2014 Pennsylvania Fed/State e-File Handbook (REV-993)

31

PENNSYLVANIA FED/STATE E-FILE HANDBOOK REV-993 (02-15) Pennsylvania e-File Handbook for Authorized e-File Providers of 2014 Pennsylvania Individual Income, Corporation, Trust and Estate and Partnership Information Returns

-

Upload

nguyenlien -

Category

Documents

-

view

223 -

download

1

Transcript of 2014 Pennsylvania Fed/State e-File Handbook (REV-993)

PENNSYLVANIA FED/STATEE-FILE HANDBOOK

REV-993 (02-15)

Pennsylvania e-File Handbook for Authorized e-File Providers of 2014

Pennsylvania Individual Income,Corporation, Trust and Estate

and Partnership Information Returns

SECTION 11. OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

SECTION 2. GENERAL INFORMATION2.1 DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2.2. PROGRAM PARTICIPATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2.3. PROVIDER RESPONSIBILITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

2.4. INCLUSION OF FEDERAL DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

2.5. TIMELY-FILED SUBMISSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2.6. AMENDED REPORTS/RETURNS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2.7. ACCEPTED FILING TYPES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2.8. SCHEMA REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2.9. SUBMISSION AND TRANSMISSION SPECIFICATIONS . . . . . . . . . . . . . . . . . . . 3

2.10. SOFTWARE ACCEPTANCE, TESTING AND APPROVAL . . . . . . . . . . . . . . . . . . . 4

2.11. SUSPENSION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2.12. ACKNOWLEDGEMENT OF SUBMISSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

SECTION 3. PARTNERSHIP E-FILE 3.1. WHAT’S NEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

3.2. ACCEPTED PENNSYLVANIA PARTNERSHIP FORMS AND SCHEDULES . . . . . . . . . 6

3.3. SCHEDULE CHANGES AND ADDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

3.4. EXCLUSIONS TO ELECTRONIC FILING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3.5. SIGNATURE REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3.6. PAYMENT OPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

3.7. RE-TRANSMISSION OF REJECTED SUBMISSION . . . . . . . . . . . . . . . . . . . . . . . 9

3.8. EXTENSION OF TIME TO FILE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

SECTION 4. CORPORATE E-FILE 4.1. WHAT’S NEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

4.2. ACCEPTED PENNSYLVANIA CORPORATE FORMS AND SCHEDULES . . . . . . . . . 11

4.3. SCHEDULE CHANGES AND ADDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.4. EXCLUSIONS TO ELECTRONIC FILING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.5. SIGNATURE REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.6. PAYMENT OPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.7. RE-TRANSMISSION OF REJECTED SUBMISSION . . . . . . . . . . . . . . . . . . . . . 13

4.8. EXTENSION OF TIME TO FILE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

PAGE

www.revenue.pa.govPENNSYLVANIA FED/STATE E-FILE HANDBOOK

SECTION 5. INDIVIDUAL INCOME E-FILE

5.1. ACCEPTED PENNSYLVANIA INDIVIDUAL INCOME TAX FORMS AND SCHEDULES . 15

5.2. SCHEDULE CHANGES AND ADDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

5.3. EXCLUSIONS TO ELECTRONIC FILING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

5.4. SIGNATURE REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

5.5. REFUND OPTIONS AND DIRECT DEPOSIT . . . . . . . . . . . . . . . . . . . . . . . . . . 16

5.6. PAYMENT OPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

5.7. RE-TRANSMISSION OF REJECTED SUBMISSION . . . . . . . . . . . . . . . . . . . . . . 19

5.8. EXTENSION OF TIME TO FILE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

SECTION 6. FIDUCIARY INCOME E-FILE

6.1. ACCEPTED PENNSYLVANIA FIDUCIARY INCOME TAX FORMS AND SCHEDULES . . 22

6.2. SCHEDULE CHANGES AND ADDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

6.3. EXCLUSIONS TO ELECTRONIC FILING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

6.4. SIGNATURE REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

6.5. REFUND OPTIONS AND DIRECT DEPOSIT . . . . . . . . . . . . . . . . . . . . . . . . . . 24

6.6. PAYMENT OPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

6.7. RE-TRANSMISSION OF REJECTED SUBMISSION . . . . . . . . . . . . . . . . . . . . . . 26

6.8. EXTENSION OF TIME TO FILE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

SECTION 7. CONTACT INFORMATION

7. CONTACT INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

PAGE

www.revenue.pa.govPENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 1

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

SECTION 1. OVERVIEWPublication REV-993, Pennsylvania e-FileHandbook provides authorized e-File providerswith specific requirements and procedures forelectronic filing through the Modernized e-File(MeF) platform provided by the Internal RevenueService (IRS) also known as Fed/State e-File andidentifies those items which are unique to theelectronic filing of Pennsylvania returns. Theprocedures in this document apply to all Fed/Statee-File Programs. All publications referenced in thisdocument are available at www.revenue.pa.gov.Check the website frequently for updatedinformation on e-filing through the Fed/Statee-File Program.

The Pennsylvania Department of Revenue, inconjunction with the IRS will be acceptingPennsylvania individual, corporation, fiduciary andpartnership returns with corresponding forms andschedules for tax year 2014. The method ofsubmission is through the MeF platform providedby the IRS. The Fed/State e-File Program allowstax preparers and taxpayers to file federal andstate returns in one electronic submission.

The process is designed to separate andencapsulate the federal and state return/reportdata in two distinct filings from one submission.The federal portion will contain only the datapertaining to the federal tax return. Theassociated state portion will contain all thedata needed for filing the state returns/reports,which includes a copy of the requested federaldata. If the state submission is associated witha federal submission, there will be a linkcontained in the state submission to theassociated federal submission.

The IRS acknowledges to the transmitter theacceptance of the federal submission and receiptof the state submission. The state submission isthen retrieved by the department and processed.The department acknowledges to the transmitterthe processing or rejection of Pennsylvaniasubmissions through the IRS.

The state submission consists of a manifest andpayload. The manifest provides identifyinginformation about the state submission andinformation the IRS needs to perform limitedvalidation. The payload includes the state XML

data, binary attachments in portable documentformat (PDF) and a copy of the requested federaldata as required by the state.

SECTION 2. GENERAL INFORMATION2.1. DEFINITIONSElectronic Return Originator (ERO) –Authorized e-file provider that originates theelectronic submission of returns to the IRS.

Federal Submission – A federal tax return withaccompanying schedules.

Received Date – The date and time the returnis received and accepted by the IRS from thetransmitter.

Schema – A document that defines the datatypes, content, structure and allowed elements.

Software Developer – A firm, organizationor individual that develops software for thepurpose of:

• formatting electronic tax return/reportinformation according to return/reportlayouts and specifications; and/or

• transmitting electronic returns/reportsinformation directly to the IRS.

State Submission - A Pennsylvania return/reportwith accompanying schedules as required by thedepartment. A state submission also includes acomplete copy of the federal return data asrequired by the department.

Transmitter – A firm, organization or individualthat transmits electronic returns/reports directlyto the IRS. A transmitter must have software andcomputers that allow it to interface with the IRS.

XML – Short for Extensible Markup Language, alanguage for defining and processing data.

RTN – Routing transit number

DAN – Deposit account number

2.2. PROGRAM PARTICIPATIONThe Fed/State e-File Program is available to allinterested parties that have been accepted asauthorized IRS e-File providers in the Federale-File Program and that transmit returns/reports

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 2

www.revenue.pa.gov

to the IRS. This includes EROs, transmitters andsoftware developers defined herein.

To participate in the Fed/State e-File Program,participants must first be accepted by the IRS fore-filing. To be accepted, potential filers mustcomplete federal Form 8633, Application toParticipate in the IRS e-File Program, and testing.The department does not require approved EROs,transmitters and software developers to registerseparately for electronic filing in Pennsylvania.

2.3. PROVIDER RESPONSIBILITIESAuthorized e-File providers must adhere to all IRSand Pennsylvania e-File rules, requirements andspecifications applicable to the e-File activitiesthey conduct. Responsibilities include, but are notlimited to:

Software Developer• Develop software in accordance with

statutory requirements and Pennsylvaniareturn preparation instructions andprovided business rules.

• Provide accurate Pennsylvaniareturns/reports in the correctelectronic format.

• Provide data validation, verification anderror detection to prevent transmission of incomplete, inaccurate or invalid return information.

• Prevent electronic filing of any form orschedule not approved for electronic filingby the department.

• Include electronic signature information inthe software.

• Successfully complete all testing as required.

• Correct any software errors that mayoccur after production begins and workwith the department to follow up on anyprocessing issues that may arise duringfiling season. If software providers needto re-release corrected software, therelease must be done in a timelymanner, and proper notification must beprovided to all customers.

Transmitter• Timely transmit returns/reports, retrieve

acknowledgement files and sendacknowledgement file information to theappropriate ERO.

• Provide an e-postmark for everyPennsylvania return/report.

• Promptly correct transmission errorscausing electronic transmissions to be rejected.

• Ensure the security of all transmitted data.

Electronic Return Originator (ERO)• Identify the paid preparer (if any) in the

appropriate field of the electronic record ofreturns and/or reports it originates.

