1 year Potential Upside Target Price ( Action Construction ... · PDF fileLKP Advisory...

8

30-November-2016 There was a case of optimism in the Indian stock market as normal monsoons after 2 consecutive years of deficit rainfall and the 7th PC recommendations gave a fillip to the India Consumption Story, But this optimism was short lived with an earnings disappointment in Q2FY17 failing to provide a clear picture on India’s premium valuation status & any pick-up in growth, causing the domestic stock markets to be in a limbo throughout October. The month of November proved to be even more fatal for domestic equities, given the double whammy of a surprise win for Donald Trump in the US Presidential Elections and the Centre’s decision to undertake demonetization of old ₹ 500 & ₹ 1,000 notes with the NIFTY 50 taking a plunge below 8,000 on November 21st. Emerging economies such as India may continue to experience some turbulence over the short term when you consider the possible fiscal stimulus by the Trump administration expected to push US GDP growth & inflation. Fall-out of BREXIT and prospects of the US FED hiking rates coupled with the short term impact on consumption following demonetization has thrown open interesting investment opportunities for the savvy long-term investor. We strongly believe that India’s consumption story would hold out, considering the positive impact of demonetization over the long term, a proactive government with a laser focus on policy reforms such as GST, fiscal stimulus and the demographic dividend enjoyed by the Indian economy. We bring to you an interesting mix of companies spanning several sectors across market cap. We believe these companies are attractively priced on the basis of both technical & fundamental parameters. Company Sector CMP (₹) 1 year Target Price (₹) Potential Upside Action Construction Equipment Cranes 48 67 40% Arvind Textile 357 450 26% Balrampur Chini Mills Sugar 121 160 32% ICICI Bank Banking 256 310 21% Jain Irrigation Systems MIS 89 120 35% KEC International T & D 143 180 26%

Transcript of 1 year Potential Upside Target Price ( Action Construction ... · PDF fileLKP Advisory...

30-November-2016

There was a case of optimism in the Indian stock market as normal monsoons after 2 consecutive years of deficit

rainfall and the 7th PC recommendations gave a fillip to the India Consumption Story, But this optimism was short

lived with an earnings disappointment in Q2FY17 failing to provide a clear picture on India’s premium valuation status

& any pick-up in growth, causing the domestic stock markets to be in a limbo throughout October. The month of

November proved to be even more fatal for domestic equities, given the double whammy of a surprise win for Donald

Trump in the US Presidential Elections and the Centre’s decision to undertake demonetization of old ₹ 500 & ₹ 1,000

notes with the NIFTY 50 taking a plunge below 8,000 on November 21st.

Emerging economies such as India may continue to experience some turbulence over the short term when you

consider the possible fiscal stimulus by the Trump administration expected to push US GDP growth & inflation. Fall-out

of BREXIT and prospects of the US FED hiking rates coupled with the short term impact on consumption following

demonetization has thrown open interesting investment opportunities for the savvy long-term investor.

We strongly believe that India’s consumption story would hold out, considering the positive impact of demonetization

over the long term, a proactive government with a laser focus on policy reforms such as GST, fiscal stimulus and the

demographic dividend enjoyed by the Indian economy.

We bring to you an interesting mix of companies spanning several sectors across market cap. We believe these

companies are attractively priced on the basis of both technical & fundamental parameters.

Company Sector CMP (₹) 1 year

Target Price (₹) Potential Upside

Action Construction Equipment Cranes 48 67 40%

Arvind Textile 357 450 26%

Balrampur Chini Mills Sugar 121 160 32%

ICICI Bank Banking 256 310 21%

Jain Irrigation Systems MIS 89 120 35%

KEC International T & D 143 180 26%

LKP Advisory

Fundamental View

Action Construction Equipment – ACE is our small cap pick to play the operating leverage from GOI driven

infrastructure revival. Presence across the 4 verticals of Cranes, Construction Equipment, Material Handling & Farm

Equipment makes ACE a perfect proxy to play the India Story

Given its 60% dominant market share in Mobile & Tower Cranes we believe that its recent merger with ACETCR

brings in high margin rental business within the listed entity.

