2016 Integrated Resource Plan Report - fmtn.org

83

4401 Fair Lakes Court Fairfax, VA 22033 USA Phone: 1.703.818.9100 www.paceglobal.com Setting the Pace in energy since 1976 2016 Integrated Resource Plan Report Prepared for: City of Farmington December 9, 2016 This Report was produced by Pace Global, a Siemens business (“Pace Global”) and is meant to be read as a whole and in conjunction with this disclaimer. Any use of this Report other than as a whole and in conjunction with this disclaimer is forbidden. Any use of this Report outside of its stated purpose without the prior written consent of Pace Global is forbidden. Except for its stated purpose, this Report may not be copied or distributed in whole or in part without Pace Global’s prior written consent. This Report and the information and statements herein are based in whole or in part on information obtained from various sources as of December 9, 2016. While Pace Global believes such information to be accurate, it makes no assurances, endorsements or warranties, express or implied, as to the validity, accuracy or completeness of any such information, any conclusions based thereon, or any methods disclosed in this Report. Pace Global assumes no responsibility for the results of any actions and inactions taken on the basis of this Report. By a party using, acting or relying on this Report, such party consents and agrees that Pace Global, its employees, directors, officers, contractors, advisors, members, affiliates, successors and agents shall have no liability with respect to such use, actions, inactions, or reliance. This Report does contain some forward-looking opinions. Certain unanticipated factors could cause actual results to differ from the opinions contained herein. Forward-looking opinions are based on historical and/or current information that relate to future operations, strategies, financial results or other developments. Some of the unanticipated factors, among others, that could cause the actual results to differ include regulatory developments, technological changes, competitive conditions, new products, general economic conditions, changes in tax laws, adequacy of reserves, credit and other risks associated with City of Farmington and/or other third parties, significant changes in interest rates and fluctuations in foreign currency exchange rates. Further, certain statements, findings and conclusions in this Report are based on Pace Global’s interpretations of various contracts. Interpretations of these contracts by legal counsel or a jurisdictional body could differ.

Transcript of 2016 Integrated Resource Plan Report - fmtn.org

4401 Fair Lakes Court Fairfax, VA 22033 USA Phone: 1.703.818.9100 www.paceglobal.com

Setting the Pace in energy since 1976

2016 Integrated Resource Plan Report

Prepared for:

City of Farmington

December 9, 2016

This Report was produced by Pace Global, a Siemens business (“Pace Global”) and is meant to be read as a whole and in conjunction with this disclaimer. Any use of this Report other than as a whole and in conjunction with this disclaimer is forbidden. Any use of this Report outside of its stated purpose without the prior written consent of Pace Global is forbidden. Except for its stated purpose, this Report may not be copied or distributed in whole or in part without Pace Global’s prior written consent.

This Report and the information and statements herein are based in whole or in part on information obtained from various sources as of December 9, 2016. While Pace Global believes such information to be accurate, it makes no assurances, endorsements or warranties, express or implied, as to the validity, accuracy or completeness of any such information, any conclusions based thereon, or any methods disclosed in this Report. Pace Global assumes no responsibility for the results of any actions and inactions taken on the basis of this Report. By a party using, acting or relying on this Report, such party consents and agrees that Pace Global, its employees, directors, officers, contractors, advisors, members, affiliates, successors and agents shall have no liability with respect to such use, actions, inactions, or reliance.

This Report does contain some forward-looking opinions. Certain unanticipated factors could cause actual results to differ from the opinions contained herein. Forward-looking opinions are based on historical and/or current information that relate to future operations, strategies, financial results or other developments. Some of the unanticipated factors, among others, that could cause the actual results to differ include regulatory developments, technological changes, competitive conditions, new products, general economic conditions, changes in tax laws, adequacy of reserves, credit and other risks associated with City of Farmington and/or other third parties, significant changes in interest rates and fluctuations in foreign currency exchange rates.

Further, certain statements, findings and conclusions in this Report are based on Pace Global’s interpretations of various contracts. Interpretations of these contracts by legal counsel or a jurisdictional body could differ.

Proprietary & Confidential i

TABLE OF CONTENTS

Executive Summary ...................................................................................................................................... 5

Motivating Questions ................................................................................................................................ 5 Evaluation Process ................................................................................................................................... 6 Preferred Resource Plan .......................................................................................................................... 6

Farmington Energy Situation Assessment .................................................................................................... 8

Farmington Profile .................................................................................................................................... 8 Generation Facilities and Power Purchase Contracts .............................................................................. 8 Supply and Demand Balance ................................................................................................................... 9

Farmington Contracts Position Assessment ............................................................................................... 11

Power Purchase Contract ....................................................................................................................... 11 Gas Supply Contract ............................................................................................................................... 12 Coal Supply Contract .............................................................................................................................. 13

Farmington IRP Objectives and Metrics ..................................................................................................... 14

Cost Objectives ....................................................................................................................................... 14 Preserve Competitive Rates ............................................................................................................... 14

Risk Objectives ....................................................................................................................................... 15 Maintain Stable Rates (Price Risk) ..................................................................................................... 15 Manage Market Risks ......................................................................................................................... 15 Minimize Development Risks ............................................................................................................. 15 Minimize Control Risks ....................................................................................................................... 15

Environmental Objectives ....................................................................................................................... 15 CO2 Footprint ...................................................................................................................................... 15 Renewable Generation ....................................................................................................................... 16

Operational Objectives ........................................................................................................................... 16 Provide Reliable Service .................................................................................................................... 16 Manage and Monitor Largest Contingency ........................................................................................ 16

Clean Power Plan Cases ............................................................................................................................ 17

Load Forecast ............................................................................................................................................. 18

San Juan Basin Outlook ......................................................................................................................... 18 Load Forecast Process ........................................................................................................................... 21

Technology Screening ................................................................................................................................ 22

Technology Screening Considerations ................................................................................................... 22 Technology Assumptions........................................................................................................................ 22

Candidate Portfolios .................................................................................................................................... 24

Candidate Portfolios Construction and Screening .................................................................................. 24 Solar Integration ................................................................................................................................. 24 Portfolio Positions: Long vs. Short ..................................................................................................... 25 CPEC Project Development ............................................................................................................... 25

Candidate Portfolios for Stochastic Analysis .......................................................................................... 25

Proprietary & Confidential ii

Stochastic Assessment of Cndidate Portfolios ........................................................................................... 27

Stochastic Input Development ................................................................................................................ 27 Stochastic Load Forecasts ................................................................................................................. 27 Other Stochastic Inputs ...................................................................................................................... 29

Stochastic Assessment Results ............................................................................................................. 29 Key Findings ....................................................................................................................................... 32

Preferred Resource Plan ............................................................................................................................. 35

Appendix A: Load Forecast Methodology ................................................................................................... 36

Appendix B: Candidate Portfolios Profiles .................................................................................................. 41

Appendix C: Power Market Overview and Key Drivers .............................................................................. 50

Appendix D: Stochastic Analysis Results ................................................................................................... 60

