A. Influences on Consumers I. CONSUMER LAW 1. Consumer= one who buys goods and services from a...

66

A. Influences on Consumers I. CONSUMER LAW 1. Consumer = one who buys goods and services from a seller 2. Contract = Legal agreement to pay for goods or services 3. Caveat emptor = “Let the buyer beware” a. In the old days consumers had no protections from unscrupulous sellers 4. Advertising = information provided by the seller regarding their products (can be useful, but also can be misleading ) NEXT

-

Upload

barnaby-hampton -

Category

Documents

-

view

214 -

download

1

Transcript of A. Influences on Consumers I. CONSUMER LAW 1. Consumer= one who buys goods and services from a...

A. Influences on Consumers

I. CONSUMER LAW

1. Consumer= one who buys goods and services from a seller

2. Contract = Legal agreement to pay for goods or services

3. Caveat emptor = “Let the buyer beware”

a. In the old days consumers had no protectionsfrom unscrupulous sellers

4. Advertising= information provided by the seller regarding their products (can be useful, but also can be

misleading)

NEXT

B. How Laws Protect the Consumer1. Federal laws

a. Prohibit misleading ads, prices and labelsb. Set standards for safety and qualityc. Create agencies to enforce standardsd. Create laws to regulate marketplacee. Protect those with disabilities

2. State laws

a. Similar to federal laws

b. Terms:class action= more than one plaintiff

takes a defendant to courtremedy= making up for harm done

cease and desist order= court orders a company to stop an illegal practice

restitution= having to repay money thatwas illegally obtained

NEXT

C. Protecting Your Rights as a Consumer1. What to do before buying a product

a. Research products (Consumer Reports)b. Compare prices

c. Consider a store’s reputation-service/delivery charges?

d. Read the warrantye. Read the contract (if applicable)

2. What to do after buying a product

a. Inspect the product (save receipts)b. Read the instructionsc. If there’s a problem:

-contact seller first (be polite but firm)-contact the manufacturer-contact a government agency

NEXT

1 2 3

3. Consumer protection agencies

a. Consumer groups b. Business and trade associationsc. Media (publicity)d. Professional associationse. State and local governmentf. Federal government

4. Taking your case to court

a. Criminal court

fraud= salesmen who knowingly lie inorder to make a sale

b. Civil courtdamages= money won as a result of an

injury or loss

rescission and restitution= court orderscontract cancelled and money refunded

specific performance= the seller isforced to carry out the contract

NEXT

Way advertisers “get” you

Buy our product receive what you see

Pop ups on the internet Puffing “World’s Best Fries” Fine print, fast talking

D. Deceptive Sales Practices1. Door-to-door and telephone sales

a. Be very wary to give your credit card number on the phone

b. donotcall.gov – good for 5 years

2. Phony contest and referral sales

3. Advertising and the consumer

a. Some ads are illegal(tobacco ads on tv, radio.)

b. Can be helpful/informative

c. Ads must be truthful-except “puffing” (opinion statements)

d. Bait and switch-luring customers into a store and then trying to sell them more expensive items

e. Mail order sales-companies must ship products quickly-read the contract carefully

f. Repairs and estimates-always get a written estimate

E. CONTRACTS1. Elements of a contract

a. Offerb. Acceptancec. Consideration= something of value must

be exchanged (usually money)

2. Minors and contracts

a. Minors may enter contracts, but generally can’t be forced to carry them out

-generally they must have a cosigner

3. Written and oral contracts

a. Either type are legal

-the law favors written contracts

4. Illegal contracts

a. Contracts contrary to the law (drugs, etc.)

