$266,158,000 - Freddie Mac · 2 properties $11,588,027 6.2% of TEL Group Georgia 2 properties...

372

Offering Circular Supplement (To Offering Circular Dated June 2, 2017) $266,158,000 (Approximate) Freddie Mac Multifamily ML Certificates Series ML-05 Offered Classes: Classes of ML Certificates shown below Trust: FRETE 2019-ML05 Trust Underlying Tax-Exempt Loans: Tax-exempt loans (each a “TEL”) Originators: Bellwether Enterprise Real Estate Capital, LLC, Berkadia Commercial Mortgage LLC, CBRE Capital Markets, Inc., Citibank, N.A., Greystone Servicing Corporation, Inc., Hunt Mortgage Partners, LLC, Jones Lang LaSalle Multifamily, LLC, NorthMarq Capital, LLC, PNC Bank, National Association and Prudential Affordable Mortgage Company, LLC Depositor: Freddie Mac Master Servicer: Freddie Mac Special Servicer: KeyBank National Association Trustee, Certificate Administrator and Custodian: U.S. Bank National Association Payment Dates: Monthly beginning in April 2019 Optional Retirement: The ML Certificates are subject to a 10% clean-up call right, as described in this offering circular supplement Form of ML Certificates: Book-entry on DTC System Offering Terms: The placement agents named below are offering the ML Certificates shown below in negotiated transactions at varying prices Tax Status: Dechert LLP will render its opinion to the effect that (i) the issuing entity will be treated as two separate partnerships that own, respectively, the California TEL Group and the Non-California TEL Group, (ii) the holders of the certificates related to each TEL Group will be treated as partners in the partnership holding that TEL Group, (iii) the holders of the California Certificates will be allocated their respective shares of all federal and California tax-exempt interest accrued on the California TEL Group and all expenses and fees incurred by the partnership in respect of the California TEL Group for both federal and California income tax purposes, and (iv) the holders of the Non-California Certificates will be allocated their respective shares of all tax-exempt interest accrued on the Non-California TEL Group and all expenses and fees incurred by the partnership in respect of the Non-California TEL Group for federal income tax purposes. Closing Date: On or about March 28, 2019 Class Original Principal Balance or Notional Amount (1) Class Coupon CUSIP Number Expected Ratings S&P (2) Final Payment Date California Certificates A-CA $ 97,686,000 3.35000% 30309HAA5 AA+(sf) November 25, 2033 X-CA $ 97,686,000 (3) 30309HAB3 NR November 25, 2033 Non-California Certificates A-US $168,472,000 3.40000% 30309HAC1 AA+(sf) January 25, 2036 X-US $168,472,000 (3) 30309HAD9 NR January 25, 2036 (1) Approximate. May vary by up to 5%. (2) See “Ratings.” The class X-CA and X-US certificates are not rated. (3) See “Summary of Offering Circular Supplement—Transaction Overview and Description of the Certificates—Distributions—Calculation of Pass-Through Rates (California Certificates)” and “—Calculation of Pass-Through Rates (Non-California Certificates)” in this offering circular supplement. The ML Certificates may not be suitable investments for you. You should consider carefully the risks of investing in them. See “Risk Factors” and “Prepayment, Yield and Suitability Considerations” in our Multifamily ML Certificates Offering Circular dated June 2, 2017 (the “Offering Circular”). You should purchase ML Certificates only if you have read and understood this offering circular supplement, the attached Offering Circular and the documents listed under “Description of the Certificates—Reports to Certificateholders and Freddie Mac; Available Information.” We guarantee certain payments of interest and principal on the ML Certificates shown above. These payments are not debts or obligations of the United States or any federal agency or instrumentality other than Freddie Mac. Because of applicable securities law exemptions, we have not registered the ML Certificates with any federal or state securities commission. No securities commission has reviewed this supplement. The certificates have not been and will not be registered or qualified under the Securities Act of 1933, as amended (the “Securities Act”), or under the securities or “blue sky” laws of any state in the United States of America (“United States”). Accordingly, the class X-CA and X-US certificates are being offered and sold only (i) to qualified institutional buyers (“Qualified Institutional Buyers”) as defined in Rule 144A under the Securities Act (“Rule 144A”) in reliance on the exemption from the registration requirements of the Securities Act provided by Rule 144A or (ii) to other institutions that are, or all of the equity owners of which are, “accredited investors” (“Institutional Accredited Investors”) within the meaning of Rule 501(a)(1), (2), (3) or (7) of Regulation D under the Securities Act (“Regulation D”). This offering circular supplement serves notice to prospective purchasers of the class X-CA and X-US certificates that the placement agents may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. For certain restrictions on resales, see “Notice to Investors.” Co-Lead Managers and Joint Bookrunners Wells Fargo Securities Jefferies Co-Managers Citigroup Ramirez & Co., Inc. Stifel, Nicolaus & Company, Incorporated March 22, 2019

Transcript of $266,158,000 - Freddie Mac · 2 properties $11,588,027 6.2% of TEL Group Georgia 2 properties...

Offering Circular Supplement(To Offering CircularDated June 2, 2017)

$266,158,000(Approximate)

Freddie MacMultifamily ML Certificates

Series ML-05Offered Classes: Classes of ML Certificates shown belowTrust: FRETE 2019-ML05 TrustUnderlying Tax-Exempt Loans: Tax-exempt loans (each a “TEL”)Originators: Bellwether Enterprise Real Estate Capital, LLC, Berkadia Commercial Mortgage LLC, CBRE Capital

Markets, Inc., Citibank, N.A., Greystone Servicing Corporation, Inc., Hunt Mortgage Partners, LLC, JonesLang LaSalle Multifamily, LLC, NorthMarq Capital, LLC, PNC Bank, National Association and PrudentialAffordable Mortgage Company, LLC

Depositor: Freddie Mac

Master Servicer: Freddie Mac

Special Servicer: KeyBank National AssociationTrustee, CertificateAdministrator and Custodian: U.S. Bank National AssociationPayment Dates: Monthly beginning in April 2019Optional Retirement: The ML Certificates are subject to a 10% clean-up call right, as described in this offering circular

supplementForm of ML Certificates: Book-entry on DTC SystemOffering Terms: The placement agents named below are offering the ML Certificates shown below in negotiated

transactions at varying pricesTax Status: Dechert LLP will render its opinion to the effect that (i) the issuing entity will be treated as two separate

partnerships that own, respectively, the California TEL Group and the Non-California TEL Group, (ii) theholders of the certificates related to each TEL Group will be treated as partners in the partnership holdingthat TEL Group, (iii) the holders of the California Certificates will be allocated their respective shares of allfederal and California tax-exempt interest accrued on the California TEL Group and all expenses and feesincurred by the partnership in respect of the California TEL Group for both federal and California incometax purposes, and (iv) the holders of the Non-California Certificates will be allocated their respective sharesof all tax-exempt interest accrued on the Non-California TEL Group and all expenses and fees incurred bythe partnership in respect of the Non-California TEL Group for federal income tax purposes.

Closing Date: On or about March 28, 2019

ClassOriginal Principal Balance or

Notional Amount(1)Class

CouponCUSIP

NumberExpected Ratings

S&P(2)Final

Payment DateCalifornia Certificates

A-CA $ 97,686,000 3.35000% 30309HAA5 AA+(sf) November 25, 2033X-CA $ 97,686,000 (3) 30309HAB3 NR November 25, 2033

Non-California CertificatesA-US $168,472,000 3.40000% 30309HAC1 AA+(sf) January 25, 2036X-US $168,472,000 (3) 30309HAD9 NR January 25, 2036

(1) Approximate. May vary by up to 5%.(2) See “Ratings.” The class X-CA and X-US certificates are not rated.(3) See “Summary of Offering Circular Supplement—Transaction Overview and Description of the Certificates—Distributions—Calculation of Pass-Through Rates (California

Certificates)” and “—Calculation of Pass-Through Rates (Non-California Certificates)” in this offering circular supplement.

The ML Certificates may not be suitable investments for you. You should consider carefully the risks of investing in them. See “Risk Factors” and“Prepayment, Yield and Suitability Considerations” in our Multifamily ML Certificates Offering Circular dated June 2, 2017 (the “Offering Circular”). Youshould purchase ML Certificates only if you have read and understood this offering circular supplement, the attached Offering Circular and the documentslisted under “Description of the Certificates—Reports to Certificateholders and Freddie Mac; Available Information.”

We guarantee certain payments of interest and principal on the ML Certificates shown above. These payments are not debts or obligations of the United Statesor any federal agency or instrumentality other than Freddie Mac. Because of applicable securities law exemptions, we have not registered the ML Certificateswith any federal or state securities commission. No securities commission has reviewed this supplement.The certificates have not been and will not be registered or qualified under the Securities Act of 1933, as amended (the “Securities Act”), or under thesecurities or “blue sky” laws of any state in the United States of America (“United States”). Accordingly, the class X-CA and X-US certificates are beingoffered and sold only (i) to qualified institutional buyers (“Qualified Institutional Buyers”) as defined in Rule 144A under the Securities Act (“Rule 144A”) inreliance on the exemption from the registration requirements of the Securities Act provided by Rule 144A or (ii) to other institutions that are, or all of theequity owners of which are, “accredited investors” (“Institutional Accredited Investors”) within the meaning of Rule 501(a)(1), (2), (3) or (7) of Regulation Dunder the Securities Act (“Regulation D”). This offering circular supplement serves notice to prospective purchasers of the class X-CA and X-US certificatesthat the placement agents may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. For certainrestrictions on resales, see “Notice to Investors.”

