293 clearchanne

355

CLEAR CHANNEL COMMUNICATIONS, INC. June 23, 2008 To the Shareholders of Clear Channel Communications, Inc.: You are cordially invited to attend the special meeting of shareholders of Clear Channel Communications, Inc., a Texas corporation, at the Watermark Hotel, 212 Crockett Street, San Antonio, Texas 78205 on July 24, 2008, at 4:00 p.m., local time. At the special meeting you will be asked to approve and adopt a merger agreement which provides for the merger of Clear Channel with a subsidiary of CC Media Holdings, Inc., a corporation formed by private equity funds sponsored by Bain Capital Partners, LLC and Thomas H. Lee Partners, L.P. If the merger agreement is approved and adopted by our shareholders, each share of Clear Channel’s common stock will be converted at the effective time of the merger into the right to receive either (1) $36.00 in cash, without interest, or (2) one share of Class A common stock of Holdings, subject to certain limitations. Except as described in the enclosed proxy statement/prospectus, you will have the right to elect the form of merger consideration you receive with respect to all or a portion of the stock and options you hold. However, the number of shares of Class A common stock that you receive as a result of your stock elections may be less than the number of shares you requested in the event that all stock elections collectively would require Holdings to issue more than 30% of the outstanding capital stock and voting power of Holdings immediately following the merger as a result of stock elections. In addition, you will not be allocated more than 11,111,112 shares of Holdings Class A common stock. In order to elect to receive the stock consideration you must submit a completed form of election and letter of transmittal, together with the share certificates or book-entry shares representing such shares, by 5:00 p.m., New York City time, on July 17, 2008, the fifth business day immediately preceding the date of the special meeting. In limited circumstances, the merger agreement provides that shareholders electing to receive cash consideration for some or all of their shares, on a pro rata basis, will be issued shares of Holdings Class A common stock in exchange for some of their shares of Clear Channel common stock for which they make a cash election, up to a cap of 1/36th of the total number of shares of Clear Channel common stock for which such shareholder makes a cash election. Any shares of Clear Channel common stock and options that are not converted into stock consideration due to failure to validly elect stock consideration, or the limitations described above, will be converted into the cash consideration except to the extent described herein. All shareholders and optionholders will also receive an additional cash payment if the merger is consummated after November 1, 2008. Holdings Class A common stock issued in the merger will not be listed on any national securities exchange. Holdings has agreed, however, to file certain reports with the Securities and Exchange Commission for a period of two years following the closing of the merger. After careful consideration, your board of directors by unanimous vote has determined that the merger is in the best interests of Clear Channel and its unaffiliated shareholders, approved the merger agreement and recommends that the shareholders of Clear Channel vote “For” the approval and adoption of the merger agreement. Your board of directors’ recommendation is limited to the cash consideration to be received by shareholders in the merger. Your board of directors makes no recommendation as to whether any shareholder should elect to receive the stock consideration and makes no recommendation regarding the Class A common stock of Holdings. The accompanying proxy statement/prospectus provides you with detailed information about the proposed merger, the special meeting and Holdings. Please give this material your careful attention. You may also obtain more information about Clear Channel from documents it has filed with the Securities and Exchange Commission. Your vote is very important regardless of the number of shares you own. The merger cannot be completed unless holders of two-thirds of the outstanding shares of Clear Channel entitled to vote at the special meeting vote for the approval and adoption of the merger agreement. Remember, failing to vote has the same effect as a vote against the approval and adoption of the merger agreement. We would like you to attend the special meeting; however, whether or not you plan to attend the special meeting, it is important that your shares be represented. If you intend to vote by proxy, please complete, date, sign and return the enclosed proxy card. Please note that if you have previously submitted a proxy card in response to Clear Channel’s prior solicitations, that proxy card will not be valid at this meeting and will not be voted. If your shares are held in “street name,” you should check the

-

Upload

finance31 -

Category

Economy & Finance

-

view

893 -

download

4

Transcript of 293 clearchanne

CLEAR CHANNEL COMMUNICATIONS, INC.June 23, 2008

To the Shareholders of Clear Channel Communications, Inc.:

You are cordially invited to attend the special meeting of shareholders of Clear Channel Communications, Inc.,a Texas corporation, at the Watermark Hotel, 212 Crockett Street, San Antonio, Texas 78205 on July 24, 2008, at4:00 p.m., local time.

At the special meeting you will be asked to approve and adopt a merger agreement which provides for themerger of Clear Channel with a subsidiary of CC Media Holdings, Inc., a corporation formed by private equityfunds sponsored by Bain Capital Partners, LLC and Thomas H. Lee Partners, L.P.

If the merger agreement is approved and adopted by our shareholders, each share of Clear Channel’s commonstock will be converted at the effective time of the merger into the right to receive either (1) $36.00 in cash, withoutinterest, or (2) one share of Class A common stock of Holdings, subject to certain limitations. Except as described inthe enclosed proxy statement/prospectus, you will have the right to elect the form of merger consideration youreceive with respect to all or a portion of the stock and options you hold. However, the number of shares of Class Acommon stock that you receive as a result of your stock elections may be less than the number of shares yourequested in the event that all stock elections collectively would require Holdings to issue more than 30% of theoutstanding capital stock and voting power of Holdings immediately following the merger as a result of stockelections. In addition, you will not be allocated more than 11,111,112 shares of Holdings Class A common stock. Inorder to elect to receive the stock consideration you must submit a completed form of election and letter oftransmittal, together with the share certificates or book-entry shares representing such shares, by 5:00 p.m.,New York City time, on July 17, 2008, the fifth business day immediately preceding the date of the specialmeeting. In limited circumstances, the merger agreement provides that shareholders electing to receive cashconsideration for some or all of their shares, on a pro rata basis, will be issued shares of Holdings Class A commonstock in exchange for some of their shares of Clear Channel common stock for which they make a cash election, upto a cap of 1/36th of the total number of shares of Clear Channel common stock for which such shareholder makes acash election. Any shares of Clear Channel common stock and options that are not converted into stockconsideration due to failure to validly elect stock consideration, or the limitations described above, will beconverted into the cash consideration except to the extent described herein. All shareholders and optionholders willalso receive an additional cash payment if the merger is consummated after November 1, 2008.

Holdings Class A common stock issued in the merger will not be listed on any national securities exchange.Holdings has agreed, however, to file certain reports with the Securities and Exchange Commission for a period of twoyears following the closing of the merger.

After careful consideration, your board of directors by unanimous vote has determined that the merger is in the bestinterests of Clear Channel and its unaffiliated shareholders, approved the merger agreement and recommends that theshareholders of Clear Channel vote “For” the approval and adoption of the merger agreement. Your board of directors’recommendation is limited to the cash consideration to be received by shareholders in the merger. Your board ofdirectors makes no recommendation as to whether any shareholder should elect to receive the stock considerationand makes no recommendation regarding the Class A common stock of Holdings.

The accompanying proxy statement/prospectus provides you with detailed information about the proposedmerger, the special meeting and Holdings. Please give this material your careful attention. You may also obtainmore information about Clear Channel from documents it has filed with the Securities and Exchange Commission.

Your vote is very important regardless of the number of shares you own. The merger cannot be completed unlessholders of two-thirds of the outstanding shares of Clear Channel entitled to vote at the special meeting vote for theapproval and adoption of the merger agreement. Remember, failing to vote has the same effect as a vote against theapproval and adoption of the merger agreement. We would like you to attend the special meeting; however, whetheror not you plan to attend the special meeting, it is important that your shares be represented.

If you intend to vote by proxy, please complete, date, sign and return the enclosed proxy card. Please note thatif you have previously submitted a proxy card in response to Clear Channel’s prior solicitations, that proxy card willnot be valid at this meeting and will not be voted. If your shares are held in “street name,” you should check the

voting instruction card provided by your broker to see which voting options are available and the procedures to befollowed. If you hold shares through a broker or other nominee, you should follow the procedures provided by yourbroker or nominee. Please complete and submit a validly executed proxy card for the special meeting, even ifyou have previously delivered a proxy. If you have any questions or need assistance in voting your shares, pleasecall our proxy solicitor, Innisfree M&A Incorporated, toll free at (877) 456-3427.

Thank you for your continued support and we look forward to seeing you on July 24, 2008.

