2016-2017 Investment Plan Update for the Alternative … · ii ABSTRACT The 2016-2017 Investment...

89

California Energy Commission COMMISSION REPORT 2016-2017 Investment Plan Update for the Alternative and Renewable Fuel and Vehicle Technology Program California Energy Commission Edmund G. Brown Jr., Governor May 2016 | CEC-600-2015-014-CMF

Transcript of 2016-2017 Investment Plan Update for the Alternative … · ii ABSTRACT The 2016-2017 Investment...

California Energy Commission

COMMISSION REPORT

2016-2017 Investment Plan Update for the Alternative and Renewable Fuel and Vehicle Technology Program

California Energy Commission Edmund G. Brown Jr., Governor

May 2016 | CEC-600-2015-014-CMF

California Energy Commission

Robert B. Weisenmiller, Ph.D.

Chair

Commissioners

Karen Douglas, J.D.

J. Andrew McAllister, Ph.D.

David Hochschild

Janea A. Scott

Jacob Orenberg

Primary Author

Jacob Orenberg

Project Manager

Jim McKinney

Program Manager

John P. Butler II

Office Manager

ZERO EMISSION VEHICLE INFRASTRUCTURE OFFICE

John Y. Kato

Deputy Director

FUELS AND TRANSPORTATION DIVISION

Robert P. Oglesby

Executive Director

i

ACKNOWLEDGEMENTS

The following California Energy Commission staff members contributed to the

development of this investment plan update:

Jennifer Allen

Jean Baronas

Leslie Baroody

Elán Bond

Eva Borges

John Butler

Phil Cazel

Elyse Cheung-Sutton

Donald Coe

Al Estrada

Andre Freeman

Tami Haas

Andrew Hom

Elizabeth John

Akasha Kaur Khalsa

Bill Kinney

Samuel Lerman

Thanh Lopez

Jim McKinney

Darren Nguyen

Hieu Nguyen

David Nichols

Tim Olson

Matthew Ong

Larry Rillera

Gordon Schremp

Lindsee Tanimoto

Eric VanWinkle

Gary Yowell

ii

ABSTRACT

The 2016-2017 Investment Plan Update for the Alternative and Renewable Fuel and

Vehicle Technology Program guides the allocation of program funding for fiscal year

2016-2017. This 2016-2017 Investment Plan Update covers the eighth year of the

program and reflects laws, executive orders, and policies to reduce greenhouse gas

emissions, petroleum dependence, and criteria emissions. It details how the California

Energy Commission determines the goal-driven priorities of the program by

incorporating input from stakeholders and the program Advisory Committee and

analyzing project opportunities for funding. These priorities are consistent with the

overall goal of the program “to develop and deploy innovative technologies that

transform California’s fuel and vehicle types to help attain the state’s climate change

policies.”

This 2016-2017 Investment Plan Update establishes recommended funding allocations

based on the identified needs and opportunities of a variety of alternative fuels and

vehicle technologies. As an update, the 2016-2017 Investment Plan Update relies on the

narrative and analyses developed in previous investment plans, most recently the 2015-

2016 Investment Plan Update.

This commission report represents the final step in the development of the 2016-2017

Investment Plan Update.

Keywords: California Energy Commission, Alternative and Renewable Fuel and Vehicle

Technology Program, AB 118, AB 8, funding program, alternative transportation fuels,

investment plan, electric vehicles, hydrogen, biofuels, biomethane, biodiesel, renewable

diesel, diesel substitutes, gasoline substitutes, renewable gasoline, ethanol, natural gas,

federal cost-sharing, workforce training, sustainability, fueling stations, fuel production,

alternative fuel infrastructure

Please use the following citation for this report:

Orenberg, Jacob. 2016. 2016-2017 Investment Plan Update for the Alternative and

Renewable Fuel and Vehicle Technology Program. California Energy Commission,

Fuels and Transportation Division. Publication Number: CEC-600-2015-014-CMF.

iii

iv

TABLE OF CONTENTS Page

Acknowledgements ............................................................................................................................ i

Abstract ................................................................................................................................................ ii

Table of Contents ............................................................................................................................. iv

List of Figures ..................................................................................................................................... v

List of Tables ....................................................................................................................................... v

Executive Summary .......................................................................................................................... 1

CHAPTER 1: Introduction .................................................................................................................. 7

CHAPTER 2: Context of the 2016-2017 Investment Plan Update........................................... 11

Implementation of the Alternative and Renewable Fuel and Vehicle Technology

Program .......................................................................................................................................... 11Alternative Financing Mechanisms and Leveraged Funding ............................................................ 13Program Outreach and Inclusion ........................................................................................................... 15Program Metrics ........................................................................................................................................ 17

Summary of Program Funding .................................................................................................. 17

ARFVTP Benefits and Evaluation .............................................................................................. 22Benefit-Cost Assessments ....................................................................................................................... 22National Renewable Energy Laboratory Program Benefits Guidance Report ............................... 22

Related Policies and Programs .................................................................................................. 26Air Quality Improvement Program/Low Carbon Transportation Program ................................... 26AB 32/Greenhouse Gas Reduction Fund .............................................................................................. 27Low-Carbon Fuel Standard ...................................................................................................................... 28Renewable Fuel Standard ........................................................................................................................ 30Executive Order on Sustainable Freight ............................................................................................... 31Executive Order on Zero-Emission Vehicles ........................................................................................ 31Charge Ahead California Initiative ........................................................................................................ 32CPUC Alternative-Fueled Vehicle Proceedings .................................................................................... 32

CHAPTER 3: Alternative Fuel Production and Supply .............................................................. 33

Biofuel Production and Supply .................................................................................................. 33

Summary of Alternative Fuel Production and Supply Allocations .................................... 39

CHAPTER 4: Alternative Fuel Infrastructure .............................................................................. 40

Electric Charging Infrastructure ............................................................................................... 40

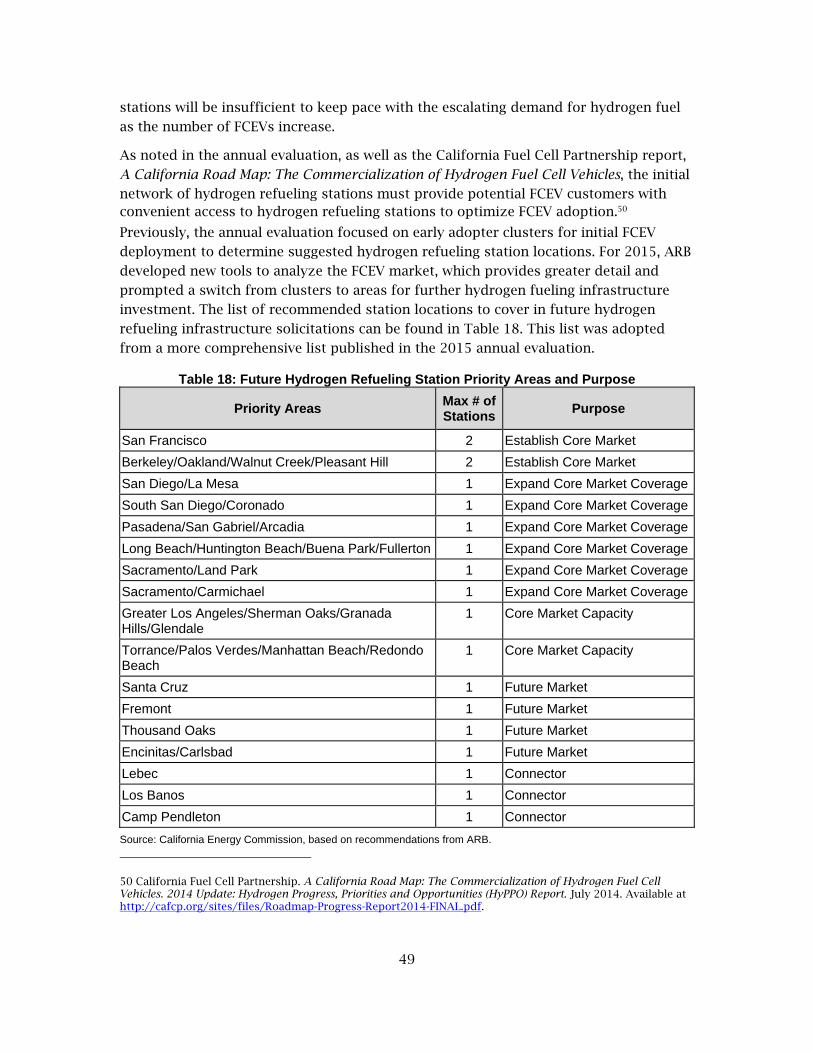

Hydrogen Refueling Infrastructure .......................................................................................... 45

Natural Gas Fueling Infrastructure ........................................................................................... 51

Summary of Alternative Fuel Infrastructure Allocations .................................................... 53

v

CHAPTER 5: Alternative Fuel and Advanced Technology Vehicles ....................................... 54

Medium- and Heavy-Duty Vehicle Technology Demonstration and Scale-Up ................. 54

Natural Gas Vehicles .................................................................................................................... 58

Light-Duty Electric Vehicles ....................................................................................................... 63

Summary of Alternative Fuel and Advanced Technology Vehicles Allocations ............. 67

CHAPTER 6: Related Needs and Opportunities ......................................................................... 68

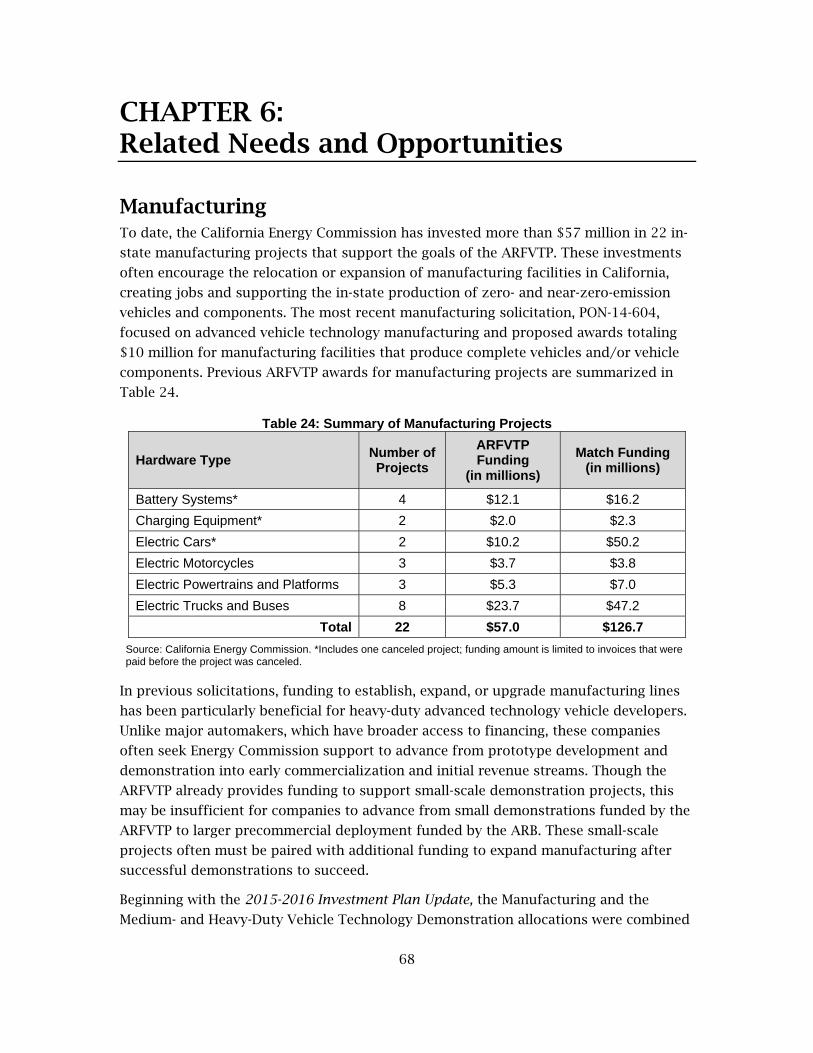

Manufacturing ............................................................................................................................... 68

