203.209.96.242203.209.96.242/backoffice/files/731.pdfPDF file203.209.96.242

1

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Note: Stock prices as of December 31, 2013

Table of Contents

StrategyStrategyStrategyStrategyStrategy 2-82-82-82-82-8

3QFY2014 Sectoral Outlook3QFY2014 Sectoral Outlook3QFY2014 Sectoral Outlook3QFY2014 Sectoral Outlook3QFY2014 Sectoral Outlook

Automobile 10

Banking 13

Capital Goods 19

Cement 21

FMCG 23

Infrastructure 25

Information Technology 28

Media 31

Metals 32

Oil & Gas 35

Pharmaceutical 38

Power 41

Telecom 43

Stock WStock WStock WStock WStock Watchatchatchatchatch 4646464646

Refer to important Disclosures at the end of the report 2

3QFY2014 Results Preview | | | | | January 3, 2014

Strategy

Export sectors to aid earnings performance

During 3QFY2014, we expect an improvement in earningsgrowth for Sensex as well as our coverage companies* ascompared to the previous quarter, driven by sectors like IT &Pharma. For the Sensex companies, we expect earnings to growby 13.1% yoy and 4.4% qoq and for our coverage companieswe expect earnings growth to come in at 12.2% yoy and9.7% qoq. Strong numbers by individual large caps like TataMotors in the automobile space and Tata Steel in the metalsspace are also expected to aid earnings.

On the revenue front, we expect Sensex companies to report agrowth of 15.0% yoy and 6.1% qoq. Similarly, our coveragecompanies are expected to post a 13.9% yoy and 5.4% qoqgrowth on the top-line front. We expect the performance ofcompanies in the Oil and Gas and IT space along with TataMotors in the automobile sector to contribute substantially tothe overall revenue performance of our coverage companies.

The persistence of headwinds in cyclical sectors is expected toweigh on their margin performance during 3QFY2014 as well.As a result, we expect margin deterioration for both the Sensexas well as our coverage companies. For the Sensex companies,we expect a margin contraction of 81bp yoy and 48bp qoq

and for our coverage universe we expect margins to contractby 65bp yoy and 28bp qoq.

Outlook and VOutlook and VOutlook and VOutlook and VOutlook and Valuation: aluation: aluation: aluation: aluation: We are anticipating markets to gainpositively on the back of supportive global cues as well as ourimproving domestic economic outlook. Our external sector ismore resilient now as the trade deficit has narrowed owing tothe boost from export performance and moderation in importdemand. We expect a revival in the economy as the investmentcycle is boosted post elections owing to greater policy certainty.With these positives shaping up, we attribute a 16x multiple toour Sensex EPS and arrive at a target of 24,600 for the Sensexover the next one year.

We continue to maintain a positive bias for export-orientedsectors like IT and Pharmaceuticals, supported by the growthrevival in advanced economies and the rupee depreciation ona yoy basis. We also maintain a positive view on select metalstocks, considering recent capacity additions and under-utilizedcapacity getting employed for exports aided by improving globalfundamentals. We continue to prefer large private banks asthese are likely to benefit from an imminent economic revivalsince they continue to remain structurally strong.

SectorSectorSectorSectorSector (%, yoy) (%, yoy) (%, yoy) (%, yoy) (%, yoy) (%, qoq)(%, qoq)(%, qoq)(%, qoq)(%, qoq) (%, yoy)(%, yoy)(%, yoy)(%, yoy)(%, yoy) (%, qoq)(%, qoq)(%, qoq)(%, qoq)(%, qoq) (bps, yoy)(bps, yoy)(bps, yoy)(bps, yoy)(bps, yoy) (bps, qoq)(bps, qoq)(bps, qoq)(bps, qoq)(bps, qoq)

Agriculture (2) 13.7 3.0 28.2 - 52 (47)

Auto (7) 16.5 6.6 40.7 (8.4) 182 (100)

Auto Anc. (6) 10.0 3.0 41.4 3.2 222 22

Banks - New private (4) 15.3 4.5 17.1 11.9 154 15

Banks - Old private (2) 2.0 2.3 (1.5) (5.3) (570) (16)

Banks - Large PSU (7) 7.0 2.7 (9.9) 25.7 (712) 83

Banks - Mid PSU (14) 6.7 1.2 (6.8) 492.2 (427) 94

Banks - Housing finance (2) 12.1 (1.3) 13.4 (1.0) (49) (22)

Capital Goods (7) (2.3) 4.5 (23.9) 16.3 (186) 207

Cement (7) (1.2) 10.1 (30.5) 41.2 (259) 287

FMCG (12) 11.0 6.0 13.8 4.1 83 14

Infrastructure (11) 7.4 16.4 4.6 30.7 69 (3)

IT (12) 27.9 2.2 29.4 3.2 132 (10)

Media (5) 17.3 8.0 9.1 16.4 (124) 277

Metals (8) 14.6 0.9 57.7 9.6 251 34

Mining (1) 0.1 12.5 (15.6) 22.4 (588) 465

Oil & Gas (4) 19.9 9.1 2.1 1.0 (313) (134)

Pharmaceuticals (12) 17.6 (0.1) 41.7 (11.5) 242 (57)

Power (2) 1.7 (1.1) 1.8 7.5 27 53

Telecom (3) 8.7 2.3 148.2 28.5 260 17

Coverage Universe (128) Coverage Universe (128) Coverage Universe (128) Coverage Universe (128) Coverage Universe (128) 13.9 13.9 13.9 13.9 13.9 5.4 5.4 5.4 5.4 5.4 12.2 12.2 12.2 12.2 12.2 9.7 9.7 9.7 9.7 9.7 (65) (65) (65) (65) (65) (28) (28) (28) (28) (28)

Exhibit 1: 3QFY2014 Angel coverage performance estimatesOperating MarginsOperating MarginsOperating MarginsOperating MarginsOperating Margins

Source: Company, Angel Research

Net PNet PNet PNet PNet ProfitrofitrofitrofitrofitNet SalesNet SalesNet SalesNet SalesNet Sales

Note: *Sesa Goa and Cipla estimates have been excluded from analysis as comparable 3QFY2013 numbers are not available

3

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Strategy

SectorSectorSectorSectorSector (%, yoy) (%, yoy) (%, yoy) (%, yoy) (%, yoy) (%, qoq)(%, qoq)(%, qoq)(%, qoq)(%, qoq) (%, yoy)(%, yoy)(%, yoy)(%, yoy)(%, yoy) (%, qoq)(%, qoq)(%, qoq)(%, qoq)(%, qoq) (bps, yoy)(bps, yoy)(bps, yoy)(bps, yoy)(bps, yoy) (bps, qoq)(bps, qoq)(bps, qoq)(bps, qoq)(bps, qoq)

Auto (5) 17.7 7.5 41.7 (7.3) 189 (113)

Finance (5) 12.0 4.3 4.0 11.3 (372) 91

Capital Goods (1) (11.0) 1.2 (40.0) 9.5 (519) 408

FMCG (2) 8.9 5.4 12.1 5.6 162 (23)

Infrastructure (1) 8.0 14.9 8.5 14.2 44 34

IT (3) 27.3 2.3 28.3 3.8 99 (5)

Metals (2) 10.6 0.3 331.3 45.2 259 (6)

Mining (1) 0.1 12.5 (15.6) 22.4 (588) 465

Oil & Gas (3) 20.0 9.2 (0.4) (1.4) (318) (138)

Pharma (2) 27.5 (3.5) 43.9 (12.8) 296 76

Power (2) 2.2 1.4 2.2 4.3 23 (37)

Telecom (1) 7.4 2.0 186.8 58.9 196 48

Sensex* (28) Sensex* (28) Sensex* (28) Sensex* (28) Sensex* (28) 15.0 15.0 15.0 15.0 15.0 6.1 6.1 6.1 6.1 6.1 13.1 13.1 13.1 13.1 13.1 4.4 4.4 4.4 4.4 4.4 (81) (81) (81) (81) (81) (48) (48) (48) (48) (48)

Exhibit 2: 3QFY2014 Sensex performance estimatesOperating MarginsOperating MarginsOperating MarginsOperating MarginsOperating Margins

Source: Company, Angel Research, Note: *Sesa Goa and Cipla estimates have been excluded as comparable3QFY2013 numbers are not available

Net PNet PNet PNet PNet ProfitrofitrofitrofitrofitNet SalesNet SalesNet SalesNet SalesNet Sales

CompanyCompanyCompanyCompanyCompany 3QFY2014E3QFY2014E3QFY2014E3QFY2014E3QFY2014E 3QFY20133QFY20133QFY20133QFY20133QFY2013 % chg% chg% chg% chg% chg 3QFY2014E3QFY2014E3QFY2014E3QFY2014E3QFY2014E 3QFY20133QFY20133QFY20133QFY20133QFY2013 % chg % chg % chg % chg % chg 3QFY2014E 3QFY2014E 3QFY2014E 3QFY2014E 3QFY2014E 3QFY20133QFY20133QFY20133QFY20133QFY2013 % chg% chg% chg% chg% chg

Axis Bank 4,725 4,110 14.9 2,769 2,362 17.2 1,568 1,347 16.4

Bajaj Auto 5,321 5,413 (1.7) 1,092 1,012 7.9 861 819 5.2

Bharti Airtel 21,761 20,254 7.4 7,070 6,184 14.3 814 284 186.8

BHEL 9,096 10,220 (11.0) 982 1,634 (39.9) 709 1,182 (40.0)

Coal India 17,336 17,325 0.1 4,379 5,395 (18.8) 3,724 4,413 (15.6)

Dr. Reddy 3,588 2,865 25.2 911 507 79.7 736 363 102.8

HDFC 1,929 1,729 11.6 1,758 1,585 10.9 1,283 1,140 12.6

HDFC Bank 6,823 5,909 15.5 3,826 3,121 22.6 2,349 1,859 26.3

Hero Moto Corp 6,869 6,188 11.0 755 569 32.9 561 488 15.0

Hindalco 6,775 6,790 (0.2) 579 582 (0.5) 224 289 (22.5)

HUL 6,938 6,434 7.8 989 868 14.0 924 879 5.2

ICICI Bank 6,556 5,714 14.7 4,012 3,452 16.2 2,475 2,250 10.0

Infosys 13,101 10,424 25.7 3,453 2,970 16.2 2,650 2,369 11.8

ITC 8,373 7,627 9.8 3,224 2,773 16.3 2,361 2,052 15.1

Gail India 13,734 12,474 10.1 1,968 2,002 (1.7) 1,229 1,285 (4.3)

L&T 16,667 15,429 8.0 1,667 1,475 13.0 1,116 1,029 8.5

M&M 10,415 10,774 (3.3) 1,378 1,211 13.8 902 836 7.8

Maruti Suzuki 10,928 11,200 (2.4) 1,211 891 35.9 620 501 23.7

NTPC 16,090 15,775 2.0 4,135 3,995 3.5 2,668 2,597 2.7

ONGC 21,643 20,987 3.1 11,529 11,342 1.6 5,558 5,563 (0.1)

RIL 117,488 93,886 25.1 7,717 8,373 (7.8) 5,508 5,502 0.1

SBI 16,120 14,803 8.9 6,808 7,791 (12.6) 2,716 3,396 (20.0)

Sun Pharma 3,700 2,852 29.7 1,558 1,261 23.6 1,054 881 19.6

Tata Motors 60,209 46,090 30.6 8,322 5,657 47.1 3,353 1,801 86.2

Tata Power 2,631 2,549 3.2 570 569 0.3 206 216 (4.7)

Tata Steel 36,257 32,107 12.9 3,654 2,239 63.2 826 (743) 211.1

TCS 21,434 16,070 33.4 6,734 4,654 44.7 4,955 3,552 39.5

Wipro 11,452 9,624 19.0 2,617 2,074 26.2 2,022 1,582 27.9

Sensex*Sensex*Sensex*Sensex*Sensex* 473,233 473,233 473,233 473,233 473,233 411,511 411,511 411,511 411,511 411,511 15.015.015.015.015.0 92,899 92,899 92,899 92,899 92,899 84,186 84,186 84,186 84,186 84,186 10.310.310.310.310.3 52,403 52,403 52,403 52,403 52,403 46,384 46,384 46,384 46,384 46,384 13.113.113.113.113.1

Exhibit 3: 3QFY2014 Sensex companies' performance estimatesNet PNet PNet PNet PNet Profit (rofit (rofit (rofit (rofit (`̀̀̀̀ cr) cr) cr) cr) cr)Operating POperating POperating POperating POperating Profit (rofit (rofit (rofit (rofit (`̀̀̀̀ cr) cr) cr) cr) cr)

Source: Company, Angel Research, Note: *Sesa Goa and Cipla estimates have been excluded as comparable 3QFY2013 numbers are not available

Net Sales (Net Sales (Net Sales (Net Sales (Net Sales ( `̀̀̀̀ cr) cr) cr) cr) cr)

Refer to important Disclosures at the end of the report 4

3QFY2014 Results Preview | | | | | January 3, 2014

Strategy

Sectoral Analysis

Automobile - Tata Motors likely to support robust

earnings performance

During 3QFY2014 volumes for our coverage automobile

companies continued to remain sluggish as demand decelerated

post the festival season owing to weak consumer sentiments.

