2015 ACA Reporting Regulations

16

2015 ACA REPORTING REGULATIONS A webinar discussing 6055 and 6056 reporting and how DATIS will help your organization ensure compliance.

-

Upload

datis -

Category

Healthcare

-

view

143 -

download

0

Transcript of 2015 ACA Reporting Regulations

2015 ACA REPORTING REGULATIONS A webinar discussing 6055 and 6056 reporting and how DATIS will help your organization ensure compliance.

Information is general. No legal advice is provided or intended.

DATIS SPEAKERS

§ Lolitha is a Benefit Specialist at DATIS and a graduate from the University of Florida. She is responsible for handling client benefits, project management, providing client support, and more. She is a certified human resources professional.

Lolitha Bose, Benefits Specialist

Jennifer Trupia, Tax and Compliance

§ Jennifer is the cornerstone of DATIS’ daily operations, processing and tax services. She has a B.S. in Accounting from St. Johns University in New York, and is also an Enrolled Agent.

Information is general. No legal advice is provided or intended.

GUEST SPEAKERS

§ Brittany is Director of Communications for Stahl & Associates for the past three years. She focuses primarily on employee communication within a benefits program, and specializes in Consumer Driven Health Plan communication, wellness programs, and compliance particularly pertaining to legislation and Health Care Reform.

Brittany Stahl, Stahl & Associates Insurance

Michael D. Malfitano, Costangy, Brooks, Smith, & Prophete, LLP

§ Mike is a partner Costangy and the Office Head of their Tampa, Lakeland and Port St. Lucie Offices. He has been recognized in publications, Best Lawyers (1995-2015) in America and Florida Super Lawyers (2006-2014). He provides companies with preventive training in all aspects of labor and employment law.

Information is general. No legal advice is provided or intended.

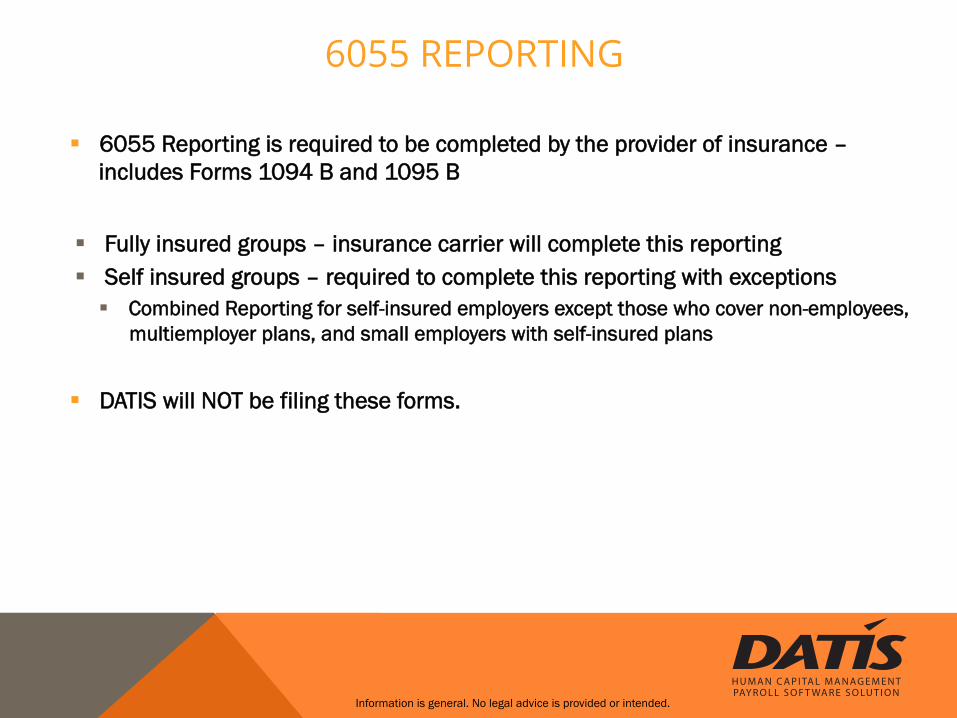

6055 REPORTING

§ 6055 Reporting is required to be completed by the provider of insurance – includes Forms 1094 B and 1095 B

§ Fully insured groups – insurance carrier will complete this reporting § Self insured groups – required to complete this reporting with exceptions

§ Combined Reporting for self-insured employers except those who cover non-employees, multiemployer plans, and small employers with self-insured plans

§ DATIS will NOT be filing these forms.

