A Guide to Completing an Auditable Special Schedule 7 · Special Schedule 7 Methodology –Part 1...

16

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 1 A Guide to Completing an Auditable Special Schedule 7 PART 1 - Key Concepts PART 2 - Guide and example) • Allen Mapstone JRA, Jeff Roorda JRA • Peer Reviewers - John Comrie, Dr Penny Burns • Developed and tested with Engineering and Finance Professionals across NSW Part 1

Transcript of A Guide to Completing an Auditable Special Schedule 7 · Special Schedule 7 Methodology –Part 1...

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 1

A Guide to Completing an Auditable Special Schedule 7

PART 1 - Key Concepts

PART 2 - Guide and example)

• Allen Mapstone JRA, Jeff Roorda JRA

• Peer Reviewers - John Comrie, Dr Penny Burns

• Developed and tested with Engineering and Finance Professionals across NSW

Part 1

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 22

Modern society is dependent on infrastructure. Asset and Risk Management Plans communicate the trade

off between risk, service levels and cost. As infrastructure ages, growth slows and risks increase, asset and

risk management plans enable evidence based decision making by Government.

The question posed by the annual reporting requirement for NSW Local Government, known as Special

Schedule 7 (SS7), is deceptively simple. How much is needed to bring infrastructure to a satisfactory

standard and maintain that standard? The question assumes Councils have adequately resourced their

charter under section 8 of the NSW Local Government Act, “ to effectively account for and manage these

assets and to have regard to the long-term and cumulative effects of its decisions”. Councils are

reasonably assumed to have service level scenarios based on forward looking financial, asset management

JRA’s experience is that most Councils have asset and risk management plans supported by improving

evidence under the NSW Integrated Planning and Reporting framework.

JRA was commissioned by a number of Councils to provide assistance with the preparation of SS7 and

decided to make this guide available to others at no cost since it represents the cumulative ideas of many,

but not of al. This guide is the result of a series of workshops with Local Government Professionals

completed in 2014 and builds on the core reference documents of the 2013 IPR Manual, the International

Infrastructure Management Manual and Australian Infrastructure Financial Management Guidelines by

Institute of Public Works Engineering Australasia.

The contribution and assistance by many local government and audit professionals in the preparation of this

guide is gratefully acknowledged..

This guide does not at this time represent the views of the NSW Office of Local Government or IPWEA

NSW. JRA welcomes any comments and will update this guide as needed subject to peer review and

make the latest version of the guide available on request at no cost.

Introduction Part 1

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 33

• The Annual Report is one of the key accountability mechanisms between a council and its community. As

such, it should be written and presented in a way that is appropriate for each council’s community. IPR

Manual Section 6.1 - March 2013

• Councils are required to report on the condition of the public works (including public buildings, public

roads; and water, sewerage and drainage works) under the control of the council as at the end of that year,

together with:

• An estimate (at current values) of the amount of money required to bring the works up to a satisfactory standard, and

• An estimate (at current values) of the annual expense of maintaining the works at that standard, and

• The council’s program of maintenance for that year in respect of the works.

• The report on the condition of public works is also included in the financial reports and is known as Special Schedule

7. Councils must complete this Schedule each year.

IPR Manual Section 6.4 - March 2013

• The Asset Management Strategy must identify assets that are critical to the council’s operations and

outline the risk management strategies for these assets. IPR Manual Section 3.4.1 - March 2013

• The Asset Management Plan/s must identify asset service standards. IPR Manual Section 3.4.2 - March 2013

• A council’s Asset Management Plan should incorporate an assessment of the risks associated with the

assets involved and the identification of strategies for the management of those risks. The strategies

should be consistent with the overall risk policy of council. The International and Australian Standard

AS/NZS/ISO/31000:2009 – Risk management – Principles and guideline provides a useful guide. IPR Manual

IPR Manual Section 3.4.2 - March 2013

JRA

The Annual Report Part 1

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 44

Key Concepts1. The report on the condition of public works (Special Schedule 7) should flow directly from the

