1 Financing Innovation in Europe Brussels / December 16, 2005 Kim Kreilgaard.

15

1 Financing Innovation in Europe Brussels / December 16, 2005 Kim Kreilgaard

-

Upload

beryl-horn -

Category

Documents

-

view

216 -

download

0

Transcript of 1 Financing Innovation in Europe Brussels / December 16, 2005 Kim Kreilgaard.

1

Financing Innovation in Europe

Brussels / December 16, 2005

Kim Kreilgaard

2

Table of Content

2. Case Studies

1. Financing Innovation in Europe

3

Financing Innovation in EuropeEIB Profile

• The EIB is the EU long-term financing institution

• The EIB has been created by the Rome Treaty 1958

• The EIB is owned by the 25 EU member states

• The EIB is a policy driven institution (EU Commission, Council and EP)

• The EIB has a subscribed capital EUR 150bn EUR 164bn

• The EIB collects its funds on the capital markets (2004: EUR 50bn)

• The EIB signed loans amounting to EUR 43.2bn in 2004

4

Financing Innovation in EuropeEIB Strategic Objectives

Five priorities

• Economic and social cohesion in an enlarged EU

• Implementing of the Innovation 2010 Initiative (i2i)

• Development of Trans-European and Access networks (TENs)

• Support of EU Development and Cooperation Policies in Partner Countries

• Environmental Protection and Improvement, including Climate Change and Renewable Energy.

EIB financing always depends on the creditworthiness of the borrower and/or the guarantor(s).

Direct and indirect Loans for private and

public entities

Global Loans(small projects/SMEs)

MidCap Facility

EIB Product Portfolio:

5

Financing Innovation in EuropeWhat the EIB can do?

• Funding Supply: Increase market supply for loans/guarantees for innovation projects from EIB own resources; from EIB SFF resources; through joint financial products with Commission (RSFF) and through co-financing with financial markets.

• Funding Costs: Pass-on funding advantage of EIB after “risk pricing” to private/public sector innovators in order to reduce the cost of innovation

• Risk Sharing: Share financial risks with promoters in innovation projects and consequently reduce their risk adjusted cost of capital

• Signaling Effects: Due the Bank’s reputation for its prudent lending policy and its strong market/technology know-how, the EIB provides learning/signaling effects for other Banks

EIB PolicySupport in i2i

Risk Sharing

Signalling Effects

Funding Supply

Funding Costs

6

• Maximum loan amount: up to 50% of project cost.

• Loan tenors: depending on the “economic life” of the investment (generally between 10 and 20 years; exceptions).

• Interest Rate: Fixed or Variable

• Minimum size per loan: > EUR 25 m (Up to EUR 12.5m: Global Loan; For loans larger than EUR 12.5m, but smaller than EUR 25m: Mid Cap Facility; Exceptions possible)

• Business plan and project definition

Minimum Requirements / Terms

General Lending Policy

• EIB follows a policy of close co-operation with the banking sector.

• EIB almost always finances projects together with other banks.

• Close co-operation with all national and regional promotional banks.

