© 2008 Morningstar, Inc. All rights reserved. 3/1/2008 LCN200803-2013997 Risk and Volatility.

1996 ANNUAL REPORT

Brought to you by Global Reports

DANONE 7, RUE DE TÉHÉRAN 75008 PARIS, FRANCE - TEL. (33) 1 44 35 20 20 - FAX (33) 1 42 25 67 16

DANONE is on the Web at: http://www.danonegroup.com

DANONE Group publishes the following documents: Annual Report (Fr./Eng.), Letter to Shareholders (French only),

and COB and offering circulars.

To obtain these or any other information, please contact:

DANONE Group - Investor Relations - 7, rue de Téhéran - 75008 PARIS, France - Tel: (33) 1 44 35 20 76 - Fax: (33) 1 45 63 88 22

Brought to you by Global Reports

Brought to you by Global Reports

CONTENTS

THE DANONE GROUP PAGE 2

GROUP MANAGEMENT PAGE 3

STRATEGY PAGE 4

MANAGEMENT REPORT PAGE 8

HUMAN RESOURCES PAGE 12

DAIRY PRODUCTS PAGE 18

GROCERY PRODUCTS PAGE 22

BISCUITS PAGE 26

BEVERAGES PAGE 28

CONTAINERS PAGE 34

INTERNATIONAL PAGE 36

CONSOLIDATED FINANCIAL STATEMENTS PAGE 42

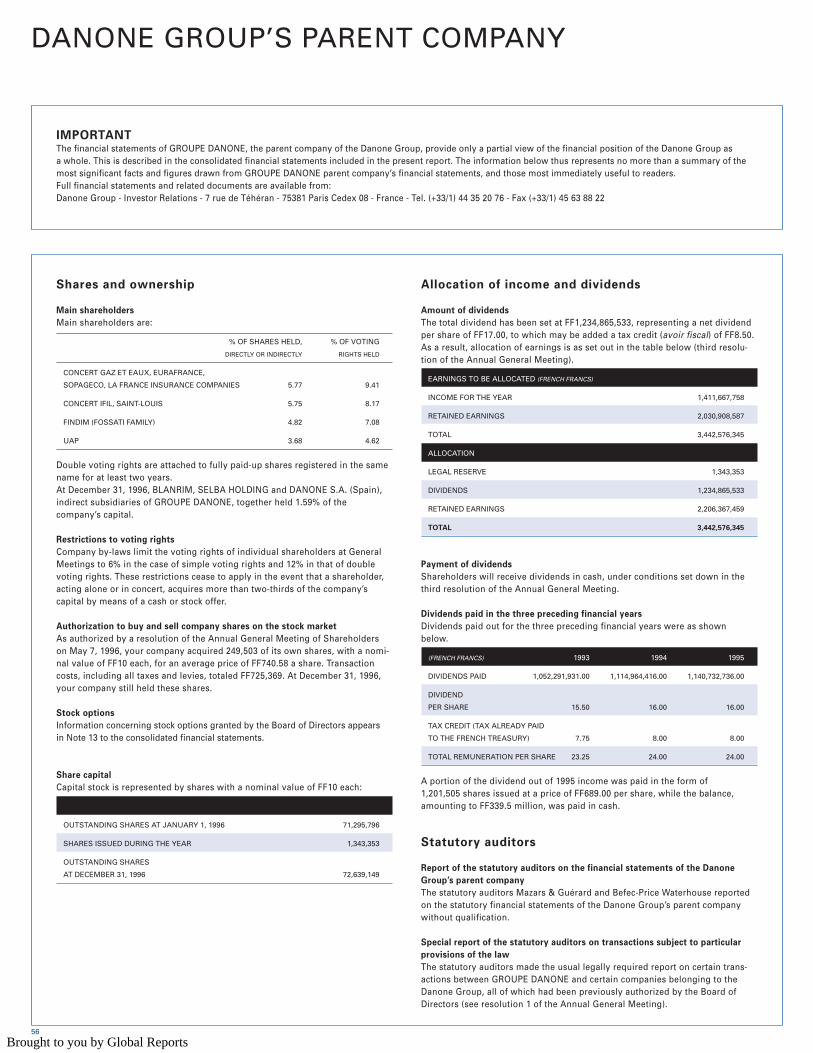

INFORMATION ON DANONE GROUP’S PARENT COMPANY PAGE 56

MAIN GROUP COMPANIES PAGE 60

ORGANIZATION CHART PAGE 64

HEADS OF SUBSIDIARIES AND DEPARTMENTS INSIDE BACK COVER

Brought to you by Global Reports

SAIW

A

INT

ER

NA

TIO

NAL PREMIUMLA

GE

R

A N N O 1 8 8 0

BIER BIERE

BR

.A

LK EN - M A E S W A A R L OOS BELG

I UM

DAL1846

peroni

••bir

ra

1846 PERO

NI

PR

OD

O T TA C ON O RZI PRIM A V

ER

ILI

QU

A

LITÀ

FRANCE

VIDRIO ESPANA

VERDOME

DANONE IS THE LEADING MULTI-PRODUCT FOODGROUP IN FRANCE, ITALY AND SPAIN, RANKINGTHIRD IN EUROPE AND SEVENTH IN THE WORLD.

Consolidated sales:FF29.6 billion

World leader in dairy

products, including

yogurts, yogurt-style

cheeses and dairy

desserts.

DAIRY PRODUCTS

Consolidated sales:FF16.7 billion

No. 1 in Europe in sauces

and condiments.

No. 2 in pasta products.

No. 3 in ready-to-serve

dishes (refrigerated,

frozen and shelf-stable).

GROCERY PRODUCTS

Consolidated sales:FF17 billion

World leader in biscuits.

BISCUITS

Consolidated sales:FF7.8 billion

Second largest brewer

in Europe.

BEER

Consolidated sales:FF7.9 billion

No. 2 worldwide.

MINERAL WATER

Consolidated sales:FF6.3 billion

No. 2 in Europe in glass

containers.

CONTAINERS

2

Brought to you by Global Reports

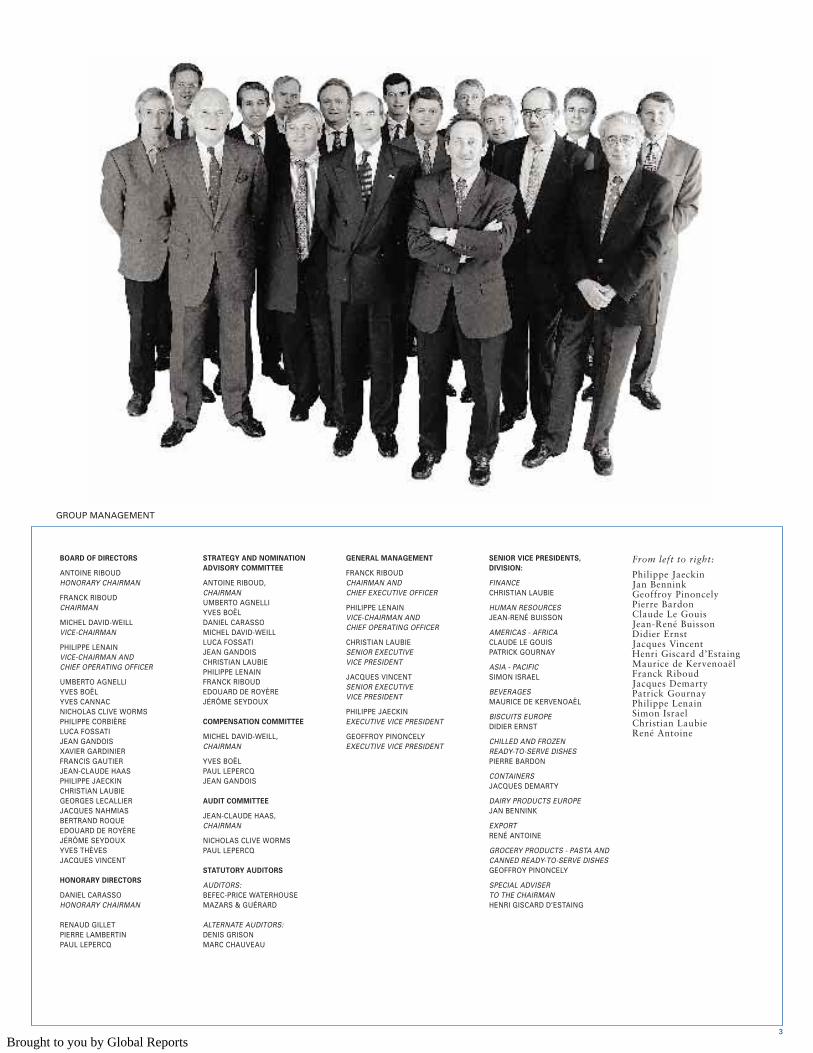

BOARD OF DIRECTORS

ANTOINE RIBOUD HONORARY CHAIRMAN

FRANCK RIBOUDCHAIRMAN

MICHEL DAVID-WEILL VICE-CHAIRMAN

PHILIPPE LENAINVICE-CHAIRMAN ANDCHIEF OPERATING OFFICER

UMBERTO AGNELLIYVES BOËLYVES CANNAC NICHOLAS CLIVE WORMSPHILIPPE CORBIÈRELUCA FOSSATIJEAN GANDOIS XAVIER GARDINIER FRANCIS GAUTIERJEAN-CLAUDE HAAS PHILIPPE JAECKINCHRISTIAN LAUBIEGEORGES LECALLIERJACQUES NAHMIASBERTRAND ROQUEEDOUARD DE ROYÈRE JÉRÔME SEYDOUX YVES THÈVESJACQUES VINCENT

HONORARY DIRECTORS

DANIEL CARASSO HONORARY CHAIRMAN

RENAUD GILLETPIERRE LAMBERTINPAUL LEPERCQ

STRATEGY AND NOMINATION

ADVISORY COMMITTEE

ANTOINE RIBOUD,CHAIRMANUMBERTO AGNELLIYVES BOËL DANIEL CARASSOMICHEL DAVID-WEILLLUCA FOSSATIJEAN GANDOISCHRISTIAN LAUBIEPHILIPPE LENAINFRANCK RIBOUDEDOUARD DE ROYÈREJÉRÔME SEYDOUX

COMPENSATION COMMITTEE

MICHEL DAVID-WEILL,CHAIRMAN

YVES BOËL PAUL LEPERCQJEAN GANDOIS

AUDIT COMMITTEE

JEAN-CLAUDE HAAS, CHAIRMAN

NICHOLAS CLIVE WORMSPAUL LEPERCQ

STATUTORY AUDITORS

AUDITORS:BEFEC-PRICE WATERHOUSEMAZARS & GUÉRARD

ALTERNATE AUDITORS:DENIS GRISONMARC CHAUVEAU

GENERAL MANAGEMENT

FRANCK RIBOUDCHAIRMAN AND CHIEF EXECUTIVE OFFICER

PHILIPPE LENAINVICE-CHAIRMAN ANDCHIEF OPERATING OFFICER

CHRISTIAN LAUBIESENIOR EXECUTIVE VICE PRESIDENT

JACQUES VINCENTSENIOR EXECUTIVE VICE PRESIDENT

PHILIPPE JAECKINEXECUTIVE VICE PRESIDENT

GEOFFROY PINONCELYEXECUTIVE VICE PRESIDENT

SENIOR VICE PRESIDENTS,

DIVISION:

FINANCECHRISTIAN LAUBIE

HUMAN RESOURCES JEAN-RENÉ BUISSON

AMERICAS - AFRICA CLAUDE LE GOUISPATRICK GOURNAY

ASIA - PACIFICSIMON ISRAEL

BEVERAGESMAURICE DE KERVENOAËL

BISCUITS EUROPEDIDIER ERNST

CHILLED AND FROZEN READY-TO-SERVE DISHESPIERRE BARDON

CONTAINERSJACQUES DEMARTY

DAIRY PRODUCTS EUROPEJAN BENNINK

EXPORTRENÉ ANTOINE

GROCERY PRODUCTS - PASTA ANDCANNED READY-TO-SERVE DISHESGEOFFROY PINONCELY

SPECIAL ADVISER TO THE CHAIRMANHENRI GISCARD D’ESTAING

From left to right:

Philippe Jaeckin Jan Bennink Geoffroy Pinoncely Pierre Bardon Claude Le Gouis Jean-René Buisson Didier Ernst Jacques Vincent Henri Giscard d’Estaing Maurice de Kervenoaël Franck Riboud Jacques Demarty Patrick Gournay Philippe Lenain Simon Israel Christian Laubie René Antoine

GROUP MANAGEMENT

3

Brought to you by Global Reports

STRATEGYIN 1996, DANONE GROUP ACHIEVED ITS KEY FINANCIAL OBJECTIVES WITH RISES IN NET INCOMEAND OPERATING MARGIN. SALES ROSE 5.7% TO FF84 BILLION, WHILE OPERATINGINCOME ROSE 6.5% AND NET INCOME 8%. OPERATING MARGIN THUS IMPROVED, FOLLOWINGFOUR YEARS OF DECLINE DUE TO THE ECONOMICSLOWDOWN IN EUROPE. AS A PERCENTAGE OFSALES, OPERATING INCOME ROSE FROM 8.8% IN1995 TO 8.9% IN 1996, MARKING A TURNAROUND INTHE PREVIOUS TREND. THIS IMPROVEMENT WAS DUE PARTLY TO COST-CUTTING BY ALL EUROPEAN ENTITIES, AND PARTLYTO EXPANSION OF INTERNATIONAL BUSINESS.

4

Brought to you by Global Reports

Group strategy is built on fivepriorities:- focus on a limited number ofcore businesses- pooling of strengths and deve-lopment of synergies within theGroup- internationalization- enhancing profitability and share-holder value- commitment to fundamentalcorporate values and adoption ofmanagement criteria in accordancewith these values.

Four core businessesfor Danone Group

Danone Group has opted to focushuman and financial resources on four core activities whichcontribute to both profitability inEurope and international growth.

Health foods, represented prin-cipally by dairy products includingyogurts, yogurt-style cheeses anddairy desserts, but also infantfoods and diet specialties foradults, benefit from a broad trendin consumer preferences whichincreasingly reflect concern forhealth and well-being. Businessin this area contributes over FF33 billion to consolidated sales.Danone is the world’s largest pro-ducer of fresh dairy products.

Snack foods also play a grow-ing role in modern eating habits,as consumers increasingly preferto grab a quick bite here andthere rather than sit down to a traditional meal. Main productsare biscuits, bakery products andpackaged cakes. Sales in this areatotal approximately FF17 billion,and Danone Group is the world’sleading producer of biscuits.

Beverage activities are mainly inbeer, bottled waters and fruitjuices. They stand to benefit fromthe worldwide trend to drinkswhich are either alcohol-free orhave only low alcohol content.Group sales in this area totalnearly FF15 billion.

