31 Jan Banfora Gold Project Delivers Robust BFS - Gryphon Minerals

21

Corporate Directory Mel Ashton Non-Executive Chairman Stephen Parsons Managing Director Didier Murcia Non-Executive Director David Netherway Non-Executive Director Andrea Hall Non-Executive Director Steven Zaninovich Chief Operating Officer Matthew Bowles Head of Corporate Development Beth Michetti Chief Financial Officer Alex Eastwood General Counsel & Co Secretary Advancing the world class 4.9Moz Banfora Gold Project Burkina Faso, West Africa EV/Resource oz $25 Contact Details Principal & Registered Office Freemasons Hall 181 Roberts Road SUBIACO WA 6008 T: +61 8 9287 4333 F: +61 8 9287 4334 E: [email protected] ASX CODE GRY Investor Relations MAGNUS Investor Relations John Gardner T: +61 413 355 997 www.gryphonminerals.com.au Note 1: Refer to Resource and Reserve estimate tables and appendices Note 2: Conversion based on the 2012 average rate of AUD/USD$1.04 Note 3: Refer to Capital costs table showing contingency amount Note 4: Valued as at 31 December 2012 Note 5: We note this is below the 3-year trailing average of ~US$1,500 ASX Announcement and Media Release 31 January 2013 Bankable Feasibility Study Demonstrates Viability of Developing Banfora Gold Project, Burkina Faso Highlights Bankable Feasibility Study (“BFS”) demonstrates the viability of developing the Banfora Gold Project to be the next gold mine in Burkina Faso. BFS based on a conventional 2Mtpa CIL processing plant and open pit mining operation using contractor mining, up-scalable to +4Mtpa. Construction period of 15 months with first gold anticipated in Q4 2014. BFS supports a maiden Ore Reserve estimate of 1.05Moz of gold 1 . Banfora Gold Project global Mineral Resource estimate increased to 4.9Moz gold 1 . 90% of the Resource and Reserve estimates are shallow - above 150 metres depth and remain ‘open’ - strong likelihood for further increases through ongoing drilling. Work continues on delivering on the project’s huge potential upside with the option to expand the plant to +4Mtpa in addition to drilling aimed at further increases in resources and reserves and new discoveries. Key operating results of the BFS on a base case of US$1,300 5 gold price include: Average gold production for the first 5 years 151,000 ounces of gold p.a. Average gold grade for the first 5 years 2.38 g/t Average cash cost for the first 5 years US$734 per ounce (A$706/oz 2 ) Capital costs US$208M (A$200M) + contingencies 3 Refer to Table 1 for further details Moving Forward Permitting: Process has commenced and, given the six month permitting process in Burkina Faso, is anticipated to be completed by Q3 2013. Funding: Strong interest has been received from a large number of financial institutions to provide funding for project development. A formal process to appoint financiers is commencing in the coming weeks. Gryphon has A$83M in cash and listed investments 4 . Mr Steve Parsons, Managing Director commented:- “The completion of this BFS is a significant step towards the Banfora Gold Project becoming a major mining operation and towards Gryphon’s transformation into a gold producer. The BFS confirms the economic viability of this low risk, conventional open pit CIL operation. Gryphon will continue to work closely with all stakeholders, including the Burkina Faso Government and local community, as it focuses on full funding and development of the Banfora Gold Project and obtains all the necessary approvals to commence construction over the coming months. “Furthermore, we are extremely excited by the huge exploration upside the project continues to deliver on. We anticipate additional conversion of resource to reserve ounces with ongoing infill drilling, plus continued resource growth from step-out shallow as well as deeper drilling and more new discoveries at Banfora”. “The Banfora Gold Project is on track for first gold production in Q4 2014, making it the next gold mine to come into operation in Burkina Faso.”

Transcript of 31 Jan Banfora Gold Project Delivers Robust BFS - Gryphon Minerals

Corporate Directory

Mel Ashton

Non-Executive Chairman

Stephen Parsons

Managing Director

Didier Murcia

Non-Executive Director

David Netherway

Non-Executive Director

Andrea Hall

Non-Executive Director

Steven Zaninovich

Chief Operating Officer

Matthew Bowles

Head of Corporate Development

Beth Michetti

Chief Financial Officer

Alex Eastwood

General Counsel & Co Secretary

Advancing the world class

4.9Moz Banfora Gold Project

Burkina Faso,

West Africa

EV/Resource oz $25

Contact Details

Principal & Registered Office

Freemasons Hall

181 Roberts Road

SUBIACO WA 6008

T: +61 8 9287 4333

F: +61 8 9287 4334

ASX CODE

GRY

Investor Relations

MAGNUS Investor Relations

John Gardner

T: +61 413 355 997

www.gryphonminerals.com.au

Note 1: Refer to Resource and Reserve estimate tables and appendices

Note 2: Conversion based on the 2012 average rate of AUD/USD$1.04

Note 3: Refer to Capital costs table showing contingency amount

Note 4: Valued as at 31 December 2012

Note 5: We note this is below the 3-year trailing average of ~US$1,500

ASX Announcement and Media Release 31 January 2013

Bankable Feasibility Study

Demonstrates Viability of Developing

Banfora Gold Project, Burkina Faso

Highlights

Bankable Feasibility Study (“BFS”) demonstrates the viability of developing the

Banfora Gold Project to be the next gold mine in Burkina Faso.

BFS based on a conventional 2Mtpa CIL processing plant and open pit mining

operation using contractor mining, up-scalable to +4Mtpa.

Construction period of 15 months with first gold anticipated in Q4 2014.

BFS supports a maiden Ore Reserve estimate of 1.05Moz of gold1.

Banfora Gold Project global Mineral Resource estimate increased to 4.9Moz gold1.

90% of the Resource and Reserve estimates are shallow - above 150 metres depth

and remain ‘open’ - strong likelihood for further increases through ongoing drilling.

Work continues on delivering on the project’s huge potential upside with the option

to expand the plant to +4Mtpa in addition to drilling aimed at further increases in

resources and reserves and new discoveries.

Key operating results of the BFS on a base case of US$1,3005 gold price include:

Average gold production for the first 5 years 151,000 ounces of gold p.a.

Average gold grade for the first 5 years 2.38 g/t

Average cash cost for the first 5 years US$734 per ounce (A$706/oz2)

Capital costs US$208M (A$200M) + contingencies3

Refer to Table 1 for further details

Moving Forward

Permitting: Process has commenced and, given the six month permitting process in

Burkina Faso, is anticipated to be completed by Q3 2013.

Funding: Strong interest has been received from a large number of financial

institutions to provide funding for project development. A formal process to appoint

financiers is commencing in the coming weeks. Gryphon has A$83M in cash and

listed investments4.

Mr Steve Parsons, Managing Director commented:- “The completion of this BFS is a

significant step towards the Banfora Gold Project becoming a major mining operation

and towards Gryphon’s transformation into a gold producer. The BFS confirms the

economic viability of this low risk, conventional open pit CIL operation. Gryphon will

continue to work closely with all stakeholders, including the Burkina Faso Government

and local community, as it focuses on full funding and development of the Banfora Gold

Project and obtains all the necessary approvals to commence construction over the

coming months.

“Furthermore, we are extremely excited by the huge exploration upside the project

continues to deliver on. We anticipate additional conversion of resource to reserve

ounces with ongoing infill drilling, plus continued resource growth from step-out shallow

as well as deeper drilling and more new discoveries at Banfora”.