Financing Innovation in EuropeEIB Lending Policy

7

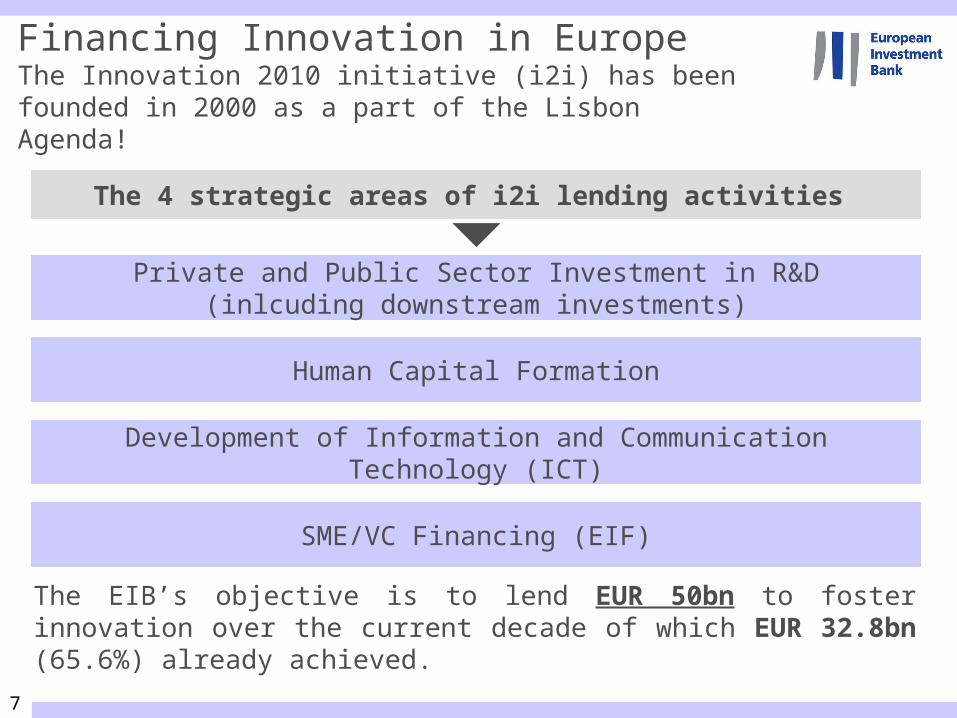

Financing Innovation in Europe The Innovation 2010 initiative (i2i) has been founded in 2000 as a part of the Lisbon Agenda!

The EIB’s objective is to lend EUR 50bn to foster innovation over the current decade of which EUR 32.8bn (65.6%) already achieved.

Private and Public Sector Investment in R&D(inlcuding downstream investments)

Human Capital Formation

Development of Information and CommunicationTechnology (ICT)

SME/VC Financing (EIF)

The 4 strategic areas of i2i lending activities

8

Financing Innovation in EuropeHigher Risk Financing – SFF and RSFF

The EIB implemented SFF as a facility – funded from own resources – aiming to provide financing for companies and projects in higher risk categories than the standard EIB requirement.

RSFF (implemented in 2007) will be based on the same objective / procedures but focused on RDI investments. Moreover, RSFF is a joint initiative of the European Union and the EIB.

Objectives

• Overcome market inefficiencies (information failures and spillover effects)

• Signalling: Catalyse the mobilization of further resources from EIB and capital markets through co-financing and EIB guarantees

• Improve access throughout the EU to financing for corporates, SPVs, public bodies, & SMEs to invest in priority technology themes

9

Financing Innovation in Europe Higher Risk Financing – SFF and RSFF

The EIB will continue its approach of EIB own resources/SFF AND enhance its activities by a continous product innovation process.

SFF Risk sharing with banks/other specialists

(e.g. Automotive RDI (GER), Coficiné (FR), Cofiloisirs (FR))

SFF Low/sub-investmentgrade companies

(e.g. Bombardier (UK), Andasol (ES), Atmel (FR))

Strategic Approaches for RDI Financing

• The EIB and the European Comission are developing under FP7 a new dedicated facility for RTD financing.

Risk Sharing Finance Facility (RSFF)

1 2

3

10

• Projects eligible under FP7

• Large European RTD projects (joint technology initiatives and large collaborative projects)

• Participants in multi-partner consortia (Midcaps, large corporates, SMEs, PPPs, etc.)

Eligibility

Financing Innovation in Europe Higher Risk Financing - RSFF

• Improve access to finance by sharing risks between EIB and the EU Budget (i) to leverage larger volume of high risk lending and (ii) to finance riskier projects

• Demonstrate the feasibility and bankability of numerous research projects

Added Value

11

Table of Content

2. Case Studies

1. Financing Innovation in Europe

12

Case Study I: Automotive RDI (I)The Supplier Dilemma

33%43% 49%

67%57% 51%

0%

20%

40%

60%

80%

100%

120%

2000 2005 2010

Reduction of R&D investment for OEMs% of total R&D Expenditure

OE

Ms

Su

pp

lier

Ca

pE

x

Ca

pE

x

Years

Suppliers are forced to take more R&D risk and to finance an increasing number of larger R&D projects.

Years

Present Future

Shorter R&D Cycles with higher CapexIllustrative

Source: Roland Berger, VDA, HVB Equity Research

• Driven by OEM* pressure to reduce their share in the overall value chain (esp. upstream), automotive suppliers find it increasingly difficult and expensive to fund R&D projects

• As a consequence, financing has become the crucial element for Suppliers to succeed in tenders of new R&D projects with leading OEMs

* OEM: Original Equipment Manufacturer

13

Case Study I: Automotive RDI (II)Tailor-made EIB Solution

OEMAutomotive Suppliers

Lesees/Final BeneficiaryDevelopment and production of a car component

Technology LeasingHard Assets + IPR

Deutsche LeasingLeading German Leasing

Financial Structuring

Saar LB

Re-Financing + Partial Credit Risk of Lesee

Global Loan

Risk Sharing

Credit Risk Distribution:Deutsche Leasing: 10% - 49%Saar LB: > 26%EIB: Max. 25%

• The combination of a classical Global Loan with a tailor-made risk sharing guarantee scheme generates a capital relief for SaarLB.