Convenience foods are in tunewith growing demand for ready-to-serve and easy-to-use prod-ucts, which are part and parcel ofmodern-day life. Products in thisarea, which represent sales ofFF13 billion, cover a wide range:sauces and condiments, as wellas canned, chilled and frozenready-to-serve dishes. Theirdiversity, reflecting in particulardifferences in products from onecountry to another, means thatbusiness of this kind plays a smaller role than others in theGroup’s international expansion.

These four categories of businessare not independent; on thecontrary, they increasingly com-plement each other. Reflectingthis, a number of new productscombine expertise from pre-viously distinct areas. Examplesinclude “Minute Maid Danone”, arefrigerated fruit juice range soonto be launched in Europe andLatin America, “Prince Coeur deLait” refrigerated dairy-creambiscuits and “Blédina Danone”refrigerated infant foods.

New emphasis oncross-company ties

Apart from this focus on four corebusinesses, representing thefoundations of its production andmarketing competence, DanoneGroup is stepping up efforts todevelop synergies between differ-ent types of activity. This is illustrated by a number ofjoint initiatives in direct market-ing. Examples include the “Bingodes marques’’ promotionalcontest bringing together 16brands and 40 products, “Danoé”magazine, now distributed to two million French consumers,and pooling of consumer data filesassembled by group companies. Similarly, a major drive is underway to improve purchasing terms– for packaging, raw materials,equipment and services – and cutcosts throughout the Group. These efforts to pool sales andproduction resources are in addi-tion to the unity long achieved infinancial and human resourcemanagement.The best illustration of this newemphasis on cross-company tiesis the use of the “Danone” brand.Originally applied only to dairyproducts, this is now not only thebanner for the Group as a wholebut also the main brand for biscuitsin Asia, as well as the name of amineral water sold in the UnitedStates. Sales under the “Danone”label have risen from FF10 billionten years ago to nearly FF23 bil-lion today, and continuing growthis expected to boost this to FF40billion five years hence.

International expansionstrides ahead

Sales outside western Europesurged from FF3.6 billion in 1992to FF15 billion in 1996. In thatyear alone, international businesswas up 33%, driven by a combi-nation of acquisitions and organicgrowth that was five times quick-er than in western Europe. Thismade a significant contribution tothe Group’s overall growth.

Danone Group is now the leadingproducer of biscuits in Asia andleading producer of fresh dairyproducts in South America. Intwo years, it has doubled the sizeof its operations in Latin America,and quadrupled its presence inChina. International business nowaccounts for 18% of total sales,compared with only 5% in 1992,and this proportion is expected toquickly reach 25 or 30%, thus pro-viding much of the momentumfor the Group as a whole.

Improved profitability,a major priority

Rises in net income and oper-ating margin are the reward forefforts of two kinds:- in Europe, cost-cutting com-bined with the benefits of inno-vation and new product launchesto raise margins- international expansion to reach critical mass and achieve steadyimprovements in margins on fast-expanding markets. The Group was thus able toreport an 8% rise in net incomefrom 1995 to 1996. Increasing shareholder value is ofprime importance to DanoneGroup, which is reviewing its cur-rent business mix and perma-nently monitors and analyzesacquisition opportunities. Return on capital employed isnow a key measure of perform-ance and is used to determinebonuses for senior managementat corporate and divisional level.

Commitment to fundamental corporatevalues

The Group is committed to a setof fundamental values and a mis-sion statement drawn up afterbroad consultation throughoutthe Group. These values, present-ed in this report, have takenconcrete shape in a wide varietyof initiatives. At the same time, there havebeen some adjustments to organ-ization following the decision ofthe Board of Directors to set up anumber of committees and reor-ganize some already existing.

Three committees will now assist the Board of Directors in pre-paring meetings:- the Strategy and NominationsAdvisory Committee, presided byMr. Antoine Riboud, with 12members- the Audit Committee, with threemembers- the Compensation Committeewith four members.

The members of the last twocommittees are all non executives.

The Board of Directors has alsodrawn up a code of businessconduct which has been distributedthroughout the Group worldwide.

Franck Riboud

5

Brought to you by Global Reports

DANONE CORPORATE IDENTITYTHE TERM CULTURE EXTENDS BEYOND BROADCONCEPTS SUCH AS HISTORY, LANGUAGE AND LIFESTYLE, TO INCLUDE THE MANY DETAILS OF EVERY-DAY LIFE – IN PARTICULAR, PREFERENCES IN TASTE,AROMA AND FOOD PRODUCTS. SOCIAL GROUPS AROUND THE GLOBE ARE DEFINEDIN PART BY THEIR CULINARY PREFERENCES AND HABITS. A WORLDWIDE CORPORATION LIKE DANONEMUST OBVIOUSLY RESPECT THIS DIVERSITY, EVEN ASIT IMPOSES THE SAME HIGH STANDARDS WHEREVERIT DOES BUSINESS. IN PRACTICAL TERMS, THISMEANS ADAPTING PRODUCTS TO MEET THE EXPEC-TATIONS OF CONSUMERS FROM DIFFERENT AGEGROUPS, COUNTRIES AND CULTURES. FOR CONSUMERS EVERYWHERE, THE DANONE NAMEIS ASSOCIATED WITH HEALTHY EATING. IN EUROPE,BOTH EASTERN AND WESTERN, ASIA AND LATINAMERICA, THIS MEANS FITNESS, GENERAL WELL-BEING, AND FOOD PRODUCTS OFFERING A GUARAN-TEE OF THE VERY HIGHEST QUALITY. BUT THE DANONE IMAGE IS MORE THAN PHYSICAL HEALTH: IT IS ALSO THE GOOD TIMES SHARED WITH FAMILYAND FRIENDS, GAMES, PICNICS, AND ALL THEPLACES PEOPLE LIKE TO MEET.FOR DANONE, EACH PRODUCT IS THE FINAL STAGE IN THE PROCESS OF GETTING FOOD FROM THE PRO-DUCER TO THE CONSUMER. EACH STAGE IS EQUALLYIMPORTANT, WHICH IS WHY IT DEVOTES AS MUCHENERGY TO SELECTING PREMIUM INGREDIENTS ASTO DESIGNING APPROPRIATE PACKAGING.

6

Brought to you by Global Reports

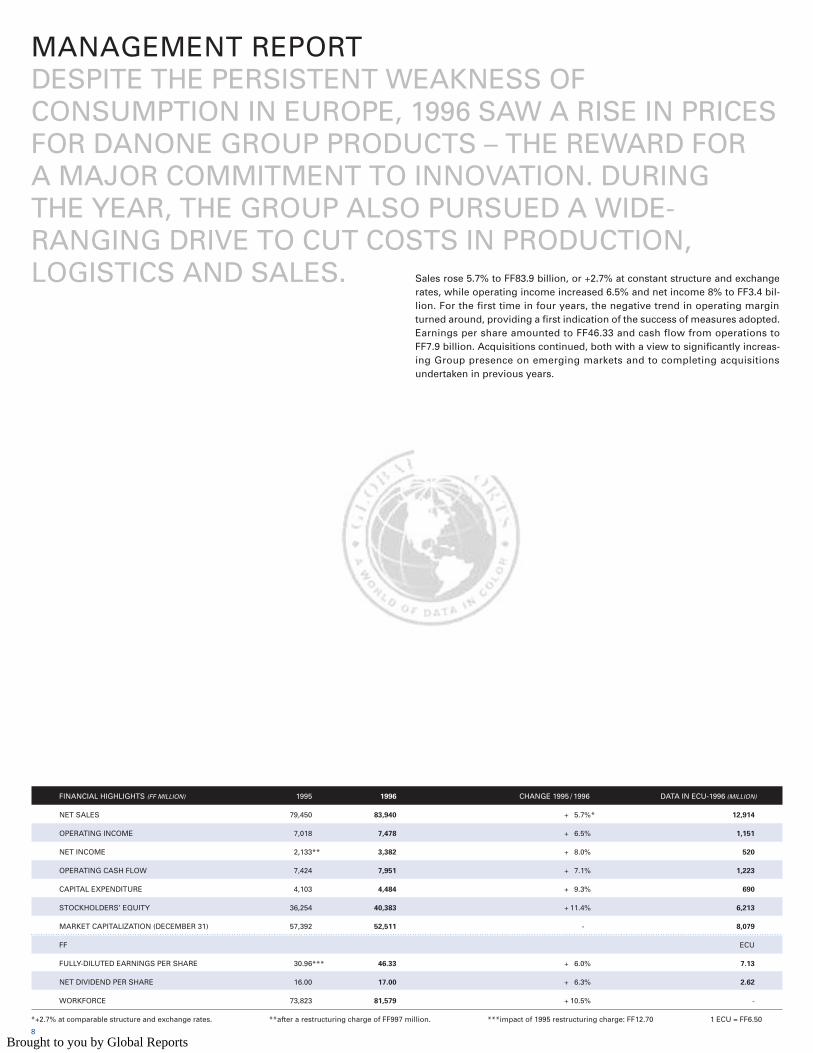

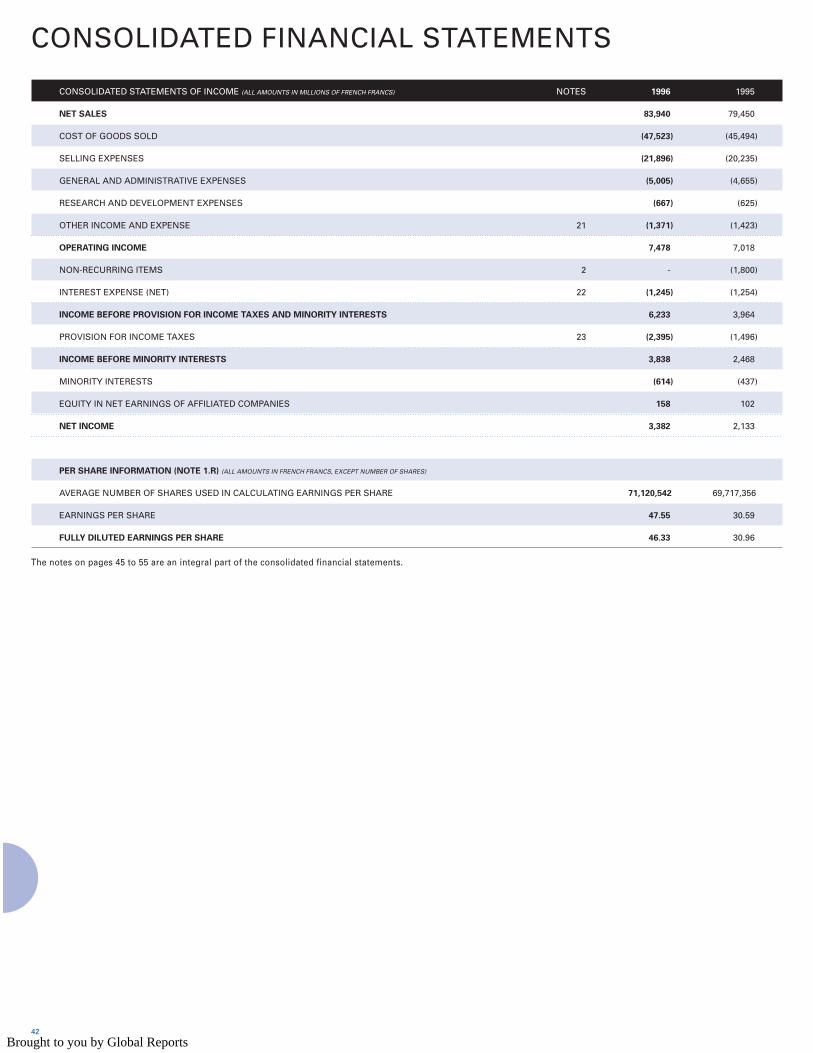

MANAGEMENT REPORTDESPITE THE PERSISTENT WEAKNESS OF CONSUMPTION IN EUROPE, 1996 SAW A RISE IN PRICESFOR DANONE GROUP PRODUCTS – THE REWARD FOR A MAJOR COMMITMENT TO INNOVATION. DURING THE YEAR, THE GROUP ALSO PURSUED A WIDE-RANGING DRIVE TO CUT COSTS IN PRODUCTION,LOGISTICS AND SALES. Sales rose 5.7% to FF83.9 billion, or +2.7% at constant structure and exchange

rates, while operating income increased 6.5% and net income 8% to FF3.4 bil-lion. For the first time in four years, the negative trend in operating margin turned around, providing a first indication of the success of measures adopted. Earnings per share amounted to FF46.33 and cash flow from operations toFF7.9 billion. Acquisitions continued, both with a view to significantly increas-ing Group presence on emerging markets and to completing acquisitionsundertaken in previous years.

FINANCIAL HIGHLIGHTS (FF MILLION) 1995 1996 CHANGE 1995 / 1996 DATA IN ECU-1996 (MILLION)

NET SALES 79,450 83,940 + 5.7%* 12,914

OPERATING INCOME 7,018 7,478 + 6.5% 1,151

NET INCOME 2,133** 3,382 + 8.0% 520

OPERATING CASH FLOW 7,424 7,951 + 7.1% 1,223

CAPITAL EXPENDITURE 4,103 4,484 + 9.3% 690

STOCKHOLDERS’ EQUITY 36,254 40,383 + 11.4% 6,213

MARKET CAPITALIZATION (DECEMBER 31) 57,392 52,511 - 8,079

FF ECU

FULLY-DILUTED EARNINGS PER SHARE 30.96*** 46.33 + 6.0% 7.13

NET DIVIDEND PER SHARE 16.00 17.00 + 6.3% 2.62

WORKFORCE 73,823 81,579 + 10.5% -

*+2.7% at comparable structure and exchange rates. **after a restructuring charge of FF997 million. ***impact of 1995 restructuring charge: FF12.70 1 ECU = FF6.50

8

Brought to you by Global Reports

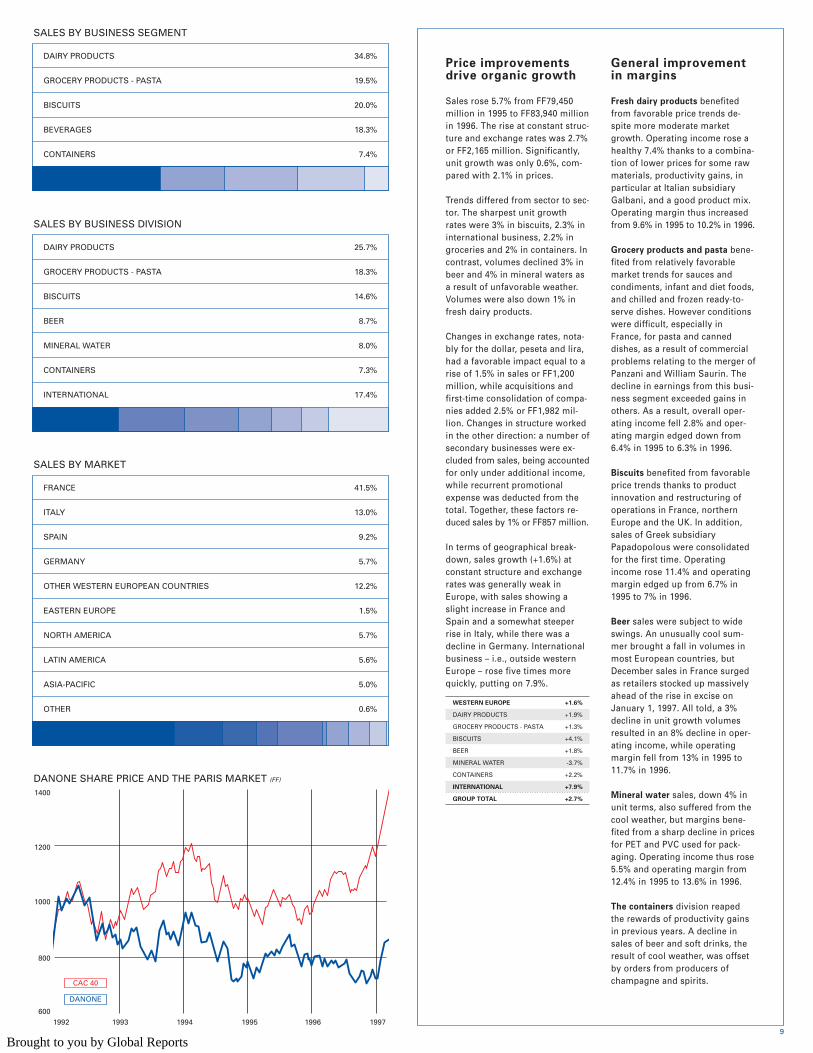

Price improvementsdrive organic growth

Sales rose 5.7% from FF79,450million in 1995 to FF83,940 millionin 1996. The rise at constant struc-ture and exchange rates was 2.7%or FF2,165 million. Significantly,unit growth was only 0.6%, com-pared with 2.1% in prices.

