2017 INVESTOR & ANALYST DAY December 14, 2017 partners, uncertainties relating to collaboration...

110

2017 INVESTOR & ANALYST DAY December 14, 2017

Transcript of 2017 INVESTOR & ANALYST DAY December 14, 2017 partners, uncertainties relating to collaboration...

2017 INVESTOR & ANALYST DAY

December 14, 2017

Forward Looking StatementsStatements in this presentation that are not strictly historical, including any statements regarding events or developments that we believe or anticipate will or may occur in the future are

"forward-looking" statements within the meaning of the federal securities laws. There are a number of important factors that could cause actual results, developments and business

decisions to differ materially from those suggested or indicated by such forward-looking statements and you should not place undue reliance on any such forward-looking statements.

These factors include, among other things, deterioration of or instability in the economy, the markets we serve and the financial markets, contractions or growth rates and cyclicality of

markets we serve, competition, our ability to develop and successfully market new products and technologies and expand into new markets, the potential for improper conduct by our

employees, agents or business partners, our compliance with applicable laws and regulations (including regulations relating to medical devices and the health care industry), our ability to

effectively address cost reductions and other changes in the health care industry, our ability to successfully identify, consummate and integrate appropriate acquisitions and successfully

complete divestitures and other dispositions, our ability to integrate the recent acquisitions of Pall Corporation and Cepheid and achieve the anticipated benefits of such transactions,

contingent liabilities relating to acquisitions and divestitures (including tax-related and other contingent liabilities relating to the distributions of each of Fortive Corporation and our

communications business), security breaches or other disruptions of our information technology systems or violations of data privacy laws, the impact of our restructuring activities on

our ability to grow, risks relating to potential impairment of goodwill and other intangible assets, currency exchange rates, tax audits and changes in our tax rate and income tax liabilities,

changes in tax laws applicable to multinational companies, litigation and other contingent liabilities including intellectual property and environmental, health and safety matters, the rights

of the United States government to use, disclose and license certain intellectual property we license if we fail to commercialize it, risks relating to product, service or software defects,

product liability and recalls, risks relating to product manufacturing, the impact of our debt obligations on our operations and liquidity, our relationships with and the performance of our

channel partners, uncertainties relating to collaboration arrangements with third parties, commodity costs and surcharges, our ability to adjust purchases and manufacturing capacity to

reflect market conditions, reliance on sole sources of supply, the impact of deregulation on demand for our products and services, labor matters, international economic, political, legal,

compliance and business factors (including the impact of the UK's decision to leave the EU), disruptions relating to man-made and natural disasters, and pension plan costs. Additional

information regarding the factors that may cause actual results to differ materially from these forward-looking statements is available in our SEC filings, including our 2016 Annual Report

on Form 10-K and Quarterly Report on Form 10-Q for the third quarter of 2017. These forward-looking statements speak only as of the date of this presentation and except to the extent

required by applicable law, the Company does not assume any obligation to update or revise any forward-looking statement, whether as a result of new information, future events and

developments or otherwise.

With respect to the non-GAAP financial measures referenced in the following presentation, the accompanying information required by SEC Regulation G can be found in the back of the

presentation and in the “Investors” section of Danaher’s web site, www.danaher.com, under the heading “Events & Presentations,” and event name “Danaher 2017 Investor & Analyst

Meeting.” All references in this presentation (1) to company-specific financial metrics relate only to the continuing operations of Danaher’s business, unless otherwise noted; (2) to

“growth” or other period-to-period changes refer to year-over-year comparisons unless otherwise indicated; (3) to Operating Profit below the segment level exclude amortization; and (4)

to “today” refers to the Company’s estimated 2017 performance (“2017E”). This presentation treats 2017E as the Company’s most recent fiscal year unless otherwise indicated. We may

also describe certain products and devices which have applications submitted and pending for certain regulatory approvals.

Agenda9:30 am Welcome Matt Gugino

9:35 am Opening Remarks Tom Joyce

10:05 am Danaher Business System

Life Sciences

Dental

Q&A

Melissa Aquino

Rainer Blair

Amir Aghdaei

Aquino, Blair, Aghdaei

11:05 am Break

11:30 am Environmental & Applied Solutions (EAS)

Product Identification

Water Quality

Diagnostics

Q&A

Joakim Weidemanis

Lance Reisman

Dan Daniel

Weidemanis, Reisman, Daniel

12:30 pm Closing Remarks & Guidance Tom Joyce

12:40 pm Q&A Tom Joyce

12:55 pm Program End / Lunch

OPENING REMARKS

Tom Joyce, President & CEO

2017 INVESTOR & ANALYST DAY

Balanced approach to deliver long-term value to shareholders

Building and evolving into a stronger, better Danaher

What You’ll Hear Today

Focused execution around our strategic priorities

2017 Financial Highlights

DOUBLE-DIGIT FREE CASH FLOW & ADJUSTED EPS GROWTH

• Expect FCF to exceed Net Income for 26th consecutive year

EXPANDING MARGINS WHILE REINVESTING FOR GROWTH

• Core OMX +60bps, R&D/S&M up (as a % of sales)

RECENT ACQUISITIONS OFF TO A GREAT START

• Cepheid, Pall, Nobel all performing well

• Closed 9 deals for ~$300M of acquisition spend

2017 Financial Highlights

ACCELERATING CORE GROWTH

• Led by Life Sciences & Product ID platforms

Building momentum as we head into 2018All financial metrics refer to the 9 months ending Sep.

29, 2017 unless otherwise indicated

Balanced approach to deliver long-term value to shareholders

Building and evolving into a stronger, better Danaher

What You’ll Hear Today

Focused execution around our strategic priorities

2017 Financial Highlights

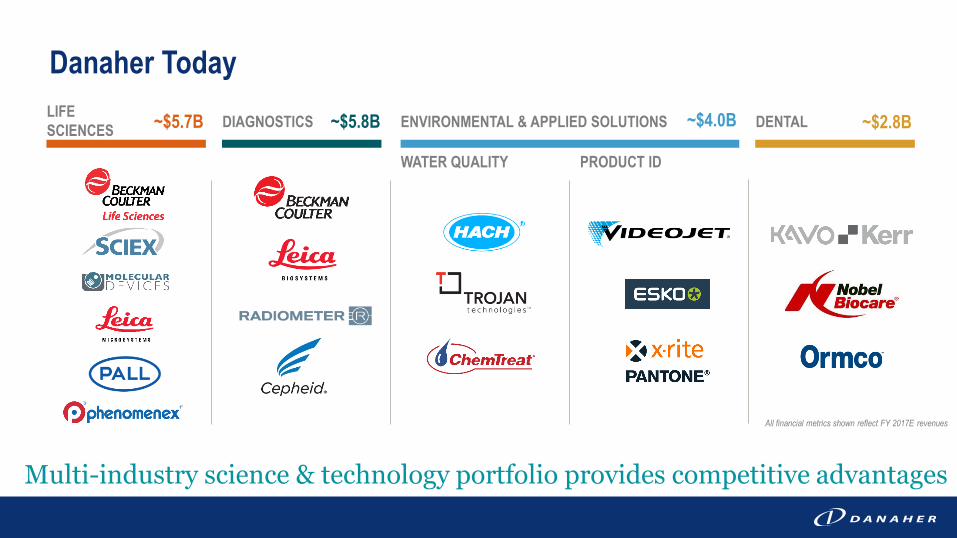

LIFE

SCIENCESDIAGNOSTICS DENTAL

WATER QUALITY

ENVIRONMENTAL & APPLIED SOLUTIONS

All financial metrics shown reflect FY 2017E revenues

PRODUCT ID

~$5.7B ~$5.8B ~$2.8B ~$4.0B

Danaher Today

Multi-industry science & technology portfolio provides competitive advantages

1984 1991 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

KEY ACQUISITIONS & PORTFOLIO MOVES

TOOLS JV

Evolution of Danaher

Significant portfolio transformation creates significant opportunity

>50%OF DANAHER TOTAL

REVENUE TODAY

~$90M REVENUE

~20% GROSS MARGIN

-- CONSUMABLES REV.

-- HGM REVENUE

~$18B REVENUE

~55% GROSS MARGIN

~65% CONSUMABLES REV.

~30% HGM

~$4B REVENUE

<40% GROSS MARGIN

<15% CONSUMABLES REV.

