2013 E.ON Russia Capital Market Update · E.ON Russia Capital Market Update 10 October 2013 Cleaner...

22

E.ON Russia Capital Market Update 10 October 2013 Cleaner & Better Energy

Transcript of 2013 E.ON Russia Capital Market Update · E.ON Russia Capital Market Update 10 October 2013 Cleaner...

E.ON Russia

Capital Market Update

10 October 2013

Cleaner & Better Energy

E.ON Russia

Management team

Important footprint of E.ON in Russia

2

Igor Popov

Deputy Director General for

Production

Joerg Tumat

Deputy Director General for

Energy Management

Ulf Backmeyer

Deputy Director General for

Finance and Economics

Maxim Shirokov

Chief Executive Officer

Acquisition of 69.3% stake in OGK4 in 2007,

rebranded to E.ON Russia in 2011

Increase of share from 69.3% to 83.7% as of

today

Installed capacity up by +20% (1.7 GW) since

acquisition to 10.3GW

0

0.5

1

1.5

2

2.5

3

3.5

2007 2008 2009 2010 2011 2012

E.ON Russia share price (RUB)

Markt Cap

RUB167bn

E.ON history

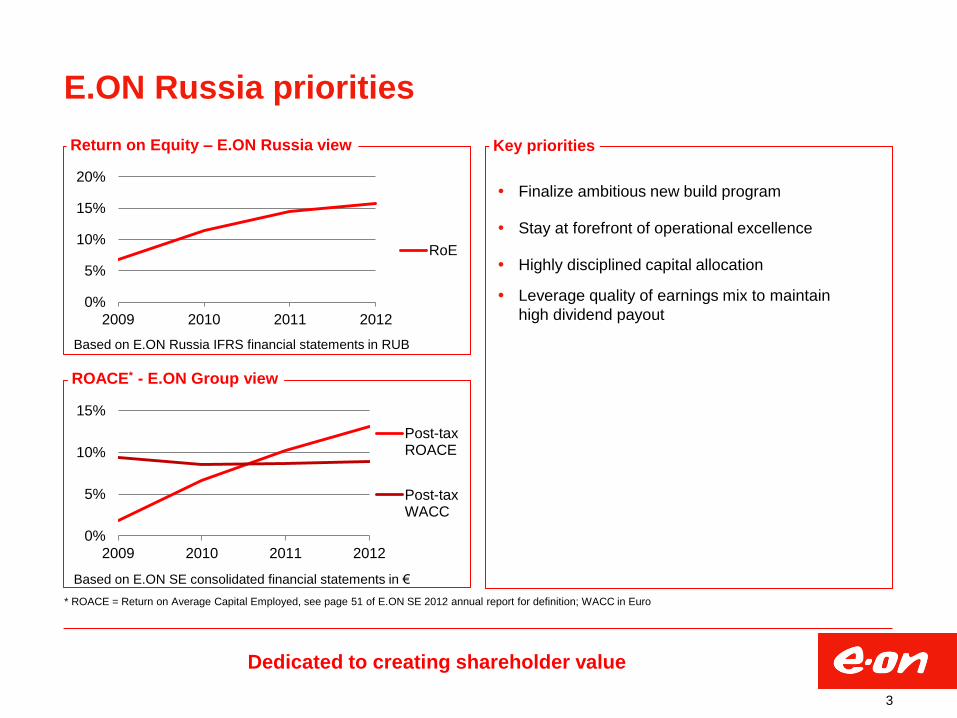

E.ON Russia priorities

Key priorities

Dedicated to creating shareholder value

3

Finalize ambitious new build program

Stay at forefront of operational excellence

Highly disciplined capital allocation

Leverage quality of earnings mix to maintain

high dividend payout

0%

5%

10%

15%

20%

2009 2010 2011 2012

RoE

Return on Equity – E.ON Russia view

Based on E.ON Russia IFRS financial statements in RUB

Based on E.ON SE consolidated financial statements in €

* ROACE = Return on Average Capital Employed, see page 51 of E.ON SE 2012 annual report for definition; WACC in Euro