Trends differed from sector to sec-tor. The sharpest unit growthrates were 3% in biscuits, 2.3% ininternational business, 2.2% ingroceries and 2% in containers. Incontrast, volumes declined 3% inbeer and 4% in mineral waters asa result of unfavorable weather.Volumes were also down 1% infresh dairy products.

Changes in exchange rates, nota-bly for the dollar, peseta and lira,had a favorable impact equal to arise of 1.5% in sales or FF1,200million, while acquisitions andfirst-time consolidation of compa-nies added 2.5% or FF1,982 mil-lion. Changes in structure workedin the other direction: a number ofsecondary businesses were ex-cluded from sales, being accountedfor only under additional income,while recurrent promotionalexpense was deducted from thetotal. Together, these factors re-duced sales by 1% or FF857 million.

In terms of geographical break-down, sales growth (+1.6%) atconstant structure and exchangerates was generally weak inEurope, with sales showing aslight increase in France andSpain and a somewhat steeperrise in Italy, while there was adecline in Germany. Internationalbusiness – i.e., outside westernEurope – rose five times morequickly, putting on 7.9%.

WESTERN EUROPE +1.6%

DAIRY PRODUCTS +1.9%

GROCERY PRODUCTS - PASTA +1.3%

BISCUITS +4.1%

BEER +1.8%

MINERAL WATER -3.7%

CONTAINERS +2.2%

INTERNATIONAL +7.9%

GROUP TOTAL +2.7%

General improvementin margins

Fresh dairy products benefitedfrom favorable price trends de-spite more moderate marketgrowth. Operating income rose ahealthy 7.4% thanks to a combina-tion of lower prices for some rawmaterials, productivity gains, inparticular at Italian subsidiaryGalbani, and a good product mix.Operating margin thus increasedfrom 9.6% in 1995 to 10.2% in 1996.

Grocery products and pasta bene-fited from relatively favorablemarket trends for sauces andcondiments, infant and diet foods,and chilled and frozen ready-to-serve dishes. However conditionswere difficult, especially inFrance, for pasta and canneddishes, as a result of commercialproblems relating to the merger ofPanzani and William Saurin. Thedecline in earnings from this busi-ness segment exceeded gains inothers. As a result, overall oper-ating income fell 2.8% and oper-ating margin edged down from6.4% in 1995 to 6.3% in 1996.

Biscuits benefited from favorableprice trends thanks to productinnovation and restructuring ofoperations in France, northernEurope and the UK. In addition,sales of Greek subsidiaryPapadopolous were consolidatedfor the first time. Operatingincome rose 11.4% and operatingmargin edged up from 6.7% in1995 to 7% in 1996.

Beer sales were subject to wideswings. An unusually cool sum-mer brought a fall in volumes inmost European countries, butDecember sales in France surgedas retailers stocked up massivelyahead of the rise in excise onJanuary 1, 1997. All told, a 3%decline in unit growth volumesresulted in an 8% decline in oper-ating income, while operatingmargin fell from 13% in 1995 to11.7% in 1996.

Mineral water sales, down 4% inunit terms, also suffered from thecool weather, but margins bene-fited from a sharp decline in pricesfor PET and PVC used for pack-aging. Operating income thus rose5.5% and operating margin from12.4% in 1995 to 13.6% in 1996.

The containers division reapedthe rewards of productivity gainsin previous years. A decline insales of beer and soft drinks, theresult of cool weather, was offsetby orders from producers ofchampagne and spirits.

DAIRY PRODUCTS 25.7%

GROCERY PRODUCTS - PASTA 18.3%

BISCUITS 14.6%

BEER 8.7%

MINERAL WATER 8.0%

CONTAINERS 7.3%

INTERNATIONAL 17.4%

SALES BY BUSINESS DIVISION

FRANCE 41.5%

ITALY 13.0%

SPAIN 9.2%

GERMANY 5.7%

OTHER WESTERN EUROPEAN COUNTRIES 12.2%

EASTERN EUROPE 1.5%

NORTH AMERICA 5.7%

LATIN AMERICA 5.6%

ASIA-PACIFIC 5.0%

OTHER 0.6%

SALES BY MARKET

DAIRY PRODUCTS 34.8%

GROCERY PRODUCTS - PASTA 19.5%

BISCUITS 20.0%

BEVERAGES 18.3%

CONTAINERS 7.4%

SALES BY BUSINESS SEGMENT

DANONE SHARE PRICE AND THE PARIS MARKET (FF)

1992 1993 1994 1995 1996 1997

1400

1200

1000

800

600

DANONE

CAC 40

9

Brought to you by Global Reports

Operating income rose 10.2% andoperating margin increased from 10%in 1995 to 11.2% in 1996.

International sales include for thefirst time sales of dairy product sub-sidiaries in eastern Europe, Argentinaand China, biscuits and beer inChina, and mineral water inArgentina. Trends in existing busi-nesses varied. Declines in Argentinaand, to a lesser extent, the US werealmost offset by good performancesin Mexico, Brazil, Canada and Asia.Earnings for 1996 were adverselyaffected by the launch of “Dannon”mineral water in a large part of theUS. Operating income rose 42% over-all and operating margin improvedfrom 5.6% in 1995 to 6% in 1996.

All told, Group operating incomerose 6.5% from FF7,018 million in1995 to FF7,478 million in 1996, whileoperating margin was up from 8.8%to 8.9%.

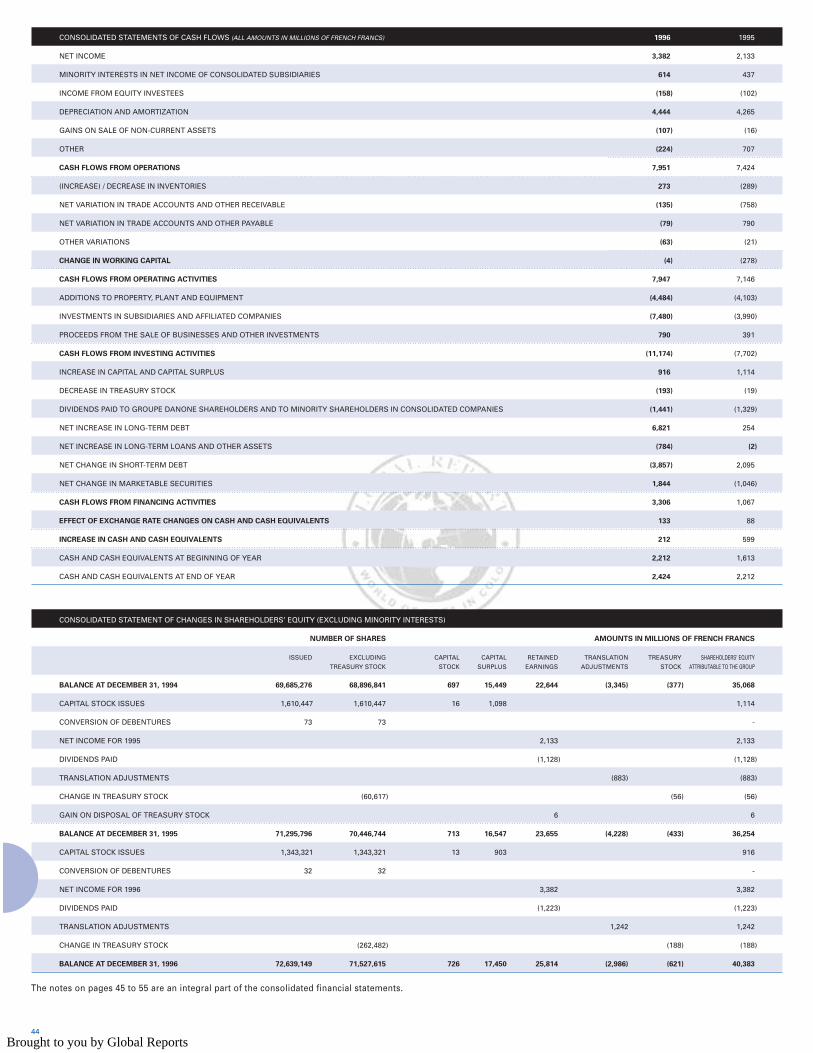

An 8% rise in net income

Despite high investment, net interestexpense eased from FF1,254 millionin 1995 to FF1,245 million in 1996,thanks to the decline in interest rates.The average rate of corporate incometax borne by the Group rose from37.7% to 38.4%, mainly as a result ofrises in income in high-tax countriessuch as Italy. Minority interests haveincreased slightly at constant struc-ture, thus excluding the impact ofrestructuring provision in 1995.Income from companies accountedfor by the equity method rose sharplyas a result of improved earnings insome companies, as well as inclusionof new businesses – Clover in SouthAfrica and Aymoré in Brazil.

Net income showed a rise of 8% fromFF3,130 million (excluding restruc-turing provisions) in 1995 to FF3,382million in 1996. Earnings per sharerose 6% to FF46.33.

Investment reaches newhigh

Cash flows from operations increased7.1% from FF7,424 million in 1995 toFF7,951 million in 1996. Free cashflow – i.e., after capital spending –amounted to FF3,467 million.

Capital expenditure totalled FF4,484million, up from FF4,103 million in1995. Main investments included thelaunch of a new PET bottle for Volvicin France, construction of a newDannon factory at West Jordan, Utah,in the US, modernization of Diépal’splant in Steenvoorde, France, andextensions to biscuit and dairy prod-uct plants in France as well as to biscuit facilities in Germany.

In addition, new equipment was installed at three container-divisionsites in France.

Net investment in subsidiaries andaffiliates rose from FF3,990 million in1995 to a new record of FF7,480 mil-lion. This reflected total outlays ofFF4,300 million to buy out minorityinterests in Panzalim in France, Galbaniin Italy and San Miguel in Spain, whileacquisitions outside western Europereached FF2,254 million, comparedwith FF1,738 million in 1995.

Acquisitions for interna-tional expansion

A number of new acquisitions weremade in 1996, with the focus onemerging markets in China, Brazil,Argentina and South Africa. This wasalso the case, albeit to a lesserextent, in Israel and Morocco.

Danone Group thus acquired 36% ofClover, South Africa’s leading pro-ducer of dairy products with annualsales equal to FF2.4 billion. Otherpurchases included 20% of the dairyproducts division of Strauss, Israel’sleading firm in this sector with salesof FF750 million, and 20% of CentraleLaitière, an ONA subsidiary which isthe largest dairy product company inMorocco with sales of FF1.3 billion.

In China, the Group made its biggestsingle acquisition in the country todate: a controlling interest in thedairy division of Wahaha, China’s lead-ing producer of dairy-based bever-ages with sales of FF530 million.Wahaha is one of the few Chinesecompanies distributing products andfamiliar to consumers throughout thevast domestic market. Two brewerswere also purchased: Haomen, sectorleader in the northern province ofHebei, and Wuhan Dongxihu, leaderin the central province of Hubei.Together, these serve a population of100 million and generate annualsales of around FF400 million. Thesethree acquisitions double DanoneGroup’s presence in China.

In Latin America, it acquired an inter-est in Aymoré, which reports annualsales of FF550 million, consolidatingits position on the Brazilian biscuitmarket. Danone also took control ofAguas Minerales, Argentina’s leadingmineral-water company with sales ofFF150 million. In 1997, DanoneGroup’s 1995 joint venture withMastellone, Argentina’s leading dairyproduct company, currently represent-ing sales of FF1 billion, was extendedto include yogurt. As a result, Danone will become the top producerof dairy products in both North andSouth America, with operations inCanada, the United States, Mexico,Brazil and Argentina.

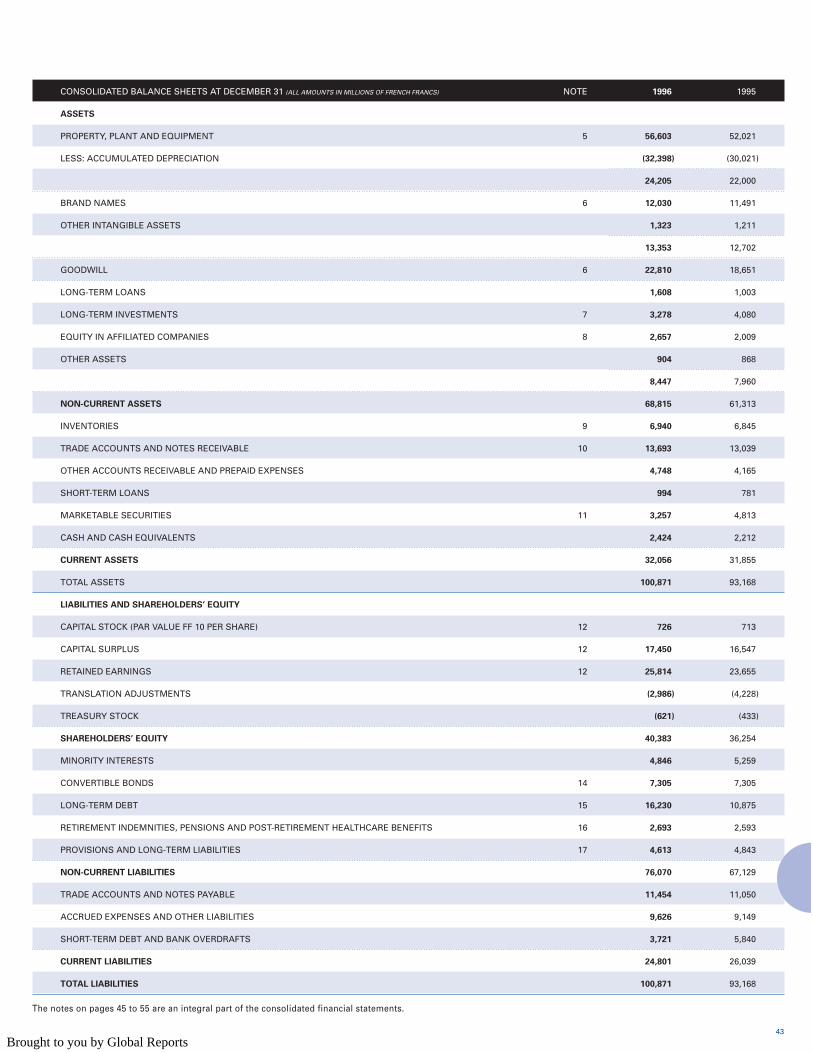

Rise in debt

The net financial borrowing ofDanone Group rose FF4.6 billion,from FF17 billion at the end of 1995to FF21.6 billion at the end of 1996.Much of this was due to the acquisi-tion of minority interests in Panzalimfor FF3 billion at the end of the year.The debt/equity ratio at year endstood at 30% if convertible bonds areincluded in equity.

