RIMS Session RIF 010 Wednesday, April 30, 2014 2:00 p.m. to 3:00 p.m .

Upload

izaiah-butlerCategory

view

218download

0

11

Joint Meeting With TheJoint Meeting With TheSchool Board & Audit CommitteeSchool Board & Audit Committee

October 31, 2007October 31, 2007

Wednesday, 5:00 – 6:00 p.m.Wednesday, 5:00 – 6:00 p.m.

22

Audit DepartmentAudit DepartmentOrganization ChartOrganization Chart

33

StaffingStaffing

9 Professional, 1 Administrative, 1 Vacancy9 Professional, 1 Administrative, 1 Vacancy

CollectivelyCollectively 9 Advanced Degrees9 Advanced Degrees 9 Professional Certificates – CPA, CIA, CISA, 9 Professional Certificates – CPA, CIA, CISA,

and CMAand CMA Over 150 Years of Auditing & Accounting Over 150 Years of Auditing & Accounting

ExperienceExperience

44

Audit Activities During 2006-2007Audit Activities During 2006-2007

A.A. Internal Funds AuditsInternal Funds Audits

B.B. Performance AuditsPerformance Audits

C.C. Special RequestsSpecial Requests

D.D. Charter School AuditsCharter School Audits

55

Results of 2006 AuditsResults of 2006 AuditsMiddle and Elementary SchoolsMiddle and Elementary Schools

Comparing to 2004 findingsComparing to 2004 findings

Areas with noticeable improvementsAreas with noticeable improvements

Areas that need improvementAreas that need improvement

Areas that need special attentionAreas that need special attention

66

Internal Funds AuditInternal Funds Audit2006 Findings Compared to 2004 Findings2006 Findings Compared to 2004 Findings

Middle and Elementary SchoolsMiddle and Elementary Schools

Areas with Noticeable ImprovementAreas with Noticeable Improvement::

Accounting record keeping (Accounting record keeping ( by 13 by 13)) Timekeeping for payroll (Timekeeping for payroll ( by 15 by 15)) Timecards not signed by employees (Timecards not signed by employees ( by 16 by 16)) Program deficit / high staffing (Program deficit / high staffing ( by 14 by 14)) Access to drop safe (Access to drop safe ( by 14 by 14))

Finding Summary (a)

77

Internal Funds AuditInternal Funds AuditAnalysis of 2006 FindingsAnalysis of 2006 Findings

Areas With ImprovementsAreas With Improvements::

Registration form (Registration form ( by 11) by 11) Lease prequalification (Lease prequalification ( by 10) by 10) Adjustment to records (Adjustment to records ( by 12) by 12)

88

Internal Funds AuditInternal Funds AuditAnalysis of 2006 FindingsAnalysis of 2006 Findings

Areas That Need ImprovementAreas That Need Improvement::

SACC students released without sign-out (SACC students released without sign-out ( by 20 by 20)) SACC students released to unauthorized person (SACC students released to unauthorized person ( by 32 by 32)) Timecard not signed by supervisor (Timecard not signed by supervisor ( by 21 by 21)) Inadequate support for disbursement (Inadequate support for disbursement ( by 47 by 47)) Lease agreement not adequately maintained (Lease agreement not adequately maintained ( by 28 by 28)) Lease – inadequate proof of insurance (Lease – inadequate proof of insurance ( by 19 by 19)) Lease – fees collected after use of facilities (Lease – fees collected after use of facilities ( by 27 by 27)) Lease – undercharged rentals (Lease – undercharged rentals ( by12 by12))

99

Internal Funds AuditInternal Funds AuditAnalysis of 2006 FindingsAnalysis of 2006 Findings

Areas That Need Special AttentionAreas That Need Special Attention::

# # Inadequate support for disbursementInadequate support for disbursement 6868 Students released to unauthorized personStudents released to unauthorized person 4848 Inadequate proof of insurance for facilities leasingInadequate proof of insurance for facilities leasing 4747 Fundraisers not adequately documentedFundraisers not adequately documented 4040 Students released without parent sign-outStudents released without parent sign-out 3838 Lease agreement not adequately maintainedLease agreement not adequately maintained 3838 Timecard not signed by supervisorTimecard not signed by supervisor 3030

309 (51% of total)309 (51% of total)

1010

New Areas of FocusNew Areas of FocusSince 2004Since 2004

ReceiptsReceipts Verify prepared deposits in schools’ drop safe & Verify prepared deposits in schools’ drop safe &

surprise check of monies collectedsurprise check of monies collected More in-depth review & verification of monies More in-depth review & verification of monies

collection records & revenues sourcescollection records & revenues sources Request financial records from banks, reconcile Request financial records from banks, reconcile

schools’ monies collection with deposit recordsschools’ monies collection with deposit records

DisbursementsDisbursements Ascertain the appropriateness of expenditures Ascertain the appropriateness of expenditures

for selected accountsfor selected accounts

Findings Summary (b)

1111

New Areas of FocusNew Areas of FocusSince 2004Since 2004

SACC ProgramSACC Program Examine SACC student records & student Examine SACC student records & student

release/dismissal proceduresrelease/dismissal procedures Reconcile SACC revenues with student Reconcile SACC revenues with student

registration & attendance recordsregistration & attendance records Test SACC payrollTest SACC payroll

Community School ProgramCommunity School Program Reconcile Community School revenues with Reconcile Community School revenues with

student registration and attendance recordsstudent registration and attendance records Test Community School payrollTest Community School payroll

1212

New Areas of FocusNew Areas of FocusSince 2004Since 2004

Leasing of School FacilitiesLeasing of School Facilities More in-depth review of leasing operations More in-depth review of leasing operations

& determine:& determine: Adequacy of documentationAdequacy of documentation Adequacy of insurance coverageAdequacy of insurance coverage Leasing revenuesLeasing revenues

1313

Principals’ Priority Principals’ Priority In Significant FindingsIn Significant Findings

Findings Summary (c)

1414

Implementation ofImplementation ofNew Rules & ProceduresNew Rules & Procedures

To Improve Controls and AccountabilityTo Improve Controls and Accountability

Sponsors retain the yellow copy of the MCR in order to Sponsors retain the yellow copy of the MCR in order to match the deposit records on match the deposit records on Official ReceiptsOfficial Receipts prepared prepared by bookkeeperby bookkeeper

Remitters record monies put in the drop safe on the new Remitters record monies put in the drop safe on the new “Drop Safe Log”“Drop Safe Log”

Incoming mails be received and opened by staff other Incoming mails be received and opened by staff other than the bookkeeper. MCR for monies received in the than the bookkeeper. MCR for monies received in the mail be prepared by mail opener and submitted to mail be prepared by mail opener and submitted to bookkeeper for depositbookkeeper for deposit

1515

Special Requests/InvestigationsSpecial Requests/InvestigationsDuring 2006-2007During 2006-2007

12 Special Requests/Investigations12 Special Requests/Investigations

InvolvedInvolved 5 High Schools5 High Schools 2 Middle Schools2 Middle Schools 5 Elementary Schools5 Elementary Schools

Most of them were related to financial mattersMost of them were related to financial matters

Results were referred to School Police / Results were referred to School Police / Employee Relations for further investigationEmployee Relations for further investigation

1616

Special Requests/InvestigationsSpecial Requests/InvestigationsDuring 2006-2007During 2006-2007

Results (as of October 24, 2007)Results (as of October 24, 2007)

Some involve multiple employeesSome involve multiple employees

2 Ongoing Investigation2 Ongoing Investigation 3 Reprimands3 Reprimands 5 Employees Resigned5 Employees Resigned 3 With Papers Referred to State Attorney3 With Papers Referred to State Attorney 1 Unfounded1 Unfounded 1 Results in Development & Implementation of New 1 Results in Development & Implementation of New

ProceduresProcedures

1717

Possible Impacts for AuditsPossible Impacts for Audits

Value added to our existing management Value added to our existing management controls and accountabilitiescontrols and accountabilities

Value added to the integrity of our systemValue added to the integrity of our system

Strengthening the control systemStrengthening the control system

1818

Possible Impacts for AuditsPossible Impacts for Audits

Ultimate results:Ultimate results: Protect our studentsProtect our students Protect school administratorsProtect school administrators Safeguard assets and ensure compliance with laws, Safeguard assets and ensure compliance with laws,

School Board Policies & guidelinesSchool Board Policies & guidelines Better controls resulting in increase in revenuesBetter controls resulting in increase in revenues Better control in operating expensesBetter control in operating expenses Provide deterrent for potential abuse of the systemProvide deterrent for potential abuse of the system Promote public confidence in the school system Promote public confidence in the school system

through public transparency, professional through public transparency, professional independence, & objective reportingindependence, & objective reporting

1919

Internal Funds Revenues AnalysisInternal Funds Revenues Analysis

Constant $ adjusted for inflation; 1996 base year.Constant $ adjusted for inflation; 1996 base year.Source: Annual Internal Funds Audit Reports and Manatee Accounting System.Source: Annual Internal Funds Audit Reports and Manatee Accounting System.