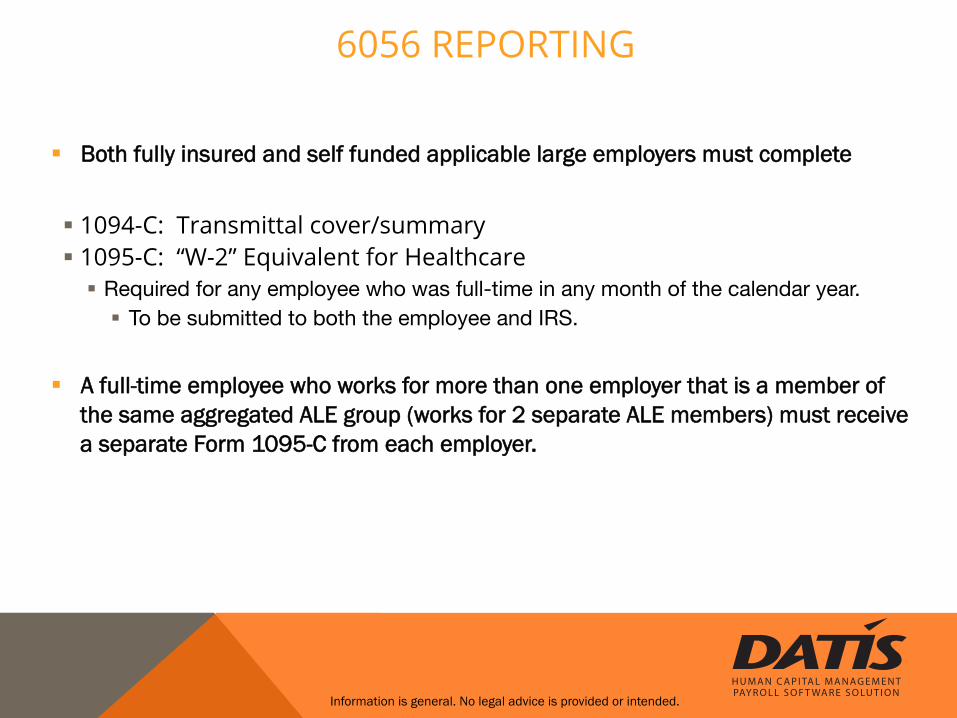

6056 REPORTING

§ Both fully insured and self funded applicable large employers must complete

§ 1094-C: Transmittal cover/summary § 1095-C: “W-2” Equivalent for Healthcare

§ Required for any employee who was full-time in any month of the calendar year. § To be submitted to both the employee and IRS.

§ A full-time employee who works for more than one employer that is a member of the same aggregated ALE group (works for 2 separate ALE members) must receive a separate Form 1095-C from each employer.

Information is general. No legal advice is provided or intended.

