2015_01_09_SAN_Short term pain to restore sustainability

40

Unauthorized redistribution of this report is prohibited. This report is intended for [email protected] from [email protected] IMPORTANT DISCLOSURE FOR U.S. INVESTORS: This document is prepared by Mediobanca Securities, the equity research department of Mediobanca S.p.A. (parent company of Mediobanca Securities USA LLC (“MBUSA”)) and it is distributed in the United States by MBUSA which accepts responsibility for its content. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. Any US person receiving this document and wishing to effect transactions in any securities discussed herein should do so with MBUSA, not Mediobanca S.p.A.. Please refer to the last pages of this document for important disclaimers. Santander 09 January 2015 Banks Update Short term pain to restore sustainability Andrea Filtri Equity Analyst €7.5bn ABB to address CET1 issues and normalize the dividend anomaly Yesterday, SAN announced €7.5bn accelerated bookbuild and the return to 3/4 2015 dividends in cash and 30-40% cash payout thereafter for 2% yield in 2015 and c.3% onwards. Lower than expected fully loaded 2014 CET1 (8.3%) implies SAN hitting 10% in 2015 and closing the gap with EU peers. Underperformance in the short term is the price to pay to correct the distortions from the €60c scrip DPS commitment and gain future flexibility, in our view. Our note excludes the ABB impact and analyses the impact from in-market M&A. ABB to fix a standalone issue, not to satisfy M&A ambitions The ABB reflects a strategic U-turn implemented by the new SAN management. In this note we analyze why SAN had to review its capital strategy and conclude that in-market M&A offers scope for accretion to address revenue pressure while allowing for geographical capital redeployment. The market is already speculating on the M&A use of the new capital, but our estimates show today‟s ABB merely serves standalone needs calling for more capital action to satisfy any potential external growth ambitions. There was enough to re-assess capital allocation SAN invested the last five years to repair the balance sheet and equip it for the new regulatory environment. The introduction of the scrip dividend raised €15bn new capital and boosted CET1 and share count by 30% and 40%, respectively. Yet, capital ratios remained well below peers. Meanwhile, we estimate SAN‟s exposure to GDP growth is down by 1/3 vs pre-crisis and cost of equity (COE) is essentially flat. Global/Local regulation remain potential issues but the implementation of Banking Union could be good news for EU operations. This justified a re-assessment of capital allocation as confirmed by the ABB. In-market M&A is on the cards: Bankia is a very good fit We benchmark the SAN-BKIA combination to the other European national champions and find that the Spanish mammoth would not differ, discharging worries of antitrust. We assess the potential synergies and identify cost, funding and capital synergies. We estimate €0.6bn cost cuts, €145m funding cost savings and €3bn writeback from BKIA‟s written off DTA. We model three potential operations assuming 15% premium to BKIA‟s market price: 1) a full share-for- share offer, 2) a cash bid complemented by €10bn rights issue, 3) a cash bid funded by the sale of Brazil. The deal would result in double digit 3-yr ROI, 4- 17% accretion to 3-yr EPS with neutral to positive (+110bp) impact to capital ratios. The latter option prevails in the comparison as it would not only provide the highest EPS accretion, but would also boost resolve the capital stretch – fully reinstating cash dividends - and could be one of the possible answers to the question of geographical capital reallocation. 7-26% upside to Target Price – Brazilian sale prevailing on other alternatives We estimate the three SAN-BKIA combinations would have a positive impact to valuation of 7-26% to our €7.6 SAN TP. The sale of Brazil offers the highest upside from: a) 50bp contraction of COE to 8.2%, b) over €7bn reduction in capital shortfall, c) €9.5bn NPV of synergies. The other alternatives fair the same on COE (8.5%), CET1 ratio (9.7-9.8%) and economic capital requirement (10.8% of RWAs), but the cash bid + €10bn rights issue provides double the accretion (14% vs 7%) as the higher SAN rating implies lower share count dilution. +44 203 0369 571 [email protected] Andres Williams Equity Analyst +44 203 0369 577 [email protected] Source: Mediobanca Securities Price: € 6.86 Target price: € 7.60 Neutral 2013 2014E 2015E 2016E EPS Adj (€) 0.42 0.50 0.55 0.58 DPS (€) 0.60 0.60 0.60 0.60 TBVPS (€) 5.02 4.66 4.77 4.89 Avg. RoTE Adj (%) 6.9% 8.9% 10.0% 10.3% P/E Adj (x) 16.4 13.7 12.4 11.8 Div.Yield(%) 8.8% 8.8% 8.8% 8.8% P/TBV (x) 1.4 1.5 1.4 1.4 Market Data Market Cap (€m) Shares Out (m) (%) Free Float (%) 100% 52 week range (€) 7.90-6.22 Rel Perf vs STOXX EUROPE 600 (%) -1m -4.3% -3m -9.0% -12m -2.6% 21dd Avg. Vol. 106,126,161 Reuters/Bloomberg SAN.MC / SAN SM

-

Upload

andrea-filtri -

Category

Documents

-

view

28 -

download

0

Transcript of 2015_01_09_SAN_Short term pain to restore sustainability

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

IMPORTANT DISCLOSURE FOR U.S. INVESTORS: This document is prepared by Mediobanca Securities, the equity research department of Mediobanca S.p.A. (parent company of Mediobanca Securities USA LLC (“MBUSA”)) and it is distributed in the United States by MBUSA which accepts responsibility for its content. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. Any US person receiving this document and wishing to effect transactions in any securities discussed herein should do so with MBUSA, not Mediobanca S.p.A.. Please refer to the last pages of this document for important disclaimers.

Santander

09 January 2015 Banks Update

Short term pain to restore sustainability Andrea Filtri

Equity Analyst

€7.5bn ABB to address CET1 issues and normalize the dividend anomaly

Yesterday, SAN announced €7.5bn accelerated bookbuild and the return to 3/4

2015 dividends in cash and 30-40% cash payout thereafter for 2% yield in 2015

and c.3% onwards. Lower than expected fully loaded 2014 CET1 (8.3%) implies

SAN hitting 10% in 2015 and closing the gap with EU peers. Underperformance in

the short term is the price to pay to correct the distortions from the €60c scrip

DPS commitment and gain future flexibility, in our view. Our note excludes the

ABB impact and analyses the impact from in-market M&A.

ABB to fix a standalone issue, not to satisfy M&A ambitions

The ABB reflects a strategic U-turn implemented by the new SAN management.

In this note we analyze why SAN had to review its capital strategy and conclude

that in-market M&A offers scope for accretion to address revenue pressure while

allowing for geographical capital redeployment. The market is already

speculating on the M&A use of the new capital, but our estimates show today‟s

ABB merely serves standalone needs calling for more capital action to satisfy any

potential external growth ambitions.

There was enough to re-assess capital allocation

SAN invested the last five years to repair the balance sheet and equip it for the

new regulatory environment. The introduction of the scrip dividend raised €15bn

new capital and boosted CET1 and share count by 30% and 40%, respectively.

Yet, capital ratios remained well below peers. Meanwhile, we estimate SAN‟s

exposure to GDP growth is down by 1/3 vs pre-crisis and cost of equity (COE) is

essentially flat. Global/Local regulation remain potential issues but the

implementation of Banking Union could be good news for EU operations. This

justified a re-assessment of capital allocation as confirmed by the ABB.

In-market M&A is on the cards: Bankia is a very good fit

We benchmark the SAN-BKIA combination to the other European national

champions and find that the Spanish mammoth would not differ, discharging

worries of antitrust. We assess the potential synergies and identify cost, funding

and capital synergies. We estimate €0.6bn cost cuts, €145m funding cost savings

and €3bn writeback from BKIA‟s written off DTA. We model three potential

operations assuming 15% premium to BKIA‟s market price: 1) a full share-for-

share offer, 2) a cash bid complemented by €10bn rights issue, 3) a cash bid

funded by the sale of Brazil. The deal would result in double digit 3-yr ROI, 4-

17% accretion to 3-yr EPS with neutral to positive (+110bp) impact to capital

ratios. The latter option prevails in the comparison as it would not only provide

the highest EPS accretion, but would also boost resolve the capital stretch – fully

reinstating cash dividends - and could be one of the possible answers to the

question of geographical capital reallocation.