Co-Lead Managers and Joint Bookrunners

Wells Fargo Securities JefferiesCo-Managers

Citigroup Ramirez & Co., Inc. Stifel, Nicolaus & Company, Incorporated

March 22, 2019

2.6% - 5.9%

6.0% - 11.9%

12.0% - 38.0%

Percentage of Initial Non-California TEL Group Balance

100.0%

Percentage of Initial California TEL Group Balance

Texas2 properties$22,273,16311.9% of TEL Group

Tennessee1 property$6,082,3703.2% of TEL Group

Connecticut1 property$5,255,5022.8% of TEL Group

Arizona1 property$4,909,9712.6% of TEL Group

Florida2 properties$11,588,0276.2% of TEL Group

Georgia2 properties$15,932,7738.5% of TEL Group

Washington2 properties$71,122,93938.0% of TEL Group

Utah2 properties$37,310,96919.9% of TEL Group

California6 properties$108,540,953100.0% of TEL Group

Kentucky1 property$12,716,3496.8% of TEL Group

Multifamily ML Certificates Series ML-05FRETE 2019-ML05 Trust

TABLE OF CONTENTS

Offering Circular SupplementPage

3

IMPORTANT NOTICE REGARDING THE CERTIFICATES................................................................................. 4IMPORTANT NOTICE ABOUT INFORMATION PRESENTED IN THIS OFFERING CIRCULAR

SUPPLEMENT ............................................................................................................................................. 4NOTICE TO RESIDENTS OF THE REPUBLIC OF KOREA .................................................................................. 4NOTICE TO RESIDENTS OF THE PEOPLE’S REPUBLIC OF CHINA ................................................................ 4NOTICE TO RESIDENTS OF JAPAN ...................................................................................................................... 5NOTICE TO RESIDENTS OF HONG KONG........................................................................................................... 5NOTICE TO RESIDENTS OF THE EUROPEAN ECONOMIC AREA................................................................... 6MIFID II PRODUCT GOVERNANCE ...................................................................................................................... 6NOTICE TO INVESTORS ......................................................................................................................................... 7SUMMARY OF OFFERING CIRCULAR SUPPLEMENT .................................................................................... 10RISK FACTORS ....................................................................................................................................................... 46CAPITALIZED TERMS USED IN THIS OFFERING CIRCULAR SUPPLEMENT............................................. 91FORWARD-LOOKING STATEMENTS................................................................................................................. 91DESCRIPTION OF THE ISSUING ENTITY .......................................................................................................... 92DESCRIPTION OF THE DEPOSITOR AND GUARANTOR ................................................................................ 93DESCRIPTION OF THE TELS AND UNDERLYING MORTGAGE LOANS...................................................... 97DESCRIPTION OF THE CERTIFICATES............................................................................................................ 137YIELD AND MATURITY CONSIDERATIONS .................................................................................................. 167THE POOLING AGREEMENT ............................................................................................................................. 173CERTAIN FEDERAL INCOME TAX CONSEQUENCES................................................................................... 228STATE AND OTHER TAX CONSIDERATIONS ................................................................................................ 229ERISA CONSIDERATIONS .................................................................................................................................. 229LEGAL INVESTMENT.......................................................................................................................................... 230USE OF PROCEEDS .............................................................................................................................................. 230PLAN OF DISTRIBUTION.................................................................................................................................... 230LEGAL MATTERS ................................................................................................................................................ 231RATINGS................................................................................................................................................................ 231GLOSSARY ............................................................................................................................................................ 233

Exhibits to Offering Circular Supplement

EXHIBIT A-1 — CERTAIN CHARACTERISTICS OF THE TELS, THE UNDERLYING MORTGAGE LOANS AND THE

RELATED MORTGAGED REAL PROPERTIES

EXHIBIT A-2 — CERTAIN INFORMATION REGARDING EACH TEL GROUP

EXHIBIT A-3 — DESCRIPTION OF THE LARGEST UNDERLYING MORTGAGE LOANS IN EACH TEL GROUP

EXHIBIT B — FORM OF CERTIFICATE ADMINISTRATOR’S STATEMENT TO CERTIFICATEHOLDERS

EXHIBIT C-1 — DEPOSITOR’S REPRESENTATIONS AND WARRANTIES

EXHIBIT C-2 — EXCEPTIONS TO DEPOSITOR’S REPRESENTATIONS AND WARRANTIES

EXHIBIT D — DECREMENT TABLES FOR THE OFFERED PRINCIPAL BALANCE CERTIFICATES

EXHIBIT E — PRICE/YIELD TABLES FOR THE CLASS X-CA AND X-US CERTIFICATES

EXHIBIT F-1 — FORM OF TRANSFEROR CERTIFICATE FOR CERTAIN TRANSFERS OF INTERESTS IN

RULE 144A GLOBAL CERTIFICATES OR DEFINITIVE CERTIFICATES

EXHIBIT F-2 — FORM OF TRANSFEREE CERTIFICATE FOR CERTAIN TRANSFERS OF INTERESTS IN

RULE 144A GLOBAL CERTIFICATES

EXHIBIT F-3 — FORM OF TRANSFEREE CERTIFICATE FOR CERTAIN TRANSFERS OF INTERESTS IN

DEFINITIVE CERTIFICATES

You should rely only on the information contained in this document or to which we have referred you.We have not authorized anyone to provide you with information that is different. This document may only beused where it is legal to sell these securities. The information in this document may only be accurate on thedate of this document.

4

IMPORTANT NOTICE REGARDING THE CERTIFICATES

NEITHER FREDDIE MAC NOR ANY OTHER PERSON INTENDS TO RETAIN A MATERIAL NETECONOMIC INTEREST IN THE SECURITIZATION CONSTITUTED BY THE ISSUANCE OF THECERTIFICATES IN A MANNER THAT WOULD CONSTITUTE A RETENTION OF A MATERIAL NETECONOMIC INTEREST FOR THE PURPOSE OF ARTICLE 6 OF REGULATION (EU) 2017/2402 (THE “EUSECURITIZATION REGULATION”) OR TO TAKE ANY OTHER ACTION THAT MAY BE REQUIRED BYINSTITUTIONAL INVESTORS (AS DEFINED IN THE EU SECURITIZATION REGULATION) FOR THEPURPOSES OF THEIR COMPLIANCE WITH THE DUE DILIGENCE REQUIREMENTS UNDER ARTICLE 5OF THE EU SECURITIZATION REGULATION. FOR ADDITIONAL INFORMATION IN THIS REGARD,SEE “RISK FACTORS—RISKS RELATED TO THE OFFERED CERTIFICATES—LEGAL ANDREGULATORY PROVISIONS AFFECTING INVESTORS COULD ADVERSELY AFFECT THE LIQUIDITYOF YOUR INVESTMENT” IN THIS OFFERING CIRCULAR SUPPLEMENT. IN ADDITION, NO PARTYWILL RETAIN RISK WITH RESPECT TO THIS TRANSACTION IN A FORM OR AN AMOUNT PURSUANTTO THE TERMS OF THE U.S. CREDIT RISK RETENTION RULE (12 C.F.R. PART 1234). SEE“DESCRIPTION OF THE DEPOSITOR AND GUARANTOR—CREDIT RISK RETENTION” IN THISOFFERING CIRCULAR SUPPLEMENT.

IMPORTANT NOTICE ABOUT INFORMATIONPRESENTED IN THIS OFFERING CIRCULAR SUPPLEMENT

THE PLACEMENT AGENTS DESCRIBED IN THIS OFFERING CIRCULAR SUPPLEMENT MAY FROMTIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENTBANKING BUSINESS FROM, ANY COMPANY NAMED IN THIS OFFERING CIRCULAR SUPPLEMENT.

THE PLACEMENT AGENTS AND/OR THEIR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIMEHAVE A LONG OR SHORT POSITION IN ANY SECURITY OR CONTRACT DISCUSSED IN THISOFFERING CIRCULAR SUPPLEMENT.

THE INFORMATION CONTAINED IN THIS OFFERING CIRCULAR SUPPLEMENT SUPERSEDESANY PREVIOUS SUCH INFORMATION DELIVERED TO ANY INVESTOR.

NOTICE TO RESIDENTS OF THE REPUBLIC OF KOREA

THIS OFFERING CIRCULAR SUPPLEMENT IS NOT, AND UNDER NO CIRCUMSTANCES IS TO BECONSTRUED AS, A PUBLIC OFFERING OF SECURITIES IN KOREA. NONE OF THE DEPOSITOR, ANYPLACEMENT AGENT OR ANY OF THEIR AGENTS MAKE ANY REPRESENTATION WITH RESPECT TOTHE ELIGIBILITY OF ANY RECIPIENTS OF THIS OFFERING CIRCULAR SUPPLEMENT TO ACQUIRETHE OFFERED CERTIFICATES UNDER THE LAWS OF KOREA, INCLUDING, BUT WITHOUTLIMITATION, THE FOREIGN EXCHANGE TRANSACTION LAW AND REGULATIONS THEREUNDER(THE “FETL”). THE OFFERED CERTIFICATES HAVE NOT BEEN REGISTERED WITH THE FINANCIALSERVICES COMMISSION OF KOREA FOR PUBLIC OFFERING IN KOREA, AND NONE OF THEOFFERED CERTIFICATES MAY BE OFFERED, SOLD OR DELIVERED, DIRECTLY OR INDIRECTLY, OROFFERED OR SOLD TO ANY PERSON FOR RE-OFFERING OR RESALE, DIRECTLY OR INDIRECTLY INKOREA OR TO ANY RESIDENT OF KOREA EXCEPT PURSUANT TO THE FINANCIAL INVESTMENTSERVICES AND CAPITAL MARKETS ACT AND THE DECREES AND REGULATIONS THEREUNDER(THE “FSCMA”), THE FETL AND ANY OTHER APPLICABLE LAWS, REGULATIONS AND MINISTERIALGUIDELINES IN KOREA.

NOTICE TO RESIDENTS OF THE PEOPLE’S REPUBLIC OF CHINA

THE OFFERED CERTIFICATES WILL NOT BE OFFERED OR SOLD IN THE PEOPLE’S REPUBLIC OFCHINA (EXCLUDING HONG KONG, MACAU AND TAIWAN, THE “PRC”) AS PART OF THE INITIAL

5

DISTRIBUTION OF THE OFFERED CERTIFICATES BUT MAY BE AVAILABLE FOR PURCHASE BYINVESTORS RESIDENT IN THE PRC FROM OUTSIDE THE PRC.

THIS OFFERING CIRCULAR SUPPLEMENT DOES NOT CONSTITUTE AN OFFER TO SELL OR THESOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN THE PRC TO ANY PERSON TO WHOM ITIS UNLAWFUL TO MAKE THE OFFER OR SOLICITATION IN THE PRC.