<10% HGM REVENUE

1984

2000

Tod

ay

Founded by

Steve & Mitch Rales OPCOS AQUIRED SINCE

2011 REPRESENT

SPINCOMMS RMT

~$18B

Shaded area represents 2017E revenue for each OpCo

~$9B

ROW

6%NA

40%

EU

24%

HGM

30%

Revenue

By Mix

By Geography

Consumables

65%

Equipment

35%

GROSS

MARGIN

FREE CASH

FLOW TO

NET INCOME

~55%

>100%

UNITED BY COMMON

BUSINESS MODEL

• Outstanding brands with market-

leading positions

• Extensive installed base

• Strong ‘captive’ recurring revenues

• High level of customer intimacy

All financial metrics based on FY 2017E unless otherwise indicated

ADJUSTED

EBITDA

MARGIN YTD>20%

Distribution

30%Direct

70%

Direct vs. Distribution

TOTAL

REVENUE~$18BSTRONG PORTFOLIO

Building & enhancing a sustainable growth, earnings

and free cash flow profile

LIFE SCIENCES DIAGNOSTICS DENTAL

~$40B ~$35B ~$20B ~$15B

REGULATORY REQUIREMENTS

ADDRESSABLE MARKET SIZE

WORKFLOW EFFICIENCY

HIGH GROWTH MARKETS

IMPROVING STANDARDS OF CARE

ENVIRONMENTAL SAFETY

Strong secular drivers with high barriers to entry

WATER QUALITY

~$10B

PRODUCT ID

Well-Positioned Portfolio Serving Attractive End-Markets

Danaher Business System (DBS) is Our Competitive Advantage

1984 1991 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017E

Evolution of the Danaher Business System (DBS)

As portfolio evolved, so has DBS – from Lean to a balanced approach

OUR SHARED PURPOSEHELPING REALIZE LIFE’S POTENTIAL

Leadership

Lean Growth

Leadership

Lean Growth

Leadership

Lean Growth

Leadership

Lean Growth

TODAY

Mid-1980s

LEAN

FOCUSED

ADDED

GROWTH

2001

2016

ADDED

LEADERSHIP

2009LAUNCHED

SHARED

PURPOSE

Balanced approach to deliver long-term value to shareholders

Building and evolving into a stronger, better Danaher

What You’ll Hear Today

Focused execution around our strategic priorities

1. Strengthen our competitive advantage with DBS

2. Enhance our portfolio via strategic M&A

3. Attract & retain exceptional talent

2017 Financial Highlights

“OMX” is Operating Margin Expansion; “WC” is Working Capital

SHAREHOLDER

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

CUSTOMER QUALITY (EXTERNAL PPM)

ON-TIME DELIVERY (OTD)

ASSOCIATEINTERNAL FILL RATE

RETENTION

8 CORE VALUE DRIVERS

DBS Is Our Competitive Advantage

“Common sense vigorously applied”

Leadership

Lean Growth

Core Revenue Growth

+Margin Expansion

+Strong Free Cash Flow

+Acquisitions

=TOP QUARTILE EPS GROWTH &

COMPOUNDING RETURNS

How We Create Value: Running the Danaher Playbook

IMPROVE COST

STRUCTURE

Balanced approach to create shareholder value

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

G&A

S&M

OMXCore

Growth

R&D

Gross

Margins

REINVEST

FOR GROWTH

ACCELERATE

MARGINS &

CORE GROWTH

Clear Runway to Accelerate Core Revenue Growth

Line of sight to MSD core revenue growth over time

NEW LARGER ACQUISITIONS

CONTINUED EXECUTION WITH IMPROVEMENT OPPORTUNITIES

MSD~3%2017E WEIGHTED

AVG. CORE

REVENUE GROWTH

DBS IS OUR

COMPETITIVE ADVANTAGE

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

Leadership

Lean Growth

2017E WEIGHTED

AVG. CORE

REVENUE GROWTH

Continued Margin Improvement With

Significant Runway Ahead

75bps+ average annual core OMX last 3 years, expect 50-75bps annually

RECENT ACQUISITIONS

IMPROVEMENTOPPORTUNITIES

STRONG EXECUTION AT CORE BUSINESSES

>600BPSAVG. OMX SINCE

ACQUISITION

AVG. OMX SINCE

ACQUISITION

>25%AVG. OPM

TODAY

>$10B COMBINED

REVENUE

20%+ ANTICIPATED

OPM OVER TIME>1,000BPS

AVG. OPM

TODAY

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

Mid/high-

teens ~20%AVG. OPM

TODAY

Operating Profit Margin (“OPM”) excludes amortization

Superior Free Cash Flow Generation

FCF expected to exceed Net Income for 26th consecutive year

2014 2015 2016 2017E 2014 - 2016 Average

DANAHER

LIFE

SCIENCE

PEERS

FCF / ADJUSTED NET

INCOME CONVERSION

>100%

~85%

FREE CASH FLOW (FCF)

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

$2.2B$2.4B $2.5B

>10% Growth Y/Y

MARKET

COMPANY

VALUATION

Our Strategic Approach to M&A

• Secular growth drivers

• Fragmented

• Higher barriers to entry

• Optionality with multi-industry

portfolio

• Competitive market position

• Strong brand / channel

• Consistent revenue visibility

• Higher margin businesses

• Cultural fit

• Focus on ROIC

• DBS opportunities

• Sustainability

• Synergies with DHR OpCos

• Combination of value & growth deals

Selectively pursuing value creation opportunities

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

“ROIC” is Return on Invested Capital

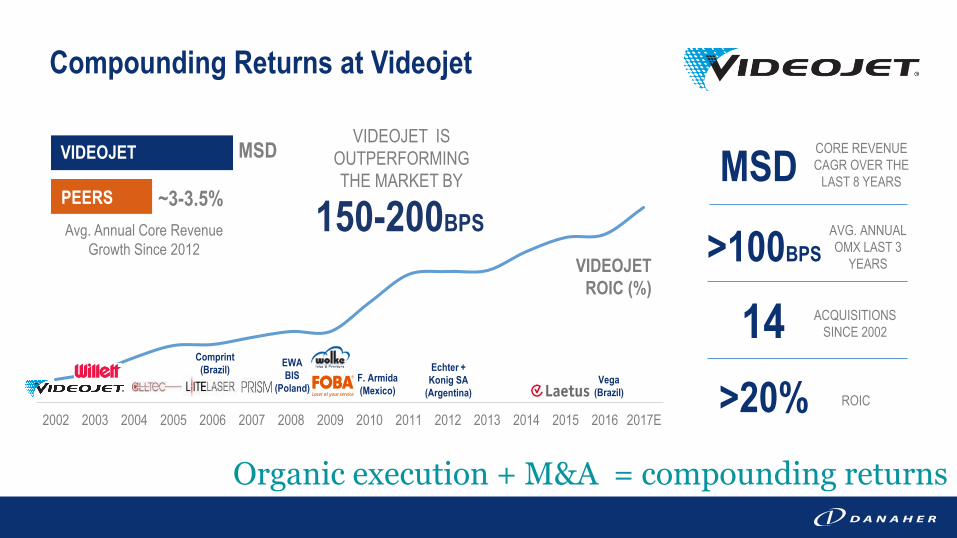

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

VIDEOJET

ROIC (%)

CORE GROWTH CAGR LSD CORE GROWTH CAGR MSD

Organic execution + M&A = compounding returns

Summing Up the Value Creation Model:

Videojet Example

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

MSDCORE REVENUE

CAGR OVER THE

LAST 8 YEARS

>100BPS

AVG. ANNUAL

OMX LAST 3

YEARS

>20% ROIC

14 ACQUISITIONS

SINCE 2002

EWA

BIS

(Poland)F. Armida

(Mexico)

Echter +

Konig SA

(Argentina)

Comprint

(Brazil)Vega

(Brazil)

DD DD

~50% ~55%

Flat/LSDMid-

teens

— LSD

AT ACQ. TODAY

1 YEAR IN

LSD MSD*

~50% >50%

High-

teens~25%

LSD MSD

Core Growth

Gross Margin

Operating

Profit Margin

ROIC

Flat/LSD MSD

~70% >70%

LDD >20%

LSD HSD

Core Growth

Gross Margin

Operating

Profit Margin

ROIC

Update on Recent Large Acquisitions

AT ACQ. TODAYAT ACQ. TODAY

Deals at or above initial expectations

2 YEARS IN3 YEARS IN

CORE REVENUE GROWTH

OMX

CASH FLOW / WC TURNS

ROIC

SHAREHOLDER

ACQUIRED DEC 2014 ACQUIRED AUG 2015 ACQUIRED NOV 2016

Core Growth

Gross Margin

Operating

Profit Margin

ROIC

* Reflects Q4E 2017

Associates are key to sustaining our competitive advantage

Evolving Strategic Approach to Talent

DEVELOPING LEADERS

• Development primarily “on the job”

TALENT

• General industrial talent

• Outsourced talent acquisition

ORGANIZATION

• OpCos & Corporate

10+ YEARS AGO

• Progressive responsibilities &

formalized development programs

• Science & technology talent

• Internal talent acquisition & cultivation

• Platform leadership driving strategic

moves & portfolio evolution

• OpCos execute strategic decisions

TODAY

OpCo Presidents & Above

>80%AVG. INTERNAL

FILL RATE

SINCE 2015

+15% R&D NEW

HIRES 2017E

+15%CUSTOMER-

FACING NEW

HIRES 2017E

INTERNAL FILL RATE

RETENTIONASSOCIATE

LIFE

SCIENCESDIAGNOSTICS DENTALENVIRONMENTAL & APPLIED SOLUTIONS

Leadership Development Across Danaher:

Recent Moves

Multi-industry structure a differentiator in talent attraction, development, retention

WATER QUALITY PRODUCT ID

PREVIOUSLY

PRESIDENT

EVP OF LIFE SCIENCES

PLATFORM

PREVIOUSLY

PRESIDENT

PRESIDENT

PREVIOUSLY EVP OF

LS & PID PLATFORMS

EVP OF DX & DENTAL

PLATFORMSPREVIOUSLY EVP OF

LS & PID PLATFORMS

EVP OF DX & DENTAL

PLATFORMS

PREVIOUSLY

PRESIDENT

PRESIDENT

PREVIOUSLY

HEAD OF R&D

PRESIDENT

PREVIOUSLY HEAD OF T&M

GROUP EXECUTIVE FOR

DENTAL

PREVIOUSLY

PRESIDENT

PREVIOUSLY

PRESIDENT IND.