• Inform taxpayers of obligations andoptions for paying balances due.Taxpayers who have balances due mustpay them by the original due dates of thereturns/reports in order to avoid interestand penalties.

• Ensure appropriate signatures areincluded in the electronic returns/reports.

• Originate the electronic submission ofreturns/reports as soon as possible afterthey are signed.

• Retain signed signature documents forthe timeframe required from the duedate of the return/report or the date thereturn/report was filed electronically,whichever date is later.

• Ensure acknowledgements are receivedfor all state submissions filed.

• Instruct taxpayers that if a Fed/Statesubmission is rejected by the IRS, a statestand-alone submission must be filed tomeet the established due date.

2.4. INCLUSION OF FEDERAL DATAEach state filing must include a copy of thefederal data using the most current publishedversion of the IRS XML schema.

Page 3

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

2.5. TIMELY FILED SUBMISSIONSAll due dates for filing paper returns apply toelectronic returns. The department recognizesthe electronic postmark as the date received bythe department. A state submission and anelectronic payment are considered timely-filed ifthe received date is prior to the due date forPennsylvania returns.

2.6. AMENDED REPORTS/RETURNS After a state submission is acknowledged asreceived, it cannot be recalled or intercepted. Ifthe ERO or taxpayer wishes to change any entryon an accepted state submission, an amendedreturn must be filed.

2.7. ACCEPTED FILING TYPESFed/State - An original federal submission andone original state submission containing a link to the original federal submission (includes thesubmission ID of the federal return in the state manifest).

The Fed/State submissions do not have to betransmitted together; however, the statesubmission must include a pointer to the originalfederal return.

Note: If a state submission is linked to afederal submission and the state submissionis to be transmitted separately, pleasetransmit the federal submission first. After it has been accepted, send in the state submission.

State Stand-Alone - An original state submissionthat does not contain a link to a previouslysubmitted original federal submission.

2.8. SCHEMA REQUIREMENTS• Software developers are required to apply

data from the Pennsylvania spreadsheetsor tax forms to the appropriate dataelement from the XML schema. State data must conform to therequirements and specifications outlined in this handbook.

• Federal data required by the departmentfor inclusion in the state submission mustconform to the most current publishedversion of the IRS XML schema.

• Values for data elements identified by thedepartment as required fields must beincluded in the XML schema and passed tothe department, even when the value ofthe data element is zero.

• Values for data elements identified by thedepartment as fields not required shouldbe included in the XML schema and passedto the department only when the taxpayerenters a value, even if the value is zero.

• All XML data must be valid andwell-formed.

2.9. SUBMISSION AND TRANSMISSION SPECIFICATIONS

• The transmission protocol will be Web Services using Simple Object Access Protocol (SOAP) with attachments messaging.

• A state submission contains XML data,binary attachments in PDF format and acopy of the federal submission as requiredby the department.

• Packaging of data and transmissionpayload must conform to all submissionand transmission file structures.

• If the IRS rejects a federal submission, thedepartment will not receive the statesubmission. The Fed/State submissionmust be corrected and re-submitted as a Fed/State submission or statestand-alone submission.

• Each submission must be in zip archive format.

• The SOAP message itself must not becompressed or zipped.

• The SOAP message must contain a header,a body and an attachment.

• The ERO and transmitter must beapproved with the IRS to submitFed/State submissions.

• The department will produceacknowledgements of processing orrejection for each state submission. Thetransmitter will then retrieve the stateacknowledgements from the IRS.

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 4

www.revenue.pa.gov

Expected Values for State Submission Manifest

For more information on conforming totransmission and submission file structures, referto IRS Publications 4163 and 4164 at www.irs.gov.

2.10. SOFTWARE ACCEPTANCE, TESTING AND APPROVAL

• All participants are required to pass theIRS’s acceptance testing systemprocedures for acceptance into theFed/State e-File Program.

• The Electronic Filer Identification Number(EFIN) and Electronic TransmitterIdentification Number (ETIN) assigned bythe IRS will be used by the department.These numbers will be required for use inevery submission foridentification/verification of testing andproduction returns.

• The software used to capture andtransmit data must be approved by theIRS and the department.

• When a software developer’s testreturns/reports have been accepted bythe IRS, the state data will be retrievedby the department for testing.

• Software developers must transmit testfiles, as specified by the department, toensure the software meets thedepartment’s specifications.

• All software developers are required totest with the department for approval ofthe software.

Note: Test materials and instructions may beobtained using the contact information inSection 6.

• Software developers must support the schedules and forms specified by the department.

• Software developers that produce afacsimile of payment vouchers, PA-8879and/or PA-8453 with a software packagemust submit the appropriate number ofcopies to the department for testing andapproval. Five copies of the substitutevoucher must be mailed to the addressbelow. Two copies of PA-8879 and twocopies of PA-8453 must be mailed oremailed in PDF format to:

JARED DUNLOPPA DEPARTMENT OF REVENUEBUREAU OF ADMINISTRATIVE SERVICES 12 TH FL 4 TH & WALNUT STHARRISBURG PA 17128Telephone: 717-705-0593Email: [email protected]

• Software developers must include theedits and verifications based on thebusiness rules for each field or dataelement specified by the department.Software developers must closely followthe requirements for each field to insureproper data formatting.

• The department will provide test resultsand vendor approval in writtenconfirmation to the vendor.

2.11. SUSPENSIONThe department reserves the right to suspend orrevoke the electronic filing privileges of anyelectronic filer who varies from the Pennsylvaniae-File requirements and specifications.

2.12. ACKNOWLEDGEMENT OFSUBMISSIONS

The department electronically acknowledges thereceipt of all state submissions. After the retrieval

FForm Submission Type

PA-40 PA1040

REV-276 EX PA40EXT

PA-41 PA1041

REV-276 EX PA41EXT

PA-20S/65 PA65PA20S65

PA-65 CORP PA65PA65CORP

RCT-101 PA20RCT101

RCT-101I PA20RCT101I

FORM 853 PA20EXT

PA65ESR PA40ESRP

REV-276 EX PA65EXT

Page 5

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

of state submissions from the IRS, the departmentwill generate acknowledgement records andtransmit them to the IRS for retrieval bytransmitters. The acknowledgement is anelectronic confirmation of receipt and informstransmitters that the Pennsylvania returns/reportstransmitted have been received and processed orrejected by the department. The acceptance code“A” indicates a return/report has met thedepartment’s processing criteria and is consideredreceived, and the rejection code “R” indicates areturn/report has failed to meet the department’sprocessing criteria.

Should a return/report be rejected, a uniquerejection code will be included in theacknowledgement to identify the reason forrejection. Transmitters should communicateacknowledgment results back to the appropriateERO for resolution if applicable.

If the return/report is rejected, thetransmitter/software developer/ERO/taxpayer isrequired to re-submit a corrected return/report orfile by other means.

SECTION 3. PARTNERSHIP E-FILE3.1. WHAT’S NEW Act 52 of 2013, instituted several changes for passthrough entities filing PA-20S/PA-65 returns for2014. The following updates are effective for taxyears beginning after Dec. 31, 2013.An entity classified as a partnership, Scorporation or limited liability company forfederal tax purposes that fails to file aPA-20S/PA-65, Information Return with theDepartment, will be subject to a $250 failure tofile penalty. A $250 penalty also applies to eachSchedule RK-1 or NRK-1 not furnished to apartner, shareholder or member.Assessments of tax may be applied at the entitylevel if there is an understatement of income formore than $1 million and the entity has 11 ormore owners or a partnership has at least oneowner that is another entity or trust.

The entity is required to keep an accurate list ofowners’ names, addresses and tax identificationnumbers. Failure to comply may result in aresponsible party assessment for the tax of thepartner for whom the department was not able to

assess. This provision permits a PIT assessmentagainst a general partner, tax matters partner,corporate officer or trustee for the liability of thepartner that could not be assessed.

Entities may now deduct start-up expenditures inthe same manner as under IRC §195 (b)(1)(A).The first $5,000 of such expenses may be directlyexpensed with any amount over $5,000 beingamortized over 180 months. If the amount ofstart-up expenses is more than $50,000, there is adollar-for-dollar reduction up to $55,000 of thedirect expense amount.

A copy of federal tax return Form 1120S, U.S.Income Tax Return for an S Corporation, or Form1065, U.S. Return of Partnership Income, nowmust be included with the entity’s PA-20S/PA-65,PA S corporation/Partnership Information Return.

An entity may elect to currently expense up toone-third of the intangible drilling anddevelopment costs (IDCs) it incurs in tax yearsbeginning after Dec. 31, 2013. The remainder ofthe IDCs may be amortized over 10 years. If theentity does not elect to currently expense its IDCs,it may amortize them over 10 years.The resident credit for taxes paid to other states orcountries is now only available as a credit for taxespaid to a state of the U.S., the District of Columbia,the Commonwealth of Puerto Rico or any territoryor possession of the U.S. The credit for taxes paidto foreign countries is no longer permitted as acredit against a personal income tax liability.Partnerships that are not LLCs will not be assigned10-digit Revenue IDs. Only S corporations andlimited liability companies will be issued 10-digitRevenue ID numbers. However partnershipsremitting CNI tax will also be assigned a 10-digitRevenue ID.Beginning with the 2015 filing season thedepartment will accept through e-file REV-276Application for Extension of Time to File thePA-20S/PA-65 Information Return.Mandatory e-filing is now required for the PA-65Corp PA Directory of Corporate Partners for anythird party preparer that prepares 11 or more PADirectory of Corporate Partners Returns. Forguidance, please review PA Bulletin, Doc. No.14-2076 Notice – Method of Filing; PA Directory ofCorporate Partners Return, PA-65 Corp.

