1 HealthcareWebSummit December, 2002 Dana E. McMurtry Vice President, Health Policy & Analysis...

24

1 HealthcareWebSummit HealthcareWebSummit December, 2002 December, 2002 Dana E. McMurtry Dana E. McMurtry Vice President, Health Policy & Vice President, Health Policy & Analysis Analysis WellPoint Health Networks Inc. WellPoint Health Networks Inc. A Case Study in Health Plan A Case Study in Health Plan Responses: WellPoint Responses: WellPoint

-

Upload

beverly-peters -

Category

Documents

-

view

213 -

download

0

Transcript of 1 HealthcareWebSummit December, 2002 Dana E. McMurtry Vice President, Health Policy & Analysis...

1

HealthcareWebSummitHealthcareWebSummit

December, 2002December, 2002

Dana E. McMurtryDana E. McMurtryVice President, Health Policy & Analysis Vice President, Health Policy & Analysis

WellPoint Health Networks Inc.WellPoint Health Networks Inc.

A Case Study in Health Plan A Case Study in Health Plan Responses: WellPointResponses: WellPoint

2

AgendaAgenda

• Current Cost Trends

• Customer Challenges

• WellPoint’s Response

• The Future?

3

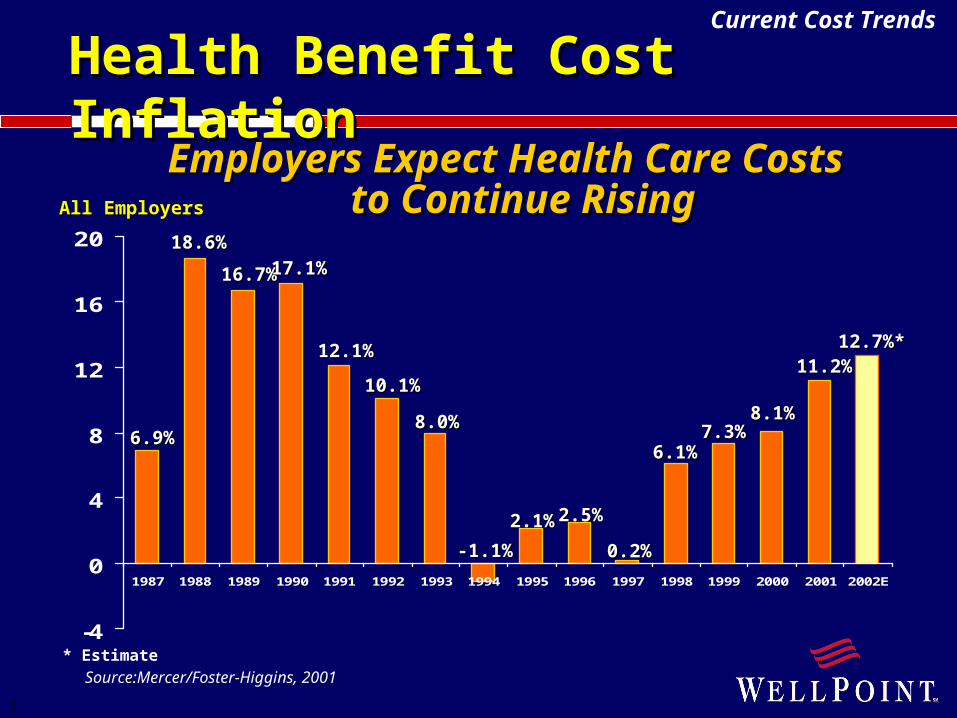

Employers Expect Health Care Costs Employers Expect Health Care Costs to Continue Risingto Continue Rising

