1. The Crop Sector in Ethiopia-Current and Future ...

31

The Crop Sector in Ethiopia- Current and Future Prospects 6 th March 2018 Eyasu Abraha (PhD), Minister, FDRE-MoANR

Transcript of 1. The Crop Sector in Ethiopia-Current and Future ...

The Crop Sector in Ethiopia-Current and Future Prospects

6th March 2018

Eyasu Abraha (PhD), Minister, FDRE-MoANR

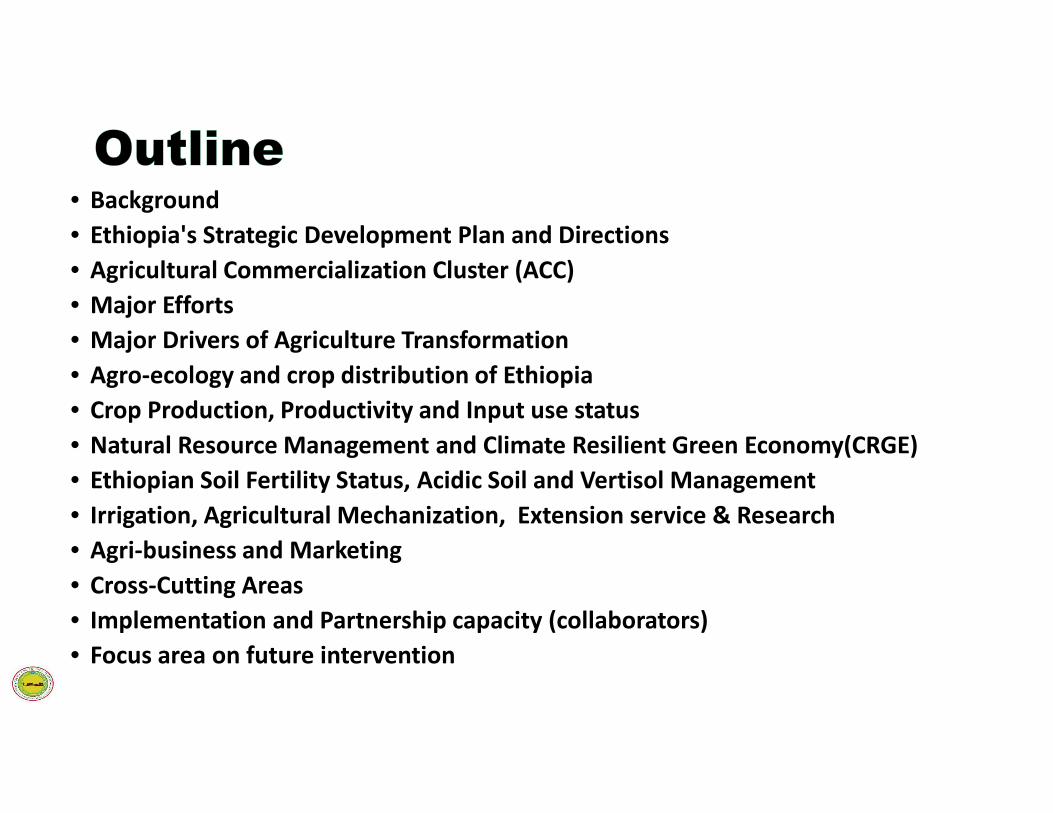

• Background

• Ethiopia's Strategic Development Plan and Directions

• Agricultural Commercialization Cluster (ACC)

• Major Efforts

• Major Drivers of Agriculture Transformation

• Agro-ecology and crop distribution of Ethiopia

• Crop Production, Productivity and Input use status

• Natural Resource Management and Climate Resilient Green Economy(CRGE)

• Ethiopian Soil Fertility Status, Acidic Soil and Vertisol Management

• Irrigation, Agricultural Mechanization, Extension service & Research

• Agri-business and Marketing

• Cross-Cutting Areas

• Implementation and Partnership capacity (collaborators)

• Focus area on future intervention

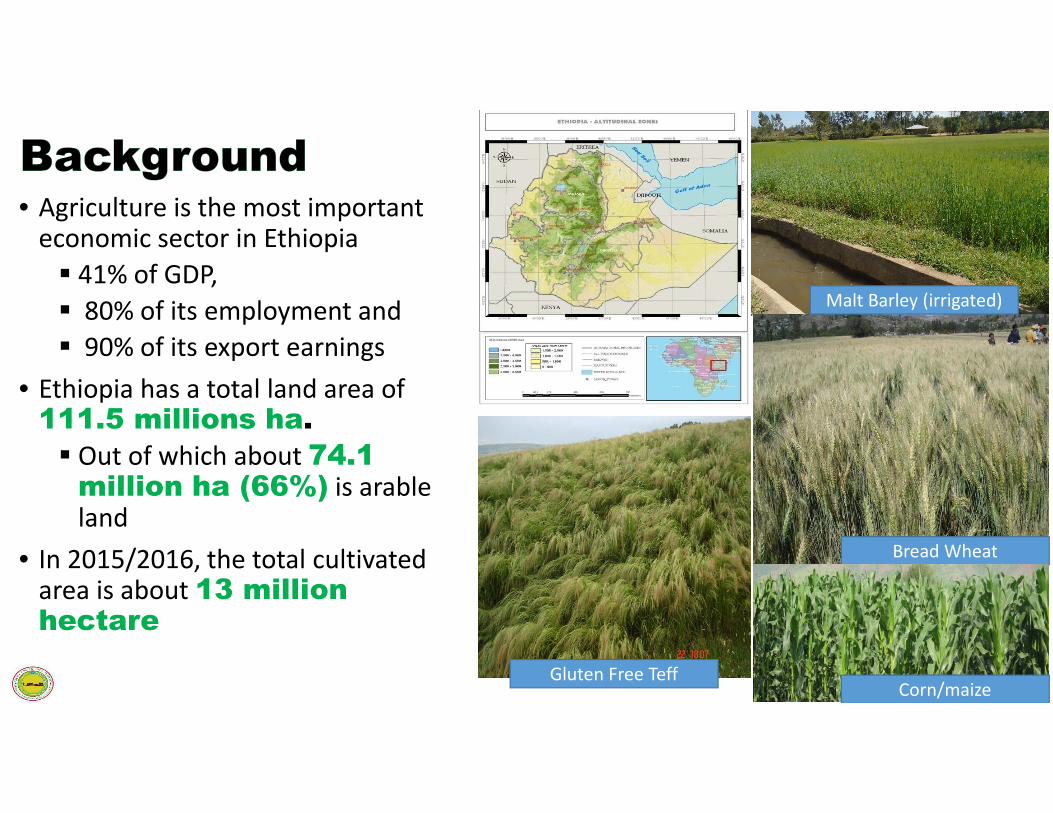

• Agriculture is the most important economic sector in Ethiopia

� 41% of GDP,

� 80% of its employment and

� 90% of its export earnings

• Ethiopia has a total land area of 111.5 millions ha.

� Out of which about 74.1 million ha (66%) is arable land

• In 2015/2016, the total cultivated area is about 13 million hectare

Malt Barley (irrigated)

Bread Wheat

Gluten Free TeffCorn/maize

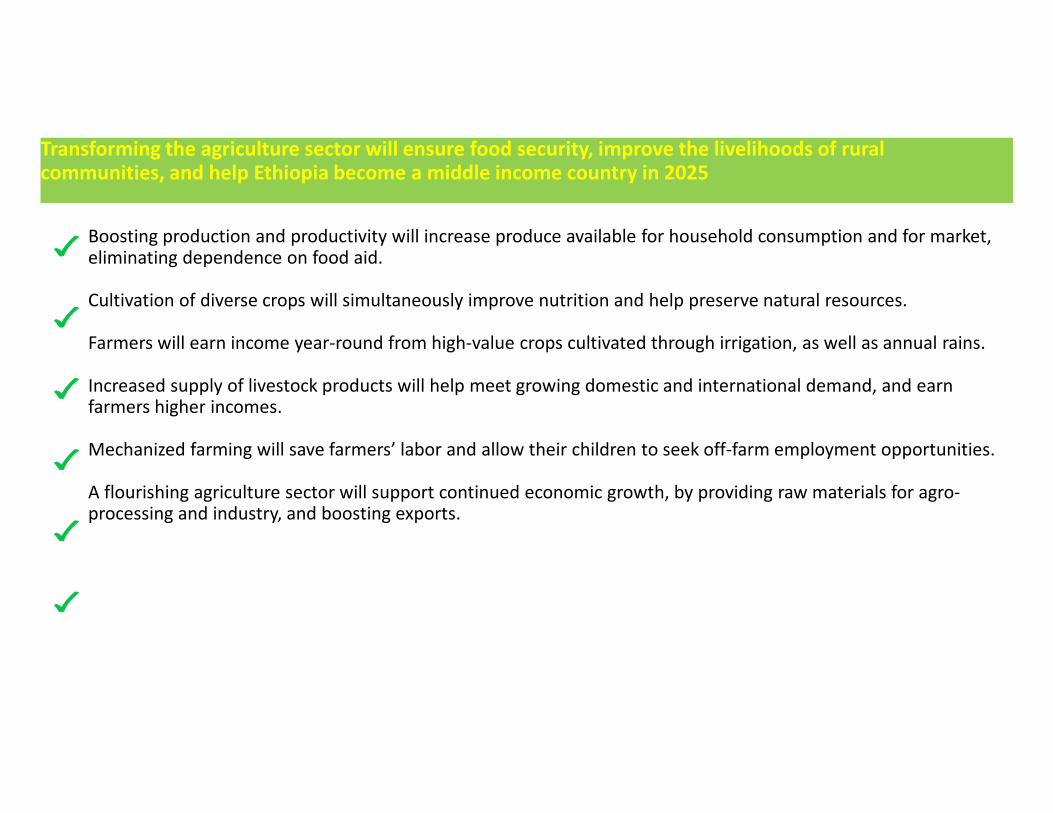

Transforming the agriculture sector will ensure food security, improve the livelihoods of rural communities, and help Ethiopia become a middle income country in 2025

Boosting production and productivity will increase produce available for household consumption and for market, eliminating dependence on food aid.

Cultivation of diverse crops will simultaneously improve nutrition and help preserve natural resources.

Farmers will earn income year-round from high-value crops cultivated through irrigation, as well as annual rains.