Delivery Program, which should define performance indicators for both existing and proposed

levels of service. These performance measures can be used to quantify the upgrade costs (or

degree of over-servicing) between existing and target service levels. (Note 1)

2. The determination of satisfactory target service levels involves an informed tradeoff using the

Long Term Financial Plan and Asset Management Plan 10 year scenarios for revenues, risks

and service levels. This approach is consistently identified in the IPR Manual and expanded in

complementary resources such the IPWEA Level of Service and Community Engagement

Practice Note 8. (Note 2)

3. Cost to bring to assets to satisfactory should be determined by asset and risk management

plans. This guide recommends that the cost to bring to satisfactory should be the total unfunded

cost to renew all high residual risk assets in the current risk register.

4. Special 7 is auditable by checking for alignment between special schedule 7 and asset and risk

management plans. The risk register establishes a consistent and evidence based cost to bring

to satisfactory and connects to good governance practice of transparent reporting of risk through

appropriate governance processes such as an audit committee.

5. Asset Risks include operational, technical, financial, legal, social and environmental risks using

the ISO 31000 framework. Supporting resources are available and this methodology is

consistently applied internationally. (Note 3)

• Note 1 – NSW Office of Local Government, IPR Manual Section 6.4 P133

• Note 2 - IPWEA Practice Note 8 – Level of Service and Community Engagement, Section 2, P2

• Note 3 – IPWEA NAMSPLUS – Asset and Risk Management Plan Templates

Part 1

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 5

A Guide to Completing an Auditable Special Schedule 7

PART 2 - Guide and Example

• Allen Mapstone JRA, Jeff Roorda JRA

• Peer Reviewers - John Comrie, Dr Penny Burns

• Developed and tested with Engineering and Finance Professionals across NSW

Part 2

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 6

• This guide was commissioned by a by a number of regional groups of local government professionals

and managers in NSW and has developed and been tested over a 6 month period with finance,

engineering and audit professionals.

• The Asset and Risk Management Plans are the essential source of Special Schedule 7 (SS7) reporting.

Auditing special schedule 7 should be based on alignment between SS7 and the asset and risk

management plans, and in particular the risk register and planned risk treatments and costs to maintain

satisfactory service levels.

• Part 2 of the guide uses an example using the IPWEA NAMSPLUS system of developing and

maintaining asset management plans. Whilst this approach is simple, economic and will provide

consistent results, Councils may choose alternative systems and still comply with the intent of Part 1.

• This guide has been based on a series of consultative workshops with senior Engineers and Accountants

throughout Australia and USA and has been peer reviewed by

• John Comrie (JAC) and

• Dr Penny Burns and

• Jeremy McAnally JRA

• Allen Mapstone JRA

About Part 2Part 2

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 77

• BTS is the sum of Modern Equivalent Renewal Cost of high residual risk assets not financed in current ornext year’s budget. This is based on assets due for renewal but not funded. Cost to bring to satisfactoryis the most efficient modern equivalent capital treatment to keep the asset to service.

• Audited by link to Asset Management Plan and Risk Register

• Deferring renewal may result in the modern equivalent renewal cost increasing and will impact future BTSreporting.

• BTS analysis must be carried out for each material asset component. Network averages should not beused to determine BTS.

• The connection to risk registers reinforces the importance of independent Audit Committees to reportservice risks to Council. This enables the essential separation of aspirational but unaffordable servicelevels with essential service levels.

• Aspirational service levels that the community does not want to pay for and do not present high residualrisks are not infrastructure backlog or financial sustainability risks.

• If service levels are declining in accordance with an adopted, agreed and communicated assetmanagement strategy this is not backlog, nor a financial sustainability risk provided risks are managed andcommunicated.