PREVIOUSLY

PRESIDENT

PREVIOUSLY GROUP EXEC

OF PID PLATFORM

EVP OF EAS PLATFORM

PREVIOUSLY

HEAD OF R&D

PRESIDENT

INTERNAL FILL RATE

RETENTIONASSOCIATE

PREVIOUSLY

PRESIDENT

GROUP EXECUTIVE FOR

WATER QUALITY

PREVIOUSLY

FINANCE

CFO

Core Revenue Growth

+Margin Expansion

+Strong Free Cash Flow

+Acquisitions

=TOP QUARTILE EPS GROWTH &

COMPOUNDING RETURNS

Putting It All Together

DBS driving the creation of shareholder value

G&A

S&M

OMXCore

Growth

R&D

Gross

Margins

G&A

AS % OF SALES

AVG. ANNUAL

CORE OMX

GROSS

MARGIN+200BPS

RESULTS: LAST 3 YEARS

-50BPS

+50BPS

>75BPS

AVG. ANNUAL

EPS GROWTHMid-teens

R&D

AS % OF SALES

Leadership

Lean Growth

Balanced approach to deliver long-term value to shareholders

Summary

Portfolio & DBS evolution have contributed to better,

stronger Danaher – with significant runway ahead

Superior FCF generation enables us to enhance our

portfolio via strategic M&A

Exceptional talent & leadership is critical to delivering and

sustaining results

DANAHER BUSINESS SYSTEM

Melissa Aquino

Vice President, DBSO

2017 INVESTOR & ANALYST DAY

DBS Enables a Balanced Approach

Not just Lean – but also Leadership and Growth

DBS FUNDAMENTALS

PROBLEM SOLVING

PROCESS

VOICE OF THE

CUSTOMER

STANDARD WORK VALUE STREAM MAPPING

TRANSACTIONAL

PROCESS IMPROVEMENT

VISUAL & DAILY

MANAGEMENT

KAIZEN 5S

Leadership

Lean Growth

DBS Growth Tools

DBS Growth comprised of innovation & commercial tools

Strategic Product

Envelope

Product Planning

Group

Customer

Segmentation

Danaher Innovation

Process

Accelerated

Product Development

Speed Design

Review…

COMMERCIAL TOOLS

EXAMPLES:

EXAMPLES:

Transformative

Marketing

Value

Selling

Lead

Nurturing

Funnel ManagementStrategic

Negotiations

Sales Force

Initiative…

Leadership

Lean Growth

Leadership

Lean Growth

INNOVATION TOOLS

DBS Innovation Tools

Replicable process for innovation provides competitive advantage

Strategic

Product

Envelope

Problem to

Portfolio

(P2P)

Product

Planning

Group

NPD

Project

Management

Launch

Excellence

Define the

attractive domain

for innovation

Define a winning

roadmap for

attractive segments

Coordinate execution

& resources across

multiple projects

Drive cross-functional

development

of each new product

Generate & fulfill

demand for the

new product

DOMAIN ROADMAP

EXECUTION &

RESOURCES

CROSS-

FUNCTIONAL DEV. FULFILL DEMAND

FROM MARKET

INSIGHT…

…TO MARKET

SHARE

Leadership

Lean Growth

DBS Innovation in Action: Speed Design Review at Hach

BASICS OF SPEED DESIGN

REVIEW (SDR)

• Gather VOC; go to Gemba

• Obeya room with cross-functional

teams together

• Simultaneous product & process

optimization

• Rapid prototyping & evaluation

SDR IN ACTION: HACH CM130 CHLORINE

MONITORING SYSTEM FOR DIALYSIS

RESULTS

NEW ADJACENT

ADDRESSABLE MARKET

+$50M1ST FDA

CLEAREDONLINE CHLORINE ANALYZER

FOR DIALYSIS

Customer purchased Hach drinking water

product to try in a dialysis capacityVOC

GEMBA

SPEED 15 product design “sprints”

Dialysis clinics are required to test

water every 4 hours

DBS Commercial Tools

Integrated marketing & sales tools to drive commercial execution, accelerate growth

DAILY MANAGEMENT | GROWTH ROOM | STANDARD WORK

Market Insight

and Visibility

Sales

Productivity

and

Prospecting

Lead

Generation

and Campaign

Awareness

Customer

Buying

Journey &

Insight

TRANSFORMATIVE MARKETINGSALES

STANDARD WORK

Market Overview

and Channel

Strategy

Sales Funnel

Management

Market attractiveness

—

How do we win?

Market segmentation

—

Customer profile

What triggers interest?

—

Sources of info

Value Proposition

—

Customer benefit

Customer Buying

BehaviorMonthly “Key”

Opportunity Review

Are we in control? What’s working? What’s not working?

Leadership

Lean Growth

Commercial Execution Driving Growth at Pall

Using DBS to improve S&M processes and drive better growth

+50%CONTACTS / VISIBILITY

LEADS

+6.5xOPPORTUNITIES

+2xWIN RATE %

+15%

RESULTS

2017 YTD

MA

RK

ET

ING

FU

NN

EL

SA

LES

FU

NN

EL

SITUATION AT ACQUISTION

• Limited process for improving market visibility

• Little to no digital marketing capabilities

• No repeatable process for generating / nurturing high-quality

sales leads

DBS ACTIONS

• Transformative Marketing: Disciplined marketing campaigns to

improve visibility & account coverage

• Lead Handling: Prioritize & deliver more qualified leads to sales

• Funnel Management: Streamlined sales funnel process to improve

win rates

BIOPHARMA

“WIN THE SPEC”

Balanced approach to deliver long-term value to shareholders

DBS is our culture and our competitive advantage

Today, DBS is not just Lean – it’s about Growth & Leadership as well

DBS Growth Tools are helping across all platforms – you’ll hear

many examples today

Summary

LIFE SCIENCES

Rainer Blair, Executive Vice President

2017 INVESTOR & ANALYST DAY

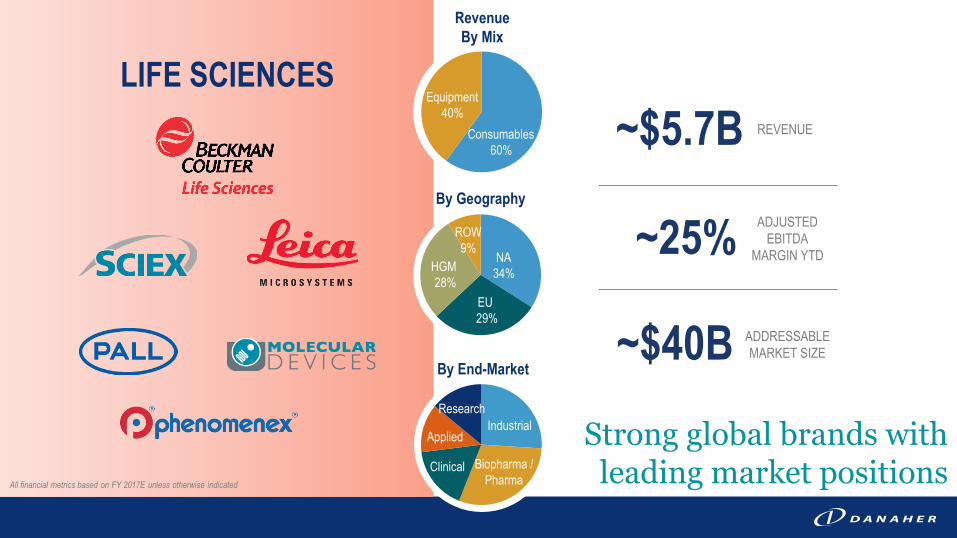

Strong global brands with leading market positions

LIFE SCIENCES

REVENUE

ADJUSTED

EBITDA

MARGIN YTD

ADDRESSABLE

MARKET SIZE

~$5.7B

~$40B

~25%

Revenue

By Mix

By Geography

By End-Market

Industrial

Clinical Biopharma /

Pharma

Research

Applied

Consumables

60%

Equipment

40%

ROW

9%NA

34%

EU

29%

HGM

28%

All financial metrics based on FY 2017E unless otherwise indicated

Strong core operating margin expansion driven by broad-based

execution across the platform

Pall continues to deliver meaningful improvements since acquisition;

building momentum and expect higher core growth in Q4

Accelerating core growth across the platform

Attractive value creation via M&A

• Phenomenex up MSD

• IDBS enhances our informatics software capabilities in biologics

2017 Highlights

Strong execution providing good momentum into 2018

LIFE SCIENCES

CORE OMX

>150BPS

PALL CORE OMX

SINCE ACQUISITION

>600BPS

LIFE SCIENCES CORE

REVENUE GROWTH 2017E

MSD

All financial metrics refer to the 9 months ending Sep. 29, 2017 unless otherwise indicated