Increased supply of livestock products will help meet growing domestic and international demand, and earn farmers higher incomes.

Mechanized farming will save farmers’ labor and allow their children to seek off-farm employment opportunities.

A flourishing agriculture sector will support continued economic growth, by providing raw materials for agro-processing and industry, and boosting exports.

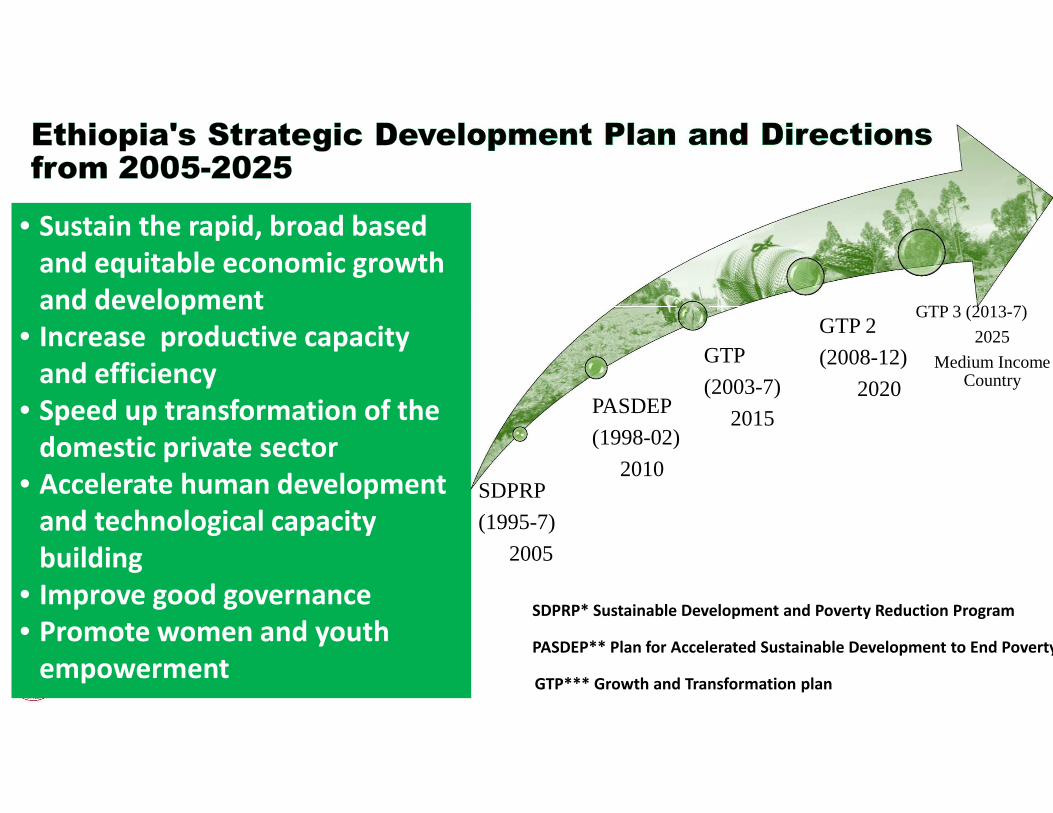

• Sustain the rapid, broad based

and equitable economic growth

and development

• Increase productive capacity

and efficiency

• Speed up transformation of the

domestic private sector

• Accelerate human development

and technological capacity

building

• Improve good governance

• Promote women and youth

empowerment

SDPRP

(1995-7)

2005

PASDEP

(1998-02)

2010

GTP

(2003-7)

2015

GTP 2

(2008-12)

2020

GTP 3 (2013-7)

2025

Medium Income Country

SDPRP* Sustainable Development and Poverty Reduction Program

PASDEP** Plan for Accelerated Sustainable Development to End Poverty

GTP*** Growth and Transformation plan

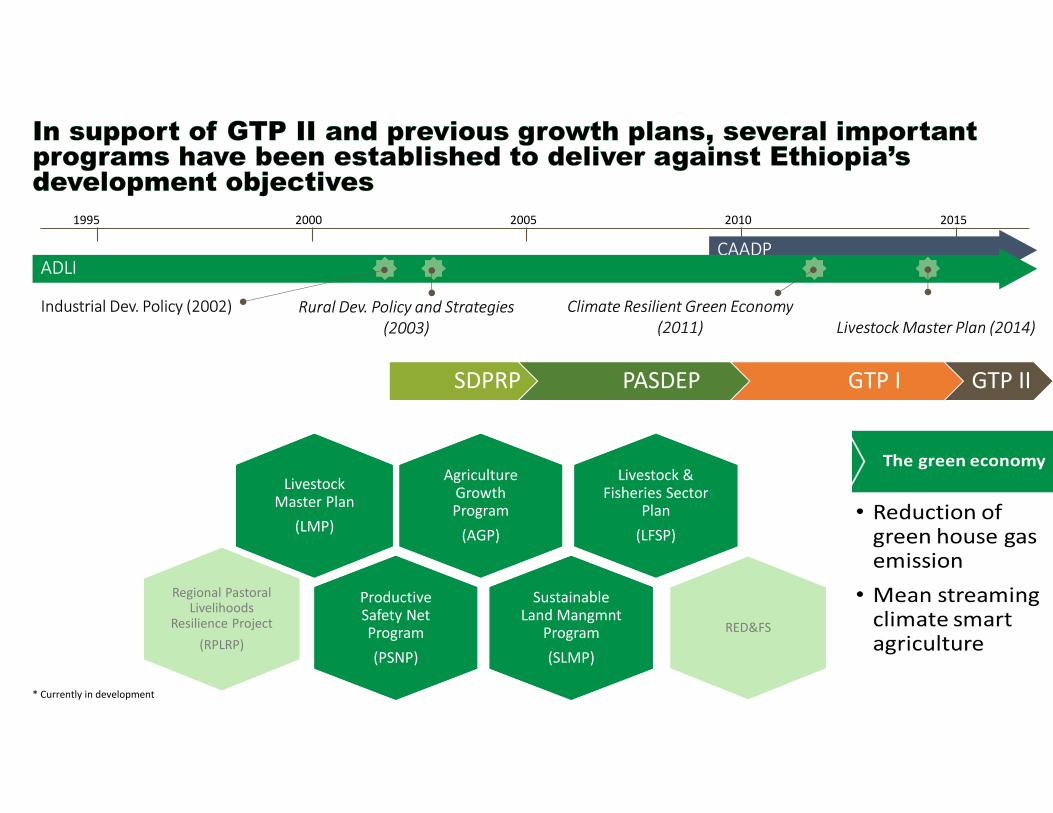

1995 2000 2005 2010 2015

CAADP

Industrial Dev. Policy (2002) Rural Dev. Policy and Strategies

(2003)

ADLI

Climate Resilient Green Economy

(2011) Livestock Master Plan (2014)

SDPRP PASDEP GTP I GTP II

Agriculture Growth Program

(AGP)

Agriculture Growth Program

(AGP)

Livestock Master Plan

(LMP)

Livestock Master Plan

(LMP)

Productive Safety Net Program

(PSNP)

Productive Safety Net Program

(PSNP)

Sustainable Land Mangmnt

Program

(SLMP)

Sustainable Land Mangmnt

Program

(SLMP)

Livestock & Fisheries Sector

Plan

(LFSP)

Livestock & Fisheries Sector

Plan

(LFSP)

RED&FS

Regional Pastoral Livelihoods

Resilience Project

(RPLRP)

* Currently in development

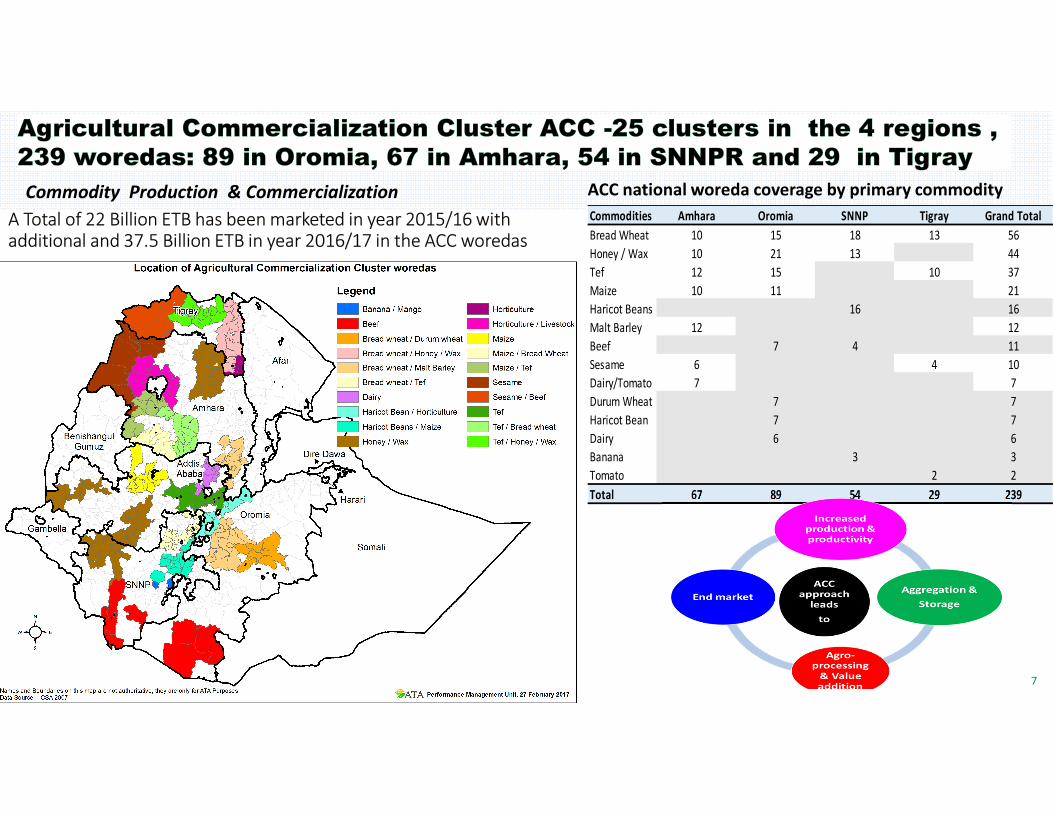

7

Commodities Amhara Oromia SNNP Tigray Grand Total

Bread Wheat 10 15 18 13 56

Honey / Wax 10 21 13 44

Tef 12 15 10 37

Maize 10 11 21

Haricot Beans 16 16

Malt Barley 12 12

Beef 7 4 11

Sesame 6 4 10

Dairy/Tomato 7 7

Durum Wheat 7 7

Haricot Bean 7 7

Dairy 6 6

Banana 3 3

Tomato 2 2

Total 67 89 54 29 239

ACC national woreda coverage by primary commodity Commodity Production & Commercialization

