52 week high/low 57/27 (Wholly owned subsidiary of Bank of ... Fire Protectio… · Nitin Fire...

21

(Wholly owned subsidiary of Bank of Baroda) Exhibit 1: Financial summary (Rs mn) Year end: March FY13 FY14 FY15e FY16e FY17e FY18e Net sales 7047 10161 11466 14570 19323 26263 Growth (%) 31.5 44.2 12.8 27.1 32.6 35.9 Operating margin (%) 11.4 11.2 10.1 11.0 11.8 12.6 PAT 614 665 671 1091 1720 2687 Adjusted PAT 594 714 671 1091 1720 2687 EPS (Rs) 2.0 2.4 2.3 3.7 5.9 9.2 Growth (%) 35.0 20.2 -6.0 62.6 57.6 56.2 P/E(x) 22.0 18.3 19.5 12.0 7.6 4.9 ROE (%) 20.4 20.7 16.5 22.4 28.0 32.7 ROCE (%) 13.5 14.0 13.1 16.5 20.3 24.4 Debt/equity (x) 1.11 1.06 0.94 0.81 0.66 0.50 P/Bv (x) 3.1 2.6 2.9 2.4 1.9 1.4 Source: Company, BOBCAPSe Nitin Fire Protection Industries Ltd. आग से स ु रा, कर अपनी रा ; initiate with BUY Any casualty from fire can be avoided if a proper fire protection system is in place. Fire protection industry plays an important role in safeguarding human life and capital. Nitin Fire Protection industries (NFPIL) is one of the key listed player who works in this space. NFPIL has certification from various institutes, which gives them an edege to sustain against competetion. We expect, NFPIL to drive its revenue/earnings growth at a CAGR of ~31.8/41.8% over FY15-18e respectively mainly due to 1) strong existing order book from India (~Rs 3.5bn orders to be executed in 7-8 months) and UAE & GCC (~Rs 14bn orders to be executed in 18 months) 2) growing opportunities in India from industrial/Infrastructure developments under the ‘Make in India’ project 3) Government of India’s thrust for 98 smart cities across the Country 4) growing opportunities in rest of the world (RoW) and in UAE under mission 2020 (UAE Government to invest USD 19.6bn for mission 2020). All the above factors can create a strong road map for NFPIL’s overall growth. We initiate coverage on NFPIL with a ‘BUY’ rating and a price target of Rs.88 (97% upside) Mumbai Fire Brigade Chief’s thoughts on fire safety: We recently released a report on fire safety & interviewed Mumbai Fire Bridage’s Chief Fire Officer, Mr. Prabhat Rahangdale, where we realised, fire safety is of utmost importance & is most ignored. This leaves the entire country in a very sorry state. Therefore, companies like NFPIL are very critical from the point of view of national safety and security of assets. Strong order book: NFPIL is present in the fire protection systems industry where 75%of revenue comes from EPC business (where NFPIL has orderbook) and rest of the business comes from distribution. NFPIL’s revenue has grown at a CAGR of ~29% over FY12-FY15. Going forward, NFPIL has an order book of ~Rs 17.5bn (~Rs 3.5bn from India-completed in to 8-9months and ~Rs 14bn from RoW – completed in to 18 month). Also the company has bid for tender worth Rs 42bn (~Rs 12bn from India and ~Rs 30bn from RoW). We believe that such a robust order book will aid NFPIL to grow at a CAGR of ~32% over FY15-18e. Opportunities from India and RoW: Apart from the strong order book of ~Rs 17.5bn, the company has tremendous opportunities coming up from India and RoW. In India, ‘Make in India’/ industrial corridor and 98 smart cities will create enormous opportunities for industrial growth which will lead to growth of fire protection market (~4%of total expenditure of projects used on fire protection system). Also, Row is expected to be a ~USD 100bn market (growing at a CAGR of 15%). Valuation: We believe with the orders worth ~Rs 17.5bn in hand, prospective orders of ~Rs 42bn, and prospective infrastructure growth in India and UAE & GCC region, can take NFPIL to the next orbit than our guesstimates. We assign 15x to FY17e EPS of Rs 5.9 and arrive to the target price of Rs 88 with a potential upside of 97%. Vaishali Parkar Kumar | [email protected] | +91 22 6138 9382 Rishabh Mehta| [email protected] | +91 22 6138 9384 Price Price Target Up/Down (%) Rs. 45 Rs. 88 Bloomberg Code NFPI IN NIFP.NS Share Holding (%) Promoters 71.89 FII 12.75 DIIs 2.51 Stock Data Nifty 8,002 Sensex 26,392 52 week high/low 57/27 Maket Cap (Rs. bn) 13.0 Face Value Rs.2 Price performance (%) 1M 3M 6M 1Y Absolute 39.6 43.4 10.3 -5.9 Relative to Sensex 45.7 48.6 20.4 -5.0 Relative Performance 97% Reuters Code As on 30th June 2015 50 70 90 110 130 150 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 BSE Sensex Nitin Fire Source:-Bloomberg SECTOR: INDUSTRIAL MACHINERY Link to our report on Fire Safety- a CSR Initiative https://www.barodaetrade.com/Upload/DownLoad s/Fire%20Safety%20%20Report%20a%20CSR% 20Initiative.pdf Initiating coverage BUY 31 st August, 2015

Transcript of 52 week high/low 57/27 (Wholly owned subsidiary of Bank of ... Fire Protectio… · Nitin Fire...

(Wholly owned subsidiary of Bank of Baroda)

Exhibit 1: Financial summary (Rs mn) Year end: March FY13 FY14 FY15e FY16e FY17e FY18e

Net sales 7047 10161 11466 14570 19323 26263 Growth (%) 31.5 44.2 12.8 27.1 32.6 35.9 Operating margin (%) 11.4 11.2 10.1 11.0 11.8 12.6 PAT 614 665 671 1091 1720 2687 Adjusted PAT 594 714 671 1091 1720 2687 EPS (Rs) 2.0 2.4 2.3 3.7 5.9 9.2 Growth (%) 35.0 20.2 -6.0 62.6 57.6 56.2 P/E(x) 22.0 18.3 19.5 12.0 7.6 4.9 ROE (%) 20.4 20.7 16.5 22.4 28.0 32.7 ROCE (%) 13.5 14.0 13.1 16.5 20.3 24.4 Debt/equity (x) 1.11 1.06 0.94 0.81 0.66 0.50 P/Bv (x) 3.1 2.6 2.9 2.4 1.9 1.4 Source: Company, BOBCAPSe

$CompanyN ame$

Nitin Fire Protection Industries Ltd.

आग से सुरक्षा, करें अपनी रक्षा ; initiate with BUY

Any casualty from fire can be avoided if a proper fire protection system is in place. Fire protection industry plays an important role in safeguarding human life and capital. Nitin Fire Protection industries (NFPIL) is one of the key listed player who works in this space. NFPIL has certification from various institutes, which gives them an edege to sustain against competetion. We expect, NFPIL to drive its revenue/earnings growth at a CAGR of ~31.8/41.8% over FY15-18e respectively mainly due to 1) strong existing order book from India (~Rs 3.5bn orders to be executed in 7-8 months) and UAE & GCC (~Rs 14bn orders to be executed in 18 months) 2) growing opportunities in India from industrial/Infrastructure developments under the ‘Make in India’ project 3) Government of India’s thrust for 98 smart cities across the Country 4) growing opportunities in rest of the world (RoW) and in UAE under mission 2020 (UAE Government to invest USD 19.6bn for mission 2020). All the above factors can create a strong road map for NFPIL’s overall growth. We initiate coverage on NFPIL with a ‘BUY’ rating and a price target of Rs.88 (97% upside)

Mumbai Fire Brigade Chief’s thoughts on fire safety: We recently released a report on fire safety & interviewed Mumbai Fire Bridage’s Chief Fire Officer, Mr. Prabhat Rahangdale, where we realised, fire safety is of utmost importance & is most ignored. This leaves the entire country in a very sorry state. Therefore, companies like NFPIL are very critical from the point of view of national safety and security of assets.

