation of this research across asset classes

Thoroughly vetted by John Hancock Investments

• John Hancock Investments’ relationship with Dimensional and due diligence of their management teams began in 2006,resulting in Dimensional-managed strategies being offered as both individual funds and through our assetallocation portfolios

As of 6/30/16.

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

At the forefront of multifactor investing

1973 1981 1992 2006 2012 2015

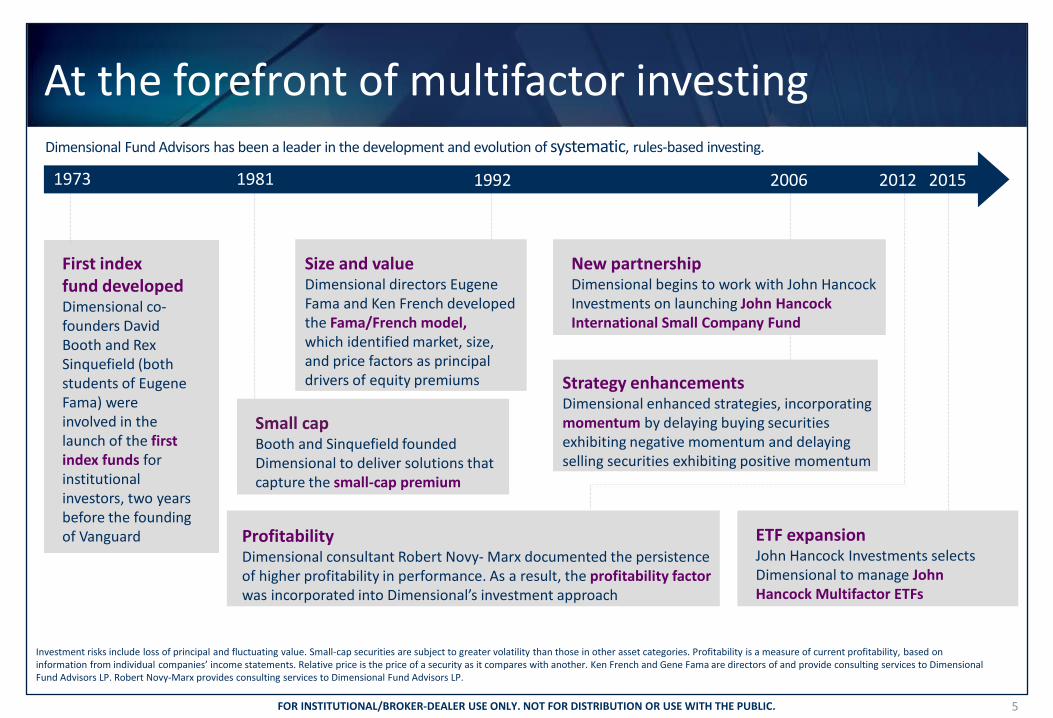

First index fund developed Dimensional co-founders David Booth and Rex Sinquefield (both students of Eugene Fama) were involved in the launch of the first index funds for institutional investors, two years before the founding of Vanguard

Size and value Dimensional directors Eugene Fama and Ken French developed the Fama/French model, which identified market, size, and price factors as principal drivers of equity premiums

New partnership Dimensional begins to work with John Hancock Investments on launching John Hancock International Small Company Fund

Strategy enhancements Dimensional enhanced strategies, incorporating momentum by delaying buying securities exhibiting negative momentum and delaying selling securities exhibiting positive momentum

Small cap Booth and Sinquefield founded Dimensional to deliver solutions that capture the small-cap premium

Profitability Dimensional consultant Robert Novy- Marx documented the persistence of higher profitability in performance. As a result, the profitability factor was incorporated into Dimensional’s investment approach

ETF expansion John Hancock Investments selects Dimensional to manage John Hancock Multifactor ETFs

Investment risks include loss of principal and fluctuating value. Small-cap securities are subject to greater volatility than those in other asset categories. Profitability is a measure of current profitability, based on information from individual companies’ income statements. Relative price is the price of a security as it compares with another. Ken French and Gene Fama are directors of and provide consulting services to Dimensional Fund Advisors LP. Robert Novy-Marx provides consulting services to Dimensional Fund Advisors LP.