Domestic industry volumes witnessed a growth of about

3.0% yoy YTD in FY2014, driven entirely by the two-wheeler

and the tractor segments, which were aided by rural demand

on the back of good monsoon.

We expect our coverage automobile companies to post a strong

earnings growth of 40.7% yoy, despite the yoy decline in

volumes, led by robust growth at Tata Motors, driven yet again

by an impressive Jaguar and Land Rover (JLR) performance.

We expect our coverage auto universe's top-line to register a

strong growth of 16.5% yoy, primarily aided by INR depreciation

on a yoy basis and price increases. Led by the price increases

and favorable currency movement, we expect our coverage auto

companies' margins to expand by 182bp yoy. Nevertheless,

excluding the performance of Tata Motors, we expect our

coverage automobile universe to register an almost flat revenue

performance while earnings report a growth of about 9.4% yoy

supported by margin expansion.

Banking - New Private banks to deliver better

numbers yet again

Over the last few years, PSU banks have continuously lost profit

market share (both on reported profit as well as on profit

adjusted for increase in net NPAs) to private banks within our

coverage. During 3QFY2014 as well, we expect earnings

divergence amongst our coverage banking stocks to continue,

as we anticipate new private banks to report a healthy earnings

growth of 17.1% yoy, while our coverage PSU banks are

expected to report weak performance with earnings de-growth

of 9.0% yoy.

New private banks are expected to deliver healthy NII growth

of 20.1% yoy, which is expected to aid healthy growth of

18.4% yoy in operating profit and 17.1% yoy in earnings. On

the other hand, PSU banks are expected to register moderate

NII growth of 10.6% yoy and de-growth of 4.8% yoy in

non-interest income. Additionally, growth in operating expenses

for PSU banks is expected to be higher at 21.6% yoy as against

11.1% yoy for new private banks.

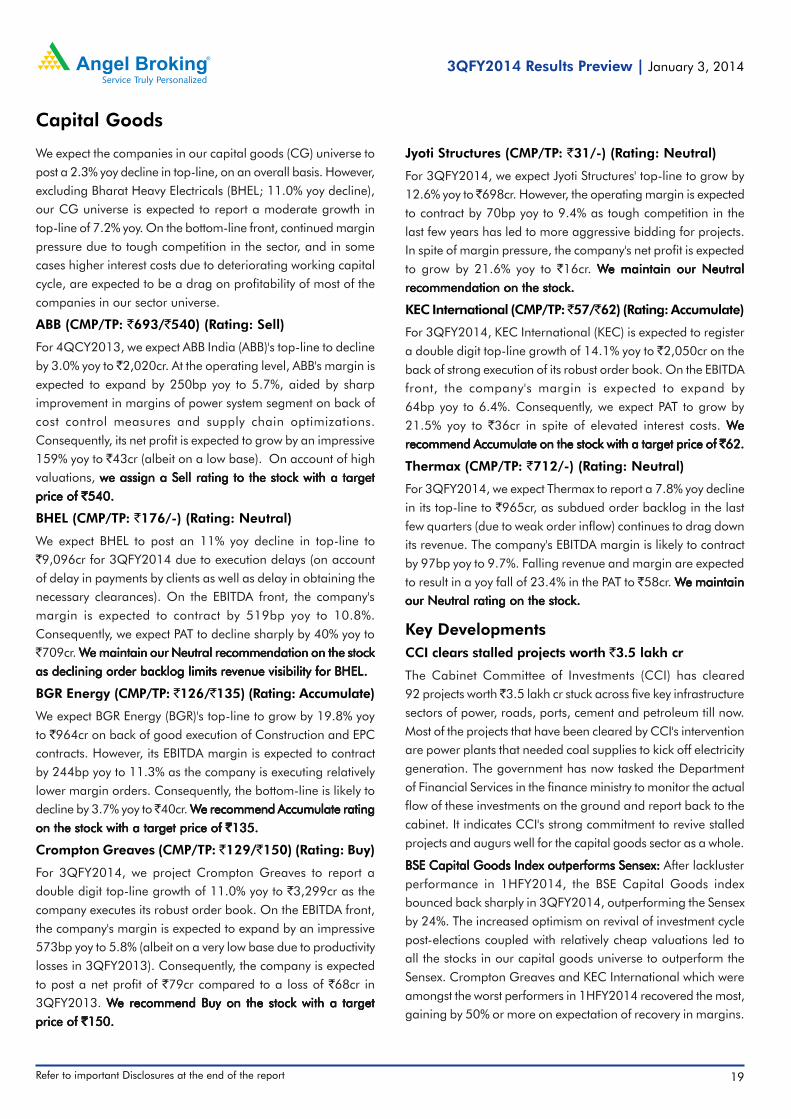

Capital goods - Margin pressure and high interest costs

remain a drag on profitability

We expect the companies in our capital goods universe to post

a decline of 2.3% yoy in revenues. However, excluding the

performance of Bharat Heavy Electricals (BHEL), our coverage

capital goods companies are expected to report a moderate

revenue growth of 7.2% yoy. BHEL's top-line is likely to be

impacted due to execution delays on account of delay in

payments by clients as well as delay in obtaining the necessary

clearances.

Overall on the bottom-line front, we expect our capital goods

universe to report a steep contraction of 23.9% yoy as most of

the companies are expected to witness continued margin

pressure due to tough competition in the sector. Furthermore,

interest costs remain at elevated levels for many companies in

our capital goods universe as execution delays (due to delay in

clearances and deferral in payment by clients) and decline in

advances (due to subdued order inflow) have led to deterioration

of working capital, which is being funded by short- term

borrowings.

Cement - Earnings to be impacted by lower realizations

We expect our coverage cement universe to report a sharp

earnings decline, impacted by lower realizations, as the demand

scenario continues to remain sluggish. Volume growth for our

cement universe is expected to be 4.1% yoy on a low base. But

we expect a 1.2% yoy decline on the revenue front, mainly due

to lower realization. Owing to lower realizations we also expect

most of the companies under our coverage to post a decline in

margins on a yoy basis. Overall we expect a 259bp yoy decline

in OPM for our cement universe.

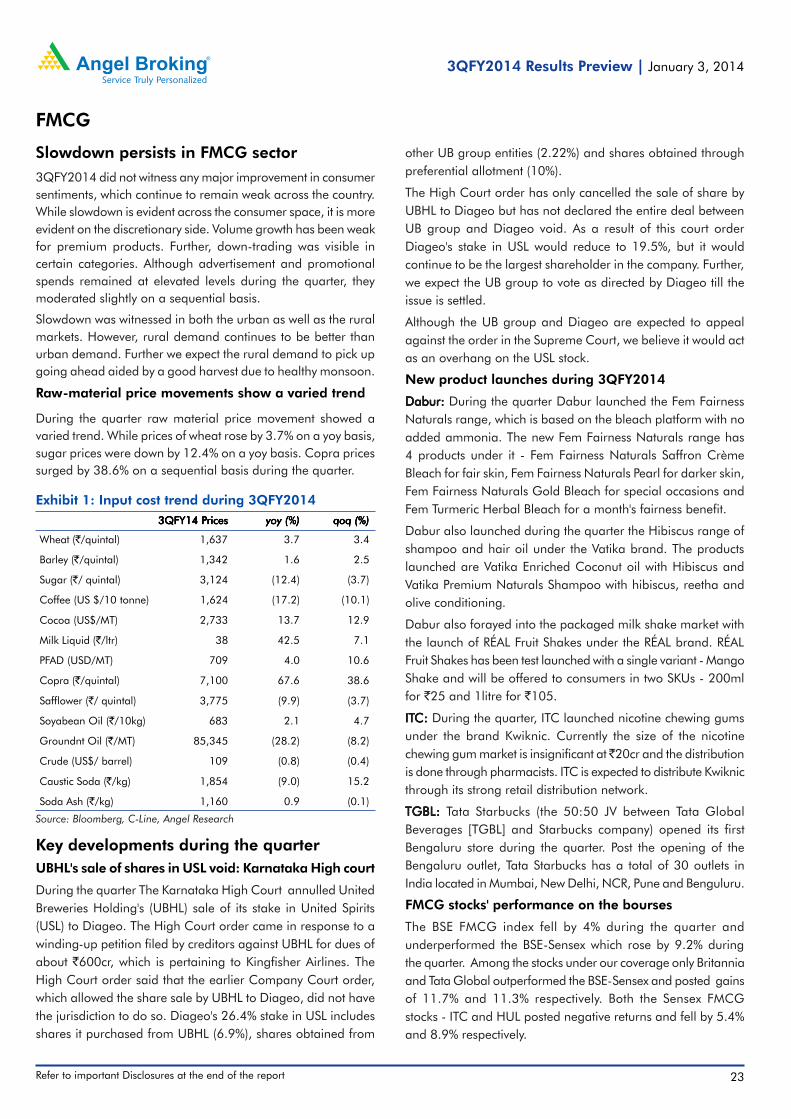

FMCG - Healthy revenue performance to aid earnings

growth

During the quarter, we expect our coverage FMCG universe to

report a 13.8% yoy earnings growth, led by healthy performance

on the top-line front. We expect our FMCG universe (excluding

ITC) to post a top-line growth of 11.4% yoy during the quarter

aided by both higher volumes and better realizations. Overall,

we expect a mixed performance on the operating front as higher

raw material prices are expected to result in a decline in gross

margins for some of our coverage FMCG companies. Also,

advertising and sales promotion expenses continue to remain

at elevated level, which along with higher freight costs are

expected to impact margin performance.

