5 - 1 © 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by...

28

5 - 1 4 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater The Accounting Cycle The Accounting Cycle Completed: Completed: Adjusting, Closing, and Adjusting, Closing, and Post-Closing Trial Balance Post-Closing Trial Balance Chapter 5 Chapter 5

-

Upload

carmel-spencer -

Category

Documents

-

view

217 -

download

2

Transcript of 5 - 1 © 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by...

5 - 1© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

The Accounting Cycle The Accounting Cycle Completed:Completed:

Adjusting, Closing, andAdjusting, Closing, andPost-Closing Trial BalancePost-Closing Trial Balance

Chapter 5Chapter 5

5 - 2© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

The Accounting CycleThe Accounting Cycle

BusinessBusinesstransactionstransactionsBusinessBusiness

transactionstransactions

11

Book ofBook oforiginal entryoriginal entry

Book ofBook oforiginal entryoriginal entry

22 Journal Journal

Book ofBook offinal entryfinal entryBook ofBook of

final entryfinal entry

33 Ledger Ledger

Trial balanceTrial balanceTrial balanceTrial balance

44

WorksheetWorksheetWorksheetWorksheet

55

5 - 3© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

The Accounting CycleThe Accounting Cycle

TrialTrialbalancebalance

TrialTrialbalancebalance AdjustmentsAdjustmentsAdjustmentsAdjustments

AdjustedAdjustedtrialtrial

balancebalance

AdjustedAdjustedtrialtrial

balancebalance

IncomeIncomestatementstatementIncomeIncome

statementstatementBalanceBalance

sheetsheetBalanceBalance

sheetsheet

BalanceBalancesheetsheet

BalanceBalancesheetsheet

Statement ofStatement ofowner’s equityowner’s equityStatement ofStatement of

owner’s equityowner’s equity

66Financial StatementsFinancial Statements

IncomeIncomestatementstatementIncomeIncome

statementstatement

5 - 4© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

The Accounting CycleThe Accounting Cycle

AdjustingAdjustingentriesentries

AdjustingAdjustingentriesentries

77

ClosingClosingentriesentriesClosingClosingentriesentries

88

Post-closingPost-closingtrial balancetrial balancePost-closingPost-closingtrial balancetrial balance

99

5 - 5© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

End of the Period ActivitiesEnd of the Period Activities

Adjusting entries must be enteredAdjusting entries must be enteredin the journal and posted.in the journal and posted.

Adjusting entries must be enteredAdjusting entries must be enteredin the journal and posted.in the journal and posted.

Closing entries must be journalizedClosing entries must be journalizedat the end of the accounting periodat the end of the accounting periodso that income can be measuredso that income can be measured

for the new period.for the new period.

Closing entries must be journalizedClosing entries must be journalizedat the end of the accounting periodat the end of the accounting periodso that income can be measuredso that income can be measured

for the new period.for the new period.

Temporary accounts are closed.Temporary accounts are closed.Temporary accounts are closed.Temporary accounts are closed.

5 - 6© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

End of the Period ActivitiesEnd of the Period Activities

Prepare adjustmentsPrepare adjustmentsPrepare adjustmentsPrepare adjustments

Complete worksheetComplete worksheetComplete worksheetComplete worksheet

Prepare reportsPrepare reportsPrepare reportsPrepare reports

Close the accounting periodClose the accounting periodClose the accounting periodClose the accounting period

5 - 7© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Objective 1Learning Objective 1

Journalizing and postingJournalizing and posting

adjusting entries.adjusting entries.

5 - 8© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-1 (Journalizing Learning Unit 5-1 (Journalizing and Posting Adjusting Entries)and Posting Adjusting Entries)

Examine each account.Examine each account.Examine each account.Examine each account.

Determine the appropriateDetermine the appropriateending account balances.ending account balances.

Determine the appropriateDetermine the appropriateending account balances.ending account balances.

Determine the requiredDetermine the requiredincrease or decrease.increase or decrease.

Determine the requiredDetermine the requiredincrease or decrease.increase or decrease.

Make an adjusting entry.Make an adjusting entry.Make an adjusting entry.Make an adjusting entry.

