8:1 CONFORMING FIXED RATE - BB&T · PDF file8:1 CONFORMING FIXED RATE LOAN PRODUCT ......

34

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives. CONFORMING FIXED RATE 4/30/2018 8:1 CONFORMING FIXED RATE LOAN PRODUCT CODES LOAN PRODUCT LOAN TERM/AMORTIZATION* 101 30 Year Fixed Rate 241- 360 months 104 20 Year Fixed Rate 181- 240 months 102 15 Year Fixed Rate 121- 180 months 110 10 Year Fixed Rate 120 months *Minimum Amortization Term- 120 months Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming and the Conforming Underwriting Guidelines section for additional information. ****************************************************************************************************************************** APPRAISALS BB&T will accept the form required by the LPA or DU response with the following limitations. The following are not allowed regardless of DU recommendation: • DU- Forms 2055, 2075, and 1075 ASSUMABILITY Not assumable CERTIFICATIONS Primary Residence and Second Home: Qualified Mortgage (QM), Higher-Priced (HPML) and High Cost (HCL) Mortgage Loan Certification or comparable form that validates QM status, HPML and HCL. BB&T does not purchase high cost loans. CREDIT SCORE Minimum Credit Score for Purchase and No Cash Out Refinance transactions: 620 Minimum Credit Score for Cash-Out Refinance transactions: 620 Reference the Price Adjustments and LTV Charts for minimum credit score requirements on specific product/loan types. Eligibility Requirements – Not all Borrowers have Usable Credit Scores Freddie Mac Loan Product Advisor (LPA) Requirements for Accept: • At least one Borrower on the transaction has a usable Credit Score, as determined by LPA, which meets BB&T Correspondent Lending minimum credit score requirements. • The transaction is a purchase or “no cash-out” refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their Primary Residence. • Borrowers with a usable Credit Score contribute more than 50% of the total monthly income. • Conforming loan amounts are eligible. • A-Minus mortgages are ineligible for delivery to BB&T Correspondent Lending.

Transcript of 8:1 CONFORMING FIXED RATE - BB&T · PDF file8:1 CONFORMING FIXED RATE LOAN PRODUCT ......

BB&T Internal The information in this document is the property of BB&T and is intended for the use of

BB&T associates and authorized representatives. CONFORMING FIXED RATE 4/30/2018

8:1 CONFORMING FIXED RATE LOAN PRODUCT CODES

LOAN PRODUCT

LOAN TERM/AMORTIZATION*

101 30 Year Fixed Rate 241- 360 months 104 20 Year Fixed Rate 181- 240 months 102 15 Year Fixed Rate 121- 180 months 110 10 Year Fixed Rate 120 months

*Minimum Amortization Term- 120 months Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming and the Conforming Underwriting Guidelines section for additional information. ****************************************************************************************************************************** APPRAISALS BB&T will accept the form required by the LPA or DU response with the following limitations.

The following are not allowed regardless of DU recommendation:

• DU- Forms 2055, 2075, and 1075

ASSUMABILITY Not assumable CERTIFICATIONS Primary Residence and Second Home: Qualified Mortgage (QM), Higher-Priced (HPML) and High Cost (HCL) Mortgage Loan Certification or comparable form that validates QM status, HPML and HCL. BB&T does not purchase high cost loans. CREDIT SCORE Minimum Credit Score for Purchase and No Cash Out Refinance transactions: 620 Minimum Credit Score for Cash-Out Refinance transactions: 620

Reference the Price Adjustments and LTV Charts for minimum credit score requirements on specific product/loan types. Eligibility Requirements – Not all Borrowers have Usable Credit Scores Freddie Mac Loan Product Advisor (LPA) Requirements for Accept:

• At least one Borrower on the transaction has a usable Credit Score, as determined by LPA, which meets BB&T Correspondent Lending minimum credit score requirements.

• The transaction is a purchase or “no cash-out” refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their

Primary Residence. • Borrowers with a usable Credit Score contribute more than 50% of the total monthly income. • Conforming loan amounts are eligible. • A-Minus mortgages are ineligible for delivery to BB&T Correspondent Lending.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of

BB&T associates and authorized representatives. CONFORMING FIXED RATE 4/30/2018

Fannie Mae Desktop Underwriter (DU) Requirements for DU Approve/Eligible Mortgages:

• At least one Borrower on the transaction has a usable Credit Score, as determined by DU, which meets BB&T Correspondent Lending minimum credit score requirements.

• The transaction is a purchase or limited cash-out refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their

Primary Residence. • Conforming loan amounts are eligible. • Borrowers with a usable Credit Score contribute more than 50% of the qualifying income. • Reserves may be required as determined by DU.

Rescoring and Credit Repair • Legitimate corrections to a borrower’s credit profile are acceptable, i.e. John Doe Jr.’s derogatory credit is

reflected on John Doe Sr.’s credit report.

• In order to ensure the accuracy of the information, corrections should be made at the credit repository level.

• Any supporting documentation sent to the credit repositories along with all copies of credit reports should be maintained in the Correspondent’s loan file and included with the file submission when delivered to BB&T Correspondent Lending.

The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower’s credit profile to improve credit scores for purposes of loan eligibility, rate/price improvement and creditworthiness is expressly prohibited by BB&T Correspondent Lending.

It is at BB&T Correspondent Lending’s discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements. DEBT-TO-INCOME RATIO (DTI) LPA- Maximum DTI must not exceed 55% DU- Maximum DTI must not exceed 50% ESCROW WAIVER Permitted when the Loan to Value is 80% or less. There is a reduction in Servicing Released Premium for waiving escrows. Refer to BB&T’s current Rate Sheet HOMEOWNERSHIP COUNSELING DISCLOSURE Homeownership Counseling Disclosure required per the 2013 HOEPA Rule, an amendment to Regulation X (RESPA). INELIGIBLE LOAN TYPES AND PROGRAMS LPA Caution A-Minus Eligible Downpayment Assistance Programs Properties subject to Property Assessed Clean Energy (PACE) Obligations LOAN PURPOSE Purchase No Cash-Out Refinance Cash-Out Refinance

BB&T Internal The information in this document is the property of BB&T and is intended for the use of

BB&T associates and authorized representatives. CONFORMING FIXED RATE 4/30/2018

LTV Reference the Price Adjustments and LTV Charts MAXIMUM INTERESTED PARTY CONTRIBUTIONS Maximum financing concessions are based on TLTV when secondary financing is present, LTV when no secondary financing is present.

OCCUPANCY LTV/TLTV AMOUNT Primary Residence Over 90% to 95% 3%

Over 75% to 90% 6% 75% and below 9%

Second Home Over 75% to 85% 6% 75% and below 9%

Investment Property All LTV’s 2% MAXIMUM LOAN AMOUNT Conforming Loan Amount Maximum MINIMUM LOAN AMOUNT None MORTGAGE INSURANCE Required on all loans with LTV’s above 80%. Refer to “Mortgage Insurance Options” in the Conforming Underwriting Guidelines section for more information. NOTE Freddie Mac 3200

Unit Number must be included in the property address line.

Refer to Legal Document Matrix for additional information. OCCUPANCY REQUIREMENTS Primary Residence Second Home Investment Property OVERLAYS Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming for additional information. POINTS AND FEES CAPS

• 3% of the total loan amount for a loan amount greater than or equal to $105,158 • $3,155 for a loan amount greater than or equal to $63,095 but less than $105,158 • 5% of the total loan amount for a loan greater than or equal to $21,032 but less than $63,095 • $1,052 for a loan amount greater than or equal to $13,145 but less than $21,032 • 8% of the total loan amount for a loan less than $13,145

PRICING Refer to the Rate Sheet and BB&T’s current Price Adjustments and LTV Charts for any price adjustments that might be applicable.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of

BB&T associates and authorized representatives. CONFORMING FIXED RATE 4/30/2018

PROPERTY TYPES Primary Residence and Investment Property- 1-4 Family, Freddie Mac Eligible Condominiums, PUDs Second Home- 1-Family, Freddie Mac Eligible Condominiums, PUDs Attached PUDs Property Insurance requirements:

• HO3/comparable full coverage homeowners insurance policy; OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit

to its condition prior to a loss claim event for attached PUDs where the homeowners association has a blanket policy covering the exterior structure only; OR

• Homeowners Association blanket policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if blanket policy covers the exterior and interior of the

unit. • HO3/comparable full coverage policies will be escrowed.