• Integrated Planning and Reporting Manual for local government in NSW MARCH 2013. Premier &

Cabinet - Division of Local Government

• International Infrastructure Management Manual (IIMM). Institute of Public Works Engineering

Australasia (IPWEA)– Nov 2011

• IPWEA NAMPLUS Advanced Risk Register Template

• IPWEA NAMSPLUS Asset Management Plan Template

Part 2Key Concept

Cost to Bring to Satisfactory (BTS)

Resource Material

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 88

Part 2Key Concept

Determining What is Satisfactory• Satisfactory service levels (SSL) are determined by Council taking into account community needs and

aspirations in the resourcing strategy scenarios and detailed in Asset Management Plans (IPR Manual

P16)

• SSL take into account Asset Management Plan risk assessment of critical assets and how risks will be

managed (P87)

• SSL align with Asset Management Plan actions required to provide a defined level of service in the most

cost-effective manner. (P88)

• Asset Management Plans should have scenarios that integrate with Long Term Financial Plans that

“show Long-term cash flow predictions for asset operation, maintenance and renewals based on local

knowledge of assets and options for meeting current or improved levels of service and for serving the

projected population”. (P87)

• SSL can be self audited or externally audited by checking alignment with the risk register showing

assets with high residual risk and modern equivalent renewal costs necessary to manage residual risk to

acceptable levels. This provides a base level of BTS. Council may have scenarios with aspirational

targets in the Asset Management Plan, but decide in consultation with the community that these

aspirational targets are not affordable. Unaffordable aspirational targets are not backlog, provided risk

is managed and communicated.

• Integrated Planning and Reporting Manual for local government in NSW MARCH 2013. Premier & Cabinet - Division of Local Government

Resource Material

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 99

• Integrated Planning and Reporting Manual for local government in NSW MARCH 2013. Premier & Cabinet - Division of Local Government

• International Infrastructure Management Manual (IIMM). Institute of Public Works

Engineering Australasia (IPWEA)– Nov 2011

• IPWEA NAMPLUS Advanced Risk Register Template

• IPWEA NAMSPLUS Asset Management Plan Template

Part 2Key Concept

Required Annual Maintenance

Resource Material

• Cost of unfunded maintenance needed to manage increased risk resulting from deferred renewal. The

risk register should include an option to discontinue the service as an alternative means of managing

risk.

• Audited by link to Risk Register – Assets with high residual risk due for Renewal but not funded. Cost

to maintain at satisfactory is unfinanced maintenance treatment option if renewal is not funded.

• Risks will increase the longer renewal deferred and the risk register should be reviewed annually.

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 1010

• IPWEA NAMSPLUS Asset Management Plan Template

Part 2

Resource Material

Example

(NAMSPLUS –Asset Management Plan Figure 7)

This shows all assets due for renewal from the Asset Register.

It should take into account service levels, risk, condition, and

modern equivalent renewal cost the component level.

This is often considered as BTS or “backlog”

• This example uses IPWEA NAMSPLUS3. All NSW Councils have had access to NAMSPLUS and training

programs were run by JRA for IPWEA over a 2 year period under the capacity building program with assistance

of Commonwealth Government National Asset Management Framework.

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 1111

• IPWEA NAMSPLUS Asset Management Plan Template

Part 2

Resource Material

Example (NAMSPLUS –Asset Management Plan Figure 7)

This shows all assets due for renewal from the Asset Register.

It should take into account service levels, risk, condition, and

modern equivalent renewal cost the component level.

