5 Tips For Planning Your Post-Retirement Career by Goldstone Financial Group

Upload

goldstone-financial-groupCategory

view

32download

0

3 STRATEGIES FOR RETIREMENT PLANNING YOU’LL NEED TO KNOW

By Goldstone Financial Group

DID YOU KNOW THAT YOU WILL PROBABLY LIVE

LONGER THAN YOU THINK?

AVERAGE LIFE EXPECTANCY HAS GROWN BY THREE MONTHS EVERY YEAR FROM 1840 TO 2007 AND SHOWS NO SIGNS OF SLOWING DOWN.

➤Family history is also not necessarily indicative of how long someone may live.

➤Lifestyle choices such as diet and exercise can have a dramatic impact on the length of life.

LONGER LIFESPANS MEAN WE HAVE MORE TIME TO

ENJOY THE THINGS AND PEOPLE WE

LOVE MOST.But they also pose a unique

challenge.

WHAT IS THE BEST METHOD TO SAVE ENOUGH MONEY TO RETIRE AND LIVE

COMFORTABLY AND WORRY-FREE?

“This presentation includes pros and cons of some of the most popular, “tried and true” retirement investment strategies and highlight their effectiveness in today’s life changing times.

Anthony Pellegrino, Founder & Principal, Goldstone Financial Group

#1. FIXED AND HYBRID ANNUITIES

Annuities are a great way to save for retirement because they can potentially generate interest over a fixed time on a principal amount that is guaranteed.

BECAUSE YOU ARE NOT REQUIRED TO ANNUITIZE

—TO RECEIVE PAYMENTS AT A REGULAR

INTERVAL FROM THE ANNUITY—CERTAIN KINDS OF ANNUITIES

ALSO OFFER THE FLEXIBILITY TO LEAVE

MONEY FOR YOUR HEIRS:

STRAIGHT LIFE

➤This is the simplest, least expensive annuity. It pays benefits until the death of the annuitant—the person receiving the funds—without an option to appoint a beneficiary.

LIFE WITH A GUARANTEED TERM

➤This somewhat more expensive option allows the annuitant to designate a beneficiary.

➤ If the annuitant dies within the guaranteed term, the beneficiary will receive the remainder of the annuity in one lump sum.

SUBSTANDARD HEALTH

➤This type of annuity is advantageous for someone with a serious health condition.

➤Although the annuity will cost more the less the annuitant is expected to live, the payouts are larger than in an annuity in which the annuitant is expected to live a long time.

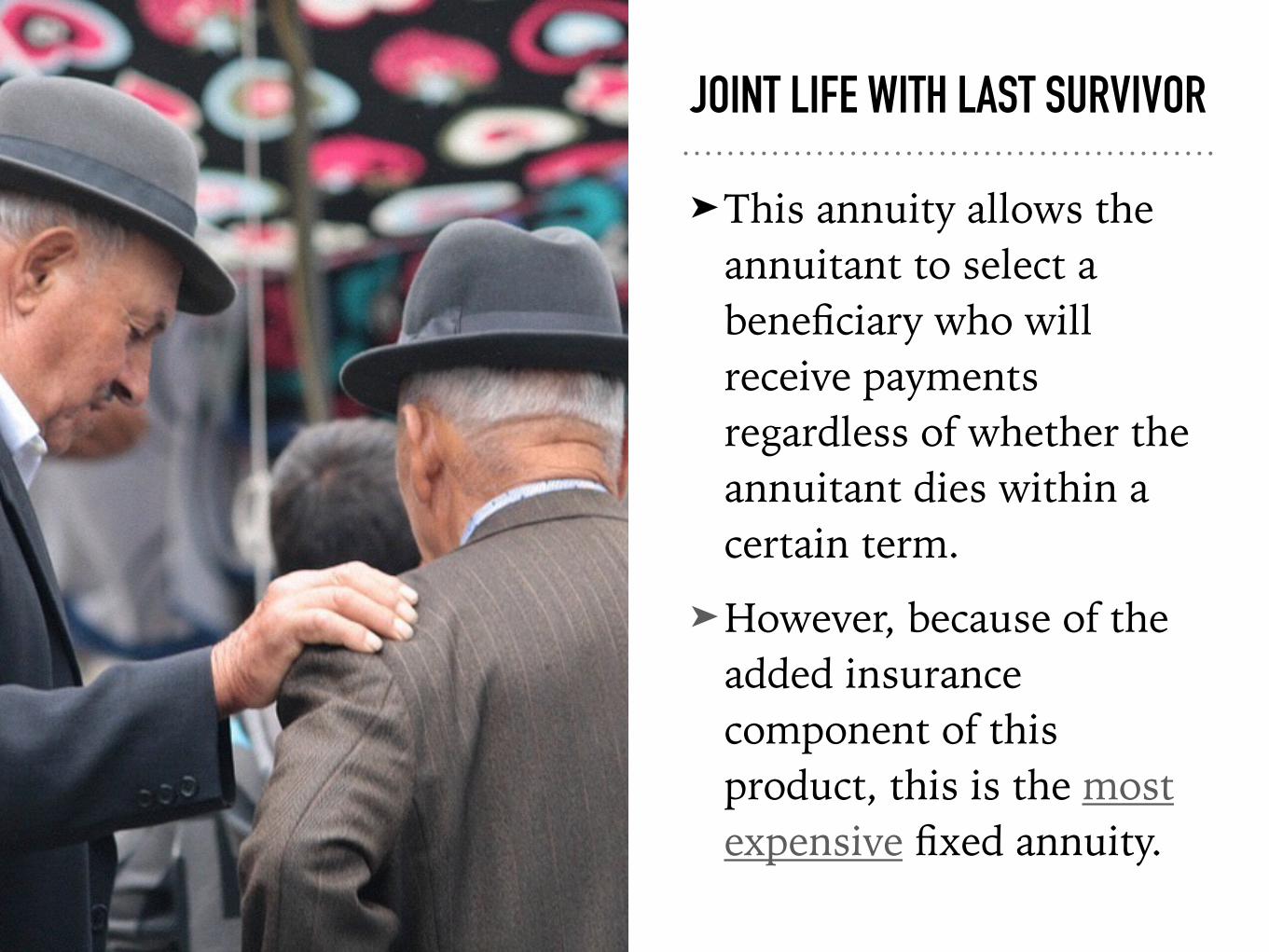

JOINT LIFE WITH LAST SURVIVOR

➤This annuity allows the annuitant to select a beneficiary who will receive payments regardless of whether the annuitant dies within a certain term.

➤However, because of the added insurance component of this product, this is the most expensive fixed annuity.

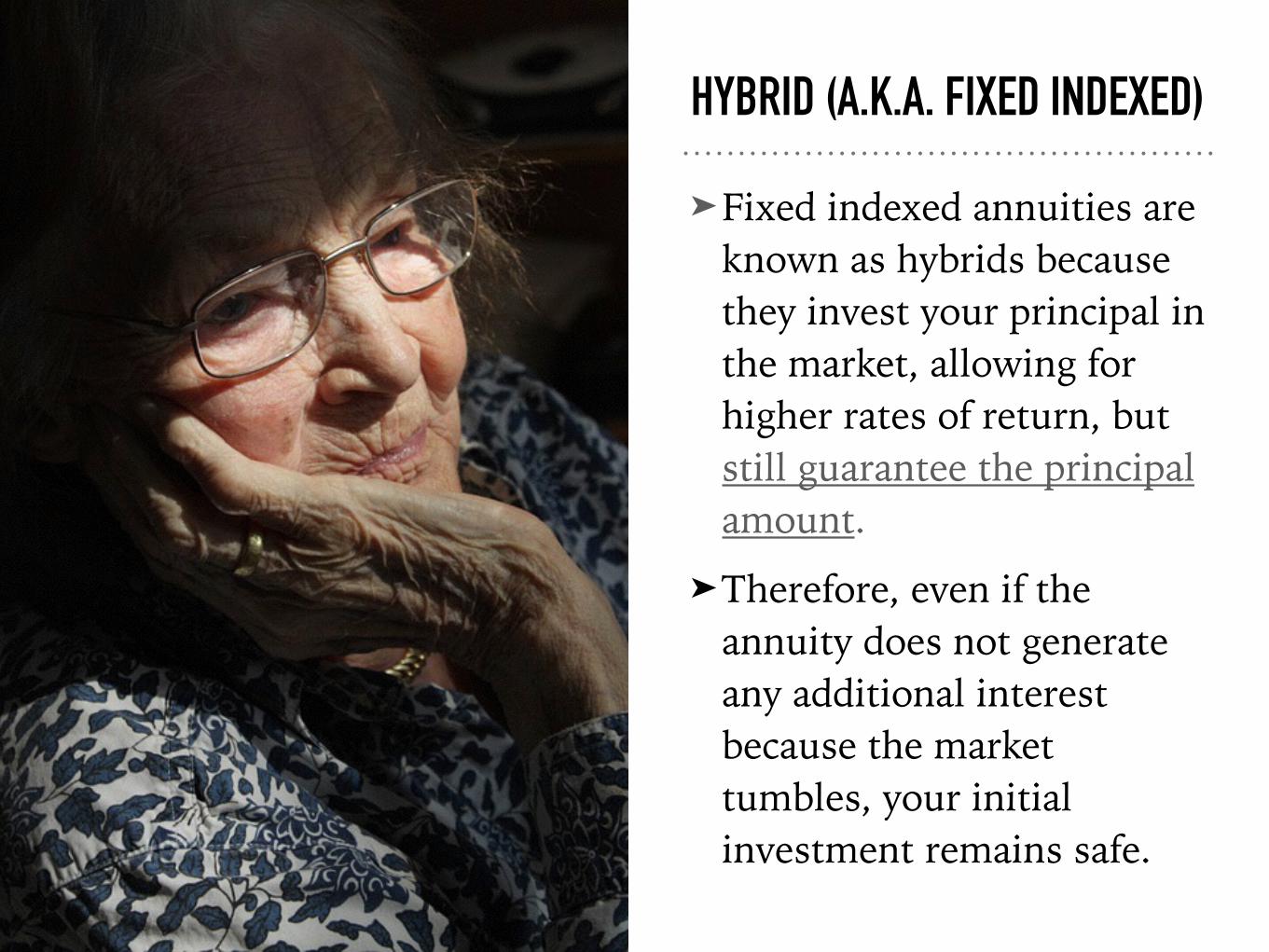

HYBRID (A.K.A. FIXED INDEXED)

➤Fixed indexed annuities are known as hybrids because they invest your principal in the market, allowing for higher rates of return, but still guarantee the principal amount.

➤Therefore, even if the annuity does not generate any additional interest because the market tumbles, your initial investment remains safe.

TRADITIONAL AND/OR ROTH IRAS

Investment retirement accounts are an excellent, tax-efficient tool for setting

funds aside.

PEOPLE WHO CONTRIBUTE TO A

TRADITIONAL IRA ARE ABLE TO DEDUCT THE CONTRIBUTION FROM

THEIR ANNUAL FEDERAL AND STATE

INCOME TAXES.

HOWEVER, ONCE THEY WITHDRAW

FUNDS IN RETIREMENT, THE

WITHDRAWAL WILL BE TAXED AS

INCOME.

CONVERSELY, CONTRIBUTIONS TO ROTH IRAS ARE NOT

TAX DEDUCTIBLE BUT FUTURE

WITHDRAWALS WON’T BE TAXED.

CHOOSING THE RIGHT IRA

DEPENDS ON SEVERAL FACTORS:

INCOME REQUIREMENTS:

➤Roth IRAs have strict and specific income requirements.

FUTURE TAX:

➤Additionally, depending on the difference between the current and potential future tax rate, one type of IRA may be more advantageous than the other.

➤Finally, traditional IRAs require you to take mandatory taxable distributions beginning at age 70½ whereas Roth IRAs do not require you to take any money.

TAXABLE DISTRIBUTIONS:

401(K)

A 401(k) is an employer-sponsored retirement fund that invests your

money in order to generate more. This savings strategy may yield excellent benefits but may also be the riskiest

option.

THE BENEFITS:

➤The amount of your annual contribution to your 401(k) is tax deductible. Additionally, many employers will match your contribution up to a certain amount—usually 3% of your annual income—essentially giving you “free” money.

THE CONS/RISKS:

➤First, the IRS sets caps on the annual amount you can put into your 401(k).

➤After you retire, withdrawals are taxed as income and may be taxed at a higher rate than your present tax rate.

➤You may also not be able to withdraw your employer’s contributions until after the vesting period concludes.

➤Additionally, should you find yourself in need of money before the age of 59½, you will be subject to a 10% withdrawal fee.

FINALLY, 401(K)S GROW

YOUR MONEY BY INVESTING IT IN MUTUAL FUNDS.

➤Whenever money is invested in such fashion, there is a risk that stocks can crash and that your 401(k) will lose significant value.

➤Fortunately, you have full control over how your money is invested, so this risk can be minimized with some education about the market and less risky investment strategies.

IF YOU LIKED THIS PIECE, PLEASE VISIT: GOLDSTONEFINANCIALGROUP.NET

It is our responsibility at Goldstone Financial Group to thoroughly understand your goals and dreams so that we can leverage our experience and expertise to help you realize them. For more information, please visit our website and follow us on Twitter and Facebook!