Dimensional Fund Advisors has been a leader in the development and evolution of systematic, rules-based investing.

5 FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

A proven approach implemented across asset classes

6

Dimensional Fund Advisors, global assets under management as of June 30, 2016 ($415B)

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., and Dimensional Japan Ltd. All assets are in billions and U.S. dollars. Numbers may not total 100% due to rounding.

United States $141.7

All-Cap Core $44.3

All-Cap Value $5.4

Growth $1.3

Large Cap $13.1

Large-Cap Value $22.0

SMID-Cap Value $13.7

Small Cap $19.0

Small-Cap Value $16.4

Micro Cap $6.5

Global Equity $25.1

All Cap / Large Cap $16.7

Value $6.3

Small / SMID Cap $2.2

Fixed Income $88.6

U.S. $47.5

U.S. Tax Exempt $5.0

Non-U.S. and Global $31.8

Inflation-Protected $4.4 Developed ex.-U.S. $77.0

All-Cap Core $21.9

All-Cap Value $3.2

Growth $0.3

Large Cap $6.5

Large-Cap Value $15.6

Small Cap $15.5

Small-Cap Value $14.0

Other $23.6

Real Estate $14.4

Commodities $1.6

Global Balanced $7.3

Target Date $0.2

Emerging Markets $58.5

All-Cap Core $21.4

Value $26.2

Large Cap $5.6

Small Cap $5.4

34.2%

18.6%

14.1%

21.4%

6.1%

1.8%

3.9%

U.S. Equity

Developed ex.-U.S. equity

Emerging-market equity

Fixed income

Global equity

Global balanced

REITs and commodities

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Backed by leading academics in finance

7

The “Dimensional U.S. mutual funds” refers to The DFA Investment Trust Company, DFA Investment Dimensions Group Inc., and Dimensional Investment Group Inc. Ken French and Gene Fama are directors of and provide consulting services to Dimensional Fund Advisors LP. Academics noted provide consulting services to Dimensional Fund Advisors LP.

Academics on Dimensional Fund Advisors LP’s Board of Directors

Eugene Fama, Ph.D., Nobel Laureate University of Chicago

Kenneth French, Ph.D. Dartmouth College

Academics on Dimensional’s U.S. Mutual Funds Board of Directors

George Constantinides, Ph.D. University of Chicago

John Gould, Ph.D. University of Chicago

Edward Lazear, Ph.D. Stanford University

Roger Ibbotson, Ph.D. Yale University

Myron Scholes, Ph.D., Nobel Laureate

Stanford University

Abbie Smith, Ph.D. University of Chicago

Academics Providing Ongoing Consulting Services to Dimensional

Robert Merton, Ph.D., Nobel Laureate

Massachusetts Institute of Technology

Robert Novy-Marx, Ph.D. University of Rochester

Sunil Wahal, Ph.D. Arizona State University

Leaders of Dimensional’s Internal Research Staff

Eduardo Repetto, Ph.D., Director, Co-Chief Executive Officer and Co-Chief Investment Officer

Gerard O’Reilly, Ph.D., Co-Chief Investment Officer and Head of Research

Stanley Black, Ph.D., Vice President

Wes Crill, Ph.D., Vice President

James Davis, Ph.D., Vice President

Massi De Santis, Ph.D., Vice President

Marlena Lee, Ph.D., Vice President

Savina Rizova, Ph.D., Vice President

Dave Twardowski, Ph.D., Vice President

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

8

Strategy overview

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Philosophy backing the index design

Market Equity premium—stocks over bonds

Company size Small-cap premium—small company stocks over large company stocks

Relative price1

Value premium—value stocks over growth stocks

Profitability2 Profitability premium—stocks of highly profitable companies over stocks of less profitable companies