0%

5%

10%

15%

2009 2010 2011 2012

Post-taxROACE

Post-taxWACC

ROACE* - E.ON Group view

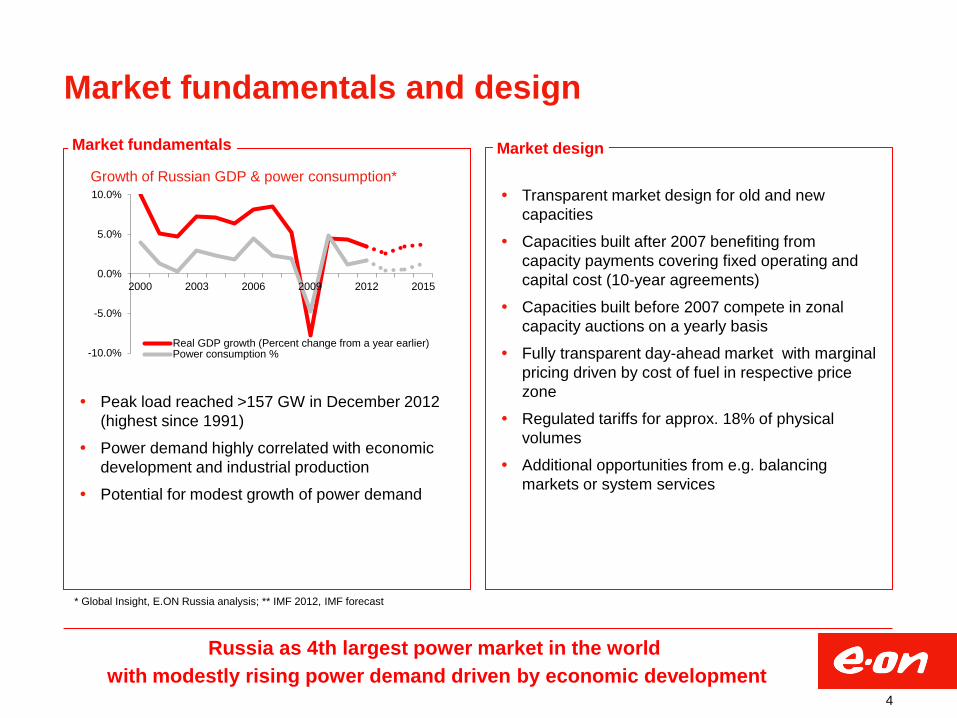

Market fundamentals and design

Russia as 4th largest power market in the world

with modestly rising power demand driven by economic development 4

Peak load reached >157 GW in December 2012

(highest since 1991)

Power demand highly correlated with economic

development and industrial production

Potential for modest growth of power demand

-10.0%

-5.0%

0.0%

5.0%

10.0%

2000 2003 2006 2009 2012 2015

Real GDP growth (Percent change from a year earlier)Power consumption %

Growth of Russian GDP & power consumption*

* Global Insight, E.ON Russia analysis; ** IMF 2012, IMF forecast

Market fundamentals

Market design

Transparent market design for old and new

capacities

Capacities built after 2007 benefiting from

capacity payments covering fixed operating and

capital cost (10-year agreements)

Capacities built before 2007 compete in zonal

capacity auctions on a yearly basis

Fully transparent day-ahead market with marginal

pricing driven by cost of fuel in respective price

zone

Regulated tariffs for approx. 18% of physical

volumes

Additional opportunities from e.g. balancing

markets or system services

2009 2010 2011 2012

El.price, 1st zone, Rub/MWh

Gas price, Moscow region,rub/1000m3

Two pricing zones

First pricing zone (European Russia, Urals) Second pricing zone (Siberia)

Two pricing zones with distinct drivers of power prices

5

System

dominated by

fossil and nuclear

plants

Old inefficient

gas units

normally set the

price

Relatively low

reserve margins

Electricity price is

driven by gas

price and

supply/demand

balance

Growth in gas

tariffs is the main

trigger for spot

prices

System

dominated by

hydro and

thermal

(predominantly

coal-fired) plants

Hydro balance

and coal price

are main drivers

of electricity

price

El.price

, 1st

zone,

Rub/M

Wh

Gas p

rice,

rub/1

000m

3

2009 2010 2011 2012

Hydro Generation 2nd zone, MWh

El.price, 2nd zone, Rub/MWh

El.p

rice, 2

nd z

one, R

ub/M

Wh

Hyd

ro G

en.

2nd z

one,

MW

h

Coal & gas

Nuclear

Hydro

Price (

Rub/M

Wh)

~180GW capacity

Price (

Rub/M

Wh)