A Total of 22 Billion ETB has been marketed in year 2015/16 with additional and 37.5 Billion ETB in year 2016/17 in the ACC woredas

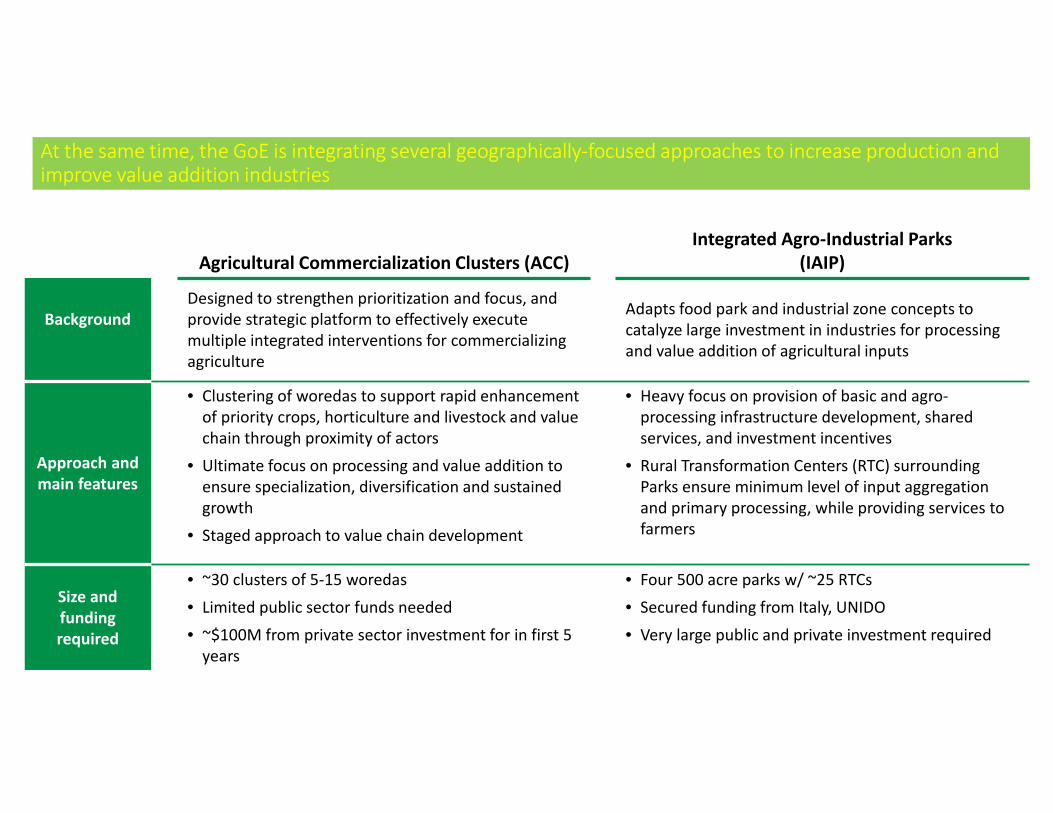

At the same time, the GoE is integrating several geographically-focused approaches to increase production and improve value addition industries

Agricultural Commercialization Clusters (ACC)

Integrated Agro-Industrial Parks

(IAIP)

Background

Designed to strengthen prioritization and focus, and

provide strategic platform to effectively execute

multiple integrated interventions for commercializing

agriculture

Adapts food park and industrial zone concepts to

catalyze large investment in industries for processing

and value addition of agricultural inputs

Approach and

main features

• Clustering of woredas to support rapid enhancement

of priority crops, horticulture and livestock and value

chain through proximity of actors

• Ultimate focus on processing and value addition to

ensure specialization, diversification and sustained

growth

• Staged approach to value chain development

• Heavy focus on provision of basic and agro-

processing infrastructure development, shared

services, and investment incentives

• Rural Transformation Centers (RTC) surrounding

Parks ensure minimum level of input aggregation

and primary processing, while providing services to

farmers

Size and

funding

required

• ~30 clusters of 5-15 woredas

• Limited public sector funds needed

• ~$100M from private sector investment for in first 5

years

• Four 500 acre parks w/ ~25 RTCs

• Secured funding from Italy, UNIDO

• Very large public and private investment required

• Conducive policy and strategies are in place• Packages, scaling up of best practices• Monitoring and Evaluation • Several stakeholders involvement • Agricultural commercialization cluster• Mass mobilization for natural resource management• Capacity building

• FTC (14,000), • ATVT (25 )• DA (66,266)• Extension service reached to 16 million house hold; • Infrastructures, massive rural job created • Massive Human Capacity Building (millions of households trained)• Model farmers average yield (27.7qtl/ha)

• Integrated Agro-industrial Parks in Ethiopia (about 4 ready from 17)

• Drive the structural transformation of the Ethiopian economy; • Reduce rural poverty; • Create a better environment for increased investment in agro-food

and allied sectors.

Rice Farm in Fogera, Amhara

Sesame farm in Metema, Amhara

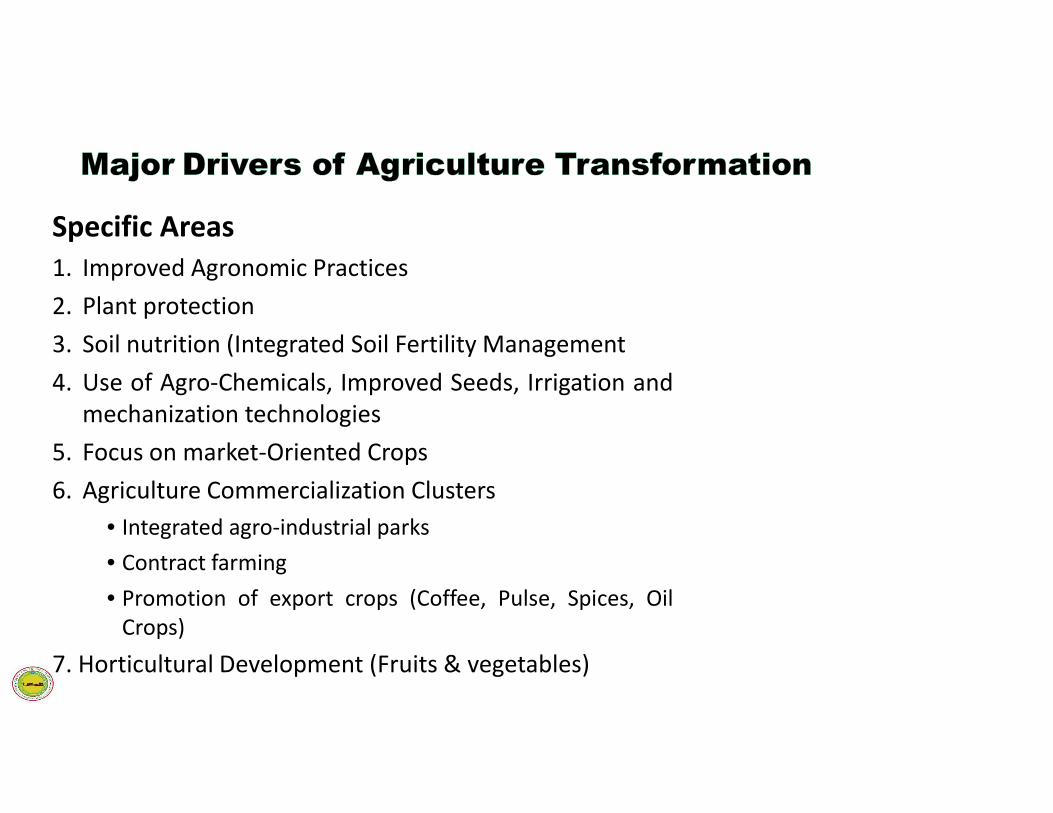

Specific Areas

1. Improved Agronomic Practices

2. Plant protection

3. Soil nutrition (Integrated Soil Fertility Management

4. Use of Agro-Chemicals, Improved Seeds, Irrigation and

mechanization technologies

5. Focus on market-Oriented Crops

6. Agriculture Commercialization Clusters

• Integrated agro-industrial parks

• Contract farming

• Promotion of export crops (Coffee, Pulse, Spices, Oil

Crops)