Sincerely,

Mark P. MaysChief Executive Officer

For a discussion of certain risk factors that you should consider in evaluating the transactions describedabove and an investment in Holdings Class A common stock, see “Risk Factors” beginning on page 31 of theaccompanying proxy statement/prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved ordisapproved of the securities to be issued under the accompanying proxy statement/prospectus, or deter-mined the accompanying proxy statement/prospectus is accurate or complete. Any representation to thecontrary is a criminal offense.

The proxy statement/prospectus is dated June 23, 2008, and is first being mailed to shareholders on or aboutJune 23, 2008.

CLEAR CHANNEL COMMUNICATIONS, INC.200 EAST BASSE ROAD

SAN ANTONIO, TEXAS 78209

NOTICE OF SPECIAL MEETING OF SHAREHOLDERSTO BE HELD ON JULY 24, 2008

June 23, 2008

To the Shareholders of Clear Channel Communications, Inc.:

A special meeting of the shareholders of Clear Channel Communications, Inc., a Texas corporation, will beheld at the Watermark Hotel, 212 Crockett Street, San Antonio, Texas 78205 on July 24, 2008, at 4:00 p.m., localtime, for the following purposes:

1. To consider and vote upon a proposal to approve and adopt the Agreement and Plan of Merger, dated asof November 16, 2006, by and among Clear Channel, BT Triple Crown Merger Co., Inc. (“Merger Sub”),B Triple Crown Finco, LLC and T Triple Crown Finco, LLC (together with B Triple Crown Finco, LLC, the“Fincos”), as amended by Amendment No. 1 thereto, dated April 18, 2007, by and among Clear Channel,Merger Sub and the Fincos, as further amended by Amendment No. 2 thereto, dated May 17, 2007, by andamong Clear Channel, Merger Sub, the Fincos and CC Media Holdings, Inc. (“Holdings”), and as furtheramended by Amendment No. 3 thereto, dated May 13, 2008, by and among Clear Channel, Merger Sub,Holdings and the Fincos (as amended, the “merger agreement”);

2. To consider and vote upon a proposal to adjourn or postpone the special meeting, if necessary orappropriate, to solicit additional proxies if there are insufficient votes at the time of the special meeting toapprove and adopt the merger agreement, as amended; and

3. To transact such other business that may properly come before the special meeting or any adjournmentor postponement thereof.

In accordance with Clear Channel’s bylaws, Clear Channel’s board of directors has fixed 5:00 p.m. New YorkCity time on June 19, 2008 as the record date for the purposes of determining shareholders entitled to notice of andto vote at the special meeting and at any adjournment or postponement thereof. All shareholders of record arecordially invited to attend the special meeting in person.

The approval and adoption of the merger agreement requires the affirmative vote of two-thirds of theoutstanding shares of Clear Channel common stock entitled to vote on the approval and adoption of the mergeragreement at the special meeting. Whether or not you plan to attend the special meeting, Clear Channel urgesyou to vote your shares by completing, signing, dating and returning the enclosed proxy card as promptly aspossible prior to the special meeting to ensure that your shares will be represented at the special meeting ifyou are unable to attend. If you sign, date and mail your proxy card without indicating how you wish to vote, yourproxy will be voted on all matters in accordance with the recommendation of the board of directors. If you fail toreturn a valid proxy card and do not vote in person at the special meeting, your shares will not be counted forpurposes of determining whether a quorum is present at the special meeting. Remember, failing to vote has thesame effect as a vote against the approval and adoption of the merger agreement. Any shareholder attendingthe special meeting may vote in person, even if he or she has returned a proxy card; such vote by ballot will revokeany proxy previously submitted. However, if you hold your shares through a bank or broker or other custodian ornominee, you must provide a legal proxy issued from such custodian or nominee in order to vote your shares inperson at the special meeting.

Please note that this proxy statement/prospectus amends and restates all proxy statements, prospectuses, andsupplements thereto previously distributed by Clear Channel or Holdings with respect to the merger.

If you intend to vote by proxy, please complete, date, sign and return the enclosed proxy card. Please note thatif you have previously submitted a proxy card in response to Clear Channel’s prior solicitations, that proxy card willnot be valid at this meeting and will not be voted. If your shares are held in “street name,” you should check thevoting instruction card provided by your broker to determine which voting options are available and the proceduresto be followed. If you hold shares through a broker or other nominee, you should follow the procedures provided byyour broker or nominee. Please complete and submit a validly executed proxy card for the special meeting,

even if you have previously delivered a proxy. If you have any questions or need assistance in voting your shares,please call our proxy solicitor, Innisfree M&A Incorporated, toll free at (877) 456-3427.

If you plan to attend the special meeting, please note that space limitations make it necessary to limitattendance to shareholders and one guest. Each shareholder may be asked to present valid picture iden-tification, such as a driver’s license or passport. Shareholders holding stock in brokerage accounts (“streetname” holders) will need to bring a copy of a brokerage statement reflecting stock ownership as of the recorddate. Cameras (including cellular telephones with photographic capabilities), recording devices and otherelectronic devices will not be permitted at the special meeting. The special meeting will begin promptly at4:00 p.m., local time.

Shareholders who do not vote in favor of the approval and adoption of the merger agreement will have the rightto seek appraisal of the fair value of their shares if the merger is completed, but only if they submit a writtenobjection to the merger to Clear Channel before the vote is taken on the merger agreement and they comply with allrequirements of Texas law, which are summarized in the accompanying proxy statement/prospectus. Clear Channelurges that you to read the entire proxy statement/prospectus carefully.

By Order of the Board of Directors

Andrew W. LevinExecutive Vice President, Chief Legal Officer, andSecretary

San Antonio, Texas

TABLE OF CONTENTS

Page

REFERENCES TO ADDITIONAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

QUESTIONS AND ANSWERS ABOUT THE MERGER AND THE SPECIAL MEETING . . . . . . . . . . 2

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING INFORMATION . . . . . . . . . . . 11

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

The Parties to the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

The Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Effects of the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Determination of the Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Determination of the Special Advisory Committee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Interests of Clear Channel’s Directors and Executive Officers in the Merger . . . . . . . . . . . . . . . . . . . . 16

Opinion of Clear Channel’s Financial Advisor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Regulatory Approvals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Material United States Federal Income Tax Consequences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Conditions to the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Solicitation of Alternative Proposals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Termination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Termination Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Limited Guarantee of the Sponsors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Transaction Fees and Certain Affiliate Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Settlement Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Escrow Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Clear Channel’s Stock Price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Shares Held by Directors and Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Dissenters’ Rights of Appraisal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Stock Exchange Listing. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Resale of Holdings Class A Common Stock. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Holdings Stockholders Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Description of Holdings’ Capital Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Comparison of Shareholder Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Management of Holdings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Risks Relating to the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Risks Relating to Ownership of Holdings Class A Common Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Risks Relating to Clear Channel’s Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