THE PRC DOES NOT REPRESENT THAT THIS OFFERING CIRCULAR SUPPLEMENT MAY BELAWFULLY DISTRIBUTED, OR THAT ANY OFFERED CERTIFICATES MAY BE LAWFULLY OFFERED,IN COMPLIANCE WITH ANY APPLICABLE REGISTRATION OR OTHER REQUIREMENTS IN THE PRC,OR PURSUANT TO AN EXEMPTION AVAILABLE THEREUNDER, OR ASSUME ANY RESPONSIBILITYFOR FACILITATING ANY SUCH DISTRIBUTION OR OFFERING. IN PARTICULAR, NO ACTION HASBEEN TAKEN BY THE PRC WHICH WOULD PERMIT A PUBLIC OFFERING OF ANY OFFEREDCERTIFICATES OR THE DISTRIBUTION OF THIS OFFERING CIRCULAR SUPPLEMENT IN THE PRC.ACCORDINGLY, THE OFFERED CERTIFICATES ARE NOT BEING OFFERED OR SOLD WITHIN THEPRC BY MEANS OF THIS OFFERING CIRCULAR SUPPLEMENT OR ANY OTHER DOCUMENT.NEITHER THIS OFFERING CIRCULAR SUPPLEMENT NOR ANY ADVERTISEMENT OR OTHEROFFERING MATERIAL MAY BE DISTRIBUTED OR PUBLISHED IN THE PRC, EXCEPT UNDERCIRCUMSTANCES THAT WILL RESULT IN COMPLIANCE WITH ANY APPLICABLE LAWS ANDREGULATIONS.

NOTICE TO RESIDENTS OF JAPAN

THE OFFERED CERTIFICATES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THEFINANCIAL INSTRUMENTS EXCHANGE ACT OF JAPAN (LAW NO. 25 OF 1948, AS AMENDED (THE“FIEL”)), AND EACH OF THE PLACEMENT AGENTS HAS AGREED THAT IT WILL NOT OFFER ORSELL ANY OFFERED CERTIFICATES, DIRECTLY OR INDIRECTLY, IN JAPAN OR TO, OR FOR THEBENEFIT OF, ANY JAPANESE PERSON, OR TO OTHERS FOR RE OFFERING OR RESALE, DIRECTLY ORINDIRECTLY, IN JAPAN OR TO ANY JAPANESE PERSON, EXCEPT PURSUANT TO AN EXEMPTIONFROM THE REGISTRATION REQUIREMENTS OF, AND OTHERWISE IN COMPLIANCE WITH, THE FIELAND ANY OTHER APPLICABLE LAWS AND REGULATIONS. FOR THE PURPOSES OF THISPARAGRAPH, “JAPANESE PERSON” SHALL MEAN ANY PERSON RESIDENT IN JAPAN, INCLUDINGANY CORPORATION OR OTHER ENTITY ORGANIZED UNDER THE LAWS AND REGULATIONS OFJAPAN.

NOTICE TO RESIDENTS OF HONG KONG

THE OFFERED CERTIFICATES ARE NOT BEING OFFERED OR SOLD AND WILL NOT BE OFFEREDOR SOLD IN HONG KONG, BY MEANS OF ANY DOCUMENT (EXCEPT FOR OFFERED CERTIFICATESWHICH ARE A “STRUCTURED PRODUCT” AS DEFINED IN THE SECURITIES AND FUTURESORDINANCE (CAP. 571) (THE “SFO”) OF HONG KONG) OTHER THAN (A) TO “PROFESSIONALINVESTORS” AS DEFINED IN THE SFO AND ANY RULES MADE UNDER THE SFO; OR (B) IN OTHERCIRCUMSTANCES WHICH DO NOT RESULT IN THE DOCUMENT BEING A “PROSPECTUS” ASDEFINED IN THE COMPANIES (WINDING UP AND MISCELLANEOUS PROVISIONS) ORDINANCE(CAP. 32) (THE “C(WUMP)O”) OF HONG KONG OR WHICH DO NOT CONSTITUTE AN OFFER TO THEPUBLIC WITHIN THE MEANING OF THE C(WUMP)O. NO ADVERTISEMENT, INVITATION ORDOCUMENT RELATING TO THE OFFERED CERTIFICATES HAS BEEN ISSUED OR WILL BE ISSUED,WHETHER IN HONG KONG OR ELSEWHERE, WHICH IS DIRECTED AT, OR THE CONTENTS OFWHICH ARE LIKELY TO BE ACCESSED OR READ BY, THE PUBLIC OF HONG KONG (EXCEPT IFPERMITTED TO DO SO UNDER THE SECURITIES LAWS OF HONG KONG) OTHER THAN WITHRESPECT TO OFFERED CERTIFICATES WHICH ARE OR ARE INTENDED TO BE DISPOSED OF ONLYTO PERSONS OUTSIDE HONG KONG OR ONLY TO “PROFESSIONAL INVESTORS” AS DEFINED INTHE SFO AND ANY RULES MADE UNDER THE SFO.

6

NOTICE TO RESIDENTS OF THE EUROPEAN ECONOMIC AREA

THIS OFFERING CIRCULAR SUPPLEMENT IS NOT A PROSPECTUS FOR THE PURPOSES OF THEPROSPECTUS DIRECTIVE 2003/71/EC (AS AMENDED OR SUPERSEDED, THE “PROSPECTUSDIRECTIVE”).

THE OFFERED CERTIFICATES ARE NOT INTENDED TO BE OFFERED, SOLD OR OTHERWISEMADE AVAILABLE TO AND SHOULD NOT BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLETO ANY RETAIL INVESTOR IN THE EUROPEAN ECONOMIC AREA (THE “EEA”). FOR THESEPURPOSES, A RETAIL INVESTOR MEANS A PERSON WHO IS ONE (OR MORE) OF THE FOLLOWING:

(I) A RETAIL CLIENT AS DEFINED IN POINT (11) OF ARTICLE 4(1) OF DIRECTIVE 2014/65/EU(AS AMENDED, “MIFID II”); OR

(II) A CUSTOMER WITHIN THE MEANING OF DIRECTIVE (EU) 2016/97, WHERE THATCUSTOMER WOULD NOT QUALIFY AS A PROFESSIONAL CLIENT AS DEFINED IN POINT(10) OF ARTICLE 4(1) OF MIFID II; OR

(III) NOT A QUALIFIED INVESTOR AS DEFINED IN THE PROSPECTUS DIRECTIVE.

CONSEQUENTLY, NO KEY INFORMATION DOCUMENT REQUIRED BY REGULATION (EU) NO1286/2014 (AS AMENDED, THE “PRIIPS REGULATION”) FOR OFFERING OR SELLING THE OFFEREDCERTIFICATES OR OTHERWISE MAKING THEM AVAILABLE TO RETAIL INVESTORS IN THE EEAHAS BEEN PREPARED AND THEREFORE OFFERING OR SELLING THE OFFERED CERTIFICATES OROTHERWISE MAKING THEM AVAILABLE TO ANY RETAIL INVESTOR IN THE EEA MAY BEUNLAWFUL UNDER THE PRIIPS REGULATION. FURTHERMORE, THIS OFFERING CIRCULARSUPPLEMENT HAS BEEN PREPARED ON THE BASIS THAT ANY OFFER OF OFFERED CERTIFICATESIN THE EEA WILL ONLY BE MADE TO A LEGAL ENTITY WHICH IS A QUALIFIED INVESTOR UNDERTHE PROSPECTUS DIRECTIVE. ACCORDINGLY, ANY PERSON MAKING OR INTENDING TO MAKE ANOFFER IN THE EEA OF THE OFFERED CERTIFICATES MAY ONLY DO SO WITH RESPECT TOQUALIFIED INVESTORS. NEITHER FREDDIE MAC NOR ANY PLACEMENT AGENT HAS AUTHORIZED,NOR DOES ANY OF THEM AUTHORIZE, THE MAKING OF ANY OFFER OF OFFERED CERTIFICATESOTHER THAN TO QUALIFIED INVESTORS.

MIFID II PRODUCT GOVERNANCE

ANY DISTRIBUTOR SUBJECT TO MIFID II THAT IS OFFERING, SELLING OR RECOMMENDINGTHE OFFERED CERTIFICATES IS RESPONSIBLE FOR UNDERTAKING ITS OWN TARGET MARKETASSESSMENT IN RESPECT OF THE OFFERED CERTIFICATES AND DETERMINING ITS OWNDISTRIBUTION CHANNELS FOR THE PURPOSES OF THE MIFID II PRODUCT GOVERNANCE RULESUNDER COMMISSION DELEGATED DIRECTIVE (EU) 2017/593 (AS AMENDED, THE “DELEGATEDDIRECTIVE”). NEITHER FREDDIE MAC NOR ANY PLACEMENT AGENT MAKES ANYREPRESENTATIONS OR WARRANTIES AS TO A DISTRIBUTOR’S COMPLIANCE WITH THEDELEGATED DIRECTIVE.

7

NOTICE TO INVESTORS

Because of the following deemed representations, warranties and covenants and the transfer restrictionsdescribed under “Description of the Certificates—Restrictions” in this offering circular supplement, purchasers areadvised to consult legal counsel prior to making any offer, resale, pledge or other transfer of the class X-CA andX-US certificates (the “Interest-Only Certificates”).

Each purchaser of the Interest-Only Certificates will be deemed to have represented, warranted and agreedas follows:

• The purchaser is either:

(i) a Qualified Institutional Buyer that—

(a) is acquiring Interest-Only Certificates for its own account or for the account ofanother Qualified Institutional Buyer, as the case may be, and

(b) is aware that the seller of the Interest-Only Certificates may be relying on theexemption from the provisions of Section 5 of the Securities Act provided byRule 144A; or

(ii) an institution that is an Institutional Accredited Investor.

• The purchaser understands that:

(i) the Interest-Only Certificates and the offer of the Interest-Only Certificates pursuant tothis offering circular supplement have not been registered under the Securities Act orregistered or qualified under any applicable state or foreign securities laws;

(ii) the Interest-Only Certificates are “restricted securities” within the meaning of Rule 144under the Securities Act;

(iii) any reoffer, resale, pledge or other transfer of the Interest-Only Certificates will besubject to various transfer restrictions described under “Description of the Certificates—Restrictions” in this offering circular supplement; and

(iv) the Interest-Only Certificates may not be reoffered, resold, pledged or otherwisetransferred in any particular jurisdiction except in accordance with all applicablesecurities laws of that jurisdiction.