7. Horticultural Development (Fruits & vegetables)

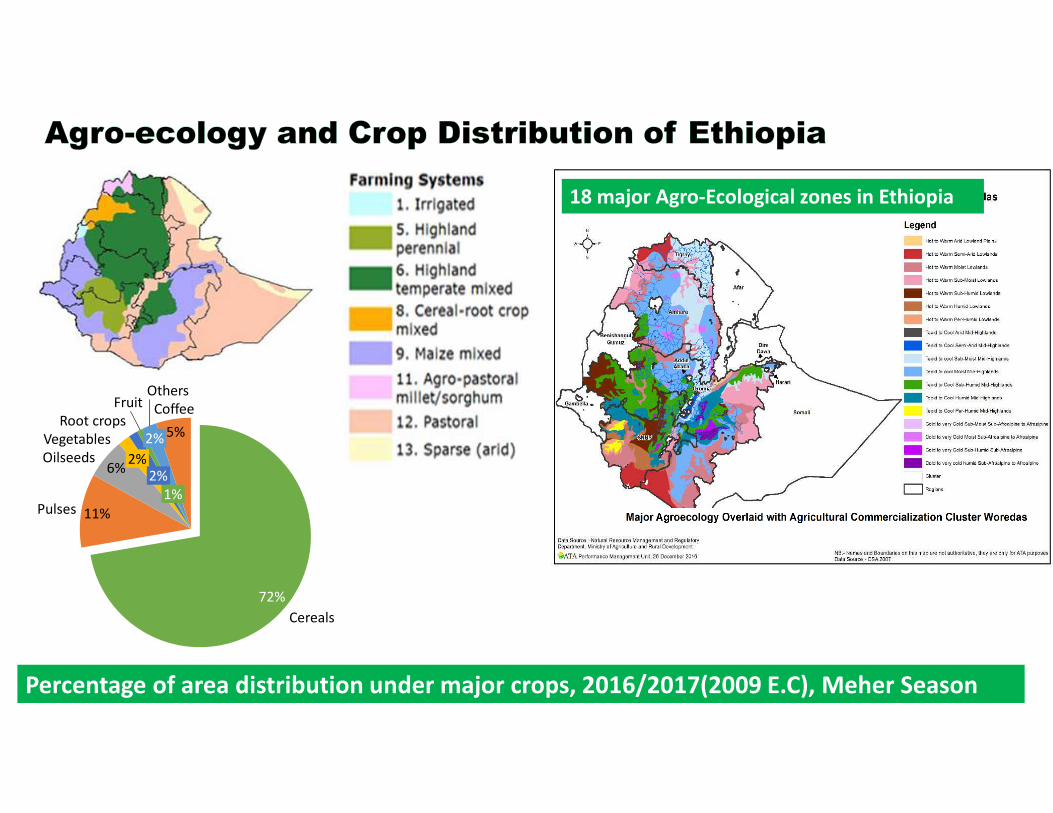

Vegetables

6%

Pulses

2%2%

Coffee

Oilseeds

11%

2%

72%

1%

Others

5%

Cereals

Fruit

Root crops

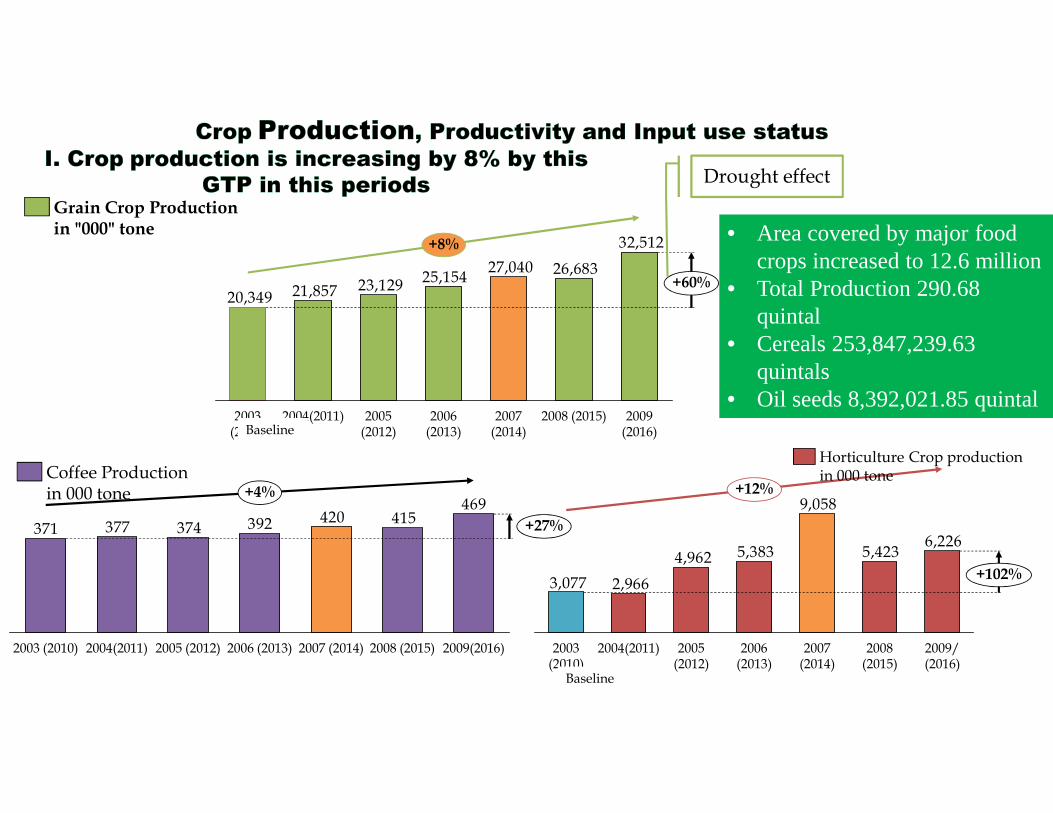

Percentage of area distribution under major crops, 2016/2017(2009 E.C), Meher Season

18 major Agro-Ecological zones in Ethiopia

6,2265,423

9,058

5,3834,962

2,9663,077

+12%

2005 (2012)

2008 (2015)

2006 (2013)

+102%

2009/ (2016)

2007 (2014)

2004(2011)2003 (2010)

469415420392374377371 +27%

2009(2016)2003 (2010) 2007 (2014)2006 (2013)2005 (2012) 2008 (2015)2004(2011)

+4%

32,512

26,68327,04025,154

23,12921,85720,349

2006 (2013)

2004(2011)2003 (2010)

2005 (2012)

+8%

2008 (2015)

+60%

2009 (2016)

2007 (2014)

Grain Crop Production in "000" tone

Baseline

Drought effect

Horticulture Crop productionin 000 tone

Baseline

Coffee Productionin 000 tone

• Area covered by major food crops increased to 12.6 million

• Total Production 290.68 quintal

• Cereals 253,847,239.63 quintals

• Oil seeds 8,392,021.85 quintal

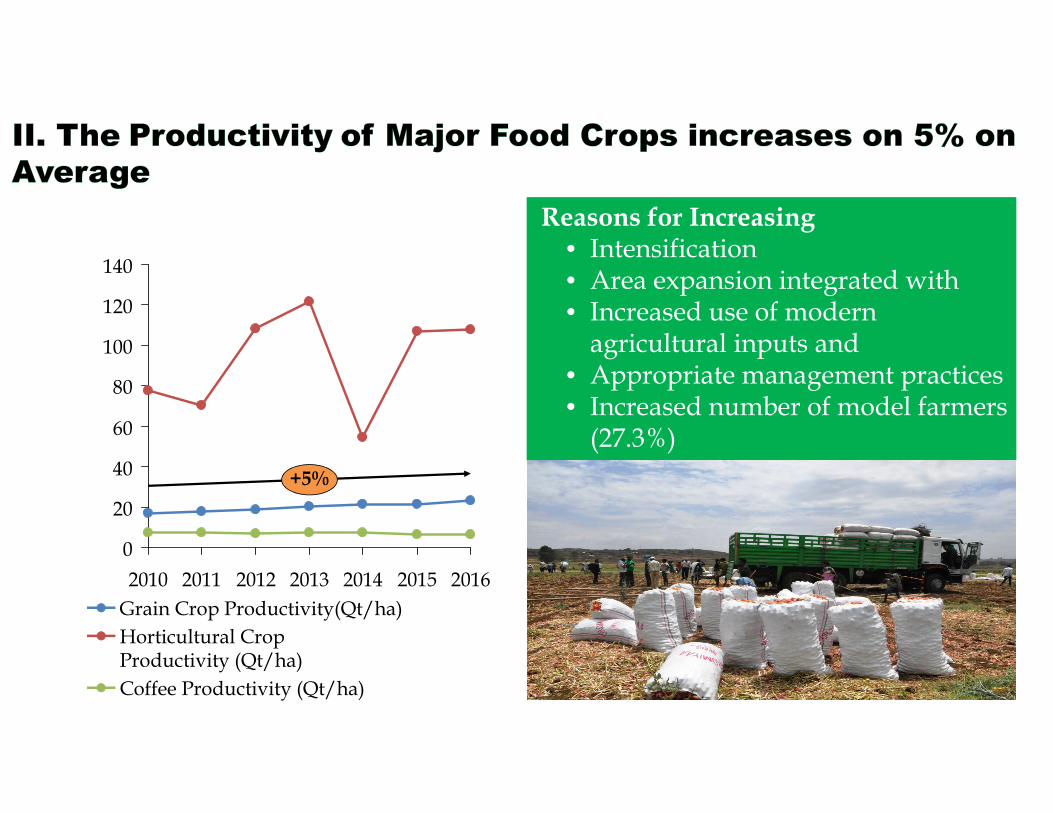

0

20

40

60

80

100

120

140

2010 2011 2012 2013 2014 2015 2016

+5%

Reasons for Increasing • Intensification• Area expansion integrated with• Increased use of modern

agricultural inputs and• Appropriate management practices • Increased number of model farmers

(27.3%)

Grain Crop Productivity(Qt/ha)

Coffee Productivity (Qt/ha)

Horticultural Crop Productivity (Qt/ha)