Its Farm Equipment business in our view should do well this fiscal on the back of a good monsoon and given its

comfortable debt equity and positive free cash flows, ACE trading at 2x book value has the potential to deliver a

40% upside for investors in one-year.

Technical View

A bullish flag pattern on the monthly time scale is formed on ACE chart.

A closer look at RSI on monthly time scales indicates that 50 has been a zone of extremely strong support and a

reversal as well.

Combining both the parameters and the recent bounce from the 200 DMA as well, we believe the stock can lead

to a strong breakout on a multi month time frame.

ACTION CONSTRUCTION EQUIPMENT CMP: ₹48

LKP Advisory

Fundamental View

The $1.3bn ARVIND is one of India’s largest integrated Textile & Apparel company. While its traditional textile

business continues to grow at high single digit, its ₹2700cr brand portfolio has been growing at 25% CAGR for

the past 3 years driven by its power brands, distribution footprint and ability to straddle its brands across the

income pyramid.

We believe that its relationships with iconic global brands and sourcing capabilities acts as an entry barrier to

competition and value unlocking from its high margin brand business coupled with de-leveraging would enhance

shareholder value going forward.

ARVIND trading at 22xFY17E earnings may not be cheap on valuation but its unique strategies and leadership in

its space make us bullish on its prospects for a one-year price objective of ₹450

Technical View

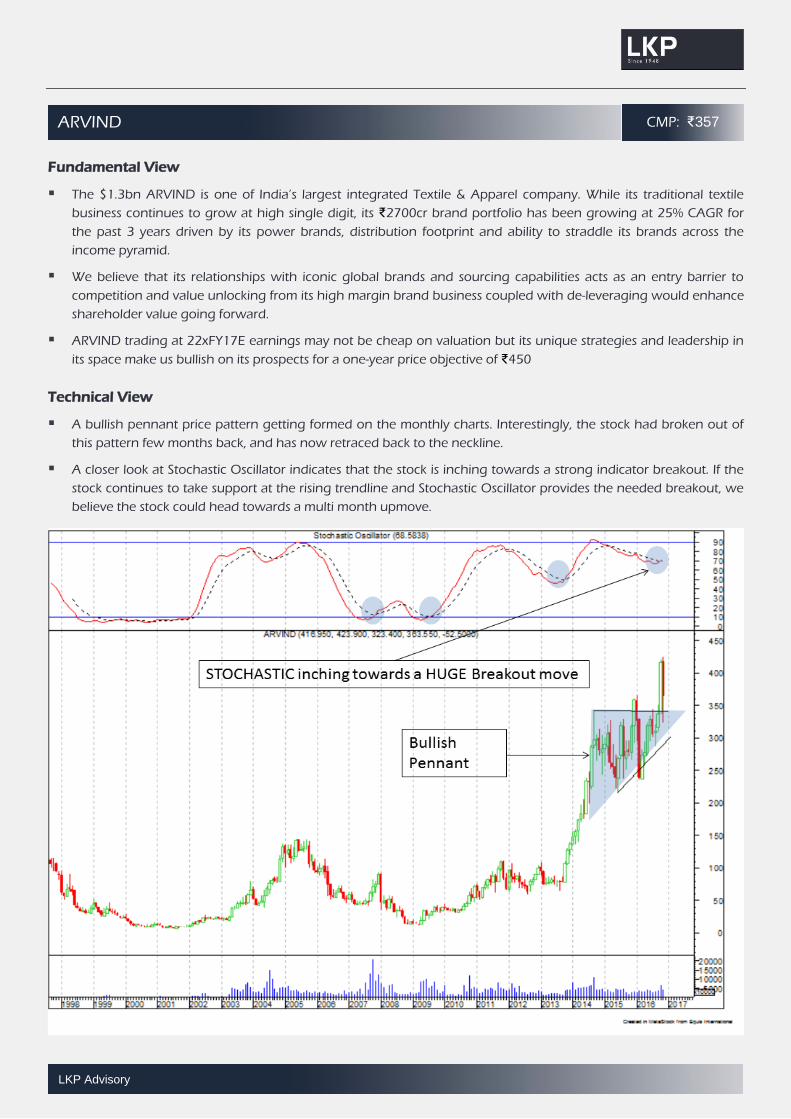

A bullish pennant price pattern getting formed on the monthly charts. Interestingly, the stock had broken out of