Condominiums Correspondents are responsible for classing Condominiums as outlined in the Conforming Underwriting Guidelines. Property Insurance requirements:

• HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its condition prior to a loss claim event for Condominiums where the condominium master policy covers the exterior structure only; OR

• Condominium master policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if master policy covers the exterior and interior of the

unit. Ineligible Property Types Manufactured Housing QM STATUS Safe Harbor: Mortgage that does not exceed limits on upfront points and fees; has an APR relative to the APOR that is equal to or less than 1.5% for first-lien loans. Rebuttable Presumption: Mortgage than does not exceed limits on upfront points and fees; has an APR that exceeds the APOR as of the date the interest rate is set by 1.5% or more for first-lien loans. Also known as “Higher-Priced”. REFINANCES Refer to Freddie Mac Seller/Servicer Guide, as well as BB&T’s current Price Adjustments and LTV Charts and the Conforming Underwriting Guidelines section. RESIDENCY STATUS US Citizens Permanent Resident Alien Non-Permanent Resident Alien – see eligible Visa types listed in Conforming Underwriting Guidelines. SECONDARY FINANCING Refer to BB&T’s current Price Adjustments and LTV Charts and the Conforming Underwriting Guidelines section.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of

BB&T associates and authorized representatives. CONFORMING FIXED RATE 4/30/2018

SECURITY INSTRUMENT Use the applicable Freddie Mac/Fannie Mae security instrument for the state in which the property is located. TEMPORARY BUYDOWNS Not Allowed UNDERWRITING BB&T expects that all eligible Conforming loans will be submitted to Loan Product Advisor or Desktop Underwriter (either directly or through a MI Company). Ineligible feedback responses: LPA Caution A-Minus eligible, LPA Caution, or DU Refer with Caution. WORKSHEETS Points and Fees Worksheet or comparable form Ability to Repay Worksheet or comparable form OR

• Income calculation for each borrower on either the Transmittal Summary or on a separate form; AND • Income and debt amounts must match on the Transmittal Summary, final application and final AUS

submission; AND • Total debt-to-income ratio on the Transmittal Summary and final AUS submission must match.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

CONFORMING 3/1, 5/1, 7/1, AND 10/1 P&I LIBOR ARMS 4/30/2018

8:2 CONFORMING 3/1, 5/1, 7/1, AND 10/1 LIBOR P&I ARMS

LOAN PRODUCT CODES

LOAN PRODUCT

340 3/1 Year Discounted or Premium Non-Convertible ARM with 2/2/5 Caps 144 5/1 Year Discounted or Premium Non-Convertible ARM with 2/2/5 Caps 375 7/1 Year Discounted or Premium Non-Convertible ARM with 5/2/5 Caps 376 10/1 Year Discounted or Premium Non-Convertible ARM with 5/2/5 Caps

Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming and the Conforming Underwriting Guidelines section for additional information. ******************************************************************************************************************************** ADDITIONAL DISCLOSURES

PRODUCT LIBOR-INDEXED ADJUSTABLE RATE MORTGAGE LOAN PROGRAM DISCLOSURE

340 3/1 Year Discounted or Premium Non-Convertible ARM with 2/2/5 Caps 144 5/1 Year Discounted or Premium Non-Convertible ARM with 2/2/5 Caps 375 7/1 Year Discounted or Premium Non-Convertible ARM with 5/2/5 Caps 376 10/1 Year Discounted or Premium Non-Convertible ARM with 5/2/5 Caps

Note: Use the Discounted disclosure if the Note rate is less than the index plus margin. Note: Use the Premium disclosure if the Note rate is equal to or greater than the index plus margin. The Consumer Handbook on Adjustable Rate Mortgages must be given to the borrower at application along with the applicable disclosure as indicated above. APPRAISALS BB&T will accept the form required by the LPA or DU response except for the following limitations. The following are not allowed regardless of DU recommendation:

• DU - Forms 2055, 2075, and 1075 ASSUMABILITY 3/1 ARM- assumable during life of loan 5/1, 7/1 & 10/1 ARMs- assumable while in the adjustable phase, not assumable during fixed hybrid period. CERTIFICATIONS Primary Residence and Second Home: Qualified Mortgage (QM), Higher-Priced (HPML) and High Cost (HCL) Mortgage Loan Certification or comparable form that validates QM status, HPML and HCL. BB&T does not purchase high cost loans. CREDIT SCORE Minimum Credit Score for Purchase and No Cash Out Refinance transactions: 620 Minimum Credit Score for Cash-Out Refinance transactions: 620 Reference the Price Adjustments and LTV Charts for minimum credit score requirements on specific product/loan types.

(Continued On Next Page)

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

CONFORMING 3/1, 5/1, 7/1, AND 10/1 P&I LIBOR ARMS 4/30/2018

Eligibility Requirements – Not all Borrowers have Usable Credit Scores

Freddie Mac Loan Product Advisor (LPA) Requirements for Accept:

• At least one Borrower on the transaction has a usable Credit Score, as determined by LPA, which meets BB&T Correspondent Lending minimum credit score requirements.

• The transaction is a purchase or “no cash-out” refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their Primary

Residence. • Borrowers with a usable Credit Score contribute more than 50% of the total monthly income. • Conforming loan amounts are eligible. • A-Minus mortgages are ineligible for delivery to BB&T Correspondent Lending.

Fannie Mae Desktop Underwriter (DU) Requirements for DU Approve/Eligible Mortgages:

• At least one Borrower on the transaction has a usable Credit Score, as determined by DU, which meets BB&T Correspondent Lending minimum credit score requirements.

• The transaction is a purchase or limited cash-out refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their Primary

Residence. • Conforming loan amounts are eligible. • Borrowers with a usable Credit Score contribute more than 50% of the qualifying income. • Reserves may be required as determined by DU.

Rescoring and Credit Repair • Legitimate corrections to a borrower’s credit profile are acceptable, i.e. John Doe Jr.’s derogatory credit is

reflected on John Doe Sr.’s credit report. • In order to ensure the accuracy of the information, corrections should be made at the credit repository level.

• Any supporting documentation sent to the credit repositories along with all copies of credit reports should be

maintained in the Correspondent’s loan file and included with the file submission when delivered to BB&T Correspondent Lending.

The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower’s credit profile to improve credit scores for purposes of loan eligibility, rate/price improvement and creditworthiness is expressly prohibited by BB&T Correspondent Lending. It is at BB&T Correspondent Lending’s discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements. DEBT-TO-INCOME RATIO (DTI) LPA - maximum DTI must not exceed 55% DU - maximum DTI must not exceed 50% ESCROW WAIVER Permitted when the Loan to Value is 80% or less. There is a reduction in Servicing Released Premium for waiving escrows Refer to BB&T’s current Rate Sheet or SRP Schedule. HOMEOWNERSHIP COUNSELING DISCLOSURE Homeownership Counseling Disclosure required per the 2013 HOEPA Rule, an amendment to Regulation X (RESPA).

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

CONFORMING 3/1, 5/1, 7/1, AND 10/1 P&I LIBOR ARMS 4/30/2018

INDEX 12 Month LIBOR index INELIGIBLE LOAN TYPES AND PROGRAMS LPA Caution A-Minus Eligible Downpayment Assistance Programs Properties subject to Property Assessed Clean Energy (PACE) Obligations INTEREST RATE ADJUSTMENTS The “Initial Interest Rate Adjustment” will be 36, 60, 84, 120 months after the first month following loan closing; thereafter, the Interest Rate will be subject to change annually. For loans which close on the first day of the month, the Initial Interest Rate Adjustment will be 36, 60, 84, 120 months after the month of loan closing; thereafter, the Interest Rate will be subject to change annually. INTEREST RATE CAPS & FLOOR

CAP 3/1 AND 5/1 P&I LIBOR ARM 7/1 AND 10/1 P&I LIBOR ARMs Initial 2% (Increase or Decrease) 5% (Increase or Decrease)

Annual 2% (Increase or Decrease) 2% (Increase or Decrease) Lifetime 5% 5%

Margin of 2.25% is the Floor INTEREST RATE FORMULA Index plus margin rounded to the nearest .125%. LOAN PURPOSE Purchase No Cash-Out Refinance Cash-Out Refinance LOAN TERM/AMORTIZATION TERM Amortization terms 181-360 months (15 years, 1 month to 30 years). The outstanding principal balance will be re-amortized over the remaining life of the loan at each interest rate change date. NOTE: Amortization terms below 181 months for Adjustable-rate products are NOT allowed. LTV/TLTV/HTLTV Reference the Price Adjustments and LTV Charts MARGIN 225 basis points (2.25%) MAXIMUM INTERESTED PARTY CONTRIBUTIONS Maximum financing concessions are based on TLTV when secondary financing is present, LTV when no secondary financing is present.