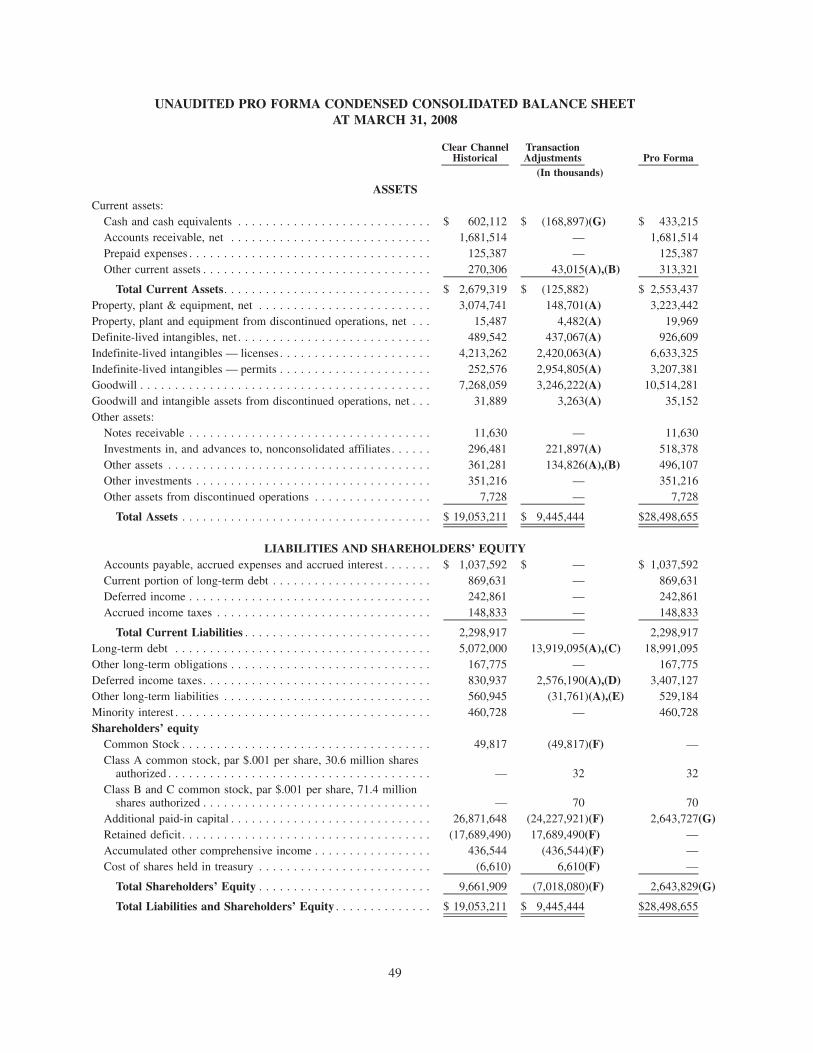

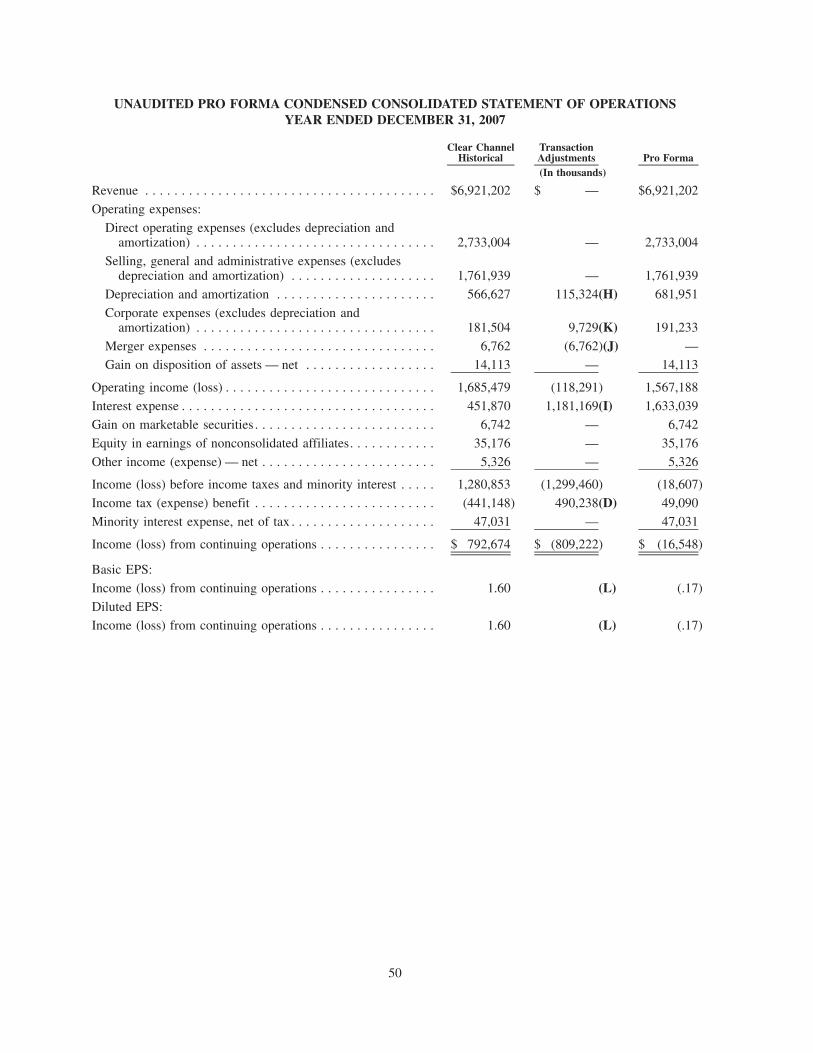

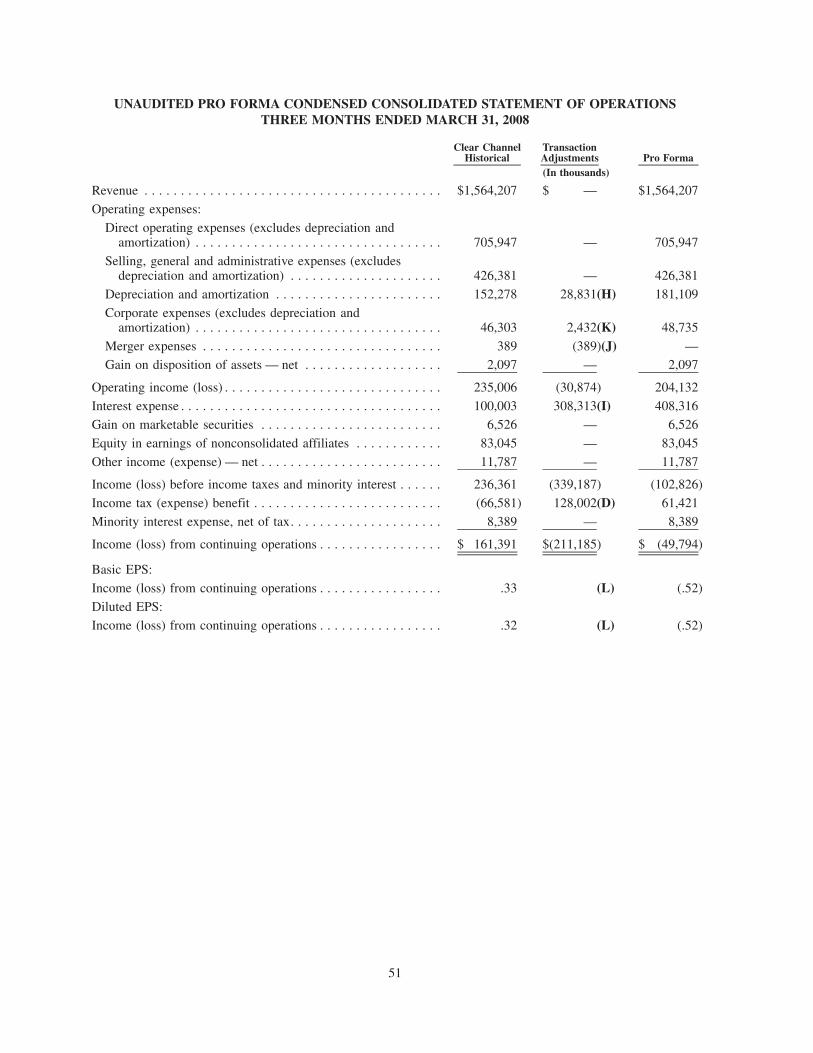

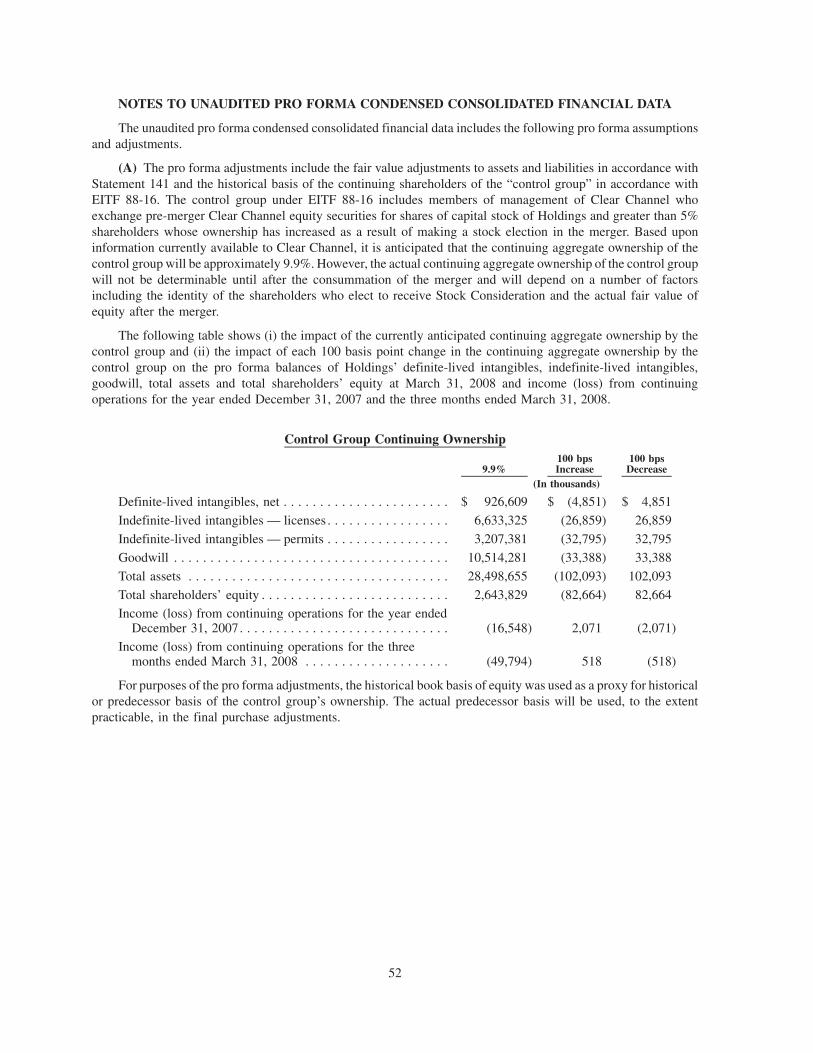

SELECTED HISTORICAL AND PRO FORMA CONSOLIDATED FINANCIAL DATA . . . . . . . . . . . . 45

Clear Channel Summary Historical Consolidated Financial Data. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Unaudited Pro Forma Condensed Consolidated Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

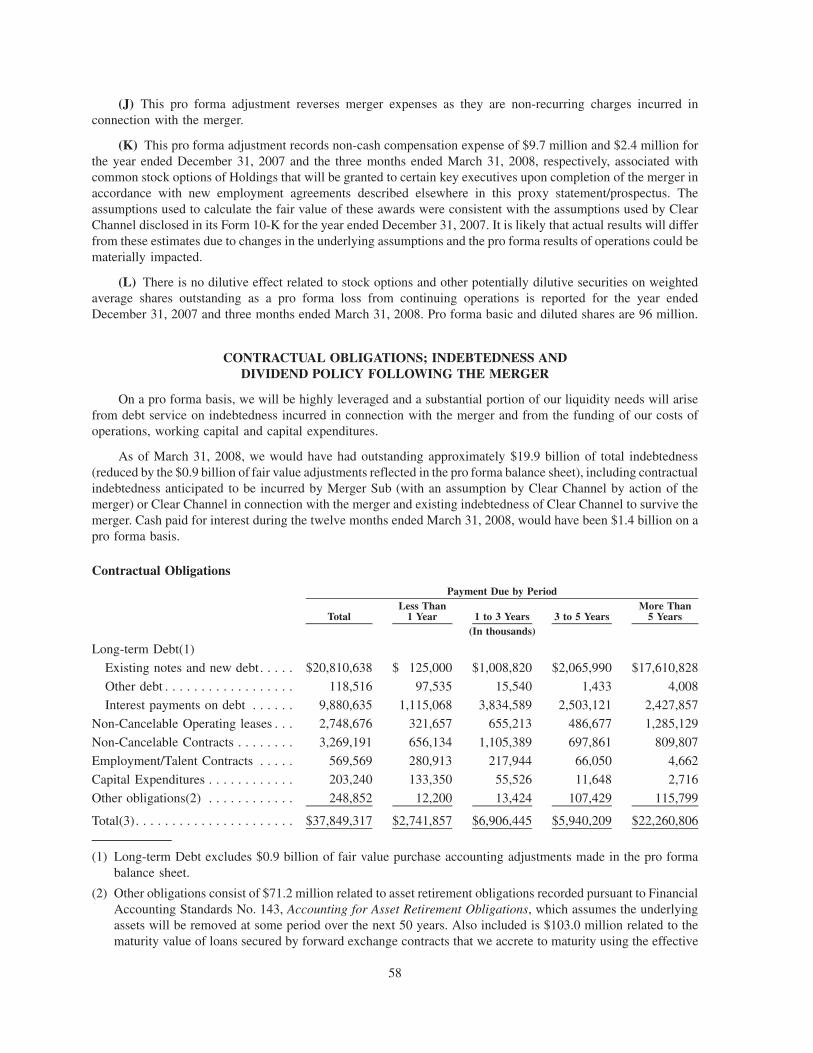

CONTRACTUAL OBLIGATIONS; INDEBTEDNESS AND DIVIDEND POLICY FOLLOWING THEMERGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Contractual Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58Indebtedness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Dividend Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

i

Page

DESCRIPTION OF BUSINESS OF HOLDINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

MANAGEMENT’S DISCUSSION AND ANALYSIS OF THE FINANCIAL CONDITION ANDRESULTS OF OPERATIONS OF CC MEDIA HOLDINGS, INC. . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

BOARD OF DIRECTORS AND MANAGEMENT OF HOLDINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Current Board of Directors and Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Anticipated Board of Directors and Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Biographies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Committees of the Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Director Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Compensation and Governance Committee Interlocks and Insider Participation . . . . . . . . . . . . . . . . . . 65

Independence of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Compensation of our Named Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Compensation Discussion and Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Overview and Objectives of Holdings’ Compensation Program . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Compensation Practices. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Elements of Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Base Salary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Annual Incentive Bonus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Long-Term Incentive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Executive Benefits and Perquisites. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Change-in-Control and Severance Arrangements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Tax and Accounting Treatment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Deductibility of Executive Compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Corporate Services Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Employment Agreements with Named Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Potential Post-Employment Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Holdings Equity Incentive Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

THE PARTIES TO THE MERGER. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

CC Media Holdings, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Clear Channel Communications, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

B Triple Crown Finco, LLC and T Triple Crown Finco, LLC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

BT Triple Crown Merger Co., Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

THE SPECIAL MEETING OF SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Time, Place and Purpose of the Special Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Who Can Vote at the Special Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Vote Required for Approval and Adoption of the Merger Agreement; Quorum . . . . . . . . . . . . . . . . . . 77

Voting By Proxy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77Submitting Proxies Via the Internet or by Telephone . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

Adjournments or Postponements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

THE MERGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Background of the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Reasons for the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

Determination of the Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

ii

Page

Determination of the Special Advisory Committee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

The Amended Merger Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

Determination of the Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

Recommendation of the Clear Channel Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

Interests of Clear Channel’s Directors and Executive Officers in the Merger . . . . . . . . . . . . . . . . . . . . 114