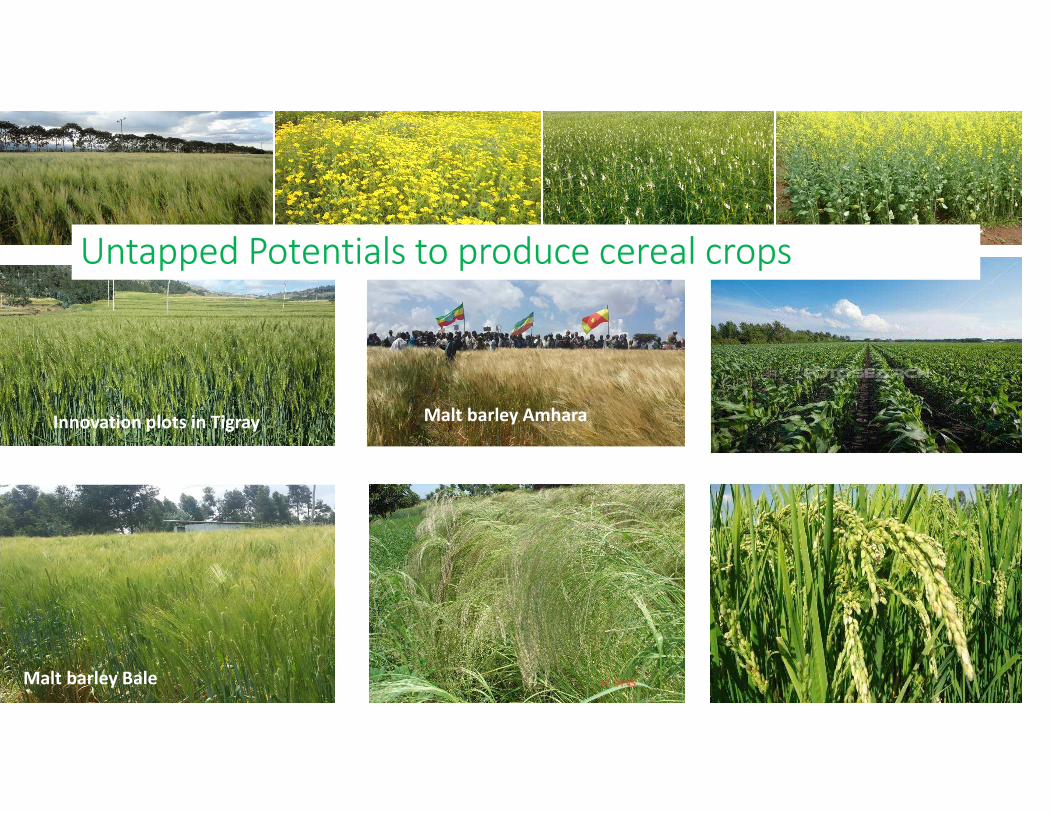

Innovation plots in Tigray

Malt barley Bale

Malt barley Amhara

Untapped Potentials to produce cereal crops

1,500,000

0

3,500,000

3,000,000

2,000,000

2,500,000

1,000,000

500,000

2013

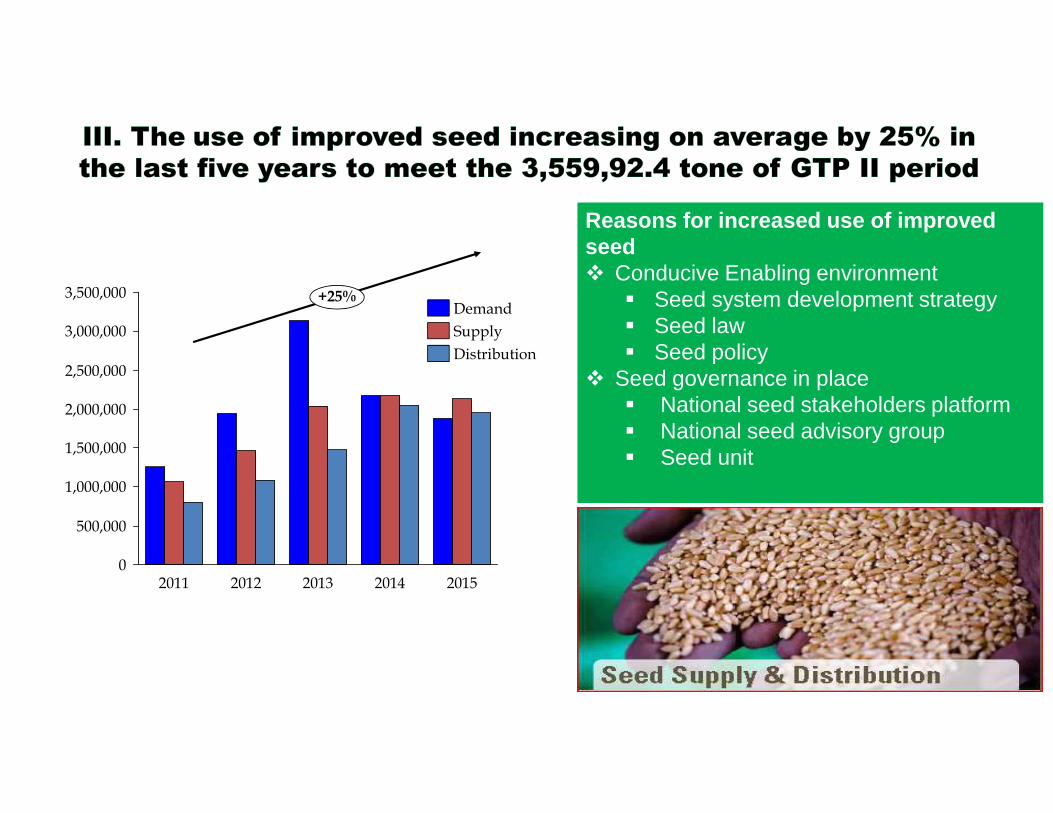

+25%

2011 2012 2014 2015

Demand

Supply

Distribution

Reasons for increased use of improved seed � Conducive Enabling environment

� Seed system development strategy� Seed law � Seed policy

� Seed governance in place� National seed stakeholders platform� National seed advisory group� Seed unit

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

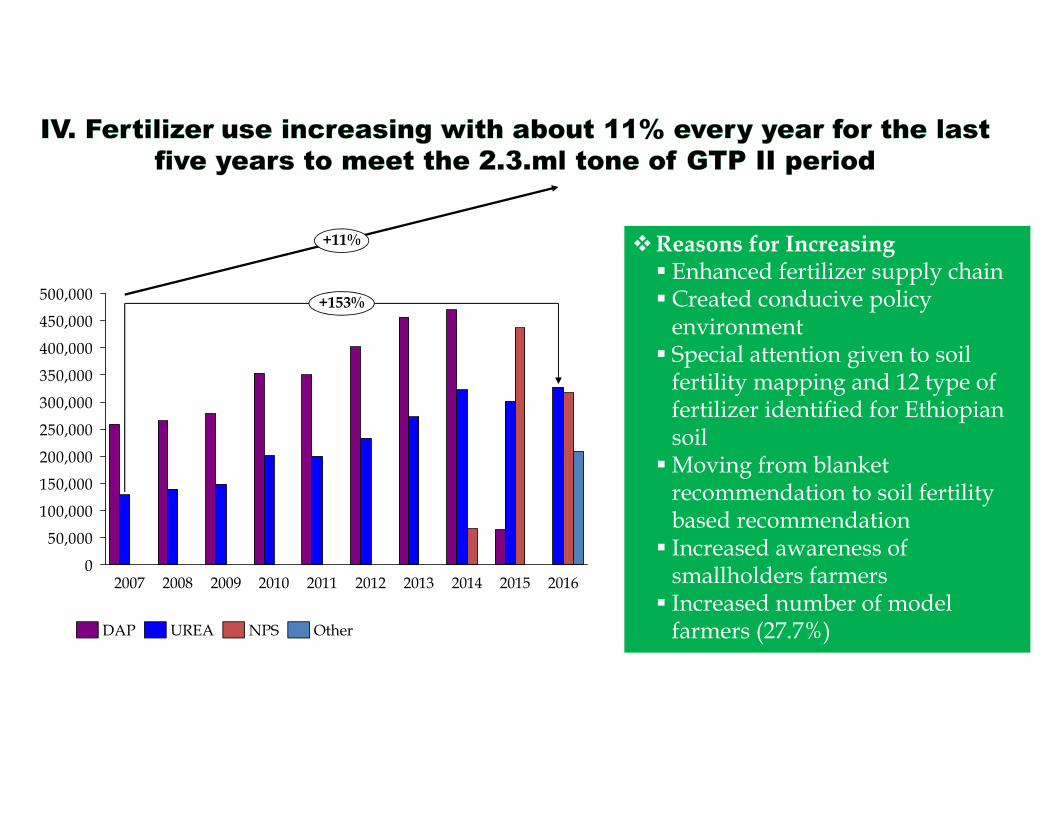

20082007 2009

+153%

20132011 20122010 2014 2015 2016

+11%

DAP NPSUREA Other

�Reasons for Increasing � Enhanced fertilizer supply chain � Created conducive policy

environment� Special attention given to soil

fertility mapping and 12 type of fertilizer identified for Ethiopian soil

� Moving from blanket recommendation to soil fertility based recommendation

� Increased awareness of smallholders farmers

� Increased number of model farmers (27.7%)

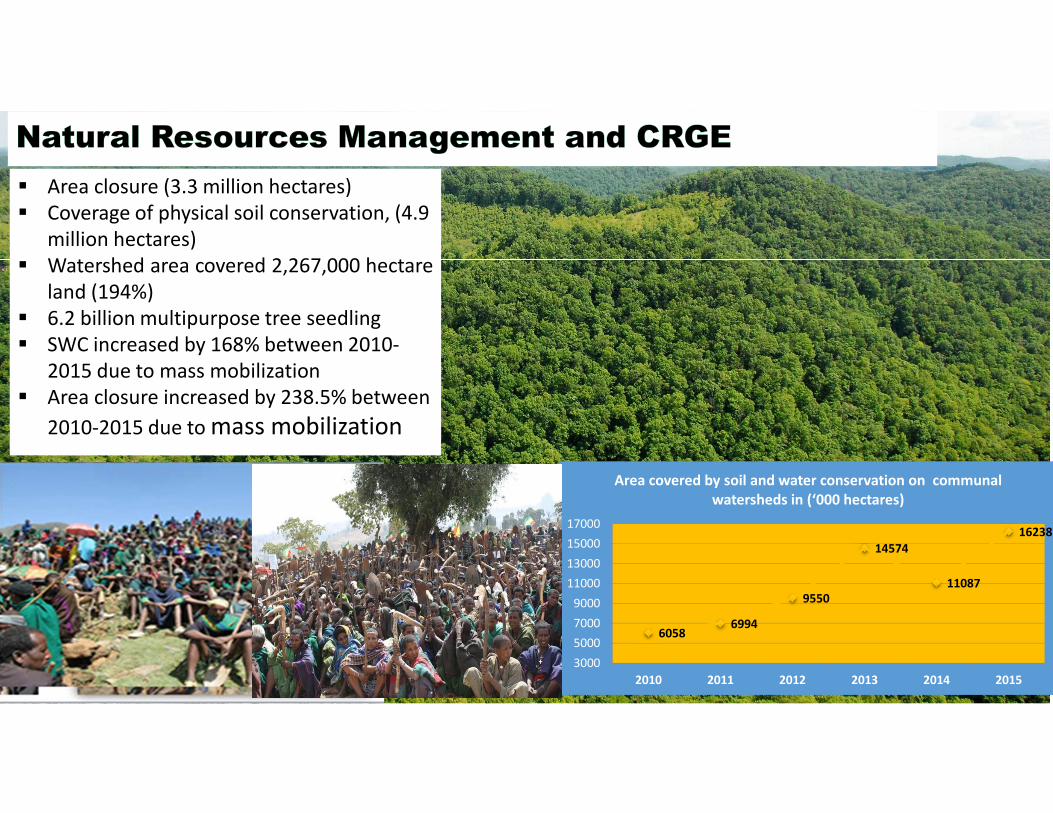

� Area closure (3.3 million hectares)

