2016 Irish Hotels Market Briefing - crowe.ie · Total Revenue €57k €42k €61k +€4k Total...

36

2016 Irish Hotels Market Briefing 28 September 2016

Transcript of 2016 Irish Hotels Market Briefing - crowe.ie · Total Revenue €57k €42k €61k +€4k Total...

2016 Irish Hotels

Market Briefing 28 September 2016

1 © 2016 Crowe Horwath

Audit | Tax | Advisory

Audit | Tax | Advisory

Hotel Market Performance and Opportunities

Aiden Murphy, Crowe Horwath

28th September 2016

2 © 2016 Crowe Horwath

Introduction

Crowe Horwath release the 21st Edition of the Annual Hotel Industry Survey

3 © 2016 Crowe Horwath

Introduction

Current hotel performance – 2016 Annual Hotel Industry Survey

Dublin hotel market

Regional hotel market

Case study on Midlands & East performance

Pressures on maintaining profit growth

Results of the Crowe Horwath “Brexit” survey

Conclusions and Opportunities

4 © 2016 Crowe Horwath

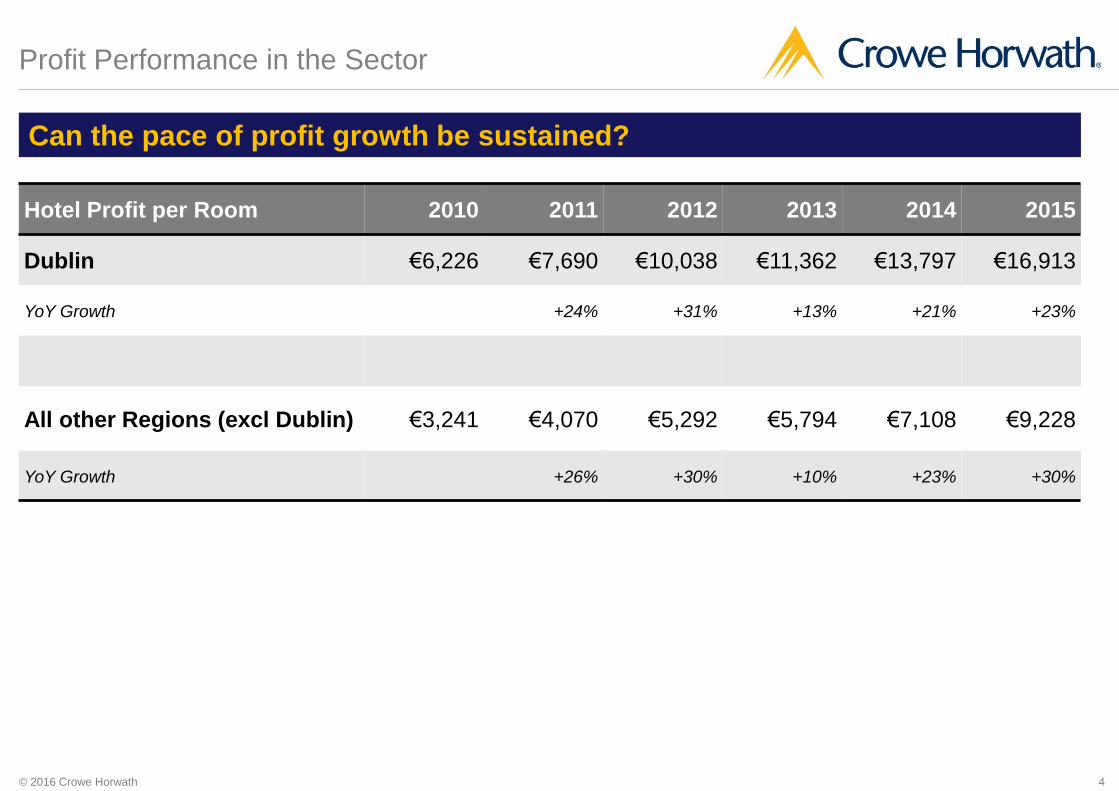

Profit Performance in the Sector

Can the pace of profit growth be sustained?