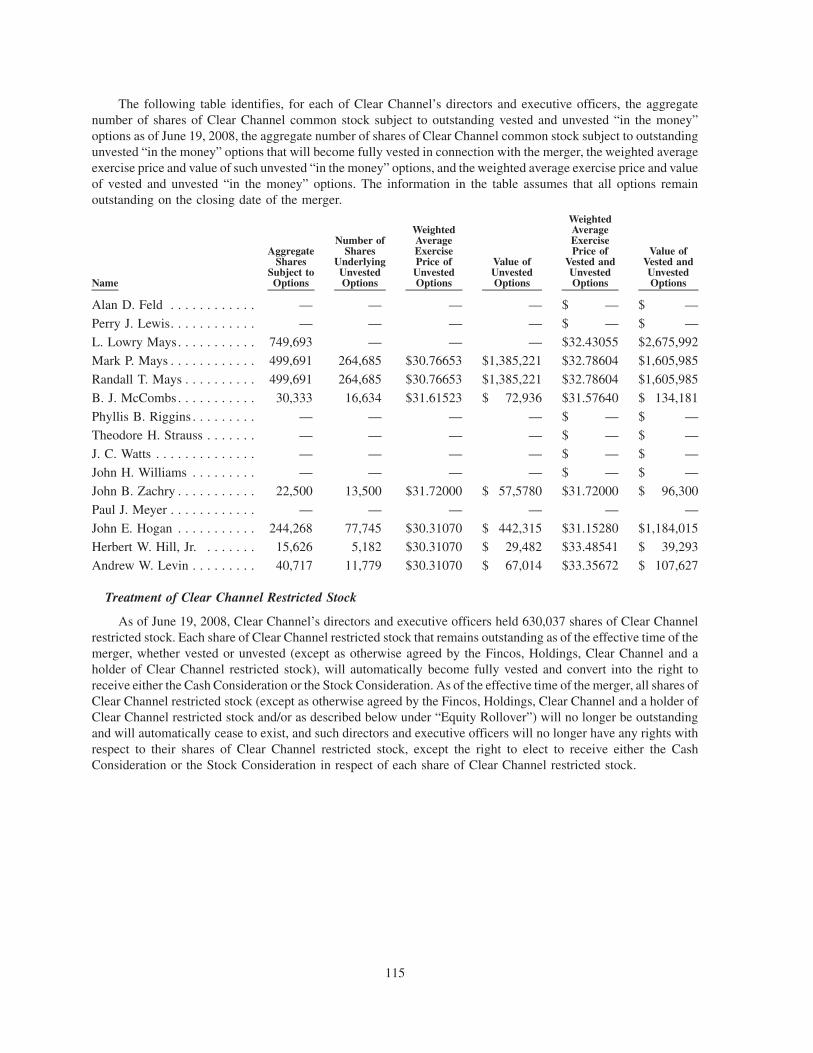

Treatment of Clear Channel Stock Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

Treatment of Clear Channel Restricted Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

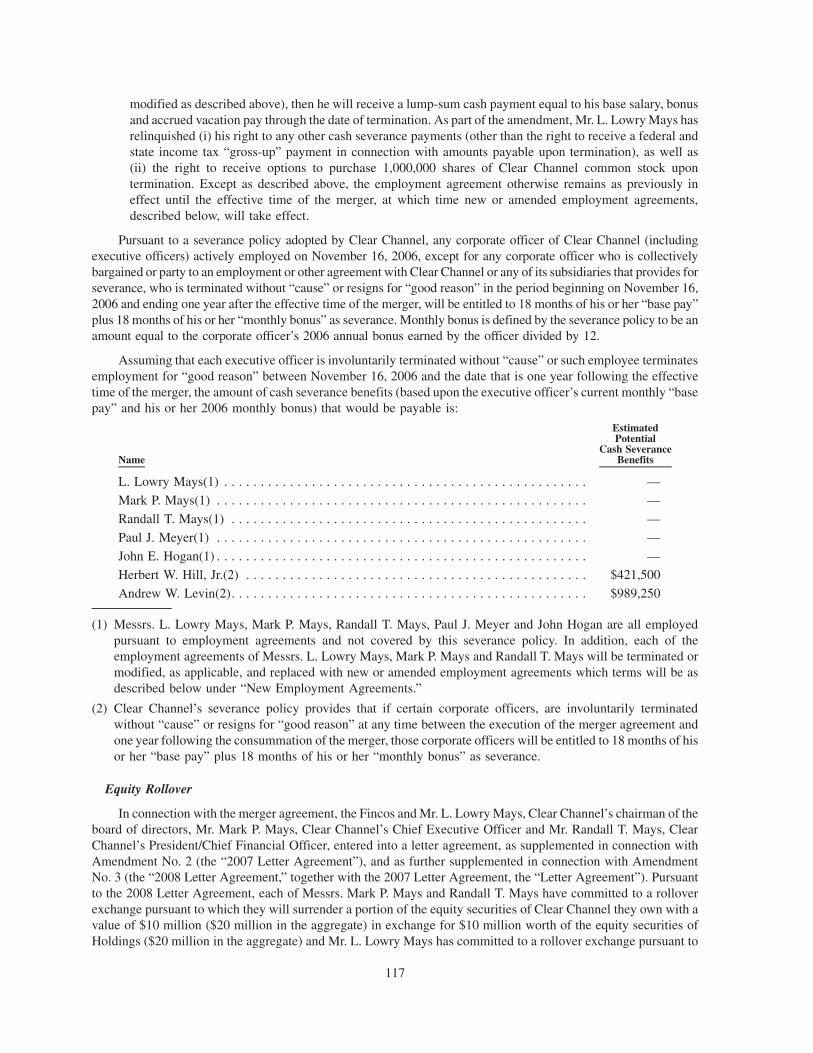

Severance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

Equity Rollover . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

New Equity Incentive Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

New Employment Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119Board of Director Representations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

Indemnification and Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

Voting Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

CERTAIN AFFILIATE TRANSACTIONS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

FINANCING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

Financing of the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

Equity Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Debt Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Senior Secured Credit Facilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Interest Rate and Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

Prepayments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

Amortization of Term Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Collateral and Guarantees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Conditions and Termination. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Certain Covenants and Events of Default . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Receivables Based Credit Facility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

Interest Rate and Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

Prepayments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Collateral and Guarantees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Senior Notes due 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Guarantees and Ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Interest Rate and Payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Optional Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132Special Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

Optional Redemption After Certain Equity Offerings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

Change of Control . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

Asset Sale Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

Certain Covenants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

Conditions and Termination. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

Events of Default . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

Registration Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134

iii

Page

OPINION OF CLEAR CHANNEL’S FINANCIAL ADVISOR. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134

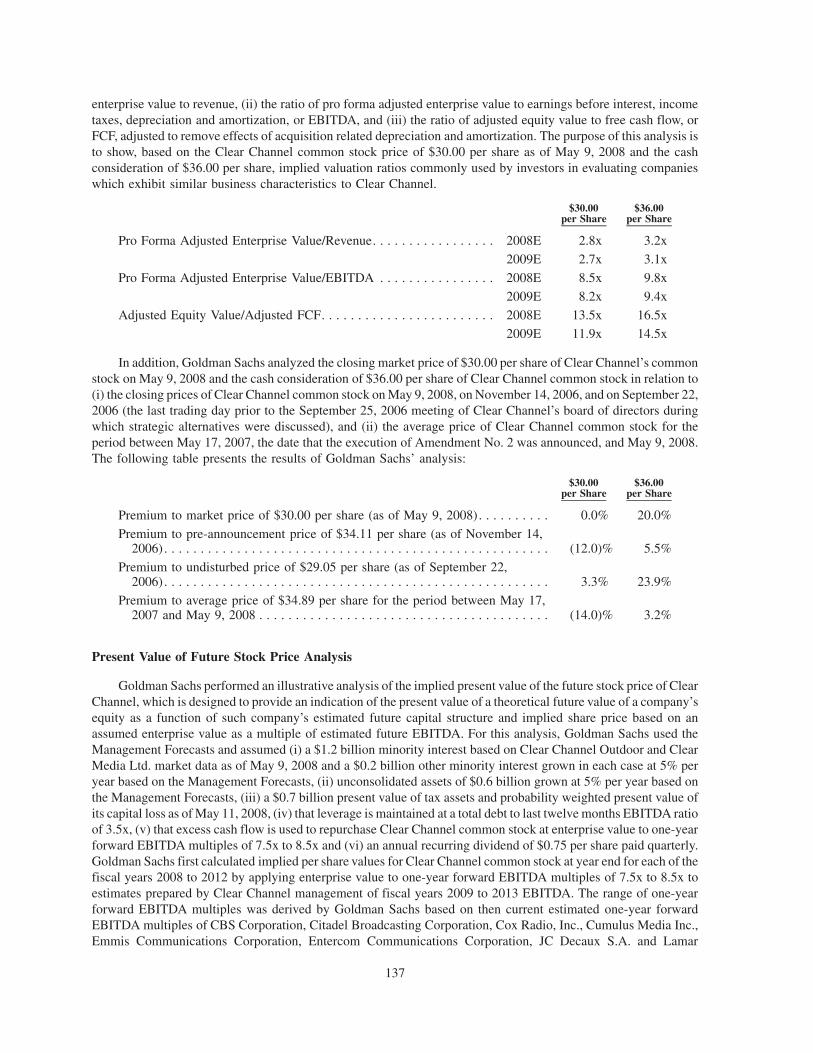

Present Value of Transaction Price Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

Analysis at Various Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

Present Value of Future Stock Price Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

