A-123, Appendix A - Internal Controls Over Financial ... · A-123, Appendix A - Internal Controls...

30

A-123, Appendix A - Internal Controls Over Financial Statements and Reporting Presented to: AGA-Kansas City Chapter Professional Development Seminar April 17, 2013 Michael A. Fiene USDA-FSA Internal Control & Planning Office (ICPO)

Transcript of A-123, Appendix A - Internal Controls Over Financial ... · A-123, Appendix A - Internal Controls...

A-123, Appendix A - Internal Controls Over

Financial Statements and Reporting

Presented to:

AGA-Kansas City Chapter

Professional Development Seminar

April 17, 2013

Michael A. Fiene

USDA-FSA

Internal Control & Planning Office

(ICPO)

Agenda

•Background: OMB Circular A-123, Appendix A

•Background: Commodity Credit Corporation (CCC)

and Farm Service Agency (FSA)

•Assessing Risks and Optimizing Controls and Testing

•Reconciliations & Account Analysis: “Always a Key

Control”

•Monitoring

2

BACKGROUND:

A-123, APPENDIX A

3

OMB Circular A-123, Appendix A, Internal Control

Over Financial Reporting

Statement of Assurance for Internal Control over Financial

Reporting. Management is required to provide a separate

assurance over the effectiveness of the internal controls over

financial reporting. This assurance is a subset of the overall

Statement of Assurance and is based on the results of

management’s assessment conducted in accordance with the

requirements in Appendix A. Refer to Appendix A Section V.

Management’s Assurance Statement on Internal Control over

Financial Reporting for a further discussion.

4

SOX for the Federal Government

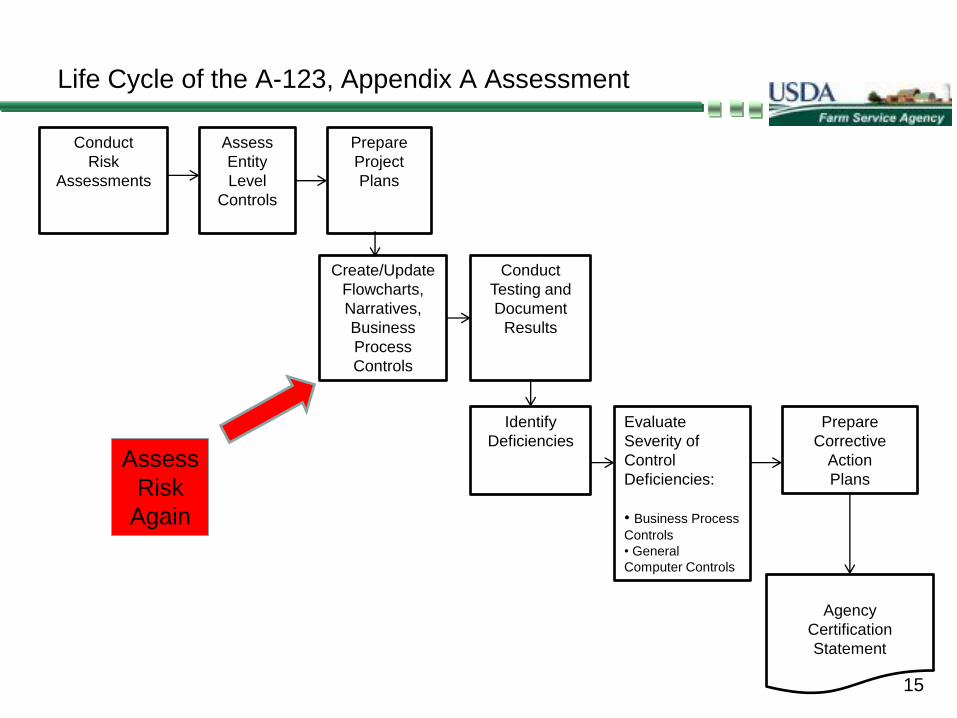

Life Cycle of the A-123, Appendix A Assessment

Conduct

Risk

Assessments

Assess

Entity

Level

Controls

Prepare

Project

Plans

Create/Update

Flowcharts,

Narratives,

Business

Process

Controls

Conduct

Testing and

Document

Results

Identify

Deficiencies

Prepare

Corrective

Action

Plans

Agency

Certification

Statement

Evaluate

Severity of

Control

Deficiencies:

• Business Process

Controls

• General

Computer Controls

5

ICPO Mission Statement

In accordance with OMB Circular A-123, Appendix A, we:

• support the FSA and CCC statements of assurance over

financial reporting by monitoring, testing and reporting on FSA’s

and CCC’s internal controls over financial reporting

•Promote and support effective and efficient financial statement

and financial related audits

•Assist in building, promoting and sustaining a comprehensive

and effective control environment over financial reporting.