Health Benefit Cost InflationHealth Benefit Cost Inflation

* EstimateSource:Mercer/Foster-Higgins, 2001

All EmployersAll Employers

6.9%6.9%

18.6%18.6%

16.7%16.7%17.1%17.1%

12.1%12.1%

10.1%10.1%

8.0%8.0%

-1.1%-1.1%

2.1%2.1% 2.5%2.5%

0.2%0.2%

6.1%6.1%7.3%7.3%

8.1%8.1%

11.2%11.2%12.7%*12.7%*

-4

0

4

8

12

16

20

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002E

Current Cost Trends

4

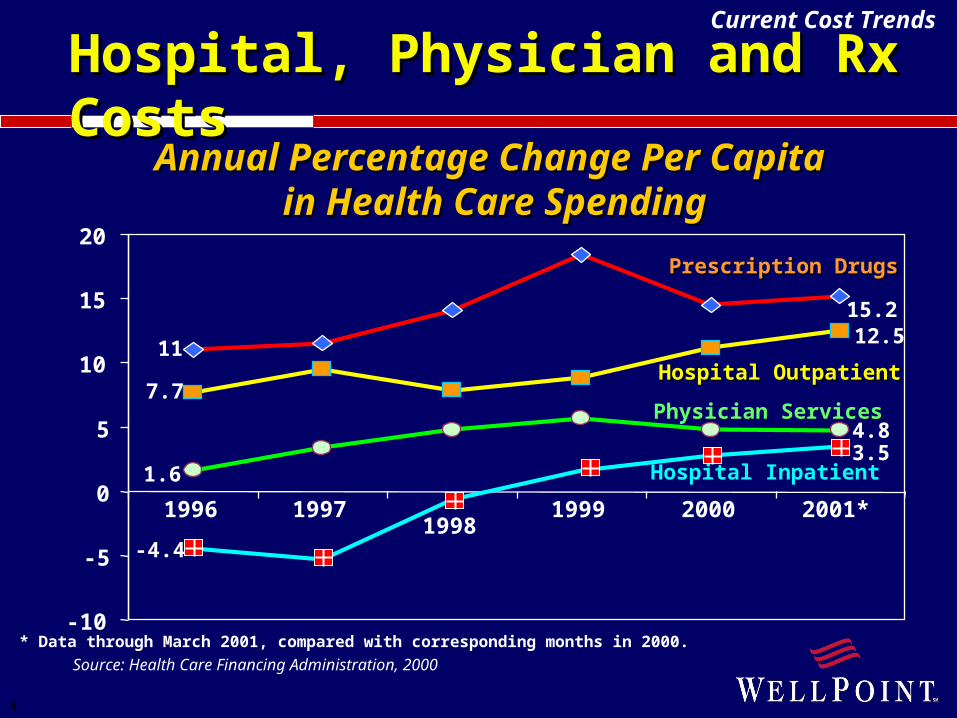

Hospital, Physician and Rx CostsHospital, Physician and Rx Costs

Source: Health Care Financing Administration, 2000

Annual Percentage Change Per Capita Annual Percentage Change Per Capita in Health Care Spendingin Health Care Spending

* Data through March 2001, compared with corresponding months in 2000.