Strong order book: NFPIL is present in the fire protection systems industry where 75%of revenue comes from EPC business (where NFPIL has orderbook) and rest of the business comes from distribution. NFPIL’s revenue has grown at a CAGR of ~29% over FY12-FY15. Going forward, NFPIL has an order book of ~Rs 17.5bn (~Rs 3.5bn from India-completed in to 8-9months and ~Rs 14bn from RoW – completed in to 18 month). Also the company has bid for tender worth Rs 42bn (~Rs 12bn from India and ~Rs 30bn from RoW). We believe that such a robust order book will aid NFPIL to grow at a CAGR of ~32% over FY15-18e.

Opportunities from India and RoW: Apart from the strong order book of ~Rs 17.5bn, the company has tremendous opportunities coming up from India and RoW. In India, ‘Make in India’/ industrial corridor and 98 smart cities will create enormous opportunities for industrial growth which will lead to growth of fire protection market (~4%of total expenditure of projects used on fire protection system). Also, Row is expected to be a ~USD 100bn market (growing at a CAGR of 15%).

Valuation: We believe with the orders worth ~Rs 17.5bn in hand, prospective orders of ~Rs 42bn, and prospective infrastructure growth in India and UAE & GCC region, can take NFPIL to the next orbit than our guesstimates. We assign 15x to FY17e EPS of Rs 5.9 and arrive to the target price of Rs 88 with a potential upside of 97%.

Vaishali Parkar Kumar | [email protected] | +91 22 6138 9382

Rishabh Mehta| [email protected] | +91 22 6138 9384

Price Price Target Up/Down (%)

Rs. 45 Rs. 88

Bloomberg Code

NFPI IN NIFP.NS

Share Holding (%)

Promoters 71.89

FII 12.75

DIIs 2.51

Stock Data

Nifty 8,002

Sensex 26,392

52 week high/low 57/27

Maket Cap (Rs. bn) 13.0

Face Value Rs.2

Price performance (%) 1M 3M 6M 1Y

Absolute 39.6 43.4 10.3 -5.9

Relative to Sensex 45.7 48.6 20.4 -5.0

Relative Performance

97%

Reuters Code

As on 30th June 2015

50

70

90

110

130

150Se

p-1

4

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

BSE Sensex Nitin Fire

Source:-Bloomberg

BUY

SECTOR: INDUSTRIAL MACHINERY 29th August, 2015

Link to our report on Fire Safety- a CSR Initiative

https://www.barodaetrade.com/Upload/DownLoads/Fire%20Safety%20%20Report%20a%20CSR%20Initiative.pdf

Initiating coverage

BUY

31st August, 2015

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 2

(Wholly owned subsidiary of Bank of Baroda)

Industry Outlook

Fire protection systems play a crucial role in preventing fire hazards. The increased risk of fire

accidents is driving the demand for fire protection systems market globally. The fire protection

systems market has experienced continuous advancement in fire protection technology.

Active fire safety systems and passive fire safety systems are the two broad segments of fire

safety systems markets. Active fire safety systems comprise of different types of firefighting

equipment and suppression systems like CO2, FM 200, and NOVEC, to suit specific

requirements. Automatic fire sprinklers coupled with detection are the most effective fire

protection system found in High Rise buildings/ industrial area which can, not only detect the

fires, but also extinguish the fires in the initial stage itself.

Passive fire safety systems include fire-resistant walls, load bearing columns and beams, and

fire-resistant floors and doors. These systems are used to protect the building structure against

collapse and prevent the spread of fire to other areas.

Global Fire protection Industry

Global Fire & Security market is estimated to be ~USD 100bn, growing in excess of GDP and

is expected to grow at CAGR of ~15%. This industry is currently lead by TYCO having 12% of

the market share along with UTC, Honeywell, Siemens in this space.

The Gulf region's fire safety systems market, (worth USD 1.2bn in 2013), is expected to grow

at 14.4% up to 2018, as end-users ramp up efforts to protect their critical infrastructure and

commercial projects. The surge in regional fire safety demand in key segments such as

petrochemicals, oil and gas, commercial and residential buildings, tunnels, airports, public

facilities and schools, presents major growth opportunities for global players to capitalise on.

The market is highly fragmented market with top five players account for less than 20% share.

NFPIL currently enjoys 0.1% share of the Global Fire Industry. There is a definite demand for

Fire Protection products worldwide with newer products under development. The Innovation

and Product Development are the critical aspects of success in the industry.

Indian Fire protection Industry

According to 'India Fire Safety Equipment’s Market Forecast & Opportunities, 2017', the fire

safety equipment market in India is expected to grow significantly in the next five years and to

surpass USD 4.26bn by the end of 2017.

The Indian Government is investing heavily in infrastructure development, upgrading existing

airports and setting up new airports and metros in various cities in India.

As in India large refineries, petrochemical complexes, biotechnology ventures, pharmaceutical,

automobile, steel, oil & gas exploration projects need to comply with various mandatory safety

regulation, these segments has been contributing hugely to the growth of the country’s fire &

safety market. The rapidly expanding IT and retail markets across the country have

significantly contributed towards the growth of the fire & safety equipment sector, and this

trend is likely to continue over the coming years.

Global Fire & Security industry estimated to be at ~USD100bn; expected to grow at CAGR of ~15%

Indian Fire &Security industry is expected to surpass USD 4.26bn by end of 2017

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 3

(Wholly owned subsidiary of Bank of Baroda)

Investment rationale

Nitin Fire protection Industries Ltd. (NFPIL) is a comprehensive solutions provider with a

wide range of products ranging from basic level fire extinguishers to sophisticated fire

protection systems and gas based suppression systems for mission critical areas as well

as services.

NFPIL is betting on India and UAE & GCC market led by a higher economic growth in

these countries which will help NFPIL to grow at a much higher pace (~4% of the total

infrastructure cost of any project is invested on the fire safety).

We expect NFPIL to grow at a CAGR of ~31.8% over FY15-18e due to 1) strong existing

order book from India (~Rs 3.50bn orders to be executed in 7-8 months) and UAE & GCC

(~Rs 14bn orders to be executed in 18 months) 2) growing opportunities in India for

industrial/Infrastructure developments under the ‘Make in India’ project 3) Government of

India’s thrust for 98 smart cities across the Country 4) growing opportunities in UAE under

mission 2020 (UAE Government to invest USD 19.6bn for mission 2020)

Certifications from various institutes - a key to grow

Fire protection systems ensure reduction in loss of capital invested and human life. NFPIL

works in the fire protection space which is human life critical and requires proper certifications

from recognized authorities (which are involved in developing standards and certifying

products used in fire extinguishing, detection and annunciation systems; smoke control

systems; and systems that assist emergency responders).

Such certifications require stringent rules and practices to be followed by the company. Also,

these certificates give an edge to the company to work in a particular geography. NFPIL has

acquired different certification (~60 domestic & international) from different institutes, which

gives reliability on its products and edge over competition. NFPIL is mainly present into EPC

business where such certifications talk about its ability to handle critical projects.

Although these approvals require a lot of investment (which the company writes off

every year; one of the reasons for lower EBITDA margins over past few years) can

create multifold opportunities in different countries. NFPIL is one of the company which

has maximum approvals from different entities, this will create huge opportunities for

the company.

Exhibit 2: Certifications received by NFPIL

Source: Company, BOBCAPSe

Certifications from various institutes Holds the key to get completion certificates.

Expenses on various certification can create a business opportunity for ~Rs 25-30bn over next few years

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 4

(Wholly owned subsidiary of Bank of Baroda)

Concentration on higher margins through EPC business

Under EPC contract, NFPIL gets industrial work where it bids for the contracts and completes

it in stipulated time. Generally, Fire protection systems could be ~4% of total infrastructure

project cost. NFPIL holds the key postion in terms of any infrastructure project getting

completion certificate, by sucessfully installing its fire protection system.

EPC gives NFPIL a steady visibility in revenue with higher margins (~20-22% EBITDA

margins) and the company is concentrating in India and UAE region for such projects.