Thermal & on-site

Hydro

~50GW capacity

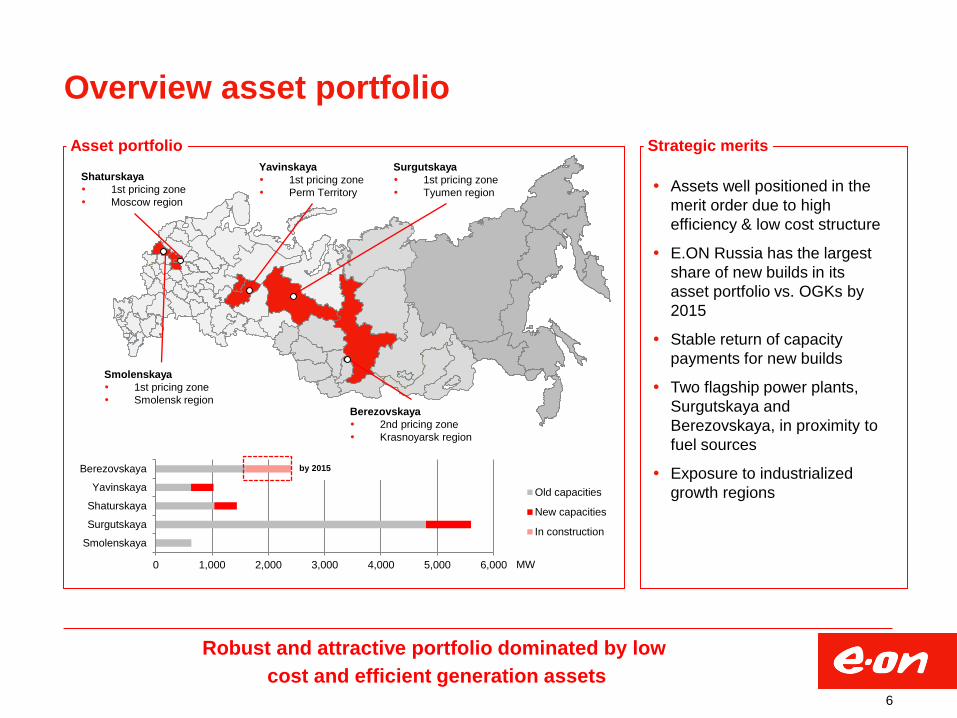

Overview asset portfolio

Asset portfolio

Robust and attractive portfolio dominated by low

cost and efficient generation assets 6

Strategic merits

Assets well positioned in the

merit order due to high

efficiency & low cost structure

E.ON Russia has the largest

share of new builds in its

asset portfolio vs. OGKs by

2015

Stable return of capacity

payments for new builds

Two flagship power plants,

Surgutskaya and

Berezovskaya, in proximity to

fuel sources

Exposure to industrialized

growth regions

0 1,000 2,000 3,000 4,000 5,000 6,000

Smolenskaya

Surgutskaya

Shaturskaya

Yavinskaya

Berezovskaya

Old capacities

New capacities

In construction

by 2015

MW

Shaturskaya

1st pricing zone

Moscow region

Yavinskaya

1st pricing zone

Perm Territory

Surgutskaya

1st pricing zone

Tyumen region

Berezovskaya

2nd pricing zone

Krasnoyarsk region

Smolenskaya

1st pricing zone

Smolensk region

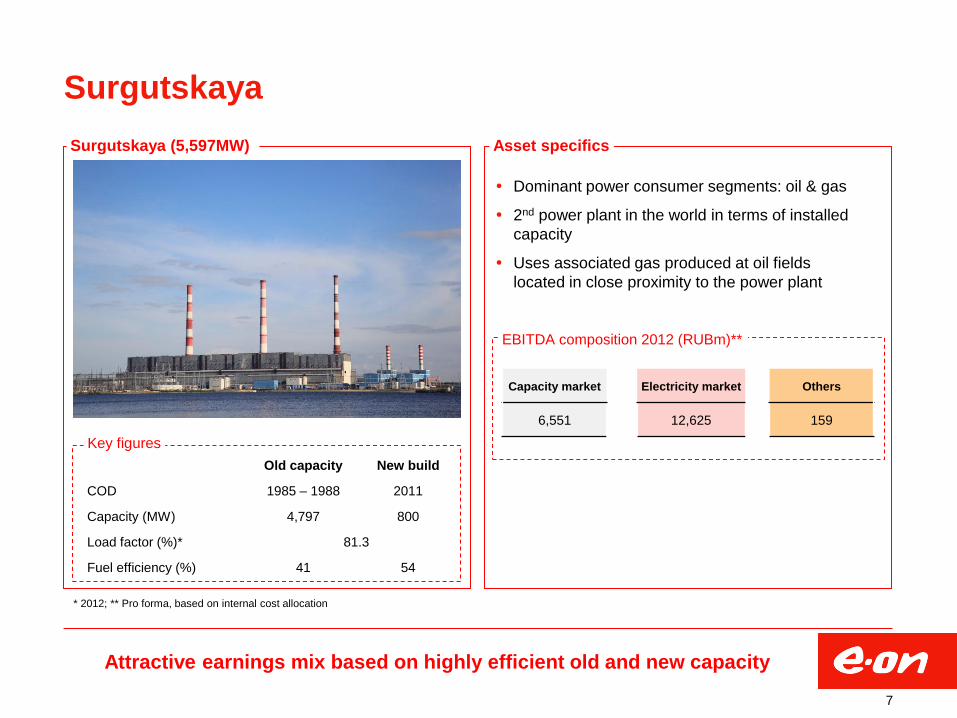

Surgutskaya

Surgutskaya (5,597MW)

Attractive earnings mix based on highly efficient old and new capacity

7

Asset specifics

Dominant power consumer segments: oil & gas

2nd power plant in the world in terms of installed

capacity

Uses associated gas produced at oil fields

located in close proximity to the power plant

Old capacity New build

COD 1985 – 1988 2011

Capacity (MW) 4,797 800

Load factor (%)* 81.3

Fuel efficiency (%) 41 54

Key figures

Capacity market Electricity market Others

6,551 12,625 159

EBITDA composition 2012 (RUBm)**

* 2012; ** Pro forma, based on internal cost allocation

Berezovskaya

Berezovskaya (1,600MW)

Achieve next level with comissioning of Berezovskaya in 2015

8

Dominant power consumer segments: metal &

mining

Major share of lignite is delivered to the plant via

two 14-km long open conveyor belts directly from

Berezovskoye coal deposit

Region has above average power demand growth

Total capex in Berezovskaya new build by 2015:

RUB43bn

Old capacity New build

COD 1987 – 1991 2015

Capacity (MW) 1,600 800

Load factor (%)* 76.4

Fuel efficiency /%) 38

Key figures

Asset specifics

Capacity market Electricity market Others

476 3,692 159

EBITDA composition 2012 (RUBm)**

* 2012; ** Pro forma, based on internal cost allocation

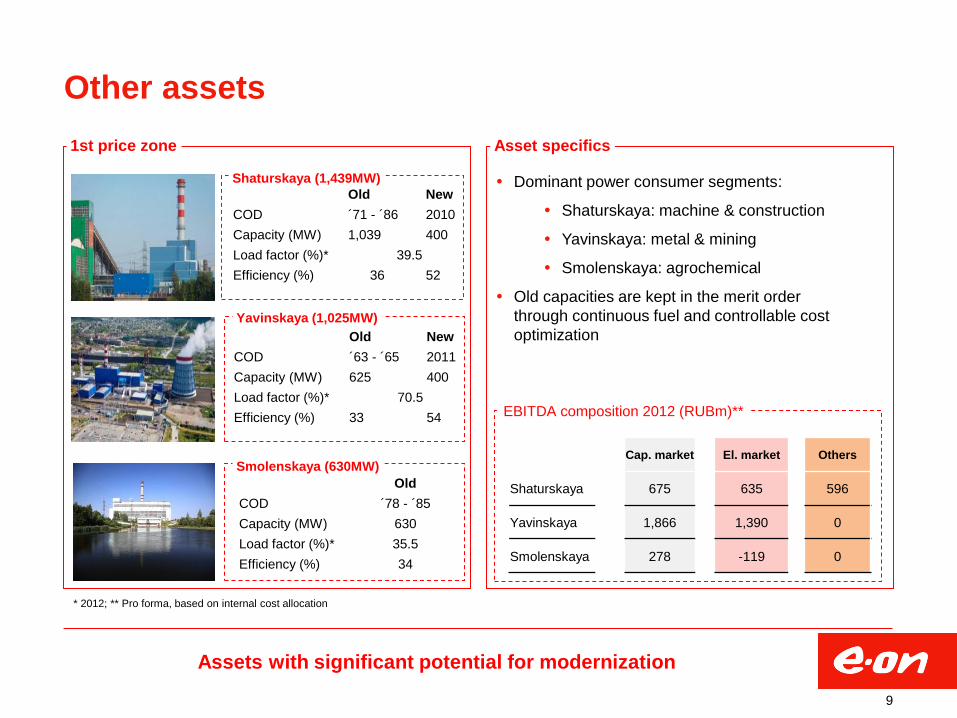

Old

COD ´78 - ´85

Capacity (MW) 630

Load factor (%)* 35.5

Efficiency (%) 34

Old New

COD ´63 - ´65 2011

Capacity (MW) 625 400

Load factor (%)* 70.5

Efficiency (%) 33 54

Old New

COD ´71 - ´86 2010

Capacity (MW) 1,039 400

Load factor (%)* 39.5

Efficiency (%) 36 52

Other assets

1st price zone

Assets with significant potential for modernization

9

Asset specifics

Dominant power consumer segments:

Shaturskaya: machine & construction

Yavinskaya: metal & mining

Smolenskaya: agrochemical

Old capacities are kept in the merit order

through continuous fuel and controllable cost

optimization

Shaturskaya (1,439MW)

Yavinskaya (1,025MW)

Smolenskaya (630MW)

EBITDA composition 2012 (RUBm)**

Cap. market El. market Others

Shaturskaya 675 635 596

Yavinskaya 1,866 1,390 0

Smolenskaya 278 -119 0

* 2012; ** Pro forma, based on internal cost allocation

Outstanding operational performance

Excellent gearing to benefit from operational performance

10

* Public filings, E.ON analysis

400 600 800

OGK-5 (ENEL)

InterRAO

OGK-2

E.ON

2012 fuel costs – RUB/MWh

Superior efficiency* Best load factors*

Lowest fuel costs* Disciplined management of non-fuel costs

250 300 350 400

OGK-5 (ENEL)

InterRAO

OGK-2

E.ON

2012 heat rate – g/kWh

20 40 60 80

OGK-5 (ENEL)

