6th Asia / Africa IFA Conference Mauritius May 10, 2012 Girish Dave Advocate, Director General of...

26

6th Asia / Africa IFA Conference Mauritius May 10, 2012 Girish Dave Advocate, Director General of Income Tax (Retd.) Mahesh Kumar Senior Associate, Nishith Desai Associates Recent Indian Tax Case Law Vodafone and Beyond Nishith Desai Associates Legal & Tax Counseling Worldwide Mumbai | Silicon Valley | Bangalore | Singapore | Mumbai-BKC | New Delhi

-

Upload

ralf-walker -

Category

Documents

-

view

215 -

download

2

Transcript of 6th Asia / Africa IFA Conference Mauritius May 10, 2012 Girish Dave Advocate, Director General of...

6th Asia / Africa IFA Conference

Mauritius

May 10, 2012

Girish Dave

Advocate, Director General of Income Tax (Retd.)

Mahesh Kumar

Senior Associate, Nishith Desai Associates

Recent Indian Tax Case Law

Vodafone and Beyond

Nishith Desai AssociatesLegal & Tax Counsel ing Worldwide

Mumbai | Silicon Valley | Bangalore | Singapore | Mumbai-BKC | New Delhi

2

Tax Planning

Over a Century of Jurisprudence

© Nishith Desai Associates

Tax Planning: Over a Century of Jurisprudence

3

• Taxpayers require certainty to efficiently plan their economic behavior.

• Cape Brandy Syndicate v. IRC, (1921) 1 KB 64 (pg 71), per Rowlatt, J:

“ In a taxing act one has to look merely at what is clearly said. There is no room for any

intendment. Nothing has to be read in, nothing has to be implied. One can only look fairly at the language used.”

• IRC v. Fisher’s Executors [1926] AC 395 at 412 (HL)

"My Lords, the highest authorities have always recognised that the subject is entitled so to arrange his

affairs as not to attract taxes imposed by the Crown, so far as he can do so within the law, and that he may

legitimately claim the advantage of any expressed terms or of any omissions that he can

find in his favour in taxing Acts. In so doing, he neither comes under liability nor incurs blame.“

• Duke of Westminster (1935) All ER 259 principle continues to prevail:

“Every man is entitled if he can to order his affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be….Given that a

document or transaction is genuine, the court cannot go behind it to some supposed

underlying substance.”© Nishith Desai Associates

4

“Anyone may arrange his affairs so that his taxes shall be as low as

possible; he is not bound to choose that pattern which best pays the treasury.

There is not even a patriotic duty to increase one’s taxes. Over and over

again courts have said that there is nothing sinister in so arranging one’s affairs to

keep taxes as low as possible. Everybody does so, rich or poor, and all do right, for

nobody owes any public duty to pay more than the law demands:

taxes are enforced exactions, not voluntary contributions.”

- Learned Hand, J

(Commissioner v. Newman, 159 F.2d 848 CA-2, 1947)

© Nishith Desai Associates

5

“If one scans through the various judgments of the House of Lords in England, which

we have already done, one thing is clear that it has been a cornerstone of law,

that a tax payer is enabled to arrange his affairs so as to reduce the

liability of tax and the fact that the motive for a transaction is to avoid tax does not

invalidate it unless a particular enactment so provides.”

(Vodafone International Holdings v. Union of India, (2012) 341 ITR 1, para 115 of

Supreme Court’s decision dated January 20, 2012)