Discounted Cash Flow Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

Sum-of-the-Parts Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

Miscellaneous . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

MATERIAL UNITED STATES FEDERAL INCOME TAX CONSEQUENCES . . . . . . . . . . . . . . . . . . . 141

Material United States Federal Income Tax Consequences to U.S. Holders . . . . . . . . . . . . . . . . . . . . . 142

ACCOUNTING TREATMENT OF TRANSACTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

REGULATORY APPROVALS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145Hart-Scott-Rodino . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

FCC Regulations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

STOCK EXCHANGE LISTING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

RESALE OF HOLDINGS CLASS A COMMON STOCK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

MERGER RELATED LITIGATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

THE MERGER AGREEMENT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Effective Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Effects of the Merger; Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Rollover by Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Treatment of Common Stock and Other Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

Clear Channel Common Stock. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

Clear Channel Stock Options. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

Clear Channel Restricted Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

Election Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

Proration Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

Additional Equity Consideration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

Exchange and Payment Procedures; Shareholder Rules. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

Representations and Warranties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

Conduct of Clear Channel’s Business Pending the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

FCC Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

Shareholders’ Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

Appropriate Actions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

Access to Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

Solicitation of Alternative Proposals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160Indemnification; Directors’ and Officers’ Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

Employee Benefit Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

Independent Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

Transaction Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

Conduct of the Fincos’ Business Pending the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

Registration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

Conditions to the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

iv

Page

Termination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166

Termination Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

Clear Channel Termination Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

Merger Sub Termination Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

Amendment and Waiver . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

Limited Guarantees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

SETTLEMENT AND ESCROW AGREEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

Settlement Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

Agreement to Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

Escrow Funding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

Termination of Actions and Release of Claims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170Certain Enforcement Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

No Admission. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

Escrow Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

Escrow Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

Disbursements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172

Shares Subject to the Stock Election . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172

At the Closing of the Merger. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172

Termination of Merger Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

Termination when there is a Company Breach or Buyer Breach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

Termination due to Failure to Obtain Shareholder Approval or when there is not a Company Breachor Buyer Breach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

MARKET PRICES OF CLEAR CHANNEL COMMON STOCK AND DIVIDEND DATA . . . . . . . . . . 175

DELISTING AND DEREGISTRATION OF CLEAR CHANNEL COMMON STOCK . . . . . . . . . . . . . . 176

SECURITY OWNERSHIP BY CERTAIN BENEFICIAL OWNERS AND MANAGEMENT . . . . . . . . . 177

HOLDINGS’ STOCK OWNERSHIP AFTER THE MERGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

STOCKHOLDERS AGREEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Parties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Voting Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Transfer Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 180

Drag-Along Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 180

“Tag-Along” and Other Sale Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 180

Effect of Termination of Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 180

Participation Rights in Future Issuances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181

Registration Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181

Withdrawal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

DESCRIPTION OF HOLDINGS’ CAPITAL STOCK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

Capitalization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182Voting Rights and Powers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

Dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183

Distribution of Assets Upon Liquidation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183

Split, Subdivision or Combination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183

Conversion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183

Certain Voting Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

v

Page

Change in Number of Shares Authorized . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

Restrictions on Stock Ownership or Transfer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

Requests for Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

Denial of Rights, Refusal to Transfer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

COMPARISON OF SHAREHOLDER RIGHTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 185

Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 186

Voting on Sale of Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 187

Antitakeover Provisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 187

Amendment of Certificate of Incorporation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 188

Amendment of Bylaws . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 188

Appraisal Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 188Special Meetings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189

Actions Without a Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189

Nomination of Director Candidates by Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189

Number of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189

Election of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 190

Vacancies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 190

Limitation of Liability of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 190

Indemnification of Officers and Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 191

Removal of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 192

Dividends and Repurchases of Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 192

Preemptive Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193

Inspection of Books and Records. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193

DISSENTERS’ RIGHTS OF APPRAISAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

EXPERTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

OTHER MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

Other Business at the Special Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

Multiple Shareholders Sharing One Address . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

WHERE YOU CAN FIND ADDITIONAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

INDEX TO ANNEXES

Annex A — Agreement and Plan of Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

Annex B — Amendment No. 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B-1

Annex C — Amendment No. 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . C-1

Annex D — Amendment No. 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . D-1

Annex E — Highfields Amended and Restated Voting Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-1Annex F — Abrams Voting Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

Annex G — Opinion of Goldman, Sachs & Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G-1

Annex H — Articles 5.11-5.13 of the Texas Business Corporation Act . . . . . . . . . . . . . . . . . . . . . . . . . . H-1

vi

REFERENCES TO ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important business and financial information about ClearChannel Communications, Inc. from other documents that are not included in, or delivered with, this proxystatement/prospectus. You can obtain documents related to Clear Channel Communications, Inc. that are incor-porated by reference in this proxy statement/prospectus, without charge, by requesting them in writing or bytelephone from either:

Clear Channel Communications, Inc. Innisfree M&A Incorporated200 East Basse Road 501 Madison Avenue

San Antonio, TX 78209 20th Floor(210) 832-3315 New York, NY 10022

Attention: Investor Relations Department (877) 456-3427

For information on where to obtain copies of such documents on the internet, see “Where You Can FindAdditional Information” elsewhere in this proxy statement/prospectus. Please note that copies of the documentsprovided to you will not include exhibits to the filings, unless those exhibits have specifically been incorporated byreference in this proxy statement/prospectus.

In order to ensure timely delivery of requested documents, any request should be made no later thanJuly 17, 2008, which is five business days prior to the special meeting.

For information on submitting your proxy, please refer to the instructions on the enclosed proxy card.

1

QUESTIONS AND ANSWERS ABOUT THE MERGER AND THE SPECIAL MEETING

The following questions and answers address briefly some questions you may have regarding the proposedmerger and the special meeting. These questions and answers may not address all questions that may be importantto you as a shareholder of Clear Channel Communications, Inc. To fully understand the proposed merger, pleaserefer to the more detailed information contained elsewhere in this proxy statement/prospectus, the annexes to thisproxy statement/prospectus and the documents referred to or incorporated by reference in this proxy statement/prospectus.

Unless otherwise stated or the context otherwise requires, all references in this proxy statement/prospectus to“Holdings,” “we,” “our,” “ours,” and “us” refer to CC Media Holdings, Inc., references to “Merger Sub” refer toBT Triple Crown Merger Co., Inc., references to “Clear Channel” refer to Clear Channel Communications, Inc.and its subsidiaries and references to the “Fincos” refer to B Triple Crown Finco, LLC and T Triple Crown Finco,LLC. In addition, unless otherwise stated or the context otherwise requires, all references in this proxy statement/prospectus to the “original merger agreement” refer to the Agreement and Plan of Merger, dated as of November 16,2006, by and among Clear Channel, Merger Sub and the Fincos, prior to amendment, all references to the “priormerger agreement” refer to the original merger agreement as amended by Amendment No. 1, dated April 18, 2007,among Clear Channel, Merger Sub and the Fincos (which we refer to as “Amendment No. 1” or the “firstamendment”), and as amended by Amendment No. 2, dated May 17, 2007, among Clear Channel, Merger Sub, theFincos and Holdings (which we refer to as “Amendment No. 2” or as the “second amendment”), all references inthis proxy statement/prospectus to the “merger agreement” refer to the prior merger agreement as amended byAmendment No. 3, dated May 13, 2008, among Clear Channel, Merger Sub, the Fincos and Holdings (which werefer to as “Amendment No. 3” or the “third amendment”), and all references to the “merger” refer to the mergercontemplated by the merger agreement. Copies of the original merger agreement, Amendment No. 1, AmendmentNo. 2, and Amendment No. 3 are attached to this proxy statement/prospectus as Annex A, Annex B, Annex C, andAnnex D, respectively.

QUESTIONS AND ANSWERS ABOUT THE MERGER

Q: What is the proposed transaction?

A: The proposed transaction is the merger of Clear Channel with Merger Sub, a company formed by privateequity funds sponsored by Bain Capital Partners, LLC and Thomas H. Lee Partners, L.P. In the merger,Merger Sub will merge with and into Clear Channel and Clear Channel will be the surviving corporation andwill become an indirect wholly-owned subsidiary of Holdings. Depending upon the number of shares ofClass A common stock of Holdings which shareholders and optionholders elect to receive in the merger aspart of the Merger Consideration (as defined below) and assuming that no Additional Equity Consideration(as defined below) is issued, up to 30% of the outstanding capital stock and voting power of Holdings will beheld by former Clear Channel shareholders and optionholders immediately following the merger.