b. Unconscionable contracts-contracts that are unfair

NEXT

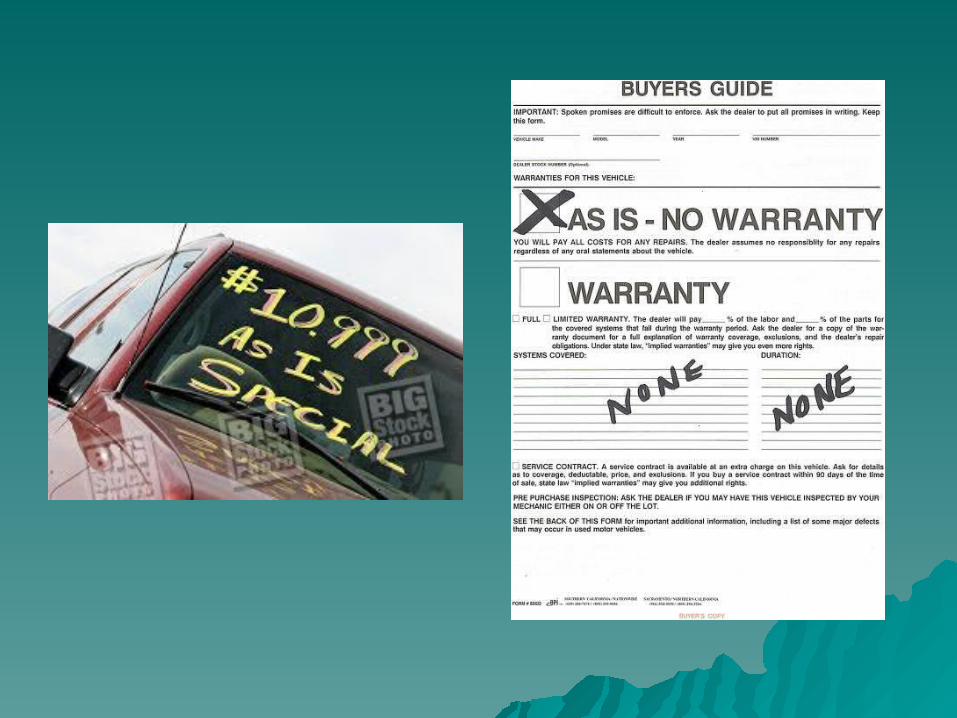

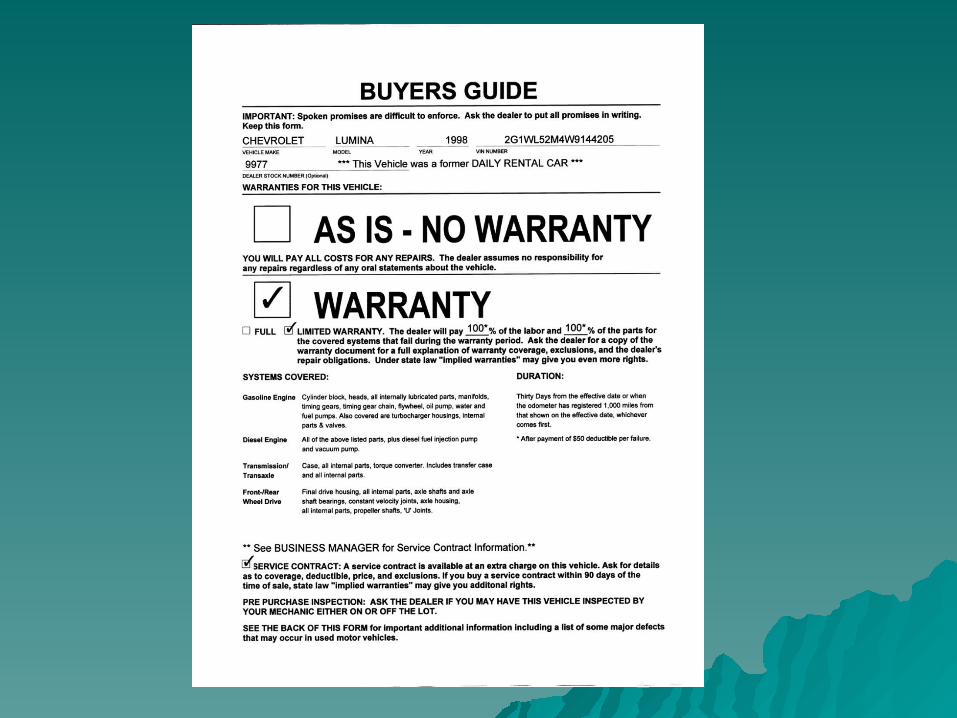

F. Warranties1. Warranty= a guarantee from the seller as to the

quality of the product

a. Breach= if the seller does not live up tothe conditions of the warranty

2. Types of warranties

a. Express warranty= statements of factsabout a products performance

b. Implied warranty= the law says that allproducts should do what they’re supposed to do

-applies to stores/dealers only

-only if product is used properly

c. Disclaimer= a seller’s attempt to limit theirresponsibility

-ie. “as is” or “with all faults”