Proprietary & Confidential iii

EXHIBITS

Exhibit 1: Farmington Existing Supply Resources .............................................................................. 9 Exhibit 2: Farmington Existing Supply Resources vs. Projected Peak Load Percentiles ................. 10 Exhibit 3: Tri-State Contract Summary ............................................................................................. 11 Exhibit 4: WAPA Contract Summary ................................................................................................ 12 Exhibit 5: Gas Contract Summary .................................................................................................... 12 Exhibit 6: Coal Contract Summary .................................................................................................... 13 Exhibit 7: Competing Stakeholder Objectives ................................................................................... 14 Exhibit 8: San Juan Basin Gas Infrastructures ................................................................................. 18 Exhibit 9: San Juan Basin Gas Production vs. Incremental Shale Production ................................. 19 Exhibit 10: San Juan Basin Gas Production and Rig Counts ............................................................. 20 Exhibit 11: San Juan Basin Gas Production Forecast ........................................................................ 20 Exhibit 12: Farmington Local Conditions ............................................................................................ 22 Exhibit 13: Technology Assumptions .................................................................................................. 23 Exhibit 14: Summary of Key Drivers in Portfolio Construction and Screening ................................... 24 Exhibit 15: Candidate Portfolios for Stochastic Analysis .................................................................... 26 Exhibit 16: Summary of Average Load Stochastic Projections ........................................................... 28 Exhibit 17: Summary of Peak Load Stochastic Projections ................................................................ 28 Exhibit 18: Average and Peak Load Percentiles (MW) ....................................................................... 29 Exhibit 19: Summary of Portfolios 1-4 ................................................................................................ 30 Exhibit 20: Summary of Portfolios 5-9 ................................................................................................ 31 Exhibit 21: Comparison of Portfolio 4 and 9 ....................................................................................... 32 Exhibit 22: Coal Retirement Decision Cost and Emission Tradeoff .................................................... 33 Exhibit 23: Key Elements of the Preferred Resource Plan ................................................................. 35 Exhibit 24: Load Forecast Process ..................................................................................................... 37 Exhibit 25: Flow Chart of the Key Elements in Load Forecasting ....................................................... 38 Exhibit 26: Upside and Downside Assumptions ................................................................................. 40 Exhibit 27: Portfolio 1 Peak Capacity vs. Peak Load .......................................................................... 41 Exhibit 28: Portfolio 2 Peak Capacity vs. Peak Load .......................................................................... 42 Exhibit 29: Portfolio 3 Peak Capacity vs. Peak Load .......................................................................... 43 Exhibit 30: Portfolio 4 Peak Capacity vs. Peak Load .......................................................................... 44 Exhibit 31: Portfolio 5 Peak Capacity vs. Peak Load .......................................................................... 45 Exhibit 32: Portfolio 6 Peak Capacity vs. Peak Load .......................................................................... 46 Exhibit 33: Portfolio 7 Peak Capacity vs. Peak Load .......................................................................... 47 Exhibit 34: Portfolio 8 Peak Capacity vs. Peak Load .......................................................................... 48 Exhibit 35: Portfolio 9 Peak Capacity vs. Peak Load .......................................................................... 49 Exhibit 36: Western Interconnect Coordinating Council (“WECC”) Footprint ..................................... 50 Exhibit 37: Expected Value Demand Projections for New Mexico ..................................................... 51 Exhibit 38: Installed Capacity Profile – New Mexico (MW) ................................................................. 52 Exhibit 39: New Mexico Zone 2016 Supply Curve.............................................................................. 53 Exhibit 40: Projected New Mexico Energy Prices ............................................................................... 54 Exhibit 41: New Resource Technology Parameters – National Average ........................................... 55 Exhibit 42: Henry Hub Price Probability Bands ................................................................................... 56 Exhibit 43: PRB Basin Price Probability Bands .................................................................................. 57

Proprietary & Confidential iv

Exhibit 44: Carbon Compliance Cost Probability Bands ..................................................................... 58 Exhibit 45: New Mexico Peak Load Probability Bands ....................................................................... 59 Exhibit 46: Portfolio 1-4 NPV Cost Ranking (2016-2035) ................................................................... 60 Exhibit 47: Portfolio 1-4 Cost Stability (95

th Percentile) NPV Costs Ranking (2016-2035) ................ 61

Exhibit 48: Portfolio 1-4 Average Energy Purchase Exposures Ranking (2016-2035) ...................... 62 Exhibit 49: Portfolio 1-4 Development Risk Assessment .................................................................... 63 Exhibit 50: Portfolio 1-4 Control Risk Assessment ............................................................................. 63 Exhibit 51: Portfolio 1-4 Risk Metric Summary ................................................................................... 64 Exhibit 52: Portfolio 1-4 CO2 Emissions in 2025 Compare to 2016 .................................................... 65 Exhibit 53: Portfolio 1-4 Renewable Generation Share Ranking in 2035 ........................................... 66 Exhibit 54: Portfolio 1-4 Environmental Metric Summary ................................................................... 67 Exhibit 55: Portfolio 1-4 Average Reserve Margin Ranking (2016-2035) ........................................... 68 Exhibit 56: Portfolio 1-4 Largest Contingency Assessment ................................................................ 69 Exhibit 57: Portfolio 1-4 Operational Metric Summary ........................................................................ 70 Exhibit 58: Portfolio 5-9 NPV Cost Ranking (2016-2035) ................................................................... 71 Exhibit 59: Portfolio 5-9 Cost Stability (95

th Percentile) NPV Costs Ranking (2016-2035) ................ 72

Exhibit 60: Portfolio 5-9 Average Energy Purchase Exposures Ranking (2016-2035) ...................... 73 Exhibit 61: Portfolio 5-9 Development Risk Assessment .................................................................... 74 Exhibit 62: Portfolio 5-9 Control Risk Assessment ............................................................................. 75 Exhibit 63: Portfolio 5-9 Risk Metric Summary ................................................................................... 76 Exhibit 64: Portfolio 5-9 CO2 Emissions in 2025 Compare to 2016 .................................................... 77 Exhibit 65: Portfolio 5-9 Renewable Generation Share Ranking in 2035 ........................................... 78 Exhibit 66: Portfolio 5-9 Environmental Metric Summary ................................................................... 79 Exhibit 67: Portfolio 5-9 Average Reserve Margin Ranking (2016-2035) ........................................... 80 Exhibit 68: Portfolio 5-9 Largest Contingency Assessment ................................................................ 81 Exhibit 69: Portfolio 5-9 Operational Metric Summary ........................................................................ 82

Proprietary & Confidential Page 5

EXECUTIVE SUMMARY

In its 2016 Integrated Resource Plan (“2016 IRP”), the City of Farmington (“Farmington” or “the City”)

identifies its preferred strategy for satisfying its electric power requirements over the 2016-2035 timeframe

(“the planning horizon”). This plan addresses Farmington’s options to best meet Farmington’s objectives

of providing for its long-term electricity needs in a reliable, cost competitive, and flexible manner under a

wide variety of market, regulatory, and economic conditions. Farmington must re-evaluate its previous

plan to build a combined cycle (“CC”) power plant in light of the increasingly stagnant load requirements

against smaller more flexible alternatives such as reciprocating engines and combustion turbines. It also

must improve the fleets’ responsiveness and to provide voltage support and spinning reserves, as well as

improving overall costs in the eastern part of its territory. In addition, the City must factor in the

requirement of the Clean Power Plan (“CPP”) into its resource plan.

Farmington is currently a net purchaser of 30-40 MW of power during peak periods. Its current peak

requirements are approximately 200 MW. It is a load serving entity (“LSE”) with an ownership share in

the coal-fired San Juan Generating Station (“SJGS”) Unit 4 and also owns hydro and natural gas-fired

capacity. Farmington is concerned with finding a least-cost, responsive, low-risk, and environmentally

responsible plan to meet its load requirements over the study period. To achieve this goal, Farmington

would also like to consider rate stability, system reliability, and future renewable generation levels. The

City is contemplating a variety of technology options including natural gas fired combined cycle capacity,

combustion turbines, reciprocating engines, solar, and combination of these options.

MOTIVATING QUESTIONS

Pace Global’s Risk-Integrated Resource Planning (“RIRP”) analysis was designed to identify solutions to

key challenges that Farmington will face over the planning horizon.

The resource planning analysis is intended to provide insight into the following key questions.

What are the prudent, cost competitive and environmentally responsible approaches in Farmington’s long term resource planning to address the trends in the energy industry and the utility space such as decreasing prices for renewables and energy storage, finalization of the carbon regulation, and the penetration of distributed energy resources?

How do these new trends impact the requirement for any new generation resources that Farmington considers adding to its fleet?

How will the potential New Mexico CPP compliance strategy impact Farmington’s choice of a Preferred Resource Plan?

Should Farmington rely on market purchases to meet a portion of its peak load given the differences of its peak and average load?

What are the pros and cons for Farmington to lock into firm supply resources either from new builds or a long term Power Purchase Agreement (“PPA”)?

Should Farmington consider solar generation additions after the expected reductions in capital costs?

How much solar capacity can Farmington integrate into its system considering the characteristics of its current generation fleet and load profile?