OCCUPANCY LTV/TLTV AMOUNT Primary Residence Over 90% to 95% 3%

Over 75% to 90% 6% 75% and below 9%

Second Home Over 75% to 85% 6% 75% and below 9%

Investment Property All LTV’s 2%

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

CONFORMING 3/1, 5/1, 7/1, AND 10/1 P&I LIBOR ARMS 4/30/2018

MAXIMUM LOAN AMOUNT Conforming Loan Amount Maximum MINIMUM LOAN AMOUNT None MORTGAGE INSURANCE Required on all loans with LTV’s above 80%. Refer to “Mortgage Insurance Options” in the Conforming Underwriting Guidelines section for more information. NEGATIVE AMORTIZATION None NOTE

PRODUCT FREDDIE MAC FANNIE MAE 340 5530 3526

144, 375, 376 5531 3528 Unit Number must be included in the property address line. Refer to Legal Document Matrix for additional information. OCCUPANCY REQUIREMENTS Primary Residence Second Home Investment Property OVERLAYS Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming for additional information. PAYMENT ADJUSTMENT The initial payment adjustment will be not less than 36, 60, 84, 120 months from the date of the first payment; thereafter, the monthly payment to change annually. POINTS AND FEES CAPS

• 3% of the total loan amount for a loan amount greater than or equal to $105,158 • $3,155 for a loan amount greater than or equal to $63,095 but less than $105,158 • 5% of the total loan amount for a loan greater than or equal to $21,032 but less than $63,095 • $1,052 for a loan amount greater than or equal to $13,145 but less than $21,032 • 8% of the total loan amount for a loan less than $13,145

PRICING Refer to the Rate Sheet and BB&T’s current Price Adjustments and LTV Charts for any price adjustments for any applicable price adjustments

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

CONFORMING 3/1, 5/1, 7/1, AND 10/1 P&I LIBOR ARMS 4/30/2018

PROPERTY TYPES Primary Residence and Investment Property- 1-4 Family, Freddie Mac Eligible Condominiums, PUDs Second Home- 1-Family, Freddie Mac Eligible Condominiums, PUDs Attached PUDs Property Insurance requirements:

• HO3/comparable full coverage homeowners insurance policy; OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to

its condition prior to a loss claim event for attached PUDs where the homeowners association has a blanket policy covering the exterior structure only; OR

• Homeowners Association blanket policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if blanket policy covers the exterior and interior of the

unit. • HO3/comparable full coverage policies will be escrowed.

Condominiums Correspondents are responsible for classing Condominiums as outlined in the Conforming Underwriting Guidelines. Property Insurance requirements:

• HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its condition prior to a loss claim event for Condominiums where the condominium master policy covers the exterior structure only; OR

• Condominium master policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if master policy covers the exterior and interior of the

unit. Ineligible Property Types Manufactured Housing . QM STATUS Safe Harbor: Mortgage that does not exceed limits on upfront points and fees; has an APR relative to the APOR that is equal to or less than 1.5% for first-lien loans. Rebuttable Presumption: Mortgage than does not exceed limits on upfront points and fees; has an APR that exceeds the APOR as of the date the interest rate is set by 1.5%. Also known as “Higher-Priced”. QUALIFYING RATE*

3/1 & 5/1 P&I LIBOR ARM Qualify at the greater of*: • Note rate plus 2.0% or • Fully indexed rate (index plus margin)

7/1 & 10/1 P&I LIBOR ARMs Qualify at note rate 7/1 & 10/1 P&I LIBOR ARMs Higher Priced Covered Transactions as defined by Reg Z 12 C.F.R. 1026.43(b) Qualify at the greater of: • Note rate or • Fully indexed rate (index plus margin)

*Correspondents must adhere to specific State requirements.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

CONFORMING 3/1, 5/1, 7/1, AND 10/1 P&I LIBOR ARMS 4/30/2018

Qualifying Rate Requirement for AUS

Fannie Mae DU ARM Plan 3/1 P&I LIBOR ARM – 2723 5/1 P&I LIBOR ARM – 2725 7/1 P&I LIBOR ARM – 2727 10/1 P&I LIBOR ARM – 2729 Freddie Mac LPA Loan Product Advisor will assess the loan and calculate the debt-to-income ratio based on the requirements listed above. REFINANCES Refer to Freddie Mac Seller/Servicer Guide, as well as BB&T’s current Price Adjustments and LTV Charts and the Conforming Underwriting Guidelines section. RESIDENCY STATUS US Citizens Permanent Resident Alien Non-Permanent Resident Alien - see eligible Visa types listed in Conforming Underwriting Guidelines. RIDER

PRODUCT FREDDIE MAC FANNIE MAE 340 5130 3189

144, 375, 376 5131 3187 Refer to Legal Document Matrix for additional information SECONDARY FINANCING Refer to BB&T’s current Price Adjustments and LTV Charts as well as the Conforming Underwriting Guidelines SECURITY INSTRUMENT Use the applicable Freddie Mac/Fannie Mae security instrument for the state in which the property is located. TEMPORARY BUYDOWNS Not Allowed UNDERWRITING BB&T expects that all eligible Conforming loans will be submitted to Loan Product Advisor or Desktop Underwriter (either directly or through a MI Company). Ineligible feedback responses: LPA Caution A-Minus eligible, LPA Caution, or DU Refer with Caution. WORKSHEETS Points and Fees Worksheet or comparable form Ability to Repay Worksheet or comparable form OR

• Income calculation for each borrower on either the Transmittal Summary or on a separate form; AND • Income and debt amounts must match on the Transmittal Summary, final application and final AUS

submission; AND • Total debt-to-income ratio on the Transmittal Summary and final AUS submission must match.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

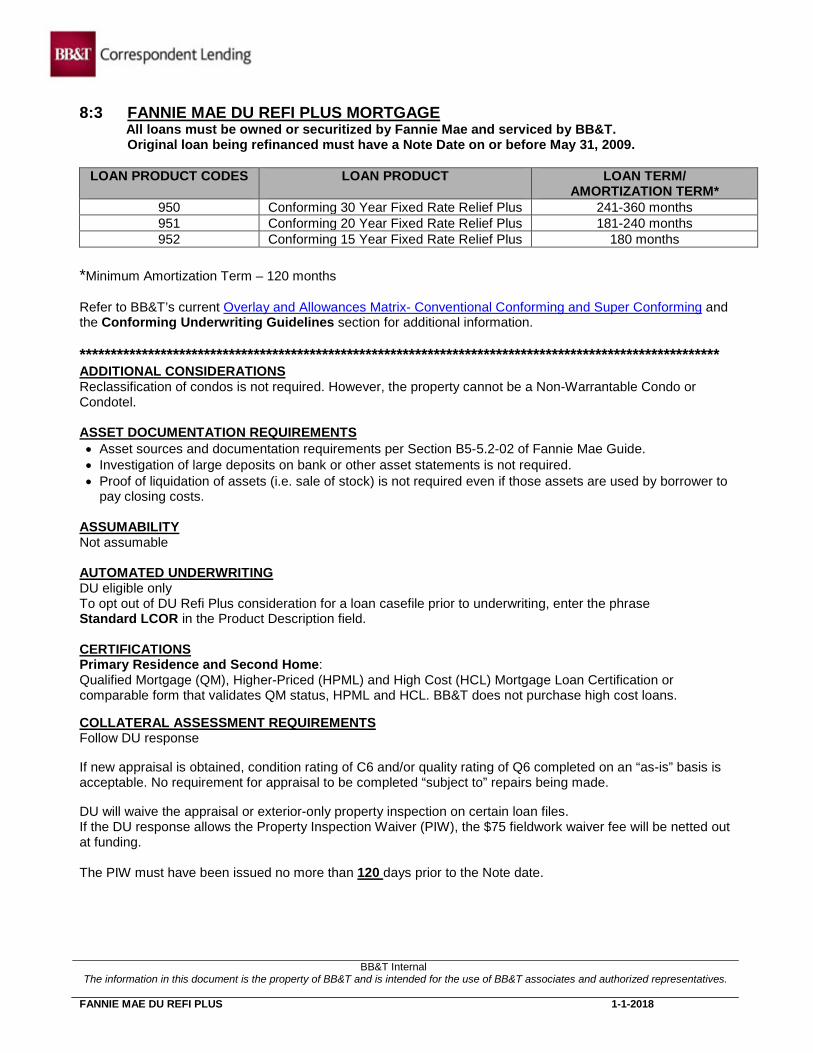

8:3 FANNIE MAE DU REFI PLUS MORTGAGE

All loans must be owned or securitized by Fannie Mae and serviced by BB&T. Original loan being refinanced must have a Note Date on or before May 31, 2009.

