120320

37

Econ203-Tut9 Vinh Nguyen Taylor Rule Question 3 Reference(s) Econ 203 Lect A, Tut C - Tutorial 9 Tutor: Vinh Nguyen 1 ([email protected]) 1 Concordia University Mar 20, 2012

-

Upload

vinh-nguyen -

Category

Documents

-

view

11 -

download

0

Transcript of 120320

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 1/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Econ 203 Lect A, Tut C - Tutorial 9

Tutor: Vinh Nguyen1

1Concordia University

Mar 20, 2012

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 2/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 3/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:• Foreign exchange rate (1960’s)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 4/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:• Foreign exchange rate (1960’s)• Money supply (1970’s – early 1990’s)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 5/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:• Foreign exchange rate (1960’s)• Money supply (1970’s – early 1990’s)• Inflation rate (early 1990’s – present)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 6/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:• Foreign exchange rate (1960’s)• Money supply (1970’s – early 1990’s)• Inflation rate (early 1990’s – present)

• Instrument: interest rate. In Canada: overnight rate (the

interest rate large financial institutions receive or pay on

loans from one day until the next )

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 7/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:• Foreign exchange rate (1960’s)• Money supply (1970’s – early 1990’s)• Inflation rate (early 1990’s – present)

• Instrument: interest rate. In Canada: overnight rate (the

interest rate large financial institutions receive or pay on

loans from one day until the next )

• A relationship:

bank rate ≈ overnight rate + 0.

25%

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 8/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Monetary Policy Targets and Instrument in Canada

• Targets:• Foreign exchange rate (1960’s)• Money supply (1970’s – early 1990’s)• Inflation rate (early 1990’s – present)

• Instrument: interest rate. In Canada: overnight rate (the

interest rate large financial institutions receive or pay on

loans from one day until the next )

• A relationship:

bank rate ≈ overnight rate + 0.

25%

• Overnight rate ↓ ⇒ commercial bank lending rates ↓ ⇒

expansion in the money supply

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 9/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

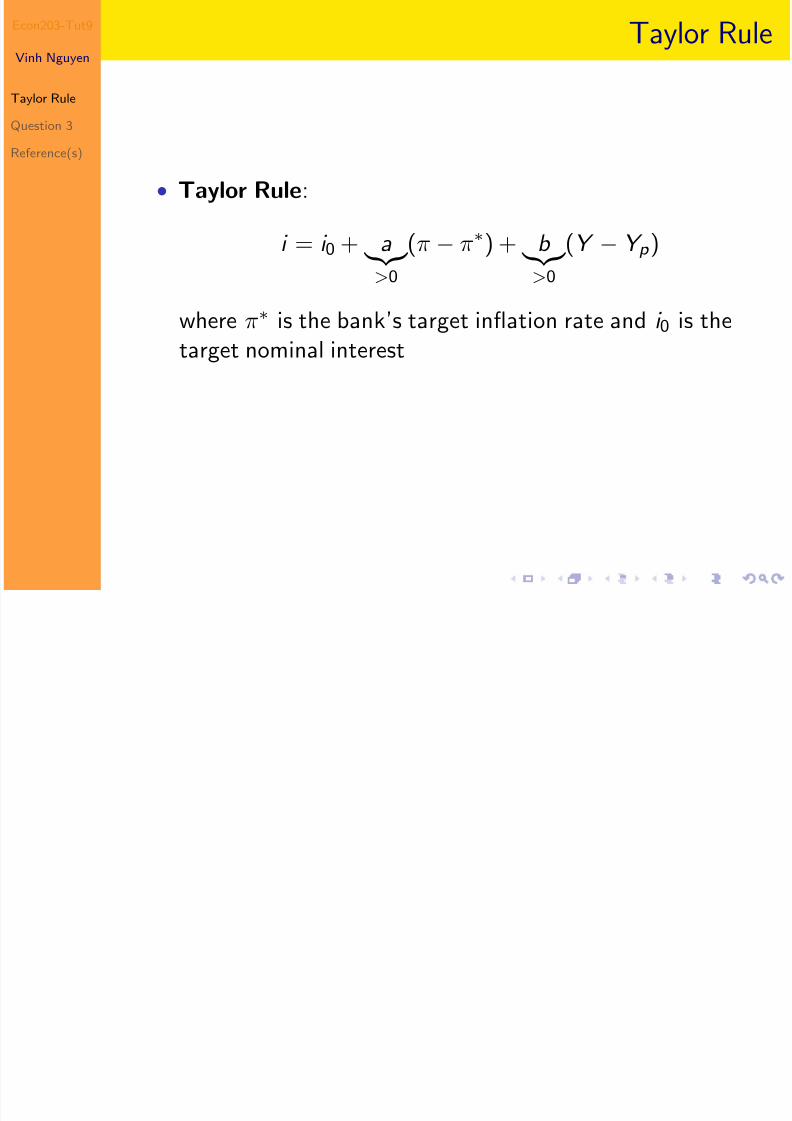

Taylor Rule

• Taylor Rule:

i = i 0 + a

>0

(π − π∗) + b

>0

(Y − Y p )

where π∗ is the bank’s target inflation rate and i 0 is the

target nominal interest

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 10/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Taylor Rule