Proprietary & Confidential Page 6

EVALUATION PROCESS

Like most electric utilities, Farmington, has to make resource decisions under a great deal of uncertainty.

A resource decision that meets all objectives when judged only under current or best guess forecasted

conditions may prove to be a future financial burden on the utility over time if the forecasts are incorrect.

Fuel market volatility, capital cost uncertainty, load uncertainty, emission regulations, and regulatory

changes will all affect how a resource portfolio performs throughout its operational life. Understanding the

range of potential market volatility and the severity of impending regulatory changes on alternative

generation portfolios is crucial to making sound portfolio choices. For Farmington, the least expensive

resource addition may not be the best if it also exposes the organization to severe market volatility or

negative effects associated with impending regulatory change. The tradeoffs between costs, risks,

reliability, operational responsiveness and flexibility, environmental stewardship, and other utility

objectives need to be quantified for each portfolio and need to inform the selection of the portfolio that will

perform best according to those objectives the utility ranks as its highest priorities. The Pace Global RIRP

methodology addresses all above important questions through a highly structured process that consisted

of the following steps:

Identify overall objectives and metrics

Recommend two CPP compliance cases

Provide load forecast

Technology screening analysis

Formulate candidate portfolios

Stochastic risk analysis of nine shortlisted portfolios to identify the Preferred Resource Plan

o Provide stochastic distributions for key variables

o Perform risk analysis for the candidate portfolios

Develop strategy and recommendations

The major steps listed above are presented in subsequent sections in this report.

PREFERRED RESOURCE PLAN

The Preferred Resource Plan needs to be flexible to adjust to uncertainties, including the San Juan Unit 4

retirement date. As a minority owner of the San Juan Unit 4, Farmington does not have full control of the

retirement date. San Juan Unit 4 provides 43 MW base load generation to Farmington’s customers,

accounting for one third of Farmington’s current total generation capacity. The San Juan Unit could retire

in 2022 or 2027 or possibly even later. The replacement of the San Juan capacity needs to be carefully

planned to have the adequate capacity (40-60 MW) and suitable technology to best achieve Farmington’s

cost, risk, environmental and operational objectives.

Pace Global recommends a Preferred Resource Plan that includes a staged new build approach to best

satisfy its cost, risk, environmental and operational objectives. Components of the Preferred Resource

Plan include:

In the near term, Farmington could build two 8.6 MW reciprocating engines in 2018. This decision is justified by three primary factors: (1) expiration of 25 MW Tri-State contract in 2017, (2) the

Proprietary & Confidential Page 7

economics of utilizing existing gas contract, and (3) need of flexible unit for voltage support.

In the mid-term, upon getting clarification of the San Juan Unit 4 retirement date, Farmington could build a combined cycle unit (~58 MW) to replace the City’s 43 MW of San Juan Unit 4.

In the long term, Farmington could build solar project (~ 5 MW) depending on load levels and ensuring reliability to City’s distribution systems. The integration of renewables can result in several benefits: diversify Farmington’s portfolio; lower the overall supply costs; and provide environmental benefits.

Proprietary & Confidential Page 8

FARMINGTON ENERGY SITUATION ASSESSMENT

FARMINGTON PROFILE

The Farmington Electric Utility System (“FEUS”), which is owned and operated by Farmington, is located

in northwest New Mexico. Farmington’s service territory of 1,718 square miles encompasses the City of

Farmington, all of San Juan County, the City of Bloomfield, and a portion of Rio Arriba County. FEUS

also provides transmission services for the City of Aztec, which owns its own substation and distribution

facilities to Williams Field Services. Williams Field Services wheels the generation output of its Milagro

facility to the Shiprock Substation for sale in the western markets. Finally, FEUS provides transmission

services to Tri-State Generation and Transmission Association.

Farmington is a load serving entity with an ownership share in the San Juan Generation Station Unit 4. It

also owns hydro and natural gas-fired capacity. As of the fiscal year that ended June 30, 2015, the

Electric System was serving 44,627 metered customers. Farmington’s current peak requirements are

approximately 198 MW. Farmington is a net purchaser of 65 MW of power during peak periods.

The key characteristics that will drive Farmington’s needs pertaining to new generation are its load growth

and the economic conditions of the surrounding area. One of the key load uncertainties will be related to

standard regional profile questions (e.g., weather, population, and usage) and resource-based economic

development activities. The San Juan basin has experienced boom-bust cycles in the past associated

with oil and gas development. Particularly, San Juan County has had a major concentration of jobs and

income in the energy and the mining and extractives sectors. A continued weak energy market could

further slowdown Farmington’s load growth. A shutdown of SJGS one or more units could particularly

impact coal use. The loss of these economic base jobs could ripple through the local economy, resulting

in additional job losses in the industries that support the extractive industries, as well as in the service

sectors.

GENERATION FACILITIES AND POWER PURCHASE CONTRACTS

As a load serving entity, Farmington has a mix of generation assets with a total peak capacity of 133 MW.

This includes an ownership share in the coal-fired SJGS Unit 4, hydro and natural gas-fired capacity.

Exhibit 1 outlines Farmington’s existing supply resources. They can be summarized as follows:

Farmington’s Bluffview Power Plant, a 63 MW combined-cycle power plant that began its commercial operation in 2002. It uses a GE LM6000 combustion turbine and a Siemens steam turbine.

An eight percent (43 MW) ownership stake in San Juan Unit 4, which has a total capacity of 507 MW and is operated by Public Service Company of New Mexico (“PNM”)

Navajo Dam Hydro Plant Units 1 and 2, which have an average capacity of 9 MW and nameplate capacity of 30 MW.

Animas Plant, which is an 18 MW simple cycle power plant, with an inefficient heat rate of 12,124 Btu/KWh.

Proprietary & Confidential Page 9

Exhibit 1: Farmington Existing Supply Resources

Source: Farmington, Pace Global.

At its peak load requirements of approximately 198 MW, Farmington is a net purchaser of approximately

43 MW of power during peak periods from Western Area Power Administration (“WAPA”) and Tri-State.

Farmington’s power purchase contract with Tri-State and WAPA expires in 2017 and 2024, respectively.

SUPPLY AND DEMAND BALANCE

Farmington’s owned capacity portfolio is not sufficient to meet its expected peak load. For example for the

near term the reserve margin is expected to decline from its current level of negative 8 percent in 2016 to

negative 20 percent in 2019 after the Tri-State contract expires. Exhibit 2 presents the current portfolio

capacity relative to expected peak load (mean, 25 percentile, and 75 percentile levels).

Status quo conditions (i.e., relying on market purchases to fill the capacity shortage) involve significant

risk throughout the planning horizon due to high market exposure and a low reserve margin. In addition,

the status quo is not consistent with Farmington’s objective to become a net generator in serving its load

and maintaining rate stability.

Forced

OutageHeat Rate

Winter

CapacityVOM FOM

SO2

Emission

Rate

NOx

Emission

Rate

CO2

Emission

Rate

% Btu/KWh MW 2013$/MWh 2013$/MWh lbs/MMBtu lbs/MMBtu lbs/MMBtu

Animas CT 100% WECC DESERT SW 2015 Gas CT 0.50% 12,124 18.0 3.00 12.36 0 0.08 117

Bluffview 100% WECC DESERT SW 2005 Gas CC 1.07% 7,573 63.0 3.56 4.43 0 0.04 116

Navajo Dam 100% WECC DESERT SW 1989 Water HY 0% N/A 9.0 0 4.88 0 0 0

San Juan

Generating

Station Unit 4

8.48% WECC DESERT SW 1982 Coal ST 2.50% 11,000 43.0 2.50 11.16 0.08 0.28 210

Prime

MoverPlant Name

NERC

Region

NERC Sub

Region

Online

YearFuel

Percent

Owned

Proprietary & Confidential Page 10

Exhibit 2: Farmington Existing Supply Resources vs. Projected Peak Load Percentiles

Note: Above graph shows an indicative retirement of SJGS Unit 4 by the end of 2027 for illustration purposes. Source: Farmington, Pace Global.