15.2

11

Prescription DrugsPrescription Drugs

12.5

7.7Hospital OutpatientHospital Outpatient

4.8

1.6

Physician Services

-10

-5

0

5

10

15

20

1996 19971998

1999 2000 2001*

-4.4

Hospital Inpatient3.5

Current Cost Trends

5

Multiple Cost Drivers Multiple Cost Drivers

• Hospital Consolidation

• Pharmaceutical Practices

• Consumer Expectations

• Aging Population

• Medical Technology

• Legislation

Current Cost Trends

6

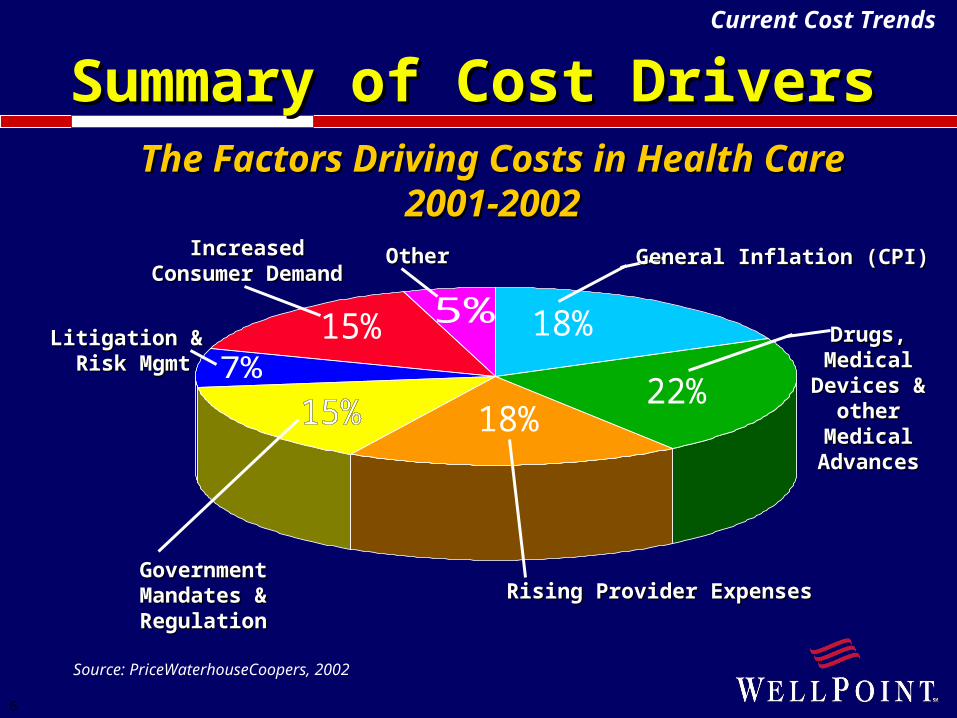

Summary of Cost DriversSummary of Cost DriversThe Factors Driving Costs in Health CareThe Factors Driving Costs in Health Care

2001-20022001-2002General Inflation (CPI)General Inflation (CPI)

Drugs, Drugs, Medical Medical

Devices & Devices & other Medical other Medical

AdvancesAdvances

Rising Provider ExpensesRising Provider ExpensesGovernmentGovernmentMandates &Mandates &RegulationRegulation

Litigation & Litigation & Risk MgmtRisk Mgmt

IncreasedIncreasedConsumer DemandConsumer Demand

OtherOther

Source: PriceWaterhouseCoopers, 2002

Current Cost Trends

7

AgendaAgenda

• Current Cost Trends

• Customer Challenges

• WellPoint’s Response

• The Future?

8

What Employers WantWhat Employers Want

Administrative Administrative EaseEase

Source:PriceWaterhouseCoopers LLP, 2001

ChoiceChoiceBudgetabilityBudgetability

Customer Challenges

9

Strategies to Control CostsStrategies to Control Costs

3%

8%

5%

8%

19%

28%

19%

11%

11%

15%

15%

14%

19%

43%

0% 10% 20% 30% 40% 50% 60%

Increase Consumerism

Add high-deductible plan

Use ROI calculations in decision-making

Use clinical risk adjustment in plan selection & pricing

Actions Employers Anticipate Taking to Manage Actions Employers Anticipate Taking to Manage Health Care Costs in Next 12 MonthsHealth Care Costs in Next 12 Months

Source: Watson Wyatt Worldwide, 2002

What Employers WantWhat Employers Want

Increase employee choice

Purchase DM programs

Develop direct contracts

Currently in place Planned in the next year

Customer Challenges

10

Competing demands of...Competing demands of...

• Choice

• Unlimited benefits

• Access to new medical technologies

• Brand name drugs

• Broad / less restrictive networks

What Consumers WantWhat Consumers Want

……All at an affordable premiumAll at an affordable premium

Customer Challenges

11

0

5

10

15

20

25

30

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996

Austria

Denmark

Finland

Germany

Ireland

UnitedKingdom

NewZealand

UnitedStates

Current Cost Trends

Consumer Out of Pocket Spending as a Percent of Consumer Out of Pocket Spending as a Percent of Total National Health Spending, 1986-1996Total National Health Spending, 1986-1996

Source: OECD, 2000, in PricewaterhouseCoopers’ HealthCast 2010, 1999

U.S. Employers Shoulder the BurdenU.S. Employers Shoulder the BurdenWhat Consumers WantWhat Consumers Want

12

AgendaAgenda

• Current Cost Trends

• Customer Challenges

• WellPoint’s Response

• The Future?