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 6

www.revenue.pa.gov

3.2. ACCEPTED PENNSYLVANIA PARTNERSHIP FORMS AND SCHEDULES

The following are the Pennsylvania partnershipforms and schedules that will be accepted for taxyear 2014 in XML format. The appropriate XMLschemas for these forms are on the department’swebsite, www.revenue.pa.gov.

3.3. SCHEDULE CHANGES AND ADDITIONS

PA-20S/PA-65 Information Return(Page 3, Part X)An e-file opt-out oval was added for entities thatrequest their preparers to file the PA-20S/PA-65Information Return in paper format.

PA-20S/PA-65 Schedule I Amortization ofIntangible Drilling CostsThis is a new schedule for reporting the currentyear deduction of Intangible Drilling Costs (IDCs).

PA-20S/PA-65 Schedule M(Part B, Section E, Line b)Revised line entry to read “Differences indepreciation/amortization taken for PA andfederal purposes”.

PA-20S/PA-65 Schedule M(Part B, Section F, Line c)Revised line entry to read “Differences indepreciation/amortization taken for PA andfederal purposes”.

PA-20S/PA-65 Schedule M(Part B, Section F, Lines h and i)Moved line “h” to line “i”. Replaced line “h” with:“Current Expensing of Intangible Drilling Costs”.

PA-65 CorpAdded “100% Corp. Owned” fill-in oval to identifypartnerships with only corporate partners. Added“payment enclosed” fill-in oval when payments aresubmitted with the form.

PA-20S/PA-65 PA S Corporation/PartnershipInformation Return

Partner/Member/ Partner/Member/ShareholderShareholder DirectoryDirectory

PA Schedule D-I Sale, Exchange or Disposition ofProperty Within PA

PA Schedule D-II Sale, Exchange or Disposition ofProperty Within PA

PA Schedule D-III Sale, Exchange or Disposition ofProperty Outside PA

PA Schedule D-IV Sale, Exchange or Disposition ofProperty Outside PA

PA Schedule E Rent and Royalty Income (Loss)

PA Schedule RK-1 Resident Schedule ofShareholder/Partner/Beneficiary PassThrough Income, Loss and Credits

PA Schedule NRK-1 Nonresident Schedule ofShareholder/Partner/Beneficiary PassThrough Income, Loss and Credits

PA Schedule M Reconciliation of Federal TaxableIncome (Loss) to PA taxable Income(Loss) – Part A

Reconciliation of Federal TaxableIncome (Loss) to PA taxable Income(Loss) – Part B

PA Schedule OC Other Credits

PA Schedule H-Corp Corporate Partner ApportionedBusiness Income (Loss)

PA-65 Corp Directory of Corporate Partners

PA Schedule CP Corporate Partner Withholding

PA Schedule A Interest Income

PA Schedule B Dividend and Capital GainsDistribution Income

PA Schedule H Apportioned Business Income (Loss)Calculation of PA Net BusinessIncome (Loss)

PA Schedule NW Nonresident Withholding PaymentsPA S Corporation and Partnerships

PA Schedule J Income from Estates or Trusts

PA Schedule T Gambling and Lottery Winnings

PA Schedule I Amortization of Intangible DrillingCosts

PA KOZ PS Schedule P-S KOZ(Keystone Opportunity Zone)

PA-65 ESR Estimated Withholding Tax forNonresident Owners

REV-276 Application for Extension to File

Page 7

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

PA-20S/PA-65 Schedule NW (Lines C and D)Moved Line C to Line D and changed the wordingfor Line D to read: “Reconciliation Payment.Subtract B and C from A, and enter here and onthe PA-20S/PA-65 Information Return”. Line C nowreads: “Payment remitted with the PA-40NRC,Nonresident Consolidated Tax Return, if allnonresident individual owners elect to participatein a group return”.

PA-20S/PA-65 Schedule OCAdded new Line 6 for the PA Organ and BoneMarrow Tax Credit. Lines 7 through 16 shifteddownwards.

Accepted PDF FormsBelow are Pennsylvania forms and schedules thatwill be accepted for tax year 2014 as binaryattachments in PDF format. When naming binaryattachments in PDF format, tax preparationsoftware must use the names noted below.

For Pennsylvania forms and schedules notidentified above, tax preparation software mustnote “PAMiscStateAttachment” as the file name.

Miscellaneous PDF files cannot exceed 60 MB. Ifadditional miscellaneous files are needed, usenumeric labeling at the end of file name. Forexample, PAMiscStateAttachment2

Note: A single-member limited liabilitycompany (SMLLC), as a disregarded entity(a branch or division), reports income on theparent RCT-101 or PA-20S/PA-65 InformationReturn. Such an entity e-filing the RCT-101for capital stock/foreign franchise taxand/or loans tax can attach in PDF format apro forma separate company federal Form1120S or 1065 and may e-file as a separatestate submission.

3.4. EXCLUSIONS TO ELECTRONIC FILING

The following Pennsylvania partnership forms andschedules cannot be filed electronically throughFed/State e-File:

• PA-20S/PA-65, PA SCorporation/Partnership Information Returnfor tax periods prior to 2012.

• PA-20S/PA-65, PA SCorporation/Partnership InformationAmended Return for tax years prior to 2012.

• PA-40 NRC, Nonresident ConsolidatedIncome Tax Return

• PA Schedule NRC-I, Directory ofNonresident Owners – Individuals

• PA-65 Corp, Directory of CorporatePartners – Only if the entity chooses topay via check instead of ACH. Ifsubmitting payment by check instead ofACH for corporate partner(s), the PA-65Corp must be attached as a paymentvoucher with the check.

• Debits from financial institutions outsideof the territorial jurisdiction of the U.S.

• The PA-20S/PA-65 is an information returnthat does not provide the option forrequesting a refund or carry-forward ofoverpayments. If the overpaid amount isnot passed through to the nonresidentindividual, estate or trust on therespective PA Schedule NRK-1, or claimedon a PA-40 Nonresident ConsolidatedIncome Tax Return, then the entity mustsend a written request to:

PA DEPARTMENT OF REVENUEBUREAU OF INDIVIDUAL TAXES PO BOX 280509HARRISBURG PA 17128-0509

The request must be on company letterhead andinclude the entity’s name, tax year, Social Securitynumber(s) of the owner(s), amount of nonresidentwithholding paid, amount of nonresidentwithholding tax liability, the requested refundamount and/or carry forward to the next year ofnonresident withholding and reason for request.Direct deposit is not an option.

3.5. SIGNATURE REQUIREMENTSAn electronic PA S Corporation/PartnershipInformation Return (PA-20S/PA-65) must be

Federal Form 3115 Application for FF3115.PDFChange in Accounting Method

Federal Form 8824 Like-Kind FF8824.PDFExchanges

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 8

www.revenue.pa.gov

signed by a general partner, principal officer orauthorized individual and in addition by the paidpreparer, if applicable. Two signature options areavailable, as described below.

• The federal self-select PIN option - Thisoption consists of two PINs, one for thetaxpayer and one for the practitioner. Inorder for the department to accept thefederal self-select PIN as a signature,software developers must display ajurat/disclosure statement, similar to thelanguage on the PA-8879-P, Page 3,Electronic Signature Specifications andmeeting the requirements of 72 P.S. §7333 and 61 Pa. Code § 121.23. Taxpayersand EROs must complete PA-8879-P,Pennsylvania e-File Signature Authorizationfor PA S Corporation/PartnershipInformation Return (PA-20S/PA-65) –Directory Of Corporate Partners (PA-65Corp), when using this method andconsenting to electronic funds withdrawals.The department requires EROs to retaincompleted PA-8879-P forms for three yearsafter the due dates of the returns or thedates the returns were filed electronically,whichever is later.

• If a taxpayer elects not to use the federalself-select PIN option, or if the statesubmission is filed as a state stand-alonereturn which means there is no link to anoriginal federal submission, the departmentrequires the ERO to complete PA-8453-P,PA S Corporation/Partnership InformationReturn (PA-20S/PA-65) – Directory OfCorporate Partners (PA-65 Corp) TaxDeclaration For A State e-File Return, andretain it for three years after the due dateof the returns or the date the returns werefiled electronically, whichever is later.PA-8453-P must be completed and signedby all appropriate parties before the returnis transmitted electronically.

In the event the department selects anelectronic return for examination, the EROmay be required to provide PA-8879-P and,if appropriate, PA-8453-P, within fivebusiness days of the request. A percentageof these forms will be randomly requested

yearly for monitoring compliance. Do notmail these forms to the department unlessrequested by the department.