LOAN PRODUCT CODES

LOAN PRODUCT

LOAN TERM/

AMORTIZATION TERM* 950 Conforming 30 Year Fixed Rate Relief Plus 241-360 months 951 Conforming 20 Year Fixed Rate Relief Plus 181-240 months 952 Conforming 15 Year Fixed Rate Relief Plus 180 months

*Minimum Amortization Term – 120 months Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming and the Conforming Underwriting Guidelines section for additional information. ******************************************************************************************************* ADDITIONAL CONSIDERATIONS Reclassification of condos is not required. However, the property cannot be a Non-Warrantable Condo or Condotel. ASSET DOCUMENTATION REQUIREMENTS • Asset sources and documentation requirements per Section B5-5.2-02 of Fannie Mae Guide. • Investigation of large deposits on bank or other asset statements is not required. • Proof of liquidation of assets (i.e. sale of stock) is not required even if those assets are used by borrower to

pay closing costs. ASSUMABILITY Not assumable AUTOMATED UNDERWRITING DU eligible only To opt out of DU Refi Plus consideration for a loan casefile prior to underwriting, enter the phrase Standard LCOR in the Product Description field. CERTIFICATIONS Primary Residence and Second Home: Qualified Mortgage (QM), Higher-Priced (HPML) and High Cost (HCL) Mortgage Loan Certification or comparable form that validates QM status, HPML and HCL. BB&T does not purchase high cost loans. COLLATERAL ASSESSMENT REQUIREMENTS Follow DU response If new appraisal is obtained, condition rating of C6 and/or quality rating of Q6 completed on an “as-is” basis is acceptable. No requirement for appraisal to be completed “subject to” repairs being made. DU will waive the appraisal or exterior-only property inspection on certain loan files. If the DU response allows the Property Inspection Waiver (PIW), the $75 fieldwork waiver fee will be netted out at funding. The PIW must have been issued no more than 120 days prior to the Note date.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

CREDIT SCORE None; however, a representative credit score is required for pricing purposes. Rescoring and Credit Repair • Legitimate corrections to a borrower’s credit profile are acceptable, i.e. John Doe Jr.’s derogatory credit is

reflected on John Doe Sr.’s credit report. • In order to ensure the accuracy of the information, corrections should be made at the credit repository level. • Any supporting documentation sent to the credit repositories along with all copies of credit reports should

be maintained in the Correspondent’s loan file and included with the file submission when delivered to BB&T Correspondent Lending.

The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower’s credit profile to improve credit scores for purposes of loan eligibility, rate/price improvement and creditworthiness is expressly prohibited by BB&T Correspondent Lending. It is at BB&T Correspondent Lending’s discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements. Reference the Price Adjustments and LTV Charts for minimum credit score requirements on specific product/loan types. DEMAND FEATURE None ELIGIBLE BORROWERS The following scenarios are eligible: • Borrower(s) on the new mortgage are the same as the current mortgage. • Borrower(s) have been added to the new mortgage and the existing borrower(s) have been retained. • Borrower(s) have been removed from the new mortgage for any reason: At least one of the original borrowers must be retained on the new loan.

Note: Borrower being removed is not required to be removed from the deed or title to the property and retain no ownership interest in the property. As a reminder, each person who has an ownership interest in the security property, even if the person’s income is not used in qualifying for the mortgage loan, must sign the security instrument (See Section B8-2-03 of the Fannie Mae Guide for additional information). ESCROWS Required on LTV’s greater than 80% ESCROW WAIVER Permitted when the Loan to Value is 80% or less. There is a reduction in Servicing Released Premium for waiving escrows. Refer to BB&T’s current Rate Sheet FANNIE MAE DOCUMENTATION Fannie Mae Checklist

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

HARDEST HIT FUNDS Unsecured financing provided through a Housing Finance Agency’s (HFA) “Hardest Hit Fund” program for the purpose of principal curtailment or closing costs for the Fannie Mae DU Refi Plus is permitted and must meet the following requirements: • Funds must be reflected as “Other Credit” in Section VII of the mortgage loan application. • Mortgage file must contain a copy of the promissory note or other documentation specifying the terms and

conditions of the loan. If documents indicate repayment is expected, the monthly payment must be included in the DTI ratio unless repayment is only due upon sale or default.

• Transfer of the loan proceeds must be reflected on the HUD-1 Settlement Statement. • Property must be located in one of the following “Hardest Hit States”: Alabama, Arizona, Florida, Georgia,

Illinois, Indiana, Kentucky, Michigan, Mississippi, Nevada, New Jersey, North Carolina, Ohio, Oregon, Rhode Island, South Carolina, Tennessee, and Washington DC.

HIGHER PRICED COVERED TRANSACTIONS Mortgages classified as a higher priced covered transaction, as defined in Regulation Z, 12 C.F.R. 1026.43(b), must meet requirements that include the following:

• Employment, income and assets must be verified according to DU findings. • Minimum credit score of 620 required. • Maximum Debt-to-Income (DTI) cannot exceed 45%

HIGHER PRICED MORTGAGE LOANS Mortgages classified as a higher priced mortgage loan must meet all requirements for Higher Priced Covered Transactions listed above along with the following:

• Escrow account has been established on the loan and will be maintained for at least the first 60 months.

Note: Higher Priced Covered Transactions and Higher Priced Mortgage Loans differ from a High-Cost Loan. BB&T’s policy prohibiting the origination of High-Cost Loans remains unchanged. HOMEOWNERSHIP COUNSELING DISCLOSURE Homeownership Counseling Disclosure required per the 2013 HOEPA Rule, an amendment to Regulation X (RESPA). INCOME DOCUMENTATION REQUIREMENTS • Income sources and documentation requirements per Section B5-5.2-02 of Fannie Mae Guide. • IRS Form 4506-T required. Form must be completed, signed and dated by each borrower at application

and closing. • Tax Transcripts (IRS Record of Account): most recent available tax transcript required for each borrower.

Note: An IRS Record of Account is acceptable in lieu of Tax Transcripts. References to “Tax Transcripts” and “Record of Account” are interchangeable for purposes of this product description.

INELIGIBLE LOAN TYPES AND PROGRAMS Existing loans not serviced by BB&T Existing loans not owned or securitized by Fannie Mae Existing loans where the original mortgage being refinanced has a Note Date after May 31, 2009. Existing and new mortgages not in first lien position Mortgage being refinanced is currently a HARP loan. HARP to HARP loans are ineligible. New mortgages as: Balloons, ARMs, Cash-Out Refinance, and Non-Warrantable Condos and Condotels New mortgages that convert interim construction financing to permanent financing New mortgages with temporary buydowns New mortgages that are manually underwritten New mortgages subject to Downpayment Assistance Programs Properties subject to Property Assessed Clean Energy (PACE) Obligations LOAN PURPOSE Limited Cash-Out Refinance Only

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

LOAN TYPE Conforming Fixed and Super-Conforming Fixed LTV/TLTV Unlimited MAXIMUM LOAN AMOUNT Up to county specific Fannie Mae Conforming or Super-Conforming (if applicable) loan limits. MINIMUM LOAN AMOUNT None MORTGAGE INSURANCE If the mortgage being refinanced has mortgage insurance and the new mortgage is not <=80% LTV, then the new DU Refi Plus Mortgage is ineligible for sale to BB&T Correspondent Lending. If the mortgage being refinanced did not have mortgage insurance, then no mortgage insurance coverage is required for the new DU Refi Plus Mortgage and the mortgage is eligible for sale to BB&T Correspondent Lending. MULTIPLE FINANCED PROPERTIES DU Refi Plus loans are exempt from the multiple financed properties guidelines listed within the Fannie Mae Selling Guide.

NOTE Freddie Mac 3200 Unit Number must be included in the property address line. Refer to Legal Document Matrix for additional information. OCCUPANCY The existing mortgage and the new DU Refi Plus do not have to represent the same occupancy. The occupancy of the subject property may have changed by the time of the new mortgage transactions. The subject property may be listed for sale at time of application for the HARP loan. OVERLAYS Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming for additional information. POINTS AND FEES CAPS • 3% of the total loan amount for a loan amount greater than or equal to $105,158 • $3,155 for a loan amount greater than or equal to $63,095 but less than $105,158 • 5% of the total loan amount for a loan greater than or equal to $21,032 but less than $63,095 • $1,052 for a loan amount greater than or equal to $13,145 but less than $21,032 • 8% of the total loan amount for a loan less than $13,145

PREPAYMENT PENALTY None

PRICING Refer to the Rate Sheet and BB&T’s current Price Adjustments and LTV Charts for any price adjustments that might be applicable.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

PROPERTY TYPES Primary Residence and Investment Property- 1-4 Family, Warrantable Condominiums, PUDs, Manufactured Housing Second Home- 1-Family, Warrantable Condominiums, PUDs, Manufactured Housing Attached PUDs Property Insurance requirements:

• HO3/comparable full coverage homeowners insurance policy; OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit

to its condition prior to a loss claim event for attached PUDs where the homeowners association has a blanket policy covering the exterior structure only; OR

• Homeowners Association blanket policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if blanket policy covers the exterior and interior of the

unit. • HO3/comparable full coverage policies will be escrowed.

Condominiums Property Insurance requirements:

• HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its condition prior to a loss claim event for Condominiums where the condominium master policy covers the exterior structure only; OR

• Condominium master policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if master policy covers the exterior and interior of the

unit.

QM STATUS Safe Harbor: Mortgage that does not exceed limits on upfront points and fees; has an APR relative to the APOR that is equal to or less than 1.5% for first-lien loans. Rebuttable Presumption: Mortgage than does not exceed limits on upfront points and fees; has an APR that exceeds the APOR as of the date the interest rate is set by 1.5% or more for first-lien loans. Also known as “Higher-Priced”. QUALIFYING RATIOS Determined by DU REFINANCE PROCEEDS New loan amount can include payoff of the unpaid principal balance on the existing first mortgage; financing of closing costs, prepaid items and points; maximum $250 cash back to the borrower. The amount in excess of $250 will be applied as a principal curtailment. Enter the amount of the first mortgage being paid off with the new transaction on “line d. Refinance” located under Section VII Details of Transaction of the loan application. This amount must match the balance of the mortgage being paid off, as shown in the liabilities section of the loan application. REQUIRED BORROWER BENEFIT • Reduction in the monthly principal and interest payment of the first lien mortgage, or • Moving into a more stable mortgage product, i.e. ARM to a Fixed Rate, fully amortizing mortgage, or • Reduction of the interest rate of the first lien mortgage, or • Reduction of the amortization term of the first lien mortgage.