13

• Participation in All Markets

• The “Health Security” Model

• Focus on Product Innovation

WellPoint’s ResponseWellPoint’s ResponseWellPoint’s Response

14

SizeSize

Individual 1Senior 1Small Group 2 – 50Key Accounts 51 – 250Major Accounts 251 – 2000Special Accounts 2001+Public EntitiesState Sponsored Programs

Organized by Customer SegmentOrganized by Customer Segment

WellPoint’s Response

Participation in All MarketsParticipation in All Markets

15

• Choice of Products

• Network Development

• Clinical Collaboration

• Targeted Medical Management

• Member Information

The “Health Security” ModelThe “Health Security” ModelWellPoint’s Response

16

Focus on Product InnovationFocus on Product InnovationIndividual & Small GroupIndividual & Small GroupPlanScapePlanScape

LOWER PRICED MEDIUM PRICED HIGHER PRICED

Basic PPO 1000PPO SaverPPO Share 2500EPO

PPO Share 1500PPO Share 1000PPO Share 500BC Life Share 1000BC Life Share 500

PlanScape Products HMO Coverage

HMO SaverIndividual HMO

LOWER PRICED MEDIUM PRICED HIGHER PRICED

FlexScapeFlexScape

Basic PPO High Deduct. PPOSaver PPOSaver HMO

PPO $40 CopayPPO $30 Copay

HMO 100%PPO $20 CopayPPO $10 CopayUltra PremiumPPO $10 Copay

WellPoint’s Response

17

WellPoint’s Response

Further choice at the member levelFurther choice at the member level

• FamilyElect for Individuals

• EmployeeElect for Small Groups

Focus on Product InnovationFocus on Product InnovationIndividual & Small GroupIndividual & Small Group

18

• ASO Services

• Rental Networks For Self-insured

• Network-Based Products

• Consumer-Driven Plans

Focus on Product InnovationFocus on Product InnovationLarge GroupLarge Group

WellPoint’s Response

19

Experimenting with Defined ContributionExperimenting with Defined Contribution

Focus on Product InnovationFocus on Product InnovationConsumer-Driven Plans Consumer-Driven Plans (Large Group)(Large Group)

WellPoint’s Response

ComponentComponent FeaturesFeatures HSA

FSA

PPO Plan

• Employer funded• First dollar coverage• Funds can be used for any service covered by the plan• Applies toward deductible• Access to negotiated discounts• Unused funds roll over to following year

• Employee funded• Pre-tax• Funds can be used for out of pocket services if HSA depleted,

copays and other IRS allowed services not covered by the plan• May apply toward deductible• Use it or lose it

• High deductible• Preventive care may be covered not subject to deductible• 90%/70% or 80%/60% once deductible met• OOP maximums

20

A coalition of 2424 health plans (representing 100100 million members million members) & 3 principle health plan associations who:• Are committed to improving the

health care experience for consumers and their doctors

• Share a common vision that some of health care’s pressing concerns can best be addressed collectively

Council for Affordable Quality HealthcareCouncil for Affordable Quality HealthcareFocus on Changing Industry Practices

WellPoint’s Response

21

CAQH ProjectsCAQH Projects

• Save Antibiotic Strength Save Antibiotic Strength - - Partnership with CDC & physicians to Partnership with CDC & physicians to educate public on antibotic resistanceeducate public on antibotic resistance

• Formulary WebsiteFormulary Website - Easily accessible, standardized, web-based database of health plan formularies

• Physician CredentialingPhysician Credentialing - Centralized electronic database for national single credentialing application

Industry CollaborationWellPoint’s Response

22

AgendaAgenda

• Current Cost Trends

• Customer Challenges

• WellPoint’s Response

• The Future?

23

The Future?The Future?• More consumer choice and involvement

• The potential of disease management is realized

• Genomics (and cloning?) will result in new therapies not yet contemplated

• The interaction between aging, medical and technological advances, and consumerism will challenge everyone

24