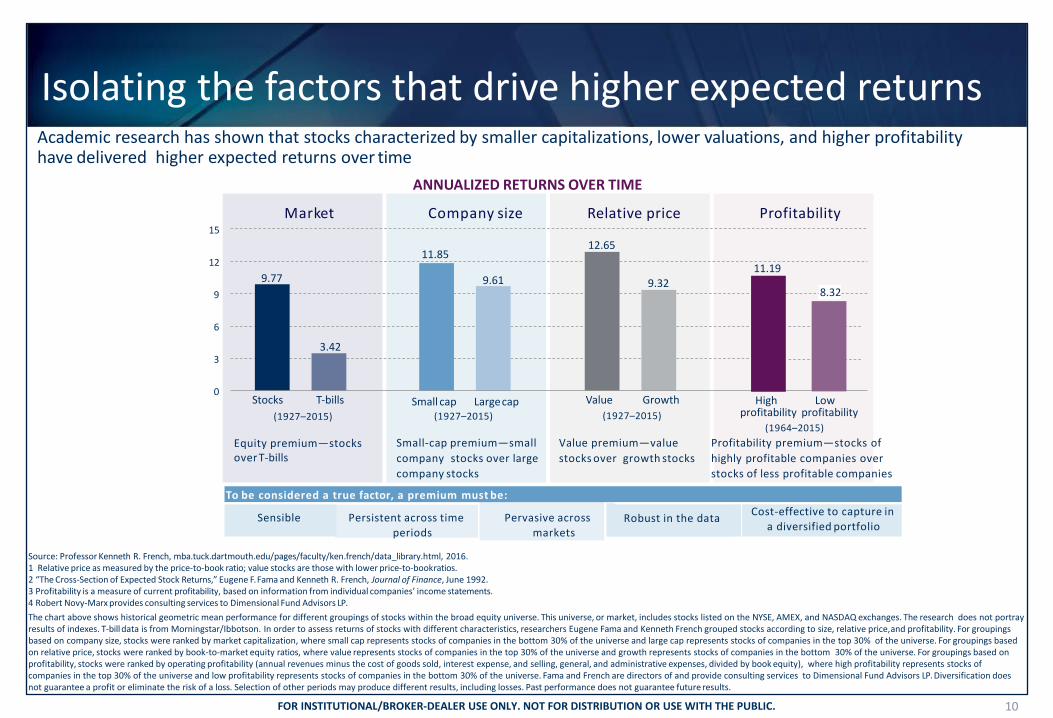

Sensible Persistent across time periods Pervasive across markets Robust in the data Cost-effective, to capture in a portfolio

To be considered a true factor, a premium must be:

Four factors driving expected returns

The indexes have been designed to capture the factors Dimensional Fund Advisors believes drive higher expected returns

1 Relative price as measured by the price-to-book ratio; value stocks are those with lower price-to-book ratios. 2 Profitability is a measure of current profitability, based on information from individual companies’ income statements.

9 FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Source: Professor Kenneth R. French, mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html, 2016. 1 Relative price as measured by the price-to-book ratio; value stocks are those with lower price-to-book ratios. 2 “The Cross-Section of Expected Stock Returns,” Eugene F. Fama and Kenneth R. French, Journal of Finance, June 1992. 3 Profitability is a measure of current profitability, based on information from individual companies’ income statements. 4 Robert Novy-Marx provides consulting services to Dimensional Fund Advisors LP. The chart above shows historical geometric mean performance for different groupings of stocks within the broad equity universe. This universe, or market, includes stocks listed on the NYSE, AMEX, and NASDAQ exchanges. The research does not portray results of indexes. T-bill data is from Morningstar/Ibbotson. In order to assess returns of stocks with different characteristics, researchers Eugene Fama and Kenneth French grouped stocks according to size, relative price, and profitability. For groupings based on company size, stocks were ranked by market capitalization, where small cap represents stocks of companies in the bottom 30% of the universe and large cap represents stocks of companies in the top 30% of the universe. For groupings based on relative price, stocks were ranked by book-to-market equity ratios, where value represents stocks of companies in the top 30% of the universe and growth represents stocks of companies in the bottom 30% of the universe. For groupings based on profitability, stocks were ranked by operating profitability (annual revenues minus the cost of goods sold, interest expense, and selling, general, and administrative expenses, divided by book equity), where high profitability represents stocks of companies in the top 30% of the universe and low profitability represents stocks of companies in the bottom 30% of the universe. Fama and French are directors of and provide consulting services to Dimensional Fund Advisors LP. Diversification does not guarantee a profit or eliminate the risk of a loss. Selection of other periods may produce different results, including losses. Past performance does not guarantee future results.