Total Receipts During 1996 - 2007Current and Constant Dollars

$30 M

$40 M

$50 M

$60 M

$70 M

$80 M

Current $ $35 M $38 M $43 M $47 M $48 M $51 M $51 M $55 M $59 M $60 M $68 M $74 M

CPI-Adjusted $ $35 M $37 M $41 M $44 M $44 M $45 M $44 M $47 M $49 M $49 M $53 M $56 M

# of Schools 129 131 136 136 138 145 149 156 160 162 165 167

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

2020

Internal Funds Revenues AnalysisInternal Funds Revenues Analysis

Constant $ adjusted for inflation; 1996 base year.Constant $ adjusted for inflation; 1996 base year.Source: Annual Internal Funds Audit Reports, Manatee Accounting System, & Budget Executive Summary Reports.Source: Annual Internal Funds Audit Reports, Manatee Accounting System, & Budget Executive Summary Reports.

Average Receipts Per Student During 1996 - 2007Current and Constant Dollars

$200

$250

$300

$350

$400

$450

$500

Current $ $271 $279 $312 $327 $326 $339 $327 $339 $349 $350 $393 $438

CPI-Adjusted $ $271 $271 $296 $306 $298 $300 $281 $287 $289 $282 $307 $331

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

2121

Internal Funds Revenues AnalysisInternal Funds Revenues Analysis

Source: Annual Internal Funds Audit Reports and Manatee Accounting System.Source: Annual Internal Funds Audit Reports and Manatee Accounting System.

Average Receipts Per SchoolDuring 2004 - 2007

$-

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

Elementary Middle High Others All Schools

2004 2005 2006 2007

2222

Internal Funds Revenues AnalysisInternal Funds Revenues Analysis

Source: Annual Internal Funds Audit Reports and Manatee Accounting System.Source: Annual Internal Funds Audit Reports and Manatee Accounting System.

Average Receipts Per School During 2004 – 2007

2004 2005 2006 2007 Elementary $ 323,029 $ 329,846 $357,676 $ 398,281 Middle $ 279,748 $ 243,004 $270,395 $ 280,762 High $ 850,713 $ 851,390 $944,067 $1,021,104 Others $ 119,434 $ 81,485 $ 81,940 $ 74,421 All Schools $ 366,146 $ 373,324 $412,461 $ 446,026

2323

SACC & Summer CampSACC & Summer CampRevenues AnalysisRevenues Analysis

Constant $ adjusted for fee increases and student enrollment; 2004 base year.Constant $ adjusted for fee increases and student enrollment; 2004 base year.Source: Manatee Accounting System and SACC Fee Schedules.Source: Manatee Accounting System and SACC Fee Schedules.

Total Revenues During 2004 - 2007Current and Constant Dollars

$15.0M

$17.0M

$19.0M

$21.0M

$23.0M

Current $ $16.6M $17.0M $18.5M $20.8M

Adjusted $ $16.6M $16.9M $17.8M $18.7M

2004 2005 2006 2007

2424

SACC & Summer CampSACC & Summer CampRevenues AnalysisRevenues Analysis

Source: TERMS System.Source: TERMS System.

Deficit in SACC

($254K)

($124K)

($65K)

22 Schools 13 Schools 8 Schools

($300K)

($250K)

($200K)

($150K)

($100K)

($50K)

0

50

2004 2005 2006

Total Deficits # of Schools with Deficits

2525

SACC & Summer CampSACC & Summer CampRevenues AnalysisRevenues Analysis

Source: Manatee Accounting System and SACC Fee Schedules.Source: Manatee Accounting System and SACC Fee Schedules.

Revenues Increase From Prior Year & Culmulative $

$0.4M

$1.5M

$2.3M

$0.4M

$1.9M

$4.3M

$0.4M

$2.4M

$6.2M

$0.0M

$1.0M

$2.0M

$3.0M

$4.0M

$5.0M

$6.0M

$7.0M

2005 2006 2007

Increase From Prior Year Increase From 2004 Culmulative Increase Since 2004

2626

SACC & Summer CampSACC & Summer CampRevenues AnalysisRevenues Analysis

Constant $ adjusted for fee increases and student enrollment; 2004 base year.Constant $ adjusted for fee increases and student enrollment; 2004 base year.Source: Manatee Accounting System and SACC Fee Schedule.Source: Manatee Accounting System and SACC Fee Schedule.

Revenues Increase From Prior Year & Culmulative $(Adjusted for Fee Increases & Student Enrollment: 2004 Base Year)

$0.3M

$0.9M $0.9M

$0.3M

$1.2M

$2.2M

$0.3M

$1.6M

$3.4M

$0.0M

$1.0M

$2.0M

$3.0M

$4.0M

2005 2006 2007

Increase From Prior Year Increase From 2004 Culmulative Increase Since 2004

2727

Leasing Revenues AnalysisLeasing Revenues Analysis

Constant $ adjusted for fee increases; 2004 base year.Constant $ adjusted for fee increases; 2004 base year.Source: Manatee Accounting System and Leasing Rate Schedules.Source: Manatee Accounting System and Leasing Rate Schedules.

Total Leasing Revenues During 2004 - 2007

$1.0M

$1.5M

$2.0M

$2.5M

$3.0M

$3.5M

$4.0M

Current $ $1.8M $2.0M $2.7M $3.2M

Adjusted $ $1.8M $2.0M $2.2M $2.6M

# of Schools 161 163 165 167

2004 2005 2006 2007

2828

Leasing Revenues AnalysisLeasing Revenues Analysis

Constant $ adjusted for fee increases; 2004 base year.Constant $ adjusted for fee increases; 2004 base year.Source: Manatee Accounting System and Leasing Rate Schedules.Source: Manatee Accounting System and Leasing Rate Schedules.

Average Leasing Revenues Per SchoolDuring 2004 - 2007

$10.0K$12.0K$14.0K$16.0K$18.0K$20.0K

Current $ $10.9K $12.3K $16.5K $19.0K

Adjusted $ $10.9K $12.3K $13.3K $15.4K

# of Schools 161 163 165 167

2004 2005 2006 2007

2929

Leasing Revenues AnalysisLeasing Revenues Analysis

Source: Manatee Accounting System.Source: Manatee Accounting System.

Leasing Revenues Increase During 2005 - 2007

$257K

$709K$458K

$257K

$966K

$1,424K

$257K

$1,223K

$2,647K

$0K

$500K

$1,000K

$1,500K

$2,000K

$2,500K

$3,000K

2005 2006 2007

Increase From Prior Year Increase From 2004 Culmulative Increase Since 2004

3030

Leasing Revenues AnalysisLeasing Revenues Analysis

Constant $ adjusted for fee increases; 2004 base year.Constant $ adjusted for fee increases; 2004 base year.Source: Manatee Accounting System and Leasing Rate Schedules.Source: Manatee Accounting System and Leasing Rate Schedules.

Leasing Revenues Increase During 2005 - 2007(Adjusted for Rate Changes: 2004 Base Year)

$257K $191K$370K

$257K

$449K

$819K

$257K

$706K

$1,525K

$0K

$500K

$1,000K

$1,500K

$2,000K

2005 2006 2007

Increase From Prior Year Increase From 2004 Culmulative Increase Since 2004

3131

Other InvolvementsOther Involvements

1.1. Provide input for the Department of Accounting Provide input for the Department of Accounting Services, After School Programming, and Adult Services, After School Programming, and Adult & Community Education in developing and & Community Education in developing and implementing new guidelines to strengthen implementing new guidelines to strengthen controls for Internal Fundscontrols for Internal Funds

2.2. Present audit results to principal groups at Present audit results to principal groups at their regular meetings so that administrators their regular meetings so that administrators can keep updated re: most common control can keep updated re: most common control weaknesses and new audit approaches to help weaknesses and new audit approaches to help administrators prevent and detect improprieties administrators prevent and detect improprieties at their schoolsat their schools

3232

Performance AuditsPerformance Audits

1.1. Audit of Implementation of Corrective Audit of Implementation of Corrective Actions in Response to Auditor Actions in Response to Auditor General’s 2004 Audit of Student FTE General’s 2004 Audit of Student FTE (August 2006)(August 2006)

and and 2.2. Audit of Corrective Actions in Audit of Corrective Actions in

Response to Auditor’s General’s 2004 Response to Auditor’s General’s 2004 Audit of Student Transportation FTE Audit of Student Transportation FTE (August 2006)(August 2006)

3333

Performance AuditsPerformance AuditsAudits of Corrective Actions for FTE AuditsAudits of Corrective Actions for FTE Audits

The The Auditor General’s 2004 Student FTE AuditAuditor General’s 2004 Student FTE Audit of the of the School District was released in 2005, and revealed School District was released in 2005, and revealed certain weaknesses in documentation of our programs. certain weaknesses in documentation of our programs. That audit resulted in total negative adjustments of That audit resulted in total negative adjustments of $2,020,203 in FEFP funding. We lost $2,020,203 in that $2,020,203 in FEFP funding. We lost $2,020,203 in that year.year.

Based on a sample of 48 schools, instances of Based on a sample of 48 schools, instances of noncompliance found were related to six departments:noncompliance found were related to six departments:

Exceptional Student EducationExceptional Student Education School Choice and Choice ProgramsSchool Choice and Choice Programs Compensation and Human Resource PlanningCompensation and Human Resource Planning Multicultural EducationMulticultural Education TransportationTransportation

3434

Performance AuditsPerformance AuditsAudits of Corrective Actions for FTE AuditsAudits of Corrective Actions for FTE Audits

These findings were in the areas ofThese findings were in the areas of Student Records for ESEStudent Records for ESE Off-campus On-the-job Training (OJT) documentation, and Off-campus On-the-job Training (OJT) documentation, and Teacher Certification with regards to ESOL strategies Teacher Certification with regards to ESOL strategies

compliancecompliance

Audit Exceptions were found involving reporting errors, Audit Exceptions were found involving reporting errors, missing records, or records that were not properly and missing records, or records that were not properly and accurately prepared.accurately prepared.

