1 Financial Accounting Financial Accounting Dr. Pietro Andrea Podda, PhD.

30

1 Financial Accounting Financial Accounting Dr. Pietro Andrea Podda , PhD Dr. Pietro Andrea Podda , PhD

-

Upload

mervin-walton -

Category

Documents

-

view

224 -

download

1

Transcript of 1 Financial Accounting Financial Accounting Dr. Pietro Andrea Podda, PhD.

11

Financial AccountingFinancial Accounting

Dr. Pietro Andrea Podda , PhDDr. Pietro Andrea Podda , PhD

22

IntroductionIntroduction

1.1. Accounting is the science that Accounting is the science that studstudiesies the collection, recording, the collection, recording, interpretation and trainterpretation and trannsmission smission of financial informationof financial information

2.2. Accounting is divided into two Accounting is divided into two main types: financial (directed main types: financial (directed to external users) and to external users) and managerial (for internalmanagerial (for internal use use))

33

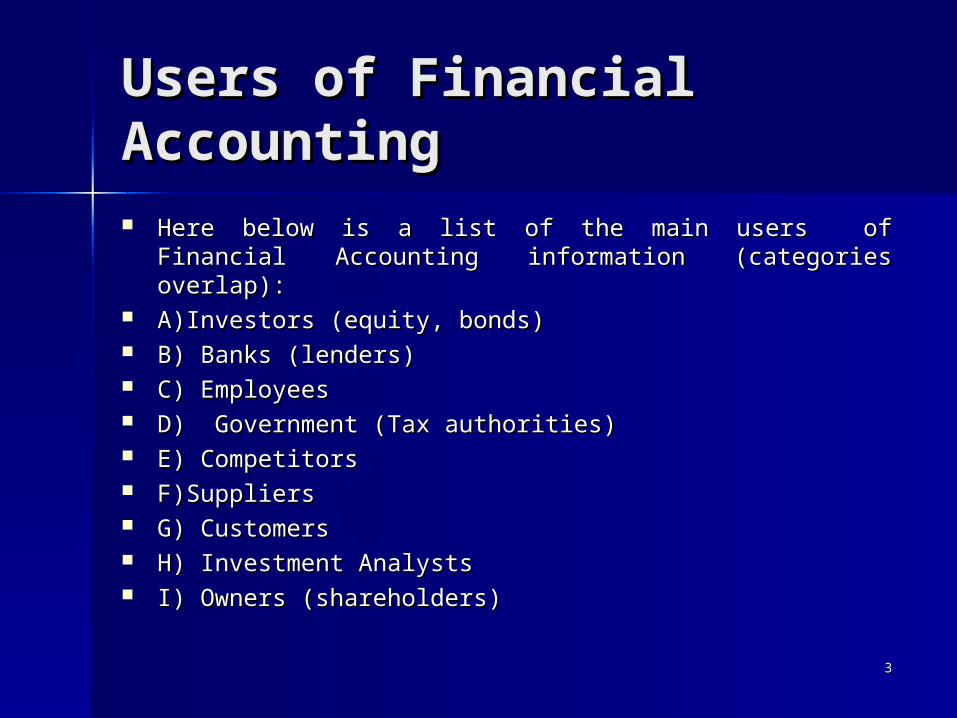

Users of Financial Users of Financial AccountingAccounting Here below is a list of the main users of Financial Here below is a list of the main users of Financial

Accounting information (categories overlap):Accounting information (categories overlap): A)Investors (equity, bonds)A)Investors (equity, bonds) B) Banks (B) Banks (llenders)enders) C) EmployeesC) Employees D) Government (Tax authorities)D) Government (Tax authorities) E) CompetitorsE) Competitors F)SuppliersF)Suppliers G) CustomersG) Customers H) Investment AnalystsH) Investment Analysts I) Owners (shareholders)I) Owners (shareholders)

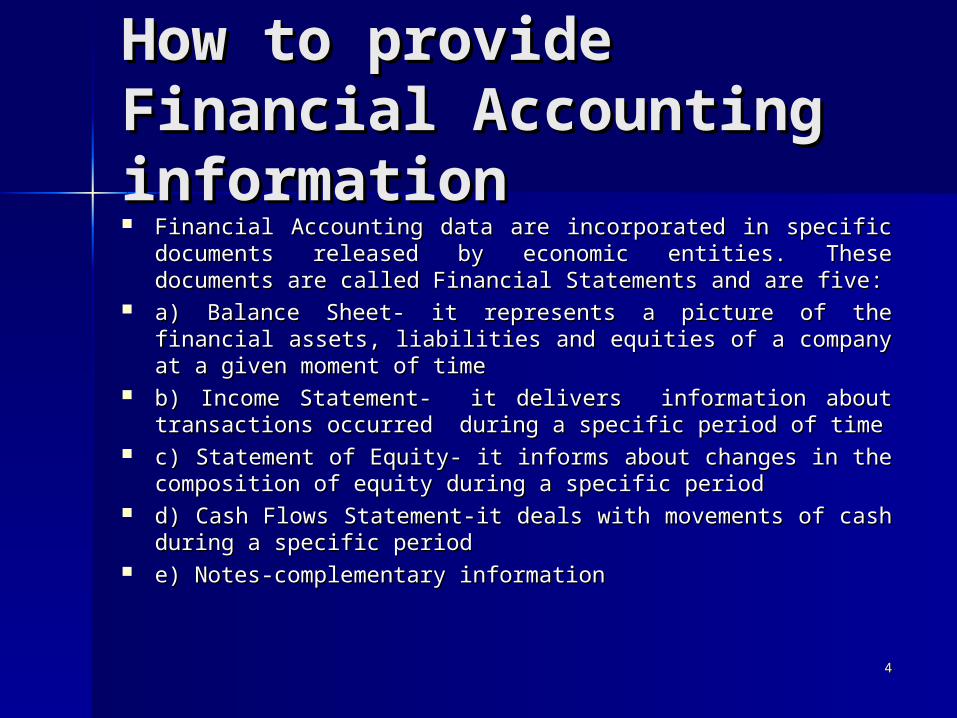

How to provide How to provide Financial Accounting Financial Accounting informationinformation Financial Accounting data are incorporated in specific Financial Accounting data are incorporated in specific

documents released by economic entities. These documents documents released by economic entities. These documents are called Financial Statements and are five:are called Financial Statements and are five:

a) Balance Sheet- it represents a picture of the financial a) Balance Sheet- it represents a picture of the financial assets, liabilities and equities of a company at a given assets, liabilities and equities of a company at a given moment of timemoment of time

b) Income Statement- it delivers information about b) Income Statement- it delivers information about transactions occurred during a specific period of timetransactions occurred during a specific period of time

c) Statement of c) Statement of EEquity- it informs about changes in the quity- it informs about changes in the composition of equity during a specific periodcomposition of equity during a specific period