Cost-effective to capture in a diversified portfolio

Persistent across time periods

Academic research has shown that stocks characterized by smaller capitalizations, lower valuations, and higher profitability have delivered higher expected returns over time

ANNUALIZED RETURNS OVER TIME

To be considered a true factor, a premium must be:

0

3

6

9

12

15

Low profitability

High profitability

Growth Value Large cap Small cap T-bills Stocks

9.77

3.42

11.85

9.61

12.65

9.32 11.19

Equity premium—stocks over T-bills

Small-cap premium—small company stocks over large company stocks

Value premium—value stocks over growth stocks

Profitability premium—stocks of highly profitable companies over stocks of less profitable companies

(1927–2015) (1927–2015) (1927–2015) (1964–2015)

Market Company size Relative price Profitability

8.32

Robust in the data Pervasive across markets

Sensible

Isolating the factors that drive higher expected returns

10

Weight the index to emphasize smaller companies, lower valuations, and higher profitability.2

Target range

600

Will hold up to

750 to minimize

unwarranted trading costs

Small

Large

Uni

vers

e of

sec

uriti

es

For illustrative purposes only. 1 See the appendix for the index description. 2 Profitability is measured as operating income before depreciation and amortization, minus interest expense scaled by book. Holdings are subject to change.

Index approach

Market Exposure

Define the target range of securities for the specific index.

Example shown is for the John Hancock Dimensional Mid Cap Index.1 Hold range could include up to 750 securities.

Implementation

Incorporate measured flexibility during reconstitution to maintain focus while balancing the trade-offs among competing premiums. This approach is designed to: Maintain focus on the asset

class and factors Control for unnecessary

turnover Minimize unnecessary trading

costs

11 FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Portfolio structure

Small Low

High

Profitability

Size

Large

Low

John Hancock exchange-traded fund lineup

12

“Net” represents the effect of a fee waiver and/or expense reimbursement, contractual through 8/31/17, and is subject to change.

Exchange-traded fund name Ticker Net expense ratio (%)

John Hancock Multifactor Large Cap ETF JHML 0.35

John Hancock Multifactor Mid Cap ETF JHMM 0.45

John Hancock Multifactor Consumer Discretionary ETF JHMC 0.50

John Hancock Multifactor Consumer Staples ETF JHMS 0.50

John Hancock Multifactor Energy ETF JHME 0.50

John Hancock Multifactor Financials ETF JHMF 0.50

John Hancock Multifactor Healthcare ETF JHMH 0.50

John Hancock Multifactor Industrials ETF JHMI 0.50

John Hancock Multifactor Materials ETF JHMA 0.50

John Hancock Multifactor Technology ETF JHMT 0.50

John Hancock Multifactor Utilities ETF JHMU 0.50

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Lukas J. Smart, CFA Lukas Smart, a senior portfolio manager and vice president, leads a team of investment professionals that manages U.S. large-cap equity and REIT portfolios. He also represents Dimensional and their portfolios in meetings with current and prospective clients.

Before joining Dimensional in 2007, Lukas did middle office and consultant work at Bank of America in Chicago. He was also a consultant and portfolio manager for Ibbotson Associates.

Lukas earned his bachelor of economics degree from the University of San Diego and his M.B.A. from the University of Chicago Booth School of Business. He is a CFA charterholder and is a member of the CFA Society of Austin.