• Taylor Rule:

i = i 0 + a

>0

(π − π∗) + b

>0

(Y − Y p )

where π∗ is the bank’s target inflation rate and i 0 is the

target nominal interest

• Long-run change: change in i 0

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 11/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Taylor Rule

• Taylor Rule:

i = i 0 + a

>0

(π − π∗) + b

>0

(Y − Y p )

where π∗ is the bank’s target inflation rate and i 0 is the

target nominal interest

• Long-run change: change in i 0

• Short-run change: temporarily set the nominal rate to i

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 12/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

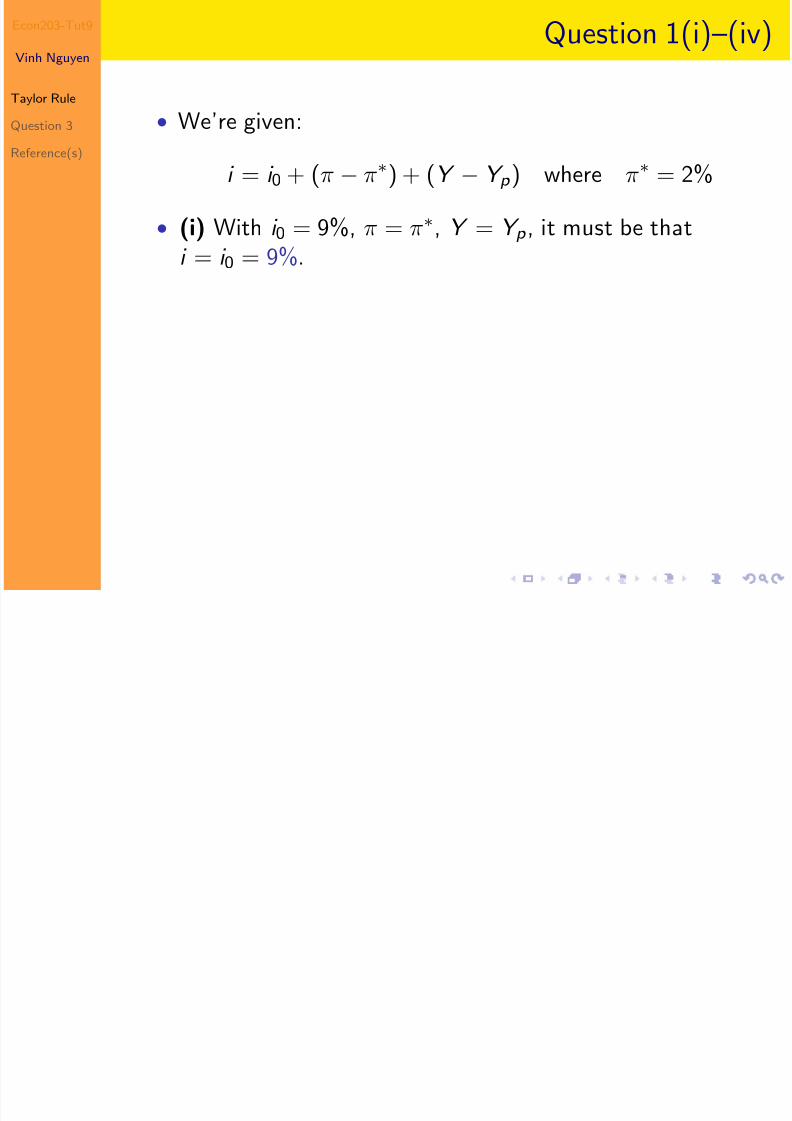

Question 1(i)–(iv)

• We’re given:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 13/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(i)–(iv)

• We’re given:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (i) With i 0 = 9%, π = π∗, Y = Y p , it must be that

i = i 0 = 9%.

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 14/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(i)–(iv)

• We’re given:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (i) With i 0 = 9%, π = π∗, Y = Y p , it must be that

i = i 0 = 9%.

• (ii) Now, we have Y − Y p = −5% and π = π∗. Then,

i = i 0 − 5% = 4%.