this pattern few months back, and has now retraced back to the neckline.

A closer look at Stochastic Oscillator indicates that the stock is inching towards a strong indicator breakout. If the

stock continues to take support at the rising trendline and Stochastic Oscillator provides the needed breakout, we

believe the stock could head towards a multi month upmove.

ARVIND CMP: ₹357

LKP Advisory

Fundamental View

There are close to 550 sugar mills in India of which BCML with a capacity of 76500TCD has the best balance sheet

among large integrated sugar mills. Its balance sheet strength enables BCML to hold on to its sugar inventory (

presently 18lac quintals costing ₹27.5 per kg ) and leverage the present buoyancy witnessed in sugar prices.

BCML has posted a huge turnaround in operations during H1 of this fiscal with net profits coming in at ₹217crs

compared to a loss of ₹84crs during the same period last fiscal. ( sugar prices in H1 of this fiscal were upwards of

₹35 per kg as against prices of ₹25 per kg in the same period last fiscal )

Its large co-generation facility of more than 150MW of saleable power and highly efficient distillery capacity of

320KLPD enables BCML to de-risk its business model during any kind of down cycle in its sugar business. We

recommend a BUY on BCML for a one-year price objective of ₹160

Technical View

One of the stronger sector from the start of 2016, the Sugar sector has provided extremely strong returns so far.

With cyclicalty nature of the sector, historically we have seen trends (up or down) lasting for few years for many of

these stocks.

Balrampur Chini has broken out of a Bullish price pattern on longer term time scales. We believe that in the near

term the stock has seen a correction and this correction halted at the rising resistance trendline.

If the indicator breaks out on the upside, we believe that Balrampur Chini can rally once again and be one of the

key performers in the sector.

BALRAMPUR CHINI MILLS. CMP: ₹121

LKP Advisory

Fundamental View

ICICI BANK is one of India’s largest banks with a large business franchise spanning close to 4500 branches and

over 14000 ATM with advances of over ₹4.5trillion. Well capitalized with Tier-I CAR of 13.25% and CASA of 45%

the bank has paid a heavy price for its high exposure to domestic corporates which now stand at 28% (exposure

to steel, cement, mining & power now stands at 12%)

While the key risk remains that of deterioration in asset quality ( NNPA now at ₹165bn is 3.2% ) we believe that its

exposure to retail loans now at 48% of total loans is growing at more than 20% and the bank should be able to

maintain 3% plus NIM quite comfortably going forward.

ICICI BANK is most widely held with FII holding at 50% and DII holding at 37%. We value the bank at 2.5x adjusted

book value to arrive at our one-year price objective of ₹310 by the end of CY 2017( The value of its Insurance

Subsidiary which is close to ₹40 per share provides additional comfort to the investor)