The next FTE Audit will be performed for the records of 2006-The next FTE Audit will be performed for the records of 2006-07 School Year by The 07 School Year by The Auditor GeneralAuditor General during 2007-08. during 2007-08.

Our own follow-up audit identified similar areas we have to Our own follow-up audit identified similar areas we have to address, based on a sample of 11 schools.address, based on a sample of 11 schools.

3535

Performance AuditsPerformance Audits

Audits of Corrective Actions for FTE AuditsAudits of Corrective Actions for FTE Audits

District’s Corrective actions must be fully implemented in District’s Corrective actions must be fully implemented in all schools effective 2006-07 School Year.all schools effective 2006-07 School Year.

District staff were developing and implementing District staff were developing and implementing guidelines and procedures that all schools should to guidelines and procedures that all schools should to follow in order to address all issues. Eventually, the follow in order to address all issues. Eventually, the District’s goal is to eliminate the negative Funding District’s goal is to eliminate the negative Funding adjustment imposed by the State.adjustment imposed by the State.

3636

Performance AuditsPerformance Audits

3.3. Audit of Boca Raton Middle School Internal Audit of Boca Raton Middle School Internal Accounts (September 15, 2006)Accounts (September 15, 2006)

School staff became aware in June 2006, that Internal School staff became aware in June 2006, that Internal Accounts records were missing. All records and files Accounts records were missing. All records and files for disbursements and receipts from July 1, 2005, for disbursements and receipts from July 1, 2005, through February 28, 2006, could not be located. As through February 28, 2006, could not be located. As stated by the previous bookkeeper, who handled the stated by the previous bookkeeper, who handled the books during that time, the records had been boxed books during that time, the records had been boxed and moved to a specific storage area. However, and moved to a specific storage area. However, repeated searches of the specific area by school staff repeated searches of the specific area by school staff did not locate the records.did not locate the records.

3737

Performance AuditsPerformance Audits

4.4. Audit of Seminole Ridge High School Audit of Seminole Ridge High School Deposit Records (November 17, 2006)Deposit Records (November 17, 2006)

Audit uncovered $31,000+ stolen by the school bookkeeper. Audit uncovered $31,000+ stolen by the school bookkeeper. Findings were referred to School Police for further Findings were referred to School Police for further investigation.investigation.

Police later filed charges against the bookkeeper.Police later filed charges against the bookkeeper. The bookkeeper was arrested later.The bookkeeper was arrested later. With assistance provided by Accounting Services Department, With assistance provided by Accounting Services Department,

corrective actions were developed and implemented corrective actions were developed and implemented immediately. Remedial actions included:immediately. Remedial actions included:

Sponsors of fundraisers for future verification will maintain a copy Sponsors of fundraisers for future verification will maintain a copy of the of the Monies Collection ReportsMonies Collection Reports

Auditors will perform unannounced verification of monies in a Auditors will perform unannounced verification of monies in a drop-safedrop-safe

Use of log book for all deposits in the drop-safeUse of log book for all deposits in the drop-safe

3838

Performance AuditsPerformance Audits

5.5. Audit of Communications Department of Alexander Audit of Communications Department of Alexander W. Dreyfoos School of the Arts (November 17, W. Dreyfoos School of the Arts (November 17, 2006)2006)

Several issues were brought up by the school principal, Several issues were brought up by the school principal, including the balance of the Year Book Account, donation including the balance of the Year Book Account, donation form the School of Arts Foundation, forging of signature form the School of Arts Foundation, forging of signature on Check Requisition, and receipt of a laptop as gift from on Check Requisition, and receipt of a laptop as gift from parents.parents.

The Year Book Account related issue was resolved. The Year Book Account related issue was resolved. Causes of the problems were due to inclusion of Causes of the problems were due to inclusion of unrelated expenditures in the Year Book Account.unrelated expenditures in the Year Book Account.

Regarding donation from the School of Arts Foundation, Regarding donation from the School of Arts Foundation, the audit revealed that the proceeds were not spent the audit revealed that the proceeds were not spent inappropriately.inappropriately.

3939

Performance AuditsPerformance Audits6.6. Audit of Boynton Beach Community High Audit of Boynton Beach Community High

School (January 19, 2007)School (January 19, 2007)

$101,884 overpayments in payroll – There were $101,884 overpayments in payroll – There were widespread inconsistencies and unaccountable widespread inconsistencies and unaccountable overpayments to staff.overpayments to staff.

Questionable pay widespread – The Community Questionable pay widespread – The Community School secretary input hours into the payroll system School secretary input hours into the payroll system for staff without proof of hours worked and supervisor for staff without proof of hours worked and supervisor approval for time and hours.approval for time and hours.

4040

Performance AuditsPerformance Audits6.6. Audit of Boynton Beach Community High Audit of Boynton Beach Community High

School (January 19, 2007)School (January 19, 2007)

Irregularities widespread in leases school facility. The Irregularities widespread in leases school facility. The audit identified repeated irregularities and audit identified repeated irregularities and noncompliance by staff in handing leases. Of the 81 noncompliance by staff in handing leases. Of the 81 executed leases,executed leases,

Lessees underpaid $12,726 for their 29 leases because non-Lessees underpaid $12,726 for their 29 leases because non-profit rates were applied; utility charges were waived; leases profit rates were applied; utility charges were waived; leases were granted undocumented fee-waivers.were granted undocumented fee-waivers.

59 leases did not provide proof of adequate liability insurance.59 leases did not provide proof of adequate liability insurance. 42 were not signed by lessees.42 were not signed by lessees. Five did not have the approved Rental Prequalification.Five did not have the approved Rental Prequalification. 35 had not made the full payment before the use of facilities, 35 had not made the full payment before the use of facilities,

as required by District guidelines.as required by District guidelines.

4141

Performance AuditsPerformance Audits6.6. Audit of Boynton Beach Community High Audit of Boynton Beach Community High

School (January 19, 2007)School (January 19, 2007)

Disbursements Not Properly DocumentedDisbursements Not Properly Documented

Change Fund Not Properly SecuredChange Fund Not Properly Secured

Access to School’s Drop SafeAccess to School’s Drop Safe

Prenumbered Document CustodianPrenumbered Document Custodian

4242

Performance AuditsPerformance Audits

7.7. Audit of Contract Compliance, WHLS of Florida, Inc. Audit of Contract Compliance, WHLS of Florida, Inc. for Fiscal Year 2006 (January 19, 2007)for Fiscal Year 2006 (January 19, 2007)

The audit concluded that:The audit concluded that:

WHLS did not achieve the objective that the percent of WHLS did not achieve the objective that the percent of WHLS students making learning gains in reading and WHLS students making learning gains in reading and math will be significantly higher than the learning gains of math will be significantly higher than the learning gains of students at other District alternative education sites.students at other District alternative education sites.

WHLS did not achieve objective that 100% of WHLS WHLS did not achieve objective that 100% of WHLS students will earn a minimum of four credits in FY 2006.students will earn a minimum of four credits in FY 2006.

The other 3 objectives were achieved: regarding students’ The other 3 objectives were achieved: regarding students’ absences; dropout rate, and percent of seniors receiving absences; dropout rate, and percent of seniors receiving employment.employment.

4343

Performance AuditsPerformance Audits

8.8. Audit of Royal Palm Beach High School Audit of Royal Palm Beach High School Cheerleading and ESE Field Trip Accounts Cheerleading and ESE Field Trip Accounts (April 13, 2007)(April 13, 2007)

The audit revealed that $12,795 in cheerleading The audit revealed that $12,795 in cheerleading program monies were unaccounted for; and $2,128 program monies were unaccounted for; and $2,128 in ESE field trip monies was also unaccounted for.in ESE field trip monies was also unaccounted for.

The Cheerleading sponsor resigned from the District The Cheerleading sponsor resigned from the District and discipline was issued to the ESE teacher.and discipline was issued to the ESE teacher.