43 43 43 43 43 43 43 43 43 43 43 43

9 9 9 9 9 9 9 9 9 9 9 9

9 9 9 9 9 9 9 9

63 63 63 63 63 63 63 63 63 63 63 63

63 63 63 63 63 63 63 63

18 18 18 18 18 18 18 18 18 18 18 18

18 18 18 18 18 18 18 18

18 18 18 18 18 18 18 18 18 18 18 18

18 18 18 18 18 18 18 18

25 25

-

25

50

75

100

125

150

175

200

225

250

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

MW

Farmington Status QuoPeak Capacity by Fuel/Unit Type vs. Peak Load Percentiles

San Juan (Coal) Navajo (Hydro) Bluffview (CC) Animas (CT) WAPA PPA Tri-State PPA Peak Load 25th Pct Peak Load 50th Pct Peak Load 75th Pct

No new resource additions; Coal retire after 2027

Proprietary & Confidential Page 11

FARMINGTON CONTRACTS POSITION ASSESSMENT

In addition to the existing and new generation resources, Pace Global explicitly considered Farmington’s

contract positions in this IRP. This section discusses the specific considerations of the power, gas and

coal contracts in the IRP study.

POWER PURCHASE CONTRACT

Farmington currently has two power purchase contracts. Exhibit 3 and Exhibit 4 present the terms of the

Tri-State and WAPA contracts that are considered in the IRP.

The PPA with Tri-State includes approximately 25 MW on-peak and 15 MW off-peak power. The Tri-State contract expires in 2017. While a renewal strategy could be negotiated and pursued, for planning purpose in this IRP, Pace Global does not assume renewal of this contract.

The PPA with WAPA includes approximately 18 MW capacity and power for summer and 17 MW for winter. The WAPA contract expires in 2024. Based on preliminary discussion with the City and for planning purpose in this IRP, Pace Global assumes renewal of this contract as a capacity-only PPA after 2024.

Exhibit 3: Tri-State Contract Summary

Source: Farmington.

On Peak

Contract Price

Off Peak

Contract Price

On Peak

Quantity

Off Peak

Quantity

Nominal $/MWh Nominal $/MWh MWh MWh

1/1/2016 1/31/2016 47.50 34.50 10,000 5,160

2/1/2016 2/29/2016 47.50 34.50 10,000 4,440

3/1/2016 3/31/2016 47.50 34.50 10,800 4,680

4/1/2016 4/30/2016 47.50 34.50 10,400 4,560

5/1/2016 5/31/2016 47.50 34.50 10,000 5,160

6/1/2016 6/30/2016 47.50 34.50 10,400 4,560

7/1/2016 7/31/2016 47.50 34.50 10,000 5,160

8/1/2016 8/31/2016 47.50 34.50 10,800 4,680

9/1/2016 9/30/2016 47.50 34.50 10,000 4,800

10/1/2016 10/31/2016 47.50 34.50 10,400 4,920

11/1/2016 11/30/2016 47.50 34.50 10,000 4,800

12/1/2016 12/31/2016 47.50 34.50 10,400 4,920

1/1/2017 1/31/2017 52.50 37.75 10,000 5,160

2/1/2017 2/28/2017 52.50 37.75 9,600 4,320

3/1/2017 3/31/2017 52.50 37.75 10,800 4,680

4/1/2017 4/30/2017 52.50 37.75 10,000 4,800

5/1/2017 5/31/2017 52.50 37.75 10,400 4,920

6/1/2017 6/30/2017 52.50 37.75 10,400 4,560

7/1/2017 7/31/2017 52.50 37.75 10,000 5,160

8/1/2017 8/31/2017 52.50 37.75 10,800 4,680

9/1/2017 9/30/2017 52.50 37.75 10,000 4,800

10/1/2017 10/31/2017 52.50 37.75 10,400 4,920

11/1/2017 11/30/2017 52.50 37.75 10,000 4,800

12/1/2017 12/31/2017 52.50 37.75 10,000 5,160

Begin Date* End Date

Proprietary & Confidential Page 12

Exhibit 4: WAPA Contract Summary

Begin Date End Date

Energy Contracted

Price ($/MWh)

Capacity Contracted Price

($/KW-month)

Summer Capacity

(MW)

Winter Capacity

(MW)

1/1/2016 12/31/2024 12.19 5.18 18 17

1/1/2025* 12/31/2035 N/A 5.18 18 17

*Note: The current WAPA PPA contract expires in 2024 and the post 2025 PPA extension is based on preliminary discussion with the City of Farmington. The extension is assumed as a capacity-only PPA.

Source: Farmington

GAS SUPPLY CONTRACT

Farmington has one gas supply contract for 14,700 MMBtu per day that expires by the end of 2020.

Exhibit 5 presents the gas contract terms. The gas supply contract is explicitly considered in the IRP in

the following aspects:

The portfolio constructions take into account of this gas contract position and include small new builds as early as 2018 in some candidate portfolios for the stochastic analysis.

The gas plants dispatch decisions are based on market prices, but in the post processing, the differential of the contract price and the market price is applied to the contracted quantity. This captures the total cost of gas to Farmington, without disadvantaging gas units’ economic dispatches. For any unused portion of the gas, the calculation assumes remarketing the gas at market prices.

The City will receive a credit of $0.2894/MMBtu as a result of a prepay gas arrangement with NMMEAA for 12,500 MMBtu per day that expires in July 30, 2019. The Gas Contract Summary contract price provided below does not reflect the NMMEAA arrangement credit.

Exhibit 5: Gas Contract Summary

Begin Date End Date

Contract Price

(including

delivery charge)

Contract Quantity

Nominal $/MMBtu MMBtu per day

10/1/2015 9/30/2016 4.77 14,700

10/1/2016 9/30/2017 4.80 14,700

10/1/2017 9/30/2018 4.85 14,700

10/1/2018 9/30/2019 4.90 14,700

10/1/2019 12/31/2020 4.90 14,700

Source: Farmington

Proprietary & Confidential Page 13

COAL SUPPLY CONTRACT

Farmington has one coal supply contract that expires in 2021. Exhibit 6 presents the coal contract prices

included during 2016-2021. The San Juan unit 4 dispatches are based on market prices, but in the post

processing, the differential of the contract price and the market price is applied to the consumed quantity.

This captures the total cost of coal to Farmington. After 2021, market prices are used in evaluating overall

portfolio costs.

Exhibit 6: Coal Contract Summary

Year Contract Prices

(2014$/MMBtu)

2016 2.08

2017 2.15

2018 2.63

2019 2.64

2020 2.57

2021 2.32

Note: The prices are calculated to include fixed costs and variable costs.

Source: Farmington

Proprietary & Confidential Page 14

FARMINGTON IRP OBJECTIVES AND METRICS

To properly evaluate resource decisions, Farmington identified the planning objectives very early in the

resource planning process. A consensus was developed around the Preferred Resource Plan by

selecting the portfolio that best met the planning objectives over a wide range of regulatory and market

outcomes. Metrics for each planning objective were created to form a basis for comparing different

portfolios.

Even with the appropriate metrics identified for each planning objective, the tradeoffs associated with

resource decisions represent the biggest challenge for resource planning. Exhibit 7 displays four

competing objectives, identified as priorities. As is shown, focus on any one objective can move the

resource plan away from focus on the others. In the IRP process, a wide range of metrics were used to

rank portfolios for each objective, helping Farmington to evaluate the tradeoffs associated with different

portfolio options and, ultimately, arrive at a resource plan that balances many competing goals.

