2017 CAGNY Presentation - Kellogg'sinvestor.kelloggs.com/.../2017/cagny-presentation.pdf · Kellogg...

28

Kellogg Company February 21, 2017 Page 1 of 28 CAGNY February 21, 2017 CAGNY 2017 Forward-Looking Statements CAGNY 2017 2 This presentation contains, or incorporates by reference, “forward-looking statements” with projections concerning, among other things, the Company’s global growth and efficiency program (Project K), the integration of acquired businesses, the Company’s strategy, zero-based budgeting, and the Company’s sales, earnings, margin, operating profit, costs and expenditures, interest expense, tax rate, capital expenditure, dividends, cash flow, debt reduction, share repurchases, costs, charges, rates of return, brand building, ROIC, working capital, growth, new products, innovation, cost reduction projects, workforce reductions, savings, and competitive pressures. Forward-looking statements include predictions of future results or activities and may contain the words “expects,” “believes,” “should,” “will,” “anticipates,” “projects,” “estimates,” “implies,” “can,” or words or phrases of similar meaning. The Company’s actual results or activities may differ materially from these predictions. The Company’s future results could also be affected by a variety of factors, including the ability to implement Project K (including the exit from its Direct Story Delivery system) as planned, whether the expected amount of costs associated with Project K will differ from forecasts, whether the Company will be able to realize the anticipated benefits from Project K in the amounts and times expected, the ability to realize the anticipated benefits from Revenue Growth Management, the ability to realize the anticipated benefits and synergies from the acquisitions in the amounts and at the times expected, the impact of competitive conditions; the effectiveness of pricing, advertising, and promotional programs; the success of innovation, renovation and new product introductions; the recoverability of the carrying value of goodwill and other intangibles; the success of productivity improvements and business transitions; commodity and energy prices; labor costs; disruptions or inefficiencies in supply chain; the availability of and interest rates on short-term and long-term financing; actual market performance of benefit plan trust investments; the levels of spending on systems initiatives, properties, business opportunities, integration of acquired businesses, and other general and administrative costs; changes in consumer behavior and preferences; the effect of U.S. and foreign economic conditions on items such as interest rates, statutory tax rates, currency conversion and availability; legal and regulatory factors including changes in food safety, advertising and labeling laws and regulations; the ultimate impact of product recalls; business disruption or other losses from war, terrorist acts or political unrest; and other items. Forward-looking statements speak only as of the date they were made, and the Company undertakes no obligation to update them publicly. This presentation includes non‐GAAP financial measures. Please refer to the Appendices for a reconciliation of these non‐GAAP financial measures to the most directly comparable GAAP financial measures. Management believes that the use of such non-GAAP measures assists investors in understanding the underlying operating performance of the company and its segments.

Transcript of 2017 CAGNY Presentation - Kellogg'sinvestor.kelloggs.com/.../2017/cagny-presentation.pdf · Kellogg...

Kellogg Company February 21, 2017

Page 1 of 28

CAGNYFebruary 21, 2017

CAGNY 2017

Forward-Looking Statements

CAGNY 2017 2

This presentation contains, or incorporates by reference, “forward-looking statements” with projections concerning, among other things, the Company’s global growth and efficiency program (Project K), the integration of acquired businesses, the Company’s strategy, zero-based budgeting, and the Company’s sales, earnings, margin, operating profit, costs and expenditures, interest expense, tax rate, capital expenditure, dividends, cash flow, debt reduction, share repurchases, costs, charges, rates of return, brand building, ROIC, working capital, growth, new products, innovation, cost reduction projects, workforce reductions, savings, and competitive pressures. Forward-looking statements include predictions of future results or activities and may contain the words “expects,” “believes,” “should,” “will,” “anticipates,” “projects,” “estimates,” “implies,” “can,” or words or phrases of similar meaning.

The Company’s actual results or activities may differ materially from these predictions. The Company’s future results could also be affected by a variety of factors, including the ability to implement Project K (including the exit from its Direct Story Delivery system) as planned, whether the expected amount of costs associated with Project K will differ from forecasts, whether the Company will be able to realize the anticipated benefits from Project K in the amounts and times expected, the ability to realize the anticipated benefits from Revenue Growth Management, the ability to realize the anticipated benefits and synergies from the acquisitions in the amounts and at the times expected, the impact of competitive conditions; the effectiveness of pricing, advertising, and promotional programs; the success of innovation, renovation and new product introductions; the recoverability of the carrying value of goodwill and other intangibles; the success of productivity improvements and business transitions; commodity and energy prices; labor costs; disruptions or inefficiencies in supply chain; the availability of and interest rates on short-term and long-term financing; actual market performance of benefit plan trust investments; the levels of spending on systems initiatives, properties, business opportunities, integration of acquired businesses, and other general and administrative costs; changes in consumer behavior and preferences; the effect of U.S. and foreign economic conditions on items such as interest rates, statutory tax rates, currency conversion and availability; legal and regulatory factors including changes in food safety, advertising and labeling laws and regulations; the ultimate impact of product recalls; business disruption or other losses from war, terrorist acts or political unrest; and other items.