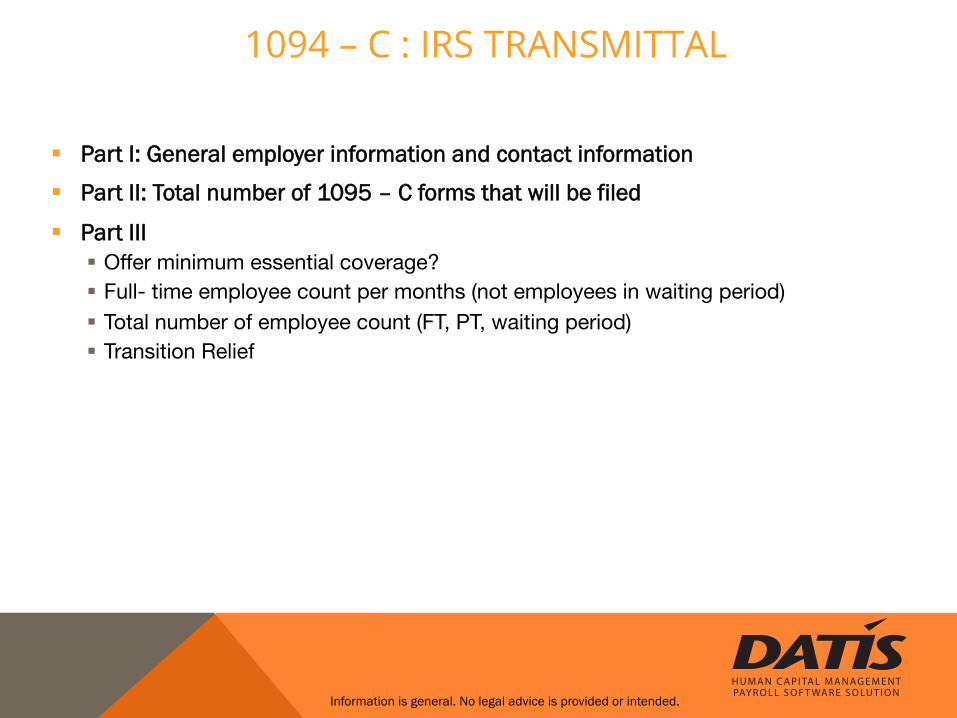

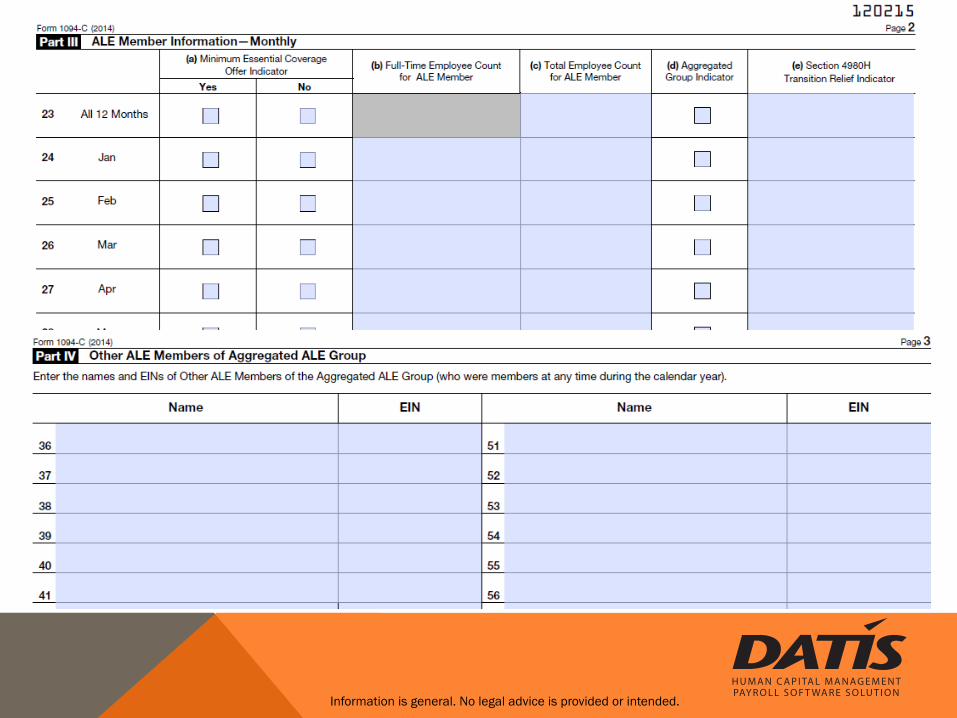

1094 – C : IRS TRANSMITTAL

§ Part I: General employer information and contact information

§ Part II: Total number of 1095 – C forms that will be filed

§ Part III § Offer minimum essential coverage? § Full- time employee count per months (not employees in waiting period) § Total number of employee count (FT, PT, waiting period) § Transition Relief

Information is general. No legal advice is provided or intended.

Information is general. No legal advice is provided or intended.

Information is general. No legal advice is provided or intended.