Exhibit 7: Competing Stakeholder Objectives

Source: Pace Global

COST OBJECTIVES

Preserve Competitive Rates

Preserving competitive rates is a common objective for utilities. In Farmington’s case, the objective is to

select the lowest-cost supply options and, therefore, minimize the rate impact on the customers. Pace

Objectives Metrics

Cost Cost Minimize power supply costs

and rate increases

2016-2035 Cost NPV ($ million)

2016-2035 Levelized Costs

Risks Cost Stability Achieve rate stability 2016-2035 95th Percentile Cost NPV ($

million)

Development

Risks

Minimize project

development risks

Project development uncertainties

Control Risks Minimize operation risks and

other uncertainties

Operational and control risks

Market Risks Decrease energy market

purchase exposure

2016-2036 Average energy market purchase

exposure

Environmental Environmental

Stewardship

Decrease emissions and

increase renewable

generation

CO2 emission in 2025 relative to 2016;

Renewable generation percentage in 2035

Operational Reserve

Margin

Ensure reliability

requirements with native

capacity

2016-2036 Average reserve margin

Largest

Contingency

Minimize largest contingency

in the generation fleet

Size of the largest contingency unit in 2035

Proprietary & Confidential Page 15

Global used portfolio cost minimization as a proxy for maintaining competitive rates. For comparative

purposes, different portfolio options were evaluated based on the levelized net present value of all

generation-related costs associated with serving Farmington’s load (in millions of dollars and dollars per

MWh). The IRP cost metric included the variable cost of generation, fixed costs, executed contracts costs,

capital cost investments, and the cost of net market transactions (purchases minus sales).

RISK OBJECTIVES

Maintain Stable Rates (Price Risk)

Rate stability can be measured by different metrics like standard deviation or probability bands. For this

analysis, portfolios were evaluated against statistically derived distributions on key market drivers like

natural gas prices, coal prices, energy demand, carbon prices, power market prices, and capital costs.

Rather than recording portfolio costs under one set of assumptions, Pace Global measured costs under a

distribution of the key assumptions drivers. In this context, portfolios were evaluated based on the

difference between the mean of the distributions of total incremental generation costs and the 95-percent

confidence band of the distribution of these costs. This represented a metric of how wide the cost

distribution could become for each portfolio. The lower the difference between the mean and the 95-

percent confidence band, the less exposed the portfolio is to market volatility.

Manage Market Risks

Although the ability to sell and buy in the spot market represents a significant benefit to Farmington by

allowing it to optimize its resources, significant reliance on the wholesale market can constitute a risk for

Farmington. The spot market could be highly volatile and the utility’s dependence on a large volume of

market transactions increases the market uncertainty and higher market transactions is assigned with an

unfavorable score

Minimize Development Risks

The availability of certain portfolio options (such as the CPEC development project) is uncertain and out

of Farmington’s control. In contrast, Farmington has greater control of the building smaller generation

resources that is closely tailored to its contracting positions, load profile and coal retirement dates.

Minimize Control Risks

As a potential minority owner of a generation station like CPEC, Farmington is unlikely able to make dispatch decisions to best support the operational flexibility of its system. Alternatively, if Farmington outright owns a generation the City can solely decide whether a dispatch is warranted. This tradeoff should be weighed against the cost effectiveness of this portfolio, should this option materialize.

ENVIRONMENTAL OBJECTIVES

CO2 Footprint

An increasing concern regarding global climate change has put specific emphasis on the carbon footprint

associated with different power generating resource options. Although coal-fired generation remains one

of the low cost resources, its environmental impacts pose a growing concern to the public and utility

planners. Moreover, the potential advent of significant costs associated with CO2 emissions constitutes a

major risk for coal plant owners. With this context in mind, different portfolio options were evaluated

Proprietary & Confidential Page 16

based on the achieved CO2 footprint growth by 2025 from the 2016 baseline. Assuming all other metrics

remain the same, any portfolio that achieves slower CO2 emission growth will be preferable.

Renewable Generation

Although the City does not face a specific regulation concerning a renewable generation target at this

time, Farmington’s environmental goals require the addition of renewable resources to the supply mix,

especially in the long term. Analysis showed that increasing generation from renewable resources will

also directly result in reduced CO2 emissions for the portfolio. The percentage of generation from

renewable resources was the metric used to reflect greater renewable stewardship. Different portfolio

options were evaluated based on the percentage of the utility’s net energy for load to be served by

renewable generation by 2035. As such higher renewable penetration portfolio is assigned with a

favorable score.

OPERATIONAL OBJECTIVES

Provide Reliable Service

In Farmington’s case, system reliability is a primary concern. Farmington is currently short on owned

capacity and has historically relied on the wholesale market to meet a portion of its load requirements.

Going forward, one of Farmington’s primary objectives is to meet its growing native load by using

generation from locally owned resources.

To assess the associated risk, Farmington’s 20 years average supply resource availability as a

percentage of peak load between 2016 and 2035 (reserve margin) was used as a risk metric for each

portfolio. Portfolios with insufficient capacity to meet native load were assigned negative scores due to

too much exposure to the market.

Manage and Monitor Largest Contingency

Farmington seeks to add smaller more flexible generation resources to improve the fleets’

responsiveness and to provide voltage support and spinning reserves, as well as improving overall costs

in the eastern part of its territory. In the IRP analysis, we monitor the largest contingency as existing

resources are replaced with new resources. The greater share or a reliance of a single resource in a

portfolio can expose to a reliability issue.

Proprietary & Confidential Page 17

CLEAN POWER PLAN CASES

The EPA released the draft performance standards, also known as the Clean Power Plan, for existing

generating units under §111(d) of the Clean Air Act on time on June 2, 2014. The final rule was released

on August 3, 2015. The CPP establishes state by state emission targets for affected existing generation

units. States drive the approach to meet their goal, including choosing to comply as a rate goal (lb

CO2/MWh) or a mass goal (short tons of CO2). Overall, the aggregate state goals (on a mass basis)

would reduce emissions from affected sources by an estimated 32 percent below 2005 levels by 2030.

The initial compliance period under the rule would begin in 2022 with the final reduction goal to be

achieved by 2030. Trading between states would be encouraged under the CPP.

On February 9, 2016, the Supreme Court of the United States granted a request to stay the Clean Power

Plan, after the D.C. Circuit Court denied this request initially. As a result, the CPP is not in effect at this

time until the D.C. Circuit Court rules on the pending legal challenges and the stay is lifted. The deadlines

for states to submit compliance plan milestones, the earliest of which would have been September of

2016, are uncertain at this time. There is a great deal of uncertainty at this time over how the states will

formulate their compliance plans as well as the extent to which legal challenges or congressional action

will change the proposed regulations. Despite these uncertainties, Pace Global assumes that the rule is

implemented on schedule and two different compliance options that New Mexico appears likely to adopt

based on their goal defined in the final rule and the expected future generation mix of the state. These

two compliance options for New Mexico are a mass-based approach to compliance whereby New Mexico

opts into a national trading scheme and mass-based approach to compliance with New Mexico only

allowing for intrastate trading amongst affected entities within the state.

New Mexico appears to be well positioned to comply with its goal prescribed under the CPP under either

a rate or mass approach. The announced retirements of San Juan units result in a significant reduction in

projected emissions from existing generating sources covered under the CPP relative to the baseline.

Adopting a mass-based approach to CPP compliance is viewed as many to be less complicated and

therefore favorable, if from an administrative standpoint only, over a rate approach. For this reason, Pace

Global assumes mass-based compliance for New Mexico for both CPP compliance cases.

Mass-based with interstate trading: New Mexico adopts a mass-based goal and opts into the national trading program. Allowances are freely traded amongst all states that also opt into the mass-based federal trading program, regardless of geographic location. Carbon value is based on the marginal cost to comply for all states in the trading program. New Mexico is expected to be in a net long position for allowances and therefore can sell additional allowances to buyers outside of the state.

Mass-based with intrastate trading: New Mexico adopts a mass-based goal but does not opt into national trading. Trading is a compliance option for affected generators located in the state but only with other in-state parties. Carbon value is based on the marginal cost to comply for New Mexico only.

Pace Global performed stochastic analysis for the nine portfolios under both CPP cases to assess the

overall performance of the portfolios.

Proprietary & Confidential Page 18

LOAD FORECAST

As part of the 2016 IRP process, Pace Global performed a long-term load forecast for resource planning

studies. In order to do so, FEUS’s historical load data and consumption patterns were analyzed.

Historically, the average load grew at a Compounded Annual Growth Rate (“CAGR”) of 0.7 percent and

the peak load at 1.8 percent between 2000 and 2015. The analysis suggested that FEUS’s load forecast

will depend on the extent of oil and gas exploration and production (“E&P”) activities undertaken in the

region. Pace’s load forecast is aligned with the outlook for exploration activities and the opportunities for

electrification in the region.