“The Banfora Gold Project is on track for first gold production in Q4 2014, making it the

next gold mine to come into operation in Burkina Faso.”

P a g e 2 www.gryphonminerals.com.au

Gryphon Minerals Limited (ASX: GRY), is pleased to announce the results of the Bankable Feasibility Study (“BFS”) at its

flagship 100% owned Banfora Gold Project in Burkina Faso. The study which confirms Banfora as an economically and

technically robust project.

Bankable Feasibility Study

The BFS was prepared on the Banfora Gold Project located in South West Burkina Faso, West Africa, 350 kilometres

South West of Burkina Faso’s capital city of Ouagadougou.

The BFS was coordinated by Lycopodium Minerals Pty Ltd with input from various industry consultants. Mine planning

and mine designs were prepared by Cube Consulting Pty Ltd and financial modelling of the BFS outputs was

undertaken by Corality Pty Ltd. Metallurgical test work was completed by ALS-AMMTEC and supervised by Lycopodium

whilst environmental and social impact assessments were carried out by a group of West African expert consultants

including MBS Environmental and Intersocial Consulting (Refer to Table 1 of Appendix One).

The BFS proposes a contract mining operation and a conventional industry standard Carbon In Leach (CIL) 2Mtpa gold

processing plant, along with associated infrastructure, to mine and process approximately 16.7Mt of ore from defined

ore reserves over an initial eight-year period. The plant has been designed for up scaling to +4Mtpa at a later date,

potentially funded from project cash flows.

A gold price of US$1,300 was used for pit optimisations and base case financial modelling. Key commercial results of

the BFS are presented below.

Table 1 | Key results in US$

US$1,300/oz

gold

US$1,600/oz

gold

US$2,000/oz

gold

Ore processed – tonnes @ g/t gold 16.7Mt @ 1.95g/t 16.7Mt @ 1.95g/t 16.7Mt @ 1.95g/t

Strip Ratio 6.1:1 6.1:1 6.1:1

Capital Cost2 US$208M US$208M US$208M

Mining Costs $23.25/t ore, $404/oz $23.25/t ore, $404/oz $23.25/t ore, $404/oz

Process Gold Recovery 92.0% 92.0% 92.0%

Current life of mine (“LOM”) 8 years 8 years 8 years

LOM Revenue US$1.3b US$1.5b US$1.9b

EBITDA3 US$455M US$714M US$1,077M

NPV undiscounted US$205M US$467M US$833M

NPV 5% discount US$121M US$328M US$618

IRR4 17% 35% 56%

Payback period 3.7 years 2.4 years 1.5 years

Royalties paid (State)5 US$50M US$77M US$96M

Avg. LOM Cash Operating Costs/oz (C1)1 US$744 (A$715)/oz US$744 (A$715)/oz US$744 (A$715)/oz

Notes:

1) Conversion based on the 2012 average rate of AUD/USD$1.04AUD

2) Excludes contingency of US$21m, Refer to Table 6 of Appendix One for breakdown of costs

3) EBITDA is earnings prior to interest, tax, depreciation and amortisation but includes Government royalties

4) IRR is calculated at the commencement of production

5) Based on the Ministerial Decree sliding scale of rates of 3-5%, dependent on gold price

P a g e 3 www.gryphonminerals.com.au

Huge Upside Potential at the Banfora Gold Project

Resource and Reserve growth (refer to pit design and block model images below)

Step out drilling around current pit designs and current infill drilling to convert resources to reserves, including 13m @

69.9g/t gold from 19m (Incl. 4m @ 207.9g/t gold from 19m) and 14m @ 36.50g/t gold from 56m (Incl. 4m @

125.1g/t gold from 65m) from the Nogbele gold deposit (Refer to ASX announcement of 24/09/2012 for full details).

Excluded from the BFS economics were all inferred resources that sit within the current pit designs. At gold prices

above US$1,300 further in-pit Resources and Ore Reserves are potentially defined as per the table below.

Table 2| Ore Reserves and Additional In-Pit Resources

US$1,300/oz

gold

US$1,600/oz

gold

US$2,000/oz

gold Current Ore Reserves 1.05Moz 1.05Moz 1.05Moz

Additional In-Pit Resources 0.05Moz 0.35Moz 0.95Moz

Notes: Additional In-Pit Resources are excluded from the BFS economics

Depth extensions (refer to pit design and block model images below)

Significant potential for depth extensions to both push the pits deeper as well as underground potential. Only 10% of

the current resources and reserve estimates sit below 150 meters vertical depth. Deeper drill results at Stinger for example include 17m @ 4.26g/t gold from 261m, 22m @ 3.19g/t gold from 119m,

5m @ 15.71g/t gold from 103m and 10m @ 8.67g/t gold from 141m indicate that high grade mineralisation continues

at depth. (Refer to ASX announcement of 02/07/2012 and 13/11/2012 for full details).

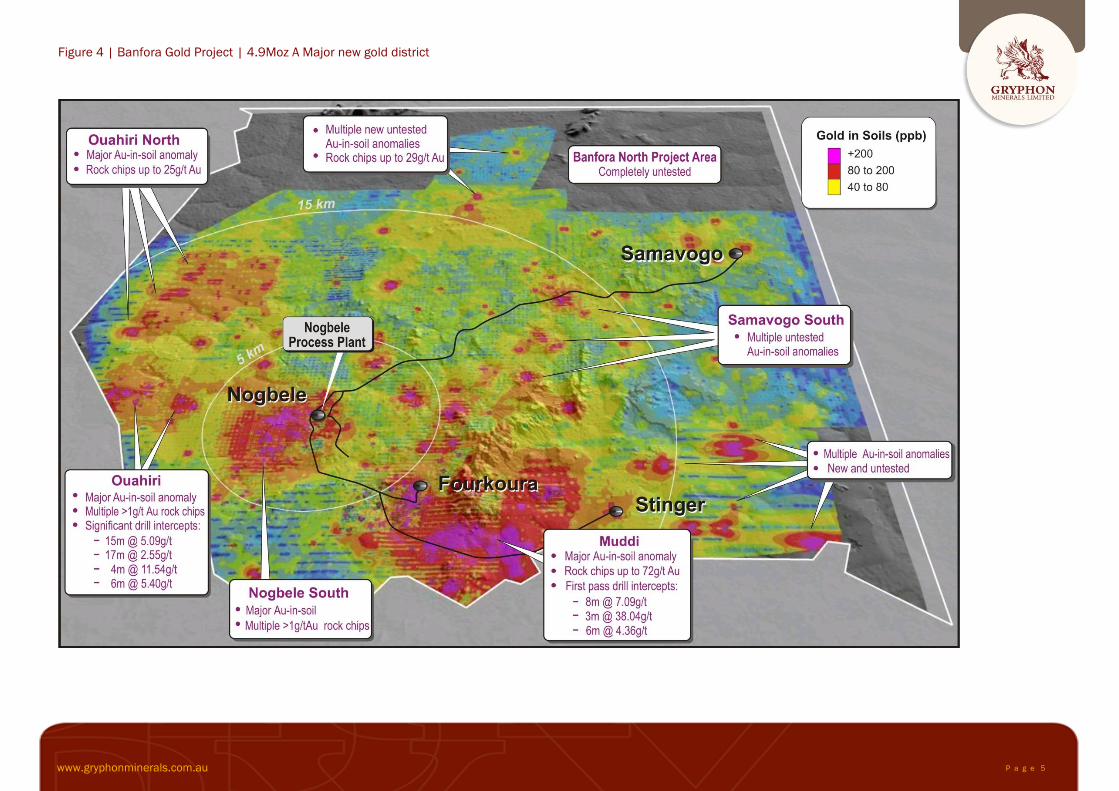

Regional discovery

Huge landholding of 1,200 square kilometres at Banfora Gold Project that remains largely untested. Several regional

targets such as Ouahiri and Stinger require further drilling with anticipated resource growth, as well as several high

priority soil geochemical anomalies that require first pass drilling in 2013.