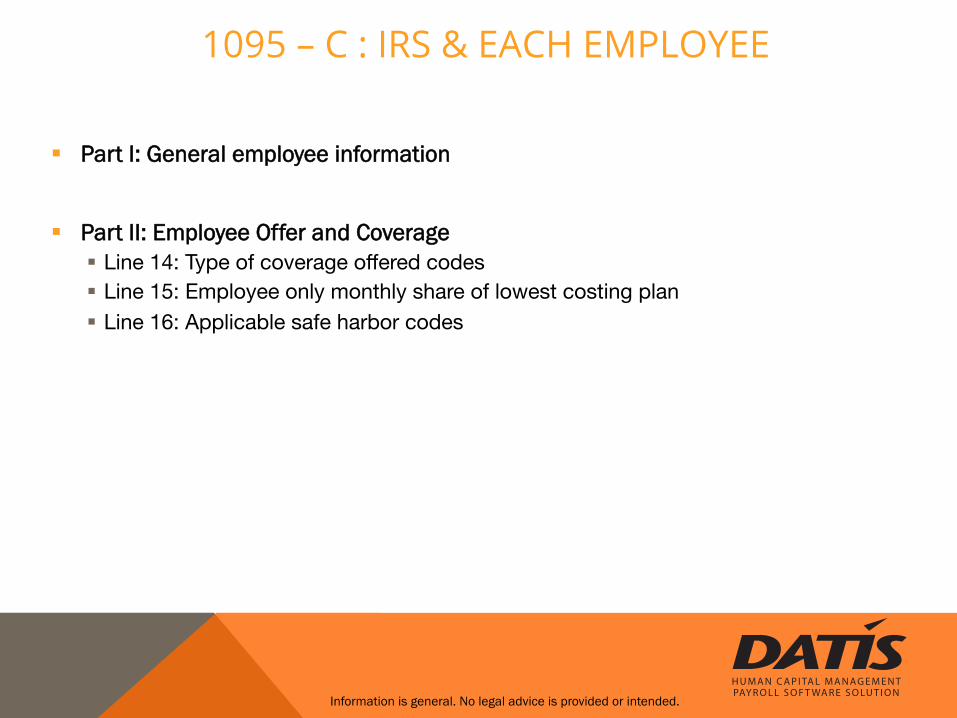

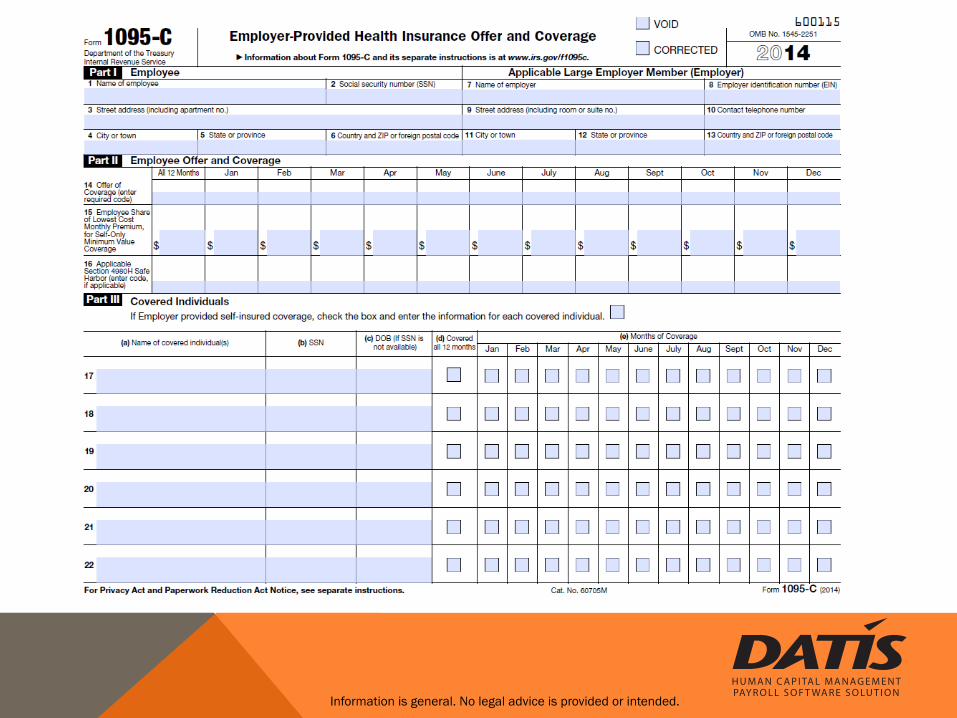

1095 – C : IRS & EACH EMPLOYEE

§ Part I: General employee information

§ Part II: Employee Offer and Coverage § Line 14: Type of coverage offered codes § Line 15: Employee only monthly share of lowest costing plan § Line 16: Applicable safe harbor codes

Information is general. No legal advice is provided or intended.