Technical View

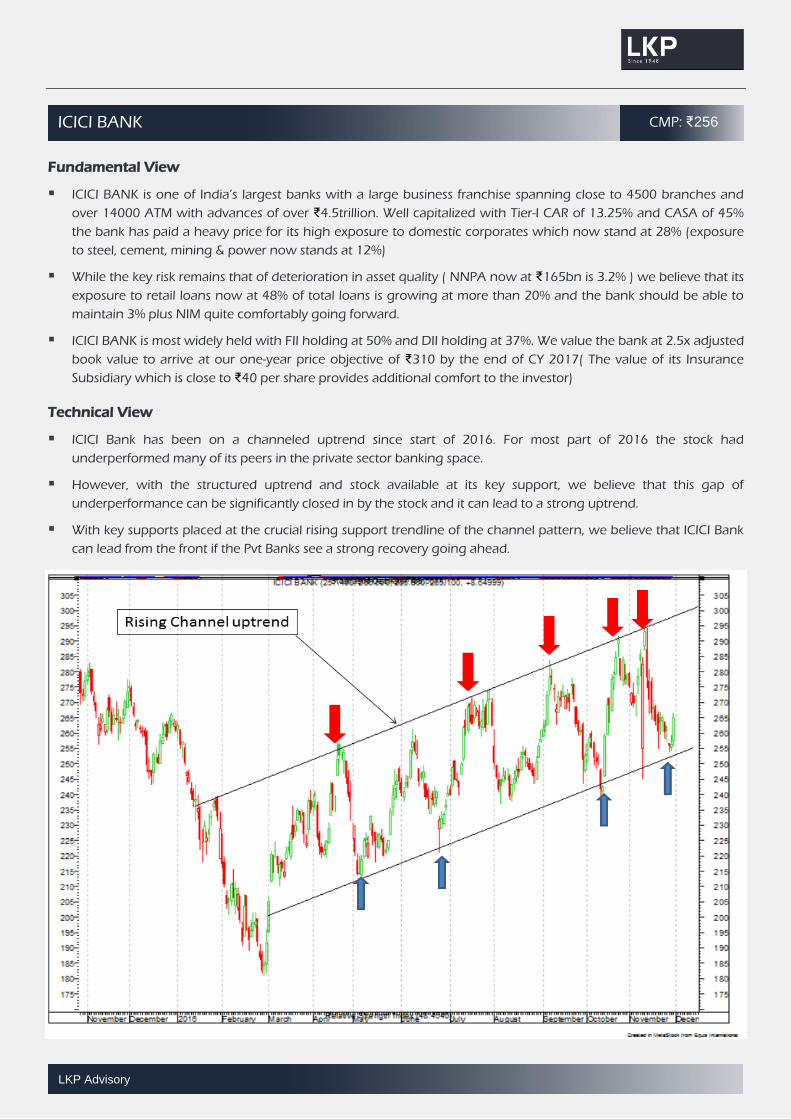

ICICI Bank has been on a channeled uptrend since start of 2016. For most part of 2016 the stock had

underperformed many of its peers in the private sector banking space.

However, with the structured uptrend and stock available at its key support, we believe that this gap of

underperformance can be significantly closed in by the stock and it can lead to a strong uptrend.

With key supports placed at the crucial rising support trendline of the channel pattern, we believe that ICICI Bank

can lead from the front if the Pvt Banks see a strong recovery going ahead.

ICICI BANK CMP: ₹256

LKP Advisory

Fundamental View

Jain Irrigation is the market leader in Micro Irrigation Systems – MIS and derives 45% of its revenues outside India.

A normal monsoon this year coming after two consecutive years of drought has brightened the prospects for the

company in some of its key markets like Maharashtra.

Jain Irrigation is also an household name in Agriculture & Plumbing solutions and its piping business is a key

beneficiary of lower polymer prices. The company stands well placed to bag orders under the AMRUT scheme of

the GOI.

Jain Irrigation has had tough times for the last two years and we expect the company to stage a turnaround in

operations this fiscal led by a good monsoon and possible structural triggers in certain key markets in India which

could provide an upside trigger as well going forward. We recommend a BUY on the stock for a one-year price

objective of ₹120

Technical View

Jain Irrigation has come out of a broadening triangle bottom formation. Spread across a multi month time frame,

such bottom patterns hold significant importance in proclaiming long term reversals.

Couple this with the increased volume participation in the last 8 odd months of this strong rally.

Recently, the price retraced to almost exactly 38.2% retracement of its recent price rally.