Focused on areas of highest growth & highest customer impact

How We Win in Life Sciences

Indexing our portfolio to high-growth end markets –

geographically and in terms of applications

Best-in-Class analytical technologies & high level of

innovation focused on key applications

Increasing aftermarket business with frequent, high-

quality touch points and differentiated offering

Global high-tech sales force to target highest growth

segments & regional opportunities

OUR STRATEGIC FOCUS

INNOVATION

SERVICE

COMMERCIAL

HIGH GROWTH

SEGMENTS

~25% ~25% ~15% ~15%% OF LS SEGMENT REVENUE

Strong secular drivers underpinning growth opportunities

~15%

Leading Global Brands Serving Attractive Markets

BIOLOGICS INDUSTRIALAPPLIED (FOOD, ENV., FORENSICS)

RESEARCH &

ACADEMIC CLINICAL

Well-positioned to win in attractive market segments

Strong Secular Growth Drivers

600

DATA SENSOR CHIPS

IN FUTURE CARS VS

300 TODAY

~100

PESTICIDES &

VETERINARY DRUGS’

MAXIMUM RESIDUAL

LEVELS TIGHTENED BY

GOV’T AGENCIES IN 2017

80%

OF TOTAL LIFE SCIENCE

R&D SPEND IS ON

BIOPHARMACEUTICALS

BIOLOGICSEVOLUTION OF

LIFE SCIENCE

RESEARCH

HIGH GROWTH

MARKETS

FOOD &

ENVIRONMENTALMICRO-

ELECTRONICS

+20%

NUMBER OF BIOLOGICS

IN THE APPROVAL

PIPELINE VS 2016

~20%

BIOPHARMA CAGR IN

CHINA EXPECTED

THROUGH 2020

New Product Innovation Driving Growth at SCIEX

TOPAZ CLINICAL MASS SPEC & VITAMIN D ASSAY

1STFULLY INTEGRATED LC-MS

SYSTEM & ASSAY FOR

CLINICAL DX TESTING

~10M VITAMIN D TESTS RUN BY

US LABS ANNUALLY

+$100M ADDRESSABLE MARKET

EXPANSION FOR SCIEX

FDA

CLEARED

Year 1 Year 2 Year 3

ASSAY

1

VIT

D

VIT

DVIT

D

Increasing customer savings & profits as additional tests are added

Helping clinical lab customers do more, save more, and deliver more confident results

ASSAY

1

ASSAY

2

New Product Innovation Driving Growth at BEC LS

Stronger cadence of innovation helping drive share gains

FlatCORE GROWTH

AT THE TIME OF

ACQUISITIONMSD

CORE REVENUE

GROWTH

CAGR LAST 3 YEARS

BIOMEK I-SERIES

AUTOMATED

WORKSTATIONS

CYTOFLEX LX

3 Years

Pre-Acq.Last 3

Years

LDT

1~3

~20Number of New Product Launches

S&M*

R&D*

+200BPS

+50BPS

RESULTS OVER THE

LAST 5 YEARS

* As a % of sales

Differentiating With Our Service Offering at SCIEX

Strategic approach to service helping drive share gains

SERVICE CONTRACT

CAPTURE RATE

SINCE 2015

SERVICE REVENUE

CAGR

LAST 5 YEARSHSD+

+500BPS

IMPROVEMENT IN

FIRST-TIME-FIX

RATE SINCE 2015>700BPSCUSTOMER-CENTRIC

• Proactive vs reactive

• Focused on customer workflow, helping

customers achieve superior results

• Improving quality & efficiencies

COMPREHENSIVE OFFERING

• Enhancing with new aftermarket products & tools

• Leveraging commercial capabilities

HOW WE WIN WITH SERVICE

Pall Update: Actions & Results Since Acquisition

Improving operational & commercial execution with DBS

ANTICIPATED CUMULATIVE COST

SAVINGS SINCE

ACQUISITIONYEAR 1: ~$125M

YEAR 2: ~$200M

YEAR 5: ~$350M

Reducing manufacturing & operating costs

Meaningful gains in quality & delivery

DBS commercial initiatives driving better go-to-

market capabilities

Accelerating innovation through reinvestment and

focused R&D processes

OPERATIONS

COMMERCIAL

INNOVATION

NUMBER OF

NEW PRODUCT LAUNCHES

NET WORKING CAPITAL

IMPROVEMENT~$100M

+50%

ON-TIME-DELIVERY

IMPROVEMENT>2,000BPS

CORE REVENUE

GROWTH EXPECTED IN

Q4 2017MSD

Running the Danaher Playbook: Life Sciences Platform

~$2.4B REVENUE

<40% AFTERMARKET

5 YEARS AGO

~$5.7B REVENUE

~60% AFTERMARKET

TODAY

2005 2009 2010 2011 2012 2013 2014 2015 2016 2017

~$19B SPENT ON 25+ ACQUISITIONS SINCE 2005

Enhancing our growth trajectory with DBS rigor & inorganic opportunities

MSD CORE REVENUE

CAGR

~300BPSGROSS MARGIN

EXPANSION

>20% OP CAGR

OPM EXPANSION

~1,000BPS

All financial metrics shown are over the last 5 years, unless otherwise indicated

OPM excludes amortization

Balanced approach to deliver long-term value to shareholders

Outstanding global brands built on best-in-class technologies,

in attractive markets

Terrific margin performance enabling reinvestment in new

product & commercial innovation

Pall executing well two years post acquisition, and performing

ahead of initial expectations

Summary

DENTAL

Amir Aghdaei, Group Executive

2017 INVESTOR & ANALYST DAY

All financial metrics based on FY 2017E unless otherwise indicated

ROW

6%NA

49%

EU 23%HGM

22%

Revenue

By Mix

By Geography

Equipment

Specialty

Consum.(implants, ortho)

Traditional

Consum.

DENTAL

REVENUE

ADJUSTED

EBITDA

MARGIN YTD

ADDRESSABLE

MARKET SIZE

~$2.8B

~$20B

~20%

Direct vs. Distribution

DirectDistribution A leading global player covering entire dental workflow

Completed year 2 of treating Dental as a “new acquisition”

Seeing benefits of Dental platform integration

Continuing to improve performance and re-invest in growth, M&A

Executing well in HGM; good growth in specialty businesses

(implants & orthodontics)

2017 Highlights

GROSS MARGIN

EXPANSION

SINCE 2015

R&D

INVESTMENT

CORE REVENUE

GROWTH AT NOBEL &

ORMCO 2017E

>100BPS

MSD

+10%

Good relative performance – with ample upside

REVENUE

GROWTH IN HGMDD

All financial metrics refer to the 9 months ending Sep.

29, 2017 unless otherwise indicated

Strong Global Growth Drivers

Strong fundamental growth drivers, diverse global customer base

PATIENT

• Aging population

• Higher aesthetic motivation

• Growing middle class & better access to care (HGM)

DENTIST

• Shifting from analog to digital technologies

• Seeking predictable treatment results

CLINIC

• “Dentistry as a business”

• Seeking efficiency and economic results (DSOs)

OF US DENTISTS

USE DIGITAL

TECHNOLOGY

DENTAL SPEND

PER CAPITA IN THE

US VS CHINA

IMPLANT

PENETRATION

GLOBALLY

<50%

~5%

30x

Pursue

Winning Vision3

Rejuvenate Innovation

and Growth2

Build a Strong Foundation 1 Reduce business complexity

Create funds for investments

Accelerate growth

Build our competitive advantage

Long-term, sustainable market leadership

1 2 3

STRONG

FOUNDATION

INNOVATION &

GROWTH

WINNING

VISION

Our Frame for Treating Dental as a “New Acquisition”

1 2 3

ACTIONS

• Consolidated number of OpCos from 10 to 4

• Reduced manufacturing & back-office sites by 30%

• Shared platform services

• DBS “basics”

RESULTS OVER THE LAST 2 YEARS

Reduce Business Complexity & Create Funds for Investment

>100BPSGROSS MARGIN

IMPROVEMENT

-50BPSG&A

AS % OF SALES

Step 1: Building a Strong Foundation

Focused structure to facilitate improving core growth & margins

STRONG

FOUNDATION

INNOVATION &

GROWTH

WINNING

VISION

1 2 3

DENTAL PLATFORM ACTIONS

OVER LAST TWO YEARS

Drive Sustainable Growth & Build Out Competitive Advantage

CORE

GROWTH Flat/LSD

At Acq.