Danone Group uses financial instru-ments to hedge against exchange-rate and interest-rate risks arisingfrom its industrial and commercialoperations. The net exposure of allsubsidiaries is managed on a central-ized basis by the Group financedepartment in accordance with theaims and principles laid down bygeneral management.

In concrete terms, exposure of sub-sidiaries to exchange-rate risk result-ing from commercial transactions inforeign currencies is first netted, andthe resulting net exposure is hedgedwith quality counterparties, mainlythrough forward contracts andoptions. As regards interest-rate risk,the Group’s finance departmentsuses swaps, caps, floors and Piborfutures to strike an overall balancebetween fixed and floating rates forthe Group’s net debt, in line withmanagement policy.

A difficult year on thestock market

In 1996, Danone shares fell 11.6%,while the CAC 40 index rose 23.7%.The low point for the year was FF677in September.

This mainly reflected investors’doubts on the Group’s capacity toreturn to satisfactory rates of earn-ings growth, given its focus onWestern Europe where consumptionremains slack and competition isfierce.

However, since the beginning of1997, Danone shares have picked up26.7%, with gains driven in particularby the announcement of 1996 earn-ings, while the CAC 40 index rose17.2% over the same period. Thepeak since the beginning of the yearwas FF955 and the low FF712. OnMarch 14, it closed at FF906 repre-senting market capitalization ofFF65.8 billion, which places Danonenumber eleven on the Paris Bourse.

Recent developments

The Group has acquired a 50% inter-est in Hayat, Turkey’s leading produc-er of bottled water, within the frame-work of a joint venture in partnershipwith the Sabanci group. Hayat reported sales of approximately FF90 million in 1996.

Outlook

The earnings improvement achievedin 1996 should continue in 1997thanks to more favorable trends insales prices backed by increasedcommitment to product innovationand significant productivity gains.Prices for raw materials including inparticular grain and plastics shouldalso remain on a favorable track. In addition, the impact of currencytranslation could be positive for theGroup. On current projections, the overall effect of shifts in interestrates should be neutral.

10

Brought to you by Global Reports

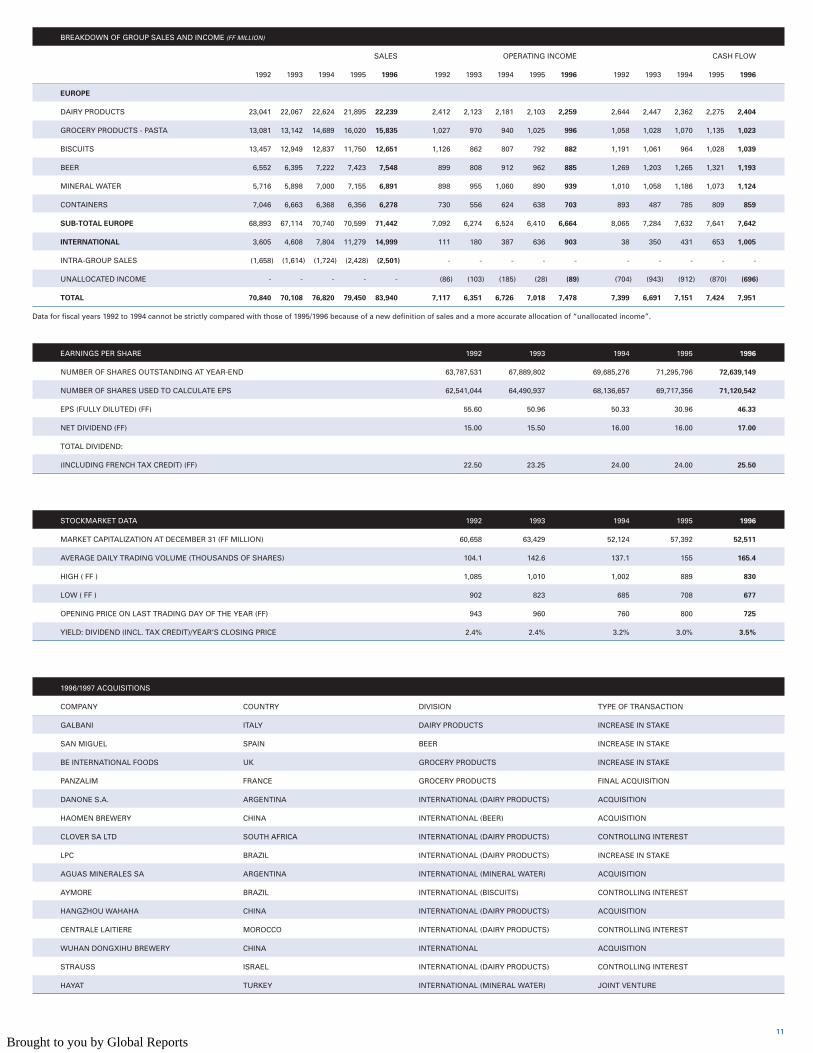

BREAKDOWN OF GROUP SALES AND INCOME (FF MILLION)

SALES OPERATING INCOME CASH FLOW

1992 1993 1994 1995 1996 1992 1993 1994 1995 1996 1992 1993 1994 1995 1996

EUROPE

DAIRY PRODUCTS 23,041 22,067 22,624 21,895 22,239 2,412 2,123 2,181 2,103 2,259 2,644 2,447 2,362 2,275 2,404

GROCERY PRODUCTS - PASTA 13,081 13,142 14,689 16,020 15,835 1,027 970 940 1,025 996 1,058 1,028 1,070 1,135 1,023

BISCUITS 13,457 12,949 12,837 11,750 12,651 1,126 862 807 792 882 1,191 1,061 964 1,028 1,039

BEER 6,552 6,395 7,222 7,423 7,548 899 808 912 962 885 1,269 1,203 1,265 1,321 1,193

MINERAL WATER 5,716 5,898 7,000 7,155 6,891 898 955 1,060 890 939 1,010 1,058 1,186 1,073 1,124

CONTAINERS 7,046 6,663 6,368 6,356 6,278 730 556 624 638 703 893 487 785 809 859

SUB-TOTAL EUROPE 68,893 67,114 70,740 70,599 71,442 7,092 6,274 6,524 6,410 6,664 8,065 7,284 7,632 7,641 7,642

INTERNATIONAL 3,605 4,608 7,804 11,279 14,999 111 180 387 636 903 38 350 431 653 1,005

INTRA-GROUP SALES (1,658) (1,614) (1,724) (2,428) (2,501) - - - - - - - - - -

UNALLOCATED INCOME - - - - - (86) (103) (185) (28) (89) (704) (943) (912) (870) (696)

TOTAL 70,840 70,108 76,820 79,450 83,940 7,117 6,351 6,726 7,018 7,478 7,399 6,691 7,151 7,424 7,951

Data for fiscal years 1992 to 1994 cannot be strictly compared with those of 1995/1996 because of a new definition of sales and a more accurate allocation of “unallocated income”.

EARNINGS PER SHARE 1992 1993 1994 1995 1996

NUMBER OF SHARES OUTSTANDING AT YEAR-END 63,787,531 67,889,802 69,685,276 71,295,796 72,639,149

NUMBER OF SHARES USED TO CALCULATE EPS 62,541,044 64,490,937 68,136,657 69,717,356 71,120,542

EPS (FULLY DILUTED) (FF) 55.60 50.96 50.33 30.96 46.33

NET DIVIDEND (FF) 15.00 15.50 16.00 16.00 17.00

TOTAL DIVIDEND:

(INCLUDING FRENCH TAX CREDIT) (FF) 22.50 23.25 24.00 24.00 25.50

STOCKMARKET DATA 1992 1993 1994 1995 1996

MARKET CAPITALIZATION AT DECEMBER 31 (FF MILLION) 60,658 63,429 52,124 57,392 52,511

AVERAGE DAILY TRADING VOLUME (THOUSANDS OF SHARES) 104.1 142.6 137.1 155 165.4

HIGH ( FF ) 1,085 1,010 1,002 889 830

LOW ( FF ) 902 823 685 708 677

OPENING PRICE ON LAST TRADING DAY OF THE YEAR (FF) 943 960 760 800 725

YIELD: DIVIDEND (INCL. TAX CREDIT)/YEAR’S CLOSING PRICE 2.4% 2.4% 3.2% 3.0% 3.5%

1996/1997 ACQUISITIONS

COMPANY COUNTRY DIVISION TYPE OF TRANSACTION

GALBANI ITALY DAIRY PRODUCTS INCREASE IN STAKE

SAN MIGUEL SPAIN BEER INCREASE IN STAKE

BE INTERNATIONAL FOODS UK GROCERY PRODUCTS INCREASE IN STAKE

PANZALIM FRANCE GROCERY PRODUCTS FINAL ACQUISITION

DANONE S.A. ARGENTINA INTERNATIONAL (DAIRY PRODUCTS) ACQUISITION

HAOMEN BREWERY CHINA INTERNATIONAL (BEER) ACQUISITION

CLOVER SA LTD SOUTH AFRICA INTERNATIONAL (DAIRY PRODUCTS) CONTROLLING INTEREST

LPC BRAZIL INTERNATIONAL (DAIRY PRODUCTS) INCREASE IN STAKE

AGUAS MINERALES SA ARGENTINA INTERNATIONAL (MINERAL WATER) ACQUISITION

AYMORE BRAZIL INTERNATIONAL (BISCUITS) CONTROLLING INTEREST

HANGZHOU WAHAHA CHINA INTERNATIONAL (DAIRY PRODUCTS) ACQUISITION

CENTRALE LAITIERE MOROCCO INTERNATIONAL (DAIRY PRODUCTS) CONTROLLING INTEREST

WUHAN DONGXIHU BREWERY CHINA INTERNATIONAL ACQUISITION

STRAUSS ISRAEL INTERNATIONAL (DAIRY PRODUCTS) CONTROLLING INTEREST

HAYAT TURKEY INTERNATIONAL (MINERAL WATER) JOINT VENTURE

11

Brought to you by Global Reports

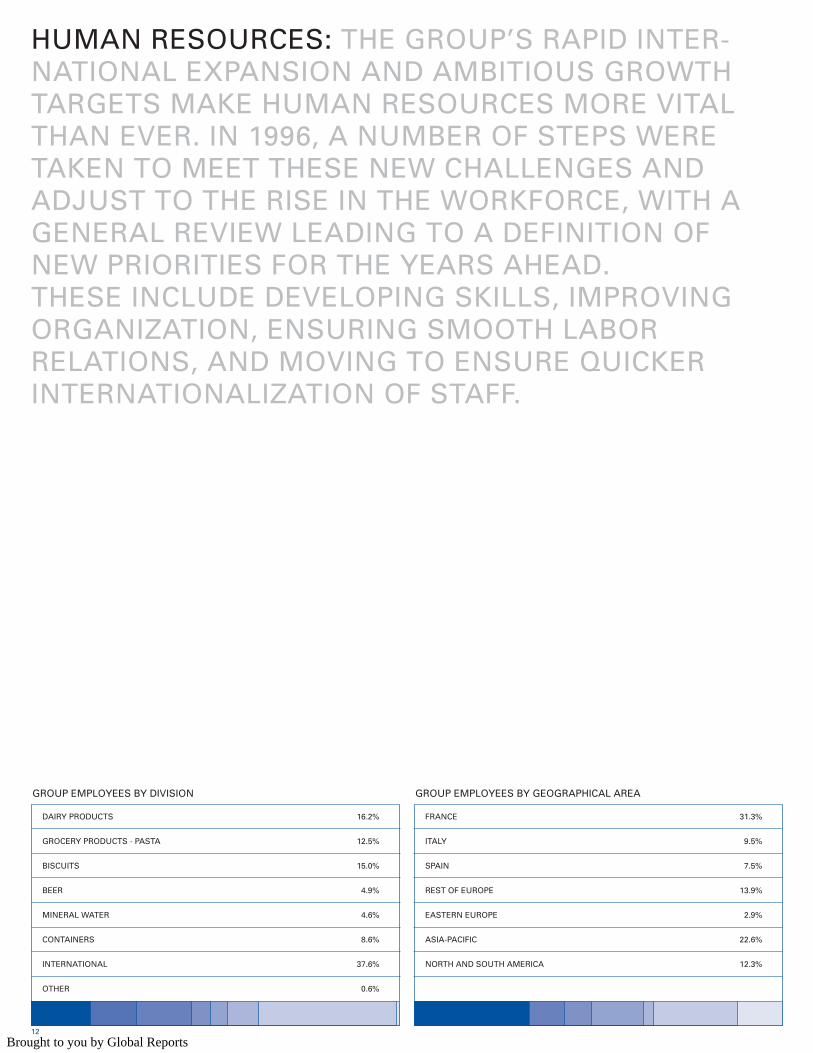

HUMAN RESOURCES: THE GROUP’S RAPID INTER-NATIONAL EXPANSION AND AMBITIOUS GROWTHTARGETS MAKE HUMAN RESOURCES MORE VITALTHAN EVER. IN 1996, A NUMBER OF STEPS WERE TAKEN TO MEET THESE NEW CHALLENGES AND ADJUST TO THE RISE IN THE WORKFORCE, WITH AGENERAL REVIEW LEADING TO A DEFINITION OFNEW PRIORITIES FOR THE YEARS AHEAD. THESE INCLUDE DEVELOPING SKILLS, IMPROVING ORGANIZATION, ENSURING SMOOTH LABOR RELATIONS, AND MOVING TO ENSURE QUICKER INTERNATIONALIZATION OF STAFF.