7-26% upside to Target Price – Brazilian sale prevailing on other alternatives

We estimate the three SAN-BKIA combinations would have a positive impact to

valuation of 7-26% to our €7.6 SAN TP. The sale of Brazil offers the highest

upside from: a) 50bp contraction of COE to 8.2%, b) over €7bn reduction in

capital shortfall, c) €9.5bn NPV of synergies. The other alternatives fair the

same on COE (8.5%), CET1 ratio (9.7-9.8%) and economic capital requirement

(10.8% of RWAs), but the cash bid + €10bn rights issue provides double the

accretion (14% vs 7%) as the higher SAN rating implies lower share count dilution.

+44 203 0369 571

Andres Williams

Equity Analyst

+44 203 0369 577

Source: Mediobanca Securities

Price: € 6.86 Target price: € 7.60 Neutral

2013 2014E 2015E 2016E

EPS Adj (€) 0.42 0.50 0.55 0.58

DPS (€) 0.60 0.60 0.60 0.60

TBVPS (€) 5.02 4.66 4.77 4.89

Avg. RoTE Adj (%) 6.9% 8.9% 10.0% 10.3%

P/E Adj (x) 16.4 13.7 12.4 11.8

Div.Yield(%) 8.8% 8.8% 8.8% 8.8%

P/TBV (x) 1.4 1.5 1.4 1.4

Market Data

Market Cap (€m)

Shares Out (m)

(%)

Free Float (%) 100%

52 week range (€) 7.90-6.22

Rel Perf vs STOXX EUROPE 600 (%)

-1m -4.3%

-3m -9.0%

-12m -2.6%

21dd Avg. Vol. 106,126,161

Reuters/Bloomberg SAN.MC / SAN SM

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 2

Price: € 6.86 Target price: € 7.60 Neutral

Valuation Matrix

Source: Mediobanca Securities

Source: Mediobanca Securities

Profit & Loss Acc(€ m) 2013 2014E 2015E 2016E Multiples 2013 2014E 2015E 2016E

Net Interest Income 28,419 29,522 30,837 32,531 P/E 17.0 13.3 11.5 11.0

Growth (%) -5.7% 3.9% 4.5% 5.5% P/E Adj. 16.4 13.7 12.4 11.8

Non-Interest Income 13,512 12,949 12,713 13,075 P/Net Op.Income 3.6 3.5 3.7 3.8

Growth (%) -0.1% -4.2% -1.8% 2.8% P/Revenues 1.9 1.8 2.0 2.0

of which Fee Income 9,622 9,609 9,846 10,150 P/TBV 1.4 1.5 1.4 1.4

of which Financial Income 3,496 2,896 2,598 2,617 P/Total Deposits (%) 12.8% 11.3% 12.1% 12.6%

Total Income 41,931 42,471 43,551 45,606 Yield (%) 8.8% 8.8% 8.8% 8.8%

Growth (%) -4.0% 1.3% 2.5% 4.7%

Total Costs -20,158 -19,952 -20,301 -21,083

Growth (%) 0.2% -1.0% 1.7% 3.9%

of which Personnel Costs -10,276 -10,128 -10,352 -10,693

Net Operating Income 21,773 22,518 23,250 24,524

Growth (%) -7.6% 3.4% 3.2% 5.5%

Provisions&Write-downs -12,864 -11,299 -10,718 -10,691 Per Share Data (€) 2013 2014E 2015E 2016E

Extraordinary Items -15 -15 -16 -16 EPS 0.40 0.51 0.60 0.62

Pre-tax profit 7,637 9,594 11,102 12,495 EPS growth (%) 76.0% 27.4% 16.0% 4.3%

Tax -2,075 -2,672 -3,043 -3,409 EPS Adj. 0.42 0.50 0.55 0.58

Tax rate(%) 27.2% 27.8% 27.4% 27.3% EPS Adj. growth (%) -20.2% 19.2% 10.8% 5.4%

Minorities and others -1,177 -1,081 -936 -997 TBVPS 5.02 4.66 4.77 4.89

Net profit 4,370 5,827 7,108 8,073 DPS Ord 0.60 0.60 0.60 0.60

Growth (%) 98.2% 33.3% 22.0% 13.6%

Adjusted net profit 4,370 5,827 7,108 8,073

Growth (%) 98.2% 33.3% 22.0% 13.6%

Balance Sheet (€ m) 2013 2014E 2015E 2016E Key Figures & Ratios 2013 2014E 2015E 2016E

Customer Loans 666,356 725,873 747,704 778,998 Avg. N° of Shares (m) 11,333 11,333 12,508 13,456

Growth(%) -4.3% 8.9% 3.0% 4.2% EoP N° of Shares (m) 11,333 11,333 12,508 13,456

Customer Deposits 607,836 686,598 710,362 734,267 Avg. Market Cap. (m) 65,912 77,702 85,755 92,252

Growth(%) -3.0% 13.0% 3.5% 3.4%

Shareholders' Funds 80,559 86,341 93,174 100,940 NII/Total Income (%) 67.8% 69.5% 70.8% 71.3%

Minorities 9,972 11,053 11,988 12,985 Fees/Total Income (%) 22.9% 22.6% 22.6% 22.3%

Total Assets 1,134,014 1,226,515 1,261,052 1,296,735 Trading/Total Income (%) 8.3% 6.8% 6.0% 5.7%

Cost Income ratio 48.1% 47.0% 46.6% 46.2%

Personnel costs/Total costs 51.0% 50.8% 51.0% 50.7%

Impairment/Average Loans 1.9% 1.6% 1.5% 1.4%

NPLs ratio 4.7% 4.3% 4.2% 4.1%

Provisions/Loans 1.3% 1.4% 1.4% 1.2%

Avg. RoTE Adj. (%) 6.9% 8.9% 10.0% 10.3%

ROA (%) 0.36% 0.46% 0.54% 0.60%

Tier 1 ratio 12.6% 12.2% 13.0% 13.7%

Basel III Core Tier 1 ratio 9.2% 9.0% 9.9% 10.8%

6.20

6.40

6.60

6.80

7.00

7.20

7.40

7.60

7.80

8.00

J F M A M J J A S O N D J

Santander STOXX EUROPE 600

8/01/15

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 3

Price: € 6.86 Target price: € 7.60 Neutral

Table of Contents

Executive Summary 4

€7.5bn capital increase: normalising the story 9

Cost-cutting consolidation to fight revenue attrition 11

SAN yet to cash in from domestic consolidation 15

Rethinking capital allocation 17

SAN-BKIA: cost, funding and capital synergies 23

7-26% TP upside potential from the transformation 32

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 4

Price: € 6.86 Target price: € 7.60 Neutral

Executive Summary This note analyses the reasons why SAN had to review its capital strategy and follows with the

potential simulation of a SAN-BKIA combination as a potential way to address revenue pressure

and geographical capital redeployment. Yesterday’s €7.5bn ABB announcement by the company

supports our analysis and confirms the new management is empowered to implement its

strategy even if this is in sharp contrast to the one implemented thus far by the bank. The

market already started to speculate about the potential use of the new funds. To us the ABB

simply addresses SAN’s own issues and does not automatically steamroll them into an M&A

scenario which could potentially require further resources. We believe any M&A option would

be mainly driven by considerations over the potential benefits from cost synergies, supporting

our favor for in-market combinations. Our note and SAN-BKIA simulations exclude the impact of

the ABB.

€7.5bn ABB announced yesterday fixing capital stretch and normalising SAN’s DPS

Yesterday SAN announced €7.5bn accelerated bookbuild (ABB) and a 2015 dividend policy returning

to three cash dividends and one scrip dividend from the current policy of four scrip dividends. Yet,

each cash dividend is capped at €0.05 per share, implying a material cut to expected payout and

likely upsetting some income-driven investors. The deal should boost CET1 ratio by 140bp, taking

SAN to c.10% Basel III fully loaded ratio in 2015E, largely closing the gap vs peers, but also reflecting

a materially lower than expected 2014 starting point (8.3% vs 8.5-8.6% target provided on Q314

results). We estimate only 2% EPS dilution from the deal as the issuance of c.10% new shares is

largely offset by the future cancellation of the scrip dividends and of the shares which would be

issued under this scheme. This normalizes SAN dividend policy correcting the distortions brought by

the €0.60 scrip DPS commitment (120% payout). The announcement of the ABB is a U-turn in capital

strategy at Santander. We highlight this change reflects the strong grip the newly appointed

management has on the bank. Yet, we see the stock trading at 12.6x 2015E PE and 1.3x P/TE for

11% RoTE post capital increase, confirming our Neutral rating on the stock.