d) Cash Flows Statement-it deals with movements of cash d) Cash Flows Statement-it deals with movements of cash during a specific periodduring a specific period

e) Notes-complementary informatione) Notes-complementary information

44

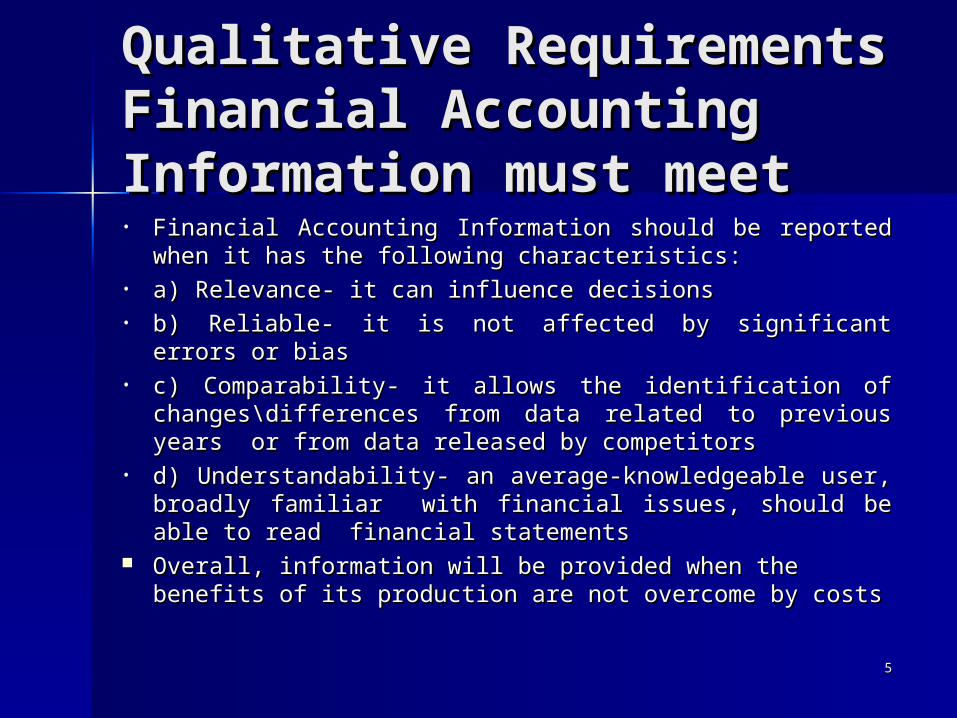

QualitQualitatatiivvee Requirement Requirements s Financial Accounting Financial Accounting InformatInformatiionon must meet must meet• Financial Accounting Information sFinancial Accounting Information should behould be reported when it reported when it

has the following characteristics:has the following characteristics:• a) Relevance- it can influence decisionsa) Relevance- it can influence decisions• b) Reliable- it is not affected by significant errors or biasb) Reliable- it is not affected by significant errors or bias• c) Comparability- it allows the identification of changesc) Comparability- it allows the identification of changes\\

differencesdifferences from data related to previous years or from data related to previous years or fromfrom data data released by competitorsreleased by competitors

• d) Understandability- an average-knowledgeable user, d) Understandability- an average-knowledgeable user, broadly familiar broadly familiar with with financial issues, should be able to read financial issues, should be able to read financial statementsfinancial statements

Overall, information will be provided when the Overall, information will be provided when the benefits of its production are not overcome by costsbenefits of its production are not overcome by costs

55

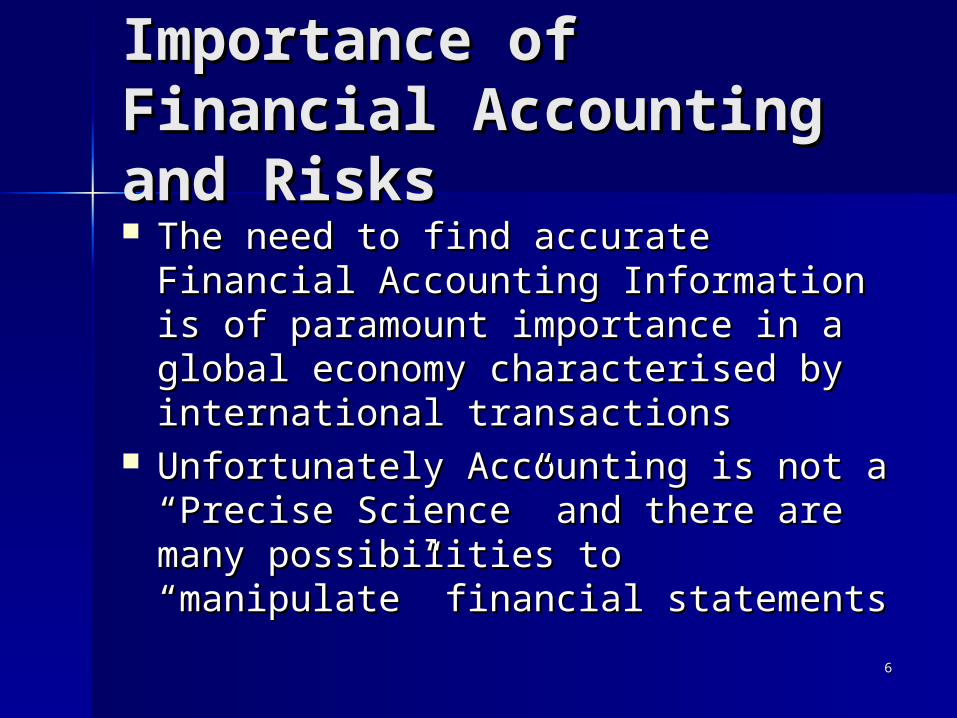

Importance of Importance of Financial Accounting Financial Accounting and Risksand Risks The need to find accurate Financial The need to find accurate Financial

Accounting Information is of Accounting Information is of paramount importance in a global paramount importance in a global economy characterised by economy characterised by international transactionsinternational transactions

Unfortunately Accounting is not a Unfortunately Accounting is not a “Precise Science” and there are many “Precise Science” and there are many possibilities to “manipulate” financial possibilities to “manipulate” financial statementsstatements