Forward-looking statements speak only as of the date they were made, and the Company undertakes no obligation to update them publicly.

This presentation includes non‐GAAP financial measures. Please refer to the Appendices for a reconciliation of these non‐GAAP financial measures to the most directly comparable GAAP financial measures. Management believes that the use of such non-GAAP measures assists investors in understanding the underlying operating performance of the company and its segments.

Kellogg Company February 21, 2017

Page 2 of 28

CAGNY 2017

CFO Transition

Thanks, Ron! Welcome, Fareed!

3

CAGNY 2017

Agenda

• Kellogg Company – Solidly on 2020 Growth Plan

• Kellogg North America – Prioritizing to Win

• U.S. Snacks – Transforming our Business

• Closing Remarks

4

Kellogg Company February 21, 2017

Page 3 of 28

CAGNY 2017

2020 Growth Plan – Kellogg Company

5

CAGNY 2017

Win in Breakfast

StabilizeCore 4

DevelopedMarkets

GrowEmergingMarkets

6

Kellogg Company February 21, 2017

Page 4 of 28

CAGNY 2017

Global Snacks Powerhouse

• Pringles growth in all Regions in 2016

• Dedicated Teams

• Revitalized Wholesome Snacks in International

2012 2013 2014 2015 2016

Kellogg International Snacks, in Kilos

+8%CAGR

2013-2016

Acquisition

7

CAGNY 2017

Emerging Markets Engine

Kellogg Emerging-Markets Volume in Tons

• Household penetration• Geographic expansion

• Acquisitions

Plus: • Joint Ventures

2012 2016

4.5%CAGR

2013-2016x-JVs and Parati

Joint Ventures

Parati, 2017

8

Kellogg Company February 21, 2017

Page 5 of 28

CAGNY 2017

Win Where the Shopper Shops

Increased small can

availability

Winning Wholesome

Snacks

Evolved Cereal offer

to win

Expanding distribution in emerging markets

High Frequency Stores

Route to Market Winning Portfolio

E-Commerce

• Digital Shelf• Click & Collect• Home Delivery

9

• Local distributors• Acquired capabilities and

scale

CAGNY 2017

Margin Expansion

• Ongoing• Project K• ZBB

Invest forImpact

PriceRealization

Productivity

10.0%

12.5%

15.0%

17.5%

20.0%

2015 2016 2017E 2018E

Currency-Neutral Comparable Basis, Operating Profit as % of Net Sales, Excluding Venezuela *

14.4%

• ROI• New Marketing model

~18%

• Revenue Growth Management

On-TrendFood

• Renovation• Innovation

15.4%+100+ bp

10

* See Appendix for reconciliation.