NEXT

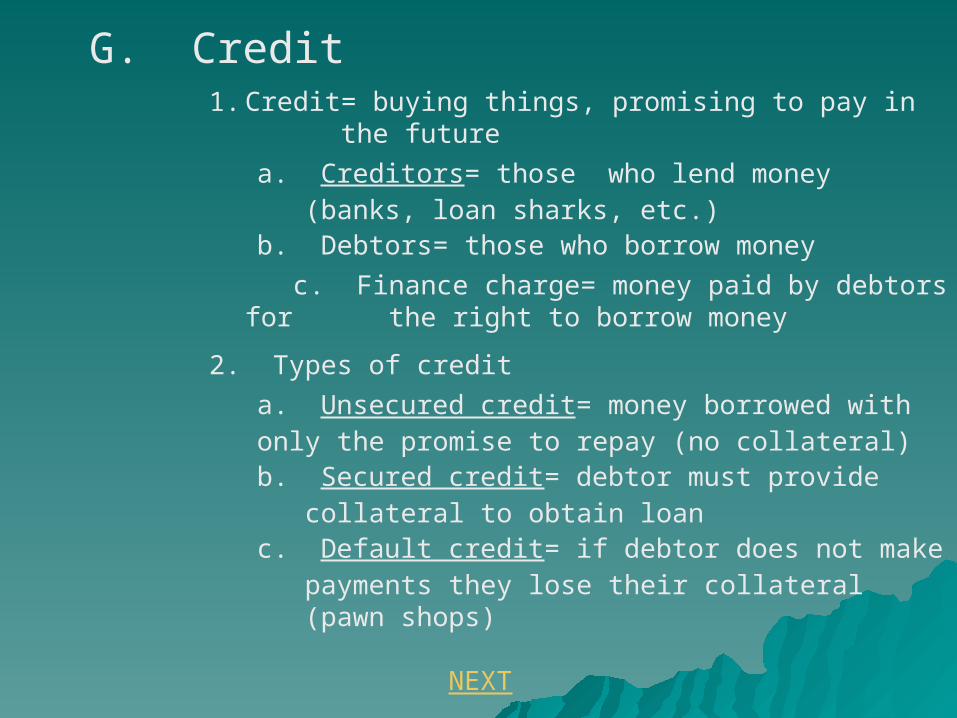

G. Credit1. Credit= buying things, promising to pay in

the future

a. Creditors= those who lend money(banks, loan sharks, etc.)

b. Debtors= those who borrow money

c. Finance charge= money paid by debtors for the right to borrow money

2. Types of credit

a. Unsecured credit= money borrowed with only the promise to repay (no collateral)

b. Secured credit= debtor must provide collateral to obtain loan

c. Default credit= if debtor does not make payments they lose their collateral (pawn shops)

NEXT

3. Credit cards and charge accounts

a. Credit cards make it easy to borrow moneyto purchase items

-APR= Annual Percentage Rate

b. If you lose your card, just report it missing

c. Debit cards= look/act like credit cards, butmoney comes directly out of onesbank account