Exhibit 3: Blended EBITDA margins for NFPIL

Revenue segment % contribution EBITDA margins Blende EBITDA

EPC 75% 20% 15

AMC contract 3-4% of EPC contracts 50% 1.5

Trading 20-25% 10% 2

Total blended EBITDA margins 18.5

Source: Company, BOBCAPSe

Blended EBITDA margins at 18.5%

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 5

(Wholly owned subsidiary of Bank of Baroda)

Growth opportunities in Middle East and GCC

NFPIL is present in UAE with its subsidiary Nitin Ventures FZE UAE and New Age Company

LLC UAE. The company took a wise decision of being a part of infrastructure development in

Middle East and GCC (Gulf Corporation Council) for its fire protection system. In these

countries the awareness for the risk of human life and capital expenditure is high which

percolates in to the full proof fire protection system. Also, critical industries like oil refineries

and exploration companies require high end systems in fire protection which can reduce

losses.

NFPIL with international certification and being the inventor of inert gas suppression system is

a preferable player in Middle East and GCC markets.

Exhibit 4: List of projects completed in UAE by NFPIL

Client Consultant Project

Meydan group llc Tak design consultant Dubai racing club cable tunnel

Tehnical engg cont Design & architecture bureau (g+2) madina mall

Sobha contracting National engineering bureau 3b+g+10 & 3b+g+4 bldg (daffodil)

Al masaood bergum Prime engineering Hameem resident

S.s.lootah Port saeed engg. Medical college

Emirates flight caterring Akkawi engineering Sp-751 renovation & improvement

Sobha contracting Al wasal Dubai police vip detection centre

Sobha contracting Dubai consultants 3b+g+3p+16 bldg.(sapphire)

Al raeel national Dorsch group 7500men camp

Arms electromechanical Saraya engineering Ware house ( tyre storage)

Modern bldg contg Bel yoahah architectural & engg. 2b+g+14 res/com bldg at al barsha

Naseem al sharq Safeer consultants Al foha mall

John sisk & son construction Upa Masfout hospital - ajman

Al hadi contracting Al arabia Lulu hypermarket

Sam building contracting Align consultant P713 caparol

City diamond cont Al takamul al handasi B+g+1 business bldg

Positiv epackaging Al jassim eng. Proposed warehous,g+m office and factory for postive packaging

Geaco Dastur consultant Executive hotel apartments

Yousuf & aman contg. Arch corp arch.eng. 3b+g+m+3 bldg.

Al hikma contg. Eng.adnan saffarini Factory & office

Aswan contg Arj consultant B+g+3 retail comm.bldg

Karyta gulf construction Al thorath engineering Tamm proto type at mirfa

Rsa logistics Torpy engineering (g+m) office warehouse

Khalfan al shaer ( desert fal) Bin dalmouk 2b+g+11+gym bldg

Amana steel Kling consultant Dj-179-dip-1 facilities famo 1& 2

Al attas contracting Civil defence fujairah Diretorate of civil defense @ fujairah

Tafseer general cont. Sustainable creative Ruwais camp

Darwish engg. Emirates Uae armed forces Misc construction at signal corps camp

S.s.lootah Port saeed engg. G+2 labour accomm.

Modern bldg contg Bel yoahah architectural & engg. B+g+12 bldg.

Zabeel contracting Art consultant B+g+7 bldg.

Al kauther contracting co Freeline eng.consultant Dewa (construction of combinated

Albatech construction The arab office Emirates steel industries

Source: Company, BOBCAPSe

Major growth to come from Middle East and GCC region

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 6

(Wholly owned subsidiary of Bank of Baroda)

Strong order book of ~Rs 14bn (RoW) to ensure revenue for next few years

NFPIL has a current order book of Rs ~14bn from UAE and GCC countries (to be executed in

18 months) and the company has bid for another Rs 30bn worth orders in this region. We

believe, this order book can increase over a period of time by looking at the infrastructure

development in these regions.

NFPIL has grown at a CAGR of ~28% over FY12-15 with the expansion in total revenue

contribution from 69% to 78% from FY11 to FY15. With the current order book of ~Rs 14bn to

complete in next 18 months, We feel, NFPIL has a huge opportunitiy in these countries and

can grow at a CAGR of ~28.7% over FY15-18e.

Exhibit 5: Revenue trend from rest of the world

0

10

20

30

40

50

-

5,000

10,000

15,000

20,000

FY13 FY14 FY15e FY16e FY17e F Y18e

(%)

Rs. M

n

Revenue from Rest of the world YoY growth %

Source: Company, BOBCAPSe

EXPO 2020 Dubai to create bigger opportunities for NFPIL

As per EXPO 2020 Dubai vision document, (running from 20 October 2020 through 10 April

2021), the Expo coincides with the country’s Golden Jubilee and will serve as a springboard to

launch a progressive and sustainable vision for the coming decades.

Preliminary estimates indicate that the economic impact generated by the Expo will be ~USD

19.6bn., to service the Expo, development will happen in tourism, aviation, construction, real

estate, engineering & infrastructure, logistics & transportation, and hospitality & retail, which

can create a huge opportunity for the fire protection system players and therefore for NFPIL.

Strong order book to drive revenue growth

~USD 19.6bn to be spent on EXPO 2020 Dubai

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 7

(Wholly owned subsidiary of Bank of Baroda)

Growth opportunities in India

Strong domestic order book

NFPIL has a current order book of Rs ~3.5bn from India (to be execute in next 7-8 month) and

the company has bid for another Rs 12bn worth orders. We believe, this order book can

increase over a period of time by looking at the development plans and the infrastructure

development under ‘Make in India’ and Industrial Corridor projects.

NFPIL has grown at a CAGR of ~30% over FY12-15 with the contribution to revenue at ~31%

to 22% from FY11 to FY15. We feel, NFPIL has a huge opportunities in India and can grow at

a CAGR of ~41% over FY15-18e led by 1) existing order book, 2) infrastructure development

through ‘Make in India’ and Industrial Corridor projects, 3) Govt. thrust for 98 smart cities

across the country in next five years.

Exhibit 6: Revenue trend from Indian operations

0

10

20

30

40

50

60

0

2000

4000

6000

8000

FY13 FY14 FY15e FY16e FY17e F Y18e

(%)

Rs. M

n

Revenue form Indian operations YoY growth %

Source: Company, BOBCAPSe

Growing investment in industrial development through ‘Make in India’ to boost revenue

Fire protection system is an important integrated services, which ensures that less damage

(human or capital) occurs due to fire. Typically 3-4% of budgeted cost of infrastructure projects

are spent on fire protection system for controlling loss arising from fire which becomes very

critical for any industry.

The Government of India’s thrust for ‘Make in India’ and industrial corridor projects will be a big

opportunity for India to spend over infrastructure. And any infrastructure projects (manufacturing

units, commercial/residential buildings) will require fire protection system.This can create a huge

opportunity for NIFPL to grow multifold.

Exhibit 7: Make in India - Sector wise Investments

Sector Total investment

Construction USD 1,000 bn

Pharmaceuticals USD 200 bn to be spent on infrastructure by 2024

Biotechnology USD 3.7 bn to be spent on biotechnology from 2012-17.

Defence Manufacturing INR 250 bn to be invested in 7-8 years.

Food Processing 42 mega food parks being set up with an allocated investment of INR 98 bn

Railways USD 1,000 bn worth of projects to be awarded through Public Private Partnership. According to the Railway budget 2015-16, Rs. 8,560 bn will be spent for the period 2015-19

Source: Company, BOBCAPSe

Strong order book from India shows revenue visibility

‘Make in India’ to boost revenue

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 8

(Wholly owned subsidiary of Bank of Baroda)