© Nishith Desai Associates

6

The Mauritius Route

© Nishith Desai Associates

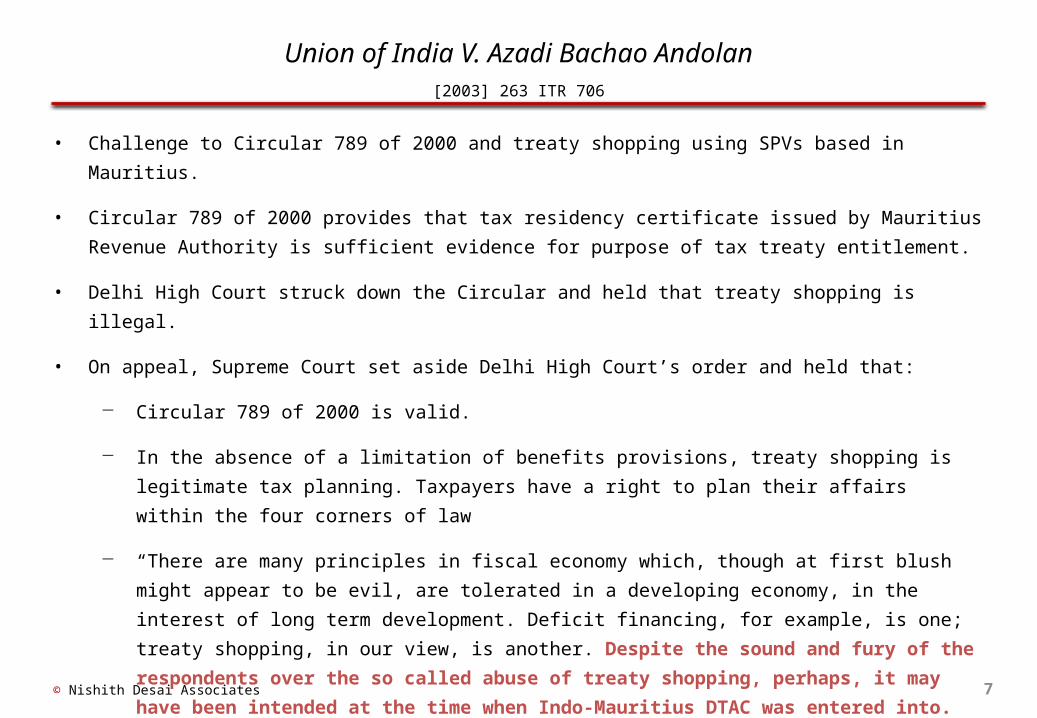

Union of India V. Azadi Bachao Andolan[2003] 263 ITR 706

7

• Challenge to Circular 789 of 2000 and treaty shopping using SPVs based in Mauritius.

• Circular 789 of 2000 provides that tax residency certificate issued by Mauritius Revenue

Authority is sufficient evidence for purpose of tax treaty entitlement.

• Delhi High Court struck down the Circular and held that treaty shopping is illegal.

• On appeal, Supreme Court set aside Delhi High Court’s order and held that:

− Circular 789 of 2000 is valid.

− In the absence of a limitation of benefits provisions, treaty shopping is legitimate tax

planning. Taxpayers have a right to plan their affairs within the four corners of law

− “There are many principles in fiscal economy which, though at first blush might appear to be evil, are

tolerated in a developing economy, in the interest of long term development. Deficit financing, for

example, is one; treaty shopping, in our view, is another. Despite the sound and fury of the

respondents over the so called abuse of treaty shopping, perhaps, it may have been intended

at the time when Indo-Mauritius DTAC was entered into. Whether it should continue, and, if so,

for how long, is a matter which is best left to the discretion of the executive as it is dependent

upon several economic and political considerations.”

© Nishith Desai Associates

Mauritius Route Consistently Upheld

8

• E* Trade Mauritius v. DIT, (2010) 324 ITR 1

• Praxair Pacific v. DIT, (2010) 326 ITR 276

• D.B. Zwirn Mauritius v. DIT, (2011) 240 CTR (AAR) 6

• In Re : Ardex Investments Mauritius, (2012) 340 ITR 272

• Vodafone International Holdings v. Union of India, [2012]341ITR1

© Nishith Desai Associates

9

Vodafone

(2012) 341 ITR 1 (Supreme Court)