4444

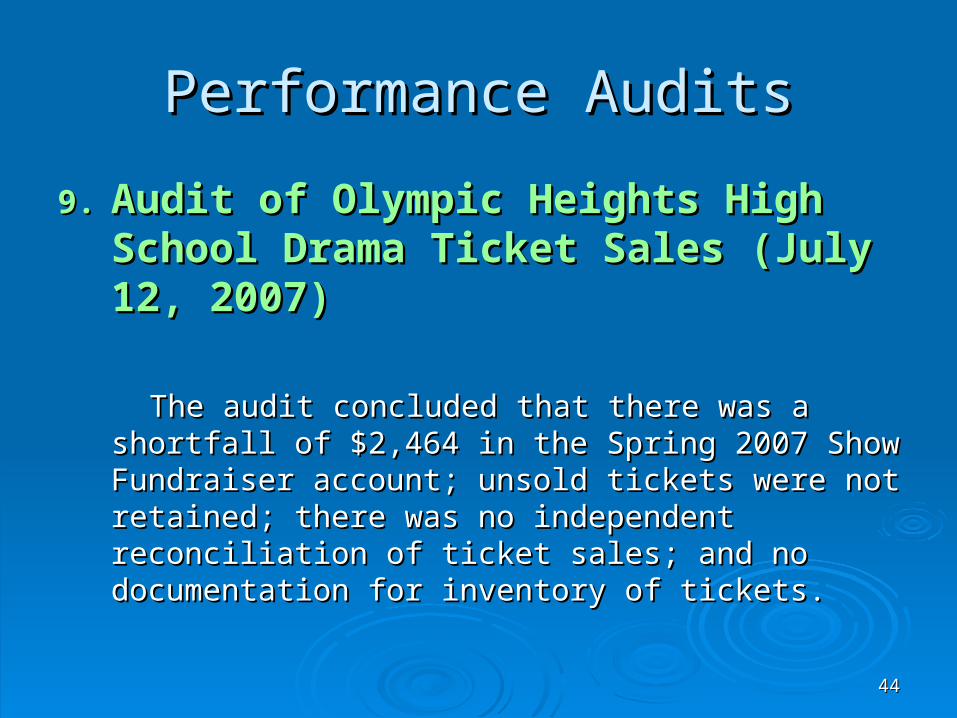

Performance AuditsPerformance Audits

9.9. Audit of Olympic Heights High School Audit of Olympic Heights High School Drama Ticket Sales (July 12, 2007)Drama Ticket Sales (July 12, 2007)

The audit concluded that there was a shortfall of $2,464 The audit concluded that there was a shortfall of $2,464 in the Spring 2007 Show Fundraiser account; unsold in the Spring 2007 Show Fundraiser account; unsold tickets were not retained; there was no independent tickets were not retained; there was no independent reconciliation of ticket sales; and no documentation for reconciliation of ticket sales; and no documentation for inventory of tickets.inventory of tickets.

4545

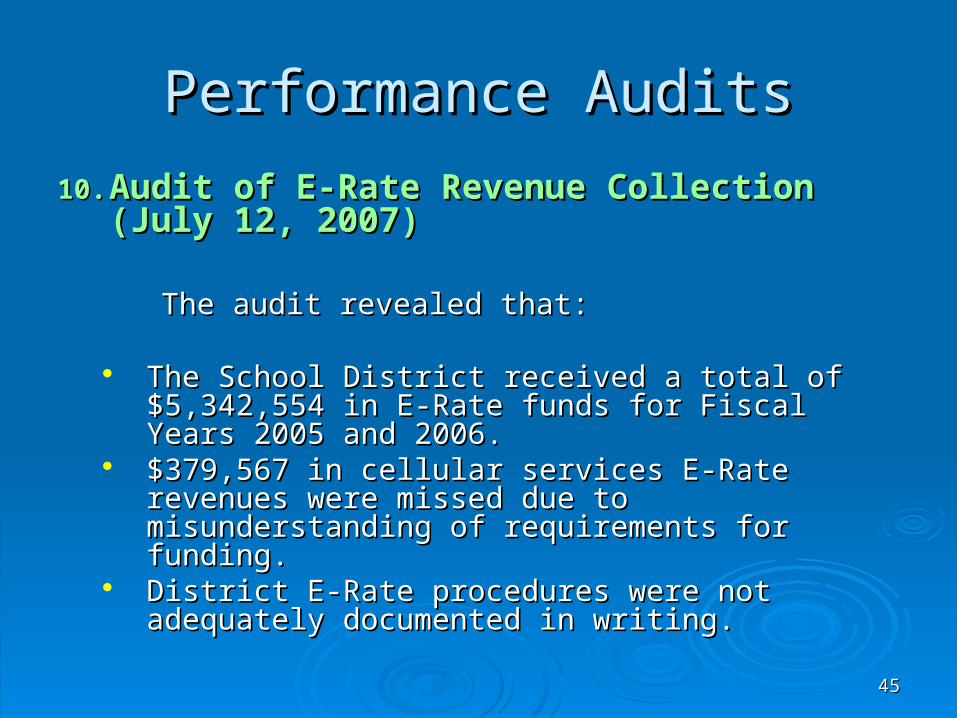

Performance AuditsPerformance Audits

10.10. Audit of E-Rate Revenue Collection (July 12, Audit of E-Rate Revenue Collection (July 12, 2007)2007)

The audit revealed that:The audit revealed that:

The School District received a total of $5,342,554 in The School District received a total of $5,342,554 in E-Rate funds for Fiscal Years 2005 and 2006.E-Rate funds for Fiscal Years 2005 and 2006.

$379,567 in cellular services E-Rate revenues were $379,567 in cellular services E-Rate revenues were missed due to misunderstanding of requirements for missed due to misunderstanding of requirements for funding.funding.

District E-Rate procedures were not adequately District E-Rate procedures were not adequately documented in writing.documented in writing.

4646

Performance AuditsPerformance Audits

11.11. Audit of Palm Bach Central High School’s Audit of Palm Bach Central High School’s Facilities Leasing (July 12, 2007)Facilities Leasing (July 12, 2007)

During School Year 2006, the school administered 91 During School Year 2006, the school administered 91 Lease Agreements and collected a total of $184,290 in Lease Agreements and collected a total of $184,290 in leasing revenues. The audit revealed widespread of leasing revenues. The audit revealed widespread of irregularities. Specifically,irregularities. Specifically,

Sixty leases (66%) did not have the required prequalification.Sixty leases (66%) did not have the required prequalification. Thirty-two leases (35%) did not have proof of adequate liability Thirty-two leases (35%) did not have proof of adequate liability

insurance.insurance. All 91 Lease Agreements were not properly executed.All 91 Lease Agreements were not properly executed. None of the Lease Agreements were signed by Principal.None of the Lease Agreements were signed by Principal.

4747

Performance AuditsPerformance Audits

11.11. Audit of Palm Bach Central High School’s Audit of Palm Bach Central High School’s Facilities Leasing (July 12, 2007)Facilities Leasing (July 12, 2007)

Five leases were neither signed by the lessees nor a Five leases were neither signed by the lessees nor a school representative.school representative.

48 leases were not signed by the lessees.48 leases were not signed by the lessees. 81 leases were not signed by a witness as required by the 81 leases were not signed by a witness as required by the

lease document.lease document. School lost $97,223 in revenues due to undercharged School lost $97,223 in revenues due to undercharged

rentals. Leasing charges for 53 (58%) of the 91 leases rentals. Leasing charges for 53 (58%) of the 91 leases were below the District approved rate schedule, resulting were below the District approved rate schedule, resulting in a total loss of $82,464 in rental income during School in a total loss of $82,464 in rental income during School Year 2006.Year 2006.

4848

Performance AuditsPerformance Audits

11.11. Audit of Palm Bach Central High School’s Audit of Palm Bach Central High School’s Facilities Leasing (July 12, 2007)Facilities Leasing (July 12, 2007)

$14,759 in total rental charges were waived for $14,759 in total rental charges were waived for seven leases without obtaining the prequalification seven leases without obtaining the prequalification approval from the Real Estate Services Department.approval from the Real Estate Services Department.

Rental charges not timely collected.Rental charges not timely collected. Monies not timely deposited.Monies not timely deposited. Sales Tax not collected for Commercial Leases.Sales Tax not collected for Commercial Leases. Incorrect allocation for utility charges.Incorrect allocation for utility charges.

4949

Performance AuditsPerformance Audits

11.11. Audit of Palm Bach Central High School’s Audit of Palm Bach Central High School’s Facilities Leasing (July 12, 2007)Facilities Leasing (July 12, 2007)

Employee accepting payment from lessee. During Employee accepting payment from lessee. During August 2006, a lessee sent a $180 check to the August 2006, a lessee sent a $180 check to the school for payment of theater technician’s services. school for payment of theater technician’s services. However, the check was made payable to the However, the check was made payable to the technician instead of the school.technician instead of the school.

No supervisor review and approval was obtained No supervisor review and approval was obtained prior to inputting into the payroll system.prior to inputting into the payroll system.

Audit conclusions were referred to Police and Audit conclusions were referred to Police and Personnel for further investigations.Personnel for further investigations.

5050

Performance AuditsPerformance Audits

12.12. Audit of Vending Machines (September 14, Audit of Vending Machines (September 14, 2007)2007)

The audit concluded that:The audit concluded that:

Schools with full-service vending machines Schools with full-service vending machines appeared to be 3% to 30% more profitable than appeared to be 3% to 30% more profitable than those with self-service vending machines.those with self-service vending machines.

Schools with both services seemed to perform Schools with both services seemed to perform even better.even better.