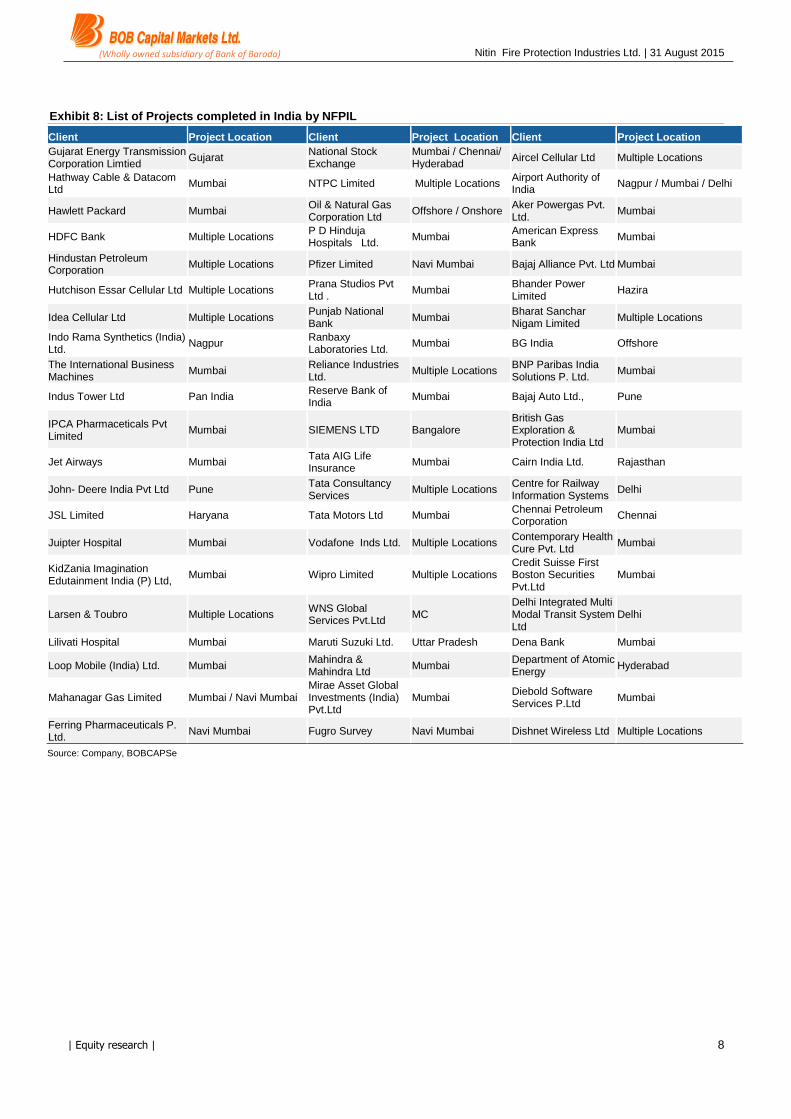

Exhibit 8: List of Projects completed in India by NFPIL

Client Project Location Client Project Location Client Project Location

Gujarat Energy Transmission Corporation Limtied

Gujarat National Stock Exchange

Mumbai / Chennai/ Hyderabad

Aircel Cellular Ltd Multiple Locations

Hathway Cable & Datacom Ltd

Mumbai NTPC Limited Multiple Locations Airport Authority of India

Nagpur / Mumbai / Delhi

Hawlett Packard Mumbai Oil & Natural Gas Corporation Ltd

Offshore / Onshore Aker Powergas Pvt. Ltd.

Mumbai

HDFC Bank Multiple Locations P D Hinduja Hospitals Ltd.

Mumbai American Express Bank

Mumbai

Hindustan Petroleum Corporation

Multiple Locations Pfizer Limited Navi Mumbai Bajaj Alliance Pvt. Ltd Mumbai

Hutchison Essar Cellular Ltd Multiple Locations Prana Studios Pvt Ltd .

Mumbai Bhander Power Limited

Hazira

Idea Cellular Ltd Multiple Locations Punjab National Bank

Mumbai Bharat Sanchar Nigam Limited

Multiple Locations

Indo Rama Synthetics (India) Ltd.

Nagpur Ranbaxy Laboratories Ltd.

Mumbai BG India Offshore

The International Business Machines

Mumbai Reliance Industries Ltd.

Multiple Locations BNP Paribas India Solutions P. Ltd.

Mumbai

Indus Tower Ltd Pan India Reserve Bank of India

Mumbai Bajaj Auto Ltd., Pune

IPCA Pharmaceticals Pvt Limited

Mumbai SIEMENS LTD Bangalore British Gas Exploration & Protection India Ltd

Mumbai

Jet Airways Mumbai Tata AIG Life Insurance

Mumbai Cairn India Ltd. Rajasthan

John- Deere India Pvt Ltd Pune Tata Consultancy Services

Multiple Locations Centre for Railway Information Systems

Delhi

JSL Limited Haryana Tata Motors Ltd Mumbai Chennai Petroleum Corporation

Chennai

Juipter Hospital Mumbai Vodafone Inds Ltd. Multiple Locations Contemporary Health Cure Pvt. Ltd

Mumbai

KidZania Imagination Edutainment India (P) Ltd,

Mumbai Wipro Limited Multiple Locations Credit Suisse First Boston Securities Pvt.Ltd

Mumbai

Larsen & Toubro Multiple Locations WNS Global Services Pvt.Ltd

MC Delhi Integrated Multi Modal Transit System Ltd

Delhi

Lilivati Hospital Mumbai Maruti Suzuki Ltd. Uttar Pradesh Dena Bank Mumbai

Loop Mobile (India) Ltd. Mumbai Mahindra & Mahindra Ltd

Mumbai Department of Atomic Energy

Hyderabad

Mahanagar Gas Limited Mumbai / Navi Mumbai Mirae Asset Global Investments (India) Pvt.Ltd

Mumbai Diebold Software Services P.Ltd

Mumbai

Ferring Pharmaceuticals P. Ltd.

Navi Mumbai Fugro Survey Navi Mumbai Dishnet Wireless Ltd Multiple Locations

Source: Company, BOBCAPSe

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 9

(Wholly owned subsidiary of Bank of Baroda)

Govt. thrust for smart cities; a big opportunity

As per the Govt. of India smart cities mission document, nearly 31% of India’s current

population lives in urban areas and contributes 63% of India’s GDP (Census 2011). With

increasing urbanization, urban areas are expected to house 40% of India’s population and

contribute 75% of India’s GDP by 2030. This requires comprehensive development of physical,

institutional, social and economic infrastructure. All are important in improving the quality of life

and attracting people and investments to the City, setting in motion a virtuous cycle of growth

and development. Development of Smart Cities is a step in that direction.

As per the Smart cities mission document, the mission will cover 98 cities in five years (FY16-

FY20). The total no. of smart cities have been distributed among the states and UT (United

Territories).

The Smart City Mission will be operated as a Centrally Sponsored Scheme (CSS) and the

Central Government proposes to give financial support to the Mission to the extent of Rs.

480bn over five years (on an average Rs. 1bn per city per year. An equal amount, on a

matching basis, will have to be contributed by the State/ULB), therefore, Rs ~1000bn of

Government/ULB funds will be available for Smart Cities development.

Such a huge investment in next five years will provide growth opportunities to many industries

including fire protection system. We believe, NIFPL can be a major beneficiary from this

scheme.

Exhibit 9: 98 cities to cover under Smart Cities project

State/Union Territory No. of Cities State/Union Territory No. of Cities

Andaman & Nicobar Islands 1 Madhya Pradesh 7

Andhra Pradesh 3 Maharashtra 10

Arunachal Pradesh 1 Manipur 1

Assam 1 Meghalaya 1

Bihar 3 Mizoram 1

Chandigarh 1 Nagaland 1

Chhattisgarh 2 Odisha 2

Daman & Diu 1 Puducherry 1

Dadra & Nagar Haveli 1 Punjab 3

Delhi 1 Rajasthan 4

Goa 1 Sikkim 1

Gujarat 6 Tamil Nadu 12

Haryana 2 Telangana 2

Himachal Pradesh 1 Tripura 1

Jharkhand 1 Uttar Pradesh 12

Karnataka 6 Uttarakhand 1

Kerala 1 West Bengal 4

Lakshaweep 1

Source: Industry, BOBCAPS

Small cities & smart cities to drive growth

As per the Smart cities mission document, 98 cities to be covered in five years (FY16-FY20)

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 10

(Wholly owned subsidiary of Bank of Baroda)

Calamites that could be avoided if the fire protection system would be in place

Infrastructure development is one of the primal reasons for a country’s growth. India is on

its growth path with numerous present and prospective infrastructure projects and the

numbers are bound to increase. With increase in such projects, the risks associated with

it also increases, specially the risk of fire. Effective safety measures have to be taken in

order to ensure that there is no/minimal loss arising due to it. Unfortunately, in India, fire

safety has been neglected and this negligence has led to various accidents resulting in

the loss of life and property.