Step 2: Rejuvenate Innovation & Growth

Today

MSD

INCREASE

IN FOTS

R&D SPEND

AS % OF SALES

>10%

+100BPS

Accelerating growth trajectory through reinvestment

STRONG

FOUNDATION

INNOVATION &

GROWTH

WINNING

VISION

EXAMPLE

>25NEW PRODUCTS

LAUNCHED SINCE

ACQUISITION

+20%R&D SPEND

SINCE 2015

>800BPSOMX SINCE

ACQUISITION

RESULTS

ACQUIRED 2014

HOW WE WIN IN CHINA

• “One stop solution” product portfolio of leading brands

• Increasing commercial coverage, invest in localized sites and R&D

• Strategic partnerships

RESULTS

1 2 3Step 2: Rejuvenate Innovation & Growth

LEADING PLAYER IN

CITIES IN CHINA

WHERE WE HAVE

A PRESENCE

‘In China for China’

>50

Leading market position in China

STRONG

FOUNDATION

INNOVATION &

GROWTH

WINNING

VISION

~$35M

2012 Today

>$150MChina Dental

Revenue

CORE REVENUE

CAGR IN CHINA

LAST 5 YEARSDD+

58

1 2 3

YESTERDAY / TODAY

POINT SOLUTIONS

Build Long-Term, Sustainable Leadership

TODAY / TOMORROW

INTEGRATED WORKFLOWS

Step 3: Pursue Winning Vision

EQUIPMENT

CONSUMABLES

SOFTWARE/DIGITAL

DIAGNOSTICS

TREATMENT PLANNING

TREATMENT EXECUTION

Integrate & optimize dentists’ workflows

STRONG

FOUNDATION

INNOVATION &

GROWTH

WINNING

VISION

NUMBER OF SOFTWARE

ENGINEERS OVER

LAST 2 YEARS

IMAGING INSTALLED BASE

GLOBALLY

OF DENTISTS’

CLINICAL SPEND

CAN BE CAPTURED

BY OUR PRODUCTS

+2.5x

>90%

Largest

Balanced approach to deliver long-term value to shareholders

Executing the DHR playbook and delivering on key strategic

priorities

Making good progress toward accelerating core growth, with

runway to 20%+ OPM

Specialty consumables businesses and High Growth Markets

performing very well

Summary

Giving Back

As a global platform supporting the packaging

value chain for food products, Product ID is

proud to support WFP’s mission to end

hunger and improve nutrition.

Hach is proud to support an

organization dedicated to improving

lives across the globe with the most

basic of human needs: clean water.

Direct Relief uses innovative approaches

for the efficient delivery of medical aid,

serving the needs of communities close to

our associates around the world.

WCRF’s cause aligns with SCIEX’s vision of

placing the power of life-changing answers

into the hands of those who care,

everywhere.

Beckman Coulter’s long-standing

partnership with LLS enables the team

to support active research projects and

help patients afford treatments.

Nobel is proud to partner with Brighter

Way as they help future dental health

professionals train to care for vulnerable

children, adults, and families.

PRODUCT ID

Joakim Weidemanis,

Executive Vice President

2017 INVESTOR & ANALYST DAY

All financial metrics based on FY 2017E unless otherwise indicated

Revenue

By Mix

By Geography

PRODUCT IDREVENUE

EAS ADJUSTED

EBITDA

MARGIN YTD

ADDRESSABLE

MARKET SIZE

~$1.8B

~$10B

>25%

By End-Market

CPG Food

& Bev

Pharma

ROW

4%

NA

30%

EU

30%

HGM

36%

Equipment

45%Consumables

55%

Other

CPG

Industrial

Leading global player supporting the entire packaging value chain

Packaging

Supply

Chain

ENVIRONMENTAL & APPLIED SOLUTIONS (EAS)

Continued share gains driven by new products, expanded service offering

• Videojet: largest installed base of remotely connected printers

• Esko: evolving software offering for digitizing packaging workflows

• X-Rite: early traction with digitizing appearance

Consistent DBS execution helping to fund reinvestment and sustain strong

track record of MSD core growth

Recent acquisitions augmenting core growth: AVT, Laetus, MediaBeacon

2017 Highlights

Running the Danaher playbook at Product ID

MAJOR NEW PRODUCT

LAUNCHES IN 2017

16

AVG. ANNUAL OMX

SINCE 2014

>100BPS

CORE REVENUE CAGR AT

VIDEOJET LAST 8 YEARS

MSD

All financial metrics refer to the 9 months ending Sep.

29, 2017 unless otherwise indicated

Growing Suite of Solutions Across the Packaging Value Chain

Solutions from concept & design through production

Pharma inspection

Pharma and food Track and Trace

Marking and

Coding

Spectrophotometers

Color formulation SW

Color standards

Color management workflow

Digital asset management and distribution SW

Packaging management SW

Packaging CAD

Pre-press automation SW

Flexography imagers

Packaging

Design

Concept and

Ideation

Artwork

Creation

Packaging

Converting

Package

Filling

Inline

Printing

Warehouse &

Logistics

Distribution &

Retail

Packaging

Strategy

In-line

inspection

Strong secular drivers across the packaging value chain

Packaging Macro Growth Drivers

OF CPG BRAND PURCHASE

DECISIONS ARE MADE AT

THE POINT OF SALE

>900

DIFFERENT FACILITIES THAT

MANUFACTURE & BOTTLE

COCA COLA GLOBALLY

PACKAGING

PROLIFERATION

GLOBAL BRAND

CONSISTENCY &

ACCURACY

REGULATORY &

CLAIMS INFORMATION

PACKAGING AS A

MARKETING VEHICLE

+85%

NUMBER OF OREO SKUs

LAUNCHED PER YEAR

TODAY VS 2012

~50%

OF GLOBAL PACKAGING

TRACK & TRACE REGULATIONS

HAVE BEEN ADDED SINCE 2015

>50%

Focused on Supporting Our Customers’ Needs

PACKAGING

VARIABILITYPACKAGING

PROLIFERATION

BRAND CONSISTENCY &

ACCURACY

REGULATORY & CLAIMS

INFORMATION

PACKAGING AS A

MARKETING VEHICLE

CONSUMER TRENDS

• Uptime & scalability

• Rapid diagnostics & recovery

• Global deployment & service capabilities

• Deep domain knowledge

• Digital workflows linking physical & digital worlds

CUSTOMER NEEDS

• Increased product launch velocity

• Focus on connectivity & remote service

• Local digital and vertical marketing

• Trusted advisor on customers’ application

• Ongoing digitization of physical workflows

OUR STRATEGIC FOCUS

DBS Driving Growth: Transformative Marketing

KEY GROWTH INITIATIVES

• Marketing integrating with sales Funnel

Management to improve sales productivity

• Honed our message from product vertical

now persona-oriented marketing

RESULTS SINCE 2013

+80%MARKET

VISIBILITY

+40%ORGANIC WEB

TRAFFIC

+90%“NEW” CUSTOMER

EQUIPMENT REVENUE

Commercial innovation helping drive above-market equipment revenue growth

Differentiating With Our Service Offering

Differentiating with service to drive share gains

• Growing through disciplined service commercialization

• Differentiating our portfolio to better address customer

needs, drive replacement

• Expanding Remote Service Solutions:

IoT-enabled 1860 printer launched in 2017

EARLY INNINGS OF REMOTE OFFERING

LARGEST REMOTELY CONNECTED

INSTALLED BASE GLOBALLY

PRINTERS CONNECTED

WITH REMOTE SERVICE

SINCE 2015

PRINTERS UNDER

SERVICE CONTRACT

SINCE 2014

SERVICE REVENUE

GROWTH 4 YEARS

IN A ROW

12x

DD

+65%

Differentiating Through Product Innovation

Innovative solutions rooted in customer needs underpin our growth

ORGANICALLY INORGANICALLYMAJOR CORE NEW PRODUCT INTRODUCTIONS

Expansion beyond core products

CIJ 1860 Platform

Predictive analytics

& remote service

TTO

iAssure

inspection

Total

Appearance

Capture

Acquisition in 2017

Expands our

in-line print

inspection

offering

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

VIDEOJET

ROIC (%)

Organic execution + M&A = compounding returns

Compounding Returns at Videojet

MSD

~3-3.5%

VIDEOJET IS

OUTPERFORMING

THE MARKET BY

150-200BPSPEERS

Avg. Annual Core Revenue

Growth Since 2012

VIDEOJET

EWA

BIS

(Poland)F. Armida

(Mexico)

Echter +

Konig SA

(Argentina)

Comprint

(Brazil)Vega

(Brazil)