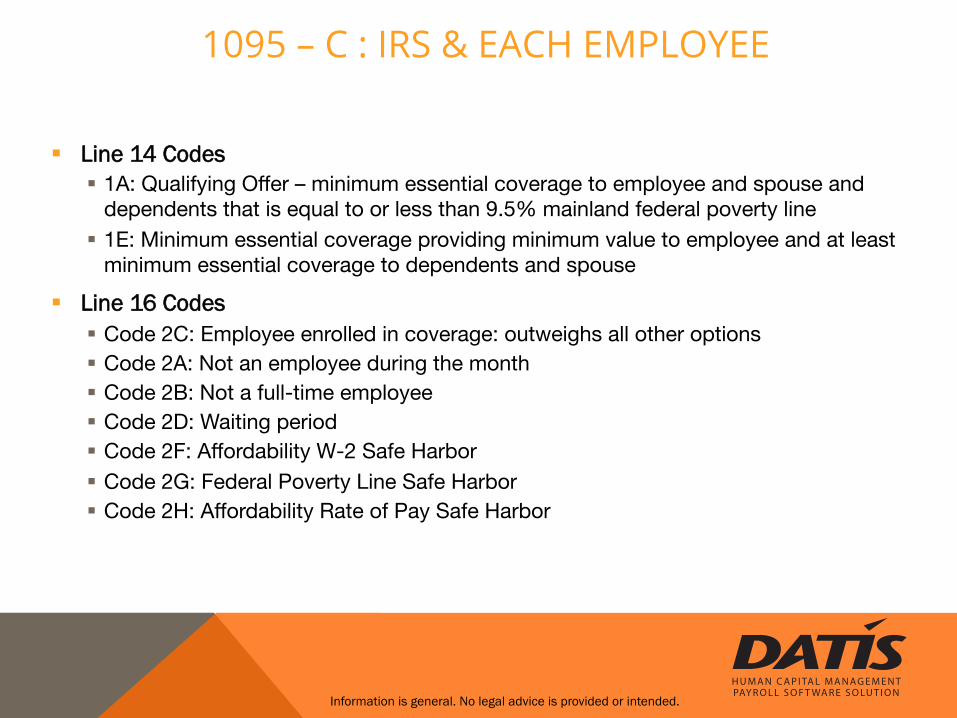

1095 – C : IRS & EACH EMPLOYEE

§ Line 14 Codes § 1A: Qualifying Offer – minimum essential coverage to employee and spouse and

dependents that is equal to or less than 9.5% mainland federal poverty line § 1E: Minimum essential coverage providing minimum value to employee and at least

minimum essential coverage to dependents and spouse

§ Line 16 Codes § Code 2C: Employee enrolled in coverage: outweighs all other options § Code 2A: Not an employee during the month § Code 2B: Not a full-time employee § Code 2D: Waiting period § Code 2F: Affordability W-2 Safe Harbor § Code 2G: Federal Poverty Line Safe Harbor § Code 2H: Affordability Rate of Pay Safe Harbor

Information is general. No legal advice is provided or intended.

1095 – C : IRS & EACH EMPLOYEE

§ Part III: Self insured employers ONLY § Covered employee & dependents, SSN, DOB, months they were covered

Information is general. No legal advice is provided or intended.

Information is general. No legal advice is provided or intended.

FILING RULES

Information is general. No legal advice is provided or intended.

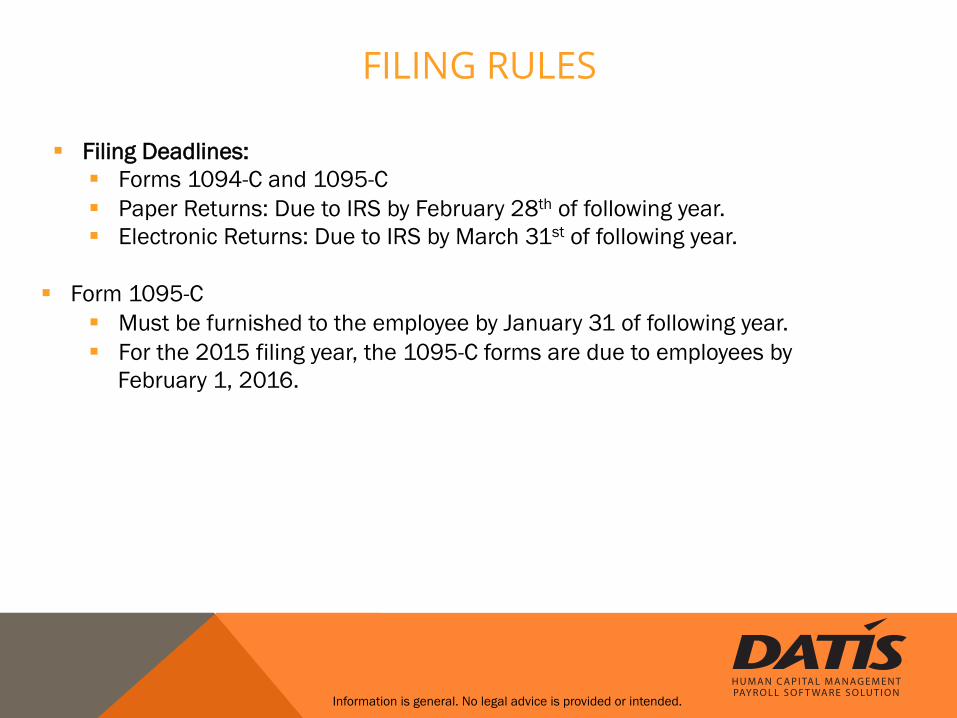

§ Filing Deadlines: § Forms 1094-C and 1095-C § Paper Returns: Due to IRS by February 28th of following year. § Electronic Returns: Due to IRS by March 31st of following year.

