1 Manufacturing Account. 2 Production Cost Production cost = Prime cost / Direct cost + Factory...

50

1 Manufacturing Account

-

Upload

terrence-nattress -

Category

Documents

-

view

248 -

download

1

Transcript of 1 Manufacturing Account. 2 Production Cost Production cost = Prime cost / Direct cost + Factory...

1

Manufacturing AccountManufacturing Account

2

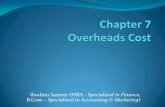

Production CostProduction Cost

Production cost = Prime cost / Direct cost + Factory overhead

expenses / Indirect cost

3

1. Direct materials • Costs of the materials used during the period.• Include the purchase price of the raw materials and

the acquisition costs related to the purchase.• Examples: Purchase of raw materials

Carriage inwards / freight charges on raw materials

4

2. Direct labour• Wages paid to the people who are directly involved

in the manufacturing process.• Example: Direct labour, Direct wages, Factory

wages, Production wages, Manufacturing wages

5

3. Direct expenses• They refer to the expenses paid according to each

unit of production.• Examples: Royalties

6

Factory Overhead Expenses / Indirect Costs Factory Overhead Expenses / Indirect Costs Cost incurred in the manufacturing process, but they ca

nnot be traced directly to the goods being produced. Include indirect materials, indirect labour and indirect ex

penses. Examples:

Indirect materials– Lubricants– Loose tools (opening balance + purchase – closing balan

ce)Indirect labour– wages, salaries, bonus or commission to cleaners, crane

drivers, foremen, supervisors and production managers.

7

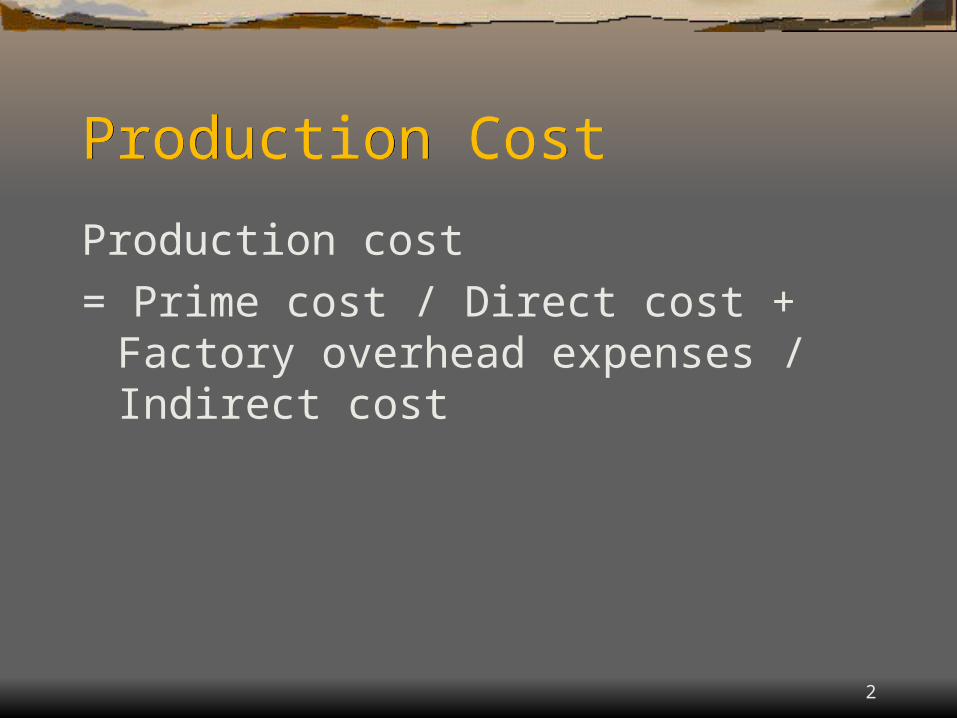

Indirect expenses related to the factory, machinery and vehicles

– Rent and rates– Depreciation– Insurance– Repairs and maintenance– Factory power / electricity– Internal transport– Loss on disposal

8

Work in Progress Work in Progress

It refers to the semi-finished goods, which should be included in the cost of goods manufactured.

