2015 Global-Survery-Report

10

JUNE 2015 SENIOR MANAGEMENT GLOBAL SURVEY REPORT 0

-

Upload

cornerstone-india -

Category

Business

-

view

60 -

download

0

Transcript of 2015 Global-Survery-Report

JUNE 2015

SENIOR MANAGEMENT

GLOBAL SURVEY REPORT

0

CAN WE PLEASE MOVE ON? It seems we have to start every survey report with an economic lament.

It’s been eight years now and we are still dealing with a curate’s egg of an economy – good in parts.

EU disarray, a restless Russia, trading sanctions, emerging market slowdown, oil price collapse are all playing their part in making sure that only some of us sleep at night while others lie awake.

51%

34%

50%

34%

60%

30%

48%

33%

66%

32%

39%

43%

See continued strong revenue growth

Believe the global recession is over

Will add to their workforce this year

Believe leadership pipeline is healthy

2015

2014

2013

1

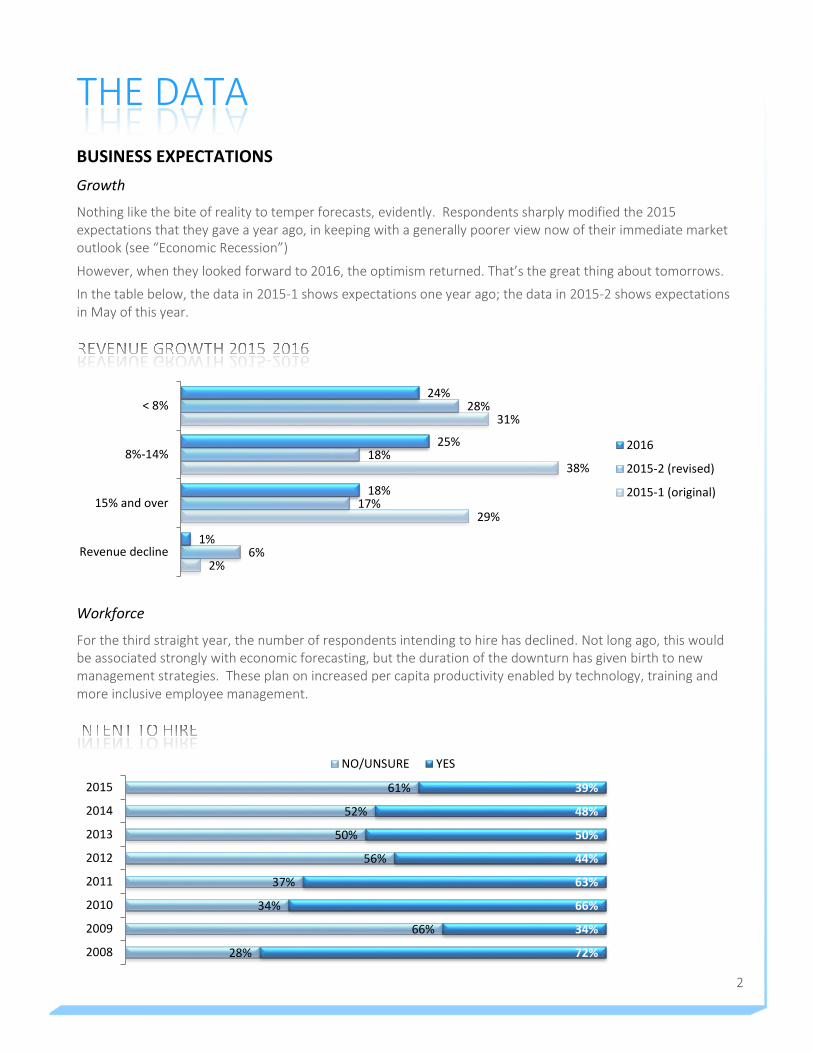

THE DATA BUSINESS EXPECTATIONS Growth

Nothing like the bite of reality to temper forecasts, evidently. Respondents sharply modified the 2015 expectations that they gave a year ago, in keeping with a generally poorer view now of their immediate market outlook (see “Economic Recession”)

However, when they looked forward to 2016, the optimism returned. That’s the great thing about tomorrows.

In the table below, the data in 2015-1 shows expectations one year ago; the data in 2015-2 shows expectations in May of this year.

Workforce

For the third straight year, the number of respondents intending to hire has declined. Not long ago, this would be associated strongly with economic forecasting, but the duration of the downturn has given birth to new management strategies. These plan on increased per capita productivity enabled by technology, training and more inclusive employee management.

2%

29%

38%

31%

6%

17%

18%

28%

1%

18%

25%

24%

Revenue decline

15% and over

8%-14%

< 8%

2016

2015-2 (revised)

2015-1 (original)

28%

66%

34%

37%

56%

50%

52%

61%

72%

34%

66%

63%

44%

50%

48%

39%

2008

2009

2010

2011

2012

2013

2014

2015

NO/UNSURE YES

2

Economic Recession

This year’s survey presents a remarkable change in attitude regarding local and global market conditions.

Historically, we have seen much greater faith in local conditions countering a general scepticism over the global economic picture. This year we have the opposite.

Although slightly more participants feel the global recession is over, almost twice as many as last year feel their local recession is not.