5

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Strategy

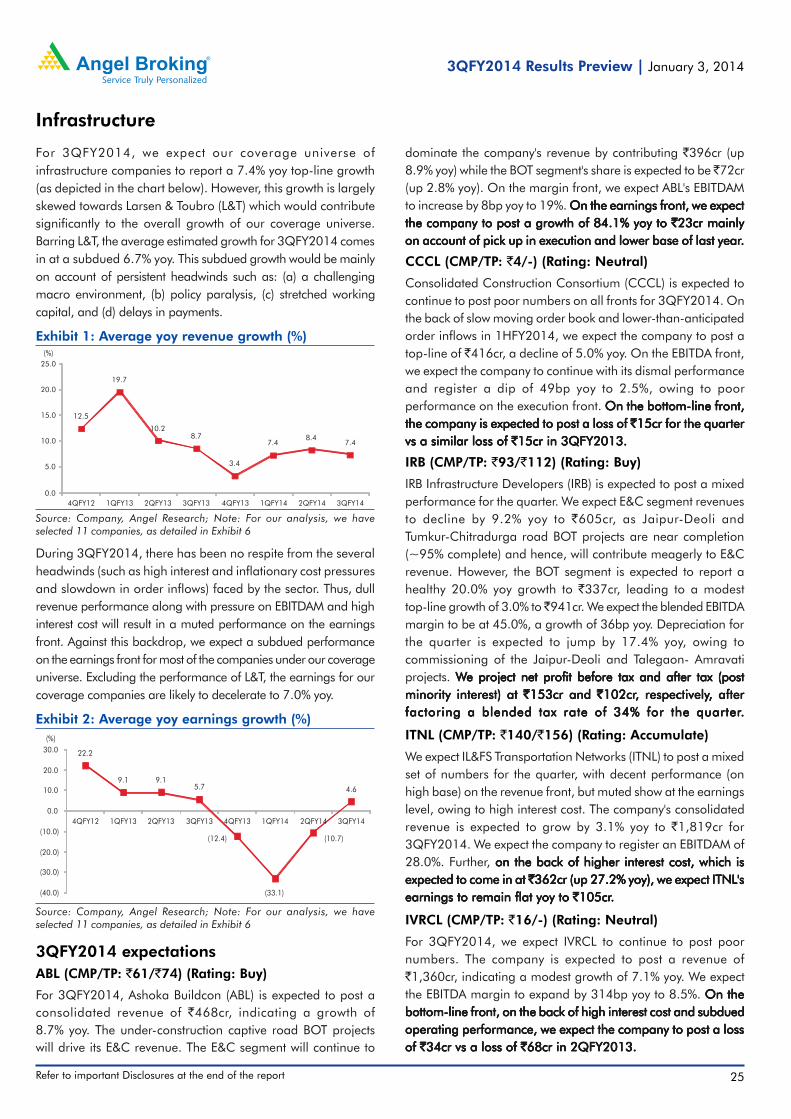

Infrastructure - Earnings likely to be supported by

performance of L&T

We expect our coverage infrastructure companies to post a

moderate earnings growth of 4.6% yoy, mainly supported by

the performance of Larsen & Toubro (L&T). Excluding L&T, the

earnings are likely to continue remaining under pressure and

we expect an earnings decline of 7.0% yoy for the remaining

infra companies in our coverage universe. We attribute the

dismal earnings performance during this quarter as well to

persistence of headwinds facing the sector such as a high interest

cost, inflationary cost pressures, stretched working capital and

delays in payments from clients.

We continue to maintain that a stock-specific approach would

yield higher returns, given the disparity among the companies

in our coverage universe. Hence, we remain positive on

companies having 1) a comfortable leverage position;

2) superior return ratios and 3) less dependence on capital

markets for raising equity for funding projects.

IT - 3Q a weak quarter, expect moderate volume growth

to aid revenues

Our coverage IT companies are expected to continue posting a

robust performance with earnings growth estimated at

29.4% yoy. Sequentially we expect earnings to witness a modest

growth of 3.2% qoq as 3Q is traditionally a weak quarter for

IT companies. We expect revenue growth during the quarter to

be largely volume driven and pricing to remain stable.

For 3QFY2014, volume growth is expected to be in the range

of 2.0-3.4% qoq for tier-I IT companies and we expect TCS to

continue to lead the pack. In INR terms, revenue growth is

expected to be in the range of 1.0-3.0% qoq for tier-I IT

companies. We expect our coverage IT companies to witness a

marginal decline on the operating margin front, ie by about

10bp qoq, due to slight sequential INR appreciation and with

volume growth expected to be relatively moderate during the

quarter.

Metals - Tata Steel likely to support robust earnings

performance

Our coverage metal companies are expected to report a robust

earnings growth of 57.7% yoy buoyed by the performance of

Tata Steel (aided by its operating profit). Excluding the

performance of Tata Steel, earnings are likely to post a growth

of 12.3% yoy. For steel companies under our coverage (except

SAIL) we expect an improvement in earnings as their revenue

and operating profits are aided mainly by higher volume growth.

We expect our coverage non-ferrous companies (except

Hindalco) to report an improvement in earnings performance.

For Hindalco, we expect the bottom-line to decline by

22.5% yoy due to higher interest and depreciation costs.

Oil and Gas - Strong revenue performance to support

earnings

Our coverage oil and gas companies are expected to report a

strong revenue growth of about 20.0% yoy. However, owing to

margin pressure (excluding for Cairn India) we expect earnings

to post a muted growth of 2.1% yoy. For Cairn India, we expect

slight improvement in margins (owing to the impact of

INR depreciation and increase in realizations) as well as revenue

performance which is likely to result in a healthy earnings growth

for the company.

Pharmaceuticals - Robust earnings performance to

continue

We expect our coverage pharmaceutical companies to continue

reporting a good set of numbers. Excluding Cipla (for which

corresponding consolidated figures are not available for

3QFY2013), we expect a strong 41.7% yoy growth in earnings

during the quarter supported by expansion of 17.6% yoy in

revenue and 242bp yoy in margin performance. The strong

performance of exports in the sector has also contributed to

top-line growth. We expect Sensex pharmaceutical companies

to post a 27.5% yoy top-line growth and margin expansion of

296bp yoy, resulting in a robust 43.9% yoy increase in the

bottom-line.

Telecom - Expect improvement in overall performance

During the quarter, we expect our coverage telecom companies

to report a good set of numbers. We expect healthy revenue

growth for the industry on the back of increase in MOU, uptick

in voice ARPM as well as growing data users, and improvement

in margin performance. Amongst the top three operators, we

expect Idea Cellular (Idea) to lead in terms of revenue growth

followed by Bharti Airtel (Bharti) and Reliance Communications

(RCom). We expect Idea to post a 4.1% sequential revenue

growth while Bharti and RCom are expected to post a revenue

growth of 2.0% and 1.7% qoq, respectively. On the margins

front, we expect the EBITDA margin of Bharti and Idea to see

marginal uptick while the EBITDA margin of RCom is expected

to decline by 94bp qoq.

Refer to important Disclosures at the end of the report 6

3QFY2014 Results Preview | | | | | January 3, 2014

Strategy

Fed embarks on tapering of bond purchases;rates to remain low

The Federal Reserve (Fed) in its recent Federal Open Market

Committee meeting decided to moderately taper its quantitative

easing (QE3) program beginning January 2014 by USD10bn

per month. The Fed has decided to reduce its monthly asset

purchases from USD85bn since September 2012 to USD75bn.

It will cut down on the pace of purchase of treasury securities by

USD5bn to USD40bn and mortgage backed securities (MBS)

by USD5bn to USD35bn.

It appears that a further reduction in the stimulus would ensue

at a measured pace through much of next year and in case

improvement in the labor market continues as expected, the

program is likely to be fully shuttered by late-2014. But at the

same time, the Fed's stance continued to be dovish and it

reiterated its commitment to an accommodative monetary policy

stance to support growth. The Fed continued to indicate that

the policy rate (at 0.25%, presently) would be maintained at

exceptionally low levels at least as long as the unemployment

rate reaches above 6.5% and price stability is maintained at or

below its 2% medium-term objective.

Markets have taken the Fed's announcement on gradual

withdrawal of stimulus in their stride since our external

Source: RBI, Angel Research

Exhibit 4: Sharp narrowing in the CAD during 2QFY14

(4.3) (4.4)(4.0)

(5.0)

(6.5)

(3.6)

(4.9)

(1.2)

(8)

(7)

(6)

(5)

(4)

(3)

(2)

(1)

-

(35)

(30)

(25)

(20)

(15)

(10)

(5)

-

3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

(% of GDP)(USD bn) CAD as % of GDP (RHS)

Source: Ministry of Commerce, Angel Research

Exhibit 5: Positive improvement in the trade balance

(20)

(10)

-

10

20

30

40

(25)

(20)

(15)

(10)

(5)

-

(%)(USD bn)

Trade balance Exports growth (RHS) Imports growth (RHS)

Jan-1

2

Feb

-12

Mar-

12

Apr-

12

May-

12

Jun-1

2

Jul-

12

Aug-1

2

Sep

-12

Oct

-12

Nov-

12

Dec-

12

Jan-1

3

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun-1

3

Jul-

13

Aug-1

3

Sep

-13

Oct

-13

Nov-

13

Source: Bloomberg, Angel Research

Exhibit 6: Stability in the INR despite Fed's QE3 taper

50.0

52.0

54.0

56.0

58.0

60.0

62.0

64.0

66.0

68.0

70.0

Mar-

13

Apr-

13

May-1

3

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov-

13

Dec-1

3

(USDINR)

Source: RBI, Angel Research

Exhibit 7: Rise in forex reserves and import coverImport cover (RHS) Forex reserves

6.0

6.5

7.0

7.5

8.0

8.5

9.0

250

260

270

280

290

300

310

320

Dec-1

2

Jan

-13

Feb

-13

Mar-

13

Apr-

13

May-1

3

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov-

13

(Months)(USD bn)

vulnerability has eased considerably. This positive reaction stands

in contrast with May 2013 when indication of a taper resulted

in immense volatility in the equity and currency markets. We

believe that the strengthening of recovery in the US and other

advanced economies is likely to have a medium-term positive

impact for emerging markets including India since improvement

in external demand would boost export growth and add to GDP

growth in the economy.

Economy on a better footing as external sector becomesresilient

The concerns emanating for the economy from the external

front as global liquidity gets tapered have eased substantially

as our CAD moderated, risks to its financing receded and forex

reserves situation improved. Driven by strong export

performance and also moderation in imports due to a collapse

in domestic demand and curbs on gold imports, the trade deficit

has narrowed to USD33bn in 2QFY2014 from USD48bn in

the corresponding quarter of the previous year. As a result,

during 2QFY2014 the CAD came sharply lower at 1.2% of

GDP as compared to 5.0% of GDP in 2QFY2013. We expect a

sustained improvement in the trade balance to continue going

forward. For FY2014 as a whole, we expect the CAD to come

in at a more manageable level of 2.5-3.0% of GDP as against

a much wider 4.8% of GDP in FY2013.

7

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Strategy

The risks surrounding the financing of the CAD have also

receded as the CAD itself has moderated to comfortable levels

and several policy measures have already been taken to garner

capital inflows in the economy. The Reserve Bank of India (RBI)

has attracted about USD34bn under its schemes to attract FCNR

(B) deposits and foreign currency borrowings. Despite reduction

in Fed's stimulus, the INR has remained stable in the 61-63

range as compared to rout in the currency that pushed it to

68-levels against the dollar in August 2013, post which timely

policy measures and improved fundamentals supported the

currency to stage a recovery.

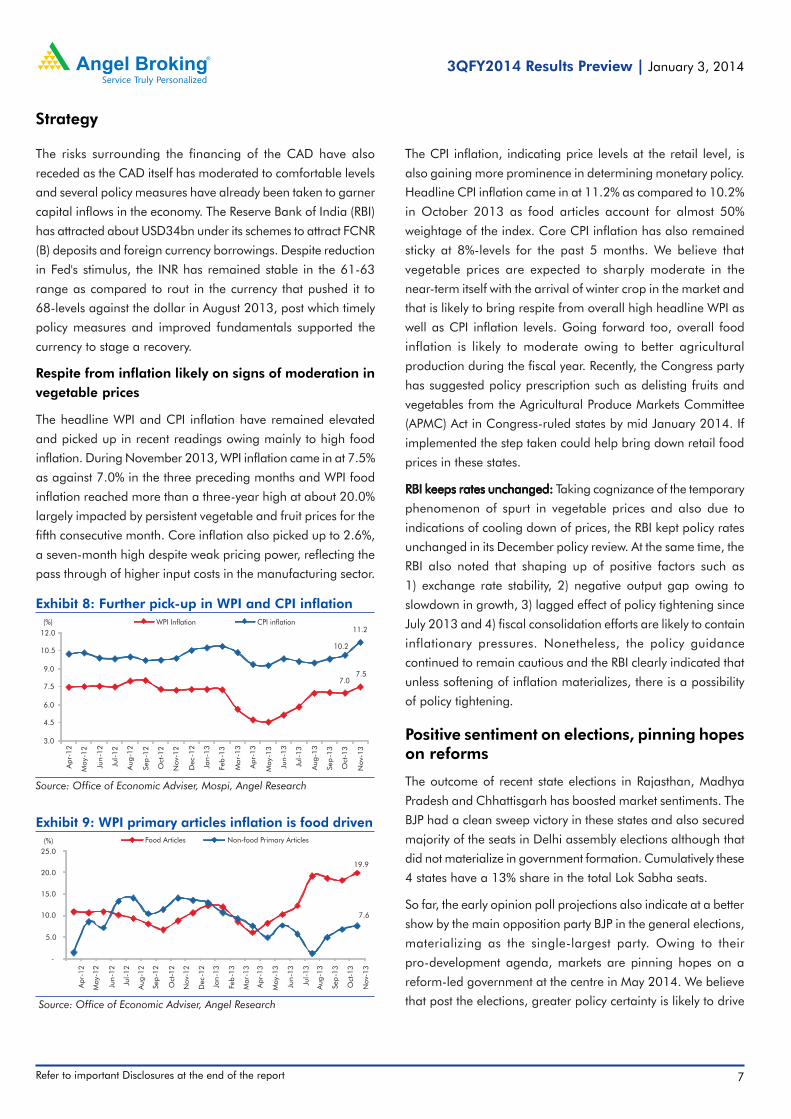

Respite from inflation likely on signs of moderation invegetable prices

The headline WPI and CPI inflation have remained elevated

and picked up in recent readings owing mainly to high food

inflation. During November 2013, WPI inflation came in at 7.5%

as against 7.0% in the three preceding months and WPI food

inflation reached more than a three-year high at about 20.0%

largely impacted by persistent vegetable and fruit prices for the

fifth consecutive month. Core inflation also picked up to 2.6%,

a seven-month high despite weak pricing power, reflecting the

pass through of higher input costs in the manufacturing sector.