Note: Extension of the amortization term of the new refinance mortgage (i.e. 15 to 30 years) is a borrower benefit if it results in a reduction in principal and interest payment.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

REQUIRED MORTGAGE PAYMENT HISTORY No 60 day lates in the past 12 months on any mortgage tradeline. No limit on payment increase, subject to the Borrower Benefit Requirements. RESIDENCY STATUS US Citizens Permanent Resident Alien Non-Permanent Resident Alien RESTRUCTURED LOANS Subsequent refinance of a restructured loan is eligible if the following are met: • At least 24 months of timely payments on the restructured loan terms are documented. • The new refinance loan meets all DU Refi Plus requirements in the Fannie Mae Selling Guide and the

BB&T Correspondent Lending product description. SEASONING REQUIREMENTS None SECONDARY FINANCING • Existing junior liens must be subordinated to the new Fannie Mae DU Refi Plus mortgage loan. • Existing junior lien may be simultaneously refinanced as long as new junior lien loan amount does not

exceed existing unpaid principal balance. • Existing junior lien may not be paid off with the proceeds of a new DU Refi Plus mortgage loan • New junior lien is only permitted if it replaces existing junior lien.

SECURITY INSTRUMENT Use the applicable Freddie Mac/Fannie Mae security instrument for the state in which the property is located. SIGNIFICANT DEROGATORY CREDIT Follow waiting periods and re-establishment of credit guidelines per the Fannie Mae Selling Guide. SPECIAL MORTGAGE TYPE DU Refi Plus TEMPORARY BUYDOWNS Not allowed WORKSHEETS Points and Fees Worksheet or comparable form Ability to Repay Worksheet or comparable form OR

• Income calculation for each borrower on either the Transmittal Summary or on a separate form; AND • Income and debt amounts must match on the Transmittal Summary, final application and final AUS

submission; AND • Total debt-to-income ratio on the Transmittal Summary and final AUS submission must match.

SPECIAL FEATURE CODES (BB&T use only) 147 Fannie Mae DU Refi Plus 807 (if Property Inspection Waiver is used) Other applicable standard SFC codes CONDO/PUD DELIVERY CODE (BB&T use only) V= Condominium E= PUD MI DELIVERY CODE (BB&T use only) 95= DU Refi Plus loans with LTV’s over 80% and no MI coverage.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FANNIE MAE DU REFI PLUS 1-1-2018

How do I determine if my client is eligible for Fannie Mae’s DU Refi Plus program? There are resources available to clients to determine their eligibility for Fannie Mae’s DU Refi Plus Program. If a client was referred to you by BB&T, eligibility may not have already been determined at that time. Following are steps that can be used to assist your client’s in determining their eligibility. Clients may also go to Making Home Affordable to learn more about the Making Home Affordable program in general. 1. The existing loan must be owned by Fannie Mae and serviced by BB&T. a. With the client’s verbal consent, Correspondent may access Fannie Mae’s website to determine if the

loan is owned by Fannie Mae. OR

b. Clients may call BB&T at 1-800-295-5744 and follow the prompts to reach Option #4 for the Homeowner Affordability and Stability Plan.

2. The new loan must not require Mortgage Insurance (MI). a. If the mortgage being refinanced has mortgage insurance and the mortgage is not <=80% LTV, then the

new DU Refi Plus mortgage is ineligible for sale to BB&T Correspondent Lending.

b. If the mortgage being refinanced did not have mortgage insurance, then no mortgage insurance coverage is required for the new DU Refi Plus mortgage, and the mortgage is eligible for sale to BB&T Correspondent Lending.

Once Correspondent has determined that the client is eligible for the Fannie Mae program, based on information provided by the client, continue the application process by following the applicable Product Description and Checklists provided by BB&T Correspondent Lending.

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

8:4 FREDDIE MAC RELIEF REFINANCE MORTGAGE

All loans must be owned or securitized by Freddie Mac and serviced by BB&T. Original loan being refinanced must have a Note Date on or before May 31, 2009.

LOAN PRODUCT CODES

LOAN PRODUCT LOAN TERM/ AMORTIZATION TERMS*

950 Conforming 30 Year Fixed Rate Relief Plus 241-360 months 951 Conforming 20 Year Fixed Rate Relief Plus 181-240 months 952 Conforming 15 Year Fixed Rate Relief Plus 180 months

*Minimum Amortization Term – 120 months Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming and the Conforming Underwriting Guidelines section for additional information. ****************************************************************************************************************************** ADDITIONAL CONSIDERATIONS Re-classification of condos is NOT required. However, all condos must be marked as “Streamlined Review”. ASSUMABILITY Not assumable AUTOMATED UNDERWRITING Not Allowed CERTIFICATIONS Primary Residence and Second Home: Qualified Mortgage (QM), Higher-Priced (HPML) and High Cost (HCL) Mortgage Loan Certification or comparable form that validates QM status, HPML and HCL. BB&T does not purchase high cost loans. COLLATERAL ASSESSMENT REQUIREMENTS • Home Value Explorer (HVE): Eligible HVE must meet the following requirements: Dated no more the 120 days from the closing date Reflect a score of “H” (High) or “M” (Medium) Standard deviation no greater than .20 Property is a 1-2 unit dwelling or Condo/PUD

OR

• New appraisal- full interior/exterior Condition rating of C5 or C6 and/or qualify rating of Q6 completed on an “as-is” basis is acceptable. No requirement for appraisal to be completed “subject to” repairs being completed. CREDIT SCORE All LTV’s- no minimum credit score requirement unless the P&I payment is increasing by more than 20%. Also, if there is no usable credit score due to inaccurate or insufficient information, the mortgage remains eligible for a HARP Refinance. Rescoring and Credit Repair • Legitimate corrections to a borrower’s credit profile are acceptable, i.e. John Doe Jr.’s derogatory credit is

reflected on John Doe Sr.’s credit report. • In order to ensure the accuracy of the information, corrections should be made at the credit repository level. • Any supporting documentation sent to the credit repositories along with all copies of credit reports should

be maintained in the Correspondent’s loan file and included with the file submission when delivered to BB&T Correspondent Lending.

(Continued On Next Page)

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower’s credit profile to improve credit scores for purposes of loan eligibility, rate/price improvement and creditworthiness is expressly prohibited by BB&T Correspondent Lending. It is at BB&T Correspondent Lending’s discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements. DEMAND FEATURE None DOCUMENTATION • Completed loan application (URAR form 1003) with stated income and assets • New credit report • Employment and Income: At least one borrower must have a source of income and that source must be

verified. -Employed Income: Verbal verification of employment is required and must meet the requirements of the Freddie Mac Seller/Servicer Guide.

-Self Employed Income: Verification of existence of the business through a third party source is required and must meet the requirements of the Freddie Mac Seller/Servicer Guide. -Other Income Sources: Verification of the source of income is required. Income source must be an eligible source of income per the Freddie Mac Seller/Servicer Guide.

Alternative to Income Verification- If Borrower has no income and the new PITI payment increase is 20% or less, the following may be utilized in lieu of verification of income source: Reserves equal to 12 full monthly payments for the new refinance mortgage may be verified in lieu of verifying a source of income. Eligible funds are limited to funds in the borrower’s depository and non-depository accounts, including, but not limited to checking, savings, money markets, stock, bond, and retirement accounts. Most recent monthly or quarterly account statements must be obtained and retained in the mortgage file. Requirements of the Freddie Mac/Seller Servicer Guide do not need to be met (i.e. investigation of large deposits or increases in balance or providing proof of liquidation of funds). However, non-depository accounts must meet the requirements of the Freddie Mac Seller/Servicer Guide. Assets/Funds to Close: All LTV’s: Verification of assets/funds to close is not required unless the P&I payment is increasing by more than 20%; loan is a Higher Priced Mortgage Loan (HPML); or a Higher Priced Covered Transaction. See applicable section for additional details. Required documentation for all Relief Refinance loans: Freddie Mac Relief Refinance Loan Amount Calculator Payoff Statement Closing Disclosure (CD)

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

ELIGIBLE BORROWERS The borrower(s) on the existing mortgage must be identical to the borrower(s) on the new mortgage, however, a borrower may be removed from the new mortgage provided that: • The mortgage file contains evidence that the remaining borrower has been making the mortgage payments,

including the payments for any secondary financing, for the most recent 12 month period; or • The remaining borrower(s) qualifies for the mortgage based on the requirements for mortgages with a

principal and interest payment increase in section 4302.2 (g); or • In case of death, a copy of the death certificate is obtained and retained in the mortgage file. • Borrower being removed is not required to be removed from the deed or title to the property and retain no

ownership interest in the property. • In all cases, at least one borrower from the existing mortgage being refinanced must be retained.