If we assume that this is the immediate medium term bottom, and use preliminary Fibonacci Projection ratios, till

61.8% projections, the stock could start a fresh rally and head towards a fresh 52 week high breakout soon.

JAIN IRRIGATION SYSTEMS CMP: ₹89

LKP Advisory

Fundamental View

KEC is a Global EPC major of the RPG Group and is a large player in Power Transmission & Distribution which

comprises of almost 70% of its ₹11000cr Order Book

Its Order Intake at ₹6000crs is up close to 30% YTD and has substantial L1 position close to 4000crs. 60% of its

business is from India and 40% is International. Its Railway Business is now gaining traction and is on a high

growth trajectory.

KEC has reported more than 100% growth in net profits during the first half of the current fiscal and is a big

beneficiary of lower interest rates going forward. We recommend a BUY on KEC with a one-year price objective of

₹180

Technical View

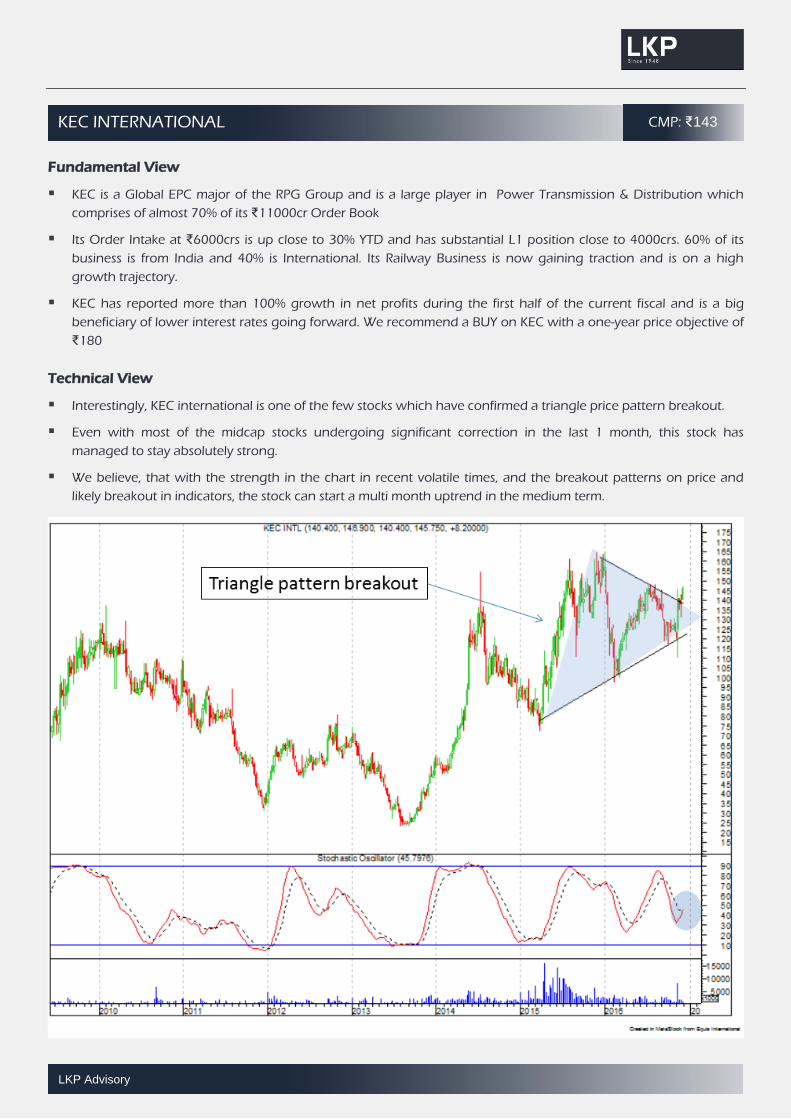

Interestingly, KEC international is one of the few stocks which have confirmed a triangle price pattern breakout.

Even with most of the midcap stocks undergoing significant correction in the last 1 month, this stock has

managed to stay absolutely strong.