Emerging Opportunities ............................................................................................................. 69

Workforce Training and Development .................................................................................... 71

Regional Readiness ...................................................................................................................... 73

Summary of Related Needs and Opportunities Allocations ............................................... 76

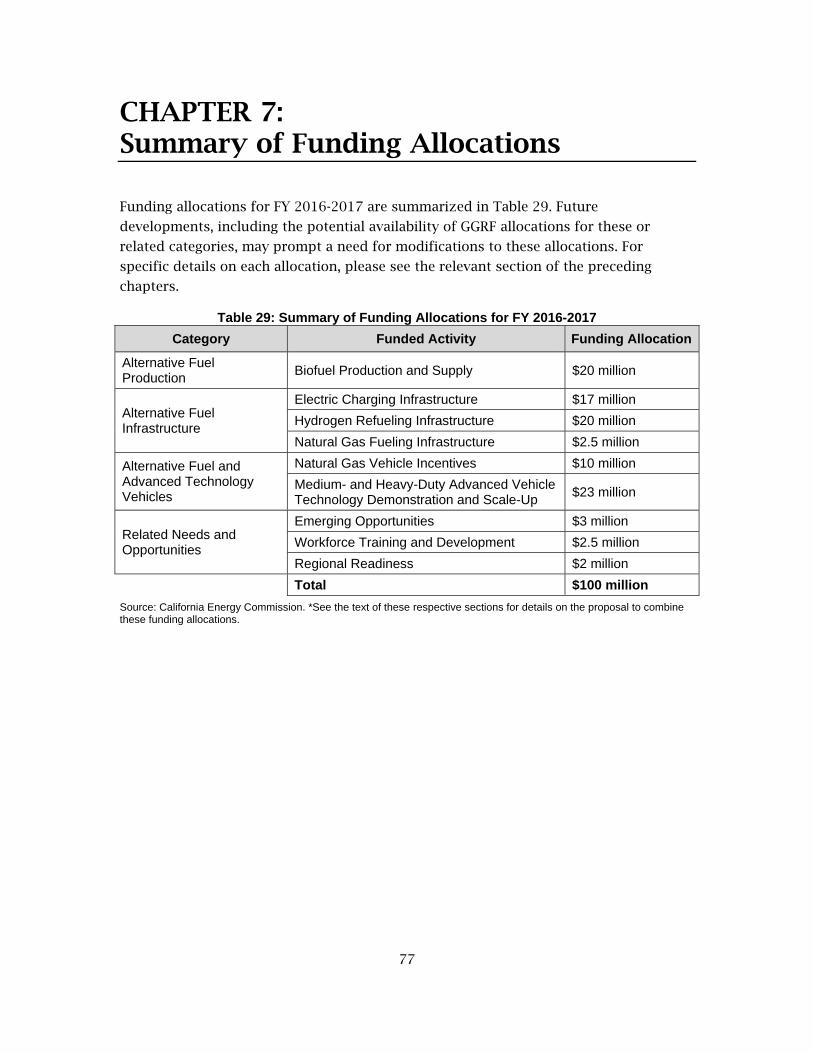

CHAPTER 7: Summary of Funding Allocations .......................................................................... 77

LIST OF FIGURES Page

Figure 1: Schematic of ARFVTP Implementation ...................................................................... 13

Figure 2: Summary of GHG Emissions Reductions From the Expected Benefits of 223

Projects Through 2025 ................................................................................................................... 24

Figure 3: GHG Reductions From Expected and Market Transformation Benefits in

Comparison to Required Market Growth Benefits .................................................................... 26

Figure 4: Low-Carbon Fuel Standard Credit Spot Market Prices ............................................ 29

Figure 5: California and National Sales of PEVs ........................................................................ 64

LIST OF TABLES Page

Table ES-1: Previous ARFVTP Awards as of December 31, 2015 .............................................. 2

Table ES-2: Most Recent and Current Investment Plan Allocations (in millions) .................. 5

Table 1: Greenhouse Gas, Fuel, and Air Quality Goals and Milestones ................................... 8

Table 2: ARFVTP Awards by Fuel Type as of December 31, 2015 ......................................... 19

Table 3: Previous ARFVTP Awards as of December 31, 2015 ................................................ 20

Table 4: Most Recent and Current Investment Plan Allocations (in millions) .................... 21

vi

Table 5: Benefit Categories in NREL Program Benefits Guidance .......................................... 23

Table 6: Summary of GHG Emission and Petroleum Fuel Reduction Benefits Based on

262 Projects ....................................................................................................................................... 25

Table 7: FY 2015-2016 AQIP and Low Carbon Transportation GGRF Allocations ............. 28

Table 8: Projected Fuel Volumes and Proposed RFS Percentages for 2014 – 2017 ........... 30

Table 9: Summary of Biofuel Production Awards to Date ...................................................... 35

Table 10: GHG Emission Reduction Potential of Commercial-Scale ARFVTP Projects ...... 36

Table 11: Sample of Precommercial ARFVTP Projects ............................................................. 37

Table 12: FY 2016-2017 Funding for Alternative Fuel Production and Supply .................. 39

Table 13: Charging Stations Funded by ARFVTP as of December 31, 2015 ........................ 40

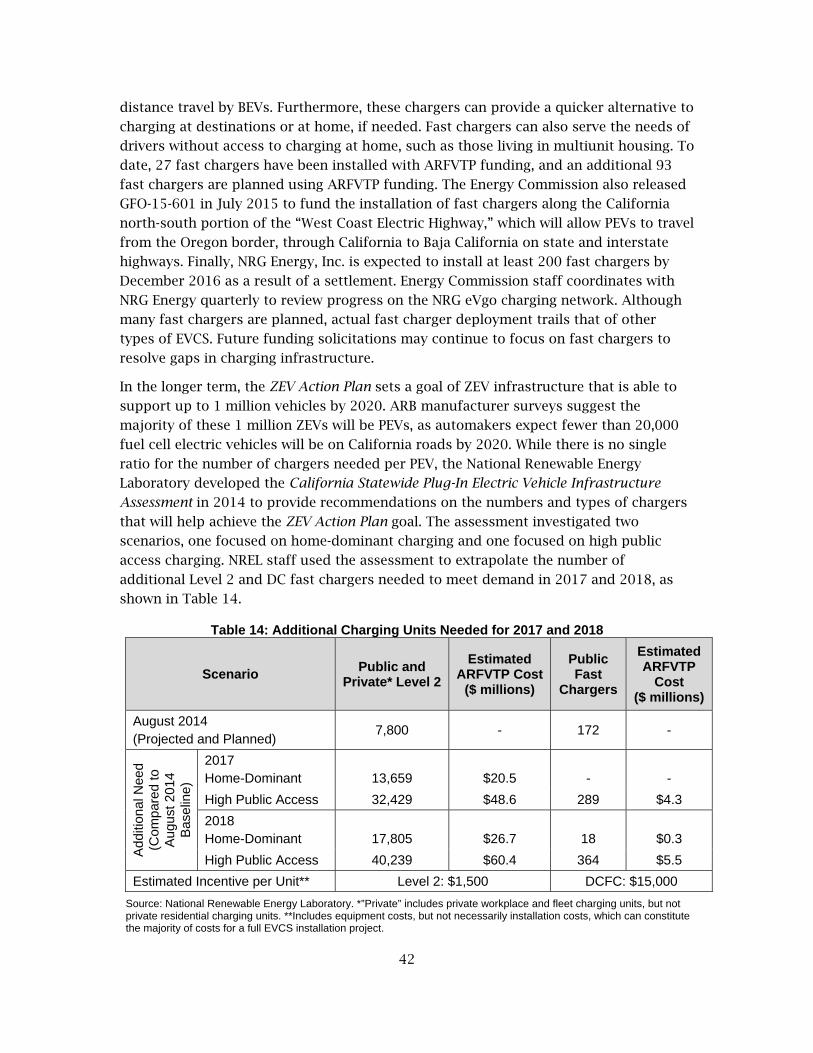

Table 14: Additional Charging Units Needed for 2017 and 2018 ......................................... 42

Table 15: Proposed and Approved Utility EVCS Investments ................................................ 44

Table 16: Publicly Available Hydrogen Refueling Stations ..................................................... 46

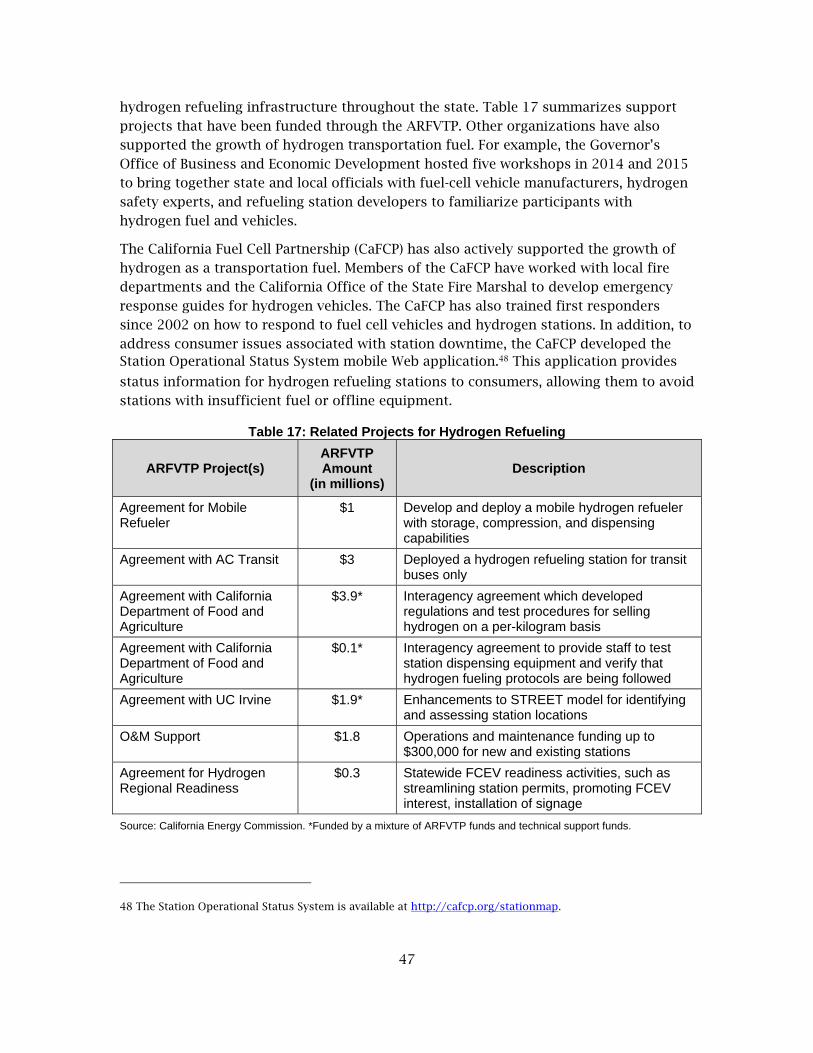

Table 17: Related Projects for Hydrogen Refueling ................................................................. 47