9

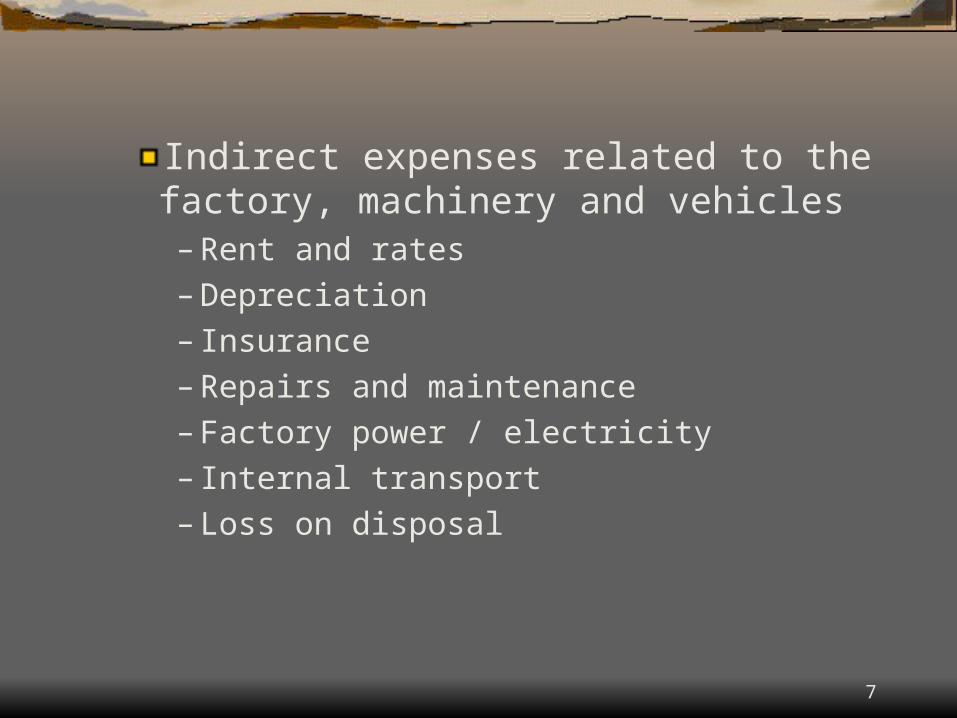

Manufacturing AccountManufacturing Account It shows the production cost or transfer price of

goods completed during the accounting period.1. Direct materials2. Direct labour3. Direct expenses4. Factory overhead expenses5. Work in progress6. Manufacturing profit / loss

10

Trading AccountTrading Account

This account shows the gross profit or loss resulted from the trading of manufactured and other purchased goods.

The account includes:SalesCost of goods sold– Manufactured goods – Other goods

11

Profit and Loss AccountProfit and Loss Account

Profit or loss of the whole business during the accounting period.

Includes all the expenses and income related to the office and the running of the whole business such as:

Gross profit / loss from the trading accountManufacturing profit / loss

12

Administration expenses

Selling and distribution expenses

Financial expenses

Increase / decrease in the provision for unrealized profit

Net abnormal loss – cash misappropriated

– losses of raw materials

– losses of finished goods

13

Some expenses are related to both the manufacturing process and the administration of the office such as:

Rent and ratesElectricityInsuranceDepreciation on premisesMotor vehiclesMotor vehicles expenses

14

These expenses should be allocated to the factory and office and debited to the manufacturing account and the profit and loss account respectively.

The bases of allocation are usually given in the examination questions.

15

Format of Manufacturing, Trading and Profit and loss

account

Format of Manufacturing, Trading and Profit and loss

account

16

Manufacturing, Trading and Profit and Loss Accountfor the year ended 31 Dec XXXX

$ $Opening stock of Raw Materials XAdd: Purchases of Raw Materials X Carriage inwards XLess: Closing stock of Raw Materials (X)Cost of Raw Materials Consumed XDirect Labour XRoyalties XPrime Cost XFactory Overhead Expenses:

Loose Tools (opening bal. + purchases –closing bal.) XRent (e.g. 25%) XProduction Manager’s salaries XFactory Power XMaintenance of plant & Machinery X

Depreciation of Plant & Machinery X X X

Direct material

Direct labour

Direct Expenses

Overhead

17

Add: Opening Work in Progress XLess: Closing Work in Progress XProduction Cost of Goods Completed XFactory profit/(loss) XTransfer price of Goods Completed X

$ $

Sales XLess: Returns inwards (X) XLess: COGS

Opening stock of finished goods X Production cost/Transfer price of Gds completed X

Less: Returns outwards (X)Fire Loss (X)Less: Closing stock of finished goods (X) X

Gross Profit XAdd: Factory Profit XAdd: Discount Received X X

The goods are transferredto trading a/c at productioncost/ transfer price

18

$ $Less: Expenses

Carriage Outwards XRent (e.g. 75%) XDiscount allowed XAdministration Expenses XDistribution Expenses XSelling Expenses XDepreciation of Delivery Van XProvision for Unrealized Profit XFire Loss X X

Net Profit X

19

Production Cost Vs.

Transfer Priceof Goods Completed

Production Cost Vs.

Transfer Priceof Goods Completed

20

Stock of raw materials, work in progress and other finished goods are valued at cost.

However, the stock of manufactured goods can be valued at production cost or the transfer price of goods completed.

Provision of unrealized profit of on stock should be made if closing stock of manufactured goods is valued at transfer price.

Production cost Vs. Transfer priceProduction cost Vs. Transfer price

21

Provision of Unrealized ProfitProvision of Unrealized Profit

Be made on the closing stock valued at production cost plus a percentage of factory profit.

Provision for unrealized profit Mark up% 100%+ Mark up(%)

= Stock (at transfer price) x

22

Example 1Example 1

23

A company manufactures and sells it own products.It also purchases and sells other finished goods.