• Hence, risk capacity for SaarLB and Deutsche Leasing for R&D financing of automotive suppliers is improved and will lead to more lending activity

• EIB will delegate due diligence to Deutsche Leasing and SaarLB (two independent and experienced players in that field)

• Support innovative models for IPR based financing

14

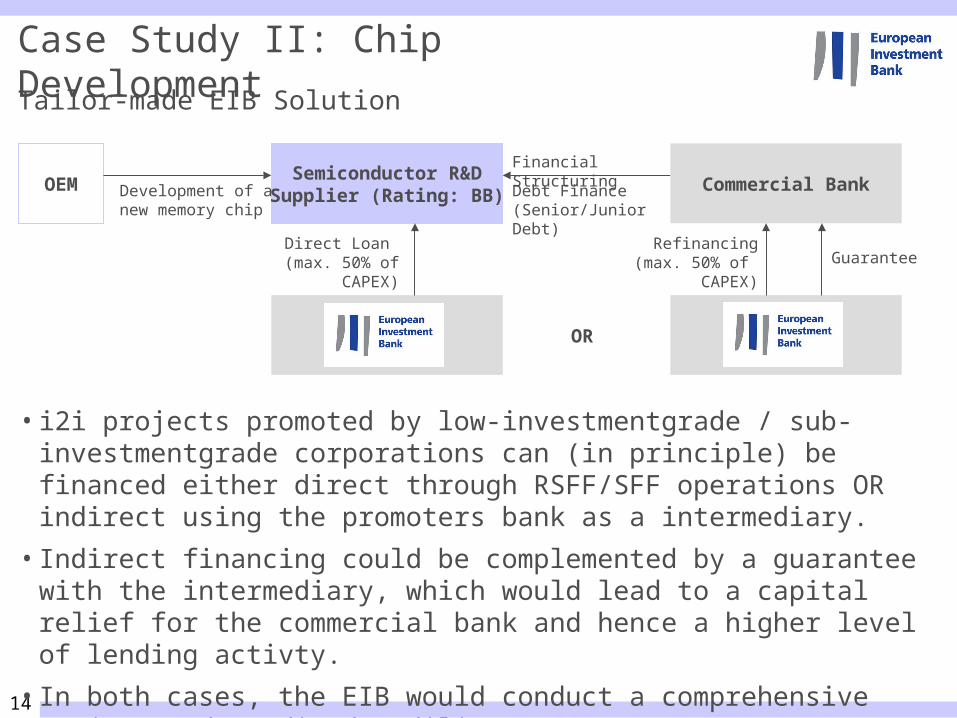

Case Study II: Chip DevelopmentTailor-made EIB Solution

OEMSemiconductor R&DSupplier (Rating: BB)Development of a

new memory chipDebt Finance(Senior/Junior Debt)

Commercial BankFinancial Structuring

Direct Loan (max. 50% of

CAPEX)

OR

Refinancing(max. 50% of

CAPEX)

Guarantee

• i2i projects promoted by low-investmentgrade / sub-investmentgrade corporations can (in principle) be financed either direct through RSFF/SFF operations OR indirect using the promoters bank as a intermediary.

• Indirect financing could be complemented by a guarantee with the intermediary, which would lead to a capital relief for the commercial bank and hence a higher level of lending activty.

• In both cases, the EIB would conduct a comprehensive project and credit due diligence.

15

Kim KreilgaardHead of Structured Finance in i2i

Phone: (+352) 4379 7116Fax: (+352) 4379 7198eMail: [email protected]

European Investment Bank100, boulevard Konrad AdenauerL-2950 Luxembourg

Thomas C. BarrettDirector AGI

Phone: (+352) 4379 7006Fax: (+352) 4379 7099eMail: [email protected]

European Investment Bank100, boulevard Konrad AdenauerL-2950 Luxembourg

Guy ClausseAssociate DirectorOperational Lending Policies

Phone: (+352) 4379 2570Fax: (+352) 4379 3494eMail: [email protected]

European Investment Bank100, boulevard Konrad AdenauerL-2950 Luxembourg

Jean-Jaques MertensAssociate Director Project Directorate

Phone: (+352) 4379 8612eMail: [email protected]

European Investment Bank100, boulevard Konrad AdenauerL-2950 Luxembourg

Thank You !