Table 18: Future Hydrogen Refueling Station Priority Areas and Purpose ......................... 49

Table 19: FY 2016-2017 Funding for Alternative Fuel Infrastructure .................................. 53

Table 20: Demonstration Projects Supported by ARFVTP ...................................................... 55

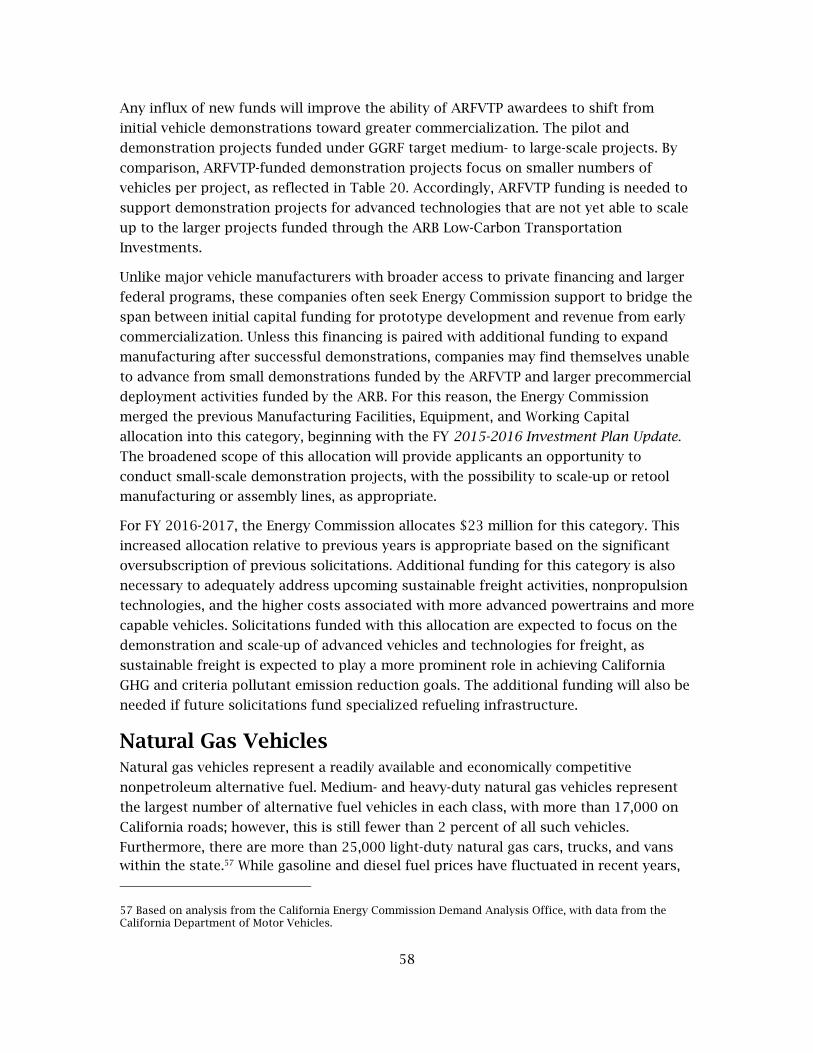

Table 21: ARFVTP Funding for Natural Gas Vehicle Deployment ......................................... 62

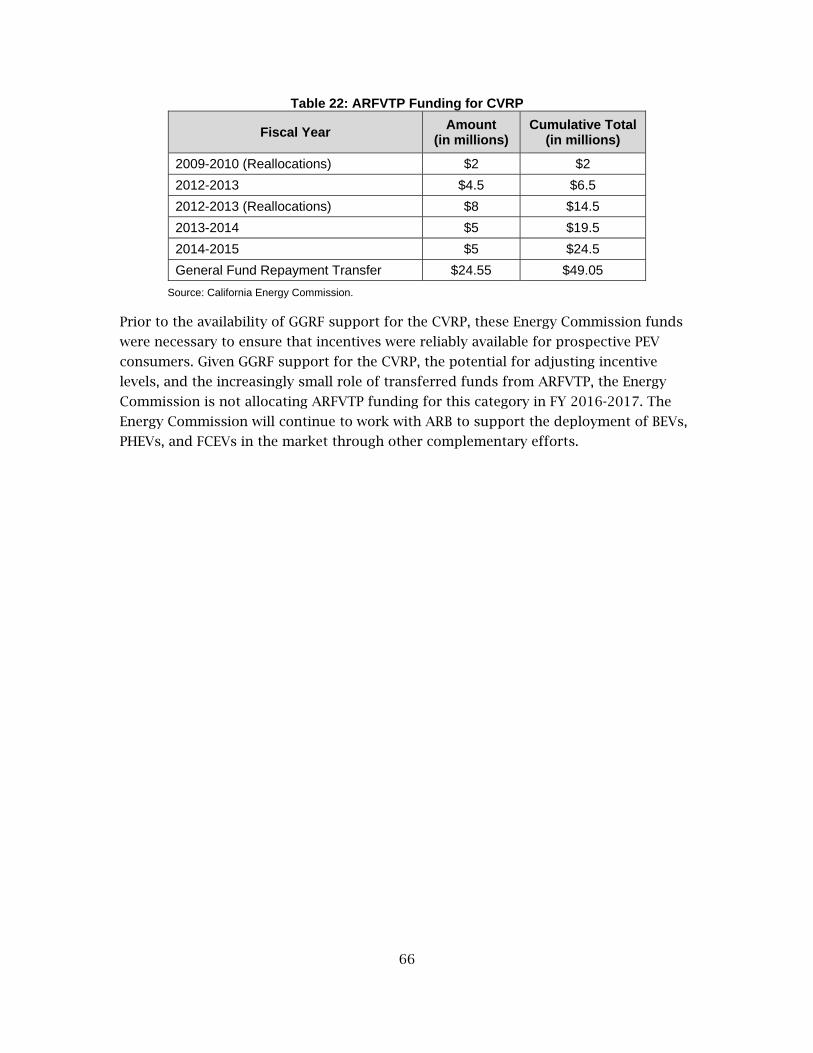

Table 22: ARFVTP Funding for CVRP ........................................................................................... 66

Table 23: FY 2016-2017 Funding for Alternative Fuel and Advanced Technology Vehicles

............................................................................................................................................................. 67

Table 24: Summary of Manufacturing Projects ......................................................................... 68

Table 25: Summary of ARFVTP Agreements From Emerging Opportunities Category .... 70

Table 26: Historical Workforce Training Funding From FY 2008-2009 Through FY 2015-

2016 .................................................................................................................................................... 72

Table 27: Regional Alternative Fuel Readiness Planning and Implementation Awards ... 75

Table 28: FY 2016-2017 Funding for Related Needs and Opportunities ............................. 76

Table 29: Summary of Funding Allocations for FY 2016-2017 .............................................. 77

vii

1

EXECUTIVE SUMMARY

California has adopted several aggressive goals for reducing greenhouse gas (GHG) emissions,

including:

A near-term goal of reducing GHG emissions to 1990 levels by 2020.

An interim goal of reducing GHG emissions to 40 percent below 1990 levels by 2030.

A long-term goal of reducing GHG emissions to 80 percent below 1990 levels by 2050.

Achieving these goals will require significant technological and market changes within the

transportation sector, which accounts for 37 percent of state greenhouse gas emissions. Both

California and the federal government have also established numerous goals and mandates to

reduce criteria air pollution and increase the prevalence of alternative fuels and vehicles.

To help address these goals, the California Legislature passed Assembly Bill 118 (Núñez, Chapter

750, Statutes of 2007). This legislation created the Alternative and Renewable Fuel and Vehicle

Technology Program (ARFVTP), administered by the California Energy Commission. With funds

collected from vehicle and vessel registration, vehicle identification plates, and smog-abatement

fees, the ARFVTP provides up to $100 million per year for projects that will "transform

California’s fuel and vehicle types to help attain the state’s climate change policies." The statute

also calls for the Energy Commission to “develop and deploy technology and alternative and

renewable fuels in the marketplace, without adopting any one preferred fuel or technology.”

Assembly Bill 8 (Perea, Chapter 401, Statutes of 2013) subsequently extended the collection of

fees that support the ARFVTP through January 1, 2024.

As part of the ARFVTP, the Energy Commission prepares and adopts an annual investment plan

update that identifies the funding priorities for the coming fiscal year. The funding allocations

reflect the potential for each alternative fuel and vehicle technology to contribute to the goals of

the program; the anticipated barriers and opportunities associated with each fuel or technology;

the effect of other entities’ investments, policies, programs, and statutes; and a portfolio-based

approach that avoids adopting any preferred fuel or technology. This commission report of the

2016-2017 Investment Plan Update is the final version of the document.

Context of the 2016-2017 Investment Plan Update The 2016-2017 Investment Plan Update builds on the analyses and recommendations contained

in previously adopted investment plans and investment plan updates. Since the first investment

plan, the Energy Commission has invested $606 million in projects that will support alternative

and renewable fuels and advanced vehicle technologies. These existing projects provide direct

feedback on how the ARFVTP can maximize value in reducing near-term greenhouse gas

emissions while supporting the transformation of the California transportation sector toward

fuels and technologies that can meet the more drastic emission reductions required by 2050.

Projects funded by the ARFVTP are summarized in Table ES-1 and support a broad portfolio of

fuel types, supply chain phases, and commercialization phases.

2

Table ES-1: Previous ARFVTP Awards as of December 31, 2015

Category Funded Activity Cumulative

Awards to Date(in millions)*

# of Projects or Units

Alternative Fuel Production

Biomethane Production $50.9 16 Projects

Gasoline Substitutes Production $27.2 14 Projects

Diesel Substitutes Production $57.4 20 Projects

Alternative Fuel Infrastructure

Electric Vehicle Charging Infrastructure $40.7 7,490 Charging Stations

Hydrogen Refueling Infrastructure $96.0 49 Fueling Stations

E85 Fueling Infrastructure $13.7 158 Fueling Stations

Upstream Biodiesel Infrastructure $4.0 4 Infrastructure Sites

Natural Gas Fueling Infrastructure $21.0 65 Fueling Stations

Alternative Fuel and Advanced

Technology Vehicles

Natural Gas Vehicle Deployment** $56.6 2,809 Vehicles

Propane Vehicle Deployment** $6.0 514 Trucks

Light-Duty Electric Vehicle Deployment $25.1 10,700 Cars

Medium- and Heavy-Duty Electric Vehicle Deployment $4.0 150 Trucks

Medium- and Heavy-Duty Vehicle Technology Demonstration and Scale-Up

$93.7 44 Demonstrations

Related Needs and Opportunities

Manufacturing $57.0 22 Manufacturing Projects

Emerging Opportunities † †

Workforce Training and Development $27.7 83 Recipients

Fuel Standards and Equipment Certification $3.9 1 Project

Sustainability Studies $2.1 2 Projects

Regional Alternative Fuel Readiness and Planning $7.6 34 Regional Plans

Centers for Alternative Fuels $5.8 5 Centers

Technical Assistance and Program Evaluation $5.6 n/a

Total $606.0

Source: California Energy Commission. *Includes all projects and agreements that have been executed or approved at an Energy Commission business meeting or are expected for business meeting approval following a notice of proposed award. Does not include cancelled projects that received no funding from ARFVTP. **Funding includes both completed and pending vehicle incentives. †Previous awards from this category have been reclassified by project type into other rows.