5 - 9© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-1 (Journalizing Learning Unit 5-1 (Journalizing and Posting Adjusting Entries)and Posting Adjusting Entries)

Assets must be adjusted to showAssets must be adjusted to showamounts used or allocated to periodsamounts used or allocated to periods

and recorded as expenses.and recorded as expenses.

Assets must be adjusted to showAssets must be adjusted to showamounts used or allocated to periodsamounts used or allocated to periods

and recorded as expenses.and recorded as expenses.

Supplies usedSupplies usedSupplies usedSupplies used

Prepaid rent expired over timePrepaid rent expired over timePrepaid rent expired over timePrepaid rent expired over time

Equipment depreciatedEquipment depreciatedEquipment depreciatedEquipment depreciated

5 - 10© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-1 (Journalizing Learning Unit 5-1 (Journalizing and Posting Adjusting Entries)and Posting Adjusting Entries)

The worksheet is complete.The worksheet is complete.The worksheet is complete.The worksheet is complete.

The books are not up to date.The books are not up to date.The books are not up to date.The books are not up to date.

Adjusting entries are taken fromAdjusting entries are taken fromthe worksheet and journalized.the worksheet and journalized.

Adjusting entries are taken fromAdjusting entries are taken fromthe worksheet and journalized.the worksheet and journalized.

The journal entries must be posted.The journal entries must be posted.The journal entries must be posted.The journal entries must be posted.

5 - 11© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-1 (Journalizing Learning Unit 5-1 (Journalizing and Posting Adjusting Entries)and Posting Adjusting Entries)

a. $500 of office supplies were used.a. $500 of office supplies were used.a. $500 of office supplies were used.a. $500 of office supplies were used.

(a) Office Supplies Expense(a) Office Supplies Expense 500500Office SuppliesOffice Supplies 500500

(a) Office Supplies Expense(a) Office Supplies Expense 500500Office SuppliesOffice Supplies 500500

b. $400 of prepaid rent expired.b. $400 of prepaid rent expired.b. $400 of prepaid rent expired.b. $400 of prepaid rent expired.

(b)(b) Rent Expense Rent Expense 400400Prepaid RentPrepaid Rent 400400

(b)(b) Rent Expense Rent Expense 400400Prepaid RentPrepaid Rent 400400

5 - 12© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-1 (Journalizing Learning Unit 5-1 (Journalizing and Posting Adjusting Entries)and Posting Adjusting Entries)

c.c. Depreciation of word processingDepreciation of word processingequipment was recorded.equipment was recorded.

c.c. Depreciation of word processingDepreciation of word processingequipment was recorded.equipment was recorded.

(c)(c) Depreciation Expense Depreciation Expense 80 80Accumulated depreciationAccumulated depreciation 80 80

(c)(c) Depreciation Expense Depreciation Expense 80 80Accumulated depreciationAccumulated depreciation 80 80

5 - 13© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Objective 2Learning Objective 2

Journalizing and postingJournalizing and posting

closing entries.closing entries.

5 - 14© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

Closing is a mechanical step which setsClosing is a mechanical step which setstemporary accounts to zero so that theytemporary accounts to zero so that they

are ready for a new measurement period.are ready for a new measurement period.

Closing is a mechanical step which setsClosing is a mechanical step which setstemporary accounts to zero so that theytemporary accounts to zero so that they

are ready for a new measurement period.are ready for a new measurement period.

5 - 15© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

AssetsAssetsAssetsAssets

LiabilitiesLiabilitiesLiabilitiesLiabilities

CapitalCapitalCapitalCapital

Balance sheet accountsBalance sheet accountsBalance sheet accountsBalance sheet accounts

5 - 16© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

Permanent accounts arePermanent accounts arealso called also called realreal accounts. accounts.Permanent accounts arePermanent accounts arealso called also called realreal accounts. accounts.

Balances are carried forward.Balances are carried forward.Balances are carried forward.Balances are carried forward.

5 - 17© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

RevenueRevenueRevenueRevenue

ExpensesExpensesExpensesExpenses

WithdrawalsWithdrawalsWithdrawalsWithdrawals

5 - 18© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

New data are accumulated each period.New data are accumulated each period.New data are accumulated each period.New data are accumulated each period.