Kellogg Company February 21, 2017

Page 6 of 28

CAGNY 2017

Agenda

• Kellogg Company – Solidly on 2020 Growth Plan

• Kellogg North America – Prioritizing to Win

• U.S. Snacks – Transforming our Business

• Closing Remarks

11

CAGNY 2017

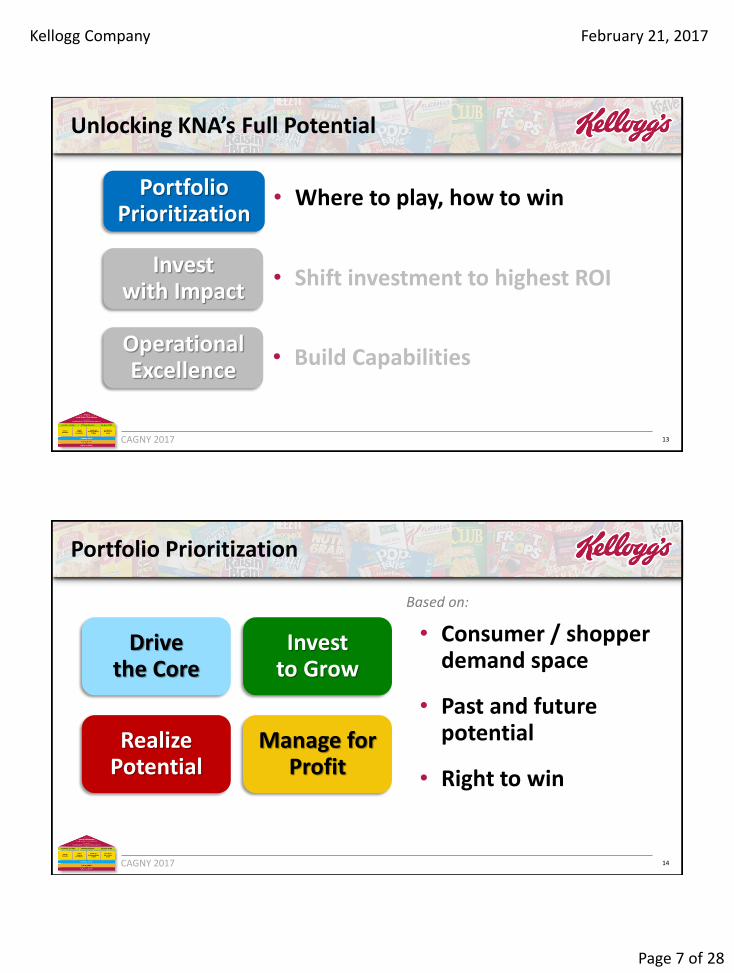

Kellogg North America

Snacks Morning Foods

Specialty

Frozen

Canada

Kashi

North AmericaOther

Category Share Position(a)

RTEC

Toaster Pastries

Crackers

Cookies

Wholesome Snacks

Frozen Waffles

Frozen Veggie(b)

#1

#1

#2

#2

#2

#1

#1(a) A.C. Nielsen, xAOC, 52 weeks through 12/31/16(b) Frozen Meat Substitutes

A Diverse Portfolio / Strong Category-Leading Positions

12

Net Sales

Kellogg Company February 21, 2017

Page 7 of 28

CAGNY 2017

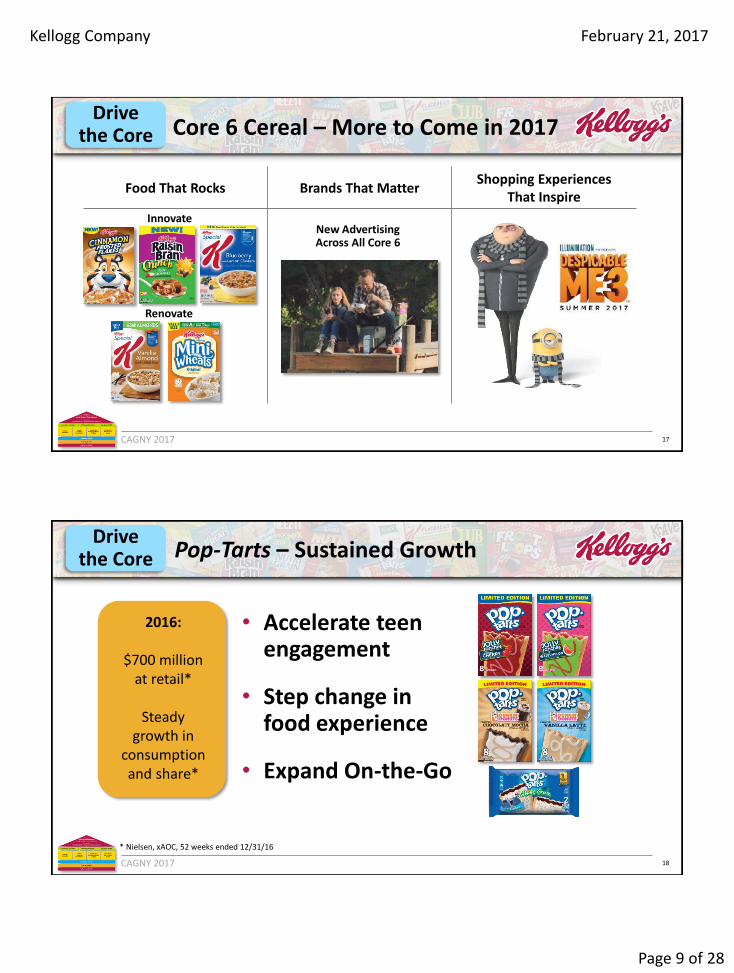

Unlocking KNA’s Full Potential

Invest with Impact

Portfolio Prioritization

Operational Excellence

• Where to play, how to win

• Shift investment to highest ROI

• Build Capabilities

13

CAGNY 2017

Portfolio Prioritization

Invest to Grow

Drive the Core

Manage for Profit

Realize Potential

• Consumer / shopper demand space

• Past and future potential

• Right to win

Based on:

14

Kellogg Company February 21, 2017

Page 8 of 28

CAGNY 2017

Driving the Core – Improving Performance

Drive the Core

• Biggest Core brands already improving share

• Significant scale

• High margin

• Powerful brand equities, cover broad set of needs

15

~40% of KNA sales

CAGNY 2017

Core 6 Cereal – Growing Share

• Our improved consumption and share performance has been driven by Core 6 brands

22.3

22.722.9

2014 2015 2016

Share of U.S. RTEC CategoryCore 6 Kellogg’s Brands

Source: Nielsen, xAOC, 52-week periods

Drive the Core

16

Kellogg Company February 21, 2017

Page 9 of 28

CAGNY 2017

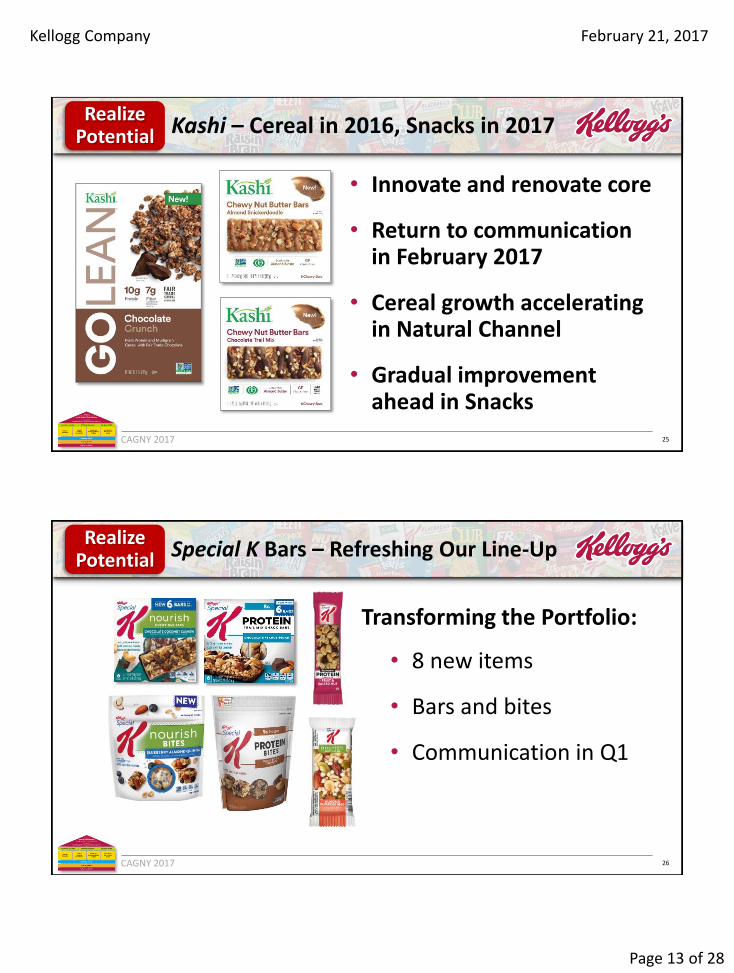

Food That Rocks Brands That MatterShopping Experiences

That Inspire

Innovate

Renovate

New Advertising Across All Core 6

Core 6 Cereal – More to Come in 2017Drive

the Core

17

CAGNY 2017

Pop-Tarts – Sustained Growth

• Accelerate teen engagement

• Step change in food experience

• Expand On-the-Go

* Nielsen, xAOC, 52 weeks ended 12/31/16

Drive the Core

2016:

$700 million at retail*

Steady growth in

consumption and share*

18

Kellogg Company February 21, 2017

Page 10 of 28

CAGNY 2017

Eggo – Returning to Growth

• Core renovation (removal of artificials)

• Family fun

• Increased brand building 2017

Drive the Core

2016:

$691 million at retail*

Consumption and share* returned to

growth in Q4

* Nielsen, xAOC; retail sales 52 weeks ended 12/31/16; Q4 performance refers to 13 weeks ended 12/31/16. 19

CAGNY 2017

Invest to Grow – Building on Momentum

• Strong growth

• High margins

• Unique and differentiated

• Significant potential to expand consumption

Invest to Grow

~25% of KNA sales

20

Kellogg Company February 21, 2017

Page 11 of 28

CAGNY 2017

Cheez-It – Stronger Than Ever

• Increase investment in core

• Expand across channels and occasions

• Source from adjacencies

Share Leader in Crackers (2016)

1996 2016

Over $1 Billion in U.S. Net Sales

Consecutive Years of Growth20

+8.6% in 20164-year CAGR ≈6% Growth

Invest to Grow

21

CAGNY 2017

• Increase investment in core

• Expand across channels

• Unlock occasion through small sizes

+4% CAGRU.S. Net Sales, 2013-2016

Pringles – More to GrowInvest

to Grow

22

Kellogg Company February 21, 2017

Page 12 of 28

CAGNY 2017

• Invest in core

• Channels and occasions

• Capitalize on seasonal and licensed opportunities

Rice Krispies Treats – Solid MomentumInvest

to Grow

+9% CAGRNet Sales, 2013-2016

2013 2014 2015 2016

23

* Net Sales in U.S.