• Either:

(i) The purchaser is not—

(a) a retirement plan or other employee benefit plan or arrangement subject toSection 406 of the Employee Retirement Income Security Act of 1974, asamended (“ERISA”), Section 4975 of the Internal Revenue Code of 1986, asamended (the “Code”), or any federal, state or local law which is to a materialextent similar to the foregoing provisions of ERISA or the Code (“Similar Law”),or

(b) directly or indirectly acquiring the Interest-Only Certificates on behalf of, asnamed fiduciary of, as trustee of, or with assets of any such plan or arrangement;or

(ii) the purchaser is a plan subject to Similar Law that is not a Benefit Plan Investor and itsacquisition and continued holding of the Interest-Only Certificates or interests in theInterest-Only Certificates will not constitute or result in a non-exempt violation ofSimilar Law.

8

• The purchaser understands that the Interest-Only Certificates will bear legends substantially to thefollowing effect, unless we determine otherwise in accordance with applicable law:

THIS CERTIFICATE HAS NOT BEEN AND WILL NOT BE REGISTERED ORQUALIFIED UNDER THE SECURITIES ACT OF 1933, AS AMENDED (THE“SECURITIES ACT”), OR THE SECURITIES LAWS OF ANY STATE OR OTHERJURISDICTION. ANY REOFFER, RESALE, PLEDGE OR OTHER TRANSFER OFTHIS CERTIFICATE OR ANY INTEREST HEREIN WITHOUT SUCHREGISTRATION OR QUALIFICATION MAY BE MADE ONLY IN ATRANSACTION WHICH DOES NOT REQUIRE SUCH REGISTRATION ORQUALIFICATION AND WHICH IS IN ACCORDANCE WITH THE PROVISIONSOF SECTION 5.02 OF THE POOLING AND SERVICING AGREEMENTREFERRED TO HEREIN.

THE HOLDER HEREOF, BY PURCHASING THIS CERTIFICATE, AGREESTHAT THIS CERTIFICATE MAY BE REOFFERED, RESOLD, PLEDGED OROTHERWISE TRANSFERRED ONLY (A)(1) PURSUANT TO RULE 144AUNDER THE SECURITIES ACT (“RULE 144A”) TO AN INSTITUTIONALINVESTOR THAT THE HOLDER REASONABLY BELIEVES IS A “QUALIFIEDINSTITUTIONAL BUYER” WITHIN THE MEANING OF RULE 144A, WHOMTHE HOLDER HAS INFORMED THAT THE REOFFER, RESALE, PLEDGE OROTHER TRANSFER IS BEING MADE IN RELIANCE ON RULE 144A OR (2) TOAN INSTITUTION THAT IS, OR ALL THE EQUITY OWNERS OF WHICH ARE,“ACCREDITED INVESTORS” AS SUCH TERM IS DEFINED IN RULE 501(a)(1),(2), (3) OR (7) OF REGULATION D UNDER THE SECURITIES ACT; AND (B) INACCORDANCE WITH ANY OTHER APPLICABLE SECURITIES LAWS OF ANYSTATE OF THE UNITED STATES OR OTHER JURISDICTION.

NO TRANSFER OF THIS CERTIFICATE OR ANY INTEREST HEREIN MAY BEMADE TO (A) ANY RETIREMENT PLAN OR OTHER EMPLOYEE BENEFITPLAN OR ARRANGEMENT THAT IS SUBJECT TO SECTION 406 OF THEEMPLOYEE RETIREMENT INCOME SECURITY ACT OF 1974, AS AMENDED(“ERISA”), SECTION 4975 OF THE INTERNAL REVENUE CODE OF 1986, ASAMENDED (THE “CODE”) OR ANY FEDERAL, STATE OR LOCAL LAWWHICH IS, TO A MATERIAL EXTENT, SIMILAR TO THE FOREGOINGPROVISIONS OF ERISA OR THE CODE, OR (B) ANY PERSON WHO ISDIRECTLY OR INDIRECTLY ACQUIRING THIS CERTIFICATE OR SUCHINTEREST HEREIN ON BEHALF OF, AS NAMED FIDUCIARY OF, ASTRUSTEE OF, OR WITH ASSETS OF, ANY SUCH RETIREMENT PLAN OROTHER EMPLOYEE BENEFIT PLAN OR ARRANGEMENT, EXCEPT INACCORDANCE WITH THE PROVISIONS OF SECTION 5.02 OF THE POOLINGAND SERVICING AGREEMENT REFERRED TO HEREIN.

• If the purchaser is acquiring an Interest-Only Certificate in reliance on its status as an InstitutionallyAccredited Investor then it will be required to hold the certificate in fully registered, certificated anddefinitive form, the purchaser will provide to the Certificate Administrator such information regardingpayment and notification instructions and such tax forms (including, to the extent appropriate, InternalRevenue Service Forms W-9, W-8BEN, W-8BEN-E, W-8ECI and W-8IMY) as the CertificateAdministrator may require.

We provide information to you about the offered certificates in this offering circular supplement, whichdescribes the specific terms of the offered certificates.

You should read this offering circular supplement in full to obtain material information concerning the offeredcertificates.

9

This offering circular supplement includes cross-references to sections in this offering circular supplementwhere you can find further related discussions. The Table of Contents in this offering circular supplement identifiesthe pages where these sections are located.

When deciding whether to invest in any of the offered certificates, you should only rely on the informationcontained in this offering circular supplement and the accompanying Offering Circular or as provided in“Description of the Depositor and Guarantor—Freddie Mac Conservatorship” and “Description of the Depositor andGuarantor—Litigation Involving the Depositor and Guarantor” in this offering circular supplement. We have notauthorized any dealer, salesman or other person to give any information or to make any representation that isdifferent. In addition, information in this offering circular supplement is current only as of the date on its cover. Bydelivery of this offering circular supplement, we are not offering to sell any securities, and are not soliciting an offerto buy any securities, in any state or other jurisdiction where the offer and sale is not permitted.

10

SUMMARY OF OFFERING CIRCULAR SUPPLEMENT

This summary highlights selected information from this offering circular supplement and does not contain all of theinformation that you need to consider in making your investment decision. To understand all of the terms of the offeredcertificates, you should carefully read this offering circular supplement and the accompanying Offering Circular in theirentirety prior to making an investment in any offered certificates, including the information set forth under “Risk Factors”in this offering circular supplement. This summary provides an overview of certain information to aid your understandingand is qualified by the full description presented in this offering circular supplement.

Transaction Overview

The offered certificates will be part of a series of multifamily mortgage pass-through certificates designated asthe Series ML-05 Multifamily ML Certificates. The certificates will consist of six classes, which comprise twogroups of certificates: the California Certificates and the Non-California Certificates. The table below identifies andspecifies various characteristics for those classes.

Class

Total InitialPrincipal Balance or

Notional Amount

Approximate %of Total Initial

CertificateGroup Principal

Balance

ApproximateInitial Credit

Support

Pass-ThroughRate

DescriptionInitial Pass-

Through Rate

AssumedWeighted

Average Life(Years)(1)(2)

AssumedPrincipal

Window(1)(3)

Assumed FinalDistribution

Date(1)(4)

California Certificates

Offered Certificates:

A-CA $ 97,686,000 89.999% 10.001% Fixed 3.35000% 12.41 1 – 176 November 25, 2033

X-CA $ 97,686,000 N/A N/A Variable IO 0.24776%(5) 12.41 N/A November 25, 2033

Non-Offered Certificates:

B-CA $ 10,854,953 10.001% 0.000% WAC 4.01776%(5) 14.66 176 – 176 November 25, 2033

Non-California Certificates

Offered Certificates:

A-US $ 168,472,000 90.000% 10.000% Fixed 3.40000% 12.64 1 – 202 January 25, 2036

X-US $ 168,472,000 N/A N/A Variable IO 0.47447%(5) 12.64 N/A January 25, 2036

Non-Offered Certificates:

B-US $ 18,720,062 10.000% 0.000% WAC 4.29447%(5) 16.93 202 – 209 August 25, 2036

(1) As to any given class of certificates shown in this table, the assumed weighted average life, the assumed principal window and the AssumedFinal Distribution Date have been calculated based on the applicable Modeling Assumptions, including, among other things, that—

(i) there are no voluntary or involuntary prepayments with respect to the TELs,

(ii) there are no delinquencies, modifications or losses with respect to the TELs,

(iii) there are no modifications, extensions, waivers or amendments affecting the monthly debt service or balloon payments on the TELs,and

(iv) the certificates are not redeemed prior to their Assumed Final Distribution Date pursuant to the clean-up call described under theheading “—The Offered Certificates—Optional Retirement” below.

(2) As to each class of the Principal Balance Certificates, the assumed weighted average life is the average amount of time in years between theassumed settlement date for the certificates and the payment of each dollar of principal on that class. As to the class X-CA and X-UScertificates, the assumed weighted average life is the average amount of time in years between the assumed settlement date for those classesand the application of each dollar to be applied in reduction of the notional amounts of those classes.

(3) As to each class of Principal Balance Certificates, the assumed principal window is the period during which holders of that class areexpected to receive distributions of principal.

(4) As to each class of Principal Balance Certificates, the Assumed Final Distribution Date is the distribution date on which the last distributionof principal and interest is assumed to be made on that class. As to the class X-CA and X-US certificates, the Assumed Final DistributionDate is the distribution date on which the last reduction to the notional amount is expected to occur.

(5) Approximate.

11

In reviewing the table above, please note that:

• Only the class A-CA, A-US, X-CA and X-US certificates are offered by this offering circular supplement.

• The class A-CA, A-US, B-CA and B-US certificates will have principal balances (collectively, the“Principal Balance Certificates”). All of the classes of certificates shown in the table will bear interest.