Hotel Profit per Room 2010 2011 2012 2013 2014 2015

Dublin €6,226 €7,690 €10,038 €11,362 €13,797 €16,913

YoY Growth +24% +31% +13% +21% +23%

All other Regions (excl Dublin) €3,241 €4,070 €5,292 €5,794 €7,108 €9,228

YoY Growth +26% +30% +10% +23% +30%

5 © 2016 Crowe Horwath

Constraints on the Sector

6 © 2016 Crowe Horwath

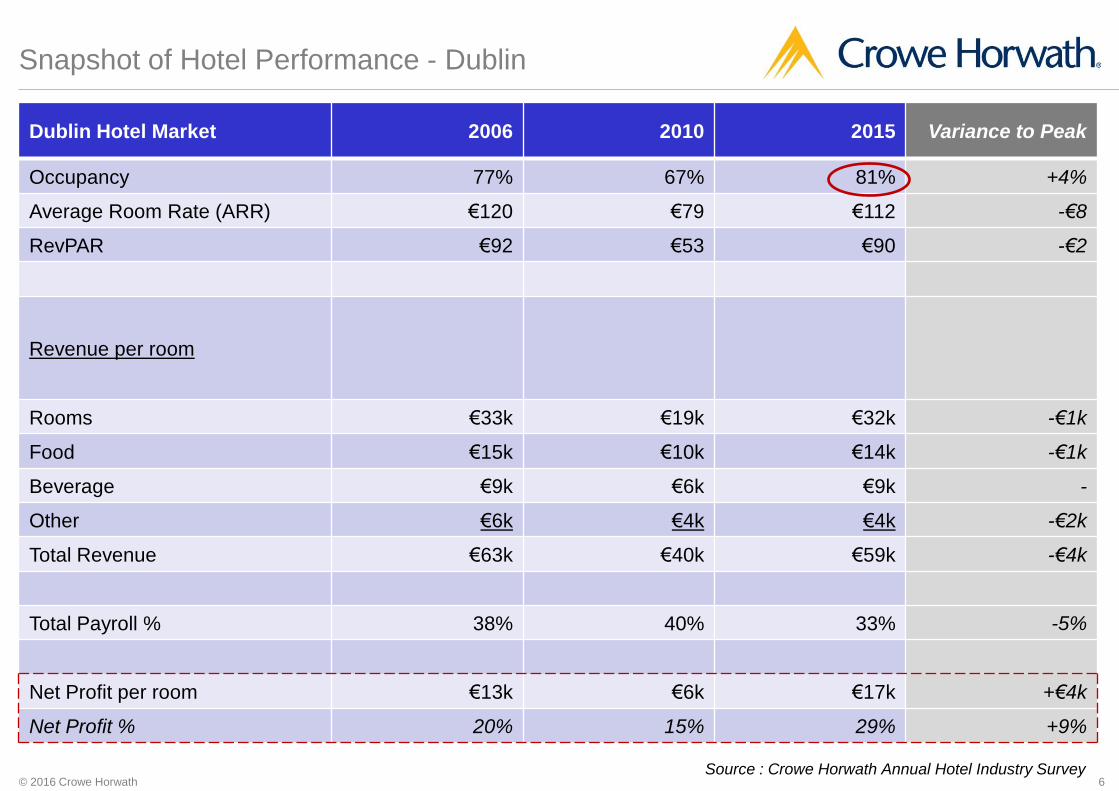

Snapshot of Hotel Performance - Dublin

Dublin Hotel Market 2006 2010 2015 Variance to Peak

Occupancy 77% 67% 81% +4%

Average Room Rate (ARR) €120 €79 €112 -€8

RevPAR €92 €53 €90 -€2

Revenue per room

Rooms €33k €19k €32k -€1k

Food €15k €10k €14k -€1k

Beverage €9k €6k €9k -

Other €6k €4k €4k -€2k

Total Revenue €63k €40k €59k -€4k

Total Payroll % 38% 40% 33% -5%

Net Profit per room €13k €6k €17k +€4k

Net Profit % 20% 15% 29% +9%

Source : Crowe Horwath Annual Hotel Industry Survey

7 © 2016 Crowe Horwath

Dublin’s Room Supply

19k

81%

50%

55%

60%

65%

70%

75%

80%

85%

5k

7k

9k

11k

13k

15k

17k

19k

21k

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Trends in Room Supply - Dublin

Bedrooms Occupancy

From 2001 to 2015 room supply

increased by 58% (+7k rooms)