5151

Performance AuditsPerformance Audits

12.12. Audit of Vending Machines (September 14, Audit of Vending Machines (September 14, 2007)2007)

As a result, the audit recommended that schools As a result, the audit recommended that schools consider using full-service vending machines. consider using full-service vending machines. Other advantages of having full-service machines Other advantages of having full-service machines include:include: Eliminating the risk of inventories loss or loss in cash Eliminating the risk of inventories loss or loss in cash

collections involved with self-service vending machinescollections involved with self-service vending machines Eliminating carrying cost for inventoriesEliminating carrying cost for inventories Reducing staff time associated with maintaining vending Reducing staff time associated with maintaining vending

machinesmachines

5252

Performance AuditsPerformance Audits

13.13. Audit of IT Security Enhancement & Control Audit of IT Security Enhancement & Control (September 14, 2007)(September 14, 2007)

In response to a hacking incident with the District In response to a hacking incident with the District Student records during 2004-05, the Department of Student records during 2004-05, the Department of Information Security (IT Security) took an initiative to Information Security (IT Security) took an initiative to strengthen the overall security infrastructure for the strengthen the overall security infrastructure for the District’s computing environment. As of June 2007, District’s computing environment. As of June 2007, various security enhancement procedures had been various security enhancement procedures had been developed and implemented.developed and implemented.

Overall, the security enhancements and procedures Overall, the security enhancements and procedures appeared sufficient, and should be able to detect and appeared sufficient, and should be able to detect and prevent unauthorized access to the District’s computer prevent unauthorized access to the District’s computer system.system.

5353

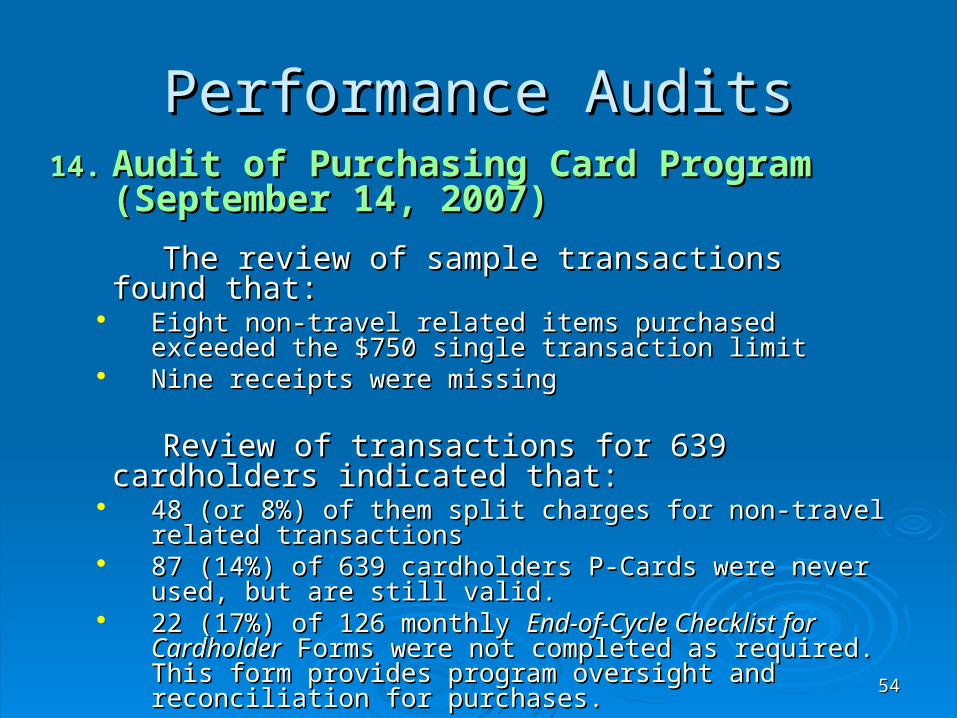

Performance AuditsPerformance Audits

14.14. Audit of Purchasing Card Program Audit of Purchasing Card Program (September 14, 2007)(September 14, 2007)

The primary objectives of this audit were to determine The primary objectives of this audit were to determine if: (1) transactions exceeded the allowed limits, (2) if: (1) transactions exceeded the allowed limits, (2) transactions were split in order to circumvent the transactions were split in order to circumvent the transaction limit, (3) P-Card transactions complied with transaction limit, (3) P-Card transactions complied with related policies and guidelines, and (4) appropriate related policies and guidelines, and (4) appropriate oversight and reconciliation of purchases were in place oversight and reconciliation of purchases were in place to detect and deter improper transactions.to detect and deter improper transactions.

5454

Performance AuditsPerformance Audits14.14. Audit of Purchasing Card Program Audit of Purchasing Card Program

(September 14, 2007)(September 14, 2007)

The review of sample transactions found that:The review of sample transactions found that: Eight non-travel related items purchased exceeded the $750 Eight non-travel related items purchased exceeded the $750

single transaction limitsingle transaction limit Nine receipts were missingNine receipts were missing

Review of transactions for 639 cardholders indicated Review of transactions for 639 cardholders indicated that:that:

48 (or 8%) of them split charges for non-travel related 48 (or 8%) of them split charges for non-travel related transactionstransactions

87 (14%) of 639 cardholders P-Cards were never used, but 87 (14%) of 639 cardholders P-Cards were never used, but are still valid.are still valid.

22 (17%) of 126 monthly 22 (17%) of 126 monthly End-of-Cycle Checklist for End-of-Cycle Checklist for CardholderCardholder Forms were not completed as required. This form Forms were not completed as required. This form provides program oversight and reconciliation for purchases.provides program oversight and reconciliation for purchases.

5555

Performance AuditsPerformance Audits15.15. Audit of Corrective Actions for Leasing of Audit of Corrective Actions for Leasing of

School Facilities (October 12, 2007)School Facilities (October 12, 2007)

The The 2004 and 2005 Annual Audits of School Internal 2004 and 2005 Annual Audits of School Internal FundsFunds revealed widespread inconsistencies and non- revealed widespread inconsistencies and non-compliance in leasing of school facilities; specifically, compliance in leasing of school facilities; specifically, lease and timelines in collection of rentals. The lease and timelines in collection of rentals. The primary objective of this audit was to assess the primary objective of this audit was to assess the sufficiency of corrective actions implemented by the sufficiency of corrective actions implemented by the Department of Real Estate Services.Department of Real Estate Services.

Noncompliance Continued – The audit selected nine Noncompliance Continued – The audit selected nine sample schools for site review, and revealed sample schools for site review, and revealed repeated noncompliance with leasing procedures repeated noncompliance with leasing procedures identified in 2004 and 2005 Internal Funds Audits.identified in 2004 and 2005 Internal Funds Audits.

5656

Performance AuditsPerformance Audits

15.15. Audit of Corrective Actions for Leasing of Audit of Corrective Actions for Leasing of School Facilities (October 12, 2007)School Facilities (October 12, 2007)

Some Staff did not Receive Training – Leasing Some Staff did not Receive Training – Leasing coordinators from middle schools and high schools coordinators from middle schools and high schools without community school program do not receive without community school program do not receive training.training.

Prequalification Request Should Include Supporting Prequalification Request Should Include Supporting Documentation – Neither proof of insurance nor Documentation – Neither proof of insurance nor proof of non-profit status was required to be proof of non-profit status was required to be submitted to Real Estate for the prequalification submitted to Real Estate for the prequalification process. As a result, there was no assurance that process. As a result, there was no assurance that prequalification and fee-waiver were approved prequalification and fee-waiver were approved accordingly.accordingly.

5757

Performance AuditsPerformance Audits15.15. Audit of Corrective Actions for Leasing of Audit of Corrective Actions for Leasing of

School Facilities (October 12, 2007)School Facilities (October 12, 2007)

Standardization at Schools NeededStandardization at Schools Needed

Inconsistent Policies, Procedures, and Documents – Inconsistent Policies, Procedures, and Documents – Currently, there are nine sources of rules and Currently, there are nine sources of rules and regulations governing community use of school regulations governing community use of school facilities. Each school also has its own way of facilities. Each school also has its own way of disseminating information to appropriate contacts. disseminating information to appropriate contacts. Due to the multiple channels of information Due to the multiple channels of information distribution, inconsistent interpretation among distribution, inconsistent interpretation among various policies and procedures could happen and various policies and procedures could happen and results in confusion and noncompliance.results in confusion and noncompliance.

Leasing Documents Need ClarificationLeasing Documents Need Clarification

5858

Performance AuditsPerformance Audits

15.15. Audit of Corrective Actions for Leasing of Audit of Corrective Actions for Leasing of School Facilities (October 12, 2007)School Facilities (October 12, 2007)

In response,In response,

The Real Estate Department has increased the The Real Estate Department has increased the number of group and individual one-on-one training number of group and individual one-on-one training sessions.sessions.

Current Rent Fee Schedules have been provided to Current Rent Fee Schedules have been provided to all schools and is now available on the Real Estate all schools and is now available on the Real Estate Services Department websiteServices Department website..

5959

Performance AuditsPerformance Audits

15.15. Audit of Corrective Actions for Leasing of Audit of Corrective Actions for Leasing of School Facilities (October 12, 2007)School Facilities (October 12, 2007)

The Facilities Management Division is working on a The Facilities Management Division is working on a Computer-Aided Facilities Management (CAFM) Computer-Aided Facilities Management (CAFM) Leasing component that will include a knowledge Leasing component that will include a knowledge base to help answer bookkeeper and school leasing base to help answer bookkeeper and school leasing personnel’s questions and further aide with the personnel’s questions and further aide with the ongoing training programongoing training program..

A training program on policy, procedures and proper A training program on policy, procedures and proper completion of forms has been created and completion of forms has been created and implemented in 2007. This supplemental program implemented in 2007. This supplemental program was offered four times focusing on the four different was offered four times focusing on the four different geographic locations within the County.geographic locations within the County.