3.6. PAYMENT OPTIONSThe only acceptable electronic payment methodfor Fed/State Partnership e-File is electronicfunds withdrawal, which is part of the currenttax year return submission and is automaticallyand electronically transferred from taxpayers’bank accounts. Beginning with the 2015 filingseason, the department will accept a finalcatch-up payment for nonresident individualsfiled with an extension using the REV-276.

The following types of payments can beelectronically transferred if filed throughFed/State e-File:

For the PA-20S/PA-65 Information Return• Final nonresident individual tax

withholding “catch-up” paymentsubmitted with the 2014 tax year return;and

• 2015 (future) estimated payments fornonresident individual quarterly taxwithholding submitted with the 2014 taxyear return.

• Capital stock/foreign franchise taxpayments if an RCT-101 is filed with thePA-20S/PA-65 Information Return.

• PA-65ESR Quarterly Estimated Paymentsfor nonresident individuals.

Future estimated nonresident individual taxwithholding payments for tax year 2015 will bestored in the system as separate electronictransaction payments until the specified due date.The nonresident individual quarterly taxwithholding payment may not be submittedthrough electronic funds transfer, credit/debitcards or e-TIDES.

The nonresident individual quarterly taxwithholding payment may not be submittedthrough electronic funds transfer, credit/debitcards or e-TIDES.

Electronic Funds WithdrawalPayments made by this method are part ofthe state submission and are automatically

Page 9

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

and electronically transferred fromtaxpayers’ bank account. The taxpayermust provide the ERO with appropriatebank account numbers, routing numbers,account types (checking or savings),payment amounts and dates to havepayments debited (normally thereturn/report due date). This allows thetaxpayer to pay the balance due as soon asthe return/report is processed or to pay thebalance due on a future date, should thetaxpayer want to file early but pay closer tothe due date. The ERO should cautiontaxpayers to ensure their financialinstitutions allow electronic fundswithdrawal from designated accountsbefore e-filing.

Check and 2014 NonresidentWithholding Payment SubstituteVoucherPayments remitted by check must beaccompanied by the 2014 NonresidentWithholding Payment Substitute Voucher.Software vendors that will include thevoucher in software must have the voucherapproved by the department.

If a state submission containing anelectronic funds withdrawal payment isrejected by the IRS or department, thetaxpayer is still required to remit thebalance due by the original return due dateof the return/report. Any balance due notpaid by the original return due date will besubject to interest and penalty fees.

Payment for corporate net income taxshould be included with the PA-65 Corp,Directory of Corporate Partners, portion ofthe transmission.

For the PA-65 Corp, Directory of Corporate PartnersCorporate net income tax withholding paymentson behalf of nonfiling corporate owner(s).

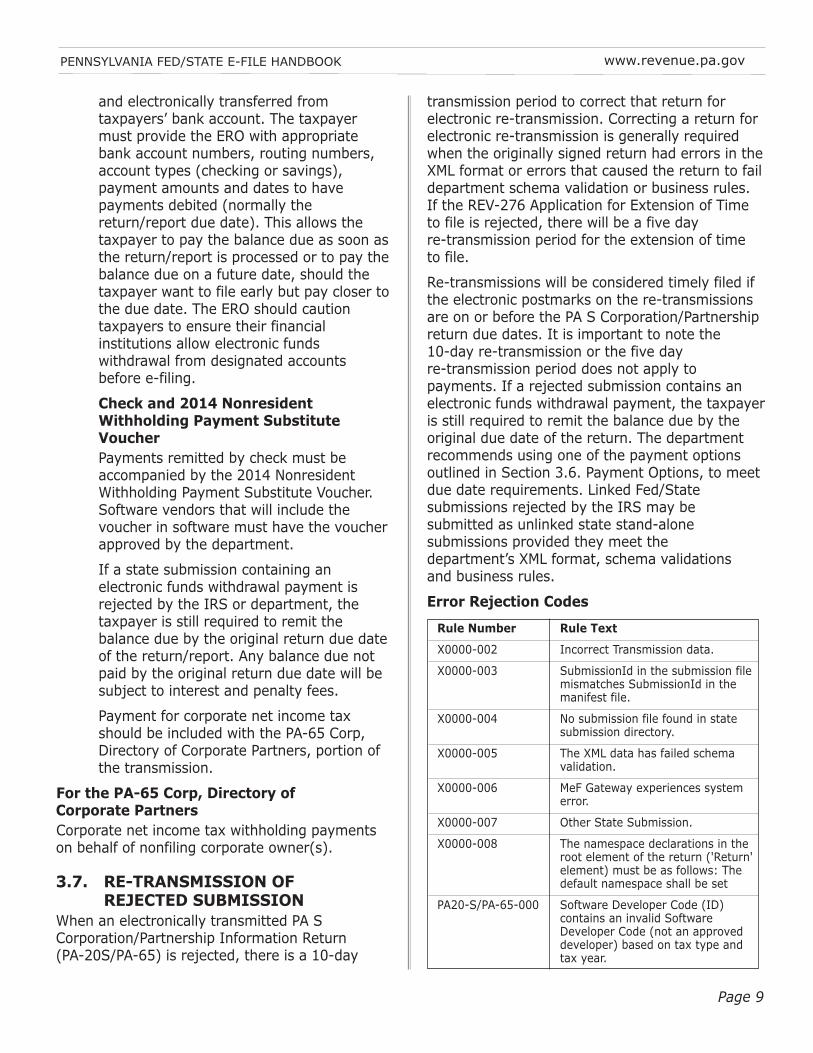

3.7. RE-TRANSMISSION OF REJECTED SUBMISSION

When an electronically transmitted PA SCorporation/Partnership Information Return(PA-20S/PA-65) is rejected, there is a 10-day

transmission period to correct that return forelectronic re-transmission. Correcting a return forelectronic re-transmission is generally requiredwhen the originally signed return had errors in theXML format or errors that caused the return to faildepartment schema validation or business rules.If the REV-276 Application for Extension of Timeto file is rejected, there will be a five dayre-transmission period for the extension of timeto file.

Re-transmissions will be considered timely filed ifthe electronic postmarks on the re-transmissionsare on or before the PA S Corporation/Partnershipreturn due dates. It is important to note the10-day re-transmission or the five dayre-transmission period does not apply topayments. If a rejected submission contains anelectronic funds withdrawal payment, the taxpayeris still required to remit the balance due by theoriginal due date of the return. The departmentrecommends using one of the payment optionsoutlined in Section 3.6. Payment Options, to meetdue date requirements. Linked Fed/Statesubmissions rejected by the IRS may besubmitted as unlinked state stand-alonesubmissions provided they meet thedepartment’s XML format, schema validationsand business rules.

Error Rejection Codes

Rule Number Rule Text

X0000-002 Incorrect Transmission data.

X0000-003 SubmissionId in the submission filemismatches SubmissionId in themanifest file.

X0000-004 No submission file found in statesubmission directory.

X0000-005 The XML data has failed schemavalidation.

X0000-006 MeF Gateway experiences systemerror.

X0000-007 Other State Submission.

X0000-008 The namespace declarations in theroot element of the return ('Return'element) must be as follows: Thedefault namespace shall be set

PA20-S/PA-65-000 Software Developer Code (ID)contains an invalid SoftwareDeveloper Code (not an approveddeveloper) based on tax type andtax year.

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 10

www.revenue.pa.gov

The PA Department of Revenue follows the sameguidelines as the IRS for a rejected submission. Ifa submission was rejected, a return can becorrected within 10 days and the received date ofthe original rejected return will be honored.

Important: The 10-day re-transmissionperiod is not an extension of time to file. It isa period of time to correct errors in theelectronic file. The 10-day re-transmissionperiod applies to business returns filed onMeF, regardless of the date filed, due date orextended due date.

Common Errors to Avoid Address on Schedule E property(ies) must becomplete, including the following:

• Address Line 1• Address Line 2 (optional)• City• State• ZIP code

Rule Number Rule Text

PA20-S/PA-65-001 PA 20-S/PA-65 return waspreviously filed through MeF

PA20-S/PA-65-002 Total Corporate Net Income taxWithholding is greater than zeroand a payment is not present.

PA20-S/PA-65-003 Net Gain (Loss) from PA ScheduleD, Line 5, Column A or B on thePA20S/65 are present andSchedules D-1 through IV are notincluded with the filing.

PA20-S/PA-65-004 Rent/Royalty Net Income (Loss)Line 6, Column A or B on thePA20S/65 are present and ScheduleE is not included with the filing.

PA20-S/PA-65-005 The State Field in Part A, Lines A,B, C or D of the Schedule E are notpresent.

PA20-S/PA-65-006 Invalid Requested Payment Date.If a payment is present, theRequested Payment Date must bepresent. The Requested paymentdate must be a valid date andcannot be greater than 365 daysafter the IRS Time Stamp Date.

PA20-S/PA-65-007 Missing required forms for returntype

PA20-S/PA-65-008 Invalid State EIN. If State EIN ispresent, it must be 7 or 10 digitsin length and only contain numericcharacters.

PA20-S/PA-65-009 Business Name Line 1 must bepresent, left justified and must notcontain any special characters otherthan a hyphen or more than oneconsecutive space.