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 5

Price: € 6.86 Target price: € 7.60 Neutral

SAN ABB simulation

2014E 2015E 2016E 2017E

Pre rights issue

Adj. net profit 5,954 7,183 8,148 9,053

Average diluted shares outstanding 11,914 12,962 13,929 14,857

Adj. EPS 0.50 0.55 0.58 0.61

DPS 0.60 0.60 0.60 0.60

Cash DPS payout 19% 17% 16% 51%

Cash DPS yield 1.7% 1.5% 1.4% 4.5%

Adj. P/E 13.7 12.4 11.7 11.3

TBVPS 4.7 4.8 4.9 4.9

P/TBVPS 1.47 1.43 1.40 1.39

ROTE 10.3% 11.7% 12.1% 12.4%

CET1 Basel III fully loaded 8.3% 9.2% 10.2% 10.3%

Post rights issue

Capital raising

7,500 7,500 7,500

New shares in issue @5% discount

1,258 1,258 1,258

Average diluted shares outstanding

13,250 13,250 13,250

Adj. EPS

0.54 0.61 0.68

EPS dilution

-2% 5% 12%

DPS @ 35% payout

0.19 0.22 0.24

Cash DPS payout

79% 100% 100%

Cash DPS yield

2.2% 3.2% 3.5%

Adj. P/E

12.6 11.1 10.0

TBVPS

5.4 5.8 6.2

P/TBVPS

1.3 1.2 1.1

ROTE

10.8% 11.1% 11.4%

CET1 Basel III fully loaded 9.7% 10.6% 11.0% 11.4%

Source: Mediobanca Securities, company data

The collapse in Spanish revenues triggered cost cutting via M&A...

Spanish NII is down 42% from its peak level. Banks have cut costs and staff by 21% and branches by

29% to compensate, mainly through domestic M&A so that 50 banks consolidated into today‟s 12

banking groups. Yet, SAN‟s operating profits are down 37%.

...while banks used short term fixes to support capital ratios...

The DTA to DTC conversion circumvented the limitation to 15% of CET coming from DTA. The move,

which propped capital ratios up in the short term and ahead of the Comprehensive Assessment,

could come under pressure under the new ECB regulatory regime.

...so that more consolidation is likely

Spanish NII is down 42% from its peak level. Banks have cut costs and staff by 21% and branches by

29% to compensate, mainly through domestic M&A so that 50 banks consolidated into today‟s 12

banking groups. Yet, operating profits are down 37%, signaling more consolidation could be due.

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 6

Price: € 6.86 Target price: € 7.60 Neutral

Consolidation cost SAN €1.5bn without any direct benefit...

Santander (SAN) directly spent c.€1.5bn through the FGD and Sareb to subsidize the restructuring of

the Spanish banking sector, implicitly transferring value to its fiercest competitors: BBVA, CABK,

SAB, BKIA. This implies SAN is yet to cash in its „credit‟ towards the system / the state.

…SAN’s structural exposure to GDP growth has been impaired…

We see the SAN‟s post crisis exposure to GDP 1/3 below the pre crisis level (lhs chart below),

mainly coming from a marked slowdown in Latina America (Latam, chart below rhs) , which is now

expected to underperform the rest of SAN‟s geographies.

SAN weighted average GDP YoY growth, %

Source: Mediobanca Securities, company data

SAN LATAM vs rest of the group ex-corporate centre and

R.E. profit growth YoY 2005-16E, %

Source: Mediobanca Securities, company data

…while COE stayed essentially stable…

While growth has slowed down, we see the SAN‟s perspective COE remaining largely flat when

compared to pre crisis levels (see chart below).

SAN COE, %

Source: Mediobanca Securities, Bloomberg

…and the capital stretch and regulatory issues remained pre-ABB

Despite five years of scrip dividend policy, which raised €15bn of new equity for SAN (30% of CET1

capital) and diluted share count by 40%, SAN‟s Basel III fully loaded capital ratio remained well

below EU peers ahead of the announcement of the capital increase. This is even more relevant

when considering SAN‟s GSIFI status and the ongoing process to introduce TLAC regulation. The

European Banking Union implementation is the only potentially positive regulatory development as

this should come with full capital and liquidity fungibility within the Union.

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2104E 2015E 2016E

0%

20%

40%

60%

80%

100% LATAM RoG ex-Corp centre, R.E.

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2104E 2015E

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 7

Price: € 6.86 Target price: € 7.60 Neutral

Basel III fully loaded CET1 ratio H114

Source: Mediobanca Securities, company data

…so that a re-assessment of capital allocation was due

With the progressive stabilization of the regulatory framework, the implementation of the Banking

Union, the slowdown in structural GDP growth exposure of the group, the further consolidation of

the Spanish market and the protracted capital stretch vs peers, we believe a revision of SAN‟s

capital allocation strategy was due and yesterday‟s ABB announcement confirms this.

SAN-BKIA: a combination worth cost, funding and capital synergies

We benchmark the SAN-BKIA combination to the other large national champions around Europe and

find that the Spanish mammoth – reaching c.23-25% market share in loans, deposits and mutual

funds - would not differ from others around the Continent, implying a low risk of antitrust issues, in

our view.

We identify €0.6bn and €145m cost and funding synergies by averaging out three bottom-up and

top-down methodologies, justifying €1.5bn restructuring charges.

SAN-BKIA synergy benchmark

Revenue Costs

Average in-market merger synergies 163 537

Average Spanish merger synergies 51 624

Cost composition 622

Average 107 594

MB Synergy Estimate 145 594

Source: Mediobanca Securities

Brazilian sale prevailing over €10bn rights issue or share-for-share deal options

We model three potential ways to deliver the deal, all assuming 15% premium to BKIA‟s share price:

1) a full share-for-share offer, 2) a cash bid complemented by €10bn rights issue, 3) a cash bid

funded by the sale of Brazil. We estimate the deal would deliver double digit 3-yr ROI with 4-17% 3-

yr EPS accretion and a neutral to positive impact to capital ratios, with the latter option emerging

as winner in the comparison with both the highest EPS accretion and the highest resulting CET1

ratio.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

SW

ED

A

SEB

SH

B

DAN

SKE

ND

A

ISP

CABK

CA

ALPH

A

BPM

DN

B

DBK

BP

NBG

HSBA

BPCE

LLO

Y

UBI

EBS

TPEIR

KBC

ING

UCG

PO

P

RBI

GLE

RBS

BBVA

BN

P

BAR

CBK

SAN

EU

RO

BAN

K

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 8

Price: € 6.86 Target price: € 7.60 Neutral

Summary of ROI, P/E, EPS and CET1 swings under SAN-BKIA simulations pre-ABB

Share for share Cash and capital raise

Cash and BRA sale

and scrip DVD cancellation

Premium to BKIA market price, % 15% 15% 15%

ROI, % 11.5% 11.5% 11.5%

3-yr EPS accretion, % 4% 10% 17%

2017E P/E SAN stand alone, x 11.3 11.3 11.3

2017E P/E SAN-BKIA, x 10.8 10.3 9.7

2015E CET1 SAN stand alone, % 9.6% 9.6% 9.6%

2015E CET1 SAN-BKIA, % 9.8% 9.7% 10.7%

Source: Mediobanca Securities

7-26% potential upside to €7.6 Target Price

We look at the implications of the three different SAN-BKIA combinations on SAN‟s valuation. We

find 7-26% potential upside to our €7.6 Target Price. The sale of Brazil offers the highest upside on

account of over €7bn reduction in capital shortfall, 50bp contraction in COE and €9.5bn NPV of

synergies. The other two alternatives fair the same on COE, CET1 ratio and economic capital

requirement, we see the cash bid complemented by a rights issue more accretive to valuation than

the share swap as the higher rating of SAN shares implies a lower share count dilution (c.1bn

shares).