CAGNY 2017

Realize Potential

Realize Potential – Investing to Get Back On Trend

~15% of KNA sales

• Significant potential but underperforming

• Investing in food and packaging

• Sales decline near-term, before returning to growth

24

Kellogg Company February 21, 2017

Page 13 of 28

CAGNY 2017

• Innovate and renovate core

• Return to communication in February 2017

• Cereal growth acceleratingin Natural Channel

• Gradual improvement ahead in Snacks

Realize Potential Kashi – Cereal in 2016, Snacks in 2017

25

CAGNY 2017

• 8 new items

• Bars and bites

• Communication in Q1

Realize Potential Special K Bars – Refreshing Our Line-Up

26

Transforming the Portfolio:

Kellogg Company February 21, 2017

Page 14 of 28

CAGNY 2017

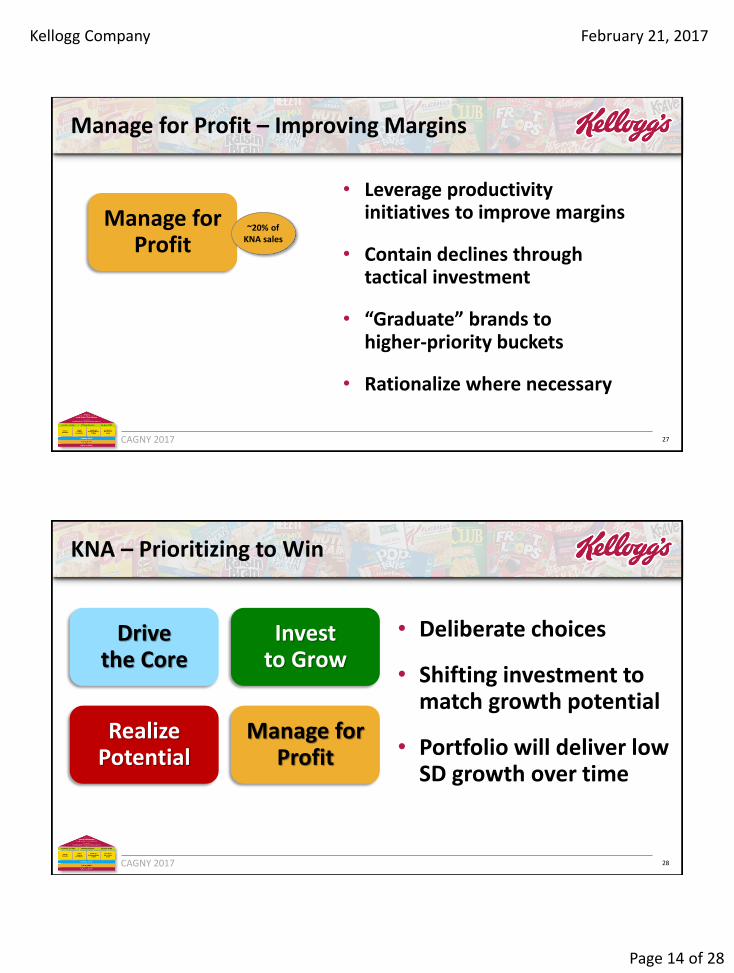

Manage for Profit – Improving Margins

Manage for Profit

• Leverage productivity initiatives to improve margins

• Contain declines through tactical investment

• “Graduate” brands to higher-priority buckets

• Rationalize where necessary

~20% of KNA sales

27

CAGNY 2017

KNA – Prioritizing to Win

Invest to Grow

Drive the Core

Manage for Profit

Realize Potential

• Deliberate choices

• Shifting investment to match growth potential

• Portfolio will deliver low SD growth over time

28

Kellogg Company February 21, 2017

Page 15 of 28

CAGNY 2017

Unlocking KNA’s Full Potential

Invest with Impact

Portfolio Prioritization

• Where to play, how to win

• Shift investment to highest ROI

• Build CapabilitiesOperational Excellence

29

CAGNY 2017

• Deploying resources to highest ROI brands and activities

• Moving from “Push” to “Pull” in Snacks

• “Agile” ROI – Marketing Mix Model moving to real-time

• Migrating with consumer to digital

Invest with Impact – Prioritization & Measurement

30

Kellogg Company February 21, 2017

Page 16 of 28

CAGNY 2017

Unlocking KNA’s Full Potential

Invest with Impact

Portfolio Prioritization

Operational Excellence

• Where to play, how to win

• Shift investment to highest ROI

• Build Capabilities

31

CAGNY 2017

Building New Capabilities

• New Marketing Model Data Analytics & Agile ROI

“Demand Chain” Shopper Segmentation

• Revenue Growth Management Pack formats

Price-pack architecture

• Productivity Zero-Based Budgeting

• Single Go-to-Market Model / E2E Supply Chain DSD Exit unlocks resources to accelerate growth

32

Kellogg Company February 21, 2017

Page 17 of 28

CAGNY 2017

Summary

• Portfolio prioritization

• Investing for impact

• Driving operational excellence

Prioritizing to Win:

• Margin expansion

• Improved core brand performanceProgress Already Evident:

• Exiting DSD