• The class A-CA, X-CA and B-CA certificates are referred to in this offering circular supplement as the“California Certificates”. The California Certificates will be entitled to distribution of amounts attributableto collections on the TELs secured by the underlying mortgage loans secured by the mortgage realproperties identified on Exhibit A-1 as “Costa Azul Senior Apartments,” “Sun Ridge Apartments,” “CopperSquare Apartments,” “College Park II,” “Casa Puleta” and “Pensione K Apartments” (collectively, the“California TEL Group”). The class A-CA and B-CA certificates are referred to in this offering circularsupplement as the “California Principal Balance Certificates”.

• The class A-US, X-US and B-US certificates are referred to in this offering circular supplement as the“Non-California Certificates”. The Non-California Certificates will be entitled to distribution of amountsattributable to collections on all of the TELs other than the California TEL Group (collectively, the “Non-California TEL Group”). The class A-US and B-US certificates are referred to in this offering circularsupplement as the “Non-California Principal Balance Certificates”.

• The California TEL Group and the Non-California TEL Group are each referred to in this offering circularsupplement as a “TEL Group”. All of the certificates comprising the California Certificates or the Non-California Certificates are sometimes referred to in this offering circular supplement as a “CertificateGroup”. The certificates comprising the California Certificates will not be entitled to any distribution offunds attributable to collections on the Non-California TEL Group. The Non-California Certificates willnot be entitled to any distributions of funds attributable to collections on the California TEL Group.

• The initial principal balance or notional amount of any class shown in the table may be larger or smallerdepending on, among other things, the actual initial balance of the applicable TEL Group. The initial TELGroup balance may be up to 5% more or less than the amount shown in the tables on pages 44 and 45,respectively, of this offering circular supplement.

• The initial balance of any TEL Group refers to the aggregate outstanding principal balance of the TELs insuch TEL Group as of the Cut-off Date, after application of all payments of principal due with respect tothe TELs in such TEL Group on or before those due dates, whether or not received.

• Each class of certificates shown in the table will bear interest and such interest will accrue based on theassumption that each year is 360 days long and consists of 12 months each consisting of 30 days (a“30/360 Basis”).

• Each class of certificates identified in the table as having a “Fixed” pass-through rate has a fixed pass-through rate that will remain constant at the initial pass-through rate shown for that class in that table.

• Each class of certificates identified in the table as having a “WAC” pass-through rate has a per annumpass-through rate equal to the applicable Weighted Average Net Mortgage Pass-Through Rate for therelated distribution date (provided, that in no event may such pass-through rate be less than zero).

• For purposes of calculating the accrual of interest as of any date of determination, the class X-CAcertificates will have a notional amount that is equal to the then outstanding principal balance of theclass A-CA certificates, and the class X-US certificates will have a notional amount that is equal to the thenoutstanding principal balance of the class A-US certificates.

• The per annum pass-through rate for the class X-CA and X-US certificates for any distribution date willequal a rate equal to the excess, if any, of (i) the applicable Weighted Average Net Mortgage Pass-ThroughRate for the related distribution date minus the applicable Guarantee Fee Rate, over (ii) the pass-through

12

rate in effect during such Interest Accrual Period for the class A-CA or A-US certificates, as applicable. Inno event may such pass-through rate be less than zero.

• “Net Mortgage Pass-Through Rate” means, with respect to any TEL (including any successor REO Loan)that accrues interest on a 30/360 Basis, for any distribution date, a per annum rate equal to the greater of(i) the Net Mortgage Interest Rate for such TEL and (ii) the Original Net Mortgage Interest Rate for suchTEL.

• “Net Mortgage Interest Rate” means, with respect to any TEL (including any successor REO Loan), therelated mortgage interest rate then in effect reduced by the sum of the annual rates at which the masterservicer surveillance fee (if any), the special servicer surveillance fee (if any), the master servicing fee, thesub-servicing fee, the certificate administrator fee, the trustee fee and the CREFC® Intellectual PropertyRoyalty License Fee are calculated.

• “Original Net Mortgage Interest Rate” means, with respect to any TEL (including any successor REOLoan), the Net Mortgage Interest Rate in effect for such TEL as of the Cut-off Date (or, in the case of anyTEL substituted in replacement of another TEL pursuant to or as contemplated by the Pooling Agreement,as of the date of substitution).

• “Weighted Average Net Mortgage Pass-Through Rate” means, with respect to each TEL Group and eachdistribution date, the weighted average of the respective Net Mortgage Pass-Through Rates with respect toall of the TELs in such TEL Group (or any successor REO Loans) for that distribution date, weighted onthe basis of their respective Stated Principal Balances immediately prior to that distribution date.

See “Description of the Certificates—Distributions—Calculation of Pass-Through Rates (California Certificates)”and “—Calculation of Pass-Through Rates (Non-California Certificates)” in this offering circular supplement.

The document that will govern the issuance of the certificates, the creation of the related issuing entity and theservicing and administration of the TELs and the related underlying mortgage loans will be a pooling and servicingagreement to be dated as of March 1, 2019 (the “Pooling Agreement”), among us, as depositor, master servicer andguarantor, KeyBank National Association, as special servicer, and U.S. Bank National Association, as trustee,certificate administrator and custodian.

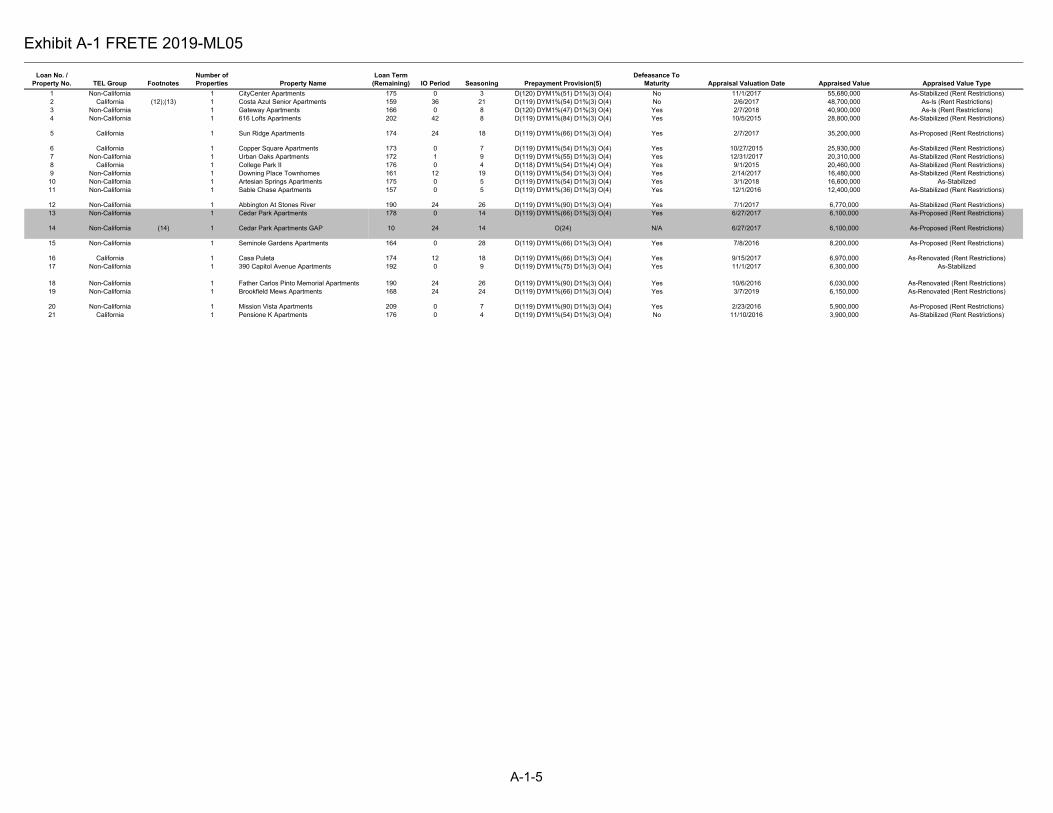

The certificates will evidence the entire beneficial ownership of the issuing entity that we intend to establish.The primary assets of that issuing entity will be a segregated pool of 21 loans (comprising two TEL Groups)intended to be tax-exempt loans, which we refer to herein as “TELs”. We did not originate the TELs, but havepurchased them from 10 sellers and servicers (the “Originators”). The TELs are funding loans made to various stateand local governmental entities (the “Governmental Authorities”), which used the TEL proceeds to make mortgageloans (such loans, the “underlying mortgage loans”) to multifamily developers and owners to finance the acquisitionand/or rehabilitation of 20 affordable multifamily housing properties identified on Exhibit A-1.

Each TEL, and the related underlying mortgage loan funded by such TEL, have identical payment terms. EachTEL is payable primarily from payments made by the related underlying borrower on the related underlyingmortgage loan without any recourse either to the related Governmental Authority, the related fiscal agent or therelated Originator for any failure of such underlying borrower to make required payments on such underlyingmortgage loan. The master servicer is the master servicer of all of the TELs and the related underlying mortgageloans. There are 10 sub-servicers of the TELs and the related underlying mortgage loans. The special servicer is thespecial servicer of the TELs, the underlying mortgage loans and the REO properties. Each underlying mortgageloan is pledged by the related Governmental Authority to the related fiscal agent, acting on behalf of the holder ofthe related TEL, as security for the payment of the related TEL. Because payments on, or in respect of, theunderlying mortgage loans are the sole source of payments on the TELs, this offering circular supplement describesthe underlying mortgage loans, the servicing of the underlying mortgage loans and other parties involved with theunderlying mortgage loans in addition to describing the TELs, the servicing of the TELs and various partiesinvolved with the TELs.

The underlying mortgage loans and therefore, the TELs, will provide for monthly debt service payments. As ofthe applicable due dates for the TELs and underlying mortgage loans in March 2019 (which will be March 1, 2019,

13

subject, in some cases, to a next succeeding business day convention), which we refer to in this offering circularsupplement as the “Cut-off Date,” the TELs and underlying mortgage loans will have the general characteristicsdiscussed under the heading “Description of the TELs and Underlying Mortgage Loans” in this offering circularsupplement.

14

Relevant Parties/Entities

Issuing Entity ........................................... FRETE 2019-ML05 Trust, a New York common law trust, will beformed on the Closing Date pursuant to the Pooling Agreement. See“Description of the Issuing Entity” in this offering circular supplement.