© Nishith Desai Associates

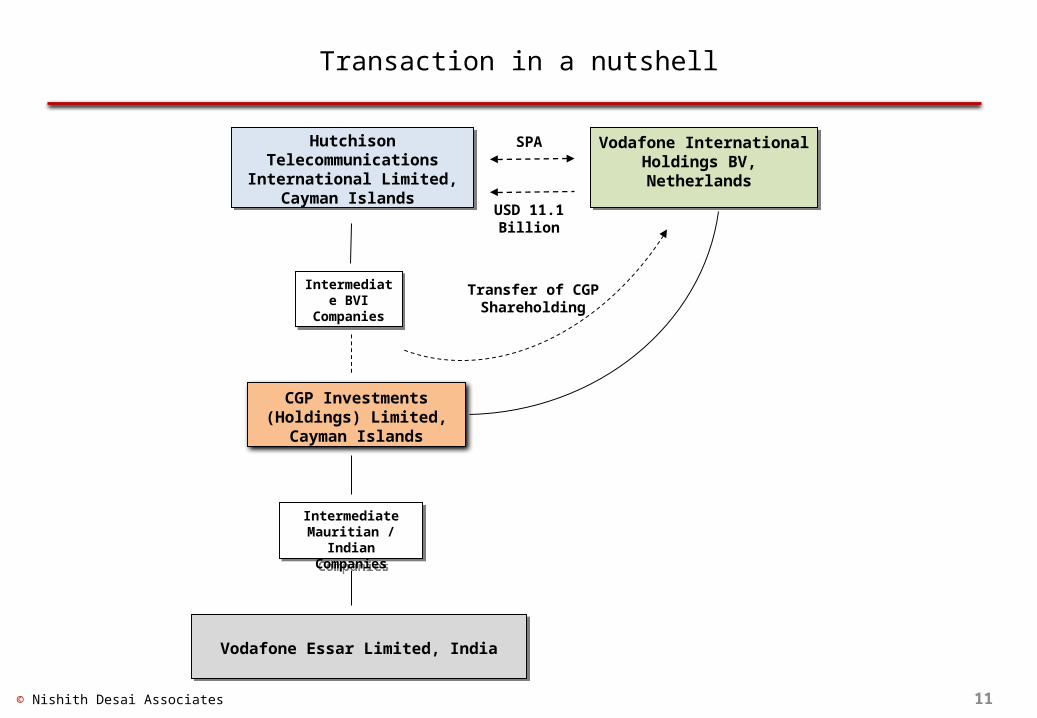

10© Nishith Desai Associates

British Virgin Islands

Netherlands

Cayman Islands

Transaction in a nutshell

11

Hutchison Telecommunications

International Limited, Cayman Islands

Hutchison Telecommunications

International Limited, Cayman Islands

Vodafone International Holdings BV, Netherlands

Vodafone International Holdings BV, Netherlands

USD 11.1 Billion

Intermediate BVI

Companies

Intermediate BVI

Companies

CGP Investments (Holdings) Limited,

Cayman Islands

Intermediate Mauritian /

Indian Companies

Intermediate Mauritian /

Indian Companies

Vodafone Essar Limited, IndiaVodafone Essar Limited, India

© Nishith Desai Associates

Transfer of CGP Shareholding

SPA

Revenue’s Case

12

Consideration paid by Vodafone to Hutch is taxable in India because in

substance it led to the transfer of interests and business in India

Vodafone should have withheld tax on the transaction

© Nishith Desai Associates

Revenue’s Arguments

13

• Sale of share of Cayman company was an artificial anti-avoidance scheme

• Cayman company interposed in the last minute

• Transaction led to the transfer of direct and indirect rights in Hutch Essar (India)

• Entire purpose of acquiring Cayman company was to assume control over Indian business

• Controlling interest and other rights are transferable property rights

• Transaction led to transfer (extinguishment) of Cayman seller’s property rights in India

• Sale of Cayman company’s share was only a mode to transfer capital assets in India

• Court must use the Dissecting Approach

− Identifying substance by dissecting individual elements / agreements of the transaction

instead of ‘looking at’ the form of the transaction as a whole

© Nishith Desai Associates

Revenue’s dissecting approach

14

1. Right to direct / indirect equity interest in HEL

2. Right to do telecom business in India

3. Right to jointly own and avail of telecom licenses

4. Right to use Hutch brand

5. Right to appoint / remove directors on HEL’s Board

6. Right to exercise control over HEL’s management & affairs

7. Right to take part in HEL’s investment, management & financial decisions

© Nishith Desai Associates

8. Right over assigned loans and advances used for business in India

9. Right of subscribing at par value in certain Indian companies

10. Right to exercise call options with Indian companies

11. Right to control premium

12. Right to non-compete against HTIL within Indian territory

13. Right to consultancy support (Oracle license)

14. Goodwill, other intangible rights, etc.

Supreme Court’s Verdict

15

• Revenue does not have jurisdiction to proceed against Vodafone

• Offshore transaction was bonafide and not a sham

• Revenue was not justified in disregarding the form of the transaction

• Subject matter of the transaction was the transfer of shareholding in a foreign company