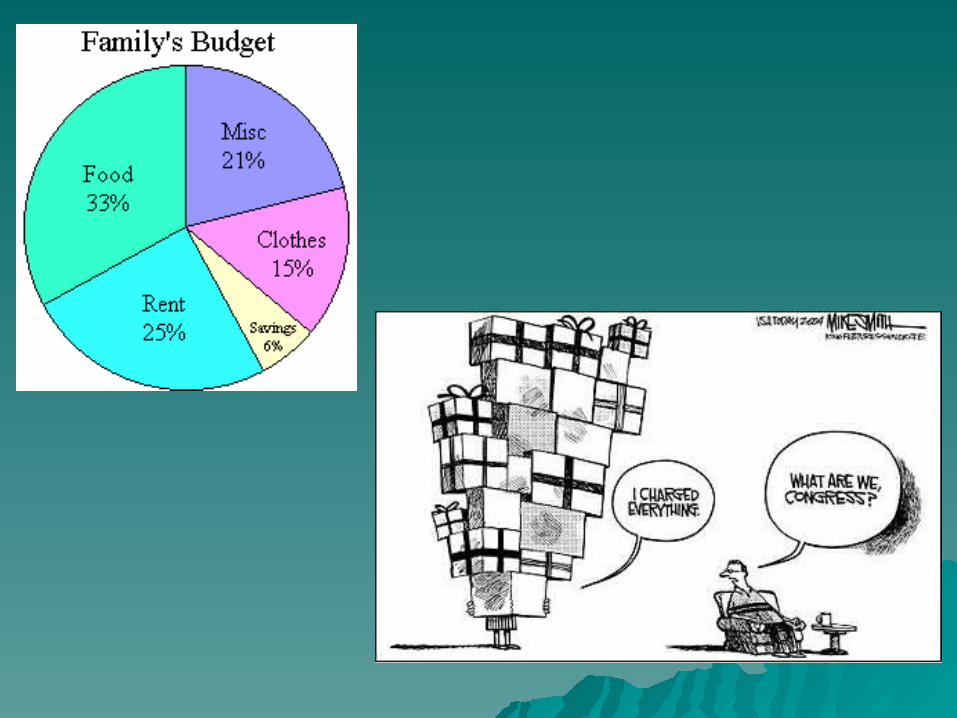

4. When should you use credit?

a. Using credit makes the item cost more, so use it sparingly (home, education, business and possibly car)

b. If possible pay credit card bills in full each month

NEXT

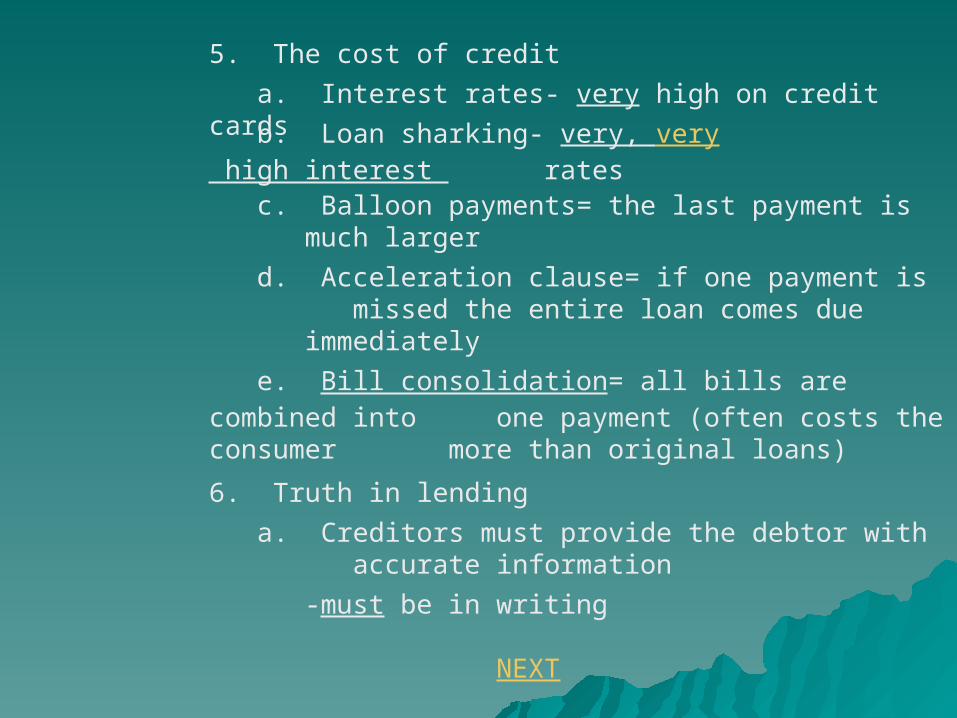

5. The cost of credit

a. Interest rates- very high on credit cards

b. Loan sharking- very, very high interest rates

c. Balloon payments= the last payment is much larger

d. Acceleration clause= if one payment is missed the entire loan comes due immediately

e. Bill consolidation= all bills are combined into one payment (often costs the consumer more than original loans)

6. Truth in lending

a. Creditors must provide the debtor with accurate information

-must be in writing

NEXT

7. What to do if you’re denied credit

a. Ask the creditor why you were turned down

b. Check your credit file

H. Default and collection practices1. Default= when a debtor can’t make his payments

a. How to avoid default

- put yourself on a budget

- ask the creditor for more time

- get financial counseling

- get help from family or friends

b. Bankruptcy

-if you’re out of choices, declaring bankruptcy may be best option

-it will be on your credit report for 10 years!!