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 15/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(i)–(iv)

• We’re given:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (i) With i 0 = 9%, π = π∗, Y = Y p , it must be that

i = i 0 = 9%.

• (ii) Now, we have Y − Y p = −5% and π = π∗. Then,

i = i 0 − 5% = 4%.

• (iii) i dropping shifts the AD and AS curves up (seeFigure 10.8 on page 260)

( ) ( )

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 16/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(i)–(iv)

• We’re given:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (i) With i 0 = 9%, π = π∗, Y = Y p , it must be that

i = i 0 = 9%.

• (ii) Now, we have Y − Y p = −5% and π = π∗. Then,

i = i 0 − 5% = 4%.

• (iii) i dropping shifts the AD and AS curves up (seeFigure 10.8 on page 260)

• (iv) i was 9% and now i = 4%, so ∆i = −5%. Thus,

π = π∗ − 1.5∆i = 2% − 1.5(−5%) = 9.5%

E 203 T 9 Q ( ) ( )

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 17/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(v),(vi)

• Again:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

E 203 T t9 Q i 1( ) ( i)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 18/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(v),(vi)

• Again:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (v) Now π = π∗ − 1.5∆i , so π − π

∗ = −1.5∆i . First,notice:

i new = i 0 − 1.5∆i + (Y − Y p ) = i old − 1.5∆i + (Y − Y p )

Econ203 Tut9 Q i 1( ) ( i)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 19/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(v),(vi)

• Again:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (v) Now π = π∗ − 1.5∆i , so π − π

∗ = −1.5∆i . First,notice:

i new = i 0 − 1.5∆i + (Y − Y p ) = i old − 1.5∆i + (Y − Y p )

• It follows that

∆i = −1.5∆i + (Y − Y p ) ⇒ 2.5∆i = (Y − Y p )

Econ203-Tut9 Q ti 1( ) ( i)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 20/37

Econ203-Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(v),(vi)

• Again:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (v) Now π = π∗ − 1.5∆i , so π − π

∗ = −1.5∆i . First,notice:

i new = i 0 − 1.5∆i + (Y − Y p ) = i old − 1.5∆i + (Y − Y p )

• It follows that

∆i = −1.5∆i + (Y − Y p ) ⇒ 2.5∆i = (Y − Y p )

• With Y − Y p = −5%, it must be that ∆i = −2%. So

i new = i old + ∆i = 9% − 2% = 7%

Econ203-Tut9 Q ti 1( ) ( i)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 21/37

Econ203 Tut9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(v),(vi)

• Again:

i = i 0 + (π − π∗) + (Y − Y p ) where π

∗ = 2%

• (v) Now π = π∗ − 1.5∆i , so π − π

∗ = −1.5∆i . First,notice:

i new = i 0 − 1.5∆i + (Y − Y p ) = i old − 1.5∆i + (Y − Y p )

• It follows that

∆i = −1.5∆i + (Y − Y p ) ⇒ 2.5∆i = (Y − Y p )

• With Y − Y p = −5%, it must be that ∆i = −2%. So

i new = i old + ∆i = 9% − 2% = 7%

• (vi) We have π = π

∗

− 1.5∆i = 2% − 1.5(−2%) = 5%.

Econ203-Tut9 Q estion 1( ii) and MC 6 from T t 8

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 22/37

03 u 9

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(vii) and MC 6 from Tut 8

• (vii) Lowering interest rate creates an upward pressure on

inflation.

Econ203-Tut9 Question 1(vii) and MC 6 from Tut 8

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 23/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(vii) and MC 6 from Tut 8

• (vii) Lowering interest rate creates an upward pressure on

inflation.

• When π is taken into account, the BoC is more carefulwith lowering the interest so as to not raising π too high.Thus, i (part (v)) is higher than i (part (ii)).

Econ203-Tut9 Question 1(vii) and MC 6 from Tut 8

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 24/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(vii) and MC 6 from Tut 8

• (vii) Lowering interest rate creates an upward pressure on

inflation.

• When π is taken into account, the BoC is more carefulwith lowering the interest so as to not raising π too high.Thus, i (part (v)) is higher than i (part (ii)).

• MC 6 from Tut 8. Long term effects allude to change inpotential output, so (C) is a right choice.

Econ203-Tut9 Question 1(vii) and MC 6 from Tut 8

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 25/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(vii) and MC 6 from Tut 8

• (vii) Lowering interest rate creates an upward pressure on

inflation.

• When π is taken into account, the BoC is more carefulwith lowering the interest so as to not raising π too high.Thus, i (part (v)) is higher than i (part (ii)).