SAN valuation range for the different simulations of the BKIA combination

Stand alone Share-for-share Cash bid + K hike Cash bid + BRA sale

Share count 13,306 15,940 14,823 12,510

COE 8.7% 8.5% 8.5% 8.2%

CET1 2015e 9.6% 9.8% 9.7% 10.7%

MB econ. capital requirement 11.0% 10.8% 10.8% 10.5%

RWAs 575,327 667,929 667,929 572,773

Excess capital -7,605 -9,007 -9,563 -318

MB 2015E Target Price (TP) 7.6 7.6 7.6 7.6

MB 2015E Fair Value 8.1 8.7 9.6

Implied P/AC 2015e 1.6 1.8 1.8 2.0

RoAC 2017e* 14% 15% 15% 14%

Implied P/E 2017e* 11.9 11.8 11.8 13.9

Upside to MB TP 7% 14% 26%

Source: Mediobanca Securities

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 9

Price: € 6.86 Target price: € 7.60 Neutral

€7.5bn capital increase: normalising the story We see the €7.5bn capital increase announced yesterday by SAN as a radical change in strategy.

This reduces the capital gap SAN has vs European peers and allows – with a limited short term

EPS dilution – the normalisation of SAN story, correcting the anomaly of a dilutive 120%

dividend payout paid in shares. We expect a negative reaction short term, given the EPS

dilution and the cut in dividend yield. Yet, this puts SAN in a more sustainable position going

forward, in our view.

€7.5bn accelerated bookbuild to close the CET1 ratio gap...

Yesterday SAN approved a capital increase in the form of €7.5bn accelerated bookbuild (ABB). This

should boost CET1 ratio by 140bp, taking 2014E Basel III fully loaded CET1 ratio to c.10% in 2015,

largely closing the capital adequacy gap vs peers (see Chart 9). This reflects a lower than expected

2014E level of 8.3% vs 8.5% target disclosed on Q314 results and 8.7% we estimated in our model.

...and normalise the SAN story

The tight capital position of SAN pre-capital increase required the quasi cancellation of cash

dividends, taking dividend yield on the cash component to 1.5%. The capital increase is triggering a

change in the 2015 dividend policy whereby three out of four dividends will be paid entirely in cash,

with a cumulative cap of €0.15 per share. From 2016 the cash dividend will hover between 30-40%

payout. We estimate this should take the cash DPS yield to 2% in 2015 and 3% thereafter.

2% estimated EPS dilution in 2015E, accretion in 2016E...

Table 1 estimates the impact of the capital increase to SAN‟s key metrics. We simulate the ABB to

take place at 5% discount, for new 1,258m shares or 10% of shares outstanding. Yet, we estimate a

an EPS dilution limited to 2% in 2015E as a result of the changed scrip dividend policy which should

materially reduce the number of new shares to be issues over the next three years. Thereafter we

see an accretive impact.

...leaving SAN on 12.6x 2015E PE, 1.3x P/TE and 11% ROTE

As a result, we see SAN post capital increase trading on 12.6x 2015E PE and 1.3x P/TE for 11% RoTE,

an unappealing level considering also the limited dividend appeal in the short term.

A marked change in strategy confirming strong leadership of the new management

The announcement of the ABB is a U-turn in capital strategy at Santander. We highlight this change

reflects the strong grip the newly appointed management has on the bank.

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 10

Price: € 6.86 Target price: € 7.60 Neutral

Table 1: SAN ABB simulation

2014E 2015E 2016E 2017E

Pre rights issue

Adj. net profit 5,954 7,183 8,148 9,053

Average diluted shares outstanding 11,914 12,962 13,929 14,857

Adj. EPS 0.50 0.55 0.58 0.61

DPS 0.60 0.60 0.60 0.60

Cash DPS payout 19% 17% 16% 51%

Cash DPS yield 1.7% 1.5% 1.4% 4.5%

Adj. P/E 13.7 12.4 11.7 11.3

TBVPS 4.7 4.8 4.9 4.9

P/TBVPS 1.47 1.43 1.40 1.39

ROTE 10.3% 11.7% 12.1% 12.4%

CET1 Basel III fully loaded 8.3% 9.2% 10.2% 10.3%

Post rights issue

Capital raising

7,500 7,500 7,500

New shares in issue @5% discount

1,258 1,258 1,258

Average diluted shares outstanding

13,250 13,250 13,250

Adj. EPS

0.54 0.61 0.68

EPS dilution

-2% 5% 12%

DPS @ 35% payout

0.19 0.22 0.24

Cash DPS payout

79% 100% 100%

Cash DPS yield

2.2% 3.2% 3.5%

Adj. P/E

12.6 11.1 10.0

TBVPS

5.4 5.8 6.2

P/TBVPS

1.3 1.2 1.1

ROTE

10.8% 11.1% 11.4%

CET1 Basel III fully loaded 9.7% 10.6% 11.0% 11.4%

Source: Mediobanca Securities, company data

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 11

Price: € 6.86 Target price: € 7.60 Neutral

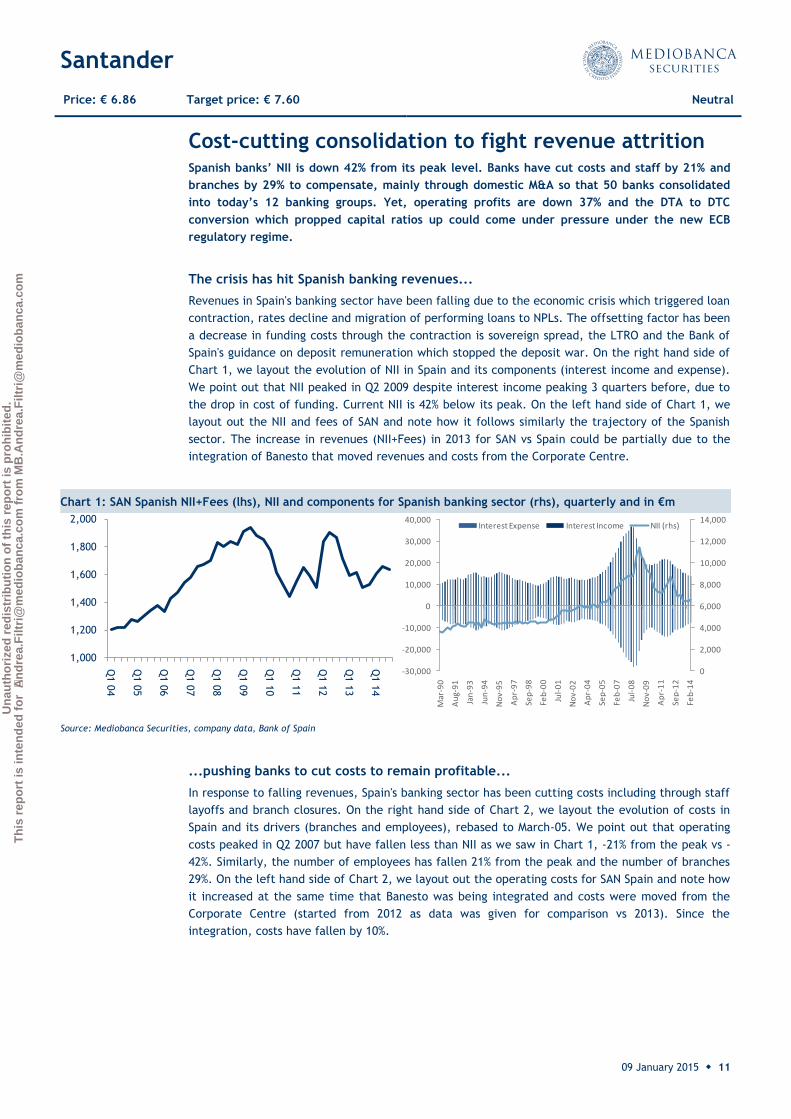

Cost-cutting consolidation to fight revenue attrition Spanish banks’ NII is down 42% from its peak level. Banks have cut costs and staff by 21% and

branches by 29% to compensate, mainly through domestic M&A so that 50 banks consolidated

into today’s 12 banking groups. Yet, operating profits are down 37% and the DTA to DTC

conversion which propped capital ratios up could come under pressure under the new ECB

regulatory regime.

The crisis has hit Spanish banking revenues...

Revenues in Spain's banking sector have been falling due to the economic crisis which triggered loan

contraction, rates decline and migration of performing loans to NPLs. The offsetting factor has been

a decrease in funding costs through the contraction is sovereign spread, the LTRO and the Bank of

Spain's guidance on deposit remuneration which stopped the deposit war. On the right hand side of

Chart 1, we layout the evolution of NII in Spain and its components (interest income and expense).