3

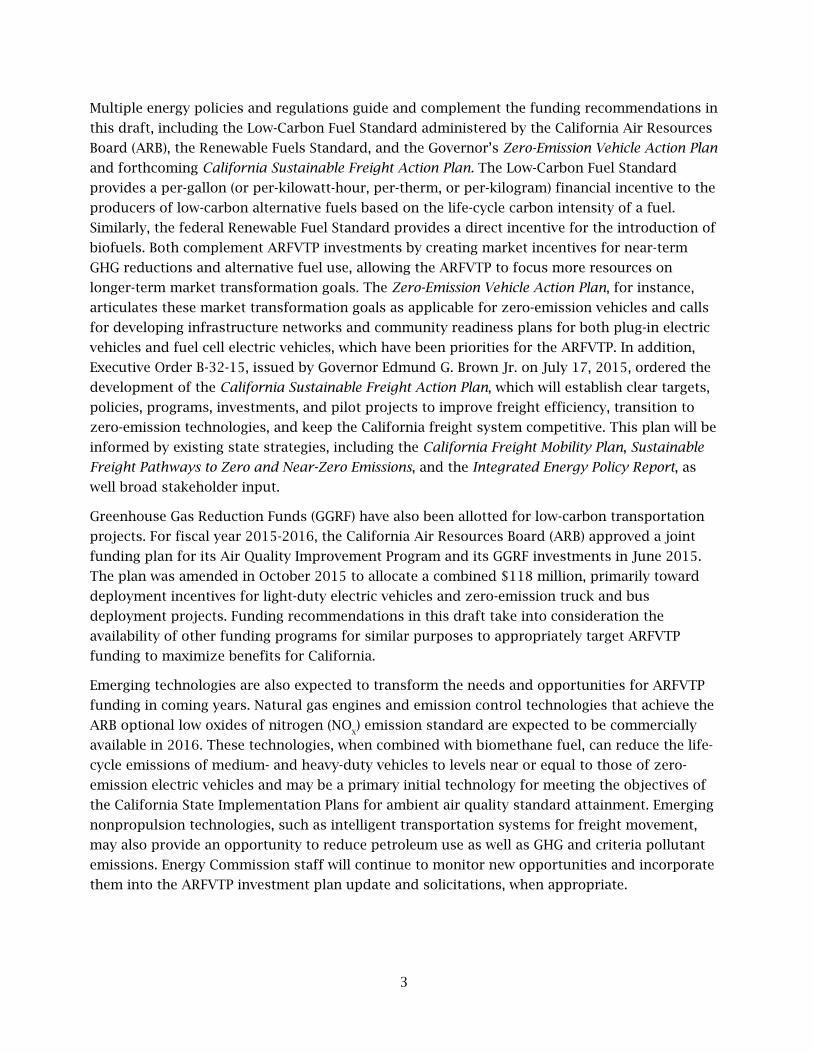

Multiple energy policies and regulations guide and complement the funding recommendations in

this draft, including the Low-Carbon Fuel Standard administered by the California Air Resources

Board (ARB), the Renewable Fuels Standard, and the Governor’s Zero-Emission Vehicle Action Plan

and forthcoming California Sustainable Freight Action Plan. The Low-Carbon Fuel Standard

provides a per-gallon (or per-kilowatt-hour, per-therm, or per-kilogram) financial incentive to the

producers of low-carbon alternative fuels based on the life-cycle carbon intensity of a fuel.

Similarly, the federal Renewable Fuel Standard provides a direct incentive for the introduction of

biofuels. Both complement ARFVTP investments by creating market incentives for near-term

GHG reductions and alternative fuel use, allowing the ARFVTP to focus more resources on

longer-term market transformation goals. The Zero-Emission Vehicle Action Plan, for instance,

articulates these market transformation goals as applicable for zero-emission vehicles and calls

for developing infrastructure networks and community readiness plans for both plug-in electric

vehicles and fuel cell electric vehicles, which have been priorities for the ARFVTP. In addition,

Executive Order B-32-15, issued by Governor Edmund G. Brown Jr. on July 17, 2015, ordered the

development of the California Sustainable Freight Action Plan, which will establish clear targets,

policies, programs, investments, and pilot projects to improve freight efficiency, transition to

zero-emission technologies, and keep the California freight system competitive. This plan will be

informed by existing state strategies, including the California Freight Mobility Plan, Sustainable

Freight Pathways to Zero and Near-Zero Emissions, and the Integrated Energy Policy Report, as

well broad stakeholder input.

Greenhouse Gas Reduction Funds (GGRF) have also been allotted for low-carbon transportation

projects. For fiscal year 2015-2016, the California Air Resources Board (ARB) approved a joint

funding plan for its Air Quality Improvement Program and its GGRF investments in June 2015.

The plan was amended in October 2015 to allocate a combined $118 million, primarily toward

deployment incentives for light-duty electric vehicles and zero-emission truck and bus

deployment projects. Funding recommendations in this draft take into consideration the

availability of other funding programs for similar purposes to appropriately target ARFVTP

funding to maximize benefits for California.

Emerging technologies are also expected to transform the needs and opportunities for ARFVTP

funding in coming years. Natural gas engines and emission control technologies that achieve the

ARB optional low oxides of nitrogen (NOX) emission standard are expected to be commercially

available in 2016. These technologies, when combined with biomethane fuel, can reduce the life-

cycle emissions of medium- and heavy-duty vehicles to levels near or equal to those of zero-

emission electric vehicles and may be a primary initial technology for meeting the objectives of

the California State Implementation Plans for ambient air quality standard attainment. Emerging

nonpropulsion technologies, such as intelligent transportation systems for freight movement,

may also provide an opportunity to reduce petroleum use as well as GHG and criteria pollutant

emissions. Energy Commission staff will continue to monitor new opportunities and incorporate

them into the ARFVTP investment plan update and solicitations, when appropriate.

4

2016-2017 Investment Plan Update

Assembly Bill 1314 (Wieckowski, Chapter 487, Statutes of 2011) reduced the scope of the annual

ARFVTP investment plan to an update. The update builds on the work of previous investment

plans while highlighting differences from those previous years. The resulting funding allocations

are intended to reflect the unique technological and market conditions for each of these fuels

and technologies. These funding allocations are discussed in detail in Chapters 3 through 6 of

this commission report, which describe the barriers and opportunities associated with

alternative fuel production, alternative fuel distribution infrastructure, alternative fuel and

advanced technology vehicles, and related activities that can accelerate progress in these areas.

Table ES-2 outlines the funding allocations of the two most recent investment plan updates, in

comparison to the funding allocations for FY 2016-2017.

5

Table ES-2: Most Recent and Current Investment Plan Allocations (in millions)

Category Funded Activity 2014-2015 2015-2016 2016-2017

Alternative Fuel Production

Biofuel Production and Supply $20 $20 $20

Alternative Fuel Infrastructure

Electric Charging Infrastructure $15 $17 $17

Hydrogen Refueling Infrastructure $20 $20 $20

Natural Gas Fueling Infrastructure $1.5 $5 $2.5

Alternative Fuel and Advanced

Technology Vehicles

Natural Gas Vehicle Incentives $10 $10 $10

Light-Duty Electric Vehicle Deployment $5 - -

Medium- and Heavy-Duty Vehicle Technology Demonstration and Scale-Up

$15 $20* $23*

Related Needs and Opportunities

Manufacturing $5

Emerging Opportunities $6 $3 $3

Workforce Training and Development Agreements $2.5 $3 $2.5

Regional Alternative Fuel Readiness and Planning - $2 $2

Total $100 $100 $100

Source: California Energy Commission. *See the text of these respective sections in Chapters 5 and 6 for details on the proposal to combine these funding allocations.

6

7

CHAPTER 1: Introduction

“We must demonstrate that reducing carbon is compatible with an abundant economy

and human well‐being.”

– Governor Edmund G. Brown Jr.1

California has been at the forefront of national efforts to reduce greenhouse gas (GHG)

emissions for nearly a decade since the Global Warming Solutions Act of 2006 was signed into law.2 With the passage of that law, California established a goal of reducing statewide GHG

emissions to 1990 levels by 2020. In addition, Executive Order S-3-05 set a longer-term goal to

reduce GHG emissions to 80 percent below 1990 levels by 2050. Governor Brown subsequently

issued Executive Order B-30-15, which set an interim goal to reduce statewide GHG emissions to

40 percent below 1990 levels by 2030 to ensure California meets the targets of Executive Order

S-3-05.

The California Greenhouse Gas Emission Inventory, prepared annually by the California Air

Resources Board (ARB), indicates that the transportation sector is responsible for 37 percent of in-state GHG emissions, making it the largest emitter in the state.3 Though low-carbon

alternative fuel use has steadily increased in recent years, petroleum-based gasoline and diesel

fuel account for more than 90 percent of California ground transportation fuel use. California

will need to continue to reduce petroleum fuel use to meet state GHG emission targets.

Accordingly, Governor Brown set an objective during his 2015 inaugural address of reducing

petroleum use in cars and trucks by up to 50 percent by 2030. An ARB analysis suggests these

reductions are possible by expanding existing efforts, which include increasing vehicle

efficiency, reducing fuel carbon intensity, and providing support for zero-emission vehicles and renewable fuel production.4

Other aspects of the transportation sector similarly challenge future health and economic

prosperity in California. In the American Lung Association 2015 State of the Air report,

California metropolitan areas represented the top five “Most Polluted Cities,” with the worst

1 Office of Governor Edmund G. Brown Jr. Governor Brown Sworn In, Delivers Inaugural Address. January 5, 2015. Available at https://www.gov.ca.gov/news.php?id=18828.

2 Assembly Bill 32, Núñez, Chapter 488, Statutes of 2006.

3 California Air Resources Board. California Greenhouse Gas Emission Inventory. June 30, 2015. Available at http://www.arb.ca.gov/cc/inventory/data/data.htm.

4 California Air Resources Board. Cutting Petroleum Use in Half by 2030. Available at http://www.arb.ca.gov/newsrel/petroleum_reductions.pdf.

8

pollution from both ozone and particle pollution (including Fresno-Madera, Visalia-Porterville-Hanford, Bakersfield, Los Angeles-Long Beach, Modesto-Merced and Sacramento-Roseville).5 In

the future, to meet federal Clean Air Act standards in two of the most heavily polluted air basins

in California, the transportation sector may need to reduce oxides of nitrogen (NOX) by almost 90

percent below 2010 levels by 2032.6 These air quality impacts may be exacerbated by drier,

hotter weather caused by climate change.