DAIRY PRODUCTS 16.2%

GROCERY PRODUCTS - PASTA 12.5%

BISCUITS 15.0%

BEER 4.9%

MINERAL WATER 4.6%

CONTAINERS 8.6%

INTERNATIONAL 37.6%

OTHER 0.6%

GROUP EMPLOYEES BY DIVISION

FRANCE 31.3%

ITALY 9.5%

SPAIN 7.5%

REST OF EUROPE 13.9%

EASTERN EUROPE 2.9%

ASIA-PACIFIC 22.6%

NORTH AND SOUTH AMERICA 12.3%

GROUP EMPLOYEES BY GEOGRAPHICAL AREA

12

Brought to you by Global Reports

Developing skills andreshaping organizationfor optimum efficiency

Professional know-how is the basisof competitiveness and efficiency. Inrecognition of this, commitment totraining was even more in evidencein 1996. There was a particular focuson continued upgrading of interna-tional management programs,which have been attended by 500staff members from all parts of theworld. In addition, a number of newinitiatives were taken: - specially designed programs tomeet needs in emerging markets,with areas covered including market-ing in China and sales, productionand administration in easternEurope- innovative programs for adminis-trative and production staff. To taketwo examples, French employeeswere given the opportunity to gainnew educational qualifications inrecognition of their professionalexpertise, while safety training wasa systematic priority for newlyacquired businesses. In 1996, Danone Group launched anoverhaul of organization. Prioritiesincluded a more customer-orientedapproach in sales and administra-tion, upgrading of IT systems, andgreater flexibility in production andproduction cycles. In each area,human resource departments atgroup level and in individual subsi-diaries were an important source ofmomentum, making essential contri-butions, for example, to the mod-ernization drive in Galbani’s salesstructures, and to the reorganizationof production at the three plants ofSpanish brewer San Miguel.

Promoting smooth laborrelations

The statement “Business successcan only be lasting if it is also a suc-cess in terms of labor relations”,underscores Danone Group’s con-tinuing commitment to this dualgoal. In 1996, this philosophy tookconcrete shape in three areas in par-ticular: solutions adopted for over-staffing; youth training and employ-ment; and commitment to corporatecitizenship.Productivity gains are a businessimperative and can involve a needfor staff cuts. When this happens inDanone Group companies, humanresource departments move quicklyto apply a founding principle of theGroup, which is to help eachemployee find a new job, either inanother part of the Group or withanother employer. In France, a solu-tion has been found for 96% of allemployees affected by suchchanges.

For Group companies, involvementin the community is an importantway to build local ties, while corpo-rate culture gains as staff membersrally to a common cause. In 1996,job search and creation schemesand business development pro-grams were extended outsideFrance – an example being recon-version of the Danone site atUlzama in Spain – while a numberof new projects were launched.These included: - construction of children’s nurseriesin eastern Europe- creation of the KronenbourgFoundation, which contributes tothe development of troubled urbanand rural areas in France by helpingset up neighborhood shops- launch of the “BSN Initiatives”program by BSN Emballage to helpsmall-business creation in France.While Danone Group clearly cannotremedy the painful problem ofyouth unemployment on its own, itbelieves that it should set anexample whenever possible in allthe countries where it operates.Since its own capacity to employyoung people is necessarily limited– although 200 joined the Group inwestern Europe during 1996 – themain focus is thus on training andapprenticeship schemes. These involve: - acceptance of interns on job-training programs in countrieswhere these exist; in France 500young people were accepted in 1996 - training for school dropouts (inSpain, the UK and Ireland)- training for young graduates inAsia and eastern Europe, in particu-lar the Czech Republic, with aroundone hundred benefiting in 1996. Danone Group aims to step up itsefforts in this area in 1997, withplans to offer some 2,000 youngpeople – equal to 2% of its total staff– a job, an internship or other training.

Internationalization ofhuman resources

Danone Group’s rapid internationalexpansion poses a number of strate-gic challenges in the field of humanresources. In particular, ways mustbe found to recruit the best avail-able managers on emerging mar-kets, and to ensure that all groupcompanies share the same cultureand methods of operation. In re-sponse to these challenges, and toadapt to the new size of the groupand the growing importance of cer-tain geographical areas, the corpo-rate Human Resource Departmentintroduced a number of organiza-tional changes at the end of 1996.These involved in particular alloca-tion of additional resources to LatinAmerica.

In emerging economies, the short-age of high-level managers com-bining technical expertise and thecapacity to adapt to the DanoneGroup culture has led to the adop-tion of special measures in additionto expatriation programs — 350Danone executives are currentlyworking away from their homecountry. These measures include:- internships for young managersfrom Asia and eastern Europe- partnerships with universities,notably in Shanghai, patterned afterarrangements already existing inEurope.

Finally Danone Group has begunrounding out and extending proce-dures to ensure that newly acquiredsubsidiaries adopt its methods ofoperation, values and culture. Theseinclude in particular the develop-ment of intensive programs for themanagers of new subsidiaries and,as was recently the case inArgentina, training in evaluation ofskills and management of change.

13

Brought to you by Global Reports

CROSS-COMPANY MARKETING INITIATIVESWORLDWIDE PROMOTION OF THE “DANONE” BRAND AND THE SEARCH FOR NEW FORMS OF COMMUNICATIONS WITH CONSUMERS LED TO A VARIETY OF CROSS-COMPANY MARKETING INITIATIVES IN 1996.

1998 World Cup – cross-company

marketing enters the international

arena

Internationally, the first major initia-tive was the partnership agreementsigned in September with the FrenchCommittee for the Organization of theFootball World Cup. “Danone” freshdairy products will be officially asso-ciated with the 1998 World Cup to beheld in France, placing it among thevery few brands represented in whatis the world’s greatest media event,expected to represent an accumulatedtotal of 37 billion TV contacts.

A clear message on product safety

and health, 24 hours a day

In response to constant shifts inconsumer attitudes and relatedexpectations of major brands, at theend of 1996 Danone set up France’sfirst consumer advice line, “DanoneConseils”. Representing all Groupcompanies in France, this service isaccessible 24 hours a day, seven daysa week. Consumers phoning in canget advice on all aspects of nutritionfrom counsellors who include expertdieticians.

“Danoé”: representing Danone

brands in two million French homes

“Danoé”, a quarterly magazine de-voted to Danone brands which firstappeared in 1995, reflects a similaremphasis on direct communications.It currently circulates to two millionFrench households – out of a total ofsome 20 million – covered by aconsumer database built up over thepast two years. This makes it themost widely read family magazine ofits type in France. Similarly, Danone’s“Bingo” promotional game represent-ing all the Group’s French companiesand “Gran Premio Grandi Marche”,the Italian equivalent, scored suc-cesses once again in 1996.

Wherever people like to eat

More generally, Danone Group isintent on rapidly expanding the pres-ence of its key brands whereverpeople eat away from home or expectfood to be available. To this end, atask force has been set up to makethe most of potential for synergiesbetween different group activities.The same team will also be respon-sible for the development of elec-tronic home shopping, a fast-growingfield in which ever more experimentsare under way around the world.Another example of moves in thisdirection was the signature in early1997 of an agreement with theFuturoscope theme park, a favoriteattraction with French families.

'1994 IS

L T

M

W O R L D C U P

OFFICIAL FRESH DAIRY PRODUCTS

14

Brought to you by Global Reports

ENVIRONMENTRESPECT FOR THE ENVIRONMENT IS A CORE VALUE OF DANONE GROUP. IN KEEPING WITH THISCOMMITMENT, MAJOR PROGRAMS HAVE BEEN SET UP IN THREE AREAS: PACKAGING, INDUSTRIALSITES, AND DEVELOPMENT OF ENVIRONMENTALAWARENESS AMONG SUPPLIERS OF AGRICULTURALPRODUCTS.

RESEARCH AND DEVELOPMENTIN 1996, DANONE GROUP INCREASED RESEARCH AND DEVELOPMENT EXPENDITURES 6.7% FROM THEPREVIOUS YEAR TO A TOTAL OF FF667 MILLION, WHILE THE NUMBER OF STAFF INVOLVED REACHED1,128 WORLDWIDE.

Research is organized around five

major programs conducted by the

group in association with private and

public sector bodies — one is de-

voted to taste, texture and perception,

a second to food safety, a third to

molecular biology and biotechnology,

a fourth to process engineering, and

the fifth to nutrition.

Food safety, a growing concern forboth consumers and the food indus-try as a whole, is the top priority andDanone is intent on consolidating itsknow-how in this field. In this regard,a number of 1996 projects focusedon agrochemicals — studying, forexample, their impact on crops aswell as the effects of veterinary treat-ment on raw materials used in theindustry. Findings will lead to thedefinition of even stricter requirementsfor suppliers, as well as rules on thetraceability of raw materials and thesafety of production processes.

Research also continued in toxi-cology, in particular the causes ofchanges in food on contact with differ-ent types of packaging. In microbio-logy, the focus was on rapid detec-tion and monitoring of microorganisms such as bacteria andviruses, as well as the reactions ofpathogens to different types of environment.

Danone Group has long been in-volved in the creation and operationof organizations for the recycling ofpackaging. In 1996, it took this onestep further by teaming up with othercompanies to found a PackagingCouncil. The Council’s goals are theadoption of a code of conduct toreduce the quantity of packaging atsource, and promotion of publicinformation. Also in 1996, Frenchauthorities renewed approval for sixyears of the Eco-Emballages andAdelphe collection and processingprograms, confirming the viability of

this approach to the disposal of house-hold waste. Finally, glass recycling inFrance showed a further increase of4% on the previous year.Europe-wide, similar bodies were setup in Spain and Portugal, and theactivities of existing entities wereexpanded.

Action plans resulting from the circu-lation of the Danone Group’s corpo-rate Charter for the Environmentconcerned 140 industrial sites aroundthe world. In each case, managementreviewed the current status of the

site, then drew up plans for improve-ments, in particular concerning theuse of natural resources, water andenergy, and waste treatment. In 1997,the drive to increase awareness ofenvironmental issues at Group pro-duction sites will be further extendedand systematically promoted.Progress to date illustrates the com-patibility of environmental qualitywith efforts to raise productivity.

Danone Group is aware of the needto extend its commitment to itssources of supply. It thus promotes

rational farming methods that recon-cile profitability with product qualityand respect for the environment.Danone Group supports theEuropean Integrated Farming initia-tive through industry associationFARRE – Forum de l’AgricultureRaisonnée Respectueuse del’Environnement, or forum for ratio-nal farming and respect for the envi-ronment. Looking ahead, it is alsocontinuing to explore possibilitiesoffered by biotechnology.

15

Brought to you by Global Reports

DANONE INSTITUTESATTITUDES TO NUTRITION VARY ENORMOUSLY, REFLECTING CONSUMERS' AGE AND SOCIETY: CHILDREN, TEENAGERS AND THE ELDERLY TAKE RADICALLY DIFFERENT APPROACHES TO NUTRITION,AS DO PEOPLE IN, FOR EXAMPLE, ASIA AND NORTHAMERICA.REFLECTING THIS DIVERSITY, THE FIRST DANONEINSTITUTE—SET UP IN FRANCE IN 1991— WASFOLLOWED BY SEVEN MORE, IN SPAIN, ITALY,BELGIUM, GERMANY, THE CZECH REPUBLIC, POLANDAND THE UNITED STATES.THESE INSTITUTES SPONSOR RESEARCH INTO HEALTHY EATING, DISSEMINATE THEIR FINDINGS TO RAISE PUBLIC AWARENESS OF THE IMPORTANCEOF DIET AND FITNESS, AND PROMOTE FOOD QUALITY IN GENERAL. AFTER FOCUSING INITIALLY ON INFANTS AND CHILDREN, THE INSTITUTE IS NOW TURNING TO SENIOR CITIZENS' NEEDS. AT THE END OF 1997, THE FIRST DANONE INTERNATIONAL NUTRITIONPRIZE WILL BE AWARDED TO A RESEARCHER WHOSEWORK HAS MADE A MAJOR CONTRIBUTION TO HUMAN NUTRITION.

16

Brought to you by Global Reports

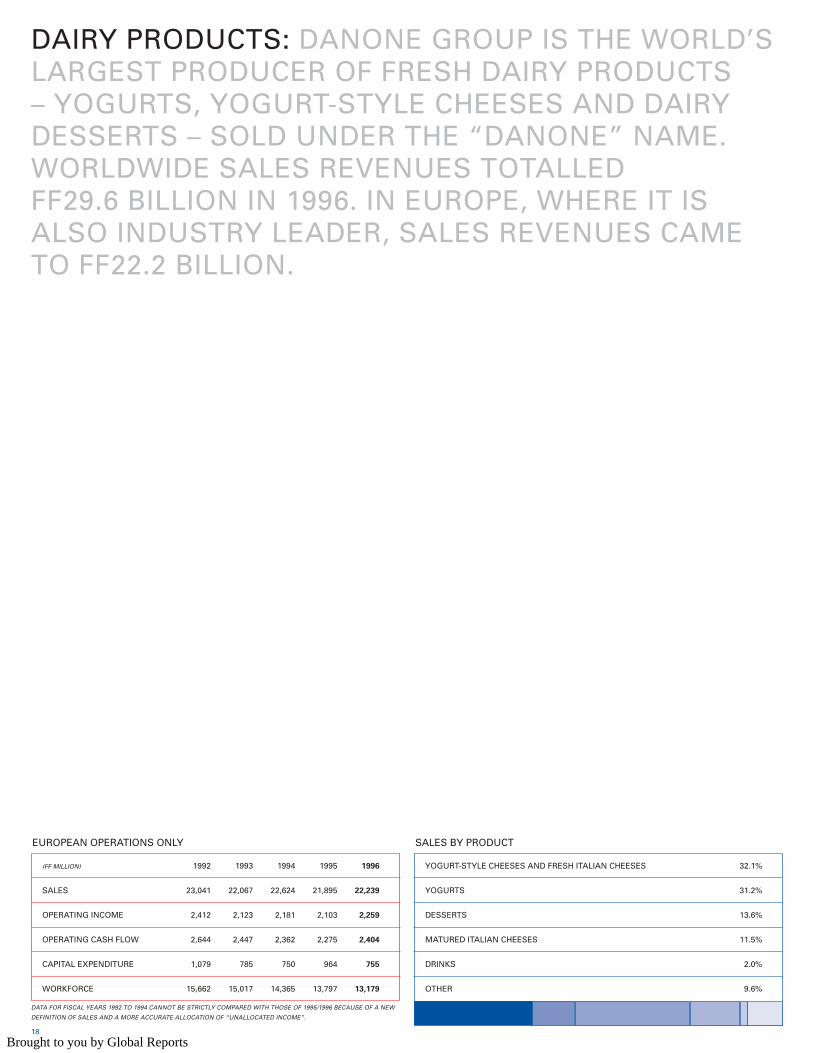

DAIRY PRODUCTS: DANONE GROUP IS THE WORLD’SLARGEST PRODUCER OF FRESH DAIRY PRODUCTS– YOGURTS, YOGURT-STYLE CHEESES AND DAIRYDESSERTS – SOLD UNDER THE “DANONE” NAME.WORLDWIDE SALES REVENUES TOTALLED FF29.6 BILLION IN 1996. IN EUROPE, WHERE IT ISALSO INDUSTRY LEADER, SALES REVENUES CAMETO FF22.2 BILLION.