66

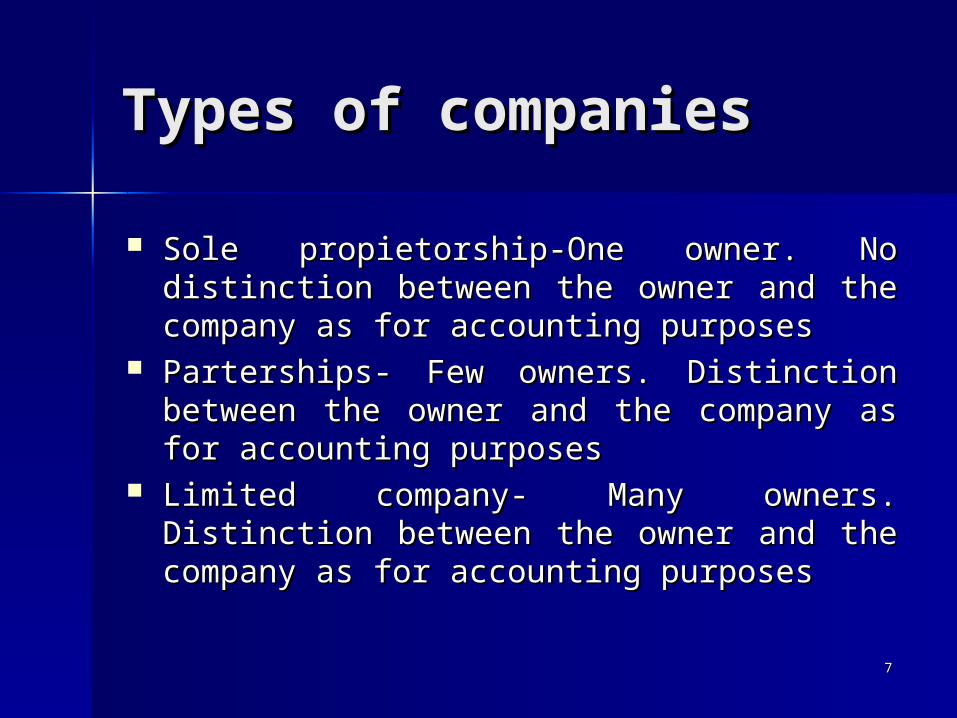

Types of companiesTypes of companies

Sole propietorship-One owner. No distinction Sole propietorship-One owner. No distinction between the owner and the company as for between the owner and the company as for accounting purposesaccounting purposes

Parterships- Few owners. Distinction between Parterships- Few owners. Distinction between the owner and the company as for the owner and the company as for accounting purposesaccounting purposes

Limited company- Many owners. Distinction Limited company- Many owners. Distinction between the owner and the company as for between the owner and the company as for accounting purposesaccounting purposes

77

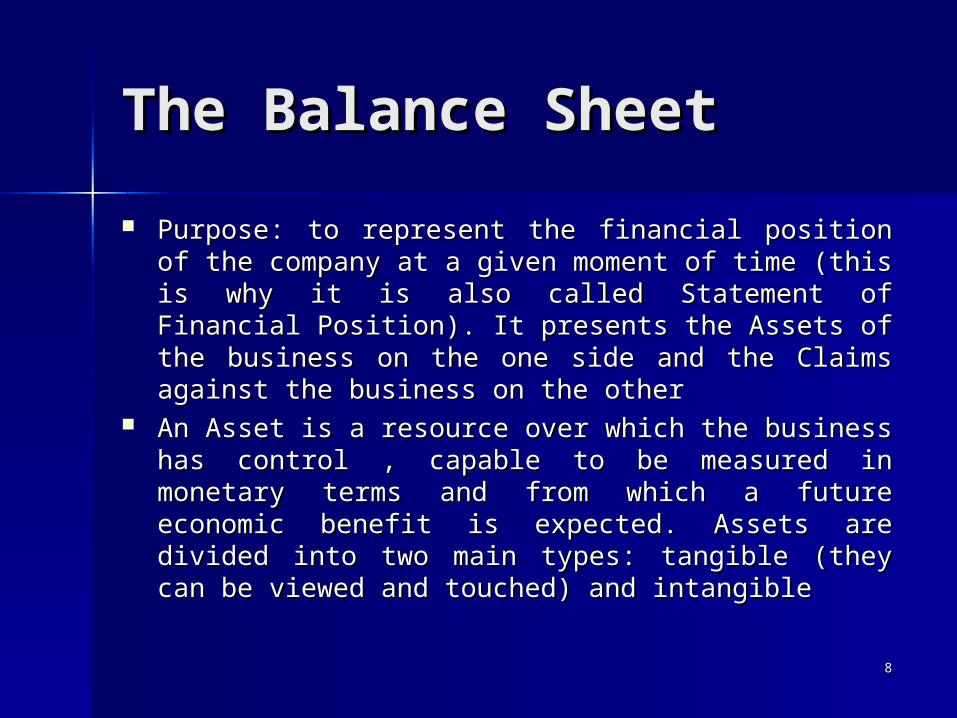

The Balance SheetThe Balance Sheet

Purpose: to represent the financial position of the Purpose: to represent the financial position of the company at a given moment of time (this is why it is company at a given moment of time (this is why it is also called Statement of Financial Position). It presents also called Statement of Financial Position). It presents the Assets of the business on the one side and the the Assets of the business on the one side and the Claims against the business on the otherClaims against the business on the other

An Asset is a resource over which the business has An Asset is a resource over which the business has control , capable to be measured in monetary terms control , capable to be measured in monetary terms and from which a future economic benefit is expected. and from which a future economic benefit is expected. Assets are divided into two main types: tangible (they Assets are divided into two main types: tangible (they can be viewed and touched) and intangible can be viewed and touched) and intangible

88

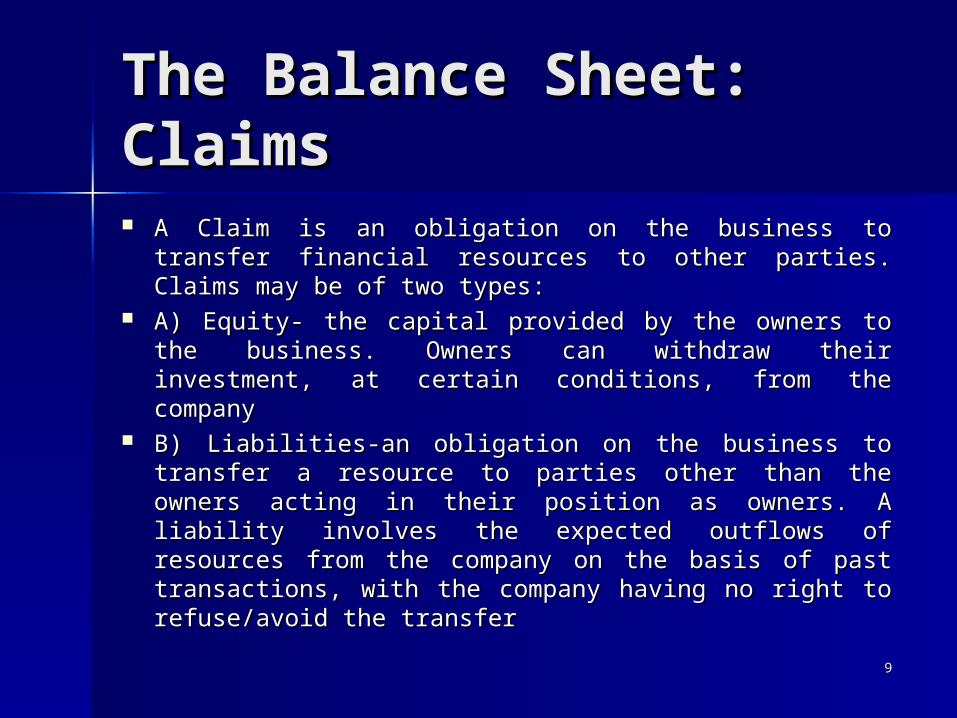

The Balance Sheet: The Balance Sheet: ClaimsClaims A Claim is an obligation on the business to transfer A Claim is an obligation on the business to transfer

financial resources to other parties. Claims may be of financial resources to other parties. Claims may be of two types:two types:

A) Equity- the capital provided by the owners to the A) Equity- the capital provided by the owners to the business. Owners can withdraw their investment, at business. Owners can withdraw their investment, at certain conditions, from the companycertain conditions, from the company

B) Liabilities-an obligation on the business to transfer B) Liabilities-an obligation on the business to transfer a resource to parties other than the owners acting in a resource to parties other than the owners acting in their position as owners. A liability involves the their position as owners. A liability involves the expected outflows of resources from the company on expected outflows of resources from the company on the basis of past transactions, with the company the basis of past transactions, with the company having no right to refuse/avoid the transfer having no right to refuse/avoid the transfer

99

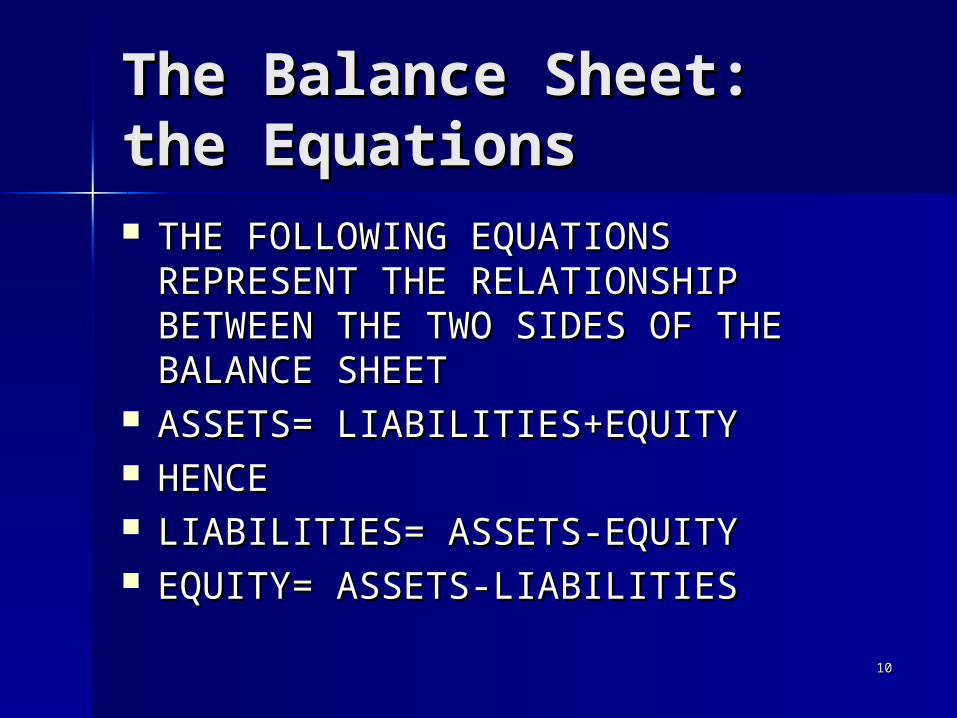

The Balance Sheet: the The Balance Sheet: the EquationsEquations THE FOLLOWING EQUATIONS THE FOLLOWING EQUATIONS

REPRESENT THE RELATIONSHIP REPRESENT THE RELATIONSHIP BETWEEN THE TWO SIDES OF THE BETWEEN THE TWO SIDES OF THE BALANCE SHEETBALANCE SHEET

ASSETS= LIABILITIES+EQUITYASSETS= LIABILITIES+EQUITY HENCEHENCE LIABILITIES= ASSETS-EQUITYLIABILITIES= ASSETS-EQUITY EQUITY= ASSETS-LIABILITIESEQUITY= ASSETS-LIABILITIES

1010

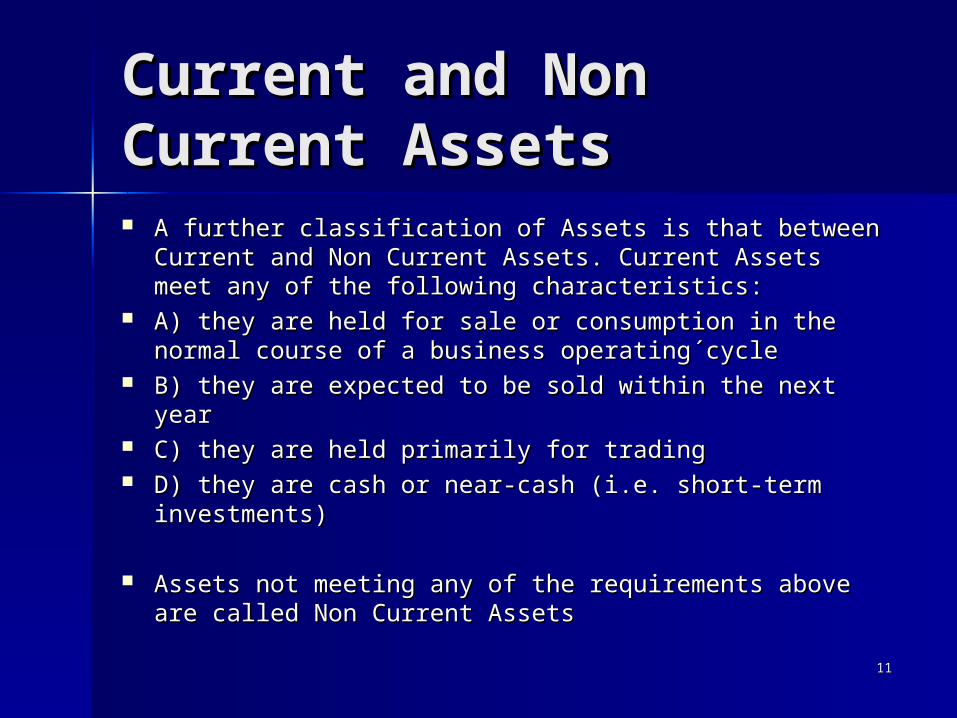

Current and Non Current and Non Current AssetsCurrent Assets A further classification of Assets is that between A further classification of Assets is that between

Current and Non Current Assets. Current Assets meet Current and Non Current Assets. Current Assets meet any of the following characteristics:any of the following characteristics:

A) they are held for sale or consumption in the normal A) they are held for sale or consumption in the normal course of a business operating´cyclecourse of a business operating´cycle