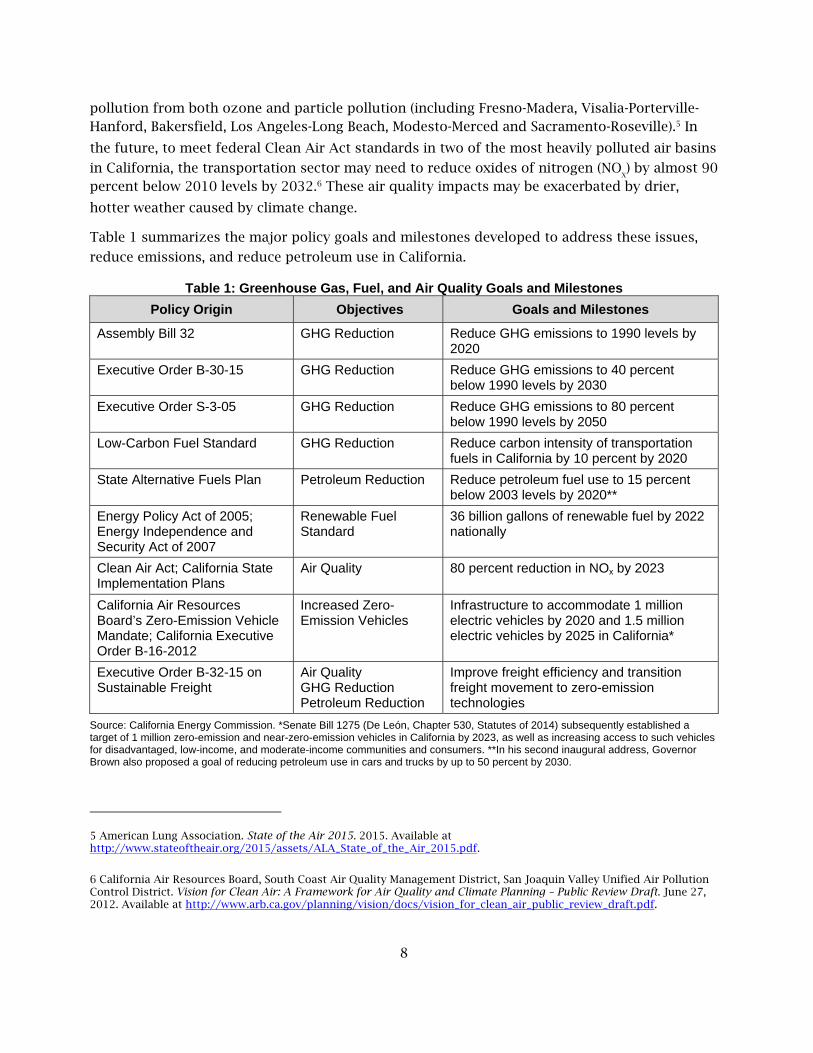

Table 1 summarizes the major policy goals and milestones developed to address these issues,

reduce emissions, and reduce petroleum use in California.

Table 1: Greenhouse Gas, Fuel, and Air Quality Goals and Milestones

Policy Origin Objectives Goals and Milestones

Assembly Bill 32 GHG Reduction Reduce GHG emissions to 1990 levels by 2020

Executive Order B-30-15 GHG Reduction Reduce GHG emissions to 40 percent below 1990 levels by 2030

Executive Order S-3-05 GHG Reduction Reduce GHG emissions to 80 percent below 1990 levels by 2050

Low-Carbon Fuel Standard GHG Reduction Reduce carbon intensity of transportation fuels in California by 10 percent by 2020

State Alternative Fuels Plan Petroleum Reduction Reduce petroleum fuel use to 15 percent below 2003 levels by 2020**

Energy Policy Act of 2005; Energy Independence and Security Act of 2007

Renewable Fuel Standard

36 billion gallons of renewable fuel by 2022 nationally

Clean Air Act; California State Implementation Plans

Air Quality 80 percent reduction in NOx by 2023

California Air Resources Board’s Zero-Emission Vehicle Mandate; California Executive Order B-16-2012

Increased Zero-Emission Vehicles

Infrastructure to accommodate 1 million electric vehicles by 2020 and 1.5 million electric vehicles by 2025 in California*

Executive Order B-32-15 on Sustainable Freight

Air Quality GHG Reduction Petroleum Reduction

Improve freight efficiency and transition freight movement to zero-emission technologies

Source: California Energy Commission. *Senate Bill 1275 (De León, Chapter 530, Statutes of 2014) subsequently established a target of 1 million zero-emission and near-zero-emission vehicles in California by 2023, as well as increasing access to such vehicles for disadvantaged, low-income, and moderate-income communities and consumers. **In his second inaugural address, Governor Brown also proposed a goal of reducing petroleum use in cars and trucks by up to 50 percent by 2030.

5 American Lung Association. State of the Air 2015. 2015. Available at http://www.stateoftheair.org/2015/assets/ALA_State_of_the_Air_2015.pdf.

6 California Air Resources Board, South Coast Air Quality Management District, San Joaquin Valley Unified Air Pollution Control District. Vision for Clean Air: A Framework for Air Quality and Climate Planning – Public Review Draft. June 27, 2012. Available at http://www.arb.ca.gov/planning/vision/docs/vision_for_clean_air_public_review_draft.pdf.

9

To help address the state objectives, the California Legislature passed Assembly Bill 118 (Núñez,

Chapter 750, Statutes of 2007). This legislation created the Alternative and Renewable Fuel and

Vehicle Technology Program (ARFVTP), administered by the California Energy Commission. With

funds collected from vehicle and vessel registration, vehicle identification plates, and smog

abatement fees, the ARFVTP provides up to $100 million per year for projects that will

"transform California’s fuel and vehicle types to help attain the state’s climate change policies."

This program includes projects that:

Reduce the use and dependence on petroleum transportation fuels and increase the use

of alternative and renewable fuels and advanced vehicle technologies.

Produce sustainable alternative and renewable low-carbon fuels in California.

Expand alternative fueling infrastructure and fueling stations available to the public,

existing fleets, public transit, and transportation corridors.

Improve the efficiency, performance, and market viability of alternative light-, medium-,

and heavy-duty vehicle technologies.

Retrofit medium- and heavy-duty on-road and off-road vehicle fleets to alternative

technologies or fuel use.

Offer incentives for the purchase of alternative fuel vehicles.

Establish workforce training programs and conduct public outreach on the benefits of

alternative transportation fuels and vehicle technologies.

Support local and regional planning efforts for zero-emission vehicle and fueling

infrastructure deployment.

The statute also calls for the Energy Commission to “develop and deploy technology and

alternative and renewable fuels in the marketplace, without adopting any one preferred fuel or technology.”7 Assembly Bill 8 (Perea, Chapter 401, Statutes of 2013) subsequently extended the

collection of fees that support the ARFVTP through January 1, 2024.

As part of the ARFVTP, the Energy Commission prepares and adopts an annual investment plan

update that identifies the funding priorities for the coming fiscal year. The funding allocations

reflect the potential for each alternative fuels and vehicle technology to contribute to the goals

of the program; the anticipated barriers and opportunities associated with each fuel or

technology; the effect of other entities’ investments, policies, programs, and statutes; and a

portfolio-based approach that avoids adopting any preferred fuel or technology. The investment

plan update also describes how the allocations will complement existing public and private

efforts, including related state programs.

The 2016-2017 Investment Plan Update is the eighth investment plan document in the history of

the ARFVTP and builds on the analyses and recommendations contained in the prior documents.

7 California Health and Safety Code Section 44272(a).

10

This commission report is the final version of the 2016-2017 Investment Plan Update. The

Energy Commission held public workshops with the ARFVTP Advisory Committee on November

6, 2015, in Sacramento and January 21, 2016, in Long Beach. Representatives from fuel and

technology industry groups, nongovernmental entities, other state agencies, and the public

discussed and commented on this document during these workshops. Comments on the 2016-2017 Investment Plan Update were also provided using the Energy Commission’s docket system.8

State law requires the Energy Commission to submit a draft of the investment plan update to the

Legislature concurrent with the Governor’s budget in January and an adopted investment plan

update concurrent with the Governor’s revised budget in May.

Chapter 2 of this document provides an update on Energy Commission implementation of the

ARFVTP to date, as well as a review of the most relevant programs, policies, and regulations that

affect the allocations of this investment plan update. The subsequent chapters are organized

according to the traditional supply chain of alternative fuels. Chapter 3 addresses the barriers

and opportunities associated with alternative fuel production and supply within California.

Chapter 4 focuses on the distribution of that alternative fuel and associated refueling

infrastructure, and Chapter 5 focuses on the vehicles that will use the alternative fuels and

advanced technologies. Chapter 6 identifies related activities and investments that can expedite

the development and deployment of alternative fuels and advanced technology vehicles. Finally,

Chapter 7 summarizes the funding allocations.

All allocations assume a complete $100 million appropriation for the ARFVTP, and the Energy

Commission expects to be fully funded for fiscal year 2016-2017. In the event that less than

$100 million is available, the allocations in this document may be revised in subsequent versions

or amended after final adoption. Future developments, including the potential availability of

funding from the Greenhouse Gas Reduction Fund for these or related categories, may also

prompt a need for modifications to these allocations.

8 The Energy Commission encourages written comments on the 2016-2017 Investment Plan Update. Please include your name or the name of your organization in the name of the attached file. Send your comments as either a Microsoft Word® document or a Portable Document Format file (PDF) to [email protected]. In the subject line, please include the docket number 15-ALT-01.

11

CHAPTER 2: Context of the 2016-2017 Investment Plan Update

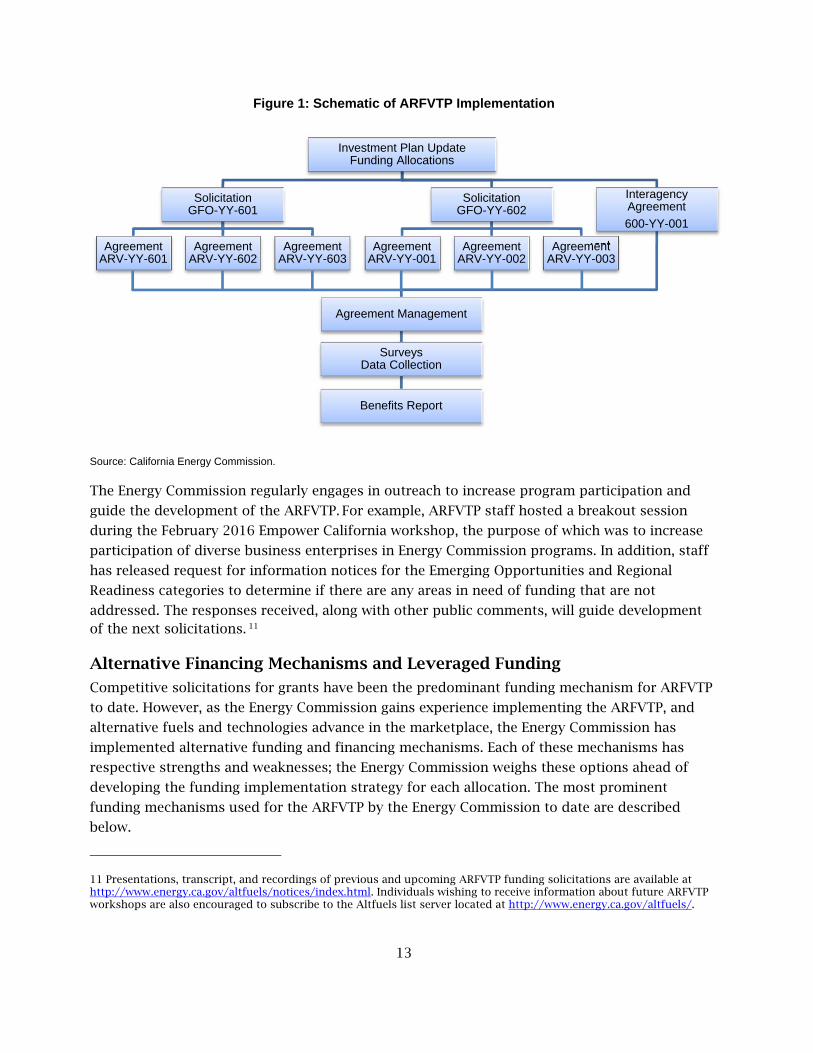

Implementation of the Alternative and Renewable Fuel and Vehicle Technology Program Since the beginning of the ARFVTP, the Energy Commission has developed a consistent approach

toward program implementation, which is summarized in Figure 1. An annual investment plan

update determines the coming fiscal-year funding allocation for categories of projects and is adopted at an Energy Commission business meeting.9 Energy Commission staff initially

proposes funding allocations based on the GHG emission reduction potential of alternative fuels

and technologies (both near-term and long-term), identification of the primary market and/or

technological opportunities and barriers, evaluation of complementary funding or regulations,

consideration of policy priorities, and a statutory directive to maintain a "portfolio-based

approach." Prior to official adoption by the Energy Commission, the investment plan update is

proposed and revised across several drafts and incorporates stakeholder input from public

Advisory Committee workshops.