� Coverage of physical soil conservation, (4.9

million hectares)

� Watershed area covered 2,267,000 hectare

land (194%)

� 6.2 billion multipurpose tree seedling

� SWC increased by 168% between 2010-

2015 due to mass mobilization

� Area closure increased by 238.5% between

2010-2015 due to mass mobilization

60586994

9550

14574

11087

16238

3000

5000

7000

9000

11000

13000

15000

17000

2010 2011 2012 2013 2014 2015

Area covered by soil and water conservation on communal

watersheds in (‘000 hectares)

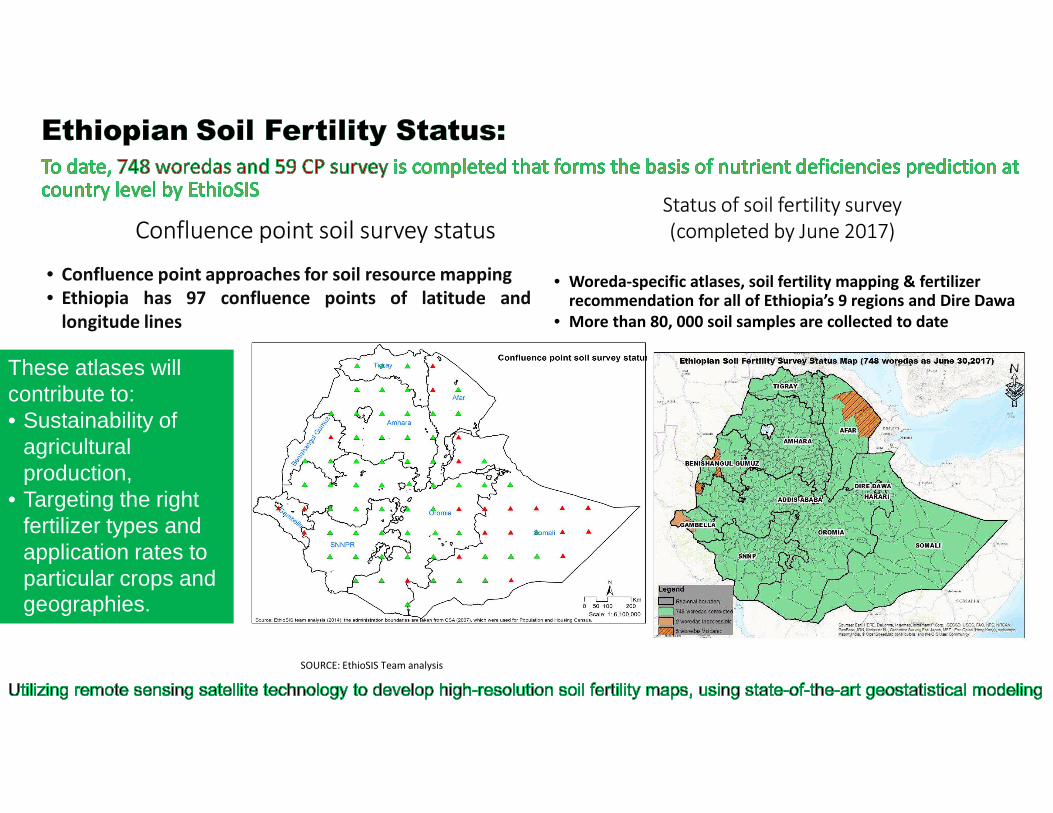

Confluence point soil survey statusStatus of soil fertility survey

(completed by June 2017)

• Confluence point approaches for soil resource mapping

• Ethiopia has 97 confluence points of latitude and

longitude lines

• Woreda-specific atlases, soil fertility mapping & fertilizer recommendation for all of Ethiopia’s 9 regions and Dire Dawa

• More than 80, 000 soil samples are collected to date

SOURCE: EthioSIS Team analysis

These atlases will contribute to:• Sustainability of

agricultural production,

• Targeting the right fertilizer types and application rates to particular crops and geographies.

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

4,500.0

5,000.0

5,500.0

6,000.0

20102011

20122013

20142015

2,210.0

1,470.0 1,512.1

6,000.0 6,000.0

1510

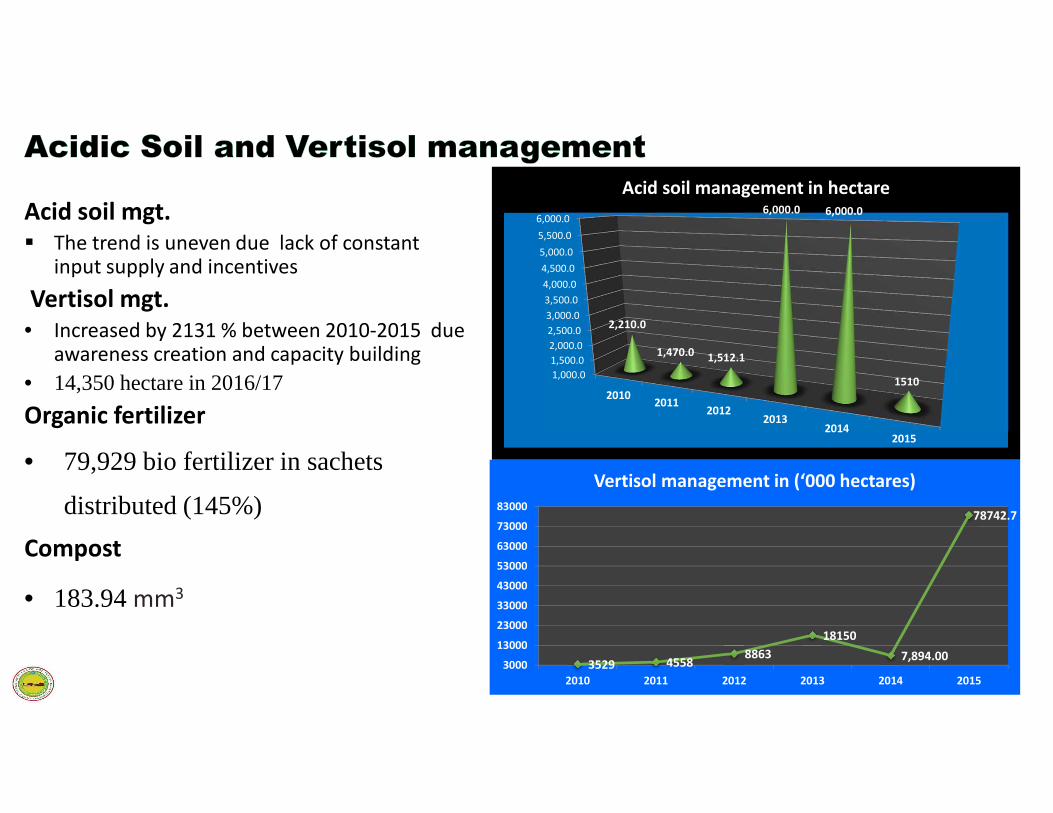

Acid soil management in hectare

Acid soil mgt.

� The trend is uneven due lack of constant input supply and incentives

Vertisol mgt.

• Increased by 2131 % between 2010-2015 due awareness creation and capacity building

• 14,350 hectare in 2016/17

Organic fertilizer

• 79,929 bio fertilizer in sachets

distributed (145%)

Compost

• 183.94 mm3

3529 45588863

18150

7,894.00

78742.7

3000

13000

23000

33000

43000

53000

63000

73000

83000

2010 2011 2012 2013 2014 2015

Vertisol management in (‘000 hectares)

:

853.1

1064.2

1460

1830

2047.4

2344.76

y = 307.94x + 522.12

500

700

900

1100

1300

1500

1700

1900

2100

2300

2500

2010 2011 2012 2013 2014 2015

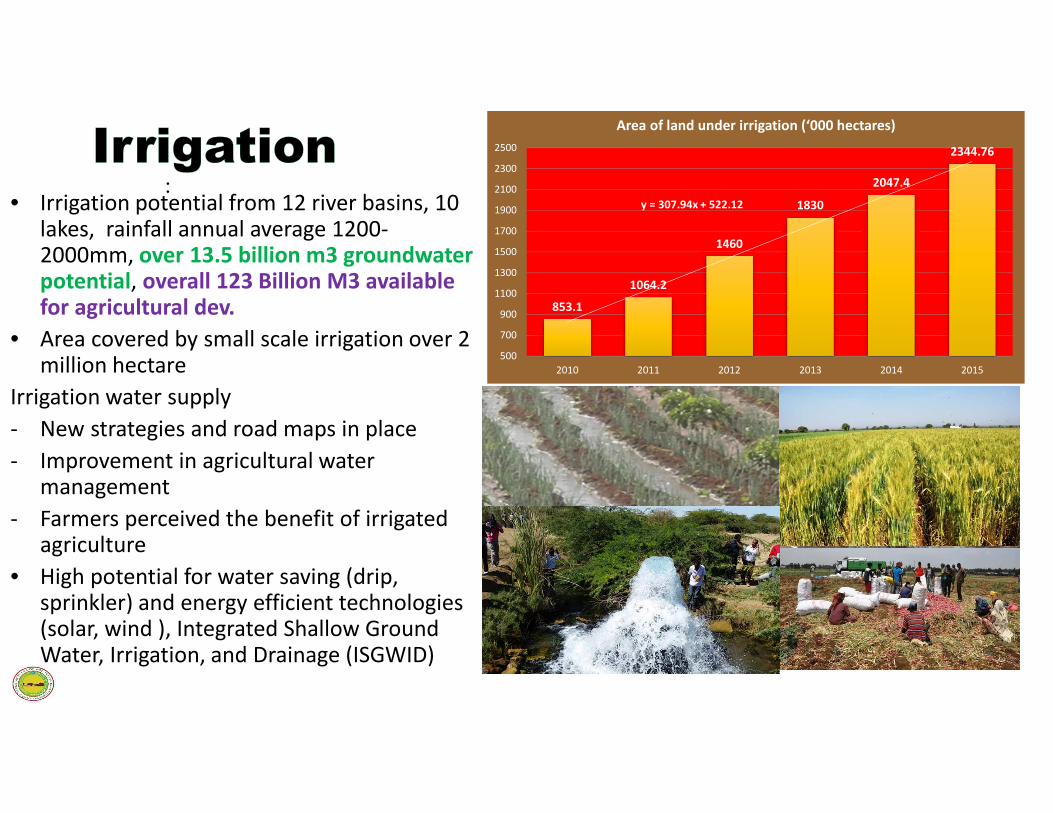

Area of land under irrigation (‘000 hectares)

• Irrigation potential from 12 river basins, 10 lakes, rainfall annual average 1200-2000mm, over 13.5 billion m3 groundwater potential, overall 123 Billion M3 available for agricultural dev.