Production 100 units $1@ $100 Sales 80 units $2@ $160Closing stock 20 units $1@ $20Expenses for this period $50

Prepare manufacturing, trading and profit and lossaccount for the following 2 situations would beshown:

1. The factory output is transferred to the trading account at factory cost.

2. The factory output is transferred to the trading account at factory cost plus 20% factory profit, and the stock of manufactured goods is valued at transfer price.

24

1.

$ $

Production cost of Gd completed (100 units*$1) 100

Sales (80 units*$2) 160

Less: COGS

Production cost of Gd completed 100

Less: Closing stock(at cost) (20 units*$1) 20 80

Gross Profit 80

Less: Expenses

Expenses 50

30

Manufacturing, trading and profit and loss account (extract)

25

2.$ $

Production cost of Gd completed (100 units*$1) 100Add: Manufacturing profit (100*0.2) 20Transfer price of Gds completed 120Sales (80 units*$2) 160Less: Cost of goods sold Transfer price of Gd completed 120Less: Closing stock(at transfer price) (20+20*0.2) 24 96Gross Profit 64Add: Manufacturing profit 20

84Less: Expenses Expenses 50 Provision for unrealized profit (24*20/120) 4 54Net Profit 30

Cost + profit

26

Increase in Provision Decrease in Provision

Dr Profit and LossCr Provision for Unrealized Profit

Dr Provision for Unrealized ProfitCr Profit and Loss

Accounting entries

Increase/ Decreased in Provision of Unrealized Profit

Increase/ Decreased in Provision of Unrealized Profit

27

Example 2Example 2

28

Goods manufactured are to be transferred to sales department at factory cost plus 20%.

1994 1995 1996 $ $ $

Stock at 1 Jan (at transfer price) - 2,400 3,600Stock at 31 Dec (at transfer price)2,400 3,600 3,000

Prepare the provision for unrealized profit account, profitand loss account and balance sheet respectively for thethree years

29

Provision for unrealized profit1994 $ 1994 $Dec 31 Bal c/d (2400*20/120) 400 Dec 31 P/L 400

Profit and Loss account (extract)

94 $ $

Gross Profit X

Less: Expenses

Increase in provision for unrealized profit

400

30

Provision for unrealized profit1994 $ 1994 $Dec 31 Bal c/d (2400*20/120) 400 Dec 31 P/L 400

1995 1995Dec 31 Bal c/d (3600*20/120) 600

Jan 1 Bal b/d 400Dec 31 P/L 200

600 600Profit and Loss account (extract)

94 $ $

Gross Profit X X

Less: Expenses

Increase in provision for unrealized profit

95 $ $

400 200

31

Provision for unrealized profit1994 $ 1994 $Dec 31 Bal c/d (2400*20/120) 400 Dec 31 P/L 400

1995 1995Dec 31 Bal c/d (3600*20/120) 600

Jan 1 Bal b/d 400Dec 31 P/L 200

1996 1996

600 600

Jan 1 bal b/d 600

Dec 31 Bal c/d (3000*20/120) 500

Dec 31 P/L 100

600 600

32

Profit and Loss account (extract)

94 $ $

Gross Profit X X XAdd: Decrease in provision for unrealized profit 100

Less: Expenses

Increase in provision for unrealized profit

95 $ $

96 $ $

400 200

33

Stock LossStock Loss

34

Stock LossStock Loss

i. Normal loss• Normal losses refer to losses related to the

ordinary activities of the business/• Examples: damaged / spoiled stock, obsolete

stock• No entry is required for normal loss

35

ii. Abnormal loss• Abnormal losses refer to losses not related to the

ordinary activities of the business.• Examples: fire loss, burglary loss

36

Loss of raw materials without an insurance claim

Dr Profit and LossCr Manufacturing

With the total loss

Loss of finished goods without an insurance claim

Dr Profit and LossCr Trading

With the total loss

Accounting entries

37

Loss of raw materials with an insurance claimDr Bank/Insurance CompanyDr Profit and LossCr Manufacturing

With the insurance claimWith the net lossWith the total loss

Loss of finished goods with an insurance claimDr Bank/Insurance CompanyDr Profit and LossCr Trading

With the insurance claimWith the net lossWith the total loss

38

Cheung Kong Enterprises

Manufacturing, Trading and Profit and Loss Account for the year ended 30 April 2004

Cost of raw materials consumed

Opening stock 160,000

Purchase 1,640,000

1,800,000

Closing stock 200,000 1,600,000

Manufacturing wages 800,000

Prime cost 2,400,000

39

Prime cost 2,400,000

Factory overheads

Manufacturing expenses 416,000

Depreciation 192,000 608,000

3,008,000

Opening work in progress 126,000

3,134,000

Closing work in progress 120,000

Cost of goods completed 3,014,000

40

41

42

43

44

45

46

47

48

49

50

Depreciation Total 2,400,000 x 10% = 240,000

Manufacturing 80% = 192,000

Administration 10% = 24,000

Selling and distribution 10% = 24,000