48%

36% 34%

30%32%

31%

39% 41%

23% 22%

21%25% 25%

47% 46%

2011 2012 2013 2014 2015

IS OVER

IS NOT OVER

UNSURE

63%

50% 48%

25%

25%

34%

25%

45%

12%16%

27%30%

2012 2013 2014 2015

IS OVER

IS NOT OVER

UNSURE

3

TALENT DEVELOPMENT Development

Over two-thirds feel employees at their firm are engaged and motivated, which is supported by the emergence of more inclusive human capital strategies.

Firms with people management goals embedded in the corporate strategy grew from 50% a year ago to 63%. Likewise, more firms offer opportunities for advancement as well as feel their leadership pipelines are being well managed.

Performance Measurement

Although the 2015 survey report shows a decline in the numbers claiming a “sound talent review and measurement”, those who do are recognizing the importance of fully integrating such a program across the organization.

The number with review programs restricted to departments has fallen significantly while the integrated programs increase. This may be recognition of the need to have universal human capital strategies that offer a leadership path regardless of skillset.

33%

39%

50%

42%

52%

63%

Our leadership pipeline is healthy

We offer opportunity for advancement

Our People strategy is embedded

2015

2014

10%

43%

47%

62%

25%

32%

54%

55%

We have no measurement program

Our program is by department only

Our program is integrated throughout the company

We have sound talent review & measurement

2015

2014

4

Coaching

More participating firms who employ coaching are recognizing its value on an ongoing basis. The popular use of coaching to date has been subject or situation specific.

Applying coaching to resolve issues and weaknesses remains the biggest single reason for coaching but ongoing development, or continuous career coaching, now is implemented by one third of respondents, up from 24%.

34%

24%

50%

40%

35%

40%

33%

48%

23%

33%

No program

Ongoing development

Resolve issues/weakness

New position

New hire (onboarding)

2015

2014

5

SEARCH & RECRUITMENT Recruiting Trends

Most respondents feel that quality candidates are both harder to find and harder to hire than in the past. This reflects a growing scarcity of high-value candidates, especially with niche skills. This contributes to the empowerment of candidates who enter the review process with very specific expectations in both business and quality of life terms.

The “Employer Brand”

The new sophistication of recruiting has seen the emergence of the “Employer Brand”, an amalgam of the values that the hiring company wishes to project.

A majority of those surveyed perceive a strong influence on candidate attitudes from the employer brand, which is in line with the increased focus of candidates to select the company that best fits their work expectations.

44%

33%

18%

5%

Harder to find and harder to hire

Harder to find, but easier to hire

Easier to find, but harder to hire

Easier to find, easier to hire

Strong influence upon candidates,

59%

No discernable influence, 38%

Negative influence, 2%

6

GOVERNANCE Management Diversity

One of the more interesting progressions revealed by these surveys has been the increasing involvement of women and ethnic minorities in the management and guidance of companies.

Boards of Directors have been slower to accept either group but we have reached 50% of respondents having women directors while ethnic minority directors are on only 20% of Boards. These figures are lower than the previous year, suggesting a different mix of companies in the responses.

Women occupy C-Level management positions in 80% of the firms surveyed, compared with 51% for minorities.

Firms with the following representation:

43%

83%

51%

80%

Minorities

Manager/director Women

Minorities

C-level Women

32%

44%

72%

23%

55%

70%

38%

20%

50%

69%

32%

We have ethnic minority Directors

We have women Directors

We have independent Directors

We have an independent chairman

2015

2014

2013

N/A

7

ABOUT THE SURVEY The Annual Survey of Senior Management reflects opinions of business leaders around the world drawn from their current experience which, of course, varies widely by region, market health and industry sector.

Invitations to complete the questionnaire are issued to executives at small, medium and large employers around the world.

Here is the composition of respondents to the 2015 survey.

18%

49%

20%

13%

United States & Canada

Latin America

Asia and South Pacific

EMEA

18%

18%

14%

9%

43%

Other

Senior Human Resources Executive

Senior Sales/Marketing executive

Senior Financial Executive

Senior Executive (CEO, COO etc)

28%

8%

33%

31%

over $1 billion

$500 million to $1 billion

$50-$500 million

Under $50 million

8

ABOUT CORNERSTONE INTERNATIONAL GROUP

Our mission is to accelerate the success of our clients by providing top-quality consulting services in the field of talent recruitment and development.

Cornerstone International Group is an organization of owner-managed firms and combines global reach and networked resources with the personal service and undivided attention delivered by each of more than 60 local offices.

The diversification of our services and depth of experience is behind our claim:

“Achieve More with Cornerstone”

Our clients include organizations in almost every industry and every major geographical region.

Each of our offices commands a leading position in its local market for repeat and referral business, be it executive search, executive coaching, or CEO and Board Advisory services.

Not The Biggest, The Best We are a member of the Association of Executive Search Consultants. The AESC is the official body representing retained executive search consulting firms worldwide with regional councils in the Americas, Europe and Asia/Pacific and an International Board of Directors. Its Code of Ethics and Professional Practice Guidelines are recognized as representing the highest level of service in our industry.

Our goal is not to be the biggest, but the best. That means the best service, the best value, and the best results – so our clients can attract and develop the very best senior management and the very best Boards in the world.

To Know More To find out more, we invite you to visit www.cornerstone-group.com.

9