• Area covered by small scale irrigation over 2 million hectare

Irrigation water supply

- New strategies and road maps in place

- Improvement in agricultural water management

- Farmers perceived the benefit of irrigated agriculture

• High potential for water saving (drip, sprinkler) and energy efficient technologies (solar, wind ), Integrated Shallow Ground Water, Irrigation, and Drainage (ISGWID)

• Commercializing the

small holder

agriculture

• Cover 209 words 25

clusters 11 strategic

crops

• Labour intensive

mechanization

equipment

• Mechanization service

provision promotion

• Creating rural job

Components and actors in sustainable agri. mechanization

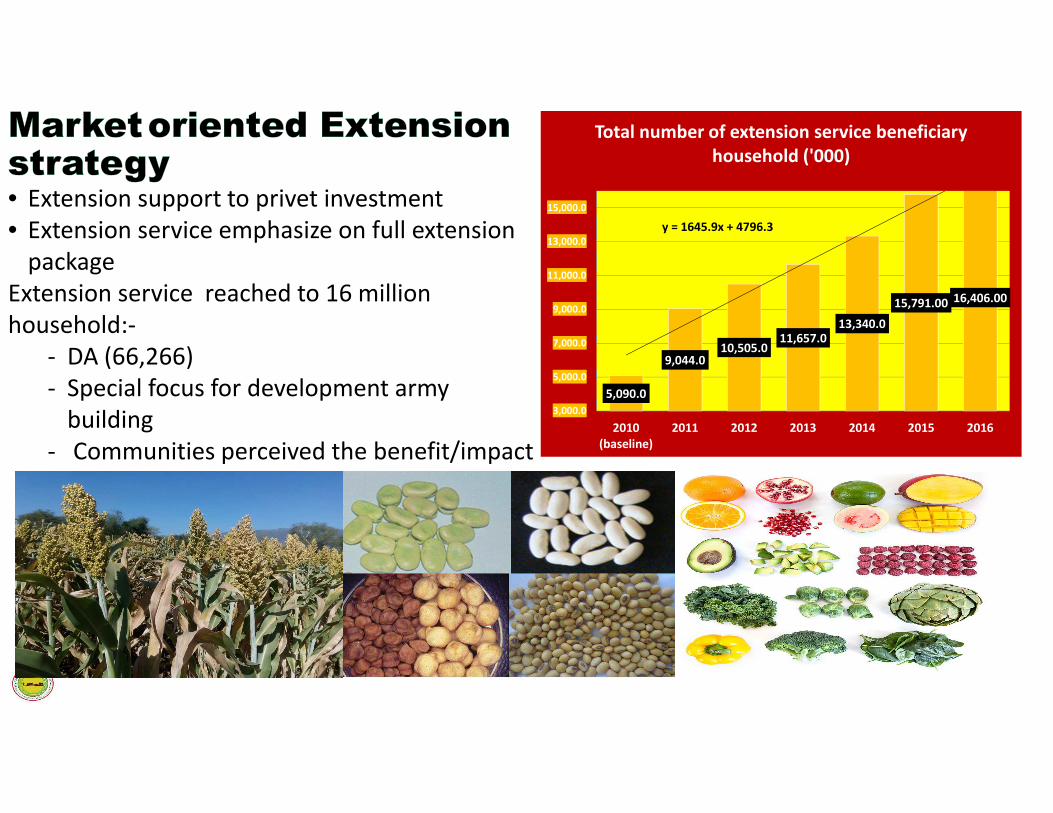

• Extension support to privet investment

• Extension service emphasize on full extension

package

Extension service reached to 16 million

household:-

- DA (66,266)

- Special focus for development army

building

- Communities perceived the benefit/impact

5,090.0

9,044.010,505.0

11,657.013,340.0

15,791.00 16,406.00

y = 1645.9x + 4796.3

3,000.0

5,000.0

7,000.0

9,000.0

11,000.0

13,000.0

15,000.0

2010

(baseline)

2011 2012 2013 2014 2015 2016

Total number of extension service beneficiary

household ('000)

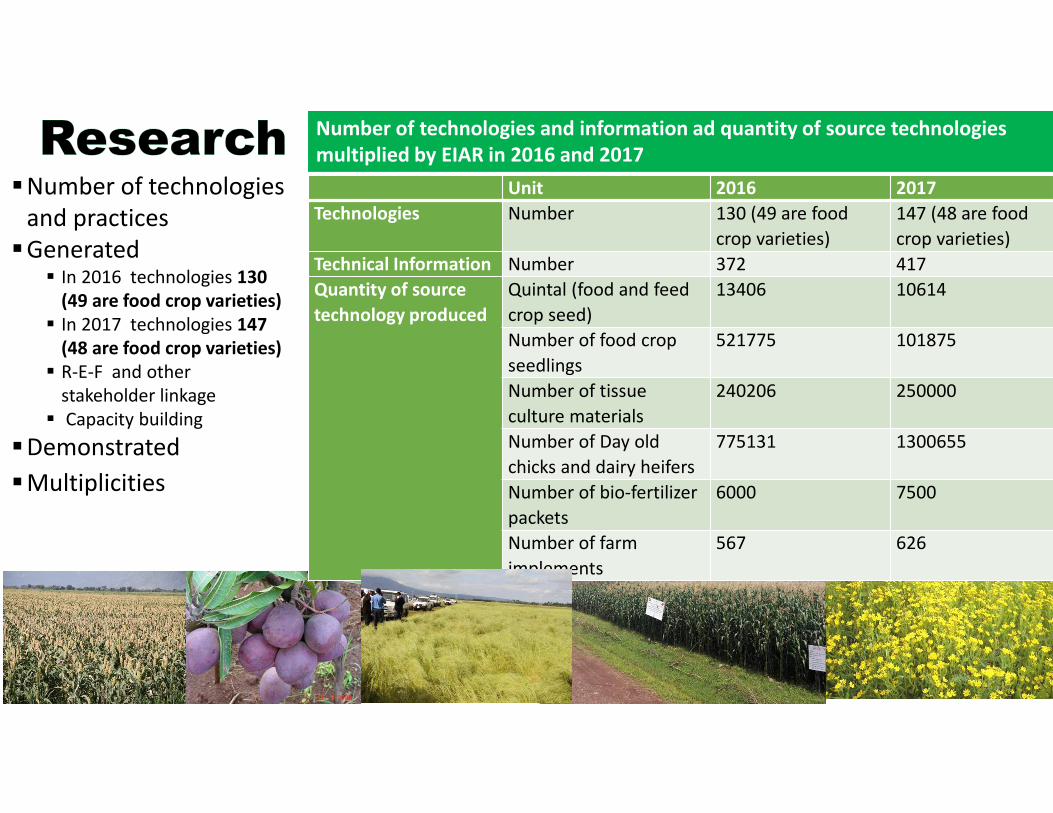

�Number of technologies

and practices

�Generated � In 2016 technologies 130

(49 are food crop varieties)

� In 2017 technologies 147

(48 are food crop varieties)

� R-E-F and other

stakeholder linkage

� Capacity building

�Demonstrated

�Multiplicities

Unit 2016 2017

Technologies Number 130 (49 are food

crop varieties)

147 (48 are food

crop varieties)

Technical Information Number 372 417

Quantity of source

technology produced

Quintal (food and feed

crop seed)

13406 10614

Number of food crop

seedlings

521775 101875

Number of tissue

culture materials

240206 250000

Number of Day old

chicks and dairy heifers

775131 1300655

Number of bio-fertilizer

packets

6000 7500

Number of farm

implements

567 626

Number of technologies and information ad quantity of source technologies

multiplied by EIAR in 2016 and 2017

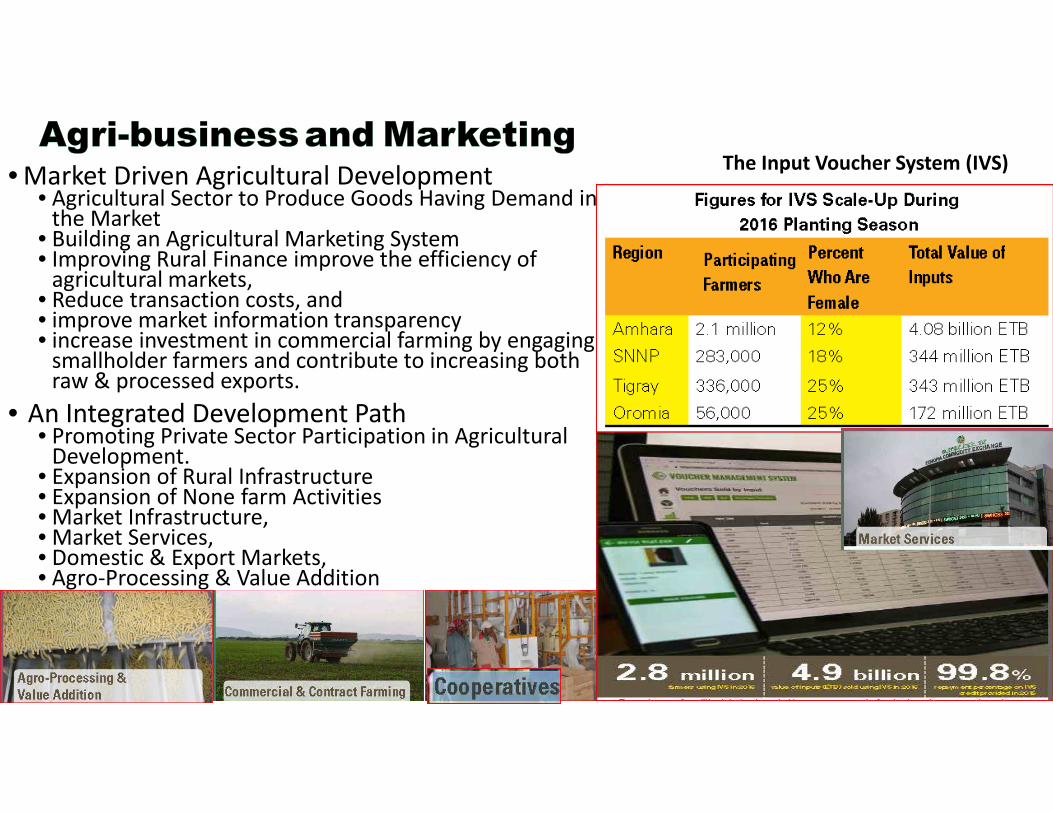

• Market Driven Agricultural Development • Agricultural Sector to Produce Goods Having Demand in

the Market • Building an Agricultural Marketing System• Improving Rural Finance improve the efficiency of

agricultural markets, • Reduce transaction costs, and• improve market information transparency• increase investment in commercial farming by engaging

smallholder farmers and contribute to increasing both raw & processed exports.