YOGURT-STYLE CHEESES AND FRESH ITALIAN CHEESES 32.1%

YOGURTS 31.2%

DESSERTS 13.6%

MATURED ITALIAN CHEESES 11.5%

DRINKS 2.0%

OTHER 9.6%

EUROPEAN OPERATIONS ONLY

(FF MILLION) 1992 1993 1994 1995 1996

SALES 23,041 22,067 22,624 21,895 22,239

OPERATING INCOME 2,412 2,123 2,181 2,103 2,259

OPERATING CASH FLOW 2,644 2,447 2,362 2,275 2,404

CAPITAL EXPENDITURE 1,079 785 750 964 755

WORKFORCE 15,662 15,017 14,365 13,797 13,179

SALES BY PRODUCT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.

18

Brought to you by Global Reports

19

Brought to you by Global Reports

In 1996, increasing efforts were put

into the development of products

designed for Europe-wide distribu-

tion. Despite slack growth in market

volumes, sales prices were much

more favorable than in the previous

year. Earnings also got a lift

from productivity gains in most

companies, particularly at Italian

subsidiary Galbani.

Sales and earnings

Division sales rose 1.6% to FF22.2billion in 1996, while at constantstructure and exchange rates therewas a 1.9% increase. Sales rose inmost areas, except in Germany andAustria. At Galbani, the eliminationof some secondary lines from itsproduct range slowed sales growth.

Operating income climbed 7.4% andoperating margin 0.6 of a percent-age point thanks to improved salesprices. Productivity gains also helped,notably at Galbani, which continuedrestructuring of production andlogistics while narrowing the focusof marketing efforts to strategiclines. In Spain, Danone began re-organizing distribution, contractinglogistics out in some parts of thecountry and revamping its salesforce. In France, industrial restruc-turing, in particular closure of plantsat Seclin and Strasbourg, was heldup, mainly for legal reasons, in1996, but will go ahead in 1997.

At the same time, raw materialcosts, mostly for packaging, werelower in 1996 than in 1995. Finally,previously smaller operations suchas those of Danone in Portugal andthe Netherlands made a more sig-nificant contribution to earnings.

Market trends and newproducts

Volume growth was generally mod-erate on Danone’s core Europeanmarkets during 1996, with slightdeclines in France and Italy offset bymodest rises in Germany, Spain andBelgium. However vigorous market-ing by Group companies brought animprovement in sales prices and asa result sales revenues rose morequickly than in 1996. Europe-wide,market share changed little,although in Italy it increased, consoli-dating Danone’s market leadership.

Innovation and growth were most inevidence in products including fruityogurts, desserts, specialties forchildren, and lines aimed at thehealth conscious. In these segmentsnew launches and relaunches madea significant contribution to rises insales and earnings. “Danone etFruits” in France, “Jahreszeit” inGermany and “Danone Frutas” inPortugal strengthened the Group’spositions on the market for fruityogurts.

Additions to the “Entremets CharlesGervais” range of traditional des-serts were well received in France,as were “Tiramisù”, “CrèmeCaramel” and “Profiterolles” linesin Italy, and the new “Dany Sahne”range in Germany.

In children’s products, a fast-expanding segment, the biglaunches of the year were “KidCréation” in France, “Mi PrimerDanone” in Spain and “JuniorSuper Coppa” in Italy.

Growth was brisk in health foodsthanks to the success of “Actimel”,launched in yogurt and drink for-mats in Germany during 1996, aswell as to the continuation of strongperformances in Belgium and, evenmore, Spain, with “CholesterolControl” doing particularly well.

Low-cal lines including “Taillefine”in France, “Vitasnella” in Italy,“Desnatado” in Spain and “CorposDanone” in Portugal scored furthergains.

The launch of new yogurt mousseproducts in Spain and France wasanother success in 1996.

In Italy, demand for cheese wassteady in volume during 1996 andGalbani held onto its share of themarket. The company narrowed itsfocus to strategic lines with freshlaunches of revamped “Galbanino”lines and “Vallelata” mozzarella proving a big success. Sales of tradi-tional cheeses under the “SelezioneGalbani” name remained on the rise.

Galbani’s pork products continuedto make headway on a steadydomestic market and exports wereup 5%.

20

Brought to you by Global Reports

21

Brought to you by Global Reports

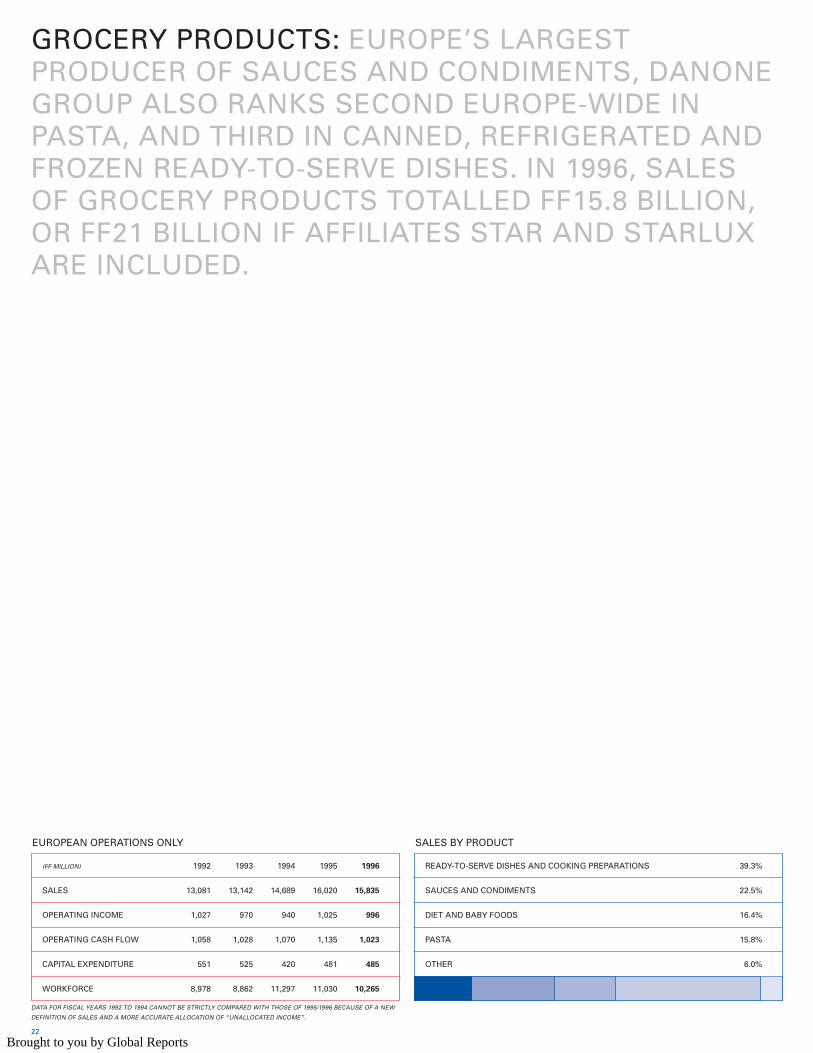

GROCERY PRODUCTS: EUROPE’S LARGEST PRODUCER OF SAUCES AND CONDIMENTS, DANONEGROUP ALSO RANKS SECOND EUROPE-WIDE INPASTA, AND THIRD IN CANNED, REFRIGERATED ANDFROZEN READY-TO-SERVE DISHES. IN 1996, SALES OF GROCERY PRODUCTS TOTALLED FF15.8 BILLION,OR FF21 BILLION IF AFFILIATES STAR AND STARLUXARE INCLUDED.

READY-TO-SERVE DISHES AND COOKING PREPARATIONS 39.3%

SAUCES AND CONDIMENTS 22.5%

DIET AND BABY FOODS 16.4%

PASTA 15.8%

OTHER 6.0%

EUROPEAN OPERATIONS ONLY

(FF MILLION) 1992 1993 1994 1995 1996

SALES 13,081 13,142 14,689 16,020 15,835

OPERATING INCOME 1,027 970 940 1,025 996

OPERATING CASH FLOW 1,058 1,028 1,070 1,135 1,023

CAPITAL EXPENDITURE 551 525 420 481 485

WORKFORCE 8,978 8,862 11,297 11,030 10,265

SALES BY PRODUCT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.

22

Brought to you by Global Reports

23

Brought to you by Global Reports

24

Brought to you by Global Reports

During the year, trends were satisfac-

tory for sauces and condiments,

infant foods and adult diet foods.

Major restructuring in the field of fro-

zen and refrigerated ready-to-serve

dishes was designed to make

“Marie” France’s leading brand for

this type of products. However, the

year proved difficult for canned

ready-to-serve dishes in France and

for pasta, which experienced difficult

trading conditions.

Sales and earnings

Division sales declined 1.2% toFF15.8 billion in 1996, but showed arise of 1.3% at constant structure andexchange rates. Operating incomedeclined 2.8% overall. Good perform-ances from infant foods and saucesdid not suffice to offset lower earn-ings on pasta and ready-to-servedishes. As a result, there was a slightdecline in operating margin.

A number of steps were taken toimprove productivity, in production,logistics and sales, as well as admini-stration and portfolios of productsand brands. In pasta and ready-to-serve dishes, Panzani and WilliamSaurin merged, while restructuringcontinued in Germany, in particularat the Seesen factory, and in Spain,where format and prices of the“La Familia” and “Ardilla” rangeswere brought into line. In sauces andcondiments, completion of the mergerof Liebig Maille with Amora broughtmajor savings. Turning to operationsin the UK, HP Foods merged with BE International and headquarters atMarket Harborough closed. HP’s canned foods business was soldto British group Hillsdown at the beginning of the year.

In refrigerated and frozen ready-to-serve dishes, the merger of Fréalimwith Générale Traiteur is to be fol-lowed by that of Gorcy and Vivagel in1997, making for greater overall com-petitiveness in frozen foods.

The “Marie” brand has replaced“Honoré Janin Traiteur” for refriger-ated ready-to-serve dishes and“Liebig” for soups, while the“Stoeffler” brand for Alsatian special-ties has been replaced by “La Tabledu Maître Kanter” with an eye onsynergies with the Group’s well-known “Kanterbräu” beer.

Finally, in Italy, Star continued rede-ployment to focus on core products –sauces, cooking preparations andinfant foods.

Markets trends and newproducts

Sauces, condiments and cooking

preparations

French demand for sauces, condi-ments and cooking preparationsremained on the rise in 1996, andLiebig Maille Amora increased itsshare of the market for “moderncondiments”, in particular mayon-naises. “Traditional condiments”, inparticular vinegar, fared less well, butthe “Pur Soup” range of vacuum-packed long shelf-life soups made astrong showing.

The Group’s range of heat-and-servesauces was rounded out with thelaunch of Amora’s “Goûtez leMonde” range. A full line-up of refrig-erated sauces including sauce tartare,sauce béarnaise and mayonnaiseswas also put on the market.

In the UK, market share of “HP”brand brown sauce and “Amoy”brand Asian specialties headed upwhile “Lea & Perrins” demonstratedits flair with the launch of its “5-minute marinade”.

Diet and infant foods

The number of births in France roseby nearly 10,000 in 1996, lendingadded momentum to sales alreadyboosted by innovative new productsthat included the “Blédina Danone”range of refrigerated dairy products,a big success. At the same time,innovations from earlier years,

including “Blédilait” formula,“Blédichef” heat-and-serve special-ties, and “Blédidéj” cereals, contin-ued to gain ground.

In Spain, sales of baby foods in glassjars and “Blédina” formula showed avigorous rise.

In Italy, Star launched a number ofnew products including “Latte Bravo”under its “Mellin” brand, whichconsolidated its overall position inthe course of the year.

In Belgium, infant foods in glass jarsswitched from the “Blédina” to the“Danone” brand at the end of theyear.

Trends were also firm on the Frenchmarket for diet foods and the“Gayelord Hauser” brand did verywell. Its product offering widenedduring the year with the launch of the“Athlon” high-energy sports drinkand “Bio Vivre” products, a range ofnatural-agriculture products takenover by the Group.

Pasta

The Group’s share of a slightly largerEuropean market showed a moderatedecline.

Despite considerable competitivepressure, Panzani held onto its posi-tion on the French market and suc-cessfully launched “Maestria” quick-cooking pasta and “Pâtes Fantaisies”.

In Germany, the “Birkel no. 1” rangemade further progress, improving theGroup’s market position.

In Italy, “Agnesi” consolidated itsposition at the top end of the market,and its “Flora” range of pre-cookedrice made a highly satisfactory showing.

Finally, in Spain, 1996 saw the launchof the “Fantasia” range, while“Ardilla” and “La Familia” pooledcommunications and adopted a jointmarketing strategy.

Ready-to-serve dishes

French demand for frozen and refrig-erated ready-to-serve dishes contin-ued rising in 1996, although growthslowed to 4.5% and 15%, respec-tively. In product innovation, high-lights included the launch of“Panzani” fresh pasta sold withaccompanying sauces, and the“Panini” range of frozen Italian-stylesandwiches. In addition, a number ofextensions to ranges of snacks, pizzas and ready-to-serve dishes werelaunched under the “Marie” name.

In Spain, “La Cocinera” increased itsmarket share, partly thanks to thelaunch of a number of new dishes.During the year, the Spanish marketfor ready-to-serve dishes grew 7%.

Conditions were tougher for cannedready-to-serve dishes in both France,where demand showed a significantdecline, and Germany, where sales ofbeef products suffered from fearsover BSE. A major drive was under-taken to adapt recipes to consumerexpectations.