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 12

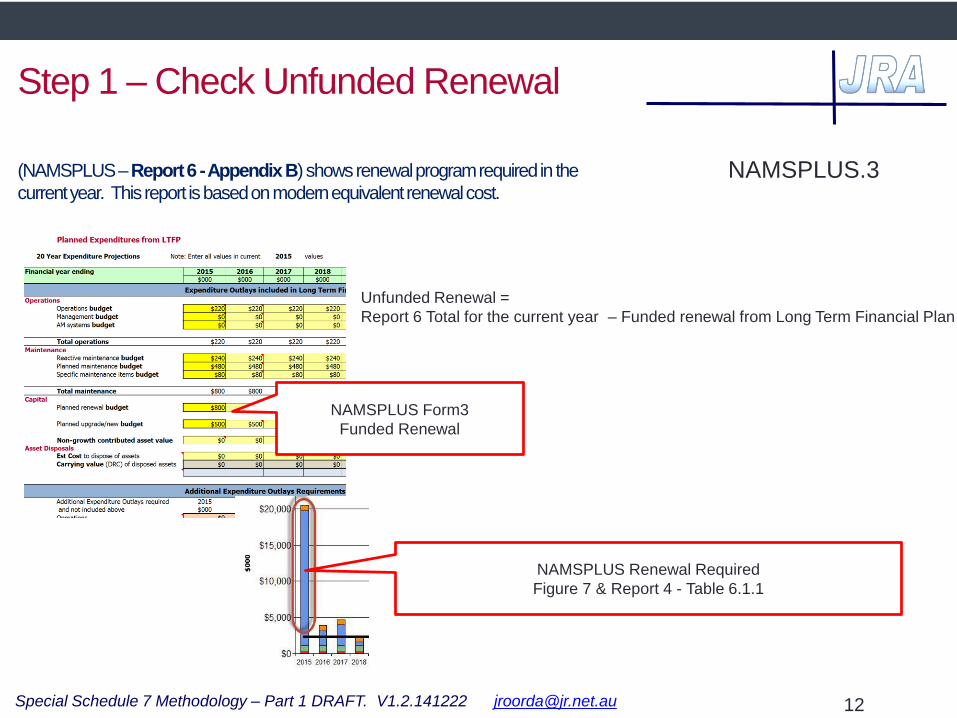

(NAMSPLUS –Report 6 -Appendix B) shows renewal program required in the

current year. This report is based on modern equivalent renewal cost.

Step 1 – Check Unfunded Renewal

NAMSPLUS.3

Unfunded Renewal =

Report 6 Total for the current year – Funded renewal from Long Term Financial Plan

NAMSPLUS Form3

Funded Renewal

NAMSPLUS Renewal Required

Figure 7 & Report 4 - Table 6.1.1

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 13

(NAMSPLUS – Risk Register Template and Risk Section

in AMP)

Step 2 – Identify High Residual Risk

NAMSPLUS.3

Risk Types

• Injury

• Service Interruption

• Reputation

• Environment

• Financial

Asset Register - Total Assets with zero remaining life in 2014

15,409,875Total Due from Asset Register

15,342,875Asset Life too short - needs to be re assessed

17,000High Risk - unfunded and due in 2014

50,000

Low Risk - deferring renewal will not have material risk or service level

consequence

What proportion of unfunded

renewal has high residual risk ?

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 14

(NAMSPLUS – Risk Register Template and Risk Section

in AMP)

Step 3 – Bring to Satisfactory (BTS)

NAMSPLUS.3

BTS = Total of unfunded renewal with

high residual risk from Risk Register

(Risk Treatment Options A - $17,000

or B $5,000 depending on post

treatment residual risk)

Risk Types

• Injury

• Service Interruption

• Reputation

• Environment

• Financial

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 15

(NAMSPLUS – Risk Register Template and Risk Section

in AMP)

Step 4 – Maintain at Satisfactory (MAS)

NAMSPLUS.3

MAS = Additional maintenance

resulting from deferred renewal

(option C)

Risk Types

• Injury

• Service Interruption

• Reputation

• Environment

• Financial

Special Schedule 7 Methodology – Part 1 DRAFT. V1.2.141222 [email protected] 16

16

Step 5.1 – Add up the modern equivalent component renewal cost and put it

in the SS7 cost to bring to satisfactory

Step 5.2 – Option C in a NAMSPLUS risk register is additional maintenance -

add that up and add to current budget and put in SS7 maintenance column.

Step 5.3 – Review and update AMP using S2 – form 2A if steps 1-3 show a

problem with the register (lives too long or short, cost too high or low)

AMP RMP and SS7 are now in alignment – and auditable.

(NAMSPLUS – Form 3

Step 5 – Align AMP and SS7