6060

Performance AuditsPerformance Audits

15.15. Audit of Corrective Actions for Leasing of Audit of Corrective Actions for Leasing of School Facilities (October 12, 2007)School Facilities (October 12, 2007)

The attendance at this program was strongly The attendance at this program was strongly recommended and well attended. This program’s recommended and well attended. This program’s attendance will become mandatory starting in FY attendance will become mandatory starting in FY 07/08. The CAFM Leasing component will have an 07/08. The CAFM Leasing component will have an online training supplement that will not replace, but online training supplement that will not replace, but complement the ongoing training program.complement the ongoing training program.

Prospective lessees are provided with a checklist of Prospective lessees are provided with a checklist of documents, at the time of prequalification.documents, at the time of prequalification.

6161

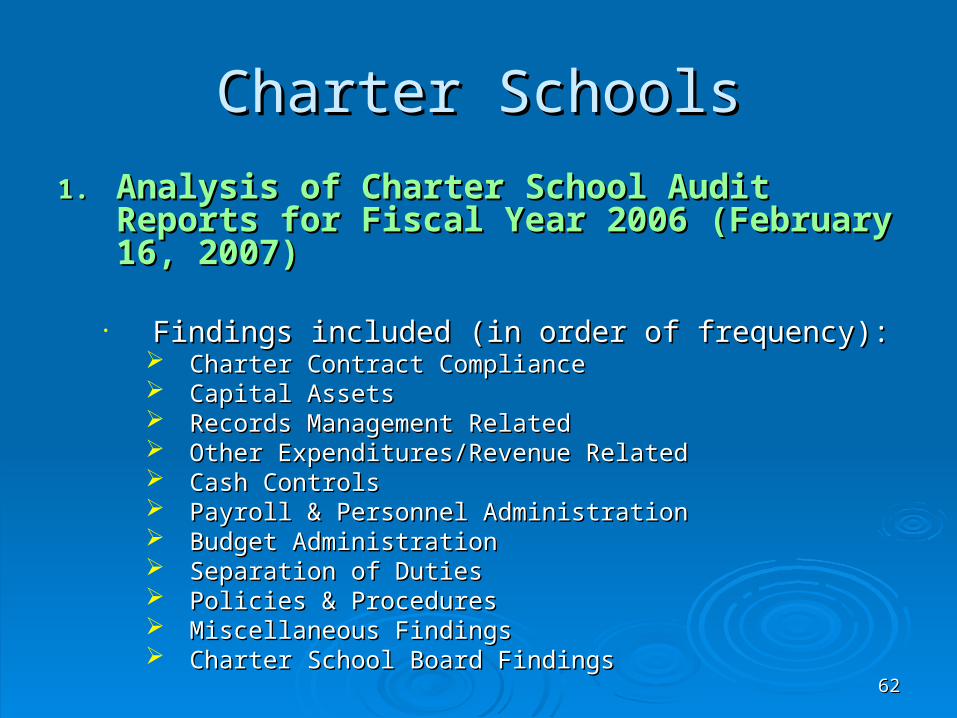

Charter SchoolsCharter Schools

1.1. Analysis of Charter School Audit Reports Analysis of Charter School Audit Reports for Fiscal Year 2006 (February 16, 2007)for Fiscal Year 2006 (February 16, 2007)

This report presents a summary of significant audit This report presents a summary of significant audit findings conducted by independent CPAs, and findings conducted by independent CPAs, and financial analysis for the 36 charter schools operating financial analysis for the 36 charter schools operating in Palm Beach County during fiscal year 2006.in Palm Beach County during fiscal year 2006.

14 (39%) of the 36 charter school audit reports had no major 14 (39%) of the 36 charter school audit reports had no major findings to report (Amended subsequent to meeting)findings to report (Amended subsequent to meeting)

The other 22 (61%) charter school audit reports included other The other 22 (61%) charter school audit reports included other major findings in internal control deficiencies or instances of major findings in internal control deficiencies or instances of noncompliance with applicable laws of rules, and need to be noncompliance with applicable laws of rules, and need to be addressed by the management of the school.addressed by the management of the school.

6262

Charter SchoolsCharter Schools

1.1. Analysis of Charter School Audit Reports Analysis of Charter School Audit Reports for Fiscal Year 2006 (February 16, 2007)for Fiscal Year 2006 (February 16, 2007)

• Findings included (in order of frequency):Findings included (in order of frequency): Charter Contract ComplianceCharter Contract Compliance Capital AssetsCapital Assets Records Management RelatedRecords Management Related Other Expenditures/Revenue RelatedOther Expenditures/Revenue Related Cash ControlsCash Controls Payroll & Personnel AdministrationPayroll & Personnel Administration Budget AdministrationBudget Administration Separation of DutiesSeparation of Duties Policies & ProceduresPolicies & Procedures Miscellaneous FindingsMiscellaneous Findings Charter School Board FindingsCharter School Board Findings

6363

Charter SchoolsCharter Schools

1.1. Analysis of Charter School Audit Reports Analysis of Charter School Audit Reports for Fiscal Year 2006 (February 16, 2007)for Fiscal Year 2006 (February 16, 2007)

26 (72%) of the 36 charter schools reported a positive year-26 (72%) of the 36 charter schools reported a positive year-end net assets, while 10 (28%) schools reported a negative end net assets, while 10 (28%) schools reported a negative net assets balance.net assets balance.

None of the 36 audit reports included findings that were None of the 36 audit reports included findings that were considered by their independent auditors to be material considered by their independent auditors to be material weaknesses in internal control.weaknesses in internal control.

Audit reports for 10 of the charter schools indicated a Audit reports for 10 of the charter schools indicated a Financial Emergency Condition pursuant to Financial Emergency Condition pursuant to Florida Statute Florida Statute 218.503’s218.503’s definition. Six of these 10 audit reports included a definition. Six of these 10 audit reports included a statement by the CPAs discussing the school’s financial statement by the CPAs discussing the school’s financial stability or ability to continue operations on an ongoing basis.stability or ability to continue operations on an ongoing basis.

6464

Charter SchoolsCharter Schools

1.1. Analysis of Charter School Audit Reports Analysis of Charter School Audit Reports for Fiscal Year 2006 (February 16, 2007)for Fiscal Year 2006 (February 16, 2007)

Pursuant to Pursuant to Florida Statute 218.503Florida Statute 218.503, and , and 1002.33 (9)(g)1002.33 (9)(g), , charter schools must notify the School District within 30 days charter schools must notify the School District within 30 days after receipt of a financial audit that finds the charter school to after receipt of a financial audit that finds the charter school to be in a state of financial emergency, and must file a detailed be in a state of financial emergency, and must file a detailed financial recovery plan.financial recovery plan.

None of the 36 audits reports included findings that were None of the 36 audits reports included findings that were considered by their independent auditors to be material considered by their independent auditors to be material weaknesses in internal control.weaknesses in internal control.

6565

Charter SchoolsCharter Schools

2.2. Follow-up Audit of Survivor Charter Follow-up Audit of Survivor Charter Schools to The Audit Committee (December Schools to The Audit Committee (December 8, 2006)8, 2006)

The Follow-Up Audit found additional evidence The Follow-Up Audit found additional evidence supported and confirmed many of the January 13, supported and confirmed many of the January 13, 2006, conclusions:2006, conclusions:

The compensations paid to the West Palm Beach and The compensations paid to the West Palm Beach and Boynton Beach Principals ($139,378 and $163,412 Boynton Beach Principals ($139,378 and $163,412 respectively), as well as the schools bookkeeper ($61,027) respectively), as well as the schools bookkeeper ($61,027) appeared to be excessive, in comparing to the District’s appeared to be excessive, in comparing to the District’s average salaries for respective employees.average salaries for respective employees.

The $25,028 in bonuses given to the West Palm Beach The $25,028 in bonuses given to the West Palm Beach Principal appeared to be inappropriate.Principal appeared to be inappropriate.

6666

Charter SchoolsCharter Schools2.2. Follow-up Audit of Survivor Charter Follow-up Audit of Survivor Charter

Schools to The Audit Committee (December Schools to The Audit Committee (December 8, 2006)8, 2006)

The West Palm Beach campus paid the Boynton Beach The West Palm Beach campus paid the Boynton Beach Principal $10,500 for unused sick leave, even though he was Principal $10,500 for unused sick leave, even though he was not employed by that campus.not employed by that campus.

The Boynton Beach Principal received $15,000 in regular The Boynton Beach Principal received $15,000 in regular wages while on personal leave for six weeks.wages while on personal leave for six weeks.

West Palm Beach Campus transferred $50,000 to establish a West Palm Beach Campus transferred $50,000 to establish a legal defense Fund, and apparent violations of Florida legal defense Fund, and apparent violations of Florida Sunshine Law.Sunshine Law.

Parents not members of governing board as required.Parents not members of governing board as required.

Some assets not recovered from both campuses.Some assets not recovered from both campuses.

6767

Charter SchoolsCharter Schools

3.3. Audit of Corebridge Educational Academy Audit of Corebridge Educational Academy Charter School (January 19, 2007)Charter School (January 19, 2007)

Although the school was closed abruptly by the charter Although the school was closed abruptly by the charter school operation during our audit, and certain school operation during our audit, and certain information was not available, the District was required information was not available, the District was required by Auditing Standards and School District Policy to by Auditing Standards and School District Policy to release the report. Due to the failure of Corebridge to release the report. Due to the failure of Corebridge to provide the District with certain information, several provide the District with certain information, several areas could not be audited.areas could not be audited.