NEXT

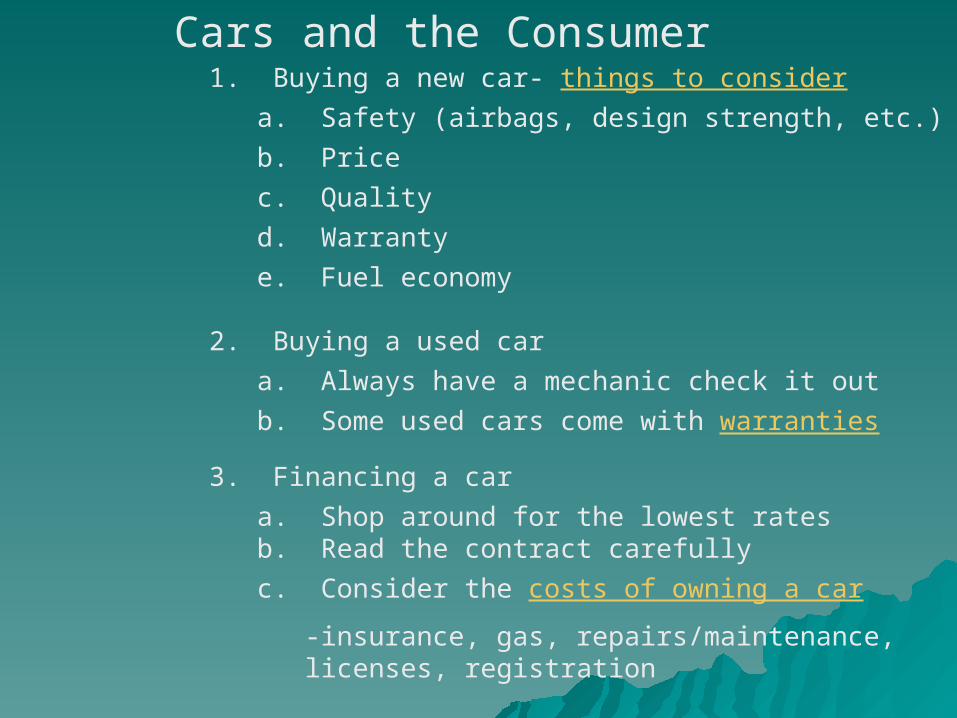

2. Buying a used car

a. Always have a mechanic check it out

b. Some used cars come with warranties

3. Financing a car

a. Shop around for the lowest ratesb. Read the contract carefully

c. Consider the costs of owning a car

-insurance, gas, repairs/maintenance, licenses, registration

Cars and the Consumer1. Buying a new car- things to consider

a. Safety (airbags, design strength, etc.)