25

Brought to you by Global Reports

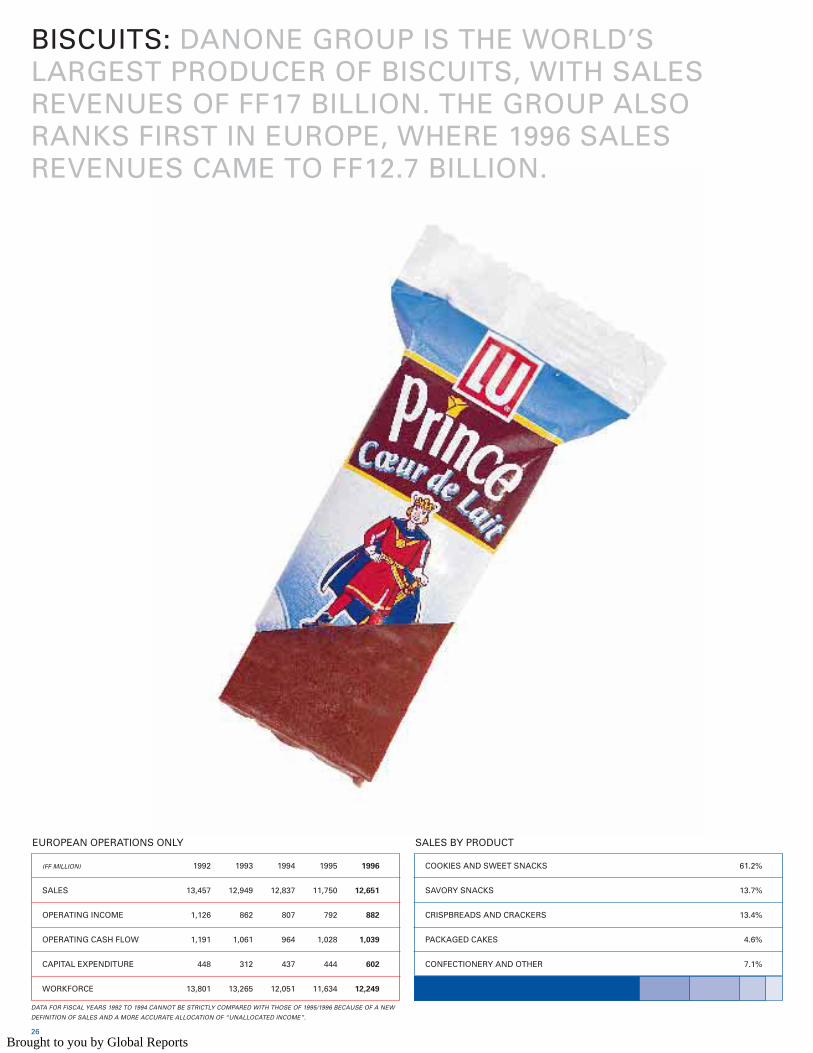

BISCUITS: DANONE GROUP IS THE WORLD’S LARGEST PRODUCER OF BISCUITS, WITH SALES REVENUES OF FF17 BILLION. THE GROUP ALSORANKS FIRST IN EUROPE, WHERE 1996 SALES REVENUES CAME TO FF12.7 BILLION.

COOKIES AND SWEET SNACKS 61.2%

SAVORY SNACKS 13.7%

CRISPBREADS AND CRACKERS 13.4%

PACKAGED CAKES 4.6%

CONFECTIONERY AND OTHER 7.1%

EUROPEAN OPERATIONS ONLY

(FF MILLION) 1992 1993 1994 1995 1996

SALES 13,457 12,949 12,837 11,750 12,651

OPERATING INCOME 1,126 862 807 792 882

OPERATING CASH FLOW 1,191 1,061 964 1,028 1,039

CAPITAL EXPENDITURE 448 312 437 444 602

WORKFORCE 13,801 13,265 12,051 11,634 12,249

SALES BY PRODUCT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.

26

Brought to you by Global Reports

After systematically reinvesting pro-

ductivity gains in product revamping

over the three previous years, in 1996

the Group turned its attention to

innovation. Improved sales volumes

and price trends brought a fresh rise

in operating margin.

Sales and earnings

European biscuit sales were up 7.7%to FF12.7 billion in 1996, while theincrease at constant structure andexchange rates was 4.1%. Operatingincome rose 11.4% and operatingmargin 0.3 of a percentage point.

In France, the merger of LU and Belinled to significant savings with the clo-sure of one head office and imple-mentation of joint industrial and salesorganization. Similarly, the “LU”brand is to be gradually extended toall French ranges of sweet and savorybiscuits and pastries. Administrativeresources were also pooled for enti-ties operating in Belgium, theNetherlands, Germany and Austria.The Amstetten factory in Austria wasclosed and related production sharedbetween units in Germany and Spain.In the UK and Ireland, restructuringbegun in the previous year continued,involving in particular the transfer ofthe head office from Reading toLiverpool, and changes in the alloca-tion of production to British and Irishunits.

Market trends and product innovation

The European market for sweet bis-cuits rose 1% in volume and 3% invalue, while that for savory biscuitsrose 4% in volume and 5% in value.Danone Group’s share of both mar-kets was steady.

In France, its share of the market wassteady in value terms despite difficul-ties in the first half resulting fromdelays in listing of some productsthrough one retail chain. Marketshare rose in the UK thanks to goodsecond-half performance for crackersand countlines, as well as in Italy,Spain and Germany for sweet bis-cuits. In contrast, sales were disap-pointing in Belgium and Ireland.

Product innovation focused on single-serve snack items, breakfast productsand products for children, togetherrepresenting the fastest growing seg-ments of the European market.

In sweet snacks, launches included“Fondant Citron” pastries andsnack-bar versions of “Pim’s” and“Petit Ecolier Choco Tendre” inFrance, as well as a revamped versionof the “Club” snack bar in the UK.

In savory snacks, the main launchwas “Big Bang” in France, while inItaly sales of the “Cipster” range surged ahead, with new additions“Cipster Mais” and “Cipgrill” providingfresh impetus. The “Tuc” range continued to do well in Belgium andGermany.

Breakfast products made a healthycontribution to business growth forcompanies operating in Italy andSpain. In Italy, the “Oro” range gained from the additions of “Oro Più”and “Oro Ciok”, while in Spain“Yayitas Desayuno”, aimed at the topof the market, continued to makehighly satisfactory progress.

A number of new products for chil-dren were launched on the Frenchmarket during the year, including“Mikado Trio” snacks and “Prosper”gingerbread teddy bears. Yet themain event was the introduction of a new-style refrigerated biscuit.Marketed under the name “PrinceCoeur de Lait”, this product is theresult of cooperation between theGroup’s dairy product and biscuitdivisions.

Single-pack “Captain Choc” children’ssnacks and “Mini Napolitain” cakesalso gained ground in 1996. In thesame segment of the German market,the new “Prinzenrolle Schoko-Vanile”rounded out the range of filled bis-cuits.

New geographical markets were alsoopened for existing products. Anexample was the French launch of“Premium”, marketed by Heudebertand produced in Italy, which repre-sents a highly promising new depar-ture in bakery products.

In Germany, the launch of “KleineHerzen”, familiar to French customersas “Petits Coeurs”, and “Goldblätter”– “Feuilleté Doré“ in France – strengthened Group positions at thetop end of the market.

27

Brought to you by Global Reports

BEVERAGES: DANONE GROUP IS EUROPE’S SECONDLARGEST BREWER, WITH SALES OF FF7.5 BILLION.THE GROUP IS ALSO THE WORLD’S SECOND LARGEST PRODUCER OF MINERAL WATER, GENERATING SALES REVENUES OF FF7.9 BILLIONINCLUDING FF6.9 BILLION IN EUROPE.ALL TOLD, BEVERAGES REPRESENTED SALESOF FF14.4 BILLION IN 1996 (NEARLY FF20 BILLIONINCLUDING UNCONSOLIDATED AFFILIATES).

28

Brought to you by Global Reports

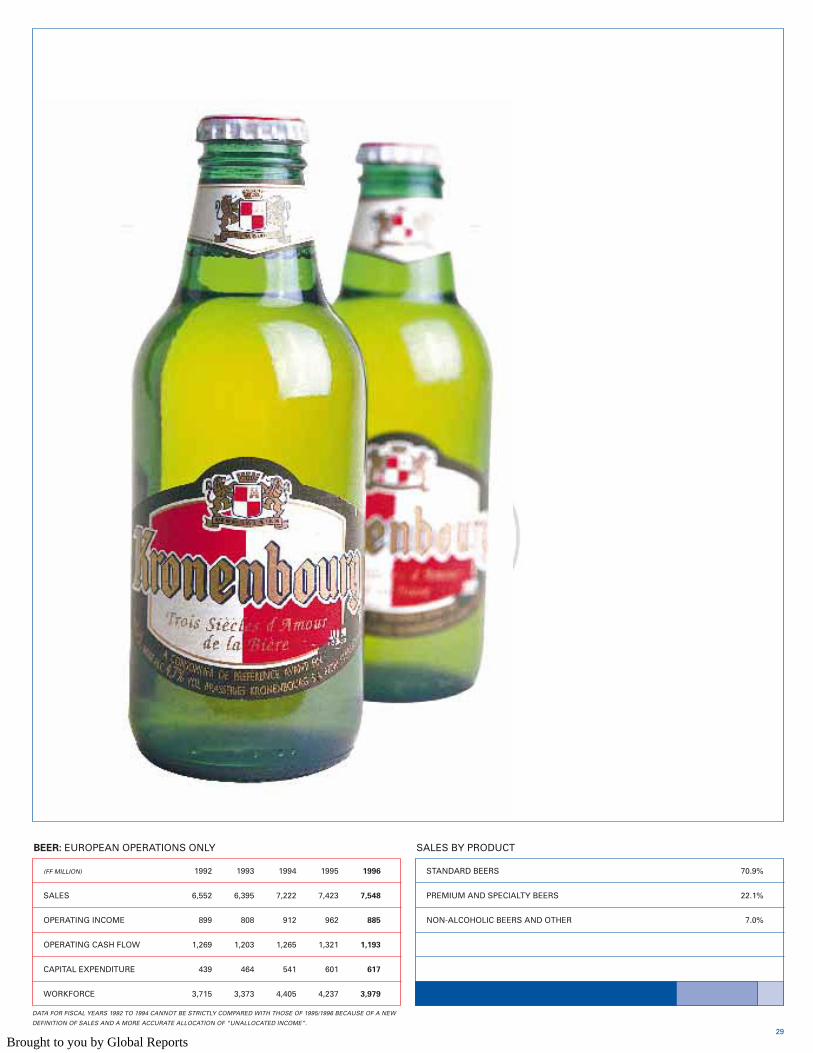

STANDARD BEERS 70.9%

PREMIUM AND SPECIALTY BEERS 22.1%

NON-ALCOHOLIC BEERS AND OTHER 7.0%

BEER: EUROPEAN OPERATIONS ONLY

(FF MILLION) 1992 1993 1994 1995 1996

SALES 6,552 6,395 7,222 7,423 7,548

OPERATING INCOME 899 808 912 962 885

OPERATING CASH FLOW 1,269 1,203 1,265 1,321 1,193

CAPITAL EXPENDITURE 439 464 541 601 617

WORKFORCE 3,715 3,373 4,405 4,237 3,979

SALES BY PRODUCT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.29

Brought to you by Global Reports

In 1996, weather was exceptionally

unfavorable, especially during the

summer months, which are usually

the best for drink sales, and, in

particular, for beer.

At the beginning of 1997, beer and

mineral operations in Europe were

brought together in a single bever-

age division. This should make for

significant synergies in purchasing,

logistics and marketing.

Sales and earnings

Beer sales rose 1.7% to FF7.5 billion,although volumes were down 3%from the previous year. Operatingincome declined 8%, and operatingmargin was down 1.3 percentagepoints.

Shortfalls in volumes and earningsdue to a very poor summer seasonwere not offset despite theDecember surge in French sales, asretailers stocked up ahead of theJanuary 1997 rise in excise.

Mineral water sales declined 3.7% toFF6.9 billion due to cool weather inFrance and, even more, the end of athree-year drought in Spain.However a fall in prices for PET andPVC, the raw materials for bottles,buoyed operating income, whichrose 5.5%. Operating margin was up1.2 percentage points over the sameperiod.

In a number of cases, reorganizationbrought savings in production andadministration costs. Thus in Spain,“Font Vella” and “Lanjarón” pooledadministration, while in Italy a sig-nificant decline in overheads atItalaquae brought a rally in earnings.

Market trends and product innovation

France

On the structurally stable Frenchmarket, beer sales suffered from anexceptionally cool summer, but thiswas partly offset at the end of theyear as retailers stocked up ahead ofa rise in excise taking effect onJanuary 1, 1997. This will probablylead to a rise in retail prices.

Volumes sold to hotels, cafés andrestaurants declined, but there wasan increase in supermarket busi-ness. Overall, market share of the“Kronenbourg” brand sufferedsome erosion. The 1995 merger ofthe “Kronenbourg” and“Kanterbräu” ranges steadied thelatter’s share of café business andwon back positions in food outlets.

As regards product innovation, “K”beer launched in 1995 continued togain ground, while “La Réserve duMaître Kanter” and “1664” premiumlager were brought out in new 75-centiliter bottles. Finally, a new ciderproduced on the basis of brewerytechniques was tested in cafés.

The French market for mineral watershowed a modest rise in 1996, when“Evian” further increased its sharein still water, while “Volvic” suffereda slight decline.

During the year, the use of PET crush-able bottles was extended to theentire “Evian” range, while prepara-tions were made for the launch of asimilar bottle for “Volvic” in 1997.

Demand for sparkling water showedpractically no increase, mainlybecause of the cool weather, whilethe Group’s overall market shareheld steady, with a continued rise insales of “Salvetat” and “Arvie” off-setting a decline for “Badoit”.

Exports of “Evian” and “Volvic” toother parts of Europe continuedupwards, especially in Germanywhere Group sales now total 130million liters. Trends were also favorable for Group brands in the UK and Switzerland.

Spain

Mainly as a result of the weather,the Spanish beer market contracted3.5% overall, with sales to cafés,hotels and restaurants showing thesteepest declines. Home consump-tion was more resilient.

San Miguel continued marketingefforts, renewing existing rangeswith innovations such as the intro-duction of screw-top bottles, andlaunching new products including inparticular “Ice Beer”. Despite this, itsuffered a slight decline in marketshare. Mahou kept pace with markettrends.

Turning to mineral water, marketvolumes were down 12%, the firstdecline in several years. This reflect-ed the end of a chronic drought inthe south of the country which hadinflated demand in previous years.“Font Vella” increased its share ofthe national market for still waters,while “Lanjarón” strengthenedregional positions in Andalusia andLevante. “Font Picant” sparklingwater doubled sales, consolidatingthe Group position in the sectoralready held through “Fonter”.

Italy

The Italian beer market contracted6% in 1996 as cool weather discour-aged domestic customers and kept

tourists away. “Peroni” suffered adecline in market share, particularlyin cafés, restaurants and hotels, as aresult of fierce competition.

Mineral water markets showed aslight increase in volume, but pricesremained under pressure. Againstthis backdrop, “Italaquae” made anexcellent showing, increasing itsmarket share thanks to a good per-formance from its top “Ferrarelle”brand, as well as a marked recoveryin sales of “Boario” and the suc-cessful launch of lower-priced“Santagata” in the previous year.

Belgium

The structural decline in the Belgianmarket continued, exacerbated bycool weather and a rise in excise.

In these difficult conditions, AlkenMaes held onto market share forcore “Maes” and “Cristal” brands,while the success of specialty beers“Blanche de Bruges” and“Grimbergen” was confirmed. Themain innovation of the year was thelaunch of ice beer “Maes Cool”which helped update the overallimage of the “Maes” brand on itsmarket.