PA20-S/PA-65-010 If Business Name Line 2 is present,it must be left justified and cannotcontain any special characters otherthan a hyphen or more than oneconsecutive space.

PA20-S/PA-65-011 Payment Amount does not equalvalues entered in the sub amounttype fields in addenda record.

PA20-S/PA-65-012 Only one sub amount type fieldequaling "C" is allowed.

PA20-S/PA-65-013 All Financial Transaction paymentsmust include an Addenda Recordwith SubAmountType.

PA20-S/PA-65-015 Invalid payment type. A subamount type of "P" is not validunless a PA-65 Corp is present.

Rule Number Rule Text

PA20-S/PA-65-016 Invalid payment type. A subamount type of "A" is not validunless a PA20-S/PA-65 or a PA65ESR is present.

PA20-S/PA-65-017 Invalid payment type. A subamount type of "C" is not validunless an RCT-101, RCT-101I orREV-853R is present.

PA20-S/PA-65-018 State Schema Version must bepresent.

PA20-S/PA-65-019 Bank Account Number and RoutingNumber cannot be the same

PA20-S/PA-65-020 Tax year in the submission fileddoes not match tax year in themanifest file

PA65ESR-001 Invalid payment type. Thesubmission cannot contain a Statepayment.

PA65ESR-002 Missing payment. The submissionmust contain at least one EstimatedPayment.

PA65EXT-001 Invalid payment type. Thesubmission cannot containEstimated Payments

Page 11

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

3.8. EXTENSION OF TIME TO FILETaxpayers who have balances due must pay themby the original due date of the return in order toavoid interest and penalties. REV-276, Applicationfor Extension of Time to File, can extend the filingdue date up to five months for filing the PA SCorporation/Partnership Information Return(PA-20S/PA-65) but it does not extend the timefor full payment of the catch-up nonresidentwithholding tax payment deadline. Taxpayers filingfor an extension should file in sufficient time forthe PA Department of Revenue to consider and actupon it. Beginning with the 2015 filing season, theREV-276 may be filed through the MeF Fed/Statee-file program.Fill in the “Extension Requested” oval at the top ofthe PA-20S/PA-65 Information Return.

• If the entity did not file REV-276,Application for Extension of Time to File,in paper form and has requested anextension for the federal return, include acopy of federal Form 7004 with thePA-20S/PA-65 Information Return as aPDF attachment.

• If the entity electronically filed a federalextension, include a statement as aPDF attachment.

• If the entity submitted REV-276,Application for Extension of Time to File,in paper form, it should not submit acopy of the extension paperworkwith the electronic PA-20S/PA-65Information Return and if a payment isdue, payment should be in paper checkform only.

Important: There is no extension of time tofile the PA-65 Corp, Directory of CorporatePartners. The PA-65 Corp is a paymentvoucher for withholding corporate net incometax for nonfiling corporate partners whichindicates how much was withheld for eachcorporate partner. It is not a tax return andtherefore has no extension provision.

SECTION 4. CORPORATE E-FILE4.1. WHAT’S NEW Loans tax was repealed for tax years beginning onor after Jan. 1, 2014.

The electronic funds transfer requirement wasreduced from $10,000 to $1,000 for all paymentsmade after Dec. 31, 2013.Corporations filing a report for any of theconditions listed below must file a paper form,RCT-101. To ensure timely processing of thereport, please mail to the address below.Examples of reports having special handlingstatus:NOTE: This list may not be all inclusive.

• Corporations requesting Extra StatutoryTreatment

• Corporations with two distinct activities(Warehousing/Trucking & DistributionTrucking); (Persons/Transportation &Property/Transportation)

• Regulated Investment Companies (RIC)• Corporations having Net Operating Loss

(NOL) limitations under IRC Section 381and IRC Section 382

PA DEPARTMENT OF REVENUEBUREAU OF CORPORATION TAXESP O BOX 280704HARRISBURG, PA 17128-0704

4.2. ACCEPTED PENNSYLVANIA CORPORATE FORMS AND SCHEDULES

RCT-101 PA Corporate Tax Report is used for boththe Original and Amended Tax Report

RCT-101I PA Corporate Inactive Report

RCT-102 Capital Stock ManufacturingExemption Schedule

RCT-103 Net Operating Loss Schedule

RCT-105 Three Factor Capital Stock/Foreign FranchiseTax Manufacturing Exemption Schedule

REV-106 Three Factor Apportionment orSpecial Apportionment Insert Sheet

REV-798 Schedule C-2 PA Dividend DeductionSchedule, Schedule X

REV-799 Schedule C-3 Adjustment for BonusDepreciation, Schedule C-4 Adjustment forDisposition of Section 168(k) Property &Recapture of Depreciation on Listed Property

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 12

www.revenue.pa.gov

4.3. SCHEDULE CHANGES AND ADDITIONS

• Loans Tax has been repealed. See“What’s New” on this page for moreinformation.

4.4. EXCLUSIONS TO ELECTRONIC FILING

The following Pennsylvania corporate forms cannotbe filed electronically through Fed/State Corporatee-File:

• RCT-101D Declaration of de minimisPennsylvania activity

• Consolidated Tax Returns: PA statutedoes not allow for consolidatedRCT-101s to be electronically filed.

4.5. SIGNATURE REQUIREMENTSAn electronic PA Corporate Tax Report, RCT-101,must be signed by an authorized corporate officerand in addition, by the paid preparer, if applicable.Two signature options for signing electronicreports are available.

• The federal self-select PIN option - Thisoption consists of two PINs, one for thetaxpayer and one for the practitioner. In

order for the department to accept thefederal self-select PIN as an acceptablesignature, software developers mustdisplay a jurat/disclosure statement,similar to the language on the PA-8453-C.Taxpayers and EROs must completePA-8879-C, PA e-File SignatureAuthorizations when using the federalself-select PIN method and consenting toelectronic funds withdrawals. Thedepartment requires EROs to retaincompleted PA-8879-C for three yearsafter the due dates of the return/reportsor the dates the return/reports were filedelectronically, whichever dates are later.The ERO must retain PA-8879-C.

• If a taxpayer elects not to use the federalself-select PIN option or if the statesubmission is filed as a state stand-alone(no link to an original federal submission),the department requires the ERO to retaina completed PA-8453-C for three yearsafter the due date of the return/reports orthe date the return/reports were filedelectronically, whichever is later. The EROmust retain PA-8453-C. PA-8453-C mustbe completed and signed by allappropriate parties before the return istransmitted electronically.

In the event the department selects an electronicreturn/report for examination, the ERO may berequired to provide PA-8879-C and, ifappropriate, PA-8453-C, within five businessdays from the date of the request. In addition, apercentage of these forms will be randomlyrequested yearly for monitoring compliance. Donot mail these forms to the department unlessrequested by the department.

4.6. PAYMENT OPTIONSTaxpayers may choose to pay tax due using oneof the methods outlined below. Tax payments of$1,000 or more are required by law to beremitted electronically. Failure to comply with thisrequirement may result in the assessment of apenalty equal to 3 percent of the total tax due,not to exceed $500. For purposes ofenforcement, “total tax due” is thepayment/remittance amount. Electronic funds

REV-860 Schedule L Balance Sheets, Schedule M-1Reconciliation of Income, Schedule M-2Reconciliation of Member’s Capital Account,C-5 Schedule of Taxes, Schedule OtherAdditions, Schedule Other Deductions

REV-861 Schedule DA Disposition of Assets

REV-934 Non-Business Income Schedule

REV-961 Schedule A-2 Reconciliation forRetained Earnings of a FederalSubchapter S Corporation

REV-961 Schedule A-3 Adjustment to Net IncomePer Books

REV-986 Schedule to support claim of Exemptionfrom Corporate Net Income Tax

REV-853 PA Corporation Taxes Annual ExtensionRequest

REV-857 Corporate Estimated Tax Payments

REV-1175 Explanation for Filing an Amended PACorporation Taxes Report Schedule

Page 13

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

withdrawal, electronic funds transfer (EFT) andcredit/debit cards qualify as acceptable electronicpayment methods.

Electronic Funds WithdrawalPayments made by this method are part ofthe state submission and are automaticallyand electronically transferred fromtaxpayers’ bank accounts. The taxpayermust provide the ERO with appropriatebank account numbers, routing numbers,account types (checking or savings),payment amounts and dates they wish tohave payments debited (normally thereturn/report due date). This allows thetaxpayer to pay the tax due as soon as thereturns/reports are processed or in thefuture, should taxpayers want to file earlybut pay closer to due dates. The ERO shouldcaution taxpayers to ensure their financialinstitutions allow electronic fundswithdrawal from designated accountsbefore e-filing.

Electronic Funds Transfer (EFT) Payments made through EFT such as ACHdebit, ACH credit/debit and certifiedcashier’s check, are made outside theFed/State e-File Program. Registration isrequired to make payments electronicallythrough EFT. More information on makingpayments via EFT can be found on thedepartment’s website at:www.revenue.pa.gov.