ESCROWS Required on LTV’s greater than 80% ESCROW WAIVER Permitted when the Loan to Value is 80% or less. There is a reduction in Servicing Released Premium for waiving escrows. Refer to BB&T’s current Rate Sheet FREDDIE MAC DOCUMENTATION Freddie Mac Checklist HARDEST HIT FUNDS The use of Hardest Hit Funds (HHF) by a Housing Finance Agency (HFA) to pay down or curtail the outstanding mortgage balance on a Borrower’s existing loan at the time of refinancing and/or to pay closing costs, financing costs and prepaids/escrows for the Freddie Mac Relief Refinance Mortgage is permitted and must meet the following requirements: • Funds provided by the Housing Finance Agency must not result in a lien on the property. • Mortgage file must contain a copy of the promissory note or other documentation specifying the terms and

conditions of the loan. • If repayment of funds is required, the verified payment must be included in the monthly DTI ratio unless the

calculation of DTI ratio is not required or repayment of funds is due only upon sale or default. • Hardest Hit Funds must be reflected on the HUD-1 Settlement Statement. • Property must be located in one of the following “Hardest Hit States”: Alabama, Arizona, Florida, Georgia,

Illinois, Indiana, Kentucky, Michigan, Mississippi, Nevada, New Jersey, North Carolina, Ohio, Oregon, Rhode Island, South Carolina, Tennessee, and Washington DC.

HIGHER PRICED COVERED TRANSACTIONS Mortgages classified as a higher priced covered transaction, as defined in Regulation Z, 12 C.F.R. 1026.43(b), must meet requirements that include the following: • New Credit Report • Minimum indicator credit score of 620 • Verification of employment and income-documentation according to Section 4302.2 (g) ii of the Freddie

Mac Seller/Servicer Guide • Verification of assets/funds to close-documentation according to Section 4302.2 (g) ii of the Freddie Mac

Seller/Servicer Guide • If repayment of Hardest Hit Funds is required, the verified payment must be included in the monthly DTI

ratio, unless repayment of funds is due only upon sale or default • Maximum Debt-to-Income (DTI) cannot exceed 45%

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

HIGHER PRICED MORTGAGE LOANS Mortgages classified as a higher priced mortgage loan must meet all requirements for Higher Priced Covered Transactions listed above along with the following:

• Escrow account has been established on the loan and will be maintained for at least the first 60 months.

Note: Higher Priced Covered Transactions and Higher Priced Mortgage Loans differ from a High-Cost Loan. BB&T’s policy prohibiting the origination of High-Cost Loans remains unchanged. HOMEOWNERSHIP COUNSELING DISCLOSURE Homeownership Counseling Disclosure required per the 2013 HOEPA Rule, an amendment to Regulation X (RESPA). INELIGIBLE LOAN TYPES AND PROGRAMS Existing loans not serviced by BB&T Existing and new mortgages not in first lien position Existing loans not owned or securitized by Freddie Mac Existing loans where the original mortgage being refinanced has a Note Date after May 31, 2009. Existing loans not seasoned for three months (that is, the Note date of the mortgage being refinanced must be at least three months prior to the Note date of the Freddie Mac Relief Mortgage). Mortgage being refinanced is currently a HARP loan. HARP-to-HARP loans are ineligible New mortgages as Cash-Out Refinance, Special Purpose Cash-Out Refinances, and Non-Warrantable Condos and Condotels New mortgages that convert interim construction financing to permanent financing New mortgages with Temporary Buydowns New mortgages subject to Downpayment Assistance Programs Properties subject to Property Assessed Clean Energy (PACE) Obligations LOAN PURPOSE No Cash-Out Refinance Only LOAN TYPE Conforming Fixed Super-Conforming Fixed LTV/TLTV/HTLTV Unlimited

Refer to our current Price Adjustments and LTV Charts for any price adjustments that might be applicable. MAXIMUM LOAN AMOUNT Up to county specific Freddie Mac Conforming or Super Conforming (if applicable) loan limits MINIMUM LOAN AMOUNT None MORTGAGE INSURANCE If the mortgage being refinanced has mortgage insurance and new mortgage is not <=80% LTV, then the new Freddie Mac Relief Refinance Mortgage is ineligible for sale to BB&T Correspondent Lending.

If the mortgage being refinanced did not have mortgage insurance, then no mortgage insurance coverage is required for the new Freddie Mac Relief Refinance Mortgage and the mortgage is eligible for sale to BB&T Correspondent Lending. NOTE Freddie Mac 3200 Unit Number must be included in the property address line. Refer to Legal Document Matrix for additional information.

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

OCCUPANCY Freddie Mac has removed the requirement that the occupancy of the mortgage being refinanced and the occupancy of the new HARP mortgage be the same. Therefore, a mortgage loan that was originally underwritten and sold to Freddie Mac as a primary residence, but is now a second home or investment property is eligible for a HARP refinance. OVERLAYS Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming for additional information POINTS AND FEES CAPS • 3% of the total loan amount for a loan amount greater than or equal to $105,158 • $3,155 for a loan amount greater than or equal to $63,095 but less than $105,158 • 5% of the total loan amount for a loan greater than or equal to $21,032 but less than $63,095 • $1,052 for a loan amount greater than or equal to $13,145 but less than $21,032 • 8% of the total loan amount for a loan less than $13,145

PREPAYMENT PENALTY None PRICING Refer to the Rate Sheet and BB&T’s current Price Adjustments and LTV Charts for any price adjustments that might be applicable. PRINCIPAL AND INTEREST PAYMENT INCREASE The following apply when the P&I payment on the new Freddie Mac Relief Refinance mortgage increases by more than 20% from the current contractually obligated payment under the Note. In the event the original Note provides for more than one payment option, use the lowest payment option to determine whether the increase exceeds 20%. • New Credit Report • Minimum indicator score of 620 • Verification of employment and income-documentation according to Section 4302.2 (g) ii of the Freddie

Mac Seller/Servicer Guide • Verification of assets/funds to close-documentation according to Section 4302.2 (g) ii of the Freddie Mac

Seller/Servicer Guide • If repayment of Hardest Hit Funds is required, the verified payment must be included in the monthly DTI

ratio, unless repayment of funds is due only upon sale or default • Maximum Debt-to-Income (DTI) cannot exceed 45%

PROPERTY TYPES Primary Residence and Investment Property- 1-4 Family, Warrantable Condominiums, PUDs, Manufactured Housing

Second Home- 1-Family, Warrantable Condominiums, PUDs, Manufactured Housing

Attached PUDs Property Insurance requirements: • HO3/comparable full coverage homeowners insurance policy; OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to

its condition prior to a loss claim event for attached PUDs where the homeowners association has a blanket policy covering the exterior structure only; OR

• Homeowners Association blanket policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if blanket policy covers the exterior and interior of the

unit. • HO3/comparable full coverage policies will be escrowed.

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

Condominiums Property Insurance requirements: • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to

its condition prior to a loss claim event for Condominiums where the condominium master policy covers the exterior structure only; OR

• Condominium master policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if master policy covers the exterior and interior of the

unit.

QM STATUS Safe Harbor: Mortgage that does not exceed limits on upfront points and fees; has an APR relative to the APOR that is equal to or less than 1.5% for first-lien loans. Rebuttable Presumption: Mortgage than does not exceed limits on upfront points and fees; has an APR that exceeds the APOR as of the date the interest rate is set by 1.5% or more for first-lien loans. Also known as “Higher-Priced”. QUALIFYING RATIOS Required if P&I payment is increasing by more than 20%. See “Principal and Interest Payment Increase” section of additional details. REFINANCE PROCEEDS The proceeds of the Freddie Mac Relief Refinance Mortgage must be used only to: • Pay off the first mortgage being refinanced which includes only the unpaid principal balance plus accrued

interest, and

• Pay related closing costs, financing costs, and prepaids/escrows not to exceed $5,000.

• Disburse cash to Borrower not to exceed $250. Under no circumstances may cash disbursed to Borrower exceed $250.

NOTE: Proceeds may not be used to pay off or pay down any junior liens.

In the event there are remaining proceeds from the Relief Refinance Mortgage after the proceeds are applied as described above: • The Mortgage amount must be reduced, or • The excess must be applied as a principal curtailment to the Relief Refinance Mortgage at closing and

must be clearly reflected on the HUD-1 form or other equivalent closing statement and the loan is subject to a three day rescission.

Verify New Loan Amount • 48 hours prior to loan closing, the Correspondent will e-mail Freddie Mac Relief Refinance

Loan Amount Calculator, Payoff Statement, and HUD-1 to [email protected] for the review. The Payoff and HUD-1 should match. If the payoff date changes, the documents noted above will need to be resubmitted to [email protected] for subsequent review and approval of the loan amount.