• MC 6 from Tut 8. Long term effects allude to change inpotential output, so (C) is a right choice.

• SRAS is a temporary measure to maintain the overnightrate so (A) is wrong. Correction: [I misread “SRAS” into“SPRA”] In any case, SRAS = “short-run aggregate

supply”, which has little to do with long term potentialoutput, so (A) is not the right choice.

Econ203-Tut9 Question 1(vii) and MC 6 from Tut 8

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 26/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(vii) and MC 6 from Tut 8

• (vii) Lowering interest rate creates an upward pressure on

inflation.

• When π is taken into account, the BoC is more carefulwith lowering the interest so as to not raising π too high.Thus, i (part (v)) is higher than i (part (ii)).

• MC 6 from Tut 8. Long term effects allude to change inpotential output, so (C) is a right choice.

• SRAS is a temporary measure to maintain the overnightrate so (A) is wrong. Correction: [I misread “SRAS” into“SPRA”] In any case, SRAS = “short-run aggregate

supply”, which has little to do with long term potentialoutput, so (A) is not the right choice.• AD can be shifted without any change to potential output

(see Figure 10.8, page 260). (B) is also wrong.

Econ203-Tut9 Question 1(vii) and MC 6 from Tut 8

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 27/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 1(vii) and MC 6 from Tut 8

• (vii) Lowering interest rate creates an upward pressure on

inflation.

• When π is taken into account, the BoC is more carefulwith lowering the interest so as to not raising π too high.Thus, i (part (v)) is higher than i (part (ii)).

• MC 6 from Tut 8. Long term effects allude to change inpotential output, so (C) is a right choice.

• SRAS is a temporary measure to maintain the overnightrate so (A) is wrong. Correction: [I misread “SRAS” into“SPRA”] In any case, SRAS = “short-run aggregate

supply”, which has little to do with long term potentialoutput, so (A) is not the right choice.• AD can be shifted without any change to potential output

(see Figure 10.8, page 260). (B) is also wrong.• (D) refers to temporary techniques. (D) is not correct.

Econ203-Tut9 Question 3(i)–(iv)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 28/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 3(i) (iv)

• (i) At equilibrium, M s = M d so i = 0.05. As such, I = 95and Y = 1375. (Note: C = 100 + 0.8(Y − 150)).

Econ203-Tut9 Question 3(i)–(iv)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 29/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 3(i) (iv)

• (i) At equilibrium, M s = M d so i = 0.05. As such, I = 95and Y = 1375. (Note: C = 100 + 0.8(Y − 150)).

• (ii) C = 1080, and S = Y − T − C = 145.

Econ203-Tut9 Question 3(i)–(iv)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 30/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 3(i) (iv)

• (i) At equilibrium, M s = M d so i = 0.05. As such, I = 95and Y = 1375. (Note: C = 100 + 0.8(Y − 150)).

• (ii) C = 1080, and S = Y − T − C = 145.

• (iii) Note that

Y = C + I + G ⇒ Y − C − T − I = G − T

Note that Y − C − T = S so we have S − I = G − T .This means the government deficit can be financed by

borrowing from private savings.

Econ203-Tut9 Question 3(i)–(iv)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 31/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Question 3(i) (iv)

• (i) At equilibrium, M s = M d so i = 0.05. As such, I = 95and Y = 1375. (Note: C = 100 + 0.8(Y − 150)).

• (ii) C = 1080, and S = Y − T − C = 145.

• (iii) Note that

Y = C + I + G ⇒ Y − C − T − I = G − T

Note that Y − C − T = S so we have S − I = G − T .This means the government deficit can be financed by

borrowing from private savings.• (iv) Multiplier 1

1−c = 5. So with ∆G = 50, ∆Y = 250,

thus new Y = 1375 + 250 = 1625.

Econ203-Tut9 Question 3(v)–(vii)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 32/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Q ( ) ( )