8 © 2016 Crowe Horwath

Review of Dublin ADR by Month

Dublin ADR (€) 2007 2013 2014 2015 Peak to 2015

Variance

January 101.66 78.04 80.89 91.37 -10

February 111.88 82.82 85.23 98.59 -13

March 112.82 89.70 90.61 102.58 -10

April 113.12 85.84 86.65 102.87 -10

May 120.80 93.53 102.82 115.17 -6

June 127.05 99.71 106.91 120.81 -6

July 122.61 97.36 102.82 121.64 -1

August 122.87 98.04 109.02 123.31 0

September 127.49 99.49 110.42 123.97 -4

October 122.93 90.88 99.91 116.82 -6

November 112.19 86.87 98.95 114.63 +2

December 110.05 85.89 92.58 107.39 -3

Month on month comparisons show Average Room Rate has only exceeded the previous peak levels for 1 month only

9 © 2016 Crowe Horwath

Comparison of Dublin Performance to EU - 2015

Dublin ADR 2015 v Other European Cities

Dublin Occupancy 2015 v Other European Cities

-

€50

€100

€150

€200

€250

€300

50%

55%

60%

65%

70%

75%

80%

85%

While Dublin’s occupancy is the highest in

Europe, ADR is mid-table (ranking 15th).

Source: STR Global

10 © 2016 Crowe Horwath

Snapshot of Hotel Performance - Regional (excl Dublin)

Regional Hotel Market 2007 2010 2015 Variance to Peak

Occupancy 66% 56% 66% -

Average Room Rate (ARR) €86 €70 €83 -€3

RevPAR €57 €39 €55 -€2

Revenue per room

Rooms €21k €14k €20k -€1k

Food €20k €15k €24k +€4k

Beverage €11k €9k €12k +€1k

Other €5k €4k €5k -

Total Revenue €57k €42k €61k +€4k

Total Payroll % 41% 43% 38% -3%

Net Profit per Room €8k €3k €9k +€1k

Net Profit % 14% 8% 15% +1%

Source : Crowe Horwath Annual Hotel Industry Survey

11 © 2016 Crowe Horwath

38k

66%

50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

5k

10k

15k

20k

25k

30k

35k

40k

45k

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Trends in Hotel Supply - Regions excl Dublin

Bedrooms Occupancy

Ireland’s Hotel Supply

Rooms by Region 2001 to 2015 # Rooms % Diff

Midlands and East +5k +62%

South West +2k +20%

Western Seaboard +3k +28%

Total +10k +34%

12 © 2016 Crowe Horwath

Snapshot of Hotel Performance – Midlands & East Market

Midlands & East Hotel Market 2006 2010 2015 Variance to Peak

Occupancy 63% 54% 65% +2%

Average Room Rate (ARR) €94 €76 €84 -€10

RevPAR €60 €41 €55 -€5

Revenue per room

Rooms €21k €15k €20k -€1k

Food €28k €18k €30k +€2k

Beverage €17k €10k €16k -€1k

Other €8k €6k €7k -€1k

Total Revenue €74k €49k €73k -€1k

Total Payroll % 40% 46% 38% -2%

Net Profit per room €10k €3k €11k +€1k

Net Profit % 14% 6% 15% +1%

Source : Crowe Horwath Annual Hotel Industry Survey

13 © 2016 Crowe Horwath

NI UK Source : Crowe Horwath Annual Hotel Industry Survey

Brexit – UK Visitors to Ireland as % of Total Visitors

1985 1995 2005 2015

UK Other Europe US/Canada ROW Source: CSO

21% 24%

20% 17%

23%

0%

5%

10%

15%

20%

25%

30%

All Hotels Dublin Midlands & East South West Western Seaboard

Hotel Bedroom Demand (2015) UK and NI Market Share

14 © 2016 Crowe Horwath

Survey issued September 2016, 3 months

after Brexit result

Replies from 80 hotels

82% of respondents in the Border region felt

that Brexit had directly impacted their

business in the last 3 months.

Respondents who answered “Yes” felt that

any impact to date was minimal.

Brexit Survey - Findings

Dublin 31%

Regional 54%

Border 15%

Profile of Respondents

Yes 43%

No 57%

Has the Brexit vote had a direct impact on your business in the last 3 months?

15 © 2016 Crowe Horwath

Hotelier Sentiment for next 12-15 Months

Increase / Remain the

Same 64%

Decrease 36%

Sentiment for Demand Levels

42%

21%

75%

58% 79% 25%

0%

20%

40%

60%

80%

100%

Dublin Regional Border

Demand By Region

Decrease Increase / Remain the Same

Decrease 13%

Increase / Remain the

Stay 87%

Sentiment for Average Room Rate

96% 88% 67% 0%

20%

40%

60%

80%

100%

Dublin Regional Border

Average Room Rate By Region

16 © 2016 Crowe Horwath

Conclusion and Opportunities for the Irish Hotel Sector

Demand has returned to a level which allows:

Opportunity to yield room rate

Need for additional room supply

Potential for new hotels in the Dublin market

Existing hoteliers will have the opportunity to expand

Repositioning of hotels (e.g. upgrade in hotel classifications)

Development of ground floor offering

Re-investment in the hotel product through capex programmes, lifting revenue

Barriers to entry remain – feasibility of new build, planning and funding

The above opportunities continue to drive asset value, transactions and

investment in the hotel sector.