B) they are expected to be sold within the next yearB) they are expected to be sold within the next year C) they are held primarily for tradingC) they are held primarily for trading D) they are cash or near-cash (i.e. short-term D) they are cash or near-cash (i.e. short-term

investments)investments)

Assets not meeting any of the requirements above are Assets not meeting any of the requirements above are called Non Current Assets called Non Current Assets

1111

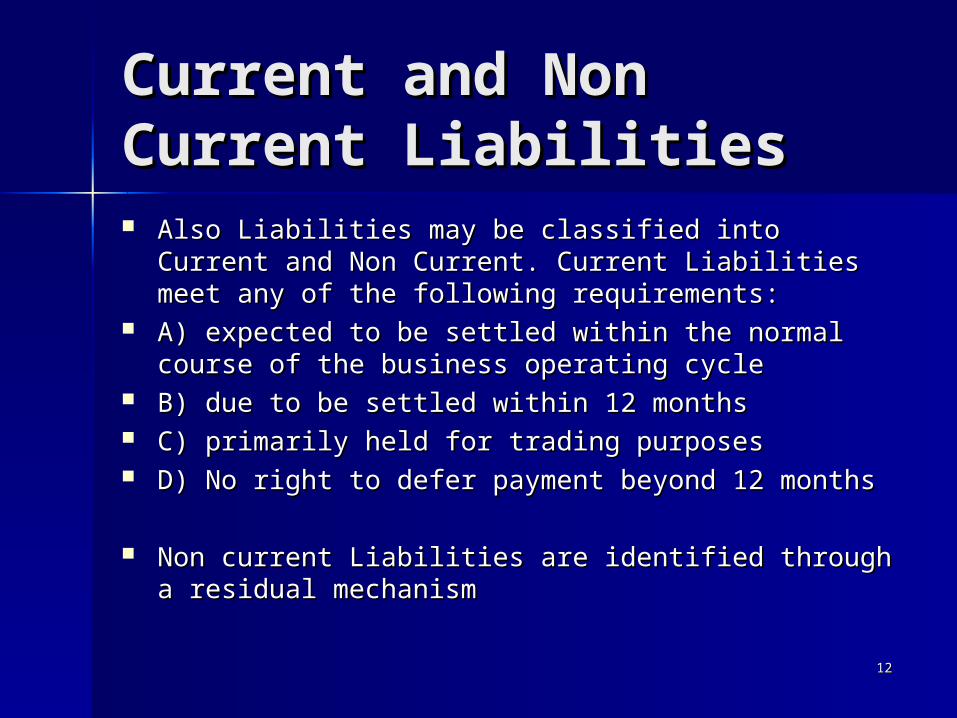

Current and Non Current and Non Current LiabilitiesCurrent Liabilities Also Liabilities may be classified into Current and Non Also Liabilities may be classified into Current and Non

Current. Current Liabilities meet any of the following Current. Current Liabilities meet any of the following requirements:requirements:

A) expected to be settled within the normal course of A) expected to be settled within the normal course of the business operating cyclethe business operating cycle

B) due to be settled within 12 monthsB) due to be settled within 12 months C) primarily held for trading purposesC) primarily held for trading purposes D) No right to defer payment beyond 12 monthsD) No right to defer payment beyond 12 months

Non current Liabilities are identified through a residual Non current Liabilities are identified through a residual mechanismmechanism

1212

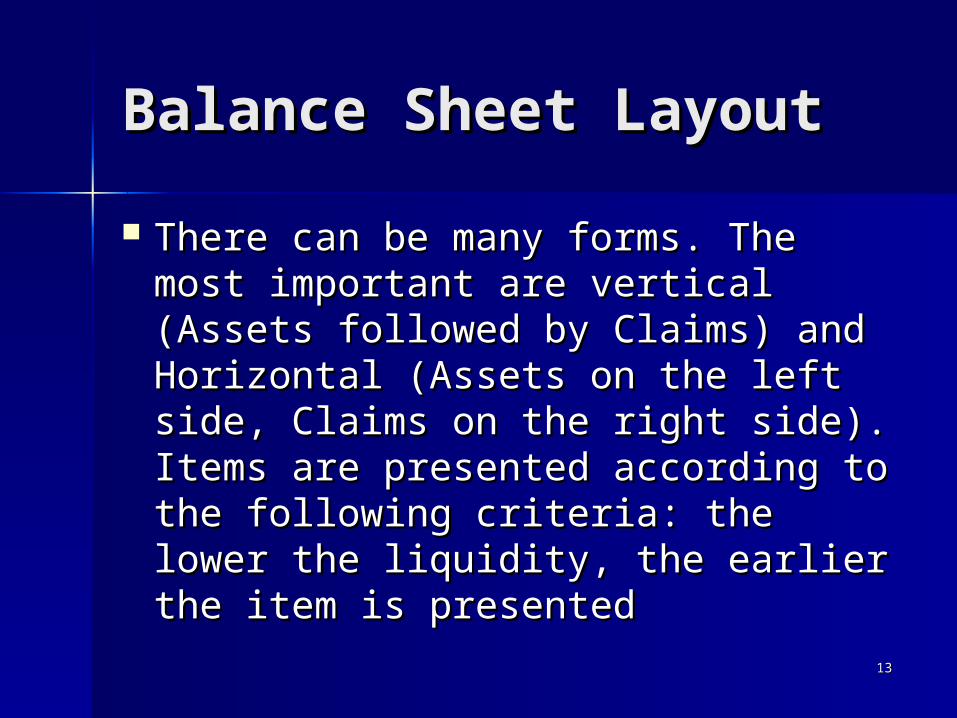

Balance Sheet LayoutBalance Sheet Layout

There can be many forms. The There can be many forms. The most important are vertical (Assets most important are vertical (Assets followed by Claims) and Horizontal followed by Claims) and Horizontal (Assets on the left side, Claims on (Assets on the left side, Claims on the right side). Items are presented the right side). Items are presented according to the following criteria: according to the following criteria: the lower the liquidity, the earlier the lower the liquidity, the earlier the item is presentedthe item is presented