Q: What will I receive for my shares of Clear Channel common stock in the merger?

A: You may elect one of the following options for each share of Clear Channel common stock you hold on therecord date:

Option 1 (which we refer to as a “Cash Election”): $36.00 per share cash consideration, without interest(which we refer to as the “Cash Consideration”); or

Option 2 (which we refer to as a “Stock Election”): one share of Class A common stock of Holdings (whichwe refer to as the “Stock Consideration”).

2

You may make a Cash Election or Stock Election (on a share-by-share basis) for each share of Clear Channelcommon stock you own as of the record date (including shares issuable on conversion of outstandingoptions), subject to the procedures, deadlines, prorations, Individual Cap and Additional Equity Consid-eration described below.

A Stock Election is purely voluntary. You are not required to make a Stock Election. A Stock Election is aninvestment decision which involves significant risks. The Clear Channel board of directors makes norecommendation as to whether you should make a Stock Election and makes no recommendationregarding the Class A common stock of Holdings. For a discussion of risks associated with the ownershipof Holdings Class A common stock see “Risk Factors” beginning on page 31 of this proxy statement/prospectus.

Other than with respect to 580,361 shares of Clear Channel common stock held by L. Lowry Mays and LLMPartners, Ltd. which will be held in escrow pursuant to the terms of an escrow agreement described in moredetail below and exchanged for Class A common stock of Holdings, shares and options held by directors oremployees of Clear Channel who have separately agreed to convert such shares or options into equitysecurities of Holdings in the merger will not affect the number of shares of Holdings Class A common stockavailable for issuance as stock consideration.

In limited circumstances described in more detail below, shareholders electing to receive cash considerationfor some or all of their shares, on a pro rata basis, will be issued shares of Holdings Class A common stock inexchange for some of their shares of Clear Channel common stock for which they make a Cash Election, up toa cap of 1/36th of the total number of shares of Clear Channel common stock for which such shareholdermakes a Cash Election (rounded down to the nearest whole share). We refer to this as the “Additional EquityConsideration.”

Q: Can I make a Cash Election for a portion of my shares of Clear Channel common stock and a StockElection for my remaining shares of Clear Channel common stock?

A: You may make your election on a share-by-share basis. As a result, you can make a Cash Election or StockElection for all or any portion of your shares of Clear Channel common stock.

Q: The Board earlier approved a transaction involving the same parties at a higher price and commencedproceedings in Texas State court against the banks financing the earlier transaction. Why did the boarddecide to accept the revised offer from the private equity group and not continue the proceedings incourt?

A: Under the terms of the prior merger agreement, Clear Channel had no contractual right to require theSponsors (as defined below), Banks (as defined below), Merger Sub, Holdings or the Fincos to perform theirrespective obligations under the prior merger agreement or the equity or debt financing agreements. ClearChannel’s rights under the prior merger agreement were limited to a right to receive a $500 milliontermination fee in the event Clear Channel terminated the prior merger agreement for failure of Holdings andthe Fincos to close when they were obligated to close under the prior merger agreement. Clear Channel wasseparately seeking damages against the Banks pursuant to the Texas Actions (as defined below).

Merger Sub was pursuing a breach of contract claim (including a claim for specific performance) against theBanks in the New York Action (as defined below) seeking to consummate the merger transaction contem-plated by the prior merger agreement, but there was no assurance that Merger Sub would have been able tocause a closing to occur even if it were successful in that action.

Complex litigation such as the New York Action, the New York Counterclaim Action (as defined below) andthe Texas Actions involve uncertainty and delay. While Clear Channel was confident in the merits of itsclaims, there was no assurance a court would have agreed with it or that, even if Clear Channel had beensuccessful in the Texas Actions, that any judgment would not have been modified or reversed on appeal.Further, litigation is time consuming and inherently subject to delay and there was no assurance that the TexasActions would have been concluded (or that all appeals would have been disposed of) on an accelerated basis,or the ultimate resolution of the litigation.

3

The Board of Directors determined that a merger on terms offering a high degree of certainty of closing andrepresenting a fair price to the shareholders was in the best interests of the shareholders when compared to thepursuit of litigation in which Clear Channel could not specifically enforce the closing of the prior transactionand Clear Channel’s damage claims were uncertain and subject to the delays inherent in litigation.

Q: Why is closing under the merger agreement more certain than the closing under the prior mergeragreement?

The merger agreement has a number of contractual features that make it more certain than the prior mergeragreement:

• the parties have entered into a Settlement Agreement (as defined below) whereby they have each agreed toperform their respective obligations under the merger agreement, the debt financing agreements, equitycommitments and the Escrow Agreement (as defined below). Pursuant to the Settlement Agreement, theparties stipulated to the entry of a court order in the New York Action directing the parties to perform theirobligations under the Settlement Agreement,

• the required debt financing is provided through fully negotiated and executed financing agreements (asopposed to debt commitment letters), thus avoiding the potential for a new dispute of the same type thatresulted in the failure of the closing of the prior transaction,

• the merger agreement, financing agreements and equity commitment letters contain fewer closingconditions than was originally the case,

• none of the merger agreement, financing agreements or equity commitment letters contains a “materialadverse change” or “MAC” condition,

• the Sponsors and the Banks have agreed to have their equity and debt commitment obligations fully fundedinto escrow pursuant to the Escrow Agreement, and

• each party (including Clear Channel) has the right to specifically enforce the merger agreement, theSettlement Agreement, the Escrow Agreement and the financing agreements.

Q: Why am I being asked to approve the transaction again?

A: Clear Channel shareholders approved the prior merger agreement at a special meeting of shareholders held inSeptember 2007. Since that time, the parties to the transaction have amended the terms of the prior mergeragreement. As part of that amendment, the cash consideration has been reduced from $39.20 per share to$36.00 per share. The merger agreement requires the approval of two thirds of the outstanding shares of ClearChannel common stock entitled to vote thereon at the special meeting.

Q: What will I receive for my options to purchase Clear Channel common stock in the merger?

A: A holder of options (whether vested or unvested) to purchase Clear Channel common stock as of the recorddate may make a Stock Election or a Cash Election with respect to the number of shares of common stockissuable upon exercise of his or her options, less the number of shares having a value (based on the CashConsideration) equal to the exercise price payable on such issuance and any required tax withholding. If aholder of options does not make a valid Stock Election, then each such outstanding option which remainsoutstanding and unexercised as of the effective time of the merger (except as otherwise agreed by the Fincos,Holdings, Clear Channel and the holder of such Clear Channel stock option), will automatically become fullyvested and convert into the right to receive a cash payment, without interest and less any applicablewithholding tax, equal to the product of (x) the excess, if any, of the Cash Consideration over the exerciseprice per share of such option and (y) the number of shares of Clear Channel common stock issuable upon theexercise of such Clear Channel stock option.

Q: How will restricted shares of Clear Channel common stock be treated in the merger?

A: In general, each restricted share of Clear Channel common stock that is outstanding as of the time of themerger, whether vested or unvested (except as otherwise agreed by the Fincos, Holdings, Clear Channel and aholder of Clear Channel restricted stock), will automatically become fully vested and will be treated the same

4

as all other shares of Clear Channel common stock outstanding at the time of the merger. The Fincos andMerger Sub have informed Clear Channel that they anticipate converting approximately 636,667 unvestedshares of Clear Channel restricted stock held by management and employees pursuant to a grant of restrictedstock made in May 2007 into restricted shares of Holdings Class A common stock on a one for one basis.These shares of Holdings Class A common stock will continue to vest in accordance with the schedule setforth in the holder’s May 2007 award agreement.

Q: What happens to the additional consideration contemplated by the prior merger agreement? Willthere be additional consideration under the terms of the amended merger agreement?

A: The additional consideration that was contemplated by the prior merger agreement is no longer in effect andtherefore will not be payable to Clear Channel shareholders.