• BB&T Correspondent Lending will verify the new loan amount calculation and e-mail the Correspondent with the approval of the loan amount.

• Deliver the loan in the usual fashion to BB&T Correspondent Lending for funding

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

REQUIRED BORROWER BENEFIT The new refinance mortgage must result in one of the following: • Reduction in the monthly principal and interest payment of the first lien mortgage. • Replacement of an ARM or Balloon mortgage with a fixed rate, fully amortizing mortgage • Reduction of the interest rate of the first lien mortgage • Reduction of the amortization term of the first lien mortgage

Note: The Freddie Mac Relief Refi mortgage may have a longer amortization term than the mortgage being refinanced as long as it meets one of the above criteria. REQUIRED MORTGAGE PAYMENT HISTORY No delinquencies in the most recent 6 months, and No more than one 30-day delinquency in the most recent 12 months (months 7-12). RESIDENCY STATUS US Citizens Permanent Resident Alien Non-Permanent Resident Alien RESTRUCTURED LOANS Subsequent refinance of a restructured loan is eligible if all Freddie Mac Relief Refinance requirements in the Freddie Mac Seller/Servicer Guide and the BB&T Correspondent Lending product description are met. SEASONING REQUIREMENTS Three months (that is, the Note date of the mortgage being refinanced must be at least three months prior to the Note date of the Freddie Mac Relief Mortgage). SECONDARY FINANCING • Existing junior liens must be subordinated to the new Freddie Mac Relief Refinance and meet the

requirements for secondary financing set forth in the Freddie Mac Seller/Servicer Guide. • An increase in the current unpaid principal amount of any junior lien is not permitted. • New secondary financing is not allowed. • The junior lien may be refinanced simultaneously with the existing first lien if the junior lien is being

refinanced for one of the following purposes: Be a reduction in the interest rate of the junior lien; or Replace an adjustable rate mortgage (ARM), an interest only junior lien, or a junior lien with a balloon or

call option with a fixed rate, fully amortizing lien: or Be a reduction in the amortization term of the junior lien Be a reduction in the monthly payment of the junior lien The unpaid principal balance of the new junior lien may not be more than the unpaid principal balance, at

the time of payoff of the junior lien being refinanced. No new funds may be added to the new junior lien. No other “new” secondary financing is permitted

There are no maximum TLTV requirements for the Relief Refinance mortgage (no change from original Relief Refinance);

Junior liens with a balloon or call feature less than five years are ineligible unless a HELOC If the current junior lien being refinanced is a fixed rate, the new junior lien cannot be an ARM

SECURITY INSTRUMENT Use the applicable Freddie Mac/Fannie Mae security instrument for the state in which the property is located. SPECIAL MORTGAGE TYPE Freddie Relief

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

TEMPORARY BUYDOWNS Not allowed WORKSHEETS Points and Fees Worksheet or comparable form Ability to Repay Worksheet or comparable form OR

• Income calculation for each borrower on either the Transmittal Summary or on a separate form; AND • Income and debt amounts must match on the Transmittal Summary, final application and final AUS

submission; AND • Total debt-to-income ratio on the Transmittal Summary and final AUS submission must match.

INVESTOR FEATURE IDENTIFIER CODES (BB&T use only) 007- No Cash-Out Refinances H06- Freddie Mac Relief Refinance 583- Mortgage with Affordable Seconds H03- HVE Point Value Estimate

BB&T Internal

The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

FREDDIE MAC RELIEF REFINANCE MORTGAGE 1-1-2018

How do I determine if my client is eligible for Freddie Mac’s Relief Refinance program? There are resources available to clients to determine their eligibility for Freddie Mac Relief Refinance Program. If a client was referred to you by BB&T, eligibility may not have already been determined at that time. Following are steps that can be used to assist your client’s in determining their eligibility. Clients may also go to Making Home Affordable to learn more about the Making Home Affordable program in general. 1. The existing loan must be owned by Freddie Mac and serviced by BB&T. a. With the client’s verbal consent, Correspondent may access Freddie Mac’s website to determine if the

loan is owned by Freddie Mac. OR

b. Clients may call BB&T at 1-800-295-5744 and follow the prompts to reach Option #4 for the Homeowner Affordability and Stability Plan.

2. The new loan must not require Mortgage Insurance (MI). a. If the mortgage being refinanced has mortgage insurance and the mortgage is not <=80% LTV, then the

new Freddie Mac Relief Refinance mortgage is ineligible for sale to BB&T Correspondent Lending.

b. If the mortgage being refinanced did not have mortgage insurance, then no mortgage insurance coverage is required for the new Freddie Mac Relief Refinance mortgage, and the mortgage is eligible for sale to BB&T Correspondent Lending.

Once Correspondent has determined that the client is eligible for the Freddie Mac program, based on information provided by the client, continue the application process by following the applicable Product Description and Checklists provided by BB&T Correspondent Lending.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

SUPER CONFORMING FINANCING PROGRAM 4/30/2018

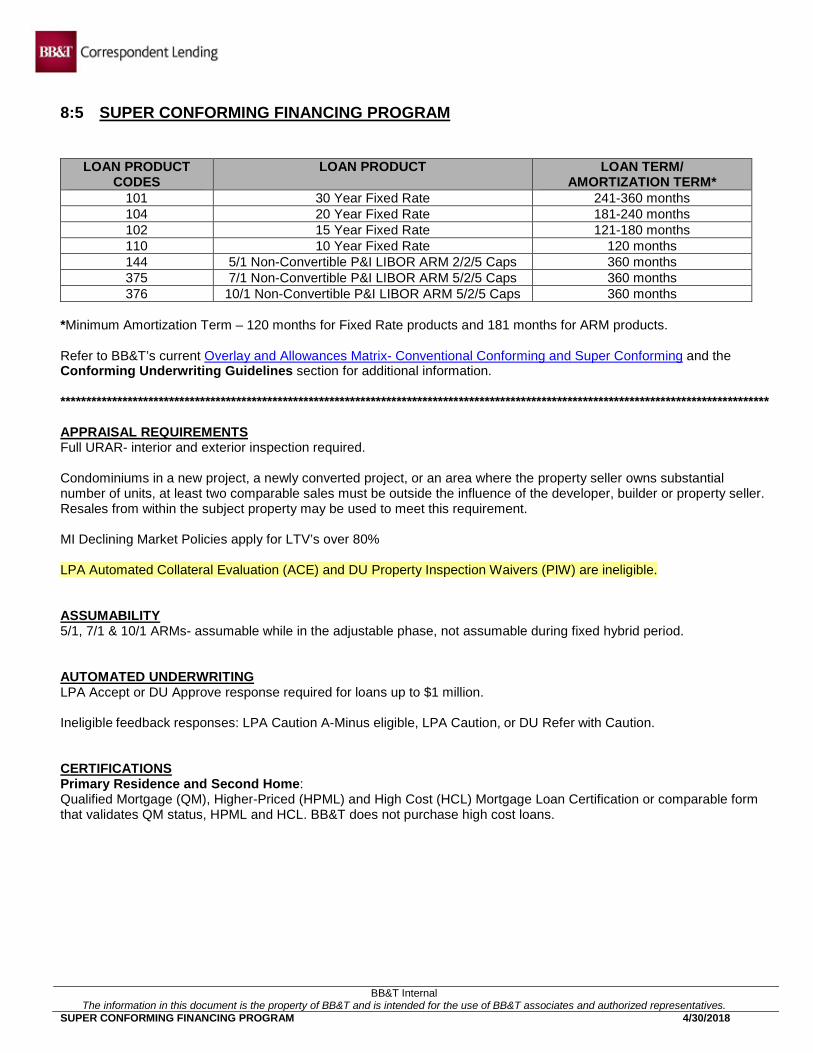

8:5 SUPER CONFORMING FINANCING PROGRAM

LOAN PRODUCT CODES

LOAN PRODUCT LOAN TERM/ AMORTIZATION TERM*

101 30 Year Fixed Rate 241-360 months 104 20 Year Fixed Rate 181-240 months 102 15 Year Fixed Rate 121-180 months 110 10 Year Fixed Rate 120 months 144 5/1 Non-Convertible P&I LIBOR ARM 2/2/5 Caps 360 months 375 7/1 Non-Convertible P&I LIBOR ARM 5/2/5 Caps 360 months 376 10/1 Non-Convertible P&I LIBOR ARM 5/2/5 Caps 360 months

*Minimum Amortization Term – 120 months for Fixed Rate products and 181 months for ARM products. Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming and the Conforming Underwriting Guidelines section for additional information. ***************************************************************************************************************************************** APPRAISAL REQUIREMENTS Full URAR- interior and exterior inspection required. Condominiums in a new project, a newly converted project, or an area where the property seller owns substantial number of units, at least two comparable sales must be outside the influence of the developer, builder or property seller. Resales from within the subject property may be used to meet this requirement. MI Declining Market Policies apply for LTV’s over 80% LPA Automated Collateral Evaluation (ACE) and DU Property Inspection Waivers (PIW) are ineligible. ASSUMABILITY 5/1, 7/1 & 10/1 ARMs- assumable while in the adjustable phase, not assumable during fixed hybrid period. AUTOMATED UNDERWRITING LPA Accept or DU Approve response required for loans up to $1 million. Ineligible feedback responses: LPA Caution A-Minus eligible, LPA Caution, or DU Refer with Caution. CERTIFICATIONS Primary Residence and Second Home: Qualified Mortgage (QM), Higher-Priced (HPML) and High Cost (HCL) Mortgage Loan Certification or comparable form that validates QM status, HPML and HCL. BB&T does not purchase high cost loans.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

SUPER CONFORMING FINANCING PROGRAM 4/30/2018

CREDIT REQUIREMENTS LPA or DU is required on all Super Conforming loans. Follow LPA or DU feedback with the following additional requirements: The borrowers’ credit reputation is acceptable if: • The mortgage receives a Risk Class of Accept or Approve/Eligible • Non-traditional credit is not allowed • Super Conforming loan amounts may not exceed $1 million and require an AUS response. • Ineligible feedback responses: LPA Caution A-Minus eligible, LPA Caution, or DU Refer with Caution.