The CPI inflation, indicating price levels at the retail level, is

also gaining more prominence in determining monetary policy.

Headline CPI inflation came in at 11.2% as compared to 10.2%

in October 2013 as food articles account for almost 50%

weightage of the index. Core CPI inflation has also remained

sticky at 8%-levels for the past 5 months. We believe that

vegetable prices are expected to sharply moderate in the

near-term itself with the arrival of winter crop in the market and

that is likely to bring respite from overall high headline WPI as

well as CPI inflation levels. Going forward too, overall food

inflation is likely to moderate owing to better agricultural

production during the fiscal year. Recently, the Congress party

has suggested policy prescription such as delisting fruits and

vegetables from the Agricultural Produce Markets Committee

(APMC) Act in Congress-ruled states by mid January 2014. If

implemented the step taken could help bring down retail food

prices in these states.

RBI keeps rates unchanged:RBI keeps rates unchanged:RBI keeps rates unchanged:RBI keeps rates unchanged:RBI keeps rates unchanged: Taking cognizance of the temporary

phenomenon of spurt in vegetable prices and also due to

indications of cooling down of prices, the RBI kept policy rates

unchanged in its December policy review. At the same time, the

RBI also noted that shaping up of positive factors such as

1) exchange rate stability, 2) negative output gap owing to

slowdown in growth, 3) lagged effect of policy tightening since

July 2013 and 4) fiscal consolidation efforts are likely to contain

inflationary pressures. Nonetheless, the policy guidance

continued to remain cautious and the RBI clearly indicated that

unless softening of inflation materializes, there is a possibility

of policy tightening.

Positive sentiment on elections, pinning hopeson reforms

The outcome of recent state elections in Rajasthan, Madhya

Pradesh and Chhattisgarh has boosted market sentiments. The

BJP had a clean sweep victory in these states and also secured

majority of the seats in Delhi assembly elections although that

did not materialize in government formation. Cumulatively these

4 states have a 13% share in the total Lok Sabha seats.

So far, the early opinion poll projections also indicate at a better

show by the main opposition party BJP in the general elections,

materializing as the single-largest party. Owing to their

pro-development agenda, markets are pinning hopes on a

reform-led government at the centre in May 2014. We believe

that post the elections, greater policy certainty is likely to drive

Source: Office of Economic Adviser, Mospi, Angel Research

Exhibit 8: Further pick-up in WPI and CPI inflationWPI Inflation CPI inflation

7.07.5

10.2

11.2

3.0

4.5

6.0

7.5

9.0

10.5

12.0

Apr-

12

May-1

2

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

Nov-

12

Dec-1

2

Jan

-13

Feb

-13

Mar-

13

Apr-

13

May-1

3

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov-

13

(%)

Source: Office of Economic Adviser, Angel Research

Exhibit 9: WPI primary articles inflation is food driven

Apr-

12

May-

12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

Nov-

12

Dec-1

2

Jan

-13

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov-

13

19.9

7.6

-

5.0

10.0

15.0

20.0

25.0

(%) Food Articles Non-food Primary Articles

Refer to important Disclosures at the end of the report 8

3QFY2014 Results Preview | | | | | January 3, 2014

Strategy

Source: Election Commission of India, Angel Research

Exhibit 10: BJP sweeps majority seats in state elections20082008200820082008 20132013201320132013 Swing inSwing inSwing inSwing inSwing in 2013 seat2013 seat2013 seat2013 seat2013 seat

seatsseatsseatsseatsseats share (%)share (%)share (%)share (%)share (%)

RajasthanRajasthanRajasthanRajasthanRajasthan

BJP 78 162 84 81.4

Congress 96 21 (75) 10.6

Others 26 16 (10) 8.0

ChhattisgarhChhattisgarhChhattisgarhChhattisgarhChhattisgarh

BJP 50 49 (1) 54.4

Congress 38 39 1 43.3

Others 2 2 - 2.2

Madhya PMadhya PMadhya PMadhya PMadhya Pradeshradeshradeshradeshradesh

BJP 143 165 22 71.7

Congress 71 58 (13) 25.2

Others 16 7 (9) 3.0

DelhiDelhiDelhiDelhiDelhi

BJP 23 32 9 45.7

Congress 43 8 (35) 11.4

AAP - 28 28 40.0

Others 4 2 (2) 2.9

new project announcements and stimulating capex. In our view,

the formation of a strong government will firmly bring back the

focus on creating more employment and boosting infrastructure

investment to kick-start growth in the economy.

Outlook and Valuation

We are anticipating markets to gain positively on the back of

supportive global cues as well as our improving domestic

economic outlook. Our external sector is more resilient now as

the trade deficit has narrowed owing to the boost from export

performance and moderation in import demand. We expect a

revival in the economy as the investment cycle is boosted post

elections owing to greater policy certainty and we also expect

monetary policy to support growth in 2HCY2014 as food

inflation cools down. With these positives shaping up, we

attribute a 16x multiple to our Sensex EPS and arrive at a target

of 24,600 for the Sensex over the next one year implying an

upside of nearly 17.0% from the present levels.

We continue to maintain a positive outlook on export-oriented

sectors like IT and pharmaceuticals supported by the growth

revival in advanced economies and the rupee depreciation on

a yoy basis. We also maintain a positive view on select metal

stocks, considering recent capacity additions and under-utilized

capacity getting employed for exports, aided by improving

global fundamentals. Amongst cyclicals we continue to prefer

large private banks, as these are likely to benefit from an

imminent economic revival since they continue to remain

structurally strong.

Source: Angel Research

Exhibit 11: Sensex EPS growth over FY2013-15

1,169

1,305

1,535

500

700

900

1,100

1,300

1,500

1,700

FY2013 FY2014E FY2015E

(`)

11.6% growth17.7% growth

Source: Angel Research

Exhibit 12: Sensex one-year forward P/E

5.0

10.0

15.0

20.0

25.0

30.0

Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13

Sensex 1 year forward P/E 15 year Avg 5 year Avg

9

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

3QFY2014 Sectoral Outlook

Refer to important Disclosures at the end of the report 10

3QFY2014 Results Preview | | | | | January 3, 2014

Automobile

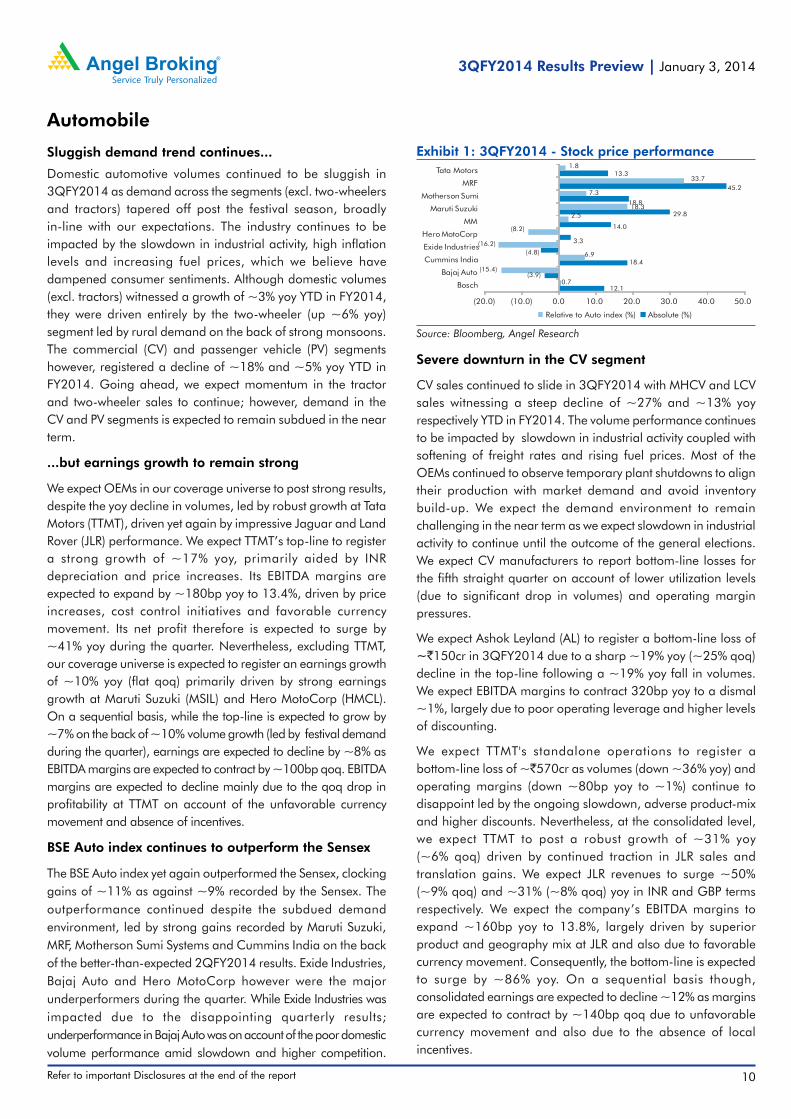

Sluggish demand trend continues...

Domestic automotive volumes continued to be sluggish in3QFY2014 as demand across the segments (excl. two-wheelersand tractors) tapered off post the festival season, broadlyin-line with our expectations. The industry continues to beimpacted by the slowdown in industrial activity, high inflationlevels and increasing fuel prices, which we believe havedampened consumer sentiments. Although domestic volumes(excl. tractors) witnessed a growth of ~3% yoy YTD in FY2014,they were driven entirely by the two-wheeler (up ~6% yoy)segment led by rural demand on the back of strong monsoons.The commercial (CV) and passenger vehicle (PV) segmentshowever, registered a decline of ~18% and ~5% yoy YTD inFY2014. Going ahead, we expect momentum in the tractorand two-wheeler sales to continue; however, demand in theCV and PV segments is expected to remain subdued in the nearterm.

...but earnings growth to remain strong

We expect OEMs in our coverage universe to post strong results,despite the yoy decline in volumes, led by robust growth at TataMotors (TTMT), driven yet again by impressive Jaguar and LandRover (JLR) performance. We expect TTMT’s top-line to registera strong growth of ~17% yoy, primarily aided by INRdepreciation and price increases. Its EBITDA margins areexpected to expand by ~180bp yoy to 13.4%, driven by priceincreases, cost control initiatives and favorable currencymovement. Its net profit therefore is expected to surge by~41% yoy during the quarter. Nevertheless, excluding TTMT,our coverage universe is expected to register an earnings growthof ~10% yoy (flat qoq) primarily driven by strong earningsgrowth at Maruti Suzuki (MSIL) and Hero MotoCorp (HMCL).On a sequential basis, while the top-line is expected to grow by~7% on the back of ~10% volume growth (led by festival demandduring the quarter), earnings are expected to decline by ~8% asEBITDA margins are expected to contract by ~100bp qoq. EBITDAmargins are expected to decline mainly due to the qoq drop inprofitability at TTMT on account of the unfavorable currencymovement and absence of incentives.