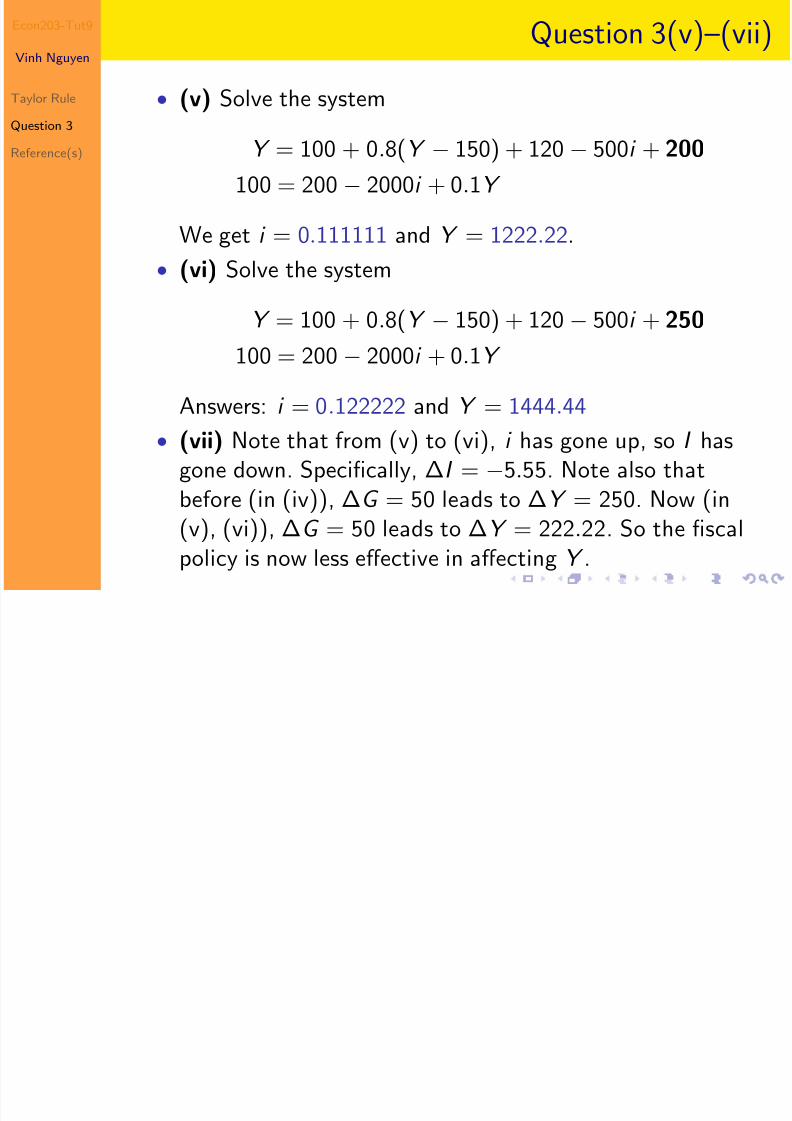

• (v) Solve the system

Y = 100 + 0.8(Y − 150) + 120 − 500i + 200100 = 200 − 2000i + 0.1Y

We get i = 0.111111 and Y = 1222.22.

Econ203-Tut9 Question 3(v)–(vii)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 33/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Q ( ) ( )

• (v) Solve the system

Y = 100 + 0.8(Y − 150) + 120 − 500i + 200100 = 200 − 2000i + 0.1Y

We get i = 0.111111 and Y = 1222.22.

• (vi) Solve the system

Y = 100 + 0.8(Y − 150) + 120 − 500i + 250

100 = 200 − 2000i + 0.1Y

Answers: i = 0.122222 and Y = 1444.44

Econ203-Tut9 Question 3(v)–(vii)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 34/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

( ) ( )

• (v) Solve the system

Y = 100 + 0.8(Y − 150) + 120 − 500i + 200100 = 200 − 2000i + 0.1Y

We get i = 0.111111 and Y = 1222.22.

• (vi) Solve the system

Y = 100 + 0.8(Y − 150) + 120 − 500i + 250

100 = 200 − 2000i + 0.1Y

Answers: i = 0.122222 and Y = 1444.44

• (vii) Note that from (v) to (vi), i has gone up, so I hasgone down. Specifically, ∆I = −5.55. Note also thatbefore (in (iv)), ∆G = 50 leads to ∆Y = 250. Now (in(v), (vi)), ∆G = 50 leads to ∆Y = 222.22. So the fiscal

policy is now less effective in affecting Y .

Econ203-Tut9 Question 3(viii)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 35/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

( )

• (viii) We have

Y = 100 + 0.8(Y − 150) + I + G = −20 + 0.8Y + I + G

Econ203-Tut9 Question 3(viii)

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 36/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

( )

• (viii) We have

Y = 100 + 0.8(Y − 150) + I + G = −20 + 0.8Y + I + G

• Therefore,

Y = −100 + 5(I + G ) ⇒ ∆Y = 5(∆I + ∆G )

Econ203-Tut9 References

5/14/2018 120320 - slidepdf.com

http://slidepdf.com/reader/full/120320 37/37

Vinh Nguyen

Taylor Rule

Question 3

Reference(s)

Curtis, Douglas; Irvine, Ian and Begg, David.

Macroeconomics. 2nd Canadian edition, USA: McGraw-HillRyerson, 2010.