We believe, that with the strength in the chart in recent volatile times, and the breakout patterns on price and

likely breakout in indicators, the stock can start a multi month uptrend in the medium term.

KEC INTERNATIONAL CMP: ₹143

DISCLAIMERS AND DISCLOSURES

LKP Securites Ltd, 13th Floor, Raheja Center, Free Press Road, Nariman Point, Mumbai-400 021. Tel :+91 22 66351234 Fax: +91 22 66351249. www.lkpsec.com

LKP Sec. ltd. (CIN-U67120MH1994PLC080039, www. Lkpsec.com) and its affiliates are a full-fledged, brokerage and financing group. LKP was established in

1992 and is one of India's leading brokerage and distribution house. LKP is a corporate trading member of Bombay Stock Exchange Limited (BSE), National

Stock Exchange of India Limited(NSE), MCX Stock Exchange Limited (MCX-SX).LKP along with its subsidiaries offers the most comprehensive avenues for

investments and is engaged in the businesses including stock broking (Institutional and retail), merchant banking, commodity broking, depository participant,

insurance broking and services rendered in connection with distribution of primary market issues and financial products like mutual funds etc.

LKP hereby declares that it has not defaulted with any stock exchange nor its activities were suspended by any stock exchange with whom it is registered in

last five years. However, SEBI and Stock Exchanges have conducted the routine inspection and based on their observations have issued advice letters or levied

minor penalty on LKP for certain operational deviations in ordinary/routine course of business. LKP has not been debarred from doing business by any Stock

Exchange / SEBI or any other authorities; nor has its certificate of registration been cancelled by SEBI at any point of time.

LKP offers research services to clients. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal

views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related

to specific recommendations or views expressed in this report.

Other disclosures by LKP and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to the subject company(s) covered in this

report-:

Research Analyst or his/her relative’s financial interest in the subject company. (NO)

LKP or its associates may have financial interest in the subject company.

LKP or its associates and Research Analyst or his/her relative’s does not have any material conflict of interest in the subject company. The research Analyst or

research entity (LKP) has not been engaged in market making activity for the subject company.

LKP or its associates may have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding

the date of publication of Research Report.

Research Analyst or his/her relatives have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately

preceding the date of publication of Research Report: (NO)

LKP or its associates may have received any compensation including for investment banking or merchant banking or brokerage services from the subject

company in the past 12 months.

LKP or its associates may have received compensation for products or services other than investment banking or merchant banking or brokerage services from

the subject company in the past 12 months.

LKP or its associates may have received any compensation or other benefits from the Subject Company or third party in connection with the research report.

Subject Company may have been client of LKP or its associates during twelve months preceding the date of distribution of the research report and LKP may

have co-managed public offering of securities for the subject company in the past twelve months.

Research Analyst has served as officer, director or employee of the subject company: (NO)

LKP and/or its affiliates may seek investment banking or other business from the company or companies that are the subject of this material. Our salespeople,

traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to

the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that may be inconsistent with the

recommendations expressed herein.

In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest

including but not limited to those stated herein. Additionally, other important information regarding our relationships with the company or companies that

are the subject of this material is provided herein. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or

resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or

regulation or which would subject LKP or its group companies to any registration or licensing requirement within such jurisdiction. Specifically, this document

does not constitute an offer to or solicitation to any U.S. person for the purchase or sale of any financial instrument or as an official confirmation of any

transaction to any U.S. person.

Unless otherwise stated, this message should not be construed as official confirmation of any transaction. No part of this document may be distributed in

Canada or used by private customers in United Kingdom.

All trademarks, service marks and logos used in this report are trademarks or registered trademarks of LKP or its Group Companies. The information contained

herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or

copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital

Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Indian Securities Market. In so far as this report

includes current or historic information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

All material presented in this report, unless specifically indicated otherwise, is under copyright to LKP. None of the material, nor its content, nor any copy of it,

may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of LKP