The merger agreement provides for payment of “Additional Per Share Consideration” if the merger closesafter November 1, 2008. If the merger is completed after November 1, 2008, but on or before December 1,2008, you will receive Additional Per Share Consideration based upon the number of days elapsed sinceNovember 1, 2008 (including November 1, 2008), equal to $36.00 multiplied by 4.5% per annum, per share.If the merger is completed after December 1, 2008, the Additional Per Share Consideration will increase andyou will receive Additional Per Share Consideration based on the number of days elapsed since December 1,2008 (including December 1, 2008) equal to $36.00 multiplied by 6% per annum, per share (plus theAdditional Per Share Consideration accrued during November 2008). See “The Merger Agreement —Treatment of Common Stock and Other Securities” beginning on page 149 of this proxy statement/prospectus.

Your election to receive Cash Consideration or Stock Consideration will not affect your right to receive theAdditional Per Share Consideration if the merger closes after November 1, 2008. The total amount of CashConsideration, Stock Consideration, Additional Equity Consideration (if any) and Additional Per ShareConsideration (if any) paid in the merger is referred to in this proxy statement/prospectus as the “MergerConsideration.”

Q: If I make a Stock Election, will I be issued fractional shares of Class A common stock of Holdings in themerger?

A: No. If you make a Stock Election, you will not receive any fractional share in the merger. Instead, you willbe paid cash for any fractional share you would have otherwise received as Stock Consideration based uponthe Cash Consideration price of $36.00 per share, taking into account all shares of common stock and alloptions for which you elected Stock Consideration.

Q: Is there an individual limit on the number of shares of Clear Channel common stock and options topurchase Clear Channel stock that may be exchanged for Class A common stock of Holdings by eachClear Channel shareholder or optionholder?

A: Yes. No holder of Clear Channel common shares or options who makes a Stock Election, may receive morethan 11,111,112 shares of Class A common stock of Holdings immediately following the merger, which werefer to as the “Individual Cap.” Any shares of common stock or options that are not converted into StockConsideration due to the Individual Cap will be reallocated to other shareholders or optionholders who havemade an election to receive Stock Consideration but have not reached the Individual Cap. Any shares that arenot converted into Stock Consideration as a result of the Individual Cap will be converted into CashConsideration, subject to the issuance of any Additional Equity Consideration, if applicable. Unless abeneficial holder of Clear Channel shares submits a request in writing to the Paying Agent prior to 5:00 p.m.,New York City time, on July 17, 2008, the fifth business day immediately preceding the date of the specialmeeting, to have the Individual Cap apply with respect to all Clear Channel shares beneficially owned bysuch holder and provides information necessary to verify such beneficial ownership, the Individual Cap willapply, in the case of shares represented by physical stock certificates, to each holder of record of those ClearChannel shares, and in the case of book-entry shares, to each account in which those Clear Channel shares areheld on the books of the applicable brokerage firm or other similar institutions.

5

Q: Is there an aggregate limit on the number of shares of Clear Channel common stock and options topurchase Clear Channel common stock that may be exchanged for Class A common stock of Holdingsin the merger?

A: Yes. The merger agreement provides that no more than 30% of the total shares of capital stock of Holdingsare issuable in exchange for shares of Clear Channel common stock (including shares issuable uponconversion of outstanding options) pursuant to the Stock Elections. The issuance of any Additional EquityConsideration may result in the issuance of more than 30% of the total shares of capital stock of Holdings inexchange for shares of Clear Channel common stock (including shares issuable upon conversion ofoutstanding options).

Q: What happens if Clear Channel shareholders or optionholders elect to exchange more than themaximum number of shares of common stock (including shares issuable upon conversion of out-standing options) that may be exchanged for shares of Class A common stock of Holdings?

A: If Clear Channel shareholders and optionholders make Stock Elections covering more than the maximumnumber of shares of Clear Channel common stock that may be exchanged for Holdings shares of Class Acommon stock, then each shareholder and/or optionholder making a Stock Election (other than certainshareholders who have separately agreed with Holdings that their respective Stock Elections will be cutbackonly in the event that the amounts to be provided under the Equity Financing (as defined below) are reduced)will receive a proportionate allocation of shares of Class A common stock of Holdings based on the numberof shares of common stock (including shares issuable upon conversion of outstanding options) for which suchholder has made a Stock Election compared to the total number of shares of common stock (including sharesissuable upon conversion of outstanding options) for which all holders have made Stock Elections. Theproration procedures are designed to ensure that no more than 30% of the total capital stock of Holdings isallocated to shareholders and/or optionholders of Clear Channel pursuant to the Stock Elections. Any sharesthat will not be converted into Stock Consideration as a result of cutback or proration will be converted intoCash Consideration, subject to the issuance of Additional Equity Consideration, if applicable.

Q: In what circumstance might I be issued Class A common stock of Holdings despite the fact that I electedto receive cash in exchange for my shares of Clear Channel stock in the merger?

A: In certain circumstances, at the election of Holdings, the Cash Consideration may be reduced by theAdditional Equity Consideration. The Additional Equity Consideration will reduce the amount of the CashConsideration if the total funds that Holdings determines it needs to fund the merger, merger-relatedexpenses, and Clear Channel’s cash requirements (such funds referred to as “Uses of Funds”) is greater thanthe sources of funds available to Merger Sub from borrowings, equity contributions, Stock Consideration andClear Channel’s available cash (such funds referred to as “Sources of Funds”).

Q: How will the amount of the Additional Equity Consideration be determined?

A: In certain circumstances, at the election of Holdings, the Cash Consideration may be reduced by theAdditional Equity Consideration. The Additional Equity Consideration is an amount equal to the lesser of:

• $1.00, or

• a fraction equal to:

• the positive difference between:

• the Uses of Funds, and

• the Sources of Funds, divided by,

• the total number of Public Shares that will receive the Cash Consideration.

Consequently, if Holdings’ Uses of Funds exceeds its Sources of Funds, then, at the option of Holdings,shareholders electing to receive the Cash Consideration for some or all of their shares, on a pro rata basis, willbe issued shares of Holdings Class A common stock in exchange for some of their shares of Clear Channelcommon stock for which they made a Cash Election, up to a cap of 1/36th of the total number of shares of

6

Clear Channel common stock for which they made a Cash Election. If the Stock Election is fully subscribed,it is unlikely that any portion of the shares of Clear Channel stock for which a Cash Election is made will beexchanged for shares of Holdings’ Class A common stock, although Holdings retains the right to do so.

Q: Will the shares of Class A common stock of Holdings be listed on a national securities exchange?

A: No. Shares of Holdings Class A common stock will not be listed on the New York Stock Exchange, whichwe refer to as the “NYSE,” or any other national securities exchange. It is anticipated that, following themerger, the shares of Holdings Class A common stock will be quoted on the Over-the-Counter Bulle-tin Board. Holdings has agreed to register the Class A common stock under the Securities Exchange Act of1934, as amended, which we refer to as the “Exchange Act,” and to file periodic reports (including reports onForms 10-K, 10-Q and 8-K) for at least two years following the merger.

Q: What if I previously elected to receive the Stock Consideration prior to the special meeting ofshareholders held on September 25, 2007?

A: All of the stock elections made in connection with the special shareholders meeting held on September 25,2007 have been cancelled and the stock certificates and letters of transmittal evidencing the shares of ClearChannel common stock submitted for exchange have been returned to the record holders thereof. If you againwish to elect to receive some or all Stock Consideration in exchange for some or all of your shares of ClearChannel common stock, you are required to make a new election in connection with all shares of ClearChannel common stock held by you.

Q: How and when do I make a Stock Election or Cash Election?

A: A form of election and a letter of transmittal will be mailed with this proxy statement/prospectus to allshareholders as of the record date. Additional copies of the form of election and the letter of transmittal maybe obtained from Clear Channel’s proxy solicitor, Innisfree M&A Incorporated, which we refer to as“Innisfree,” by calling toll free at (877) 456-3427. Clear Channel will also make a copy of the form of electionand letter of transmittal available on its website at www.clearchannel.com/Investors. You should carefullyreview and follow the instructions in the letter of transmittal, which will include information regarding howto return the form of election, the letter of transmittal, and any shares for which you have made a StockElection for holders of shares of common stock held in “street name” through a bank, broker or othercustodian or nominee. The form of election and the letter of transmittal will need to be properly completed,signed and delivered prior to 5:00 p.m., New York City time, on July 17, 2008, the fifth business dayimmediately preceding the date of the special meeting.

Q: Can I revoke my form of election after I have submitted it to the paying agent?