Depositor .................................................. Freddie Mac, a corporate instrumentality of the United States createdand existing under Title III of the Emergency Home Finance Act of1970, as amended (the “Freddie Mac Act”), or any successor to it, willcreate the issuing entity and transfer the TELs to it. Freddie Mac willalso act as the master servicer of the TELs and the related underlyingmortgage loans and guarantor of the offered certificates (in suchcapacity, the “Guarantor”). Freddie Mac maintains an office at8200 Jones Branch Drive, McLean, Virginia 22102. See “Descriptionof the Depositor and Guarantor” in this offering circular supplement.

Originators ............................................... Each TEL was originated by one of the Originators and was acquiredby the depositor. See “Description of the TELs and UnderlyingMortgage Loans—Significant Originators” in this offering circularsupplement for information regarding any Originator that hasoriginated a significant portion of the TELs pool. As of the ClosingDate, all of the underlying mortgage loans and TELs will be sub-serviced by various sub-servicers pursuant to sub-servicing agreementsbetween the master servicer and each of the sub-servicers (each, a“Sub-Servicing Agreement”). Subject to meeting certain requirements,each Originator has the right to, and may, appoint itself or its affiliateor a third party as the sub-servicer for any of the underlying mortgageloans and TELs it originated. See “The Pooling Agreement—Significant Sub-Servicers” and “—Summary of Significant Sub-Servicing Agreements” in this offering circular supplement forinformation regarding any sub-servicer that is sub-servicing asignificant portion of the TELs and underlying mortgage loans andinformation regarding the terms of the related Sub-ServicingAgreement. See Exhibit A-1 for the identity of the applicableOriginator for each underlying mortgage loan and TEL.

Fiscal Agents ............................................ A fiscal agent is a third-party financial institution appointed by theGovernmental Authority to take an assignment of and to administer theunderlying mortgage loan, which is the sole security for theGovernmental Authority’s obligations on the TEL. If a servicer hadnot been appointed for an underlying mortgage loan, the fiscal agentwould have been required to collect payments on the underlyingmortgage loan from the underlying borrower and remit those paymentsto the issuing entity, as the owner of the related TEL. Upon theoccurrence of an event of default with respect to any TEL or the relatedunderlying mortgage loan, pursuant to the related TEL loan agreement,the issuing entity’s representative, which will be the special servicer,may instruct the related fiscal agent to take any actions to protect andenforce the rights of the issuing entity and the fiscal agent, includingdeclaring the TEL immediately due and payable and commencingforeclosure proceedings on the related mortgaged real property, whichwill be performed by the special servicer on behalf of the fiscal agent.See Exhibit A-1 for the identity of the fiscal agent for each TEL andunderlying mortgage loan.

15

Master Servicer........................................ Freddie Mac will act as the master servicer with respect to the TELs(including the underlying mortgage loans). Freddie Mac is also thedepositor and the guarantor of the offered certificates. Freddie Macmaintains a servicing office at 8100 Jones Branch Drive, McLean,Virginia 22102.

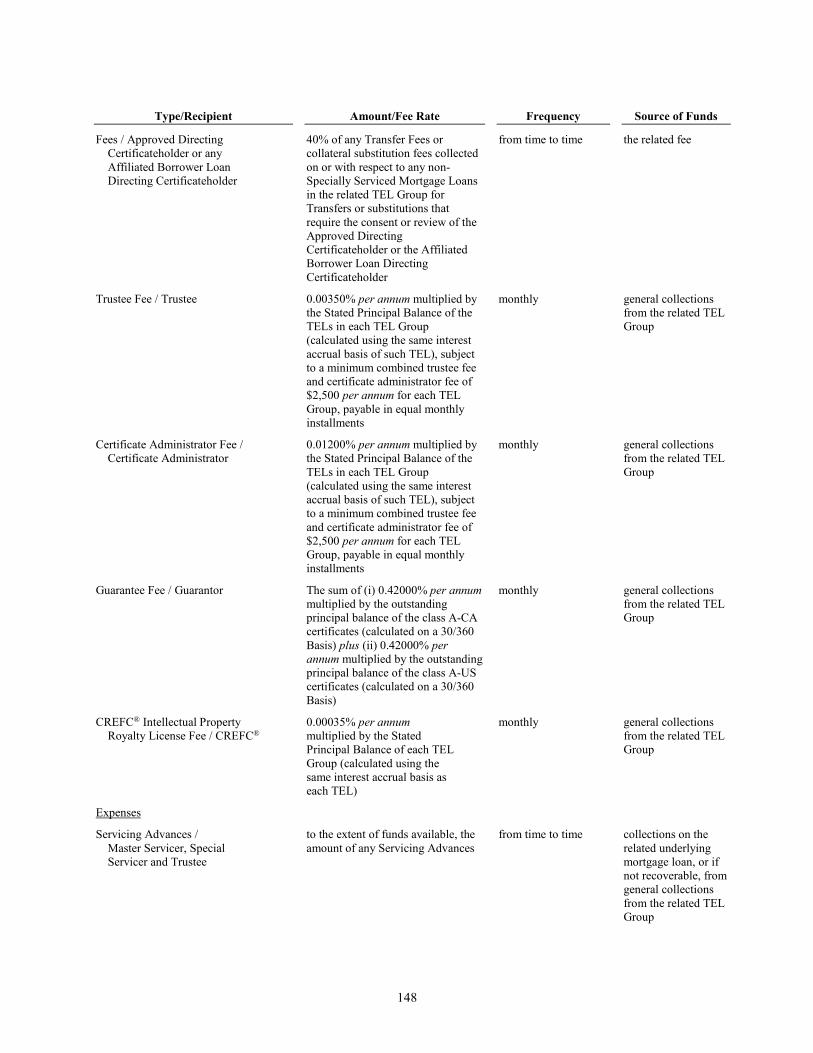

As consideration for servicing the TELs and the related underlyingmortgage loans, the master servicer will receive a master servicing feeand a sub-servicing fee with respect to each TEL and underlyingmortgage loan. The sub-servicing fee is then paid by the masterservicer to the applicable sub-servicer with respect to each TEL andunderlying mortgage loan.

In addition, the master servicer will receive a master servicersurveillance fee with respect to each Surveillance Fee Mortgage Loan,subject to the rights of the sub-servicers described in “The PoolingAgreement—Servicing and Other Compensation and Payment ofExpenses—The Servicing Fee” in this offering circular supplement.See “Description of the Certificates—Fees and Expenses” in thisoffering circular supplement for the applicable rates at which such feesaccrue and “The Pooling Agreement—Servicing and OtherCompensation and Payment of Expenses—The Servicing Fee” in thisoffering circular supplement for further information regarding suchfees.

The master servicing fee rate, the master servicer surveillance fee rateand the sub-servicing fee rate are components of the “AdministrationFee Rate” set forth on Exhibit A-1. Such fees are calculated on thesame basis as interest on each TEL and will be paid out of interestpayments received on the TELs prior to any distributions being madeon the offered certificates. The master servicer will also be entitled toadditional servicing compensation in the form of borrower-paid fees asmore particularly described in this offering circular supplement. See“The Pooling Agreement—Servicing and Other Compensationand Payment of Expenses—Additional Servicing Compensation” and“—The Master Servicer” in this offering circular supplement.

Special Servicer........................................ KeyBank National Association, a national banking association(“KeyBank”), is expected to act as the special servicer with respect tothe TELs and the related underlying mortgage loans. KeyBank alsomay, in certain circumstances, act as the Affiliated Borrower LoanDirecting Certificateholder with respect to underlying mortgage loansand TELs that are not Affiliated Borrower Special Servicer Loans andmay, if requested, act as the Directing Certificateholder ServicingConsultant. The principal commercial mortgage special servicingoffices of KeyBank are located at 11501 Outlook Street, Suite 300,Overland Park, Kansas 66211.

The special servicer will, in general, be responsible for servicing andadministering:

• underlying mortgage loans and TELs that, in general, are indefault or as to which default is reasonably foreseeable; and

• any real estate or other property acquired by the issuing entityupon foreclosure of a Defaulted TEL.

16

As consideration for servicing any underlying mortgage loan and TELif it is being specially serviced and the related underlying mortgageloans if the related mortgaged real property or REO Property hasbecome subject to a foreclosure proceeding, the special servicer willreceive a special servicing fee. In addition, the special servicer willreceive a special servicer surveillance fee with respect to eachSurveillance Fee Mortgage Loan. The special servicer surveillance feerate is a component of the “Administration Fee Rate” set forth onExhibit A-1. Such fees will be calculated on the same basis as intereston the TELs and will generally be payable to the special servicermonthly from collections on the TELs. Additionally, the specialservicer will, in general, be entitled to receive a workout fee withrespect to the TEL and underlying mortgage loan if it becomes aSpecially Serviced Mortgage Loan that has been returned to performingstatus. The special servicer will also be entitled to receive a liquidationfee with respect to each TEL and the related underlying mortgage loanif it becomes a Specially Serviced Mortgage Loan for which it obtains afull, partial or discounted payoff or otherwise recovers LiquidationProceeds. However, no liquidation fee is payable in connection withcertain purchases by the applicable directing certificateholder, thedepositor or the special servicer. See “Description of the Certificates—Fees and Expenses” in this offering circular supplement for theapplicable rates at which such fees accrue and “The PoolingAgreement—Servicing and Other Compensation and Payment ofExpenses—Principal Special Servicing Compensation” in this offeringcircular supplement for further information regarding such fees.

The special servicer may be terminated by the applicable directingcertificateholder with respect to the related TEL Group, who mayappoint a successor special servicer with respect to such TEL Groupmeeting the Successor Servicer Requirements, including Freddie Mac’sapproval, which approval may not be unreasonably withheld ordelayed. See “The Pooling Agreement—Resignation, Removal andReplacement of Servicers; Transfer of Servicing Duties” and “—TheSpecial Servicer” in this offering circular supplement.

Fees payable to the master servicer and special servicer are paid onlywith respect to the combination of the related TEL and the underlyingmortgage loan pursuant to the Pooling Agreement. No separate fee ispayable with respect to both a TEL and the related underlying mortgageloan for services provided.