Expandability of plant

2Mtpa to +4Mtpa operation at Banfora with anticipated Ore Reserve growth. Comminution modelling and process plant

layout design for the 2Mtpa circuit support a readily up-scalable operation to +4Mtpa through the addition of a Ball Mill

and extension of the leaching circuit and associated support services.

Importantly, this option enables production to continue on target, substantially lowers and de-risks funding

requirements and enables future upgrades to be funded by cash flows from the existing operation.

Silver

There is potential for silver credits from the operation. Drill results of up to 10g/t Ag have been reported at the Nogbele

deposit. Any silver recovered in the process plant will form part of the gold doré and will result in credits applied at the

time of refinement.

Heap leach studies

Initial metallurgical results showed excellent recoveries averaging +90% gold after only 45 days leaching

time. Gryphon is now undertaking detailed metallurgical heap leach testing which could potentially target low cost

cash flows early in the project life. Results from detailed metallurgical test work are expected in Q2 2013 with a

feasibility decision to follow.

West Africa Regional targeting

Ongoing exploration at high priority targets in Mauritania and Cote d’Ivoire have the potential to bring through a

pipeline of new organic discoveries for Gryphon.

P a g e 4 www.gryphonminerals.com.au

Figures 1 to 3 | US$1,300 pit outline with block models and selected drill intercepts

P a g e 5 www.gryphonminerals.com.au

Figure 4 | Banfora Gold Project | 4.9Moz A Major new gold district

P a g e 6 www.gryphonminerals.com.au

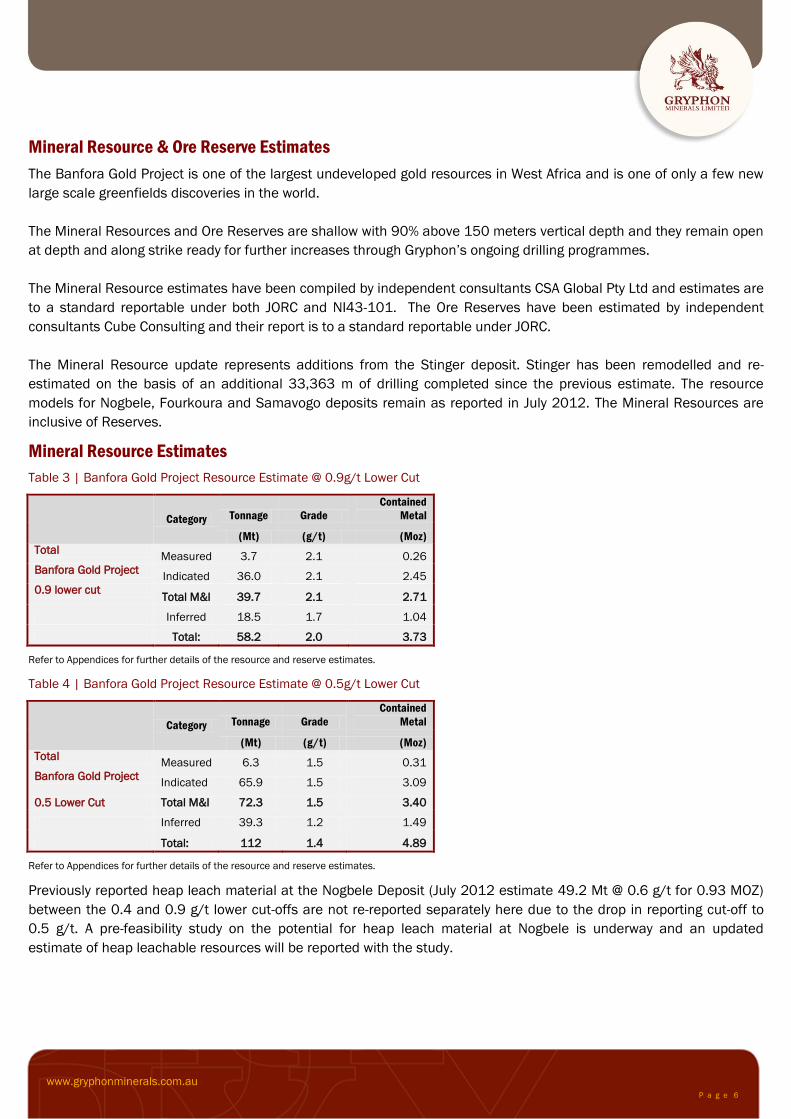

Mineral Resource & Ore Reserve Estimates

The Banfora Gold Project is one of the largest undeveloped gold resources in West Africa and is one of only a few new

large scale greenfields discoveries in the world.

The Mineral Resources and Ore Reserves are shallow with 90% above 150 meters vertical depth and they remain open

at depth and along strike ready for further increases through Gryphon’s ongoing drilling programmes.

The Mineral Resource estimates have been compiled by independent consultants CSA Global Pty Ltd and estimates are

to a standard reportable under both JORC and NI43-101. The Ore Reserves have been estimated by independent

consultants Cube Consulting and their report is to a standard reportable under JORC.

The Mineral Resource update represents additions from the Stinger deposit. Stinger has been remodelled and re-

estimated on the basis of an additional 33,363 m of drilling completed since the previous estimate. The resource

models for Nogbele, Fourkoura and Samavogo deposits remain as reported in July 2012. The Mineral Resources are

inclusive of Reserves.

Mineral Resource Estimates

Table 3 | Banfora Gold Project Resource Estimate @ 0.9g/t Lower Cut

Category Tonnage Grade

Contained

Metal

(Mt) (g/t) (Moz)

Total Measured 3.7 2.1 0.26

Banfora Gold Project Indicated 36.0 2.1 2.45

0.9 lower cut Total M&I 39.7 2.1 2.71

Inferred 18.5 1.7 1.04

Total: 58.2 2.0 3.73

Refer to Appendices for further details of the resource and reserve estimates.

Table 4 | Banfora Gold Project Resource Estimate @ 0.5g/t Lower Cut

Category Tonnage Grade

Contained

Metal

(Mt) (g/t) (Moz)

Total Measured 6.3 1.5 0.31

Banfora Gold Project Indicated 65.9 1.5 3.09

0.5 Lower Cut Total M&I 72.3 1.5 3.40

Inferred 39.3 1.2 1.49

Total: 112 1.4 4.89

Refer to Appendices for further details of the resource and reserve estimates.

Previously reported heap leach material at the Nogbele Deposit (July 2012 estimate 49.2 Mt @ 0.6 g/t for 0.93 MOZ)

between the 0.4 and 0.9 g/t lower cut-offs are not re-reported separately here due to the drop in reporting cut-off to

0.5 g/t. A pre-feasibility study on the potential for heap leach material at Nogbele is underway and an updated

estimate of heap leachable resources will be reported with the study.

P a g e 7 www.gryphonminerals.com.au

Ore Reserve Estimates

Table 5 | Banfora Gold Project Ore Reserves Estimate

Deposit

Category Tonnage Grade

Contained

Metal

(Mt) (g/t) (Moz)

Total Proved 2.7 1.77 0.16

Banfora Gold Project Probable 14.0 1.98 0.89

Total: 16.7 1.95 1.05

NB: Nogbele oxide and transition reported at a 0.5g/t cut-off grade (“COG”), remainder at 0.6 g/t COG

Refer to Appendices for further details of the resource and reserve estimates.

Banfora Mining Operation

Plant Design & Processing

The 2Mtpa processing plant includes a single stage milling circuit (SAG Mill) and conventional CIL gold recovery

processes. The mill is designed for a 30/70 oxide/sulphide blend for the LOM and using a coarse grind of 106µm will

result in average gold recoveries of 92.0%.

Gold grades will average 1.95g/t for the current 8 year LOM, with higher grades of 2.38g/t during the first 5 years

which have a positive impact by reducing cash costs to US$734/oz (A$706/oz) which are at the lower end of industry

standards.

The first deposit has been paid on the long lead item SAG mill and is currently in the detailed design phase with

delivery time expected to be 60 weeks.

The plant has been designed to be up-scaled to +4Mtpa at a later date, potentially funded from project cash flows.

Comminution modelling and process plant layout design support a readily up-scalable operation through the addition of

a Ball Mill and extension of the leaching circuit and associated support services.

Mining

The project will be mined by a mining contractor using open pit methods including drilling and blasting, excavation and

haulage. Ore will be trucked from the three satellite deposits of Samavogo, Fourkoura and Stinger to the processing

plant at the Nogbele deposit. Gryphon is preparing the tender for the mining contract which it expects to award in Q3

2013.

Infrastructure

Gryphon has already commenced negotiations with key initial site works contractors including road upgrades,

construction accommodation and other temporary facilities.

Power for the Project is intended to be sourced from the grid in Cote d’Ivoire. Discussions with Burkina Faso and Cote

d’Ivoire authorities are well advanced and a Memorandum of Understanding between all parties is anticipated to be

signed this quarter. Site evaluations for the power supply route are well advanced.

Raw water for the Project will be pumped to the plant site from a water harvest dam. There is anticipated excess water

capacity for the 2Mtpa process plant from average annual rainfall.

P a g e 8 www.gryphonminerals.com.au

Permitting

The permitting process for the Banfora Gold Project has commenced and is anticipated to be completed by Q3 2013.

In Burkina Faso permitting is generally a short six month process from formal submission, subject to no variations in

the application being requested by regulatory authorities. This timing is in line with other recent successful mine

applications in Burkina Faso. There is also precedent for permission to commence minor early works prior to the

formal granting of a Mining Permit, which the company is exploring.

Environmental and Social Studies

The content and scope of impact assessments are defined under Burkina Faso environmental legislation. The

environmental and social assessment report will be submitted in accordance with these requirements to the Burkina

Faso Ministry of Mines and other relevant departments along with all technical reports required for the permitting

process.

Financing

Gryphon has received strong expressions of interest from a number of financial institutions to provide funding to

develop the Banfora Gold Project. A formal financing process is commencing in the coming weeks with selection of the

financing syndicate expected by the end of Q2 2013 with loan facility agreements to be completed by the end of Q3

2013.

Benefits to Burkina Faso

Along with the development and production at Banfora it is expected that significant benefits will be enjoyed by the

local economy through investment, job creation (both directly and indirectly) and training and development.

On the commencement of steady-state operations the Project is expected to employ some 250 workers along with the

shorter term jobs created during construction. Gryphon will endeavour to use local contractors wherever possible. It is

anticipated that a majority of expatriate staff will be replaced by local workers after the first few years of steady-state

production.

Royalty payments based on gold, assuming a gold price of US$1,500 or greater, attract a 5% government royalty which

will earn the Burkinabe government approximately US$77m in royalties and approximately a further $52m in dividends

through its 10% free carried interest in the ownership of the production company. These benefits do not include

corporate taxes, withholding taxes and income taxes.

In addition to environmental and social studies undertaken as part of the BFS, Gryphon is actively involved in

supporting the local community through various initiatives. Gryphon has employed a full-time Burkinabe community

manager to liaise with the local community in its efforts to engage effectively with all project stakeholders. Some of

Gryphon’s recent initiatives include:

The supply of over 160 wheelchairs for children predominantly in the local communities in which we operate.

The sponsorship and development of a Banfora based weekly radio program.

The supply of hospital equipment to local clinics.

In addition, in the last 12 months, Gryphon has made donations of furniture, equipment and books to a primary

school in Niankarodougou; supported tree planting for World Environmental Day; purchased an ambulance; and

committed to arranging advanced driver training to ambulance drivers in the local district; and repaired local

roads and bridge infrastructure.

P a g e 9 www.gryphonminerals.com.au

Presentation

Please refer to the Company’s website to view an updated Corporate Presentation: www.gryphonminerals.com.au.

Detailed information on all aspects of Gryphon Minerals projects can be found on the Company’s comprehensive

website www.gryphonminerals.com.au.

Yours faithfully

Steve Parsons

Managing Director

Competent Persons Statement

The information in this report that relates to Exploration Results is based on information compiled by Mr Sam Brooks who is a member of the Australian Institute of

Geoscientists. Mr Brooks is a full time employee of Gryphon Minerals. Mr Brooks has sufficient experience which is relevant to the style of mineralisation and type of

deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the “Australasian Code

for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Mr Brooks consents to the inclusion in the report of the matters based on his

information in the form and context in which it appears.

The information in this report that relates to Mineral Resources is based on information compiled by Mr Dmitry Pertel, who is a member of the Australian Institute of

Geoscientists. Mr Pertel is an employee of CSA Global Pty. Ltd. Mr Pertel has sufficient experience relevant to the style of mineralisation and type of deposit under

consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the “Australasian Code for Reporting of

Exploration Results, Mineral Resources and Ore Reserves”. Mr Pertel consents to the inclusion in the report of the matters based on his information in the form and

context in which it appears.

The information in this report that relates to Ore Reserves has been compiled by Mr Quinton de Klerk, who is a Member of The Australasian Institute of Mining and

Metallurgy. Mr de Klerk is an employee of Cube Consulting Pty Ltd. Mr de Klerk has sufficient experience which is relevant to the style of mineralisation and type of

deposits under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code

for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr de Klerk consents to the inclusion in the report of the matters based on his

information in the form and context in which it appears.

Investors Media/Other

Steve Parsons John Gardner

Managing Director, Gryphon Minerals MAGNUS Investor Relations

+61 8 9287 4333 +61 413 355 997

P a g e 10 www.gryphonminerals.com.au

Appendix One | Banfora Gold Project

Bankable Feasibility Study Summary

Location

The Banfora Gold Project (Gryphon 100%) covers 1,200 kilometres square and is located in south west Burkina Faso, West

Africa, approximately 510 kilometres by road south-west of Ouagadougou and 778 kilometres from the port city of Abidjan (Cote

d’Ivoire). A 100 kilometre sealed road connects Banfora town to the city of Bobo-Dioulasso with Burkina Faso’s capital city

Ouagadougou, a further 350 kilometres away.

Figure A | Banfora Gold Project Location

Study Development Lycopodium Minerals Pty Ltd were engaged to coordinate the preparation of a Bankable Feasibility Study (BFS), in collaboration

with various specialist consultants with experience in project development in the region. Independent contributors to the BFS,

and their areas of contribution, are listed below.

Table 1 | Study Contributors

Contribution by Area

CSA Global Mineral resources

Peter O’Bryan & Associates Mine geotechnical

Cube Consulting Mine engineering

ALS-AMMTEC Metallurgical testwork

Lycopodium Minerals BFS management, Metallurgy, Process plant & Infrastructure, Project

implementation, Capital & Operating costs, Risk assessment and management

Knight Piésold Site geotechnical Tailings storage facility, Water harvest dam, Roads

MBS Environmental, KBC Environmental Environmental baseline studies and impact assessment

Plexus, Socrege Burkina Faso, KBC Environmental Health & social impact assessment

Intersocial Consulting Resettlement studies and action plan

Orway Mineral Consultants Comminution circuit

BEC Engineering Power supply

Corality Financial analysis

Project

Location

P a g e 11 www.gryphonminerals.com.au

Mineral Resource & Ore Reserve Estimates

The Mineral Resource and Ore Reserve estimates were independently estimated and classified by CSA Global to a standard

suitable for reporting in accordance with the 2004 Australasian Code for Reporting of Mineral Resources and Ore Reserves

(2004 JORC Code). Statistical and geostatistical analysis was undertaken on the mineralised material prior to grade estimation

of the resources (2004 JORC code & NI43-101) using Ordinary Kriging.

This has resulted in estimated Mineral Resources above a 0.5 g/t Au cut-off for the Project of 72.3 million tonnes at 1.5 g/t Au

for 3.4 million ounces of gold of global Measured and Indicated Resources, and 39.3 million tonnes at 1.2 g/t Au for 1.5 million

ounces of gold of global Inferred Resources (refer Appendix Two following).

Table 2 |Banfora Gold Project Mineral Resource Estimates @ 0.5 and 0.9 g/t Gold Lower Cut

Table 2 includes 49.2Mt @ 0.6g/t gold for 0.93Moz gold below the 0.9g/t lower cut from the Nogbele deposit that is currently

the basis for the Heap Leach test work.

Table 3 | Ore Reserve Estimates Banfora Gold Project

Note: Nogbele oxide and transition reported at a 0.5g/t cut-off grade, remainder at 0.6 g/t.

Tonnage Grade

Contained

Metal Tonnage Grade

Contained

Metal Tonnage Grade

Contained

Metal Tonnage Grade

Contained

Metal

(Mt) (g/t) (Moz) (Mt) (g/t) (Moz) (Mt) (g/t) (Moz) (Mt) (g/t) (Moz)

Nogbele 6.3 1.53 0.31 31.6 1.4 1.42 38.0 1.4 1.73 21.9 1.1 0.77

Fourkoura 7.6 1.3 0.32 7.6 1.3 0.32 3.6 1.2 0.14

Samavogo 12.5 1.8 0.71 12.5 1.8 0.71 8.5 1.3 0.36

Stinger 14.2 1.4 0.64 14.2 1.4 0.64 5.3 1.3 0.22

Total 6.3 1.53 0.31 65.9 1.5 3.09 72.3 1.5 3.40 39.3 1.2 1.49

Deposit

0.5g/t gold lower cut

Measured Indicated Measured + Indicated Inferred

Tonnage GradeContained

MetalTonnage Grade

Contained

MetalTonnage Grade

Contained

MetalTonnage Grade

Contained

Metal

(Mt) (g/t) (Moz) (Mt) (g/t) (Moz) (Mt) (g/t) (Moz) (Mt) (g/t) (Moz)

Nogbele 3.7 2.1 0.26 14.7 2.2 1.06 18.4 2.2 1.32 8.6 1.8 0.48

Fourkoura 4.2 1.8 0.25 4.2 1.8 0.25 1.7 1.7 0.10

Samavogo 8.7 2.2 0.63 8.7 2.2 0.63 5.3 1.7 0.29

Stinger 8.4 1.9 0.51 8.4 1.9 0.51 2.9 1.8 0.17

Total 3.7 2.1 0.26 36.0 2.1 2.45 39.7 2.1 2.71 18.5 1.7 1.04

Deposit

0.9g/t gold lower cut

Measured Indicated Measured + Indicated Inferred

P a g e 12 www.gryphonminerals.com.au

The maiden Ore Reserves for the Banfora Gold Project have been derived by Cube Consulting under the direction of Quinton de

Klerk to a standard reportable in accordance with the “Australasian Code for Reporting of Exploration Results, Mineral

Resources (JORC Code 2004 & NI43-101) and Ore Reserves” (JORC Code 2004) and are based on the Mineral Resource

Models estimated by CSA Global in this announcement.

The Ore Reserve estimate is based on the Mineral Resources classified as “Measured” and “Indicated” after consideration of all

mining, metallurgical, social, environmental and financial aspects of the operation. The Proved Ore Reserve has been derived

from the Measured Mineral Resource, and the Probable Ore Reserve has been derived from the Indicated Mineral Resource.

The cut-off grades used in the estimation of the Banfora Ore Reserves are the non-mining, break-even gold grade taking into

account mining recovery and dilution, metallurgical recovery, site operating costs, royalties and revenues. For reporting of Ore

Reserves the calculated cut-off grades were rounded to the first decimal gram per tonne of gold. The cut-off grades vary

depending on the material type and the pit location. Both are shown in the Ore Reserves table below.

The grades and metal stated in the Ore Reserves Estimate include mining recovery and dilution estimates. The Ore Reserve

Estimate is reported within the open pit designs prepared as part of the BFS.

Contained within the pit designs on which the Ore Reserves are based, is a total of 102.7 Mt of waste material, resulting in an

waste:ore strip ratio of 6.1:1. Included in this waste tonnage is 0.4 Mt of material classified as an Inferred resource, above the

reserve cut off grade. The average grade of this Inferred material is 1.7 g/t. No economic value has been assigned to this

Inferred material in the estimation of these Ore Reserves.

Outside the currently defined and evaluated deposits, the Project area remains highly prospective for further discoveries.

Mining

The components of the mining study include geotechnical studies, hydrology and hydrological assessments, and mine

engineering evaluation.

A definitive mine geotechnical assessment of open pit mining was carried out to provide base case wall design parameters for

open pit mining evaluation.

The majority of the defined mineral resources at the Project are within 150 metres depth from the surface. Conventional open

pit mining techniques using drill and blast with material movement by hydraulic excavator and trucks will be employed, with

some mechanical excavation of oxidised materials possible. The project scale suits 120 tonne class excavators in a backhoe

configuration matched to 90 tonne class mine haul trucks, and 5 metre bench heights.

It is noted that the Fourkoura, Stinger and Samavogo pits are 6, 15 and 25 kilometres from the process plant (respectively).

Conventional on-road trucks will be used to move ore mined from these pits to the ROM stockpile.

The BFS proposes that mining activities be undertaken by an experienced contractor. There are a number of companies

operating in the region and engaging a mining contractor will benefit the project via: reduced capital costs, reduced operational

risk and reduced recruitment burden. Gryphon’s operations team retain responsibility for technical services comprising: mine

planning, production scheduling, grade control, surveying and management of the mining contractor.

The results of the open pit optimisations conducted on all deposits were put in context of sensitivities, risks, contained ounces,

mine life and total project size. The shell selection process represents a strategic decision point for the Company, and as such

the decision was made to use the highest revenue factor shells.

Final pit designs were prepared for each deposit to enable practical and efficient access to each bench. The designs were

based on the optimised shells and prepared using design criteria recommended in the study conducted by Peter O’Bryan and

Associates, with ramp width configurations suited to the mine fleet.

The mine schedule was developed with the primary aim of supplying the best value material first to maximise the value to the

Project. In doing so, the schedule was developed to satisfy all physical and practical constraints.

P a g e 13 www.gryphonminerals.com.au

Figure B | Resource Block Model Typical Cross-Sections, US$1,300 Pit Shells

P a g e 14 www.gryphonminerals.com.au

Metallurgy

The detailed metallurgical testwork programme conducted for the BFS confirmed a conventional CIL process route for gold

extraction, with a coarse grind size of 80% passing 106 µm. The Banfora ores are all ‘non-refractory’, typically 'free-milling' with

a high gold recovery by cyanidation leach and low to moderate reagent consumptions.

The Nogbele, Fourkoura, Samavogo and Stinger ores were all included in the BFS testwork program and proved to have similar

comminution and metallurgical characteristics. Ore mineralisation is classified into three main types based on rock alteration

and degree of weathering; namely oxide, transition and primary, with approximately 40% of the deposit in the oxide category.

Oxide ores are typically low to moderately abrasive, low competency ores with low comminution energy requirements. Primary

ores are typically abrasive, medium to high competency ores with average to above average comminution energy requirements.

The anticipated gold and silver recoveries are summarised in the table below. Life of Mine (“LOM”) average gold recovery is

predicted to be 92%.

Table 4 | Metal Recoveries - Testwork Summary

Ore Type LOM

Quantity

[Mt]

LOM

Proportion

[%]

Testwork Recoveries

% Gold % Silver

Oxide 7.2 43% 92.5 51.3

Transition 3.0 18% 96.8 47.2

Primary 6.6 39% 89.3 62.8

TOTAL 16.7 100% 92.0 55.1

Process Plant

The process plant design is based on a conventional CIL gold process flowsheet consisting of primary crushing, single stage

SAG milling, pebble crushing, carbon-in-leach, elution, electro-winning and gold smelting. A simplified flowsheet is provided

overleaf, followed by the plant layout.

The process plant design for the Project is based on a robust metallurgical flowsheet designed for optimum recovery with

minimum operating costs. The key criteria for equipment selection are suitability for duty, reliability and ease of maintenance.

The process selected is based on industrially proven unit processes and presents low technical risk.

The major components of the plant design are:

Primary jaw crusher to produce a crushed product size of 80% passing (P80) 140 mm.

Crushed ore surge bin with discharge ore conveyed directly to the mill, and overflow reporting to a dead stockpile.

SAG mill with single 7MW drive in closed circuit with a pebble recycle crusher and hydro-cyclones to produce a P80 grind

size of 106 µm.

Pre-leach thickener to increase slurry density feeding the CIL circuit to minimise CIL tankage, improve slurry mixing

characteristics and reduce overall reagent consumption.

CIL circuit incorporating six stages with carbon in all stages for gold adsorption.

Anglo-American elution circuit, electrowinning and gold smelting to recover gold from the loaded carbon to produce doré.

Tailings thickening to recover and recycle process water from the CIL tailings, with tailings pumping to the TSF.

`

www.gryphonmineerals.com.au P a g e 1 5

Figure C | Banfora Simplified Process Flowsheet

`

www.gryphonmineerals.com.au P a g e 1 6

Figure D | Banfora Process Plant Layout

Services

Goldroom

Reagents

CIL

Grinding

Rom Pad

Crushing

Tails

Stockpile

Desorption

Cyclones

Recycle Crushing

www.gryphonminerals.com.au

Page 15

P a g e 1 7

Infrastructure and Services

An acceptable power supply of sufficient quality is a key component to the success of the Project. The maximum power demand

for the project is 11.2 megawatts. The power source is planned to be supplied from the HV electricity grid in Côte d’Ivoire, in

cooperation with the Burkina Faso power authority, SONABEL. The grid supply from Côte d’Ivoire is by world standards more

economically priced and more financially viable than self-generation options.

A 90 kV line will run approximately 94 kilometres from the substation in Côte d’Ivoire to the project site, following an existing HV

transmission line from Ferkessedougou to Sikasso in Mali.

Importantly, Burkina Faso and Côte d’Ivoire have an existing relationship given Burkina Faso currently imports between 50 and

70 MW of power from Côte d’Ivoire.

Other Project infrastructure has been designed to support the mining operation and includes the following:

Tailings storage facility - consisting of a cross-valley embankment, forming a footprint area of 116 ha for the Stage 1 TSF

increasing to 263 ha for the final TSF.

Water harvesting dam with a storage volume of 0.5 million cubic metres.

Site access roads and haul roads.

Accommodation facilities

Mine services facilities, including fuel storage and workshops.

Administrative buildings and support facilities.

Process plant support facilities and services.

Environmental and Social Responsibility

Based on the Project description and a review of the existing environment, potential environmental and social impacts

associated with the construction and implementation of the Project have been identified, with mitigations researched. These

are considered as common to project development in the region.

In accordance with the Environmental Code of Burkina Faso and as part of this BFS, Gryphon has undertaken an

Environmental, Social and Health Impact Assessment which will form part of Gryphon’s application for a Mining Licence in first

quarter 2013. The Project will likely be subject to assessment by the International Finance Corporation (IFC), for compliance

with IFC performance standards, Environmental Health and Safety Guidelines and the Equator Principles.

Intersocial Consulting has been engaged to conduct all resettlement action planning, having been involved in numerous similar

schemes both in Burkina Faso and for other mining projects in West Africa. The Project requires the relocation of approximately

900 households as part of the first 3 years of development, and these costs are included in the capital cost estimate.

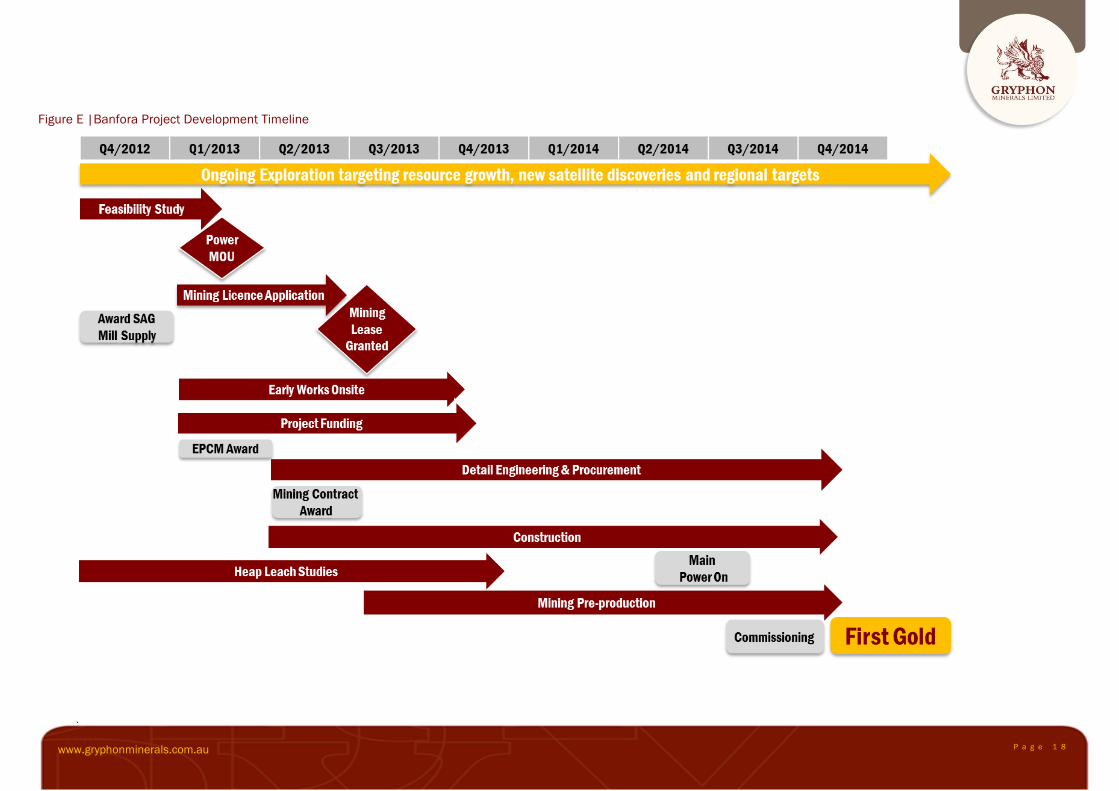

Project Implementation

A project specific implementation plan has been developed to outline the methodology for delivery & commissioning of a mining

operation and treatment plant, including all associated infrastructure and support services.

In developing the project implementation plan the shortest practical implementation period that did not compromise safety or

quality was determined. Consideration was given at all levels, to the utilisation of contractors and personnel located in Burkina

Faso, and/or having appropriate Burkina Faso work experience.

Subject to the timing of the receipt of key permits and the financing of the Project, the Project development duration of 21-22

months will support Gryphon’s goal of first gold before the end of 2014. The project development timeline is provided below.

`

P a g e 1 8 www.gryphonminerals.com.au

Figure E |Banfora Project Development Timeline

www.gryphonminerals.com.au P a g e 1 9

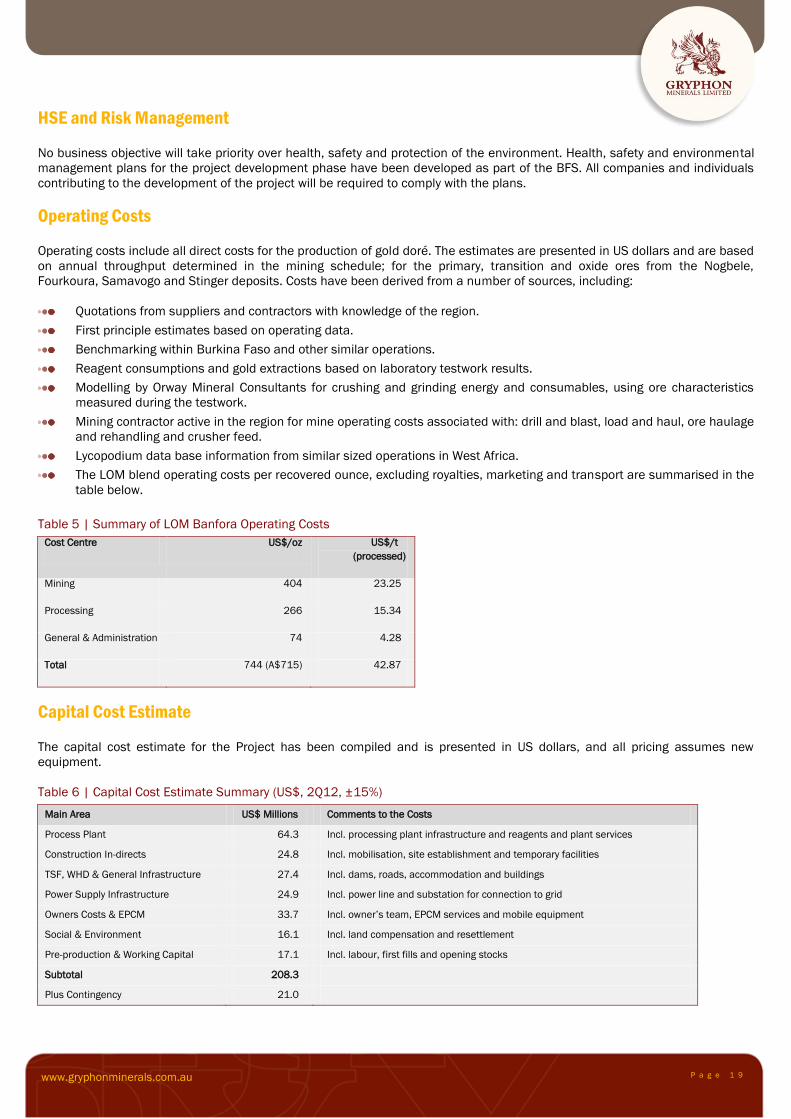

HSE and Risk Management

No business objective will take priority over health, safety and protection of the environment. Health, safety and environmental

management plans for the project development phase have been developed as part of the BFS. All companies and individuals

contributing to the development of the project will be required to comply with the plans.

Operating Costs

Operating costs include all direct costs for the production of gold doré. The estimates are presented in US dollars and are based

on annual throughput determined in the mining schedule; for the primary, transition and oxide ores from the Nogbele,

Fourkoura, Samavogo and Stinger deposits. Costs have been derived from a number of sources, including:

Quotations from suppliers and contractors with knowledge of the region.

First principle estimates based on operating data.

Benchmarking within Burkina Faso and other similar operations.

Reagent consumptions and gold extractions based on laboratory testwork results.

Modelling by Orway Mineral Consultants for crushing and grinding energy and consumables, using ore characteristics

measured during the testwork.

Mining contractor active in the region for mine operating costs associated with: drill and blast, load and haul, ore haulage

and rehandling and crusher feed.

Lycopodium data base information from similar sized operations in West Africa.

The LOM blend operating costs per recovered ounce, excluding royalties, marketing and transport are summarised in the

table below.

Table 5 | Summary of LOM Banfora Operating Costs

Cost Centre US$/oz US$/t

(processed)

Mining 404 23.25

Processing 266 15.34

General & Administration 74 4.28

Total 744 (A$715) 42.87

Capital Cost Estimate

The capital cost estimate for the Project has been compiled and is presented in US dollars, and all pricing assumes new

equipment.

Table 6 | Capital Cost Estimate Summary (US$, 2Q12, ±15%)

Main Area US$ Millions Comments to the Costs

Process Plant 64.3 Incl. processing plant infrastructure and reagents and plant services

Construction In-directs 24.8 Incl. mobilisation, site establishment and temporary facilities

TSF, WHD & General Infrastructure 27.4 Incl. dams, roads, accommodation and buildings

Power Supply Infrastructure 24.9 Incl. power line and substation for connection to grid

Owners Costs & EPCM 33.7 Incl. owner’s team, EPCM services and mobile equipment

Social & Environment 16.1 Incl. land compensation and resettlement

Pre-production & Working Capital 17.1 Incl. labour, first fills and opening stocks

Subtotal 208.3

Plus Contingency 21.0

P a g e 2 0 www.gryphonminerals.com.au

Appendix Two | Banfora Gold Project

Resource Estimation Parameters

The seventh gold resource estimate completed at Banfora Gold Project has been undertaken by CSA Global based in Perth,

Western Australia. Initial geological interpretation was provided by Gryphon Minerals geological staff which formed the basis of

the CSA model interpretation. Estimation has been conducted in compliance with the N43-101 and JORC code of reporting and

includes the following parameters and considerations.