MSDCORE REVENUE

CAGR OVER THE

LAST 8 YEARS

>100BPS

AVG. ANNUAL

OMX LAST 3

YEARS

>20% ROIC

14 ACQUISITIONS

SINCE 2002

Balanced approach to deliver long-term value to shareholders

Differentiated product offering to support customer needs

across packaging workflows

Sustained market outperformance driven by DBS for

commercial & new product innovation

“Running the Danaher playbook” enables the pursuit of high-

impact organic & inorganic growth opportunities

Summary

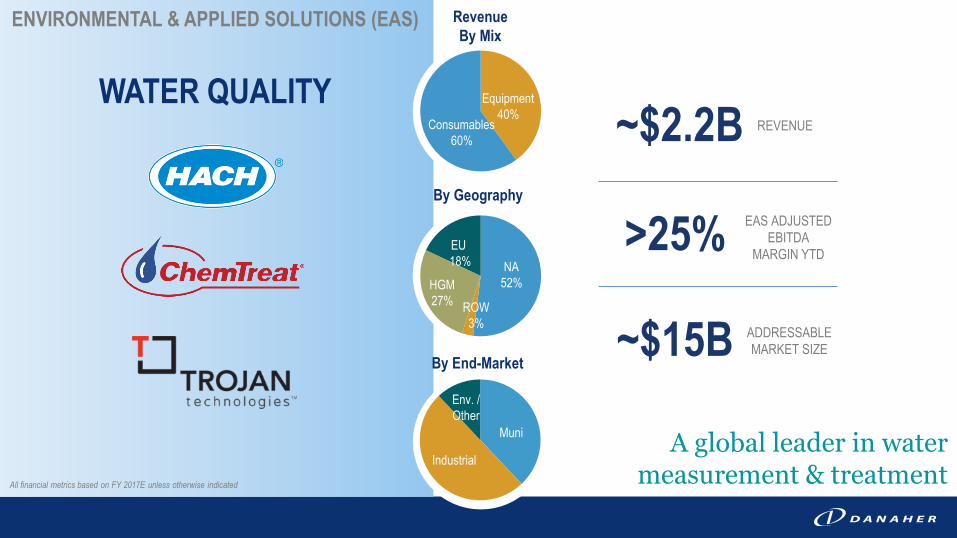

WATER QUALITY

Lance Reisman, Group Executive

2017 INVESTOR & ANALYST DAY

All financial metrics based on FY 2017E unless otherwise indicated

REVENUE

ADDRESSABLE

MARKET SIZE

~$2.2B

~$15B

WATER QUALITY

Revenue

By Mix

By Geography

By End-Market

Muni

ROW

3%

NA

52%

EU

18%

HGM

27%

Equipment

40%Consumables

60%

Industrial

Env. /

Other

A global leader in water measurement & treatment

ENVIRONMENTAL & APPLIED SOLUTIONS (EAS)

EAS ADJUSTED

EBITDA

MARGIN YTD>25%

Continued share gains across the platform

• ChemTreat & Trojan executing well

• Solid performance at Hach in core muni & industrial businesses

DBS growth tools helping drive new product & commercial innovation,

while enabling entry into new market segments

• Trojan win rate up >750bps y/y

• Introduced Hach CM130 dialysis chlorine monitoring system

Bolt-on acquisitions enhancing platform growth trajectory

• Closed 2 deals: AppliTek (online analyzers) and Enviscience

(Thailand distributor)

2017 Highlights

New markets, new products & commercial execution driving share gains

2017E CORE REVENUE GROWTH

AT TROJAN & CHEMTREAT

MSD

INCREASE IN FOTS

IN NA & HGM

DD

ACQUISITIONS

OVER THE LAST 4 YEARS

10

All financial metrics refer to the 9 months ending Sep. 29, 2017 unless otherwise indicated

TREATING

MEASURING

Winning with strong brands, full water cycle expertise & DBS

Where We Play & How We Win in Water Quality

WATER

STORED WATER

TREATED WATER

USED

Environmental Municipal IndustrialBRAND LEADERSHIP:

LEADING PLAYER

PRODUCT INNOVATION &

COMMERCIAL EXECUTION

DIFFERENTIATED

CHANNEL

Winning

Dimensions

Well-positioned for long-term trends

Strong Secular Growth Drivers

OF MUNICIPAL ENERGY

BUDGETS ARE CONSUMED

BY WATER TREATMENT

+220M

PEOPLE NEWLY CONNECTED

TO WASTEWATER TREATMENT

UNDER CHINA’S LATEST 5

YEAR PLAN

INCREASING

REGULATORY

REQUIREMENTS

HIGH GROWTH

MARKETS

WATER SCARCITY /

SUSTAINABILITY

DATA ANALYTICS &

GREATER

EFFICIENCIES

+50%

NUMBER OF US STATES THAT

HAVE ADOPTED NUTRIENT

DISCHARGE LIMIT STANDARDS

SINCE 2008

~500M

PEOPLE GLOBALLY

EXPERIENCE WATER

SCARCITY YEAR-ROUND

~35%

Strategic Focus: Supporting Customers’ Needs

PACKAGING

VARIABILITYWATER SCARCITY /

SUSTAINABILITY

REGULATORY

REQUIREMENTS

HIGH GROWTH

MARKETS

DATA ANALYTICS &

GREATER EFFICIENCIES

TRENDS IN WATER QUALITY

• Respond to increasing & changing reporting

requirements

• Greater interest in conservation &

addressing scarcity challenges

• Demand for full workflow solutions

CUSTOMER NEEDS

• Maximizing commercial investments and

effectiveness in HGM

• Enhancing strategic account management

• Accelerating digital marketing capabilities

• Increasing cadence of new product innovation

including software

OUR STRATEGIC FOCUS

How We Differentiate and Win Through Innovation

Customers talk, we listen

CM130 Chlorine

Monitoring System

1st FDA cleared

system for dialysis

Claros™

Data, instrument

& process

management

CUSTOMER ADOPTION OF

CHEMTREAT’S WEB-BASED

WATER MANAGEMENT SINCE 2015DDREVENUE GROWTH IN

TROJAN REUSE

SINCE 2015>10%

UVFlex™

Expanded

technology

capabilities to

include water reuse application

at nearly any sized wastewater

facility

NEW ADDRESSABLE

MARKET WITH

CLAROS CAPABILITIES+$500M

CTVista+®

Water

management

software tracks

& records real-time

data 24/7 to help customers

optimize water treatment

Commercial Execution: Leveraging Scale at the Platform Level

Expanding commercial leadership contributing to share gains

KEY GROWTH INITIATIVES

• Accelerating digital marketing capabilities using DBS

• Platform approach to strategic key accounts

• Increasing local presence in High Growth Markets

RESULTS

~40%DIGITAL REVENUE

CAGR SINCE 2014

+DDCAGR IN KEY ACCOUNT

WINS & RENEWALS

SINCE 2015

+40%HGM REVENUE

GROWTH

OVER LAST 5 YEARS

EXAMPLES OF KEY ACCOUNTS

ACROSS WATER QUALITY

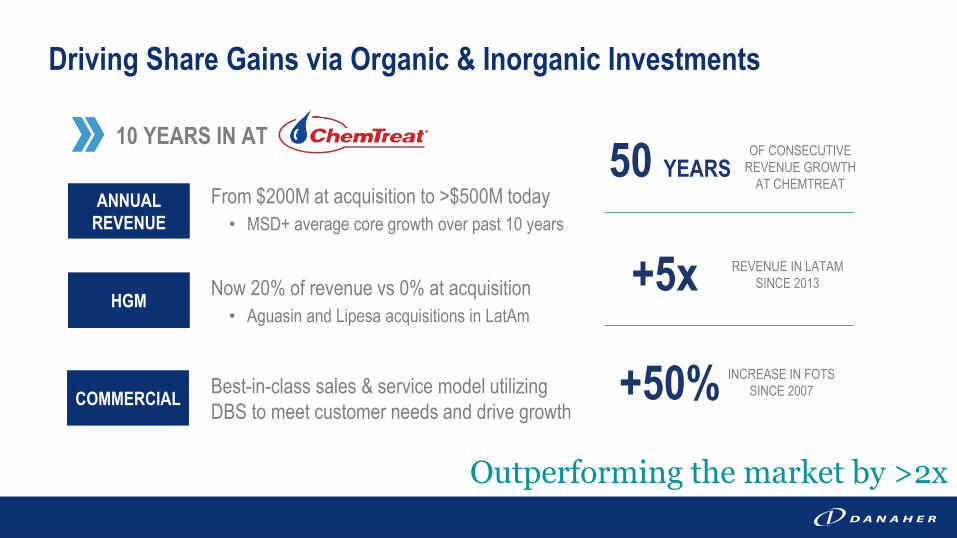

Driving Share Gains via Organic & Inorganic Investments

Outperforming the market by >2x

10 YEARS IN AT

From $200M at acquisition to >$500M today

• MSD+ average core growth over past 10 years

Now 20% of revenue vs 0% at acquisition

• Aguasin and Lipesa acquisitions in LatAm

Best-in-class sales & service model utilizing

DBS to meet customer needs and drive growth

ANNUAL

REVENUE

HGM

COMMERCIAL

OF CONSECUTIVE

REVENUE GROWTH

AT CHEMTREAT

REVENUE IN LATAM

SINCE 2013

INCREASE IN FOTS

SINCE 2007

50 YEARS

+50%

+5x

Balanced approach to deliver long-term value to shareholders

Strong position in highly attractive end-markets

Winning in our markets through product innovation &

commercial execution

Continuing to invest organically and inorganically to expand

our market opportunity

Summary

DIAGNOSTICS

Dan Daniel, Executive Vice President

2017 INVESTOR & ANALYST DAY

Strong brands with a broad global presence

DIAGNOSTICS

REVENUE

ADJUSTED

EBITDA

MARGIN YTD

ADDRESSABLE

MARKET SIZE

~$5.8B

~$35B

>20%

Revenue

By Mix

By Geography

By End-Market

Beckman

Diagnostics

Radiometer

LBS

Cepheid

Consumables

80%

Equipment

20%

All financial metrics based on FY 2017E unless otherwise indicated

ROW

6%NA

39%

EU 19%

HGM

36%

Outstanding first year at Cepheid, with DBS having a meaningful

impact helping to deliver & sustain mid-teens operating margins

Innovation & test menu expansion contributing to MSD core

revenue growth at Leica Biosystems and Radiometer

High growth markets continue to drive growth

• Cepheid increased FOS in China 2x resulting in >40% core growth

• Beckman continues to expand its direct channel in China & Middle East

2017 Highlights

Focus on innovation, accelerating growth and driving long-term results

CORE REVENUE

GROWTH AT CEPHEID

DD

NEW PRODUCTS’

CONTRIBUTION TO CORE

GROWTH AT LBS

~100BPS

REVENUE GROWTH IN

HIGH GROWTH MARKETS

HSDAll financial metrics refer to the 9 months ending Sep. 29, 2017 unless otherwise indicated

Well-positioned to win in an attractive market

Strong Secular Growth Drivers

>350%

INCREASE IN

HEALTHCARE SPEND

IN CHINA FROM

2005-2015

~30%

PENETRATION OF

MOLECULAR DX

IN THE US TODAY

~10K

PEOPLE IN THE US

TURN 65

EVERY DAY

PREDICTIVE &

PREVENTIVE CAREAGING

POPULATION

SKILLED LABOR

SHORTAGE

ADOPTION OF

NEW

TECHNOLOGIES

HIGH GROWTH

MARKETS

>70%

OF TREATMENT

DECISIONS ARE

INFORMED BY CLINICAL

DIAGNOSTICS

>50%

OF A TYPICAL

HOSPITAL LAB’S

COSTS ARE

PERSONNEL

Innovative clinical workflow solutions enable customers to improve operations

How We Win & Where We Play in Diagnostics

OUR COMPETITIVE ADVANTAGE

COMPREHENSIVE PRODUCT SUITE

PROVIDING SUPERIOR WORKFLOW EFFICIENCY

AUTOMATION &

SOFTWARE

DIFFERENTIATED OFFERING FOR OUR CUSTOMERS

FASTEST TURN-

AROUND TIMEHIGHEST

THROUGHPUT

HIGH QUALITY,

WITH BROADEST

MENUBOND / Advanced Staining Chemistry / IA & Automation

WHERE WE PLAY

TEST MENU

EXPANSION

GLOBAL

DISTRIBUTION &

SERVICE NETWORK

Surgical,

Intensive Care

Anatomic Pathology,

Cytology,Molecular Medicine Labs

Hematology,

Chemistry, Microbiology

Blood Banking,

Urinalysis

Point of Care

Oncology,

Tumor Boards

Emergency

Neo-natal

Cepheid Update: Actions & Results Since Acquisition

DBS helping to deliver sustainable core growth & margin expansion

Lean tools contribute to manufacturing productivity

gains and capacity expansion

DBS driving meaningful improvement in OTD

+3x sales team in China, small hospitals, POLs

Using Funnel Management to drive +2X increase in

qualified leads and win rate tracking

Continued menu expansion with Flu Express &

Group A Strep

OPERATIONS

COMMERCIAL

INNOVATION

DD DD

~50% ~55%

Flat/LSDMid-

teens

<80% >95%

AT ACQ. TODAY1 YEAR IN

Core Growth

Gross Margin

Operating

Profit Margin

On-time Delivery

(OTD)

Accelerating Growth Through Product Innovation

Well-positioned for improved growth in 2018 and beyond

DX R&D SPEND AS

% OF SALES OVER

LAST 3 YEARS+100BPS

RECENT NEW INSTRUMENTS & TECHNOLOGIES

Beckman DxC 700AU, DxH

500, Access 2, DxONE

LBS Bond III, Spectra

Stainer, Peloris III

Radiometer ABL 800,

TCM 5

PELORIS IIIXPERT XPRESS

GROUP A STREPRECENT TEST MENU ADDITIONS

Beckman hsTnI: High-

sensitivity troponin (CE),

Vitamin D, AMH

Radiometer Creatinine,

urea (CE), PCT (China)

Cepheid Flu Xpress, Group

A Strep Xpress

Accelerating Growth Through Commercial Execution

Strong execution with DBS accelerating growth opportunities

CONTINUE TO WIN INHIGH GROWTH MARKETS

DBS GROWTH TOOLS

China, Mexico

Expanding direct channel

Funnel Management, Lead

Generation

Strategic Account

Management

Clinical trial execution

NUMBER OF DX

PLATFORM’S

CLINICAL TRIALS

OVER LAST 3 YEARS+>2x

BEC DX FOTS

ADDED IN CHINA

SINCE 2015>50%

Adding FOTS

At Beckman, Cepheid

Localizing

China R&D, manufacturing

REVENUE GROWTH

IN HGM LAST 10

CONSEC. QUARTERSHSD+

Balanced approach to deliver long-term value to shareholders

Great start at Cepheid, expected to add ~100 bps of annual

organic growth for the platform

DBS accelerating new product innovation and improved

growth trajectory

Commercial execution continuing to improve organic growth

and driving penetration in High Growth Markets

Summary

SUMMARY & OUTLOOK

Tom Joyce, President & CEO

2017 INVESTOR & ANALYST DAY

Balanced approach to deliver long-term value to shareholders

What You Heard Today

Solid 2017 performance with momentum building as we

head into 2018

Continue to strategically build a better, stronger Danaher –

but with significant growth and margin runway ahead

Enhancing our competitive advantage through the evolution

of the Danaher Business System

Core revenue growth of 3.5-4.0%, accelerating from 2017 levels, with ~35% fall-through

• Cepheid & Phenomenex now part of core growth

• Expect improved core growth performance at Pall & Water Quality

F/X tailwind of ~$200M in revenue and ~$0.04 in adjusted EPS

Tax rate of ~21%, consistent with 2017

Anticipated EPS seasonality (as a % of FY 2018 adjusted EPS guidance)

• Q1: ~21% Q2: ~25% Q3: ~24% Q4: ~30%

2018 Outlook

2018 adjusted EPS guidance of $4.25-4.35* *Does not include accretion from any future acquisitions

5 Year Adjusted EPS Summary

Low-teens adjusted EPS CAGR from 2014 – 2018E

2014 2015 2016 2017E 2018E*

$2.98

$3.96 - $4.00$3.61

$2.66

$4.25 - $4.35

*Does not include accretion

from any future acquisitions

NON-GAAP RECONCILIATIONS

2017 INVESTOR & ANALYST DAY

Non-GAAP Reconciliations

($ in Millions)

Life Sciences Diagnostics Dental EASCorporate

Office

Total

Danaher

Operating Profit (GAAP) 680.0$ 554.9$ 301.4$ 666.0$ (127.2)$ 2,075.1$

Depreciation 88.6 271.8 29.7 31.6 5.6 427.3

Amortization 229.9 160.2 61.0 41.8 0.0 492.9

Adjusted EBITDA (Non-GAAP) (1) 998.5$ 986.9$ 392.1$ 739.4$ (121.6)$ 2,995.3$

Interest, net (115.3)

Income Taxes (346.6)

Depreciation (427.3)

Amortization (492.9)

Net Income Continuing Ops (GAAP) 1,613.2$

Net Sales 4,085.0$ 4,216.0$ 2,052.1$ 2,890.9$ 13,244.0$

Adjusted EBITDA Margin (Non-GAAP) (1) ≈25% >20% ≈20% >25% >20%

Nine-Month Period Ended September 29, 2017

(1) Management defines "Adjusted EBITDA" as GAAP operating income for the segment excluding (1) depreciation and (2) amortization, and

defines "Adjusted EBITDA Margin" as Adjusted EBITDA divided by sales for the particular segment.