17 © 2016 Crowe Horwath

Bastow Charleton Member Crowe Horwath International

Marine House

Clanwilliam Court

Dublin 2

Ireland

www.crowehorwath.ie

Thank You.

Aiden Murphy

Partner | Restructuring, Advisory & Insolvency

Hotel Investment Market in Ireland

Breakfast Briefing 28 September 2016

19 Cushman & Wakefield |

“Need to fast track hotel projects

in Dublin City is critical”

“€20m redevelopment of Dublin's

Ormond Hotel gets go ahead”

“New €40m, 257 bed hotel

gets green light” “Hudson Bay Group planning

new 263 bedroom hotel for

Dublin”

“Dublin faces hotel shortage as

visitor numbers rise”

“Hotel site ready to go in

Dublin city centre for €5m”

“Dublin is facing a hotel room

shortage that could stifle its

growth as a tourist hub”

Cushman & Wakefield |

Agenda Investment Market – H1 2016

• Where and what type of properties sold?

• Who’s selling?

• Who’s buying?

Development

• Need for development?

• Analysis of the supply pipeline

• Concerns

Conclusion

21 Cushman & Wakefield |

Market Transactions

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 (H1)

2 2 4

28

40

60 59

27

Number of Transactions 2009 - H1 2016

22 Cushman & Wakefield |

Source – Cushman & Wakefield Research

Type

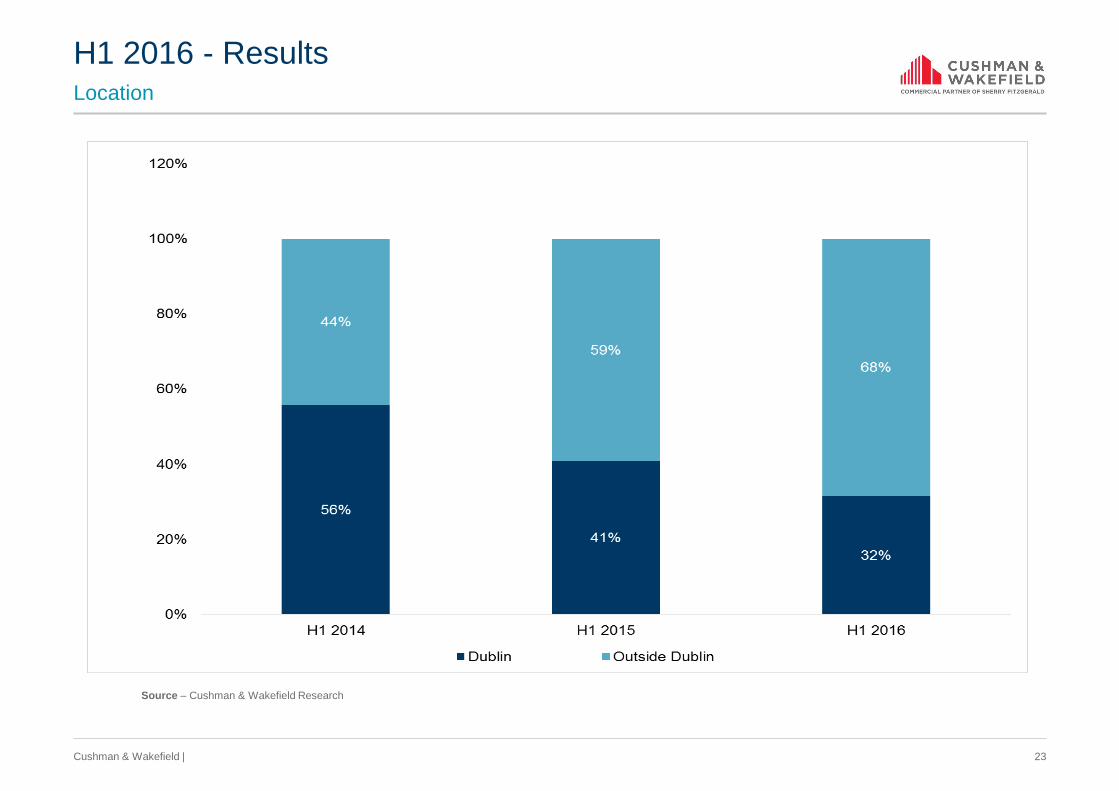

H1 2016 - Results

4 Star 52%

(14 Hotels)