BSE Auto index continues to outperform the Sensex

The BSE Auto index yet again outperformed the Sensex, clockinggains of ~11% as against ~9% recorded by the Sensex. Theoutperformance continued despite the subdued demandenvironment, led by strong gains recorded by Maruti Suzuki,MRF, Motherson Sumi Systems and Cummins India on the backof the better-than-expected 2QFY2014 results. Exide Industries,Bajaj Auto and Hero MotoCorp however were the majorunderperformers during the quarter. While Exide Industries wasimpacted due to the disappointing quarterly results;underperformance in Bajaj Auto was on account of the poor domesticvolume performance amid slowdown and higher competition.

Source: Bloomberg, Angel Research

Exhibit 1: 3QFY2014 - Stock price performance

Relative to Auto index (%) Absolute (%)

12.1

(3.9)

18.4

(4.8)

3.3

14.0

29.8

18.8

45.2

13.3

0.7

(15.4)

6.9

(16.2)

(8.2)

2.5

18.3

7.3

33.7

1.8

(20.0) (10.0) 0.0 10.0 20.0 30.0 40.0 50.0

MRF

Tata Motors

Severe downturn in the CV segment

CV sales continued to slide in 3QFY2014 with MHCV and LCVsales witnessing a steep decline of ~27% and ~13% yoyrespectively YTD in FY2014. The volume performance continuesto be impacted by slowdown in industrial activity coupled withsoftening of freight rates and rising fuel prices. Most of theOEMs continued to observe temporary plant shutdowns to aligntheir production with market demand and avoid inventorybuild-up. We expect the demand environment to remainchallenging in the near term as we expect slowdown in industrialactivity to continue until the outcome of the general elections.We expect CV manufacturers to report bottom-line losses forthe fifth straight quarter on account of lower utilization levels(due to significant drop in volumes) and operating marginpressures.

We expect Ashok Leyland (AL) to register a bottom-line loss of~`150cr in 3QFY2014 due to a sharp ~19% yoy (~25% qoq)decline in the top-line following a ~19% yoy fall in volumes.We expect EBITDA margins to contract 320bp yoy to a dismal~1%, largely due to poor operating leverage and higher levelsof discounting.

We expect TTMT's standalone operations to register abottom-line loss of ~`570cr as volumes (down ~36% yoy) andoperating margins (down ~80bp yoy to ~1%) continue todisappoint led by the ongoing slowdown, adverse product-mixand higher discounts. Nevertheless, at the consolidated level,we expect TTMT to post a robust growth of ~31% yoy(~6% qoq) driven by continued traction in JLR sales andtranslation gains. We expect JLR revenues to surge ~50%(~9% qoq) and ~31% (~8% qoq) yoy in INR and GBP termsrespectively. We expect the company’s EBITDA margins toexpand ~160bp yoy to 13.8%, largely driven by superiorproduct and geography mix at JLR and also due to favorablecurrency movement. Consequently, the bottom-line is expectedto surge by ~86% yoy. On a sequential basis though,consolidated earnings are expected to decline ~12% as marginsare expected to contract by ~140bp qoq due to unfavorablecurrency movement and also due to the absence of localincentives.

11

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Automobile

Source: Company; Angel Research

Exhibit 2: TTMT and AL – Quarterly volumes

SegmentSegmentSegmentSegmentSegment 3QFY20143QFY20143QFY20143QFY20143QFY2014 3QFY20133QFY20133QFY20133QFY20133QFY2013 yoy (%)yoy (%)yoy (%)yoy (%)yoy (%) 9MFY20149MFY20149MFY20149MFY20149MFY2014 9MFY20139MFY20139MFY20139MFY20139MFY2013 yoy (%)yoy (%)yoy (%)yoy (%)yoy (%)

TTMTTTMTTTMTTTMTTTMT 130,353130,353130,353130,353130,353 203,852203,852203,852203,852203,852 (36.1)(36.1)(36.1)(36.1)(36.1) 434,991434,991434,991434,991434,991 613,716613,716613,716613,716613,716 (29.1)(29.1)(29.1)(29.1)(29.1)

Total CV 95,377 149,402 (36.2) 325,886 424,703 (23.3)

Total PV 34,976 54,450 (35.8) 109,105 189,013 (42.3)

Exports (incl. above) 11,225 11,654 (3.7) 36,260 39,403 (8.0)

ALALALALAL 18,45318,45318,45318,45318,453 22,66122,66122,66122,66122,661 (18.6)(18.6)(18.6)(18.6)(18.6) 63,25463,25463,25463,25463,254 80,08480,08480,08480,08480,084 (21.0)(21.0)(21.0)(21.0)(21.0)

MHCV 10,698 14,576 (26.6) 41,478 55,453 (25.2)

LCV ( incl. Dost) 7,755 8,085 (4.1) 21,776 24,631 (11.6)

Exports (incl. above) 1,713 1,702 0.6 6,146 6,788 (9.5)

Exhibit 4: BJAUT, HMCL and TVSL – Quarterly volumes

SegmentSegmentSegmentSegmentSegment 3QFY20143QFY20143QFY20143QFY20143QFY2014 3QFY20133QFY20133QFY20133QFY20133QFY2013 yoy (%)yoy (%)yoy (%)yoy (%)yoy (%) 9MFY20149MFY20149MFY20149MFY20149MFY2014 9MFY20139MFY20139MFY20139MFY20139MFY2013 yoy (%)yoy (%)yoy (%)yoy (%)yoy (%)

BJABJABJABJABJAUTUTUTUTUT 993,690993,690993,690993,690993,690 1,127,7411,127,7411,127,7411,127,7411,127,741 (11.9)(11.9)(11.9)(11.9)(11.9) 2,934,2952,934,2952,934,2952,934,2952,934,295 3,255,9203,255,9203,255,9203,255,9203,255,920 (9.9)(9.9)(9.9)(9.9)(9.9)

Motorcycles 887,671 986,263 (10.0) 2,597,112 2,897,410 (10.4)

Three-wheelers 106,019 141,478 (25.1) 337,183 358,510 (5.9)

Exports (incl. above) 422,506 376,222 12.3 1,186,099 1,182,152 0.3

HMCLHMCLHMCLHMCLHMCL 1,680,9401,680,9401,680,9401,680,9401,680,940 1,573,1351,573,1351,573,1351,573,1351,573,135 6.96.96.96.96.9 4,656,1544,656,1544,656,1544,656,1544,656,154 4,546,2304,546,2304,546,2304,546,2304,546,230 2.42.42.42.42.4

TVSLTVSLTVSLTVSLTVSL 519,308519,308519,308519,308519,308 518,496518,496518,496518,496518,496 0.20.20.20.20.2 1,520,4191,520,4191,520,4191,520,4191,520,419 1,523,6551,523,6551,523,6551,523,6551,523,655 (0.2)(0.2)(0.2)(0.2)(0.2)

Two-wheelers 498,941 504,894 (1.2) 1,460,889 1,488,761 (1.9)

Three-wheelers 20,367 13,602 49.7 59,530 34,894 70.6

Exports (incl. above) 74,289 58,894 26.1 227,590 179,627 26.7

Source: Company; Angel Research

Exhibit 3: MSIL and MM – Quarterly volumes

SegmentSegmentSegmentSegmentSegment 3QFY20143QFY20143QFY20143QFY20143QFY2014 3QFY20133QFY20133QFY20133QFY20133QFY2013 yoy (%)yoy (%)yoy (%)yoy (%)yoy (%) 9MFY20149MFY20149MFY20149MFY20149MFY2014 9MFY20139MFY20139MFY20139MFY20139MFY2013yoy (%)yoy (%)yoy (%)yoy (%)yoy (%)

MSILMSILMSILMSILMSIL 288,151288,151288,151288,151288,151 301,453301,453301,453301,453301,453 (4.4)(4.4)(4.4)(4.4)(4.4) 830,171830,171830,171830,171830,171 827,725827,725827,725827,725827,725 0.30.30.30.30.3

Domestic 268,185 268,957 (0.3) 755,093 742,175 1.7

Exports 19,966 32,496 (38.6) 75,078 85,550 (12.2)

MMMMMMMMMM 207,843207,843207,843207,843207,843 211,678211,678211,678211,678211,678 (1.8)(1.8)(1.8)(1.8)(1.8) 582,951582,951582,951582,951582,951 588,361588,361588,361588,361588,361 (0.9)(0.9)(0.9)(0.9)(0.9)

Automotive - domestic120,929 140,378 (13.9) 349,366 389,450 (10.3)

Automotive - exports 8,495 6,500 30.7 21,325 24,690 (13.6)

Tractor - domestic 76,132 62,341 22.1 204,758 165,699 23.6

Tractor - exports 2,287 2,459 (7.0) 7,502 8,522 (12.0)

Source: Company; Angel Research

led by capacity expansion at Honda Motors and Scooters India(HMSI) and Hero MotoCorp coupled with the success of theMaestro and Jupiter models. Motorcycle sales too have revivedand grown strongly by ~12% yoy during the quarter, ledby rural demand and the festival cheer. Going ahead, weexpect the momentum in 2W sales to continue driven byrural demand.

HMCL is expected to lead the earnings growth in the 2W segmentfollowing a strong volume growth of ~7% yoy (~19% qoq), ledby rural demand amid the festival season. We expect EBITDAmargins to improve ~180bp yoy to ~11% led by betterproduct-mix, price increases and also on account of the costreduction initiatives. Consequently the net profit is expected tosurge ~15% yoy (~17% qoq) during the quarter.

We expect Bajaj Auto (BJAUT) to register a ~5% earnings growthdespite a ~2% yoy decline in the top-line. The top-lineperformance is expected to be impacted due to weakness inthe domestic segment (down ~24% yoy), even though the exportvolumes registered a strong growth of ~12% yoy. The company’snet average realization though, is expected to grow strongly by~12% yoy (flat qoq), mainly due to the INR depreciation. Ledby favorable exchange rate, the company’s EBITDA marginsare expected to surge ~180bp yoy to 20.5% during the quarter.

PV sales too remain subdued

The PV segment registered a decline of ~5% yoy YTD in FY2014as challenging macro-economic environment continues toimpact demand. The growth has been affected across all thesegments with the passenger car and utility vehicle segmentsregistering a decline of ~5% and ~6% yoy respectively. Theonly bright spot in the segment remain the rural sales, whichcontinue to hold up well, and strong traction in new launcheslike Grand i10, Amaze and EcoSport. Going ahead, we expectthe sluggish sales trend to continue in the near term as consumersentiments remain subdued.

We expect MSIL to register a strong earnings growth of~24% yoy in 3QFY2014 despite decline in the top-line asEBITDA margins are expected to improve ~310bp yoy to 11.1%on a low base and also due to the impact of Suzuki PowertrainIndia (SPIL) merger. Nonetheless, on a sequential basis, weexpect the top-line to register a growth of ~4%, driven by a~5% qoq growth in volumes on the back of the festival demandduring the quarter. EBITDA margins are likely to decline by~150bp qoq due to adverse product-mix, higher discounts andunfavorable forex movement. As a result, earnings are expectedto decline by ~7% sequentially during the quarter.

Strong scooter sales though insulates the 2W segment

The 2W segment, which registered a growth of ~4% yoy in1HFY2014, has picked up pace and is estimated to have grownby ~12% yoy in 3QFY2014 led by strong rural demand on theback of favorable monsoons. Scooters continued with theirstrong sales momentum and surged by ~25% yoy in 3QFY2014,

Auto ancillaries

Auto ancillary companies in our coverage universe are expectedto post a strong performance on a yoy basis, largely due to thebase effect. However, on a sequential basis the performance isexpected to remain muted due to continued slowdown indemand from OEMs. We expect Motherson Sumi Systems (MSS)to witness a strong earnings growth (yoy as well as sequential)led by continued improvement in utilization at the new plantsand also due to the favorable forex movement.