1313

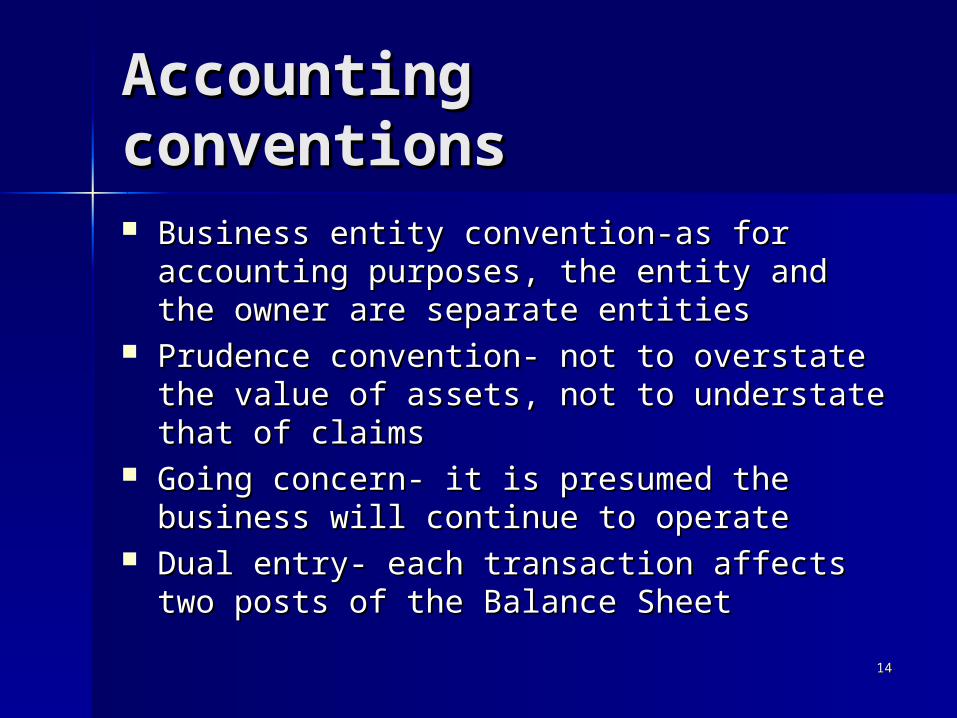

Accounting Accounting conventionsconventions Business entity convention-as for accounting Business entity convention-as for accounting

purposes, the entity and the owner are purposes, the entity and the owner are separate entitiesseparate entities

Prudence convention- not to overstate the Prudence convention- not to overstate the value of assets, not to understate that of value of assets, not to understate that of claimsclaims

Going concern- it is presumed the business Going concern- it is presumed the business will continue to operatewill continue to operate

Dual entry- each transaction affects two Dual entry- each transaction affects two posts of the Balance Sheetposts of the Balance Sheet

1414

Goodwill versus Goodwill versus Intangible AssetsIntangible Assets Goodwill is that part of the value of a company which cannot Goodwill is that part of the value of a company which cannot

be valued directly. Goodwill is not separable from the rest of be valued directly. Goodwill is not separable from the rest of the Assets and cannot be measured directlythe Assets and cannot be measured directly

Internally generated goodwill cannot be reported. However Internally generated goodwill cannot be reported. However an acquirer of a company is allowed to report the value of an acquirer of a company is allowed to report the value of goodwill of the acquireegoodwill of the acquiree

It is difficult nowadays to establish a clear separating line It is difficult nowadays to establish a clear separating line between goodwill and intangible assets. In any case between goodwill and intangible assets. In any case examples of components of goodwill can be the motivation examples of components of goodwill can be the motivation of workforce, its capacity to find new clients, the customer of workforce, its capacity to find new clients, the customer portfolio of a companyportfolio of a company

1515

Reporting Assets: Reporting Assets: Historic Costs and Loss Historic Costs and Loss of valueof value Assets can be reported at their historic costs. The loss Assets can be reported at their historic costs. The loss

of value occurred after the acquisition of the Asset is of value occurred after the acquisition of the Asset is also taken into account and subtracted from the also taken into account and subtracted from the historic costhistoric cost

As for finite-life Assets (it is already known when they As for finite-life Assets (it is already known when they will not be useful any longer), loss of value is called will not be useful any longer), loss of value is called Depreciation (tangible Assets) or Amortisation Depreciation (tangible Assets) or Amortisation (intangible ones). The loss of value can be planned (intangible ones). The loss of value can be planned according to a precise schedule according to a precise schedule

As for infinite-life Assets (it is not known when they As for infinite-life Assets (it is not known when they will cease to be useful) loss of value cannot be will cease to be useful) loss of value cannot be planned or scheduled. Indeed, it is assessed each year planned or scheduled. Indeed, it is assessed each year (Impairment)(Impairment)

1616

Reporting Assets: Fair Reporting Assets: Fair ValueValue Another way of reporting the value of Assets is Another way of reporting the value of Assets is

through the Fair Value method. The Fair Value is through the Fair Value method. The Fair Value is the price which is considered would be paid in a the price which is considered would be paid in a transaction involving two willing, independent transaction involving two willing, independent and knowledgeable parties exchanging a and knowledgeable parties exchanging a good/service similar to the one whose value must good/service similar to the one whose value must be reportedbe reported

In comparison with Historic Cost method, the Fair In comparison with Historic Cost method, the Fair Value method offers a more realistic idea of the Value method offers a more realistic idea of the value of an Asset. However, there are not perfect value of an Asset. However, there are not perfect methods for calculating the Fair Value of an item methods for calculating the Fair Value of an item

1717

Income statement

This particular financial statement provides information about the flows of transactions occurred during a given period

Revenues and Expenses are recorded. Revenues are economic benefits arising from the ordinary activities of the business, whereas expenses are economic outflows. When the former exceeds the latter, then the company reports a profit. Gross profits measure just the difference between the revenue from goods sold and their cost, whereas the operating profit subtracts operating expenses from the gross profit. In turn, net profit is given by the residual obtained when interest and loan net expenses are deducted from the operating profit

Revenues and expenses are recognised on the basis of the principle of Accrual. On the basis of this, revenues and expenses are recognised whenever the ownership and control of the good is transferred. Services are normally recognised when rendered

Income statement

Challenges arise because sometimes certain items are produced within a long period of time. Hence the generating revenues and expenses may be recognised across various accounting periods

Goods and services are recognised on the basis of Accrual rule, independently from the actual flow of cash

Overall, revenue is recognised when it can be measured reliably and there is an expected economic benefit accruing to the company

Methods of depreciating assets Assets with an economic finite life may

be depreciated acccording to two main methods:

Straight-line method: in this case the amount of depreciation is the same over the whole economic life of the asset

Reducing balance method: in this case the percentual amount on the basis of which the amount of depreciation is calculated is the same each year. However, the amount itself varies. There is a formula useful to calculate the percentage needed.