We point out that NII peaked in Q2 2009 despite interest income peaking 3 quarters before, due to

the drop in cost of funding. Current NII is 42% below its peak. On the left hand side of Chart 1, we

layout out the NII and fees of SAN and note how it follows similarly the trajectory of the Spanish

sector. The increase in revenues (NII+Fees) in 2013 for SAN vs Spain could be partially due to the

integration of Banesto that moved revenues and costs from the Corporate Centre.

Chart 1: SAN Spanish NII+Fees (lhs), NII and components for Spanish banking sector (rhs), quarterly and in €m

Source: Mediobanca Securities, company data, Bank of Spain

...pushing banks to cut costs to remain profitable...

In response to falling revenues, Spain's banking sector has been cutting costs including through staff

layoffs and branch closures. On the right hand side of Chart 2, we layout the evolution of costs in

Spain and its drivers (branches and employees), rebased to March-05. We point out that operating

costs peaked in Q2 2007 but have fallen less than NII as we saw in Chart 1, -21% from the peak vs -

42%. Similarly, the number of employees has fallen 21% from the peak and the number of branches

29%. On the left hand side of Chart 2, we layout out the operating costs for SAN Spain and note how

it increased at the same time that Banesto was being integrated and costs were moved from the

Corporate Centre (started from 2012 as data was given for comparison vs 2013). Since the

integration, costs have fallen by 10%.

1,000

1,200

1,400

1,600

1,800

2,000

Q1 0

4

Q1 0

5

Q1 0

6

Q1 0

7

Q1 0

8

Q1 0

9

Q1 1

0

Q1 1

1

Q1 1

2

Q1 1

3

Q1 1

4

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

Mar

-90

Au

g-9

1

Jan

-93

Jun

-94

No

v-9

5

Ap

r-9

7

Sep

-98

Feb

-00

Jul-

01

No

v-0

2

Ap

r-0

4

Sep

-05

Feb

-07

Jul-

08

No

v-0

9

Ap

r-1

1

Sep

-12

Feb

-14

Interest Expense Interest Income NII (rhs)

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 12

Price: € 6.86 Target price: € 7.60 Neutral

Chart 2: SAN Operating Costs, €m (lhs), Oper. costs, branches and employees for Spanish sector, rebased to 100 (rhs)

Source: Mediobanca Securities, company data, Bank of Spain

...with consolidation as the main way to extract higher efficiency…

The main way Spanish banks have used to squeeze higher efficiency out of their distribution

networks has been M&A. In Table 2, we have laid out the banks and cajas that have been part of

the consolidation in Spain (excluding the Co-op Caja Rurales). On the left hand side we can see that

the 52 banks that used to exist in Spain have given birth to today‟s 12 much larger banking groups.

500

600

700

800

900

1,000

1,100

Q1 0

4

Q1 0

5

Q1 0

6

Q1 0

7

Q1 0

8

Q1 0

9

Q1 1

0

Q1 1

1

Q1 1

2

Q1 1

3

Q1 1

4

60

80

100

120

140

160

180

Mar-0

5

Mar-0

6

Mar-0

7

Mar-0

8

Mar-0

9

Mar-1

0

Mar-1

1

Mar-1

2

Mar-1

3

Mar-1

4

Oper Costs Branches Employees

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 13

Price: € 6.86 Target price: € 7.60 Neutral

SAN’s operating profit is 37% down from the peak

Chart 3 shows the evolution of Spanish core revenues (NII+fees), costs and operating profits of SAN

rebased to Q104 (lhs) and in absolute value. These show that:

Cost cutting has almost caught up with revenues attrition but not fully;

So that operating profit is down 37% from the peak, i.e. €1.7bn lower on annualized basis

or 8% of the 2014E group estimate.

Table 2: Consolidation of the Spanish banking sector and loan market share Q314

Before After Mkt share Before After Mkt share

La Caixa

CaixaBank 17%

Caixa Sabadell

BBVA 18%

Caixa Girona Caixa Terrassa

Cajasol Caixa Manlleu

Caja de Guadalajara Caixa Catalunya

Caja Navarra Caixa Tarragona

Caja de Burgos Caixa Manresa

Caja Canarias Unicaja

Unicaja Banco 4% Banco de Valencia Caja Jaen

Barclays Caja España

Caja Madrid

Bankia 13%

Caja Duero

Bancaja Caixa Galicia Banesco NA

La Caja de Canarias Caixanova

Caixa Laietana CCM

Liberbank 2% Caja de Avila Cajastur

Caja Segovia Caja de Extremadura

Caja Rioja Caja Cantabria

CAM Banco Sabadell 8%

Caja Inmaulada de Aragon

Ibercaja Banco 3% Caixa Penedes Circulo de Burgos

Cajasur

Kutxabank 3%

Caja de Badajoz

BBK Ibercaja

Kutxa Banco Popular

Banco Popular 8% Vital Kutxa Banco Pastor

Caja Murcia

BMN 2%

Citibank España

Caja Granada Banco Santander

Santander 16% Banesto

Sa Nostra

Source: Mediobanca Securities

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 14

Price: € 6.86 Target price: € 7.60 Neutral

Chart 3: SAN evolution of Spanish revenues, costs, operating profit rebased to Q104 (lhs) and absolute (rhs)

Source: Mediobanca Securities,

DTA/DTC could come under pressure as a capital item with the Common Regulator...

The recognition of deferred tax assets (DTA) are limited to 15% of CET1, after the application of all

deductions, including other specified items (investments in financial institutions, mortgage servicing

rights) under Basel 3 regulatory framework. However, Spanish legislation in December 2013 that

approved the conversion of the majority of DTAs into tax credits (DTC). This change in legal

framework, alleviated BKIA the most in meeting Basel 3 requirements. As we can see in the chart

below, BKIA had the highest amount of DTA as a percentage of regulatory capital ratios in Spain,

followed by SAB and CABK.

We believe that now that the ECB has taken over as bank regulator, BKIA's large reliance on tax

assets/tax credits could be taken into question as the new common regulator looks at harmonizing

the quality of capital across banks in the Banking Union.

138140

133

80

100

120

140

160

180

200

220

Q1 0

4Q

3 0

4Q

1 0

5Q

3 0

5Q

1 0

6Q

3 0

6Q

1 0

7Q

3 0

7Q

1 0

8Q

3 0

8Q

1 0

9Q

3 0

9Q

1 1

0Q

3 1

0Q

1 1

1Q

3 1

1Q

1 1

2Q

3 1

2Q

1 1

3Q

3 1

3Q

1 1

4Q

3 1

4

Core revenues Costs Operating profit

1,662

908

733

200

700

1,200

1,700

2,200

Q1 04

Q4 04

Q3 05

Q2 06

Q1 07

Q4 07

Q3 08

Q2 09

Q1 10

Q4 10

Q3 11

Q2 12

Q1 13

Q4 13

Q3 14

Core revenues Costs

Operating profit

Chart 4: Basel III fully loaded 2014E and

Source: Mediobanca Securities, company data

0%

2%

4%

6%

8%

10%

12%

14%

BANKIA POP BBVA BKT SAN CABK SAB

Fully-Loaded Basel III CET1 - 2014E DTA derecognition

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 15

Price: € 6.86 Target price: € 7.60 Neutral

SAN yet to cash in from domestic consolidation Santander (SAN) directly spent c.€1.5bn through the FGD and Sareb to subsidize the

restructuring of the Spanish banking sector, implicitly transferring value to its fiercest

competitors: BBVA, CABK, SAB, BKIA. This implies SAN is yet to cash in its ‘credit’ towards the

system / the state.

Deposit Guarantee Fund in negative equity…

Chart 5 shows the evolution of the capital of the Spanish Deposit Guarantee Fund (DGF) from 1980

to 2013. We highlight the following points:

1. The harsh 1993 crisis only implied €0.8bn hit to the DGF, compared with €10bn hit taken in

the 2009-13 period;

2. In 2012-13 losses were so large to require €2.4bn extraordinary contributions from policy

holders;

3. The DGF has remained with negative funds for three straight years.

The DGF was utilised as the initial tool to restructure the Spanish banking bust. This provided Asset

Protection Schemes (APS) for Caja Castilla y la Mancha (CCM), Unnim Banc and Banco CAM.

…despite 5x increase in annual contributions...

Chart 6 shows the annual contribution of Spanish banks to the DGF. These averaged €300m per

annum from 1980-2009, implying c.6% of the outstanding capital from 1997-2009. With the

bankruptcy of the Spanish banking sector, annual contributions demanded from banks have

increased fivefold to €1.5bn to restore loss absorption capacity at the DGF‟s.