6

BACKGROUND:

COMMODITY CREDIT CORP. (CCC)

&

FARM SERVICE AGENCY (FSA)

7

Background: CCC and FSA

CCC and FSA Mission Statement

•Stabilize, support and protect farm incomes and prices

•Conserve soil, air and water resources and protect and

improve wildlife habitats

•Maintain balanced and adequate supplies of agricultural

commodities and aiding in their orderly distribution

•Develop new domestic and foreign markets and marketing

facilities for agricultural commodities

8

Background: CCC and FSA

As of September 30, 2012

Item

CCC

(In Millions)

FSA

(In Millions)

Total Budget Authority $23,254 $7,605

Gross Outlays $19,075 $5,325

Loan Portfolio (Gross) $6,510 $8,089

Net Cost of Operations $9,725 $2,226

9

Background

Assessable Entities and Business Cycles

CORE G/L

Funds

Management

Funds

Control

Financial

Reporting

Commodity

Loans

Producer

Payments

Cr. Mngt.

Direct Loans

PL-480

Cr. Mngt.

Guar. Loans

GSM

Farm

Storage

Facility Loans

Commodity

Procurement

(WBSCM)

Tobacco

Transition

Payment Prog.

Revenue &

Receivables

Management

FMMI

G/L

CORE

G/L PLAS

(FLP) G/L

Funds Management

Funds Control

Financial Reporting

HR

Management

Reimbursable

Agreements

Producer

Payments Cr. Mngt.

Direct Loans

Cr. Mngt.

Guar. Loans

CCC (26 Funds) FSA (55 Funds)

10

Reimbursable

Agreements $403 M

$714 M

$4,470 M

$923 M $7,951M

$138 M

Total Loan Portfolio = $6,510 M

Total Loan Portfolio = $8,089 M

ASSESSING RISKS

&

OPTIMIZING CONTROLS

&

TESTING

11

Optimizing Controls and Testing Approach

•Optimizing Controls: Identifying and testing those

controls that address the risks most significant to our

financial reporting

•Risk assessment at the individual risk level (A-123)

•“Not all risks are created equal”

•“Doing less with less”

12

13

Low Risk

14

High Risk

Life Cycle of the A-123, Appendix A Assessment

Conduct

Risk

Assessments

Assess

Entity

Level

Controls

Prepare

Project

Plans

Create/Update

Flowcharts,

Narratives,

Business

Process

Controls

Conduct

Testing and

Document

Results

Identify

Deficiencies

Prepare

Corrective

Action

Plans

Agency

Certification

Statement

Evaluate

Severity of

Control

Deficiencies:

• Business Process

Controls

• General

Computer Controls

15

Assess

Risk

Again

16

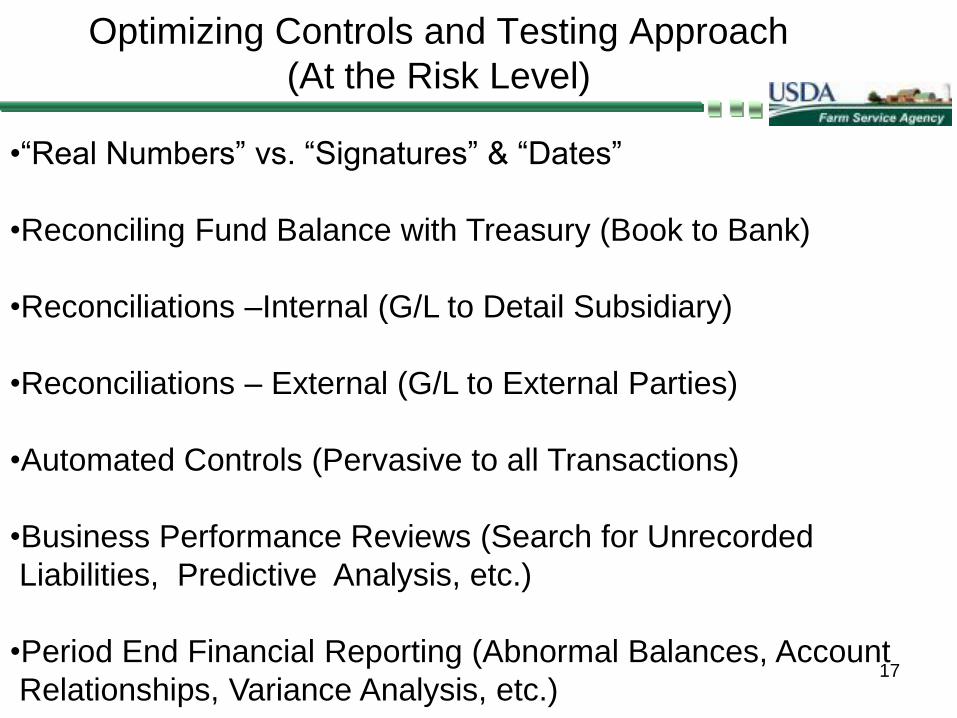

Optimizing Controls and Testing Approach

(At the Risk Level)

•“Real Numbers” vs. “Signatures” & “Dates”

•Reconciling Fund Balance with Treasury (Book to Bank)

•Reconciliations –Internal (G/L to Detail Subsidiary)

•Reconciliations – External (G/L to External Parties)

•Automated Controls (Pervasive to all Transactions)

•Business Performance Reviews (Search for Unrecorded

Liabilities, Predictive Analysis, etc.)

•Period End Financial Reporting (Abnormal Balances, Account

Relationships, Variance Analysis, etc.)

17

Optimizing Controls and Testing Approach

“Real Numbers” vs. “Signatures” & “Dates”

Trial Balances (tied to Financial Statements)

18

ACCOUNT RECONCILIATIONS

& ANALYSIS

“ALWAYS A KEY CONTROL”