SAN JUAN BASIN OUTLOOK

The San Juan Basin currently accounts for 3.5 percent of Lower 48 gas production (2.5 Bcf/d), down from

5.5 percent five years ago (3.2 Bcf/d). Primarily a dry gas play with little oil production but with some

incremental Natural Gas Liquid (“NGL”) production, the San Juan Basin provides gas supplies to markets

in California, Arizona, and New Mexico. 55 percent of San Juan gas comes from coal bed methane

(“CBM”) deposits, with the other 45 percent from conventional drilling. By 2030, this balance is expected

to shift to 40 percent and 60 percent, respectively. CBM and conventional supplies have faced increasing

gas-on-gas competition from new shale resources. While California remains an important premium

market and expected new Gulf Coast demand (LNG exports, etc.) will help to stabilize long-term

production, the San Juan Basin is not expected to be a region of new natural gas production growth. In

terms of infrastructure, San Juan Basin gas supply is accessed via El Paso, Transwestern,

Transcolorado, Northwest, and others as shown in Exhibit 8.

Exhibit 8: San Juan Basin Gas Infrastructures

Source: Pace Global, Energy Velocity

Proprietary & Confidential Page 19

San Juan gas production has seen steady declines since 2006. It faces increasing competition from new

shale gas sources such as the nearby Eagle Ford play but also the more distant Utica and Marcellus

plays. San Juan economics are less favorable than new shale resources. The resulting gas-on-gas

competition is crowding out the San Juan, which only a large increase in demand will help to reverse.

Exhibit 9 shows the comparison of San Juan Basin gas production vs. incremental shale gas production

since 2006.

Exhibit 9: San Juan Basin Gas Production vs. Incremental Shale Production

Source: Pace Global

In the near term to 2020, San Juan gas production will continue to decline in the absence of new drilling.

Drilling rig counts have effectively gone to zero in the San Juan Basin as production has shifted toward

low-cost shale plays. The rig count and production forecasts in Exhibit 10 takes into account the current

economic reality (i.e., forwards trading) in the San Juan Basin. Existing wells will continue to produce

over the long tail of production curves in the San Juan Basin, but absent new drilling this recent

production trend will continue.

-

5,000

10,000

15,000

20,000

25,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Incre

men

tal

Sh

ale

(M

Mcf/

d)

San

Ju

an

(M

Mcf/

d)

San Juan Basin Gas Production vs. Incremental Shale since 2006 from the Eagle Ford, Marcellus, and Utica

San Juan Production Incremental Shale

Proprietary & Confidential Page 20

Exhibit 10: San Juan Basin Gas Production and Rig Counts

Source: Pace Global

Outlook for San Juan gas production depends on new demand markets and recovery in gas prices.

Under Scenario One, gas prices remain persistently low allowing San Juan production to continue a slow

decline. Under Scenario Two, anticipated new LNG demand in Gulf Coast markets, continued demand

from California, and rising consumption from gas-fired plants helps to move San Juan production back to

a slow rise. By 2030, shale plays will have matured, raising production costs and shifting production back

to conventional and CBM resources like the San Juan Basin. Exhibit 11 shows the San Juan Basin gas

production forecast scenarios.

Exhibit 11: San Juan Basin Gas Production Forecast

Source: Pace Global

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Ja

n-0

6

Sep

-06

Ma

y-0

7

Ja

n-0

8

Sep

-08

Ma

y-0

9

Ja

n-1

0

Sep

-10

Ma

y-1

1

Ja

n-1

2

Sep

-12

Ma

y-1

3

Ja

n-1

4

Sep

-14

Ma

y-1

5

Ja

n-1

6

Sep

-16

Ma

y-1

7

Ja

n-1

8

Sep

-18

Ma

y-1

9

MM

cf/

d

San Juan Basin Gas Production History and Forecast (Short-Term)

Colorado San Juan New Mexico San Juan

Forecast

0

5

10

15

20

25

30

Ja

n-0

6

Oct-

06

Ju

l-0

7

Ap

r-0

8

Ja

n-0

9

Oct-

09

Ju

l-1

0

Ap

r-1

1

Ja

n-1

2

Oct-

12

Ju

l-1

3

Ap

r-1

4

Ja

n-1

5

Oct-

15

Ju

l-1

6

Ap

r-1

7

Ja

n-1

8

Oct-

18

Ju

l-1

9

Gas R

ig C

ou

nts

San Juan Basin - Gas Rig Counts

Colorado San Juan New Mexico San Juan

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

MM

cf/

d

San Juan Basin Gas Production - Long Term Forecast by Scenario

Scenario One Scenario Two

Proprietary & Confidential Page 21

LOAD FORECAST PROCESS

The base load forecast was driven by the San Juan Basin gas production outlook. As discussed, there

are two types of impacts to the load: direct and indirect (also called services) impacts. The former

quantifies the direct load addition to the base case forecast, due to factors like oil and gas field

electrification opportunities or compressor requirements for pumping. The latter quantifies the change in

population due to influx of people moving into Farmington’s service area or decline in population due to

people moving out (mine closure effects). These population shifts lead to changes in residential and

commercial load. Additional details can be found in Appendix A: Load Forecast Methodology.

Pace Global also considered studies performed by the Federal Energy Regulatory Commission (“FERC”)

on demand response potential. This information is publicly available. According to this study, the

expected peak reduction over a 10-year period will be 15 percent of the unadjusted peak. Pace Global

used this data in the load forecasting exercise for Farmington.

Proprietary & Confidential Page 22

TECHNOLOGY SCREENING

TECHNOLOGY SCREENING CONSIDERATIONS

The goal of the technology screening is to identify technically feasible and commercially viable generation

resources that could be used as building blocks in constructing portfolios. For this reason, the technology

screening focuses on resource options could meet Farmington’s new generation resource requirements,

including:

Size of the new generation resource, which is informed by factors including load profile, existing resources retirement, and PPA expiration, etc.

Resource type: base load, intermediate, intermittent, or peaking resources

Characteristics: ramping rates, ability to provide voltage support, flexibility

Fuel type: fossil-fueled or renewable generations

Farmington local considerations: altitude, pressure, natural wind or solar resources, etc.

The technology selection considered a combination of dispatchable fossil-fueled generation resources

and renewable technologies. Fossil-fueled resources included combustion turbines (“CTs”), combined

cycle gas turbines (“CCGTs”), reciprocating engines, as well as a conversion options that allows

development flexibility, i.e., build CT initially and add steam turbine generator (“STG”) later to convert into

a CC facility. For renewables, though both wind and solar are possible in Farmington area, marginal wind

resources, attractive solar resources, and rapidly declining solar costs favor solar.

Since the capacity and heat rate of gas turbine-based power plants significantly decreases with increases

in altitude and temperature, Farmington’s local conditions were used to derive factors for adjusting the

rated capacity and heat rate of each gas-fired technology option. The local conditions in Farmington used

to make this adjustment are presented below in Exhibit 12.

Exhibit 12: Farmington Local Conditions

Site Metric Units Measure

Altitude ft amsl 5,300

Ambient Dry Bulb Temp Deg. F 59.3

Ambient Wet Bulb Temp Deg. F 48.4

Barometric Pressure mm of Hg 1,013.3

Relative Humidity % 33.8

Source: Tutiempo Network, Pace Global

TECHNOLOGY ASSUMPTIONS

Technology performance and costs were estimated for several gas-fired and solar technologies which

could become part of the City of Farmington’s future power generation portfolio. For each technology,

capital costs were estimated to include EPC contract, required owner’s costs, and financing costs. The

estimated capital costs were somewhat higher than might be expected in the broader market areas

Proprietary & Confidential Page 23

because (1) the smaller unit size resulted in a diseconomy of scale relative to larger units, and (2) the site

elevation conditions resulted in a substantial unit derate, which in turn would require Farmington to

purchase a larger unit at a higher cost than might otherwise be necessary to generate the required

capacity.

A variety of gas-fired technologies were considered and all were sized to meet the City of Farmington’s

potential demand. Adjusted (for local conditions) performance and current capital cost estimates for gas-

fired technologies are provided in Exhibit 13 and are used as the basis for portfolios construction in this

IRP.