b. Price

c. Quality

d. Warranty

e. Fuel economy

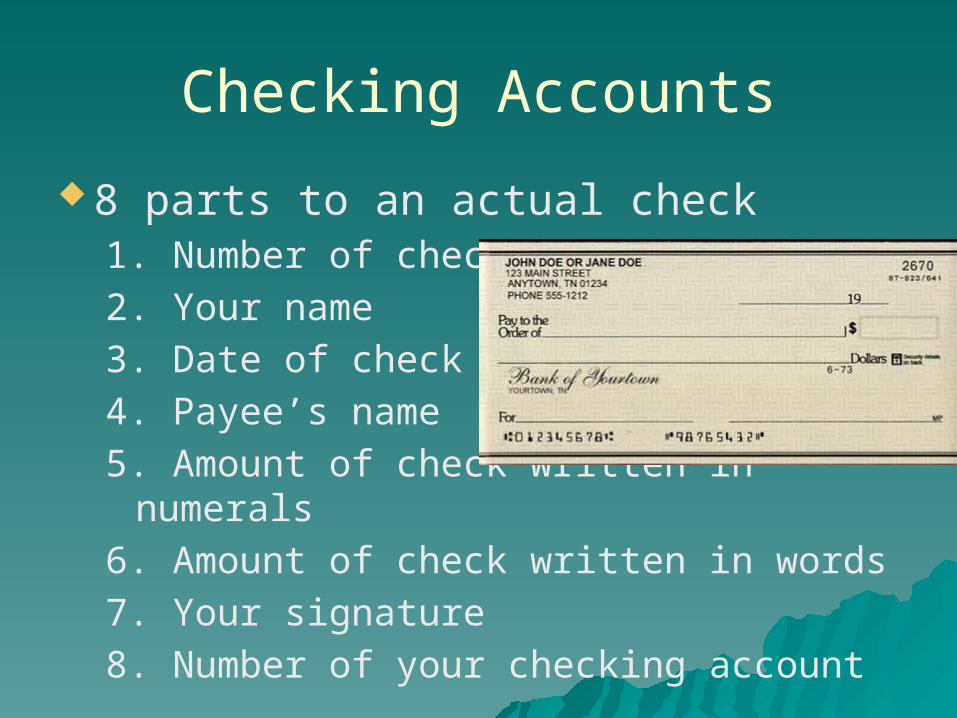

Checking Accounts

8 parts to an actual check1. Number of check2. Your name3. Date of check4. Payee’s name5. Amount of check written in numerals6. Amount of check written in words7. Your signature8. Number of your checking account

Two types of Checking Accounts

Service Charge No interest being

charged to you but… $.50 a month and $.10

each check written are charged to you

Free Checking You’re checking

account is free if you stay above a minimum number of dollars in your account

Mechanics of Checking

Balance – amount in your account Deposit – putting money into your

account Withdrawal – taking money out of

account Canceled Checks – checks that

people (the payees) have turned in in order to get cash

Mechanics of Checking cont

Statement – bank’s sheet telling you how much is in your account, service charges, # and amount of checks written for that particular month, etc

Checkbook- contains your checks and….

Check Register – an organized way to keep your balance right on the spot and compare your balance to your banks balance

4 more…

Overdraft – when you spend more than what’s in your account

Bounces – when you write a check larger then what’s in your account

Cover – re-writing a check to the receiver of the bounced check

Stop-payment – letting the bank know not to let a check be cashed

Differences between the Plastic

Debit- a plastic card in the form of checks, all payments are subtracted from checking account

Charge- a plastic card in which you defer all payments until the end of each month– Pay each month in full

One more…credit card

Credit- Plastic cards make it easy to borrow money to purchase items, unpaid credit gathers interest– APR= Annual Percentage Rates

In any case, if you lose one of these cards, call the provider and cancel it!!!

Default and collection practices1. Default= when a debtor can’t make his payments

a. How to avoid default

- put yourself on a budget

- ask the creditor for more time- get financial counseling

- get help from family or friends

b. Bankruptcy

-if you’re out of choices, declaring bankruptcy may be best option

-it will be on your credit report for 10 years!!

C. Creditor collection practices

-calls and letters may not be harassing

-repossession= creditor takes the purchased item back

-court action= creditor takes the debtor to court-garnishment= court orders a creditor be paid by taking money directly from a debtor’s pay check

Savings – Methods

Saving Accounts- accounts maintained by retail financial institutions that pay interest but cannot be used directly as money

CD’s- a time deposit, a financial product commonly offered to consumers in the United States by banks, thrift institutions, and credit unions.

1 more method

Bonds- Certificates that represent money a government or corporation has borrowed from other entities

More on Savings

Why save? Emergency

Take advantage of opportunities

Reach financial goals

Pay yourself first Save to reach goals

From each paycheck – save 1st, spend 2nd

Vocab – last one of Consumer Law

26 – corrective advertising 27 – cease and desist orders,

restitution, FTC, FDA 28 – none! 29 – tenant, landlord, lease, warranty

of habitability, sublease clause, right to quiet enjoyment

What’s collected Friday

12 bell ringers between 4/25-5/12– 6pts

Notes on Warranties, Checking, Credit, and Savings/Investment– 8pts

Contracts

3 things that make up a contract Minors and contracts What makes voids a contract Identify parties of contract

Warranties

Express Warranties Implied Warranties

– Merchantability– Fitness for a Particular Purpose– Title

Checking Accounts

Parts of a check Types of checking accounts Mechanics of Checking

More concepts

Credit– Types of Plastic– Bankruptcy– Collection practices

– Savings Accounts – Banks, CD’s, Bonds

More concepts

Housing– Tenant, landlord, lease, sublease, right

to quiet enjoyment– Identify a Lease

Cars– Things to look at before buying, what

resources to look at, Interest Rates on loans

2 more concepts

DSP– What we went over today in class

Basic Consuming– FTC, FDA, Angie’s List, Consumer

Reports, Nutrition Facts