19

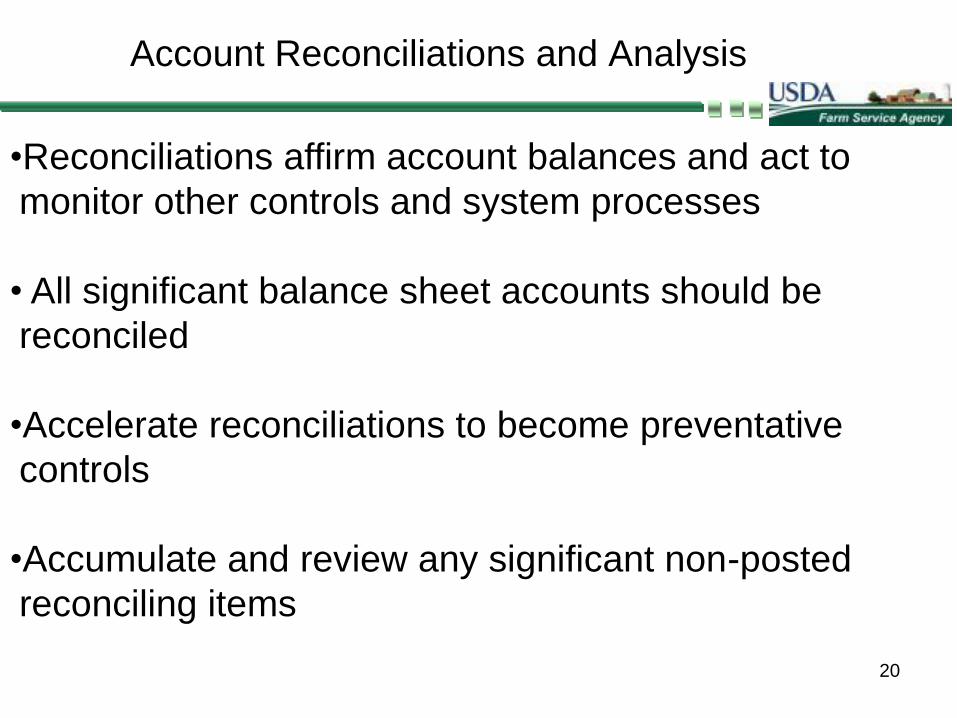

Account Reconciliations and Analysis

•Reconciliations affirm account balances and act to

monitor other controls and system processes

• All significant balance sheet accounts should be

reconciled

•Accelerate reconciliations to become preventative

controls

•Accumulate and review any significant non-posted

reconciling items

20

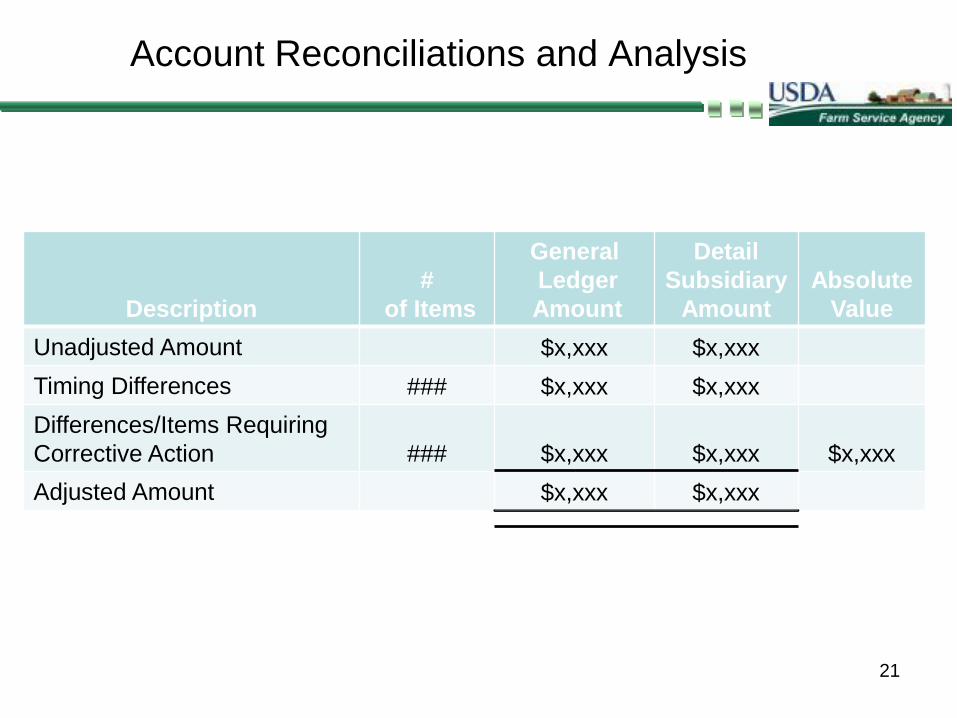

Account Reconciliations and Analysis

21

Description

#

of Items

General

Ledger

Amount

Detail

Subsidiary

Amount

Absolute

Value

Unadjusted Amount $x,xxx $x,xxx

Timing Differences ### $x,xxx $x,xxx

Differences/Items Requiring

Corrective Action ### $x,xxx $x,xxx $x,xxx

Adjusted Amount $x,xxx $x,xxx

Account Reconciliations and Analysis

•Account analysis affirm account balances and act to

monitor other controls and system processes

• Examples:

•Account Relationships (Bud = Prop)

•Abnormal Account Balances

•Variance Analysis

•Predictive Analysis

22

MONITORING

23

Monitoring

•A-123 Internal Control Standards (COSO):