The Pooling Agreement provides that in certain circumstances theApproved Directing Certificateholder (if any) may, at its own expense,request that a person (which may be the special servicer) (in suchcapacity, the “Directing Certificateholder Servicing Consultant”)prepare and deliver a recommendation relating to a requested waiver ofa “due-on-sale” or “due-on-encumbrance” clause or, with respect tonon-Specially Serviced Mortgage Loans, a requested consent to certainmajor decisions affecting the TELs, the underlying mortgage loans orrelated mortgaged real properties. See “The Pooling Agreement—Enforcement of “Due-on-Sale” and “Due-on-Encumbrance” Clauses”and “—Modifications, Waivers, Amendments and Consents” in thisoffering circular supplement.

17

Trustee, Certificate Administratorand Custodian....................................... U.S. Bank National Association, a national banking association (“U.S.

Bank”), will act as the trustee on behalf of the certificateholders. Thetrustee’s principal address is One Federal Street, 3rd Floor, Mail CodeEX-MA-FED, Boston, Massachusetts 02110. As consideration foracting as trustee, U.S. Bank will receive a trustee fee. The trustee feerate is a component of the “Administration Fee Rate” set forth onExhibit A-1. Such fee will be calculated on the same basis as intereston the TELs. See “Description of the Certificates—Fees andExpenses” in this offering circular supplement for the applicable rate atwhich such fee accrues and “The Pooling Agreement—MattersRegarding the Trustee, the Certificate Administrator and theCustodian” in this offering circular supplement for further informationregarding such fee.

U.S. Bank will also act as the certificate administrator, the custodianand the certificate registrar. The certificate administrator’s principaladdress is One Federal Street, 3rd Floor, Mail Code EX-MA-FED,Boston, Massachusetts 02110 (and for certificate transfer purposes,111 Fillmore Avenue, St. Paul, Minnesota 55107, Attention:Bondholder Services - FRETE 2019-ML05), and it has a custodialoffice at 60 Livingston Ave., Suite 800, St. Paul, Minnesota 55107,Attention: FRETE 2019-ML05. As consideration for acting ascertificate administrator, custodian and certificate registrar, U.S. Bankwill receive a certificate administrator fee. The certificateadministrator fee rate is a component of the “Administration Fee Rate”set forth on Exhibit A-1. Such fee will be calculated on the same basisas interest on the TELs. See “Description of the Certificates—Fees andExpenses” in this offering circular supplement for the applicable rate atwhich such fee accrues, “The Pooling Agreement—Matters Regardingthe Trustee, the Certificate Administrator and the Custodian” in thisoffering circular supplement for further information regarding such fee,and “The Pooling Agreement—The Trustee, Certificate Administratorand Custodian” in this offering circular supplement for furtherinformation about the trustee, the certificate administrator and thecustodian.

18

Parties ....................................................... The following diagram illustrates the various parties involved in thetransaction and their functions.

Directing Certificateholders ................... There will be two directing certificateholders under the PoolingAgreement. Each Certificate Group will have a correspondingdirecting certificateholder and a corresponding Controlling ClassMajority Holder. For more information regarding the identity andselection of the applicable directing certificateholder and the procedurefor a Controlling Class Majority Holder becoming or designating anApproved Directing Certificateholder, see “The Pooling Agreement—Realization Upon Mortgage Loans—Directing Certificateholders” inthis offering circular supplement. For purposes of this offering circularsupplement, the “directing certificateholder,” “Approved DirectingCertificateholder” or “Controlling Class Majority Holder” means, asapplicable, the directing certificateholder, Approved DirectingCertificateholder or Controlling Class Majority Holder with respect tothe applicable Certificate Group, as provided below. The applicabledirecting certificateholder, Approved Directing Certificateholder orControlling Class Majority Holder will only have rights with respect todecisions involving solely the underlying mortgage loans and the TELsin the related TEL Group or solely the related Certificate Group or asotherwise set forth in the Pooling Agreement.

As and to the extent described under “The Pooling Agreement—Realization Upon Mortgage Loans—Asset Status Report” in thisoffering circular supplement, the Approved Directing Certificateholder(if any) may direct the master servicer or the special servicer withrespect to various servicing matters involving each of the underlyingmortgage loans in the related TEL Group. Any applicable directingcertificateholder that is not an Approved Directing Certificateholderwill not have such rights with respect to such servicing matters, but willbe entitled to exercise the Controlling Class Majority Holder Rightsdescribed in this offering circular supplement with respect to each ofthe TELs in the related TEL Group. Upon the occurrence and during

Bellwether Enterprise Real Estate Capital, LLC, Berkadia Commercial Mortgage LLC,CBRE Capital Markets, Inc., Citibank, N.A., Greystone Servicing Corporation, Inc.,Hunt Mortgage Partners, LLC, Jones Lang LaSalle Multifamily, LLC, NorthMarq

Capital, LLC, PNC Bank, National Association and Prudential Affordable MortgageCompany, LLC(Originators)

Freddie Mac(Depositor and Guarantor of the

offered certificates)

FRETE 2019-ML05 Trust(Issuing Entity)

U.S. Bank National Association(Certificate Administrator and Custodian)

U.S. Bank National Association(Trustee)

KeyBank National Association(Special Servicer)

Various(Sub-Servicers)

Freddie Mac(Master Servicer)

19

the continuance of any Affiliated Borrower Loan Event with respect toany underlying mortgage loan, any right of the applicable directingcertificateholder to (i) approve and consent to certain actions withrespect to such underlying mortgage loan, (ii) exercise an option topurchase any Defaulted TELs from the issuing entity and (iii) accesscertain information and reports regarding such underlyingmortgage loan will be restricted as described in “The PoolingAgreement—Realization Upon Mortgage Loans—Asset Status Report”and “—Purchase Option,” as applicable, in this offering circularsupplement. Upon the occurrence and during the continuance of anAffiliated Borrower Loan Event, the special servicer, as the AffiliatedBorrower Loan Directing Certificateholder, will be required to exerciseany approval, consent, consultation or other rights with respect to anymatters related to an Affiliated Borrower Loan as described in “ThePooling Agreement—Realization Upon Mortgage Loans—Asset StatusReport” in this offering circular supplement.

As of the Closing Date, no Affiliated Borrower Loan Event is expectedto exist with respect to (i) all of the TELs in the California TEL Groupand the Initial California Directing Certificateholder and (ii) all of theTELs in the Non-California TEL Group and the Initial Non-CaliforniaDirecting Certificateholder.

Directing Certificateholder(California TEL Group)................... The “directing certificateholder” with respect to the California

Certificates will be the Controlling Class Majority Holder with respectto the California Certificates or its designee; provided that if the classA-CA certificates are the Controlling Class with respect to theCalifornia Certificates, Freddie Mac, or its designee will act as thedirecting certificateholder with respect to the California Certificatesand be deemed an Approved Directing Certificateholder with respect tothe California Certificates. It is anticipated that PAC ML05, LLC, aDelaware limited liability company and an affiliate of PreferredApartment Communities Operating Partnership, LP, will be designatedto serve as the initial directing certificateholder with respect to theCalifornia Certificates (the “Initial California DirectingCertificateholder”).

With respect to the California TEL Pool, the Pooling Agreementprovides that in certain circumstances the Approved DirectingCertificateholder (if any) may, at its own expense, request that theDirecting Certificateholder Servicing Consultant prepare and deliver arecommendation relating to a requested waiver of any “due-on-sale” or“due-on-encumbrance” clause or, with respect to non-SpeciallyServiced Mortgage Loans, a requested consent to certain majordecisions affecting the TELs, the underlying mortgage loans or relatedmortgaged real properties with respect to the California TEL Group.See “The Pooling Agreement—Enforcement of “Due-on-Sale” and“Due-on-Encumbrance” Clauses” and “—Modifications, Waivers,Amendments and Consents” in this offering circular supplement. TheApproved Directing Certificateholder (if any) will be entitled to certainborrower-paid fees in connection with such assumptions, modifications,waivers, amendments or consents. See “Description of theCertificates—Fees and Expenses” in this offering circular supplement.

20

Directing Certificateholder(Non-California TEL Group) .......... The “directing certificateholder” with respect to the Non-California

Certificates will be the Controlling Class Majority Holder with respectto the Non-California Certificates or its designee; provided that if theclass A-US certificates are the Controlling Class with respect to theNon-California Certificates, Freddie Mac, or its designee will act as thedirecting certificateholder with respect to the Non-CaliforniaCertificates and be deemed an Approved Directing Certificateholderwith respect to the Non-California Certificates. It is anticipated thatPAC ML05, LLC, a Delaware limited liability company and an affiliateof Preferred Apartment Communities Operating Partnership, LP, willbe designated to serve as the initial directing certificateholder withrespect to the Non-California Certificates (the “Initial Non-CaliforniaDirecting Certificateholder”).

With respect to the Non-California TEL Pool, the Pooling Agreementprovides that in certain circumstances the Approved DirectingCertificateholder (if any) may, at its own expense, request that theDirecting Certificateholder Servicing Consultant prepare and deliver arecommendation relating to a requested waiver of any “due-on-sale” or“due-on-encumbrance” clause or, with respect to non-SpeciallyServiced Mortgage Loans, a requested consent to certain majordecisions affecting the TELs, the underlying mortgage loans or relatedmortgaged real properties with respect to the Non-California TELGroup. See “The Pooling Agreement—Enforcement of “Due-on-Sale”and “Due-on-Encumbrance” Clauses” and “—Modifications, Waivers,Amendments and Consents” in this offering circular supplement. TheApproved Directing Certificateholder (if any) will be entitled to certainborrower-paid fees in connection with such assumptions, modifications,waivers, amendments or consents. See “Description of theCertificates—Fees and Expenses” in this offering circular supplement.

Guarantor................................................. Freddie Mac will act as Guarantor of the class A-CA, A-US, X-CA andX-US certificates offered by this offering circular supplement. FreddieMac is entitled to a Guarantee Fee as described under “Description ofthe Certificates—Distributions—Freddie Mac Guarantee” in thisoffering circular supplement. For a discussion of the Freddie MacGuarantee, see “—The Offered Certificates—Freddie Mac Guarantee”below and “Description of the Depositor and Guarantor—ProposedOperation of Multifamily Mortgage Business on a Stand-Alone Basis”in this offering circular supplement.