Each investment plan update identifies funding allocations for particular segments of the supply

chain for alternative fuel or vehicle technologies. They typically do not, however, determine the

specific focus of future funding solicitations. Based on these funding allocations, the Energy

Commission subsequently issues a series of competitive solicitations, known as grant funding

opportunities (GFOs, designated as “GFO-[Year]-XXX”; formerly program opportunity notices, or

PONs). Each solicitation has a set of scoring criteria that reflect project selection preferences established by statute.10 Cost-related scoring criteria are generally given more weight for

commercially mature technologies. Priority is also given to projects that will benefit

economically disadvantaged areas or areas with poor air quality. Some solicitations are first-

come, first-served and establish minimum requirements that must be achieved to be eligible for

funding.

Energy Commission staff reviews, scores, and ranks the proposals for each solicitation using the

evaluation criteria developed for that particular solicitation. Outside agencies and contractors

may also provide technical assessments of the proposals. Based on the total scores of each

application, the Energy Commission releases a notice of proposed awards (NOPA) for each

9 The most recently adopted investment plan update, covering fiscal year 2015-2016, was adopted at the April 8, 2015, Energy Commission Business Meeting. It is available at http://energy.ca.gov/2014-ALT-01/documents/.

10 These preference criteria are listed in Health and Safety Code Section 44272 (c) and (d).

12

solicitation. The NOPA ranks each application by score and provides a proposed funding amount

for each proposal in order of score until available funding within the solicitation has been

recommended for award. For specialized agreements with certain partner agencies, including,

but not limited, to the California Employment Training Panel, the University of California

campuses, and the Division of Measurement Standards, the Energy Commission has the

discretion to develop interagency agreements without using the solicitation process.

AB 8 added a “benefit-cost score” element to the selection of projects for ARFVTP funding. This

addition factors into the scoring and selection of projects during the proposal review period of a

solicitation. The benefit-cost score is defined as “…a project’s expected or potential greenhouse

gas emissions reduction per dollar awarded by the commission to the project.” AB 8 requires the

Energy Commission to rank applications for funding based on existing solicitation scoring

criteria, with “additional preference to funding those projects with higher benefit-cost scores.”

In recent solicitations, this preference has been incorporated both as part of the general scoring

criteria and as a potential tie-breaker in the event of proposals receiving equal scores.

Each funded application becomes an agreement (usually designated as “ARV-[Year]-XXX”) once it

has been executed by the Energy Commission and the applicant. Energy Commission staff

oversees the completion of these agreements according to the respective schedules, budgets,

scopes of work, and terms and conditions of these agreements.

Data collection and project review are also key parts of ARFVTP implementation. The Energy

Commission periodically surveys funding recipients on the anticipated results of their projects,

with a broad array of questions relating to alternative fuel use, petroleum displacement, GHG

emission reductions, and in-state economic benefits. The Energy Commission also continues to

collect data from funding recipients after completion of a project, typically for six months.

Information from all these efforts feeds into the development of a biennial ARFVTP benefits

report, as well as other ARFVTP measurement, verification, and evaluation efforts.

13

Figure 1: Schematic of ARFVTP Implementation

Source: California Energy Commission.

The Energy Commission regularly engages in outreach to increase program participation and

guide the development of the ARFVTP. For example, ARFVTP staff hosted a breakout session

during the February 2016 Empower California workshop, the purpose of which was to increase

participation of diverse business enterprises in Energy Commission programs. In addition, staff

has released request for information notices for the Emerging Opportunities and Regional

Readiness categories to determine if there are any areas in need of funding that are not

addressed. The responses received, along with other public comments, will guide development of the next solicitations. 11

Alternative Financing Mechanisms and Leveraged Funding

Competitive solicitations for grants have been the predominant funding mechanism for ARFVTP

to date. However, as the Energy Commission gains experience implementing the ARFVTP, and

alternative fuels and technologies advance in the marketplace, the Energy Commission has

implemented alternative funding and financing mechanisms. Each of these mechanisms has

respective strengths and weaknesses; the Energy Commission weighs these options ahead of

developing the funding implementation strategy for each allocation. The most prominent

funding mechanisms used for the ARFVTP by the Energy Commission to date are described

below.

11 Presentations, transcript, and recordings of previous and upcoming ARFVTP funding solicitations are available at http://www.energy.ca.gov/altfuels/notices/index.html. Individuals wishing to receive information about future ARFVTP workshops are also encouraged to subscribe to the Altfuels list server located at http://www.energy.ca.gov/altfuels/.

Investment Plan UpdateFunding Allocations

SolicitationGFO-YY-601

AgreementARV-YY-601

AgreementARV-YY-602

AgreementARV-YY-603

SolicitationGFO-YY-602

AgreementARV-YY-001

AgreementARV-YY-002

AgreementARV-YY-003

InteragencyAgreement

600-YY-001

Agreement Management

SurveysData Collection

Benefits Report

14

Competitive Solicitation for Grants – This type of solicitation represents the most

common funding mechanism for the ARFVTP to date. It is flexible, as project

requirements and scoring criteria can be adapted for a broad variety of commercial and

technological maturity levels. Competitive scoring allows for increased scrutiny on key

issues for each project type. Because of the amount of time and attention required to

review each application (and oversee each subsequent award), this approach is more

manageable when funding larger projects (typically at least several hundreds of

thousands of dollars). The specific time window for applying under these solicitations, as

well as the uncertainty of receiving an award, may also provide greater uncertainty for

project investors and applicants.

Competitive Solicitation for Federal Cost-Sharing – This is similar to above, but with a

specific emphasis on applications that can demonstrate federal cost-sharing

opportunities. This solicitation can provide an additional economic benefit to the

ARFVTP portfolio by encouraging federal investment within the state; however, it is also

more difficult to coordinate and plan, as federal solicitations come and go throughout

the year.

First-Come, First-Served – This type of funding mechanism has been used primarily for

vehicle incentives by both the Energy Commission ARFVTP and the ARB Air Quality

Improvement Program. Once eligibility requirements are established, the funding can be

administered relatively quickly and can provide greater market certainty for a project

type. Without a method for evaluating the funding need for each project, however, these

incentives may fund activities that would have already occurred without public

investment. The first applicants in line for funding are likely to be those who are already

the most interested in the activity.

Production or Operation Incentives – To date, the Energy Commission has used these

types of incentives for both in-state ethanol production and hydrogen refueling station

operation and maintenance. The primary aim of these incentives is to provide greater

market certainty, which allows for further outside investment. This funding typically

requires commercial operation and would be poorly suited for projects focused more on

technological research, development, or demonstration. It is also important that the

ARFVTP seek options that limit such support to finite amounts of time or funding and

avoid providing a perpetual subsidy without encouraging market expansion.

Loan Loss Reserve/Loan Guarantees – Being tested by the ARFVTP, these financing

types may increase the opportunity to leverage private financing and transition

alternative fuel and vehicle investments from public to private sources. These funding

mechanisms become more appropriate as technologies and markets mature and are

being considered for the biofuel production and electric vehicle charging categories.

In general, the most important factor in considering the appropriate funding mechanism for an

activity has been the technological and market maturity of the fuel or technology. Public

subsidies, most commonly in the form of grants, are vital to advance early stage technologies

since private financiers are often unwilling to accept the high risks associated with these

15

projects. As a technology or market matures, however, alternative financing mechanisms

become a more effective method of support and can better leverage public funds with private

financing. The Energy Commission will continue to explore alternative financing strategies for

the ARFVTP, such as loans, loan loss reserves, loan guarantees, and property assessment

financing, as appropriate.

The Energy Commission is funding a $2 million pilot financing program with the California

Pollution Control Authority to administer a loan loss reserve for electric vehicle charging station

loans. A loan loss reserve provides funds to cover losses on defaulted or nonpaying loans,

thereby reducing risk to lenders. This financing program will use ARFVTP funds to motivate

lenders to finance the acquisition and installation of electric vehicle charging stations by eligible

small businesses in California. The initial $2 million investment is expected to leverage up to

$10 million in private sector loans. This leveraged fund ratio is significantly higher than what is

typical for a grant program.

Program Outreach and Inclusion

The Energy Commission is committed to ensuring that a diverse range of applicants have the

opportunity to participate in ARFVTP projects, including small businesses, women, minorities,

and disabled veterans, and is similarly committed to increasing their ARFVTP participation rates.

During legislative testimony and at other public forums, Commissioner Janea Scott has

reiterated her commitment of targeted outreach to these communities to ensure a broad and

diverse range of applicants in the ARFVTP. The Energy Commission also seeks to increase the

participation of disadvantaged and underrepresented communities from a diverse range of

geographical regions while implementing the ARFVTP. This includes:

Initiating and implementing an outreach plan to ensure that a diverse range of potential

applicants know about, and understand how to participate in, ARFVTP activities,

especially solicitations for projects.

Targeting particular geographic regions within the state for certain program activities

(for example, job training or workforce planning in economically depressed

communities).

Including initiatives addressing transportation energy-related challenges and

opportunities in economically depressed communities.

Reaching out to women, minority, and disabled veteran groups, sharing information from

the ARFVTP Web page and encouraging their presence and participation in ARFVTP

workshops. These groups included:

o All 35 local air districts.

o Legislative staff, to share with their constituents.

o The African American, Hispanic, and Asian chambers of commerce in California.

o The Association of Women in Water, Energy, and Environment.

o California Association of Black Lawyers.

16

o California Minority Counsel Program staff.

o Hispanic Bar Association of Orange County.

o National Association of Black Accountants.

o National Society of Black Engineers.

o Southern California Chapter of American Association of Blacks in Energy.

Hosting five public outreach workshops around the state (Sacramento, Fresno, Oakland,

Los Angeles, and San Bernardino) in October 2014, explaining the ARFVTP application

process and highlighting Energy Commission commitment to diversity in the ARFVTP.

Distributing ARFVTP information at key expositions and conferences throughout the

state.

Developing and posting online “Grant Funding Opportunities 101,” a presentation on how to apply for ARFVTP funding.12

Hosting a breakout session during the February 2016 Empower California workshop to

increase participation of diverse business enterprises in the ARFVTP.