• Transforming U.S. SnacksTransformation Continues:

33

CAGNY 2017

Agenda

• Kellogg Company – Solidly on 2020 Growth Plan

• Kellogg North America – Prioritizing to Win

• U.S. Snacks – Transforming our Business

• Closing Remarks

34

Kellogg Company February 21, 2017

Page 18 of 28

CAGNY 2017

U.S. Snacks – Portfolio Overview

35

Crackers

Cookies

Bars

Salty

Fruit Snacks

2016 Net Sales$3.2 billion

Retail Sales*$1.0 bn

Retail Sales*$0.2 bn

each

Retail Sales*$0.5 bn

Retail Sales*$0.2 bn

each

Retail Sales*$0.7 bn

* Retail sales figures are from Nielsen, xAOC, with Cheez-It figures xAOC+Convenience; 52 weeks ended 12/31/2016

CAGNY 2017

Exiting DSD – Rationale & Benefits

• More effective and efficient route to market= Lower costs, higher fill rate, lower

inventory

• Investment to accelerate growth= More support across more brands

• Scale behind One Kellogg route to market= Cross category promotions

Drivers to Exit DSD

• Category requirements not dependent on DSD

• Consumer splintering trips across more channels

• Evolving Customer landscape not serviced by DSD

• Increased sophistication in Customer warehouse

• Higher share & fill-rates in warehouse channel

US Snacks Benefits

36

Kellogg Company February 21, 2017

Page 19 of 28

CAGNY 2017

Simplified Route to Market – Customer Benefits

SIMPLIFIED ROUTE TO MARKET CUSTOMER BENEFITS

1. Margin Expansion

2. Inventory Management

3. Increased Growth

37

CAGNY 2017

Transition Plan in Place

• DSD network• Incentive plans• Manufacturing network

Infrastructure Intact1.

Seasoned Transition Team

3. • Playbook from M&A integrations• Fully resourced, cross-functional team • Retailer support

Established Warehouse System 2. • Already serves 75% of Kellogg U.S.

• IT, invoicing and customer service in place

38

Kellogg Company February 21, 2017

Page 20 of 28

CAGNY 2017

Financial Impact

2016 2017 2018 2019 KNA 2016

US Snacks Operating Margin Expansion*

* Currency-neutral comparable basis

• Accelerated Net Sales Growth after Transition

• Increased Brand Investment

• Higher OP Margin

CAGNY 2017

US Snacks – Roadmap

Reset Transform Accelerate

2016 2017 2018/2019

• Improve Efficiencies

• Focus Investments

• Establish RGM Capability

• Exit DSD

• Optimize Portfolio

• From “Push” to “Pull”

• Increase Brand Investment

• Stronger, leaner portfolio

• Joint Business Partnership

40

Kellogg Company February 21, 2017

Page 21 of 28

CAGNY 2017

Reset

Reset the Business Fundamentals

• Project K Network Consolidation• Launched ZBB

• Focused on Priority Brands− Cheez-It, Pringles, Rice Krispies Treats

• Established Price-Pack Architectures

1.

2.

3.