• No transfer of rights and entitlements in India

• There is no provision in law permitting the taxation of such a transfer

• Revenue does not have territorial tax jurisdiction to tax such an offshore transaction

• Vodafone was not require to withhold an tax on the USD 11.1 billion paid to Hutch

• Revenue to return INR 2,500 crores deposited by Vodafone along with 4% interest

© Nishith Desai Associates

Respecting the form of the transaction

16

• Revenue to ‘look at’ at the transaction documents in its proper context and ascertain true legal nature of transaction

• Look at the transaction holistically: Do not apply dissecting approach

• Difference between pre-ordained tax-avoidance transaction and investment to participate in India

• Strategic investment by foreign residents to be viewed in a holistic manner:

− Participation in investment

− Duration of holding structure

− Period of business operation

− Generation of taxable revenues in India

− Continuity of business on exit

• Corporate veil to be pierced only if the transaction is sham

© Nishith Desai Associates

Dynamics of cross-border holding structures

17

• MNCs create elaborate horizontal and vertical holding structures for a number of strategic reasons

− Corporate governance

− Operational efficiency

− Ring fencing legal liabilities

− Hedging business risks

− Consolidation

− Leverage

− Mobility of investments

− Tax efficient structures to prevent double taxation

− Efficient exit route

− Maximizing value to shareholders

© Nishith Desai Associates

Respecting the corporate veil

18

• Company and shareholders are distinct legal entities having separate corporate personalities

(Rule in Salomon v. Salomon [1897] AC 22)

• Corporate veil should not be lifted just because:

− Parent company holds 100% of shareholding in subsidiary

− Subsidiary has received all its funds from its parent company

− Parent company exercises shareholder control or specific management rights over subsidiary

− Foreign holding company has no assets other than investment in India

− Parent company has played a role in the negotiation of contracts entered into by the subsidiary

− Subsidiary transfers all its profits to the parent company

• Decisive criteria: Does the parent company exercise “such steering interference with

the subsidiary’s core activities that the subsidiary can no longer be regarded to

perform those activities on the authority of its own executive directors”

© Nishith Desai Associates

Vodafone-Hutch structure is legitimate tax planning

19

• Supreme Court applied the ‘look at’ test while holding that the Vodafone-Hutch structure is not

a sham

− Hutch structure was in place since 1994

− Hutch India has paid direct / indirect taxes of around INR 20,242 crore

− There has been continuity of telecom business by Vodafone post transaction

− Downstream Hutch subsidiaries were not mere puppets. They only exercised persuasive

power over subsidiaries in the interest of smooth functioning of the group

− Exit rights (including options, right of first refusal, tag along rights) coupled with

continuity of business indicates commercial / business substance of a transaction

− Rights identified by the Revenue neither flowed from the share purchase agreement nor

were legally transferable by the Cayman company

− Sale of the Cayman company allowed Vodafone to acquire interests in other key operating

companies which would not have been possible if it directly acquired the shares of Hutch