Temporary accounts are alsoTemporary accounts are alsocalled called nominalnominal accounts. accounts.

Temporary accounts are alsoTemporary accounts are alsocalled called nominalnominal accounts. accounts.

Balances are set to zero.Balances are set to zero.Balances are set to zero.Balances are set to zero.

5 - 19© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

There are four steps to perform.There are four steps to perform.There are four steps to perform.There are four steps to perform.

1. Debit revenue accounts and credit1. Debit revenue accounts and creditthe Income Summary account.the Income Summary account.

1. Debit revenue accounts and credit1. Debit revenue accounts and creditthe Income Summary account.the Income Summary account.

2. Debit the Income Summary account2. Debit the Income Summary accountand credit expense accounts.and credit expense accounts.

2. Debit the Income Summary account2. Debit the Income Summary accountand credit expense accounts.and credit expense accounts.

5 - 20© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

3. Debit or credit the Income Summary account3. Debit or credit the Income Summary accountand debit or credit the Capital account.and debit or credit the Capital account.

3. Debit or credit the Income Summary account3. Debit or credit the Income Summary accountand debit or credit the Capital account.and debit or credit the Capital account.

4. Debit the Capital account and4. Debit the Capital account andcredit the Withdrawals account.credit the Withdrawals account.

4. Debit the Capital account and4. Debit the Capital account andcredit the Withdrawals account.credit the Withdrawals account.

5 - 21© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

Four Steps in Journalizing Closing Entries:Four Steps in Journalizing Closing Entries:

Step 1:Step 1:RevenueRevenueStep 1:Step 1:

RevenueRevenueStep 2:Step 2:

ExpensesExpensesStep 2:Step 2:

ExpensesExpenses

Step 4:Step 4:WithdrawalsWithdrawals

Step 4:Step 4:WithdrawalsWithdrawals

Step 3:Step 3:Income SummaryIncome Summary

Net Income or LossNet Income or Loss

Step 3:Step 3:Income SummaryIncome Summary

Net Income or LossNet Income or Loss

CapitalCapitalCapitalCapital

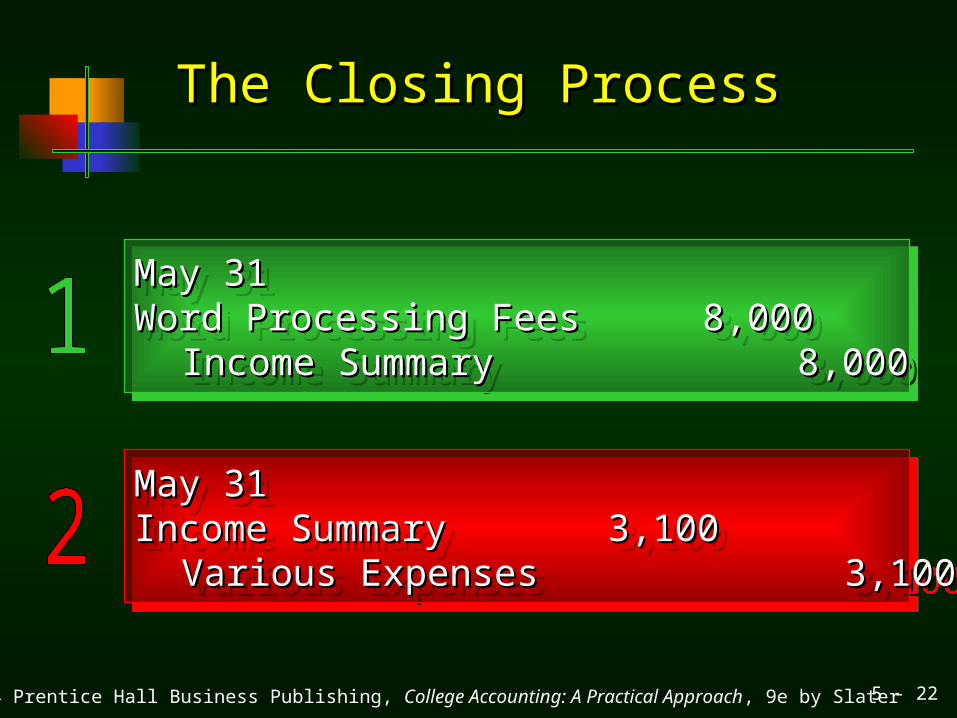

5 - 22© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

The Closing ProcessThe Closing Process

May 31May 31Word Processing FeesWord Processing Fees 8,0008,000

Income SummaryIncome Summary 8,0008,000

May 31May 31Word Processing FeesWord Processing Fees 8,0008,000

Income SummaryIncome Summary 8,0008,000

May 31May 31Income SummaryIncome Summary 3,1003,100

Various ExpensesVarious Expenses 3,1003,100

May 31May 31Income SummaryIncome Summary 3,1003,100

Various ExpensesVarious Expenses 3,1003,100

5 - 23© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

The Closing ProcessThe Closing Process

May 31May 31Income SummaryIncome Summary 4,9004,900

B. Clark, CapitalB. Clark, Capital 4,9004,900

May 31May 31Income SummaryIncome Summary 4,9004,900

B. Clark, CapitalB. Clark, Capital 4,9004,900

May 31May 31B. Clark, CapitalB. Clark, Capital 625 625

B. Clark, WithdrawalsB. Clark, Withdrawals 625 625

May 31May 31B. Clark, CapitalB. Clark, Capital 625 625

B. Clark, WithdrawalsB. Clark, Withdrawals 625 625

5 - 24© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-2 (Journalizing Learning Unit 5-2 (Journalizing and Posting Closing Entries)and Posting Closing Entries)

8,0008,000 8,0008,0003,1003,100

3,1003,100

ExpensesExpenses

Income SummaryIncome SummaryRevenueRevenue

8,0008,000

3,1003,100

B. Clark, CapitalB. Clark, Capital

B. Clark, WithdrawalsB. Clark, Withdrawals

625625

4,9004,900

4,9004,900625625

625625

5 - 25© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Objective 3Learning Objective 3

Prepare a post-closingPrepare a post-closing

trial balance.trial balance.

5 - 26© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-3 (The Post-Learning Unit 5-3 (The Post-Closing Trial Balance)Closing Trial Balance)

The post-closing trial balanceThe post-closing trial balancehelps prove the accuracy of thehelps prove the accuracy of theadjusting and closing process.adjusting and closing process.

The post-closing trial balanceThe post-closing trial balancehelps prove the accuracy of thehelps prove the accuracy of theadjusting and closing process.adjusting and closing process.

It contains the true ending figure for capital.It contains the true ending figure for capital.It contains the true ending figure for capital.It contains the true ending figure for capital.

It contains only permanent accounts.It contains only permanent accounts.It contains only permanent accounts.It contains only permanent accounts.

5 - 27© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

Learning Unit 5-3 (The Post- Learning Unit 5-3 (The Post- Closing Trial Balance)Closing Trial Balance)

Clark’s Word Processing ServicesPost-closing Trial Balance

May 31, 200x

CashCashAccounts ReceivableAccounts ReceivableOffice SuppliesOffice SuppliesPrepaid RentPrepaid RentWord Processing EquipmentWord Processing EquipmentAccumulated DepreciationAccumulated DepreciationAccounts PayableAccounts PayableSalaries PayableSalaries PayableBrenda Clark, CapitalBrenda Clark, Capital TotalsTotals

CashCashAccounts ReceivableAccounts ReceivableOffice SuppliesOffice SuppliesPrepaid RentPrepaid RentWord Processing EquipmentWord Processing EquipmentAccumulated DepreciationAccumulated DepreciationAccounts PayableAccounts PayableSalaries PayableSalaries PayableBrenda Clark, CapitalBrenda Clark, Capital TotalsTotals

6,1556,155 5,0005,000 100100 800800 6,0006,000

8080 3,3503,350 35035014,27514,275

18,05518,055 18,05518,055

6,1556,155 5,0005,000 100100 800800 6,0006,000

8080 3,3503,350 35035014,27514,275

18,05518,055 18,05518,055

Dr. Cr.

5 - 28© 2004 Prentice Hall Business Publishing, College Accounting: A Practical Approach, 9e by Slater

End of Chapter 5End of Chapter 5