Significant Dates and Periods

Cut-off Date.............................................. The TELs will be considered assets of the issuing entity as of theirapplicable due dates in March 2019 (which will be March 1, 2019,subject, in some cases, to a next succeeding business day convention).All payments and collections received on each of the TELs after theCut-off Date, excluding any payments or collections that representamounts due on or before the Cut-off Date, will belong to the issuingentity.

Closing Date ............................................. The date of initial issuance for the certificates will be on or aboutMarch 28, 2019.

21

Due Dates.................................................. Subject, in some cases, to a next succeeding business day convention,monthly installments of principal and/or interest will be due on the firstday of the month with respect to each of the TELs.

Determination Date ................................. The monthly cut-off for collections on the TELs that are to bedistributed, and information regarding the TELs that is to be reported,to the holders of the certificates on any distribution date will be theclose of business on the determination date in the same month as thatdistribution date. The determination date will be the 11th calendar dayof each month, commencing in April 2019, or, if the 11th calendar dayof any such month is not a Business Day, then the next succeedingBusiness Day.

Distribution Date ..................................... Distributions of principal and/or interest on the certificates arescheduled to occur monthly, commencing in April 2019. Thedistribution date will be the 25th calendar day of each month, or, if the25th calendar day of any such month is not a Business Day, then thenext succeeding Business Day.

Record Date.............................................. The record date for each monthly distribution on a certificate will bethe last Business Day of the prior calendar month. The registeredholders of the certificates at the close of business on each record datewill be entitled to receive any distribution on those certificates on thefollowing distribution date, except that the final distribution on anyoffered certificate will be made only upon presentation and surrender ofthat certificate at a designated location.

Collection Period...................................... Amounts available for distribution on the certificates of eitherCertificate Group on any distribution date will depend on the paymentsand other collections received, and any advances of payments due, onor with respect to the TELs in the related TEL Group during the relatedCollection Period. Each Collection Period—

• will relate to a particular distribution date;

• will begin when the prior Collection Period ends or, in thecase of the first Collection Period, will begin on the Cut-offDate; and

• will end at the close of business on the determination date thatoccurs in the same month as the related distribution date.

Interest Accrual Period ........................... The amount of interest payable with respect to the interest-bearingclasses of certificates on any distribution date will be a function of theinterest accrued during the related “Interest Accrual Period”, which forany distribution date will be the calendar month immediately precedingthe month in which that distribution date occurs and will be deemed toconsist of 30 days.

Assumed Final Distribution Date ........... For each class of offered certificates, the applicable date set forth on thecover page.

22

The Offered Certificates

General ..................................................... The certificates offered by this offering circular supplement are theclass A-CA, A-US, X-CA and X-US certificates. Each class of offeredcertificates will have the initial principal balance or notional amountand pass-through rate set forth or described in the table on page 10 orotherwise described above under “—Transaction Overview”. There areno other securities offered by this offering circular supplement.

Certificate Groups ................................... The certificates will be divided into two Certificate Groups: theCalifornia Certificates (backed by the California TEL Group) and theNon-California Certificates (backed by the Non-California TELGroup). Each Certificate Group will be entitled to distributions ofamounts attributable to collections on the TELs in the related TELGroup and will not be entitled to any distributions of funds attributableto collections on the TELs in any other TEL Group.

Collections ................................................ The master servicer or the special servicer, as applicable, will berequired to make reasonable efforts in accordance with the ServicingStandard to collect all payments due under the terms and provisions ofthe TELs and underlying mortgage loans. Underlying borrowers on theunderlying mortgage loans make debt service payments to the relatedsub-servicer, or if a servicer had not been appointed with respect to anunderlying mortgage loan, to the fiscal agent, which, in turn, wouldforward such payments to the master servicer. Such payments will bedeposited in the collection account on a daily basis.

Distributions............................................. Funds collected or advanced on each TEL Group will be distributed oneach corresponding distribution date to the holders of certificates in therelated Certificate Group, in each case, net of (i) specified issuing entityexpenses, including master servicing fees, special servicing fees,sub-servicing fees, master servicer surveillance fees, special servicersurveillance fees, certificate administrator fees, trustee fees, GuaranteeFees, CREFC® Intellectual Property Royalty License Fees, certainexpenses, related compensation and indemnities in respect of thecorresponding TEL Group or Certificate Group, (ii) amounts used toreimburse advances made by the master servicer, the special servicer orthe trustee in respect of the corresponding TEL Group or CertificateGroup and (iii) amounts used to reimburse Balloon GuarantorPayments or interest on such amounts in respect of the correspondingTEL Group or Certificate Group.

Subordination .......................................... The charts below under “—Priority of Distributions (CaliforniaCertificates)” and “—Priority of Distributions (Non-CaliforniaCertificates)” describe the manner in which the rights of various classeswill be senior to the rights of other classes in each applicableCertificate Group. Entitlement to receive principal and interest on anydistribution date is depicted in descending order. The manner in whichTEL losses are allocated is depicted in ascending order.

23

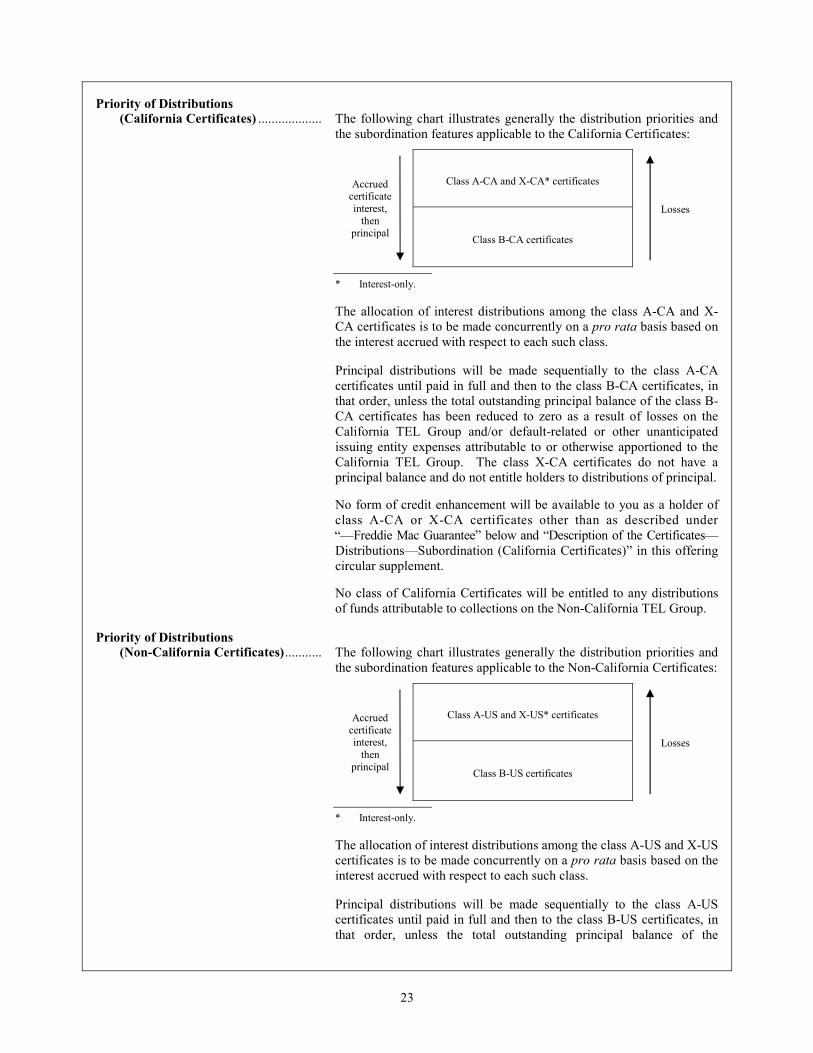

Priority of Distributions(California Certificates) ................... The following chart illustrates generally the distribution priorities and

the subordination features applicable to the California Certificates:

Accruedcertificateinterest,

thenprincipal

Class A-CA and X-CA* certificates

Losses

Class B-CA certificates

* Interest-only.

The allocation of interest distributions among the class A-CA and X-CA certificates is to be made concurrently on a pro rata basis based onthe interest accrued with respect to each such class.

Principal distributions will be made sequentially to the class A-CAcertificates until paid in full and then to the class B-CA certificates, inthat order, unless the total outstanding principal balance of the class B-CA certificates has been reduced to zero as a result of losses on theCalifornia TEL Group and/or default-related or other unanticipatedissuing entity expenses attributable to or otherwise apportioned to theCalifornia TEL Group. The class X-CA certificates do not have aprincipal balance and do not entitle holders to distributions of principal.

No form of credit enhancement will be available to you as a holder ofclass A-CA or X-CA certificates other than as described under

Freddie Mac Guarantee” below and “Description of the Certificates—Distributions—Subordination (California Certificates)” in this offeringcircular supplement.

No class of California Certificates will be entitled to any distributionsof funds attributable to collections on the Non-California TEL Group.

Priority of Distributions(Non-California Certificates)........... The following chart illustrates generally the distribution priorities and

the subordination features applicable to the Non-California Certificates:

Accruedcertificateinterest,

thenprincipal

Class A-US and X-US* certificates

Losses

Class B-US certificates

* Interest-only.

The allocation of interest distributions among the class A-US and X-UScertificates is to be made concurrently on a pro rata basis based on theinterest accrued with respect to each such class.

Principal distributions will be made sequentially to the class A-UScertificates until paid in full and then to the class B-US certificates, inthat order, unless the total outstanding principal balance of the

“—

24

class B-US certificates has been reduced to zero as a result of losses onthe Non-California TEL Group and/or default-related or otherunanticipated issuing entity expenses attributable to or otherwiseapportioned to the Non-California TEL Group. The class X-UScertificates do not have a principal balance and do not entitle holders todistributions of principal.

No form of credit enhancement will be available to you as a holder ofclass A-US or X-US certificates other than as described under Freddie Mac Guarantee” below and “Description of the Certificates—Distributions—Subordination (Non-California Certificates)” in thisoffering circular supplement.

No class of Non-California Certificates will be entitled to anydistributions of funds attributable to collections on the California TELGroup.