Non-GAAP Reconciliations

($ in Billions)

Free Cash Flow from Continuing Operations: 2014 2015 2016

Operating Cash Flows from Continuing Operations (GAAP) 2.7$ 2.8$ 3.1$

Less: purchases of property, plant & equipment (capital expenditures) from continuing operations

(GAAP) (0.5) (0.5) (0.6)

Plus: proceeds from sale of property, plant & equipment (capital disposals) from continuing

operations (GAAP) 0.0 0.1 0.0

Free Cash Flow from Continuing Operations (Non-GAAP) 2.2$ 2.4$ 2.5$

Adjusted Net Earnings from Continuing Operations: 2014 2015 2016

1.6$ 1.7$ 2.2$

Pretax amortization of acquisition-related intangible assets 0.3 A 0.4 A 0.6 A

Pretax charge for early extinguishment of borrowings - - 0.2 B

Pretax acquisition-related transaction costs deemed significant, change in control payments,

restructuring costs and fair value adjustments to inventory and deferred revenue

- 0.2 C 0.1 D

Pretax gain on sales of marketable equity securities (0.1) E - -

Pretax gain on sales of investments - - (0.2) F

Tax effect of all adjustments reflected above - (0.1) G (0.3) G

Discrete tax adjustments and other tax-related adjustments 0.1 H (0.1) H (0.1) H

1.9$ 2.1$ 2.5$

Net Earnings from Continuing Operations (GAAP)

Adjusted Net Earnings from Continuing Operations (Non-GAAP)

Years Ended December 31

Non-GAAP Reconciliations

Ratio of Free Cash Flow to Adjusted Net Earnings from Continuing Operations ($ in

billions): 2014 2015 2016

2014 - 2016

Average

(rounded to

nearest 5%)

Free Cash Flow from Continuing Operations (Non-GAAP) 2.2$ 2.4$ 2.5$

Adjusted Net Earnings from Continuing Operations (Non-GAAP) 1.9 2.1 2.5

Free Cash Flow from Continuing Operations to Adjusted Net Earnings from Continuing Operations

Conversion Ratio (Non-GAAP) ~115% ~110% ~100% >100%

We define free cash flow as operating cash flows from continuing operations, less payments for purchases of property, plant and equipment from continuing

operations (“capital expenditures”) plus the proceeds from the sale of plant, property and equipment from continuing operations (“capital disposals”).

Non-GAAP Reconciliations

Adjusted Net Earnings from Continuing Operations Notes

A

2014 2015 2016

Pretax $ 0.3 $ 0.4 $ 0.6

After-tax 0.2 0.3 0.4

B

C

Amortization of acquisition-related intangible assets in the following historical periods ($ in billions) (only the pretax amounts set forth

below are reflected in the amortization line item above):

Years Ended December 31

Charge for early extinguishment of borrowings ($0.2 billion pretax as presented in this line item, $0.1 billion after-tax) incurred in the third

quarter of 2016. The Company did not incur any charges related to the early extinguishment of borrowings in 2014 or 2015, and therefore

no such elimination item is reflected in the calculation of Adjusted Net Earnings From Continuing Operations for any other period

presented.

Fair value adjustments to inventory ($0.02 billion pretax as presented in this line item, $0.02 billion after-tax) incurred in the year ended

December 31, 2015, in connection with the acquisition of Nobel Biocare. Acquisition-related transaction costs deemed significant ($0.02

billion pretax as presented in this line item, $0.02 billion after-tax), change in control payments, and fair value adjustments to inventory

and deferred revenue, net of the impact of freezing pension benefits, in each case related primarily to the acquisition of Pall Corporation

and incurred in the year ended December 31, 2015 ($0.1 billion pretax as presented in this line item, $0.08 billion after-tax). The Company

deems acquisition-related transaction costs incurred in a given period to be significant (generally relating to the Company's larger

acquisitions) if it determines that such costs exceed the range of acquisition-related transaction costs typical for the Company in a given

period.

Non-GAAP Reconciliations

Adjusted Net Earnings from Continuing Operations Notes

A

2014 2015 2016

Pretax $ 0.3 $ 0.4 $ 0.6

After-tax 0.2 0.3 0.4

B

C

Amortization of acquisition-related intangible assets in the following historical periods ($ in billions) (only the pretax amounts set forth

below are reflected in the amortization line item above):

Years Ended December 31

Charge for early extinguishment of borrowings ($0.2 billion pretax as presented in this line item, $0.1 billion after-tax) incurred in the third

quarter of 2016. The Company did not incur any charges related to the early extinguishment of borrowings in 2014 or 2015, and therefore

no such elimination item is reflected in the calculation of Adjusted Net Earnings From Continuing Operations for any other period

presented.

Fair value adjustments to inventory ($0.02 billion pretax as presented in this line item, $0.02 billion after-tax) incurred in the year ended

December 31, 2015, in connection with the acquisition of Nobel Biocare. Acquisition-related transaction costs deemed significant ($0.02

billion pretax as presented in this line item, $0.02 billion after-tax), change in control payments, and fair value adjustments to inventory

and deferred revenue, net of the impact of freezing pension benefits, in each case related primarily to the acquisition of Pall Corporation

and incurred in the year ended December 31, 2015 ($0.1 billion pretax as presented in this line item, $0.08 billion after-tax). The Company

deems acquisition-related transaction costs incurred in a given period to be significant (generally relating to the Company's larger

acquisitions) if it determines that such costs exceed the range of acquisition-related transaction costs typical for the Company in a given

period.

D

E

F

G

H

Gain on sales of investments in the year ended December 31, 2016 ($0.2 billion pretax as presented in this line item, $0.1 billion after-tax).

This line item reflects the aggregate tax effect of all nontax adjustments reflected in the table above. In addition, the footnotes above

indicate the after-tax amount of each individual adjustment item. Danaher estimates the tax effect of the adjustment items identified in

the reconciliation schedule above by applying Danaher's overall estimated effective tax rate to the pretax amount, unless the nature of

the item and/or the tax jurisdiction in which the item has been recorded requires application of a specific tax rate or tax treatment, in

which case the tax effect of such item is estimated by applying such specific tax rate or tax treatment.

For 2014, discrete income tax charges net of discrete income tax gains and benefits from a lower than expected effective tax rate

(compared to the anticipated 2014 effective tax rate publicly communicated in December 2013), due primarily to year-end tax law

changes for the year ended December 31, 2014. For 2015, discrete income tax gains net of discrete income tax charges ($0.1 billion)

incurred in the year ended December 31, 2015. For 2016, discrete income tax gains net of discrete income tax charges and Fortive

separation-related tax costs related to repatriation of earnings and legal entity realignments incurred in the year ended December 31,

2016 ($0.1 billion).

Acquisition-related transaction costs deemed significant ($0.01 billion pretax as presented in this line item, $0.01 billion after-tax), change

in control payments and restructuring costs ($0.05 billion pretax as presented in this line item, $0.03 billion after-tax), and fair value

adjustments to inventory and deferred revenue ($0.02 billion pretax as presented in this line item, $0.01 billion after-tax), in each case

related primarily to the acquisition of Cepheid and incurred in the year ended December 31, 2016.

Gain on sales of marketable equity securities in the year ended December 31, 2014 ($0.1 billion pretax is presented in this line item, $0.08

billion after-tax).

Non-GAAP Reconciliations

Adjusted Forecasted Diluted Net Earnings Per Share from Continuing Operations

Low End of

Guidance Range

High End of

Guidance

Range

3.50$ 3.60$

Pretax amortization of acquisition-related intangible assets 0.95 A 0.95 A

Tax effect of all adjustments reflected above (0.20) B (0.20) B

4.25$ 4.35$

1

Year Ending December 31, 2018

Forecasted Diluted Net Earnings Per Share from Continuing Operations

(GAAP) 1

Forecasted Adjusted Diluted Net Earnings Per Share from Continuing

Operations (Non-GAAP) 1

The forward-looking estimates set forth above do not reflect future gains and charges that are inherently difficult to

predict and estimate due to their unknown timing, effect and/or significance, such as certain future gains or losses on

the sale of investments, acquisition or divestiture-related gains or charges and discrete tax items.

Non-GAAP Reconciliations

Adjusted Forecasted Diluted Net Earnings Per Share from Continuing Operations Notes

A

Year Ending

December 31,

2018 E

Pretax $ 671

After-tax 530

B

Amortization of acquisition-related intangible assets as quantified below ($ in millions) (only the pretax amounts set forth below are

reflected in the amortization line item above):

This line item reflects the aggregate tax effect of all nontax adjustments reflected in the table above. In addition, the footnote above

indicates the after-tax amount of each individual adjustment item. Danaher estimates the tax effect of the adjustment items identified in

the reconciliation schedule above by applying Danaher's overall estimated effective tax rate to the pretax amount, unless the nature of

the item and/or the tax jurisdiction in which the item has been recorded requires application of a specific tax rate or tax treatment, in

which case the tax effect of such item is estimated by applying such specific tax rate or tax treatment.