Chart 5: DGF capital and extraordinary contributions, € m

Source: Mediobanca Securities, DGF data

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Extraordinary contribution Fund capital

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 16

Price: € 6.86 Target price: € 7.60 Neutral

...implying c.€0.7bn higher bill for SAN...

We calculate SAN‟s market share in deposits stands at 14%. Taking the pro-rata share of DGF fees

for the 2010-13 period, we calculate SAN disbursed €0.84bn, i.e. €0.68bn more than it would have

paid has DGF fees not been multiplied to fund the rescues of bank bailouts.

...confirmed by latest DGF developments on contributions

The Spanish DGF approved the new EBA-dictated rules which will link individual bank contributions

to their risk profile based on five parameters:

1. Capital (leverage, excess capital, CET1 ratio)

2. Liquidity (LCR, NSFR, liquid assets/total assets)

3. Asset quality (NPL ratio, funding costs)

4. Business model (RWA/assets, ROA)

5. Maximum loss (assets/deposits)

National authorities will be able to emphasise more some parameters than others. The changes will

be implemented by June 2016 at the latest and national funds will have to make sure they reach

resources for 0.8% of insured deposits by 2024.

The new rules confirm that sounder banks have been subsidizing the bank sector‟s restructuring in

Spain also through the FGD. Yet, while BBVA, SAB and CABK increased their FGD contributions, and

then benefitted from these through the subsidised acquisitions of Unnim and CAtalunya Banc, CAM

and Banca Civica and Banco de Valencia, so far Santander only took part to the contributors‟ group

with no membership to the beneficiaries‟ one.

€0.8bn invested into Sareb, taking subsidy to competitors to €1.5bn

With 17.3% stake in Sareb‟s equity and sub. debt, SAN is the largest private investor in the „bad

bank‟. The investment required €0.8bn injection by the bank €0.2bn on the equity, €0.6bn in bonds.

This takes SAN‟s subsidy to restructure the Spanish banking sector to €1.5bn so far, largely

benefitting Bankia, CABK, BBVA and SAB.

Chart 6: annual contributions to the DGF, € m

Source: Mediobanca Securities, DGF data

0

500

1,000

1,500

2,000

2,500

3,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 17

Price: € 6.86 Target price: € 7.60 Neutral

Rethinking capital allocation Despite five years of scrip dividends, which raised €15bn new capital and boosted CET1 capital

by 30% vs 40% higher share count, SAN shows a higher than peer balance sheet gearing,

suggesting a change in strategy could be evaluated. We estimate SAN’s GDP growth exposure

has been structurally impaired during the crisis, while COE stayed essentially flat. We see Latin

American growth slowing down in coming years and regulation remaining a potential burden.

Yet, the advent of Banking Union should favour liquidity and capital fungibility within the

Union, improving the opportunity cost of onshoring capital back to Europe. We believe this

could suffice to promote a re-assessment of SAN’s capital allocation.

Lower growth, same COE: SAN’s model is less attractive post crisis but the capital increase could change the picture

Post-crisis SAN-weighted GDP exposure down 1/3 vs pre-crisis...

Chart 7 shows the exposure of Santander to GDP, weighted for the capital allocated to the

geographies the group in each given year of the 2005-16E period. This shows a pre-crisis (2005-08)

average of 3.1%, dropping sharply to 0.8% in the worst of the crisis (2009-13) and stabilising at 2% in

the post crisis (2014-16E). This suggests the crisis impaired the overall growth profile of the group.

...with COE essentially flat

Chart 8 shows the evolution of SAN‟s COE calculated by holding the beta (1.1) and the risk premium

constant and applying the risk free rate weighted by the geographical capital allocation of SAN in

each given year. We conclude that the COE corresponding to the weighted GDP growth rates above

stand at: 10%, 11.4% and 10.3%, suggesting that the overall picture has structurally worsened, with

COE up and GDP down.

Chart 7: SAN weighted average GDP YoY growth, %

Source: Mediobanca Securities, Bloomberg

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2104E 2015E 2016E

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 18

Price: € 6.86 Target price: € 7.60 Neutral

Capital significantly more geared than peers, despite scrip

Capital was stretched vs peers...

Chart 9 shows the Basel III fully loaded comparison for European banks. With c.8.5% pre-capital

increase, SAN positioned at the end of the spectrum, over 200bp below the peer group average

(10.9%, see No need to stress, 8 Sept 2014).

...despite five years of scrip dividends...

Table 3 shows the breakdown of SAN‟s DPS from 2007 to H114 between cash and scrip. The bank

introduced the first scrip option in 2009, paying 20% of the annual dividend in shares. Over the

years, this progressively went to 100% in 2012 and there has remained till today and has been

confirmed for the whole of 2014E.

Chart 8: SAN COE, %

Source: Mediobanca Securities, Bloomberg

Chart 9: Basel III fully loaded CET1 ratio H114

Source: Mediobanca Securities, company data

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2104E 2015E

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

SW

ED

A

SEB

SH

B

DAN

SKE

ND

A

ISP

CABK

CA

ALPH

A

BPM

DN

B

DBK

BP

NBG

HSBA

BPCE

LLO

Y

UBI

EBS

TPEIR

KBC

ING

UCG

PO

P

RBI

GLE

RBS

BBVA

BN

P

BAR

CBK

SAN

EU

RO

BAN

K

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 19

Price: € 6.86 Target price: € 7.60 Neutral

...raising €15bn (30% of 2009 CET1 capital) net new capital vs 40% share dilution...

Table 4 shows the average shares outstanding at SAN and the corresponding split of cash and scrip

dividends paid to shareholders from 2007 to H114, together with the RWA evolution. We highlight

the following:

Since the introduction of scrip dividends, SAN paid €8bn cash dividends and €23bn scrip

dividends, implying €15bn net capital retention...

...equivalent to 30% of the 2009 CT1 capital. From 2009 to H114, SAN‟s core capital has

only grown by €5bn, which includes the negative hit from the implementation of Basel 3

rules this year. We estimate a positive gross capital creation of €14bn by 2014YE, in line

with the estimated capital retention through scrip dividends;

The numbers of outstanding shares inflated by 40%, outpacing the capital creation in

percentage terms;

We estimate RWAs to be down 1% at 2014YE vs 2009.

...for over 20% TBVPS dilution, 30 p.p. below EU banks

This above analysis suggests that, despite the huge capital effort made, the scrip dividend policy

has not fixed SAN‟s capital stretch. At the same time, the large issuance of new shares has brought

about over 20% dilution in SAN‟s TBVPS vs 2009, comparing with 11% accretion for European banks,

despite the latter have suffered from very significant and dilutive rights issues.

Table 3: SAN DPS split, cash vs scrip, 2007-H114, € per share

DPS analysis 2007 2008 2009 2010 2011 2012 2013 2014E

Scrip 0.000 0.000 0.120 0.236 0.465 0.604 0.602 0.304

Cash 0.651 0.651 0.480 0.364 0.135 0.000 0.000

Total DPS 0.651 0.651 0.600 0.600 0.600 0.604 0.602 0.304

Cash share of DPS 100% 100% 80% 61% 23% 0% 0% 0%

Source: Mediobanca Securities, company data

Table 4: SAN DPS split, cash vs scrip, 2007-H114, € per share

DPS analysis 2007 2008 2009 2010 2011 2012 2013 2014E

Avg share count 6,254 7,124 8,111 8,279 8,619 9,615 10,827 11,333

Cash 4,070 4,636 3,893 3,014 1,165 0 0 0

Scrip 0 0 973 1,954 4,008 5,808 6,518 3,445

RWAs 515,050 514,013 561,684 604,885 528,048 557,030 489,736 555,740

Source: Mediobanca Securities

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 20

Price: € 6.86 Target price: € 7.60 Neutral

LATAM is slowing and getting more volatile

Rest of the group outpacing LATAM profit growth post crisis makes it less appealing

Chart 11 shows the YoY net profit growth from 2005 to 2016E for SAN‟s LATAM division and for the

rest of the group excluding the corporate centre and the R.E. runoff (ROG). The analysis includes

changes to the group‟s perimeter both in LATAM and in ROG, yet, over the period this should

provide a feel for the directional trends ongoing at the bank. We note that:

Before the crisis, LATAM delivered average annual profit growth of 27%, 3x ROG;

During the crisis, LATAM maintained its annual profits flat, while ROG fell by 10% annually,

on average;

Post crisis, we expect ROG to outperform LATAM average annual profit growth by 4x.