3 Star 37%

(10 Hotels)

2 Star 4%

(1 Hotel)

Unknown 7%

(2 Hotels)

23 Cushman & Wakefield |

Location

Source – Cushman & Wakefield Research

H1 2016 - Results

24 Cushman & Wakefield |

Source – Cushman & Wakefield Research

Foreign 68%

Domestic 32%

Domestic 52%

Foreign 48%

H1 2015

Domestic v International Purchasers

H1 2016

74%

26%

Domestic Foreign

H1 2014

25 Cushman & Wakefield |

International buyers

27%

51% 17%

5%

26 Cushman & Wakefield |

Changing Vendors and Changing Purchasers?

Vendors of

last 5 years

Receivership Focussed

Current Vendors Consensual Sales

Purchasers of

last 5 years • Opportunity Funds

• High Net Worth Investors

• Smaller Domestic Funds

Current

Purchasers • Institutional Type

Purchasers

• Building Portfolios

27 Cushman & Wakefield |

Activity

• Sales numbers levelled off

• Few distressed properties remaining with NAMA

and main Banks

• Future activity likely to be initiated by New Loan

Holders and Resales

• Critical need for Development in Dublin

28 Cushman & Wakefield |

SUPPLY DEMAND

29 Cushman & Wakefield |

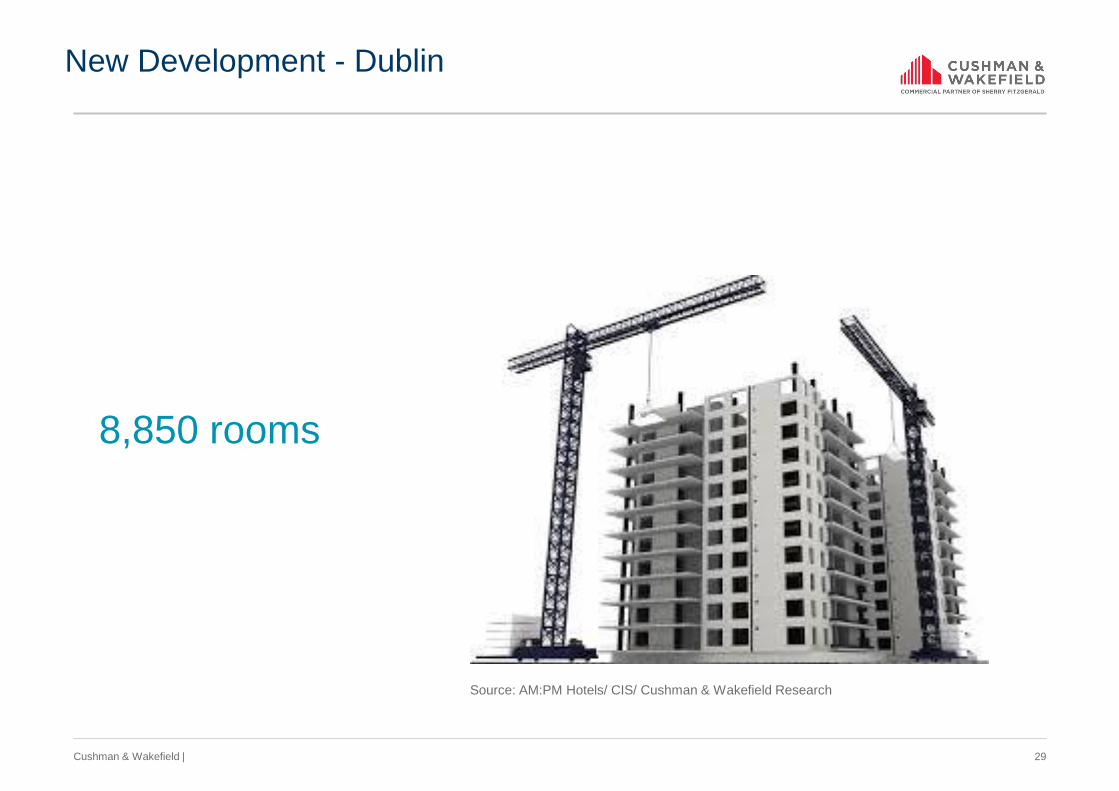