Exhibit 13: Technology Assumptions

Source: Pace Global estimates and analysis.

When Pace Global selected new generation options for inclusion in portfolios, a particular unit design

based on an actual product is chosen as representative of a class of similar units. In all cases, there is at

least one additional unit available from a different manufacturer with similar enough characteristics that

competitive bidding will be possible at the time a project is implemented.

Site Capacity Site Heat Rate net Capex

kW net Btu/kWh HHV $2014/kW net site

GE 1xLM6000 PF 39,386 9,299 1,319

GE 1xLM6000 PG 43,846 8,942 1,325

LM6000 PF 1X1 CC with Duct Fire, Wet Cooling 57,917 7,490 1,643

2x1 LM6000 PC SPRINT 106,589 7,628 1,296

GE J920 Flex 8,600 7,729 1,155

Wartsila 20V34SG 18,513 8,394 1,040

20 MW Aero SCGT, LM2500 PJ 18,354 10,774 1,771

Siemens SCC-800 59,309 7,515 1,872

Siemens SCC-800 with Duct Fire 71,064 7,700 1,301

Solar (Fixed Mount) N/A N/A 1,986

Solar (Tracking System) N/A N/A 2,234

Equipment Model

Proprietary & Confidential Page 24

CANDIDATE PORTFOLIOS

CANDIDATE PORTFOLIOS CONSTRUCTION AND SCREENING

Based on the technology screening assumptions as shown in Exhibit 13, Pace Global and Farmington

screened portfolios that would add gas or solar resources to the current asset base during the planning

horizon. Exhibit 14 presents a summary of the key drivers in the portfolio construction and screening.

The portfolios construction takes into account of several important considerations, including:

Near-term decision of relying on market purchases or building new resources (recips or CTs)

SJGS Unit 4 retirement: by 2022 or 2027

Different market exposures to have generation capacity long, short or at load

Different technologies for gas-fired generation resources

Acquisition (Clean Path Energy Center (“CPEC”) shares vs. new build options

Gas only new resources vs. a combination of gas and renewable generations

Exhibit 14: Summary of Key Drivers in Portfolio Construction and Screening

Source: Pace Global

Solar Integration

In constructing and screening the portfolios, the level of solar integration is considered. The ability of

Farmington’s fossil fueled peaking units to accommodate a high level of solar is prohibitive, because the

Animus simple cycle unit cannot be used for cycling purpose due to it technical limitations and inefficient

Proprietary & Confidential Page 25

heat rate. Moderate level of solar capacity ranging 5 MW to 15 MW was identified with the City and is

incorporated into certain candidate portfolios.

Portfolio Positions: Long vs. Short

Currently, markets are soft, which suggests that having an “open” position (buying power from the market)

is sound for a portion of its needs until markets strengthen. Farmington is part of the southwest reserve

sharing group and has historically procured both capacity and energy to cover short peak positions.

Because Farmington’s average load is on average 60 MW lower than the peak load in 2016 and expected

to grow over time, Farmington’s planning strategy is not to overcommit its capacity levels significantly

above its peak load. Rather rely on PPA contracts or market purchases to cover a small portion of short

term peak load shortages. This is likely a preferred path for the City because there are load uncertainties

due to distributed generation and other cogeneration opportunities that could result in lower than

anticipated load over time.

Typically, in an IRP, we consider some portfolios that are short against others that are at or long relative

to the load, so that the risks of being heavily exposed to the market are reflected in the risk analysis. An

initial cost assessment indicates that a significant surplus capacity portfolio generally commands some

cost premium for the City of Farmington. It does not reward building long portfolios. As a result of the

assessment it is explicitly reflected in the screening analysis to form the nine candidate portfolios.

CPEC Project Development

It is uncertain whether the proposed CPEC project could be sufficiently “de-risked” by early 2017 for it to

be a viable option. CPEC is an early stage development project sponsored by Wester Energy Partners

(WEP), SNC-Lavalin, and Stonepeak Infrastructure Partners. The generation facility will include combined

cycle natural gas-fired capacity of 715 MW and solar photovoltaic (“PV”) capacity of 55 MW. It will be

located in Waterflow, San Juan County, New Mexico, adjacent to Farmington’s service territory. Currently,

CPEC is aiming for Commercial Operation Date (“COD”) by April 2021, and is seeking one or more

buyers. In addition, it is uncertain whether an initial purchase of 50 MW, followed by additional purchase

of approximately 50 MW (based on the load growth and San Juan Unit 4 retirement schedule) is

commercially viable and acceptable to the project sponsors. From an operation perspective, Farmington

needs responsive and flexible units, and the potential minority ownership of the CPEC project could

compromise this objective. CPEC presents uncertainties and risks that could offset its competitiveness

from a cost perspective.

CANDIDATE PORTFOLIOS FOR STOCHASTIC ANALYSIS

Pace Global and Farmington screened to construct nine candidate portfolios as presented in Exhibit 15.

These portfolios allow for the consideration of a reasonable range of uncertainties. Each of these

portfolios is evaluated in the stochastic analysis under two CPP cases.

Proprietary & Confidential Page 26

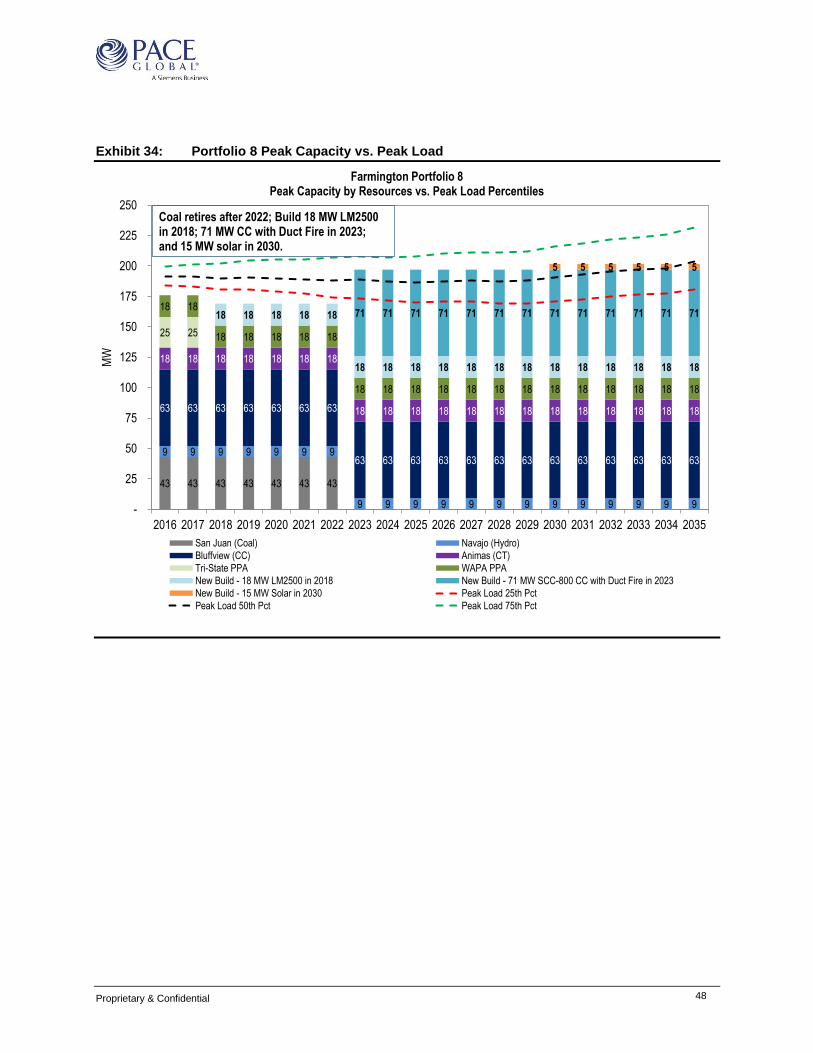

Exhibit 15: Candidate Portfolios for Stochastic Analysis

Note: San Juan unit 4 retirement year is an assumption for the IRP modeling purpose only. The coal unit, as of the

date of this analysis, has not announced a potential retirement date. Source: Pace Global, Farmington

Proprietary & Confidential Page 27

STOCHASTIC ASSESSMENT OF CNDIDATE PORTFOLIOS

STOCHASTIC INPUT DEVELOPMENT

Stochastic inputs used in the risk integrated resource planning process were based on a combination of

historic volatility and expectations for future market trends. Pace Global’s market insight was used to

develop a view on future market trends; statistical and modeling tools were then employed to quantify the

uncertainty around the expected trends and evaluate the performance of each portfolio under different

uncertainties. The stochastic analyses required that uncertainties in these forecasts be determined. The

effects of the load, fuel prices, CO2 prices, and capital costs uncertainty on the portfolios were quantified

over the study horizon under 200 different simulations.