In addition to the above actions, the Energy Commission has also provided a scoring preference

for projects located in or benefitting disadvantaged communities, as defined by the

CalEnviroScreen 2.0 tool available online from the California Office of Environmental Health Hazard Assessment.13 These preferences were used in recent solicitations, including:

Advanced Vehicle Technology Manufacturing (PON-14-604).

Medium- and Heavy-Duty Advanced Vehicle Technology Demonstration (PON-14-605).

Centers for Alternative Fuels and Advanced Vehicle Technology in Central California

(PON-14-606).

Natural Gas Fueling Infrastructure (PON-14-608).

The Energy Commission plans to continue and enhance existing efforts and implement new

activities to ensure that participation in the ARFVTP reflects the rich and diverse characteristics

of California and its people. These plans include, but are not limited to:

Targeting particular geographic regions within California for a variety of program

activities that will further Energy Commission outreach efforts, especially in Southern

California and the Central Valley.

12 California Energy Commission. Grant Funding Opportunities 101: Alternative and Renewable Fuels and Vehicle Technology Program. October 2014. Available at http://www.energy.ca.gov/altfuels/notices/2014-10_workshops/ARFVTP_Solicitation_Grant_Tutorial.pdf.

13 Office of Environmental Health Hazard Assessment. CalEnviroScreen 2.0. October 2014. Available at http://oehha.ca.gov/ej/ces2.html.

17

Continuing to meet with small businesses, veteran, women, minority, and other

interested groups to provide informational materials on partnering for success through

the ARFVTP. The materials will also be available on the Energy Commission website.

Continuing to hold preapplication and prebid workshops to explain requirements for

grant and contract funding opportunities, answer questions, and encourage networking

and partnering among potential applicants.

Program Metrics

State statutes provide directives and preferences that are used as metrics to measure and

evaluate the benefits of the ARFVTP. These metrics include petroleum and GHG emission

reductions, market transformation, technology advancement, sustainability, air quality benefits,

economic development, and benefit-cost assessments. Of these metrics, measuring the near- and

long-term reductions in petroleum fuel use and GHG emissions from the transportation sector is

of primary importance for evaluating the effectiveness of the ARFVTP.

The ARFVTP considers these metrics when evaluating potential projects for funding by using a

series of weighted scoring factors. The extent to which these scoring factors are applied to each

solicitation varies, depending on the characteristics of each technology area. Given the ARFVTP

legislative requirement not to adopt any one preferred fuel or technology for the program, the

metrics cannot be applied equally to all project types. To do so could lead to a preference for

certain fuels or technologies while neglecting other project types that provide different but

important benefits.

The Energy Commission has investigated how best to apply metrics to the selection of projects

and for the evaluation of the program. In June 2014, the Energy Commission hosted a public

workshop to discuss the use of metrics in the ARFVTP, the findings of which are discussed in

Chapter 4 of the 2014 Integrated Energy Policy Report Update and are integrated into subsequent ARFVTP solicitations.14 In addition, contracts with the National Renewable Energy

Laboratory (NREL) and the RAND Corporation have been developed to analyze and assess the

benefits attributable to the ARFVTP. The NREL contract is discussed in greater detail in the

ARFVTP Benefits and Evaluation section of this chapter.

Summary of Program Funding Through December 2015, the Energy Commission has issued or proposed roughly $606 million

in ARFVTP funding across 545 agreements. A summary of these agreements by fuel type is

provided in Table 2, and these agreements are further summarized by project type in Table 3.

The agreements support a broad portfolio of fuel types, supply chain phases, and

commercialization phases. In most cases, projects are still in progress: production facilities are

14 California Energy Commission. 2015. 2014 Integrated Energy Policy Report Update. Publication Number: CEC-100-2014-001-CMF. Available at http://energy.ca.gov/2014publications/CEC-100-2014-001/CEC-100-2014-001-CMF.pdf.

18

still being sited and constructed, infrastructure is still being installed, and vehicles are still being

demonstrated or deployed. Major highlights of the ARFVTP funding portfolio to date include:

50 projects to promote the production of sustainable, low-carbon biofuels within

California. Most will use waste-based feedstocks, which have some of the lowest carbon-

intensity pathways recognized under the Low-Carbon Fuel Standard. Furthermore, 19 of

these projects are commercial-scale operations that will expand in-state biofuel

production capacity by a combined 88 million diesel-equivalent gallons per year.

7,490 installed and planned charging stations for plug-in electric vehicles, including

4,176 residential charging stations, 3,194 commercial and workplace charging stations,

and 120 direct current (DC) fast chargers.

49 new or upgraded hydrogen refueling stations that will help serve a nascent population

of fuel cell electric vehicles, plus the development of retail fueling standards to enable

hydrogen sales on a per-kilogram basis. Once built, these stations will represent nearly

half of the initial network of 100 hydrogen refueling stations called for by Assembly Bill 8.

44 projects to demonstrate zero- and near-zero-emission advanced technologies and

alternative fuels in a variety of medium- and heavy-duty vehicle applications.

2,809 natural gas vehicles now or soon to be in operation in a variety of applications.

65 natural gas fueling stations to support a growing population of natural gas vehicles.

These include at least six stations that will incorporate low-carbon biomethane into

some, if not all, of the dispensed fuel.

$49.1 million to fund nearly 21,000 incentives for all-electric and plug-in hybrid electric

vehicles via the Air Resources Board Clean Vehicle Rebate Project (CVRP), accounting for

more than one out of every six rebates issued or reserved through the end of FY 2014-

2015.

22 manufacturing projects that will support in-state economic growth while reducing the

supply-side barriers for alternative fuels and advanced technology vehicles, primarily in

electric drive-related components and vehicles.

Workforce training for 14,762 trainees and more than 240 businesses that will translate

clean technology investments into sustained employment opportunities.

Five Centers for Alternative Fuels and Advanced Vehicle Technologies, located

throughout the state, which are dedicated to expanding the role of alternative fuels and

advanced vehicle technologies in California.

34 alternative fuels readiness planning and implementation grants to help regions plan

for vehicle deployment, new fueling infrastructure, and permit streamlining. These

grants include 25 electric vehicle readiness plans, five hydrogen readiness plans, and six

multifuel readiness plans.

The ARFVTP has funded projects throughout California. About 20 percent of funds have been

awarded to projects in the Central Valley, 21 percent in Northern California, 35 percent in

Southern California, and 24 percent with a statewide focus. The details associated with each

project type are discussed further in respective sections of this investment plan update. In

19

addition, Table 4 outlines the funding allocations of the two most recent investment plan

updates, in comparison to the funding allocations for FY 2016-2017.

Table 2: ARFVTP Awards by Fuel Type as of December 31, 2015

Fuel Type Cumulative Awards

to Date (in millions)

Cumulative Number of Projects to Date

Biomethane $50.9 16

Ethanol $43.6 19

Biodiesel $49.3 19

Renewable Diesel $12.1 5

Electricity $199.2 153

Hydrogen $113.0 72

Natural Gas $88.9 154

Propane $6.0 31

Multiple/Other* $43.0 76

Total $606.0 545

Source: California Energy Commission. *Some agreements, such as those for multifuel regional readiness plans or workforce training, cannot be readily categorized by fuel type.

20

Table 3: Previous ARFVTP Awards as of December 31, 2015

Category Funded Activity Cumulative

Awards to Date(in millions)*

# of Projects or Units

Alternative Fuel Production

Biomethane Production $50.9 16 Projects

Gasoline Substitutes Production $27.2 14 Projects

Diesel Substitutes Production $57.4 20 Projects

Alternative Fuel Infrastructure

Electric Vehicle Charging Infrastructure $40.7 7,490 Charging Stations

Hydrogen Refueling Infrastructure $96.0 49 Fueling Stations

E85 Fueling Infrastructure $13.7 158 Fueling Stations

Upstream Biodiesel Infrastructure $4.0 4 Infrastructure Sites

Natural Gas Fueling Infrastructure $21.0 65 Fueling Stations

Alternative Fuel and Advanced Technology Vehicles

Natural Gas Vehicle Deployment** $56.4 2,809 Vehicles

Propane Vehicle Deployment** $6.0 514 Trucks

Light-Duty Electric Vehicle Deployment $25.1 10,700 Cars

Medium- and Heavy-Duty Electric Vehicle Deployment $4.0 150 Trucks

Medium- and Heavy-Duty Vehicle Technology Demonstration and Scale-Up

$93.7 44 Demonstrations

Related Needs and Opportunities

Manufacturing $57.0 22 Manufacturing Projects

Emerging Opportunities † †

Workforce Training and Development $27.7 83 Recipients

Fuel Standards and Equipment Certification $3.9 1 Project

Sustainability Studies $2.1 2 Projects

Regional Alternative Fuel Readiness and Planning $7.6 34 Regional Plans

Centers for Alternative Fuels $5.8 5 Centers

Technical Assistance and Program Evaluation $5.6 n/a

Total $606.0

Source: California Energy Commission. *Includes all agreements that have been approved at an Energy Commission business meeting, or are expected for business meeting approval following a notice of proposed award. For canceled and completed projects, includes only funding received from ARFVTP, which may be smaller than initial award. **Funding includes both completed and pending vehicle incentives, as well as encumbered funds for future incentives. †Previous awards have been reclassified by project type into other rows.

21

Table 4: Most Recent and Current Investment Plan Allocations (in millions)

Category Funded Activity 2014-2015 2015-2016 2016-2017

Alternative Fuel Production

Biofuel Production and Supply $20 $20 $20

Alternative Fuel Infrastructure

Electric Charging Infrastructure $15 $17 $17

Hydrogen Refueling Infrastructure $20 $20 $20

Natural Gas Fueling Infrastructure $1.5 $5 $2.5

Alternative Fuel and Advanced Technology Vehicles

Natural Gas Vehicle Incentives $10 $10 $10

Light-Duty Electric Vehicle Deployment $5 - -

Medium- and Heavy-Duty Vehicle Technology Demonstration and Scale-Up

$15 $20* $23*

Related Needs and Opportunities

Manufacturing $5

Emerging Opportunities $6 $3 $3

Workforce Training and Development Agreements $2.5 $3 $2.5

Regional Alternative Fuel Readiness and Planning - $2 $2

Total $100 $100 $100

Source: California Energy Commission. *See the text of these respective sections in Chapters 5 and 6 for details on the combination of these funding allocations.

22

ARFVTP Benefits and Evaluation The Energy Commission periodically reviews and evaluates its implementation of the ARFVTP to

improve program efficiency, identify future funding needs, and select higher-quality projects.

Much of this can be done in-house by reviewing previous investment plans, reviewing funding

solicitations, comparing past awards, visiting sites, surveying ARFVTP grantees, and performing

other program analyses.

Benefit-Cost Assessments AB 8 introduced the GHG benefit-cost score as a new element into the list of policy and scoring

preferences for ARFVTP. It is defined as “…a project’s expected or potential greenhouse gas emissions reduction per dollar awarded by the Commission to the project.”15 AB 8 also directs

the Energy Commission to “give additional preference to funding those projects with higher benefit-cost scores.”16 The benefit-cost provision preference is applied when evaluating

proposals for similar types of projects during funding solicitations.