30

Brought to you by Global Reports

STILL WATER 66.6%

SPARKLING WATER 30.3%

HOTEL, LEISURE AND OTHER 3.1%

MINERAL WATER: EUROPEAN OPERATIONS ONLY

(FF MILLION) 1992 1993 1994 1995 1996

SALES 5,716 5,898 7,000 7,155 6,891

OPERATING INCOME 898 955 1,060 890 939

OPERATING CASH FLOW 1,010 1,058 1,186 1,073 1,124

CAPITAL EXPENDITURE 506 383 492 507 447

WORKFORCE 3,189 4,088 3,965 3,900 3,726

SALES BY PRODUCT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.31

Brought to you by Global Reports

THE KRONENBOURG FOUNDATIONIN DEPRESSED URBAN AND RURAL AREAS,COMMUNITY LIFE IS MORE IMPORTANT THAN EVER. HERE THE SIMPLE INITIATIVES TAKEN DAILY BYMEN AND WOMEN COMMITTED TO IMPROVINGEVERYONE'S LOT CAN OFFER MUCH-NEEDED HOPE.BEER IS A TRADITIONAL PART OF SOCIAL INTERACTION. THE KRONENBOURG BREWERIES SUPPORTCOMMUNITY WORK THROUGH A FOUNDATION THATHELPS YOUNG PEOPLE IN DIFFICULTY FIND A PLACEIN SOCIETY. THIS FOUNDATION PROVIDES FINANCIALCONTRIBUTIONS, BUT ALSO EXPERT INPUT AND ADVICE TO HELP BENEFICIARIES OPEN A CAFÉ IN ALESS-FAVORED NEIGHBORHOOD, SET UP A LOCALSHOP TO BREATH FRESH LIFE INTO A VILLAGE, ORFOUND A RESTAURANT STAFFED BY PEOPLE IN DIFFICULT STRAITS. THE KRONENBOURGFOUNDATION HAS ALREADY LENT ITS SUPPORT TOMORE THAN TEN SUCH PROJECTS.

32

Brought to you by Global Reports

Brought to you by Global Reports

CONTAINERS: DANONE GROUP IS EUROPE’S SECONDLARGEST PRODUCER OF GLASS BOTTLES AND JARS.IN 1996, SALES REVENUES TOTALLED FF6.3 BILLION.PRODUCTION IS CENTERED ON FRANCE, SPAIN ANDTHE NETHERLANDS.

BOTTLES 73.5%

JARS 17.7%

TABLE GLASSWARE AND OTHER 8.8%

(FF MILLION) 1992 1993 1994 1995 1996

SALES 7,046 6,663 6,368 6,356 6,278

OPERATING INCOME 730 556 624 638 703

OPERATING CASH FLOW 893 487 785 809 859

CAPITAL EXPENDITURE 404 366 434 424 506

WORKFORCE 9,023 7,834 7,596 7,468 7,035

SALES BY PRODUCT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.

34

Brought to you by Global Reports

On some markets, notably soft

drinks and beer, unusually cool

summer weather hurt demand for

bottles. However this was offset

by strong demand for wine

bottles, food jars and, even more,

champagne bottles.

Despite a squeeze on prices, the

high proportion of sales at the

upper end of the market and

significant productivity gains

allowed a further improvement in

operating margin.

Sales and earnings

Sales dipped 1.2% to FF6.3 billionin 1996, reflecting in particular thesale early in the year of glasstableware operations of Frenchsubsidiary VMC to Bormioli Roccoin Italy. At constant structure andexchange rates, sales were up2.2%. Operating income rose10.2%, driven by major productivegains, particularly in Spain, andoperating margin was up 1.2 per-centage points. During the year,productivity drives were alsoconducted at VMC and Verdômein France, as well as in theNetherlands.

Market trends and product innovation

France

The overall rise in French demandfor glass bottles during 1996 wasthe result of contrasting trends.On the one hand, there was asharp rise in orders for cham-pagne bottles – which will be onthe shelves in the year 2000 –while on the other, there was adecline in demand for beer andsoft-drink bottles.

The Group nonetheless held ontoits share of the market.Development projects focused onreducing bottle weight continuedin response to a basic trend indemand, which was also behindthe launch of the “Optima” rangein the previous year. All told, 60new bottle designs were put onthe market. Export sales to neigh-boring countries were also on afavorable track.

Turning to food jars, prices cameunder strong competitive pres-sure, notably from foreign pro-ducers. Despite this, VMC madesatisfactory progress on exportmarkets.

Spain

The Spanish market for glasscontainers grew nearly 4% in1996, reflecting vigorous demandfor wine bottles, notably frommakers of sparkling wines such asCavas, as well as for food jars.Group business expanded in stepwith the market.

The Netherlands

In the Netherlands, orders forfood jars were on the rise, butdemand for bottles in the beerand spirits sector declined.Vereenigde Glasfabrieken per-formed in line with the market inthese areas, while at the sametime reporting a sharp rise instemware sales thanks to im-proved sales targeting. During theyear, the company developed 90new bottle designs.

35

Brought to you by Global Reports

36

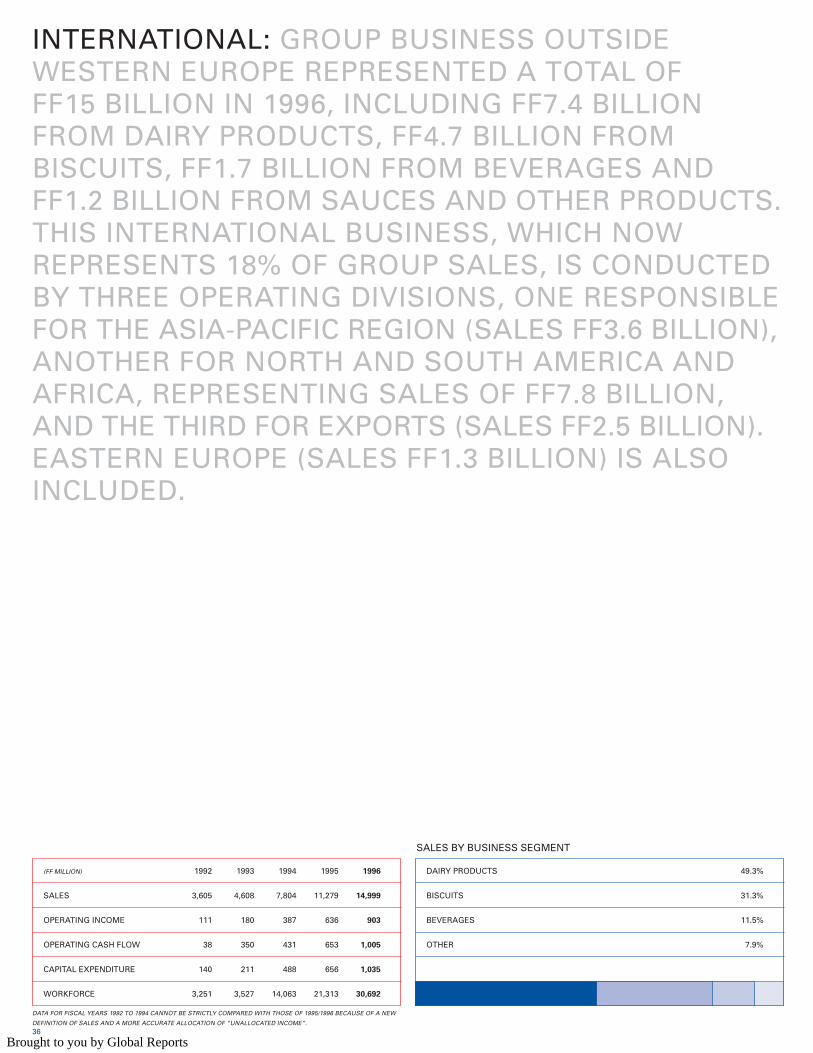

INTERNATIONAL: GROUP BUSINESS OUTSIDE WESTERN EUROPE REPRESENTED A TOTAL OF FF15 BILLION IN 1996, INCLUDING FF7.4 BILLIONFROM DAIRY PRODUCTS, FF4.7 BILLION FROM BISCUITS, FF1.7 BILLION FROM BEVERAGES AND FF1.2 BILLION FROM SAUCES AND OTHER PRODUCTS.THIS INTERNATIONAL BUSINESS, WHICH NOW REPRESENTS 18% OF GROUP SALES, IS CONDUCTEDBY THREE OPERATING DIVISIONS, ONE RESPONSIBLEFOR THE ASIA-PACIFIC REGION (SALES FF3.6 BILLION),ANOTHER FOR NORTH AND SOUTH AMERICA ANDAFRICA, REPRESENTING SALES OF FF7.8 BILLION,AND THE THIRD FOR EXPORTS (SALES FF2.5 BILLION).EASTERN EUROPE (SALES FF1.3 BILLION) IS ALSO INCLUDED.

DAIRY PRODUCTS 49.3%

BISCUITS 31.3%

BEVERAGES 11.5%

OTHER 7.9%

(FF MILLION) 1992 1993 1994 1995 1996

SALES 3,605 4,608 7,804 11,279 14,999

OPERATING INCOME 111 180 387 636 903

OPERATING CASH FLOW 38 350 431 653 1,005

CAPITAL EXPENDITURE 140 211 488 656 1,035

WORKFORCE 3,251 3,527 14,063 21,313 30,692

SALES BY BUSINESS SEGMENT

DATA FOR FISCAL YEARS 1992 TO 1994 CANNOT BE STRICTLY COMPARED WITH THOSE OF 1995/1996 BECAUSE OF A NEW

DEFINITION OF SALES AND A MORE ACCURATE ALLOCATION OF “UNALLOCATED INCOME”.

Brought to you by Global Reports

NORTH AMERICA 30.3%

LATIN AMERICA 30.6%

ASIA-PACIFIC 26.2%

EASTERN EUROPE 9.2%

AFRICA 3.7%

INTERNATIONAL SALES BY GEOGRAPHICAL ZONE

37

Brought to you by Global Reports

International sales rose 33% in 1996,

driven by a string of acquisitions as

well as first consolidation of a num-

ber of other companies in eastern

Europe, China and Argentina. This

was in addition to 7.9% growth in

existing business, which, while

moderate, was five times quicker

than in western Europe. International

sales thus showed a fourfold rise in

just five years. During 1996, manage-

ment structures in Asia were en-

hanced, with operational headquarters

for the region set up in Singapore.

Sales and earnings

Operating income rose 42% and op-erating margin 0.4 of a percentagepoint. The rise was limited by costsarising from the launch of “Dannon”brand mineral water in the US.

These results reflect relatively steadyperformances from existing opera-tions in North and South Americaand in Asia, as well as a healthy newcontribution from dairy product op-erations in eastern Europe.

Major productivity gains at Bagley inArgentina offset the effects of reces-sion, while marketing and sales wererevamped to achieved a better fitwith the market.

Market trends and product innovation

Dairy products

After several years of robust growth,the US market for dairy products slowed in 1996, with demand up onlyaround 3%. At the same time, compe-tition heated up in low-calorie prod-ucts. Initiatives during the year included extension of the “DoubleDelights” range and the launch of“Sprinkl’ins Magic Crystals”, ayogurt especially for children.

In Brazil, market growth was moremoderate following the surge of theprevious year, and Danone was ableto consolidate its position. At thesame time, production on a sub-contracted basis got under way in thecountry’s Nordeste, now undergoingrapid development.

With Argentina suffering from a deeprecession, demand for dairy productsheld steady. Danone Group beganreorganizing marketing of yogurt-style cheeses and desserts in its firstjoint venture in the run-up to theextension of this to “La Serenisima”yogurt range in 1997. Major productlaunches in the course of 1996 included“Casancrem dulce de leche” cheesespread and “Budin de Manzana”dessert.

In Canada, where market growth alsoslowed, the Group turned in a goodperformance, recapturing its topposition thanks to new products launched under the “Danone” name,notably the “Passion” range.Production capacity is being expanded.

In Mexico, where the economy gotback onto a firmer track, the marketgrew 5%, but Danone suffered adecline in its share following the arri-val of new competitors.

In eastern Europe, demand for dairyproducts soared. Danone also suc-ceeded in increasing its share of mar-kets in all countries in the area, whileat the same time raising sales pricesand expanding ranges. Strongest per-formances were in Poland, the CzechRepublic, Slovakia and Hungary.Bulgarian business, in contrast, suf-fered a sharp decline, reflecting theseverity of the country’s economictroubles.

In Japan, the focus for the “Danone”brand in 1996 was on cutting costs inpurchasing, production and distribu-tion.

In China, sales of “Wahaha” milk-based fruit drinks showed a vigorous41% rise during the year.

Biscuits

The biscuit market in Argentina grewaround 2.5% in 1996, but as a resultof the recession demand focused onlower-price ranges. Competition wasfierce, and Bagley suffered a slightdecline in market share, but reorgani-zation of sales and a major programto introduce existing products ofother Group companies should meana rapid return to satisfactory busi-ness growth. In 1996, launches in-cluded “Rex Pizza” savory snacks and“Petits Coeurs” sweet biscuits, bothusing recipes from European units.

In Brazil, where demand for biscuitsincreased 3%, Campineira’s share ofthe market declined slightly whileAymoré’s rose.

New Zealand subsidiary Griffinsbrought out a large number of newproducts and significantly improvedmarket share in the savory snackssegment.

In India, Britannia consolidated itsmarket leadership with a 25% rise inbiscuit sales, rewarding renewal ofcore ranges as well as innovation. Itspackaged cakes business did particular-ly well, with market share doubling.

In Indonesia, biscuit production launched under the “Danone” nameat the end of 1995 beat targets andplans are now being made to increasecapacity.

In Malaysia, where a large number ofproducts have also been put underthe “Danone” name, a major drivewas undertaken to increase marketshare in major retailing chains.

In China, units in Shanghai andJiangmen have adopted the“Danone” brand for their production,and distribution has been extendedto Beijing. A major program toenhance quality and productivity gotunder way at the Jiangmen plant.

Despite political uncertainties, theGroup consolidated its market leader-ship in Pakistan, with sales showing avigorous rise during the year.

In the Czech Republic and Slovakia,biscuit business was highly satisfac-tory, thanks in particular to renewalof some core products, launches ofnew snacks, and very successfulexport sales.

In Russia, Bolshevik had a difficultyear against a backdrop of persistentweakness in consumer demand.

Biscuit exports rose 14%, with much ofthe impetus coming from the launch ofthe new “LU” international range inthe US, Southeast Asia and Scandinavia.

Beverages

The main highlight of the year wasthe launch of “Dannon” brand bot-tled mineral water in the easternUnited States. This consolidates theGroup’s leadership on the fast-growing US market, where “Evian”ranks first. “Dannon Natural SpringWater” won an 11% share of super-market sales and took the lead in fiveMidwestern states. Distribution is tobe extended to other parts of thecountry in 1997.

In Canada, sales of “Aquaterra” wereon the rise, particularly in the homeand office delivery sector in Ontarioand Quebec.

In Mexico, “Bonafont” mineral waterincreased its share of a market whichgrew around 3%, and distribution wasput on a nationwide basis.