•Control Environment

•Risk Assessment

•Control Activities

•Information and Communication

•Monitoring

24

Monitoring

•Ongoing Monitoring

Occurs when the routine operations of an

organization provides feedback to those

responsible for the effectiveness of the internal

control system

•Separate Evaluations

Designed to evaluate controls periodically and are

not ingrained in the routine operations of the

organization

25

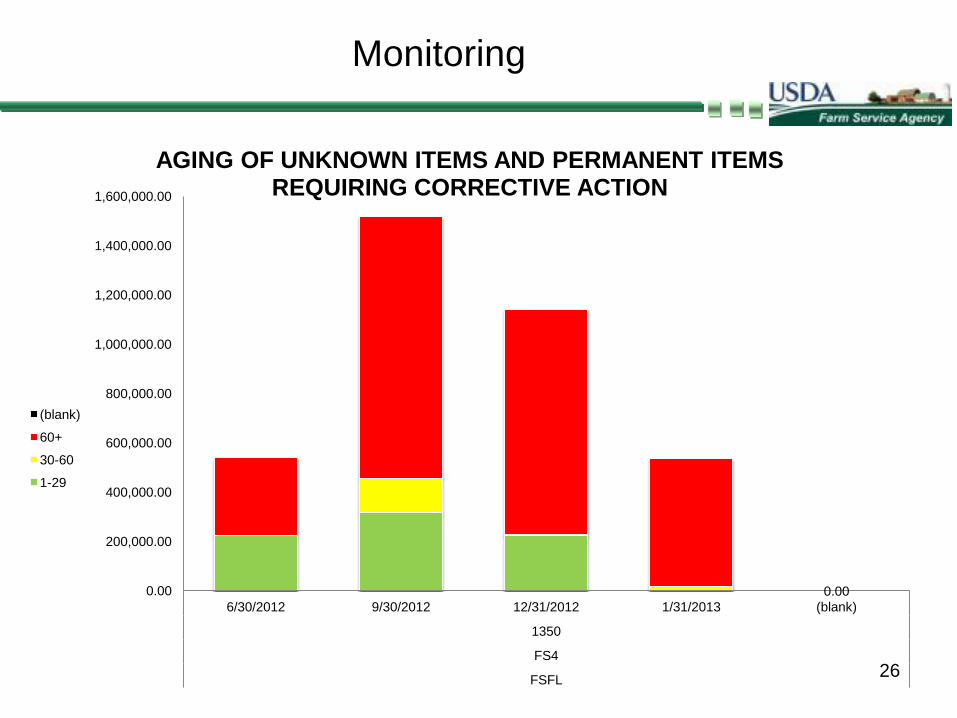

Monitoring

26

0.00 0.00

200,000.00

400,000.00

600,000.00

800,000.00

1,000,000.00

1,200,000.00

1,400,000.00

1,600,000.00

6/30/2012 9/30/2012 12/31/2012 1/31/2013 (blank)

1350

FS4

FSFL

AGING OF UNKNOWN ITEMS AND PERMANENT ITEMS REQUIRING CORRECTIVE ACTION

(blank)

60+

30-60

1-29

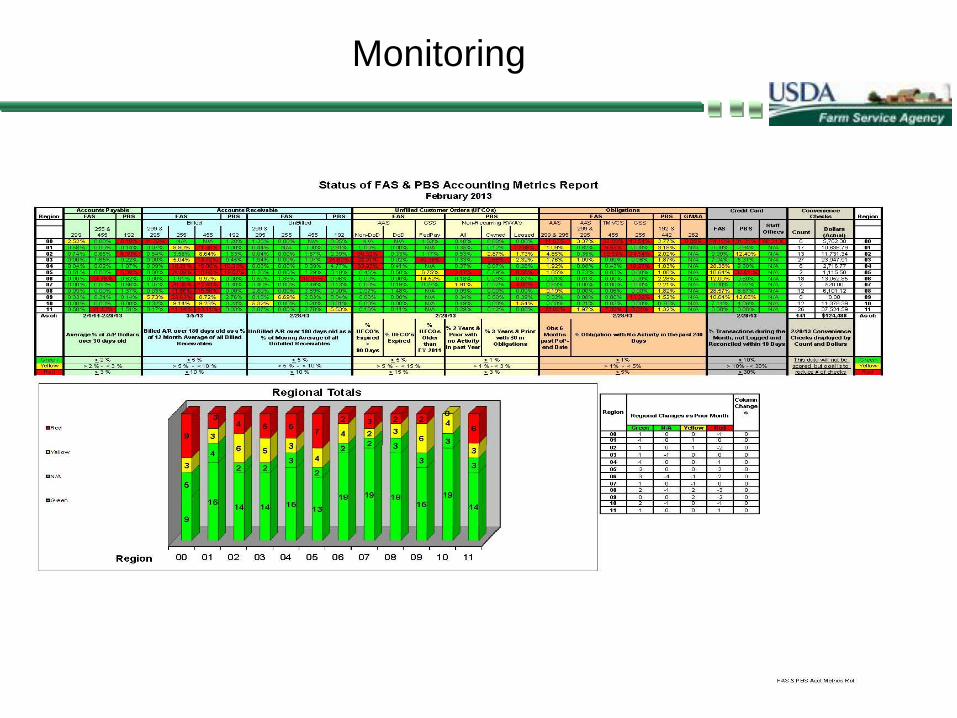

Monitoring

27

$-

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

Cash Reconciliation

Monitoring

28

Monitoring

29

“Monitoring promotes good control operation. When people who are

responsible for internal control know their work is subject to oversight

through monitoring, they are more likely to perform their duties properly

over time.”

COSO Guidance on Monitoring Internal Control Systems,

January, 2009

QUESTIONS?

30

Office: (816) 823-2833

Cell: (816) 719-4518