Allocating the cost of sales In case of goods of the same type

which are bought at different prices, the costs of sales may be allocated according to three methods:

FIFO (First in, first out)- the first goods to be bought are considered the first to be sold

LIFO (Last in, first out)- the last goods to be bought are considered the first to be sold

AVCO (Average cost method)- the costs of goods sold are calculated as a weighted average of the total of goods purchased

Cash-Flow Statement

The Cash Flow Statement is a summary of the cash receipt and payment during a given time. It contains a picture of cash and cash-equivalents

Cash is notes and coins in the hands of a company, as well as bank deposits accessible on demand. Cash-equivalents are short-term (3 months maximum), highly liquid investments with an insignificant risk. Cash-equivalents are held to meet short-term cash committments

Cash is divided into three categories: operating, investing and financing

How to deal with Bad Debts Not all trade receivables are always paid back by

debtors. Some of them are left unpaid (Bad debts)

Each year a company must write bad debts off and report an estimate of those receivables which are probably going to be written off in the future

If it results that the company has over(under)stated the extent of future bad debts, then it must adjust the financial statements of future years. For example, if the future amount of bad debts was overstated, then the company will report the residual in Revenue

Cash-Flow Statement

Operating Cash indicates receipts and payments related to the main activity of the reporting entity. It equals the cash receipt from the sale of goods/services minus the cash paid to buy inventories, pay workers, rent and so on. Also taxes actually paid are counted

Investing Cash is cash related to the investments of the company to buy additional non current assets or to the disposal of non current assets. It includes also investments in other entities (acquisitions), receipt of dividends for shares in other companies, payment for loans to other companies

Financing cash indicates the long-term financing of the company. It includes bank borrowing, cash collected through the issue of shares and bonds

Cash-Flow Statement

The Operating Cash Flow statement may be prepared following two methods:Direct and Indirect Method

The Direct Method starts from the books kept by the company and calculates all cash movements

Cash-Flow Statement: The Indirect Method The Indirect Method is used to draw the Cash-Flow

from the Income Statement and the Balance Sheet. It starts from the operating profit, it adds the depreciation of assets, + (-) the decrease (increase) in inventories, + (-) decrease (increase) in trade receivables, + (-) increase (decrease) in trade payables, less interest paid *, less taxation. The result is the Net Cash Flows from operating activities

* Interest paid may appear also in other parts of the Cash-Flow Statement

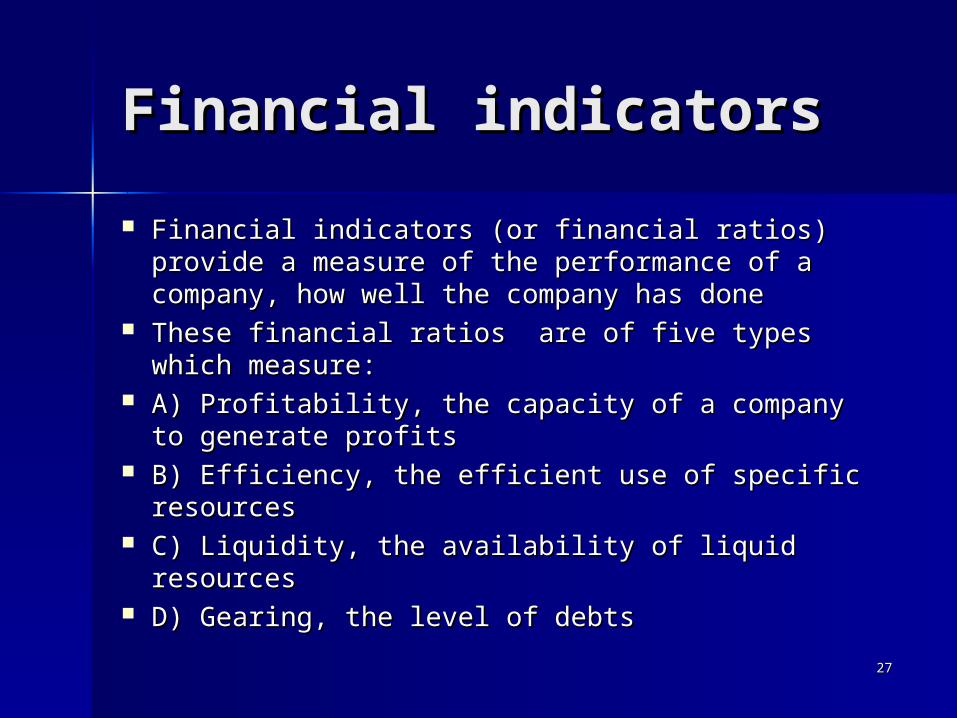

Financial indicatorsFinancial indicators

Financial indicators (or financial ratios) provide a Financial indicators (or financial ratios) provide a measure of the performance of a company, how measure of the performance of a company, how well the company has donewell the company has done

These financial ratios are of five types which These financial ratios are of five types which measure:measure:

A) Profitability, the capacity of a company to A) Profitability, the capacity of a company to generate profitsgenerate profits

B) Efficiency, the efficient use of specific B) Efficiency, the efficient use of specific resourcesresources

C) Liquidity, the availability of liquid resourcesC) Liquidity, the availability of liquid resources D) Gearing, the level of debtsD) Gearing, the level of debts

2727

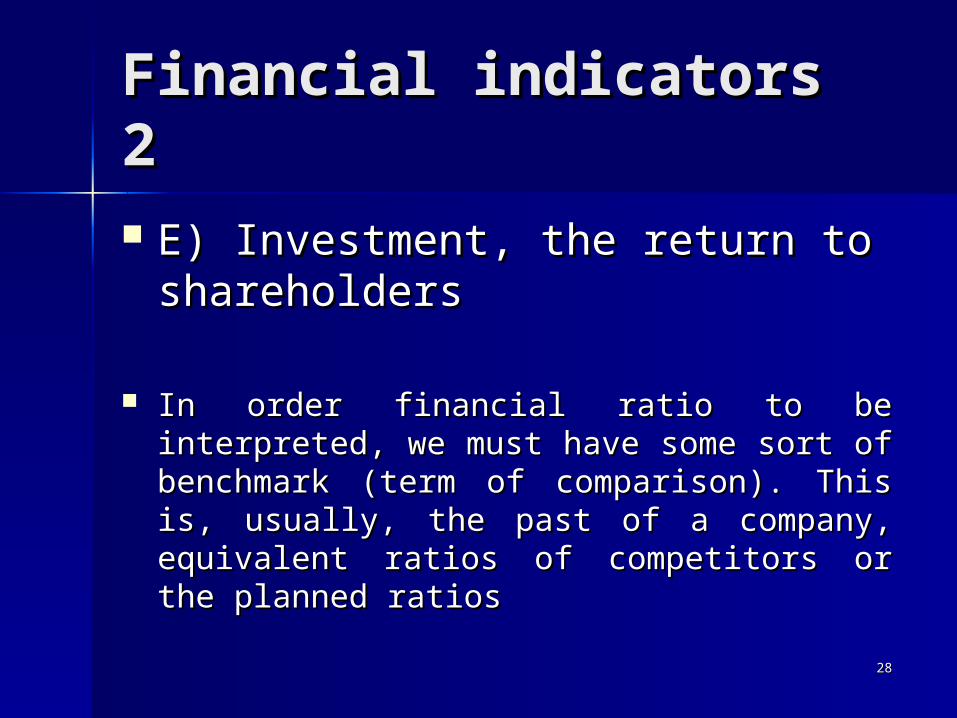

Financial indicators 2Financial indicators 2

E) Investment, the return to E) Investment, the return to shareholdersshareholders