Cost-benefit measurements and scoring are incorporated into the development of solicitations

and the review of proposals for the ARFVTP. The “benefit” is calculated as the amount of

conventional fuel displaced per year by the resulting alternative fuel or technology, multiplied by the carbon intensity of that fuel or technology relative to conventional fuel.17 This results in

an estimate of direct GHG reduction benefits from a proposed project. The “cost” is based on

the requested ARFVTP funding amount. Dividing the “benefit” by the “cost” produces a benefit-

cost ratio that staff uses in ranking similar proposals within a competitive solicitation.

The benefit-cost ratio is one of several project selection criteria established in statute and is

accordingly just one of several criteria used to evaluate project applications. The benefit-cost

ratio is given greater scoring weight in solicitations that focus on technologically mature and

commercially established project types. Conversely, the benefit-cost ratio is given smaller

weighting in solicitations that focus on precommercial or evolving technologies. In recent

solicitations, this preference has also been incorporated both as part of the general scoring

criteria and as a potential tie-breaker in the event of proposals receiving equal scores.

National Renewable Energy Laboratory Program Benefits Guidance Report

The Energy Commission has also worked with the NREL to develop an approach for quantifying

the petroleum displacement, GHG reduction, and air quality benefits of projects funded by the

ARFVTP, which is required by Assembly Bill 109 (Núñez, Chapter 313, Statutes of 2008). In June

2014, NREL issued a Program Benefits Guidance draft report that describes its method for

15 California Health and Safety Code, Sec. 44270.3(a).

16 California Health and Safety Code, Sec. 44272(d).

17 Carbon intensity is defined here as the amount of carbon dioxide equivalent greenhouse gasses by weight emitted per unit of energy consumed.

23

categorizing and assessing a series of benefit categories. 18 The methods and results of this

report are discussed in the 2014 Integrated Energy Policy Report Update. For 2015, NREL

analyzed updated ARFVTP project data for 262 projects totaling $552 million, representing the

ARFVTP project portfolio technical projects as of June 30, 2015. In reviewing ARFVTP benefits,

NREL identified four relevant categories, as summarized in Table 5. These categories range from

benefits with relatively high levels of certainty about past trends and near-term projects to

benefits with high levels of uncertainty regarding technological innovation and market

transformation. The first category, Baseline Benefits, is a conceptual category that represents

GHG reductions without ARFVTP projects. Since its report focused on benefits associated with

ARFVTP, NREL focused on other categories within the report.

Table 5: Benefit Categories in NREL Program Benefits Guidance

Benefits Category Description

Baseline Benefits Expected to accrue without support from ARFVTP.

Expected Benefits Directly associated with vehicles and fuels deployed by projects receiving ARFVTP funds.

Market Transformation Benefits

Accrued due to influence of ARFVTP projects on future market conditions to accelerate the adoption of new technologies.

Required Carbon Market Growth Benefits

Projections of future market growth trends comparable to those needed for deep GHG reductions by 2050.

Source: California Energy Commission, based on categories developed by NREL.

The second category, Expected Benefits, is defined as the benefits most likely to occur from

ARFVTP projects being executed successfully, assuming a one-to-one substitution of existing

fuel or technology with a new fuel or technology. Figure 2 summarizes the estimated GHG

emission reductions from the Expected Benefits category through 2025.

18 Melaina, Marc, Ethan Warner, Yongling Sun, Emily Newes, and Adam Ragatz (National Renewable Energy Laboratory). 2014. Program Benefits Guidance: Analysis of Benefits Associated With Projects and Technologies Supported by the Alternative and Renewable Fuel and Vehicle Technology Program. CEC-600-2014-005-D. Available at http://www.energy.ca.gov/2014publications/CEC-600-2014-005/CEC-600-2014-005-D.pdf.

24

Figure 2: Summary of GHG Emissions Reductions From the Expected Benefits of 223 Projects Through 2025

Source: NREL.

25

The third category of benefits considered by NREL, Market Transformation Benefits,

corresponds to the core mission of ARFVTP to transform the California transportation

system into a low-carbon, low-emission system of alternative fuel and vehicle

technologies. Market transformation benefits are tangible but more challenging to

quantify because they are assessments of how ARFVTP-funded projects will contribute

to reducing the barriers of future alternative fuel and technology deployments. Because

of the greater uncertainty from this type of benefit, NREL incorporated a low and high

range.

Table 6: Summary of GHG Emission and Petroleum Fuel Reduction Benefits Based on 262 Projects

Category Project

Class/Range

GHG Reductions (thousand tonnes CO2e)

Petroleum Reductions

(million gallons)

2015 2020 2025 2015 2020 2025

Expected Benefits

Fueling Infrastructure 79.9 518.8 529.2 18.7 96.6 98.4

Vehicles 106.9 605.0 1,119.3 25.1 81.3 141.9

Fuel Production 39.2 589.8 782.5 3.5 55.0 73.2

TOTAL 226.0 1,713.7 2,431.0 47.4 232.8 313.5

Market Transformation

Benefits

Low Case 214.8 378.1 802.6 24.8 48.7 93.6

High Case 483.9 2,038.3 3,184.0 65.3 245.2 364.6

Required Carbon Market Growth

Low Case - 2,333 6,375 - 237.2 957.3

High Case - 6,397 15,189 - 665.4 1,959

Source: NREL.

The estimates for Expected Benefits and Market Transformation Benefits are

summarized in Table 6. Expected Benefits for all project classes by 2025 total about

2.43 million metric tons of carbon dioxide equivalent (MMTCO2e). The range of Market

Transformation Benefits by 2025 range from 802,600 metric tons CO2e in the Low Case

to 3.18 MMTCO2e in the High Case. Combining this range of benefits with the Expected

Benefits category yields a GHG reduction range of 3.2 MMTCO2e to 5.6 MMTCO

2e by

2025. Cumulative petroleum reductions for Expected and Market Transformation

Benefits range from 407.1 million to 678.1 million gallons by 2025.

These categories can be compared against the fourth category, Required Market Growth

Benefits. This category represents an approximate trajectory for how California will

need to reduce GHG emissions to meet its 2050 goal. Total Expected Benefits and

Market Transformation Benefits represent a significant contribution to overall efforts to

reduce transportation-related GHG emissions; more than half of the roughly 7 MMTCO2e

needed in the 2020 to 2025 time frame is indicated by Figure 3. Another comparative

26

reference is that the high case GHG reduction estimate of 5.6 MMTCO2e would represent

one-third of the 15 MMTCO2e in transportation GHG emissions reductions projected for

the Low Carbon Fuel Standard program in 2020.19 The comparisons are shown in Figure

3, which depicts steady progress along this trajectory but with a clear need for future

investments as well.

Figure 3: GHG Reductions From Expected and Market Transformation Benefits in Comparison to Required Market Growth Benefits

Source: NREL.

Related Policies and Programs

Air Quality Improvement Program/Low Carbon Transportation Program

In addition to the ARFVTP, AB 118 also created the Air Quality Improvement Program

(AQIP), to be administered by the ARB. While the ARFVTP focuses primarily on achieving

state GHG reduction goals within the transportation sector, the AQIP is primarily

responsible for reducing air pollutants from the transportation sector. The two

19 California Air Resources Board. 2014 LCFS Advisory Panel. May 19, 2014. Available at http://www.arb.ca.gov/fuels/lcfs/workgroups/advisorypanel/051914advisorypanelpresentation.pdf.

27

programs have worked in concert to maximize the benefits to the state and avoid

duplication of efforts. For instance, the ARFVTP has invested in light-duty electric

vehicle charging infrastructure, regional planning, and manufacturing projects, while

the AQIP has provided deployment incentives for light-duty electric vehicles through the

CVRP. Similarly, the Energy Commission has supported the demonstration of early

hybrid and electric truck and bus models, while the AQIP has provided deployment

incentives for such vehicles through the Hybrid and Zero-Emission Truck and Bus

Voucher Incentive Project (HVIP) and other planned larger-scale pilot deployment

projects. Finally, AQIP has also provided loans to assist fleets in modernizing their

diesel trucks.

Prior to the availability of greenhouse gas reduction funds, the ARFVTP provided $49.1

million in funding to backfill CVRP needs, as well as an additional $4 million in HVIP

incentives. Beginning with FY 2014-2015, ARB combined the AQIP and the Low-Carbon

Transportation Investments into one funding plan, as discussed in the AB

32/Greenhouse Gas Reduction Fund section below. The joint funding plan is meant to

ensure synergistic investments between the two programs.

AB 32/Greenhouse Gas Reduction Fund

Assembly Bill 32 (Núñez, Chapter 488, Statutes of 2006), also known as the Global

Warming Solutions Act of 2006, required the ARB to adopt a statewide GHG emission

limit for 2020 equivalent to the statewide GHG emission levels in 1990. Executive Order

S-3-05 also set an objective of reducing emissions to 80 percent below 1990 levels by

2050, which is consistent with an Intergovernmental Panel on Climate Change analysis

of the emissions trajectory that would stabilize atmospheric GHG concentrations at

450 parts per million CO2e and reduce the danger of catastrophic climate change. In

addition, Executive Order B-30-15 set an interim goal to reduce statewide GHG

emissions to 40 percent below 1990 levels by 2030, to ensure California meets the

targets of Executive Order S-3-05.

As part of its regulation, the ARB developed a cap-and-trade program that set a limit on

the amount of permissible GHG emissions from regulated sectors. Covered entities must

then pay an allowance price for their GHG emissions from those sectors. Revenue from

these payments goes into the Greenhouse Gas Reduction Fund (GGRF) and is

appropriated by the Legislature each year in the annual budget act.

The ARB allocated a combined $118 million in its AQIP and Low Carbon Transportation

investments funding plan, as amended in October 2015. Table 7 summarizes this funding plan.20,21

20 California Air Resources Board. Proposed Fiscal Year 2015-16 Funding Plan for Low Carbon Transportation Investments and the Air Quality Improvement Program. May 21, 2015. Available at http://www.arb.ca.gov/msprog/aqip/fundplan/proposed_fy15-16_funding_plan.pdf.

28

Table 7: FY 2015-2016 AQIP and Low Carbon Transportation GGRF Allocations

Project Category AQIP Funding for FY 15-16 (in millions)

GGRF Funding for FY 15-16 (in millions)

Light-Duty Vehicle Projects

Clean Vehicle Rebate Project $3 $75

Light-Duty Pilot Projects to Benefit Disadvantaged Communities

- $10

Heavy-Duty Vehicle and Equipment Projects

Hybrid and Zero-Emission Truck and Bus Voucher Incentive Project

$2 $5

Low NOx Truck Incentives $2 -

Truck Loan Assistance Program $15 -

Reserve for Revenue Uncertainty $1 -

State Operations for Low Carbon Transportation - $5

Total $23 $95

Source: California Air Resources Board.

The first three project categories listed in Table 7 have particular importance to the

goals and strategies of the ARFVTP and are further discussed in the Light-Duty Electric

Vehicle subsection and Medium- and Heavy-Duty Vehicle Technology Demonstration

and Scale-Up subsection of this investment plan update.

Low-Carbon Fuel Standard The ARB adopted the Low-Carbon Fuel Standard (LCFS) regulation in April 2009, with a goal of reducing the overall carbon intensity of fuel within the transportation sector by 10 percent by 2020. Since then, regulated parties have had to slowly reduce the carbon intensity of their fuel.

A “credit” under the LCFS is equivalent to the reduction of 1 metric ton of CO2e, roughly

equivalent to the amount of CO2e released from the combustion of 90 gallons of