On a consolidated basis, we expect Apollo Tyres (APTY) toregister a top-line growth of ~5% yoy (down ~2% qoq) drivenprimarily by robust revenue growth in Europe aided by afavorable exchange rate. Domestic and South Africa revenuesare however expected to decline by ~7% and ~4% yoy

Refer to important Disclosures at the end of the report 12

3QFY2014 Results Preview | | | | | January 3, 2014

Automobile

Analyst - YAnalyst - YAnalyst - YAnalyst - YAnalyst - Yaresh Karesh Karesh Karesh Karesh Kothariothariothariothariothari

Exhibit 5: Quarterly estimates – Automobile (`̀̀̀̀ cr)

Source: Company, Angel Research; Note: Price as on December 31, 2013; * Consolidated numbers; ^ OPM adjusted for royalty payment; @ P/E not adjusted for the value of subsidiaries

CompanyCompanyCompanyCompanyCompany CMPCMPCMPCMPCMP Net SalesNet SalesNet SalesNet SalesNet Sales OPM (%)OPM (%)OPM (%)OPM (%)OPM (%) Net PNet PNet PNet PNet Profitrofitrofitrofitrofit EPS (EPS (EPS (EPS (EPS (`̀̀̀̀))))) EPS (EPS (EPS (EPS (EPS (`̀̀̀̀))))) P/E (x)P/E (x)P/E (x)P/E (x)P/E (x) T T T T Targetargetargetargetarget Reco.Reco.Reco.Reco.Reco.

(((((`̀̀̀̀))))) 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E % chg% chg% chg% chg% chg 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E chg bpchg bpchg bpchg bpchg bp 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E % chg% chg% chg% chg% chg 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E % chg% chg% chg% chg% chg FY13FY13FY13FY13FY13 FY14EFY14EFY14EFY14EFY14E FY15EFY15EFY15EFY15EFY15E FY13FY13FY13FY13FY13 FY14EFY14EFY14EFY14EFY14E FY15EFY15EFY15EFY15EFY15E (((((`̀̀̀̀)))))

Ashok Leyland 17 1,953 (18.9) 1.1 (323) (151) 86.0 (0.6) 86.0 0.6 (1.4) 0.7 28.1 - 26.2 - Neutral

Bajaj Auto 1,911 5,321 (1.7) 20.5 183 861 5.2 29.8 5.2 105.2 120.5 142.0 18.2 15.9 13.5 2,272 Buy

Hero MotoCorp^ 2,075 6,869 11.0 11.0 181 561 15.0 28.1 15.0 106.1 107.9 150.8 19.6 19.2 13.8 2,262 Accum.

Maruti Suzuki 1,763 10,928 (2.4) 11.1 312 620 23.7 20.5 23.7 79.2 96.7 111.1 22.3 18.2 15.9 - Neutral

Mah. & Mah.@ 944 10,415 (3.3) 13.2 199 902 7.8 15.3 7.8 54.7 60.4 65.2 17.2 15.6 14.5 1,050 Accum.

Tata Motors* 376 60,209 30.6 13.8 155 3,353 86.2 10.4 84.5 32.9 41.3 48.3 11.4 9.1 7.8 419 Accum.

TVS Motor 76 2,051 14.0 6.1 19 69 30.8 1.4 30.8 4.4 5.2 6.6 17.4 14.7 11.5 - Neutral

Exhibit 6: Quarterly estimates – Auto Ancillary (`̀̀̀̀ cr)

Source: Company, Angel Research; Note: Price as on December 31, 2013, * Consolidated numbers; # December ending; & Full year EPS is consolidated

CompanyCompanyCompanyCompanyCompany CMPCMPCMPCMPCMP Net SalesNet SalesNet SalesNet SalesNet Sales OPM (%)OPM (%)OPM (%)OPM (%)OPM (%) Net PNet PNet PNet PNet Profitrofitrofitrofitrofit EPS (EPS (EPS (EPS (EPS (`̀̀̀̀))))) EPS (EPS (EPS (EPS (EPS (`̀̀̀̀))))) P/E (x)P/E (x)P/E (x)P/E (x)P/E (x) T T T T Targetargetargetargetarget Reco.Reco.Reco.Reco.Reco.

(((((`̀̀̀̀))))) 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E % chg% chg% chg% chg% chg 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E chg bpchg bpchg bpchg bpchg bp 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E % chg% chg% chg% chg% chg 3QFY14E3QFY14E3QFY14E3QFY14E3QFY14E % chg% chg% chg% chg% chg FY13FY13FY13FY13FY13 FY14EFY14EFY14EFY14EFY14E FY15EFY15EFY15EFY15EFY15E FY13FY13FY13FY13FY13 FY14EFY14EFY14EFY14EFY14E FY15EFY15EFY15EFY15EFY15E (((((`̀̀̀̀)))))

Apollo Tyres* 107 3,368 4.7 12.2 32 189 4.8 3.8 4.8 11.8 14.6 15.8 9.1 7.3 6.8 - Neutral

Bharat Forge& 329 858 27.6 25.9 473 93 95.7 4.0 95.7 7.8 16.9 22.2 42.1 19.5 14.8 - Neutral

Bosch# 10,087 2,221 4.2 15.8 336 239 39.0 76.2 39.0 313.2 369.0 448.6 32.2 27.3 22.5 11,215 Accum.

Exide Industries 123 1,500 2.5 14.5 326 134 28.8 1.6 28.8 6.2 6.8 8.1 20.0 18.2 15.2 135 Accum.

FAG Bearings# 1,614 388 11.8 13.9 199 34 14.0 20.4 14.0 73.0 97.8 125.1 22.1 16.5 12.9 1,751 Accum.

Motherson Sumi* 183 7,610 14.2 9.9 226 302 80.7 5.1 80.7 10.3 11.7 13.6 17.7 15.7 13.4 218 Buy

We expect Motherson Sumi Systems (MSS) to post favorableresults on the back of the improving utilization levels at the newfacilities and also due to INR depreciation. On the consolidatedfront, we expect the top-line to post a strong growth of ~14%yoy (~5% qoq), driven primarily by ~20% and ~13% yoy growthin Samvardhana Motherson Reflectec (SMR) and Peguformrevenues respectively. We expect EBITDA margins to improve~230bp yoy (~30bp qoq) to 9.9%, aided by better utilizationlevels and also due to cost control initiatives. The net profittherefore is expected to register a strong growth of ~81% yoy(~18% qoq) during the quarter.

Outlook

While the near term environment continues to remainchallenging for the automotive sector, we believe the long-termstructural growth drivers for the industry such as GDP growth(leading to increasing affluence of rural and urban consumers),favorable demographics, low penetration levels, entry of globalplayers and easy availability of finance will remain intact. Wecontinue to prefer stocks that have strong fundamentals, highexposure to rural and export markets and command superiorpricing power. WWWWWe maintain our positive view on Bajaj Auto,e maintain our positive view on Bajaj Auto,e maintain our positive view on Bajaj Auto,e maintain our positive view on Bajaj Auto,e maintain our positive view on Bajaj Auto,Mahindra & Mahindra and TMahindra & Mahindra and TMahindra & Mahindra and TMahindra & Mahindra and TMahindra & Mahindra and Tata Motors.ata Motors.ata Motors.ata Motors.ata Motors.

respectively due to a weak demand scenario. We expect EBITDAmargins to improve marginally by ~30bp yoy to 12.2%(flat qoq) leading to an ~5% yoy (down ~14% qoq) growth inearnings.

For Bharat Forge (BHFC), we expect the standalone earnings toswell ~96% yoy largely due to the base effect. Its top-line isexpected to jump ~28% yoy led by ~17% and ~10% yoy growthin volumes and net average realization respectively. Thecompany’s EBITDA margins are expected to improve sharplyby ~470bp yoy to 25.9% driven by better product-mix andfavorable exchange rate. Nevertheless, on a sequential basis,we expect the company’s bottom-line to decline by ~4% asEBITDA margins are expected to contract 50bp qoq due to costpressures.

We expect Bosch (BOS) to post a modest top-line growth of~4% yoy (~3% qoq) largely driven by exports. On the operatingfront, margins are expected to expand by ~340bp yoy (~65bpqoq) to 15.8% led by cost control measures. Consequently, itsnet profit is expected to increase by ~39% yoy (~2% qoq) duringthe quarter.

We expect Exide Industries (EXID) to register a modest top-linegrowth of ~3% yoy (~5% qoq) primarily due to slowdown indemand from OEMs. Nonetheless, we expect its EBITDA marginsto improve ~330bp yoy (~50bp qoq) to 14.5% due to thepricing action and easing of lead prices. As a result, we expectthe company’s bottom-line to register a growth of ~29% yoy(~13% qoq) during the quarter.