Joel P. Schneider Joel Schneider, a senior portfolio manager and vice president, leads a team of investment professionals who manage global equity portfolios. He also represents Dimensional in meetings with current and prospective clients.

Before joining Dimensional, Joel worked as a management consultant at ZS Associates in Chicago, where he developed statistical models to optimally allocate resources and measure the return on investment. Joel also worked in engineering and business development at Lockheed Martin, designing and developing communication systems for the U.S. Navy and Air Force as part of their leadership development program.

Joel has an M.B.A. from the University of Chicago Booth School of Business, an M.S. in industrial engineering from the University of Minnesota, and a B.S. in computer engineering from Iowa State University.

Lukas J. Smart, CFA, and Joel P. Schneider work for Dimensional Fund Advisors LP, the subadvisor to the John Hancock Multifactor ETFs.

Portfolio manager biographies

13 FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

14

Q & A

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

15

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Appendix

16

INDEX DESCRIPTIONS ___________________________________________________________________________________________________________________________________________________

John Hancock Dimensional Large Cap Index is designed to comprise a subset of securities in the U.S. Universe issued by companies whose market capitalizations are larger than that of the 801st largest U.S. company at the time of reconstitution. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

• Adjustments for market capitalization: Eligible securities are assigned into one of three size groups,with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest marketcapitalization group will have their free-float market capitalization increased by a size-adjustment factor. Securities in the middle group will have their free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization willreceive the lowest size adjustment factor of the three groups.

• Adjustments for relative price and profitability: Adjustments for relative price and profitability are implemented on a sector-by-sector basis. Within each sector, securities (other than REITs) are assigned to a relative price group and to a profitability group. REITs are generally assigned to separate relative price and profitability groups. Relative price adjustment factors are assigned withthe intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors areassigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability. Relative price and profitabilityadjustment factors for REITs will generally act to reduce their weight relative to their unadjustedweight in the U.S. Universe.

• Securities are then weighted after taking into account their free-float, size, relative price andprofitability adjustments, subject to a cap of 4% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by

Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

John Hancock Dimensional Mid Cap Index is designed to comprise a subset of securities in the U.S. Universe issued by companies whose market capitalizations are between the 200th and 951st largest U.S. company at the time of reconstitution. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

• Adjustments for market capitalization: Eligible securities are assigned into one of two size groups,with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the group ofcompanies with smaller market capitalizations will have their free-float market capitalization adjusted by a larger size-adjustment factor than securities in the group of companies with larger market capitalizations.

• Adjustments for relative price and profitability: Adjustments for relative price and profitability are implemented on a sector-by-sector basis. Within each sector, securities (other than real estate investment trusts (REITs)) are assigned to a relative price group and to a profitability group. REITsare generally assigned to separate relative price and profitability groups. Relative price adjustmentfactors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustmentfactors are assigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability. Relative price and profitabilityadjustment factors for REITs will generally act to reduce their weight relative to their unadjustedweight in the U.S. Universe.

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

17

INDEX DESCRIPTIONS ____________________________________________________________________________________________________________________________________________________________________________ Securities are then weighted after taking into account their free-float, size, relative price and

profitability adjustments, subject to a cap of 4% on a single company at time ofreconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

John Hancock Dimensional Consumer Discretionary Index is designed to comprise securities in the consumer discretionary sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

Adjustments for market capitalization: Securities within the eligible universe are assigned into one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest market capitalization group will have their free-float marketcapitalization increased by a size-adjustment factor. Securities in the middle group will havetheir free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustmentfactor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group and to a profitability group. Relative price adjustment factors are assigned with the intent

increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors are assigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

Securities are then weighted after taking into account their free-float, size, relative price andprofitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The consumer discretionary sector is composed of companies in areas such as restaurants, media, consumer retail, leisure equipment and products, hotels, apparel, automobiles, and consumer durable goods. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

The fund is non-diversified, which means that it may invest its assets in a smaller number of issuers than a diversified fund.