InterRAO

OGK-2

E.ON

2012 load factor - %

80

100

120

140

2008 2009 2010 2011 2012

Inde

x 1

00

in

20

08

Non-fuelcosts -RUB/MW

RussianCPI

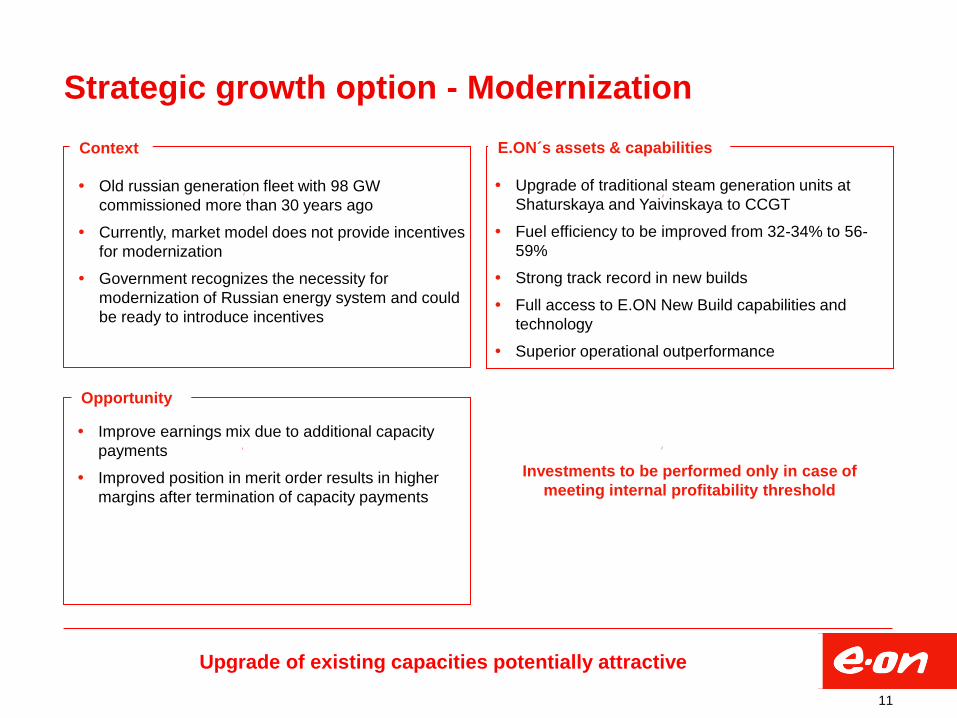

Strategic growth option - Modernization

Old russian generation fleet with 98 GW

commissioned more than 30 years ago

Currently, market model does not provide incentives

for modernization

Government recognizes the necessity for

modernization of Russian energy system and could

be ready to introduce incentives

Improve earnings mix due to additional capacity

payments

Improved position in merit order results in higher

margins after termination of capacity payments

Upgrade of traditional steam generation units at

Shaturskaya and Yaivinskaya to CCGT

Fuel efficiency to be improved from 32-34% to 56-

59%

Strong track record in new builds

Full access to E.ON New Build capabilities and

technology

Superior operational outperformance

Investments to be performed only in case of

meeting internal profitability threshold

Upgrade of existing capacities potentially attractive

Context E.ON´s assets & capabilities

Opportunity

11

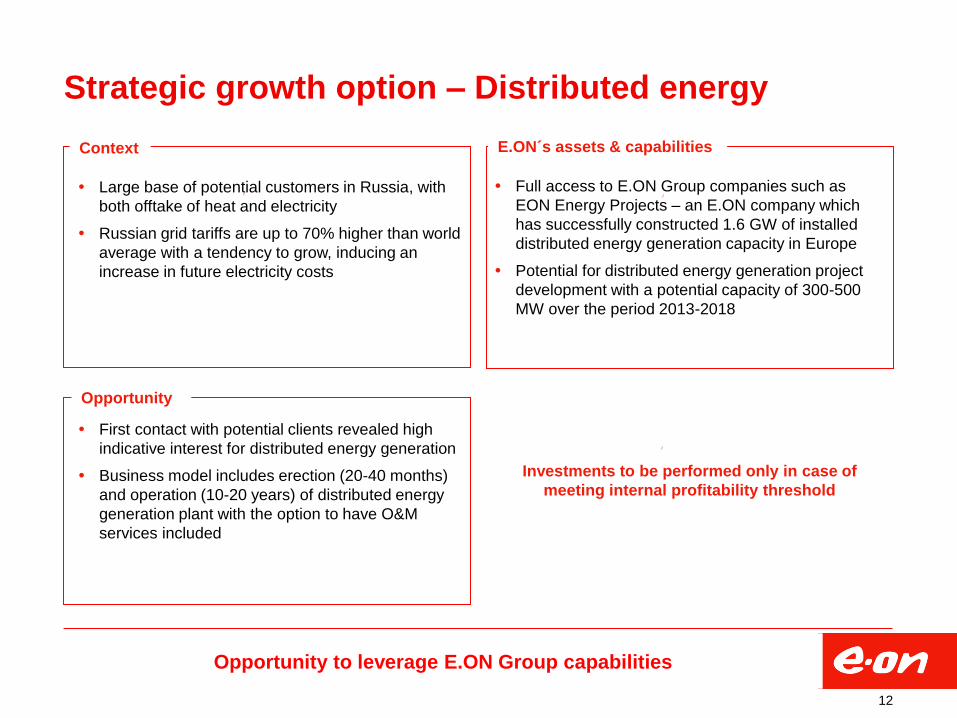

Strategic growth option – Distributed energy

Large base of potential customers in Russia, with

both offtake of heat and electricity

Russian grid tariffs are up to 70% higher than world

average with a tendency to grow, inducing an

increase in future electricity costs

First contact with potential clients revealed high

indicative interest for distributed energy generation

Business model includes erection (20-40 months)