Improve Efficiencies

Focus Investments

Revenue Growth Management

41

CAGNY 2017

The Playbook – 2016 Cheez-It Pilot

Invest to Grow Platform InnovationExpand Occasions/Formats

Net Sales* • Gross Margin* • Consumption • Share

Big increaseIn Brand Building

Dial-up Digital

Expand into Social/Mobile

42

* Currency-neutral comparable basis

Kellogg Company February 21, 2017

Page 22 of 28

CAGNY 2017

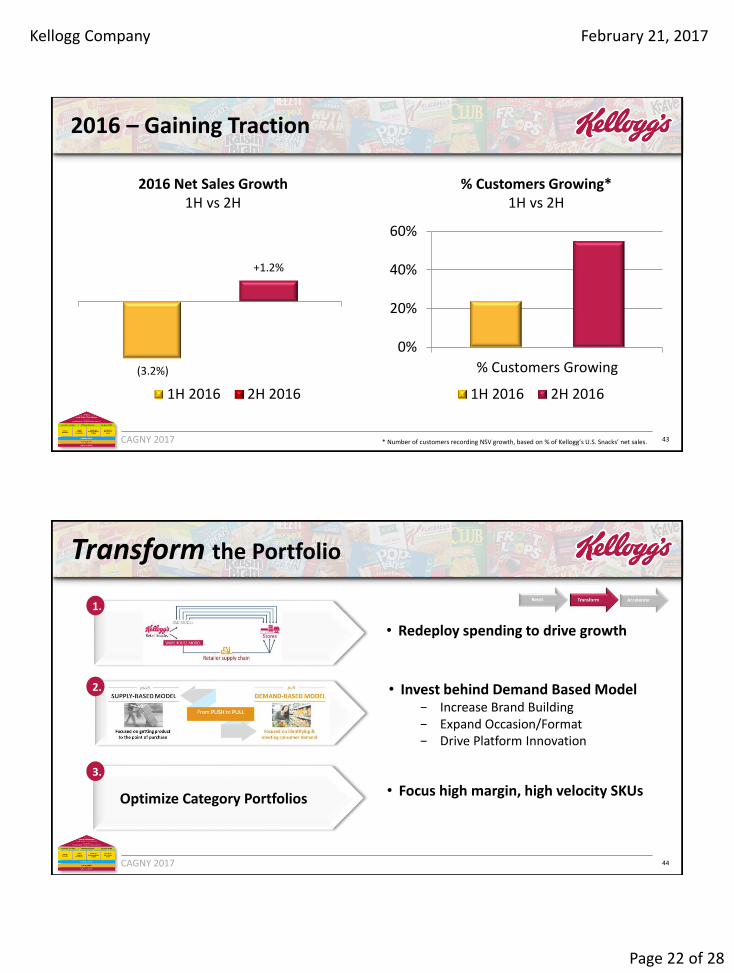

2016 – Gaining Traction

2016 Net Sales Growth1H vs 2H

% NSV

1H 2016 2H 2016

(3.2%)

+1.2%

% Customers Growing*1H vs 2H

0%

20%

40%

60%

% Customers Growing

1H 2016 2H 2016

43* Number of customers recording NSV growth, based on % of Kellogg’s U.S. Snacks’ net sales.

CAGNY 2017

Transform the Portfolio

• Redeploy spending to drive growth

1.

• Invest behind Demand Based Model− Increase Brand Building− Expand Occasion/Format− Drive Platform Innovation

2.

• Focus high margin, high velocity SKUs

3.

Optimize Category Portfolios

44

Kellogg Company February 21, 2017

Page 23 of 28

CAGNY 2017

Accelerate Growth Behind “Pull” Model

• Higher investment, higher ROI• Broader support across portfolio

• Grow new margin enhanced portfolio • Higher-velocity shelf set

• Launch cross-category programs• Partner of Choice for eCommerce

1.

2.

3.