This naturally makes the LATAM presence relatively less attractive than in the past, in our view.

Chart 10: TBVPS evolution, SAN vs European Banks, 2009-H114

Source: Bloomberg

70

75

80

85

90

95

100

105

110

115

Dec-0

9

Feb-1

0

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

Dec-1

0

Feb-1

1

Apr-

11

Jun-1

1

Aug-1

1

Oct-

11

Dec-1

1

Feb-1

2

Apr-

12

Jun-1

2

Aug-1

2

Oct-

12

Dec-1

2

Feb-1

3

Apr-

13

Jun-1

3

Aug-1

3

Oct-

13

Dec-1

3

Feb-1

4

Apr-

14

Jun-1

4

SAN SX7P

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 21

Price: € 6.86 Target price: € 7.60 Neutral

Regulation could continue to be a burden...

GSIFI and TLAC: bigger is no longer better…

The Financial Stability Board (FSB) has been introducing regulation on banks to limit their „too big

to fail risk‟. These lead to Global Systemically Important Financial Institutions (GSIFI) buffers (see

below) and will lead to the introduction of „Total Loss-Absorbing Capacity‟ (TLAC) in February 2015.

Chart 11: SAN LATAM vs rest of the group ex-corporate centre and R.E. profit growth YoY

2005-16E, %

Source: Mediobanca Securities, company data

Table 5: GSIFI buffer, Nov 2014

GSIFI buffer

HSBA 2.50%

BARC 2.00%

BNPP 2.00%

DBK 2.00%

RBS 1.50%

CA 1.00%

UBS 1.00%

BBVA 1.00%

Group BPCE 1.00%

ING 1.00%

NDA 1.00%

SAN 1.00%

GLE 1.00%

STAN 1.00%

UCG 1.00%

Source: Financial Stability Board

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

LATAM RoG ex-Corp centre, R.E.

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 22

Price: € 6.86 Target price: € 7.60 Neutral

TLAC aims at setting a Pillar 2 buffer for GSIFI banks to reduce the overall resources available in a

resolution, limiting the potential systemic damage. In „TLAC: dividends over earnings risk, 24 Oct

2014‟, we estimated an average 6.5% risk to 2016E EPS of European GSIFIs. We therefore concluded

that TLAC would represent more a risk to DPS than EPS.

From the information released so far, we understand TLAC requirements will be imposed only on

GSIFI names, providing a potential competitive advantage for smaller, domestic banks given a

resulting lower cost of funding. This would only compensate if COE contraction for „safer‟ TLAC

compliant banks would drop so much to compensate the extra interest expenses to service the

newly issued funding instruments.

...and global banks continue to put up with mounting requests from local regulators

On top of FSB-imposed regulation, large global banks are having to put up with mounting requests

from local regulators on the requirements of the group‟s subsidiaries in the different jurisdictions.

Each local regulator is toughening rules on local capital, liquidity, compliance, making it relatively

more costly and risky to be a multinational group, in our view.

...but Banking Union could be a catalyst to rethink capital allocation

One regulator, larger shoulders...

While being a multinational bank is getting more and more difficult, the ongoing implementation of

the Banking Union in Europe could be making things easier as a single regulatory contact point with

a single rule book should at least simplify banks‟ life and reduce compliance costs.

...capital and liquidity synergies and lower COE...

In a longer term horizon, the implementation of real free mobility of capital and liquidity across the

Union should offer maximisation opportunities with positive reflection on structural RoTE. Also, the

Banking Union‟s Common Resolution and Deposit Insurance schemes should grant for lower Cost of

Equity (COE) over the longer term.

...provides an incentive to repatriate capital back to the Banking Union

If the above assumptions materialise, ceteris paribus, we could assist to a progressive

reconsideration of the geographical capital allocation of international groups with large non-

Eurozone operations.

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 23

Price: € 6.86 Target price: € 7.60 Neutral

SAN-BKIA: cost, funding and capital synergies Market speculation on the potential use of the new capital at SAN has already started, with

potential M&A targets across borders up strongly in yesterday’s trading day. We believe the

operation addresses SAN’s stand alone issues but in an M&A scenario would favour in-market

options such as BKIA. We benchmark the SAN-BKIA combination to the other large national

champions around Europe and find that the Spanish mammoth would not differ from others

around the Continent. We identify €0.6bn and €145m cost and funding synergies by averaging

out three bottom-up and top-down methodologies, justifying €1.5bn restructuring charges. We

model three potential ways to deliver the deal, all assuming 15% premium to BKIA’s share price:

1) a full share-for-share offer, 2) a cash bid complemented by €10bn rights issue, 3) a cash bid

funded by the sale of Brazil. We estimate the deal would deliver double digit 3-yr ROI with 4-

17% 3-yr EPS accretion and a neutral to positive impact to capital ratios, with the latter option

emerging as winner in the comparison with both the highest EPS accretion and the highest

resulting CET1 ratio. This analysis does not take into account the freshly announced capital

increase.

A ‘national champion’ like others in Europe

Table 2 shows the loan, deposit and AUM market share of the various „national champions‟ around

Europe, comparing these with the potential SAN-BKIA combination. We estimate the Spanish

conglomerate would hit 24%, 23% and 25% share, respectively, a very homogeneous level across

products. The deposit share – usually the most sensitive for antitrust purposes – would stand in line

with UK‟s Lloyds Banking Group and well below Credit Agricole‟s 31%. This would imply the deal is

likely doable from an antitrust standpoint.

€622m bottom up cost cuts...

Table 7 shows our cost synergy estimates for the SAN-BKIA combination. We assume:

100% cut of marketing, IT and Communication G&A;

50% cut of depreciation,

15% cut of staff costs,

No savings from rent/insurance/procurement

We believe this is conservative particularly on the staff cost side, where we have seen much harsher

targets from the integrations announced so far in Spain.

This totals €622m cost savings, or 32.6% of BKIA‟s 2013 cost base.

Table 6: comparison of national champions market shares, Q314

SAN BKIA SAN+BKIA ISP LLOY CA

Loans 13% 11% 24% 15% 19% 29%

Deposits 14% 9% 23% 16% 22% 31%

Mutual Funds 20% 5% 25% 22% 10% 17%

Source: Mediobanca Securities, company data

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 24

Price: € 6.86 Target price: € 7.60 Neutral

...and up to €290m funding savings...

Table 8 shows an estimate of the potential funding cost savings of the SAN-BKIA combination. We

conservatively estimate c.30bp lower deposit costs (excluding all other funding sources). This alone

would generate €290m lower funding costs.

...in line with Spanish and European benchmarks...

Table 9 shows the summary of the revenues and cost synergy targets of the main banking M&A deals

of the last ten years as a percentage of the target‟s revenues and costs. We note that:

We calculate an average of 24% cost cuts and 4% revenue boost in our sample;

As expected, in-market deals have targeted higher cost savings (31%) and similar revenue

boost;

Table 7: BKIA’s cost synergies

Bankia's Cost Structure 2013 % Synergy Targeted

Total Cost 1,905 100% 622

Staff Cost 1,117 59% 168

G&A 613 32%

Rent 246 13%

... o/w property, fixture, supplies 170 9%

... o/w Security 22 1%

... o/w Insurance 54 3%

Non-staff and rent 366 19% 366

... o/w IT & Communication 179 9%

... o/w Marketing 44 2%

... o/w Taxes 4 0%

... o/w Technical reports 62 3%

... o/w Other 77 4%

Depreciation 175 9% 88

Source: Mediobanca Securities

Table 8: potential funding cost savings in the SAN-BKIA combination, €

BKIA SAN Delta

Cost of time deposit, front book 0.85% 0.55% 0.30%

Cost of time deposit, back book 1.83% 1.20% 0.63%

CUSTOMER DEPOSIT COST 1.08% 0.75% 0.33%

Deposits 87,975 178,000

o/w time deposits 75,320 78,000

o/w demand deposits 12,655 99,000

o/w retail commercial paper 0 1,000

Potential savings

290

Source: Mediobanca Securities, company data

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 25

Price: € 6.86 Target price: € 7.60 Neutral

Isolating the recent Spanish M&A, targets skewed towards more aggressive cost savings

(36%) and minimal revenue synergies (1%).