and operation (10-20 years) of distributed energy

generation plant with the option to have O&M

services included

Full access to E.ON Group companies such as

EON Energy Projects – an E.ON company which

has successfully constructed 1.6 GW of installed

distributed energy generation capacity in Europe

Potential for distributed energy generation project

development with a potential capacity of 300-500

MW over the period 2013-2018

Opportunity to leverage E.ON Group capabilities

Context E.ON´s assets & capabilities

Opportunity

12

Investments to be performed only in case of

meeting internal profitability threshold

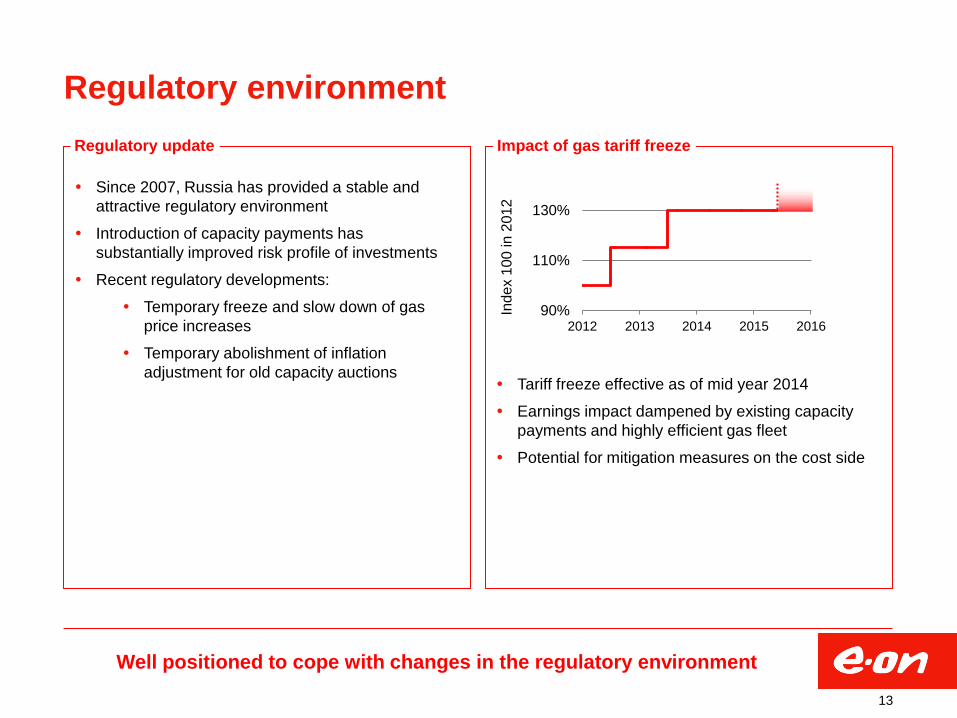

90%

110%

130%

2012 2013 2014 2015 2016

Regulatory environment

Regulatory update

Well positioned to cope with changes in the regulatory environment

13

Impact of gas tariff freeze

Since 2007, Russia has provided a stable and

attractive regulatory environment

Introduction of capacity payments has

substantially improved risk profile of investments

Recent regulatory developments:

Temporary freeze and slow down of gas

price increases

Temporary abolishment of inflation

adjustment for old capacity auctions

Tariff freeze effective as of mid year 2014

Earnings impact dampened by existing capacity

payments and highly efficient gas fleet

Potential for mitigation measures on the cost side

Inde

x 1

00

in

20

12

2008 2009 2010 2011 2012 2013 2014 2015

Financial outlook

Further step-change in earnings due to Berezovskaya

14

Berezovskaya new build, to be commissioned

early in 2015 will increase the total EBITDA of

the company by ~ RUB14bn per year

Increasing capacity payments reduce exposure

to commodity price volatility

Earnings impact Earnings outlook

RUBbn (EBITDA)

Short- term

Mid- term

Long- term

E E E

Gas tariff freeze

Decline in capacity price

in second price zone

Commissioning of

Berezovskaya

Tightening of supply

Modest increasing power

demand and gas prices

OPEX increase below

inflation

29

23

15

9 6

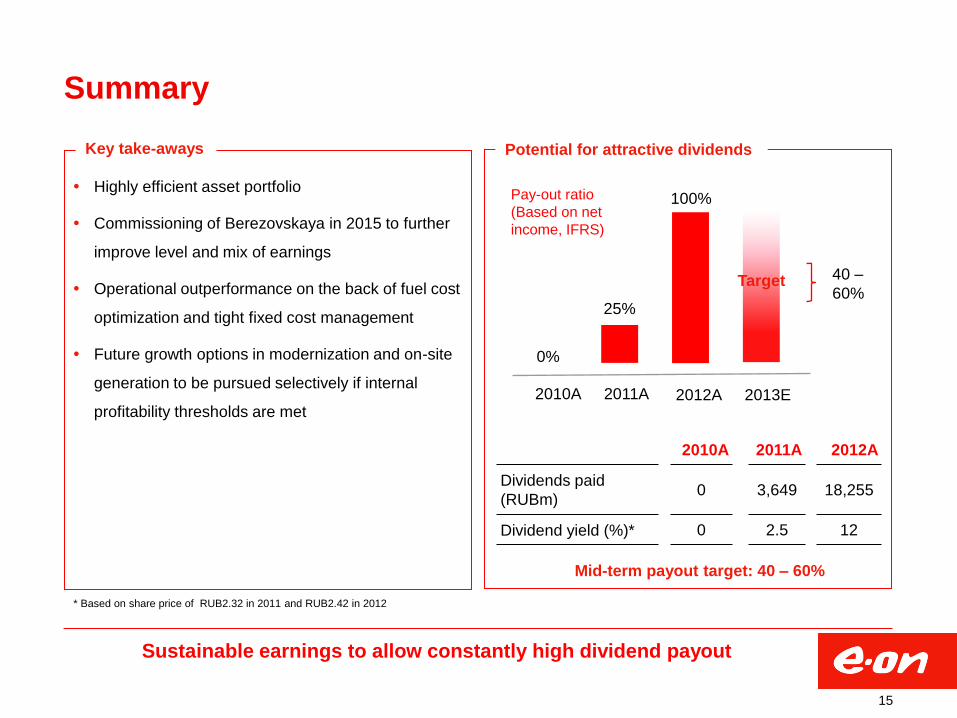

Summary

Key take-aways

15

Potential for attractive dividends

Sustainable earnings to allow constantly high dividend payout

2010A 2011A 2012A 2013E

40 –

60%

Pay-out ratio

(Based on net

income, IFRS)