Credit/Debit CardPayments by credit/debit card are madeoutside the Fed/State Corporate e-FileProgram. You can pay your Pennsylvaniataxes with a major credit or debit card.Credit card transactions are charged a 2.49percent convenience fee ($1 minimumcharge), and debit card transaction feesstart at $3.95. You can use your AmericanExpress, Discover, MasterCard or Visa creditcard to pay your taxes online or by phone.You may also use a MasterCard or Visadebit card to make payments online. Selectone of these options to pay using yourcredit/debit card:

Internet: Go to Official PaymentsCorporation at www.officialpayments.com

Telephone: Call 1-800-2PAYTAX (1-800-272-9829)

Check and CT-V, PA Corporation TaxesFed/State Payment Voucher Payments remitted by check must beaccompanied by the CT-V, PA CorporationTaxes Fed/State Payment Voucher. Softwarevendors that will include the voucher insoftware must have the voucher approvedby the department.

If a state submission containing anelectronic funds withdrawal payment isrejected by the IRS or department, thetaxpayer is still required to remit thebalance due by the original due date of thereturn/report. In this situation, a paymentcan be remitted through EFT, by credit/debitcard, or if the payment is less than$10,000, by check and accompanyingpayment voucher. Any balance due not paidby the original return due date will besubject to interest and penalty fees.

4.7. RE-TRANSMISSION OF REJECTED SUBMISSIONS

Taxpayers choosing to resubmit submissionsrejected by the IRS or the department mustcorrect and retransmit their electronicreturn/reports. Resubmissions will be consideredtimely filed if the electronic postmarks on theresubmissions are on or before the applicablePennsylvania corporate tax due dates. If arejected submission contains an electronic fundswithdrawal payment, the taxpayer is required toremit the balance due by the original due date ofthe return/report. The department recommendsusing one of the payment options outlined inSection 4.6 Payment Options, to meet due daterequirements. Linked Fed/State submissions thatare rejected by the IRS may be submitted as anunlinked state stand-alone submission providedthe requirements and specifications provided bythe department are met.

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 14

www.revenue.pa.gov

Error Rejection Codes

Rule Number Rule Text

X0000-002 Incorrect Transmission data.

X0000-003 SubmissionId in the submission filemismatches SubmissionId in themanifest file.

X0000-004 No submission file found in statesubmission directory.

X0000-005 The XML data has failed schemavalidation.

X0000-006 MeF Gateway experiences systemerror.

X0000-007 Other State Submission.

X0000-008 The namespace declarations in theroot element of the return ('Return'element) must be as follows:Thedefault namespace shall be set.

PA1120-000 Software Developer Code (ID)contains an invalid SoftwareDeveloper Code (not an approveddeveloper) based on tax type andtax year.

PA1120-002 Invalid State EIN. If State EIN ispresent, it must be 7 or 10 digits inlength and only contain numericcharacters.

PA1120-006 Invalid Requested Payment Date.If a payment is present, theRequested Payment Date must bepresent. The Requested paymentdate must be a valid date andcannot be greater than 365 daysafter the IRS Time Stamp Date.

PA1120-011 Payment Amount does not equalvalues entered in the sub amounttype fields in addenda record.

PA1120-012 Only One sub amount type fieldequaling C is allowed.

PA1120-013 All Financial Transaction paymentsmust include an Addenda Recordwith SubAmountType.

PA1120-015 Invalid payment type. A subamount type of "P" is not validunless a PA-65 Corp is present.

PA1120-016 Invalid payment type. A subamount type of "A" is not validunless a PA20-S/PA-65 or a PA65ESR is present.

PA1120-017 Invalid payment type. A subamount type of "C" is not validunless a RCT-101, a RCT-101I oran REV-853R is present.

PA1120-018 State Schema Version must bepresent.

Rule Number Rule Text

PA1120-019 Bank account Number and RoutingNumber cannot be the same. Bankaccount Number and RoutingNumber cannot be the same.

PA1120-020 Tax year in the submission filedoes not match tax year in themanifest file.

PA20-S/PA-65-001 PA 20-S/PA-65 return waspreviously filed through MeF.

PA20-S/PA-65-002 Total Corporate Net Income taxWithholding is greater than zeroand a payment is not present.

PA20-S/PA-65-003 Net Gain (Loss) from PA ScheduleD, Line 5, Column A or B on thePA20S/65 are present andSchedules D-1 through IV are notincluded with the filing.

PA20-S/PA-65-004 Rent/Royalty Net Income (Loss)Line 6, Column A or B on thePA20S/65 are present andSchedule E is not included withthe filing.

PA20-S/PA-65-005 The State Field in Part A, Lines A,B, C or D of the Schedule E arenot present.

PA20-S/PA-65-006 Invalid Debit Payment Date. IfDebit Payment is present, theDirect Debit Date must be present.If a Direct Debit Payment ispresent then the Direct Debit Datemust be greater than or equal tothe IRS Time Stamp Date minus 3and it must be a valid date.

PA20-S/PA-65-007 Missing required forms for returntype.

PA20-S/PA-65-009 Business Name Line 1 must bepresent, left justified and must notcontain any special charactersother than a hyphen or more thanone consecutive space.

PA20-S/PA-65-010 If Business Name Line 2 is present,it must be left justified and cannotcontain any special charactersother than a hyphen or more thanone consecutive space.

PA20-S/PA-65-015 Invalid payment type. A subamount type of "P" is not validunless a PA-65 Corp is present.

PA20-S/PA-65-016 Invalid payment type. A subamount type of "A" is not validunless a PA20-S/PA-65 or a PA65ESR is present.

PA20-S/PA-65-017 Invalid payment type. A subamount type of "C" is not validunless a RCT-101, a RCT-101I oran REV-853R is present.

Page 15

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

4.8. EXTENSION OF TIME TO FILETaxpayers granted an extension to file the federalincome tax return will automatically be grantedan extension to file the PA Corporate Report,RCT-101. Corporate taxpayers granted a federalextension must indicate this on Page 1 of theRCT-101 and include a copy of the federalextension request with the report.

SECTION 5. INDIVIDUAL INCOME E-FILE5.1. ACCEPTED PENNSYLVANIA

INDIVIDUAL INCOME TAX FORMS AND SCHEDULES

The following Pennsylvania individual income taxforms and schedules may be transmittedelectronically (refund, equal and balance due, withor without payment), and payment must be madeby electronic funds withdrawal, check, moneyorder or credit/debit card.

5.2. SCHEDULE CHANGES AND ADDITIONS

Changes to the PA-40 and PA-40 Schedules:• PA-40, Lines 32 through 36 – Donation

organization names were removed andcode boxes were added to the lines toallow taxpayers to select an alphadonation code for up to five of theseven donation organizations.

• Schedule A was revised to alter therequirements of what to report and whenthe schedule is required to be includedwith the return. Schedule A now startswith the federal interest income andrequires taxpayers to adjust that number

Rule Number Rule Text

PA65ESR-001 Invalid payment type. Thesubmission cannot contain a Statepayment.

PA65ESR-002 Missing payment. The submissionmust contain at least oneEstimated Payment.

PA-40 Pennsylvania Individual IncomeTax Return (includes nonresidentand part-year resident returns)

PA-40 Schedule A Interest (3 schedules or less)

PA-40 Schedule B Dividends (3 schedules or less)

PA-40 Schedule C Profit or Loss From Business orProfession (10 schedules or less)

PA-40 Schedule D Sale, Exchange or Disposition ofProperty (3 schedules or less)

PA-40 Schedule D-1 Computation of Installment SaleIncome (6 schedules or less)

PA-40 Schedule D-71 Sale or Exchange of PropertyPrior to June 1, 1971(3 schedules or less)

PA-40 Schedule E Rent, Royalty, Patent andCopyright Income or Loss(10 schedules or less)

PA-40 Schedule F Farm Income and Expenses(2 schedules or less)

PA-40 Schedule G-L Out-of-State Credit, Long Form(43 schedules or less)

PA-40 Schedule J Estate & Trust Income

PA-40 Schedule W-2S Wage Statement Summary(5 schedules or less)

PA-40 Schedule SP Tax Forgiveness Credit(1 schedule)

PA Schedule RK-1 Resident Schedule ofShareholder/Partner/BeneficiaryPass Through Income, Loss andCredits (100 schedules or less)

PA Schedule NRK-1 Nonresident Schedule ofShareholder/Partner/BeneficiaryPass Through Income, Loss andCredits (100 schedules or less)

PA-40 Schedule UE Allowable Employee BusinessExpenses (10 schedules or less)

PA-40 Schedule OC Other Credits (1 schedule)

PA-40 Schedule O Other Deductions (1 schedule)

PA-40 Schedule T Gambling and Lottery Winnings(1 schedule)

REV-1630 Underpayment of Estimated Taxby Individuals (1 schedule)

REV-1630A Underpayment of Estimated Taxby Farmers (1 schedule)

PA-40 Schedule 19 Sale of a Principal Residence(1 schedule)

PA-40 Schedule NRH Apportioning Income byNonresident Individuals(10 schedules or less)

Schedule PA-40X Amended Schedule(1 schedule)

REV-276 Extension of Time to File

REV-459B Consent to Transfer, Adjust orCorrect PA Estimated PersonalIncome Tax Account

W-2 RW PA W-2 Reconciliation Worksheet

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 16

www.revenue.pa.gov

to the PA interest income amount via aseries of additions and subtractions.Schedule A is required regardless of theamount of income reported on theschedule if any amounts appear onLines 2 through 15.