John Hancock Dimensional Financials Index is designed to comprise securities in the financials sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

18

INDEX DESCRIPTIONS _________________________________________________________________________________________________________________________________________________________________________

Adjustments for market capitalization: Securities within the eligible universe are assigned into one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest market capitalization group will have their free-float market capitalization increased by a size-adjustment factor. Securities in the middle group will have their free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group

and to a profitability group. Relative price adjustment factors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors are assigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

Securities are then weighted after taking into account their free-float, size, relative price and

profitability adjustments, subject to a cap of 4% on a single company at time of reconstitution. A cap of 4.75% on a single company applies between reconstitutions.

The Index is reconstituted and rebalanced on a semiannual basis. The financials sector is composed of companies in areas such as banking, savings and loans, insurance, consumer finance, investment brokerage, asset management, or other diverse financial services. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets. The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries. The fund is non-diversified, which means that it may invest its assets in a smaller number of issuers than a diversified fund. John Hancock Dimensional Healthcare Index is designed to comprise securities in the healthcare sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks.

The selection and weighting of securities in the Index involves a rules based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

Adjustments for market capitalization: Securities within the eligible universe are assigned into

one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest market capitalization group will have their free-float market capitalization increased by a size-adjustment factor. Securities in the middle group will have their free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group

and to a profitability group. Relative price adjustment factors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors are assigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

Securities are then weighted after taking into account their free-float, size, relative price and

profitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The healthcare sector is composed of companies in areas such as the manufacture of healthcare equipment and supplies, biotechnology, home or long-term healthcare facilities, hospitals, pharmaceuticals, or the provision of basic healthcare services. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

_____________________________________________________________________________________________________________________________________________________________________

19

INDEX DESCRIPTIONS

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

The fund is non-diversified, which means that it may invest its assets in a smaller number of issuers than a diversified fund.

John Hancock Dimensional Technology Index is designed to comprise securities in the technology sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

Adjustments for market capitalization: Securities within the eligible universe are assigned into one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in thesmallest market capitalization group will have their free-float market capitalization increased by asize-adjustment factor. Securities in the middle group will have their free-float marketcapitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group and to a profitability group. Relative price adjustment factors are assigned with the intent ofincreasing the weights of names with lower relative prices and decreasing the weights of nameswith higher relative prices. Similarly, profitability adjustment factors are assigned with the intentof increasing the weights of names with higher profitability and decreasing the weights of nameswith lower profitability.

Securities are then weighted after taking into account their free-float, size, relative price andprofitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The technology sector is composed of companies in areas such as the creation, development or provision of software, hardware, internet services, database management, information technology consulting and services, data processing, or semi-conductors. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

The fund is non-diversified, which means that it may invest its assets in a smaller number of issuers than a diversified fund.

John Hancock Dimensional Consumer Staples Index is designed to comprise securities in the consumer staples sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

_____________________________________________________________________________________________________________________________________________________________________

20

INDEX DESCRIPTIONS

��Adjustments for market capitalization: Securities within the eligible universe are assigned into one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in thesmallest market capitalization group will have their free-float market capitalization increased by asize-adjustment factor. Securities in the middle group will have their free-float marketcapitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group and to a profitability group. Relative price adjustment factors are assigned with the intent ofincreasing the weights of names with lower relative prices and decreasing the weights of nameswith higher relative prices. Similarly, profitability adjustment factors are assigned with the intentof increasing the weights of names with higher profitability and decreasing the weights of nameswith lower profitability.

• Securities are then weighted after taking into account their free-float, size, relative price andprofitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The consumer staples sector is composed of companies involved in areas such as the production, manufacture, distribution or sale of food, beverages, tobacco, household goods, or personal products. The U.S. Universe is defined as a free float- adjusted market capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

John Hancock Dimensional Energy Index is designed to comprise securities in the energy sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability.

Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

�� Adjustments for market capitalization: Securities within the eligible universe are assigned into one of three size groups, with the intent of increasing the weights of smaller nameswithin the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest market capitalization group will have their free-float market capitalization increased by a size-adjustment factor. Securities in the middle groupwill have their free-float market capitalization increased by a lesser size-adjustment factor.Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group and to a profitability group. Relative price adjustment factors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors areassigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

• Securities are then weighted after taking into account their free-float, size, relative price and profitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The energy sector is composed of companies involved in areas such as the production, distribution, or sale of alternative fuels, coal, electricity, natural gas, nuclear power, oil, and other forms of energy. The U.S. Universe is defined as a free float-adjusted market-capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

_____________________________________________________________________________________________________________________________________________________________________

21

INDEX DESCRIPTIONS

John Hancock Dimensional Industrials Index is designed to comprise securities in the industrials sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows: �� Adjustments for market capitalization: Securities within the eligible universe are assigned into one

of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest market capitalization group will have their free-float market capitalization increased by a size-adjustment factor. Securities in the middle group will have their free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group

and to a profitability group. Relative price adjustment factors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors are assigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

• Securities are then weighted after taking into account their free-float, size, relative price and

profitability adjustments, subject to a cap of 6% on a single company at time of reconstitution. The Index is reconstituted and rebalanced on a semiannual basis. The industrials sector is composed Of companies involved in areas such as aerospace and defense, construction and engineering, machinery, building products and equipment, road/rail/air/marine transportation and infrastructure, industrial trading and distribution, and related services. The U.S. Universe is defined as a free float-adjusted market- capitalization-weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries. John Hancock Dimensional Materials Index is designed to comprise securities in the materials sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows: �� Adjustments for market capitalization: Securities within the eligible universe are assigned

into one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in the smallest market capitalization group will have their free-float market capitalization increased by a size-adjustment factor. Securities in the middle group will have their free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price

group and to a profitability group. Relative price adjustment factors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors are assigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

• Securities are then weighted after taking into account their free-float, size, relative price

and profitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

_____________________________________________________________________________________________________________________________________________________________________

22

INDEX DESCRIPTIONS

The Index is reconstituted and rebalanced on a semiannual basis. The materials sector is composed of companies involved in areas such as chemicals, metals, paper products, containers and packaging, and construction materials. The U.S. Universe is defined as a free float-adjusted market-capitalization- weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market-capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

John Hancock Dimensional Utilities Index is designed to comprise securities in the utilities sector within the U.S. Universe whose market capitalizations are larger than that of the 1001st largest U.S. company at the time of reconstitution. Stocks that compose the Index include those that may be considered medium or smaller capitalization company stocks. The selection and weighting of securities in the Index involves a rules-based process that may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta. Securities are classified according to their market capitalization, relative price, and profitability. Weights for individual securities are then determined by adjusting their free-float adjusted market capitalization weight within the universe of eligible names so that names with smaller market capitalizations, lower relative price and higher profitability generally receive an increased weight relative to their unadjusted weight, and vice versa. This process can be summarized as follows:

• Adjustments for market capitalization: Securities within the eligible universe are assigned into one of three size groups, with the intent of increasing the weights of smaller names within the eligible universe and decreasing weights of larger names within the eligible universe. Securities in thesmallest market capitalization group will have their free-float market capitalization increased by asize-adjustment factor. Securities in the middle group will have their free-float market capitalization increased by a lesser size-adjustment factor. Securities in the group with the largest market capitalization will receive the lowest size adjustment factor of the three groups.

Adjustments for relative price and profitability: Securities are assigned to a relative price group and to a profitability group. Relative price adjustment factors are assigned with the intent of increasing the weights of names with lower relative prices and decreasing the weights of names with higher relative prices. Similarly, profitability adjustment factors areassigned with the intent of increasing the weights of names with higher profitability and decreasing the weights of names with lower profitability.

• Securities are then weighted after taking into account their free-float, size, relative price and profitability adjustments, subject to a cap of 6% on a single company at time of reconstitution.