CREDIT SCORE Minimum credit score requirements - Freddie Mac Loan Product Advisor (LPA) Accept or Fannie Mae Desktop Underwriter (DU) Approve/Eligible:

Purchase and No Cash Out Refinance Transactions: 620

Cash Out Refinance Transactions: 620 Eligibility Requirements – Not all Borrowers have Usable Credit Scores Freddie Mac Loan Product Advisor (LPA) Requirements for Accept Mortgages:

• At least one Borrower on the transaction has a usable Credit Score, as determined by LPA, which meets BB&T Correspondent Lending minimum credit score requirements.

• The transaction is a purchase or “no cash-out” refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their Primary

Residence. • Borrowers with a usable Credit Score contribute more than 50% of the total monthly income. • Super Conforming loan amounts are eligible. • A-Minus mortgages are ineligible for delivery to BB&T Correspondent Lending.

Fannie Mae Desktop Underwriter (DU) Requirements for DU Approve/Eligible Mortgages: All borrowers must have usable credit scores. Rescoring and Credit Repair • Legitimate corrections to a borrower’s credit profile are acceptable, i.e. John Doe Jr.’s derogatory credit is reflected

on John Doe Sr.’s credit report. • In order to ensure the accuracy of the information, corrections should be made at the credit repository level. • Any supporting documentation sent to the credit repositories along with all copies of credit reports should be

maintained in the Correspondent’s loan file and included with the file submission when delivered to BB&T Correspondent Lending.

The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower’s credit profile to improve credit scores for purposes of loan eligibility, rate/price improvement and creditworthiness is expressly prohibited by BB&T Correspondent Lending. It is at BB&T Correspondent Lending’s discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements. DOCUMENTATION Follow LPA or DU feedback and refer to the Conforming Underwriting Guidelines for any overlays.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

SUPER CONFORMING FINANCING PROGRAM 4/30/2018

DOWNPAYMENT AND ASSETS Follow LPA or DU

LTV/TLTV/HTLTV Minimum Borrower Contribution required from Borrower’s own Funds

80% or less

1-4 Unit Primary Residences

& Second Homes

None – All funds to complete the transaction can come from a gift.

Greater than 80%

1 unit Primary Residence

None – All funds to complete the transaction can come from a gift.

2-4 Unit Primary Residences

& Second Homes

5% - After the minimum Borrower contribution has been met, gifts can be used to supplement the down payment, closing costs & reserves.

Proof of liquidation of asset accounts is required, regardless of LPA or DU feedback. EMPLOYMENT HISTORY Follow LPA or DU feedback and refer to the Conforming Underwriting Guidelines for any overlays. ESCROWS Required for LTV’s greater than 80% ESCROW WAIVER Permitted when the Loan to Value is 80% or less, and the loan is not designated as a Higher Priced Mortgage Loan (HPML) Escrow waivers are NOT permitted under the following scenarios: (no exceptions permitted under Federal Law) • Loans with LTVs greater than 80% • Higher Priced Mortgage Loans (HPMLs), regardless of LTV • Properties within a flood hazard area must have flood insurance escrows.

Refer to BB&T’s current Rate Sheet or SRP Schedule. There is a reduction in Servicing Released Premium for waiving escrows. HOMEOWNERSHIP COUNSELING DISCLOSURE Homeownership Counseling Disclosure required per the 2013 HOEPA Rule, an amendment to Regulation X (RESPA). INDEX 12 Month LIBOR index INELIGIBLE LOAN TYPES AND PROGRAMS ARMs other than 5/1 ARMs with 2/2/5; 7/1 and 10/1 ARMs with 5/2/5 Downpayment Assistance Programs HOME Now and Neighborhood HOME Loan amounts greater than $1 million LPA Caution A-Minus Eligible Properties subject to Property Assessed Clean Energy (PACE) Obligations Special Purpose Cash-Out

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

SUPER CONFORMING FINANCING PROGRAM 4/30/2018

INTEREST RATE ADJUSTMENTS The “Initial Interest Rate Adjustment” will be 60, 84, and 120 months after the first month following loan closing; thereafter, the Interest Rate will be subject to change annually. For loans which close on the first day of the month, the Initial Interest Rate Adjustment will be 60, 84, and 120 months after the month of loan closing; thereafter, the Interest Rate will be subject to change annually. INTEREST RATE CAPS & FLOOR

CAP 5/1 P&I LIBOR ARM 7/1 AND 10/1 P&I LIBOR ARMs Initial 2% (Increase or Decrease) 5% (Increase or Decrease)

Annual 2% (Increase or Decrease) 2% (Increase or Decrease) Lifetime 5% 5%

Margin of 2.25% is the Floor INTEREST RATE FORMULA Index plus margin rounded to the nearest .125%. LOAN PURPOSE Purchase No Cash-Out Refinance Cash-Out Refinance LOAN AMOUNT All properties must be located in a market eligible for the high-cost loan limits. Please visit the FHFA website to determine if a market qualifies. Federal Housing Finance Agency – Conforming Loan Limit LTV/TLTV/HTLTV Reference the Price Adjustments and LTV Charts MARGIN 225 basis points (2.25%) MAXIMUM CASH-OUT No Maximum MAXIMUM INTERESTED PARTY CONTRIBUTIONS Maximum financing concessions are based on TLTV when secondary financing is present, LTV when no secondary financing is present.

OCCUPANCY LTV/TLTV AMOUNT Primary Residence Over 90% 3%

Over 75% to 90% 6% 75% and below 9%

Second Home Over 75% to 85% 6% 75% and below 9%

Investment Property All LTV’s 2%

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

SUPER CONFORMING FINANCING PROGRAM 4/30/2018

MORTGAGE INSURANCE Required on all loans with LTV’s above 80% Financed MI is not allowed. Lender Paid MI (Single Premium) is allowed. Refer to “Mortgage Insurance Options” in the Conforming Underwriting Guidelines section for more information. NEGATIVE AMORTIZATION None NOTE

PRODUCT FREDDIE MAC/FANNIE MAE 101, 104, 102, 110 3200

PRODUCT FREDDIE MAC FANNIE MAE

144 5531 3528 375 5531 3528 376 5531 3528

Unit Number must be included in the property address line. Refer to Legal Document Matrix for additional information OCCUPANCY REQUIREMENTS Primary Residence Second Home Investment Property OVERLAYS Refer to BB&T’s current Overlay and Allowances Matrix- Conventional Conforming and Super Conforming for additional information. PAYMENT ADJUSTMENT The initial payment adjustment will be not less than 60, 84, 120 months from the date of the first payment; thereafter, the monthly payment to change annually. POINTS AND FEES CAPS

• 3% of the total loan amount for a loan amount greater than or equal to $105,158 • $3,155 for a loan amount greater than or equal to $63,095 but less than $105,158 • 5% of the total loan amount for a loan greater than or equal to $21,032 but less than $63,095 • $1,052 for a loan amount greater than or equal to $13,145 but less than $21,032 • 8% of the total loan amount for a loan less than $13,145

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

SUPER CONFORMING FINANCING PROGRAM 4/30/2018

PROPERTY TYPES Primary Residence and Investment Property- 1-4 Family, Freddie Mac Eligible Condominiums, PUDs Second Home- 1-Family, Freddie Mac Eligible Condominiums, PUDs Attached PUDs Property Insurance requirements:

• HO3/comparable full coverage homeowners insurance policy; OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its

condition prior to a loss claim event for attached PUDs where the homeowners association has a blanket policy covering the exterior structure only; OR

• Homeowners Association blanket policy covering the exterior AND interior of the unit. • HO3/comparable full coverage policies will be escrowed.

Condominiums Correspondents are responsible for classing Condominiums as outlined in the Conforming Underwriting Guidelines. Property Insurance requirements:

• HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its condition prior to a loss claim event for Condominiums where the condominium master policy covers the exterior structure only; OR