6868

Charter SchoolsCharter Schools

3.3. Audit of Corebridge Educational Academy Audit of Corebridge Educational Academy Charter School (January 19, 2007)Charter School (January 19, 2007)

Major conclusions of the Corebridge Audit include:Major conclusions of the Corebridge Audit include:

Confidential Student Information and Financial Records Confidential Student Information and Financial Records Discarded, Scattered around Dumpster – Discarded, Scattered around Dumpster – On June 20, On June 20, 2006, school financial records and confidential student records 2006, school financial records and confidential student records were found scattered around a garbage dumpster area were found scattered around a garbage dumpster area outside the school facility. Discarding of public records is a outside the school facility. Discarding of public records is a violation of violation of Florida Statute 119Florida Statute 119. Also, . Also, Florida Statute Florida Statute 1022.221022.22 stipulates that every student has the a right to privacy stipulates that every student has the a right to privacy with respect to educational records.with respect to educational records.

6969

Charter SchoolsCharter Schools

3.3. Audit of Corebridge Educational Academy Audit of Corebridge Educational Academy Charter School (January 19, 2007)Charter School (January 19, 2007)

Dysfunctional Governing BoardDysfunctional Governing Board – The Governing Board of – The Governing Board of Corebridge Education Academy did not properly discharge its Corebridge Education Academy did not properly discharge its fiduciary responsibilities by not maintaining an adequate fiduciary responsibilities by not maintaining an adequate number of members, not providing effective oversight over the number of members, not providing effective oversight over the school’s operations, and allowing the school to operate with a school’s operations, and allowing the school to operate with a poor system of internal controls and be financially poor system of internal controls and be financially mismanaged.mismanaged.

Required Insurance Coverage Cancelled for Non Payment Required Insurance Coverage Cancelled for Non Payment of Premium of Premium – The school’s Commercial Insurance Package – The school’s Commercial Insurance Package including Automobile, and Excess Liability coverages were including Automobile, and Excess Liability coverages were cancelled as of October 25, 2005, and workers compensation cancelled as of October 25, 2005, and workers compensation coverage was cancelled as of November 16, 2005.coverage was cancelled as of November 16, 2005.

7070

Charter SchoolsCharter Schools

3.3. Audit of Corebridge Educational Academy Audit of Corebridge Educational Academy Charter School (January 19, 2007)Charter School (January 19, 2007)

School Continually Unwilling to Provide Financial School Continually Unwilling to Provide Financial RecordsRecords – The Principal had continually denied the School – The Principal had continually denied the School District from access to financial records, despite repeated District from access to financial records, despite repeated requests made to the Principal before, during, and subsequent requests made to the Principal before, during, and subsequent to audit fieldwork.to audit fieldwork.

Repeatedly Failed to Take Corrective Action Repeatedly Failed to Take Corrective Action – – Management Letters issued in September 2003, 2004, 2005, Management Letters issued in September 2003, 2004, 2005, repeatedly reported (1) the school did not prepare formal repeatedly reported (1) the school did not prepare formal voucher disbursements for its payables, (2) disbursements voucher disbursements for its payables, (2) disbursements were paid based on a copy of the invoice, and management were paid based on a copy of the invoice, and management had not corrected these recurring problem. Management had not corrected these recurring problem. Management Letters issued in September 2004, and 2005, reported that the Letters issued in September 2004, and 2005, reported that the school (1) physically held checks from its operating account school (1) physically held checks from its operating account due to insufficient cash-flow.due to insufficient cash-flow.

7171

Charter SchoolsCharter Schools3.3. Audit of Corebridge Educational Academy Audit of Corebridge Educational Academy

Charter School (January 19, 2007)Charter School (January 19, 2007)

Financial EmergencyFinancial Emergency – According to the school’s – According to the school’s Independent Auditor’s Report and Financial Statements for the Independent Auditor’s Report and Financial Statements for the year ended June 30, 2005, the school was in state of financial year ended June 30, 2005, the school was in state of financial emergency for failure to transmit to the Federal Government emergency for failure to transmit to the Federal Government (1) income tax withholdings, and (2) social security taxes for (1) income tax withholdings, and (2) social security taxes for employer and employees. The Auditor’s Report also indicated employer and employees. The Auditor’s Report also indicated that as of September 22, 2005, the school had not paid payroll that as of September 22, 2005, the school had not paid payroll taxes because it had no cash.taxes because it had no cash.

Inappropriate Uses of Public MoniesInappropriate Uses of Public Monies – The school was – The school was unable to provide 44, or 73% of the 60 requested invoices or unable to provide 44, or 73% of the 60 requested invoices or documentation for the selected expenditure. The audit could documentation for the selected expenditure. The audit could not ascertain if these expenditures were appropriate uses of not ascertain if these expenditures were appropriate uses of public funds.public funds.

7272

Charter SchoolsCharter Schools

3.3. Audit of Corebridge Educational Academy Audit of Corebridge Educational Academy Charter School (January 19, 2007)Charter School (January 19, 2007)

Other findings included:Other findings included:

Total Lack of Accountability and Internal ControlsTotal Lack of Accountability and Internal Controls

Some Assets Not Recovered from the SchoolSome Assets Not Recovered from the School

7373

Charter SchoolsCharter Schools

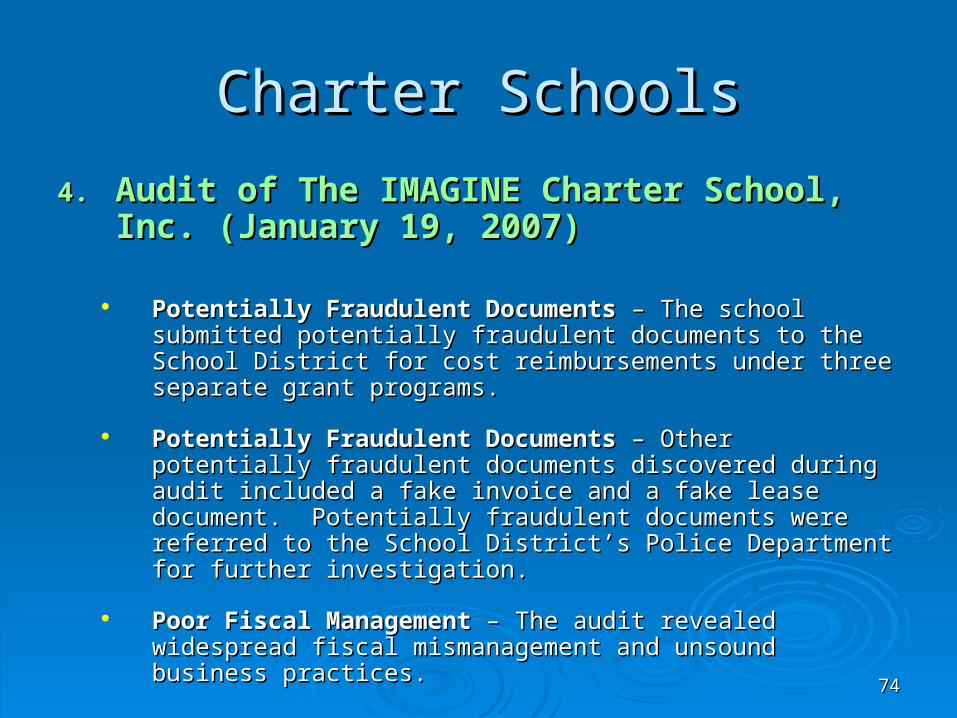

4.4. Audit of The IMAGINE Charter School, Inc. Audit of The IMAGINE Charter School, Inc. (January 19, 2007)(January 19, 2007)

The audit was conducted in response to the request of The audit was conducted in response to the request of the Charter Schools and Accounting Departments. the Charter Schools and Accounting Departments. During the audit, the school notified the School District During the audit, the school notified the School District of its intent to cease operations effective July 1, 2007. of its intent to cease operations effective July 1, 2007. The audit revealed the following major conclusions:The audit revealed the following major conclusions:

Deteriorating Financial ConditionDeteriorating Financial Condition – The school had been – The school had been unable to achieve the budgeted enrollment levels, and unable to achieve the budgeted enrollment levels, and enrollment had been steadily decreasing. The school’s enrollment had been steadily decreasing. The school’s financial condition had been steadily deteriorating and resulted financial condition had been steadily deteriorating and resulted in increasing negative fund balance, perpetual cash overdraft, in increasing negative fund balance, perpetual cash overdraft, and failure to contribute to retirement plan.and failure to contribute to retirement plan.

7474

Charter SchoolsCharter Schools

4.4. Audit of The IMAGINE Charter School, Inc. Audit of The IMAGINE Charter School, Inc. (January 19, 2007)(January 19, 2007)

Potentially Fraudulent DocumentsPotentially Fraudulent Documents – The school submitted – The school submitted potentially fraudulent documents to the School District for cost potentially fraudulent documents to the School District for cost reimbursements under three separate grant programs.reimbursements under three separate grant programs.