New Development - Dublin

8,850 rooms

Source: AM:PM Hotels/ CIS/ Cushman & Wakefield Research

30 Cushman & Wakefield |

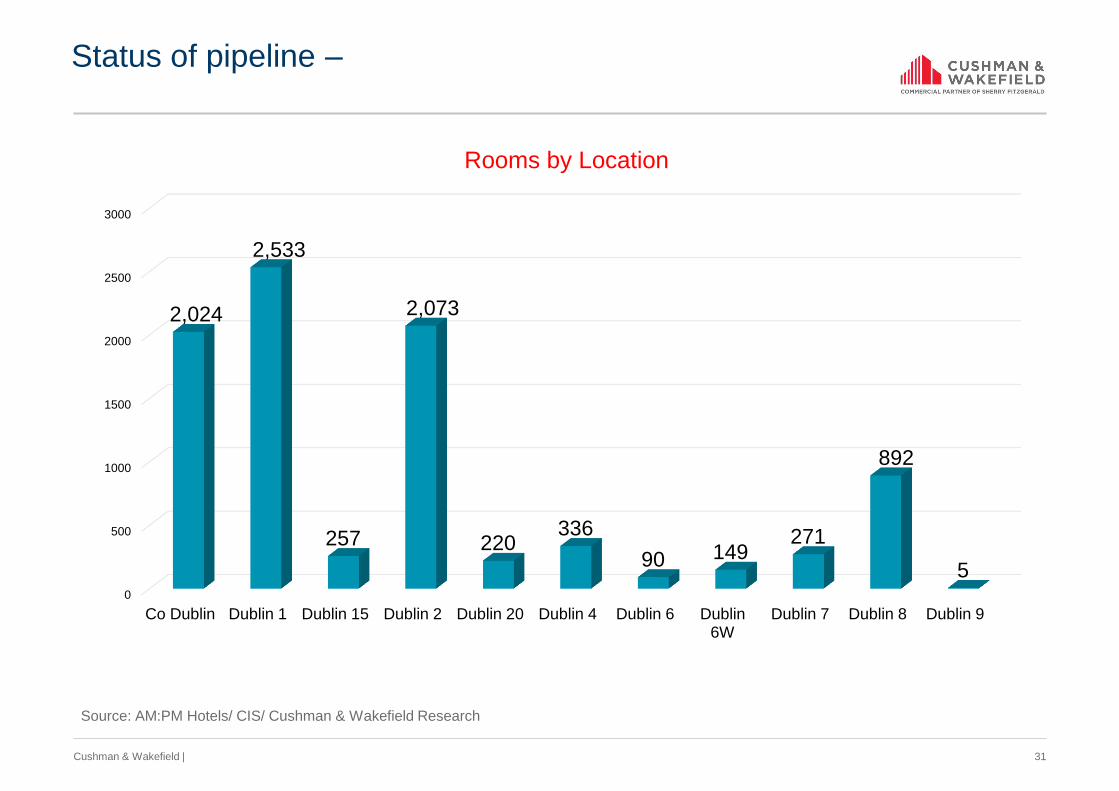

Status of pipeline –

Source: AM:PM Hotels/ CIS/ Cushman & Wakefield Research

0

1000

2000

3000

4000

5000

6000

On site Plans Granted Plans Submitted

1,199

5,972

1,679

31 Cushman & Wakefield |

Source: AM:PM Hotels/ CIS/ Cushman & Wakefield Research

Status of pipeline –

0

500

1000

1500

2000

2500

3000

Co Dublin Dublin 1 Dublin 15 Dublin 2 Dublin 20 Dublin 4 Dublin 6 Dublin 6W

Dublin 7 Dublin 8 Dublin 9

2,024

2,533

257

2,073

220 336

90 149 271

892

5

Rooms by Location

32 Cushman & Wakefield |

Concerns

1. Timing

2. Periphery Hotels

3. Oversupply

4. Brexit

33 Cushman & Wakefield |

Conclusion

Development

• Need for Development in Dublin City Centre

• Long Term Implications

• Feasibility Studies

Kirsty Rothwell MSCSI MRICS

Director & Head of Trading Assets

Telephone: +353 1 639 9386

E-mail: [email protected]

Disclaimer information

35 Cushman & Wakefield |

2016 Irish Hotels

Market Briefing 28 September 2016