The Index is reconstituted and rebalanced on a semiannual basis. The utilities sector is composed of companies involved in areas such as the provision of gas, electric and water power, energy trading or the provision of related infrastructure or services. The U.S. Universe is defined as a free float-adjusted market- capitalization weighted portfolio of U.S. operating companies listed on the New York Stock Exchange (NYSE), NYSE MKT LLC, NASDAQ Global Market, or such other securities exchanges deemed appropriate in accordance with the rules-based methodology that is maintained by Dimensional Fund Advisors LP. This means that the market capitalization of a particular company within the eligible universe of stocks is adjusted to exclude the share capital of a company that is not considered freely available for trading in the public equity markets.

The fund, using an indexing investment approach, attempts to approximate the investment performance of the Index by investing in a portfolio of securities that generally replicates the Index. The fund may concentrate its investments in a particular industry or group of industries to the extent that the Index concentrates in an industry or group of industries.

Appendix

FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

The indexes are calculated by NYSE or its affiliates (NYSE). The funds, which are based on the indexes, are not issued, sponsored, endorsed, sold, or promoted by NYSE, and NYSE makes no representation regarding the advisability of investing in such product. NYSE makes no express or implied warranties, and hereby expressly disclaims all warranties, of merchantability or fitness for a particular purpose with respect to the index or any data included therein. In no event shall NYSE have any liability for any special, punitive, indirect, or consequential damages, including lost profits, even if notified of the possibility of such damages. Investing involves risks, including the potential loss of principal. Large company stocks could fall out of favor. The stock prices of midsize and small companies can change more frequently and dramatically than those of large companies, and value stocks may decline in price. A portfolio concentrated in one industry or sector or that holds a limited number of securities may fluctuate more than a diversified portfolio. Shares may trade at a premium or discount to their NAV in the secondary market, and a fund’s holdings and returns may deviate from those of its index. These variations may be greater when markets are volatile or subject to unusual conditions. Errors in the construction or calculation of a fund’s index may occur from time to time. Please see the funds’ prospectuses for additional risks. John Hancock Multifactor ETF shares are bought and sold at market price (not NAV), and are not individually redeemed from the fund. Brokerage commissions will reduce returns. Dimensional Fund Advisors LP receives compensation from John Hancock in connection with licensing rights to the John Hancock Dimensional indexes. Neither John Hancock Advisers, LLC nor Dimensional Fund Advisors LP guarantees the accuracy and/or completeness of an index (each an underlying index) or any data included therein, and neither John Hancock Advisers, LLC nor Dimensional Fund Advisors LP shall have any liability for any errors, omissions, or interruptions therein. Neither John Hancock Advisers, LLC nor Dimensional Fund Advisors LP makes any warranty, express or implied, as to results to be obtained by a fund, owners of the shares of a fund, or any other person or entity from the use of an underlying index, trading based on an underlying index, or any data included therein, either in connection with a fund or for any other use. Neither John Hancock Advisers, LLC nor Dimensional Fund Advisors LP makes any express or implied warranties, and expressly disclaims all warranties, of merchantability or fitness for a particular purpose or use with respect to an underlying index or any data included therein. Without limiting any of the foregoing, in no event shall either John Hancock Advisers, LLC or Dimensional Fund Advisors LP have any liability for any special, punitive, direct, indirect, or consequential damages, including lost profits, arising out of matters relating to the use of an underlying index, even if notified of the possibility of such damages.

Clients should carefully consider a fund’s investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other important information about the fund. To obtain a prospectus, call John Hancock Investments at 800-225-6020, or visit our website at jhinvestments.com/etf. Clients should read the prospectus carefully before investing or sending money.

John Hancock ETFs are distributed by Foreside Fund Services, LLC, and are subadvised by Dimensional Fund Advisors LP. Foreside is not affiliated with John Hancock Funds, LLC or Dimensional Fund Advisors LP.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE. NOT INSURED BY ANY GOVERNMENT AGENCY. FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC. JHAN-2016-08-29-0396

@JH_Investments | jhinvestmentsblog.com

INDEX DESCRIPTIONS ___________________________________________________________________________________________________________________________________

Connect with John Hancock Investments: