2Q11 LDK Investor Presentation FINAL

25

2Q 2011 Update September 2011

-

Upload

ana-syarif -

Category

Documents

-

view

218 -

download

0

Transcript of 2Q11 LDK Investor Presentation FINAL

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 1/25

2Q 2011 Update

September 2011

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 2/25

2

Disclaimer

The presentation is prepared by LDK Solar Co., Ltd. (“LDK" or the “Company”) and is being

presented solely for the purp ose of corpor ate communicat ion and g eneral reference. The

presentation is not intended as an offer to sel l , or to sol ic i t an offer to bu y or form any basis of

investment decis ion for any class of securi t ies of the Company in any jur isdict ion. Al l such

informat ion should n ot be u sed or rel ied on withou t professional advice. The presentat ion is a

brief summary in nature and do es not purpo rt to be a comp lete descript ion of the Company, its

business, i ts current or histor ical operat ing resul ts or i ts future prospects.

This presentat ion c ontains forw ard-looking statements that involve risks and un certaint ies. Al l

s tatements o ther than statements of histor ical facts are forw ard-looking statements. Thesestatements involve know n and u nknow n risks, uncertaint ies and o ther factors that may cause our

actual resul ts , performance or achievements to be materially di f ferent from those expressed or

impl ied by the forw ard-looking statements.

This presentat ion is pro vided withou t any warranty or representat ion of any kind, ei ther

expressed or im pl ied. The Company speci f ically disc laims al l responsibi l i t ies in respect of any

use or rel iance of any informat ion, whether f inancial or otherwise, contained in this presentat ion.

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 3/25

3

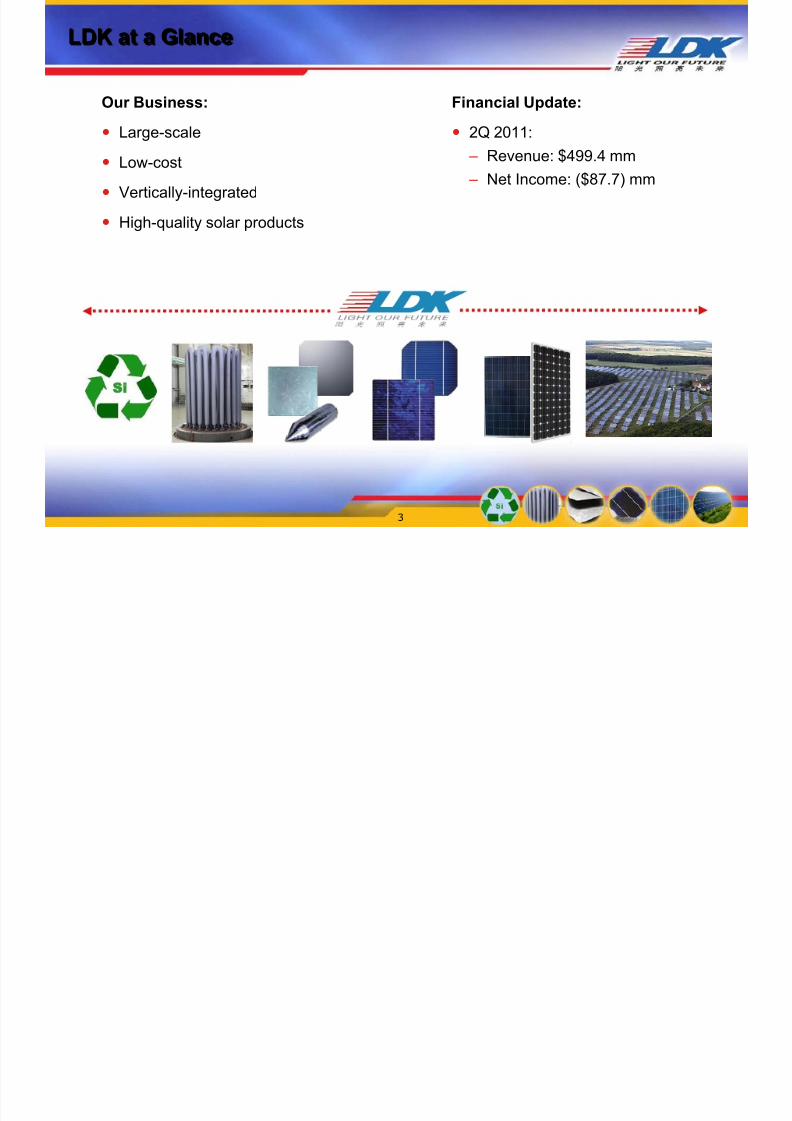

LDK at a Glance

Our Business:

Large-scale

Low-cost

Vertically-integrated

High-quality solar products

Financial Update:

2Q 2011:

– Revenue: $499.4 mm

– Net Income: ($87.7) mm

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 4/25

$7,057

$5,435$4,939

$4,385

$3,329

$2,639 $2,316$1,874

$1,553 $1,478

Suntech First Solar Yingli SunPower Trina Solar JA Solar Renesola Jinko Solar Hanwha

SolarOne

US$ MM

Top US-Listed Solar Company Globally by Assets

4

#1 by Assets, 1H 2011

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 5/25

$571

$470

$421

$375

$271$241

$239

$137

$79

$42

First Solar Yingli Trina Solar Renesola JA Solar Jinko Solar Hanwha

SolarOne

Suntech Sunpower

Top 2 US-Listed Solar Company by Operating Income

#2by Operating Income, Last Twelve Months

5

US$ MM

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 6/25

Key Growth Strategies

6

Large-Scale Vertical Integration Across Solar

Value Chain

1

Continue Cost Reductions To Achieve GridParity

2

A Long-TermWinner

in Solar & LED

Industry

Capture Growing Opportunities in LED Industry6

Maintain Premium-to-Market ASP by OfferingHigh Quality Products and Services3

Penetrate & Expand PV Projects Business withFinancing Solutions from China-Based Banks

4

Diversify and Grow Customer Base5

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 7/257

Strong Growth in Solar DemandTo Continue in 2011 and 2012

5.0 5.9

6.4 7.5

13.1

18.2

0

5

10

15

20

25

30

35

40

45

50

2008 2009 2010

(GW)

14.8

26.3

15.7

31.2

18.2

38.2

21.9

47.2

2011 2012 2013 2014

Forecast Actual Forecast Range

Source: Marketbuzz 2Q 2011.

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 8/258

Truly Vertically Integrated Leader in the Solar Industry

Polysilicon

In-House &Third Party

Ingot / Wafer

In-House

Cell

In-House &Third Party

Module

In-House

System / Project

In-House &Third Party

C a p a c i t y

SiliconRecycling

In-House

6,000 – 8,000MT per year

Current:12,000 MT

1H 2012:25,000MT

Current:3.7 GW

2011:4.0 GW

Current:1.3 GW

2011:2.0 GW

Current:1.6 GW

2011:3.0 GW

>500 MWpipelines inEurope, US,Asia andChina

L e a d e r s h i p

Largestrecyclingcapacityglobally

Expect to bea topproducer bycapacityglobally

#1 in wafershipmentsglobally

#2 in capacityglobally by endof 2011

Expect to betop 5 incapacityglobally by endof 2011

Expect to be#1 in c-Sicapacityglobally byend of 2011

Globalpresence

U.S. SPI, LDKEurope & SGT,China EPCProjects

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 9/259

Benefits of Vertical Integration

CustomerDiversification

Capture HigherMargins Across

Value Chain

Expand

AddressableMarket

Stability of Supply

Increase DemandVisibility

Reduce Volatility ofAny SingleBusiness

Quality Control

Less Than 300 Miles From Silicon to Module

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 10/25

7031,196 1,228

1,925

2,479 2,774

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

10

Polysilicon Capacity and Production Scale-Up

Polysilicon Production (MT)Polysilicon Capacity (MT)

10,000

22,000

4Q10 1H12

Ma Hong Plant

1,000

3,000

4Q10 1H12

Xia Cun Plant

Total

11,000

25,000

4Q10 1H12

463

951 1,049

1,626

2,172 2,487

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

Ma Hong Plant

Xia Cun Plant

Total

+ 5,000 (Line 3)

+ 7,000(Debottlenecking)

+ 2,000 (Line 2& Debottlenecking)

240 245179

299 307287

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 11/2511

Processing Cost Reduction – Polysilicon

Polysilicon Production Cost

(approximate % from 4Q10)Measures

A. Use of natural gas

B. Scale up to reduce depreciation and power

consumption

C. De-bottlenecking

D. Yield improvement

E. Localize consumables

F. Co-gen to supply steam

G. Others

Q4

2010

A B C D E F G Q4

2011E

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 12/2512

Wafer Capacity and Production Scale-Up

Wafer Capacity (MW)

1,400

1,800

3,000

4,000

2008 2009 2010 2011E

Historical conventions for watt per piece:

2008: 3.7w / piece2009 & 2010: 3.8w / piece2011: 4.1w / piece

Note: For 6-inch wafer

Increase in Conversion Rate

Effective Jan 1st, 2011, LDK has adjusted itsefficiency calculation to reflect currentindustry wafer/cell conversion efficiencies

We now assume an average conversion

efficiency of 16.9% for mono/multi-crystallinewafer/cell (up from 15.6%), or 4.1w / piece

We are using this new conversion conventionbeginning 2011

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 13/25

0.31

0.41

0.31

0.39

0.33

0.31

0.31

0.30

0.26

0.27

0.26

0.34

0.26

0.28

0.25

0.27

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11E 4Q11E

Processing Costs Polysilicon Cost

Processing Cost Reduction – Wafer

Target $0.02/Watt/Quarter

in Wafer Production Cost Through 2011

Target Wafer Production Cost ($/Watt)

$0.72

$0.64

$0.61 $0.53 $0.60$0.54

$0.52

$0.70

(1) Increase in 3Q10 processing cost is due to a one-time expenditureon spare parts and maintenance to equipment to improve future yield.

Measures

Thinner wafer for in-house cell use

Reduce kerf loss

Larger ingot sizes

Optimizing polysilicon mix through partial use

of in-house polysilicon production

Proprietary equipment upgrades to increase

capacity

Improvements in wafer quality

Greater manufacturing and purchasing

economies of scale

Increased consumables and polysilicon

recycling

Slurry recovery

13

Based on 3.8w / pc Based on 4.1w / pc

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 14/25

$0.27

$0.21 $0.21

$0.23

$0.19$0.18

3Q10 4Q10 1Q11 2Q11 3Q11E 4Q11E

Processing Cost Reduction – Cell

Target $0.01/Watt Reduction in CellProcessing Costs from 4Q10 to the end of 2011

Cell Capacity Scale Up (MW) Target Cell Processing Cost ($/Watt)

Measures

Increase economy of scale

Lower usages of paste

Improve overall yield

Improve cell efficiency

120 180

570

1,260

3Q10 4Q10 1Q11 2Q11

14

(1)

(1) 2Q 11 cell processing cost increased due to initial ramp upof Hefei facilities

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 15/25

25%

75%

20%

80%

Dec-10 Poly Ingot &

Wafer

Cell Module Q4 2011

Target

15

Fast Track to Achieve Grid Parity

In-House Silicon-To-Module R&D Production Program:

Already Succeeded At Below $1.00/Watt In Dec 2010

Non-silicon Cost

Silicon Cost

< $1.00

< $0.90

($/Watt)

Cost Reduction Roadmap:<$0.90/Watt in 2011

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 16/2516

Fast Track to Achieve Grid Parity (Con’t)

China US

$0.04

$0.05

$0.06

$0.07

$0.08

$0.09

$0.10

$0.11

$0.12

2010 2011 2012 2013

($/KWh) ($/KWh)

$0.04

$0.05

$0.06

$0.07

$0.08

$0.09

$0.10

$0.11

$0.12

2010 2011 2012 2013

Source: Company estimates, EIA, Xinhua News

LCOE stands for Levelized Cost of Electricity. Calculated by using current LDK system cost, divided by the present value ofelectricity produced by the PV system during its entire usage life. LCOE calculations assume: (1) Module and BOS costdecrease 5% per year from 2010; (2) Sunlight condition of 1500 kwh/kwp for China and USA; (3) Discount rate at 5%; (4)System usage life of 20 years; (5) Before LDK’s margin

Current RetailElectricity Price

LDK’s LCOE

Current RetailElectricity Price

LDK’s LCOE

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 17/2517

Update on System / Project Pipelines

SPI

209 MW

U.S.

Solar GreenTechnology

19 MW

Europe

96 MW

China

LDK Europe

Italy: 50MW

Bulgaria:15 MW

Germany:20 MW

Projects under development and pipel ine

Thailand:9 MW

India: 5 MW

Asia

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 18/2518

Diversified and High-Quality Customer Base

LDK su ppl ies leading solar companies wi th PV products aroun d the world!

Canada

Czech Republic

HHI-

KOMAX

Japan

India

Taiwan

France

U.S.

Belgium

Greece

Big Solar

Italy

Australia

KOMEX

Korea

Netherlands Germany

Portugal

Spain

China

“Golden Sun” Projects

Wafer Customers

Module Customers

Polysilicon Customers

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 19/25

Revenue by Geography

China

44.4%

Asia

Pacific,

others30.7%

Europe

24.7%

America

0.2%

2Q11 Sales 1Q11 Sales

19

China39.6%

AsiaPacific,others25.4%

Europe27.6%

America7.4%

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 20/25

Continue to Enhance Balance Sheet

20

Focus on strong operating cash flow and capex efficiency

Capital markets strategies:

January 2011: Follow-on offering of US$164 million

Convert short-term maturities into long-term maturities

February 2011: Bond offering of RMB1.2 billion

Polysilicon fundraising strategies

June 2011 closed CDB investment of US$240 million

Monetizing PV project assets

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 21/25

23

23

31

31

74

74

88

6

94

153

4

157

103

16119

65

14

79

0

50

100

150

200

250

4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q11 2Q'11

288

52

340

257

170

427

378

133

511

487

83

570

596

32

628

624

8

632

428

1

429

0

200

400

600

800

1,000

4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11

21

Strong Sales Track Record

Wafer Shipments

(MW)

Module Shipments

(MW)

Own Sales

OEM

ASP

$/w(own

sales)

$0.83 $0.83 $0.85 $0.87 $0.94 $0.84 $0.66

ASP

$/w(own

sales)

$1.64 $1.74 $1.77 $1.88 $1.86 $1.79 1.56

Own SalesOEM

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 22/25

Strong Operating Performance

Revenue Gross Profit

Operating Income Net Income

(US$ MM) (US$ MM)

(US$ MM)(US$ MM)

$304.6 $347.6

$565.3$675.6

$920.9

$766.3

$499.4

0

300

600

900

1,200

4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11

$30.2$54.5

$101.8

$150.0

$251.4$241.6

$11.0

0

100

200

300

4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11

-$16.1 $33.0

$78.6 $119.5

$203.8$196.1

($47.9)(100)

(50)

0

50

100150

200

250

4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11

($24.3) $7.2 $45.0

$93.4

$145.2 $135.4

($87.7)(150)

(100)

(50)

0

50100

150

200

4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11

Gross

Margin 9.9% 15.7% 18.0% 22.2% 27.3%

Operat ing

Margin NM 9.5% 13.9% 17.7% 22.1%

Net Income

Margin NM 2.1% 8.0% 13.8% 15.8%

22

31.5%

25.6% NMNM

2.2%

17.7%

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 23/25

23

3Q 2011 and FY 2011 Outlook

3Q 2011 Guidance FY 2011 Guidance

Revenues $630mm – $680mm $2.5bn – $2.7bn

Gross Margin 11.0% – 16.0% 15.0% – 20.0%

Wafer Shipments 350MW – 400MW 1.8GW – 2.0GW

ModuleShipments

250MW – 300MW 750MW – 800MW

In-house PolysiliconProduction

2,600MT – 2,700MT 10,000MT – 11,000MT

In-house Cell Production 200MW – 220MW 600MW – 700MW

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 24/25

24

Unaudited Condensed Financial Information

Balance Sheet Summary

2Q 2011

Cash and Cash Equivalents 636.4

Restricted Cash 515.3

Short-term borrowings and current installments of long-term borrowings 2,214.0

Convertible senior notes, less debt discount (current portion) 0.0Long-term borrowings, excluding current installments 804.4

Convertible senior notes, and senior RMB-denominated notes, less debt discount (long-term) 297.0

Total LDK Solar Co., Ltd. shareholders’ equity 1,347.8

Non-controlling interests 13.5

Total equity 1,361.3

As of June 30, 2011

(US$ MM)

(US$ MM, except per ADS data)

2Q 2011 1Q 2011

Net sales 499.4 766.3

Gross profit 11.0 241.6

Income from operations (47.9) 196.1

Net income attributable to LDK Solar shareholders (87.7) 135.4

Net income per ADS, Diluted ($0.62) $0.95

Income Statement Summary

8/10/2019 2Q11 LDK Investor Presentation FINAL

http://slidepdf.com/reader/full/2q11-ldk-investor-presentation-final 25/25

Thank You

www.ldksolar.com