13

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

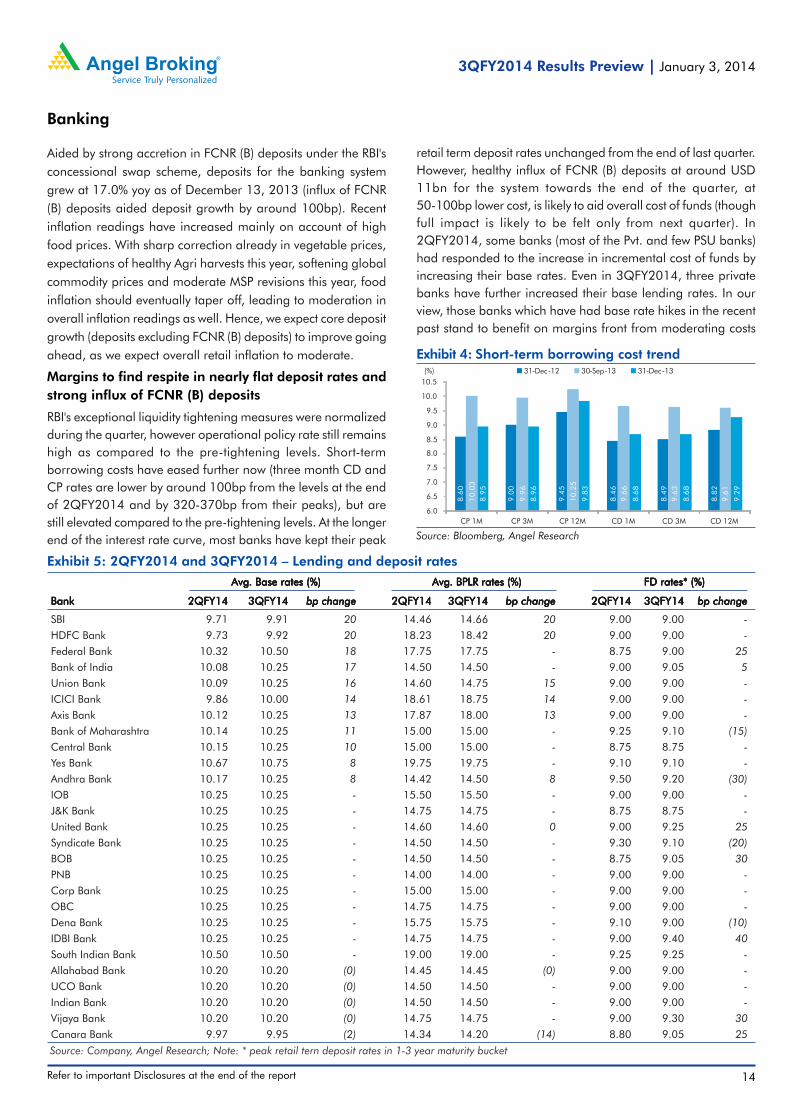

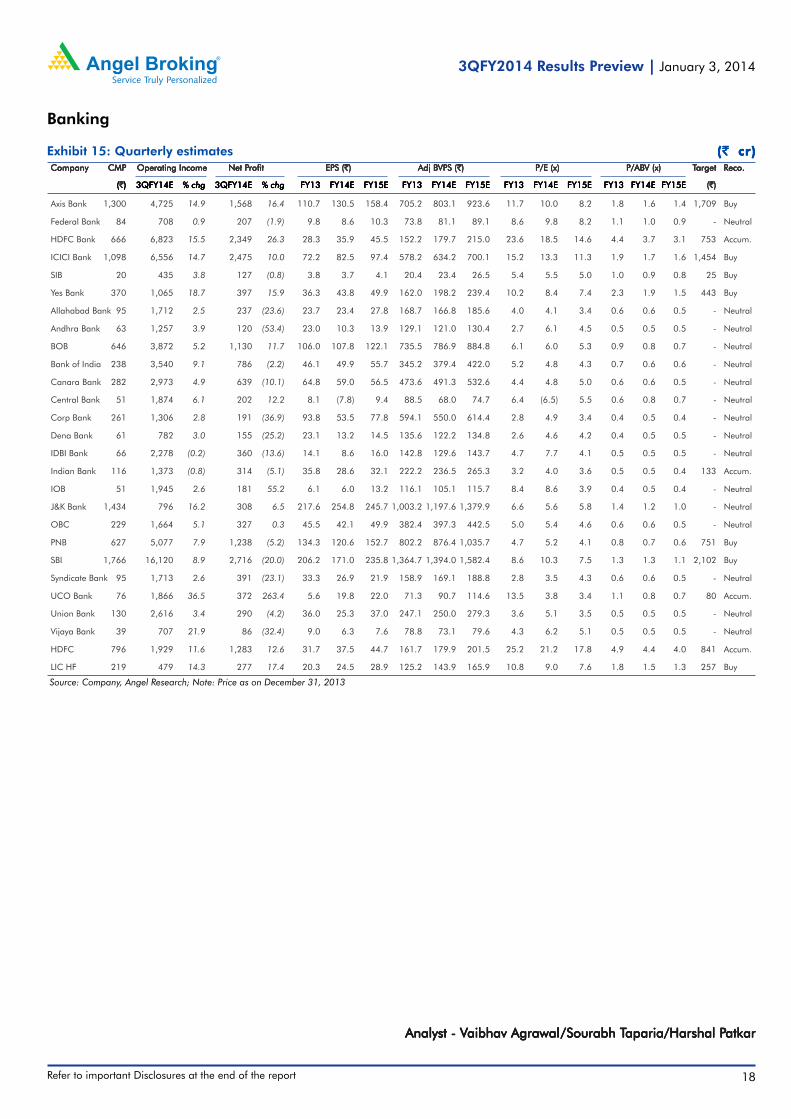

Banking

Banking stocks outperformed broader markets onimproved liquidity, sentiments

Banking stocks outperformed the broader markets during3QFY2014, as more than two-third of our coverage banksregistered a sequential gain of more than 15%. During thequarter, the RBI normalized its exceptional liquidity tighteningmeasures taken in the previous quarter, as its other structuralmeasures (gold import curbs, swap facility for OMCs banksetc) restored stability in the currency markets. The RBI alsoincreased repo rate once during the quarter by 25bp, so as toanchor inflationary expectations, while it eased systemic liquidityby introducing Term Repos (7 and 14 days) to the extent of0.5% of the NDTL or `40,000cr. Recently it injected another`10,000cr via Term Repos to support advance tax related payoutfrom banks.

As the RBI normalized most of its exceptional liquidity tighteningmeasures, short term rates have come off by 100-125bp qoq(though they are still elevated compared to pre-tightening levels).At the longer end of the interest rate curve, most banks have

Source: RBI, Angel Research

Exhibit 2: FCNR (B) deposits aid deposits growthCredit Gr. (%) Deposits Gr. (%)

10.00

11.00

12.00

13.00

14.00

15.00

16.00

17.00

18.00

19.00

20.00

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

Nov-

12

Dec-1

2

Jan

-13

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov-

13

Source: RBI, Angel Research

Exhibit 3: Liquidity remains comfortable

(2,500)

(2,000)

(1,500)

(1,000)

(500)

-

500

Nov-

12

Dec-1

2

Jan

-13

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov-

13

Dec-1

3

(` bn)Repo Term Repo MSF

kept their peak retail term deposit rates unchanged from theend of last quarter. Higher short-term funding cost is likely toresult in margin pressures for those banks which have not takencorresponding base rate hikes. Moreover, the un-provided MTMlosses as of 2QFY2014 end would also affect profitability forsome PSU banks (no provisioning required for new private bankson that count as they have already provided fully).

Overall, we expect earnings divergence amongst our coveragebanking stocks to continue during 3QFY2014 as well. We expectour coverage new private banks to deliver earnings growth of17.1% yoy, while our coverage PSU and old private banks areexpected to register bottom-line de-growth of 9.0% and1.5% yoy, respectively.

Credit growth remains moderate; strong FCNR (B)deposit mobilization aids healthy deposit growth

Credit growth for the banking system, after witnessing suddenacceleration in 2QFY2014 to 17.7% yoy aided by shift fromCommercial Paper borrowings to loans, has now againmoderated to 15.3% yoy as of December 13, 2013. Achallenging macro environment and policy woes in select sectorshas affected investment sentiments for quite some time now.Hence incremental credit demand from corporates remainsweak, largely comprising of working capital needs. Goingforward, in our view, credit growth for FY2014 is likely to bearound 15%, as credit disbursement pipeline for banks, asindicated by their Managements, remains thin, largelycomprising of sanctions already in place.

Exhibit 1: 3QFY2014 stock performance(%)(%)(%)(%)(%) Returns (qoq)Returns (qoq)Returns (qoq)Returns (qoq)Returns (qoq) Returns (yoy)Returns (yoy)Returns (yoy)Returns (yoy)Returns (yoy)

Indian Bank 72.3 (41.7)

OBC 58.1 (34.6)

Bank of India 50.6 (30.6)

Federal Bank 47.7 (21.9)

Syndicate Bank 39.8 (26.2)

PNB 32.8 (47.0)

Dena Bank 35.8 (28.1)

BOB 30.3 (4.2)

UCO Bank 30.8 (25.5)

Axis Bank 28.8 (20.2)

Yes Bank 28.9 (4.2)

Canara Bank 27.5 (43.2)

J&K Bank 24.3 (3.5)

Allahabad Bank 25.1 (44.1)

ICICI Bank 26.1 10.9

Andhra Bank 21.4 (46.8)

Union Bank 18.6 (9.4)

LIC HF 16.6 (39.8)

IOB 16.7 (24.7)

IDBI Bank 12.3 (1.9)

HDFC Bank 13.7 (40.4)

Vijaya Bank 9.4 (25.9)

SBI 9.2 9.0

Corp Bank 7.1 (43.4)

United Bank 6.6 (60.0)

HDFC 2.5 (25.4)

South Indian Bank (SIB) 4.0 (4.1)

Central Bank 1.7 (39.0)

Bank of Maharashtra (3.9) (40.3)

Source: Bloomberg, Angel Research

Refer to important Disclosures at the end of the report 14

3QFY2014 Results Preview | | | | | January 3, 2014

Banking

Exhibit 5: 2QFY2014 and 3QFY2014 – Lending and deposit rates

Source: Company, Angel Research; Note: * peak retail tern deposit rates in 1-3 year maturity bucket

Avg Avg Avg Avg Avg. Base rates (%). Base rates (%). Base rates (%). Base rates (%). Base rates (%) Avg Avg Avg Avg Avg. BPLR rates (%). BPLR rates (%). BPLR rates (%). BPLR rates (%). BPLR rates (%) FD rates* (%) FD rates* (%) FD rates* (%) FD rates* (%) FD rates* (%)

BankBankBankBankBank 2QFY142QFY142QFY142QFY142QFY14 3QFY143QFY143QFY143QFY143QFY14 bp changebp changebp changebp changebp change 2QFY142QFY142QFY142QFY142QFY14 3QFY143QFY143QFY143QFY143QFY14 bp changebp changebp changebp changebp change 2QFY142QFY142QFY142QFY142QFY14 3QFY143QFY143QFY143QFY143QFY14 bp changebp changebp changebp changebp change

SBI 9.71 9.91 20 14.46 14.66 20 9.00 9.00 -

HDFC Bank 9.73 9.92 20 18.23 18.42 20 9.00 9.00 -

Federal Bank 10.32 10.50 18 17.75 17.75 - 8.75 9.00 25

Bank of India 10.08 10.25 17 14.50 14.50 - 9.00 9.05 5

Union Bank 10.09 10.25 16 14.60 14.75 15 9.00 9.00 -

ICICI Bank 9.86 10.00 14 18.61 18.75 14 9.00 9.00 -

Axis Bank 10.12 10.25 13 17.87 18.00 13 9.00 9.00 -

Bank of Maharashtra 10.14 10.25 11 15.00 15.00 - 9.25 9.10 (15)

Central Bank 10.15 10.25 10 15.00 15.00 - 8.75 8.75 -

Yes Bank 10.67 10.75 8 19.75 19.75 - 9.10 9.10 -

Andhra Bank 10.17 10.25 8 14.42 14.50 8 9.50 9.20 (30)

IOB 10.25 10.25 - 15.50 15.50 - 9.00 9.00 -

J&K Bank 10.25 10.25 - 14.75 14.75 - 8.75 8.75 -

United Bank 10.25 10.25 - 14.60 14.60 0 9.00 9.25 25

Syndicate Bank 10.25 10.25 - 14.50 14.50 - 9.30 9.10 (20)

BOB 10.25 10.25 - 14.50 14.50 - 8.75 9.05 30

PNB 10.25 10.25 - 14.00 14.00 - 9.00 9.00 -

Corp Bank 10.25 10.25 - 15.00 15.00 - 9.00 9.00 -

OBC 10.25 10.25 - 14.75 14.75 - 9.00 9.00 -

Dena Bank 10.25 10.25 - 15.75 15.75 - 9.10 9.00 (10)

IDBI Bank 10.25 10.25 - 14.75 14.75 - 9.00 9.40 40

South Indian Bank 10.50 10.50 - 19.00 19.00 - 9.25 9.25 -

Allahabad Bank 10.20 10.20 (0) 14.45 14.45 (0) 9.00 9.00 -

UCO Bank 10.20 10.20 (0) 14.50 14.50 - 9.00 9.00 -

Indian Bank 10.20 10.20 (0) 14.50 14.50 - 9.00 9.00 -

Vijaya Bank 10.20 10.20 (0) 14.75 14.75 - 9.00 9.30 30

Canara Bank 9.97 9.95 (2) 14.34 14.20 (14) 8.80 9.05 25

Aided by strong accretion in FCNR (B) deposits under the RBI'sconcessional swap scheme, deposits for the banking systemgrew at 17.0% yoy as of December 13, 2013 (influx of FCNR(B) deposits aided deposit growth by around 100bp). Recentinflation readings have increased mainly on account of highfood prices. With sharp correction already in vegetable prices,expectations of healthy Agri harvests this year, softening globalcommodity prices and moderate MSP revisions this year, foodinflation should eventually taper off, leading to moderation inoverall inflation readings as well. Hence, we expect core depositgrowth (deposits excluding FCNR (B) deposits) to improve goingahead, as we expect overall retail inflation to moderate.

Margins to find respite in nearly flat deposit rates andstrong influx of FCNR (B) deposits

RBI's exceptional liquidity tightening measures were normalizedduring the quarter, however operational policy rate still remainshigh as compared to the pre-tightening levels. Short-termborrowing costs have eased further now (three month CD andCP rates are lower by around 100bp from the levels at the endof 2QFY2014 and by 320-370bp from their peaks), but arestill elevated compared to the pre-tightening levels. At the longerend of the interest rate curve, most banks have kept their peak

retail term deposit rates unchanged from the end of last quarter.However, healthy influx of FCNR (B) deposits at around USD11bn for the system towards the end of the quarter, at50-100bp lower cost, is likely to aid overall cost of funds (thoughfull impact is likely to be felt only from next quarter). In2QFY2014, some banks (most of the Pvt. and few PSU banks)had responded to the increase in incremental cost of funds byincreasing their base rates. Even in 3QFY2014, three privatebanks have further increased their base lending rates. In ourview, those banks which have had base rate hikes in the recentpast stand to benefit on margins front from moderating costs

Source: Bloomberg, Angel Research

Exhibit 4: Short-term borrowing cost trend

8.6

0

9.0

0

9.4

5

8.4

6

8.4

9

8.8

2

10.0

3

9.9

6

10.2

5

9.6

6

9.6

3

9.6

1

8.9

5

8.9

6

9.8

3

8.6

8

8.6

8

9.2

9

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

CP 1M CP 3M CP 12M CD 1M CD 3M CD 12M

(%) 31-Dec-12 30-Sep-13 31-Dec-13

15

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Banking

of funds, aided by nearly flat deposit rates, lower cost ofborrowings qoq and healthy influx of FCNR (B) deposits.