Legislations: The legislations, standards and codes have a vital role in forcing the occupiers to

provide the required fire protection system, both active and passive. The National Building Code

of India, 2005, is the basic model code in India on matters relating to building construction and

fire safety. Many of the code provisions has been incorporated by various State Governments

and Local Bodies in their own building regulations. However, in India such rules and regulations,

code and standards related fire safety are seldom followed.

Casualty due to fires and related causes: On an average, in India, every year, about 25,000

persons die due to fires and related causes. It is estimated that about 42 females (66% killed in

fire accidents) and 21 males die every day in India due to fire. According to the statistics released

by the National Crime Records Bureau, fire accounts for about 5.9% (23,281) of the total deaths

reported due to natural and un-natural causes during the year 2012. Probably many of these

deaths could have been prevented, through enough fire protection measures.

economic losses suffered on account of fires: According to the INDUSTRIAL SAFETY

REVIEW Magazine on Fire Safety & Electronic Security Industry, the major losses reported by

the Indian Insurance Companies in the year 2007-2008 indicate, that about 45% of the claims are

due to fire losses. According to another estimate about Rs. 100bn are lost every year due to fire.

Fire losses are reported both in industrial and non-industrial premises like hospitals, commercial

complexes, educational institutions, assembly halls, hotels, residential buildings, etc.

Lives were lost, where they should have been saved

On 9 December 2011, a fire occurred at the Advanced Medical Research Institute (AMRI)

Hospital in South Kolkata early in the morning. The fire was due to alleged negligence, which

caused flammable substances kept in the basement of the building to catch fire after a short

circuit in the electrical system. It is reported that 95 people, including members of the staff, died

due to asphyxiation. There were 160 patients at the time of the incident, of which around 50 were

in the ICU.

Mumbai High Rise Fire

At least seven people lost their lives and 22 injured when a fire broke out in a 21-storey

residential building. The incident took place on 6 June 2015, in Chandivali, Mumbai. The blaze

occurred in the 14th floor of the residential complex ’Lake Homes’, initially, but soon spread on to

the 15th floor. Fifteen fire tenders were rushed to the spot to respond to the Grade 2 fire.

Calamities could have been/can be avoided…

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 11

(Wholly owned subsidiary of Bank of Baroda)

Parliament without Fire safety Certificate

As per articles, the Parliament House, one of India's most protected structures, spread over 12

acres does not have a fire safety certificate for nearly a decade. The building has seen two fires

recently.

In August 2013, the Delhi Fire Service carried out an inspection of the 12-gated complex and

recommended corrective measures to the Lok Sabha Secretariat. Some changes were made -

high power hoses, hydrant systems and smoke detectors were installed.

The fire department also asked for the installation of sprinklers, modification of emergency exits

and rewiring of cables. But none of these are in place as per articles, so one of India's most

important buildings is functioning without a mandatory safety clearance.

Is our Route Relay interlocking systems safe?

As per the media report fire had broken out at the Route Relay Interlocking (RRI) panel at Itarsi

Railway Station (Madhya Pradesh, India on June 17, 2015), leading to major disruption in railway

traffic and leading to cancellation of 2,404 odd trains. It took ~34 days to get in to normalcy. As

per the reports, Indian railway had to incur loss over Rs 10bn. Such incidence could have been

avoided if the fire protection system would be at the RRI.

As per reports, there are more than 1400 electronic interlocking systems. These are very

important and a heart of an any railway transportation.

Exhibit 10: Numbers of stations with some form of electronic interlocking systems

India Railway routes No. of Interlocking system

Central Railway 18.00

Eastern Ralway 195.00

Northen Railway 263.00

North Eastern Railway 22.00

Northeast Frontier Railway 43.00

Southern Railway 55.00

South Central Railway 101.00

South Eastern Railway 132.00

Western Railway 44.00

East Central Railway 130.00

East Coast Railway 99.00

North Central Railways 154.00

North Western Railway 13.00

South East Central Railway 71.00

South western Railway 34.00

Western Central Railway 76.00

Total 1450.00

Source: Industry, BOBCAPS

Indian railway plans to spend ~USD 137bn in next five years to expand and modernise its vast railway network, which gives huge opportunities for the fire safety industry

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 12

(Wholly owned subsidiary of Bank of Baroda)

Growth opportunities in rest of the world

North American business opportunities – a bigger market to get a pie from

All developed markets keep human safety on a priority basis which creates an entry point for a

company like NFPIL (present in to full integrated fire protection system with various certification

from different institutions). NFPIL is planning to capture the gigantic North American market and

Europen markets. NFPIL is already present in the UK market with its subsidiary, Firetec Systems

Ltd., UK. The company is planning to enter into the North American market (estimated ~USD

20bn market) by FY18 and can get benefited from lower cost of production as compared to its

global competitor.

Well accepted auditor ‘Deloitte Haskins & sells LLP’ to add value in terms of global authenticity

NFPIL has ‘Haribhakti as their auditor from FY11. albeit it is very respected and reputed name in

domestic space. Howecver science the company is grow in the RoW, it is important that the

international top auditor is apoppinted to look after books of accounts. This gives tremendous

authenticity to the figure stated in annual report. From the investors and corporate governance

issue this becomes a major positive and reliable development.

‘Deloitte Haskins & sells LLP’ appointed as the joint statutory Auditorr

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 13

(Wholly owned subsidiary of Bank of Baroda)

Key risk

General economic and cyclical industry conditions may adversely affect the company

revenue: Any economic and cyclical downturn in industries like oil and gas, chemical and

petrochemical, mining and general industrial companies, can impact the liquidity and financial

position of its customers which can further impact their ability to pay in full and/or on a timely

basis. During such economic downturns, customers in these industries historically had tendency

to delay major capital projects, including Greenfield construction, expensive maintenance projects

and upgrades. Such incidence can create revenue risk for the company. However, NFPIL is well

diversified in terms of country and industry.

Delay in project completion by customers can impact revenue: NFPIL is mainly into EPC

business (75% of total revenue) which requires project completion from customer’s side. Any

delay in project completion can impact NFPIL’s revenue for that period

Currency risk: NFPIL’s ~Rs.8.9bn revenue came from outside India (in FY15) which contributes

around 78% of total revenue. Also, the company imports ~30-40% of the total cost of production

and therefore has a currency risk. NFPIL hedge ~50% at the time of purchases.

High working capital risk: NFPIL WCC is quite high (~156 days) led by EPC nature of business.

Any economic or cyclical downturn can create high working capital risk

Higher D:E ratio: D:E ratio (~0.9 by FY15) of the company is expected to remain at higher

trajectory for few years as NFPIL’s nature of business (higher short term loan), the company

invests in certifications from different entities (help to surge in revenue).

Status of accounts with banks:The account of a company is not NPA/ neither restructured, not

classified as stressed by any bank however, some delay in payment is reported.

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 14

(Wholly owned subsidiary of Bank of Baroda)

Valuation:

Nitin Fire Protection Industries Ltd. (NFPIL) is one of the key listed player in fire protection

system business. The company is present mainly in to industrial fire protaction with EPC

contracts. NFPIL has a strong order book of ~Rs 17.5bn (to be executed in next two years)

from India and RoW, also the company had bid for ~Rs42bn tenders.

NFPIL trades at 19.5x P/E, and we expect following factors will further drive the stock

upside: 1) fast earnings growth (~32% CAGR over FY15-FY18e), 2) improveing operating

leverage, 2) more certainty in revenue from focusing international business,

3)strengthening financial health with improveing ROE (from 16.5% in FY15 to 32.7% in

FY18e), 4) improving EBITDA margins ~250bps, 5) improvement in WCC

We believe with the orders ~Rs 17.5bn in hand, prospective orders of ~Rs 42bn, and

prospective infrastructure growth in India and UAE & GCC region can take NFPIL to next

orbit than our guesstimates. We assign 15x to FY17e EPS of Rs 5.9 and arrive to the

target price of Rs 88 with a potential upside of 97%.