In order financial ratio to be interpreted, we In order financial ratio to be interpreted, we must have some sort of benchmark (term of must have some sort of benchmark (term of comparison). This is, usually, the past of a comparison). This is, usually, the past of a company, equivalent ratios of competitors or company, equivalent ratios of competitors or the planned ratiosthe planned ratios

2828

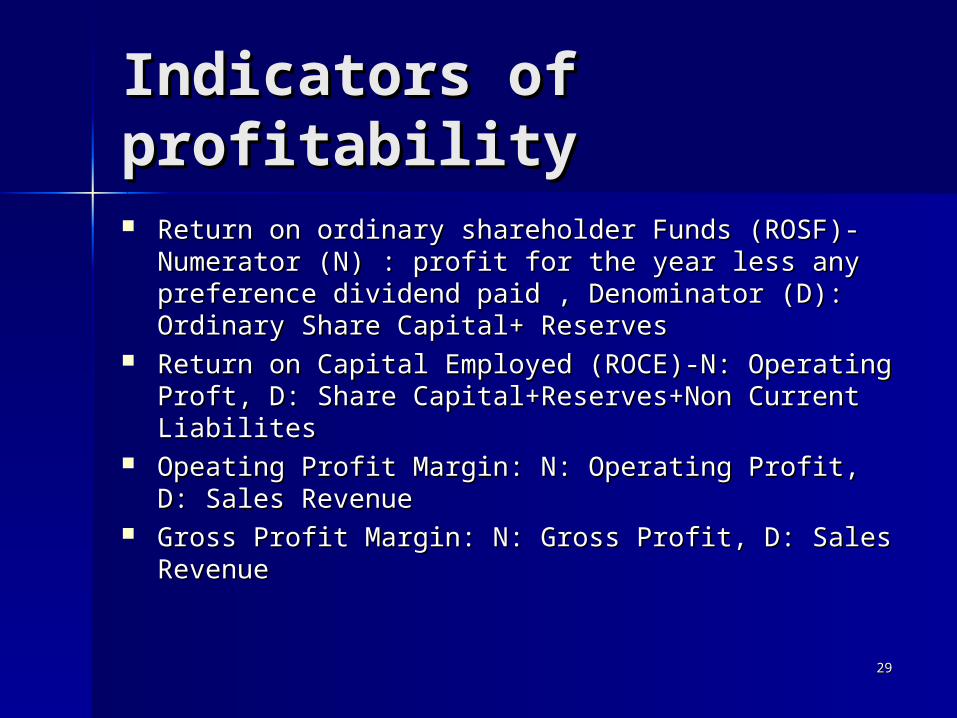

Indicators of Indicators of profitabilityprofitability Return on ordinary shareholder Funds (ROSF)- Return on ordinary shareholder Funds (ROSF)-

Numerator (N) : profit for the year less any preference Numerator (N) : profit for the year less any preference dividend paid , Denominator (D): Ordinary Share dividend paid , Denominator (D): Ordinary Share Capital+ ReservesCapital+ Reserves

Return on Capital Employed (ROCE)-N: Operating Return on Capital Employed (ROCE)-N: Operating Proft, D: Share Capital+Reserves+Non Current Proft, D: Share Capital+Reserves+Non Current LiabilitesLiabilites

Opeating Profit Margin: N: Operating Profit, D: Sales Opeating Profit Margin: N: Operating Profit, D: Sales RevenueRevenue

Gross Profit Margin: N: Gross Profit, D: Sales RevenueGross Profit Margin: N: Gross Profit, D: Sales Revenue

2929

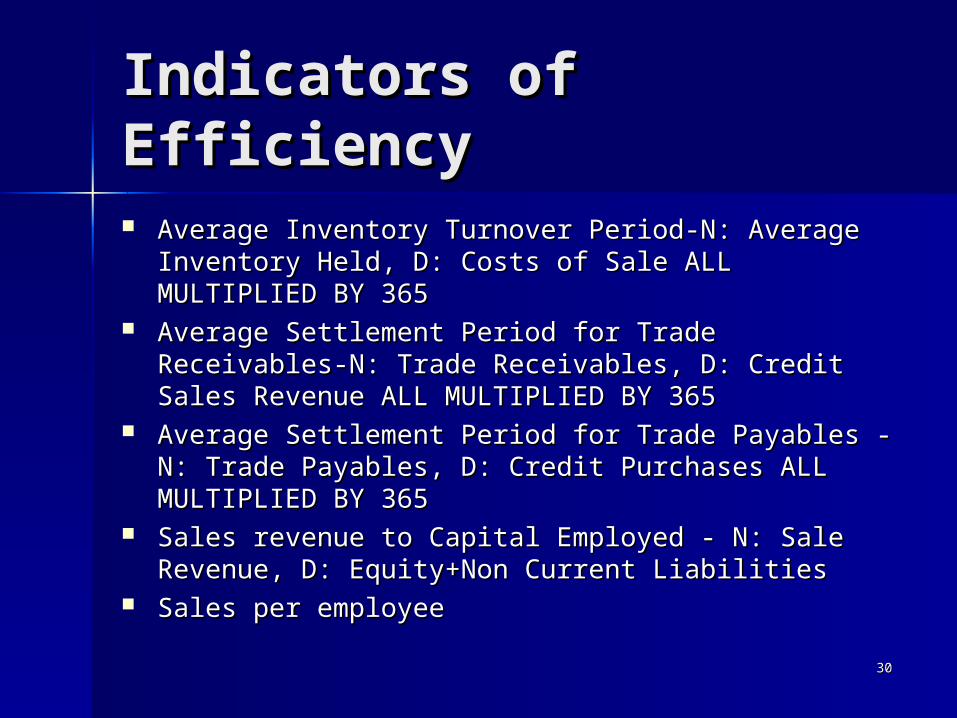

Indicators of EfficiencyIndicators of Efficiency

Average Inventory Turnover Period-N: Average Average Inventory Turnover Period-N: Average Inventory Held, D: Costs of Sale ALL MULTIPLIED BY Inventory Held, D: Costs of Sale ALL MULTIPLIED BY 365 365

Average Settlement Period for Trade Receivables-N: Average Settlement Period for Trade Receivables-N: Trade Receivables, D: Credit Sales Revenue ALL Trade Receivables, D: Credit Sales Revenue ALL MULTIPLIED BY 365 MULTIPLIED BY 365

Average Settlement Period for Trade Payables -N: Average Settlement Period for Trade Payables -N: Trade Payables, D: Credit Purchases ALL MULTIPLIED Trade Payables, D: Credit Purchases ALL MULTIPLIED BY 365BY 365

Sales revenue to Capital Employed - N: Sale Revenue, Sales revenue to Capital Employed - N: Sale Revenue, D: Equity+Non Current LiabilitiesD: Equity+Non Current Liabilities

Sales per employeeSales per employee

3030