Increase Brand Investment

Stronger, Leaner Portfolio

Joint Business Partnership

45

CAGNY 2017

Invest to Grow

Cheez-It – Sustain Momentum

Increased Media Investment--Multi-cultural--Millennials

Expand Occasions /Formats Innovation

Invest to Grow

46

Kellogg Company February 21, 2017

Page 24 of 28

CAGNY 2017

Pringles – Dial Up Growth

• Increased Media, Dial-up Digital

• Millennial & Multi-cultural Focus

• Tent Pole Merch Activation

Invest to Grow Expand Occasions /Formats Innovation

Invest to Grow

47

CAGNY 2017

Rice Krispies Treats – Sustain Growth

New Campaign--Millennial Focus--Multi-cultural

Seasonal Minis/Fun Sheets

Invest to Grow Expand Occasions /Formats Innovation

Invest to Grow

48

Kellogg Company February 21, 2017

Page 25 of 28

CAGNY 2017

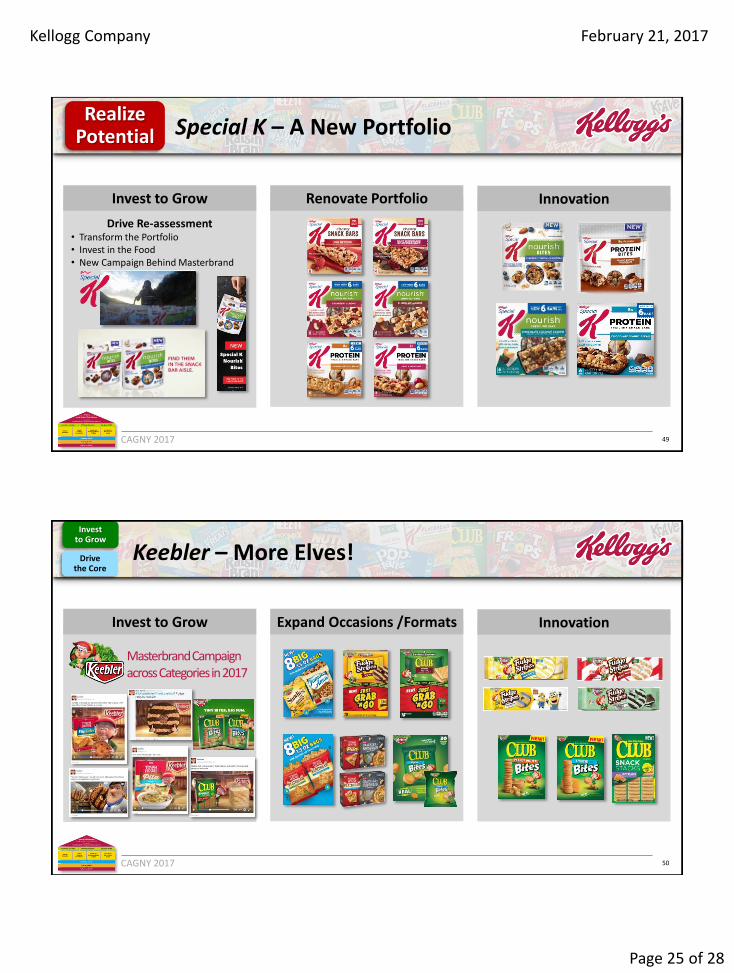

Special K – A New Portfolio

Drive Re-assessment• Transform the Portfolio• Invest in the Food• New Campaign Behind Masterbrand

Invest to Grow Renovate Portfolio Innovation

Realize Potential

49

CAGNY 2017

Keebler – More Elves!

Masterbrand Campaign across Categories in 2017

Invest to Grow Expand Occasions /Formats Innovation

Invest to Grow

Drive the Core

50

Kellogg Company February 21, 2017

Page 26 of 28

CAGNY 2017

In-store Activation – Stronger Than Ever

EstablishedTent-pole

Events

Pre-builtShipper & Modules

51

CAGNY 2017

Transforming Snacks

Good Progress Made in 2016

• Focused investment drove priority brands• Savings programs drove margin expansion• Sales turned to growth in 2H

DSD Exit Unlocks Resources for Accelerated growth

• Solid plans around transition• Boosting investment in Brand Building

A Stronger Kellogg Snacks is Emerging

• Better Growth and Profitability Over Time

52

Kellogg Company February 21, 2017

Page 27 of 28

CAGNY 2017

Agenda

• Kellogg Company – Solidly on 2020 Growth Plan

• Kellogg North America – Prioritizing to Win

• U.S. Snacks – Transforming our Business

• Closing Remarks

53

CAGNY 2017

In Summary…

54

Good Progress on 2020 Growth Plan• Stabilizing Developed RTEC• Expanding Snacks Worldwide• Building Scale in Emerging Markets• Increased Confidence in 2018 OP Margin Goal

KNA is Prioritizing to Win• Growing the brands in which we are investing• Investing in our food, and marketing for impact and ROI• Driving margin expansion

Transforming U.S. Snacks• Build on momentum of invest-to-grow brands• DSD exit enables step-change in investment• Positioning portfolio for accelerated growth

Kellogg Company February 21, 2017

Page 28 of 28

Q&AQ&A

55

CAGNY 2017

Appendix

Kellogg Company and Subsidiaries

Reconciliation of Non-GAAP Amounts - Reported Operating Margin to Comparable Operating Margin

excluding Venezuela

Year ended 2016 and 2015

2016 2015

Reported operating margin 10.7% 8.1%

Mark-to-market -2.0% -3.3%

Project K and cost reduction activities -2.5% -2.4%

Other costs impacting comparability 0.0% 0.5%

Integration and transaction costs -0.1% -0.2%

Venezuela remeasurement -0.1% -0.9%

Comparable operating margin 15.4% 14.4%

Comparable operating margin excluding Venezuela 15.4% 14.4%

56