Exhibit 11: One year forward PE chart

0

5

10

15

20

25

30

31

-Au

g-1

0

29

-Dec

-10

28

-Ap

r-1

1

26

-Au

g-1

1

24

-Dec

-11

22

-Ap

r-1

2

20

-Au

g-1

2

18

-Dec

-12

17

-Ap

r-1

3

15

-Au

g-1

3

13

-Dec

-13

12

-Ap

r-1

4

10

-Au

g-1

4

8-D

ec-1

4

7-A

pr-

15

5-A

ug-

15

(x)

PE(x) avg5 yr mean = 15x

Current = 5.8x

Source: Industry, BOBCAPS

Prospective infrastructure growth in India and UAE & GCC region can take NFPIL to next orbit than our guesstimates.

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 15

(Wholly owned subsidiary of Bank of Baroda)

Financial Summary

Strong order book to drive revenue growth: NFPIL has grown at a CAGR of~29% over FY12-

15. We expect NFPIL can grow at a CAGR of 31.8% over FY15-18e. The reason for the strong

growth would be 1) NFPIL has a total current order book of ~Rs17.5bn - Rs 14bn /Rs 3.5bn for

rest of the world /India, (to be executed in next 24 months/9months respectively), 2) infrastructure

development under Dubai vision 2020 , 3) infrastructure spending under ‘Make in India’ and

industrial corridor, 100 smart cities by 2019. We believe, all this infrastructure development will be

backed by proper safety (especially fire safety).

Exhibit 12: Net sales to grow at a CAGR of ~31.8% over FY-18e

(20.0)

-

20.0

40.0

60.0

80.0

-

5,000

10,000

15,000

20,000

25,000

30,000

FY13 F14 F15e F16e F17e F18e

%

Rs

mn

Net sales growth (%)

Source: Company, BOBCAPSe

EBITDA margin to improve by ~250 bps: NFPIL witnessed EBITDA margin contraction of ~250

bps due to policy of writing off the expenses incurred on R&D and obtaining various certificates

from Underwriter Laboratories, Conformité Européenne, Loss Prevention Certificate Board etc.

the expenditure incurred on obtaining these certificates is written off in the year when they are

incurred however, the benefits of the same Will be derieved over next few years amounting to

Rs ~20-25bn. We believe, these expenses in future will be much lower as compared to the

revenue growth the company may record over next few years. We expect EBITDA margin to

improve by ~250 bps led by optimum capacity utlisation and operational efficiency.

Exhibit 13: EBITDA margins to improve by ~250 bps

0.0

5.0

10.0

15.0

0

1000

2000

3000

4000

FY13 FY14 FY15e FY16e FY17e F Y18e

(%)

Rs.

Mn

EBITDA EBITDA margin %

Source: Company, BOBCAPSe

Strong order book of ~Rs 17.5bn to drive sales growth in next two years

EBITDA margins to show improvement led by optimum capacity utlisation and operational efficiency

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 16

(Wholly owned subsidiary of Bank of Baroda)

Return ratios to improve: NFPIL’s overall improvement in the operational efficiency

(Revenue/earnings CAGR growth of 31.5%/41.4% over FY15-18e) will improve its ROE and ROCE.

Exhibit 14: Return ratios to improve over FY15-18e

0

5

10

15

20

25

30

35

FY13 FY14 FY15e FY16e FY17e F Y18e

%

ROE ROCE

Source: Company, BOBCAPSe

Working capital cycle to improve: NFPIL always had high working capital cycle (~156 days)

due to its nature of business. The company is paying high interest cost which can be reduced if it opts for Foreign currency loan or EPBG (Export Promotion Bank Guaranty) options, however we have not factored in the benefits arising out of such transaction. However, with the sturdy revenue growth and improvement in profitability, we expect the company would be able to fund WCC through internal accruals. Further business efficiency will help to bring down the WCC going forward.

Exhibit 15: WCC to improve over a period of time

-10

20

50

80

110

140

170

FY13 FY14 FY15e FY16e FY17e F Y18e

No

fo

Da

ys

Debtors Days Inventory Days Creditors Days WCC

Source: Company, BOBCAPSe

ROE to improve from 16.5% in FY15 to 32.7% in FY18e

Further business efficiency will help to bring down the WCC going forward.

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 17

(Wholly owned subsidiary of Bank of Baroda)

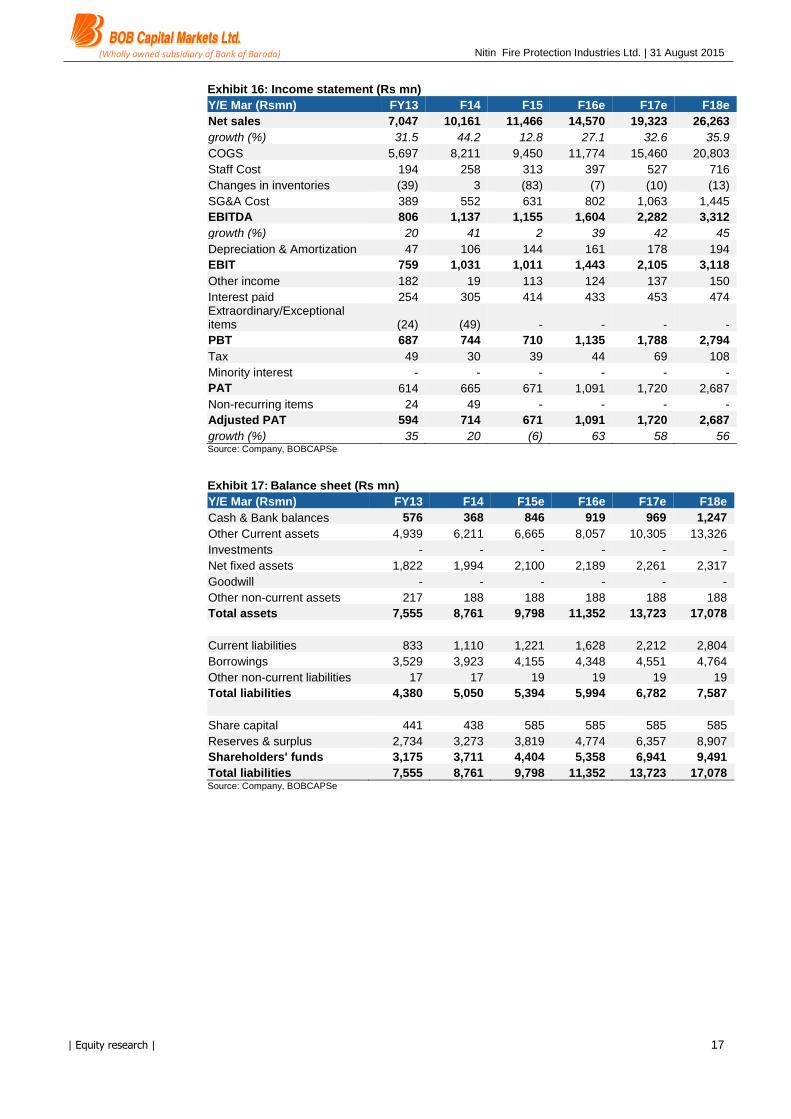

Exhibit 16: Income statement (Rs mn)

Y/E Mar (Rsmn) FY13 F14 F15 F16e F17e F18e

Net sales 7,047 10,161 11,466 14,570 19,323 26,263

growth (%) 31.5 44.2 12.8 27.1 32.6 35.9

COGS 5,697 8,211 9,450 11,774 15,460 20,803

Staff Cost 194 258 313 397 527 716

Changes in inventories (39) 3 (83) (7) (10) (13)

SG&A Cost 389 552 631 802 1,063 1,445

EBITDA 806 1,137 1,155 1,604 2,282 3,312

growth (%) 20 41 2 39 42 45

Depreciation & Amortization 47 106 144 161 178 194

EBIT 759 1,031 1,011 1,443 2,105 3,118

Other income 182 19 113 124 137 150

Interest paid 254 305 414 433 453 474 Extraordinary/Exceptional items (24) (49) - - - -

PBT 687 744 710 1,135 1,788 2,794

Tax 49 30 39 44 69 108

Minority interest - - - - - -

PAT 614 665 671 1,091 1,720 2,687

Non-recurring items 24 49 - - - -

Adjusted PAT 594 714 671 1,091 1,720 2,687

growth (%) 35 20 (6) 63 58 56 Source: Company, BOBCAPSe

Exhibit 17: Balance sheet (Rs mn)