100%

25%

0%

Mid-term payout target: 40 – 60%

2010A 2011A 2012A

Dividends paid

(RUBm) 0 3,649 18,255

Dividend yield (%)* 0 2.5 12

Highly efficient asset portfolio

Commissioning of Berezovskaya in 2015 to further

improve level and mix of earnings

Operational outperformance on the back of fuel cost

optimization and tight fixed cost management

Future growth options in modernization and on-site

generation to be pursued selectively if internal

profitability thresholds are met

Target

* Based on share price of RUB2.32 in 2011 and RUB2.42 in 2012

Backup

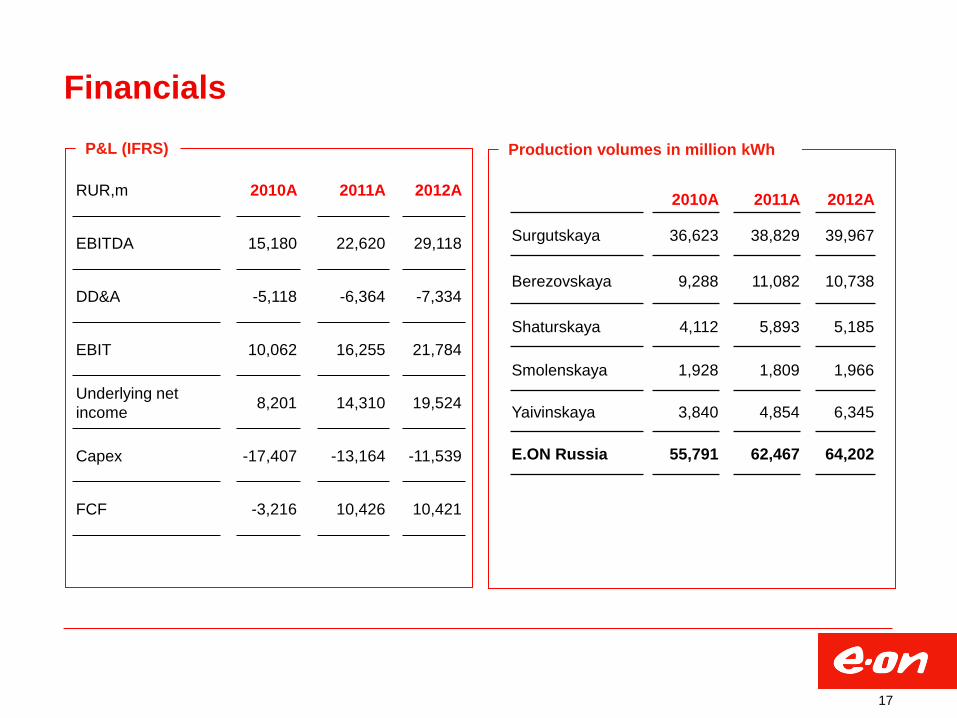

Financials

P&L (IFRS)

17

2010A 2011A 2012A

Surgutskaya 36,623 38,829 39,967

Berezovskaya 9,288 11,082 10,738

Shaturskaya 4,112 5,893 5,185

Smolenskaya 1,928 1,809 1,966

Yaivinskaya 3,840 4,854 6,345

E.ON Russia 55,791 62,467 64,202

Production volumes in million kWh

RUR,m 2010A 2011A 2012A

EBITDA 15,180 22,620 29,118

DD&A -5,118 -6,364 -7,334

EBIT 10,062 16,255 21,784

Underlying net

income 8,201 14,310 19,524

Capex -17,407 -13,164 -11,539

FCF -3,216 10,426 10,421

One market design

18

CAPACITY MARKET ELECTRICITY MARKET

Old capacity (built before 2007)

New capacity (built after 2007)

Capacity payments supposed to cover opex

Zonal capacity auctions, marginal pricing

Price caps and price floors in regions with limited competition

Regulated tariffs for must-run and expensive plants

Ca. 25% sold under regulated tariffs

Capacity payments supposed to cover fixed costs and ensure capital remuneration

10-year capacity supply agreements

Benchmark capex, opex

13-14% allowed rate of return, 15-year payback

Various adjustment coefficients

Cover 71-95% of total new build project costs

Old capacity & New capacity (built before 2007) (built after 2007)

Day-ahead market (~75% of physical volumes)

Marginal pricing

Price driven by cost of fuel

Other

Balancing market

Bilateral contracts

System services

Power arbitrage

Heat sales

Regulated agreements

Ca. 18% of physical volumes

Tariffs set by regulator on cost-plus basis

19

Outstanding performance in new builds

Delay of commissioning

Name Type Capacity (MW)