• Schedule B was revised to alter therequirements of what to report and whenthe schedule is required to be includedwith the return. Schedule B now startswith the federal dividend income andrequires taxpayers to adjust that numberto the PA dividend and capital gainsdistributions income amount via a seriesof additions and subtractions. Schedule Bis required regardless of the amount ofincome reported on the schedule if anyamounts appear on Lines 2 through 9.

• Schedules C-EZ, G-R and G-S have beendiscontinued or eliminated.

• Schedule C – Three new lines were addedto the Schedule C, they are Line 34,Line 35 and Line 36.

• REV-276 Extension may now beelectronically filed.

• PA-40 W-2 RW – PA W-2 ReconciliationWorksheet may now to be electronicallyfiled.

• REV-459B – Consent to Transfer, Adjustor Correct PA Estimated Personal IncomeTax Account may now be electronicallyfiled.

5.3. EXCLUSIONS TO ELECTRONIC FILING

The following Pennsylvania forms/schedulescannot be filed electronically throughFed/State e-File:

• Non-calendar, fiscal-year returns;

• Amended individual income tax returnsfor years prior to 2010;

• Form PA-40NRC - NonresidentConsolidated Income Tax Returns;

• Form PA-40 KOZ - Pennsylvania IncomeTax Keystone Opportunity Zone Return;

• Returns containing more than theallowable amounts of Federal forms; and

• Returns containing forms/schedules notlisted under “Accepted PennsylvaniaForms/Schedules.”

5.4. SIGNATURE REQUIREMENTSThe department accepts the federal self-select PINand the federal practitioner PIN as valid signatureson Pennsylvania returns filed through theFed/State e-File Program. In order for thedepartment to accept the federal self-select PIN, itrequires software developers to display ajurat/disclosure statement, similar to the languageon PA-8453, Pennsylvania Individual Income TaxDeclaration for Electronic Filing, in the softwareprogram when taxpayers elect the federal PINoption for signatures.

When a valid PIN is entered as the signature, thedepartment does not require taxpayers tocomplete PA-8453 form. If the IRS does notaccept the PIN, PA-8453 form must be completedand signed. If a taxpayer is not present to enterhis/her PIN or if the practitioner PIN is used tosign the return, a PA-8879 form must becompleted and signed by the taxpayer. Thecompleted and signed PA-8879 form must beretained in the practitioner’s file for three yearsfrom the return due date.

Note: Federal self-select PINS may not beused as valid signatures on amended returns.

5.5. REFUND OPTIONS AND DIRECT DEPOSIT

Taxpayers may elect to have 2014 refunds paid inone of the following ways:

• Remitted as a paper check; and

• Deposited into a financialinstitution account.

Taxpayers also have the option of distributingoverpayments as follows:

• Credit to the 2015 estimated tax account;

• Donation to the PA Breast CancerCoalition’s Breast and Cervical CancerResearch Fund;

• Donation to the Wild ResourceConservation Fund;

Page 17

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

• Donation to the Military Family ReliefAssistance Program;

• Donation to the Governor Robert P. CaseyMemorial Organ and Tissue DonationAwareness Trust Fund;

• Donation to the Juvenile (Type 1)Diabetes Cure Research Fund;

• Donation to PA Children’s Trust Fund;

• Donation to American Red Cross.

Direct DepositThe direct deposit option is available only forelectronically filed refund returns for tax year2014. Refunds by direct deposit are electronicallytransferred to the financial institution accountindicated in the Pennsylvania return record.

The federal Office of Foreign Assets Control hasimposed additional reporting requirements on allelectronic banking transactions that directlyinvolve a financial institution outside of theterritorial jurisdiction of the U.S. Thesetransactions are called international ACHtransactions (IAT) and include credit (directdeposit of refunds) transactions. Presently, thePennsylvania Department of Revenue does notsupport IAT. Taxpayers who instruct thedepartment to process electronic bankingtransactions on their behalf are certifying that thetransactions do not directly involve a financialinstitution outside of the territorial jurisdiction ofthe U.S. at any point in the process.

Note: The financial institution accounts intowhich the Pennsylvania refund and the IRSrefund are deposited may be different.Therefore, the state and federal routingtransit numbers (RTN) and deposit accountnumbers (DAN) may differ.

Requirements for Direct DepositThe department will refund an overpayment bydirect deposit to a taxpayer’s financial institution ifthe following requirements have been met:

• Taxpayer electronically filed returns; and

• Taxpayer provided acceptable proof of anestablished or existing account.

IRS Publication 1345 sets forth detailed eligibilityrequirements, responsibilities and instructions

governing tax preparers, transmitters and EROswho offer taxpayers the option of direct deposit.Those same rules, policies and procedures applywhen offering direct deposit on the state return.

Before authorizing a direct deposit, taxpayersshould confirm with their financial institutionsthat the institutions can accept directdeposit transactions.

Preparers and EROs must stress to taxpayers theimportance of supplying correct information,because the direct deposit election, RTN and DANmay not be changed once a return has beenacknowledged by the department.

Taxpayers usually receive refunds by directdeposit within four to five weeks of filingtheir returns.

If any of the following conditions exist, a papercheck will be issued:

• Invalid RTN or DAN; and/or

• Rejection by the receiving depositoryfinancial institution. Some financialinstitutions do not permit deposit of ajoint refund into an individual account.The department is not responsiblewhen a financial institution refuses adirect deposit.

The Pennsylvania acknowledgment only indicatesthe acceptance of the return at the department.It does not indicate proof that a refund check willbe issued or that a direct deposit will be honored.

5.6. PAYMENT OPTIONSThe taxpayer is responsible for submittingpayment due to the department by April 15, 2015.Following are three types of payment options thetaxpayer may elect to use:

Electronic Funds Withdrawal Electronic funds withdrawal is available forbalance-due returns for tax year 2014. Paymentsby electronic funds withdrawal are automaticallyand electronically transferred from the financialinstitution account indicated in the Pennsylvaniareturn record.

The federal Office of Foreign Assets Control hasimposed additional reporting requirements on allelectronic banking transactions that directly

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 18

www.revenue.pa.gov

involve a financial institution outside of theterritorial jurisdiction of the U.S. Thesetransactions are called international ACHtransactions (IAT) and include electronic debit (taxpayments) transactions. Presently, the departmentdoes not support IAT. Taxpayers who instruct thedepartment to process electronic bankingtransactions on their behalf are certifying that thetransactions do not directly involve a financialinstitution outside of the territorial jurisdiction ofthe U.S. at any point in the process.

The financial institution accounts from which thePennsylvania payment and the IRS payment arewithdrawn may be different. Therefore, the stateand federal RTN and DAN may differ.

Taxpayers who choose this option must providethe ERO with account numbers and routingnumbers for the qualified savings, checking orshare draft accounts. This information is bestobtained from official financial records, accountcards, checks or shared drafts that contain thetaxpayer’s name and address. The ERO shouldcaution taxpayers to determine, before they file,that their financial institutions support electronicfunds withdrawal requests.

Taxpayers must specify the bank accounts fromwhich they wish to have the balances paid and thedates on which the debits will be made. Thisallows taxpayers to pay the balances as soon asthe returns are processed or delay it to futuredates, not later than the return due dates. Forexample, the ERO may transmit the return inMarch, and the taxpayer can specify that the debitbe made on any specific day on or before April 15.The taxpayer does not have to do anything at alater date. For returns transmitted after April 15,the debit will be processed on the day theelectronic return is processed.

The ERO that collects already completed returns,including returns from drop-off collection pointsand from taxpayers who elect to pay balances dueby electronic funds withdrawals, should be carefulto ensure that all the information needed forelectronic funds withdrawal requests is included inthe returns. Taxpayers must provide all of thefollowing: routing number; account number; typeof account (checking or savings); date ofwithdrawal; and amount to be withdrawn. In

addition, the ERO must provide those taxpayerswith printouts of the electronic return data.

If the taxpayer does not provide all of the neededinformation, the ERO must contact the taxpayer. Ifthe ERO is unsuccessful in obtaining the electronicfunds withdrawal information, but the returns areotherwise complete, the ERO should proceed withthe transmission of the electronic return data tothe IRS. The ERO must notify the taxpayer(s), inwriting, that other arrangements must be made topay the balance due.

Revoking an Electronic FundsWithdrawal AuthorizationA taxpayer can revoke an electronic fundswithdrawal authorization by notifying the PADepartment of Revenue in writing no later thantwo business days prior to the debit date. Writtenrequests to revoke the electronic funds withdrawalmust include the taxpayer’s name, address, SSN,RTN, DAN and payment amount. Written requestscan be faxed to 717-772-9310 or emailed [email protected].

Requirement for Electronic Funds WithdrawalThe department will allow payment ofPennsylvania tax due from a taxpayer’s financialinstitution if the taxpayer provides acceptableproof of an established or existing account. IRSPublication 1345 sets forth detailed eligibilityrequirements, responsibilities and instructionsgoverning tax preparers, transmitters and EROsthat offer taxpayers the option of electronic fundswithdrawal. Those same rules, policies, andprocedures apply when offering an electronicpayment on the state return.