Y/E Mar (Rsmn) FY13 F14 F15e F16e F17e F18e

Cash & Bank balances 576 368 846 919 969 1,247

Other Current assets 4,939 6,211 6,665 8,057 10,305 13,326

Investments - - - - - -

Net fixed assets 1,822 1,994 2,100 2,189 2,261 2,317

Goodwill - - - - - -

Other non-current assets 217 188 188 188 188 188

Total assets 7,555 8,761 9,798 11,352 13,723 17,078

Current liabilities 833 1,110 1,221 1,628 2,212 2,804

Borrowings 3,529 3,923 4,155 4,348 4,551 4,764

Other non-current liabilities 17 17 19 19 19 19

Total liabilities 4,380 5,050 5,394 5,994 6,782 7,587

Share capital 441 438 585 585 585 585

Reserves & surplus 2,734 3,273 3,819 4,774 6,357 8,907

Shareholders' funds 3,175 3,711 4,404 5,358 6,941 9,491

Total liabilities 7,555 8,761 9,798 11,352 13,723 17,078 Source: Company, BOBCAPSe

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 18

(Wholly owned subsidiary of Bank of Baroda)

Exhibit 18: Ratios

Y/E Mar FY13 F14 F15e F16e F17e F18e

Per share data (Rs)

EPS 2.0 2.4 2.3 3.7 5.9 9.2

CEPS 2.2 2.8 2.8 4.3 6.5 9.9

DPS 0.2 0.2 0.4 0.5 0.5 0.5

BV 14.4 16.9 15.1 18.3 23.7 32.5

Profitability ratios (%)

Gross margins 16.4 16.7 14.9 16.5 17.3 18.1

Operating margins 11.4 11.2 10.1 11.0 11.8 12.6

Net margins 8.4 7.0 5.9 7.5 8.9 10.2

Valuation ratios (x)

PE 22.0 18.3 19.5 12.0 7.6 4.9

P/BV 3.1 2.6 3.0 2.4 1.9 1.4

EV/EBITDA 15.9 11.7 14.2 10.3 7.3 5.0

EV/Sales 1.8 1.3 1.4 1.1 0.9 0.6

RoE 20.4 20.7 16.5 22.4 28.0 32.7

RoCE 13.5 14.0 13.1 16.5 20.3 24.4

RoIC 10 10 9 13 18 23

Source: Company, BOBCAPSe

Exhibit 19: Cash flow statement (Rs mn)

Y/E Mar (Rsmn) FY13 F14 F15e F16e F17e F18e

Profit after tax 570 665 671 1,091 1,720 2,687

Depreciation 30 99 144 161 178 194

Chg in working capital (396) (964) (341) (986) (1,663) (2,429)

Total tax paid (2) (2) - - - - Cash flow from operations 202 (202) 475 266 234 452

Capital expenditure (386) (271) (250) (250) (250) (250)

Change in investments - - - - - - Cash flow from investments (386) (271) (250) (250) (250) (250)

Free cash flow (184) (473) 225 16 (16) 202

Issue of shares - (3) 146 - - -

Net inc/dec in debt 603 394 231 193 203 213

Dividend (incl. tax) (13) (1) (1) (1) (1) (1)

Other financing activities (40) (125) (123) (136) (136) (136) Cash flow from financing 551 265 253 57 66 76 Inc/(Dec) in Cash & Bank bal. 367 (208) 478 73 51 278

Source: Company, BOBCAPSe

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 19

(Wholly owned subsidiary of Bank of Baroda)

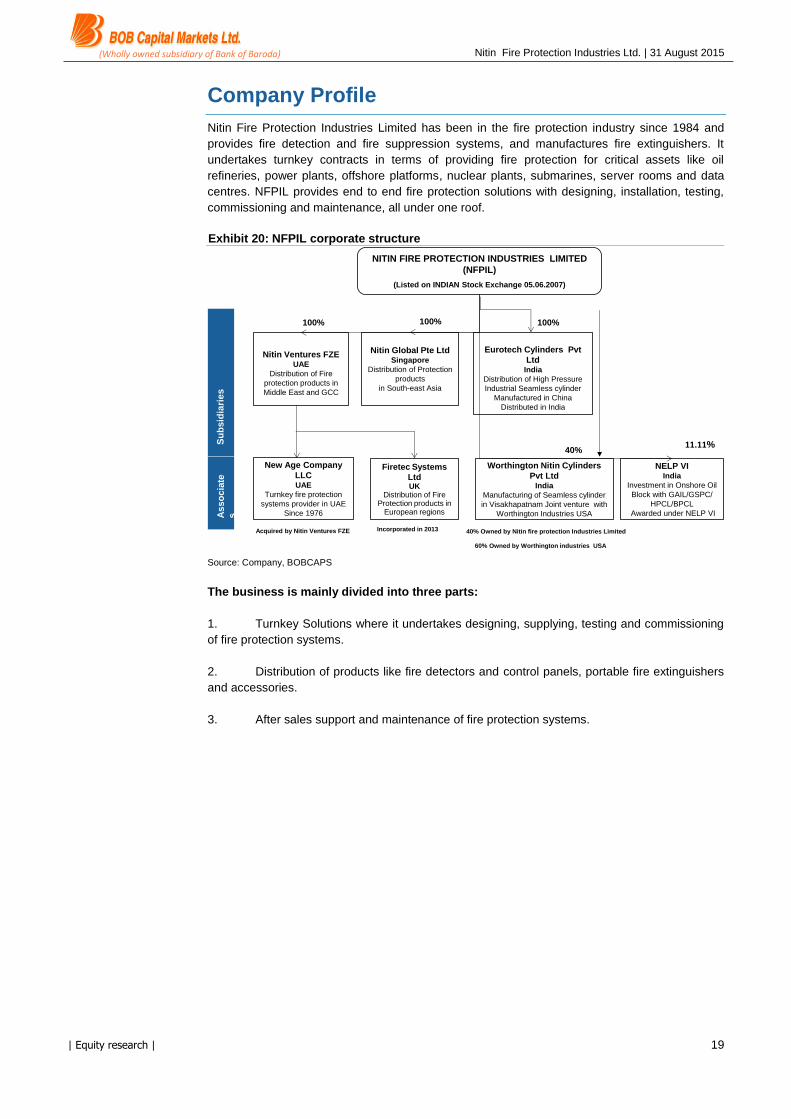

Company Profile

Nitin Fire Protection Industries Limited has been in the fire protection industry since 1984 and

provides fire detection and fire suppression systems, and manufactures fire extinguishers. It

undertakes turnkey contracts in terms of providing fire protection for critical assets like oil

refineries, power plants, offshore platforms, nuclear plants, submarines, server rooms and data

centres. NFPIL provides end to end fire protection solutions with designing, installation, testing,

commissioning and maintenance, all under one roof.

Exhibit 20: NFPIL corporate structure

Su

bs

idia

rie

sA

ss

oc

iate

s

Nitin Global Pte LtdSingapore

Distribution of Protection

products

in South-east Asia

Nitin Ventures FZEUAE

Distribution of Fire

protection products in

Middle East and GCC

Eurotech Cylinders Pvt

LtdIndia

Distribution of High Pressure

Industrial Seamless cylinder

Manufactured in China

Distributed in India

Worthington Nitin Cylinders

Pvt LtdIndia

Manufacturing of Seamless cylinder

in Visakhapatnam Joint venture with

Worthington Industries USA

New Age Company

LLCUAE

Turnkey fire protection

systems provider in UAE

Since 1976

100% 100%

40%

100%

NITIN FIRE PROTECTION INDUSTRIES LIMITED

(NFPIL)

(Listed on INDIAN Stock Exchange 05.06.2007)

NELP VIIndia

Investment in Onshore Oil

Block with GAIL/GSPC/

HPCL/BPCL

Awarded under NELP VI

11.11%

Firetec Systems

LtdUK

Distribution of FireProtection products in

European regions

60% Owned by Worthington industries USA

40% Owned by Nitin fire protection Industries LimitedIncorporated in 2013Acquired by Nitin Ventures FZE

Source: Company, BOBCAPS

The business is mainly divided into three parts:

1. Turnkey Solutions where it undertakes designing, supplying, testing and commissioning

of fire protection systems.