Potentially Fraudulent DocumentsPotentially Fraudulent Documents – Other potentially – Other potentially fraudulent documents discovered during audit included a fake fraudulent documents discovered during audit included a fake invoice and a fake lease document. Potentially fraudulent invoice and a fake lease document. Potentially fraudulent documents were referred to the School District’s Police documents were referred to the School District’s Police Department for further investigation.Department for further investigation.

Poor Fiscal ManagementPoor Fiscal Management – The audit revealed widespread – The audit revealed widespread fiscal mismanagement and unsound business practices.fiscal mismanagement and unsound business practices.

7575

Charter SchoolsCharter Schools

4.4. Audit of The IMAGINE Charter School, Inc. Audit of The IMAGINE Charter School, Inc. (January 19, 2007)(January 19, 2007)

Conflicts of Interest and Related Party TransactionsConflicts of Interest and Related Party Transactions – The – The school principal is the owner of at least five other businesses school principal is the owner of at least five other businesses that either utilize school’s facilities or use the business that either utilize school’s facilities or use the business address for correspondence. The school has an agreement address for correspondence. The school has an agreement with one of the principal’s private companies to administer with one of the principal’s private companies to administer health and workers compensation insurance plans, as well as health and workers compensation insurance plans, as well as the employee retirement plan. The principal recently used the employee retirement plan. The principal recently used pension plan funds, along with his personal funds, along with pension plan funds, along with his personal funds, along with his personal funds, for down payment on a house.his personal funds, for down payment on a house.

The Principal neither demanded payment from the private The Principal neither demanded payment from the private school, nor paid all monies owed the IMAGINE school. Also, school, nor paid all monies owed the IMAGINE school. Also, the school allowed one of the principal’s other private schools the school allowed one of the principal’s other private schools to utilize a portion of the IMAGINE school’s facilities for free, to utilize a portion of the IMAGINE school’s facilities for free, and without a written sub-lease agreement.and without a written sub-lease agreement.

7676

Charter SchoolsCharter Schools5.5. Audit of G-Star School of the Arts for Motion Audit of G-Star School of the Arts for Motion

Pictures and Television (January 19, 2007)Pictures and Television (January 19, 2007)

The audit concluded that:The audit concluded that:

The school did not maintain documentation that demonstrated The school did not maintain documentation that demonstrated the reimbursement amount fully compensated the school for the reimbursement amount fully compensated the school for the Caribbean Cruise expenses incurred. An account the Caribbean Cruise expenses incurred. An account receivable related to this event was not recorded on the receivable related to this event was not recorded on the school’s financial records, and partial reimbursement was school’s financial records, and partial reimbursement was received more than one year after the school incurred the received more than one year after the school incurred the expenses.expenses.

The Governing board awarded the founder a $150,000 bonus The Governing board awarded the founder a $150,000 bonus but it was not disclosed or recorded on any of the school’s but it was not disclosed or recorded on any of the school’s financial records. The school’s independent auditors notified financial records. The school’s independent auditors notified them of the potentially undisclosed $150,000 debt, as well as them of the potentially undisclosed $150,000 debt, as well as other issues identified in this report.other issues identified in this report.

7777

Charter SchoolsCharter Schools

5.5. Audit of G-Star School of the Arts for Motion Audit of G-Star School of the Arts for Motion Pictures and Television (January 19, 2007)Pictures and Television (January 19, 2007)

Free use of facilities by for-profit businesses.Free use of facilities by for-profit businesses.

Supplies and two-year free use of a building for a private for-Supplies and two-year free use of a building for a private for-profit company.profit company.

$2,700 paid to contractor.$2,700 paid to contractor.

Poor record keeping.Poor record keeping.

School founder overpaid in errorSchool founder overpaid in error..

7878

Charter SchoolsCharter Schools

5.5. Audit of G-Star School of the Arts for Motion Audit of G-Star School of the Arts for Motion Pictures and Television (January 19, 2007)Pictures and Television (January 19, 2007)

Fix assets not adequately tagged or recorded Fix assets not adequately tagged or recorded (Note: District (Note: District Auditor’s Office will perform an updated inventory of the Auditor’s Office will perform an updated inventory of the school, and the results will be released as a subsequent event school, and the results will be released as a subsequent event report.)report.)

Use of facilities without lease agreements.Use of facilities without lease agreements.

Inadequate backup documentation maintained.Inadequate backup documentation maintained.

Tenant did not undergo required criminal background Tenant did not undergo required criminal background screening.screening.

7979

Other InvolvementsOther Involvements

1.1. Assist the Charter School Department in Assist the Charter School Department in revising the model revising the model Charter AgreementCharter Agreement for for charter schoolscharter schools

2.2. Assist Legal Department in preparing for legal Assist Legal Department in preparing for legal proceedings related to auditsproceedings related to audits

3.3. Assist School Police & Employee Relations Assist School Police & Employee Relations Departments in their investigation of Departments in their investigation of improprietiesimproprieties

4.4. Assist Employee Relations Department in Assist Employee Relations Department in designing training for certain employeesdesigning training for certain employees

8080

Possible Impacts for AuditsPossible Impacts for Audits

Value added to our existing management Value added to our existing management controls and accountabilitiescontrols and accountabilities

Value added to the integrity of our systemValue added to the integrity of our system

Strengthening the control systemStrengthening the control system

8181

Possible Impacts for AuditsPossible Impacts for Audits

Ultimate results:Ultimate results: Protect our studentsProtect our students Protect school administratorsProtect school administrators Safeguard assets and ensure compliance with laws, Safeguard assets and ensure compliance with laws,

School Board Policies & guidelinesSchool Board Policies & guidelines Better controls resulting in increase in revenuesBetter controls resulting in increase in revenues Better control in operating expensesBetter control in operating expenses Provide deterrent for potential abuse of the systemProvide deterrent for potential abuse of the system Promote public confidence in the school system Promote public confidence in the school system

through public transparency, professional through public transparency, professional independence, & objective reportingindependence, & objective reporting

8282

OthersOthers

KPMG’s Management Letter for KPMG’s Management Letter for Year-Ended June 30, 2006 (February 16, 2007)Year-Ended June 30, 2006 (February 16, 2007)

No changes in significant accounting policies.No changes in significant accounting policies.

No significant unusual accounting transactions were No significant unusual accounting transactions were encountered for which there is lack of authoritative encountered for which there is lack of authoritative guidance or consensus.guidance or consensus.

Audit adjustments were done without objections from Audit adjustments were done without objections from the District.the District.

There was one Reportable Condition and four other There was one Reportable Condition and four other comments in the Management Letter.comments in the Management Letter.

8383

OthersOthers

KPMG’s Management Letter for KPMG’s Management Letter for Year-Ended June 30, 2006 (February 16, 2007)Year-Ended June 30, 2006 (February 16, 2007)

Reportable Conditions:Reportable Conditions:

Detailed Account AnalysisDetailed Account Analysis - The accounting department did not - The accounting department did not perform reviews and analyses of general ledger accounts to ensure perform reviews and analyses of general ledger accounts to ensure that information is accurately and completely reported. This that information is accurately and completely reported. This represents a deficiency in the design or operations of internal represents a deficiency in the design or operations of internal control and could adversely affect the School District’s ability to control and could adversely affect the School District’s ability to record, process, summarize, and report financial data consistent record, process, summarize, and report financial data consistent with the assertions of management in the financial statements.with the assertions of management in the financial statements.

Staff agreed with the finding, and stated that some key accounting Staff agreed with the finding, and stated that some key accounting staff members and the dedication of resources to the ERP staff members and the dedication of resources to the ERP implementation limited the department’s level of account analysis. implementation limited the department’s level of account analysis. The increasing complexity of some financial transactions also The increasing complexity of some financial transactions also requires additional analysis. The District plants to fill current requires additional analysis. The District plants to fill current accountant vacancies and provide staff development to ensure accountant vacancies and provide staff development to ensure accounts are analyzed at an in-depth level on a periodic basis.accounts are analyzed at an in-depth level on a periodic basis.

8484

OthersOthers

KPMG’s Management Letter for KPMG’s Management Letter for Year-Ended June 30, 2006 (February 16, 2007)Year-Ended June 30, 2006 (February 16, 2007)

Other CommentsOther Comments

Compensated Absences – Terminal Leave PayoutCompensated Absences – Terminal Leave Payout - - The School The School District’s written policy regarding annual and sick leave payout upon District’s written policy regarding annual and sick leave payout upon separation is not consistent with the practice that has been implemented separation is not consistent with the practice that has been implemented by management.by management.

Testing of Recovery ProceduresTesting of Recovery Procedures - Formal testing of recovery - Formal testing of recovery procedures is not part of the School District’s regular backup and procedures is not part of the School District’s regular backup and recovery process.recovery process.

Password Change PolicyPassword Change Policy - The School District’s policy for password - The School District’s policy for password maintenance can be overridden by system Super-users.maintenance can be overridden by system Super-users.

Improved Security ProcessImproved Security Process - KPMG became aware of security incident - KPMG became aware of security incident regarding the information system during the audit. Once made aware, regarding the information system during the audit. Once made aware, the School District personnel made several changes over the security.the School District personnel made several changes over the security.

8585

Projects for 2006-07 Audit PlanProjects for 2006-07 Audit Plan

Proposed Audit Plan 2007-08