Table 9: summary of the revenue and costs synergy targets as % of the target, 2004-2014

Date Revenue Costs

RBS/Charter One May-04 12% 24%

Santander/Abbey Nov-04 5% 17%

Danske/Irish NAB Dec-04 0% 19%

ABN AMRO/Antonveneta Mar-05 5% 15%

UCG/HVB Jul-05 1% 15%

Commerzbank/Eurohypo Oct-05 5% 15%

BNP/BNL Feb-06 7% 14%

Natixis Mar-06 9% 9%

BCP/BPI Apr-06 0% 40%

BIN-SPI Aug-06 3% 19%

BIN-SPI (realised) Aug-06 3% 27%

BPVN-BPI Oct-06 17% 22%

Credit Agricole / Cariparma Oct-06 5% 9%

Danske/Sampo Bank Nov-06 0% 18%

BPU/ BL Nov-06 0% 21%

UCG/CAP May-07 6% 24%

RBS/ABN Amro Jul-07 2% 8%

MPS/Antonveneta Nov-07 6% 25%

ISP/Carifirenze Jun-08 9% 29%

DBK/DPB Sep-08 6% 25%

Lloyds/HBOS Sep-08 0% 15%

BNP/Fortis Oct-08 3% 20%

Bankia May-11 0% 17%

POP/Pastor Oct-11 0% 40%

SAB/CAM Dec-11 4% 32%

BBVA/Unnim Mar-12 3% 40%

CABK/BdV Nov-12 0% 38%

SAN/Banesto Dec-12 4% 51%

BBVA/CX Jul-14 0% 40%

POP/Citi Jun-14 0% 20%

CABK/BARC Sep-14 0% 42%

Average (Mean) 4% 24%

Average in-market (Mean) 4% 31%

Average in Spain (Mean) 1% 36%

Source: Mediobanca Securities

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 26

Price: € 6.86 Target price: € 7.60 Neutral

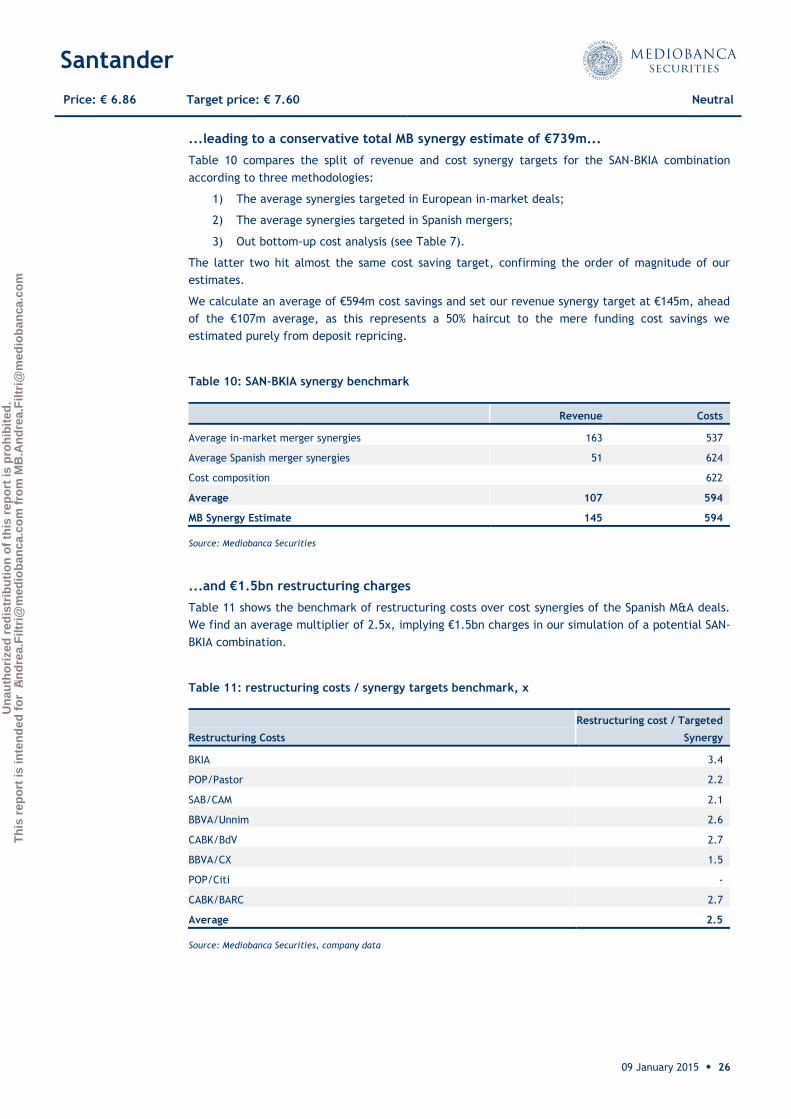

...leading to a conservative total MB synergy estimate of €739m...

Table 10 compares the split of revenue and cost synergy targets for the SAN-BKIA combination

according to three methodologies:

1) The average synergies targeted in European in-market deals;

2) The average synergies targeted in Spanish mergers;

3) Out bottom-up cost analysis (see Table 7).

The latter two hit almost the same cost saving target, confirming the order of magnitude of our

estimates.

We calculate an average of €594m cost savings and set our revenue synergy target at €145m, ahead

of the €107m average, as this represents a 50% haircut to the mere funding cost savings we

estimated purely from deposit repricing.

...and €1.5bn restructuring charges

Table 11 shows the benchmark of restructuring costs over cost synergies of the Spanish M&A deals.

We find an average multiplier of 2.5x, implying €1.5bn charges in our simulation of a potential SAN-

BKIA combination.

Table 10: SAN-BKIA synergy benchmark

Revenue Costs

Average in-market merger synergies 163 537

Average Spanish merger synergies 51 624

Cost composition 622

Average 107 594

MB Synergy Estimate 145 594

Source: Mediobanca Securities

Table 11: restructuring costs / synergy targets benchmark, x

Restructuring Costs

Restructuring cost / Targeted

Synergy

BKIA 3.4

POP/Pastor 2.2

SAB/CAM 2.1

BBVA/Unnim 2.6

CABK/BdV 2.7

BBVA/CX 1.5

POP/Citi -

CABK/BARC 2.7

Average 2.5

Source: Mediobanca Securities, company data

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r A

nd

rea.

Filt

ri@

med

iob

anca

.co

m f

rom

MB

.An

dre

a.F

iltri

@m

edio

ban

ca.c

om

Santander

09 January 2015 ◆ 27

Price: € 6.86 Target price: € 7.60 Neutral

Three simulations: share-for-share, cash and Brazilian sale We run three simulations covering three alternative options of how the SAN-BKIA combination could

be structured:

1) A full share-for-share deal, limiting the capital impact but entailing controversial

governance issues;

2) A full cash deal, highly accretive from an EPS standpoint but bringing along a high balance

sheet gearing, complemented by a €10bn rights issue aimed at keeping SAN‟s CET1 ratio

unchanged;

3) A full cash deal, highly accretive from an EPS standpoint but bringing along a high balance

sheet gearing, supported by the redeployment of the proceeds from the sale of the

Brazilian unit.

Double digit 3-yr ROI, 4-17% EPS accretion and neutral-positive to CET1

Table 12 summarises the main results from our three simulations. Assuming a 15% premium to the

current BKIA share price, we see the 3-yr ROI at 11.5%, with 4-17% accretion to the 3-yr EPS and

neutral to positive (up to 110bp) impact to CET1 ratio. Among the three simulations, the numbers

suggest the following pecking order:

1) Brazilian sale the best option on paper – the BKIA cash takeover funded by the sale of

Brazil results in 110bp CET1 boost, taking SAN to 10.7%, closer to the peer average and

100bp north of the two alternative options. This should allow the cancellation of the scrip

dividend, resulting in an overall 2017E EPS accretion of 17%, 4x and 70% ahead of the

alternatives;

2) Cash and €10bn capital raise – this simulation positions #2, with a similar CET1 ratio of

the share for share option but with 10% EPS upgrade vs 4%;

3) Share for share the least likely option – the share-for-share option is the one which on

paper emerges with the least appealing outcome as – compared to the cash option – results

in: higher PE, lower EPS accretion, same CET1 ratios. Also, we regard this option the least

likely given the governance implications this would have, i.e. the FROB would become the

largest SAN shareholder with c.10% ownership.