2Q11 Institutional Presentation

36

2Q11 I tit ti l P t ti Institutional Presentation

-

Upload

pineriweb -

Category

Economy & Finance

-

view

78 -

download

0

Transcript of 2Q11 Institutional Presentation

2Q11I tit ti l P t tiInstitutional Presentation

History and Profile

Summary

History and ProfilePINE at a GlanceHistoryOrganizational Structure

Business StrategyCompetitive LandscapeDiversity of ProductsCorporate CreditHedging DeskHedging DeskPINE InvestimentosDistributionThe Current Scenario and Future Prospects

Highlights and Results

Corporate Governance and SharesCorporate GovernanceMain CommitteesShareholders’ StructureShareholders ProfileDividends

Other Highlights2Q11 Events and HighlightsSocial Responsibility

2/36Investor Relations | 2Q11 |

Appendix

History and Profile

PINE at a GlancePINE specializes in providing financial solutions for mid and large companies

Credit Portfolio by Clients’ Annual Revenues

Focused on establishing long-term relationships withcompanies

As of June 30, 2011

Up to R$150 million

15%

PINE thoroughly understands the needs and strategies ofits clients, offering a broad range of financialinstruments in local and foreign currencies

S l i hi i h li li h d

Over R$1 billion50%

R$150 million to

R$500 million

16%

15%

Strong relationship with clients: clients that are servedby more than one product, in average, are served by 2.8products

Business is structured along four primary business lines:

R$500 million to

R$1 billion19%

16%

g p y• Corporate Credit: credit and financing products• Hedging Desk: Instruments for hedging and risk

management• Distribution: investment solutions for foreign and

local investors

Solid Credit Ratings

local investors• PINE Investimentos: vehicle for Investment

Banking and Asset Management

Strategy based on: Br A Brazil national scale

A1.br Brazil national scale

Ba2 Long term foreign currency deposit

gy• Product diversity• Qualified human capital• Efficient risk management• Agility

BB- Long term foreign currency deposit – Positive Outlook

A(bra) Brazil national scale

BB Long term foreign currency

4/36Investor Relations | 2Q11 |

BB- Long term foreign currency deposit

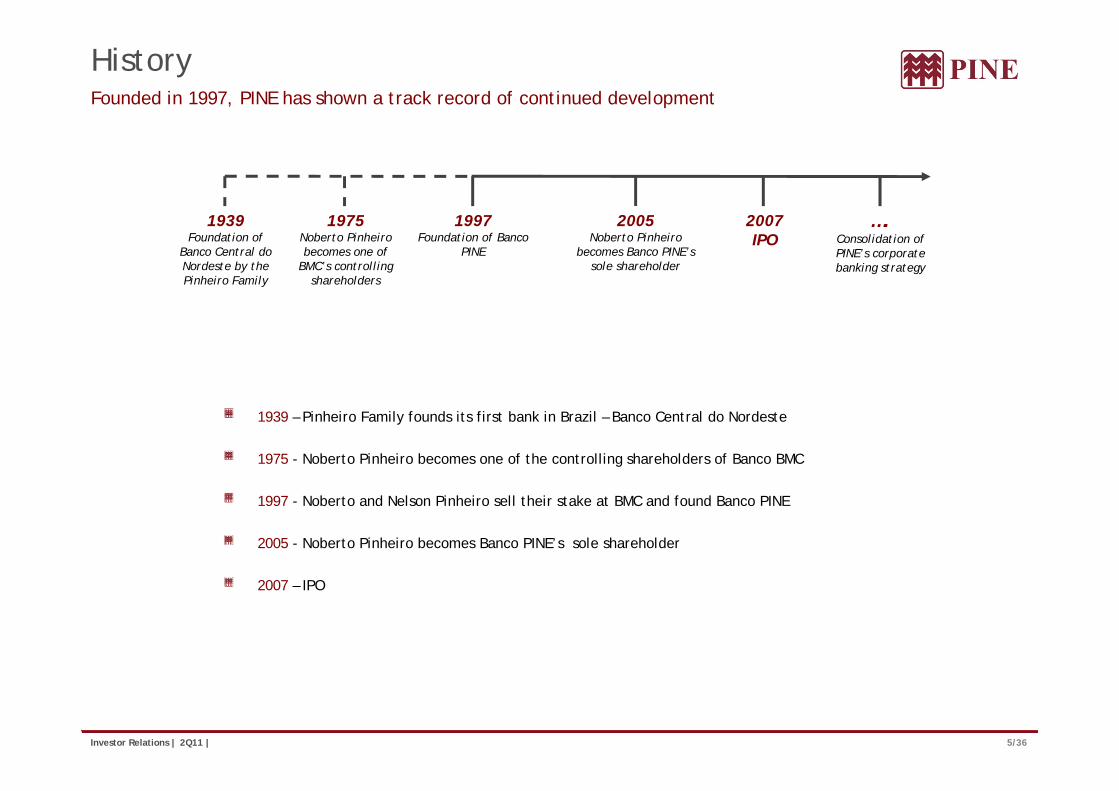

HistoryFounded in 1997, PINE has shown a track record of continued development

1997 20051939 1975 20071997Foundation of Banco

PINE

2005Noberto Pinheiro

becomes Banco PINE’s sole shareholder

1939Foundation of

Banco Central do Nordeste by the Pinheiro Family

1975Noberto Pinheiro becomes one of

BMC’s controlling shareholders

….Consolidation of PINE’s corporate banking strategy

2007IPO

1939 – Pinheiro Family founds its first bank in Brazil – Banco Central do Nordeste

1975 - Noberto Pinheiro becomes one of the controlling shareholders of Banco BMC

1997 - Noberto and Nelson Pinheiro sell their stake at BMC and found Banco PINE

2005 - Noberto Pinheiro becomes Banco PINE’s sole shareholder

2007 – IPO

5/36Investor Relations | 2Q11 |

Organizational StructureNon-bureaucratic structure and flat hierarchy, streamlining the decision making process

Board of Directors

Internal AuditorsTikara Yoneya

Internal AuditorsTikara Yoneya

External AuditorsPwC

External AuditorsPwC

Noberto Pinheiro Chairman

Noberto N. Pinheiro Jr.Vice-Chairman

Maurizio MauroIndependent

Member

Fernando AlbinoExternal Member

Mailson da NóbregaIndependent

Member

Antonio HermannIndependent

Member

Fiscal Council

O ti l Ri kO ti l Ri k

Tikara YoneyaTikara Yoneya PwCPwC

Sidney VenezianiSérgio MachadoAlcindo Itikawa

Sidney VenezianiSérgio MachadoAlcindo Itikawa

Fiscal Council

CEONoberto N. Pinheiro Jr.

CEONoberto N. Pinheiro Jr.

Operational Risk& Compliance

Operational Risk& Compliance

PINE InvestimentosGustavo Junqueira

PINE InvestimentosGustavo Junqueira

Planning and ControlSusana Waldeck

Planning and ControlSusana Waldeck

Sales & TradingNorberto Zaiet Jr.Sales & Trading

Norberto Zaiet Jr.Origination

Clive BotelhoOrigination

Clive BotelhoCredit Risk & Analysis

Gabriela ChisteCredit Risk & Analysis

Gabriela ChisteOperations

Ulisses AlcantarillaOperations

Ulisses Alcantarillaqq

Corporate Credit• 14 origination

platforms• São Paulo• Campinas• Ribeirão Preto

Corporate Credit• Analysis and granting

of credit• Credit risk monitoring

and analysis by sector

Market and liquidity RisksHuman ResourcesAccountingControllingT Pl i

Investment Banking• Capital Markets• Corporate Finance• Distressed and

Special Situations

Investment

Corporate Processing and FormalizationLegal

TradingHedging Desk• Fixed Income• Currencies• Commodities

Local Distribution• São José do Rio Preto• Rio de Janeiro• Curitiba• Porto Alegre• Belo Horizonte• Recife• Fortaleza

Tax PlanningManagementAsset Management

Local DistributionInternational DistributionMacro and Commodities ResearchProductsInvestor Relations

6/36Investor Relations | 2Q11 |

Fortaleza

Business Strategy

Brazilian Competitive LandscapeFinancial sector consolidation reduced options to our target segment

Focus on the upper middle and low corporatesegments

Large Multiple banks

Large Multiple banks

segments

Consolidation in the banking sector causedreduction in the supply of credit lines and

Corporate sector mid-sized banks Opportunity to expand operations

PINE f d l i f

reduction in the supply of credit lines andfinancial instruments to the bank’s segment

Unique approach: offering diversity of products toPINE: focused on complete service for companies, offering tailor-made products.

Unique approach: offering diversity of products toa market segment poorly serviced by the bankingindustry

IB and Foreign Banks

IB and Foreign Banks

Competitive Advantages:Fast responseDedicated team of specialists with deepknowledge of the clients business, balance

Mid-sized banksMid-sized bankssheet and market positioningTailor-made solutions based on a diverseproduct base

8/36Investor Relations | 2Q11 |

Client-oriented StrategyA diversity of financial instruments to better serve our clients needs

CDIs

Interest Rates

CDs

LCIs

CCBs PrivatePlacements

Currency

Commodities

CDBs

RDBs

LCAs

Eurobonds

Placements

Financial Letters

Local Currency Pricing of Assets and Liabilities

OverdraftAccounts

EquitiesDebenturesCRIs

TreasuryDistribution

Foreign Currency

LiquidityManagement

TradingWorking Capital

Underwriting

BNDES Onlending

Bank Guarantees

Compror/Vendor

ACC/ACE

ClientsCorporate

Credit PINE

Investimentos

Capital Markets

Corporate Finance

Special

Local Currency

Onlending

Foreign Currency

Trade Finance(Import and Export)

Private Placements

Financial Advisory

WarrantiesExclusive Funds

Project Finance

ACC/ACE

Export Finance

Finimp

Letters ofCredit

2 770 onlending

Sales DeskSpecial Situations

Investment Management

Interest Rates Currency

(Import and Export)

Structured FinanceCredit Funds

Portfolio Management

Swap NDFStructured Swaps

2,770 onlending

Syndicated andStructured Loans

te est ates Cu e cy

Commodities

9/36Investor Relations | 2Q11 |

Structured Swaps

Options

Corporate CreditConstantly searching for diversification and expansion of our credit exposure

Actions

Personalized, agile service, working closely with clientsand keeping a low ratio of companies per officer: eachaccount manager covers only 10 economic groups on

Credit Portfolio by ProductAs of June 30, 2011

Bank Guarantees

Trade finance11.9% Private

S iti *

(*) Includes debentures

account manager covers only 10 economic groups onaverage.

Origination staff comprised of 79 people focused onspecific geographic areas. It provides the bank with localand highly updated credit intelligence.

BNDES

Guarantees22.0%

Securities*1.6%

2770 Resolution

0.2%

Relationship with more than 600 different economicgroups

Origination network is comprised of 10 branches dividedinto 14 b siness platforms in different Bra ilian economic

Working

BNDES Onlendings

14.4%

into 14 business platforms in different Brazilian economiccenters

More than 30 credit analysts that guarantee intelligentanalysis in each sector

gCapital50.0%

Credit Approval: Electronic Process

Efficient loan and collaterals process, documentation andcontrols, which results in historically low NPL ratios

Origination OfficersOrigination Officers

Credit origination Credit analysis, visit to clients, data updates, interaction with internal

Credit AnalystsCredit Analysts

Discussion around sizing, collateral, structure etc

Regional Heads of Origination and Credit

Analysis

Regional Heads of Origination and Credit

Analysis

Presentation to the Credit Committee

Chief Credit Officerand Credit AnalystsChief Credit Officerand Credit Analysts

Centralized and unanimous decision making process

CREDIT COMMITTEE (5 Members)

CREDIT COMMITTEE (5 Members)

10/36Investor Relations | 2Q11 |

updates, interaction with internal research team

collateral, structure etc decision making process

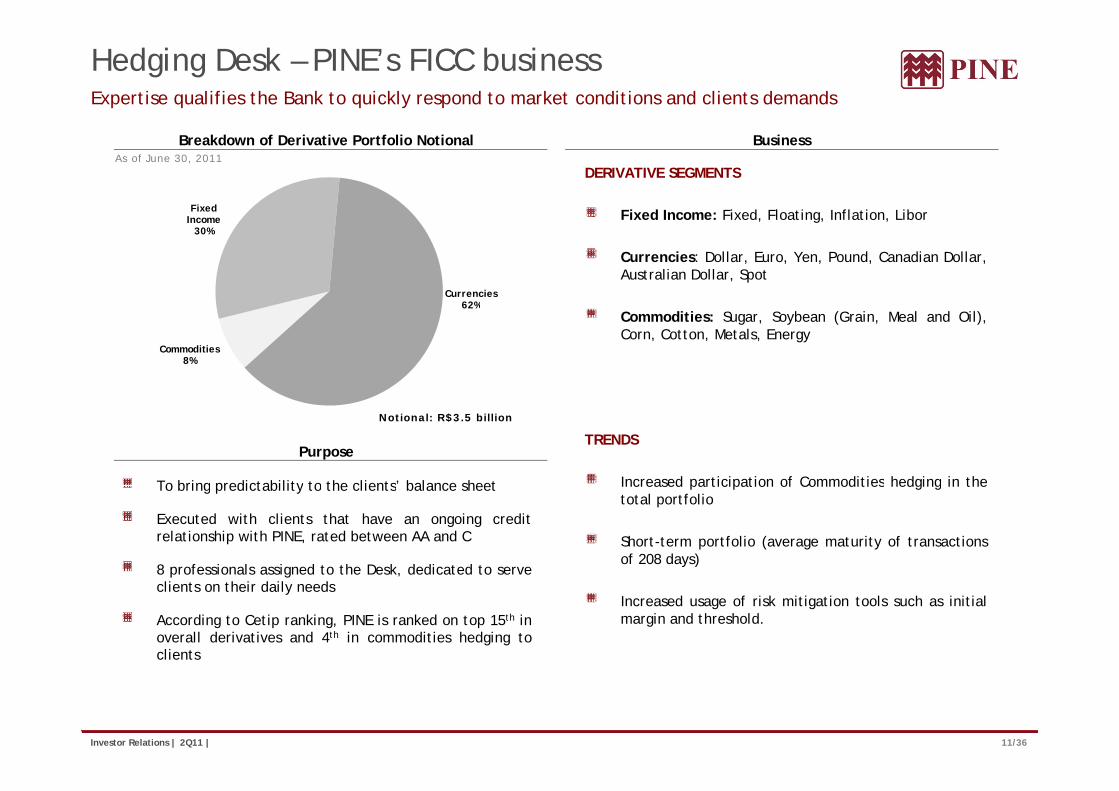

Hedging Desk – PINE’s FICC businessExpertise qualifies the Bank to quickly respond to market conditions and clients demands

Breakdown of Derivative Portfolio Notional Business

DERIVATIVE SEGMENTS

Fixed Income: Fixed Floating Inflation Libor

As of June 30, 2011

Fixed I Fixed Income: Fixed, Floating, Inflation, Libor

Currencies: Dollar, Euro, Yen, Pound, Canadian Dollar,Australian Dollar, Spot

Income30%

Currencies62%

Commodities: Sugar, Soybean (Grain, Meal and Oil),Corn, Cotton, Metals, Energy

Commodities8%

62%

Purpose

To bring predictability to the clients’ balance sheet

TRENDS

Increased participation of Commodities hedging in the

Notional: R$3.5 billion

To bring predictability to the clients balance sheet

Executed with clients that have an ongoing creditrelationship with PINE, rated between AA and C

8 professionals assigned to the Desk, dedicated to serve

Increased participation of Commodities hedging in thetotal portfolio

Short-term portfolio (average maturity of transactionsof 208 days)

p g ,clients on their daily needs

According to Cetip ranking, PINE is ranked on top 15th inoverall derivatives and 4th in commodities hedging toclients

Increased usage of risk mitigation tools such as initialmargin and threshold.

11/36Investor Relations | 2Q11 |

PINE InvestimentosCreating new values for clients and optimizing the use of the Bank’s Capital

PINE Investimentos offers unique solutions for its clients in Investment Banking and Investment Management.

With a highly qualified team and deep knowledge of the market this area operates as an advisor and not asWith a highly qualified team and deep knowledge of the market, this area operates as an advisor and not ascounterparty, serving the interests and needs of companies and their shareholders, in a customized manner and withdiversity of products.

Investment Banking Investment Management

Asset ManagementFixed Income Funds

Capital MarketsStructuring and Placement of Securities

Credit FundsExclusive Mandates

Wealth ManagementP tf li M t

IntermediationStructured Transactions

Corporate FinanceM&A Portfolio ManagementM&APrivate PlacementsStrategic and Financial AdvisoryRestructuringCorporate Governance

Distressed & Special SituationsAdvisory on WorkoutsNegotiation of NPLsAdvisory on Acquisitions of Stressed

12/36Investor Relations | 2Q11 |

y qAssets

DistributionInvestment alternatives in local and foreign currency to domestic and foreign investors

PINE’s Distribution Desk is responsible for serving investors, offering traditional investment products and alsoalternatives linked to the credit origination platform, capital market, asset management and other structuredtransactions.

The objective is to provide the clients with a diversified portfolio of investments in line with market development,that adjusts to investors’ risk profiles. The Distribution Desk counts on PINE’s expertise in structuring andintermediation of fixed income transactions.

Our Distribution Desk is segmented by type of investor to provide a personalized service.

ProductsInvestors

Family Offices

Individuals

Local CurrencyTraditional investments (local deposits such asCDB/RDB/CDI, LCA/LCI)Senior and subordinated local notes

Products

Companies

Asset Managers

Senior and subordinated local notesDebt Capital Markets (CCBs, Debentures, FIDCs, CRIs,CRAs, CDCAs, among others)Derivatives

F i CFinancial Institutions

Pension Funds

Foreign Investors

Foreign CurrencyTime Deposits and CD – Certificate of DepositSenior and Subordinated bonds issued by PINEDebt Capital Markets (CCB, Credit Fund, Bonds) – throughCredit Linked Notes

13/36Investor Relations | 2Q11 |

Foreign InvestorsDerivatives

The Current Scenario and Future ProspectsPINE has the key resources to continue developing its strategy: adequate capitalization, efficient funding and strong management team

Adequate capital structure Efficient funding structure

funding and strong management team

US$125 million subordinated debt, approved by theBrazilian Central Bank as Tier II capital in June 2010

Regulatory Capital: R$ 1.1 billion (Jun/11)

Lengthening of average maturities: 19 months(Jun/11)

Greater diversification of funding sources

Capital Adequacy Ratio (BIS) of 16.6% (Jun/11)

DEG and PINE partnership (Mar/11)

USD 106 million A/B Loan (Jan/11)

R$ 300 million FIDC (Apr/11)

Strong and motivated teamCorporate clients Strong and motivated teamMeritocracy

Incentives

Corporate clientsCustomized service

Deep knowledge of clients needs

QualificationProduct diversity

14/36Investor Relations | 2Q11 |

Highlights and Results

2Q11 HighlightsImprovement on the major KPIs in the 2Q11...

Corporate Credit (R$ Million)

7.9%

* Total Funding(R$ Million)

6.1%

Corporate Net Income (R$ Million)

11.0%

5,792 6,249

5,447 5,780 35.4 39.3

Mar-11 Jun-11 Mar-11 Jun-11 1Q11 2Q11Mar-11 Jun-11(*) Includes debentures

Mar-11 Jun-11 1Q11 2Q11

Net Income (R$ Million)

14 7%

ROAE

210 bps

Corporate ROAE

180 bps14,7% 210 bps 180 bps

31.5 36.1

15.2%

17.3%

17.2%

19.0%

16/36Investor Relations | 2Q11 |

1Q11 2Q11 1Q11 2Q11 1Q11 2Q11

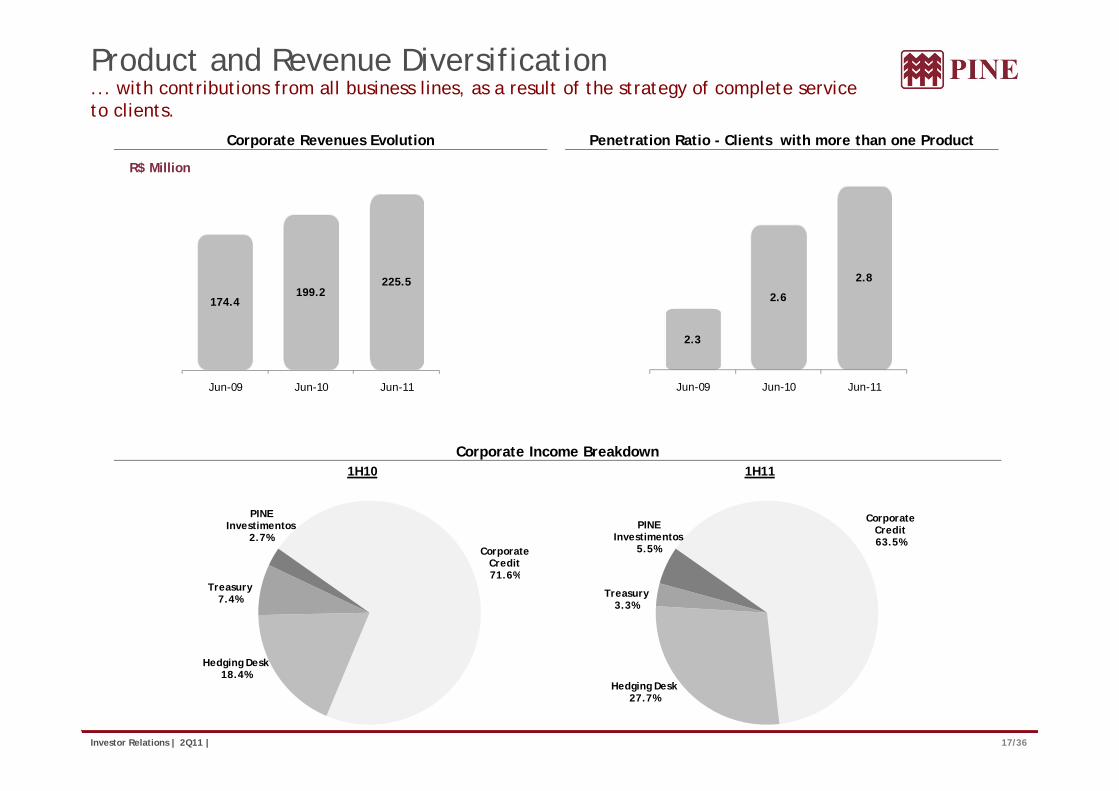

Product and Revenue Diversification ... with contributions from all business lines, as a result of the strategy of complete service to clients.

Corporate Revenues Evolution Penetration Ratio - Clients with more than one Product

R$ Million

174.4199.2

225.52.6

2.8

.

Jun-09 Jun-10 Jun-11

2.3

Jun-09 Jun-10 Jun-11

Corporate Income Breakdown1H10 1H11

Corporate Credit71 6%

PINE Investimentos

2.7%

Corporate Credit63.5%

PINE Investimentos

5.5%

71.6%

Hedging Desk

Treasury7.4% Treasury

3.3%

17/36Investor Relations | 2Q11 |

Hedging Desk 18.4%

Hedging Desk 27.7%

Credit PortfolioCredit portfolio evolution remained positive, posting a 7.9% growth in the quarter...

6 249

558

534 601 751

-

-71

97 Corporate Credit Breakdown (R$ Million)

Private Securities*

4 462

4,794

5,265

5,7475,792

6,249

Corporate credit portfolio grew 30.3% in 12 months.

242 455

629 833

871 902

511 634

842

827

1,022 1,117 1,372

695

728 764

705

--

--

-

Trade finance

Bank Guarantees

3,068

3,416

4,1184,462

1 964 2,284

2,703 2,821 2,792 3,251 3,358 3,132 3,126

68 87

176 242 455

292

350 744

Onlendings

(*) Includes debentures Total Credit Portfolio (R$ Million)

1,964

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

Working Capital

( )

8 01

016

022

,439

Total Credit Portfolio (R$ Million)

Increase of the corporateloan portfolio, whichrepresents 98% of the totalcredit portfolio.

3,89

3

4,08

9

4,73

1

4,96

0

5,18

8

5,60 6,0

6,0 6,

18/36Investor Relations | 2Q11 |

(**) Includes corporate credit, debentures, remaining payroll-deductible loans and credit acquired from financial institutions

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

Credit Portfolio Profile - Corporate... growing in a diversified manner, both in sectors and products...

Mid-West12%

North2%

C di P f li b S

Geographic Distribution

Northeast5%

12%Credit Portfolio by Sector

Infrastructure8%

Transportation and Logistics

6%

Meat packing5% Foreign Trade

5%

Financial

Southeast72%

South 9%

l

Construction8%

Financial Institutions

4%

Metal and Mining4%

Bank

Trade finance11 9%

Credit Portfolio by Product

Electric and

Agriculture9%

Telecom3%

Specialized Services Bank

Guarantees22.0%

11.9% Private Securities*

1.6%

2770 Resolution

0.2%Sugar and Ethanol

Electric and Renewable

Energy9%

Services3%

Vehicles and Parts3%

Pharmaceutical

BNDES Onlendings

14.4%

16%Pharmaceutical and Cosmetic

2%Other15%

19/36Investor Relations | 2Q11 |

Working Capital50.0%

(*) Includes debentures

Credit Portfolio Quality... with quality, collaterals and credit coverage.

Credit Portfolio Quality – June 2011 Non Performing Loans

B23.2%

Contracts Overdue

Instalments Overdue

C5.7% 1.

1%

9%

AA-A67.8%

D-E1.4%

F-H1.9%

0.

0.5%

0.5%

0.4%

0.4%

0.3%

0.2%

0.2%

0.2%

0.1%

0.1%

Total Credit Coverage Collaterals

More than 15 days

More than 30 days

More than 60 days

More than 90 days

More than 120 days

More than 180 days

94 b

Receivables38%Property

Pledge16%

94 bps4 bps

Products PledgeInvestments

1.76%

2.66% 2.70%

20/36Investor Relations | 2Q11 |

40%6%

Jun-10 Mar-10 Jun-11

FundingFunding is growing with quality and diversity...

102

Funding Mix( R$ Million)

Private Placements

Capital Market5.589

5 3755.447

5.780

829 898

413 377

435 596

419 249

192 152

125

92

230 239 227

200 160

282

267

75 276 203

194 194 201

220

77 87 151

166 179 172

102 Multilateral Lines

Loan Assignments

Trade Finance

5.375

4.8714.6344.531

3.8523.674

1,463 1 559 1 114 1,287

91 85 175

198 214 218

212

39 50 36

46 42 41

53

85

206 248 201

224 320 272

209

87

176 242 453

626 867 898

596

527

525 448

405

650 529

419 330

247 225 116 108 78 72

BNDES

Interbank deposits

Demand deposits

1 225 1,570 1,566 1,646 1,654 1,564 1,720 1,845

807

840

1,123 1,064 1,124 1,463 1,559 1,114

88

89 77

63 84

85 68

87 596 Demand deposits

Individuals

Corporate Clients

861 1,225

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

Institutional

Foreign Funding – Multilateral Agencies

A/B Loan (January, 2011)

21/36Investor Relations | 2Q11 |

US$106.0 Million

Funding and Credit Portfolio Maturities ... posting a 4 months positive gap between credit and funding,

R$ million

Credit Funding

2,61

6

9 6

-

1,71

9

1,23

5

384

186

53

1,41

2

1,78

6

1,38

0

555

395

No Maturity Up to 3 months

(includes Cash)

From 3 to 12 months

From 1 to 3 years

From 3 to 5 years

More than 5 years

Average Maturity

Credit: 15 months

22/36Investor Relations | 2Q11 |

Funding: 19 months

Capital Adequacy Ratio (BIS)... while BIS ratio remained at a comfortable level.

0 6%

BIS Tier II Tier I

19.3%17.2%

15 6% 18 4% 17 4%

11% MinimumRegulatoty Capital

0.6%

0.5%0.5% 0.5% 3.9% 3.6%

3.6% 3.7% 3.4%

15.6%14.9%

18.5% 18.4% 17.4%17.1% 16.6%

18.7%16.7% 15.1% 14.4% 14.6% 14.8% 13.8% 13.4% 13.2%

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

BIS R ti Equity (R$ Thousand)

BIS Ratio

(%)

Tier I 907,057 13.2%

Tier II 230,523 3.4%

BIS 1,137,580 16.6%

23/36Investor Relations | 2Q11 |

Balance Sheet Strength and ProfitabilityIn summary, PINE shows profitability and buffers of liquidity, capital and credit portfolio coverage.

ROAE Total Loan Credit Coverage Ratio

5%

16.3

%

15.9

%

45%

.66%

2.70

%

10.

1H09 1H10 1H11

1.76

%

1.74

% 2.4 2 2

Capital Cash/Time Deposits DEG Regulatory Capital 11% Minimum Regulatoty Capital

Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

0.7%

17,3%17.3%

18.5

%

18.4

%

17.4

%

17.1

%

16.6

%

43%40%

43% 42% 42%

24/36Investor Relations | 2Q11 |

Jun-10 Sep-10 Dec-10 Mar-11 Jun-11Jun-10 Sep-10 Dec-09 Mar-11 Jun-11

Corporate Governance and Shares

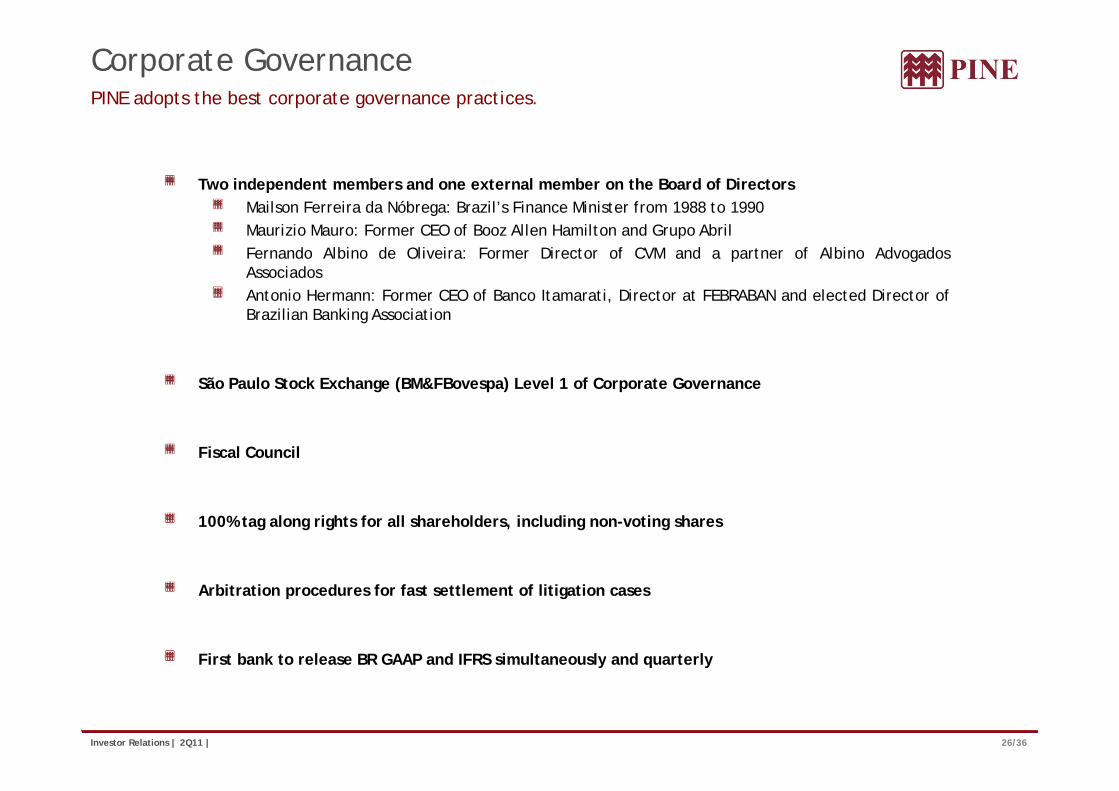

Corporate GovernancePINE adopts the best corporate governance practices.

Two independent members and one external member on the Board of DirectorsMailson Ferreira da Nóbrega: Brazil’s Finance Minister from 1988 to 1990Maurizio Mauro: Former CEO of Booz Allen Hamilton and Grupo AbrilFernando Albino de Oliveira: Former Director of CVM and a partner of Albino AdvogadosAssociadosAntonio Hermann: Former CEO of Banco Itamarati, Director at FEBRABAN and elected Director ofBrazilian Banking Association

São Paulo Stock Exchange (BM&FBovespa) Level 1 of Corporate Governance

Fiscal Council

100% tag along rights for all shareholders, including non-voting shares

Arbitration procedures for fast settlement of litigation cases

First bank to release BR GAAP and IFRS simultaneously and quarterly

26/36Investor Relations | 2Q11 |

y q y

Main CommitteesPINE believes that the use of the best corporate governance practices substantially enhancesits business outcome.its business outcome.

Main decisions are taken by committees: Board of Directors and a structure of specificcommitteesNon stop exchange of knowledge and informationNon-stop exchange of knowledge and informationTransparency

Board ofBoard ofBoard ofDirectorsBoard ofDirectors

Fiscal CouncilFiscal Council

PwCPwC

ExecutiveCommitteeExecutiveCommittee

TreasuryCommittee

(ALCO)

TreasuryCommittee

(ALCO)

ProductsCommitteeProducts

CommitteeCredit

CommitteeCredit

Committee

Internal Controls and

Audit

Internal Controls and

Audit DelinquencyCommittee

DelinquencyCommittee

Corporate Finance

Committee

Corporate Finance

Committee(ALCO)(ALCO) CommitteeCommitteeCommitteeCommittee

Cayman Committee

Cayman Committee

PerformanceEvaluationCommittee

PerformanceEvaluationCommittee

EthicsCommittee

EthicsCommittee

ITCommittee

ITCommittee

HumanResourcesCommittee

HumanResourcesCommittee

Risks Committee

Risks Committee

27/36Investor Relations | 2Q11 |

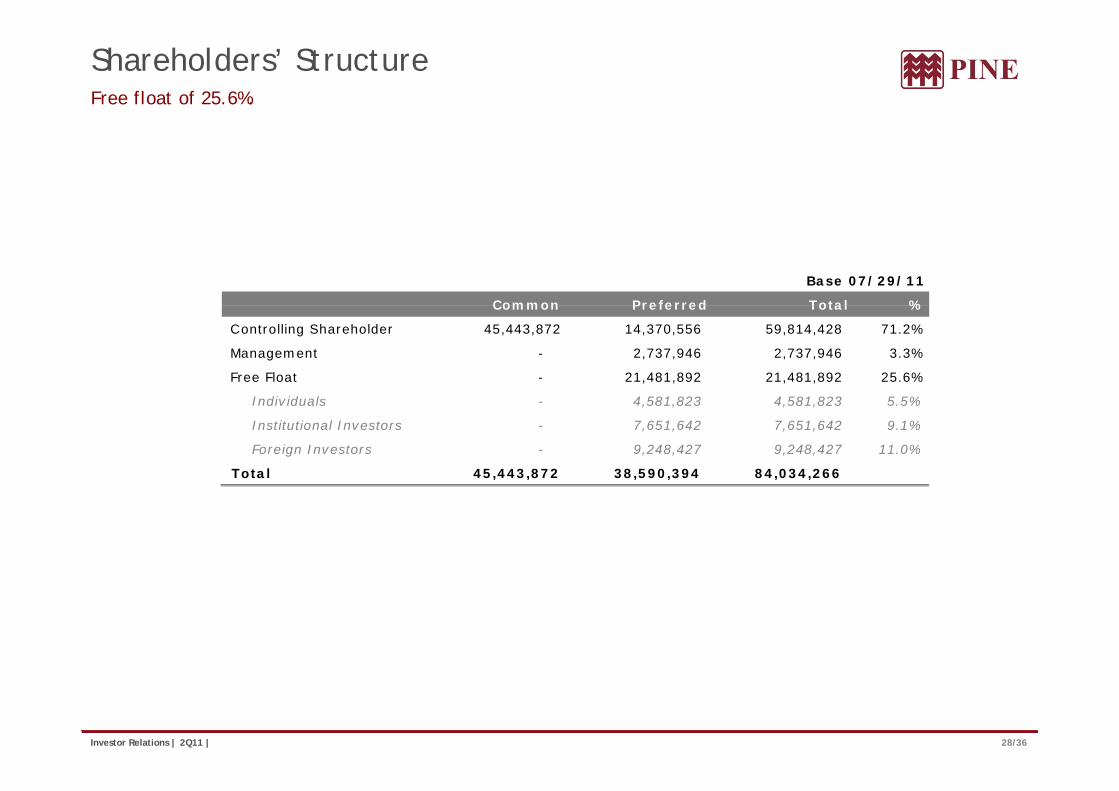

Shareholders’ StructureFree float of 25.6%.

Base 07/29/11

Common Preferred Total %Common Preferred Total %

Controlling Shareholder 45,443,872 14,370,556 59,814,428 71.2%

Management - 2,737,946 2,737,946 3.3%

Free Float - 21,481,892 21,481,892 25.6%

Individuals - 4,581,823 4,581,823 5.5%

Institutional Investors - 7,651,642 7,651,642 9.1%

Foreign Investors - 9,248,427 9,248,427 11.0%

Total 45,443,872 38,590,394 84,034,266

28/36Investor Relations | 2Q11 |

DividendsSince 2008, Banco PINE has paid dividends/interest on own capital on a quarterly-basis.

Dividends and Interest on Own Capital

R$ million R$

Gross Amount Total Amount Amount per share

1Q11 15.0 0.18

2Q11 20.0 0.24 Q

Total paid in 1H11 35.0 0.42

Dividends and Interest on Own Capital (R$ Million)

45 40

16

25 25

33 30 35

40 35

29/36Investor Relations | 2Q11 |

1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11

Other Highlights

2Q11 Events and HighlightsMarket Recognition.

PINE was ranked the 14th largest bank in Brazil in corporate credit and among the 12 largest banks in credit forlarge corporations, according to the Maiores e Melhores (Largest & Best) ranking compiled by Exame magazine.

PINE was ranked the 15th largest bank in Cetip’s overall derivatives ranking, and the 4th largest in commoditieshedging for clients.

Austin Rating upgraded PINE’s long-term rating in July 2011 from ‘A’ to ‘A+’ in July 2011.

On April 6th, PINE’s first Corporate Credit FIDC was successfully implemented. The amount of the fund is R$ 300million, with a AA+ rating attributed by S&P.

PINE was considered “The Most Green Bank” byInternational Finance Corporation’s (IFC) privateprograms agency of the World Bank. This was due to itsTrade Finance Program (GTFP) transactions worldwideand to its Corporate Loans to companies focused onand to its Corporate Loans to companies focused onrenewable energy and the ethanol market .

31/36Investor Relations | 2Q11 |

Social ResponsibilityBanco PINE supports and promotes Brazilian culture

SocialCasa HopeInstituto Alfabetização Solidária

CultureDiário de Navegação: addresses the first yearsof the occupation of the Brazilian coast by thePortuguese colonizers

Instituto Casa da ProvidênciaHospital Pequeno PríncipeGRAACC - Grupo de Apoio ao Adolescente e à Criança com CâncerColégio Mão Amiga

Paulo von Poser: exhibit of the painter Paulovon Poser, who is one of the main figures inBrazilian artTeatro Cultura Artística: it is one of thesponsors of the project for the renovation of theCultura Artística TheaterColégio Mão Amiga

SportsMinas Tênis Clube: training program forthl t

Cultura Artística TheaterQuebrando o Tabu: documentary based on theanalysis from the former President of Brazil,Fernando Henrique Cardoso, on the fight againstdrugsAlém da Estrada: motion picture whichathletes

Tênis Sobre Rodas: a project conducted bythe Brilho Brasileiro Institute founded by tennisplayer Vanessa Menga, which benefits 80disabled tennis players

Além da Estrada: motion picture, whichreceived the award for best director in the 2010Rio Festival

Responsible Credit

Green Building

“Lists of Exceptions”: the Bank does not finance –with multilateral organizations lines - projects orthose organizations that damage theenvironment, are involved in illegal laborpractices or produce, sell or use products,substances or activities considered prejudicial tosociety.

System of environmental monitoring, financed bythe IADB and coordinated by FGV, and internally-

d d t i bilit t f t

32/36Investor Relations | 2Q11 |

produced sustainability reports for corporateloans.

Appendix

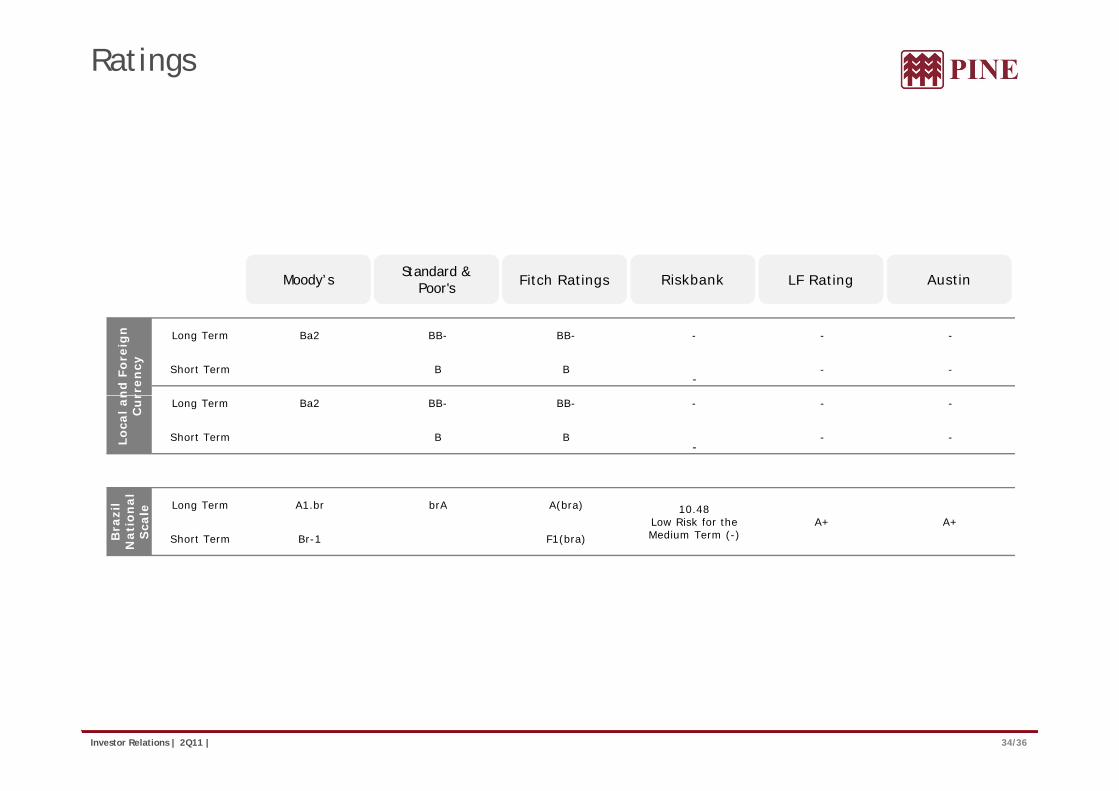

Ratings

Fitch RatingsFitch Ratings LF RatingLF Rating AustinAustinRiskbankRiskbankMoody’sMoody’s Standard & Poor's

Standard & Poor's

nd

Fo

reig

n

rren

cy

Long Term Ba2 BB- BB- - - -

Short Term B B-

- -

Lo

cal an

Cu

r

Long Term Ba2 BB- BB- - - -

Short Term B B-

- -

Bra

zil

Nati

on

al

Sca

le Long Term A1.br brA A(bra) 10.48Low Risk for the Medium Term (-)

A+ A+

Short Term Br-1 F1(bra)

34/36Investor Relations | 2Q11 |

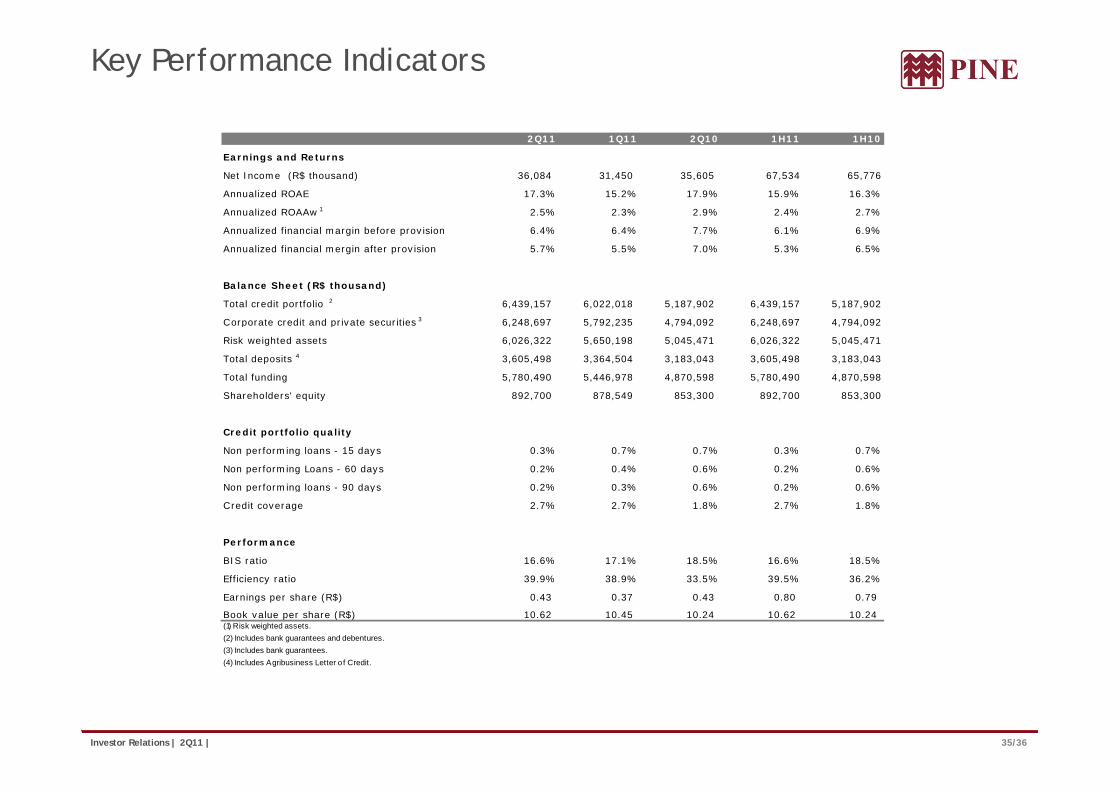

Key Performance Indicators

2Q11 1Q11 2Q10 1H11 1H10

Earnings and Returns

Net Income (R$ thousand) 36,084 31,450 35,605 67,534 65,776

Annualized ROAE 17.3% 15.2% 17.9% 15.9% 16.3%

Annualized ROAAw 1 2.5% 2.3% 2.9% 2.4% 2.7%

Annualized financial margin before provision 6.4% 6.4% 7.7% 6.1% 6.9%

Annualized financial mergin after provision 5.7% 5.5% 7.0% 5.3% 6.5%

Balance Sheet (R$ thousand)

Total credit portfolio 2 6 439 157 6 022 018 5 187 902 6 439 157 5 187 902Total credit portfolio 6,439,157 6,022,018 5,187,902 6,439,157 5,187,902

Corporate credit and private securities 3 6,248,697 5,792,235 4,794,092 6,248,697 4,794,092

Risk weighted assets 6,026,322 5,650,198 5,045,471 6,026,322 5,045,471

Total deposits 4 3,605,498 3,364,504 3,183,043 3,605,498 3,183,043

Total funding 5,780,490 5,446,978 4,870,598 5,780,490 4,870,598

Shareholders' equity 892 700 878 549 853 300 892 700 853 300Shareholders equity 892,700 878,549 853,300 892,700 853,300

Credit portfolio quality

Non performing loans - 15 days 0.3% 0.7% 0.7% 0.3% 0.7%

Non performing Loans - 60 days 0.2% 0.4% 0.6% 0.2% 0.6%

Non performing loans 90 days 0 2% 0 3% 0 6% 0 2% 0 6%Non performing loans - 90 days 0.2% 0.3% 0.6% 0.2% 0.6%

Credit coverage 2.7% 2.7% 1.8% 2.7% 1.8%

Performance

BIS ratio 16.6% 17.1% 18.5% 16.6% 18.5%

ffi i i 39 9% 38 9% 33 % 39 % 36 2%Efficiency ratio 39.9% 38.9% 33.5% 39.5% 36.2%

Earnings per share (R$) 0.43 0.37 0.43 0.80 0.79

Book value per share (R$) 10.62 10.45 10.24 10.62 10.24 (1) Risk weighted assets.(2) Includes bank guarantees and debentures.(3) Includes bank guarantees.(4) Includes Agribusiness Letter of Credit.

35/36Investor Relations | 2Q11 |

(4) Includes Agribusiness Letter o f Credit.

Investor Relations

Norberto Zaiet Junior

CFOCFO

Nira Bessler

Head of Investor Relations

Alexandre Cavalcanti

Investor Relations Manager

Alejandra Hidalgo

Investor Relations Analyst

Phone: +55-11-3372-5553

b i b /iwww.bancopine.com.br/ir

36/36Investor Relations | 2Q11 |

This presentation contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and those related to growth prospects of Banco Pine. These aremerely projections and, as such, are based exclusively on the expectations of Banco Pine’s management concerning the future of the business and its continued access to capital to fund the Company’sbusiness plan. Such forward-looking statements depend, substantially, on changes in market conditions, government regulations, competitive pressures, the performance of the Brazilian economy and theindustry, among other factors and risks disclosed in Banco Pine’s filed disclosure documents and are, therefore, subject to change without prior notice.