Preparing Taxpayers for Pennsylvania Electronic Funds WithdrawalBefore authorizing an electronic funds withdrawal,taxpayers should confirm with their financialinstitutions that the institutions can acceptelectronic funds withdrawals. The preparer andERO must stress to taxpayers the importance ofsupplying correct information, because theelectronic payment election, RTN and DAN maynot be changed once a return has beenacknowledged by the department. If any of thefollowing conditions exist, a paper check or money

Page 19

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

order will need to be issued by the taxpayer forpayment of Pennsylvania taxes:

• Invalid RTN or DAN;

• Invalid payment date selected; and/or

• Rejection by the taxpayer’s financialinstitution.

The Pennsylvania acknowledgment indicates theacceptance of the return at the department. Itdoes not indicate proof that an electronic paymentwill be honored by the taxpayer’s bank.

Checks or Money OrderA Pennsylvania payment voucher, PA-V, is includedin the taxpayer’s 2014 Pennsylvania personalincome tax booklet or the taxpayer’s paymentvoucher letter. The payment voucher must bemailed with the taxpayer’s check made payable tothe PA Department of Revenue to:

PA DEPARTMENT OF REVENUEPAYMENT ENCLOSED1 REVENUE PLACEHARRISBURG PA 17129-0001

If your tax preparation software prints a PA-Vfacsimile approved by the department, that PA-Vmay be used when no preprinted PA-V is available.Mail the PA-V and check to the above address.

In the event the taxpayer does not have apreprinted voucher and your software is unable toproduce a department-approved facsimile, makethe check or money order payable to department.Write the last four digits of the taxpayer’s SSN,"2014 PA-V" and the taxpayer’s daytime telephonenumber on the check or money order. If filing ajoint return, enter the last four digits of the SSNshown first on the return. The department willneed the last four digits of the SSN to accuratelyapply the payment.

Credit/Debit PaymentsYou can pay your Pennsylvania taxes with a majorcredit or debit card. Credit card transactions arecharged a 2.49 percent convenience fee ($1minimum charge), and debit card transaction feesstart at $3.95. You can use your AmericanExpress, Discover, MasterCard or Visa credit cardto pay your taxes online or by phone. You mayalso use a MasterCard or Visa debit card to make

payments online. Select one of these options topay using your credit/debit card:

Internet: Go to Official Payments Corporation atwww.officialpayments.com

Telephone: Call 1-800-2PAYTAX (1-800-272-9829)

Note: In addition to charging the balancedue on a credit or debit card, taxpayers cancharge estimated tax payments, extensionpayments and delinquent tax payments.

The ERO must inform taxpayers that payment oftaxes due must be made no later than April 15,2015. If the taxpayer does not make full paymentof income taxes due on or before April 17, anassessment will be sent requesting payment. Theassessment will indicate the tax due and interestand penalty for late payment.

5.7. RE-TRANSMISSION OF REJECTED SUBMISSIONS

When an electronically transmitted PA-40Individual Income Tax Return or REV-276.Application for Extension of Time to File, isrejected, there is a five-day transmission period tocorrect that return for electronic re-transmission.Correcting a return for electronic re-transmissionis generally required when the originally signedreturn had errors in the XML format or errors thatcaused the return to fail department schemavalidation or business rules.

Re-transmissions will be considered timely filed ifthe electronic postmarks on the re-transmissionsare on or before the PA-40 Individual Income taxReturn due dates. It is important to note thefive-day re-transmission period does not apply topayments. If a rejected submission contains anelectronic funds withdrawal payment, the taxpayeris still required to remit the balance due by theoriginal due date of the return. The departmentrecommends using one of the payment optionsoutlined in Section 5.6 Payment Options, tomeet due date requirements. Linked Fed/Statesubmissions rejected by the IRS may besubmitted as unlinked state stand-alonesubmissions provided they meet thedepartment’s XML format, schema validationsand business rules.

PENNSYLVANIA FED/STATE E-FILE HANDBOOK

Page 20

www.revenue.pa.gov

The PA Department of Revenue follows the sameguidelines as the IRS for a rejected submission.If a submission was rejected, a return can becorrected within five days and the received dateof the original rejected return will be honored.

Important: The five-day re-transmissionperiod is not an extension of time to file. It isa period of time to correct errors in theelectronic file. The five-day re-transmissionperiod applies to business returns filed onMeF, regardless of the date filed, due date orextended due date.

Error Rejection Codes

Rule Number Rule Text

PA40-005 Invalid Primary Filer First Name. PrimaryFirst Name must be present and leftjustified and must not contain anyspecial characters other than a hyphenor more than one consecutive space.

PA40-007 Invalid Filer's Address Line. Either PAAddress Line 1 or Foreign StreetAddress must be present and PAAddress Line 1 must not contain two ormore consecutive spaces, a period, or acomma.

PA40-008 Invalid Filer's Address City. Either thePA City or PA Foreign City or Provincemust be present and the PA city mustnot contain a character other than ahyphen, alpha, or an ampersand and itmust be left justified.

PA40-000 Software Developer Code (ID) containsan invalid Software Developer Code (notan approved developer) based on taxtype and tax year.

PA40-010 Invalid School District Code.

PA40-011 Invalid Unreimbursed EmployeeBusiness Expenses. If UnreimbursedEmployee Business Expenses arepresent then Gross Compensation mustbe present or if Unreimbursed EmployeeBusiness Expenses are present then thePA Schedule UE must be present.

PA40-012 Invalid Net Compensation. If NetCompensation is present andUnreimbursed Employee BusinessExpenses is less than or equal to GrossCompensation then the NetCompensation must be equal to theGross Compensation minusUnreimbursed Employee BusinessExpenses or if Net Compensation ispresent and Unreimbursed EmployeeBusiness Expenses is greater thanGross Compensation then the NetCompensation must be equal to '0'.

PA40-013 Invalid Total PA Taxable Income. TotalPA Taxable Income must be equal to thesum of Net Compensation; InterestIncome; Dividend and Capital GainsDistribution Income; Net Income or(loss) From the Operation of a Business,Profession or Farm; Net Gain or (loss)From the Sale, Exchange, or Dispositionof Property; Net Income or (loss) FromRents, Royalties, Patents, andCopyrights; Estate and Trust Income;and Gambling and Lottery Winnings.

Rule Number Rule Text

X0000-002 Incorrect Transmission data.

X0000-003 SubmissionId in the submission filemismatches SubmissionId in themanifest file.

X0000-004 No submission file found in statesubmission directory.

X0000-005 The XML data has failed schemavalidation.

X0000-006 MeF Gateway experiences system error.

X0000-007 Other State Submission.

X0000-008 The namespace declarations in the rootelement of the return ('Return' element)must be as follows: The defaultnamespace shall be set.

PA0000-002 Duplicate Filing.

PA40-001 Incomplete Direct Deposit/DebitPayment Data. If a Direct Deposit orDebit Payment is present, then theDirect Debit Amount, State RoutingTransit, State Deposit Account Numberand State Checking Account or StateSavings Account must be present aswell.

PA40-002 Invalid Debit Payment Date. If a DebitPayment is present, the Direct DebitDate must be present and must begreater than or equal to the IRS TimeStamp Date minus 3 and it must be avalid date for the calendar year.

PA40-003 Invalid Primary Filer Last Name. PrimaryLast Name must be present, leftjustified and must not contain anyspecial characters other than a hyphenor more than one consecutive space.

Page 21

PENNSYLVANIA FED/STATE E-FILE HANDBOOK www.revenue.pa.gov

Rule Number Rule Text

PA40-014 Invalid Total Estimated Payments andCredits. If Credit From 2013 PA TaxReturn plus 2014 Estimated Paymentsplus 2014 Extension Payment plusNonresident Tax Withheld equals '0' thenTotal Estimated Payments and Creditsmust be equal to '0' or if Credit From2013 PA Tax Return plus 2014 EstimatedPayments plus 2014 Extension Paymentplus Nonresident Tax Withheld is greaterthan '0' then Total Estimated Paymentsand Credits must be equal to CreditFrom 2013 PA Tax Return plus 2014Estimated Payments plus 2014 ExtensionPayment plus Nonresident Tax Withheld.

PA40-015 Invalid Eligibility Income or TaxForgiveness Credit. If Eligibility Incomefrom PA Schedule SP or Tax ForgivenessCredit from PA Schedule SP are presentthen the PA Schedule SP must bepresent and if Eligibility Income from PASchedule SP is present then theEligibility Income from PA Schedule SPmust be greater than or equal to theTotal PA Taxable Income.

PA40-016 Invalid Resident Credit. If ResidentCredit is present then Resident Creditmust be less than or equal to PA TaxLiability.

PA40-017 Invalid Total Payments and Credits. IfTotal Payments and Credits are presentthen Total Payments and Credits mustbe equal to Total PA Tax Withheld plusTotal Estimated Payments and Creditsplus Tax Forgiveness Credit from PASchedule SP plus Resident Credit plusTotal Other Credits.