§ Form 1095-C § Must be furnished to the employee by January 31 of following year. § For the 2015 filing year, the 1095-C forms are due to employees by

February 1, 2016.

WHAT DATIS WILL PROVIDE

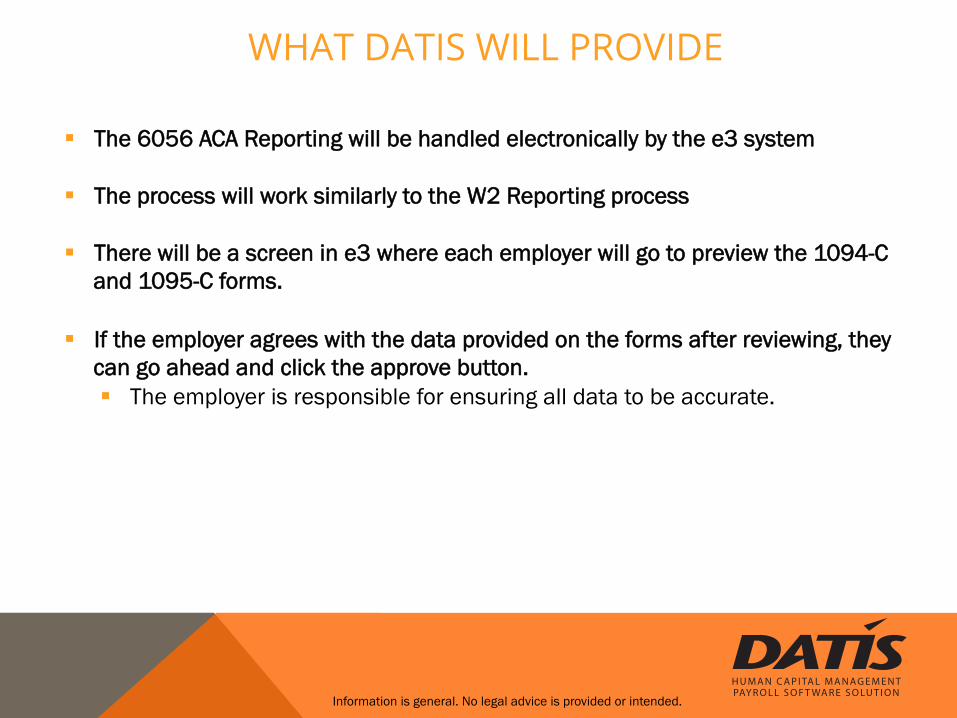

§ The 6056 ACA Reporting will be handled electronically by the e3 system § The process will work similarly to the W2 Reporting process § There will be a screen in e3 where each employer will go to preview the 1094-C

and 1095-C forms. § If the employer agrees with the data provided on the forms after reviewing, they

can go ahead and click the approve button. § The employer is responsible for ensuring all data to be accurate.

Information is general. No legal advice is provided or intended.

ELECTRONIC FORM DISTRIBUTION

§ The 1095-C forms will then populate in each employee’s My e3 screen to download and print after the forms have been approved. § DATIS will not be providing paper copies of the 1095-C to any employees.

§ DATIS will have acknowledgements set up so that each employee can either accept

or decline an electronic copy of the 1095-C. § If the employee declines the electronic copy, the employer will be responsible for

printing the 1095-C form for each employee and distributing a paper copy. § DATIS will file both the 1094-C and 1095-C forms with the IRS on the employers

behalf.

§ DATIS is standing by for the IRS to release the file specs so that we can create this feature. We will notify all clients when it becomes available.

Information is general. No legal advice is provided or intended.

QUESTIONS? Visit community.datis.com for regular updates, release notifications, and training materials.

![ACA Annual Reporting [Infographic]](https://static.fdocuments.in/doc/165x107/55cb9a98bb61ebdd728b4587/aca-annual-reporting-infographic.jpg)