India from the Mauritian holding companies© Nishith Desai Associates

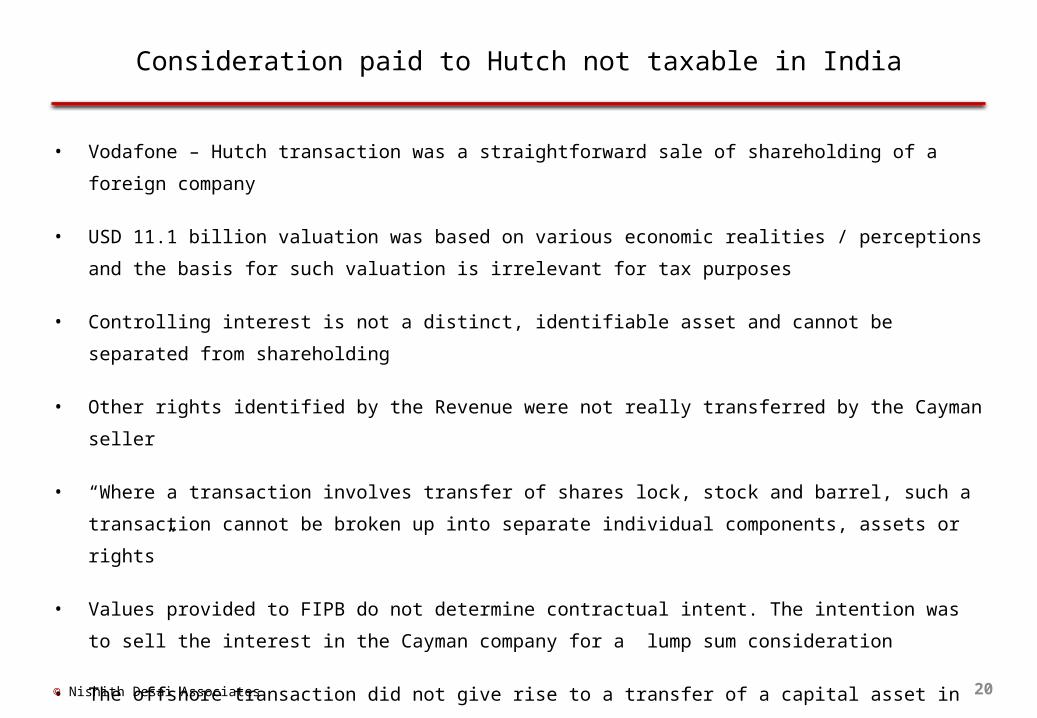

Consideration paid to Hutch not taxable in India

20

• Vodafone – Hutch transaction was a straightforward sale of shareholding of a foreign company

• USD 11.1 billion valuation was based on various economic realities / perceptions and the basis

for such valuation is irrelevant for tax purposes

• Controlling interest is not a distinct, identifiable asset and cannot be separated from

shareholding

• Other rights identified by the Revenue were not really transferred by the Cayman seller

• “Where a transaction involves transfer of shares lock, stock and barrel, such a transaction

cannot be broken up into separate individual components, assets or rights”

• Values provided to FIPB do not determine contractual intent. The intention was to sell the

interest in the Cayman company for a lump sum consideration

• The offshore transaction did not give rise to a transfer of a capital asset in India. The

consideration received by Hutch was not taxable since the income did not arise in India

© Nishith Desai Associates

Mauritius route upheld

21

• The Supreme Court upholds its earlier decision in Azadi Bachao Andolan (2003) 263 ITR 706

• Mauritius tax treaty does not have a ‘limitation of benefits clause’

“No presumption can be drawn that the Union of India or the Tax Department is unaware that

the quantum of both FDI and FII do not originate from Mauritius but from other global investors

situate outside Mauritius.” Para 95, Radhakrishnan, J

• LOB and look through provisions cannot be read into a tax treaty

“In the absence of LOB Clause and the presence of Circular No. 789 of 2000 and TRC

certificate, on the residence and beneficial interest/ownership, tax department cannot at the

time of sale/disinvestment/exit from such FDI, deny benefits to such Mauritius companies of

the Treaty by stating that FDI was only routed through a Mauritius company” Para 97,

Radhakrishnan, J

• TRC does not prevent enquiry into tax fraud, sham, round tripping, etc.

© Nishith Desai Associates

22

Impact of Vodafone on

similar M&A cases

© Nishith Desai Associates

23© Nishith Desai Associates

Transfer of AT&T Mauritius shares for USD 150 million

AT&T Mauritius

Idea Cellular, IndiaIdea Cellular, India

New Cingular Wireless Services Inc.

India

Birla Group,India

Financial Institutions,

India

Tata Industries,India

1.7% 33.7% 31.69%

32.91%

Transfer of Idea shares for USD 150

million

AT&T , Aditya Birla Nuvo2011 (113) Bom LR 2706

24© Nishith Desai Associates

ShanH, France

Shantha Biotechnics, India

Shantha Biotechnics, India

Groupe Industrial Marcel Dassault,

France

Sanofi Pasteur Holding, France

80%

Groupe Industrial Marcel Dassault,

France

Transfer of ShanH shares for INR 25 billion

Sanofi(2012) 340 ITR 353

25© Nishith Desai Associates

Mauritius Co

Indian CoIndian Co

25.06%

A Mauritus, In re[2012] 20 Taxmann 52

US Co Singapore Co

48.87% 27.37%

SH

AR

E

BU

YB

AC

K

Singapore Parent Co

US Parent Co

Thank You

Nishith Desai AssociatesLegal & Tax Counsel ing Worldwide

Mumbai | Silicon Valley | Bangalore | Singapore | Mumbai-BKC | New Delhi

Girish Dave

Mahesh Kumar