• An Integrated Development Path• Promoting Private Sector Participation in Agricultural

Development. • Expansion of Rural Infrastructure• Expansion of None farm Activities • Market Infrastructure, • Market Services, • Domestic & Export Markets, • Agro-Processing & Value Addition

The Input Voucher System (IVS)

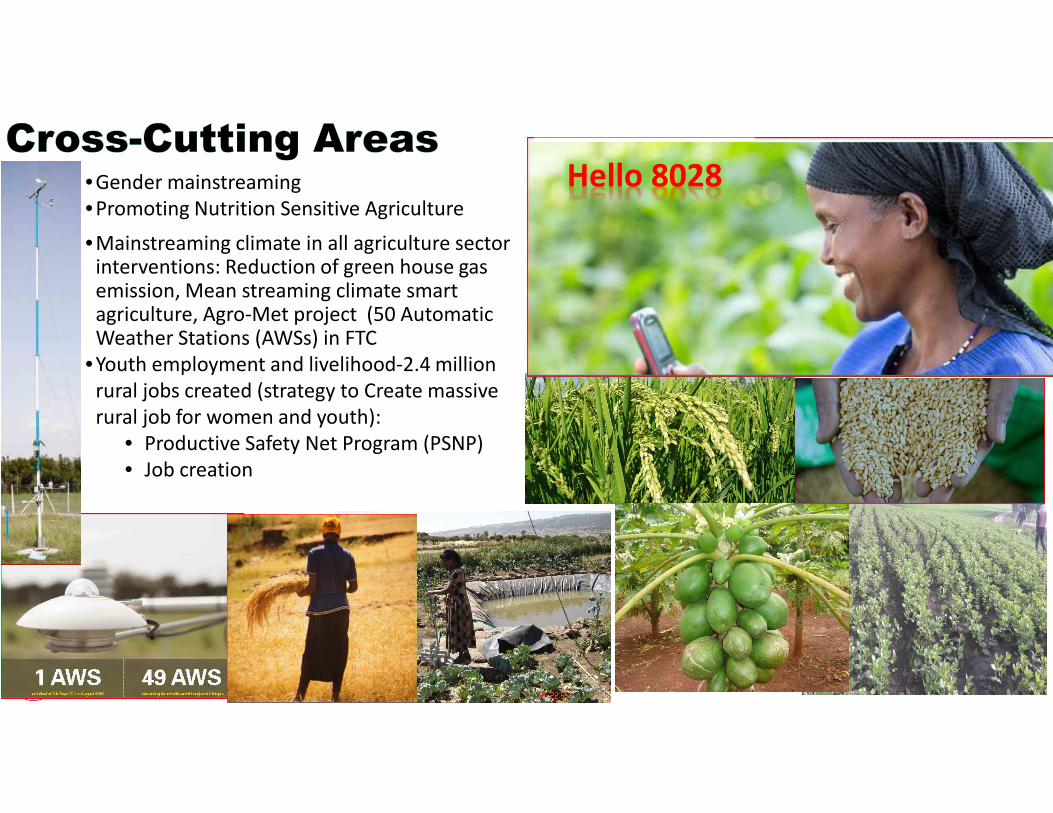

•Gender mainstreaming

•Promoting Nutrition Sensitive Agriculture

•Mainstreaming climate in all agriculture sector interventions: Reduction of green house gas emission, Mean streaming climate smart agriculture, Agro-Met project (50 Automatic Weather Stations (AWSs) in FTC

•Youth employment and livelihood-2.4 million

rural jobs created (strategy to Create massive

rural job for women and youth):

• Productive Safety Net Program (PSNP)

• Job creation

Hello 8028

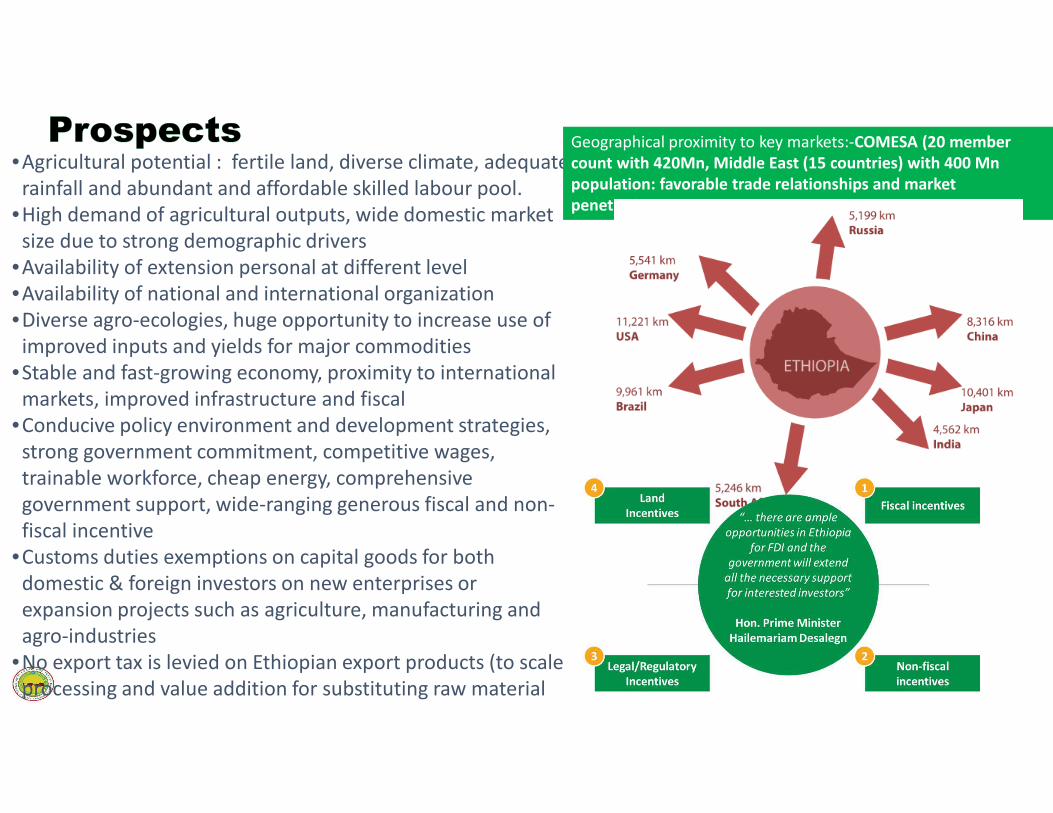

•Agricultural potential : fertile land, diverse climate, adequate

rainfall and abundant and affordable skilled labour pool.

•High demand of agricultural outputs, wide domestic market

size due to strong demographic drivers

•Availability of extension personal at different level

•Availability of national and international organization

•Diverse agro-ecologies, huge opportunity to increase use of

improved inputs and yields for major commodities

•Stable and fast-growing economy, proximity to international

markets, improved infrastructure and fiscal

•Conducive policy environment and development strategies,

strong government commitment, competitive wages,

trainable workforce, cheap energy, comprehensive

government support, wide-ranging generous fiscal and non-

fiscal incentive

•Customs duties exemptions on capital goods for both

domestic & foreign investors on new enterprises or

expansion projects such as agriculture, manufacturing and

agro-industries

•No export tax is levied on Ethiopian export products (to scale

processing and value addition for substituting raw material

and processed agricultural imports)

Geographical proximity to key markets:-COMESA (20 member

count with 420Mn, Middle East (15 countries) with 400 Mn

population: favorable trade relationships and market

penetration

FloricultureMedicinal

Fiber

Spices

Root crops

Oil crops

Coffee

Ethiopia is the center of origin and center of diversity for the following crops

Tef , Noug , Enset, Coffee , Wheat , Khat (chat), Highland kale

……Four Integrated Agro-Industrial Parks (IAIPs) operational and 17 under development

Priority to agro-food and allied sectors, IAIPs will have the state of the art infrastructure in roads, power, water,

communications, drainage, sewerage, sewage treatment plant, effluent treatment plant, storm water drains, rain water

harvesting, and firefighting facilities. Other specialized infrastructures such as cold storage units, quarantine facilities, quality control labs, quality certification centers, raw material storage, controlled and modified atmospheric

storage, central processing centers

• Implementation and Partnership capacity

• Human Resource Capacity: Knowledge, Skills, Attitude and Behavior

• Institutional/organizational Capacity: Structures, Systems & Org. arrangement

• Programs & Projects: AGP, PASDIP, SLMP,

• Collaborators/partners: ATA, CGIAR (IWMI, IFPRI), DAG, NGO’s,…

• Private/Public Sectors

• Affiliated Institutions: EIAR, FCA, Coffee & Tea Authority

• Platforms: RED & FS, CAADP,..

• COMESA, IGADIMF, World Bank, African Development Bank, USAID, Irish Aid, DFID,EU, SIDA, CIDA, DANIDA, WFP, UNDP, ….

BMGF

DANIDA

GACRNE

Irish Aid

NEPAD

AG

� Comprehensive implementation capacity building at all level

• Improving investment in agricultural sector with robust private sectors

participation

• Laying down strong M&E system, Market-Oriented extension system,

Improve capacity of Technology adaption; generation multiplication and

distribution

• Enhancing agro- skills: field prep., planting, IPM, harvesting, irrigation, skill

of farmers to use full extension package

• Ensuring quality assurance and traceability of export crops to enhance

competitiveness in the international markets

• Strengthen the input supply and distribution networks for major

commodities

• Promoting the agricultural mechanization leasing system

Together Changing Lives of Ethiopian Farmers and

Pastoralists!