2. Distribution of products like fire detectors and control panels, portable fire extinguishers

and accessories.

3. After sales support and maintenance of fire protection systems.

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 20

(Wholly owned subsidiary of Bank of Baroda)

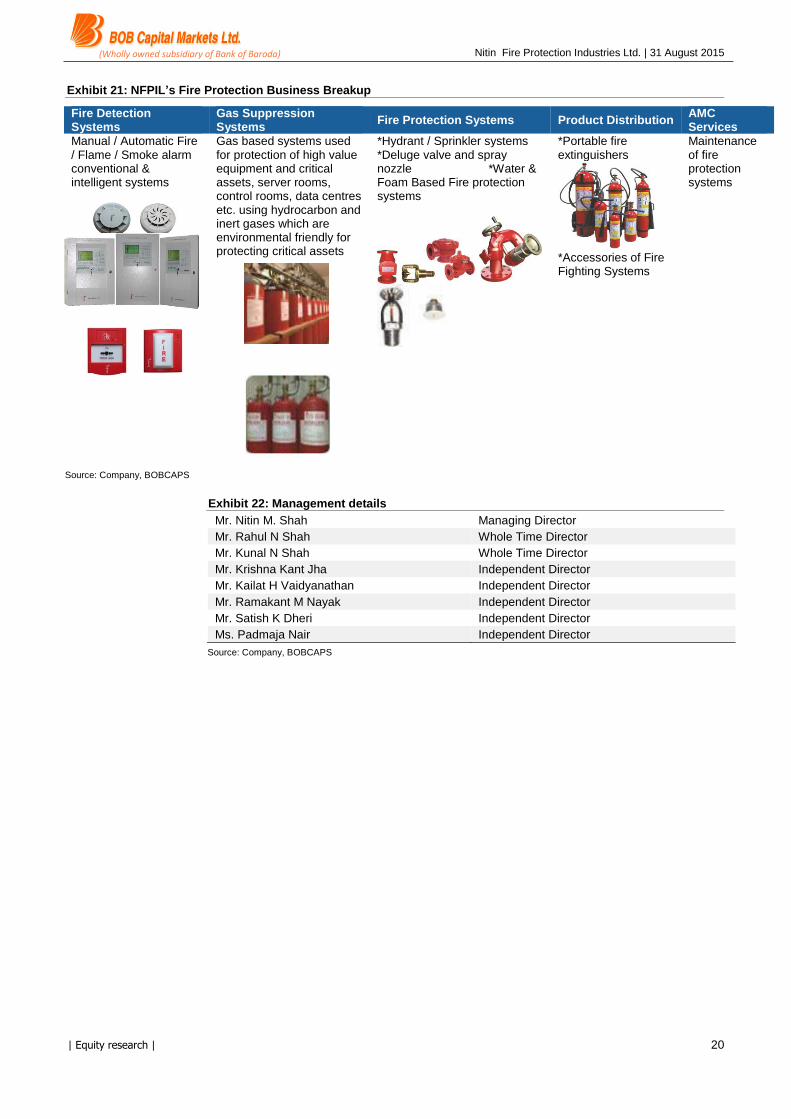

Exhibit 21: NFPIL’s Fire Protection Business Breakup

Fire Detection Systems

Gas Suppression Systems

Fire Protection Systems Product Distribution AMC Services

Manual / Automatic Fire / Flame / Smoke alarm conventional & intelligent systems

Gas based systems used for protection of high value equipment and critical assets, server rooms, control rooms, data centres etc. using hydrocarbon and inert gases which are environmental friendly for protecting critical assets

*Hydrant / Sprinkler systems *Deluge valve and spray nozzle *Water & Foam Based Fire protection systems

*Portable fire extinguishers

*Accessories of Fire Fighting Systems

Maintenance of fire protection systems

Source: Company, BOBCAPS

Exhibit 22: Management details

Mr. Nitin M. Shah Managing Director

Mr. Rahul N Shah Whole Time Director

Mr. Kunal N Shah Whole Time Director

Mr. Krishna Kant Jha Independent Director

Mr. Kailat H Vaidyanathan Independent Director

Mr. Ramakant M Nayak Independent Director

Mr. Satish K Dheri Independent Director

Ms. Padmaja Nair Independent Director

Source: Company, BOBCAPS

Nitin Fire Protection Industries Ltd. | 31 August 2015

| Equity research | 21

(Wholly owned subsidiary of Bank of Baroda)

Disclaimer BUY. We expect the stock to deliver >15% absolute returns. HOLD. We expect the stock to deliver 5-15% absolute returns. SELL. We expect the stock to deliver <5% absolute returns. Not Rated (NR). We have no investment opinion on the stock. “The BoB Capital Markets research team hereby certifies that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report."

BOB Capital Markets Ltd. generally prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. Additionally, BOB Capital Markets Ltd. generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. We are not soliciting any action based on this material. It is for the general information of clients of BOB Capital Markets Ltd.. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, clients should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. BOB Capital Markets Ltd. does not provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding any potential investment in certain transactions — including those involving futures, options, and other derivatives as well as non investment-grade securities —that give rise to substantial risk and are not suitable for all investors. The material is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed are our current opinions as of the date appearing on this material only. We endeavor to update on a reasonable basis the information discussed in this material, but regulatory, compliance, or other reasons may prevent us from doing so.

We and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance of this material, may from time to time have "long" or "short" positions in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein and may from time to time add to or dispose of any such securities (or investment). We and our affiliates may act as market maker or assume an underwriting commitment in the securities of companies discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or advisory services for or relating to those companies and may also be represented in the supervisory board or any other committee of those companies.

For the purpose of calculating whether BOB Capital Markets Ltd. and its affiliates hold, beneficially own, or control, including the right to vote for directors, 1% or more of the equity shares of the subject, the holding of the issuer of a research report is also included.

BOB Capital Markets Ltd. and its non-US affiliates may, to the extent permissible under applicable laws, have acted on or used this research to the extent that it relates to non-US issuers, prior to or immediately following its publication. Foreign currency denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of or income derived from the investment. In addition, investors in securities such as ADRs, the value of which are influenced by foreign currencies, affectively assume currency risk. In addition, options involve risks and are not suitable for all investors. Please ensure that you have read and understood the current derivatives risk disclosure document before entering into any derivative transactions. In the US, this material is only for Qualified Institutional Buyers as defined under rule 144(a) of the Securities Act, 1933.No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without BOB Capital Markets Ltd.’s prior written consent. No part of this document may be distributed in Canada or used by private customers in the United Kingdom.

Sales and Dealing Team

Purvesh Shelatkar – Senior Vice President & Head Equity +91-22-6138 9330 [email protected]

Anil Pawar – Senior Manager – Dealing +91-22-6138 9325 [email protected]

Sachin Sambare – Manager– Dealing +91-22-61389331/33 [email protected]

Ashwin Patil – Executive – Dealing +91-22-6138 9326 [email protected]

Research Team Sectors

Vaishali Parkar Kumar – Analyst Agri, Auto, Defence +91-22-6138 9382 [email protected]

Padmaja Ambekar – Analyst Auto Ancillary, Infra, Midcap +91-22-6138 9381 [email protected]

Akanksha Tripathi – Analyst Footwear, FMCG +91-22-6138 9383 [email protected]

Rishabh Mehta – Associate +91-22-6138 9384 [email protected]

Hareesha Kakkera - Associate +91-22-6138 9351 [email protected]

Retail Dealing Team

Kshitij Kelkar +91-22-61389386 [email protected]

Kiran Sawardekar +91-22-61389385 [email protected]

Mohan Shinde +91-22-61389386 [email protected]

Debt Dealing Team

Minaxi Tiwari +91-22-61389336 [email protected]

UTI Tower, 3rd Floor, South Wing, Bandra-Kurla Complex, Bandra (E), Mumbai - 400 051. India.

Ph.: +91.22.6138.9300 || Fax: +91.22.6671.8535 ||

Email: [email protected]|| Web: www.bobcaps.in

NSE SEBI No. (CASH): INB231304537

NSE SEBI No. (DERIVATIVES): INF231304537

BSE SEBI No. : INB011304533