Stochastic Load Forecasts

For incorporation in the risk-integrated portfolio analysis, Pace Global developed a stochastic load

forecast for the average and peak load. The load forecasting process consisted of two steps: Step 1,

called the “Parametric forecast”, was performed by building a regression model using weather and

personal income as explanatory variables. This step consists of building the weather response functions

for average and peak load. To forecast future weather, a random sampling of the past weather (from 17-

years history) was performed. To predict future personal income, a Geometric Brownian Motion (“GBM”)

model was developed.

Step 2, called the “quantum forecast”, was performed to quantify the additional uncertainty due to

demand side management measures. This step captured the up and downside risks to the load forecast

developed in Step 1. Downside potential stemmed from energy efficiency and demand response

programs. Additional details on load forecast methodology can be found in Appendix A: Load Forecast

Methodology.

The inputs used for the stochastic process were based on a combination of historical volatility and growth

rate for personal income and population. They were also based on Pace Global’s expectations for future

load growth trends. These trends were aligned with the expectation of new electrification opportunities

(driven by exploration) in the San Juan basin. Statistical and modeling tools were then employed to

quantify the uncertainty around the expected trends.

Analysis revealed that Farmington’s load growth uncertainty contains nearly as much downside as upside.

For the average load, the expected case (mean) has an estimated CAGR of 0.52 percent for the time

period 2016 to 2036. The peak load’s CAGR is 0.56 percent for the same time period. Both the average

and peak loads remain more-or-less flat from 2016 to 2030, at less than 0.1 percent. Beyond 2030, the

uptick in the load growth rate is driven by expectation of new exploration & production rigs in the region.

Exhibit 16 and Exhibit 17 display the details pertaining to average and peak load stochastic projections.

Exhibit 18 displays percentile bands for the average and peak load stochastic distributions.

Proprietary & Confidential Page 28

Exhibit 16: Summary of Farmington’s Average Load Stochastic Projections

Source: Pace Global.

Exhibit 17: Summary of Farmington’s Peak Load Stochastic Projections

Source: Pace Global

Proprietary & Confidential Page 29

Exhibit 18: Farmington’s Average and Peak Load Percentiles (MW)

Source: Pace Global

Other Stochastic Inputs

Pace Global developed distributions of other key inputs to represent the probability of occurrence over a

range of outcomes. Below are some of the key drivers of the stochastic analysis, with detailed inputs

presented in Appendix B.

Capital Costs: Capital cost uncertainty was evaluated by defining stochastic bands around the capital costs of each resource addition in the portfolio for each year of the study period, based on historical commodity cost volatility and breakdowns of capital costs for different generating technologies.

Natural Gas Prices: Gas price projections were developed according to primary supply and demand drivers that influence domestic production costs as well as international market dynamics.

CO2 Price Projections: CO2 price projections were developed according to expectations for state and federal policy and regulations.

Coal Price Projections in the Region and for the San Juan Generating Station: Coal price projections were developed according to primary supply and demand drivers as well as plant-specific analysis at San Juan.

STOCHASTIC ASSESSMENT RESULTS

In performing the portfolio analysis, all cost, risk, environmental, and operational metrics were recorded for each of the options in line with the categories outlined above. Exhibit 19 and Exhibit 20 provide a summary of the portfolio performance for the cost, risk, environmental and operational metrics for the portfolios 1-4 and portfolios 5-9 separately. Detailed analysis results in each category are presented in Appendix D: Stochastic Analysis Results.

Average Load Peak Load

Mean 5th Pct 25th Pct 50th Pct 75th Pct 95th Pct Mean 5th Pct 25th Pct 50th Pct 75th Pct 95th Pct

2016 130 118 125 130 135 146 2016 193 175 184 192 200 218

2017 131 116 124 129 135 150 2017 194 172 183 191 201 223

2018 130 114 122 128 137 153 2018 193 169 181 190 202 229

2019 131 113 121 128 137 158 2019 194 168 179 190 204 236

2020 131 111 120 128 138 161 2020 194 165 178 189 205 240

2021 131 108 119 128 138 163 2021 193 161 176 188 204 244

2022 130 108 117 126 138 165 2022 193 159 173 187 206 246

2023 130 105 116 127 140 169 2023 194 155 172 188 207 253

2024 130 104 116 126 139 171 2024 193 153 171 186 206 254

2025 130 103 115 126 139 171 2025 192 152 169 186 206 256

2026 130 103 115 126 140 172 2026 193 151 170 187 209 258

2027 130 102 115 126 141 172 2027 194 151 170 187 210 258

2028 130 101 113 126 142 175 2028 193 149 168 186 210 262

2029 130 99 113 126 142 173 2029 193 147 168 187 211 261

2030 132 100 115 127 144 178 2030 196 148 170 189 215 268

2031 133 101 116 129 146 180 2031 198 150 172 192 218 270

2032 135 101 117 131 149 182 2032 201 150 174 195 221 273

2033 136 102 118 132 150 183 2033 203 150 175 196 223 275

2034 138 103 120 133 152 187 2034 204 151 176 197 225 279

2035 141 104 122 137 155 191 2035 209 153 179 203 230 288

2036 145 107 125 140 160 198 2036 216 157 186 208 240 297

Proprietary & Confidential Page 30

Exhibit 19: Summary of Portfolios 1-4

Source: Pace Global

Proprietary & Confidential Page 31

Exhibit 20: Summary of Portfolios 5-9

Source: Pace Global

Portfolio 4 and 9 ranks the best in an overall ranking when we assume two different San Juan 4

retirements. Between the two best portfolios, Portfolio 4 results in ~3% lower expected costs than

Portfolio 9. Exhibit 21 presents the comparison of Portfolio 4 and 9.

Proprietary & Confidential Page 32

Exhibit 21: Comparison of Portfolio 4 and 9

Source: Pace Global

Key Findings

Coal Retirement

Stochastic results show retiring San Juan in 2027 rather than 2022 would likely lower Farmington’s

portfolio cost. However, retiring San Juan Unit 4 earlier timeline, in 2022, reduces Farmington's carbon

footprint between 2022 and 2027.

Under the CPP mass-based with intrastate trading case, the San Juan Unit 4 is expected to provide more than 10 percent incremental generation during 2022-2027. This further lowers the costs and risks compared to the CPP mass-based with interstate trading case results. The tradeoff is that the incremental outputs result in higher CO2 emissions from the unit.

For portfolio comparison purposes, the yearly distributions of all portfolios were summarized into a levelized annuity, which is the Net Present Value (“NPV”) of total portfolio costs spread into an average dollar per MWh metric over the planning horizon. Exhibit 22 shows the tradeoff of cost and emission for both CPP cases.

Proprietary & Confidential Page 33

Exhibit 22: Coal Retirement Decision Cost and Emission Tradeoff

Source: Pace Global

Two CPP Cases

Key findings of the stochastic analysis under the two CPP cases are fairly consistent. The New Mexico

power prices are expected to be slightly lower (~2 percent) under the mass-based intrastate trading case.

The lower market prices affect Farmington’s market purchase position and result in lower overall costs for

Farmington’s portfolios.

Proprietary & Confidential Page 34

CPEC Purchase Option

Purchasing a portion of the CPEC plant provides the lowest cost portfolio option. This is largely driven by