For comparison with previous resource estimates refer to ASX announcements dated, 17th September 2007, 8th April 2009,

21st September 2009, 31st March 2011 and 9th of July 2012.

Statement includes an upgraded resource for the Stinger Prospect estimation is based on assays received up to the end of

2012. The Stinger estimate reported contains a 21% increase in total reported metal and a significant conversion to indicated

category from the July 2012 resource.

The currently reported resource at Stinger is based on a 121% increase in drill meters at the prospect since the July 2012

statement.

Statements for Nogbele, Fourkoura and Samavogo remain unchanged from the July 2012 announced resource. New drilling

subsequently released on the ASX is yet to be incorporated into a new resource model for these prospects.

Totals have been rounded to two significant figures from the detailed estimate, the reported headline global figure is based

upon a 0.9 g/t lower cutoff for all resource areas for comparison purposes with previous resources, and a 0.5 g/t to align with

lowest cutoff grades used in the reporting of Reserves. Engineering studies and economic analysis determined a cut-off grade

of 0.5 g/t for oxide material.

The Nogbele Mineral resource occurs as multiple zones within the Nogbele Granodiorite pluton and adjacent mafic volcanics

to the west. Currently defined resources occur within a 2.5km radius around the contact zone. Mineralised zones vary from

sericite pyrite altered quartz vein zones and hematite, sericite, pyrite, iron carbonate, altered zones with little quartz veining.

The Fourkoura Mineral Resource occurs within single and multiple sub‐parallel shears with 2.4 km of strike. Mineralisation is

associated with iron carbonate, pyrite alteration in the felsic intrusive adjacent to the Fourkoura Dolerite.

The Samavogo Mineral resource is associated with a NE trending shear along a granitoid contact with mineralisation currently

defined over 4.3 km of strike. The main lode is defined by high grade plunging shoots, with minor hanging wall zones in the

north of the orebody. Mineralisation is associated with disseminated pyrite in sheared volcanics with occasional significant

quartz veins.

The Stinger resource occurs both on the contact and internal in a diorite- granodiorite dyke swarm and is controlled by a NE

trending shear network and has been drilled for 2.3 km strike. Mineralisation occurs in multiple moderately dipping stacked

lodes and is associated with sericite, carbonate, pyrite mineralization with silica flooding. Mineralisation remains open both

down dip and along strike.

Nogbele Resource is nominally drilled on a 25 x 25m grid with areas of 50 x 25m drilling oriented perpendicular to individual

domains, 3 main orientations were used 180, 145, 225 UTM based on 988 RC holes 88,568m and 84 diamond holes for

14,280 (including pre-collar). Aircore drilling contributed to geological interpretation and wireframes. Aircore assays have

been excluded from resource calculations. A total of 1441 RC holes for 137176m, 30 DD holes for 4610m and 102 DD holes

with an RC precollar for 19707m were included in the estimation

Fourkoura Resource is based on 50 x 25m drilling oriented towards 270 UTM, 170 RC holes for 16,901m and six diamond

holes for 952m (including pre-collar). A total of 179 RC holes for 17863 m, 8 DD holes for 710m and 4 DD holes with an RC

precollar for 769m were included in the estimation.

Samavogo Resource is based on 40 x 40m drilling orientated towards 325 UTM A total of 481 RC holes for 51376 m, 7 DD

holes for 765m and 21 DD holes with an RC precollar for 4658m were included in the estimation.

Stinger Resource is based on 40 x 40m drilling oriented towards 135 UTM, a total of 403 RC holes for 42028m, 63 DD holes

for 15869m and 14 DD holes with an RC precollar for 3146m were included in the estimation

90% of resource ounces are above 150 m vertical

Drilling includes RC face sample bit methods with 55-60 degree inclined holes. Oriented diamond drilling with RC pre‐collars,

has been completed at all prospects.

Sample weights are measured every 1m drilled, showing acceptable sample recoveries and no bias related to sample weight.

Samples have also been collected at the drill as 4m field composites with the 1m samples submitted based on composited

assay results. The 1m sampling was taken and stored at the same time as the composite sampling. Sample bags are sealed

after preparation with laboratory first opening 1m sample bags. All samples split with single tier riffle splitter, were submitted

at nominal sample weights between 3 and 4kgs.

Diamond core was sawn in half with half core submitted for assay mostly at 1m samples.

P a g e 2 1 www.gryphonminerals.com.au

Blind QAQC samples were inserted every 10th drill sample, including in rotation Blanks, Field Duplicates and Certified

Standards.

All resource assays by 50g Fire Assay method with AAS finish at Transworld in Ghana and SGS, Abilabs and Bigs laboratories

in Burkina Faso. All Lab rejects have been retained in storage.

Samavogo was divided into 3 structural domains, Fourkoura and Stinger- 2 structural domains and Nogbele 21 structural

domains for variography and the applications of upper cuts.

Individual domains were assessed for top cut based on natural breaks in the cumulative frequency plots. Top cuts applied by

domain vary from 6.5g/t to 38g/t.

Bulk Dry Density based on core measurements obtained using volume displacement in water. No bulk density work has been

conducted at the Stinger prospect and the densities used are based on measurements obtained by similar lithology at

Nogbele.

- 1.8 t/cu.m for oxidized material

- 2.2 t/cu.m for quartz veins in the oxide profile

- 2.5 t/cu.m for transition material

- 2.7 t/cu.m for fresh granitic rocks

- 2.8 t/cu.m for fresh mafic rocks

- Oxidation boundaries were wire framed and included in modeling.

All drill hole collars originally surveyed by GPS. Most drill hole collars surveyed with DGPS control. Rls have been generated

using stereoscopic imagery collected by World View 2, this imagery has been processed and tied into DGPS pickup.

Most drill holes have down hole surveys and all holes have been resurveyed at collar where down hole surveys were not taken

for dip and azimuth.

Drill hole samples have been composited to 1m intervals for calculations.

Blockmodelling was done using 10 x 10 x 5 m cell size with sub-blocking, estimation was conducted to parent cells only.

Oriented search ellipsoids were defined for each of the Domains modeled.

The Estimate has been reported using Ordinary Kriging within wireframes interpreted from cross sections has been reported.

IDW2 and IDW3 were also conducted for verification into the same models.

Wireframes based on a nominal low grade mineralized outline, 0.2g/t-0.25 g/t drill cutoff grade depending on domain,

combined with geological interpretation honoring oriented diamond core information and surface structural work from

trenching.

Quartz veins were modeled and hard bounded where possible, veins were treated as a separate domain from disseminated

and selvedge related mineralization for the estimation.

Further lithological models were used to code domains for assignment of bulk density.

Geological logging of percussion drilling includes lithology, oxidation, alteration and shearing intensity. Diamond core logging

includes oriented structural logging.

Wireframe interpretations and resource modeling completed using Micromine software.