Start-up date

1 Shaturskaya CCGT 393 On-line

2 Surgutskaya CCGT 797 On-line

3 Yaivinskaya CCGT 425 On-line

4 Berezovskaya Upgrade 100 On-line

5 Berezovskaya Coal 800 2015

Project execution

1 2

3 5

Name Months of delay

Owner

Shaturskaya unit 7

2 E.ON Russia

Surgutskaya unit 7 unit 8

3 1

E.ON Russia

Yaivinskaya unit 6

0 E.ON Russia

Nyaganskaya unit 1 unit 2

~ 11 ~ 14

Fortum

Gusinoozerskaya unit 4

~ 10 INTER RAO – Electric

Power Plants

Vologodskaya unit 2

~ 10 Siberian Generating

Company

Novomoskovskaya unit 6

~ 6 Quadra - Power

Generation

Livenskaya unit 5

~ 2 Quadra - Power

Generation

Novokuybyshevkaya unit 4 unit 5 unit 6

~ 3 ~ 3 ~ 3

IES-Holding

20

Dr. Marc Spieker

Head of IR T+49 2 11-45 79-3 45

Peter Blankenhorn

Regions/Sales, SRI, Retail, T +49 2 11-45 79-4 81

Facts & Figures [email protected]

François Poullet

Generation, Gas T +49 2 11-45 79-3 32

Marc Koebernick

Renewables, Trading T +49 2 11-45 79-2 39

Dr. Stephan Schönefuß

Politics & Regulation, Regions/Distribution T +49 2 11-45 79-48 08

Carmen Schneider

Technology & Innovation,

Roadshow planning & management, T +49 2 11-45 79-3 45

Shareholder ID & Targeting [email protected]

E.ON Investor Relations Contact

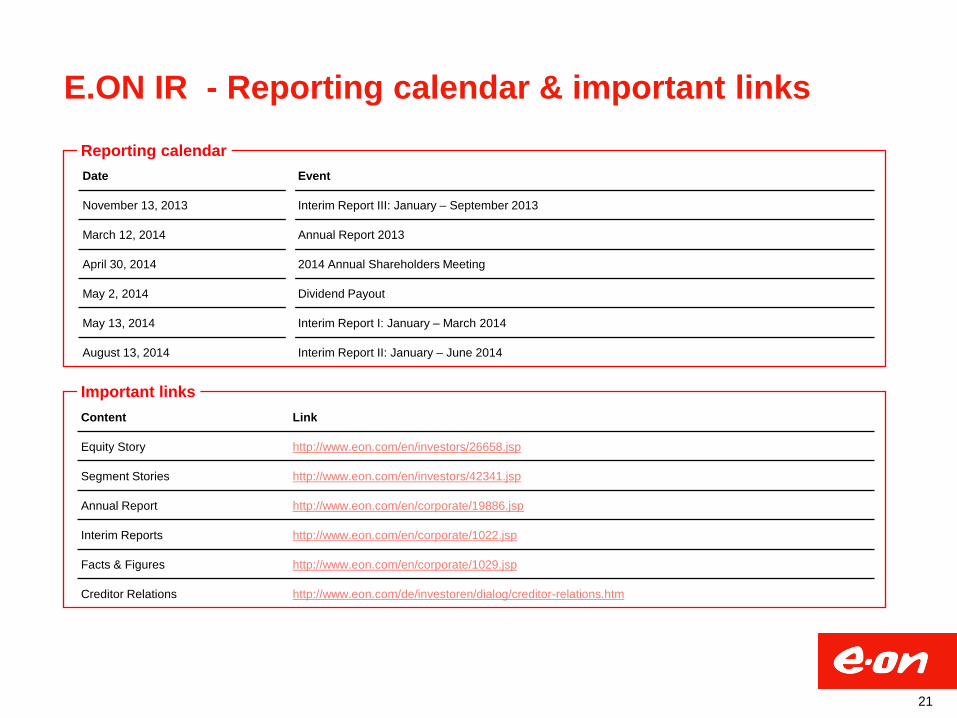

E.ON IR - Reporting calendar & important links

Date Event

November 13, 2013 Interim Report III: January – September 2013

March 12, 2014 Annual Report 2013

April 30, 2014 2014 Annual Shareholders Meeting

May 2, 2014 Dividend Payout

May 13, 2014 Interim Report I: January – March 2014

August 13, 2014 Interim Report II: January – June 2014

Content Link

Equity Story http://www.eon.com/en/investors/26658.jsp

Segment Stories http://www.eon.com/en/investors/42341.jsp

Annual Report http://www.eon.com/en/corporate/19886.jsp

Interim Reports http://www.eon.com/en/corporate/1022.jsp

Facts & Figures http://www.eon.com/en/corporate/1029.jsp

Creditor Relations http://www.eon.com/de/investoren/dialog/creditor-relations.htm

Important links

Reporting calendar

21

This presentation may contain forward-looking statements based on current assumptions and forecasts made

by E.ON Group management and other information currently available to E.ON. Various known and unknown

risks, uncertainties and other factors could lead to material differences between the actual future results,

financial situation, development or performance of the company and the estimates given here. E.ON SE does

not intend, and does not assume any liability whatsoever, to update these forward-looking statements or to

conform them to future events or developments.

Disclaimer