Aided by strong accretion in FCNR (B) deposits under the RBI'sconcessional swap scheme, deposits for the banking systemgrew at 17.0% yoy. Systemic liquidity has improved aided bycapital flows under RBI swap facility for banking capital andFCNR (B) deposits. On back of improved liquidity amidstmoderate credit demand, most of our coverage banks kepttheir peak retail term deposit rates unchanged during thequarter. Four of our coverage banks reduced their retail termdeposit rates by 10-30bp qoq, drawing comfort from ampleliquidity, while seven of them increased their retail term depositrates. Highest increase in retail term deposit rates was witnessed incase of IDBI Bank (40bp qoq), followed by BOB and Vijaya Bank by30bp qoq and Canara Bank and United Bank by 25bp qoq.

As far as lending rates are concerned, three of our coveragebanks further increased their base rates during the quarter (SBIand HDFC Bank by 20bp and Federal Bank by 10bp), citingelevated incremental costs of funds. Hence, on an average basis,the base lending rate would be higher for those three banksand also for eight others which had raised their lending ratessometime in last quarter. Highest sequential increase in baselending rate would be for SBI and HDFC Bank (by 20bp each),followed by Federal Bank, Bank of India and Union Bank (by16-18bp each) and ICICI Bank and Axis Bank (by 13-14bpeach), while in case of Canara Bank it would be lower marginallyby 2bp.

Asset quality pressures likely to remain elevated

Asset quality stress has remained at elevated levels for Indian

banks for quite some time now, and has severely dented the

sector's performance and outlook. Slippages for the banking

industry have continued to trend northwards over the last few

years. Even in 2QFY2014, Indian banks' fresh NPL formation

remained high at 3.1%, which although was slightly better on a

qoq/yoy basis (3.7% in 1QFY2014 and 3.4% in 2QFY2013).

Recent healthy exports growth has provided a much needed

breather to the economy and more specifically to stressed sectors

like textiles. Expectations of sustained moderation in inflation

going ahead owing to lower food inflation is likely to act as a

single biggest positive catalyst for our economy. Sustained

moderation in inflation, as and when it happens, would

eventually provide room to lower interest rates, thereby leading

to improvement in growth, higher savings and investments

mobilization and improvement in asset quality outlook.

Until then, in the near term, while we expect slippages to

moderate here on, they are likely to remain at elevated levels.

Recoveries/upgrades performance can be expected to be better

than earlier, aided by the recent pick up in sale of assets to

ARCs. Overall, we expect net slippages to trend lower here on.

Private banks have not been spared from asset quality pressures,

however, they have not only been reporting much lower

slippages, but have also performed reasonably on the recoveries

and upgrades front and have managed to keep their asset

quality largely intact until now in a challenging economic

environment. Even going ahead, we expect private banks to

continue outperforming their nationalized peers on the asset

quality front.

During 2QFY2014, few banks like Bank of India, Allahabad

Bank, witnessed a sudden spurt in their recoveries from written

off accounts, largely aided by asset sale to ARCs, which

contributed significantly to their earnings for the quarter. Given

the determined efforts across banks to improve their asset quality

before the end of the fiscal, asset sale to ARCs is likely to pick

up further, with media reports suggesting that few banks taken

together have put up assets worth `4,000cr for sale to ARCs

during the quarter (SBI - ̀ 1,200cr, Dena Bank - ̀ 600cr, OBC -

`640cr, Allahabad Bank - `350cr). Healthy quantum of asset

sale to ARCs is likely to remain a significant contributor to

profitability for many of these banks in 3QFY2014.

On the restructuring front, corporate debt restructuring (CDR)referrals have also risen significantly over the last severalquarters, closely tracking the deteriorating economic growth

New private banks to deliver better numbersyet againDuring 3QFY2014, we expect earnings divergence amongstour coverage banking stocks to continue. We expect ourcoverage new private banks to deliver healthy earnings growthof 17.1% yoy, while our coverage PSU and old private banksare expected to register bottom-line de-growth of 9.0% and1.5% yoy, respectively.

New private banks are expected to deliver healthy NII growthof 20.1% yoy, which is expected to aid healthy growth of 15.3%yoy in operating income, dragged by moderate performanceon non-interest income (at 6.9% yoy). On back of healthyoperating profit growth of 18.4% yoy, our coverage new privatebanks are expected to report healthy earnings growth of17.1% yoy. On the other hand, PSU and old private banks areexpected to register moderate NII growth of 10.6% and9.6% yoy, respectively and muted non-interest incomeperformance with yoy de-growth of 4.8% and 21.9%,respectively. Additionally, operating expenses growth for PSUand old private banks is expected to be higher than new privatebanks at 21.6% and 15.3% yoy, respectively. Overall, we expectour coverage PSU and old private banks to register bottom-linede-growth of 9.0% and 1.5% yoy, respectively.

Refer to important Disclosures at the end of the report 16

3QFY2014 Results Preview | | | | | January 3, 2014

Banking

Referred Referred Referred Referred Referred Approved Approved Approved Approved ApprovedNo. of casesNo. of casesNo. of casesNo. of casesNo. of cases Add. (Add. (Add. (Add. (Add. (`̀̀̀̀ cr) cr) cr) cr) cr) No. of casesNo. of casesNo. of casesNo. of casesNo. of cases Add. (Add. (Add. (Add. (Add. (`̀̀̀̀ cr) cr) cr) cr) cr)

FY10 31 20,175 31 17,763

FY11 49 22,614 27 6,615

1QFY12 18 4,595 10 8,141

2QFY12 18 21,095 7 2,095

3QFY12 23 19,187 17 21,364

4QFY12 28 23,012 16 8,001

FY12 87 67,889 50 39,601

1QFY13 41 20,528 17 17,957

2QFY13 33 18,907 18 18,925

3QFY13 25 20,957 35 24,581

4QFY13 31 31,256 39 17,035

FY13 130 91,648 109 78,498

1QFY14 27 39,370 14 21,266

2QFY14 31 24,859 16 22,007

Outstanding 580 362,370 431 272,286

Exhibit 10: CDR snapshot

Source: CDR Cell, Angel Research

environment. Under CDR mechanism, fresh approvals of around`22,000cr in 2QFY2014 (unless the implementation is delayedfor any reason) and the pending cases of around `44,000cr(only those which are approved and implemented during thequarter), would add to the restructuring book of participatingbanks during the current quarter.

As far as the progress on SEB restructuring under the centre'sFinancial Restructuring Plan (FRP) is concerned, so far six states- Tamil Nadu, Uttar Pradesh, Haryana, Rajasthan, MadhyaPradesh and Punjab have finalized restructuring of their short-term debt upto March 2012 under the FRP. Further, CCEA hasalso allowed Jharkhand, Bihar and Andhra Pradesh torestructure their short-term debt upto March 2013 under theFRP. FRP entails conversion of 50% of the short-term debt ofdiscoms into bonds (which would be eventually taken over bystates over a period of 2-5 years), while the balance 50% wouldbe restructured by the banks. Conversion of short-term debt tobonds (priced at around 9-10%) would result in 200-300bpreduction in yields for banks and would be negative for banksfrom an NIM perspective. At the same time, it would also entailrelease of 300-325bp provisioning on this debt (part of whichis converted to bonds), making the arrangement positive on an

overall basis.

As indicated by their Managements, the restructuring pipeline

appears sizable for banks like Canara Bank (~`6,500cr of which

~`3,000cr would be discoms under FRP), SBI (~`6,000cr over

Source: Company, Angel Research

Exhibit 9: Net NPA trend (%) for the banking industry

1.08 1.071.00 0.99

1.04

1.281.36

1.30

1.49

1.741.80

1.72

2.09

2.25

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

2.50

1Q

FY11

2Q

FY11

3Q

FY11

4Q

FY11

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

Source: Company, Angel Research

Exhibit 8: Gross NPA trend (%) for the banking industry

2.43 2.472.40

2.282.43

2.732.85 2.80

3.09

3.413.49

3.32

3.80

4.02

2.10

2.30

2.50

2.70

2.90

3.10

3.30

3.50

3.70

3.90

4.10

4.30

1Q

FY1

1

2Q

FY1

1

3Q

FY1

1

4Q

FY1

1

1Q

FY1

2

2Q

FY1

2

3Q

FY1

2

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

Source: Company, Angel Research

Exhibit 6: Gross NPA trends (%) – Private vs PSU

2.80 2.702.57

2.362.33 2.24 2.17

2.01 2.05 2.06 2.00 1.90 2.00 2.02

2.34 2.42 2.35 2.272.45

2.853.02 2.98

3.34

3.75 3.873.67

4.264.52

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

1Q

FY1

1

2Q

FY1

1

3Q

FY1

1

4Q

FY1

1

1Q

FY1

2

2Q

FY1

2

3Q

FY1

2

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

Pvt Banks PSU Banks

Source: Company, Angel Research

Exhibit 7: Net NPA trends (%) – Private vs PSU

0.920.79

0.690.56 0.56 0.54 0.54 0.46 0.49 0.54 0.55 0.53 0.62 0.66

1.121.131.07 1.09 1.16

1.47 1.56 1.501.73

2.04 2.12 2.01

2.472.65

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1Q

FY1

1

2Q

FY1

1

3Q

FY1

1

4Q

FY1

1

1Q

FY1

2

2Q

FY1

2

3Q

FY1

2

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

Pvt Banks PSU Banks

the next few quarters), Union Bank (~`3,000cr, majority of which

comprises discom restructuring under FRP), OBC (~`2,300cr),

Syndicate Bank (~`2,100cr, majority of which comprises

discoms under FRP), Andhra Bank (~`3,000cr) and Central

Bank (~`2,000cr).

17

3QFY2014 Results Preview | | | | | January 3, 2014

Refer to important Disclosures at the end of the report

Banking

Source:C-line, Angel Research, Note:* For PSU banks excl. SBI and IDBI

Exhibit 13: PSU banks’ price band (P/ABV)*

0.30

0.60

0.90

1.20

1.50

1.80

2.10

Dec-0

4

Jun

-05

Dec-0

5

Jun

-06

Dec-0

6

Jun

-07

Dec-0

7

Jun

-08

Dec-0

8

Jun

-09

Dec-0

9

Jun

-10

Dec-1

0

Jun

-11

Dec-1

1

Jun

-12

Dec-1

2

Jun

-13

Dec-1

3

Source:C-line, Angel Research, Note:*under our coverage

Exhibit 14: New Private banks’ price band (P/ABV)*

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Dec-0

4

Jul-

05

Feb

-06

Sep

-06

Apr-

07

Nov-

07

Jun

-08

Jan

-09

Aug

-09

Mar-

10

Oct

-10

May-

11

Dec-1

1

Jul-

12

Feb

-13

Sep

-13

IndustryIndustryIndustryIndustryIndustry No.No.No.No.No. AggAggAggAggAgg. Debt (. Debt (. Debt (. Debt (. Debt (`̀̀̀̀ cr) cr) cr) cr) cr) %%%%%

Iron& Steel 46 41,812 21.3

Infrastructure 20 35,543 18.1

Textiles 47 19,545 10.0

Power 13 17,225 8.8

Telecom 5 9,808 5.0

Ship-Breaking/Ship Building 3 6,732 3.4

Pharmaceuticals 9 6,375 3.3

NBFC 6 6,257 3.2

Paper/Packaging 15 5,280 2.7

Sugar 16 4,955 2.5

Petrochemicals 2 4,852 2.5

Hospitality 10 4,806 2.5

Fertilizers 6 4,193 2.1

Computer hardware 2 3,113 1.6

Cements 7 2,242 1.1

Electronics 1 2,230 1.1

Others 53 21,299 10.8

TTTTTotalotalotalotalotal 261261261261261 196,267196,267196,267196,267196,267 100100100100100

Exhibit 11: Industry-wise live approved cases under CDR

Source: CDR Cell, Angel Research

Source: Bloomberg, Angel Research

Exhibit 12: Corporate and G-Sec bond yields

9.0

6

9.1

0

9.0

6

7.9

3

8.0

3

8.0

5

9.8

4

9.9

4

9.9

6

8.7

0

8.8

5

8.7

6

9.8

5

9.6

3

9.6

2

8.5

6

8.8

9

8.8

3

6.0

7.0

8.0

9.0

10.0

11.0

12.0

AAA 3 Yr AAA 5 Yr AAA 10 Yr Gsec 3Yr Gsec 5Yr Gsec 10Yr

(%) 31-Dec-12 30-Sep-13 31-Dec-13

Un-provided MTM losses to require meaningfulprovisioning for some PSU banks